EXHIBIT 99.1

Overview

We are a global power company, dedicated to improving lives by providing safe, reliable and sustainable energy solutions in every market we serve. We own a portfolio of electricity generation and distribution businesses on five continents in 27 countries, with total capacity of approximately 42,600 Megawatts (“MW”) and distribution networks serving approximately 12 million customers as of December 31, 2011. In addition, we have approximately 2,400 MW under construction in eight countries. We were incorporated in Delaware in 1981.

We own and operate two primary types of businesses. The first is our Generation business, where we own and/or operate power plants to generate and sell power to wholesale customers such as utilities and other intermediaries. The second is our Utilities business, where we own and/or operate utilities to generate, distribute, transmit and sell electricity to end-user customers in the residential, commercial, industrial and governmental sectors within a defined service area.

Our assets are diverse with respect to fuel source and type of market, which helps reduce certain types of operating risk. Our portfolio employs a broad range of fuels, including coal, diesel, fuel oil, natural gas, biomass and renewable sources such as hydroelectric power, wind and solar, which reduces the risks associated with dependence on any one fuel source. Our portfolio combines a presence in stable markets in developed countries with faster growing emerging markets. In addition, our Generation portfolio is largely contracted, which reduces the risk related to market prices of electricity and fuel. We also attempt to limit risk by matching the currency of most of our subsidiary debt to the revenue of the underlying business and by hedging some of our interest rate and commodity risk. However, our business is still subject to these and other risks, which are further described in Item 1A.—Risk Factors of the 2011 Form 10-K.

Our goal is to maximize value for our shareholders by growing cash flow and earnings per share and achieving better returns on our investments. We will expand our platforms in our core markets, specifically Brazil, Chile, Colombia and the United States, and will work to develop growth platforms in key markets including Turkey, Poland and the United Kingdom. Over time, by focusing our growth and exiting select non-strategic markets, we expect to narrow our geographic focus to achieve better results with fewer countries. Across our portfolio, we will work to optimize profitability, as well as reduce our overhead and business development costs. Finally, we have announced our intent to initiate a dividend beginning in the third quarter of 2012, with the first payment expected to be made in the fourth quarter of 2012.

Key Lines of Business

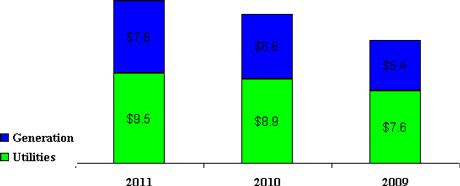

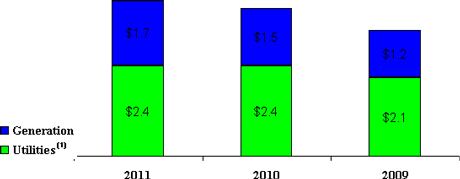

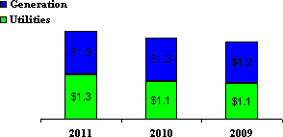

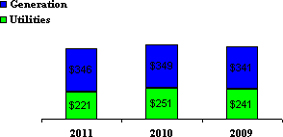

AES’ primary sources of revenue and gross margin today are from Generation and Utilities. These businesses are distinguished by the nature of the customers, operational differences, cost structure, regulatory environment and risk exposure. The breakout of revenue and gross margin between Generation and Utilities for the years ended December 31, 2011, 2010 and 2009, respectively, is shown below. Operating results for integrated utilities, which have both Generation and Utilities, are reflected in the Utilities amounts below.

1

Revenue

($ in billions)

Gross Margin

($ in billions)

| (1) | Utilities gross margin includes the margin from generation businesses owned by the Company and from whom the utility purchases energy. |

Generation

We currently own or operate a generation portfolio of approximately 32,300 MW, excluding the generation capabilities of our integrated utilities, consisting of 96 Generation facilities in 22 countries on five continents at our generation businesses. We also have approximately 2,100 MW of capacity currently under construction in four countries. We are a major power source in many countries, such as Chile, where AES Gener (“Gener”) is the second largest electricity generation company in terms of capacity. Our Generation business uses a wide range of technologies and fuel types including coal, combined-cycle gas turbines, hydroelectric power and biomass. Generation revenue was $7.6 billion, $6.8 billion and $5.4 billion for the years ended December 31, 2011, 2010 and 2009, respectively.

Performance drivers for our Generation businesses include, among other factors, plant reliability, fuel costs, power prices, volume and fixed-cost management. Growth in the Generation business is largely tied to securing new power purchase agreements (“PPAs”), expanding capacity in our existing facilities, reducing our fixed costs and building or acquiring new power plants.

2

The majority of the electricity produced by our Generation businesses is sold under long-term PPAs, to wholesale customers. In 2011, approximately 71% of the revenue from our Generation business was from plants that operate under PPAs of three years or longer for 75% or more of their output capacity. These businesses often reduce their exposure to fuel supply risks by entering into long-term fuel supply contracts or fuel tolling arrangements where the customer assumes full responsibility for purchasing and supplying the fuel to the power plant. These long-term contractual agreements help reduce the volatility of our cash flows and earnings and also reduce exposure to volatility in the market price for electricity and fuel; however, the amount of earnings and cash flow predictability varies from business to business based on the degree to which its exposure is limited by the contracts it has negotiated.

Our Generation businesses with long-term contracts face most of their competition from other utilities and independent power producers (“IPPs”) prior to the execution of a power sales agreement during the development phase of a project or upon expiration of an existing agreement. Once a project is operational, we traditionally have faced limited competition due to the long-term nature of the generation contracts. However, as our existing contracts expire, we may face increased competition to attract new customers and maintain our current customer base.

The balance of our Generation business sells power through competitive markets under short-term contracts, directly in the spot market or, in some cases, at regulated prices. As a result, the cash flows and earnings associated with these businesses are more sensitive to fluctuations in the market price for electricity, natural gas, coal and other fuels. Competitive factors for these facilities include price, reliability, operational cost and third-party credit requirements.

Utilities

AES utility businesses distribute power to over 12 million people in six countries on five continents and consist primarily of 13 companies owned or operated under management agreements, each of which operates in defined service areas. These businesses also include 29 generation plants in two countries with generation capacity totaling approximately 8,500 MW. These businesses have a variety of structures ranging from pure distribution businesses to fully integrated utilities, which generate, transmit and distribute power. For instance, our wholly-owned subsidiary in the U.S., Indianapolis Power & Light (“IPL”), has the exclusive right to provide retail services to approximately 470,000 customers in Indianapolis, Indiana. The Dayton Power and Light Company (“DP&L”) serves approximately 500,000 customers in West Central Ohio. Eletropaulo Metropolitana Electricidade de São Paulo S.A. (“AES Eletropaulo” or “Eletropaulo”), serving the São Paulo metropolitan region for over 100 years, has approximately six million customers and is the largest electricity distribution company in Latin America in terms of revenue and electricity distributed. Utilities revenue was $9.5 billion, $8.9 billion and $7.6 billion for the years ended December 31, 2011, 2010 and 2009, respectively.

Performance drivers for Utilities include, but are not limited to, reliability of service, management of working capital, negotiation of tariff adjustments, compliance with extensive regulatory requirements, and in developing countries, reduction of commercial and technical losses. The results of operations of our Utilities businesses are sensitive to changes in economic growth, regulations and variations in weather conditions in the areas in which they operate. In certain locations, our distribution businesses face increased competition as a result of changes in laws and regulations which allow wholesale and retail services to be provided on a competitive basis.

The majority of our utilities face relatively little direct competition due to significant barriers to entry, which are present in these markets. Competition is a factor in efforts to acquire existing businesses. In this arena, we compete against a number of other market participants, some of which have greater financial resources, have been engaged in distribution related businesses for longer periods of time and/or have accumulated more significant portfolios. Relevant competitive factors for our power distribution businesses include financial resources, governmental assistance, regulatory restrictions and access to non-recourse financing.

Renewables and Other Initiatives

In recent years, as demand for renewable sources of energy has grown, we have developed projects in wind, solar and other renewable initiatives including energy storage. In 2005, we started a wind generation business (“Wind Generation”), which currently has 21 plants in operation in five countries totaling approximately 1,800 MW in generation capacity and is one of the largest producers of wind power in the U.S. In addition, 205 MW are under

3

construction in four countries. In March 2008, we formed AES Solar Energy LLC (“AES Solar”), a joint venture with Riverstone Holdings, LLC (“Riverstone”), a private equity firm, which has since commenced commercial operations of 26 plants totaling 151 MW of solar projects in Bulgaria, France, Greece, Italy and Spain. We also have a line of business to develop and implement utility scale energy storage systems (such as batteries), which store and release power when needed. None of these initiatives are currently material to our operations, however, there are risks associated with these initiatives, which are further described in Item 1A.—Risk Factors of the 2011 Form 10-K.

Risks

We routinely encounter and address risks, some of which may cause our future results to be different, sometimes materially different, than we presently anticipate. The categories of risk we have identified in Item 1A.—Risk Factors of the 2011 Form 10-K include the following:

| | • | | risks related to our high level of indebtedness; |

| | • | | risks associated with our ability to raise needed capital; |

| | • | | external risks associated with revenue and earnings volatility; |

| | • | | risks associated with our operations; |

| | • | | risks associated with governmental regulation and laws; and |

| | • | | risks associated with our disclosure controls and internal controls over financial reporting. |

The categories of risk identified above are discussed in greater detail in Item 1A.—Risk Factors of the 2011 Form 10-K. These risk factors should be read in conjunction with Item 7.—Management’s Discussion and Analysis of Financial Condition and Results of Operations, and the Consolidated Financial Statements and related notes included elsewhere in this report.

Our Organization and Segments

We believe our broad geographic footprint allows us to focus development in targeted markets with opportunities for new investment, and provides stability through our presence in more developed regions. In addition, our presence in each region affords us important relationships and helps us identify local markets with attractive opportunities for new investment. The management reporting structure is organized along two lines of business—Generation and Utilities, each led by a Chief Operating Officer (“COO”), who in turn reports to our Chief Executive Officer (“CEO”). Our CEO and COOs are based in Arlington, Virginia. During the first quarter of 2012, the Company completed the restructuring of its operational management and reporting process. For financial reporting purposes, the Company has identified seven reportable segments which include:

| | • | | Generation—Latin America—Other; |

| | • | | Generation—North America; |

| | • | | Utilities—Latin America; |

| | • | | Utilities—North America. |

As discussed in Note 16—Segment and Geographic Information to the Consolidated Financial Statements, based on the application of the segment accounting guidance, Tietê is reported as a separate segment for purposes of the required segment accounting disclosures, but is included in Generation—Latin America within the discussion of operating results for revenue and gross margin in management’s discussion and analysis as is it managed with the other Latin American generation businesses.

4

Corporate and Other—The Company’s Europe Utilities, Africa Utilities, Africa Generation and Wind Generation businesses as well as the Company’s renewables initiatives are reported within “Corporate and Other” because they do not require separate disclosure under segment reporting accounting guidance. See Item 7.—Management’s Discussion and Analysis of Financial Condition and Results of Operations for further discussion of the Company’s segment structure used for financial reporting purposes.

The following describes our businesses by their geographical area of operations:

Latin America

Our Latin America operations accounted for 65%, 65% and 67% of consolidated AES revenue in 2011, 2010 and 2009, respectively. The following table provides highlights of our Latin America operations:

| | |

| Countries | | Argentina, Brazil, Chile, Colombia, Dominican

Republic, El Salvador and Panama |

| Generation Capacity | | 12,616 Gross MW |

| Utilities Penetration | | 8.7 million customers (48,470 Gigawatt Hours (“GWh”)) |

| Generation Facilities | | 56 (including 1 under construction) |

| Utilities Businesses | | 6 |

| Key Generation Businesses | | Gener, Tietê and Alicura |

| Key Utilities Businesses | | Eletropaulo and Sul |

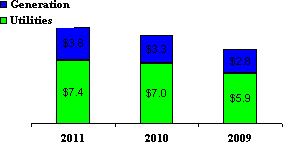

The bar charts below shows the breakdown between our Latin America Generation and Utilities segments as a percentage of total Latin America revenue and gross margin for the years ended December 31, 2011, 2010, and 2009. See Note 16—Segment and Geographic Information in the Consolidated Financial Statements in Item 8 of this Form 8-K for information on revenue from external customers, Adjusted Gross Margin (a non-GAAP measure) and total assets by segment.

| | |

Revenue ($ in billions)

| | Gross Margin ($ in billions)

|

Latin America Generation. Our largest generation business in Latin America, AES Tietê (“Tietê”), located in Brazil, represents approximately 18% of the total generation capacity in the state of São Paulo and is the tenth largest generator in Brazil. AES holds a 24% economic interest in Tietê. In Chile, we are the second largest generator of power. We currently have one new generation plant under construction—a coal plant in Chile with a generation capacity of 270 MW.

5

Set forth below is a list of our Latin America Generation facilities:

Generation

| | | | | | | | | | | | | | | | |

Business | | Location | | Fuel | | Gross

MW | | | AES Equity

Interest

(Percent,

Rounded) | | | Year

Acquired

or Began

Operation | |

Alicura | | Argentina | | Hydro | | | 1,050 | | | | 99 | % | | | 2000 | |

Gener - TermoAndes | | Argentina | | Gas/Diesel | | | 643 | | | | 71 | % | | | 2000 | |

Los Caracoles(1) | | Argentina | | Hydro | | | 125 | | | | 0 | % | | | 2009 | |

Paraná-GT | | Argentina | | Gas/Diesel | | | 845 | | | | 99 | % | | | 2001 | |

Quebrada de Ullum(1) | | Argentina | | Hydro | | | 45 | | | | 0 | % | | | 2004 | |

Rio Juramento - Cabra Corral | | Argentina | | Hydro | | | 102 | | | | 99 | % | | | 1995 | |

Rio Juramento - El Tunal | | Argentina | | Hydro | | | 10 | | | | 99 | % | | | 1995 | |

San Juan - Sarmiento | | Argentina | | Gas/Diesel | | | 33 | | | | 99 | % | | | 1996 | |

San Juan - Ullum | | Argentina | | Hydro | | | 45 | | | | 99 | % | | | 1996 | |

San Nicolás | | Argentina | | Coal/Gas/Oil | | | 675 | | | | 99 | % | | | 1993 | |

Tietê(2) | | Brazil | | Hydro | | | 2,659 | | | | 24 | % | | | 1999 | |

Uruguaiana | | Brazil | | Gas | | | 639 | | | | 46 | % | | | 2000 | |

Gener - Electrica Angamos | | Chile | | Coal | | | 545 | | | | 71 | % | | | 2011 | |

Gener - Electrica Santiago(3) | | Chile | | Gas/Diesel | | | 479 | | | | 64 | % | | | 2000 | |

Gener - Electrica Ventanas(4) | | Chile | | Coal | | | 272 | | | | 71 | % | | | 2010 | |

Gener - Gener(5) | | Chile | | Hydro/Coal/Diesel/Biomass | | | 1,003 | | | | 71 | % | | | 2000 | |

Gener - Guacolda(6),(7) | | Chile | | Coal/Pet Coke | | | 608 | | | | 35 | % | | | 2000 | |

Gener - Norgener | | Chile | | Coal/Pet Coke | | | 277 | | | | 71 | % | | | 2000 | |

Chivor | | Colombia | | Hydro | | | 1,000 | | | | 71 | % | | | 2000 | |

Andres | | Dominican Republic | | Gas | | | 319 | | | | 100 | % | | | 2003 | |

Itabo(8) | | Dominican Republic | | Coal | | | 295 | | | | 50 | % | | | 2000 | |

Los Mina | | Dominican Republic | | Gas | | | 236 | | | | 100 | % | | | 1996 | |

AES Nejapa | | El Salvador | | Landfill Gas | | | 6 | | | | 100 | % | | | 2011 | |

Bayano | | Panama | | Hydro | | | 260 | | | | 49 | % | | | 1999 | |

Changuinola | | Panama | | Hydro | | | 223 | | | | 100 | % | | | 2011 | |

Chiriqui - Esti | | Panama | | Hydro | | | 120 | | | | 49 | % | | | 2003 | |

Chiriqui - La Estrella | | Panama | | Hydro | | | 48 | | | | 49 | % | | | 1999 | |

Chiriqui - Los Valles | | Panama | | Hydro | | | 54 | | | | 49 | % | | | 1999 | |

| | | | | | | | | | | | | | | | |

| | | | | | | 12,616 | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| (1) | AES operates these facilities through management or operations and maintenance (“O&M”) agreements and owns no equity interest in these businesses. |

| (2) | Tietê plants: Água Vermelha, Bariri, Barra Bonita, Caconde, Euclides da Cunha, Ibitinga, Limoeiro, Mog-Guaçu, Nova Avanhandava, Promissão, Sao Joaquim and seven other small hydroelectric plants below Tietê’s wholly-owned subsidiary “PCH Minas Ltda”. |

| (3) | Gener—Electrica Santiago plants: Nueva Renca and Renca. |

| (4) | Gener—Electrica Ventanas plant: Nueva Ventanas. |

| (5) | Gener—Gener plants: Alfalfal, Constitución, Laguna Verde, Laguna Verde Turbogas, Laja, Los Vientos, Maitenas, Queltehues, San Francisco de Mostazal, Santa Lidia, Ventanas and Volcán. |

| (6) | Gener—Guacolda plants: Guacolda 1, Guacolda 2, Guacolda 3 and Guacolda 4. |

| (7) | Unconsolidated entities for which the results of operations are reflected in Equity in Earnings of Affiliates. |

| (8) | Itabo plants: Itabo complex (two coal-fired steam turbines and one gas-fired steam turbine). |

6

Generation under construction

| | | | | | | | | | | | | | | | |

Business | | Location | | Fuel | | Gross

MW | | | AES Equity

Interest

(Percent,

Rounded) | | | Expected

Year of

Commercial

Operations | |

Campiche | | Chile | | Coal | | | 270 | | | | 71 | % | | | 2013 | |

Latin America Utilities. Each of our Utilities businesses in Latin America sells electricity under regulated tariff agreements and has transmission and distribution capabilities but none of them has generation capability. AES Eletropaulo, a consolidated subsidiary of which AES owns a 16% economic interest and which has served the São Paulo, Brazil area for over 100 years, has approximately six million customers and is the largest electricity distribution company in Latin America in terms of revenue and electricity distributed. Pursuant to its concession agreement, AES Eletropaulo is entitled to distribute electricity in its service area until 2028. AES Eletropaulo’s service territory consists of 24 municipalities in the greater São Paulo metropolitan area and adjacent regions that account for approximately 17% of Brazil’s GDP and 40% of the population in the State of São Paulo. AES Sul (“Sul”), a wholly-owned subsidiary, serves over one million customers.

Set forth below is a list of our Latin America Utilities facilities:

Distribution

| | | | | | | | | | | | | | | | | | |

Business | | Location | | Approximate Number

of Customers Served as

of 12/31/2011 | | | GWh

Sold in

2011 | | | AES Equity

Interest

(Percent,

Rounded) | | | Year

Acquired | |

Eletropaulo | | Brazil | | | 6,348,000 | | | | 36,817 | | | | 16 | % | | | 1998 | |

Sul | | Brazil | | | 1,260,000 | | | | 8,223 | | | | 100 | % | | | 1997 | |

CAESS | | El Salvador | | | 516,000 | | | | 2,060 | | | | 75 | % | | | 2000 | |

CLESA | | El Salvador | | | 304,000 | | | | 786 | | | | 64 | % | | | 1998 | |

DEUSEM | | El Salvador | | | 62,000 | | | | 108 | | | | 74 | % | | | 2000 | |

EEO | | El Salvador | | | 229,000 | | | | 476 | | | | 89 | % | | | 2000 | |

| | | | | | | | | | | | | | | | | | |

| | | | | 8,719,000 | | | | 48,470 | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

North America

Our North America operations accounted for 15%, 16% and 18% of consolidated revenue in 2011, 2010 and 2009, respectively. The following table provides highlights of our North America operations:

| | |

| Countries | | U.S., Puerto Rico and Mexico |

| Generation Capacity | | 15,756 Gross MW |

| Utilities Penetration | | 970,000 customers (16,890 GWh) |

| Generation Facilities | | 15 |

| Utilities Businesses | | 2 integrated utilities (includes 18 generation plants) |

| Key Generation Businesses | | Southland and TEG/TEP |

| Key Utilities Businesses | | IPL, DPL (Since November 28, 2011) |

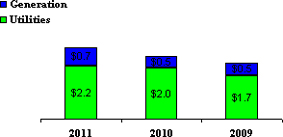

The bar charts below shows the breakdown between our North America Generation and Utilities segments as a percentage of total North America revenue and gross margin for the years ended December 31, 2011, 2010 and 2009. See Note 16—Segment and Geographic Information in the Consolidated Financial Statements in Item 8 of this Form 8-K for information on revenue from external customers, Adjusted Gross Margin (a non-GAAP measure) and total assets by segment.

7

| | |

Revenue ($ in billions)

| | Gross Margin ($ in millions)

|

North America Generation. Approximately 92% of the generation capacity is supported by long-term power purchase or tolling agreements. Our North America Generation business consists of seven gas-fired, five coal-fired and three petroleum coke-fired plants in the United States, Puerto Rico, Mexico, and Trinidad.

Our largest generation business is AES Southland. This business operates three gas-fired plants, representing generation capacity of 3,853 MW, in the Los Angeles basin under a long-term tolling agreement. Other significant generation facilities include TEG and TEP, which represent a total of 460 MW of long-term contracted generation capacity in Mexico.

Set forth below is a list of our North America Generation facilities:

Generation

| | | | | | | | | | | | | | | | |

Business | | Location | | Fuel | | Gross

MW | | | AES Equity

Ownership

(Percent,

Rounded) | | | Year

Acquired

or Began

Operation | |

Mérida III | | Mexico | | Gas | | | 484 | | | | 55 | % | | | 2000 | |

Termoelectrica del Golfo (TEG) | | Mexico | | Pet Coke | | | 230 | | | | 99 | % | | | 2007 | |

Termoelectrica del Peñoles (TEP) | | Mexico | | Pet Coke | | | 230 | | | | 99 | % | | | 2007 | |

Trinidad | | Trinidad | | Gas | | | 394 | | | | 10 | % | | | 2011 | |

Southland - Alamitos | | USA - CA | | Gas | | | 2,047 | | | | 100 | % | | | 1998 | |

Southland - Huntington Beach | | USA - CA | | Gas | | | 430 | | | | 100 | % | | | 1998 | |

Southland - Redondo Beach | | USA - CA | | Gas | | | 1,376 | | | | 100 | % | | | 1998 | |

Hawaii | | USA - HI | | Coal | | | 203 | | | | 100 | % | | | 1992 | |

Warrior Run | | USA - MD | | Coal | | | 205 | | | | 100 | % | | | 2000 | |

Red Oak(1) | | USA - NJ | | Gas | | | 832 | | | | 100 | % | | | 2002 | |

Shady Point | | USA - OK | | Coal | | | 360 | | | | 100 | % | | | 1991 | |

Beaver Valley | | USA - PA | | Coal | | | 125 | | | | 100 | % | | | 1985 | |

Ironwood(1) | | USA - PA | | Gas | | | 710 | | | | 100 | % | | | 2001 | |

Puerto Rico | | USA - PR | | Coal | | | 454 | | | | 100 | % | | | 2002 | |

Deepwater | | USA - TX | | Pet Coke | | | 160 | | | | 100 | % | | | 1986 | |

| | | | | | | | | | | | | | | | |

| | | | | | | 8,240 | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| (1) | These businesses met the held for sale criteria in February 2012 and the sale transactions subsequently closed in April 2012. The earnings from these businesses will be reported as part of discontinued operations through the dates of transaction close. See Note 22—Discontinued Operations and Held for Sale Businesses to theConsolidated Financial Statements for further information. |

8

Generation under construction

| | | | | | | | | | | | | | | | |

Business | | Location | | Fuel | | Gross

MW | | | AES Equity

Interest

(Percent,

Rounded) | | | Expected

Year of

Commercial

Operations | |

Trinidad | | Trinidad | | Gas | | | 394 | | | | 10 | % | | | 2012 | |

North America Utilities. AES has two integrated utilities in North America, IPL, which it owns through IPALCO Enterprises, Inc. (“IPALCO”), the parent holding company of IPL and The Dayton Power and Light Company (“DP&L”), which it owns through DPL Inc. (“DPL”), the parent company of DP&L. IPL generates, transmits, distributes and sells electricity to approximately 470,000 customers in the city of Indianapolis and neighboring areas within the state of Indiana. IPL owns and operates four generating stations. Two of the generating stations are primarily coal-fired stations. The third station has a combination of units that use coal (base load capacity) and natural gas and/or oil (peaking capacity) for fuel to produce electricity. The fourth station is a small peaking station that uses gas-fired combustion turbine technology for the production of electricity. IPL’s gross electric generation capacity is 3,699 MW. Approximately 45% of IPL’s coal is provided by one supplier with which IPL has long-term contracts. A key driver for the business is tariff recovery for environmental projects through the rate adjustment process. IPL’s customers include residential, industrial, commercial and all other which made up 33%, 13%, 36% and 6%, respectively, of North America Utilities revenue for 2011. The remaining 12% of North America Utilities revenue is from DPL.

DP&L generates, transmits, distributes and sells electricity to more than 500,000 customers in a 6,000 square mile area of West Central Ohio. DP&L, with certain other Ohio utilities and their affiliates, commonly owns seven coal-fired electric generating facilities and numerous transmission facilities. DP&L also has one wholly-owned coal-fired plant. DP&L is affiliated with DPL Energy, LLC (“DPLE”) which owns peaking generation units located in Ohio and Indiana. DP&L’s wholly-owned plants and share of the capacity of its jointly-owned plants and DPLE’s wholly-owned peaking units aggregates to approximately 3,817 MW. During the period November 28, 2011 through December 31, 2011, approximately 80% of DP&L’s coal was provided by four suppliers and DP&L has long-term contracts with three of them. DP&L’s customers include residential, commercial, industrial and governmental, which make up 67%, 21% and 12%, respectively, of DP&L’s revenue for the period after acquisition in November 2011.

Generation

| | | | | | | | | | | | | | | | |

Business | | Location | | Fuel | | Gross

MW | | | AES Equity

Interest

(Percent,

Rounded) | | | Year

Acquired

or Began

Operation | |

IPL(1) | | USA - IN | | Coal/Gas/Oil | | | 3,699 | | | | 100 | % | | | 2001 | |

DP&L(2) | | USA - OH | | Coal/Diesel/Solar | | | 3,817 | | | | 100 | % | | | 2011 | |

| | | | | | | | | | | | | | | | |

| | | | | | | 7,516 | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| (1) | IPL plants: Eagle Valley, Georgetown, Harding Street and Petersburg. |

| (2) | DP&L wholly-owned plants: Hutchings, Tait Units 1-3 and diesels, Yankee Street, Yankee Solar, Monument and Sidney. DP&L jointly-owned plants: Beckjord Unit 6, Conesville Unit 4, East Bend Unit 2, Killen, Miami Fort Units 7 & 8, Stuart and Zimmer. In addition to the above, DP&L, also owns a 4.9% equity ownership in OVEC, an electric generating company. OVEC has two plants in Cheshire, Ohio and Madison, Indiana with a combined generation capacity of approximately 2,655 MW. DP&L’s share of this generation capacity is approximately 111 MW. DPLE plants: Tait Units 4-7 and Montpelier Units 1-4. |

9

Distribution

| | | | | | | | | | | | | | | | | | |

Business | | Location | | Approximate

Number of

Customers Served as

of 12/31/2011 | | | GWh

Sold in

2011 | | | AES Equity

Interest

(Percent,

Rounded) | | | Year

Acquired | |

IPL | | USA - IN | | | 470,000 | | | | 15,647 | | | | 100 | % | | | 2001 | |

DP&L(1) | | USA - OH | | | 500,000 | | | | 1,243 | | | | 100 | % | | | 2011 | |

| | | | | | | | | | | | | | | | | | |

| | | | | 970,000 | | | | 16,890 | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| (1) | GWh sold from the acquisition on November 28, 2011 through December 31, 2011. |

Europe

The following table provides highlights of our Europe operations:

| | |

| Countries | | Bulgaria, Hungary, Jordan, Kazakhstan, Netherlands, Spain, Turkey, Ukraine and the United Kingdom |

| Generation Capacity | | 8,779 Gross MW |

| Utilities Penetration | | 1.8 million customers (10,862 GWh) |

| Generation Facilities | | 20 |

| Utilities Businesses | | 4 |

| Key Generation Businesses | | Maritza, Ballylumford, Kilroot |

| Key Utilities Businesses | | Kievoblenergo and Rivneenergo |

Our Utilities operations in Europe are discussed further under Corporate and Other below.

Europe Generation. Our Generation operations in Europe accounted for 9%, 8% and 6% of our consolidated revenue in 2011, 2010 and 2009, respectively. In 2011, our Maritza facility in Bulgaria, a 670 MW coal-fired plant, commenced commercial operations. As a result of the announced sale of 80% of our interest in Cartagena, a 1,199 MW gas-fired plant in Spain, we have classified Cartagena as “held for sale” on the Consolidated Balance Sheets. AES operates four power plants in Kazakhstan which account for 8% of the country’s total installed generation capacity. In the United Kingdom, we own and operate more than 1,900 MW at the Ballylumford plant and the Kilroot facility. See Note 16—Segment and Geographic Information in the Consolidated Financial Statements in Item 8 of this Form 8-K for revenue, Adjusted Gross Margin (a non-GAAP measure) and total assets by segment. Key business drivers of this segment are: foreign currency exchange rates, new legislation and regulations including those related to the environment.

Set forth below is a list of our Europe Generation facilities:

Generation

| | | | | | | | | | | | | | | | |

Business | | Location | | Fuel | | Gross

MW | | | AES Equity

Interest

(Percent,

Rounded) | | | Year

Acquired

or Began

Operation | |

Maritza | | Bulgaria | | Coal | | | 670 | | | | 100 | % | | | 2011 | |

Tisza II | | Hungary | | Gas/Oil | | | 900 | | | | 100 | % | | | 1996 | |

Amman East | | Jordan | | Gas | | | 380 | | | | 37 | % | | | 2009 | |

Shulbinsk HPP(1) | | Kazakhstan | | Hydro | | | 702 | | | | 0 | % | | | 1997 | |

Sogrinsk CHP | | Kazakhstan | | Coal | | | 301 | | | | 100 | % | | | 1997 | |

Ust - Kamenogorsk HPP(1) | | Kazakhstan | | Hydro | | | 331 | | | | 0 | % | | | 1997 | |

Ust - Kamenogorsk CHP | | Kazakhstan | | Coal | | | 1,354 | | | | 100 | % | | | 1997 | |

Elsta(2) | | Netherlands | | Gas | | | 630 | | | | 50 | % | | | 1998 | |

Cartagena(3) | | Spain | | Gas | | | 1,199 | | | | 71 | % | | | 2006 | |

Damlapinar(2),(4) | | Turkey | | Hydro | | | 16 | | | | 51 | % | | | 2010 | |

Girlevik II-Mercan(2),(4) | | Turkey | | Hydro | | | 12 | | | | 51 | % | | | 2007 | |

Kepezkaya(2),(4) | | Turkey | | Hydro | | | 28 | | | | 51 | % | | | 2010 | |

Yukari-Mercan(2),(4) | | Turkey | | Hydro | | | 14 | | | | 51 | % | | | 2007 | |

Kumkoy(2),(4) | | Turkey | | Hydro | | | 18 | | | | 51 | % | | | 2011 | |

Bursa(2),(5) | | Turkey | | Gas | | | 156 | | | | 50 | % | | | 2011 | |

Kocaeli(2),(5) | | Turkey | | Gas | | | 158 | | | | 50 | % | | | 2011 | |

Istanbul (Koc University)(2),(5) | | Turkey | | Gas | | | 2 | | | | 50 | % | | | 2011 | |

Ballylumford | | United Kingdom | | Natural Gas | | | 1,246 | | | | 100 | % | | | 2010 | |

Kilroot(6) | | United Kingdom | | Coal/Gas/Oil | | | 662 | | | | 99 | % | | | 1992 | |

| | | | | | | | | | | | | | | | |

| | | | | | | 8,779 | | | | | | | | | |

| | | | | | | | | | | | | | | | |

10

| (1) | AES operates these facilities under concession agreements until 2017. |

| (2) | Unconsolidated entities, the results of operations of which are reflected in Equity in Earnings of Affiliates. |

| (3) | In October 2011, the Company met held for sale criteria and expects to dispose of 80% of its interest in this business within the next twelve months. Until the business is sold, it will be reported as a held for sale business on the Consolidated Balance Sheets and reflected in continuing operations on the Consolidated Statements of Operations, as the Company continues to hold an ownership interest in the business. |

| (4) | Joint Venture with I.C. Energy. |

| (5) | Joint Venture with Koc Holding. |

| (6) | Includes Kilroot Open Cycle Gas Turbine (“OCGT”). |

Asia

Our Asia operations accounted for 4%, 4% and 3% of consolidated revenue in 2011, 2010 and 2009, respectively. Asia’s Generation business operates 7 power plants with a total capacity of 3,802 MW in four countries. In Asia, AES operates generation facilities only. See Note 16—Segment and Geographic Information in the Consolidated Financial Statements in Item 8 of this Form 8-K for revenue, Adjusted Gross Margin (a non-GAAP measure) and total assets by segment. The following table provides highlights of our Asia operations:

| | |

Countries | | China, India, the Philippines and Sri Lanka |

Generation Capacity | | 3,802 Gross MW |

Utilities Penetration | | None |

Generation Facilities | | 8 (including 1 under construction) |

Utilities Businesses | | None |

Key Businesses | | Masinloc, Kelanitissa and Yangcheng |

Asia Generation. More than half of our generation capacity in Asia is located in China. In 1996, AES joined with Chinese partners to build Yangcheng, the first “coal-by-wire” power plant with the generation capacity of 2,100 MW. In April 2008, the Company completed the purchase of a 92% interest in a 660 MW coal-fired thermal power generation facility in Masinloc, Philippines (“Masinloc”).

Set forth below is a list of our generation facilities in Asia:

Generation

| | | | | | | | | | | | | | | | |

Business | | Location | | Fuel | | Gross

MW | | | AES Equity

Interest

(Percent,

Rounded) | | | Year

Acquired

or Began

Operation | |

Chengdu(1) | | China | | Gas | | | 50 | | | | 35 | % | | | 1997 | |

Cili | | China | | Hydro | | | 25 | | | | 51 | % | | | 1994 | |

JHRH(1) | | China | | Hydro | | | 379 | | | | 35 | % | | | 2010 | |

Yangcheng(1) | | China | | Coal | | | 2,100 | | | | 25 | % | | | 2001 | |

OPGC(1) | | India | | Coal | | | 420 | | | | 49 | % | | | 1998 | |

Masinloc | | Philippines | | Coal | | | 660 | | | | 92 | % | | | 2008 | |

Kelanitissa | | Sri Lanka | | Diesel | | | 168 | | | | 90 | % | | | 2003 | |

| | | | | | | | | | | | | | | | |

| | | | | | | 3,802 | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| (1) | Unconsolidated entities for which the results of operations are reflected in Equity in Earnings of Affiliates. |

11

Generation under construction

| | | | | | | | | | | | | | | | |

Business | | Location | | Fuel | | Gross

MW | | | AES Equity

Interest

(Percent,

Rounded) | | | Expected

Year of

Commercial

Operation | |

Mong Duong II | | Vietnam | | Coal | | | 1,200 | | | | 51 | % | | | 2015 | |

Corporate and Other

“Corporate and Other” includes the net operating results from our Utilities businesses in Africa and Europe, Africa Generation and Wind Generation and other renewables projects. These operations do not require separate segment disclosure. The following provides additional details about our Utilities businesses in Africa and Europe, Africa generation and Wind Generation, which are reported within “Corporate and Other” for financial reporting purposes.

Europe Utilities. Our distribution businesses in the Ukraine and Kazakhstan together serve approximately 1.8 million customers.

Distribution

| | | | | | | | | | | | | | | | | | |

Business | | Location | | Approximate

Number of

Customers Served as

of 12/31/2011 | | | GWh

Sold in

2011 | | | AES Equity

Interest

(Percent,

Rounded) | | | Year

Acquired | |

Eastern Kazakhstan REC(1),(2),(3) | | Kazakhstan | | | 459,000 | | �� | | 3,444 | | | | 0 | % | | | | |

Ust-Kamenogorsk Heat Nets(1),(4) | | Kazakhstan | | | 96,000 | | | | — | | | | 0 | % | | | | |

Kievoblenergo | | Ukraine | | | 874,000 | | | | 5,079 | | | | 89 | % | | | 2001 | |

Rivneenergo | | Ukraine | | | 409,000 | | | | 2,339 | | | | 84 | % | | | 2001 | |

| | | | | | | | | | | | | | | | | | |

| | | | | 1,838,000 | | | | 10,862 | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| (1) | AES operates these businesses through management agreements and owns no equity interest in these businesses. |

| (2) | In November 2011, AES sent notification to the Kazakhstan Government regarding the early termination of the management agreement for these companies. Transfer of management rights to the Kazakhstan Government should be completed within 180 days. |

| (3) | Shygys Energo Trade, a retail electricity company, is 100% owned by Eastern Kazakhstan REC (“EK REC”) and purchases distribution service from EK REC and electricity in the wholesale electricity market and resells to the distribution customers of EK REC. |

| (4) | Ust-Kamenogorsk Heat Nets provide transmission and distribution of heat with a total heat generating capacity of 224 Gcal. |

Africa Utilities. AES owns a 56% interest in an integrated utility, Société Nationale d’Electricité (“Sonel”). Sonel generates, transmits and distributes electricity to over half a million people and is the sole distributor of electricity in Cameroon.

Set forth below is a list of the generation and distribution facilities of Sonel:

Sonel’s generation facilities

| | | | | | | | | | | | | | | | |

Business | | Location | | Fuel | | Gross

MW | | | AES Equity

Interest

(Percent,

Rounded) | | | Year

Acquired

or Began

Operation | |

Sonel(1) | | Cameroon | | Hydro/Diesel/Heavy Fuel Oil | | | 936 | | | | 56 | % | | | 2001 | |

| (1) | Sonel plants: Bafoussam, Bassa, Djamboutou, Edéa, Lagdo, Limbé, Logbaba I, Logbaba II, Oyomabang I, Oyomabang II, Song Loulou, and other small remote network units. |

12

Sonel’s distribution facility

| | | | | | | | | | | | | | | | | | |

Business | | Location | | Approximate

Number of

Customers Served as

of 12/31/2011 | | | GWh

Sold in

2011 | | | AES Equity

Interest

(Percent,

Rounded) | | | Year

Acquired | |

Sonel | | Cameroon | | | 660,000 | | | | 3,345 | | | | 56 | % | | | 2001 | |

Africa Generation. Set forth below is a list of our generation facilities in Africa:

Generation

| | | | | | | | | | | | | | | | |

Business | | Location | | Fuel | | Gross

MW | | | AES Equity

Interest

(Percent,

Rounded) | | | Year

Acquired

or Began

Operation | |

Dibamba | | Cameroon | | Heavy Fuel Oil | | | 86 | | | | 56 | % | | | 2009 | |

Ebute | | Nigeria | | Gas | | | 294 | | | | 95 | % | | | 2001 | |

| | | | | | | | | | | | | | | | |

| | | | | | | 380 | | | | | | | | | |

| | | | | | | | | | | | | | | | |

Generation under construction

| | | | | | | | | | | | | | | | |

Business | | Location | | Fuel | | Gross

MW | | | AES Equity

Interest

(Percent,

Rounded) | | | Expected

Year of

Commercial

Operations | |

Kribi | | Cameroon | | Gas | | | 216 | | | | 56 | % | | | 2013 | |

Wind Generation. We own and operate 1,616 MW of wind generation capacity and operate an additional 134 MW of capacity through operating and management agreements. Our wind business is located primarily in North America where we operate wind generation facilities that have generation capacity of 1,266 MW.

Set forth below is a list of Wind Generation facilities:

Generation

| | | | | | | | | | | | | | | | |

Business | | Location | | Power Source | | Gross

MW | | | AES Equity

Interest

(Percent,

Rounded) | | | Year

Acquired

or Began

Operation | |

St. Nikola | | Bulgaria | | Wind | | | 156 | | | | 89 | % | | | 2010 | |

Dong Qi(1),(2) | | China | | Wind | | | 49 | | | | 49 | % | | | 2010 | |

Huanghua I(1),(2) | | China | | Wind | | | 49 | | | | 49 | % | | | 2009 | |

Huanghua II(1),(2) | | China | | Wind | | | 49 | | | | 49 | % | | | 2010 | |

Hulunbeier(1),(2) | | China | | Wind | | | 49 | | | | 49 | % | | | 2008 | |

InnoVent(2),(3) | | France | | Wind | | | 75 | | | | 40 | % | | | 2003-2009 | |

St. Patrick | | France | | Wind | | | 35 | | | | 100 | % | | | 2010 | |

North Rhins | | Scotland | | Wind | | | 22 | | | | 100 | % | | | 2010 | |

Altamont | | USA - CA | | Wind | | | 40 | | | | 100 | % | | | 2005 | |

Mountain View I & II(4) | | USA - CA | | Wind | | | 67 | | | | 100 | % | | | 2008 | |

Palm Springs | | USA - CA | | Wind | | | 30 | | | | 100 | % | | | 2005 | |

Tehachapi | | USA - CA | | Wind | | | 38 | | | | 100 | % | | | 2006 | |

Storm Lake II(4) | | USA - IA | | Wind | | | 78 | | | | 100 | % | | | 2007 | |

Lake Benton I(4) | | USA - MN | | Wind | | | 106 | | | | 100 | % | | | 2007 | |

Condon(4) | | USA - OR | | Wind | | | 50 | | | | 100 | % | | | 2005 | |

Armenia Mountain(4) | | USA - PA | | Wind | | | 101 | | | | 100 | % | | | 2009 | |

Buffalo Gap I(4) | | USA - TX | | Wind | | | 121 | | | | 100 | % | | | 2006 | |

Buffalo Gap II(4) | | USA - TX | | Wind | | | 233 | | | | 100 | % | | | 2007 | |

Buffalo Gap III(4) | | USA - TX | | Wind | | | 170 | | | | 100 | % | | | 2008 | |

Laurel Mountain | | USA - WV | | Wind | | | 98 | | | | 100 | % | | | 2011 | |

Wind generation facilities(5) | | USA | | Wind | | | 134 | | | | 0 | % | | | 2005 | |

| | | | | | | | | | | | | | | | |

| | | | | | | 1,750 | | | | | | | | | |

| | | | | | | | | | | | | | | | |

13

| (1) | Joint Venture with Guohua Energy Investment Co. Ltd. |

| (2) | Unconsolidated entities for which the results of operations are reflected in Equity in Earnings of Affiliates. |

| (3) | InnoVent plants: Bignan, Chepy, Croixrault-Moyencourt, Eurotunel, Frenouville, Gapree, Grand Fougeray, Guehenno, Hargicourt, Hescamps, LePortal, Les Diagots, Nibas, Plechatel, Saint-Hilaire la Croix and Valhoun. InnoVent owns various percentages of underlying projects. |

| (4) | AES owns these assets together with third party tax equity investors with variable ownership interests. The tax equity investors receive a portion of the economic attributes of the facilities, including tax attributes that vary over the life of the projects. The proceeds from the issuance of tax equity are recorded as Noncontrolling Interest in the Company’s Consolidated Balance Sheets. |

| (5) | AES operates these facilities through management or O&M agreements and owns no equity interest in these businesses. |

Wind Generation projects under construction

| | | | | | | | | | | | | | | | |

Business | | Location | | Power Source | | Gross

MW | | | AES Equity

Interest

(Percent,

Rounded) | | | Expected

Year of

Commercial

Operation | |

InnoVent(1) | | France | | Wind | | | 39 | | | | 40 | % | | | 2012 | |

Chen Qi(2) | | China | | Wind | | | 49 | | | | 49 | % | | | 2012 | |

Saurashtra | | India | | Wind | | | 39 | | | | 100 | % | | | 2012 | |

Drone Hill | | United Kingdom | | Wind | | | 29 | | | | 100 | % | | | 2012 | |

Mountain View IV | | US-CA | | Wind | | | 49 | | | | 100 | % | | | 2012 | |

| | | | | | | | | | | | | | | | |

| | | | | | | 205 | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| (1) | InnoVent plants: Allery, Audrieu, Lamballe, Lefaux and Vron. InnoVent owns various percentages of underlying projects. |

| (2) | Joint Venture with Guohua Energy Investment Co. Ltd. |

Other. AES Solar and certain other unconsolidated businesses are accounted for using the equity method of accounting. Therefore, their operating results are included in “Net Equity in Earnings of Affiliates” on the face of the Consolidated Statements of Operations, not in revenue and gross margin. AES Solar was formed in March 2008 to develop, own and operate solar installations. Since its launch, AES Solar has commenced commercial operations of 151 MW of solar projects in Bulgaria, France, Greece, Italy and Spain; and has 106 MW under construction in Bulgaria, France, Greece, India, Italy and the U.S.

“Corporate and Other” also includes costs related to corporate overhead which are not directly associated with the operations of our six reportable segments and other intercompany charges such as self-insurance premiums which are fully eliminated in consolidation. See Note 16—Segment and Geographic Information in the Consolidated Financial Statements in Item 8 of this Form 8-K for information on revenue from external customers, Adjusted Gross Margin (a non-GAAP measure) and total assets by segment.

14

Financial Data by Country

The table below presents information, by country, about our consolidated operations for each of the three years ended December 31, 2011, 2010 and 2009, respectively, and property, plant and equipment as of December 31, 2011 and 2010, respectively. Revenue is recognized in the country in which it is earned and assets are reflected in the country in which they are located.

| | | | | | | | | | | | | | | | | | | | |

| | | Revenue | | | Property, Plant &

Equipment, net | |

| | | 2011 | | | 2010 | | | 2009 | | | 2011 | | | 2010 | |

| | | (in millions) | |

United States(1) | | $ | 2,110 | | | $ | 1,952 | | | $ | 1,851 | | | $ | 7,829 | | | $ | 5,379 | |

| | | | | | | | | | | | | | | | | | | | |

Non-U.S.: | | | | | | | | | | | | | | | | | | | | |

Brazil(2) | | | 6,640 | | | | 6,355 | | | | 5,292 | | | | 5,896 | | | | 6,263 | |

Chile | | | 1,608 | | | | 1,355 | | | | 1,239 | | | | 2,781 | | | | 2,560 | |

Argentina(3) | | | 979 | | | | 771 | | | | 571 | | | | 279 | | | | 270 | |

El Salvador | | | 752 | | | | 648 | | | | 619 | | | | 268 | | | | 261 | |

Dominican Republic | | | 674 | | | | 535 | | | | 429 | | | | 662 | | | | 625 | |

United Kingdom(4) | | | 587 | | | | 364 | | | | 228 | | | | 523 | | | | 507 | |

Philippines | | | 480 | | | | 501 | | | | 250 | | | | 766 | | | | 784 | |

Ukraine | | | 418 | | | | 356 | | | | 286 | | | | 94 | | | | 86 | |

Mexico | | | 404 | | | | 409 | | | | 329 | | | | 774 | | | | 786 | |

Cameroon | | | 386 | | | | 422 | | | | 370 | | | | 901 | | | | 823 | |

Colombia | | | 365 | | | | 393 | | | | 347 | | | | 384 | | | | 387 | |

Puerto Rico | | | 298 | | | | 253 | | | | 267 | | | | 581 | | | | 596 | |

Spain(5) | | | 258 | | | | 411 | | | | — | | | | — | | | | — | |

Bulgaria(6) | | | 251 | | | | 44 | | | | — | | | | 1,619 | | | | 1,825 | |

Hungary(7) | | | 204 | | | | 252 | | | | 259 | | | | 6 | | | | 73 | |

Panama | | | 189 | | | | 194 | | | | 168 | | | | 1,040 | | | | 921 | |

Kazakhstan | | | 145 | | | | 138 | | | | 123 | | | | 86 | | | | 63 | |

Sri Lanka | | | 140 | | | | 100 | | | | 109 | | | | 22 | | | | 69 | |

Jordan | | | 124 | | | | 120 | | | | 104 | | | | 216 | | | | 224 | |

Qatar(8) | | | — | | | | — | | | | — | | | | — | | | | — | |

Pakistan(9) | | | — | | | | — | | | | — | | | | — | | | | — | |

Oman(10) | | | — | | | | — | | | | — | | | | — | | | | — | |

Other Non-U.S.(11) | | | 116 | | | | 112 | | | | 133 | | | | 395 | | | | 291 | |

| | | | | | | | | | | | | | | | | | | | |

Total Non-U.S. | | | 15,018 | | | | 13,733 | | | | 11,123 | | | | 17,293 | | | | 17,414 | |

| | | | | | | | | | | | | | | | | | | | |

Total | | $ | 17,128 | | | $ | 15,685 | | | $ | 12,974 | | | $ | 25,122 | | | $ | 22,793 | |

| | | | | | | | | | | | | | | | | | | | |

| (1) | Excludes revenue of $374 million, $662 million and $695 million for the years ended December 31, 2011, 2010 and 2009, respectively, and property, plant and equipment of $619 million and $788 million as of December 31, 2011 and 2010, respectively, related to Eastern Energy, Thames, Ironwood and Red Oak which were reflected as discontinued operations and businesses held for sale in the accompanying Consolidated Statements of Operations and Consolidated Balance Sheets. |

| (2) | Excludes revenue of $124 million, $118 million and $102 million for the years ended December 31, 2011, 2010 and 2009, respectively, and property, plant and equipment of $151 million as of December 31, 2010, related to Brazil Telecom, which was reflected as discontinued operations and businesses held for sale in the accompanying Consolidated Statements of Operations and Consolidated Balance Sheets. |

| (3) | Excludes revenue of $102 million, $116 million and $113 million for the years ended December 31, 2011, 2010 and 2009, respectively, and property, plant and equipment of $189 million as of December 31, 2010, related to our Argentina distribution businesses, which were reflected as discontinued operations and businesses held for sale in the accompanying Consolidated Statements of Operations and Consolidated Balance Sheets. |

15

| (4) | Excludes revenue of $17 million, $21 million and $11 million for the years ended December 31, 2011, 2010 and 2009, respectively, and property, plant and equipment of $20 million as of December 31, 2010, related to carbon reduction projects, which were reflected as discontinued operations and businesses held for sale in the accompanying Consolidated Statements of Operations and Consolidated Balance Sheets. |

| (5) | Excludes property, plant and equipment of $620 million and $667 million as of December 31, 2011 and 2010, respectively, related to Cartagena, which was reflected as businesses held for sale in the accompanying Consolidated Balance Sheets. |

| (6) | Maritza and our wind project in Bulgaria were under development and therefore not operational as of December 31, 2009. Our wind project in Bulgaria started operations in 2010 and Maritza started operations in June 2011. |

| (7) | Excludes revenue of $14 million, $44 million and $58 million for the years ended December 31, 2011, 2010 and 2009, respectively, and property, plant and equipment of $7 million as of December 31, 2010, related to Borsod and Tiszapalkonya, which were reflected as discontinued operations and businesses held for sale in the accompanying Consolidated Statements of Operations and Consolidated Balance Sheets. |

| (8) | Excludes revenue of $129 million and $163 million for the years ended December 31, 2010 and 2009, respectively, related to Ras Laffan, which was reflected as discontinued operations and businesses held for sale in the accompanying Consolidated Statements of Operations. |

| (9) | Excludes revenue of $299 million and $470 million for the years ended December 31, 2010 and 2009, respectively, related to Lal Pir and Pak Gen, which were reflected as discontinued operations and businesses held for sale in the accompanying Consolidated Statements of Operations. |

| (10) | Excludes revenue of $62 million and $101 million for the years ended December 31, 2010 and 2009, respectively, related to Barka, which was reflected as discontinued operations and businesses held for sale in the accompanying Consolidated Statements of Operations. |

| (11) | Excludes revenue of $1 million for the year ended December 31, 2011, and property, plant and equipment of $2 million and $18 million as of December 31, 2011, and 2010, respectively, related to alternative energy and carbon reduction projects, which were reflected as discontinued operations and businesses held for sale in the accompanying Consolidated Statements of Operations and Consolidated Balance Sheets. |

| ITEM 6. | SELECTED FINANCIAL DATA |

The following table sets forth our selected financial data as of the dates and for the periods indicated. You should read this data together with Item 7.—Management’s Discussion and Analysis of Financial Condition and Results of Operations and the Consolidated Financial Statements and the notes thereto included in Item 8 of this Form 8-K. The selected financial data for each of the years in the five year period ended December 31, 2011 have been derived from our audited Consolidated Financial Statements. Prior period amounts have been restated to reflect discontinued operations in all periods presented. Our historical results are not necessarily indicative of our future results.

Acquisitions, disposals, reclassifications and changes in accounting principles affect the comparability of information included in the tables below. Please refer to the Notes to the Consolidated Financial Statements included in Item 8.—Financial Statements and Supplementary Data of this Form 8-K for further explanation of the effect of such activities. Please also refer to Item 1A.—Risk Factors of the 2011 Form 10-K and Note 25—Risks and Uncertainties to the Consolidated Financial Statements included in Item 8 of this Form 8-K for certain risks and uncertainties that may cause the data reflected herein not to be indicative of our future financial condition or results of operations.

16

SELECTED FINANCIAL DATA

| | | | | | | | | | | | | | | | | | | | |

| | | Year Ended December 31, | |

| Statement of Operations Data | | 2011(1) | | | 2010 | | | 2009 | | | 2008 | | | 2007 | |

| | | (in millions, except per share amounts) | |

| | | | | |

Revenue | | $ | 17,128 | | | $ | 15,685 | | | $ | 12,974 | | | $ | 14,034 | | | $ | 11,739 | |

Income from continuing operations(2) | | | 1,534 | | | | 1,461 | | | | 1,798 | | | | 1,836 | | | | 552 | |

| | | | | |

Income from continuing operations attributable to The AES Corporation, net of tax | | | 451 | | | | 476 | | | | 718 | | | | 1,093 | | | | 172 | |

Discontinued operations, net of tax | | | (393 | ) | | | (467 | ) | | | (60 | ) | | | 141 | | | | (267 | ) |

Net income (loss) attributable to The AES Corporation | | $ | 58 | | | $ | 9 | | | $ | 658 | | | $ | 1,234 | | | $ | (95 | ) |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Basic (loss) earnings per share: | | | | | | | | | | | | | | | |

Income from continuing operations attributable to The AES Corporation, net of tax | | $ | 0.58 | | | $ | 0.62 | | | $ | 1.08 | | | $ | 1.63 | | | $ | 0.26 | |

Discontinued operations, net of tax | | | (0.51 | ) | | | (0.61 | ) | | | (0.09 | ) | | | 0.21 | | | | (0.40 | ) |

| | | | | | | | | | | | | | | | | | | | |

Basic earnings (loss) per share | | $ | 0.07 | | | $ | 0.01 | | | $ | 0.99 | | | $ | 1.84 | | | $ | (0.14 | ) |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Diluted (loss) earnings per share: | | | | | | | | | | | | | | | |

Income from continuing operations attributable to The AES Corporation, net of tax | | $ | 0.58 | | | $ | 0.62 | | | $ | 1.07 | | | $ | 1.62 | | | $ | 0.25 | |

Discontinued operations, net of tax | | | (0.51 | ) | | | (0.61 | ) | | | (0.09 | ) | | | 0.20 | | | | (0.39 | ) |

| | | | | | | | | | | | | | | | | | | | |

Diluted earnings (loss) per share | | $ | 0.07 | | | $ | 0.01 | | | $ | 0.98 | | | $ | 1.82 | | | $ | (0.14 | ) |

| | | | | | | | | | | | | | | | | | | | |

| |

| | | December 31, | |

| Balance Sheet Data: | | 2011(1) | | | 2010 | | | 2009 | | | 2008 | | | 2007 | |

| | | (in millions) | |

Total assets | | $ | 45,333 | | | $ | 40,511 | | | $ | 39,535 | | | $ | 34,806 | | | $ | 34,453 | |

Non-recourse debt (long-term) | | $ | 13,412 | | | $ | 11,084 | | | $ | 11,532 | | | $ | 10,443 | | | $ | 9,794 | |

Non-recourse debt (long-term) - Discontinued operations | | $ | 1,198 | | | $ | 1,460 | | | $ | 1,332 | | | $ | 1,426 | | | $ | 1,536 | |

Recourse debt (long-term) | | $ | 6,180 | | | $ | 4,149 | | | $ | 5,301 | | | $ | 4,994 | | | $ | 5,332 | |

Cumulative preferred stock of a subsidiary | | $ | 78 | | | $ | 60 | | | $ | 60 | | | $ | 60 | | | $ | 60 | |

Retained earnings (accumulated deficit) | | $ | 678 | | | $ | 620 | | | $ | 650 | | | $ | (8 | ) | | $ | (1,241 | ) |

The AES Corporation stockholders’ equity | | $ | 5,946 | | | $ | 6,473 | | | $ | 4,675 | | | $ | 3,669 | | | $ | 3,164 | |

| (1) | DPL was acquired on November 28, 2011 and its results of operations have been included in AES’ consolidated results of operations from the date of acquisition. See Note 23—Acquisitions and Dispositions to the Consolidated Financial Statements included in Item 8.—Financial Statements and Supplementary Data of this Form 8-K for further information. |

| (2) | Includes pretax impairment expense of $242 million, $410 million, $142 million, $175 million and $408 million for the years ended December 31, 2011, 2010, 2009, 2008 and 2007, respectively. |

| ITEM 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

Overview of Our Business

We are a global power company. We operate two primary lines of business. The first is our Generation business, where we own and/or operate power plants to generate and sell power to wholesale customers such as utilities, other intermediaries and certain end-users. The second is our Utilities business, where we own and/or operate utilities which distribute, transmit and sell electricity to end-user customers in the residential, commercial, industrial and governmental sectors within a defined service area and in certain circumstances, generate and sell

17

electricity on the wholesale market. For the year ended December 31, 2011, our Generation and Utilities businesses comprised approximately 45% and 55% of our consolidated revenue, respectively. For additional information regarding our business, see Item 1.—Business of this Form 8-K.

Our wind and solar businesses are not material contributors to our operating results. For additional information regarding our business, see Item 1.—Business of this Form 8-K.

Our Organization—The management reporting structure is organized along our two lines of business—Generation and Utilities. These lines of businesses are further disaggregated geographically for management reporting. Accordingly, management’s discussion and analysis of revenue and gross margin is organized as follows:

| | • | | Generation—Latin America; |

| | • | | Generation—North America; |

| | • | | Utilities—Latin America; |

| | • | | Utilities—North America; |

As discussed in Note 16—Segment and Geographic Information, based on application of the segment accounting guidance, Tietê is reported as a separate segment for purposes of the required segment accounting disclosures, but is included in Generation—Latin America within the discussion of operating results for revenue and gross margin in management’s discussion and analysis as is it managed with the other Latin American generation businesses.

Corporate and Other—The Company’s Europe Utilities, Africa Utilities, Africa Generation, Wind Generation operating segments and climate solutions and other renewables projects are reported within “Corporate and Other” because they do not meet the criteria to allow for aggregation with another operating segment or the quantitative thresholds that would require separate disclosure under segment reporting accounting guidance. None of these operating segments are currently material to our financial statement presentation of reportable segments, individually or in the aggregate. “Corporate and Other” also includes costs related to corporate overhead which are not directly associated with the operations of our six reportable segments and other intercompany charges such as self-insurance premiums which are fully eliminated in consolidation.

Components of Revenue and Cost of Sales—Revenue includes revenue earned from the sale of energy from our utilities and the production of energy from our generation plants, which are classified as regulated and non-regulated on the Consolidated Statements of Operations, respectively. Revenue also includes the gains or losses on derivatives (including embedded derivatives other than foreign currency embedded derivatives) associated with the sale of electricity. Cost of sales includes costs incurred directly by the businesses in the ordinary course of business. Examples include electricity and fuel purchases, maintenance, operations, non-income taxes and bad debt expense and recoveries as well as depreciation and general and administrative and support costs, including employee-related costs, that are directly associated with the operations of a particular business. Cost of sales also includes the gains or losses on derivatives (including embedded derivatives other than foreign currency embedded derivatives) associated with the purchase of electricity or fuel.

Key Drivers of Our Results. Our Generation and Utilities businesses are distinguished by the nature of their customers, operational differences, cost structure, regulatory environment and risk exposure. As a result, each line of business has different drivers which affect operating results. Performance drivers for our Generation businesses include, among other things, plant reliability and efficiency, power prices, volume, management of fixed and variable operating costs, management of working capital including collection of receivables, and the extent to which our plants have hedged their exposure to currency and commodities such as fuel. For our Generation businesses which sell power under short-term contracts or in the spot market, the most crucial factors are the current market price of electricity and the marginal costs of production. Growth in our Generation business is largely tied to securing new PPAs, expanding capacity in our existing facilities and building or acquiring new power plants. Performance drivers for our Utilities businesses include, but are not limited to, reliability of service; management of

18

working capital, including collection of receivables; negotiation of tariff adjustments; compliance with extensive regulatory requirements; management of pension assets; and in developing countries, reduction of commercial and technical losses. The operating results of our Utilities businesses are sensitive to changes in inflation, economic growth and weather conditions in areas in which they operate. In addition to these drivers, as explained below, the Company also has exposure to currency exchange rate fluctuations.

One of the key factors which affect our Generation business is our ability to enter into contracts for the sale of electricity and the purchase of fuel used to produce that electricity. Long-term contracts are intended to reduce the exposure to volatility associated with fuel prices in the market and the price of electricity by fixing the revenue and costs for these businesses. The majority of the electricity produced by our Generation businesses is sold under long-term contracts, or PPAs, to wholesale customers. In turn, most of these businesses enter into long-term fuel supply contracts or fuel tolling arrangements where the customer assumes full responsibility for purchasing and supplying the fuel to the power plant. While these long-term contractual agreements reduce exposure to volatility in the market price for electricity and fuel, the predictability of operating results and cash flows vary by business based on the extent to which a facility’s generation capacity and fuel requirements are contracted and the negotiated terms of these agreements. Entering into these contracts exposes us to counterparty credit risk. For further discussion of these risks, see “Supplier and/or customer concentration may expose the Company to significant financial credit or performance risks.” in Item 1A.—Risk Factors of the 2011 Form 10-K.

When fuel costs increase, many of our businesses are able to pass these costs on to their customers. Generation businesses with long-term contracts in place do this by including fuel pass-through or fuel indexing arrangements in their contracts. Utilities businesses can pass costs on to their customers through increases in current or future tariff rates. Therefore, in a rising fuel cost environment, the increased fuel costs for these businesses often result in an increase in revenue to the extent these costs can be passed through (though not necessarily on a one-for-one basis). Conversely, in a declining fuel cost environment, the decreased fuel costs can result in a decrease in revenue. Increases or decreases in revenue at these businesses that have the ability to pass through costs to the customer have a corresponding impact on cost of sales, to the extent the costs can be passed through, resulting in a limited impact on gross margin, if any. Although these circumstances may not have a large impact on gross margin, they can significantly affect gross margin as a percentage of revenue. As a result, gross margin as a percentage of revenue is a less relevant measure when evaluating our operating performance. To the extent our businesses are unable to pass through fuel cost increases to their customers, gross margin may be adversely affected.

Global diversification also helps us mitigate risk. Our presence in mature markets helps mitigate the exposure associated with our businesses in emerging markets. Additionally, our portfolio employs a broad range of fuels, including coal, gas, fuel oil, water (hydroelectric power), wind and solar, which reduces the risks associated with dependence on any one fuel source. However, to the extent the mix of fuel sources enabling our generation capabilities in any one market is not diversified, the spread in costs of different fuels may also influence the operating performance and the ability of our subsidiaries to compete within that market. For example, in a market where gas prices fall to a low level compared to coal prices, power prices may be set by low gas prices which can affect the profitability of our coal plants in that market. In certain cases, we may attempt to hedge fuel prices to manage this risk, but there can be no assurance that these strategies will be effective.

We also attempt to limit risk by hedging much of our interest rate and commodity risk, and by matching the currency of most of our subsidiary debt to the revenue of the underlying business. However, we only hedge a portion of our currency and commodity risks, and our businesses are still subject to these risks, as further described in Item 1A.—Risk Factors of the 2011 Form 10-K, “We may not be adequately hedged against our exposure to changes in commodity prices or interest rates.” Commodity and power price volatility could continue to impact our financial metrics to the extent this volatility is not hedged. For a discussion of our sensitivities to commodity, currency and interest rate risk, see Item 7A.—Quantitative and Qualitative Disclosures About Market Risk of the 2011 Form 10-K.

Due to our global presence, the Company has significant exposure to foreign currency fluctuations. The exposure is primarily associated with the impact of the translation of our foreign subsidiaries’ operating results from their local currency to U.S. dollars that is required for the preparation of our consolidated financial statements. Additionally, there is a risk of transaction exposure when an entity enters into transactions, including debt agreements, in currencies other than their functional currency. These risks are further described in Item 1A.—Risk Factors of the 2011 Form 10-K, “Our financial position and results of operations may fluctuate significantly due to fluctuations in currency exchange rates experienced at our foreign operations.” In the year ended December 31,

19

2011, changes in foreign currency exchange rates have had a significant impact on our operating results. If the current foreign currency exchange rate volatility continues, our gross margin and other financial metrics could be affected.

Another key driver of our results is our ability to bring new businesses into commercial operations successfully and to integrate acquisitions. We currently have approximately 2,391 MW of projects under construction in nine countries. Our prospects for increased operating results and cash flows are dependent upon successful completion of these projects on time and within budget. However, as disclosed in Item 1A.—Risk Factors of the 2011 Form 10-K, “Our business is subject to substantial development uncertainties,” construction is subject to a number of risks, including risks associated with site identification, financing and permitting and our ability to meet construction deadlines. Delays or the inability to complete projects and commence commercial operations can result in increased costs, impairment of assets and other challenges involving partners and counterparties to our construction agreements, PPAs and other agreements. Similarly, failure to integrate acquisitions and manage market risk, including the Company’s recent acquisition of DPL, could impact our future operating results as disclosed in Item 1A.—Risk Factors of the 2011 Form 10-K, “After completion of the DPL acquisition, the Company, may fail to realize the anticipated benefits and cost savings of the acquisition, which could adversely affect the value of the Company’s common stock” andKey Trends and Uncertainties—Goodwill, below.

Our gross margin is also impacted by the fact that in each country in which we conduct business, we are subject to extensive and complex governmental regulations such as regulations governing the generation and distribution of electricity, and environmental regulations which affect most aspects of our business. Regulations differ on a country by country basis (and even at the state and local municipality levels) and are based upon the type of business we operate in a particular country, and affect many aspects of our operations and development projects. Our ability to negotiate tariffs, enter into long-term contracts, pass through costs related to capital expenditures and otherwise navigate these regulations can have an impact on our revenue, costs and gross margin. Environmental and land use regulations, including existing and proposed regulation of GHG emissions, could substantially increase our capital expenditures or other compliance costs, which could in turn have a material adverse effect on our business and results of operations. For a further discussion of the Regulatory Environment, see Item 1.—Business—Regulatory Matters—Environmental and Land Use Regulations and Item 1A.—Risk Factors—Risks Associated with Government Regulation and Laws of the 2011 Form 10-K.

Management’s Priorities

Management has re-evaluated its priorities following the appointment of its new CEO in September 2011. Management is focused on the following priorities:

| | • | | Execution of our geographic concentration strategy to maximize shareholder value through disciplined capital allocation including: |

| | • | | platform expansion in Brazil, Chile, Colombia, and the United States, |

| | • | | platform development in Turkey, Poland, and the United Kingdom, |

| | • | | corporate debt reduction, and |

| | • | | a return of capital to shareholders, including our intent to initiate a dividend in 2012; |

| | • | | Closing the sales of businesses for which we have signed agreements with counterparties and prudently exiting select non-strategic markets; |

| | • | | Optimizing profitability of operations in the existing portfolio; |

| | • | | Integration of DPL into our portfolio; |

| | • | | Implementing a management realignment of our businesses under two business lines: Utilities and Generation, and achieving cost savings through the alignment of overhead costs with business requirements, systems automation and optimal allocation of business development spending; and |

20

| | • | | Completion of an approximately 2,400 MW construction program and the integration of new projects into existing businesses. During the year ended December 31, 2011, the following projects commenced commercial operations: |

| | | | | | | | | | | | |

Project | | Location | | Fuel | | Gross

MW | | | AES Equity

Interest

(Percent,

Rounded) | |

| | | | |

AES Solar(1) | | Various | | Solar | | | 62 | | | | 50 | % |

Angamos | | Chile | | Coal | | | 545 | | | | 71 | % |

Changuinola | | Panama | | Hydro | | | 223 | | | | 100 | % |

Kumkoy(2) | | Turkey | | Hydro | | | 18 | | | | 51 | % |

Laurel Mountain | | US-WV | | Wind | | | 98 | | | | 100 | % |

Maritza | | Bulgaria | | Coal | | | 670 | | | | 100 | % |

Sao Joaquim | | Brazil | | Hydro | | | 3 | | | | 24 | % |

Trinidad(3) | | Trinidad | | Gas | | | 394 | | | | 10 | % |

| (1) | AES Solar Energy Ltd. is a Joint Venture with Riverstone Holdings and is accounted for as an equity method investment. Plants that came online during the year include: Kalipetrovo, Ugento, Soemina, Francavilla Fontana, Latina, Cocomeri, Francofonte, Scopeto, Sabaudia, Aprilla-1, Siracusa 1-3 Complex, Manduria Apollo and Rinaldone. |

| (2) | Joint Venture with I.C. Energy. |

| (3) | An equity method investment held by AES. |

Key Trends and Uncertainties

Our operations continue to face many risks as discussed in Item 1A.—Risk Factors of the 2011 Form 10-K. Some of these challenges are also described below in “Key Drivers of Results in 2011”. We continue to monitor our operations and address challenges as they arise.

Operations

In August 2010, the Esti power plant, a 120 MW run-of-river hydroelectric power plant in Panama, was taken offline due to damage to its tunnel infrastructure. AES Panama is partially covered for business interruption losses and property damage under existing insurance programs. The Esti power plant is currently being repaired and is projected to resume operations by the second quarter of 2012. However, due to the inherent uncertainties associated with construction, it is possible that commercial operations may resume after this timeframe which could impact our results for 2012.

Regulatory tariff revisions have a potential to adversely impact the results of our utility businesses. For example, Eletropaulo, our utility business in Brazil, is currently billing its customers under the pre-existing tariff as required by the regulator. In July 2011, the regulator postponed the review and reset of Eletropaulo’s regulated tariff, which includes a tariff component that determines the margin Eletropaulo is allowed to earn. The review and reset of the regulated tariff is performed every four years. Management believes that it is probable that the new tariff rate will be lower than the current tariff rate, resulting in future refunds to customers, and based on its best estimate continues to record the amount of estimated future refunds as a reduction of revenue and a regulatory liability. The estimate is sensitive to the key assumption regarding the regulatory asset base that will be used by the regulator to determine the return included in the revised tariff. This assumption is subject to ongoing discussions with the regulator. As the periodic review and reset process progresses with the regulator into 2012, it is at least reasonably possible that the estimated amount of refunds will change in amounts that could require more refunds than we currently expect, in amounts that could be material.

See Item 1—Business—Regulatory Matters—United States—The Dayton Power and Light Company included in the 2011 Form 10-K for further information regarding DPL’s expected filing with PUCO to propose either a new ESP or MRO to be effective January 1, 2013. The outcome of the proceeding could have a material impact on our results.

Global Economic Considerations

During the past few years, economic conditions in some countries where our subsidiaries conduct business have deteriorated. Global economic conditions remain volatile and could have an adverse impact on our businesses in the event these recent trends continue.

21