0000874766 us-gaap:InterestRateContractMember us-gaap:FairValueInputsLevel3Member us-gaap:FairValueMeasurementsRecurringMember 2018-12-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

____________________________________

FORM 10-Q

____________________________________

(Mark One)

| ☒ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended June 30, 2019

or

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ____________ to ______________

Commission file number 001-13958

____________________________________

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 13-3317783 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

One Hartford Plaza, Hartford, Connecticut 06155

(Address of principal executive offices) (Zip Code)

(860) 547-5000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| Common Stock, par value $0.01 per share | HIG | The New York Stock Exchange |

| 6.10% Notes due October 1, 2041 | HIG 41 | The New York Stock Exchange |

| 7.875% Fixed-to-Floating Rate Junior Subordinated Debentures due 2042 | HGH | The New York Stock Exchange |

| Depositary Shares, Each Representing a 1/1,000th Interest in a Share of 6.000% Non-Cumulative Preferred Stock, Series G, par value $0.01 per share | HIG PR G | The New York Stock Exchange |

1

| Indicate by check mark: | ||||

| • whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. | Yes | ☒ | No | ☐ |

| • whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). | Yes | ☒ | No | ☐ |

| • whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and "emerging growth company" in Rule 12b-2 of the Exchange Act. | ||||

| Large accelerated filer | ☒ | Accelerated filer | ☐ | Non-accelerated filer | ☐ | Smaller reporting company | ☐ | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

| • whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). | Yes | ☐ | No | ☒ |

As of July 29, 2019, there were outstanding 361,581,394 shares of Common Stock, $0.01 par value per share, of the registrant.

2

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

QUARTERLY REPORT ON FORM 10-Q

FOR THE QUARTERLY PERIOD ENDED JUNE 30, 2019

TABLE OF CONTENTS

| Item | Description | Page |

| 1. | FINANCIAL STATEMENTS | |

| REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM | ||

| CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS - FOR THE THREE AND SIX MONTHS ENDED JUNE 30, 2019 AND 2018 | ||

| CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS) - FOR THE THREE AND SIX MONTHS ENDED JUNE 30, 2019 AND 2018 | ||

| CONDENSED CONSOLIDATED BALANCE SHEETS - AS OF JUNE 30, 2019 AND DECEMBER 31, 2018 | ||

| CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS' EQUITY - FOR THE THREE AND SIX MONTHS ENDED JUNE 30, 2019 AND 2018 | ||

| CONDENSED CONOLIDATED STATEMENTS OF CASH FLOWS - FOR THE SIX MONTHS ENDED JUNE 30, 2019 AND 2018 | ||

| NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS | ||

| 2. | MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | |

| 3. | QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK | [a] |

| 4. | CONTROLS AND PROCEDURES | |

| 1. | LEGAL PROCEEDINGS | |

| 1A. | RISK FACTORS | |

| 2. | UNREGISTERED SALES OF EQUITY SECURITIES AND USE OF PROCEEDS | |

| 6. | EXHIBITS | |

| EXHIBITS INDEX | ||

| SIGNATURE | ||

[a]The information required by this item is set forth in the Enterprise Risk Management section of Item 2, Management's Discussion and Analysis of Financial Condition and Results of Operations and is incorporated herein by reference.

3

Forward-Looking Statements

Certain of the statements contained herein are forward-looking statements made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Forward-looking statements can be identified by words such as “anticipates,” “intends,” “plans,” “seeks,” “believes,” “estimates,” “expects,” “projects,” and similar references to future periods.

Forward-looking statements are based on management's current expectations and assumptions regarding future economic, competitive, legislative and other developments and their potential effect upon The Hartford Financial Services Group, Inc. and its subsidiaries (collectively, the "Company" or "The Hartford"). Because forward-looking statements relate to the future, they are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict. Actual results could differ materially from expectations, depending on the evolution of various factors, including the risks and uncertainties identified below, as well as factors described in such forward-looking statements or in Part I, Item 1A, Risk Factors in The Hartford’s 2018 Form 10-K Annual Report; and our other filings with the Securities and Exchange Commission ("SEC").

| • | Risks Relating to Economic, Political and Global Market Conditions: |

| ◦ | challenges related to the Company’s current operating environment, including global political, economic and market conditions, and the effect of financial market disruptions, economic downturns, changes in trade regulation including tariffs and other barriers or other potentially adverse macroeconomic developments on the demand for our products and returns in our investment portfolios; |

| ◦ | market risks associated with our business, including changes in credit spreads, equity prices, interest rates, inflation rate, and market volatility; |

| ◦ | the impact on our investment portfolio if our investment portfolio is concentrated in any particular segment of the economy; |

| ◦ | the impacts of changing climate and weather patterns on our businesses, operations and investment portfolio including on claims, demand and pricing of our products, the availability and cost of reinsurance, our modeling data used to evaluate and manage risks of catastrophes and severe weather events, the value of our investment portfolios and credit risk with reinsurers and other counterparties; |

| ◦ | the risks associated with the change in or replacement of the London Inter-Bank Offered Rate ("LIBOR") on the securities we hold or may have issued, other financial instruments and any other assets and liabilities whose value is tied to LIBOR; |

| ◦ | the impacts associated with the withdrawal of the United Kingdom (“U.K.”) from the European Union (“E.U.”) on our international operations in the U.K. and E.U. |

| • | Insurance Industry and Product-Related Risks: |

| ◦ | the possibility of unfavorable loss development, including with respect to long-tailed exposures; |

| ◦ | the significant uncertainties that limit our ability to estimate the ultimate reserves necessary for asbestos and environmental claims; |

| ◦ | the possibility of a pandemic, earthquake, or other natural or man-made disaster that may adversely affect our businesses; |

| ◦ | weather and other natural physical events, including the intensity and frequency of storms, hail, wildfires, flooding, winter storms, hurricanes and tropical storms, as well as climate change and its potential impact on weather patterns; |

| ◦ | the possible occurrence of terrorist attacks and the Company’s inability to contain its exposure as a result of, among other factors, the inability to exclude coverage for terrorist attacks from workers' compensation policies and limitations on reinsurance coverage from the federal government under applicable laws; |

| ◦ | the Company’s ability to effectively price its property and casualty policies, including its ability to obtain regulatory consents to pricing actions or to non-renewal or withdrawal of certain product lines; |

| ◦ | actions by competitors that may be larger or have greater financial resources than we do; |

| ◦ | technological changes, such as usage-based methods of determining premiums, advancements in automotive safety features, the development of autonomous vehicles, and platforms that facilitate ride sharing, which may alter demand for the Company's products, impact the frequency or severity of losses, and/or impact the way the Company markets, distributes and underwrites its products; |

| ◦ | the Company's ability to market, distribute and provide insurance products and investment advisory services through current and future distribution channels and advisory firms; |

| ◦ | the uncertain effects of emerging claim and coverage issues; |

| • | Financial Strength, Credit and Counterparty Risks: |

| ◦ | risks to our business, financial position, prospects and results associated with negative rating actions or downgrades in the Company’s financial strength and credit ratings or negative rating actions or downgrades relating to our investments; |

4

| ◦ | capital requirements which are subject to many factors, including many that are outside the Company’s control, such as NAIC risk based capital formulas, Funds at Lloyd's and Solvency Capital Requirement, which can in turn affect our credit and financial strength ratings, cost of capital, regulatory compliance and other aspects of our business and results; |

| ◦ | losses due to nonperformance or defaults by others, including credit risk with counterparties associated with investments, derivatives, premiums receivable, reinsurance recoverables and indemnifications provided by third parties in connection with previous dispositions; |

| ◦ | the potential for losses due to our reinsurers' unwillingness or inability to meet their obligations under reinsurance contracts and the availability, pricing and adequacy of reinsurance to protect the Company against losses; |

| ◦ | state and international regulatory limitations on the ability of the Company and certain of its subsidiaries to declare and pay dividends; |

| • | Risks Relating to Estimates, Assumptions and Valuations: |

| ◦ | risk associated with the use of analytical models in making decisions in key areas such as underwriting, pricing, capital management, reserving, investments, reinsurance and catastrophe risk management; |

| ◦ | the potential for differing interpretations of the methodologies, estimations and assumptions that underlie the Company’s fair value estimates for its investments and the evaluation of other-than-temporary impairments on available-for-sale securities; |

| ◦ | the potential for further impairments of our goodwill or the potential for changes in valuation allowances against deferred tax assets; |

| • | Strategic and Operational Risks: |

| ◦ | the Company’s ability to maintain the availability of its systems and safeguard the security of its data in the event of a disaster, cyber or other information security incident or other unanticipated event; |

| ◦ | the potential for difficulties arising from outsourcing and similar third-party relationships; |

| ◦ | the risks, challenges and uncertainties associated with capital management plans, expense reduction initiatives and other actions, which may include acquisitions, divestitures or restructurings; |

| ◦ | risks associated with acquisitions and divestitures, including the challenges of integrating acquired companies or businesses or separating from our divested businesses, which may result in our inability to achieve the anticipated benefits and synergies and may result in unintended consequences; |

| ◦ | difficulty in attracting and retaining talented and qualified personnel, including key employees, such as executives, managers and employees with strong technological, analytical and other specialized skills; |

| ◦ | the Company’s ability to protect its intellectual property and defend against claims of infringement; |

| • | Regulatory and Legal Risks: |

| ◦ | the cost and other potential effects of increased federal, state and international regulatory and legislative developments, including those that could adversely impact the demand for the Company’s products, operating costs and required capital levels; |

| ◦ | unfavorable judicial or legislative developments; |

| ◦ | the impact of changes in federal or state tax laws; |

| ◦ | regulatory requirements that could delay, deter or prevent a takeover attempt that stockholders might consider in their best interests; and |

| ◦ | the impact of potential changes in accounting principles and related financial reporting requirements. |

Any forward-looking statement made by the Company in this document speaks only as of the date of the filing of this Form 10-Q. Factors or events that could cause the Company’s actual results to differ may emerge from time to time, and it is not possible for the Company to predict all of them. The Company undertakes no obligation to publicly update any forward-looking statement, whether as a result of new information, future developments or otherwise.

5

Part I - Item 1. Financial Statements

Item 1. Financial Statements

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Directors and Stockholders of

The Hartford Financial Services Group, Inc.

Hartford, Connecticut

Results of Review of Interim Financial Information

We have reviewed the accompanying condensed consolidated balance sheet of The Hartford Financial Services Group, Inc. and subsidiaries (the "Company") as of June 30, 2019, the related condensed consolidated statements of operations, comprehensive income (loss), and changes in stockholders' equity for the three-month and six-month periods ended June 30, 2019 and 2018, and the condensed consolidated statement of cash flows for the six-month periods ended June 30, 2019 and 2018, and the related notes (collectively referred to as the "interim financial information"). Based on our reviews, we are not aware of any material modifications that should be made to the accompanying interim financial information for it to be in conformity with accounting principles generally accepted in the United States of America.

We have previously audited, in accordance with the standards of the Public Company Accounting Oversight Board (United States) (PCAOB), the consolidated balance sheet of the Company as of December 31, 2018, and the related consolidated statements of operations, comprehensive income (loss), changes in stockholders' equity, and cash flows for the year then ended (not presented herein); and in our report dated February 22, 2019, we expressed an unqualified opinion on those consolidated financial statements. In our opinion, the information set forth in the accompanying condensed consolidated balance sheet as of December 31, 2018, is fairly stated, in all material respects, in relation to the consolidated balance sheet from which it has been derived.

Basis for Review Results

This interim financial information is the responsibility of the Company's management. We are a public accounting firm registered with the PCAOB and are required to be independent with respect to the Company in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our reviews in accordance with standards of the PCAOB. A review of interim financial information consists principally of applying analytical procedures and making inquiries of persons responsible for financial and accounting matters. It is substantially less in scope than an audit conducted in accordance with the standards of the PCAOB, the objective of which is the expression of an opinion regarding the financial statements taken as a whole. Accordingly, we do not express such an opinion.

/s/ DELOITTE & TOUCHE LLP

Hartford, Connecticut

August 1, 2019

6

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

Condensed Consolidated Statements of Operations

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||

| (In millions, except for per share data) | 2019 | 2018 | 2019 | 2018 | |||||||||

| (Unaudited) | |||||||||||||

| Revenues | |||||||||||||

| Earned premiums | $ | 4,166 | $ | 3,958 | $ | 8,106 | $ | 7,885 | |||||

| Fee income | 326 | 327 | 640 | 650 | |||||||||

| Net investment income | 488 | 428 | 958 | 879 | |||||||||

| Net realized capital gains (losses): | |||||||||||||

| Total other-than-temporary impairment ("OTTI") losses | — | — | (4 | ) | (2 | ) | |||||||

| OTTI losses recognized in other comprehensive income (“OCI”) | — | — | 2 | 2 | |||||||||

| Net OTTI losses recognized in earnings | — | — | (2 | ) | — | ||||||||

| Other net realized capital gains | 80 | 52 | 245 | 22 | |||||||||

| Total net realized capital gains | 80 | 52 | 243 | 22 | |||||||||

| Other revenues | 32 | 24 | 85 | 44 | |||||||||

| Total revenues | 5,092 | 4,789 | 10,032 | 9,480 | |||||||||

| Benefits, losses and expenses | |||||||||||||

| Benefits, losses and loss adjustment expenses | 2,934 | 2,738 | 5,619 | 5,433 | |||||||||

| Amortization of deferred policy acquisition costs ("DAC") | 392 | 344 | 747 | 686 | |||||||||

| Insurance operating costs and other expenses | 1,141 | 1,067 | 2,189 | 2,104 | |||||||||

| Loss on extinguishment of debt | — | 6 | — | 6 | |||||||||

| Loss on reinsurance transaction | 91 | — | 91 | — | |||||||||

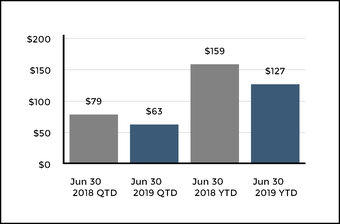

| Interest expense | 63 | 79 | 127 | 159 | |||||||||

| Amortization of other intangible assets | 15 | 18 | 28 | 36 | |||||||||

| Total benefits, losses and expenses | 4,636 | 4,252 | 8,801 | 8,424 | |||||||||

| Income from continuing operations, before tax | 456 | 537 | 1,231 | 1,056 | |||||||||

| Income tax expense | 84 | 103 | 229 | 194 | |||||||||

| Income from continuing operations, net of tax | 372 | 434 | 1,002 | 862 | |||||||||

| Income from discontinued operations, net of tax | — | 148 | — | 317 | |||||||||

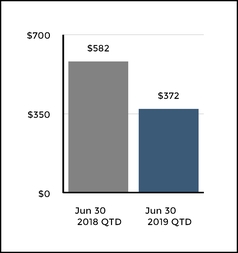

| Net income | 372 | 582 | 1,002 | 1,179 | |||||||||

| Preferred stock dividends | — | — | 5 | — | |||||||||

| Net income available to common stockholders | $ | 372 | $ | 582 | $ | 997 | $ | 1,179 | |||||

| Income from continuing operations, net of tax, available to common stockholders per common share | |||||||||||||

| Basic | $ | 1.03 | $ | 1.21 | $ | 2.76 | $ | 2.41 | |||||

| Diluted | $ | 1.02 | $ | 1.19 | $ | 2.73 | $ | 2.37 | |||||

| Net income available to common stockholders per common share | |||||||||||||

| Basic | $ | 1.03 | $ | 1.62 | $ | 2.76 | $ | 3.29 | |||||

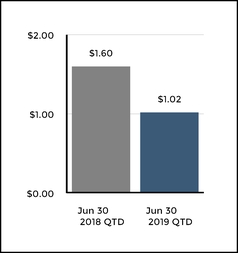

| Diluted | $ | 1.02 | $ | 1.60 | $ | 2.73 | $ | 3.24 | |||||

See Notes to Condensed Consolidated Financial Statements.

7

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

Condensed Consolidated Statements of Comprehensive Income (Loss)

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||

| (In millions) | 2019 | 2018 | 2019 | 2018 | |||||||||

| (Unaudited) | |||||||||||||

| Net income | $ | 372 | $ | 582 | $ | 1,002 | $ | 1,179 | |||||

| Other comprehensive income (loss): | |||||||||||||

| Changes in net unrealized gain on securities | 664 | (1,138 | ) | 1,343 | (1,993 | ) | |||||||

| Changes in OTTI losses recognized in other comprehensive income | — | 2 | 1 | — | |||||||||

| Changes in net gain on cash flow hedging instruments | 11 | 12 | 16 | (32 | ) | ||||||||

| Changes in foreign currency translation adjustments | 3 | 1 | 4 | (5 | ) | ||||||||

| Changes in pension and other postretirement plan adjustments | 9 | 9 | 17 | 19 | |||||||||

| OCI, net of tax | 687 | (1,114 | ) | 1,381 | (2,011 | ) | |||||||

| Comprehensive income (loss) | $ | 1,059 | $ | (532 | ) | $ | 2,383 | $ | (832 | ) | |||

See Notes to Condensed Consolidated Financial Statements.

8

| (In millions, except for share and per share data) | June 30, 2019 | December 31, 2018 | ||||

| (Unaudited) | ||||||

| Assets | ||||||

| Investments: | ||||||

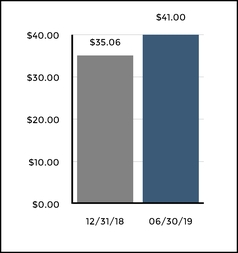

| Fixed maturities, available-for-sale, at fair value (amortized cost of $39,429 and $35,603) | $ | 41,166 | $ | 35,652 | ||

| Fixed maturities, at fair value using the fair value option | 49 | 22 | ||||

| Equity securities, at fair value | 1,533 | 1,214 | ||||

| Mortgage loans (net of allowances for loan losses of $0 and $1) | 3,612 | 3,704 | ||||

| Limited partnerships and other alternative investments | 1,734 | 1,723 | ||||

| Other investments | 311 | 192 | ||||

| Short-term investments | 2,364 | 4,283 | ||||

| Total investments | 50,769 | 46,790 | ||||

| Cash | 226 | 112 | ||||

| Restricted cash | 57 | 9 | ||||

| Premiums receivable and agents’ balances, net | 4,726 | 3,995 | ||||

| Reinsurance recoverables, net | 5,394 | 4,357 | ||||

| Deferred policy acquisition costs | 722 | 670 | ||||

| Deferred income taxes, net | 615 | 1,248 | ||||

| Goodwill | 1,913 | 1,290 | ||||

| Property and equipment, net | 1,222 | 1,006 | ||||

| Other intangible assets, net | 1,191 | 657 | ||||

| Other assets | 2,637 | 2,173 | ||||

| Total assets | $ | 69,472 | $ | 62,307 | ||

| Liabilities | ||||||

| Unpaid losses and loss adjustment expenses | $ | 36,104 | $ | 33,029 | ||

| Reserve for future policy benefits | 644 | 642 | ||||

| Other policyholder funds and benefits payable | 790 | 767 | ||||

| Unearned premiums | 6,833 | 5,282 | ||||

| Short-term debt | 500 | 413 | ||||

| Long-term debt | 4,050 | 4,265 | ||||

| Other liabilities | 5,259 | 4,808 | ||||

| Total liabilities | 54,180 | 49,206 | ||||

| Commitments and Contingencies Note (12) | ||||||

| Stockholders’ Equity | ||||||

| Preferred stock, $0.01 par value — 50,000,000 shares authorized, 13,800 shares issued at June 30, 2019 and December 31, 2018, aggregate liquidation preference of $345 | 334 | 334 | ||||

| Common stock, $0.01 par value — 1,500,000,000 shares authorized, 384,923,222 shares issued at June 30, 2019 and December 31, 2018 | 4 | 4 | ||||

| Additional paid-in capital | 4,300 | 4,378 | ||||

| Retained earnings | 11,836 | 11,055 | ||||

| Treasury stock, at cost — 23,317,797 and 25,772,238 shares | (984 | ) | (1,091 | ) | ||

| Accumulated other comprehensive loss, net of tax | (198 | ) | (1,579 | ) | ||

| Total stockholders’ equity | 15,292 | 13,101 | ||||

| Total liabilities and stockholders’ equity | $ | 69,472 | $ | 62,307 | ||

See Notes to Condensed Consolidated Financial Statements.

9

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

Condensed Consolidated Statements of Changes in Stockholders' Equity

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||

| (In millions, except for share data) | 2019 | 2018 | 2019 | 2018 | |||||||||

| (Unaudited) | |||||||||||||

| Preferred Stock | $ | 334 | $ | — | $ | 334 | $ | — | |||||

| Common Stock | 4 | 4 | 4 | 4 | |||||||||

| Additional Paid-in Capital | |||||||||||||

| Additional Paid-in Capital, beginning of period | 4,329 | 4,363 | 4,378 | 4,379 | |||||||||

| Issuance of shares under incentive and stock compensation plans | (6 | ) | (9 | ) | (74 | ) | (83 | ) | |||||

| Stock-based compensation plans expense | 21 | 22 | 76 | 83 | |||||||||

| Issuance of shares for warrant exercise | (44 | ) | (2 | ) | (80 | ) | (5 | ) | |||||

| Additional Paid-in Capital, end of period | 4,300 | 4,374 | 4,300 | 4,374 | |||||||||

| Retained Earnings | |||||||||||||

| Retained Earnings, beginning of period | 11,572 | 10,156 | 11,055 | 9,642 | |||||||||

| Cumulative effect of accounting changes, net of tax | — | — | — | 5 | |||||||||

| Adjusted balance, beginning of period | 11,572 | 10,156 | 11,055 | 9,647 | |||||||||

| Net income | 372 | 582 | 1,002 | 1,179 | |||||||||

| Dividends declared on preferred stock | — | — | (5 | ) | — | ||||||||

| Dividends declared on common stock | (108 | ) | (89 | ) | (216 | ) | (177 | ) | |||||

| Retained Earnings, end of period | 11,836 | 10,649 | 11,836 | 10,649 | |||||||||

| Treasury Stock, at cost | |||||||||||||

| Treasury Stock, at cost, beginning of period | (1,014 | ) | (1,141 | ) | (1,091 | ) | (1,194 | ) | |||||

| Treasury stock acquired | (27 | ) | — | (27 | ) | — | |||||||

| Issuance of shares under incentive and stock compensation plans | 14 | 14 | 85 | 95 | |||||||||

| Net shares acquired related to employee incentive and stock compensation plans | (1 | ) | (3 | ) | (31 | ) | (34 | ) | |||||

| Issuance of shares for warrant exercise | 44 | 2 | 80 | 5 | |||||||||

| Treasury Stock, at cost, end of period | (984 | ) | (1,128 | ) | (984 | ) | (1,128 | ) | |||||

| Accumulated Other Comprehensive Income (Loss), net of tax | |||||||||||||

| Accumulated Other Comprehensive Income (Loss), net of tax, beginning of period | (885 | ) | (239 | ) | (1,579 | ) | 663 | ||||||

| Cumulative effect of accounting changes, net of tax | — | — | — | (5 | ) | ||||||||

| Adjusted balance, beginning of period | (885 | ) | (239 | ) | (1,579 | ) | 658 | ||||||

| Total other comprehensive income (loss) | 687 | (1,114 | ) | 1,381 | (2,011 | ) | |||||||

| Accumulated Other Comprehensive Loss, net of tax, end of period | (198 | ) | (1,353 | ) | (198 | ) | (1,353 | ) | |||||

| Total Stockholders’ Equity | $ | 15,292 | $ | 12,546 | $ | 15,292 | $ | 12,546 | |||||

| Preferred Shares Outstanding | |||||||||||||

| Preferred Shares Outstanding, beginning of period | 13,800 | — | 13,800 | — | |||||||||

| Issuance of preferred shares | — | — | — | — | |||||||||

| Preferred Shares Outstanding, end of period | 13,800 | — | 13,800 | — | |||||||||

| Common Shares Outstanding | |||||||||||||

| Common Shares Outstanding, beginning of period (in thousands) | 360,865 | 358,077 | 359,151 | 356,835 | |||||||||

| Treasury stock acquired | (505 | ) | — | (505 | ) | — | |||||||

| Issuance of shares under incentive and stock compensation plans | 325 | 272 | 1,859 | 2,042 | |||||||||

| Return of shares under incentive and stock compensation plans to treasury stock | (20 | ) | (42 | ) | (621 | ) | (637 | ) | |||||

| Issuance of shares for warrant exercise | 940 | 52 | 1,721 | 119 | |||||||||

| Common Shares Outstanding, at end of period | 361,605 | 358,359 | 361,605 | 358,359 | |||||||||

| Cash dividends declared per common share | $ | 0.30 | $ | 0.25 | $ | 0.60 | $ | 0.50 | |||||

| Cash dividends declared per preferred share | $ | — | $ | — | $ | 375.00 | $ | — | |||||

10

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

Condensed Consolidated Statements of Cash Flows

| Six Months Ended June 30, | ||||||

| (In millions) | 2019 | 2018 | ||||

| Operating Activities | (Unaudited) | |||||

| Net income | $ | 1,002 | $ | 1,179 | ||

| Adjustments to reconcile net income to net cash provided by operating activities: | ||||||

| Net realized capital losses (gains) | (243 | ) | 31 | |||

| Amortization of deferred policy acquisition costs | 747 | 744 | ||||

| Additions to deferred policy acquisition costs | (799 | ) | (701 | ) | ||

| Depreciation and amortization | 221 | 237 | ||||

| Loss on extinguishment of debt | — | 6 | ||||

| Gain on sale | — | (213 | ) | |||

| Other operating activities, net | 64 | 291 | ||||

| Change in assets and liabilities: | ||||||

| Decrease in reinsurance recoverables | 57 | 136 | ||||

| Decrease (increase) in accrued and deferred income taxes | 277 | (112 | ) | |||

| Increase (decrease) in insurance liabilities | 565 | (77 | ) | |||

| Net change in other assets and other liabilities | (887 | ) | (251 | ) | ||

| Net cash provided by operating activities | 1,004 | 1,270 | ||||

| Investing Activities | ||||||

| Proceeds from the sale/maturity/prepayment of: | ||||||

| Fixed maturities, available-for-sale | 10,770 | 14,712 | ||||

| Fixed maturities, fair value option | 4 | 11 | ||||

| Equity securities, at fair value | 1,024 | 1,027 | ||||

| Mortgage loans | 346 | 234 | ||||

| Partnerships | 122 | 331 | ||||

| Payments for the purchase of: | ||||||

| Fixed maturities, available-for-sale | (11,027 | ) | (13,261 | ) | ||

| Equity securities, at fair value | (951 | ) | (953 | ) | ||

| Mortgage loans | (280 | ) | (383 | ) | ||

| Partnerships | (167 | ) | (316 | ) | ||

| Net proceeds from (payments for) derivatives | 45 | (234 | ) | |||

| Net additions of property and equipment | (44 | ) | (59 | ) | ||

| Net proceeds from (payments for) short-term investments | 2,090 | (2,427 | ) | |||

| Other investing activities, net | (1 | ) | (4 | ) | ||

| Proceeds from business sold, net of cash transferred | — | 1,115 | ||||

| Amount paid for business acquired, net of cash acquired | (1,901 | ) | — | |||

| Net cash provided by (used for) investing activities | 30 | (207 | ) | |||

| Financing Activities | ||||||

| Deposits and other additions to investment and universal life-type contracts | 106 | 1,814 | ||||

| Withdrawals and other deductions from investment and universal life-type contracts | (77 | ) | (9,206 | ) | ||

| Net transfers from separate accounts related to investment and universal life-type contracts | — | 6,949 | ||||

| Repayments at maturity or settlement of consumer notes | — | (2 | ) | |||

| Net increase (decrease) in securities loaned or sold under agreements to repurchase | (178 | ) | (671 | ) | ||

| Repayment of debt | (413 | ) | (826 | ) | ||

| Proceeds from the issuance of debt | — | 490 | ||||

| Net issuance (return) of shares under incentive and stock compensation plans | (39 | ) | 5 | |||

| Treasury stock acquired | (27 | ) | — | |||

| Dividends paid on preferred stock | (11 | ) | — | |||

| Dividends paid on common stock | (216 | ) | (180 | ) | ||

| Net cash used for financing activities | (855 | ) | (1,627 | ) | ||

| Foreign exchange rate effect on cash | (17 | ) | (6 | ) | ||

| Net increase (decrease) in cash, including cash classified as assets held for sale | 162 | (570 | ) | |||

| Less: Net increase (decrease) in cash classified as assets held for sale | — | (537 | ) | |||

| Net increase (decrease) in cash and restricted cash | 162 | (33 | ) | |||

| Cash and restricted cash – beginning of period | 121 | 180 | ||||

| Cash and restricted cash– end of period | $ | 283 | $ | 147 | ||

| Supplemental Disclosure of Cash Flow Information | ||||||

| Income tax paid | $ | (1 | ) | $ | (1 | ) |

| Interest paid | $ | 137 | $ | 156 | ||

11

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Dollar amounts in millions, except for per share data, unless otherwise stated)

1. BASIS OF PRESENTATION AND SIGNIFICANT ACCOUNTING POLICIES

Basis of Presentation

The Hartford Financial Services Group, Inc. is a holding company for insurance and financial services subsidiaries that provide property and casualty insurance, group life and disability products and mutual funds and exchange-traded products to individual and business customers (collectively, “The Hartford”, the “Company”, “we” or “our”).

On May 23, 2019, the Company completed the previously announced acquisition of The Navigators Group, Inc. ("Navigators Group"), a global specialty underwriter, for $70 a share, or $2.136 billion in cash, including transaction expenses. For further discussion of this transaction, see Note 2 - Business Acquisition of Notes to Condensed Consolidated Financial Statements.

On May 31, 2018, Hartford Holdings, Inc., a wholly owned subsidiary of the Company, completed the sale of the issued and outstanding equity of Hartford Life, Inc. (“HLI”), a holding company, for its life and annuity operating subsidiaries. For further discussion of this transaction, see Note 17 - Business Disposition and Discontinued Operations of Notes to Condensed Consolidated Financial Statements.

The Condensed Consolidated Financial Statements have been prepared in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”) for interim financial information, which differ materially from the accounting practices prescribed by various insurance regulatory authorities. These Condensed Consolidated Financial Statements and Notes should be read in conjunction with the Consolidated Financial Statements and Notes thereto included in the Company's 2018 Form 10-K Annual Report. The results of operations for interim periods are not necessarily indicative of the results that may be expected for the full year.

The accompanying Condensed Consolidated Financial Statements and Notes are unaudited. These financial statements reflect all adjustments (generally consisting only of normal accruals) which are, in the opinion of management, necessary for the fair presentation of the financial position, results of operations and cash flows for the interim periods. The Company's significant accounting policies are summarized in Note 1 - Basis of Presentation and Significant Accounting Policies of Notes to Consolidated Financial Statements included in the Company's 2018 Form 10-K Annual Report.

Consolidation

The Condensed Consolidated Financial Statements include the accounts of The Hartford Financial Services Group, Inc., and entities in which the Company directly or indirectly has a controlling financial interest. Entities in which the Company has significant influence over the operating and financing decisions but does not control are reported using the equity method. All intercompany transactions and balances between The Hartford and its subsidiaries and affiliates that are not held for sale have been eliminated.

Discontinued Operations

The results of operations of a component of the Company are reported in discontinued operations when certain criteria are met as of the date of disposal, or earlier if classified as held-for-sale. When a component is identified for discontinued operations reporting, amounts for prior periods are retrospectively reclassified as discontinued operations. Components are identified as discontinued operations if they are a major part of an entity's operations and financial results such as a separate major line of business or a separate major geographical area of operations.

Use of Estimates

The preparation of financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

The most significant estimates include those used in determining property and casualty and group long-term disability insurance product reserves, net of reinsurance; evaluation of goodwill for impairment; valuation of investments and derivative instruments; valuation allowance on deferred tax assets; and contingencies relating to corporate litigation and regulatory matters.

Reclassifications

Certain reclassifications have been made to prior year financial information to conform to the current year presentation. In particular:

| • | Restricted cash has been reclassified out of cash to a separate line on the Condensed Consolidated Balance Sheets. Restrictions on cash primarily relate to funds that are held to support regulatory and contractual obligations. |

Adoption of New Accounting Standards

Hedging Activities

On January 1, 2019, the Company adopted the Financial Accounting Standards Board's ("FASB") updated guidance for hedge accounting through a cumulative effect adjustment of less than $1 to reclassify cumulative ineffectiveness on cash flow hedges from retained earnings to accumulated other comprehensive income ("AOCI"). The updates allow hedge accounting for new types of interest rate hedges of financial instruments and simplify documentation requirements to qualify for hedge accounting. In addition, any gain or loss from hedge ineffectiveness is reported in the same income statement line with the effective hedge results and the hedged transaction. For cash flow hedges, the ineffectiveness is recognized in earnings only when the hedged transaction affects earnings; otherwise,

12

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

the ineffectiveness gains or losses remain in AOCI. Under previous accounting, total hedge ineffectiveness was reported separately in realized capital gains and losses apart from the hedged transaction. The adoption did not affect the Company’s financial position or cash flows or have a material effect on net income.

Leases

On January 1, 2019, the Company adopted the FASB’s updated lease guidance. Under the updated guidance, lessees with operating leases are required to recognize a liability for the present value of future minimum lease payments with a corresponding asset for the right of use of the property. Prior to the new guidance, future minimum lease payments on operating leases were commitments that were not recognized as liabilities on the balance sheet. Leases are classified as financing or operating leases. Where the lease is economically similar to a purchase because The Hartford obtains control of the underlying asset, the lease is classified as a financing lease and the Company recognizes amortization of the right of use asset and interest

expense on the liability. Where the lease provides The Hartford with only the right to control the use of the underlying asset over the lease term and the lease term is greater than one year, the lease is an operating lease and the lease cost is recognized as rental expense over the lease term on a straight-line basis. Leases with a term of one year or less are also expensed over the lease term but not recognized on the balance sheet. On adoption, The Hartford recorded a lease payment obligation of $160 for outstanding leases and a right of use asset of $150, which is net of $10 in lease incentives received, with no change to comparative periods. As permitted by the new guidance, as of the implementation date, the Company did not reassess whether expired or existing contracts are leases or contain leases, did not change the classification of expired or existing operating leases, and did not reassess initial direct costs for existing leases to determine if deferred costs should be written-off or recorded on adoption. The adoption did not impact net income or cash flows.

2. BUSINESS ACQUISITION

Navigators Group

On May 23, 2019, The Hartford acquired 100% of the outstanding shares of Navigators Group for $70 a share, or $2.121 billion in cash, comprised of cash of $2.098 billion and a liability for cash awards to replace share-based awards of $23. The acquisition of the specialty underwriter expands product offerings and geographic reach, and adds underwriting and industry talent to strengthen the Company’s value proposition to agents and customers.

Fair Value of Assets Acquired and Liabilities Assumed at the Acquisition Date

| As of May 23, 2019 | |||

| Assets | |||

| Cash and invested assets | $ | 3,848 | |

| Premiums receivable | 492 | ||

| Reinsurance recoverables | 1,100 | ||

| Prepaid reinsurance premiums | 238 | ||

| Other intangible assets | 580 | ||

| Property and equipment | 83 | ||

| Other assets | 99 | ||

| Total Assets Acquired | 6,440 | ||

| Liabilities | |||

| Unpaid losses and loss adjustment expenses | 2,823 | ||

| Unearned premiums | 1,219 | ||

| Long-term debt | 284 | ||

| Deferred income taxes, net | 48 | ||

| Other liabilities | 568 | ||

| Total Liabilities Assumed | 4,942 | ||

| Net identifiable assets acquired | 1,498 | ||

| Goodwill [1] | 623 | ||

| Net Assets Acquired | $ | 2,121 | |

[1] Non-deductible for income tax purposes.

13

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

Intangible Assets Recorded in Connection with the Acquisition

| Asset | Amount | Weighted Average Expected Life | ||

| Value of in-force contracts - Property and Casualty ("P&C") | $ | 180 | 1 | |

| Distribution relationships | 302 | 15 | ||

| Trade name | 17 | 10 | ||

| Total finite life intangibles | 499 | 10 | ||

| Capacity of Lloyd's Syndicate | 66 | |||

| Licenses | 15 | |||

| Total indefinite life intangibles | 81 | |||

| Total other intangible assets | $ | 580 | ||

The value of in-force contracts represents the estimated profits relating to the unexpired contracts in force net of related prepaid reinsurance at the acquisition date through expiry of the contracts. The value of distribution relationships was estimated using net cash flows expected to come from the renewals of in-force contracts and new business sold through existing distribution partners less costs to service the related policies. The value of the trade name was estimated using an assumed cost of a market-based royalty fee applied to net cash flows expected to come from business marketed as Navigators, a brand of The Hartford. Lloyd's of London is an insurance market-place operating worldwide ("Lloyd's"). Lloyd's does not underwrite risks. Corporate members accept underwriting risks through the syndicates that they form. The Company accepts risks as the sole corporate member of Lloyd's Syndicate 1221 ("Lloyd's Syndicate"). The value of the capacity of Lloyd’s Syndicate was estimated using net cash flows attributable to Navigators Group's right to underwrite business up to an approved level of premium in the Lloyd’s market. The values for in-force contracts, the distribution relationships, trade name and the capacity of the Lloyd's Syndicate were estimated using a discounted cash flow method. Significant inputs to the valuation models include estimates of expected new business, premium retention rates, investment returns, claim costs, expenses and discount rates based on a weighted average cost of capital. The value of licenses to write insurance in over 50 U.S. jurisdictions was estimated based on recent transactions for shell companies.

Expected Pre-tax Amortization Expense [1] for Acquired Intangibles as of June 30, 2019

| Value of In-force Contracts | Other Intangible Assets | |||||

| 2019 (six months) | $ | 84 | $ | 11 | ||

| 2020 | $ | 47 | $ | 22 | ||

| 2021 | $ | 21 | $ | 22 | ||

| 2022 | $ | 9 | $ | 22 | ||

| 2023 | $ | — | $ | 22 | ||

[1] In the Condensed Consolidated Statements of Operations, the amortization of value of in-force contracts is reported in amortization of deferred policy acquisition costs and the amortization of other intangible assets is reported in amortization of other intangible assets.

Property and equipment includes real estate owned and right of use assets under leases that were valued based on current values and market rental rates, software that was valued based on estimated replacement cost and furniture and equipment. These will be amortized over periods consistent with the Company’s policy.

The fair value of unpaid losses and loss adjustment expenses net of related reinsurance recoverables was estimated based on the present value of expected future net unpaid loss and loss adjustment expense payments discounted using a risk-free interest rate as of the acquisition date plus a risk margin. The discount and risk margin amounts substantially offset.

Debt assumed in the transaction was valued based on the principal and interest payments discounted at the current market yield. The resulting premium will be amortized to interest expense using the interest method.

The $623 of goodwill recognized is largely attributable to the acquired employee workforce and underwriting talent, leverageable operating platform, improved investment yield and economies of scale. Goodwill is allocated to the Company's Commercial Lines reporting segment.

Immediately after closing on the acquisition of Navigators Group, effective May 23, 2019, the Company purchased an aggregate excess of loss reinsurance agreement covering adverse reserve development (“Navigators ADC”) from National Indemnity Company ("NICO") on behalf of Navigators Insurance Company and certain of its affiliates (collectively, the “Navigators Insurers”). Under the Navigators ADC, the Navigators Insurers paid NICO a reinsurance premium of $91 in exchange for reinsurance coverage, subject to limited exceptions, of $300 of adverse net loss reserve development that attaches $100 above the Navigators Insurers' existing net loss and allocated loss adjustment reserves as of December 31, 2018 subject to the treaty of $1.816 billion for accidents and losses prior to December 31, 2018. In addition to recognizing a$91 before tax charge to earnings in the second quarter of 2019 for the Navigators ADC reinsurance premium, the Company recognized a charge against earnings of $97 before tax in the second quarter of 2019 as a result of a review of Navigators Insurers’ net acquired reserves upon acquisition of the business. Navigators Insurers had previously recognized $52 before tax of adverse reserve development in the first quarter of 2019, including $32 of adverse development subject to the Navigators ADC. As such, reserve development of $97 before tax in the second quarter of 2019 included $68 remaining of the $100 Navigators ADC retention for 2018 and prior accident years and $29 of adverse reserve development related to the 2019 accident year which is not covered by the ADC. The $68 of reserve development for the 2018 and prior accident years recorded in the second quarter of 2019 was net of a $91 reinsurance recoverable recognized under the Navigators ADC with the Company having ceded $91 of the $300 available limit, leaving $209 of remaining limit. The Navigators ADC will be accounted for as retroactive reinsurance and future adverse reserve development, if any, would result in recognizing a deferred gain.

Since the acquisition date of May 23, 2019, the revenues and net losses of the business acquired have been included in the Company's Consolidated Statements of Operations in the Commercial Lines reporting segment and were $178 and $141, respectively, during the period from the acquisition date to June

14

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

30, 2019, including the $91 before tax ($72 net of tax) of premium paid for the Navigators ADC and the charge of $97 before tax ($77 net of tax) for the increase in acquired reserves following the acquisition.

The Company recognized $15 of acquisition related costs for the six months ended June 30, 2019. These costs are included in insurance operating costs and other expenses in the Condensed Consolidated Statement of Operations.

The acquisition date fair values of assets and liabilities, including insurance reserves and intangible assets, as well as the related estimated useful lives of intangibles, are provisional and are subject to revision within one year of the acquisition date.

The following table presents supplemental unaudited pro forma amounts of revenue and net income for the six months ended

June 30, 2019 and 2018 for the Company as though the business was acquired on January 1, 2018. Pro forma adjustments include the revenue and earnings of Navigators Group for each period as well as amortization of identifiable intangible assets acquired.

Pro Forma Results for the Six Months Ended June 30

| Revenue | Earnings | |||||

| 2019 Supplemental (unaudited) combined pro forma | $ | 10,708 | $ | 997 | ||

2018 Supplemental (unaudited) combined pro forma | $ | 10,185 | $ | 1,235 | ||

3. EARNINGS PER COMMON SHARE

| Computation of Basic and Diluted Earnings per Common Share | |||||||||||||

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||

| (In millions, except for per share data) | 2019 | 2018 | 2019 | 2018 | |||||||||

| Earnings | |||||||||||||

| Income from continuing operations, net of tax | $ | 372 | $ | 434 | $ | 1,002 | $ | 862 | |||||

| Less: Preferred stock dividends | — | — | 5 | — | |||||||||

| Income from continuing operations, net of tax, available to common stockholders | 372 | 434 | $ | 997 | $ | 862 | |||||||

| Income from discontinued operations, net of tax, available to common stockholders | — | 148 | — | 317 | |||||||||

| Net income available to common stockholders | $ | 372 | $ | 582 | $ | 997 | $ | 1,179 | |||||

| Shares | |||||||||||||

| Weighted average common shares outstanding, basic | 361.4 | 358.3 | 360.7 | 357.9 | |||||||||

| Dilutive effect of stock-based awards under compensation plans | 3.2 | 4.0 | 3.3 | 4.2 | |||||||||

| Dilutive effect of warrants [1] | 0.5 | 1.9 | 0.9 | 2.0 | |||||||||

| Weighted average common shares outstanding and dilutive potential common shares | 365.1 | 364.2 | 364.9 | 364.1 | |||||||||

| Earnings per common share | |||||||||||||

| Basic | |||||||||||||

| Income from continuing operations, net of tax, available to common stockholders | $ | 1.03 | $ | 1.21 | $ | 2.76 | $ | 2.41 | |||||

| Income from discontinued operations, net of tax, available to common stockholders | — | 0.41 | — | 0.88 | |||||||||

| Net income available to common stockholders | $ | 1.03 | $ | 1.62 | $ | 2.76 | $ | 3.29 | |||||

| Diluted | |||||||||||||

| Income from continuing operations, net of tax, available to common stockholders | $ | 1.02 | $ | 1.19 | $ | 2.73 | $ | 2.37 | |||||

| Income from discontinued operations, net of tax, available to common stockholders | — | 0.41 | — | 0.87 | |||||||||

| Net income available to common stockholders | $ | 1.02 | $ | 1.60 | $ | 2.73 | $ | 3.24 | |||||

4. SEGMENT INFORMATION

The Company currently conducts business principally in five reporting segments including Commercial Lines, Personal Lines, Property & Casualty Other Operations, Group Benefits and

Hartford Funds, as well as a Corporate category. The Company includes in the Corporate category discontinued operations related to the life and annuity business sold in May 2018,

15

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

reserves for run-off structured settlement and terminal funding agreement liabilities, capital raising activities (including debt financing and related interest expense), transaction expenses incurred in connection with an acquisition, certain purchase accounting adjustments related to goodwill and other expenses not allocated to the reporting segments. Corporate also includes investment management fees and expenses related to managing third party business, including management of the invested assets of Talcott Resolution Life, Inc. and its subsidiaries ("Talcott Resolution"). Talcott Resolution is the new holding company of the life and annuity business the Company sold in May 2018. In

addition, Corporate includes a 9.7% ownership interest in the legal entity that acquired the sold life and annuity business. For further discussion of continued involvement in the life and annuity business sold in May 2018, see Note 17 - Business Disposition and Discontinued Operations of Notes to Condensed Consolidated Financial Statements.

The Company's revenues are generated primarily in the United States ("U.S.") as well as in the United Kingdom, continental Europe and other international locations.

Net Income

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||

| 2019 | 2018 | 2019 | 2018 | ||||||||||

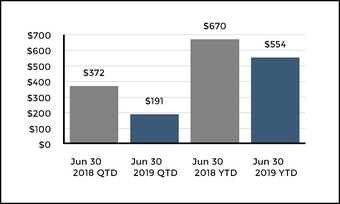

| Commercial Lines | $ | 191 | $ | 372 | $ | 554 | $ | 670 | |||||

| Personal Lines | 62 | 6 | 158 | 95 | |||||||||

| Property & Casualty Other Operations | 11 | 5 | 34 | 22 | |||||||||

| Group Benefits | 113 | 96 | 231 | 150 | |||||||||

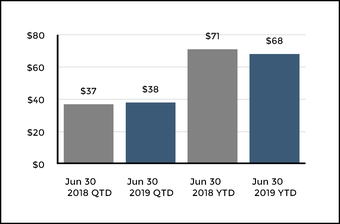

| Hartford Funds | 38 | 37 | 68 | 71 | |||||||||

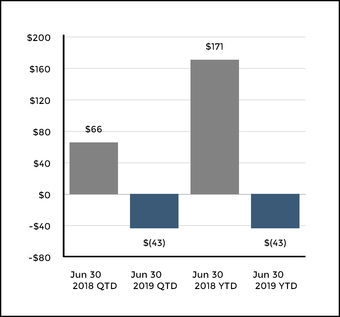

| Corporate | (43 | ) | 66 | (43 | ) | 171 | |||||||

| Net income | 372 | 582 | 1,002 | 1,179 | |||||||||

| Preferred stock dividends | — | — | 5 | — | |||||||||

| Net income available to common stockholders | $ | 372 | $ | 582 | $ | 997 | $ | 1,179 | |||||

16

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

Revenues

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||

| 2019 | 2018 | 2019 | 2018 | ||||||||||

| Earned premiums and fee income: | |||||||||||||

| Commercial Lines | |||||||||||||

| Workers’ compensation | $ | 832 | $ | 832 | $ | 1,656 | $ | 1,650 | |||||

| Liability | 233 | 159 | 401 | 310 | |||||||||

| Marine | 27 | — | 27 | — | |||||||||

| Package business | 365 | 338 | 717 | 670 | |||||||||

| Property | 175 | 152 | 331 | 302 | |||||||||

| Professional liability | 98 | 63 | 166 | 125 | |||||||||

| Bond | 65 | 61 | 125 | 119 | |||||||||

| Assumed reinsurance | 29 | — | 29 | — | |||||||||

| Automobile | 172 | 148 | 330 | 297 | |||||||||

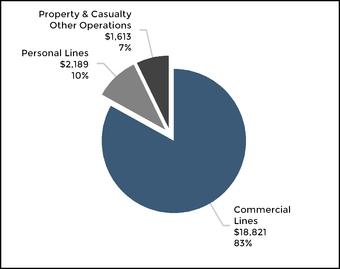

| Total Commercial Lines | 1,996 | 1,753 | 3,782 | 3,473 | |||||||||

| Personal Lines | |||||||||||||

| Automobile | 565 | 604 | 1,126 | 1,211 | |||||||||

| Homeowners | 246 | 262 | 493 | 524 | |||||||||

| Total Personal Lines [1] | 811 | 866 | 1,619 | 1,735 | |||||||||

| Group Benefits | |||||||||||||

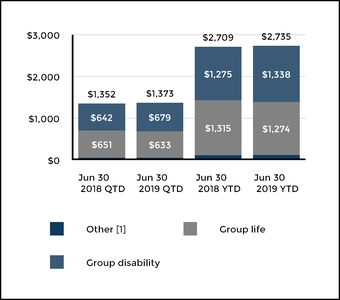

| Group disability | 723 | 690 | 1,427 | 1,367 | |||||||||

| Group life | 638 | 652 | 1,281 | 1,316 | |||||||||

| Other | 61 | 59 | 123 | 119 | |||||||||

| Total Group Benefits | 1,422 | 1,401 | 2,831 | 2,802 | |||||||||

| Hartford Funds | |||||||||||||

| Mutual fund and Exchange-Traded Products ("ETP") | 227 | 236 | 443 | 468 | |||||||||

| Talcott Resolution life and annuity separate accounts [2] | 24 | 25 | 46 | 51 | |||||||||

| Total Hartford Funds | 251 | 261 | 489 | 519 | |||||||||

| Corporate | 12 | 4 | 25 | 6 | |||||||||

| Total earned premiums and fee income | 4,492 | 4,285 | 8,746 | 8,535 | |||||||||

| Net investment income | 488 | 428 | 958 | 879 | |||||||||

| Net realized capital gains | 80 | 52 | 243 | 22 | |||||||||

| Other revenues | 32 | 24 | 85 | 44 | |||||||||

| Total revenues | $ | 5,092 | $ | 4,789 | $ | 10,032 | $ | 9,480 | |||||

| [1] | For the three months ended June 30, 2019 and 2018, AARP members accounted for earned premiums of $726 and $758, respectively. For the six months ended June 30, 2019 and 2018, AARP members accounted for earned premiums of $1.4 billion and $1.5 billion, respectively. |

| [2] | Represents revenues earned for investment advisory services on the life and annuity separate account AUM sold in May 2018 that is still managed by the Company's Hartford Funds segment. |

17

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

Revenue from Non-Insurance Contracts with Customers

| Three months ended June 30, | Six months ended June 30, | |||||||||||||

| Revenue Line Item | 2019 | 2018 | 2019 | 2018 | ||||||||||

| Commercial Lines | ||||||||||||||

| Installment billing fees | Fee income | $ | 9 | $ | 8 | $ | 18 | $ | 17 | |||||

| Personal Lines | ||||||||||||||

| Installment billing fees | Fee income | 10 | 10 | 19 | 20 | |||||||||

| Insurance servicing revenues | Other revenues | 23 | 23 | 42 | 42 | |||||||||

| Group Benefits | ||||||||||||||

| Administrative services | Fee income | 45 | 44 | 90 | 88 | |||||||||

| Hartford Funds | ||||||||||||||

| Advisor, distribution and other management fees | Fee income | 228 | 239 | 446 | 477 | |||||||||

| Other fees | Fee income | 22 | 22 | 43 | 42 | |||||||||

| Corporate | ||||||||||||||

| Investment management and other fees | Fee income | 11 | 4 | 24 | 6 | |||||||||

| Transition service revenues | Other revenues | 6 | 2 | 12 | 2 | |||||||||

| Total non-insurance revenues with customers | $ | 354 | $ | 352 | $ | 694 | $ | 694 | ||||||

5. FAIR VALUE MEASUREMENTS

The Company carries certain financial assets and liabilities at estimated fair value. Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in the principal or most advantageous market in an orderly transaction between market participants. Our fair value framework includes a hierarchy that gives the highest priority to the use of quoted prices in active markets, followed by the use of market observable inputs, followed by the use of unobservable inputs. The fair value hierarchy levels are as follows:

| Level 1 | Fair values based primarily on unadjusted quoted prices for identical assets or liabilities, in active markets that the Company has the ability to access at the measurement date. |

| Level 2 | Fair values primarily based on observable inputs, other than quoted prices included in Level 1, or based on prices for similar assets and liabilities. |

| Level 3 | Fair values derived when one or more of the significant inputs are unobservable (including assumptions about risk). With little or no observable market, the determination of fair values uses considerable judgment and represents the Company’s best estimate of an amount that could be realized in a market exchange for the asset or liability. Also included are securities that are traded within illiquid markets and/or priced by independent brokers. |

The Company will classify the financial asset or liability by level based upon the lowest level input that is significant to the determination of the fair value. In most cases, both observable inputs (e.g., changes in interest rates) and unobservable inputs (e.g., changes in risk assumptions) are used to determine fair values that the Company has classified within Level 3.

18

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

| Assets and (Liabilities) Carried at Fair Value by Hierarchy Level as of June 30, 2019 | ||||||||||||

| Total | Quoted Prices in Active Markets for Identical Assets (Level 1) | Significant Observable Inputs (Level 2) | Significant Unobservable Inputs (Level 3) | |||||||||

| Assets accounted for at fair value on a recurring basis | ||||||||||||

| Fixed maturities, AFS | ||||||||||||

| Asset-backed-securities ("ABS") | $ | 1,029 | $ | — | $ | 1,024 | $ | 5 | ||||

| Collateralized loan obligations ("CLOs") | 1,925 | — | 1,639 | 286 | ||||||||

| Commercial mortgage-backed securities ("CMBS") | 3,905 | — | 3,870 | 35 | ||||||||

| Corporate | 16,748 | — | 16,180 | 568 | ||||||||

| Foreign government/government agencies | 1,072 | — | 1,069 | 3 | ||||||||

| Municipal | 10,278 | — | 10,278 | — | ||||||||

| Residential mortgage-backed securities ("RMBS") | 4,566 | — | 3,808 | 758 | ||||||||

| U.S. Treasuries | 1,643 | 282 | 1,361 | — | ||||||||

| Total fixed maturities | 41,166 | 282 | 39,229 | 1,655 | ||||||||

| Fixed maturities, FVO | 49 | — | 49 | — | ||||||||

| Equity securities, at fair value | 1,533 | 1,227 | 234 | 72 | ||||||||

| Derivative assets | ||||||||||||

| Credit derivatives | 9 | — | 9 | — | ||||||||

| Equity derivatives | 1 | — | — | 1 | ||||||||

| Interest rate derivatives | 1 | — | 1 | — | ||||||||

| Total derivative assets [1] | 11 | — | 10 | 1 | ||||||||

| Short-term investments | 2,364 | 929 | 1,435 | — | ||||||||

| Total assets accounted for at fair value on a recurring basis | $ | 45,123 | $ | 2,438 | $ | 40,957 | $ | 1,728 | ||||

| Liabilities accounted for at fair value on a recurring basis | ||||||||||||

| Derivative liabilities | ||||||||||||

| Credit derivatives | 1 | — | 1 | — | ||||||||

| Equity derivatives | (4 | ) | — | — | (4 | ) | ||||||

| Foreign exchange derivatives | (5 | ) | — | (5 | ) | — | ||||||

| Interest rate derivatives | (63 | ) | — | (63 | ) | — | ||||||

| Total derivative liabilities [2] | (71 | ) | — | (67 | ) | (4 | ) | |||||

| Contingent consideration [3] | (21 | ) | — | — | (21 | ) | ||||||

| Total liabilities accounted for at fair value on a recurring basis | $ | (92 | ) | $ | — | $ | (67 | ) | $ | (25 | ) | |

19

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

| Assets and (Liabilities) Carried at Fair Value by Hierarchy Level as of December 31, 2018 | ||||||||||||

| Total | Quoted Prices in Active Markets for Identical Assets (Level 1) | Significant Observable Inputs (Level 2) | Significant Unobservable Inputs (Level 3) | |||||||||

| Assets accounted for at fair value on a recurring basis | ||||||||||||

| Fixed maturities, AFS | ||||||||||||

| Asset-backed-securities ("ABS") | $ | 1,276 | $ | — | $ | 1,266 | $ | 10 | ||||

| Collateralized loan obligations ("CLOs") | 1,437 | — | 1,337 | 100 | ||||||||

| Commercial mortgage-backed securities ("CMBS") | 3,552 | — | 3,540 | 12 | ||||||||

| Corporate | 13,398 | — | 12,878 | 520 | ||||||||

| Foreign government/government agencies | 847 | — | 844 | 3 | ||||||||

| Municipal | 10,346 | — | 10,346 | — | ||||||||

| Residential mortgage-backed securities ("RMBS") | 3,279 | — | 2,359 | 920 | ||||||||

| U.S. Treasuries | 1,517 | 330 | 1,187 | — | ||||||||

| Total fixed maturities | 35,652 | 330 | 33,757 | 1,565 | ||||||||

| Fixed maturities, FVO | 22 | — | 22 | — | ||||||||

| Equity securities, at fair value | 1,214 | 1,093 | 44 | 77 | ||||||||

| Derivative assets | ||||||||||||

| Credit derivatives | 5 | — | 5 | — | ||||||||

| Equity derivatives | 3 | — | — | 3 | ||||||||

| Foreign exchange derivatives | (2 | ) | — | (2 | ) | — | ||||||

| Interest rate derivatives | 1 | — | 1 | — | ||||||||

| Total derivative assets [1] | 7 | — | 4 | 3 | ||||||||

| Short-term investments | 4,283 | 1,039 | 3,244 | — | ||||||||

| Total assets accounted for at fair value on a recurring basis | $ | 41,178 | $ | 2,462 | $ | 37,071 | $ | 1,645 | ||||

| Liabilities accounted for at fair value on a recurring basis | ||||||||||||

| Derivative liabilities | ||||||||||||

| Credit derivatives | (2 | ) | — | (2 | ) | — | ||||||

| Equity derivatives | 1 | — | 1 | — | ||||||||

| Foreign exchange derivatives | (5 | ) | — | (5 | ) | — | ||||||

| Interest rate derivatives | (62 | ) | — | (63 | ) | 1 | ||||||

| Total derivative liabilities [2] | (68 | ) | — | (69 | ) | 1 | ||||||

| Contingent consideration [3] | (35 | ) | — | — | (35 | ) | ||||||

| Total liabilities accounted for at fair value on a recurring basis | $ | (103 | ) | $ | — | $ | (69 | ) | $ | (34 | ) | |

| [1] | Includes derivative instruments in a net positive fair value position after consideration of the accrued interest and impact of collateral posting requirements which may be imposed by agreements and applicable law. See footnote 2 to this table for derivative liabilities. |

| [2] | Includes derivative instruments in a net negative fair value position (derivative liability) after consideration of the accrued interest and impact of collateral posting requirements which may be imposed by agreements and applicable law. |

| [3] | For additional information see the Contingent Consideration section below. |

In connection with the acquisition of Navigators Group, the Company has overseas deposits in Other Invested Assets of $49 as of June 30, 2019, which are measured at fair value using the net asset value as a practical expedient. There were no overseas deposits held as of December 31, 2018.

Fixed Maturities, Equity Securities, Short-term Investments, and Derivatives

Valuation Techniques

The Company generally determines fair values using valuation techniques that use prices, rates, and other relevant information

evident from market transactions involving identical or similar instruments. Valuation techniques also include, where appropriate, estimates of future cash flows that are converted into a single discounted amount using current market expectations. The Company uses a "waterfall" approach comprised of the following pricing sources and techniques, which are listed in priority order:

| • | Quoted prices, unadjusted, for identical assets or liabilities in active markets, which are classified as Level 1. |

| • | Prices from third-party pricing services, which primarily utilize a combination of techniques. These services utilize recently reported trades of identical, similar, or benchmark securities making adjustments for market observable inputs available through the reporting date. If there are no recently |

20

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

reported trades, they may use a discounted cash flow technique to develop a price using expected cash flows based upon the anticipated future performance of the underlying collateral discounted at an estimated market rate. Both techniques develop prices that consider the time value of future cash flows and provide a margin for risk, including liquidity and credit risk. Most prices provided by third-party pricing services are classified as Level 2 because the inputs used in pricing the securities are observable. However, some securities that are less liquid or trade less actively are classified as Level 3. Additionally, certain long-dated securities, such as municipal securities and bank loans, include benchmark interest rate or credit spread assumptions that are not observable in the marketplace and are thus classified as Level 3.

| • | Internal matrix pricing, which is a valuation process internally developed for private placement securities for which the Company is unable to obtain a price from a third-party pricing service. Internal pricing matrices determine credit spreads that, when combined with risk-free rates, are applied to contractual cash flows to develop a price. The Company develops credit spreads using market based data for public securities adjusted for credit spread differentials between public and private securities, which are obtained from a survey of multiple private placement brokers. The market-based reference credit spread considers the issuer’s financial strength and term to maturity, using an independent public security index and trade information, while the credit spread differential considers the non-public nature of the security. Securities priced using internal matrix pricing are classified as Level 2 because the inputs are observable or can be corroborated with observable data. |

| • | Independent broker quotes, which are typically non-binding, use inputs that can be difficult to corroborate with observable market based data. Brokers may use present value techniques using assumptions specific to the security types, or they may use recent transactions of similar securities. Due to the lack of transparency in the process that brokers use to develop prices, valuations that are based on independent broker quotes are classified as Level 3. |

The fair value of derivative instruments is determined primarily using a discounted cash flow model or option model technique and incorporates counterparty credit risk. In some cases, quoted market prices for exchange-traded and over-the-counter ("OTC") cleared derivatives may be used and in other cases independent broker quotes may be used. The pricing valuation models primarily use inputs that are observable in the market or can be corroborated by observable market data. The valuation of certain derivatives may include significant inputs that are unobservable, such as volatility levels, and reflect the Company’s view of what other market participants would use when pricing such instruments.

Valuation Controls

The fair value process for investments is monitored by the Valuation Committee, which is a cross-functional group of senior management within the Company that meets at least quarterly. The purpose of the committee is to oversee the pricing policy and procedures, as well as to approve changes to valuation methodologies and pricing sources. Controls and procedures used to assess third-party pricing services are reviewed by the

Valuation Committee, including the results of annual due-diligence reviews.

There are also two working groups under the Valuation Committee: a Securities Fair Value Working Group (“Securities Working Group”) and a Derivatives Fair Value Working Group ("Derivatives Working Group"). The working groups, which include various investment, operations, accounting and risk management professionals, meet monthly to review market data trends, pricing and trading statistics and results, and any proposed pricing methodology changes.

The Securities Working Group reviews prices received from third parties to ensure that the prices represent a reasonable estimate of the fair value. The group considers trading volume, new issuance activity, market trends, new regulatory rulings and other factors to determine whether the market activity is significantly different than normal activity in an active market. A dedicated pricing unit follows up with trading and investment sector professionals and challenges prices of third-party pricing services when the estimated assumptions used differ from what the unit believes a market participant would use. If the available evidence indicates that pricing from third-party pricing services or broker quotes is based upon transactions that are stale or not from trades made in an orderly market, the Company places little, if any, weight on the third party service’s transaction price and will estimate fair value using an internal process, such as a pricing matrix.

The Derivatives Working Group reviews the inputs, assumptions and methodologies used to ensure that the prices represent a reasonable estimate of the fair value. A dedicated pricing team works directly with investment sector professionals to investigate the impacts of changes in the market environment on prices or valuations of derivatives. New models and any changes to current models are required to have detailed documentation and are validated to a second source. The model validation documentation and results of validation are presented to the Valuation Committee for approval.

The Company conducts other monitoring controls around securities and derivatives pricing including, but not limited to, the following:

| • | Review of daily price changes over specific thresholds and new trade comparison to third-party pricing services. |

| • | Daily comparison of OTC derivative market valuations to counterparty valuations. |

| • | Review of weekly price changes compared to published bond prices of a corporate bond index. |

| • | Monthly reviews of price changes over thresholds, stale prices, missing prices, and zero prices. |

| • | Monthly validation of prices to a second source for securities in most sectors and for certain derivatives. |

In addition, the Company’s enterprise-wide Operational Risk Management function, led by the Chief Risk Officer, is responsible for model risk management and provides an independent review of the suitability and reliability of model inputs, as well as an analysis of significant changes to current models.

21

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

Valuation Inputs

Quoted prices for identical assets in active markets are considered Level 1 and consist of on-the-run U.S. Treasuries,

money market funds, exchange-traded equity securities, open-ended mutual funds, certain short-term investments, and exchange traded futures and option contracts.

| Valuation Inputs Used in Levels 2 and 3 Measurements for Securities and Derivatives | |||

Level 2 Primary Observable Inputs | Level 3 Primary Unobservable Inputs | ||

| Fixed Maturity Investments | |||

| Structured securities (includes ABS, CLOs, CMBS and RMBS) | |||

• Benchmark yields and spreads • Monthly payment information • Collateral performance, which varies by vintage year and includes delinquency rates, loss severity rates and refinancing assumptions • Credit default swap indices Other inputs for ABS and RMBS: • Estimate of future principal prepayments, derived from the characteristics of the underlying structure • Prepayment speeds previously experienced at the interest rate levels projected for the collateral | • Independent broker quotes • Credit spreads beyond observable curve • Interest rates beyond observable curve Other inputs for less liquid securities or those that trade less actively, including subprime RMBS: • Estimated cash flows • Credit spreads, which include illiquidity premium • Constant prepayment rates • Constant default rates • Loss severity | ||

| Corporates | |||

• Benchmark yields and spreads • Reported trades, bids, offers of the same or similar securities • Issuer spreads and credit default swap curves Other inputs for investment grade privately placed securities that utilize internal matrix pricing: • Credit spreads for public securities of similar quality, maturity, and sector, adjusted for non-public nature | • Independent broker quotes • Credit spreads beyond observable curve • Interest rates beyond observable curve Other inputs for below investment grade privately placed securities: • Independent broker quotes • Credit spreads for public securities of similar quality, maturity, and sector, adjusted for non-public nature | ||

| U.S. Treasuries, Municipals, and Foreign government/government agencies | |||

• Benchmark yields and spreads • Issuer credit default swap curves • Political events in emerging market economies • Municipal Securities Rulemaking Board reported trades and material event notices • Issuer financial statements | • Credit spreads beyond observable curve • Interest rates beyond observable curve | ||

| Equity Securities | |||

| • Quoted prices in markets that are not active | • For privately traded equity securities, internal discounted cash flow models utilizing earnings multiples or other cash flow assumptions that are not observable | ||

| Short-term Investments | |||

• Benchmark yields and spreads • Reported trades, bids, offers • Issuer spreads and credit default swap curves • Material event notices and new issue money market rates | Not applicable | ||

| Derivatives | |||

| Credit derivatives | |||

• Swap yield curve • Credit default swap curves | Not applicable | ||

| Equity derivatives | |||

• Equity index levels • Swap yield curve | • Independent broker quotes • Equity volatility | ||

| Foreign exchange derivatives | |||

• Swap yield curve • Currency spot and forward rates • Cross currency basis curves | Not applicable | ||

| Interest rate derivatives | |||

| • Swap yield curve | • Independent broker quotes • Interest rate volatility | ||

22

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

| Significant Unobservable Inputs for Level 3 - Securities | |||||||||

| Assets accounted for at fair value on a recurring basis | Fair Value | Predominant Valuation Technique | Significant Unobservable Input | Minimum | Maximum | Weighted Average [1] | Impact of Increase in Input on Fair Value [2] | ||

| As of June 30, 2019 | |||||||||

| CLOs [3] | $ | 236 | Discounted cash flows | Spread | 250 bps | 257 bps | 253 bps | Decrease | |

| CMBS [3] | $ | 25 | Discounted cash flows | Spread (encompasses prepayment, default risk and loss severity) | 9 bps | 1,279 bps | 189 bps | Decrease | |

| Corporate [4] | $ | 387 | Discounted cash flows | Spread | 117 bps | 710 bps | 254 bps | Decrease | |

| RMBS [3] | $ | 710 | Discounted cash flows | Spread [6] | 9 bps | 416 bps | 70 bps | Decrease | |

| Constant prepayment rate [6] | 1% | 13% | 6% | Decrease [5] | |||||

| Constant default rate [6] | 1% | 6% | 3% | Decrease | |||||

| Loss severity [6] | —% | 100% | 65% | Decrease | |||||

| As of December 31, 2018 | |||||||||

| CMBS [3] | $ | 2 | Discounted cash flows | Spread (encompasses prepayment, default risk and loss severity) | 9 bps | 1,040 bps | 182 bps | Decrease | |