Exhibit 99.5

Structured Credit Data

Q2 2008

Cautionary Note on Forward Looking Statements

XL Capital Ltd

Structured Credit Data

This document contains forward-looking statements. Statements that are not historical facts, including

statements about XL’s beliefs, plans or expectations, are forward-looking statements. These statements are

based on current plans, estimates, and expectations. Actual results may differ materially from those included

in such forward-looking statements and therefore you should not place undue reliance on them. A non-

exclusive list of the important factors that could cause actual results to differ materially from those in such

forward-looking statements includes the following: (a) the risk that the closing of the transactions contemplated by the Master Agreement between XL and SCA does not occur for any reason, (b) greater risk of loss in connection with obligations guaranteed by certain of our insurance company operating affiliates due to recent deterioration in the credit markets stemming from the poor performance of sub-prime residential mortgage loans; (c) greater frequency or severity of claims and loss activity than XL’s underwriting, reserving or investment practices anticipate based on historical experience or industry data; (d) trends in rates for property and casualty insurance and reinsurance; (e) developments, including further volatility, in the world’s credit, financial and capital markets that adversely affect the performance of XL’s investments or access to such markets, including but not limited to, further market developments relating to sub-prime and residential mortgages; (f) changes in general economic conditions, including foreign currency exchange rates, inflation and other factors; (g) changes in the size of XL's claims relating to natural catastrophe losses due to the preliminary nature of some reports and estimates of loss and damage to date and (h) the other factors set forth in XL’s most recent reports on Form 10-K, Form 10-Q, and other documents on file with the Securities and Exchange Commission, as well as management’s response to any of the aforementioned factors. XL undertakes no obligation to update or revise publicly any forward-looking statement, whether as a result of new information, future developments or otherwise.

2

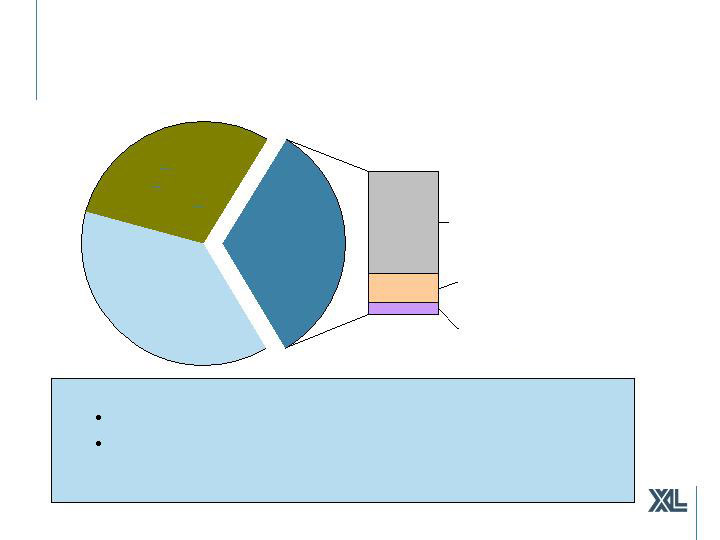

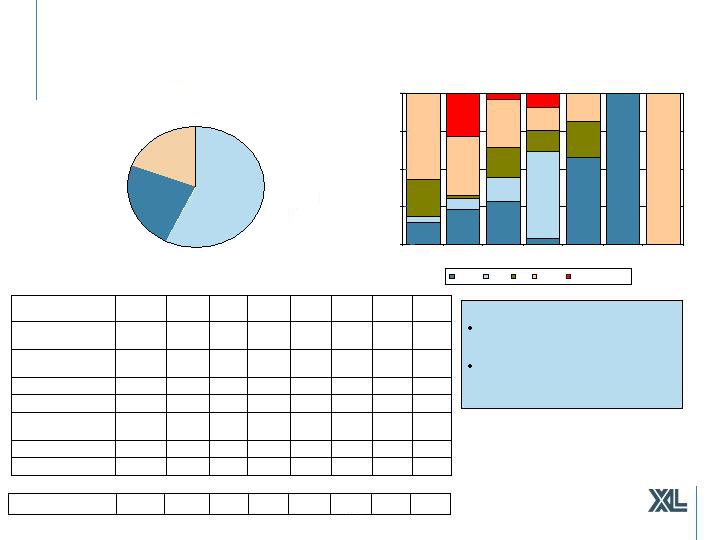

Corporates

37%

CDOs

3%

Structured

Credit Portfolio

32%

Non-Real Estate

6%

Real Estate

23%

Government,

Agency & Cash

31%

Total Fixed Income Portfolio

As at June 30, 2008

Composition ($34.3 billion)

Fixed Income Portfolio (AA rated) comprised of:

Structured Credit Portfolio (AA+ rated): $10.9B

Non-Structured Credit Portfolio: $23.4B

- Government, Agency & Cash (AA+ rated) $ 10.8B

- Corporate Credit (A rated) $ 12.6B

3

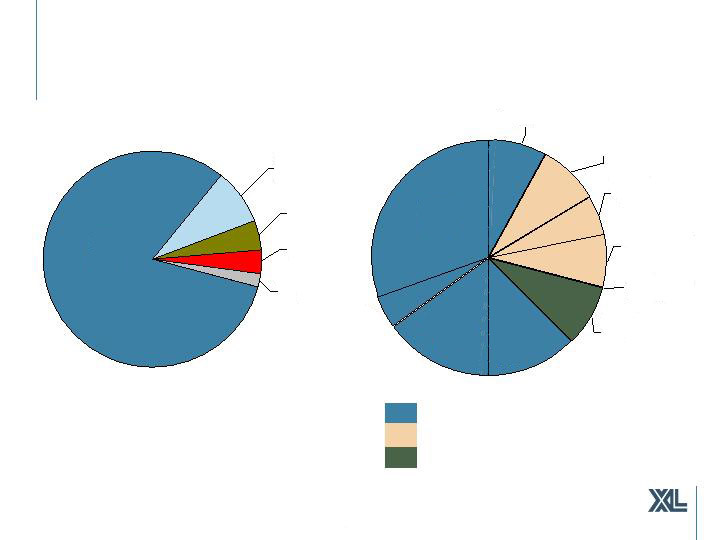

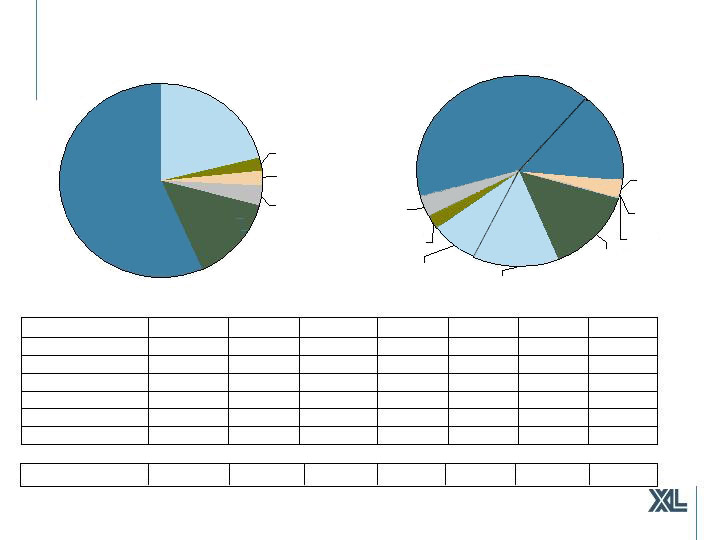

Structured Credit Portfolio- Overview

As at June 30, 2008

BBB

4%

A

5%

BB & Below

1%

AAA

82%

AA

8%

CDO (Excluding ABS CDO)

Non-Real Estate

Real Estate

Alt A

5%

Agency

14%

Whole

Loans

14%

Core CDOs

8%

CDOs - Sub-

Prime, 0%

ABS - Other

7%

ABS - Credit

Card, 6%

ABS - Auto

8%

ABS - RE

7%

CMBS

31%

4

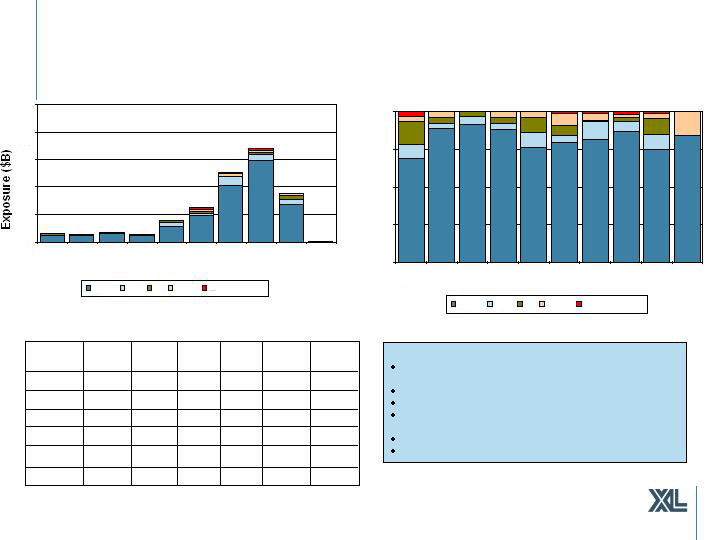

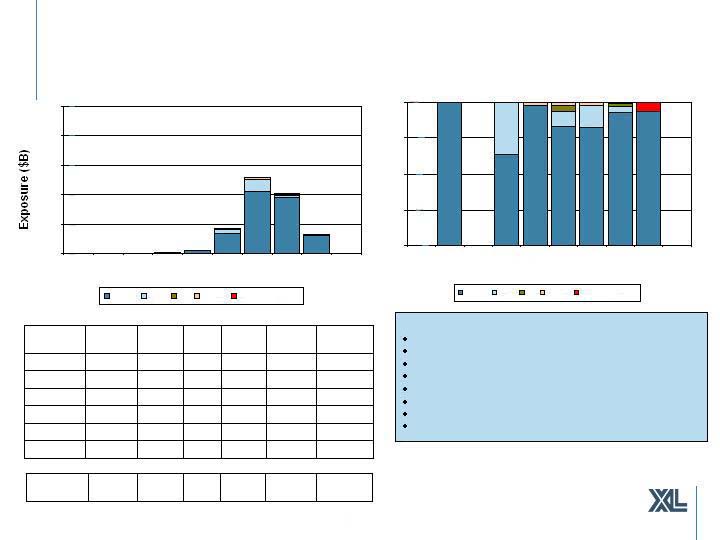

Rating & Vintage Breakdown ($B)

$0

$1

$2

$3

$4

$5

Pre

2000

'00

'01

'02

'03

'04

'05

'06

'07

'08

AAA

AA

A

BBB

BB & Below

Structured Credit Portfolio: $10.9 billion

As at June 30, 2008

Exposures in $Millions

Rating & Vintage Breakdown (%)

0%

25%

50%

75%

100%

Pre

2000

'00

'01

'02

'03

'04

'05

'06

'07

'08

AAA

AA

A

BBB

BB & Below

41

2

7

-

-

32

2008

1,793

13

77

168

185

1,350

2007

10,931

129

426

516

923

8,937

Total

158

111

73

BBB

202

300

236

AA

2,569

2,045

2,941

AAA

3,202

37

236

Other

2,507

24

27

2005

3,388

53

85

2006

Total

BB &

Below

A

Vintage

Key Characteristics:

Includes all US and Non US Asset Backed and Mortgage

Related Securities

Exposure dominated by AAA

Weighted Average Life 4.8 yrs

207 Securities ($440 million) downgraded in Q2’08, of which

$225M related to monoline downgrades

$338 million on negative credit watch

OTTI: Q2 $45 million

5

Rating & Vintage Breakdown ($B)

$0.0

$0.1

$0.2

$0.3

$0.4

$0.5

Pre

2000

'00

'01

'02

'03

'04

'05

'06

'07

'08

AAA

AA

A

BBB

BB & Below

Sub Prime First Lien Securities: $724 million

As at June 30, 2008

Exposures in $Millions

Net Unrealized Gain (Loss) $Millions

(212)

(43)

(13)

(24)

(59)

(73)

Net

Unrealized

Rating & Vintage Breakdown (%)

0%

25%

50%

75%

100%

Pre

2000

'00

'01

'02

'03

'04

'05

'06

'07

'08

AAA

AA

A

BBB

BB & Below

-

-

-

-

-

-

2008

229

4

41

21

46

117

2007

724

24

59

59

163

419

Total

10

4

4

BBB

17

70

30

AA

70

92

140

AAA

120

3

20

Other

184

13

5

2005

191

4

13

2006

Total

BB &

Below

A

Vintage

Key Characteristics:

Overall average credit support: 33%

Weighted average LTV of holdings: 78%

61% pools have weighted average LTVs < 80%

Historical cumulative loss average: 2.3%

Average delinquencies 60+days: 28%

Weighted average life 3.2 years

72 Securities ($155 million) downgraded in Q2’08

OTTI: Q2 $4 million

6

Alt A Securities: $635 million

As at June 30, 2008

Exposures in $Millions

Net Unrealized Gain (Loss) $Millions

(175)

(4)

(4)

(5)

(24)

(138)

Net

Unrealized

-

-

-

-

-

-

2008

67

4

-

-

-

63

2007

635

6

8

10

58

553

Total

2

6

-

BBB

10

40

8

AA

86

213

191

AAA

101

-

3

Other

261

-

2

2005

206

2

5

2006

Total

BB &

Below

A

Vintage

Rating & Vintage Breakdown (%)

0%

25%

50%

75%

100%

Pre

2000

'00

'01

'02

'03

'04

'05

'06

'07

'08

AAA

AA

A

BBB

BB & Below

Rating & Vintage Breakdown ($B)

$0.0

$0.1

$0.2

$0.3

$0.4

$0.5

Pre

2000

'00

'01

'02

'03

'04

'05

'06

'07

'08

AAA

AA

A

BBB

BB & Below

Key Characteristics:

Overall average credit support: 27%

Weighted average LTV of holdings: 73%

69% pools have weighted average LTVs < 80%

Historical cumulative loss average: 1.4%

Average delinquencies 60+days: 14%

Weighted average life 2.9 years

13 Securities ($26 million) downgraded in Q2’08

OTTI: Q2 $12 million

7

Second Lien Securities: $66 million

As at June 30, 2008

Exposures in $Millions

Net Unrealized Gain (Loss) $Millions

(8)

(2)

(3)

(2)

(1)

-

Net

Unrealized

Rating & Vintage Breakdown (%)

0%

25%

50%

75%

100%

Pre

2000

'00

'01

'02

'03

'04

'05

'06

'07

'08

AAA

AA

A

BBB

BB & Below

-

-

-

-

-

-

2008

-

-

-

-

-

-

2007

66

3

10

12

12

29

Total

6

3

1

BBB

8

4

-

AA

11

18

-

AAA

39

2

12

Other

26

1

-

2005

1

-

-

2006

Total

BB &

Below

A

Vintage

Rating & Vintage Breakdown ($B)

$0.0

$0.1

$0.2

$0.3

$0.4

$0.5

Pre

2000

'00

'01

'02

'03

'04

'05

'06

'07

'08

AAA

AA

A

BBB

BB & Below

Key Characteristics:

Overall average credit support: 35%

Weighted average LTV of holdings: 70%

54% pools have weighted average LTVs < 80%

Historical cumulative loss average: 8.2%

Average delinquencies 60+days: 17%

Weighted average life 2.5 years

27 Securities ($12 million) downgraded in Q2’08

OTTI: Q2 $2 million

8

ABS CDOs w/ Sub Prime Collateral: $18 million

As at June 30, 2008

Exposures in $Millions

Net Unrealized Gain (Loss) $Millions

(5)

(1)

-

(1)

(3)

-

Net

Unrealized

Rating & Vintage Breakdown (%)

0%

25%

50%

75%

100%

Pre

2000

'00

'01

'02

'03

'04

'05

'06

'07

'08

AAA

AA

A

BBB

BB & Below

-

-

-

-

-

-

2008

-

-

-

-

-

-

2007

18

7

-

1

5

5

Total

-

-

-

BBB

-

5

-

AA

3

2

-

AAA

3

-

-

Other

12

4

1

2005

3

3

-

2006

Total

BB &

Below

A

Vintage

Rating & Vintage Breakdown ($B)

$0.0

$0.1

$0.2

$0.3

$0.4

$0.5

Pre

2000

'00

'01

'02

'03

'04

'05

'06

'07

'08

AAA

AA

A

BBB

BB & Below

Key Characteristics:

Stress scenarios reflect high probability of principal loss on

certain ABS CDO

Weighted average life 4.5 years

12 Securities ($15 million) downgraded in Q2‘08

OTTI: Q2 $4 million

9

Exposures in $Millions

Net Unrealized Gain (Loss) $Millions

(262)

(14)

(83)

(23)

(111)

(31)

Net

Unrealized

Core CDOs (excl ABS CDO): $903 million

As at June 30, 2008

Rating & Vintage Breakdown (%)

0%

25%

50%

75%

100%

Pre

2000

'00

'01

'02

'03

'04

'05

'06

'07

'08

AAA

AA

A

BBB

BB & Below

-

-

-

-

-

-

2008

170

3

26

17

89

35

2007

903

16

169

65

415

238

Total

39

62

42

BBB

7

151

168

AA

73

73

57

AAA

141

10

12

Other

299

2

11

2005

293

1

25

2006

Total

BB &

Below

A

Vintage

Rating & Vintage Breakdown ($B)

$0.0

$0.1

$0.2

$0.3

$0.4

$0.5

Pre

2000

'00

'01

'02

'03

'04

'05

'06

'07

'08

AAA

AA

A

BBB

BB & Below

Key Characteristics:

All third party managed structures

72% of holdings in CLO; limited covenant lite

Limited residential and commercial real estate

BBB and BB are managed by CDO specialists

160 issues of diversified collateral

Average credit subordination 21%

Weighted average life 6.2 years

3 Securities ($133 thousand) downgraded in Q2’08

OTTI: Q2 $3 million

10

CMBS: $3.4 billion

As at June 30, 2008

Exposures in $Millions

Net Unrealized Gain (Loss) $Millions

(201)

(4)

(3)

(3)

(2)

(189)

Net

Unrealized (1)

Rating & Vintage Breakdown (%)

0.0%

25.0%

50.0%

75.0%

100.0%

Pre

2000

'00

'01

'02

'03

'04

'05

'06

'07

'08

AAA

AA

A

BBB

BB & Below

-

-

-

-

-

-

2008

371

1

1

6

2

361

2007

3,366

26

19

20

22

3,279

Total

4

2

12

BBB

15

2

3

AA

1,191

660

1,067

AAA

1,236

18

8

Other

668

1

3

2005

1,091

6

3

2006

Total

BB &

Below

A

Vintage

Rating & Vintage Breakdown ($B)

$-

$0.2

$0.4

$0.6

$0.8

$1.0

$1.2

$1.4

Pre

2000

'00

'01

'02

'03

'04

'05

'06

'07

'08

AAA

AA

A

BBB

BB & Below

Key Characteristics:

97% AAA; 91% Super/Senior tranches

Average Number of Loans: 166

51% of pools have > 140 loans

57% in Pre 2006 pools; 11% in 2007

Wtd Avg. Credit Enhancement: 26.3%, Levels>20%: 79%

Wtd. Avg. LTV: 67%, Wtd. Avg. DSCR: 1.6

41% experiencing 0% 60+ day delinquency; 78% have rates <1%

4 Securities ($5 million) downgraded in Q2’08

(1) Of the net unrealized losses on CMBS securities, $94 million is the result of the

weakening USD and is offset by the cumulative translation adjustment

11

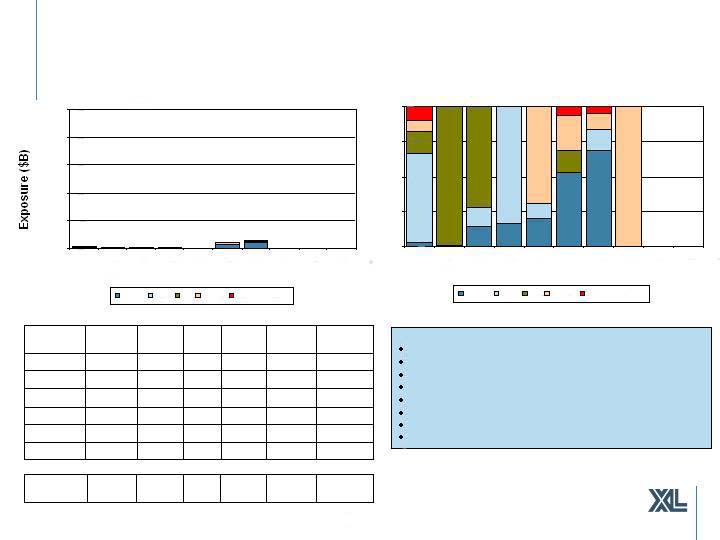

Guarantor Wrapped Assets: $533 million

As at June 30, 2008

By Sector ($M)

Structured

Credit, $305

Corporate,

$125

Muni, $103

Exposures in $Millions

Net Unrealized Gain (Loss) $Millions

(1)

-

(68)

-

(3)

(13)

(22)

(29)

Net Unrealized

Ratings of Underlying (%)

0.0%

25.0%

50.0%

75.0%

100.0%

AMBAC

FGIC

FSA

MBIA

MGIC

RAA

XLCA

AAA

AA

A

BBB

BB & Below

Notes:

Corporate bucket is made up of structured

corporate credit bonds of whole business

assets (non USD)

$57 million of the exposure above relates to “topical” structured credit ($37million Sub Prime; $14 million 2nd Lien; $7 million Alt-A)

128

-

-

1

8

33

51

35

Other

41

-

-

-

3

21

12

5

Auto ABS

57

1

8

-

4

14

10

20

“Topical” (Subprime,

2nd Lien, Alt-A)

150

31

-

46

MBIA

224

27

5

132

AMBAC

533

103

7

197

Total

-

-

11

-

8

Diversified Business

Securitization

-

-

-

-

2

Public Finance

Projects

1

8

12

19

119

Total

-

MGIC

4

FGIC

41

FSA

-

-

Municipal

RAA

SCA

Guarantor

12

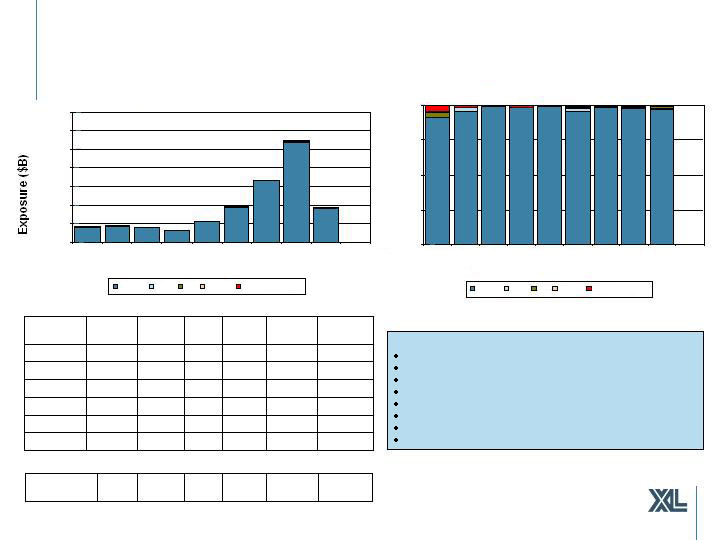

Consumer ABS: $1.5 billion

As at June 30, 2008

8%

117

-

-

-

-

-

117

Student Loan

1,532

558

857

Total

21

-

21

AAA

Wrapped

56%

2

2

30

15

787

Autos

100%

3

42

185

20

1,261

Total

40

BBB

5

AA

357

AAA

36%

1

155

Credit Card

% of

Total

BB &

Below

A

Exposures in $Millions

Credit Card Rating & Vintage Breakdown ($B)

$0.0

$0.1

$0.2

$0.3

$0.4

$0.5

$0.6

Pre

2000

'00

'01

'02

'03

'04

'05

'06

'07

AAA

AA

A

BBB

BB & Below

(4)

(24)

-

(18)

-

-

(2)

Net Unrealized

Net Unrealized Gain (Loss) $Millions

Autos:

Average credit support: 22.1%

11 bonds ($21 million) downgraded in Q2’08

Weighted average life 1.0 years

Credit Cards:

Average excess spread: 14%

Average credit enhancement to charge off

ratio: 4.05

Weighted average life 3.2 years

ABS Auto Rating & Vintage Breakdown ($B)

$0.0

$0.1

$0.2

$0.3

$0.4

$0.5

$0.6

Pre

2000

'00

'01

'02

'03

'04

'05

'06

'07

AAA

AA

A

BBB

BB & Below

13

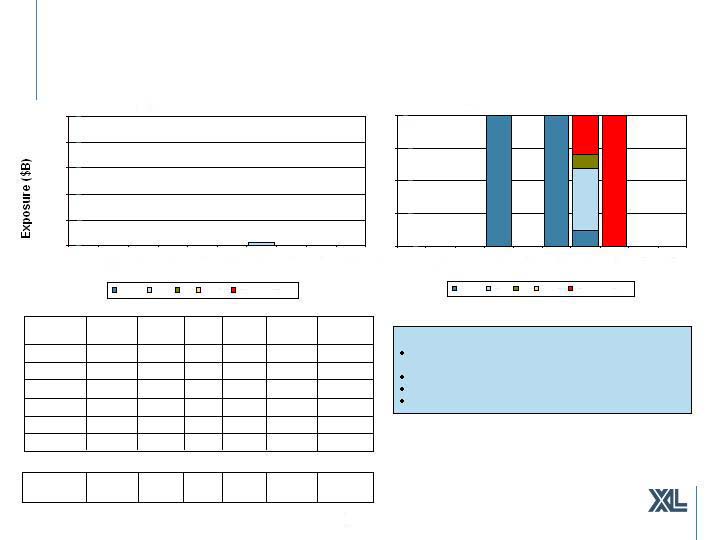

Total US Agency: $3.0 billion

As at June 30, 2008

71

-

-

-

-

71

GNMA

1,508

-

3

-

225

1,209

MBS

426

-

-

177

246

FHLB

97

-

-

-

97

Other

1,209

73

387

406

Senior Debt

17

-

10

7

Preferred Stock

241

-

4

60

Subordinated

626

-

FHLMC

1,683

1

FNMA

2,976

73

Total

1

-

Common Stock

Total

Farmer

Capital

FHLB

14%

Other

3%

Farmer Mac

2%

GNMA, 2%

FHLMC

21%

FNMA

58%

GNMA MBS

2%

Preferred Stock

1%

FNMA Debt

16%

Farmer Debt

2%

Common Equity

0%

FNMA MBS

42%

Other Debt

2%

FHLMC MBS

8%

FHLB Debt

14%

FHLMC Debt

13%

(1)

2

0

(8)

5

(8)

(6)

Net Unrealized

Total Agency Exposures in $Millions

Net Unrealized Gain (Loss) $Millions

14