UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_________________________________________

FORM 10-K

_________________________________________

(Mark One)

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended March 27, 2021

OR

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number 0-19357

_________________________________________

Monro, Inc.

(Exact name of Registrant as specified in its Charter)

New York | 16-0838627 | |||

(State or other jurisdiction | (I.R.S. Employer | |||

| ||||

200 Holleder Parkway, | ||||

Rochester, New York | 14615 | |||

(Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: (585) 647-6400

_________________________________________

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

Common Stock, par value $.01 per share | MNRO | The Nasdaq Stock Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES x NO o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. YES o NO x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES x NO o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit such files). YES x NO o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large Accelerated Filer | x |

| Accelerated Filer | o |

Non-Accelerated Filer | o | Smaller Reporting Company | o | |

Emerging Growth Company | o |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. x

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). YES o NO x

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the Registrant, based on the closing price of the shares of common stock on The Nasdaq Stock Market on September 25, 2020 was $1,331,800,000.

The number of shares of Registrant’s Common Stock outstanding as of May 21, 2021 was 33,492,878.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive Proxy Statement for its 2021 Annual Meeting of Shareholders to be held hereafter are incorporated by reference into Part III of this report.

TABLE OF CONTENTS

PART I

Cautionary Note Regarding Forward-Looking Statements

This Annual Report on Form 10-K contains “forward-looking statements” as that term is used in the Private Securities Litigation Reform Act of 1995. Forward-looking statements can be identified by the fact that they address future events, developments and results and do not relate strictly to historical facts. Any statements contained herein that are not statements of historical fact may be deemed to be forward-looking statements. Forward-looking statements include, without limitation, statements preceded by, followed by or including words such as “anticipate,” “appear,” “believe,” “contemplate,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “potential,” “see,” “strategy,” “vision,” “will,” “would” and variations thereof and similar expressions. Forward-looking statements are subject to risks, uncertainties and other important factors that could cause actual results to differ materially from those expressed. For example, our forward-looking statements include, without limitation, statements regarding:

•the potential effect of general business or economic conditions on our business, including the direct and indirect effects of the novel strain of coronavirus (“COVID-19”) pandemic on the economy, consumer spending levels, and unemployment in our markets;

•the uncertainty of the impact of the COVID-19 pandemic and public health measures on our business and results of operations, including uncertainties surrounding possible disruptions in our supply chain or sources of supply, the physical and financial health of our customers, the effectiveness and duration of government assistance programs to individuals, households and businesses to support consumer spending, levels of traffic in our stores, changes in customer demand for our services, and increased expenses for higher wages and compensation paid to employees and the cost of personal protective equipment and additional cleaning supplies and protocols for the safety of our employees;

•our expectations regarding cost increases in the future, including costs relating to our COVID-19 response initiatives, increases in the minimum wage by states and localities, potential federal minimum wage legislation, increases in distribution and fuel costs and potential new legal requirements to provide increased pay for employees who work during pandemic restrictions;

•the effect of economic conditions, seasonality and the impact of weather conditions and natural disasters on customer demand;

•the dependence on and our expectation regarding competition within the primary markets in which our stores are located;

•our growth plans, including our plans to add, renovate, re-brand, expand, remodel, relocate or close stores and any related costs or charges, our leasing strategy for future expansion, and our ability to renew leases at existing store locations;

•the impact of competitive services and pricing;

•the reliability of, and cost associated with, our sources of parts supply, particularly imported goods such as those sourced from China;

•the impact of trade relations and the ongoing trade dispute between the United States and China, including the actual and potential effect of Section 301 tariffs on Chinese goods imposed by the United States Trade Representative, uncertainties surrounding the policies of the new presidential administration, and other potential impediments to imports;

•the impact of industry regulation;

•our ability to service our debt obligations, including our expected annual interest expense;

•our cash needs, including our ability to fund our future capital expenditures and working capital requirements;

•our anticipated sales, comparable store sales, gross profit margin, costs of goods sold (including product mix), operating, selling, general and administrative expenses and other fixed costs, and our ability to leverage those costs;

•advances in automotive technologies;

•risks relating to disruption or unauthorized access to our computer systems;

•our failure to protect customer and employee personal data;

•business interruptions;

•potential outcomes related to pending or future litigation matters;

•risks relating to acquisitions and the integration of acquired businesses with ours;

•the effect of changes in labor laws, and the effect of the Fair Labor Standards Act as it relates to the qualification of our managers for exempt status, minimum wage and health care law;

•our assessment of the materiality and impact on our business of recent accounting pronouncements adopted by the Financial Accounting Standards Board (“FASB”);

•management’s estimates and expectations as they relate to income tax liabilities, deferred income taxes and uncertain tax positions; and

•management’s estimates associated with our critical accounting policies, including business combinations, self-insurance liabilities and valuations for our goodwill and indefinite-lived intangible assets impairment analyses.

Any of these factors, as well as such other factors as discussed in Part I, Item 1A., “Risk Factors” and throughout Part II, Item 7., “Management’s Discussion and Analysis of Financial Condition and Results of Operations” of this Annual Report on Form 10-K (“Form 10-K”), as well as in our periodic filings with the Securities and Exchange Commission (the “SEC”), could cause our actual results to differ materially from our anticipated results. The information provided in this Form 10-K is based upon the facts and circumstances known as of the date of this report, and any forward-looking statements made by us in this Form 10-K speak only as of the date on which they are made. Except as required by law, we undertake no obligation to update these forward-looking statements after the date of this Form 10-K to reflect events or circumstances after such date, or to reflect the occurrence of unanticipated events.

Introductory Note

Unless otherwise stated, references to “we,” “our,” “us,” “Monro” or the “Company” generally refer to Monro, Inc. and its direct and indirect subsidiaries on a consolidated basis. Unless specifically indicated otherwise, any references to “2021” or “fiscal 2021,” “2020” or “fiscal 2020,” and “2019” or “fiscal 2019” relate to the years ended March 27, 2021, March 28, 2020 and March 30, 2019, respectively.

Available Information

Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 are available free of charge on our website at www.monro.com as soon as reasonably practicable after electronic filing of such reports with the SEC.

Our investor presentation regarding the financial results for the fiscal year ended March 27, 2021 is available and accessible at Monro's Investor Relations page at https://corporate.monro.com/investors. Information available on our website is not a part of, and is not incorporated into, this Form 10-K. We intend to make future investor presentations available exclusively through our Investor Relations page.

Item 1. Business

General

We are a leading nation-wide operator of retail tire and automotive repair stores in the United States. We offer to our customers, referred to as “guests”, replacement tires and tire related services, automotive undercar repair services as well as a broad range of routine maintenance services, primarily on passenger cars, light trucks and vans. We also provide other products and services for brakes; mufflers and exhaust systems; and steering, drive train, suspension and wheel alignment.

We believe the convenience and value we offer are key factors in serving and growing our base of customers. At March 27, 2021, we operated 1,263 retail tire and automotive repair stores and serviced approximately 4.8 million vehicles in fiscal 2021.

Our retail tire and automotive repair stores operate primarily under the names “Monro Auto Service and Tire Centers,” “Tire Choice Auto Service Centers,” “Mr. Tire Auto Service Centers,” “Car-X Tire & Auto,” “Tire Warehouse Tires for Less,” “Ken Towery’s Tire & Auto Care,” “Tire Barn Warehouse,” and “Free Service Tire & Auto Centers.”

Company-operated Store Brands as of March 27, 2021 | Stores | |

Monro Auto Service and Tire Centers | 375 | |

Tire Choice Auto Service Centers | 358 | |

Mr. Tire Auto Service Centers | 321 | |

Car-X Tire & Auto | 57 | |

Tire Warehouse Tires for Less | 55 | |

Ken Towery's Tire & Auto Care | 34 | |

Tire Barn Warehouse | 27 | |

Free Service Tire & Auto Centers | 10 | |

Other (a) | 26 | |

Total | 1,263 |

(a)Recent 2021 and 2020 acquisition stores to be converted to Tire Choice Auto Service Centers brand.

The typical format for a Monro store is a free-standing building consisting of a sales area, fully-equipped service bays and a parts/tires storage area. Most service bays are equipped with above-ground electric vehicle lifts. Generally, each store is located within 25 miles of a “key” store which carries approximately double the inventory of a typical store and serves as a mini-distribution point for slower moving inventory for other stores in its area. Individual store sizes, number of bays and stocking levels vary greatly and are dependent primarily on the availability of suitable store locations, population, demographics and intensity of competition among other factors.

A certain number of our retail locations also service commercial customers. Our locations that serve commercial customers generally operate consistently with our other retail locations, except that the sales mix for these locations includes a higher number of commercial tires.

As of March 27, 2021, Monro had seven wholesale locations and three retread facilities. The wholesale locations, in most cases, sell tires to customers for resale, although these tire sales do not include installation or other tire related services. The retread facilities re-manufacture tires through the replacement of tread on worn tires that are later sold to customers. Monro also had 95 Car-X franchised locations as of March 27, 2021. (Two franchised locations were closed during 2021.)

Our operations are organized and managed in one operating segment. The internal management financial reporting that is the basis for evaluation in order to assess performance and allocate resources by our chief operating decision maker consists of consolidated data that includes the results of our retail, commercial and wholesale locations. As such, our one operating segment reflects how our operations are managed, how resources are allocated, how operating performance is evaluated by senior management and the structure of our internal financial reporting.

Monro incorporated in New York in 1959. We maintain our corporate headquarters in Rochester, New York.

Business Strategy

Our vision is to be America’s leading auto and tire service center, trusted by consumers as the best place in their neighborhoods for quality automotive service and tires. We believe that success in this vision will position Monro to deliver consistent and sustainable organic growth as well as lead to strong, long-term financial performance. Specifically, we are committed to seeing this vision executed across all aspects of the business, through the following actions:

•Exceed guest expectations. We will continue to invest in and execute strategic initiatives to improve our guests’ in-store experience. This ranges from modernized store infrastructure through rebranding and reimaging investments, new tire pricing and category management technology to match customer demand and building an omni-channel presence.

•Provide consistent value. We intend to be able to offer better value than new car dealers to more price-sensitive consumers. Vehicles generally need more service and repairs as they advance in age. However, as consumers’ vehicles age, the consumers’ willingness to pay higher prices decreases. Monro’s service menu is focused on items that are purchased frequently, like oil changes and other scheduled services, along with higher value services like tires, brakes and other undercar services. Our tire pricing and category management system allows us to dynamically track demand trends and make rapid adjustments to optimize our tire assortment by leveraging the breadth of our tire brand portfolio to offer the right tires at what we believe are the right price points.

•Build a committed, knowledgeable organization of friendly and professional teammates. We will continue to invest in technology and training to accelerate productivity and team engagement. This includes our data-driven cloud-based store staffing and scheduling software that re-balances our store technician labor to meet customer demand as well as utilizing Monro University, an extensive cloud-based learning curriculum, to provide our employees, referred to as “teammates,” with the technical training needed to effectively serve our customers today and into the future.

We are committed to building an omni-channel presence through our primary retail websites in order to create a seamless buying experience for our customers. With responsive optimized design for mobile users, a streamlined tire search and improved content and functionality, our retail websites better position us to address our customers’ needs. These websites, aligned with our primary retail names, help customers search for store locations, access coupons, make service appointments, shop for tires and access information on our services and products, as well as car care tips. Importantly, they better showcase the solutions we provide to our customers, including our Good, Better, Best product and service packages.

To minimize the impact of the COVID-19 pandemic on our business, we modified our plans for some of our strategic initiatives, including temporarily suspending all reimaging and rebranding investments related to our store transformation program during the first three months of fiscal 2021. With sales improvement throughout the year, we resumed these investments and completed the store transformation of 147 stores in fiscal 2021. To date, we have completed the transformation of 366 stores.

Growth Strategy

Executing on accretive acquisition opportunities remains a key element of our growth strategy. We have a robust pipeline and believe the fragmentation of our industry allows for many opportunities for consolidation. Using consumer demographic analytics, we believe we are able to better identify targets that operate in the markets with favorable demographics and customer trends, allowing us to enter regions from which we are poised to benefit most. Additionally, to ensure we are capitalizing on these opportunities, we have added talent and an organizational structure to our mergers and acquisitions team, who will work with our management team to ensure we capitalize on the momentum in the market.

During the last five years, we have completed 19 acquisitions, adding 262 locations and approximately $411 million in annualized revenue. Additionally, during this time, we have entered seven states, solidifying our presence in the Southern markets as well as expanding into the Western region. As of March 27, 2021, we have stores in 32 states.

Although acquisition activity was temporarily paused in response to the COVID-19 pandemic during the first six months of fiscal 2021, we continued to evaluate potential acquisition candidates that we believe would fit our growth strategy while maintaining financial discipline, and we acquired 17 retail tire and automotive repair stores located in California during December 2020.

Subsequent to March 27, 2021, we acquired 30 retail tire and automotive repair stores located in California from Mountain View Tire & Service, Inc. on April 25, 2021.

In addition to our plan to continue to seek suitable acquisitions, we plan to add new greenfield stores. Greenfield stores include new construction as well as the acquisition of one to four store operations.

Key factors in market and site selection for selecting new greenfield store locations include population, demographic characteristics, vehicle population and the intensity of competition. We partner with a customer analytics firm to provide market segmentation and demographic data specific to a geographic area in close proximity to a Monro location to identify high value lookalike customers and market directly to them. We attempt to cluster stores in market areas in order to achieve economies of scale in advertising, supervision and distribution costs. All new greenfield sites presently under consideration are within our established market areas.

Purchasing and Distribution

We believe that our substantial buying power and our flexibility in making sourcing decisions contributes to our successful purchasing strategy. We also believe our ability to negotiate with our vendor partners allows us to ensure we are receiving competitive pricing and terms as well as minimize the margin impact of economic pressures such as tariffs.

We select and purchase tires, parts and supplies for all Company-operated stores on a centralized basis through an automatic replenishment system based on operational data we collect from stores on a daily basis. This allows us to control store inventory on a near real-time basis. Additionally, each store has access to the inventory carried by up to the 14 stores or distribution center nearest to it. Management believes that this feature improves customer satisfaction and store productivity by reducing the time required to locate out-of-stock parts and tires. It also improves profitability because it reduces the amount of inventory which must be purchased outside Monro from local vendors. Purchases outside Monro are made when needed at the store level and accounted for approximately 18 percent of all parts and tires used in 2021.

Our ten largest vendors accounted for approximately 73 percent of our total stocking purchases, with the largest vendor accounting for approximately 24 percent of total stocking purchases in 2021. In 2021, Monro imported approximately 26 percent of our parts (excluding batteries, oil and supplies) and tire purchases. We purchase parts, oil and tires from 98 vendors. Management believes that our relationships with vendors are excellent and that alternative sources of supply exist, at comparable cost, for substantially all parts used in our business.

We enter into contracts with certain parts and tire suppliers, some of which require us to buy (at market competitive prices) up to 100 percent of our annual purchases of specific products. These agreements expire at various dates. We believe these agreements provide us with high quality, branded merchandise at preferred pricing, along with strong marketing and training support.

The majority of our parts supply is distributed to our stores through our network of distribution centers, and vendors ship the majority of our tires supply directly to our stores. Stores are generally replenished at least bi-weekly, and such replenishment fills, on average, 96 percent of all items ordered by the automatic replenishment system. Monro operates eleven distribution centers in California, Kentucky, Maryland, New Hampshire, New York, North Carolina, South Carolina and Tennessee.

Human Capital

At Monro, our business success is built upon our dedicated, passionate and diverse teammates who work and live in the communities we serve. We are committed to providing a safe, healthy, inclusive and supportive work environment where teammates embrace our core value of collaboration, feel empowered and are motivated to have enriching and successful careers. We seek to be an employer of choice to attract and retain top talent. To that end, we strive to provide an engaging work experience that excites and motivates our teammates to deliver their best every day as well as provides opportunities for learning and growth, to ensure our team is always the best in the business.

As of March 27, 2021, Monro had approximately 7,800 employees, of whom 7,270 were employed in the field organization, 210 were employed at the distribution centers, 260 were employed at our corporate headquarters, referred to as store support center, and 60 were employed in other offices. Monro's employees are not members of any union. Due to the impact of the COVID-19 pandemic, we reduced our workforce through furlough or other reduction. With sales improvement, we adjusted our workforce to meet demand.

Teammate Retention

We understand that our teammates will benefit from a clear path to advancement and from investments in their continuous learning to allow them to achieve their personal development needs and career growth. To that end, we invest in training and development programs at all levels within the Company. We also leverage annual processes that support individual performance planning, individual professional development planning and a broad review of talent throughout our organization. Our continuous efforts are reflected in our turnover rates, which are our lowest since 2015.

During fiscal 2020 our online training platform, Monro University, was initially focused on the technical and operational excellence training that technicians need to effectively serve our customers today and prepare them to handle future requirements. We have since expanded the platform across a wide variety of topics accessible to our teammates in our stores, distribution centers and store support center.

New technician development has been an area of particular focus for Monro to increase productivity and retention and make it easier for technicians to overcome barriers of joining the industry. One way we do this is by offering a tool purchase program through which trainee technicians can acquire their own set of tools. We also provide Automotive Service Excellence (“ASE”) certification in eight different categories as technicians advance in their careers.

Store and operations managers also have courses available through Monro University that are supplemented with live and on-line vendor training courses. Management training covers topics including safety, customer service, human resources, leadership and scheduling, and is delivered on a regular basis. We believe that involving operations management in the development and delivery of these sessions results in more relevant and actionable training for store managers, helping improve staff retention as well as overall performance.

Monro University also provides targeted training for corporate management and staff, including diversity training, harassment training and people manager training.

We also foster development through annual reviews at which time employees can discuss with their manager goals for aligning their own development with our business objectives.

The compensation for our teammates is tied to, and increases with, increased productivity. Our store compensation plan also streamlines bonus programs, creating consistency and providing us the ability to use human capital more productively across our stores.

In fiscal 2022, we will provide all teammates with an engagement and satisfaction survey, and intend to use those results to inform further strategy and goal-setting.

In addition to providing ongoing learning and development opportunities, ensuring our teammates feel supported is also important in teammate retention. Besides standard employee benefits we offer a confidential Employee Assistance Program with 24/7 support, financial counseling, estate planning, and online resources for parents whose children struggle with developmental disabilities, as well as other services aimed at enhancing our teammates’ well-being.

Workplace Safety

We are committed to providing a safe and secure work environment and have specific safety programs. To identify elevated safety-related risk areas more effectively, we have increased our focus on data gathering, tracking and analysis. With greater insight into real-time data, we can prioritize focus on areas that present the biggest potential hazards to our teammates and identify process improvements. Another important component of our risk analysis is conducting formal and thorough investigations into safety-related incidents. Investigations are analyzed by our Vice President of Risk and Safety as well as our Risk Management Team to determine a root cause, and pro-active plans are in place to improve safety related patterns that emerge, determining the next steps to address these patterns.

Monro’s training programs are key to our strong safety culture. Training increases awareness and helps to reduce and eliminate workplace accidents and injuries. Our Monro University platform has allowed us to conduct more robust and structured trainings based on a teammates’ job position, and Monro’s safety manuals are available at every workstation within our stores and distribution centers and serve as the basis for our safety training and protocols.

COVID-19

Given the significant impact of the COVID-19 pandemic, the end of fiscal 2020 and all of fiscal 2021 presented a unique set of challenges. In February 2020, we formed a COVID-19 Crisis Committee comprised of members of management that has been leading and coordinating the Company’s overall response. This team leads efforts to develop and monitor mitigation and business continuity plans; track all relevant state and local government guidelines, directives and regulations; develop work-from-home plans for non-store teammates; implement safe working protocols for store teams; assess appropriate return-to-office protocols; and provide timely and transparent communications to teammates and key stakeholders. We also incurred additional costs in procuring and distributing the supplies necessary to keep our teammates safe, such as cleaning supplies, face masks and other protective equipment, including sneeze guards installed at each sales counter, as well as investments in technology to allow our teammates to work remotely.

Diversity, Equity and Inclusion

Diversity is one of our core values and we are committed to driving diversity, equity and inclusion across our Company. This commitment will continue to be supported by training and awareness programs as well as focused efforts to recruit, retain, develop and promote a diverse workforce. Our Code of Ethics lays out a zero-tolerance policy for discrimination or harassment behavior.

We are taking action to increase the focus on our diversity efforts and are committed to making continuous progress. In 2020, we formed a Team Resource Group (“TRG”), comprised of a cross-functional coalition of teammates to educate and provide resources and training to help Monro build and maintain an inclusive culture where every teammate feels they belong, can contribute and are

able to reach their full potential. A Diversity, Equity & Inclusion (“DE&I”) expert consultant and the TRG have also been working with the Senior Leadership Team to assist in the formulation of an official DE&I strategy which will include goals and a long-term plan.

We have also added resources to our recruitment team to help launch new hiring initiatives aimed at reaching diverse groups and are also expanding the recruitment platforms we use to broaden our pool of candidates.

We also view training as a tool to foster inclusion and, through Monro University, we provide Unconscious Bias Diversity and Inclusion Awareness courses to our teammates.

Competition

Our segment of the retail industry is fragmented and highly competitive, and the number, size and strength of competitors vary widely from region to region. We operate in the automotive repair service and tire industry, which is currently and is expected to continue to be highly competitive with respect to price, store location, name awareness and customer service. Monro's primary competitors include national and regional undercar, tire specialty and general automotive service chains, both franchised and company-operated; car dealerships, mass merchandisers’ operating service centers; and, to a lesser extent, gas stations, independent garages and Internet tire sellers. Monro considers TBC Corporation (operating primarily under the NTB, Midas and Tire Kingdom brands), Firestone Complete Auto Care service stores, The Pep Boys – Manny, Moe and Jack service stores, Meineke, and Mavis Discount Tire to be direct competitors.

Regulation

We maintain programs to facilitate compliance with various federal, state and local laws and governmental regulations relating to the operation of our business, including, among other things, those regarding employment and labor practices, workplace safety, building and zoning requirements, the handling, storage and disposal of hazardous substances contained in the products that we sell and use in our service bays, the recycling of batteries, tires and used lubricants, and the ownership and operation of real property. We believe that we are in compliance with these applicable laws and regulations, and our related compliance costs are not material.

Monro stores new oil and recycled antifreeze and generates and/or handles used tires and automotive oils, antifreeze and certain solvents, which are disposed of by licensed third-party contractors. In certain states, as required, we also recycle oil filters. Accordingly, we are subject to numerous federal, state and local environmental laws including the Comprehensive Environmental Response Compensation and Liability Act. In addition, the United States Environmental Protection Agency (the "EPA"), under the Resource Conservation and Recovery Act ("RCRA"), as well as various state and local environmental protection agencies, regulate our handling and disposal of certain waste products and other materials. The EPA, under the Clean Air Act, also regulates the installation of catalytic converters, engines and equipment sold or distributed in the United States by periodically spot checking repair jobs, and may impose sanctions, including but not limited to civil penalties of approximately $45,000 per violation (or approximately $45,000 per day for certain willful violations or failures to cooperate with authorities), for violations of RCRA and the Clean Air Act.

Monro strives to maintain an environmentally conscious corporate culture, demonstrated by our recycling policies at our offices, distribution centers and stores. In 2021, Monro recycled approximately 2.5 million gallons of oil and 3.3 million tires, as well as approximately 73,000 vehicle batteries and 316 tons of cardboard, all as part of our commitment to the environment.

Seasonality

Although our business is not highly seasonal, customers do purchase more undercar service during the period of March through October than the period of November through February, when miles driven tend to be lower. Sales of tires are more heavily weighted in the months of May through August, and October through December. The slowest months are typically January through April and September. As a result, profitability is typically lower during slower sales months, or months where mix is more heavily weighted toward tires, which is a lower margin category.

Sales can also be volatile in areas in which we operate as a result of warmer weather in winter months, which typically causes a decline in tire sales, or severe weather, which can result in store closures.

Given our use of a fiscal calendar, there may be some fluctuations between quarters due to holiday shifts in the calendar year and the number of days in a particular fiscal quarter or year. In addition, the COVID-19 outbreak has had an impact on consumer behaviors and customer traffic that may result in temporary changes in the seasonal fluctuations of our business.

Item 1A. Risk Factors

In addition to the risks discussed elsewhere in this annual report, the following are the important factors that could cause Monro’s actual results to differ materially from those projected in any forward looking statements:

Risks Related to our Business

Matters related to the COVID-19 pandemic have and will continue to significantly and adversely impact our business, financial position, results of operations and cash flows.

The spread of COVID-19 has created a global public health crisis that has resulted in widespread volatility and deteriorations in household, business, economic and market conditions. We have experienced negative impacts to demand for our products and services from the COVID-19 pandemic, which has and will continue to adversely affect our results of operations, and we are continuing to experience significant disruption to our normal business operations and may experience further disruption to our planned implementation of certain strategic initiatives.

Our business will continue to be affected by the broader economic effects from the COVID-19 pandemic and related regulatory and individual actions, including customer demand for our products and services. Because more people in the United States are working from home, those workers will likely drive less often, and are less likely to require our services or will require our services less often. If this trend continues, we may see a permanent decline in demand for our services. Although travel by car may replace air travel as the preferred means of transportation because of fear of the spread of COVID-19, the recessionary economic environment resulting from the COVID-19 pandemic may reduce levels of leisure travel, which would reduce the demand for our products and services. We anticipate disruption to the demand for our products and services throughout the course of the pandemic. For example, in fiscal 2021, we experienced significant declines in comparable store sales compared to 2020 due to lower store traffic and reduced store hours as a result of our, individuals’, and governmental responses to the COVID-19 pandemic. Additionally, our growth strategy was impacted by the pandemic, as we paused all store acquisition, rebrand, and reimage initiatives during the first quarter of fiscal 2021 in order to focus our efforts on determining the full impact of the COVID-19 pandemic on our business before restarting them later in fiscal 2021. Given the continuing uncertainty during the pandemic, we may have to pause these initiatives again if necessary to mitigate the effects of the pandemic.

While we have so far been able to source required products at reasonable cost, the pandemic may also affect our supply chain in ways that are beyond our control. We may also incur costs or experience further disruption to comply with new or changing regulations in response to the pandemic.

In addition, our continuing response to the pandemic could divert management’s attention from our key strategic priorities, increase costs as we prioritize health and safety matters for our employees and customers, cause us to reduce, delay, alter or abandon initiatives that may otherwise increase our long-term value, increase vulnerability to information technology or cybersecurity related risks as certain of our employees work remotely and otherwise continue to disrupt our business operations. For example, we have and expect to continue to incur additional costs and investments in supplies necessary to keep our employees and customers safe, such as face masks, hand sanitizer and cleaning supplies. We expect to encounter labor inefficiencies as we adjust to new operating models to adapt to operating during the pandemic while experiencing what we believe will be an increase in sales activity from 2021. Those labor inefficiencies may include difficulty in hiring employees if enhanced unemployment benefits are signed into law. As our employees return to more normalized store hours, there will also be increased risks to the health and safety of our employees and customers, particularly if there were to be one or more clusters of COVID-19 cases occurring at any of our stores or our corporate headquarters. We may also be subject to enhanced legal risks, including potential litigation related to the COVID-19 pandemic.

The overall magnitude of the COVID-19 pandemic, including the extent of its direct and indirect impact on our business, financial position, results of operations or liquidity is inherently uncertain due to the fluidity of the situation. Further, the ultimate impact of the COVID-19 pandemic depends on many factors that are not within our control, including, but not limited to: governmental, business and individuals' actions that have been and continue to be taken in response to the COVID-19 pandemic; the severity and duration of outbreaks of the virus; the effectiveness of vaccines; the impact of the COVID-19 pandemic and actions taken in response on global and regional economies, travel, and economic activity; the availability of federal, state, local or non-U.S. funding programs; general economic uncertainty in key global markets and financial market volatility; global economic conditions and levels of economic growth; and the pace of recovery, particularly in our markets, when the COVID-19 pandemic subsides.

We are unable to estimate the impact of the COVID-19 pandemic with certainty on our business and operations at this time. The pandemic could cause us to experience impairment of our goodwill and other financial assets, further reduce demand for our products and services and other adverse impacts on our financial position, results of operations and cash flows. Sustained adverse effects may also prevent us from satisfying financial covenants in our credit agreement, which would prevent us from paying dividends, or result in downgrades in our credit ratings.

We operate in the highly competitive automotive repair industry.

The automotive repair industry in which we operate is generally highly competitive and fragmented, and the number, size and strength of our competitors vary widely from region to region. We believe that competition in the industry is based primarily on customer service, reputation, store location, name awareness and price. Our primary competitors include national and regional undercar, tire specialty and general automotive service chains, both franchised and company-operated, car dealerships, mass merchandisers operating service centers and, to a lesser extent, gas stations, independent garages and Internet tire sellers. Some of our competitors have greater financial resources, are more geographically diverse and have better name recognition than we do, which might place us at a competitive disadvantage to those competitors. Because we seek to offer competitive prices, if our competitors reduce prices, we may be forced to reduce our prices, which could have a material adverse effect on our business, financial condition and results of operations. Further, our success within this industry also depends upon our ability to respond in a timely manner to changes in customer demands for both products and services. We cannot assure that we, or any of our stores, will be able to compete effectively. If we are unable to compete successfully in new and existing markets, we may not achieve our projected revenue and profitability targets.

We are subject to cycles in the general economy and customers’ use of vehicles and seasonality, which may impact demand for our products and services.

Our industry is influenced by the number of miles driven by automobile owners. Factors that may cause the number of miles driven by automobile owners to decrease include the weather, travel patterns, gas prices and fluctuations in the general economy. For example, as a result of the COVID-19 pandemic, there has been a marked decrease in the number of miles driven by automobile owners due to the various stay-at-home orders across the regions in which we operate. As a result of this reduction in the number of miles driven by automobile owners, there has been a negative effect on the demand for our products and services. As another example, when the retail cost of gasoline increases, the number of miles driven by automobile owners may decrease, which could result in less frequent service intervals and fewer repairs. The number of vehicle miles driven may also decrease if consumers begin to rely more heavily on mass transportation.

Sales can decline in areas in which we operate as a result of warmer weather in winter months or severe weather, which can result in store closures. Although our business is not highly seasonal, our customers typically purchase more undercar services during the period of March through October than the period of November through February, when miles driven tend to be lower. Further, customers may defer or forego vehicle maintenance at any time during periods of inclement weather. Sales of tires are more heavily weighted in the months of May through August, and October through December. The slowest months are typically January through April and September. As a result, profitability is typically lower during slower sales months or months where mix is more heavily weighted toward tires, which is a lower margin category.

Any continued significant reduction in the number of miles driven by automobile owners will have a material adverse effect on our business and results of operations.

Our business is affected by advances in automotive technology.

The demand for our products and services could be adversely affected by continuing developments in automotive technology. Automotive manufacturers are producing cars that last longer and require service and maintenance at less frequent intervals in certain cases. Quality improvement of manufacturers’ original equipment parts has in the past reduced, and may in the future reduce, demand for our products and services, adversely affecting our sales. For example, manufacturers’ use of stainless steel exhaust components has significantly increased the life of those parts, thereby decreasing the demand for exhaust repairs and replacements. Longer and more comprehensive warranty or service programs offered by automobile manufacturers and other third parties also could adversely affect the demand for our products and services. We believe that a majority of new automobile owners have their cars serviced by a dealer during the period that the car is under warranty.

Advances in electric vehicle technology and production may adversely affect the demand for our services because electric vehicles do not have traditional engines, transmissions, and certain related parts. An increase in the proportion of electric vehicles sold could decrease our service-related revenue. In addition, advances in automotive technology continue to require us to incur additional costs to update our diagnostic capabilities and technical training programs. Changes in vehicle and powertrain technology and advances in accident avoidance technology, electric vehicles, autonomous vehicles and mobility could have a negative effect on our business, results of operations or investors’ perception of our business, any of which could have an adverse effect upon the price of our common stock.

Changes in economic conditions that impact consumer spending could harm our business.

The automotive repair industry and our financial performance are sensitive to changes in overall economic conditions that impact consumer spending, including the economic volatility resulting from the COVID-19 pandemic. Future economic conditions affecting consumer income such as employment levels, business conditions, interest rates, inflation and tax rates could reduce consumer spending or cause consumers to shift their spending to other products. During periods of good economic conditions, consumers may decide to purchase new vehicles rather than servicing their older vehicles. In addition, if automobile manufacturers offer lower pricing on new or leased cars, more consumers may purchase or lease new vehicles rather than servicing older vehicles. A general reduction in the level of consumer spending or shifts in consumer spending to other services could have a material adverse effect on our growth, sales and profitability.

Changes in the U.S. trade environment, including the imposition of import tariffs, could adversely affect our consolidated results of operations and cash flows.

In recent years, trade tensions between the U.S. government and China have increased as the U.S. government has implemented and proposed tariffs and the Chinese government proposed retaliatory tariffs. Although we have no foreign operations and do not manufacture any products, tariffs imposed on products that we sell, such as tires, may cause our expenses to increase, which could adversely affect our profitability unless we are able to raise our prices for these products. If we increase the price of products impacted by tariffs, our service offerings may become less attractive relative to services offered by our competitors or cause our customers to delay needed maintenance. Given the uncertainty regarding the scope and duration of these trade actions by the U.S. or other countries, the impact of these trade actions on our operations or results remains uncertain. However, the tariffs, along with any additional tariffs or retaliatory trade restrictions implemented by other countries, could adversely affect the operating profits of our business, which could have an adverse effect on our consolidated results of operations and cash flows.

We depend on our relationships with our vendors, including foreign sources, for certain inventory. Our business may be negatively affected by the risks associated with such relationships and international trade.

We depend on close relationships with our vendors for parts, tires and supplies and for our ability to purchase products at competitive prices and terms. Our ability to purchase at competitive prices and terms results from the volume of our purchases from these vendors. We have entered into various contracts with parts suppliers that require us to buy from them (at market competitive prices) up to 100 percent of our annual purchases of specific products. These agreements expire at various dates.

We believe that alternative sources exist for most of the products we sell or use at our stores, and we would not expect the loss of any one supplier to have a material adverse effect on our business, financial condition or results of operations. If any of our suppliers do not perform adequately or otherwise fail to distribute parts or other supplies to our stores, our inability to replace the suppliers in a timely manner and on acceptable terms could increase our costs and could cause shortages or interruptions that could have a material adverse effect on our business, financial condition and results of operations.

Because we purchase products such as oil and tires, which are subject to cost variations related to commodity costs, if we cannot pass along cost increases, our profitability would be negatively impacted.

In addition, we depend on a number of products (e.g. brake parts, tires, oil filters) produced in foreign markets. Any changes in U.S. trade policies, or uncertainty with respect to the future of U.S. trade policies, resulting in increased costs which we are not able to offset with pricing increases of our own could adversely affect our financial performance.

We also face other risks associated with the delivery of inventory originating outside the United States, including:

potential economic and political instability in countries where our suppliers are located;

increases in shipping costs;

transportation delays and interruptions, including those occurring as a result of the COVID-19 pandemic;

compliance with the United States Foreign Corrupt Practices Act, which generally prohibits U.S. companies from engaging in bribery or making other prohibited payments to foreign officials; and

significant fluctuations in exchange rates between the U.S. dollar and foreign currencies.

If we are unable to generate sufficient cash flows from our operations, our liquidity will suffer and we may be unable to satisfy our obligations.

We currently rely on cash flow from operations and our $600 million revolving credit facility with eight banks (the “Credit Facility”) to fund our business. Amounts outstanding on the Credit Facility are reported as debt on our balance sheet. While we believe that we have the ability to sufficiently fund our planned operations and capital expenditures for the foreseeable future, various risks to our business could result in circumstances that would materially affect our liquidity. For example, cash flows from our operations could be affected by changes in consumer spending habits, the failure to maintain favorable vendor payment terms or our inability to successfully implement sales growth initiatives, among other factors. We may be unsuccessful in securing alternative financing when needed on terms that we consider acceptable.

On March 27, 2020, we borrowed $350 million available under the Credit Facility in order to enhance liquidity and financial flexibility given the uncertain market conditions caused by the COVID-19 pandemic. We subsequently repaid the $350 million previously borrowed during 2021 and there is $190.0 million outstanding under the Credit Facility as of March 27, 2021. A significant increase in our leverage could have the following risks:

our ability to obtain additional financing for working capital, capital expenditures, store renovations, acquisitions or general corporate purposes may be impaired in the future;

our failure to comply with the financial and other restrictive covenants governing our debt, which, among other things, require us to comply with certain financial ratios and limit our ability to incur additional debt and sell assets, could result in an event of default that, if not cured or waived, could have a material adverse effect on our business, financial condition and results of operations; and

our exposure to certain financial market risks, including fluctuations in interest rates associated with bank borrowings could become more significant.

Although we believe that we will remain in compliance with our debt covenants, if we are not able to do so our lenders may restrict our ability to draw on our Credit Facility, which could have a negative impact on our operations, ability to pay dividends, and growth potential, including our ability to complete acquisitions.

Legal, Regulatory and Technological Risks

Our industry is subject to environmental, consumer protection and other regulation.

We are subject to various federal, state and local environmental laws, building and zoning requirements, employment and labor laws and other governmental regulations regarding the operation of our business. For example, we are subject to rules governing the handling, storage and disposal of hazardous substances contained in some of the products such as motor oil that we sell and use at our stores, the recycling of batteries, tires and used lubricants, and the ownership and operation of real property. These laws and regulations can impose fines and criminal sanctions for violations as well as require the installation of pollution control equipment or operational changes to decrease the likelihood of accidental hazardous substance releases. Accordingly, we could become subject to material liabilities relating to the investigation and cleanup of contaminated properties, and to claims alleging personal injury or property damage as a result of exposure to, or release of, hazardous substances. In addition, stricter interpretation of existing laws and regulations, new laws and regulations, the discovery of previously unknown contamination or the imposition of new or increased requirements could require us to incur costs or become the basis of new or increased liabilities that could have a material adverse effect on our business, financial condition and results of operations.

National automotive repair chains have also been the subject of investigations and reports by consumer protection agencies and the Attorneys General of various states. Publicity in connection with these kinds of investigations could have an adverse effect on our sales and, consequently, our business, financial condition and results of operations. State and local governments have also enacted numerous consumer protection laws with which we must comply.

The costs of operating our stores may increase if there are changes in laws governing minimum hourly wages, working conditions, overtime, workers’ compensation and health insurance rates, unemployment tax rates or other laws and regulations. We have experienced and expect further increases in payroll expenses as a result of federal, state and local mandated increases in the minimum wage. In addition, our vendors may be affected by higher minimum wage standards, which may increase the prices we pay for their products. A material increase in these costs that we were unable to offset by increasing our prices or by other means could have a material adverse effect on our business, financial condition and results of operations.

We are involved in litigation from time to time arising from the operation of our business and, as such, we could incur substantial judgments, fines, legal fees or other costs.

We are sometimes the subject of complaints or litigation from customers, employees or other third parties for various actions. From time to time, we are involved in litigation involving claims related to, among other things, breach of contract, negligence, tortious conduct and employment and labor law matters, including payment of wages. We may also face claims related to the COVID-19 pandemic, including claims from employees or customers who contract COVID-19 at our stores or offices. The damages sought against us in some of these litigation proceedings could be substantial.

As disclosed in Part I, Item 3, “Legal Proceedings,” an action has been brought against us by an individual seeking to represent a putative class of store managers for unpaid overtime wages, damages and attorneys’ fees under the Fair Labor Standards Act and class certification under Pennsylvania law for alleged violations of state wage payment laws. Plaintiff alleges that improper deductions were made from store managers’ pay. If we settle these claims or the action is not resolved in our favor, we may suffer reputational damage and incur legal costs, settlements or judgments that exceed the amounts covered by our existing insurance policies. We can provide no assurances that our insurer will insure the legal costs, settlements or judgements we incur in excess of our deductible. If we are unsuccessful in defending ourselves from these claims or if our insurer does not insure us against legal costs we incur in excess of our deductible, the result may materially adversely affect our business, results of operations and financial condition.

Although we maintain liability insurance for some litigation claims, if one or more of the claims were to greatly exceed our insurance coverage limits or if our insurance policies do not cover a claim, this could have a material adverse effect on our business, financial condition, results of operations and cash flows.

Business interruptions may negatively impact our store operations, availability of products and/or the operability of our computer systems, which may have a material negative effect on our business and results of operations. A breach of our computer systems could damage our reputation and have a material adverse effect on our business and results of operations.

If any of our locations in a particular region are unexpectedly closed permanently or for a period of time, it could have a negative impact on our business. Such closures could occur as a result of circumstances out of our control, including war, acts of terrorism, global health crises, extreme weather conditions and other natural disasters. Further, if our ability to obtain products and merchandise for use in our stores is impeded, it could have a negative impact on our business. Factors that could negatively affect our ability to obtain products and merchandise include the sudden inability to import goods into the United States for any reason and the curtailment or delay of commercial transportation. While we do maintain business interruption insurance, there is no guarantee that we will be able to use such insurance for any particular location closure or other interruption in operations.

Additionally, given the number of individual transactions we process each year, it is critical that we maintain uninterrupted operation of our computer and communications hardware and software systems. Our systems could be subject to damage or interruption from power outages, computer and telecommunications failures, computer viruses, security breaches, including breaches of our transaction processing or other systems that result in the compromise of confidential customer data, catastrophic events such as fires, tornadoes and hurricanes, and usage errors by our employees. If our systems are breached, damaged or cease to function properly, we may have to make a significant investment to fix or replace them, we may suffer interruptions in our operations in the interim, we may face costly litigation, and our reputation with our customers may be harmed. The risk of disruption is increased in periods where complex and significant systems changes are undertaken. Any material interruption in our computer operations may have a material adverse effect on our business or results of operations.

If we experience a data security breach and confidential customer or employee information is disclosed, we may be subject to penalties and experience negative publicity, which could affect our customer relationships and have a material adverse effect on our business. We may incur increasing costs in an effort to minimize these cyber security risks.

The nature of our business involves the receipt and storage of personally identifiable data of our customers and employees. This type of data is subject to legislation and regulation in various jurisdictions. We have been subject to cyber-attacks in the past and we may suffer data security breaches arising from future attacks. We may currently be at a higher risk of a security breach due to the COVID-19 pandemic and the increased number of our employees who are working remotely. Data security breaches suffered by well-known companies and institutions have attracted a substantial amount of media attention, prompting state and federal legislative proposals addressing data privacy and security. We may become exposed to potential liabilities with respect to the data that we collect, manage and process, and may incur legal costs if our information security policies and procedures are not effective or if we are required to defend our methods of collection, processing and storage of personal data. Future investigations, lawsuits or adverse publicity relating to our methods of handling personal data could adversely affect our business, results of operations, financial condition and cash flows due to the costs and negative market reaction relating to such developments.

We may not have the resources or technical expertise to anticipate or prevent rapidly evolving types of cyber-attacks. Attacks have been targeted at us, our customers, or others who have entrusted us with information. Actual or anticipated attacks will cause us to incur increased costs, including costs to hire additional personnel, purchase additional protection technologies, train employees, and engage third-party experts and consultants. In addition, data and security breaches can also occur as a result of non-technical issues, including breach by us or by persons with whom we have commercial relationships that result in the unauthorized release of personal or confidential information. Any compromise or breach of our security could result in violation of applicable privacy and other laws, significant legal and financial exposure, and a loss of confidence in our security measures, which could have a material adverse effect on our results of operations and our reputation.

Risks Related to our Strategic Initiatives

We may not be successful in integrating new and acquired stores.

Management believes that our continued growth in sales and profit is dependent, in large part, upon our ability to operate new stores that we open or acquire on a profitable basis. In order to do so, we must find reasonably priced new store locations and acquisition candidates that meet our criteria and we must integrate any new stores (opened or acquired) into our system. Our growth and profitability could be adversely affected if we are unable to open or acquire new stores or if new or existing stores do not operate at a sufficient level of profitability. In addition, our profitability could be adversely affected if we fail to retain key personnel from acquired stores or assume unanticipated liabilities of acquired businesses. To the extent we acquire stores or expand into new geographic regions, we must anticipate the needs of customers and the vehicle population in those regions, which may differ from our existing customers and the vehicle populations we serve, while integrating the stores in the new geographic region into our existing network of stores. If new stores do not achieve expected levels of profitability or we are unable to integrate stores in new geographic regions into our business, our ability to remain in compliance with our debt covenants or to make required payments under our credit facility may be adversely impacted.

If our capital investments in remodeling existing or acquired stores, building new stores, and improving technology do not achieve appropriate returns, our competitive position, financial condition and results of operations could be adversely affected.

Our business depends, in part, on our ability to remodel existing or acquired stores and build new stores in a manner that achieves appropriate returns on our capital investment. Pursuing the wrong remodel or new store opportunities and any delays, cost increases, disruptions or other uncertainties related to those opportunities could adversely affect our results of operations.

We are currently making, and expect to continue to make, significant investments in technology to improve customer experience and certain management systems. The effectiveness of these investments can be less predictable than remodeling stores, and might not provide the anticipated benefits or desired rates of return.

Pursuing the wrong investment opportunities, making an investment commitment significantly above or below our needs, or failing to effectively incorporate acquired businesses into our business could result in the loss of our competitive position and adversely affect our financial condition or results of operations.

Any impairment of goodwill, other intangible assets or long-lived assets could negatively impact our results of operations.

Our goodwill is subject to an impairment test on an annual basis. Goodwill, other intangible assets and long-lived assets are also tested whenever events and circumstances indicate that goodwill, other intangible assets and/or long-lived assets may be impaired. Any excess goodwill resulting from the impairment test must be written off in the period of determination. Intangible assets (other than goodwill and indefinite-lived intangible assets) and other long-lived assets are generally amortized or depreciated over the useful life of such assets. In addition, from time to time, we may acquire or make an investment in a business that will require us to record goodwill based on the purchase price and the value of the acquired tangible and intangible assets. We have significantly increased our goodwill as a result of our acquisitions. We may subsequently experience unforeseen issues with the businesses we acquire, which may adversely affect the anticipated returns of the business or value of the intangible assets and trigger an evaluation of recoverability of the recorded goodwill and intangible assets. Future determinations of significant write-offs of goodwill, intangible assets or other long-lived assets, as a result of an impairment test or any accelerated amortization or depreciation of other intangible assets or other long-lived assets, including those caused by the impact of the COVID-19 pandemic, could have a material negative impact on our results of operations and financial condition.

Planned store closings have resulted in acceleration of costs and future store closings could result in additional costs.

From time to time, in the ordinary course of our business, we close certain stores, generally based on considerations of store profitability, competition, strategic factors and other considerations. The economic impact of the COVID-19 pandemic may require us

to close certain stores either temporarily or permanently. Closing a store could subject us to costs including the write-down of leasehold improvements, equipment, furniture and fixtures. In addition, we could remain liable for future lease obligations.

General Risk Factors

We may not pay or may reduce the dividends on our common stock.

Holders of our common stock are only entitled to receive such dividends as our Board of Directors may declare out of funds legally available for such payments. Although we have historically declared cash dividends on our common stock, we are not required to do so and may reduce or eliminate our common stock dividend in the future. This could adversely affect the market price of our common stock.

We rely on an adequate supply of skilled field personnel.

In order to continue to provide high quality services, we require an adequate supply of skilled field managers and technicians. Trained and experienced automotive field personnel are in high demand, and may be in short supply in some areas. We cannot assure that we will be able to attract, motivate and maintain an adequate skilled workforce necessary to operate our existing and future stores efficiently, or that labor expenses will not increase as a result of a shortage in the supply of skilled field personnel, thereby adversely impacting our financial performance. While the automotive repair industry generally operates with high field employee turnover, any material increases in employee turnover rates in our stores, inability to recruit new employees or any widespread employee dissatisfaction could also have a material adverse effect on our business, financial condition and results of operations.

We depend on the services of our key executives.

Our senior executives are important to our success because they have been instrumental in setting our strategic direction, operating our business, identifying, recruiting and training key personnel, identifying expansion opportunities and arranging necessary financing. Losing the services of any of these individuals could adversely affect our business until a suitable replacement is found. It may be difficult to replace them quickly with executives of comparable experience and capabilities. Although we have employment agreements with certain of our executives, we cannot prevent them from terminating their employment with us. To the extent we have turnover within our management team, we may have to spend more time and resources training new members of management and integrating them in our company. The loss of service of any one of our key executives would likely cause a disruption in our business plans and may adversely impact our results of operations.

We have had significant changes in executive leadership, and more changes could occur. Changes to strategic or operating goals, which can occur with the appointment of new executives, can create uncertainty, and may ultimately be unsuccessful. In addition, executive leadership transition periods, including adding new personnel, could be difficult as new executives gain an understanding of our business and strategy. Difficulty integrating new executives, or the loss of key individuals could limit our ability to successfully execute our business strategy and could have an adverse effect on our overall financial condition.

The market price of our common stock may be volatile and could expose us to shareholder action including securities class action litigation.

The stock market and the price of our common stock may be subject to wide fluctuations based upon general economic and market conditions. Downturns in the stock market may cause the price of our common stock to decline. The market price of our stock may also be affected by our ability to meet analysts’ expectations. Failure to meet such expectations, even slightly, could have an adverse effect on the price of our common stock. In the past, following periods of volatility in the market price of a company’s securities, shareholder action including securities class action litigation has often been instituted against such a company. If similar litigation were instituted against us, it could result in substantial costs and a diversion of our management’s attention and resources, which could have an adverse effect on our business.

Item 1B. Unresolved Staff Comments

None.

Item 2. Properties

Company-operated Stores as of March 27, 2021 | Stores | Company-operated Stores as of March 27, 2021 | Stores | |||

Arkansas | 2 | Minnesota | 9 | |||

California | 68 | Missouri | 26 | |||

Connecticut | 36 | Nevada | 14 | |||

Delaware | 6 | New Hampshire | 29 | |||

Florida | 107 | New Jersey | 44 | |||

Georgia | 13 | New York | 145 | |||

Idaho | 4 | North Carolina | 56 | |||

Illinois | 33 | Ohio | 142 | |||

Indiana | 39 | Pennsylvania | 130 | |||

Iowa | 3 | Rhode Island | 11 | |||

Kentucky | 33 | South Carolina | 18 | |||

Louisiana | 17 | Tennessee | 17 | |||

Maine | 18 | Vermont | 7 | |||

Maryland | 70 | Virginia | 70 | |||

Massachusetts | 40 | West Virginia | 10 | |||

Michigan | 31 | Wisconsin | 15 | |||

Total | 1,263 |

Company-operated Stores and Other Properties as of March 27, 2021 | Distribution | Retread | ||||

Stores | Centers | Facilities | ||||

Owned | 329 | 2 | 1 | |||

Leased | 871 | 9 | 2 | |||

Owned buildings on leased land | 63 | — | — | |||

Total | 1,263 | 11 | 3 |

Our policy is to situate new Company-operated stores in the best locations, without regard to the form of ownership required to develop the locations. In general, we lease store sites for a ten-year period with several renewal options (up to ten years). Giving effect to all renewal options, approximately 63 percent of the leases (587 stores) expire after March 2031. Certain leases provide for contingent rental payments if a percentage of annual gross sales exceed the base fixed rental amount. The highest contingent percentage rent of any lease is 7.5 percent, and no such lease has adversely affected profitability of the store subject thereto.

Our seven wholesale locations are situated within distribution centers that are leased.

We own our corporate headquarters building located in Rochester, New York, and we lease and own additional office space elsewhere in the U.S.

Item 3. Legal Proceedings

From time to time we are a party to or otherwise involved in legal proceedings arising out of the normal course of business. Legal matters are subject to inherent uncertainties and there exists the possibility that the ultimate resolution of one or more of these matters could have a material adverse impact on the Company, its financial condition and results of operations.

On June 12, 2020, former service store manager Mark Cerini filed suit in the U.S. District Court for the Western District of Pennsylvania. The Plaintiff is seeking nationwide collective action certification to represent similarly-situated store managers for unpaid overtime wages, damages and attorneys’ fees under the Fair Labor Standards Act and class certification under Pennsylvania law for alleged violations of state wage payment laws. Plaintiff alleges that improper deductions were made from store managers’ pay. We dispute and believe we have meritorious defenses against these claims and plan to vigorously defend ourselves.

Item 4. Mine Safety Disclosures

Not applicable.

PART II

Item 5. Market for the Company's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Market Information

Monro’s common stock, par value $.01 per share, (the “Common Stock”) is traded on the Nasdaq Stock Market under the symbol "MNRO".

Holders of Record

At May 14, 2021, Monro’s Common Stock was held by approximately 43 shareholders of record. This figure does not include an estimate of the indeterminate number of beneficial holders whose shares may be held of record by brokerage firms and clearing agencies.

Dividends

The declaration of and determination as to the payment of future dividends will be at the discretion of the Board of Directors and will depend on our financial condition, results of operations, capital requirements, compliance with charter and contractual restrictions, and such other factors as the Board of Directors deems relevant. We currently expect that comparable cash dividends will continue to be paid in the future. Under our Credit Facility, we may declare, make or pay any dividend or distribution up to $38.5 million in the aggregate for the period from June 30, 2020 to June 30, 2021 if we are in compliance with the financial covenants and other restrictions in the Credit Facility, as amended. For additional information regarding our Credit Facility, see Note 7 to the Company’s consolidated financial statements.

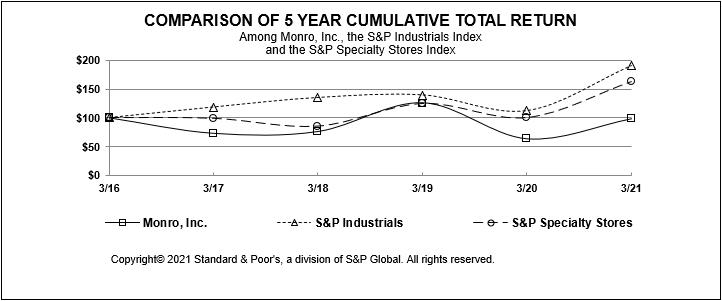

Fiscal Years Ended March | ||||||||||||||||||

2016 | 2017 | 2018 | 2019 | 2020 | 2021 | |||||||||||||

Monro, Inc. | $ | 100.00 | $ | 73.76 | $ | 76.97 | $ | 125.70 | $ | 64.51 | $ | 98.46 | ||||||

S&P Industrials Index | 100.00 | 118.38 | 134.89 | 139.25 | 112.14 | 190.20 | ||||||||||||

S&P Specialty Stores Index | 100.00 | 98.60 | 85.19 | 124.31 | 99.97 | 162.33 | ||||||||||||