Exhibit 99.2

October 30, 2017 Management Presentation Third Quarter 2017 Results

1 FORWARD LOOKING STATEMENTS & OTHER INFORMATION This presentation, including our “ 2017 Financial Outlook”, contains forward - looking statements . The Company’s representatives may also make forward - looking statements orally from time to time . Statements in this presentation that are not historical facts, including statements about the Company’s beliefs and expectations, earnings guidance, recent business and economic trends, potential acquisitions, and estimates of amounts for redeemable noncontrolling interests and deferred acquisition consideration, constitute forward - looking statements . These statements are based on current plans, estimates and projections, and are subject to change based on a number of factors, including those outlined below . Forward - looking statements speak only as of the date they are made, and the Company undertakes no obligation to update publicly any of them in light of new information or future events, if any . Forward - looking statements involve inherent risks and uncertainties . A number of important factors could cause actual results to differ materially from those contained in any forward - looking statements . Such risk factors include, but are not limited to, the following : • risks associated with severe effects of international, national and regional economic conditions ; • the Company’s ability to attract new clients and retain existing clients; • the spending patterns and financial success of the Company’s clients; • the Company’s ability to retain and attract key employees; • the Company’s ability to remain in compliance with its debt agreements and the Company’s ability to finance its contingent pa yme nt obligations when due and payable, including but not limited to those relating to redeemable noncontrolling interests and deferred acquisition consideration; • the successful completion and integration of acquisitions which compliment and expand the Company’s business capabilities; • foreign currency fluctuations; and • risks associated with the ongoing Canadian class litigation claim. The Company’s business strategy includes ongoing efforts to engage in acquisitions of ownership interests in entities in the marketing communications services industry . The Company intends to finance these acquisitions by using available cash from operations and through incurrence of bridge or other debt financing, either of which may increase the Company’s leverage ratios, or by issuing equity, which may have a dilutive impact on existing shareholders proportionate ownership . At any given time the Company may be engaged in a number of discussions that may result in one or more acquisitions . These opportunities require confidentiality and may involve negotiations that require quick responses by the Company . Although there is uncertainty that any of these discussions will result in definitive agreements or the completion of any transactions, the announcement of any such transaction may lead to increased volatility in the trading price of the Company’s securities . Investors should carefully consider these risk factors and the additional risk factors outlined in more detail in the Annual Report on Form 10 - K under the caption “Risk Factors” and in the Company’s other SEC filings .

2 THIRD QUARTER 2017 SUMMARY » Strong execution with solid financial results across all key financial metrics » Industry - leading organic revenue growth, including gains in the U.S. in key verticals such as CPG, and continued double - digit growth internationally » Increases in both Adjusted EBITDA and Adjusted EBITDA margin aided by the continued growth of our business, yields from investments made in emerging growth areas, and leverage of our cost structure » Ongoing success securing high profile, global and integrated assignments » Best year - to - date working capital performance since MDC Media strategy launched in 2014 » Deferred acquisition consideration and minority interest at new five year low » On track to achieve all of our full year financial targets; guidance reiterated Note: See appendix for definitions of non - GAAP measures

3 » Revenue increased 7.6% to $375.8 million from $349.3 million » Organic revenue growth of 7.8%, including a 180 basis points benefit from increased billable pass - through costs » Net income attributable to MDC Partners common shareholders increased to $16.5 million from a loss of ($32.1) million last year 1 » Adjusted EBITDA increased 16.4% to $53.8 million from $46.3 million, with margins of 14.3% versus 13.2% a year ago » Net new business wins of $25.6 million THIRD QUARTER 2017 FINANCIAL HIGHLIGHTS 1 Revised due to the correction of prior period financial statements relating to the Company’s deferred tax liability and incom e t ax expense. Note: See appendix for definitions of non - GAAP measures

4 » Revenue increased 11.6% to $1.11 billion from $995.3 million » Organic revenue growth of 8.4%, including a 200 basis points benefit from increased billable pass - through costs » Net income attributable to MDC Partners common shareholders increased to $14.8 million from a loss of ($54.9) million last year 1 » Adjusted EBITDA increased 13.0% to $136.6 million from $121.0 million, with margins of 12.3% versus 12.2% a year ago » Net new business wins of $77.2 million YEAR - TO - DATE FINANCIAL HIGHLIGHTS 1 Revised due to the correction of prior period financial statements relating to the Company’s deferred tax liability and incom e t ax expense. Note: See appendix for definitions of non - GAAP measures

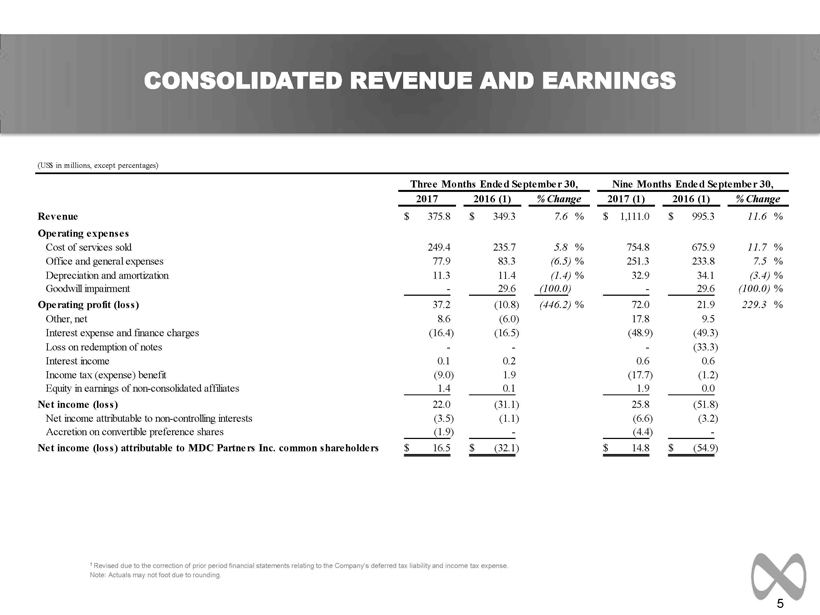

5 CONSOLIDATED REVENUE AND EARNINGS 1 Revised due to the correction of prior period financial statements relating to the Company’s deferred tax liability and incom e t ax expense. Note: Actuals may not foot due to rounding. (US$ in millions, except percentages) 2017 2016 (1) 2017 (1) 2016 (1) Revenue 375.8$ 349.3$ 7.6 % 1,111.0$ 995.3$ 11.6 % Operating expenses Cost of services sold 249.4 235.7 5.8 % 754.8 675.9 11.7 % Office and general expenses 77.9 83.3 (6.5) % 251.3 233.8 7.5 % Depreciation and amortization 11.3 11.4 (1.4) % 32.9 34.1 (3.4) % Goodwill impairment - 29.6 (100.0) - 29.6 (100.0) % Operating profit (loss) 37.2 (10.8) (446.2) % 72.0 21.9 229.3 % Other, net 8.6 (6.0) 17.8 9.5 Interest expense and finance charges (16.4) (16.5) (48.9) (49.3) Loss on redemption of notes - - - (33.3) Interest income 0.1 0.2 0.6 0.6 Income tax (expense) benefit (9.0) 1.9 (17.7) (1.2) Equity in earnings of non-consolidated affiliates 1.4 0.1 1.9 0.0 Net income (loss) 22.0 (31.1) 25.8 (51.8) Net income attributable to non-controlling interests (3.5) (1.1) (6.6) (3.2) Accretion on convertible preference shares (1.9) - (4.4) - Net income (loss) attributable to MDC Partners Inc. common shareholders 16.5$ (32.1)$ 14.8$ (54.9)$ % Change Three Months Ended September 30, Nine Months Ended September 30, % Change

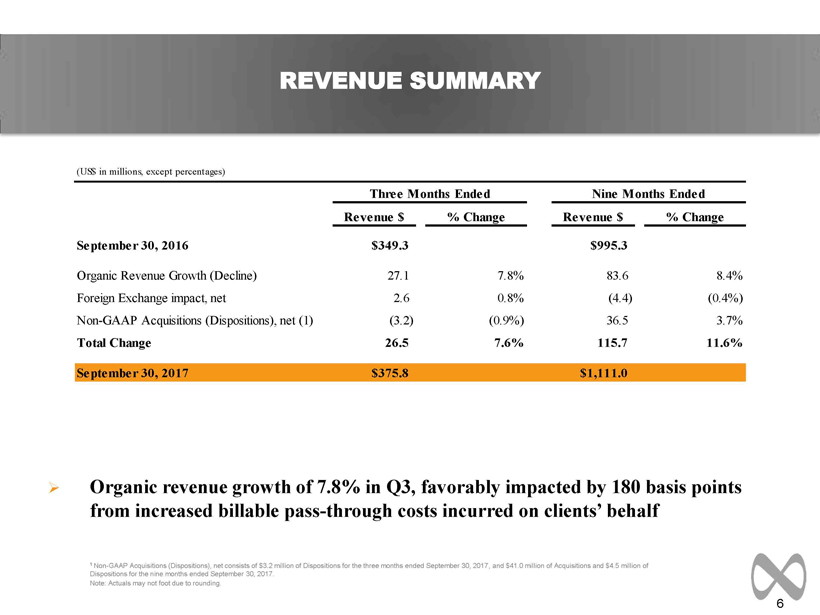

6 » Organic revenue growth of 7.8% in Q3, favorably impacted by 180 basis points from increased billable pass - through costs incurred on clients’ behalf REVENUE SUMMARY 1 Non - GAAP Acquisitions (Dispositions), net consists of $3.2 million of Dispositions for the three months ended September 30, 2017 , and $41.0 million of Acquisitions and $4.5 million of Dispositions for the nine months ended September 30, 2017. Note: Actuals may not foot due to rounding. (US$ in millions, except percentages) Revenue $ % Change Revenue $ % Change September 30, 2016 $349.3 $995.3 Organic Revenue Growth (Decline) 27.1 7.8% 83.6 8.4% Foreign Exchange impact, net 2.6 0.8% (4.4) (0.4%) Non-GAAP Acquisitions (Dispositions), net (1) (3.2) (0.9%) 36.5 3.7% Total Change 26.5 7.6% 115.7 11.6% September 30, 2017 $375.8 $1,111.0 Three Months Ended Nine Months Ended

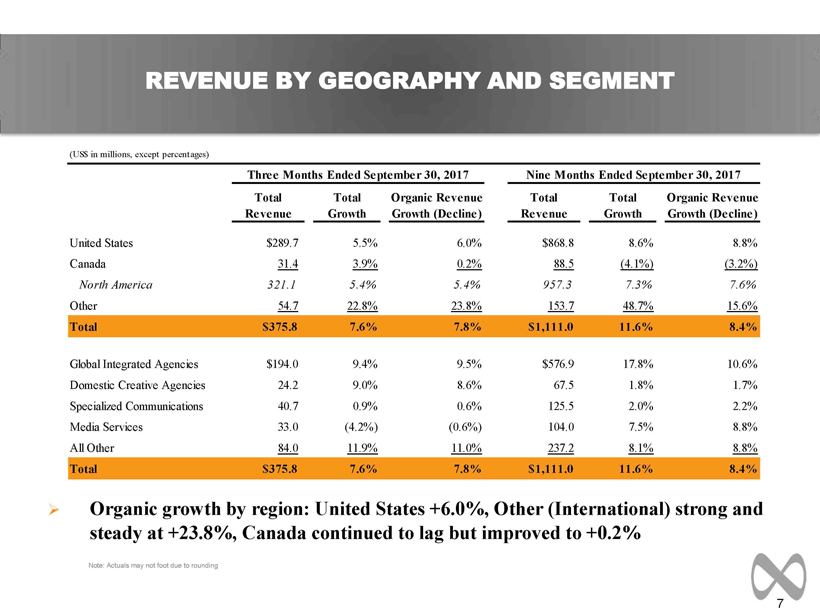

7 REVENUE BY GEOGRAPHY AND SEGMENT » Organic growth by region: United States +6.0%, Other (International) strong and steady at +23.8%, Canada continued to lag but improved to +0.2% Note: Actuals may not foot due to rounding (US$ in millions, except percentages) Total Total Organic Revenue Total Total Organic Revenue Revenue Growth Growth (Decline) Revenue Growth Growth (Decline) United States $289.7 5.5% 6.0% $868.8 8.6% 8.8% Canada 31.4 3.9% 0.2% 88.5 (4.1%) (3.2%) North America 321.1 5.4% 5.4% 957.3 7.3% 7.6% Other 54.7 22.8% 23.8% 153.7 48.7% 15.6% Total $375.8 7.6% 7.8% $1,111.0 11.6% 8.4% Global Integrated Agencies $194.0 9.4% 9.5% $576.9 17.8% 10.6% Domestic Creative Agencies 24.2 9.0% 8.6% 67.5 1.8% 1.7% Specialized Communications 40.7 0.9% 0.6% 125.5 2.0% 2.2% Media Services 33.0 (4.2%) (0.6%) 104.0 7.5% 8.8% All Other 84.0 11.9% 11.0% 237.2 8.1% 8.8% Total $375.8 7.6% 7.8% $1,111.0 11.6% 8.4% Three Months Ended September 30, 2017 Nine Months Ended September 30, 2017

8 Year - over - Year Growth by Category » Best performing sectors: Communications, Financials, Food & Beverage » Top 10 clients decreased to 22.3% of revenue vs 22.4% a year ago (largest <4%) REVENUE BY CLIENT INDUSTRY Q3 2017 2017 YTD Above 10% Communications, Financials, Food & Beverage, Consumer Products Communications, Food & Beverage, Financials, Consumer Products 0% to 10% Healthcare, Transportation & Travel Healthcare, Automotive, Transportation & Travel Below 0% Technology, Retail, Automotive Retail, Technology Note: Actuals may not foot due to rounding. Year - over - year category growth shown on a reported basis. Q3 2017 Mix

9 » Margin expansion of 110 basis points during Q3 and 10 basis points year - to - date ADJUSTED EBITDA 1 Adjusted EBITDA is a non - GAAP measure. See appendix for the definition. Note: Actuals may not foot due to rounding. (US$ in millions, except percentages) 2017 2016 2017 2016 Advertising and Communications Group 62.4$ 53.4$ 16.8 % 161.7$ 148.9$ 8.5 % Global Integrated Agencies 31.9 28.4 12.5 % 73.9 69.5 6.3 % Domestic Creative Agencies 6.2 4.9 26.4 % 15.5 16.3 (5.1) % Specialized Communications 6.8 6.0 14.0 % 20.0 18.6 7.5 % Media Services 3.6 3.0 18.4 % 12.4 9.0 37.7 % All Other 13.8 11.1 24.7 % 39.8 35.4 12.3 % Corporate Group (8.5) (7.1) 19.7 % (25.0) (28.0) (10.5) % Adjusted EBITDA (1) 53.8$ 46.3$ 16.4 % 136.6$ 121.0$ 13.0 % margin 14.3% 13.2% 12.3% 12.2% % Change Three Months Ended September 30, Nine Months Ended September 30, % Change

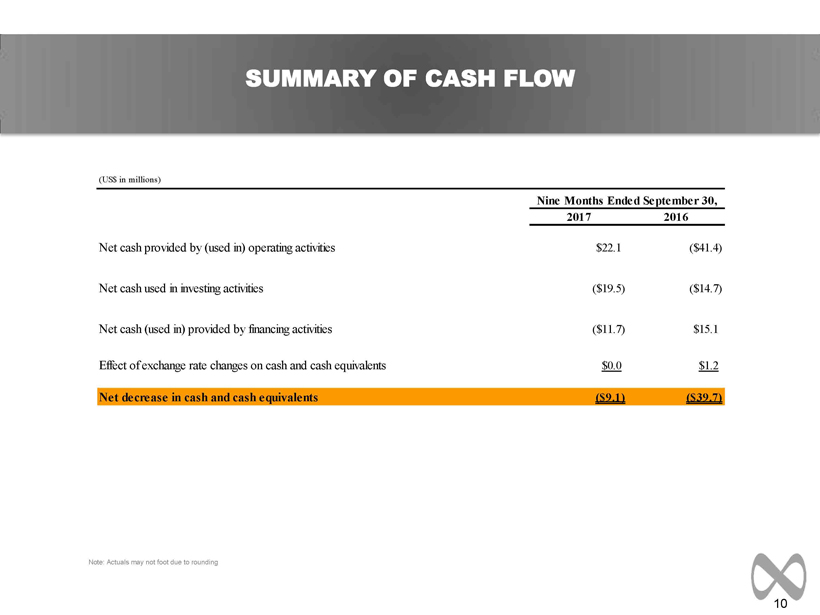

10 SUMMARY OF CASH FLOW Note: Actuals may not foot due to rounding (US$ in millions) 2017 2016 Net cash provided by (used in) operating activities $22.1 ($41.4) Net cash used in investing activities ($19.5) ($14.7) Net cash (used in) provided by financing activities ($11.7) $15.1 Effect of exchange rate changes on cash and cash equivalents $0.0 $1.2 Net decrease in cash and cash equivalents ($9.1) ($39.7) Nine Months Ended September 30,

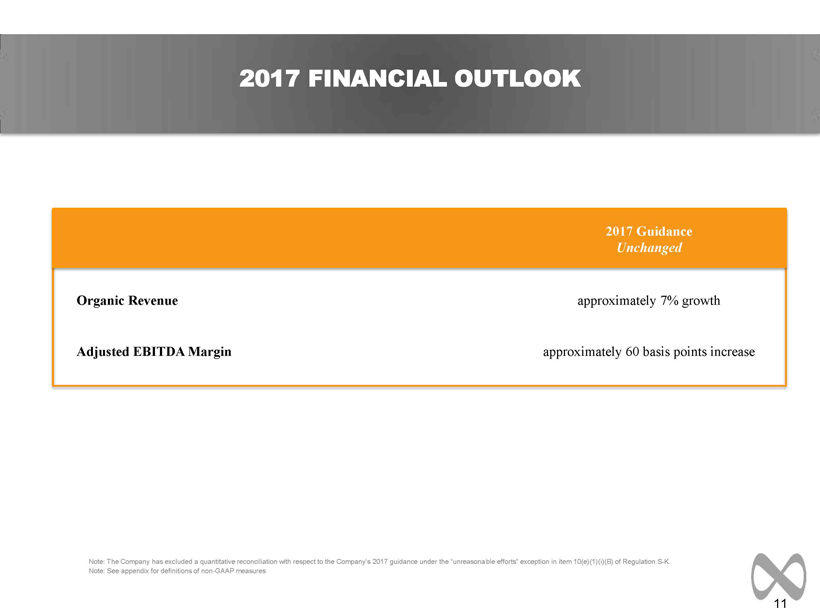

11 2017 FINANCIAL OUTLOOK Organic Revenue Adjusted EBITDA Margin Note: The Company has excluded a quantitative reconciliation with respect to the Company’s 2017 guidance under the “unreasona ble efforts” exception in item 10(e)(1)( i )(B) of Regulation S - K. Note: See appendix for definitions of non - GAAP measures approximately 7% growth approximately 60 basis points increase 2017 Guidance Unchanged

12 APPENDIX

13 REVENUE TRENDING SCHEDULE Note: See appendix for definitions of non - GAAP measures Note: Actuals may not foot due to rounding (US$ in thousands, except percentages) Q1 Q2 Q3 Q4 FY Q1 Q2 Q3 Q4 FY Q1 Q2 Q3 YTD Revenue United States $252,018 $271,375 $270,512 $291,147 $1,085,051 $252,199 $272,992 $274,506 $304,016 $1,103,712 $274,682 $304,463 $289,701 $868,847 Canada 29,826 35,433 29,560 34,221 129,039 28,406 33,614 30,233 31,848 124,101 26,470 30,583 31,418 88,470 North America 281,843 306,807 300,072 325,368 1,214,090 280,605 306,606 304,739 335,864 1,227,813 301,152 335,046 321,119 957,317 Other 20,379 29,799 28,345 33,645 112,168 28,437 30,442 44,515 54,578 157,972 43,548 55,487 54,680 153,715 Total $302,222 $336,606 $328,417 $359,013 $1,326,258 $309,042 $337,048 $349,254 $390,442 $1,385,785 $344,700 $390,533 $375,799 $1,111,032 % of Revenue United States 83.4% 80.6% 82.4% 81.1% 81.8% 81.6% 81.0% 78.6% 77.9% 79.6% 79.7% 78.0% 77.1% 78.2% Canada 9.9% 10.5% 9.0% 9.5% 9.7% 9.2% 10.0% 8.7% 8.2% 9.0% 7.7% 7.8% 8.4% 8.0% North America 93.3% 91.1% 91.4% 90.6% 91.5% 90.8% 91.0% 87.3% 86.0% 88.6% 87.4% 85.8% 85.4% 86.2% Other 6.7% 8.9% 8.6% 9.4% 8.5% 9.2% 9.0% 12.7% 14.0% 11.4% 12.6% 14.2% 14.6% 13.8% Total 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% Total Growth % United States 10.1% 11.6% 8.6% 6.9% 9.2% 0.1% 0.6% 1.5% 4.4% 1.7% 8.9% 11.5% 5.5% 8.6% Canada (3.5%) (9.2%) (22.3%) (19.3%) (14.2%) (4.8%) (5.1%) 2.3% (6.9%) (3.8%) (6.8%) (9.0%) 3.9% (4.1%) North America 8.5% 8.7% 4.5% 3.4% 6.1% (0.4%) (0.1%) 1.6% 3.2% 1.1% 7.3% 9.3% 5.4% 7.3% Other 34.9% 73.3% 27.6% 33.9% 40.8% 39.5% 2.2% 57.0% 62.2% 40.8% 53.1% 82.3% 22.8% 48.7% Total 10.0% 12.4% 6.1% 5.6% 8.4% 2.3% 0.1% 6.3% 8.8% 4.5% 11.5% 15.9% 7.6% 11.6% Organic Revenue Growth (Decline) % United States 6.9% 6.6% 6.1% 5.9% 6.4% (1.2%) (0.1%) 1.0% 4.3% 1.1% 8.9% 11.5% 6.0% 8.8% Canada 3.2% 2.1% (5.5%) (4.3%) (1.4%) 4.5% (0.6%) 2.0% (6.0%) (0.2%) (7.6%) (2.5%) 0.2% (3.2%) North America 6.5% 6.0% 4.6% 4.5% 5.4% (0.6%) (0.1%) 1.1% 3.2% 1.0% 7.2% 10.0% 5.4% 7.6% Other 23.7% 45.5% 20.0% 39.9% 31.9% 41.4% 4.7% 19.1% 9.5% 16.5% (11.1%) 28.5% 23.8% 15.6% Total 7.4% 8.3% 5.7% 7.2% 7.1% 2.2% 0.3% 2.7% 3.8% 2.3% 5.6% 11.7% 7.8% 8.4% Growth % from Foreign Exchange United States 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% Canada (11.2%) (11.3%) (16.8%) (15.0%) (13.7%) (9.3%) (4.6%) 0.3% 0.5% (3.2%) 3.2% (4.6%) 4.2% 0.7% North America (1.3%) (1.6%) (2.2%) (2.0%) (1.8%) (1.0%) (0.5%) 0.0% 0.1% (0.3%) 0.3% (0.5%) 0.4% 0.1% Other (12.5%) (16.5%) (11.7%) (7.6%) (12.1%) (4.3%) (3.0%) (7.4%) (13.4%) (7.5%) (9.8%) (11.7%) 3.0% (4.9%) Total (2.0%) (2.4%) (2.9%) (2.4%) (2.5%) (1.2%) (0.7%) (0.6%) (1.2%) (0.9%) (0.6%) (1.5%) 0.8% (0.4%) Growth % from Acquisitions (Dispositions), net United States 3.2% 5.0% 2.5% 1.0% 2.8% 1.3% 0.7% 0.4% 0.2% 0.6% 0.0% 0.0% (0.5%) (0.2%) Canada 4.5% 0.0% 0.0% 0.0% 0.9% 0.0% 0.0% 0.0% (1.5%) (0.4%) (2.4%) 2.0% (0.5%) (1.6%) North America 3.4% 4.3% 2.1% 0.8% 2.6% 1.2% 0.6% 0.4% 0.0% 0.5% (0.2%) (0.2%) (0.5%) (0.3%) Other 23.8% 44.2% 19.3% 1.6% 21.0% 2.4% 0.5% 45.3% 66.1% 31.9% 74.1% 65.5% (3.9%) 37.9% Total 4.5% 6.6% 3.4% 0.9% 3.8% 1.3% 0.6% 4.3% 6.2% 3.2% 6.6% 5.7% (0.9%) 3.7% 2015 2016 2017

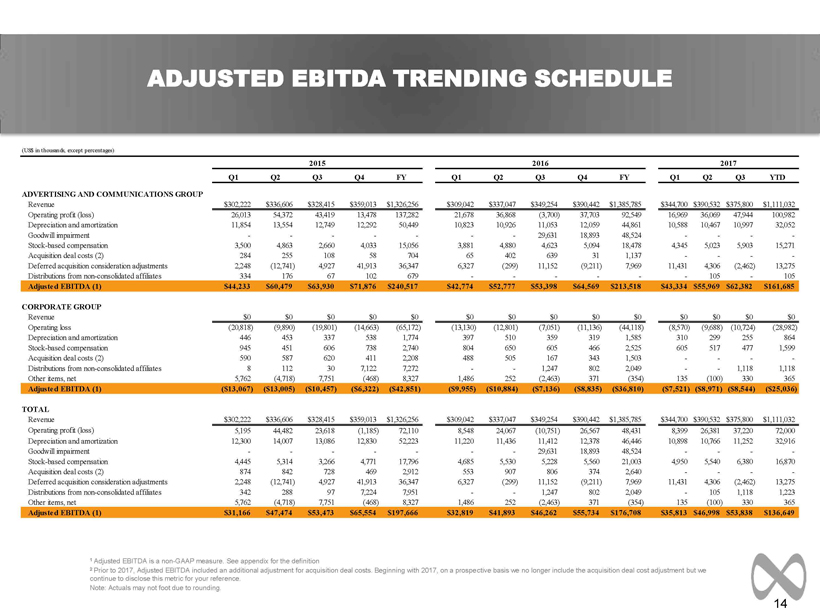

14 ADJUSTED EBITDA TRENDING SCHEDULE 1 Adjusted EBITDA is a non - GAAP measure. See appendix for the definition 2 Prior to 2017, Adjusted EBITDA included an additional adjustment for acquisition deal costs. Beginning with 2017, on a prospe cti ve basis we no longer include the acquisition deal cost adjustment but we continue to disclose this metric for your reference. Note: Actuals may not foot due to rounding. (US$ in thousands, except percentages) Q1 Q2 Q3 Q4 FY Q1 Q2 Q3 Q4 FY Q1 Q2 Q3 YTD ADVERTISING AND COMMUNICATIONS GROUP Revenue $302,222 $336,606 $328,415 $359,013 $1,326,256 $309,042 $337,047 $349,254 $390,442 $1,385,785 $344,700 $390,532 $375,800 $1,111,032 Operating profit (loss) 26,013 54,372 43,419 13,478 137,282 21,678 36,868 (3,700) 37,703 92,549 16,969 36,069 47,944 100,982 Depreciation and amortization 11,854 13,554 12,749 12,292 50,449 10,823 10,926 11,053 12,059 44,861 10,588 10,467 10,997 32,052 Goodwill impairment - - - - - - - 29,631 18,893 48,524 - - - - Stock-based compensation 3,500 4,863 2,660 4,033 15,056 3,881 4,880 4,623 5,094 18,478 4,345 5,023 5,903 15,271 Acquisition deal costs (2) 284 255 108 58 704 65 402 639 31 1,137 - - - - Deferred acquisition consideration adjustments 2,248 (12,741) 4,927 41,913 36,347 6,327 (299) 11,152 (9,211) 7,969 11,431 4,306 (2,462) 13,275 Distributions from non-consolidated affiliates 334 176 67 102 679 - - - - - - 105 - 105 Adjusted EBITDA (1) $44,233 $60,479 $63,930 $71,876 $240,517 $42,774 $52,777 $53,398 $64,569 $213,518 $43,334 $55,969 $62,382 $161,685 CORPORATE GROUP Revenue $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 Operating loss (20,818) (9,890) (19,801) (14,663) (65,172) (13,130) (12,801) (7,051) (11,136) (44,118) (8,570) (9,688) (10,724) (28,982) Depreciation and amortization 446 453 337 538 1,774 397 510 359 319 1,585 310 299 255 864 Stock-based compensation 945 451 606 738 2,740 804 650 605 466 2,525 605 517 477 1,599 Acquisition deal costs (2) 590 587 620 411 2,208 488 505 167 343 1,503 - - - - Distributions from non-consolidated affiliates 8 112 30 7,122 7,272 - - 1,247 802 2,049 - - 1,118 1,118 Other items, net 5,762 (4,718) 7,751 (468) 8,327 1,486 252 (2,463) 371 (354) 135 (100) 330 365 Adjusted EBITDA (1) ($13,067) ($13,005) ($10,457) ($6,322) ($42,851) ($9,955) ($10,884) ($7,136) ($8,835) ($36,810) ($7,521) ($8,971) ($8,544) ($25,036) TOTAL Revenue $302,222 $336,606 $328,415 $359,013 $1,326,256 $309,042 $337,047 $349,254 $390,442 $1,385,785 $344,700 $390,532 $375,800 $1,111,032 Operating profit (loss) 5,195 44,482 23,618 (1,185) 72,110 8,548 24,067 (10,751) 26,567 48,431 8,399 26,381 37,220 72,000 Depreciation and amortization 12,300 14,007 13,086 12,830 52,223 11,220 11,436 11,412 12,378 46,446 10,898 10,766 11,252 32,916 Goodwill impairment - - - - - - - 29,631 18,893 48,524 - - - - Stock-based compensation 4,445 5,314 3,266 4,771 17,796 4,685 5,530 5,228 5,560 21,003 4,950 5,540 6,380 16,870 Acquisition deal costs (2) 874 842 728 469 2,912 553 907 806 374 2,640 - - - - Deferred acquisition consideration adjustments 2,248 (12,741) 4,927 41,913 36,347 6,327 (299) 11,152 (9,211) 7,969 11,431 4,306 (2,462) 13,275 Distributions from non-consolidated affiliates 342 288 97 7,224 7,951 - - 1,247 802 2,049 - 105 1,118 1,223 Other items, net 5,762 (4,718) 7,751 (468) 8,327 1,486 252 (2,463) 371 (354) 135 (100) 330 365 Adjusted EBITDA (1) $31,166 $47,474 $53,473 $65,554 $197,666 $32,819 $41,893 $46,262 $55,734 $176,708 $35,813 $46,998 $53,838 $136,649 2015 2016 2017

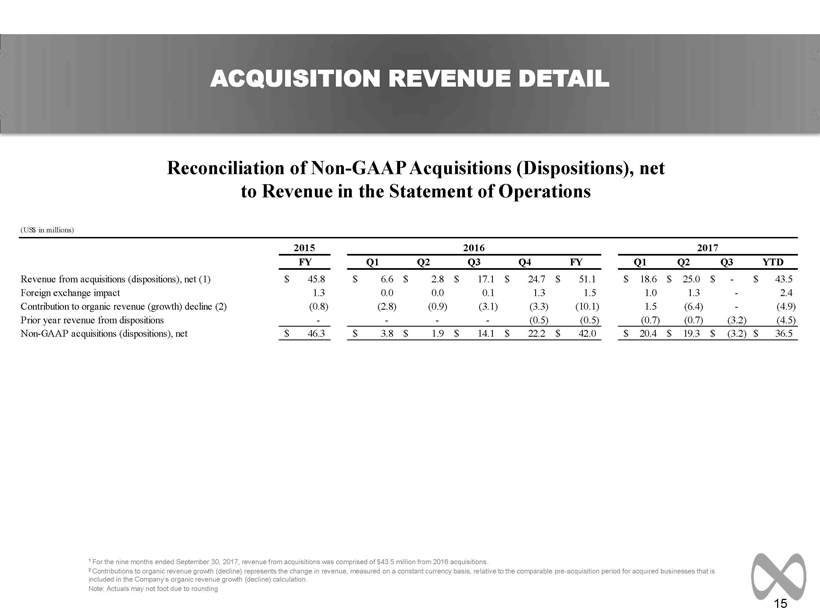

15 ACQUISITION REVENUE DETAIL 1 For the nine months ended September 30, 2017, revenue from acquisitions was comprised of $43.5 million from 2016 acquisitions . 2 Contributions to organic revenue growth (decline) represents the change in revenue, measured on a constant currency basis, re lat ive to the comparable pre - acquisition period for acquired businesses that is included in the Company’s organic revenue growth (decline) calculation. Note: Actuals may not foot due to rounding Reconciliation of Non - GAAP Acquisitions (Dispositions), net to Revenue in the Statement of Operations (US$ in millions) 2015 FY Q1 Q2 Q3 Q4 FY Q1 Q2 Q3 YTD Revenue from acquisitions (dispositions), net (1) 45.8$ 6.6$ 2.8$ 17.1$ 24.7$ 51.1$ 18.6$ 25.0$ -$ 43.5$ Foreign exchange impact 1.3 0.0 0.0 0.1 1.3 1.5 1.0 1.3 - 2.4 Contribution to organic revenue (growth) decline (2) (0.8) (2.8) (0.9) (3.1) (3.3) (10.1) 1.5 (6.4) - (4.9) Prior year revenue from dispositions - - - - (0.5) (0.5) (0.7) (0.7) (3.2) (4.5) Non-GAAP acquisitions (dispositions), net 46.3$ 3.8$ 1.9$ 14.1$ 22.2$ 42.0$ 20.4$ 19.3$ (3.2)$ 36.5$ 2016 2017

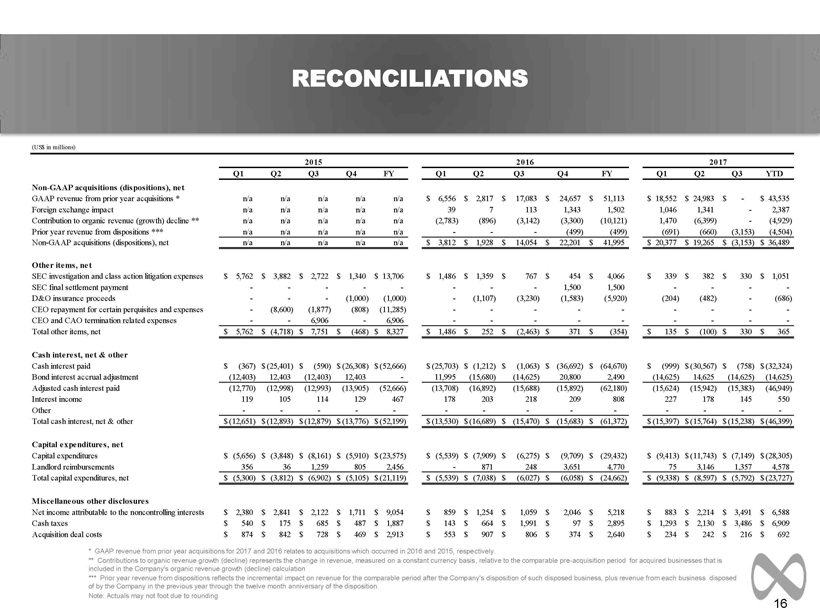

16 RECONCILIATIONS * GAAP revenue from prior year acquisitions for 2017 and 2016 relates to acquisitions which occurred in 2016 and 2015, respe cti vely. ** Contributions to organic revenue growth (decline) represents the change in revenue, measured on a constant currency basis , r elative to the comparable pre - acquisition period for acquired businesses that is included in the Company's organic revenue growth (decline) calculation *** Prior year revenue from dispositions reflects the incremental impact on revenue for the comparable period after the Comp any 's disposition of such disposed business, plus revenue from each business disposed of by the Company in the previous year through the twelve month anniversary of the disposition. Note: Actuals may not foot due to rounding (US$ in millions) Q1 Q2 Q3 Q4 FY Q1 Q2 Q3 Q4 FY Q1 Q2 Q3 YTD Non-GAAP acquisitions (dispositions), net GAAP revenue from prior year acquisitions * n/a n/a n/a n/a n/a 6,556$ 2,817$ 17,083$ 24,657$ 51,113$ 18,552$ 24,983$ -$ 43,535$ Foreign exchange impact n/a n/a n/a n/a n/a 39 7 113 1,343 1,502 1,046 1,341 - 2,387 Contribution to organic revenue (growth) decline ** n/a n/a n/a n/a n/a (2,783) (896) (3,142) (3,300) (10,121) 1,470 (6,399) - (4,929) Prior year revenue from dispositions *** n/a n/a n/a n/a n/a - - - (499) (499) (691) (660) (3,153) (4,504) Non-GAAP acquisitions (dispositions), net n/a n/a n/a n/a n/a 3,812$ 1,928$ 14,054$ 22,201$ 41,995$ 20,377$ 19,265$ (3,153)$ 36,489$ Other items, net SEC investigation and class action litigation expenses 5,762$ 3,882$ 2,722$ 1,340$ 13,706$ 1,486$ 1,359$ 767$ 454$ 4,066$ 339$ 382$ 330$ 1,051$ SEC final settlement payment - - - - - - - - 1,500 1,500 - - - - D&O insurance proceeds - - - (1,000) (1,000) - (1,107) (3,230) (1,583) (5,920) (204) (482) - (686) CEO repayment for certain perquisites and expenses - (8,600) (1,877) (808) (11,285) - - - - - - - - - CEO and CAO termination related expenses - - 6,906 - 6,906 - - - - - - - - - Total other items, net 5,762$ (4,718)$ 7,751$ (468)$ 8,327$ 1,486$ 252$ (2,463)$ 371$ (354)$ 135$ (100)$ 330$ 365$ Cash interest, net & other Cash interest paid (367)$ (25,401)$ (590)$ (26,308)$ (52,666)$ (25,703)$ (1,212)$ (1,063)$ (36,692)$ (64,670)$ (999)$ (30,567)$ (758)$ (32,324)$ Bond interest accrual adjustment (12,403) 12,403 (12,403) 12,403 - 11,995 (15,680) (14,625) 20,800 2,490 (14,625) 14,625 (14,625) (14,625) Adjusted cash interest paid (12,770) (12,998) (12,993) (13,905) (52,666) (13,708) (16,892) (15,688) (15,892) (62,180) (15,624) (15,942) (15,383) (46,949) Interest income 119 105 114 129 467 178 203 218 209 808 227 178 145 550 Other - - - - - - - - - - - - - - Total cash interest, net & other (12,651)$ (12,893)$ (12,879)$ (13,776)$ (52,199)$ (13,530)$ (16,689)$ (15,470)$ (15,683)$ (61,372)$ (15,397)$ (15,764)$ (15,238)$ (46,399)$ Capital expenditures, net Capital expenditures (5,656)$ (3,848)$ (8,161)$ (5,910)$ (23,575)$ (5,539)$ (7,909)$ (6,275)$ (9,709)$ (29,432)$ (9,413)$ (11,743)$ (7,149)$ (28,305)$ Landlord reimbursements 356 36 1,259 805 2,456 - 871 248 3,651 4,770 75 3,146 1,357 4,578 Total capital expenditures, net (5,300)$ (3,812)$ (6,902)$ (5,105)$ (21,119)$ (5,539)$ (7,038)$ (6,027)$ (6,058)$ (24,662)$ (9,338)$ (8,597)$ (5,792)$ (23,727)$ Miscellaneous other disclosures Net income attributable to the noncontrolling interests 2,380$ 2,841$ 2,122$ 1,711$ 9,054$ 859$ 1,254$ 1,059$ 2,046$ 5,218$ 883$ 2,214$ 3,491$ 6,588$ Cash taxes 540$ 175$ 685$ 487$ 1,887$ 143$ 664$ 1,991$ 97$ 2,895$ 1,293$ 2,130$ 3,486$ 6,909$ Acquisition deal costs 874$ 842$ 728$ 469$ 2,913$ 553$ 907$ 806$ 374$ 2,640$ 234$ 242$ 216$ 692$ 2015 2016 2017

17 AVAILABLE LIQUIDITY 1 1 Subject to available borrowings under the Credit Facility. Note: Actuals may not foot due to rounding (US$ in millions) September 30, 2017 December 31, 2016 Commitment Under Facility $325.0 $325.0 Drawn 48.6 54.4 26.7$ Undrawn Letters of Credit 5.0 4.4 Undrawn Commitments Under Facility $271.4 $266.2 Total Cash & Cash Equivalents 18.9 27.9 Liquidity $290.3 $294.1

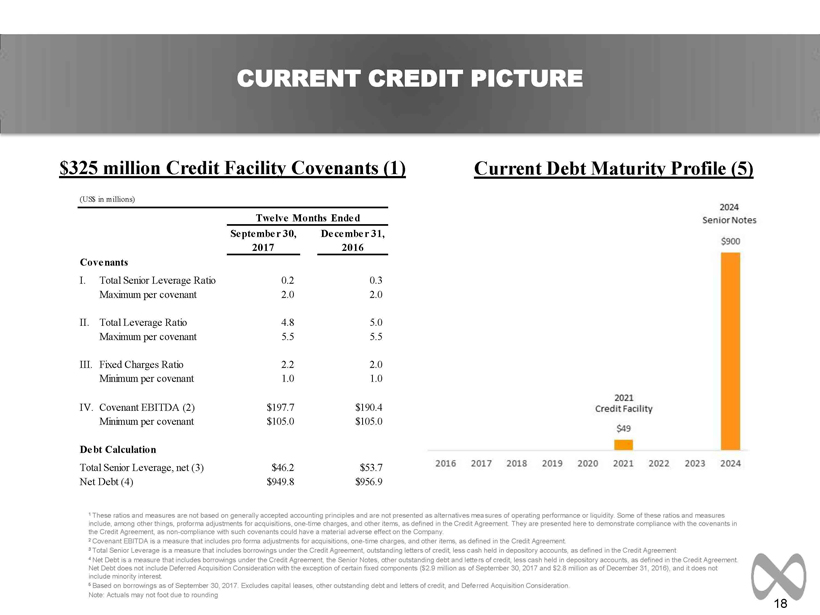

18 CURRENT CREDIT PICTURE 1 These ratios and measures are not based on generally accepted accounting principles and are not presented as alternatives mea sur es of operating performance or liquidity. Some of these ratios and measures include, among other things, proforma adjustments for acquisitions, one - time charges, and other items, as defined in the Credit Agreement. They are presented here to demonstrate compliance with the covenants in the Credit Agreement, as non - compliance with such covenants could have a material adverse effect on the Company. 2 Covenant EBITDA is a measure that includes pro forma adjustments for acquisitions, one - time charges, and other items, as defined in the Credit Agreement. 3 Total Senior Leverage is a measure that includes borrowings under the Credit Agreement, outstanding letters of credit, less c ash held in depository accounts, as defined in the Credit Agreement 4 Net Debt is a measure that includes borrowings under the Credit Agreement, the Senior Notes, other outstanding debt and lette rs of credit, less cash held in depository accounts, as defined in the Credit Agreement. Net Debt does not include Deferred Acquisition Consideration with the exception of certain fixed components ($2.9 million as of September 30, 2017 and $2.8 million as of December 31, 2016), and it does not include minority interest. 5 Based on borrowings as of September 30, 2017. Excludes capital leases, other outstanding debt and letters of credit, and Defe rre d Acquisition Consideration. Note: Actuals may not foot due to rounding Current Debt Maturity Profile (5) $325 million Credit Facility Covenants (1) (US$ in millions) September 30, December 31, 2017 2016 Covenants I. Total Senior Leverage Ratio 0.2 0.3 Maximum per covenant 2.0 2.0 II. Total Leverage Ratio 4.8 5.0 Maximum per covenant 5.5 5.5 III. Fixed Charges Ratio 2.2 2.0 Minimum per covenant 1.0 1.0 IV. Covenant EBITDA (2) $197.7 $190.4 Minimum per covenant $105.0 $105.0 Debt Calculation Total Senior Leverage, net (3) $46.2 $53.7 Net Debt (4) $949.8 $956.9 Twelve Months Ended

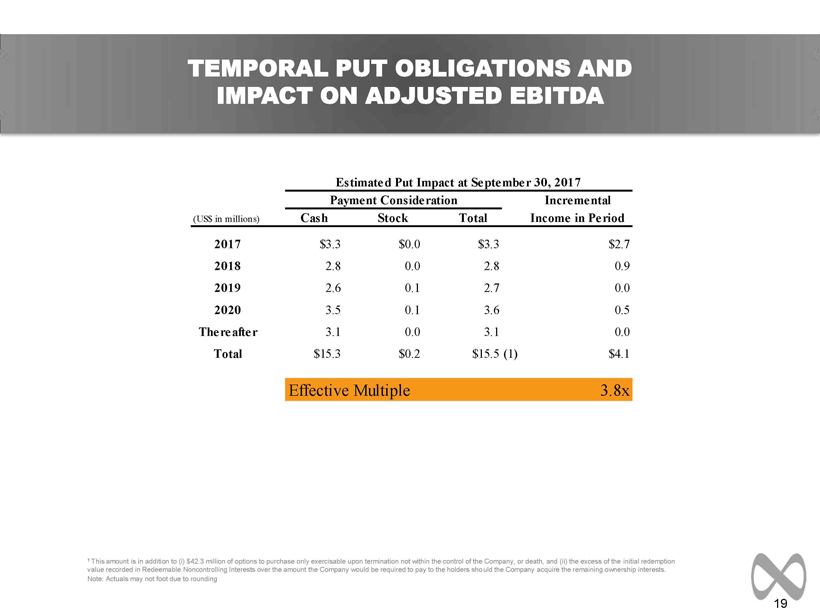

19 TEMPORAL PUT OBLIGATIONS AND IMPACT ON ADJUSTED EBITDA 1 This amount is in addition to ( i ) $42.3 million of opti ons to purchase only exercisable upon termination not within the control of the Company, or death, and (ii) the excess of the in itial redemption value recorded in Redeemable Noncontrolling Interests over the amount the Company would be required to pay to the holders sho uld the Company acquire the remaining ownership interests. Note: Actuals may not foot due to rounding Incremental (US$ in millions) Cash Stock Total Income in Period 2017 $3.3 $0.0 $3.3 $2.7 2018 2.8 0.0 2.8 0.9 2019 2.6 0.1 2.7 0.0 2020 3.5 0.1 3.6 0.5 Thereafter 3.1 0.0 3.1 0.0 Total $15.3 $0.2 $15.5(1) $4.1 Effective Multiple 3.8x Estimated Put Impact at September 30, 2017 Payment Consideration

20 DEFINITION OF NON - GAAP MEASURES In addition to its reported results, MDC Partners has included in its earnings release and supplemental management presentati on certain financial results that the Securities and Exchange Commission defines as "non - GAAP financial measures." Management believes that such non - GAAP financial m easures, when read in conjunction with the Company's reported results, can provide useful supplemental information for investors analyzing period t o p eriod comparisons of the Company's results. Such non - GAAP financial measures include the following: Organic Revenue: Organic Revenue: “Organic revenue growth” and “organic revenue decline” refer to the positive or negative results, respective l y, of subtracting both the foreign exchange and acquisition (disposition) components from total revenue growth. The acquisition (disposition) c omp onent is calculated by aggregating prior period revenue for any acquired businesses, less the prior period revenue of any businesses that were dispo sed of during the current period. The organic revenue growth (decline) component reflects the constant currency impact of (a) the change in revenue of the partner fir ms which the Company has held throughout each of the comparable periods presented, and (b) “non - GAAP acquisitions (dispositions), net”. Non - GAAP acquisitions (dispositions), net consists of ( i ) for acquisitions during the current year, the revenue effect from such acquisition as if the acquisition had been owned durin g t he equivalent period in the prior year and (ii) for acquisitions during the previous year, the revenue effect from such acquisitions as if they had been owned durin g t hat entire year (or same period as the current reportable period), taking into account their respective pre - acquisition revenues for the applicable periods, and (iii) for dispositions, the revenue effect from such disposition as if they had been disposed of during the equivalent period in the prior year. Net New Business: Estimate of annualized revenue for new wins less annualized revenue for losses incurred in the period. Adjusted EBITDA: Adjusted EBITDA is a non - GAAP measure that represents operating profit (loss) plus depreciation and amortization, stock - based compensation, deferred acquisition consideration adjustments, distributions from non - consolidated affiliates, and other items. P rior to 2017, Adjusted EBITDA included an additional adjustment for acquisition deal costs. Beginning with 2017, on a prospective basis we no longer includ e t he acquisition deal cost adjustment but we continue to disclose this metric for your reference. Included in the Company’s earnings release and supplemental management presentation are tables reconciling MDC Partners’ repo rte d results to arrive at certain of these non - GAAP financial measures. We are unable to reconcile our projected 2017 organic revenue growth to the corresponding GAAP measure because we are unable to predict the 2017 impact of foreign exchange due to the unpredictability of future changes in foreign exchange r ate s and because we are unable to predict the occurrence or impact of any acquisitions, divestitures or other potential changes. We are unable to reconcile ou r p rojected 2017 increase in Adjusted EBITDA margin to the corresponding GAAP measure because the amount and timing of many future charges that impact these measur es (such as amortization of future acquired intangible assets, foreign exchange transaction gains or losses, impairment charges, and provision or benefit fo r income taxes) are variable, uncertain, or out of our control and therefore cannot be reasonably predicted without unreasonable effort, if at all. As a re sul t, we are unable to provide reconciliations of these measures. In addition, we believe such reconciliations could imply a degree of precision that might be confusing or misleading to investors. Note: A reconciliation of non - GAAP to US GAAP reported results has been provided by the Company in the tables included in the earnings release issued on October 30, 2017.

MDC Partners Innovation Center 745 Fifth Avenue, Floor 19 New York, NY 10151 646 - 429 - 1800 www.mdc - partners.com