UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F/A

Amendment No. 1

[ ] REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended November 30, 2010

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from: _________________ to ___________________

OR

[ ] SHELL COMPANY REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Date of event requiring this shell company report:Not Applicable

Commission file number:000-25489

Pure Nickel Inc.

(Exact name of Registrant as specified in its charter)

Canada

(Jurisdiction of incorporation or organization)

Suite 900 – 95 Wellington St. West, Toronto, Ontario Canada, M5J 2N7

(Address of principal executive offices)

Jeffrey D. Sherman, 416.644.0066, Chief Financial Officer, info@purenickel.com,

Suite 900 – 95Wellington St. West, Toronto, Ontario Canada, M5J 2N7

(Name, Telephone, E-mail and/ or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:None

Securities registered or to be registered pursuant to Section 12(g) of the Act:Common Shares, without par value

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:None

Number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:67,832,226

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes [ ] No [X]

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15 (d) of the Securities Exchange Act of 1934.

Yes [ ] No [X]

Note – Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15 (d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrants was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes [X] No [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act (Check one):

| Large accelerated filer [ ] | Accelerated filer [ ] | Non-accelerated filer [X] |

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP [ ] | International Financial Reporting Standards [ ] | Other [X] |

Indicate by check mark which financial statement item the registrant has elected to follow

Item 17 [X] Item 18 [ ]

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes [ ] No [X]

EXPLANATORY NOTE

This Amendment No. 1 to our Annual Report on Form 20-F for the year ended November 30, 2010, or Amendment No. 1, amends our Annual Report on Form 20-F for the year ended November 30, 2010 initially filed with the United States Securities and Exchange Commission, on February 17, 2011, or the Originally Filed 20-F. Amendment No. 1 is being filed for the sole purpose of including the Financial Statements referred to in Item 17, which were inadvertently not included in the Originally Filed 20-F.

Other than the foregoing items, no part of the Originally Filed 20-F is being amended. Amendment No. 1 does not reflect events occurring after the filing of the Originally Filed 20-F and does not modify or update the disclosures therein in any way other than as required to reflect the amendments described above.

1

TABLE OF CONTENTS

| SPECIAL INFORMATION | 3 | |

| NOTE REGARDING FORWARD-LOOKING STATEMENTS | 8 | |

| PART I | 9 | |

| ITEM 1. | Identity of Directors, Senior Management and Advisors | 9 |

| ITEM 2. | Offer Statistics and Expected Timetable | 9 |

| ITEM 3. | Key Information | 9 |

| ITEM 4. | Information on the Company | 17 |

| ITEM 4A. | Unresolved Staff Comments | 31 |

| ITEM 5. | Operating and Financial Review and Prospects | 32 |

| ITEM 6. | Directors, Senior Management and Employees | 37 |

| ITEM 7. | Major Shareholders and Related Party Transactions | 50 |

| ITEM 8. | Financial Information | 51 |

| ITEM 9. | Offer and Listing Details | 52 |

| ITEM 10. | Additional Information | 53 |

| ITEM 11. | Quantitative and Qualitative Disclosures about Market Risk | 61 |

| ITEM 12. | Description of Securities other than Equity Securities | 62 |

| PART II | 62 | |

| ITEM 13. | Defaults, Dividend Arrearages and Delinquencies | 62 |

| ITEM 14. | Material Modifications to the Rights of Securities Holders and Use of Proceeds | 62 |

| ITEM 15T. | Controls and Procedures | 62 |

| ITEM 16A. | Audit Committee Financial Expert | 63 |

| ITEM 16B. | Code of Ethics | 63 |

| ITEM 16C. | Principal Accountant Fees and Services | 64 |

| ITEM 16D. | Exemptions from the Listing Standards for Audit Committees | 64 |

| ITEM 16E. | Purchases of Equity Securities by the Issuer and Affiliated Purchasers | 64 |

| ITEM 16F. | Change in Registrant’s Certifying Accountant | 64 |

| ITEM 16G. | Corporate Governance | 64 |

| PART III | 64 | |

| ITEM 17. | Financial Statements | 64 |

| ITEM 18. | Financial Statements | 64 |

| ITEM 19. | Exhibits | 65 |

2

SPECIAL INFORMATION

Glossary of Technical Terms

AeroTEM | Helicopter-borne Time Domain Electromagnetic System: a helicopter-borne electromagnetic system used to identify potential deposits based upon conductive properties. |

BHEM | Bore Hole Electro Magnetic: an imaging system that involves placing a transmitter and receiver in a borehole, and the underlying geological structure is viewed by a process similar to medical tomographic imaging. This creates an image of the structure from a series of flat cross-sectional images. |

breccia | A rock in which angular fragments are surrounded by a mass of finer-grained material. |

chalcopyrite | A sulphide mineral of copper and iron; the most common ore mineral of copper. |

concentrate | A fine, powdery product of the milling process containing a high percentage of valuable metal. |

diamond drill(ing) | A rotary type of rock drill in which the cutting is done by abrasion rather than percussion. The cutting bit is set with diamonds and is attached to the end of long hollow rods through which water or other fluid is pumped to the cutting face as a lubricant. The drill cuts a core of rock that is recovered in long cylindrical sections, two centimeters or more in diameter. |

disseminated | Ore carrying small particles of valuable minerals spread more or less uniformly through the host rock. |

exploration stage | The search for mineral deposits which are not in either the development or production stage. |

fault | A break in the Earth’s crust caused by tectonic forces which have moved the rock on one side with respect to the other. Faults may extend many kilometers, or be only a few centimeters in length. Similarly, the movement or displacement along the fault may vary widely. |

fracture | A break in the rock, the opening of which affords the opportunity for entry of mineral-bearing solution. A ‘cross fracture’ is a minor break extending at more- or-less right angles to the direction of the principal fracture. |

form 43-101 | Technical report issued pursuant to Canadian security rules, the objective of which is to provide a summary of scientific and technical information concerning mineral exploration, development and production activities on a mineral property that is material to an issuer. The Form 43-101F1 is prepared in accordance with the National Instrument 43-101 Standards of Disclosure for Mineral Projects. The 43-101 form sets out specific requirements for the preparation and contents of a technical report. |

feasibility study | An economic study assessing whether a mineral deposit can be mined profitably, by estimating costs of a mine and the potential revenues from production. |

grade | The metal content of rock with precious metals. Grade can be expressed as troy ounces or grams per tonne of rock. |

hectare | A metric unit of area measurement equivalent to 10,000m² |

hydrothermal | Relating to hot fluids circulating in the earth’s crust. |

igneous | A type of rock which has been formed from magma, a molten substance from the earth’s core. |

intrusion | A body of igneous rock formed by the consolidation of magma intruded into other rocks, in contrast to lavas, which are extruded upon the surface. |

mafic | Igneous rock composed mostly of dark, iron and magnesium-rich minerals. |

metasedimentary | Originally sedimentary rocks which have been subsequently affected by the process of metamorphism |

metamorphic | A type of rock which, through heat and pressure, has been changed from igneous or sedimentary rock. |

3

mineral reserve | National Instrument 43-101Standards of Disclosure for Mineral Projectsof the Canadian Securities Administrators, adopting the definition of the Canadian Institute of Mining, Metallurgy and Petroleum (CIM), defines a ‘mineral reserve’ as the economically mineable part of a Measured or Indicated Mineral Resource demonstrated by at least a Preliminary Feasibility Study (a comprehensive study of the viability of a mineral project that has advanced to a stage where the mining method has been established and an effective method of mineral processing has been determined and includes a financial analysis based on reasonable assumptions of technical, engineering, legal, operating, economic, social, and environmental factors and the evaluation of other relevant factors which are sufficient for a Qualified Person (an individual who is an engineer or geoscientist with at least five years of experience in mineral exploration, mine development or operation or mineral project assessment, or any combination of these; has experience relevant to the subject matter of the mineral project and the technical report; and is a member or licensee in good standing of a professional association), acting reasonably, to determine if all or part of the Mineral Resource may be classified as a Mineral Reserve). This study must include adequate information on mining, processing, metallurgical, economic and other relevant factors that demonstrate, at the time of reporting, that economic extraction can be justified. A Mineral Reserve includes diluting materials and allowances for losses that may occur when the material is mined. Mineral Reserves are sub-divided in order of increasing confidence into Probable Mineral Reserves and Proven Mineral Reserves. A Probable Mineral Reserve has a lower level of confidence than a Proven Mineral Reserve. (1)Probable Mineral Reserve.A ‘Probable Mineral Reserve’ is the economically mineable part of an Indicated, and in some circumstances a Measured Mineral Resource demonstrated by at least a Preliminary Feasibility Study. This study must include adequate information on mining, processing, metallurgical, economic, and other relevant factors that demonstrate, at the time of reporting, that economic extraction can be justified. (2)Proven Mineral Reserve.A ‘Proven Mineral Reserve’ is the economically mineable part of a Measured Mineral Resource demonstrated by at least a Preliminary Feasibility Study. This study must include adequate information on mining, processing, metallurgical, economic, and other relevant factors that demonstrate, at the time of reporting, that economic extraction is justified. |

4

mineral resource | National Instrument 43-101Standards of Disclosure for Mineral Projectsof the Canadian Securities Administrators, adopting the definition of the Canadian Institute of Mining, Metallurgy and Petroleum (CIM), defines a ‘Mineral Resource’ as a concentration or occurrence of diamonds, natural solid inorganic material, or natural solid fossilized organic material including base and precious metals, coal and industrial minerals in or on the Earth’s crust in such form and quantity and of such a grade or quality that it has reasonable prospects for economic extraction. The location, quantity, grade, geological characteristics and continuity of a Mineral Resource are known, estimated or interpreted from specific geological evidence and knowledge. Mineral Resources are sub-divided, in order of increasing geological confidence, into Inferred, Indicated and Measured categories. An Inferred Mineral Resource has a lower level of confidence than that applied to an Indicated Mineral Resource. An Indicated Mineral Resource has a higher level of confidence than an Inferred Mineral Resource but has a lower level of confidence than a Measured Mineral Resource. (1)Inferred Mineral Resource.An ‘Inferred Mineral Resource’ is that part of a Mineral Resource for which quantity and grade or quality can be estimated on the basis of geological evidence and limited sampling and reasonably assumed, but not verified, geological and grade continuity. The estimate is based on limited information and sampling gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes. (2)Indicated Mineral Resource.An ‘Indicated Mineral Resource’ is that part of a Mineral Resource for which quantity, grade or quality, densities, shape and physical characteristics can be estimated with a level of confidence sufficient to allow the appropriate application of technical and economic parameters, to support mine planning and evaluation of the economic viability of the deposit. The estimate is based on detailed and reliable exploration and testing information gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes that are spaced closely enough for geological and grade continuity to be reasonably assumed. (3)Measured Mineral Resource.A ‘Measured Mineral Resource’ is that part of a Mineral Resource for which quantity, grade or quality, densities, shape, physical characteristics are so well established that they can be estimated with confidence sufficient to allow the appropriate application of technical and economic parameters, to support production planning and evaluation of the economic viability of the deposit. The estimate is based on detailed and reliable exploration, sampling and testing information gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes that are spaced closely enough to confirm both geological and grade continuity. |

Net Smelter Royalty (NSR) | A Net Smelter Returns Royalty has been generically described as follows: “A royalty calculated on the net smelter return is essentially calculated on the amount received by the mine or mill owner from the sale of the mineral product to the treatment plant that converts the output of the mill to marketable metal. From the gross proceeds received there may be deductions for costs incurred by the owner after the product leaves the mine property and before sale, such as the costs of: transportation, insurance or security, penalties, sampling and assaying, refining and smelting, and marketing. No deductions are made for the operating costs of the mine-mill complex.” (B.J. Barton,Canadian Law of Mining (Calgary: Institute of Resources Law, 1993) at 461.) |

ore | A mixture of minerals and host rock from which at least one metal can be extracted at a profit. |

open pit | A mining method whereby the mineral reserves are accessed from surface by the successive removal of layers of material usually creating a large pit at the surface of the earth. |

patent | The ultimate stage of holding a mineral claim, after which no more assessment work is necessary because all mineral rights have been earned. |

5

pegmatite | A coarse-grained, igneous rock, generally coarse, but irregular in texture, and similar to granite in composition; usually occurs in dykes or veins and sometimes contains valuable minerals. |

pentlandite | Nickel iron sulphide, the most common nickel ore. |

petrology | A field of geology which focuses on the study of rocks and the conditions by which they form. There are three branches of petrology, corresponding to the three types of rocks: igneous, metamorphic, and sedimentary. |

PGE | Platinum Group Elements include platinum, palladium, rhodium, iridium, osmium, and ruthenium. They commonly occur together in nature and are among the most scarce of the metallic elements. |

pre-feasibility study | A comprehensive study of the viability of mineral project that has advanced to a stage where the mining methods, in the case of underground mining, or the pit configurations, in the case of an open pit, has been established, where effective methods of mineral processing have been determined, and includes a financial analysis based on reasonable assumptions of technical, engineering, legal, operating, and economic factors and evaluation of other relevant factors which are sufficient or a Qualified Person acting reasonably, to determine if all or part of the Mineral Resources may be classified as a Mineral Reserve. |

probable reserve | Valuable mineralization not sampled enough to be termed “proven”. |

prospect | (noun) The possibility of future success for economic minerals based on geological, geophysical, geochemical and other criteria. or (verb) To search for or explore (a region) for mineral deposits or oil. |

production stage | All companies engaged in the exploitation of a mineral deposit (reserve). |

qualified person | An individual who is an engineer or geoscientist with at least five years experience in mineral exploration, mine development or operation or mineral project assessment, or any combination of these; has experience relevant to the subject matter of the mineral project and the Technical Report; and is a member or licensee in good standing of a professional association. |

reserve | A known resource that can be exploited for profit with available technology under existing political and economic conditions. |

royalty | An amount of money paid at regular intervals, or based on production, by the lessee or operator of an exploration or mining property to the current or former owner of the mineral interests. Generally based on a certain amount per unit weight or a percentage of the total production, revenues or profits. A ‘net smelter royalty’ is a type of royalty based on a percentage of the proceeds, net of smelting, refining and transportation cost and penalties, from the sale of the metals extracted from products by the smelter or refinery. |

sedimentary | A type of rock which has been created by the deposition of solids from a liquid. |

serpentine | A greenish, metamorphic mineral consisting of magnesium silicate. |

shear | The deformation of rocks by lateral movement along innumerable parallel planes, generally resulting from pressure and producing such metamorphic structures as cleavage and schistosity. |

strike | The direction, or bearing, from true north of a vein or rock formation measured on a horizontal surface. |

sulphide | A compound of sulphur and some other element; most base-metal ore minerals are sulphides. |

tonne | Metric ton, equal to 2,205 pounds. |

ultramafic | A term used to describe igneous rock or magmas that are rich in iron and magnesium and very poor in silica. |

vein | A tabular body of rock typically of narrow thickness and mineralized occupying a fault, shear, fissure or fracture crosscutting another pre-existing rock. |

VTEM | The VTEM (Versatile Time-Domain Electromagnetic) survey is the leading airborne geophysical system in use today and is particularly suited to the identification of copper-zinc massive sulphide deposits. |

6

Metric Conversion Table

The following table sets forth certain factors for converting metric measurements into imperial equivalents. To convert from metric to imperial units, divide the metric unit by its corresponding value in the middle column. To convert from imperial to metric units, multiply the imperial unit by its corresponding value in the middle column.

Metric Units | Conversion Factor | Imperial Units |

Description and abbreviation |

| Description and abbreviations |

Length |

| Length |

Millimeters – mm | 25.400 | Inches – in |

Meters – m | 0.3048 | Feet – ft |

Meters – m | 0.9144 | Yards – yd |

Kilometers – km | 1.609 | Miles – mile |

Area |

| Area |

Square centimeters - cm² | 6.4516 | Square inches - in² |

Square meters - m² | 0.0929 | Square feet - ft² |

Hectares - ha | 0.40469 | Acres – acre |

Square Kilometers - km² | 2.5900 | Square miles – sq miles |

Weight |

| Weight |

Tonne (1,000 kg) - t | 0.907185 | Short ton (2,000 lbs) - st |

Currency

Unless otherwise indicated, all references in this Annual Report to “dollars” or “$” are to Canadian dollars.

Other Information

Pure Nickel Inc. (formerly “Nevada Star Resource Corp.”) was incorporated under the laws of British Columbia, Canada, on April 29, 1987, and was continued under theCanada Business Corporations Act on April 7, 2009. In this document, the terms “we,” “our,” “us,” and “the Company” refer to Pure Nickel Inc. and its subsidiaries. Our consolidated financial statements are prepared in accordance with Canadian generally accepted accounting principles (“Canadian GAAP”), are reconciled to the United States generally accepted accounting principles (“GAAP” or “U.S. GAAP”), and are presented in Canadian dollars except where indicated in conversions of convenience. We file reports and other information with the Securities and Exchange Commission (“SEC”) located at 100 F Street, N.E., Washington, D.C. 20549.

Copies of our filings with the SEC may be obtained by accessing the SEC’s website located atwww.sec.gov. Further, we also file reports under Canadian regulatory requirements on the System for Electronic Document Analysis and Retrieval, which is a filing system that provides access to most public securities documents and information filed by public companies and investment funds with the Canadian Securities Administrators (“SEDAR”). Copies of our reports filed on SEDAR can be obtained by accessing SEDAR’s website atwww.sedar.com.

Our principal executive office is located at Suite 900 – 95 Wellington St. West, Toronto, Ontario Canada, M5J 2N7, Telephone: 416.644.0066, Fax: 416.644.0069, email addressinfo@purenickel.comand websitehttp://www.purenickel.com. Unless explicitly referred to herein, the information contained on our internet site is not incorporated by reference in this report and it should not be considered part of this report.

Except as noted, the information set forth in this Annual Report is as of November 30, 2010, and all information included in this document should only be considered accurate as of that date. Our business, financial condition or results of operations may have changed since that date.

7

NOTE REGARDING FORWARD-LOOKING STATEMENTS

This document and the documents incorporated by reference herein contain forward-looking statements. In addition to this Annual Report on Form 20-F, our management may make forward-looking statements orally or in writing to investors, analysts, the media and others. Forward-looking statements express our expectations or beliefs regarding future events or results. They are not guarantees and are subject to many risks and uncertainties. There are a number of factors that could cause actual events or results to be significantly different from those described in the forward-looking statements. Our forward-looking statements may include, but are not limited to, the following:

requirements for additional capital and anticipated financing activities;

anticipated strategic alliances or arrangements with partners;

projected development, production and exploration timelines;

results of production and exploration activities;

the estimation or realization of mineral reserves and resources;

forecasts of the prices of minerals relevant to our exploration effort and general economic performance;

forecasts of ore grade or recovery rates;

discussions regarding the failure rates of plant, equipment or processes to operate as anticipated;

labor relations;

timing regarding governmental approvals and permits;

descriptions of plans or objectives of management for future operations;

the timing and amount of capital expenditures, costs and timing of the development of new deposits; and

descriptions or assumptions underlying or relating to any of the above items.

Forward-looking statements can be identified by the fact that they do not relate strictly to historical or current facts or events. They use words such as “anticipate,” “estimate,” “expect,” “project,” “intend,” “opportunity,” “plan,” “potential,” “believe,” or words of similar meaning. They may also use words such as “will,” “would,” “should,” “could,” or “may.”

Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. Moreover, we do not assume responsibility for the accuracy and completeness of such statements. We intend that the forward-looking statements contained herein will be covered by the safe harbor provisions for forward-looking statements contained in Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). We do not intend to update any of the forward-looking statements after the date of this report to conform such statements to actual results except as required by law. Given these uncertainties, you should not place undue reliance on these forward-looking statements, which speak only as of the date of this report. You should carefully consider all available information about us before you make an investment decision. You should review carefully the risks and uncertainties identified in this Annual Report on Form 20-F.

8

PART 1

| ITEM 1. Identity of Directors, Senior Management and Advisors |

Not applicable. This Form 20-F is being filed as an Annual Report under the Exchange Act.

| ITEM 2. Offer Statistics and Expected Timetable |

Not applicable. This Form 20-F is being filed as an Annual Report under the Exchange Act.

| ITEM 3. Key Information |

Selected Financial Data

Following is selected financial data expressed in Canadian dollars for the fiscal years ended November 30, 2010, 2009, 2008 and 2007 and for the period from May 18, 2006 to November 30, 2006 (the date of the acquisition discussed below), which were prepared in accordance with Canadian GAAP, which differs substantially from United States generally accepted accounting principles (“GAAP” or “U.S. GAAP”). Reference is made to Note 20 to the audited financial statements for the years ended November 30, 2010 and 2009 and Note 19 to the audited financial statements for the years ended November 30, 2009 and 2008 in “Item 17.Financial Statements” for a description of the differences between Canadian GAAP and U.S. GAAP.

The selected financial data was derived from financial statements that were audited by SF Partnership LLP as indicated in the reports included elsewhere in this Annual Report. This selected financial data should be read in conjunction with the financial statements and other financial information include elsewhere in this Annual Report.

We completed the acquisition of (old) Pure Nickel Inc., a private company incorporated on May 18, 2006, on March 30, 2007. From a Canadian legal and accounting perspective, the transaction was deemed to be a reverse takeover. Our financial statements reflect the combined results of (old) Pure Nickel Inc. and Nevada Star Resource for the fiscal years ended November 30, 2010, 2009, 2008 and 2007 and the period from incorporation on May 18, 2006 to November 30, 2006.

The selected financial data is set out below.

| 12 months | 12 months | 12 months | 12 months | May 18, | |||||||||||

| ended | ended | ended | ended | 2006 to | |||||||||||

| Nov. 30, | Nov. 30, | Nov. 30, | Nov. 30, | Nov. 30, | ||||||||||

| 2010 | 2009 | 2008 | 2007 | 2006 | ||||||||||

| $ | $ | $ | $ | $ | ||||||||||

Revenues | Nil | Nil | Nil | Nil | Nil | ||||||||||

Operating expenses | 1,481,601 | 1,269,173 | 1,972,406 | 4,946,798 | 103,441 | ||||||||||

Loss from operations | (1,481,601 | ) | (1,269,173 | ) | (1,972,406 | ) | (4,946,798 | ) | (103,441 | ) | |||||

Other expenses, net | (827,165 | ) | (142,015 | ) | (459,634 | ) | (2,778,777 | ) | (35,082 | ) | |||||

Net loss | (2,308,766 | ) | (1,411,188 | ) | (2,432,040 | ) | (7,725,575 | ) | (138,523 | ) | |||||

Total assets | 42,899,214 | 44,773,605 | 46,210,759 | 48,410,479 | 2,945,022 | ||||||||||

Shareholders’ equity | 42,460,757 | 44,448,587 | 45,754,932 | 47,933,403 | 2,945,022 | ||||||||||

Outstanding common shares | 67,832,226 | 67,765,559 | 67,765,559 | 67,765,559 | 24,100,001 | ||||||||||

Dividends per common share | Nil | Nil | Nil | Nil | Nil | ||||||||||

Net income (loss) per share, fully diluted | (0.03 | ) | (0.02 | ) | (0.04 | ) | (0.18 | ) | (0.02 | ) |

9

Under Canadian GAAP, the Company capitalizes all costs related to the acquisition, exploration and development of non-producing mineral properties. Under U.S. GAAP, acquisition costs of mineral rights are capitalized, but exploration and development costs are expensed as incurred, until the establishment of commercially mineable reserves is complete, at which time any further exploration costs are capitalized. Under Canadian GAAP, enterprises in the development stage are encouraged to disclose cumulative information from the inception of the development stage. Under U.S. GAAP, this disclosure is required. Cumulative net losses since inception aggregate $14,016,092. The differences in accounting for mineral properties under Canadian and U.S. GAAP had the following effects on the Company’s financial statements.

(i) Net Loss and Loss per Share

| 12 months | 12 months | 12 months | ||||||

| ended | ended | ended | ||||||

| Nov. 30, | Nov. 30, | Nov. 30, | ||||||

| 2010 | 2009 | 2008 | ||||||

| $ | $ | $ | ||||||

Net loss under Canadian GAAP | (2,308,766 | ) | (1,411,188 | ) | (2,432,040 | ) | |||

Capitalized expenditures on unproven mineral properties | 785,160 | (635,126 | ) | (3,581,188 | ) | ||||

Net loss under U.S. GAAP | (1,523,606 | ) | (2,046,314 | ) | (6,013,228 | ) | |||

Loss per share under U.S. GAAP – basic and diluted | (0.02 | ) | (0.03 | ) | (0.09 | ) |

(ii) Mineral Properties

| Nov. 30, | Nov. 30, | Nov. 30, | ||||||

| 2010 | 2009 | 2008 | ||||||

| $ | $ | $ | ||||||

Mineral properties under Canadian GAAP | 38,555,291 | 39,071,469 | 38,365,557 | ||||||

Capitalized expenditures on unproven mineral properties | (18,801,891 | ) | (19,587,051 | ) | (18,951,925 | ) | |||

Reclassification to investment in joint venture | (69,024 | ) | − | − | |||||

Mineral properties under U.S. GAAP | 19,684,376 | 19,484,418 | 19,413,632 |

(iii) Investment in Joint Venture

| Nov. 30, | Nov. 30, | Nov. 30, | |||||||

| 2010 | 2009 | 2008 | ||||||

| $ | $ | $ | ||||||

Investment in joint venture under Canadian GAAP | − | − | − | ||||||

Reclassification from mineral properties | 69,024 | − | − | ||||||

Investment in joint venture under U.S. GAAP | 69,024 | − | − |

(iv) Deficit

| Nov. 30, | Nov. 30, | Nov. 30, | ||||||

| 2010 | 2009 | 2008 | ||||||

| $ | $ | $ | ||||||

Deficit under Canadian GAAP | (14,016,092 | ) | (11,707,326 | ) | (10,296,138 | ) | |||

Capitalized expenditures on unproven mineral properties | (18,801,891 | ) | (19,587,051 | ) | (18,951,925 | ) | |||

Deficit under U.S. GAAP | (32,817,983 | ) | (31,294,377 | ) | (29,248,063 | ) |

10

For Canadian GAAP, cash flows relating to mineral property exploration are reported as investing activities. For U.S. GAAP, these costs would be characterized as operating activities.

Since June 1, 1970, the Government of Canada has permitted a floating exchange rate to determine the value of the Canadian dollar as compared to the U.S. dollar. On February 11, 2011, the exchange rate in effect for Canadian dollars exchanged for U.S. dollars, expressed in terms of Canadian dollars, was $0.9903. This exchange rate is based on the average noon buying rates of the Bank of Canada, as obtained from the websitewww.bankofcanada.ca.

For the fiscal years ended November 30, 2010, 2009 and 2008 and for the six month period between August 1, 2010, and January 31, 2011, the following exchange rates were in effect for Canadian dollars exchanged for U.S. dollars, calculated in the same manner as above:

| Period | Average | ||

| Period from May 16, 2006 to November 30, 2006 | $ | 1.1228 | |

| Year ended November 30, 2007 | $ | 1.0867 | |

| Year ended November 30, 2008 | $ | 1.0478 | |

| Year ended November 30, 2009 | $ | 1.1565 | |

| Year ended November 30, 2010 | $ | 1.0340 |

The following table sets forth the high and low exchange rate for the six month period between August 1, 2010 and January 31, 2011:

| U.S. Dollar/Canadian Dollar Exchange Rates | ||||||

| Month | High | Low | ||||

| August 2010 | 1.0674 | 1.0108 | ||||

| September 2010 | 1.0604 | 1.0216 | ||||

| October 2010 | 1.0374 | 0.9986 | ||||

| November 2010 | 1.0286 | 0.9980 | ||||

| December 2010 | 1.0216 | 0.9931 | ||||

| January 2011 | 1.0060 | 0.9848 | ||||

B. Capitalization and Indebtedness

Not applicable. This Form 20-F is being filed as an Annual Report under the Exchange Act.

C. Reasons for the Offer and Use of Proceeds

Not applicable. This Form 20-F is being filed as an Annual Report under the Exchange Act.

D. Risk Factors

Any investment in our common shares involves a high degree of risk. In addition to the other information presented in this Annual Report, you should consider the following risk factors carefully in evaluating the Company, its business and the mineral exploration and mining industry. If any of these risks or uncertainties occurs, our business, financial condition or operating results could be materially harmed. In that case the trading price of our common stock could decline and you could lose all or part of your investment. The risks and uncertainties described below are not the only ones we may face. For further information you are encouraged to review our filings with the SEC on EDGAR, as well as those appearing on the Canadian site SEDAR atwww.sedar.com.

11

We have a limited operating history and as a result there is no assurance we can operate profitably or with a positive cash flow.

We have a limited operating history and are an exploration stage company. Our operations are subject to all the risks inherent in the establishment of an exploration stage enterprise and the uncertainties arising from the absence of a significant operating history. Investors should be aware of the difficulties normally encountered by mineral exploration companies and the high rate of failure of such enterprises. The likelihood of success must be considered in light of the problems, expenses, difficulties, complications and delays encountered in connection with the exploration of the mineral properties that the Corporation plans to undertake. These potential problems include, but are not limited to, unanticipated problems relating to exploration, and additional costs and expenses that may exceed current estimates. The amounts disbursed by us in the exploration of the mineral claims may not result in the discovery of mineral deposits. Problems such as unusual or unexpected formations of rock or land and other conditions are involved in mineral exploration and often result in unsuccessful exploration efforts. If the results of future exploration programs do not reveal viable commercial mineralization, we may decide to abandon our claims, and in fact have abandoned some already.

If we do not obtain additional financing, our business will fail and investors could lose their investment.

We had cash and equivalents of $1,799,715 and working capital was $3,843,307 at November 30, 2010. We do not currently generate revenues or cash flows from operations (except for interest income and payments that are credited to mineral resources on the balance sheet rather than being identified as revenues in our statement of operations). Our business plan calls for substantial investment and costs in connection with the exploration of our mineral properties. In order to maintain certain of our property claims, we must incur certain minimum exploration expenditures on an ongoing basis. There can be no assurance that we will have the funds required to make such expenditures or that those expenditures will result in positive cash flow. There are no arrangements in place for additional financing and there is no assurance that we will be able to find such financing on acceptable terms, or at all, if required.

We are an exploration company with an accumulated deficit of $14,016,092 as at November 30, 2010. With ongoing cash requirements for exploration, development and new operating activities, it will be necessary to raise substantial funds from external sources. If we do not raise these funds, we will be unable to pursue our business activities, and our investors could lose all of their investment. If we are able to raise funds, investors could experience a dilution of their interests that would negatively affect the market value of the shares.

There are no known reserves of minerals on our mineral claims and there is no assurance that we will find any commercial quantities of minerals.

We have not found any mineral reserves on our claims and there can be no assurance that any of the mineral claims under exploration contain commercial quantities of any minerals. Even if commercial quantities of minerals are identified, there can be no assurance that we will be able to exploit the reserves or, if we are able to exploit them, that it will be profitable. Substantial expenditures will be required to locate and establish mineral reserves, to develop metallurgical processes and to construct mining and processing facilities at a particular site, and substantial additional financing may be required. It is impossible to ensure that the exploration or development programs planned by us will result in a profitable commercial mining operation. The decision as to whether a particular property contains a commercial mineral deposit and should be brought into production will depend on the results of exploration programs and/or feasibility studies, and the recommendations of duly qualified engineers and geologists. Several significant factors will be considered, including, but not limited to: (i) the particular attributes of the deposit, such as size, grade and proximity to infrastructure; (ii) metal prices, which are highly volatile; (iii) government regulations, including regulations relating to prices, taxes, royalties, land tenure, land use, importing and exporting of minerals and environmental protection; (iv) ongoing costs of production; and (v) availability and cost of additional funding. The effect of these factors cannot be accurately predicted, but the combination of these factors may result in us receiving no return or an inadequate return on invested capital.

Because of the speculative nature of the exploration of natural resource properties, there is substantial risk that our business will fail.

While the discovery of a commercially viable ore body may result in substantial rewards, few mineral properties which are explored are ultimately developed into producing mines. There is no assurance that any of the claims that we will explore or acquire will contain commercially exploitable reserves of minerals. Exploration for natural resources is a speculative venture involving substantial risk. Even a combination of careful evaluation, experience and knowledge may not eliminate such risk. Hazards such as unusual or unexpected geological formations, formation pressures, fires, power outages, labour disruptions, flooding, cave-ins, landslides, and the inability of us to obtain suitable machinery, equipment or labour are all risks involved with the conduct of exploration programs and the operation of mines.

12

Development and exploration activities depend, to one degree or another, on adequate infrastructure. Reliable roads, bridges, power sources and water supply are important determinants, which affect capital and operating costs. Unusual or infrequent weather phenomena, sabotage, government or other interference in the maintenance or provision of such infrastructure could adversely affect our operations, financial condition and results of operations.

Because there is no assurance that we will generate revenues, we face a high risk of business failure.

We have not earned any revenues to date and have never had positive cash flow. Before being able to generate revenues, we will incur substantial operating and exploration expenditures without receiving any revenues. Therefore we expect to incur significant losses into the foreseeable future. If we are unable to generate significant revenues from our activities, we will not be able to earn profits or continue operations. Based upon current plans, we expect to incur significant operating losses in the future. We cannot guarantee that we will be successful in raising capital to fund these operating losses or generate revenues in the future. There is no assurance that we will ever generate any operating revenues or ever achieve profitable operations. If we are unsuccessful in addressing these risks, our business may fail and our investors could lose some or all of their investment.

The current credit and financial market conditions may exacerbate certain risks affecting our business.Increased concerns about credit markets, consumer confidence, economic conditions, volatile corporate profits and reduced capital spending could negatively impact us. The recent tightening of credit in financial markets may adversely affect the ability of our business partners to obtain financing, which could result in a decrease in, or deferrals or cancellations of, their payment obligations to fund our exploratory activities. If global economic and market conditions, or economic conditions in the United States or Canada, remain uncertain or persist, we may experience a material adverse effect on our business and financial condition. Unstable economic, political and social conditions may make it difficult for our partners to accurately forecast and plan future business activities. If such conditions persist, our business and financial condition could suffer.

The failure of any banking institution in which we deposit our funds or the failure of such banking institution to provide services in the current economic environment could have a material adverse effect on our results of operations or financial condition.

The capital and credit markets have been experiencing volatility and disruption. In some cases, the markets have exerted downward pressure on stock prices and credit capacity for certain issuers, as well as pressured the solvency of some financial institutions. Some of these financial institutions, including banks, have had difficulty performing regular services and in some cases have failed or otherwise been largely taken over by governments. If we are unable to access some or all of our cash on deposit, either temporarily or permanently, it could have a negative impact on our operations or our financial position, or both.

We are subject to uninsurable risks, which could reduce or eliminate any future profitability.

In the course of exploration, development and production of mineral properties, risks including but not limited to unexpected or unusual geological or operating conditions, may occur. It is not always possible to insure against such risks, and we may decide not to take out insurance against such risks as a result of high premiums or other reasons. Should such liabilities arise they could reduce or eliminate any future profitability and result in an increase in costs and a decline in value of our shares. We are not insured against environmental risks. Insurance against environmental risks (including potential liability for pollution or other hazards as a result of the disposal of waste products occurring from exploration and production) has not been generally available to companies within our industry. Therefore, if we were to become subject to environmental liabilities, the payment of such liabilities would reduce or eliminate our available funds or could exceed our funds and result in business failure and possibly bankruptcy.

We are subject to market factors and volatility of commodity prices beyond our control.

The marketability of mineralized material that we may acquire or discover will be affected by many factors beyond our control. These factors include market fluctuations in the prices of minerals sought which are highly volatile, the proximity and capacity of natural resource markets and processing equipment, and government regulations, including regulations relating to prices, taxes, royalties, land tenure, land use, importing and exporting of minerals and environmental protection. The effect of these factors cannot be predicted, but may result in receiving a very low or negative return on invested capital. Prices of certain minerals have fluctuated widely, particularly in recent years, and are affected by numerous factors beyond our control. Future mineral prices cannot be accurately predicted. A severe decline in the price of a mineral being produced or expected to be produced by us would have a material adverse effect on us, and could result in the suspension of our exploration programs or mining operations.

13

Our stock price is volatile.

Market prices of securities of many public companies have experienced significant fluctuations in price that have not been related to the operating performance, underlying asset values or prospects of such companies. The market price of our common shares has been and is likely to remain volatile. Results of exploration activities, the price of nickel, future operating results, changes in estimates of our performance by securities analysts, market conditions for natural resource companies in general, and other factors beyond our control could cause a significant decline of the market price of our common shares.

If we do not make certain payments or fulfill other contractual obligations, we may lose our option rights and interests in our joint ventures.

We may, in the future, be unable to meet our share of costs incurred under option or joint venture agreements to which we are a party and we may have our interest in the properties subject to such agreements reduced as a result. Furthermore, if other parties to such agreements do not meet their share of such costs, we may be unable to finance the cost required to complete exploration programs. The loss of any option rights or interest in joint ventures would have a material, adverse effect on us.

We may not have good title to our mining claims, potentially impairing our value.

Our mineral property interests may be subject to prior unregistered agreements of transfers or native land claims, and title may be affected by undetected defects. There can be no assurance that we will be able to obtain good title without unreasonable expense in the event we are faced with defects of title for any of our mineral projects.

If key employees or consultants leave the company, we will be harmed since we are heavily dependent upon them for all aspects of our activities.

We are dependent upon key employees and contractors, the loss of any of whom could have a negative impact on our ability to operate the business and could cause a decline in the value of, or cash flows from, our properties or additional costs resulting from a delay in development or exploration of properties.

If we do not comply with all applicable regulations, we may be forced to halt our business activities and/or incur significant expense.

We are subject to government and environmental regulations. Permits from a variety of regulatory authorities are required for many aspects of exploration, mining operations and reclamation. We cannot predict the extent to which future legislation and regulation could cause additional expense, capital expenditures, restrictions, and delays in the development of our Canadian and/or U.S. properties, including those with respect to unpatented mining claims.

Failure to comply with applicable environmental laws, regulations and permitting requirements may result in enforcement actions including orders issued by regulatory or judicial authorities that may result in operations ceasing or being curtailed; and may include corrective measures requiring capital expenditures, installation of additional equipment, or other expensive and/or time-consuming remedial actions. Parties engaged in the exploration or development of exploration properties may be required to compensate those suffering loss or damage by reason of such parties’ activities and may have civil or criminal fines or penalties imposed for violations of applicable laws or regulations.

Our activities are not only subject to extensive federal, provincial, state and local regulations controlling the exploration and mining of mineral properties, but also the possible effects of such activities upon the environment as well as costs, cancellations and delays resulting from lobbying activities of environmental groups. Future legislation and regulations could cause additional disbursements, capital expenditures, restrictions and delays in the development of our properties, the extent of which cannot be predicted. Also, as noted above, permits from a variety of regulatory authorities are required for many aspects of mine operation and reclamation. In the context of environmental permitting, including the approval of reclamation plans, we must comply with known standards, existing laws and regulations that may entail greater or lesser costs and delays, depending on the nature of the activity to be permitted and how stringently the regulations are implemented by the permitting authority. If we become more active on our properties, compliance with environmental regulations may increase our costs. Such compliance may include feasibility studies on the surface impact of proposed operations; costs associated with minimizing surface impact, water treatment and protection, reclamation activities including rehabilitation of sites, ongoing efforts at alleviating the mining impact on wildlife, and permits or bonds as may be required to ensure our compliance with applicable regulations. The costs and delays associated with such compliance may result in us deciding not to proceed with exploration, development or mining operations on any mineral properties.

14

Exercise of outstanding warrants, options, and other future issuances of securities will result in dilution of our common shares.

As of November 30, 2010, there were 67,832,226 common shares issued and outstanding as well as options, as set out in Note 8 – Share Capital in our attached financial statements. The holders of the options are given an opportunity to profit from a rise in the market price of the common shares with a resulting dilution in the interest of the other shareholders. Our ability to obtain additional financing during the period such rights are outstanding may be adversely affected and the existence of the rights may have an adverse effect on the price of the common shares. The holders of options may exercise such securities at a time when we would otherwise be able to obtain any needed capital by a new offering of securities on terms more favourable than those provided by those outstanding rights. Any increase in the number of common shares issued and outstanding as a result of the exercise of options or from the sales of such shares may depress the market price of our common shares and will dilute the proportionate interests and votes of existing shareholders.

Proposed legislation affecting the mining industry could have an adverse effect on us.

During the past several years, the United States Congress considered a number of proposed amendments to the General Mining Law of 1872, which governs mining claims and related activities on federal lands. In 1992, a federal holding fee of $100 per claim was imposed upon unpatented mining claims located on federal lands. This fee was increased to $125 per claim in 2005 ($133.50 total with the accompanying County fees included). Beginning in October 1994, a moratorium on processing of new patent applications was approved. In addition, a variety of legislation over the years has been proposed by the United States Congress to further amend the General Mining Law. There has not been material progress on any of these proposed reformations as of the date of this report. For example, the U.S. House of Representatives considered H.R. 699, the Hardrock Mining and Reclamation Act of 2009, which did not pass. That proposal would have placed a royalty on hardrock mining on federal lands, permitted state of local governments or Indian tribes to petition for withdrawal of lands from the operation of the mining laws, and expanded the ability of the Secretary of the Interior to limit mining on federal lands. The extent of any future congressional action is difficult to predict. If enacted, the legislation could adversely affect the economics of developing and operating mines because many of our properties consist of unpatented mining claims on federal lands. Our financial performance could therefore be materially and adversely affected by passage of legislation, which could force us to curtail or cease our business operations in the United States.

Directors and management may be subject to conflicts of interest.

Certain directors and officers are directors and/or officers of other mineral exploration companies and as such may have a conflict of interest requiring them to abstain from certain decisions. Conflicts of interest that arise will be subject to and governed by procedures prescribed by our governing corporate law statute which requires a director of a corporation who is a party to, or is a director or an officer of, or has some material interest in any person who is a party to, a material contract or proposed material contract with the Company to disclose his or her interest and, in the case of directors, to refrain from voting on any matter in respect of such contract unless otherwise permitted under such legislation.

Wemay be adversely affected by exchange rate fluctuations.

Exchange rate fluctuations between the Canadian dollar and the United States dollar may adversely affect our financial position and results. United States-based shareholders need to consider the risk of an investment that reports its results in Canadian funds. Our results are reported in Canadian dollars, but since we operate in the United States, some of our financial instruments and transactions are denominated in United States funds. Fluctuation in the exchange rates between the United States dollar and the Canadian dollar could have a material effect on our business, financial condition and results of operations. At November 30, 2010, we had net monetary assets denominated in United States funds of $586,671 (US$571,470). Based upon the year-end balance, an increase of 15% in the Canada to U.S. dollar exchange would result in an increase in the net loss and comprehensive loss of $88,000, and a reduction of 15% would result in a reduction in the net loss and comprehensive loss of $107,000. We believe that it is possible that the exchange rate could fluctuate by more than 15% within the next 12 months.

15

The trading market for our shares is not always liquid.

Although our shares trade on the Toronto Stock Exchange and the Over the Counter Bulletin Board, the volume of shares traded at any one time can be limited, and, as a result, there may not be a liquid trading market for our shares.

Our stock is a “penny stock” which imposes significant restrictions on broker-dealers recommending the stock for purchase.

SEC regulations define “penny stock” to include common stock that has a market price of less than $5.00 per share, subject to certain exceptions. These regulations include the following requirements: broker-dealers must deliver, prior to the transaction, a disclosure schedule prepared by the SEC relating to the penny stock market; broker-dealers must disclose the commissions payable to the broker-dealer and its registered representative; broker-dealers must disclose current quotations for the securities; if a broker-dealer is the sole market-maker, the broker-dealer must disclose this fact and the broker-dealers presumed control over the market; and a broker-dealer must furnish its customers with monthly statements disclosing recent price information for all penny stocks held in the customer’s account and information on the limited market in penny stocks. Additional sales practice requirements are imposed on broker-dealers who sell penny stocks to persons other than established customers and accredited investors. For these types of transactions, the broker-dealer must make a special suitability determination for the purchaser and must have received the purchaser’s written consent to the transaction prior to sale. While our shares are subject to these penny stock rules these disclosure requirements may have the effect of reducing the level of trading activity. Accordingly, this may result in a lack of liquidity in the shares and investors may be unable to sell their shares at prices considered reasonable by them.

As a foreign private issuer, our shareholders may have less complete and timely data than they would with a typical U.S. public company.

The submission of proxy and annual meeting of shareholder information (prepared to Canadian standards) in Form 6-K may result in shareholders having less complete and timely information in connection with shareholder actions. The exemption from Section 16 of the Exchange Act and the rules promulgated thereunder regarding reports of beneficial ownership and purchases and sales of common shares by insiders and restrictions on insider trading in our securities may result in shareholders having less data and there being fewer restrictions on insiders’ activities in our securities.

We do not plan to pay any dividends in the foreseeable future.

We have never paid a dividend and it is unlikely that we will declare or pay a dividend unless and until warranted based on the factors outlined below. The declaration, amount and date of distribution of any dividends in the future will be decided by the board of directors, based upon, and subject to, our earnings, financial requirements and other conditions prevailing at the time. Investors cannot expect to receive a dividend on their investment in the foreseeable future, or at all.

United States stockholders may be subject to unexpected or unwanted tax consequences as a result of acquiring, holding, or disposing of our shares.

As discussed in detail below under “Item 10.E (iv). United States Federal Income Tax Considerations,” the tax implications of an investment in us are difficult to determine, can be different for different individuals and entities, and generally require that an investor consult his or her investment and taxation professionals. Under certain circumstances, the acquisition, holding or disposition of our shares may generate unwanted tax consequences for a holder or investor in our shares.

16

Our management may not be subject to United States legal process making it more difficult for U.S. investors to sue them.

Investors may have a difficult time enforcing civil judgements against us because all of our officers and most of our directors are neither citizens nor residents of the United States. U.S. shareholders may not be able to effect service of process within the United States upon such persons. U.S. shareholders may not be able to enforce, in United States courts, judgments against such persons obtained in such courts predicated upon the civil liability provisions of United States federal or state securities laws. Appropriate courts outside the United States may not be able to enforce judgments of United States courts obtained in actions against such persons predicated upon the civil liability provisions of the federal securities laws. The appropriate courts outside the United States may not be able to enforce, in original actions, liabilities against such persons predicated solely upon the United States federal securities laws. However, U.S. laws would generally be enforced by a Canadian court provided that those laws are not contrary to Canadian public policy, are not foreign penal laws or laws that deal with taxation or the taking of property by a foreign government and provided that they are in compliance with applicable Canadian legislation regarding the limitation of actions. As we are incorporated pursuant to the laws of Canada, duties of our directors and officers, and the ability of shareholders to initiate a lawsuit on our behalf, are governed by the

Canada Business Corporations Act.

| ITEM 4. Information on the Company |

A. History and Development of the Company

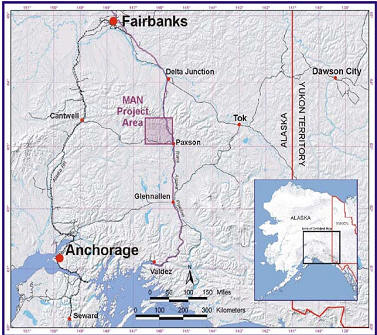

We are principally engaged in the acquisition, development, and operation of mineral properties and exploration for, in particular, nickel, PGEs, copper, gold, silver and associated base and precious metals. At present, operations are located in Canada and the United States. Operations in Canada are conducted through the parent corporation, Pure Nickel Inc. Operations in the United States are carried out through our wholly-owned subsidiary Nevada Star Resource Corp. (U.S.) (a Nevada corporation). We also seek joint venture or option agreements where appropriate to enhance shareholder value, on certain of our mineral properties and the surrounding areas. Our MAN Alaska property is held through MAN Alaska LLC, a Delaware limited liability company, in which we have a 70% interest.

We were incorporated under the laws of British Columbia, Canada, on April 29, 1987, and were continued under theCanada Business Corporations Act on April 7, 2009. We prepare our financial statements in Canadian dollars and in accordance with Canadian GAAP. Unless otherwise indicated herein, all dollar amounts in this Annual Report are stated in Canadian dollars.

The address and telephone number of our principal executive office and information on the Company generally can be found above under “Special Information: Other Information.” The registered agent in the United States for our United States subsidiaries is CT Wolters Kluwer, 111 Eighth Avenue, New York, NY 10011.

On March 30, 2007, we (then known as Nevada Star Resource Corp., (“Nevada Star”), completed the acquisition of all of the shares of (old) Pure Nickel Inc. (“old PNi”), a private company incorporated on May 18, 2006. From a Canadian legal and accounting perspective, the transaction was deemed to be a reverse takeover. Old PNi, the new subsidiary of Nevada Star, was deemed to be the acquirer and its financial statements are the basis of the continuing financial statements of Nevada Star, which simultaneously changed its name to Pure Nickel Inc. As a result, our financial statements reflect the combined results of old PNi and Nevada Star for the period from May 18, 2006 to November 30, 2006, and the fiscal years ended November 30, 2007, 2008, 2009 and 2010.

At the same time as the reverse takeover, we consolidated our common shares on a one-for-five basis, and they continued to be traded on the Toronto Stock Exchange Venture Exchange (TSX-V) and in the United States on the Over the Counter Bulletin Board. Our share listings have now graduated to the senior Canadian exchange, and since August 14, 2007 have been listed on the Toronto Stock Exchange.

During the second quarter of 2007, we completed a financing of $9,000,000 by the sale of 10,000,000 units for $0.90 each. Each unit consisted of one common share and one-half of one warrant. Each whole warrant is exercisable into one common share at $1.20 for a term of 18 months. The agent for this financing received a cash commission of 7% of the gross proceeds and advisory warrants equal to 5% of the gross number of securities sold in the offering. Each advisory warrant was exercisable into one common share at $0.90 each for a period of 18 months. These warrants have since expired.

17

During the third quarter, 2007, we completed a financing of $27,500,000 by the sale of 22,000,000 units for $1.25 each. This financing contained a U.S. private placement portion, which was conducted pursuant to the rules promulgated under Section 4(2) of the Securities Act of 1933, as amended. Each unit consisted of one common share and one half of one warrant, each whole warrant being exercisable for a period of 18 months into a common share of the Company for $1.75 per share. These warrants have since expired.

Prior to February 2007, we had three properties in different stages of exploration: (i) the MAN Property located in Alaska, United States; (ii) the Salt Chuck Alaska PGE Property located in Alaska, United States; and (iii) the Milford Utah Copper Property located in Beaver County, Utah. Prior to February 2007, old PNi had two exploration properties: (i) Fond du Lac, located in Saskatchewan, Canada and (ii) Fox River, located in Manitoba, Canada. The Fond du Lac property was originally under option from Red Dragon Resources Corp. and, on May 8, 2007, we acquired 100% interest in the property from Red Dragon Resources Corp. for $100,000 and the issuance of 1,000,000 shares of our common stock. On November 6, 2007, we announced we had elected not to renew the option for the Fox River property.

On May 15, 2007, we completed a major acquisition comprising the purchase of the Xstrata property portfolio for $15,250,000 in cash and the issuance of 4,000,000 warrants to purchase common shares with an exercise price of $2.00 per share for a period of three years from the issuance of the warrants. These warrants have since expired. Properties included in the acquisition were:

- William Lake and Manibridge in Manitoba;

- POV, Nuvilik, SR1, HPM, East Hudson (joint venture with Soquem Inc.) and Forgues in Quebec;

- Harp Lake and Florence Lake in Newfoundland; and

- Rainbow in Nunavut.

In addition, Xstrata was granted:

- a net smelter royalty of 2% on each property with us having the right to reacquire 1% by payment of $1,000,000 with respect to a particular property at any time up to twelve months after commercial production has been achieved on that property;

- off-take and marketing rights for all concentrate or product produced from the properties; and

- the right to retain one back-in right to 50% for any one (only) of any mining project with an economic threshold of 15,000,000 tons of resources.

On September 18, 2007, we entered into an option agreement with Exploration Syndicate Inc., a private company, for the option to earn up to 100% interest in 160,000 hectares of prospective property in central Manitoba. In March 2008, we drilled two conductors identified from a November VTEM airborne survey. Drill success was limited and in June 2008 we announced our intent to end the option agreement.

On November 6, 2007, we granted an option to Manicouagan Minerals Inc. under which they may earn up to a 70% interest in 39 mining claims comprising the Forgues and HPM project in Québec. In November 2009 Manicouagan Minerals had made the required option payments and exploration expenditures to earn a 50% interest in the property. Manicouagan has elected not to exercise its option to earn an additional 20% in the property; a formal 50-50 joint venture agreement is currently in process. As referenced above, on November 6, 2007, we announced that we would not renew our option for the Fox River project in Manitoba. We also announced that we had allowed our claims on the Florence Lake project in Newfoundland and Labrador to lapse.

On November 15, 2007, we announced a 50/50 joint venture agreement with Crowflight Minerals Ltd. (“Crowflight”) to explore the past producing Manibridge Mine area. Each party contributed properties and mineral rights to the joint venture and made an initial contribution of $3 million over a three year period to fund preliminary exploration activities within the joint venture area and to perform further detailed technical studies as necessary to evaluate the potential for development and mining on the properties. Crowflight is the operator of the joint venture. In addition, we have an option to earn a 50% interest from Crowflight in an area surrounding the joint venture area by spending an additional $1.5 million over a three year period. Properties contributed by us to the joint venture contain the claims and tailings disposal area of the past producing Manibridge Mine and are subject to rights held by Xstrata pursuant to an exploration property purchase agreement entered into between Xstrata and the Company on August 2, 2007. Specifically, Xstrata will, among other things (i) retain an off-take option to purchase all or any portion of concentrates and other mineral products produced from the affected properties; and (ii) be entitled to a 2% net smelter return (NSR) royalty with respect to the our claims.

18

On November 20, 2007, we filed on SEDAR, and furnished on a 6-K through EDGAR, an Independent Technical Report on our 100% owned William Lake property in the Thompson Nickel Belt, Manitoba. We commissioned the NI 43-101 report from Scott Wilson Roscoe Postle Associates Inc. to summarize previous work, and in particular the exploration activity undertaken by Xstrata through its predecessor company, Falconbridge Limited. The technical report highlighted the significant nickel mineralization outlined by 13 years of previous exploration activity that commenced in 1989. This technical report conforms to NI 43-101 Standards of Disclosure for Mineral Projects and its recommendations form the basis for our future exploration programs to develop a resource estimate.

On December 19, 2007, Jay Jaski, our CEO and Chairman, unexpectedly passed away. David McPherson was appointed interim President and CEO and Robert Angrisano was appointed as interim Chairman of the Board. On April 3, 2008 these appointments were confirmed by the Board on a non-interim basis.

On February 21, 2008, we announced that we had entered into an option agreement with Rockcliff Resources Inc. whereby Rockcliff may earn up to a 70% interest in the Tower VMS property. This property is comprised of 35 mining claims located at the north end of our William Lake Property. The agreement requires Rockcliff to drill 2,000 meters in the first year as well as the granting to us of warrants to purchase 1,250,000 shares of Rockcliff at $1.50 per share with a term of 2 years. These warrants expired in February 2010. In February 2010, this agreement was amended to extend the time for performance of work on the Tower Property and as consideration, Rockcliff granted us 1,250,000 common share purchase warrants exercisable at $1.50 per share with a term of two years.

On May 15, 2008, we relinquished our rights to the East Hudson properties in Quebec.

On June 5, 2008, we granted Minergy Ltd., a private company, an option to earn up to 70% interest in 393 mining claims comprising the Nuvilik and POV properties located in the Raglan district in Quebec.

On October 31, 2008, we granted ITOCHU Corporation, a Japanese conglomerate, an option to earn up to a 75% interest in the MAN, Alaska property. Pursuant to the agreement, ITOCHU reimbursed us for expenditures incurred in 2008 and funded exploration activity for 2009 at MAN to a combined maximum of USD$6.5 million for 2008 and 2009. Under the agreement, exploration activity may be funded through 2014 to a total of $40 million subject to ITOCHU exercising its option to continue at the end of 2009 and 2013. Under the terms of the agreement at that time, ITOCHU could earn a 60% interest in MAN by incurring an aggregate of $30 million of exploration expenditures over the first six years of the option period. Once ITOCHU had earned a 60% interest, it had the option to earn-in an additional 15% interest in the MAN property by incurring an additional $10 million of exploration expenditures during the seventh year of the agreement. The agreement provided for the acceleration of the earn-in timetable, and we earn a 10% management fee and remain as operator.

In May 2009, we were informed by the Quebec Ministry of Natural Resources that the 148 claims that comprise the POV property were no longer open for exploration work. The claims fell within a boundary for a proposed provincial park and certain exploration milestones needed to be reached in order to extend the development of the park. Pure Nickel and its option partner Minergy Ltd. were aware of the proposed park since the property came to the company through the Xstrata property purchase in August 2007 and we relinquished the claims in May 2009.

19

In June 2009, we filed an action for declaratory relief against Western Utah Copper Company (WUCC) in the United States District Court, Utah requesting for interpretation of and the status and rights under an agreement regarding certain royalties we are entitled to receive from production at WUCC property.

On July 20, 2009, WUCC filed an answer and counterclaim, and on August 31, 2009 we filed a response to the counterclaim. We believe that the counterclaim is without merit.

On November 18, 2009 our Option partner Manicouagan Minerals made the required option payment and exploration expenditures to earn a 50% interest in the HPM/Forgues property.

On March 5, 2010 we extended the time for our option partner, Rockcliff Resources Inc. to perform the exploration work required under the agreement with us for our Tower property. In consideration for extending the time, Rockcliff granted us 1,250,000 common share purchase warrants exercisable at $1.50 per share and an expiry of the earlier of February 21, 2013 or two years after Rockcliff is able to commence exploration of the Tower property,

On March 23, 2010 we announced that we did not renew the Harp Lake, Labrador claims. The decision was based on the low potential of the Harp Lake property in relation to our other property claims.

On March 25, 2010 ITOCHU Corporation, our partner on the MAN Alaska property, vested its interest in the property. ITOCHU had expended the required funds on exploration to vest a 20% interest however in consideration of increasing the 2010 exploration budget and compressing the time period for the second tranche of the option earn-in, we granted ITOCHU the right to vest a 30% interest in 2010. A new company was created called MAN Alaska LLC to hold the MAN property claims. MAN Alaska LLC is jointly owned (70% by our subsidiary Nevada Star Resource Corp (U.S) and 30% by ITC Mineral Resources Development (U.S.A) Inc, a wholly owned subsidiary of ITOCHU Corporation.

On April 30, 2010, R. David Russell was appointed Chair of the Board.

In May 2010 we expanded our Rainbow, Nunavut property by 19 claims which amounts to an eight fold increase of contiguous holdings, bringing the Rainbow property to 19,850 hectares.

On May 18, 2010, Western Utah Copper Company (WUCC) and its parent Copper King Mining Corporation filed voluntary petitions for reorganization under Chapter 11 of the United States Bankruptcy Code. On August 27, 2010 WUCC filed an action in bankruptcy court in Utah, U.S.A, against Nevada Star Resource Corp and Pure Nickel. This action is very similar to the counterclaims made in response to the original lawsuit in 2009. We believe that this new action is without merit.

On July 7, 2010, we announced that our option agreement with Minergy Ltd. on the Nuvilik property in Quebec was terminated.

In November 2010, we decided not to renew the mining claims on the SR1 portion of the Raglan, Quebec property.

B. Business Overview

General

We are in the business of acquiring, exploring and developing mineral properties, primarily those containing nickel, platinum group elements, copper, gold, silver and associated base and precious metals. We have a practice of taking grassroots or undeveloped properties with the expectation of developing them to a level where an ore body is indicated or likely. If an ore body is indicated or likely, then we have a policy of looking to develop a joint venture or purchase option with a larger mining company to further develop the property and, if justified, to take the property into production. In all cases, we retain a percentage of ownership. In the case of a partnership, we receive a percentage of royalty from the production of product resulting from a mining operation. The market prices for minerals have been and will likely continue to be very volatile.

20