UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-06373

Sit Mutual Funds, Inc.

(Exact name of registrant as specified in charter)

80 South Eighth Street

3300 IDS Center

Minneapolis, MN 55402

(Address of principal executive offices)

Paul E. Rasmussen, VP Treasurer

Sit Mutual Funds, Inc.

80 South Eighth Street

3300 IDS Center

Minneapolis, MN 55402

(Name and address of agent for service)

Registrant’s telephone number, including area code: (612) 332-3223

Date of fiscal year end: June 30, 2023

Date of reporting period: December 31, 2023

| Item 1: | Reports to Stockholders |

Semi-Annual Report

December 31, 2023

|

Balanced Fund

Dividend Growth Fund

Global Dividend Growth Fund

Large Cap Growth Fund

ESG Growth Fund

Mid Cap Growth Fund

Small Cap Dividend Growth Fund

Small Cap Growth Fund

International Growth Fund

Developing Markets Growth Fund

Sit Mutual Funds

Sit Mutual Funds

Sit Mutual Funds STOCK FUNDS SEMI-ANNUAL REPORT

|

| Page | ||||

| 2 | ||||

Fund Review and Schedules of Investments | ||||

| 4 | ||||

| 10 | ||||

| 14 | ||||

| 18 | ||||

| 22 | ||||

| 26 | ||||

| 30 | ||||

| 34 | ||||

| 40 | ||||

| 46 | ||||

| 50 | ||||

| 52 | ||||

| 54 | ||||

| 58 | ||||

| 72 | ||||

| 79 | ||||

| 81 | ||||

This document must be preceded or accompanied by a Prospectus.

February 5, 2024

Dear Fellow Shareholders:

2023 was a solid year for global equities, as investors looked forward to the end of the Federal Reserve tightening cycle amidst a resilient U.S. economy. After a year of spectacular returns for technology stocks, highlighted by the “Magnificent Seven,” we expect a broadening of participation in equity gains in 2024.

Economic Summary

The U.S. economy enters 2024 on a solid footing. Supply chains have largely normalized; labor markets are becoming less tight; inflation continues to recede; and consumer spending remains resilient. Not only did the economy avert a widely-predicted recession in 2023, but it also grew faster than it did in the previous year – at least in real GDP terms. The Atlanta Fed’s GDPNow model projects fourth quarter 2023 real GDP growth of +2.3%, bringing full-year growth to +2.5% year over year versus +1.9% in 2022. The more dire predictions for 2023 failed to materialize due to some fortuitous developments. A continued recovery in immigration helped the labor force grow by 2.8 million (putting it 1.4 million above its historical trend), thus halting a wage-price spiral. The regional banking crisis also did not broaden into a credit crunch. In addition, atypical pro-cyclical fiscal stimulus boosted GDP, and consumers did not skip a beat by tapping excess savings and credit to sustain spending. However, the surging personal debt, at very high interest rates, could soon become a headwind rather than a tailwind. Also, some of these 2023 tailwinds will dissipate in the year ahead, just as the full effects of restrictive monetary policy set in, resulting in softer growth in 2024. But how soft?

Admittedly, soft and hard landings typically follow similar paths until the lagged effects of monetary tightening hit the labor market (which responds slowly to policy changes). Further, in addition to the different time lags, the actual size and scope of the response to monetary policy varies widely. Also, while many leading indicators have continued to signal an imminent recession, the historical lag between the first rate hike (or even the yield curve inversion) put a recession in play through 2025. The bottom line is the economy is not out of the woods yet, following the most aggressive monetary tightening cycle in decades, and is especially vulnerable to a shock. Yet, there are undeniable positives. The recent uptick in productivity is encouraging and remains the critical factor driving real GDP growth potential, while keeping a lid on inflation. Plus, higher-end consumers still have excess cash to spend; private credit is filling the gaps left by weakening bank loan growth; inventory destocking is less of a drag; and the outlook for single-family housing is improving.

The Federal Reserve surprised financial markets in December by pivoting from a hawkish hold to a dovish bias. The “dot plot” now signals three 25-basis point fed funds rate cuts in 2024 based on

a median PCE inflation forecast of +2.4% at year end. Monetary policymakers seem comforted by the recent pace of disinflation. However, we should be mindful that even if the Fed stays put on rates, monetary policy will become incrementally more restrictive on a real basis as inflation continues to ebb. Which is not to mention the added tightening tied to the Fed’s ongoing balance sheet reduction. Naturally, investors, previously braced for “higher-for-longer” rates, swung eagerly on the Fed’s dovish (or less hawkish) pivot and are currently interpreting three cuts as six, with the first coming in midyear. The easier (market-driven) financial conditions that have followed could lift economic growth, but therein lies the rub. Higher demand might also cause inflation pressures to reemerge, putting the Fed back on the offensive and making a soft landing less likely.

Overseas economies are generally struggling, particularly the Euro Area, which is teetering on the brink of a technical recession, after bouncing along the bottom over the last four quarters. Given the slump in economic growth, the European Central Bank (ECB) likely pushed through its final rate hike last September. While growth is likely to remain tepid, at best, improving real disposable incomes, excess savings, and resilient labor markets should support consumer spending, keeping a recession relatively shallow if one occurs at all. In China, we anticipate the post-pandemic decelerating trend to continue into 2024. Consumption, a key growth driver, will moderate as the reopening effects fade, and investment growth will likely remain stable or slightly improve, partially reflecting policy support. We also expect growth to slow in Japan after a relatively solid year in 2023, as the services recovery that sustained growth since early 2022 has run its course. An inflation-burdened consumer and embattled manufacturing sector may not sufficiently take up the baton.

Equity Strategy

Global stocks posted exceptionally strong returns in 2023, aided by a broad-based rally in the final two months of the year. Still-high economic uncertainty, elevated policy/geopolitical risks, and “fair” equity valuations support our quality bias amidst a better environment for stock pickers in 2024.

Investors piled into U.S. stocks in the final two months of 2023, with about $96 billion flowing into U.S. equity mutual funds and ETFs in November and December. According to the American Association of Individual Investors (AAII) Investor Sentiment Survey, retail investor sentiment also swung from “panic” in early November to “euphoria” by mid-December, although the AAII survey often is used as a contrarian indicator. As for institutional investors, the NAAIM Exposure Index shows that active portfolio managers progressively increased risk exposure in November and December, before paring back in the year’s final week. Overbought technical

| 2 | SIT MUTUAL FUNDS SEMI-ANNUAL REPORT | |

conditions and elevated sentiment imply stocks are susceptible to profit-taking or at least a pause in the near term, as investors digest recent gains. Looking further out, we expect the U.S. presidential election will undoubtedly add to already-elevated economic, policy, and geopolitical uncertainty. On average, the S&P 500® Index has historically moved sideways in the first half of a presidential election year but rallied in the second to deliver a +6.9% annual return. But the 2024 election promises to be anything but average.

The spectacular performance of the “Magnificent Seven” (M7) stocks (i.e., Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla) dominated headlines over the past year, and we suspect those companies will continue to garner a lot of investor attention in the year ahead. While valuations for the M7 stocks have moved well above market averages, it is important to note that earnings growth has been a key basis for investor enthusiasm, as the group grew earnings by over +40% year over year, on average. In contrast, overall S&P 500® earnings decelerated to low-single-digit growth in 2023. Yet, we believe that elevated valuations and more difficult earnings comparisons for the M7 stocks relative to the rest of the market may set the stage for broader equity gains in 2024. We generally maintain positions in the most attractive M7 stocks but also see compelling opportunities in other technology segments, including semiconductors, software/services, and cybersecurity. In addition to technology, we expect early cycle and rate-sensitive sectors to fare well in the year ahead. Transportation companies, for example, have been struggling with excess customer inventories and cost pressures, but pricing has remained solid, and the freight backdrop is set to rebound in 2024. Sentiment is also broadly improving for financial stocks. Given pent-up demand for initial public offerings, debt issuance, and M&A, we see the most attractive opportunities for a strong rebound in capital markets businesses. We are emphasizing segments such as property and casualty companies and broad financial services.

Due to several factors, dividend-paying stocks produced their weakest relative returns in years, especially against the AI-driven rally that pushed the M7 and other non-dividend-paying tech stocks much higher in 2023. Looking ahead, we see an emerging backdrop that has historically led to solid relative performance for high-quality dividend-paying growth stocks. Key elements of our forecast include modest economic growth, lower interest rates (including fed funds rate cuts), and the likelihood of an increase in market volatility from the exceptionally low levels at present. In addition to the groups noted above, we see attractive growth and income opportunities in diverse areas, such as energy, P&C insurance, drug distributors, and select pharmaceutical companies. The sharp rise in interest rates in 2023 provided stiff competition for dividend payers from bonds, particularly for slower growth “bond proxies,” including utilities,

consumer staples, and REITs. While we prefer “growthier” stocks, these low-beta sectors are cheap insurance against market volatility or a severe recession and offer modest earnings growth, well-above-average dividend yields, and attractive valuations.

For international portfolios, we generally remain cautious on Europe, as tepid economic growth will constrain company earnings growth, although there are select opportunities in industrials, health care, and technology. In emerging markets, we are positive on South Korea, Singapore, India, Australia, Mexico, and Brazil. Chinese equities derated in 2023 owing to disappointing economic growth and rising geopolitical tensions. Although Chinese stocks currently trade at highly depressed valuations, we remain highly selective until there is more clarity on economic growth catalysts, which may take some time. Overall, we believe emerging market stocks are attractively valued, with the MSCI Emerging Market Index trading at the low end of its historical range relative to the MSCI USA Index. Still, underlying corporate earnings prospects are highly variable, making country emphasis and stock selection critical in the year ahead.

| Roger J. Sit |

| Chairman, President, CEO and Global CIO |

| DECEMBER 31, 2023 | 3 | |

OBJECTIVE & STRATEGY

The dual objectives of the Sit Balanced Fund are to seek long-term growth of capital consistent with the preservation of principal and to provide regular income. It pursues its objectives by investing in a diversified portfolio of stocks and bonds. The Fund may emphasize either equity securities or fixed-income securities, or hold equal amounts of each, dependent upon the Adviser’s analysis of market, financial and economic conditions.

The Fund’s permissible investment allocation is: 35-65% in equity securities and 35-65% in fixed-income securities. At all times at least 25% of the fixed-income assets will be invested in fixed-income senior securities.

Fund Performance

The Sit Balanced Fund’s return for the 6-month period ended December 31, 2023 was +8.39%. The S&P 500® Index return was +8.04% over the period, while the Bloomberg Aggregate Bond Index increased +3.37%.

Factors that Influenced the Fund’s Performance

For the 6-month period ended December 31, 2023, returns for the fixed income portion of the Fund outperformed the Bloomberg Aggregate Bond Index. The fixed income portfolio primarily benefitted from its income advantage during the period, while price increases in the bond holdings also outpaced the price return of the index. Corporate bonds were the best performing sector during the period, as declining inflation and strong economic growth pushed recession fears lower and drove strong returns from credit-sensitive sectors. Mortgage pass-through securities struggled during the period despite their income advantage, as their lower overall interest rate sensitivity resulted in mortgage securities not keeping up with other sectors as bond prices rose. The outperformance in the equity portion of the Fund during the period was driven heavily by strong stock selection in the technology services and electronic technology sectors, combined with an underweight position in the lagging consumer durables sector. Key holdings included Broad-com, Intuit, Salesforce, and Lululemon Athletic. Conversely, an underweight position in the finance sector and negative stock selection in the consumer non-durables sector detracted from performance.

Outlook and Positioning

The yield curve twisted during the 6-month period. Interest rates on securities inside of six months to maturity increased, in conjunction with the last increase to the federal funds target rate in July, while 10+ year maturity interest rates rose modestly. This was in stark contrast to a drop in interest rates for intermediate maturity bonds, as the apparent end to the Federal Reserve’s rate hiking cycle resulted in a shift in sentiment. Looking ahead, investors now believe that the rapidly declining inflation picture means the next likely change in the fed funds rate will be a cut rather than another hike. We believe the large gap between the current rate target of 5.25% to 5.50% and core inflation of closer to 2.5% gives the Fed ample room to eventually cut rates, while remaining restrictive to keep inflation subdued. We now expect the Fed may successfully engineer a short, shallow recession or a “soft landing,” characterized by continued economic growth and inflation within 0.5% of their 2% target. As such, we have maintained an overweight to spread-sensitive sectors, which should outperform in a growing economy. We expect banks, in particular, to outperform, as the yield curve reverts to its normal upward-sloping shape. Overall, for 2024, we expect the fixed income

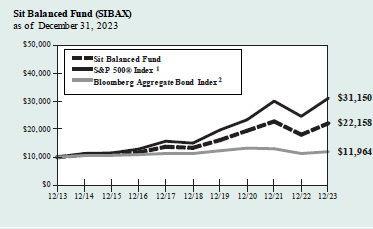

HYPOTHETICAL GROWTH OF $10,000

The chart above illustrates the total value of a hypothetical $10,000 investment in the Fund over the past 10 years as compared to the performance of the S&P 500® Index and the Bloomberg Aggregate Bond Index. Past performance does not guarantee future results. Returns include the reinvestment of distributions. The chart does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

1 S&P 500® Index is an unmanaged capitalization-weighted index that measures the performance of 500 widely held common stocks of large-cap companies. It is not possible to invest directly in an index. This is the primary index for the equity portion of the Fund.

2 Bloomberg Aggregate Bond Index is an unmanaged market value weighted index which measures the performance of investment grade debt securities with maturities of at least one year. It is not possible to invest directly in an index. This is the primary index for the fixed income portion of the Fund.

portion of the portfolio’s yield advantage to drive outperformance, regardless of the change in the level of interest rates or the shape of the yield curve. In the equity portion of the Fund, we have maintained a large overweight position in technology companies that should benefit from secular trends, such as artificial intelligence, cloud spending, and Big Data. Additionally, we are looking to selectively grow our exposure to early-stage cyclicals, such as producer manufacturing, which should benefit more than the market as economic growth improves during 2024.

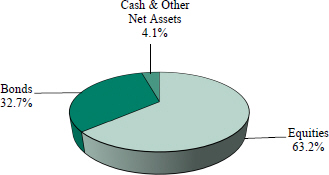

As of December 31, 2023, the asset allocation of the Fund was 63.2% equity, 32.7% fixed income, and 4.1% cash and equivalents.

Roger J. Sit

Bryce A.

Doty Ronald D. Sit

Portfolio Managers

| 4 | SIT MUTUAL FUNDS SEMI-ANNUAL REPORT | |

|

COMPARATIVE RATES OF RETURNS

as of December 31, 2023

| Sit Balanced Fund | | S&P 500® Index1 |

| | Bloomberg Aggregate Bond Index2 |

| ||||||

Six Month | 8.39% | 8.04 | % | 3.37 | % | |||||||

One Year | 22.64 | 26.29 | 5.53 | |||||||||

Five Year | 10.63 | 15.69 | 1.10 | |||||||||

Ten Year | 8.28 | 12.03 | 1.81 | |||||||||

Since Inception (12/31/93) | 7.37 | 10.14 | 4.41 | |||||||||

Performance figures are historical and do not guarantee future results. Investment returns and principal value will vary, and you may have a gain or loss when you sell shares. Current performance may be lower or higher than the performance data quoted. Contact the Fund for performance data current to the most recent month-end. Returns include changes in share price as well as reinvestment of all dividends and capital gains. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Management fees and administrative expenses are included in the Fund’s performance. Returns for periods greater than one year are compounded average annual rates of return.

1 S&P 500® Index is an unmanaged capitalization-weighted index that measures the performance of 500 widely held common stocks of large-cap companies. It is not possible to invest directly in an index.

2 Bloomberg Aggregate Bond Index is an unmanaged market value weighted index which measures the performance of investment grade debt securities with maturities of at least one year.

PORTFOLIO SUMMARY

Net Asset Value 12/31/23: | $30.83 Per Share | |

Net Asset Value 6/30/23: | $28.76 Per Share | |

Net Assets: | $55.9 Million | |

TOP HOLDINGS

Top Equity Holdings:

1. Microsoft Corp.

2. Apple, Inc.

3. Alphabet, Inc.

4. NVIDIA Corp.

5. Broadcom, Inc.

Top Fixed Income Holdings:

1. U.S. Treasury Notes, 4.50%, 11/15/33

2. Federal National Mortgage Association, 6.00%, 10/1/53

3. Federal National Mortgage Association, 4.50%, 9/1/52

4. Federal National Mortgage Association, 4.50%, 7/1/52

5. JP Morgan Mortgage Trust, 5.00%, 7/25/52

Based on net assets as of December 31, 2023.

FUND DIVERSIFICATION

Based on net assets as of December 31, 2023.

| DECEMBER 31, 2023 | 5 | |

SCHEDULE OF INVESTMENTS (Unaudited)

December 31, 2023

Sit Balanced Fund

Investments are grouped by economic sectors.

| Name of Issuer | Quantity | Fair Value ($) | ||||||

Common Stocks - 63.2% | ||||||||

Consumer Durables - 0.3% | ||||||||

YETI Holdings, Inc. * | 3,500 | 181,230 | ||||||

|

| |||||||

Consumer Non-Durables - 2.2% | ||||||||

Constellation Brands, Inc. | 2,750 | 664,813 | ||||||

Mondelez International, Inc. | 3,400 | 246,262 | ||||||

PepsiCo, Inc. | 1,825 | 309,958 | ||||||

|

| |||||||

| 1,221,033 | ||||||||

|

| |||||||

Consumer Services - 2.1% | ||||||||

McDonald’s Corp. | 1,450 | 429,939 | ||||||

Visa, Inc. | 2,800 | 728,980 | ||||||

|

| |||||||

| 1,158,919 | ||||||||

|

| |||||||

Electronic Technology - 13.4% | ||||||||

Apple, Inc. | 13,700 | 2,637,661 | ||||||

Applied Materials, Inc. | 2,600 | 421,382 | ||||||

Arista Networks, Inc. * | 765 | 180,165 | ||||||

Broadcom, Inc. | 1,485 | 1,657,631 | ||||||

NVIDIA Corp. | 4,025 | 1,993,260 | ||||||

Palo Alto Networks, Inc. * | 1,835 | 541,105 | ||||||

|

| |||||||

| 7,431,204 | ||||||||

|

| |||||||

Energy Minerals - 1.5% | ||||||||

ConocoPhillips | 5,775 | 670,304 | ||||||

Shell, PLC, ADR | 2,400 | 157,920 | ||||||

|

| |||||||

| 828,224 | ||||||||

|

| |||||||

Finance - 3.4% | ||||||||

Ameriprise Financial, Inc. | 1,150 | 436,805 | ||||||

Chubb, Ltd. | 1,400 | 316,400 | ||||||

Goldman Sachs Group, Inc. | 1,600 | 617,232 | ||||||

JPMorgan Chase & Co. | 2,925 | 497,542 | ||||||

|

| |||||||

| 1,867,979 | ||||||||

|

| |||||||

Health Services - 3.0% | ||||||||

Centene Corp. * | 2,475 | 183,670 | ||||||

HCA Healthcare, Inc. | 850 | 230,078 | ||||||

UnitedHealth Group, Inc. | 2,450 | 1,289,851 | ||||||

|

| |||||||

| 1,703,599 | ||||||||

|

| |||||||

Health Technology - 4.0% | ||||||||

Abbott Laboratories | 3,550 | 390,749 | ||||||

Dexcom, Inc. * | 5,260 | 652,713 | ||||||

Gilead Sciences, Inc. | 3,925 | 317,964 | ||||||

Johnson & Johnson | 1,250 | 195,925 | ||||||

Thermo Fisher Scientific, Inc. | 1,200 | 636,948 | ||||||

|

| |||||||

| 2,194,299 | ||||||||

|

| |||||||

Industrial Services - 0.8% | ||||||||

Cheniere Energy, Inc. | 2,750 | 469,453 | ||||||

|

| |||||||

Process Industries - 1.5% | ||||||||

Linde, PLC | 1,225 | 503,120 | ||||||

Sherwin-Williams Co. | 1,000 | 311,900 | ||||||

|

| |||||||

| 815,020 | ||||||||

|

| |||||||

Producer Manufacturing - 5.2% | ||||||||

Aptiv, PLC * | 2,375 | 213,085 | ||||||

General Dynamics Corp. | 700 | 181,769 | ||||||

Honeywell International, Inc. | 1,450 | 304,079 | ||||||

Motorola Solutions, Inc. | 1,400 | 438,326 | ||||||

| Name of Issuer | Quantity | Fair Value ($) | ||||||

Northrop Grumman Corp. | 375 | 175,552 | ||||||

Parker-Hannifin Corp. | 1,350 | 621,945 | ||||||

Safran SA, ADR | 11,550 | 509,701 | ||||||

Siemens AG, ADR | 5,175 | 484,069 | ||||||

|

| |||||||

| 2,928,526 | ||||||||

|

| |||||||

Retail Trade - 6.5% | ||||||||

Amazon.com, Inc. * | 9,700 | 1,473,818 | ||||||

Home Depot, Inc. | 1,825 | 632,454 | ||||||

Lululemon Athletica, Inc. * | 885 | 452,492 | ||||||

Netflix, Inc. * | 460 | 223,965 | ||||||

TJX Cos., Inc. | 5,100 | 478,431 | ||||||

Ulta Beauty, Inc. * | 795 | 389,542 | ||||||

|

| |||||||

| 3,650,702 | ||||||||

|

| |||||||

Technology Services - 17.2% | ||||||||

Accenture, PLC | 2,025 | 710,593 | ||||||

Adobe, Inc. * | 810 | 483,246 | ||||||

Alphabet, Inc. - Class A * | 12,400 | 1,732,156 | ||||||

Alphabet, Inc. - Class C * | 4,100 | 577,813 | ||||||

Atlassian Corp. * | 1,050 | 249,753 | ||||||

Autodesk, Inc. * | 1,275 | 310,437 | ||||||

Dynatrace, Inc. * | 4,250 | 232,433 | ||||||

Intuit, Inc. | 1,200 | 750,036 | ||||||

Meta Platforms, Inc. * | 635 | 224,765 | ||||||

Microsoft Corp. | 7,800 | 2,933,112 | ||||||

Paycom Software, Inc. | 600 | 124,032 | ||||||

Salesforce, Inc. * | 3,650 | 960,461 | ||||||

ServiceNow, Inc. * | 560 | 395,634 | ||||||

|

| |||||||

| 9,684,471 | ||||||||

|

| |||||||

Transportation - 1.7% | ||||||||

FedEx Corp. | 1,775 | 449,022 | ||||||

Union Pacific Corp. | 2,050 | 503,521 | ||||||

|

| |||||||

| 952,543 | ||||||||

|

| |||||||

Utilities - 0.4% | ||||||||

NextEra Energy, Inc. | 4,140 | 251,464 | ||||||

|

| |||||||

Total Common Stocks | 35,338,666 | |||||||

|

| |||||||

| Name of Issuer | Principal Amount ($) | Fair Value ($) | ||||||

Bonds – 29.1% | ||||||||

Asset-Backed Securities - 0.3% | ||||||||

Small Business Administration: | ||||||||

2008-20A 1, 5.17%, 1/1/28 | 10,230 | 10,104 | ||||||

2007-20H 1, 5.78%, 8/1/27 | 9,396 | 9,326 | ||||||

Towd Point Mortgage Trust: | ||||||||

2020-MH1 A1A, 2.18%, 2/25/60 1, 4 | 64,815 | 61,679 | ||||||

2019-MH1 A2, 3.00%, 11/25/58 1, 4 | 100,000 | 98,252 | ||||||

|

| |||||||

| 179,361 | ||||||||

|

| |||||||

Collateralized Mortgage Obligations - 6.3% |

| |||||||

Chase Home Lending Mortgage Trust: | ||||||||

2023-6 A2, 6.00%, 6/25/54 1, 4 | 147,071 | 147,421 | ||||||

See accompanying notes to financial statements.

| 6 | SIT MUTUAL FUNDS SEMI-ANNUAL REPORT | |

| Name of Issuer | Principal Amount ($) | Fair Value ($) | ||||||

Fannie Mae: | ||||||||

2017-84 JP, 2.75%, 10/25/47 | 16,745 | 14,835 | ||||||

2003-34 A1, 6.00%, 4/25/43 | 22,695 | 22,922 | ||||||

2004-T1 1A1, 6.00%, 1/25/44 | 13,645 | 13,842 | ||||||

1999-17 C, 6.35%, 4/25/29 | 3,965 | 3,996 | ||||||

2001-82 ZA, 6.50%, 1/25/32 | 6,552 | 6,635 | ||||||

2009-30 AG, 6.50%, 5/25/39 | 23,942 | 24,990 | ||||||

2013-28 WD, 6.50%, 5/25/42 | 21,594 | 23,021 | ||||||

2004-T1 1A2, 6.50%, 1/25/44 | 34,832 | 35,656 | ||||||

2004-W9 2A1, 6.50%, 2/25/44 | 23,398 | 23,852 | ||||||

2010-108 AP, 7.00%, 9/25/40 | 290 | 302 | ||||||

2004-T3 1A3, 7.00%, 2/25/44 | 4,774 | 4,948 | ||||||

Freddie Mac: | ||||||||

5280 A, 3.50%, 1/25/50 | 152,570 | 142,693 | ||||||

4812 CZ, 4.00%, 5/15/48 | 158,446 | 149,906 | ||||||

4293 BA, 5.27%, 10/15/47 1 | 7,301 | 7,476 | ||||||

2122 ZE, 6.00%, 2/15/29 | 21,296 | 21,614 | ||||||

2126 C, 6.00%, 2/15/29 | 14,837 | 14,992 | ||||||

2480 Z, 6.00%, 8/15/32 | 18,095 | 18,345 | ||||||

2485 WG, 6.00%, 8/15/32 | 18,457 | 18,952 | ||||||

2575 QE, 6.00%, 2/15/33 | 7,173 | 7,362 | ||||||

2980 QA, 6.00%, 5/15/35 | 9,584 | 9,965 | ||||||

5354 AB, 6.00%, 5/25/49 | 194,669 | 200,359 | ||||||

2357 ZJ, 6.50%, 9/15/31 | 14,342 | 14,469 | ||||||

4520 HM, 6.50%, 8/15/45 | 11,954 | 12,817 | ||||||

3704 CT, 7.00%, 12/15/36 | 7,741 | 8,219 | ||||||

2238 PZ, 7.50%, 6/15/30 | 6,227 | 6,529 | ||||||

Government National Mortgage Association: |

| |||||||

2021-86 WB, 4.74%, 5/20/51 1 | 134,236 | 133,183 | ||||||

2021-104 HT, 5.50%, 6/20/51 | 169,077 | 172,358 | ||||||

2021-27 AW, 5.85%, 2/20/51 1 | 183,318 | 192,976 | ||||||

2015-80 BA, 7.00%, 6/20/45 1 | 6,527 | 6,814 | ||||||

2018-147 AM, 7.00%, 10/20/48 | 22,396 | 23,706 | ||||||

2018-160 DA, 7.00%, 11/20/48 | 21,782 | 23,006 | ||||||

2014-69 W, 7.20%, 11/20/34 1 | 10,252 | 10,724 | ||||||

2013-133 KQ, 7.30%, 8/20/38 1 | 12,303 | 12,960 | ||||||

2005-74 HA, 7.50%, 9/16/35 | 219 | 222 | ||||||

JP Morgan Mortgage Trust: | ||||||||

2021-6 A4, 2.50%, 10/25/51 1, 4 | 288,026 | 251,672 | ||||||

2021-13 A4, 2.50%, 4/25/52 1, 4 | 258,191 | 225,046 | ||||||

2021-6 A12, 5.00%, 10/25/51 1, 4 | 276,517 | 269,276 | ||||||

2021-13 A11, 5.00%, 4/25/52 1, 4 | 281,143 | 260,643 | ||||||

2022-1 A11, 5.00%, 7/25/52 1, 4 | 329,208 | 303,241 | ||||||

2022-2 A11, 5.00%, 8/25/52 1, 4 | 311,398 | 288,546 | ||||||

2023-6 A2, 6.00%, 12/26/53 1, 4 | 140,568 | 141,079 | ||||||

2023-10 A8, 6.00%, 5/25/54 1, 4 | 150,000 | 152,990 | ||||||

New Residential Mortgage Loan Trust: | ||||||||

2018-3A A1, 4.50%, 5/25/58 1, 4 | 33,126 | 32,009 | ||||||

Sequoia Mortgage Trust: | ||||||||

2020-4 A5, 2.50%, 11/25/50 1, 4 | 39,938 | 35,929 | ||||||

Vendee Mortgage Trust: | ||||||||

2008-1 B, 5.80%, 3/15/25 1 | 6,183 | 6,275 | ||||||

Wells Fargo Mortgaged Backed Securities Trust: | ||||||||

2020-5 A3, 2.50%, 9/25/50 1, 4 | 32,506 | 29,121 | ||||||

|

| |||||||

| 3,527,894 | ||||||||

|

| |||||||

| Name of Issuer | Principal Amount ($) | Fair Value ($) | ||||||

Corporate Bonds - 11.2% | ||||||||

American Tower Trust, 5.49%, 3/15/28 4 | 150,000 | 152,258 | ||||||

Bank of America Corp., 5.20%, 4/25/29 1 | 50,000 | 50,350 | ||||||

Bank of New York Mellon Corp., 6.47%, 10/25/34 1 | 175,000 | 194,113 | ||||||

Booz Allen Hamilton, Inc., 5.95%, 8/4/33 | 75,000 | 79,230 | ||||||

British Airways 2020-1 Class B Pass Through Trust, 8.38%, 11/15/28 4 | 39,707 | 41,032 | ||||||

Charles Stark Draper Lab., Inc., 4.39%, 9/1/48 | 100,000 | 91,004 | ||||||

Consolidated Edison Co. of New York, Inc., 5.90%, 11/15/53 | 175,000 | 193,205 | ||||||

Consumers Energy Co., 4.35%, 8/31/64 | 50,000 | 41,780 | ||||||

CVS Health Corp., 5.05%, 3/25/48 | 200,000 | 187,925 | ||||||

CVS Pass-Through Trust, 7.51%, 1/10/32 4 | 136,327 | 143,508 | ||||||

Delta Air Lines 2015-1 Class AA Pass Through Trust, 3.63%, 7/30/27 | 114,005 | 107,421 | ||||||

Dow Chemical Co., 6.90%, 5/15/53 | 175,000 | 211,091 | ||||||

Duke Energy Florida, LLC: | ||||||||

2.54%, 9/1/29 | 42,928 | 40,196 | ||||||

2.86%, 3/1/33 | 120,000 | 105,547 | ||||||

Entergy Louisiana, LLC, 4.95%, 1/15/45 | 200,000 | 183,833 | ||||||

Equifax, Inc., 7.00%, 7/1/37 | 116,000 | 129,774 | ||||||

Evergy Kansas Central, Inc., 5.90%, 11/15/33 | 175,000 | 187,544 | ||||||

Exelon Corp., 7.60%, 4/1/32 | 75,000 | 85,270 | ||||||

Fairfax Financial Holdings, 7.75%, 7/15/37 | 150,000 | 163,720 | ||||||

First-Citizens Bank & Trust Co. | 175,000 | 168,941 | ||||||

GATX Corp., 6.90%, 5/1/34 | 175,000 | 192,974 | ||||||

Genuine Parts Co., 1.88%, 11/1/30 | 200,000 | 162,744 | ||||||

Georgia-Pacific, LLC, 8.88%, 5/15/31 | 150,000 | 187,044 | ||||||

Halliburton Co., 7.60%, 8/15/96 4 | 75,000 | 90,951 | ||||||

J M Smucker Co., 6.50%, 11/15/53 | 175,000 | 202,765 | ||||||

JPMorgan Chase & Co., 4.59%, 4/26/33 1 | 100,000 | 96,790 | ||||||

Kellanova, 7.45%, 4/1/31 | 125,000 | 143,394 | ||||||

KeyCorp, 2.55%, 10/1/29 | 225,000 | 191,607 | ||||||

Leidos, Inc., 7.13%, 7/1/32 | 50,000 | 54,812 | ||||||

Louisville Gas & Electric Co., 5.45%, 4/15/33 | 50,000 | 52,176 | ||||||

Lowe’s Cos., Inc., 5.85%, 4/1/63 | 200,000 | 210,371 | ||||||

Morgan Stanley, 5.12%, 2/1/29 1 | 100,000 | 100,540 | ||||||

Nationwide Mutual Insurance Co. | 195,000 | 194,808 | ||||||

Northern Trust Corp. (Subordinated), 3 Mo. | 250,000 | 231,299 | ||||||

Polar Tankers, Inc., 5.95%, 5/10/37 4 | 93,479 | 96,754 | ||||||

SBA Tower Trust, 6.60%, 1/15/28 4 | 145,000 | 149,130 | ||||||

Security Benefit Life Insurance Co. (Subordinated), 7.45%, 10/1/33 4 | 100,000 | 93,907 | ||||||

State Street Corp., 5.16%, 5/18/34 1 | 175,000 | 176,639 | ||||||

Tennessee Gas Pipeline, LLC, 7.00%, 10/15/28 | 213,000 | 230,827 | ||||||

Textron, Inc., 6.10%, 11/15/33 | 175,000 | 186,863 | ||||||

Truist Financial Corp., 7.16%, 10/30/29 1 | 175,000 | 189,203 | ||||||

Union Electric Co., 4.00%, 4/1/48 | 100,000 | 82,094 | ||||||

United Airlines 2019-2 Class AA Pass Through Trust, 2.70%, 5/1/32 | 125,021 | 105,854 | ||||||

Unum Group, 7.25%, 3/15/28 | 25,000 | 26,639 | ||||||

US Bancorp, 5.78%, 6/12/29 1 | 175,000 | 179,924 | ||||||

Westlake Corp., 3.38%, 8/15/61 | 150,000 | 96,954 | ||||||

|

| |||||||

| 6,284,805 | ||||||||

|

| |||||||

See accompanying notes to financial statements.

| DECEMBER 31, 2023 | 7 | |

SCHEDULE OF INVESTMENTS (Unaudited)

December 31, 2023

Sit Balanced Fund (Continued)

| Name of Issuer | Principal Amount ($) | Fair Value ($) | ||||||

Federal Home Loan Mortgage Corporation - 0.2% |

| |||||||

7.50%, 7/1/29 | 43,060 | 44,212 | ||||||

8.50%, 5/1/31 | 47,976 | 49,663 | ||||||

|

| |||||||

| 93,875 | ||||||||

|

| |||||||

Federal National Mortgage Association - 2.9% |

| |||||||

4.50%, 7/1/52 | 319,412 | 310,057 | ||||||

4.50%, 9/1/52 | 322,934 | 313,476 | ||||||

5.00%, 1/1/30 | 139,418 | 139,678 | ||||||

5.50%, 8/1/56 | 154,726 | 160,067 | ||||||

6.00%, 7/1/41 | 128,739 | 134,370 | ||||||

6.00%, 9/1/53 | 169,555 | 172,291 | ||||||

6.00%, 10/1/53 | 344,904 | 351,008 | ||||||

6.50%, 9/1/27 | 13,754 | 14,095 | ||||||

7.00%, 1/1/32 | 4,255 | 4,248 | ||||||

7.00%, 3/1/33 | 8,278 | 8,410 | ||||||

7.00%, 12/1/38 | 6,902 | 7,007 | ||||||

8.40%, 7/15/26 | 594 | 593 | ||||||

|

| |||||||

| 1,615,300 | ||||||||

|

| |||||||

Government National Mortgage Association - 1.8% |

| |||||||

3.50%, 2/20/52 | 262,641 | 244,616 | ||||||

4.00%, 9/20/52 | 238,029 | 221,306 | ||||||

5.00%, 5/20/48 | 23,789 | 24,124 | ||||||

5.50%, 9/20/52 | 88,537 | 87,499 | ||||||

5.50%, 8/20/62 | 218,225 | 217,481 | ||||||

6.00%, 9/20/53 | 174,233 | 175,430 | ||||||

6.50%, 11/20/38 | 8,798 | 8,965 | ||||||

7.00%, 12/15/24 | 1,144 | 1,143 | ||||||

7.00%, 11/20/27 | 3,556 | 3,659 | ||||||

7.00%, 9/20/29 | 11,461 | 11,823 | ||||||

7.00%, 9/20/38 | 5,673 | 5,973 | ||||||

7.50%, 4/20/32 | 7,449 | 7,604 | ||||||

|

| |||||||

| 1,009,623 | ||||||||

|

| |||||||

Taxable Municipal Securities - 5.1% | ||||||||

Benton & Polk Sch. Dist. No. 17J G.O., 5.47%, 6/15/27 | 150,000 | 154,283 | ||||||

Chicago Park Dist., 2.53%, 1/1/34 | 235,000 | 189,347 | ||||||

CO Health Facs. Auth., 3.13%, 5/15/27 | 250,000 | 224,722 | ||||||

Colorado Edu. & Cultural Fac. Auth., 3.97%, 3/1/56 | 205,000 | 165,939 | ||||||

Coventry Local Sch. Dist., 2.20%, 11/1/29 | 200,000 | 175,064 | ||||||

LaGrange Co. Regional Utility Dist., 2.98%, 1/1/40 | 230,000 | 184,209 | ||||||

Maricopa Co. Industrial Dev. Auth., 3.50%, 7/1/44 4 | 100,000 | 76,182 | ||||||

Massachusetts Edu. Auth.: | ||||||||

4.00%, 1/1/32 | 20,000 | 19,552 | ||||||

4.41%, 7/1/34 | 15,000 | 14,681 | ||||||

4.95%, 7/1/38 | 200,000 | 192,980 | ||||||

5.95%, 7/1/44 | 150,000 | 153,890 | ||||||

MN Hsg. Fin. Agy., 2.31%, 1/1/27 | 135,000 | 125,894 | ||||||

NJ Higher Edu. Student Assit. Auth., 3.50%, 12/1/39 8 | 70,000 | 67,584 | ||||||

NY State Dormitory Auth., 2.69%, 7/1/35 | 200,000 | 161,390 | ||||||

Oregon State Fac. Auth., 2.68%, 7/1/31 | 350,000 | 289,170 | ||||||

Public Fin. Auth., 4.23%, 7/1/32 | 105,000 | 100,173 | ||||||

State of Connecticut G.O., 5.09%, 10/1/30 | 100,000 | 100,804 | ||||||

Texas Children’s Hospital, 3.37%, 10/1/29 17 | 115,000 | 109,624 | ||||||

| Name of Issuer | Principal Amount ($) | Fair Value ($) | ||||||

Utah Charter Sch. Fin. Auth., 2.40%, 10/15/27 | 205,000 | 189,432 | ||||||

VA Hsg. Dev. Auth., 2.13%, 7/25/51 | 1,254 | 952 | ||||||

WA State Hsg. Fin. Comm., 3.50%, 7/1/24 4 | 20,000 | 19,752 | ||||||

Wichita Falls, 1.65%, 9/1/28 | 145,000 | 128,714 | ||||||

|

| |||||||

| 2,844,338 | ||||||||

|

| |||||||

U.S. Treasury / Federal Agency Securities - 1.3% |

| |||||||

U.S. Treasury - 1.3% |

| |||||||

U.S. Treasury Bonds: | ||||||||

3.63%, 2/15/53 | 275,000 | 255,170 | ||||||

4.13%, 8/15/53 | 75,000 | 76,172 | ||||||

U.S. Treasury Notes 4.50%, 11/15/33 | 400,000 | 420,812 | ||||||

|

| |||||||

| 752,154 | ||||||||

|

| |||||||

Total Bonds | 16,307,350 | |||||||

|

| |||||||

| Name of Issuer | Quantity | Fair Value ($) | ||||||

Investment Companies 3.6% | ||||||||

BlackRock Credit Allocation Income Trust | 17,750 | 183,180 | ||||||

BlackRock Enhanced Government Fund | 4,174 | 40,632 | ||||||

BlackRock Income Trust, Inc. | 5,300 | 64,554 | ||||||

BlackRock Municipal Income Fund, Inc. | 2,300 | 26,772 | ||||||

BlackRock Municipal Income Trust | 2,100 | 21,147 | ||||||

BlackRock Taxable Municipal Bond Trust | 10,671 | 173,511 | ||||||

DWS Municipal Income Trust | 9,800 | 87,122 | ||||||

Eaton Vance California Municipal Bond Fund | 1,700 | 15,555 | ||||||

First Trust Mortgage Income Fund | 3,800 | 46,056 | ||||||

MFS Intermediate Income Trust | 63,700 | 170,716 | ||||||

Nuveen AMT-Free Muni Credit Income Fund | 20,900 | 247,038 | ||||||

Nuveen AMT-Free Quality Muni Income Fund | 15,100 | 166,100 | ||||||

Nuveen Multi-Market Income Fund | 13,253 | 78,325 | ||||||

Nuveen Quality Municipal Income Fund | 12,500 | 143,125 | ||||||

Nuveen Taxable Municipal Income Fund | 5,967 | 94,219 | ||||||

Putnam Master Intermediate Income Trust | 61,000 | 194,590 | ||||||

Putnam Premier Income Trust | 45,692 | 163,120 | ||||||

TCW Strategic Income Fund, Inc. | 18,000 | 82,620 | ||||||

|

| |||||||

Total Investment Companies | 1,998,382 | |||||||

|

| |||||||

Short-Term Securities - 3.5% | ||||||||

Fidelity Inst. Money Mkt. Gvt. Fund, 5.29% | 1,973,150 | 1,973,150 | ||||||

|

| |||||||

Total Investments in Securities - 99.4% |

| 55,617,548 | ||||||

Other Assets and Liabilities, net - 0.6% |

| 320,060 | ||||||

|

| |||||||

Net Assets - 100.0% | $55,937,608 | |||||||

|

| |||||||

See accompanying notes to financial statements.

| 8 | SIT MUTUAL FUNDS SEMI-ANNUAL REPORT | |

| * | Non-income producing security. |

| 1 | Variable rate security. Rate disclosed is as of December 31, 2023. Certain variable rate securities are not based on a published reference rate and spread but are determined by the issuer or agent and are based on current market conditions, or, for mortgage-backed securities, are impacted by the individual mortgages which are paying off over time. These securities do not indicate a reference rate and spread in their descriptions. |

| 4 | 144A Restricted Security. The total value of such securities as of December 31, 2023 was $3,355,186 and represented 6.0% of net assets. These securities have been determined to be liquid by the Adviser in accordance with guidelines established by the Board of Directors. |

| 8 | Securities the income from which is treated as a tax preference that is included in alternative minimum taxable income for purposes of computing federal alternative minimum tax (AMT). At December 31, 2023, 0.1% of net assets in the Fund was invested in such securities. |

| 17 | Security that is either an absolute and unconditional obligation of the United States Government or is collateralized by securities, loans, or leases guaranteed by the U.S. Government or its agencies or instrumentalities. |

ADR — American Depositary Receipt |

LLC — Limited Liability Company |

PLC — Public Limited Company |

Numeric footnotes not disclosed are not applicable to this Schedule of Investments.

A summary of the levels for the Fund’s investments as of December 31, 2023 is as follows (see Note 2 - significant accounting policies in the notes to financial statements):

Investment in Securities | ||||||||||||||||

| Level 1 | Level 2 | Level 3 | ||||||||||||||

| Quoted | Other significant | Significant | ||||||||||||||

| Prices ($) | observable inputs ($) | unobservable inputs ($) | Total ($) | |||||||||||||

Common Stocks** | 35,338,666 | — | — | 35,338,666 | ||||||||||||

Asset-Backed Securities | — | 179,361 | — | 179,361 | ||||||||||||

Collateralized Mortgage Obligations | — | 3,527,894 | — | 3,527,894 | ||||||||||||

Corporate Bonds | — | 6,284,805 | — | 6,284,805 | ||||||||||||

Federal Home Loan Mortgage Corporation | — | 93,875 | — | 93,875 | ||||||||||||

Federal National Mortgage Association | — | 1,615,300 | — | 1,615,300 | ||||||||||||

Government National Mortgage Association | — | 1,009,623 | — | 1,009,623 | ||||||||||||

Taxable Municipal Securities | — | 2,844,338 | — | 2,844,338 | ||||||||||||

U.S. Treasury / Federal Agency Securities | — | 752,154 | — | 752,154 | ||||||||||||

Investment Companies | 1,998,382 | — | — | 1,998,382 | ||||||||||||

Short-Term Securities | 1,973,150 | — | — | 1,973,150 | ||||||||||||

Total: | 39,310,198 | 16,307,350 | — | 55,617,548 | ||||||||||||

| ** | For equity securities categorized in a single level, refer to the detail above for further breakdown. |

There were no transfers into or out of level 3 during the reporting period.

See accompanying notes to financial statements.

| DECEMBER 31, 2023 | 9 | |

OBJECTIVE & STRATEGY

The objective of the Sit Dividend Growth Fund is to provide current income that exceeds the dividend yield of the S&P 500® Index and that grows over a period of years. Secondarily, the Fund seeks long-term capital appreciation.

The Fund seeks to achieve its objectives by investing, under normal market conditions, at least 80% of its net assets in dividend-paying common stocks. The Fund may invest the balance of its assets in preferred stocks, convertible bonds, U.S. Treasury securities and closed-end investment companies.

Fund Performance

The Sit Dividend Growth Fund Class I posted a +6.27% return during the 6-month period ended December 31, 2023, compared to the +8.04% return for the S&P 500® Index. The Fund’s gross dividend yield (before deducting Fund expenses) was 1.99% as of 12/31/23, compared to 1.48% for the S&P 500® Index.

Factors that Influenced the Fund’s Performance

The Fund posted positive absolute returns over the 6-month period, although it underperformed the S&P500® Index. The primary reason for the underperformance was that lower beta, dividend payers lagged the overall market. Investors embraced riskier technology stocks linked to artificial intelligence (AI), such as NVIDIA and Salesforce. A second reason for trailing performance was not owning any weight loss drug (GLP-1) producers, such as Eli Lilly, which saw strong stock appreciation. Strong stock selection in the producer manufacturing sector added to returns. Key holdings here were General Dynamics, which benefitted from strong global defense spending and Gulfstream demand, and Eaton, a beneficiary of increased utility spending and the growth of electrification. An underweight position in the consumer durables sector, specifically not owning Tesla due to the stock’s expensive valuation further enhanced performance.

Outlook and Positioning

Due to several factors, dividend-paying stocks produced their weakest relative returns in years, especially against the AI-driven rally that pushed the “Magnificent Seven” and other non-dividend-paying tech stocks much higher in 2023. Looking ahead, we see an emerging backdrop that has historically led to solid relative performance for high-quality, dividend-paying growth stocks. Key elements of our forecast include modest economic growth, lower interest rates (including fed funds rate cuts), and the likelihood of an increase in stock price volatility from exceptionally low levels. In addition to technology, early cycle and rate-sensitive sectors, such as transportation and producer manufacturing should fare well in the year ahead. We also see attractive

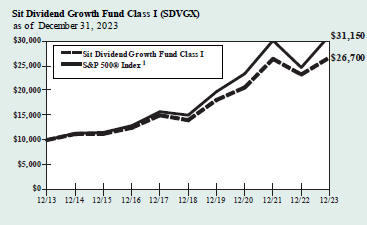

HYPOTHETICAL GROWTH OF $10,000

The chart above illustrates the total value of a hypothetical $10,000 investment in the Fund over the past 10 years as compared to the performance of the S&P 500® Index. Past performance does not guarantee future results. Returns include the reinvestment of distributions. The chart does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

1 S&P 500® Index is an unmanaged capitalization-weighted index that measures the performance of 500 widely held common stocks of large-cap companies. It is not possible to invest directly in an index. This is the Fund’s primary index.

growth and income opportunities in diverse areas, including energy, P&C insurance, drug distributors, and select pharmaceutical companies. The sharp rise in interest rates in 2023 provided stiff competition for dividend payers from bonds, particularly for slower growth “bond proxies,” including utilities, consumer staples, and REITs. While we prefer “growthier” stocks, these low-beta sectors are cheap insurance against market volatility or a severe recession and offer earnings growth, well-above-average dividend yields, and attractive valuations.

Roger J. Sit

Kent L. Johnson

Portfolio Managers

Information on this page is unaudited.

| 10 | SIT MUTUAL FUNDS SEMI-ANNUAL REPORT | |

|

COMPARATIVE RATES OF RETURNS

as of December 31, 2023

| Sit Dividend Growth Fund | ||||||||||||

| Class I | Class S | | S&P 500® Index1 | | ||||||||

Six Month | 6.27 | % | 6.12 | % | 8.04 | % | ||||||

One Year | 14.88 | 14.62 | 26.29 | |||||||||

Five Year | 13.75 | 13.48 | 15.69 | |||||||||

Ten Year | 10.32 | 10.04 | 12.03 | |||||||||

Since Inception-Class I | 9.97 | n/a | 9.69 | |||||||||

(12/31/03) | ||||||||||||

Since Inception-Class S | n/a | 9.45 | 9.78 | |||||||||

(3/31/06) | ||||||||||||

Performance figures are historical and do not guarantee future results. Investment returns and principal value will vary, and you may have a gain or loss when you sell shares. Current performance may be lower or higher than the performance data quoted. Contact the Fund for performance data current to the most recent month-end. Returns include changes in share price as well as reinvestment of all dividends and capital gains. Returns do not reflect the deduction of the 2% redemption fee imposed if shares are redeemed or exchanged within 30 calendar days from their date of purchase. If imposed, the fee would reduce the performance quoted. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Management fees and administrative expenses are included in the Fund’s performance. Returns for periods greater than one year are compounded average annual rates of return.

1 S&P 500® Index is an unmanaged capitalization-weighted index that measures the performance of 500 widely held common stocks of large-cap companies. It is not possible to invest directly in an index.

PORTFOLIO SUMMARY

Class I: | ||||||

Net Asset Value 12/31/23: | $ | 14.90 | Per Share | |||

Net Asset Value 6/30/23: | $ | 14.64 | Per Share | |||

Net Assets: | $ | 204.3 | Million | |||

Class S: | ||||||

Net Asset Value 12/31/23: | $ | 14.80 | Per Share | |||

Net Asset Value 6/30/23: | $ | 14.54 | Per Share | |||

Net Assets: | $ | 21.3 | Million | |||

Weighted Average Market Cap: | $ | 565.7 | Billion | |||

TOP 10 HOLDINGS

1. Microsoft Corp.

2. Apple, Inc.

3. Broadcom, Inc.

4. UnitedHealth Group, Inc.

5. Exxon Mobil Corp.

6. Johnson & Johnson

7. ConocoPhillips

8. JPMorgan Chase & Co.

9. Alphabet, Inc. - Class A

10. Oracle Corp.

Based on net assets as of December 31, 2023.

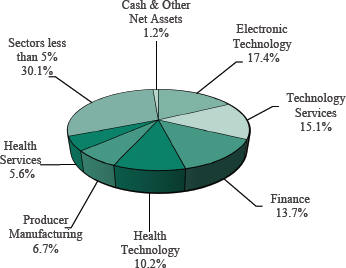

SECTOR ALLOCATION

Based on net assets as of December 31, 2023.

Information on this page is unaudited.

| DECEMBER 31, 2023 | 11 | |

SCHEDULE OF INVESTMENTS (Unaudited)

December 31, 2023

Sit Dividend Growth Fund

Investments are grouped by economic sectors.

| Name of Issuer | Quantity | Fair Value ($) | ||||||

Common Stocks - 98.8% | ||||||||

Commercial Services - 2.8% | ||||||||

Booz Allen Hamilton Holding Corp. | 15,200 | 1,944,232 | ||||||

S&P Global, Inc. | 6,260 | 2,757,655 | ||||||

Sysco Corp. | 21,100 | 1,543,043 | ||||||

|

| |||||||

| 6,244,930 | ||||||||

|

| |||||||

Communications - 0.8% | ||||||||

American Tower Corp. | 8,750 | 1,888,950 | ||||||

|

| |||||||

Consumer Non-Durables - 4.9% | ||||||||

Mondelez International, Inc. | 33,675 | 2,439,080 | ||||||

NIKE, Inc. | 12,750 | 1,384,268 | ||||||

PepsiCo, Inc. | 20,975 | 3,562,394 | ||||||

Procter & Gamble Co. | 24,625 | 3,608,547 | ||||||

|

| |||||||

| 10,994,289 | ||||||||

|

| |||||||

Consumer Services - 3.2% | ||||||||

McDonald’s Corp. | 7,725 | 2,290,540 | ||||||

Starbucks Corp. | 17,600 | 1,689,776 | ||||||

Visa, Inc. | 12,010 | 3,126,803 | ||||||

|

| |||||||

| 7,107,119 | ||||||||

|

| |||||||

Electronic Technology - 17.4% | ||||||||

Analog Devices, Inc. | 9,650 | 1,916,104 | ||||||

Apple, Inc. | 69,235 | 13,329,815 | ||||||

Applied Materials, Inc. | 21,900 | 3,549,333 | ||||||

Broadcom, Inc. | 7,250 | 8,092,812 | ||||||

Cisco Systems, Inc. | 30,425 | 1,537,071 | ||||||

Garmin, Ltd. | 18,275 | 2,349,068 | ||||||

International Business Machines Corp. | 16,275 | 2,661,776 | ||||||

NVIDIA Corp. | 5,885 | 2,914,370 | ||||||

TE Connectivity, Ltd. | 20,150 | 2,831,075 | ||||||

|

| |||||||

| 39,181,424 | ||||||||

|

| |||||||

Energy Minerals - 4.2% | ||||||||

ConocoPhillips | 34,400 | 3,992,808 | ||||||

Exxon Mobil Corp. | 53,725 | 5,371,425 | ||||||

|

| |||||||

| 9,364,233 | ||||||||

|

| |||||||

Finance - 13.7% | ||||||||

Air Lease Corp. | 35,850 | 1,503,549 | ||||||

American International Group, Inc. | 33,125 | 2,244,219 | ||||||

Ameriprise Financial, Inc. | 4,550 | 1,728,227 | ||||||

Axis Capital Holdings, Ltd. | 26,450 | 1,464,537 | ||||||

Bank of New York Mellon Corp. | 53,750 | 2,797,687 | ||||||

Carlyle Group, Inc. | 36,500 | 1,485,185 | ||||||

Chubb, Ltd. | 1,325 | 299,450 | ||||||

Everest Group, Ltd. | 7,290 | 2,577,598 | ||||||

Goldman Sachs Group, Inc. | 5,600 | 2,160,312 | ||||||

Intercontinental Exchange, Inc. | 21,075 | 2,706,662 | ||||||

JPMorgan Chase & Co. | 23,300 | 3,963,330 | ||||||

Morgan Stanley | 19,860 | 1,851,945 | ||||||

Realty Income Corp. | 57,653 | 3,310,435 | ||||||

Reinsurance Group of America, Inc. | 17,950 | 2,903,951 | ||||||

|

| |||||||

| 30,997,087 | ||||||||

|

| |||||||

Health Services - 5.6% | ||||||||

Cardinal Health, Inc. | 18,975 | 1,912,680 | ||||||

HCA Healthcare, Inc. | 6,630 | 1,794,609 | ||||||

Quest Diagnostics, Inc. | 20,525 | 2,829,987 | ||||||

| Name of Issuer | Quantity | Fair Value ($) | ||||||

UnitedHealth Group, Inc. | 11,790 | 6,207,081 | ||||||

|

| |||||||

| 12,744,357 | ||||||||

|

| |||||||

Health Technology - 10.2% | ||||||||

Abbott Laboratories | 28,885 | 3,179,372 | ||||||

AbbVie, Inc. | 9,325 | 1,445,095 | ||||||

AstraZeneca, PLC, ADR | 51,225 | 3,450,004 | ||||||

Gilead Sciences, Inc. | 35,190 | 2,850,742 | ||||||

Johnson & Johnson | 32,125 | 5,035,272 | ||||||

Medtronic, PLC | 22,425 | 1,847,371 | ||||||

Novo Nordisk A/S, ADR | 13,100 | 1,355,195 | ||||||

Thermo Fisher Scientific, Inc. | 2,445 | 1,297,782 | ||||||

Zimmer Biomet Holdings, Inc. | 21,325 | 2,595,253 | ||||||

|

| |||||||

| 23,056,086 | ||||||||

|

| |||||||

Industrial Services - 2.1% | ||||||||

Waste Management, Inc. | 14,900 | 2,668,590 | ||||||

Williams Cos., Inc. | 57,690 | 2,009,343 | ||||||

|

| |||||||

| 4,677,933 | ||||||||

|

| |||||||

Non-Energy Minerals - 0.5% | ||||||||

Glencore, PLC, ADR | 103,310 | 1,237,654 | ||||||

|

| |||||||

Process Industries - 1.2% | ||||||||

Air Products & Chemicals, Inc. | 10,100 | 2,765,380 | ||||||

|

| |||||||

Producer Manufacturing - 6.7% | ||||||||

Eaton Corp., PLC | 9,750 | 2,347,995 | ||||||

Emerson Electric Co. | 28,675 | 2,790,938 | ||||||

General Dynamics Corp. | 12,650 | 3,284,825 | ||||||

Honeywell International, Inc. | 13,175 | 2,762,929 | ||||||

Lockheed Martin Corp. | 1,375 | 623,205 | ||||||

Parker-Hannifin Corp. | 3,635 | 1,674,645 | ||||||

Siemens AG, ADR | 18,550 | 1,735,167 | ||||||

|

| |||||||

| 15,219,704 | ||||||||

|

| |||||||

Retail Trade - 2.9% | ||||||||

Home Depot, Inc. | 7,740 | 2,682,297 | ||||||

Target Corp. | 6,500 | 925,730 | ||||||

TJX Cos., Inc. | 30,160 | 2,829,310 | ||||||

|

| |||||||

| 6,437,337 | ||||||||

|

| |||||||

Technology Services - 15.1% | ||||||||

Accenture, PLC | 10,250 | 3,596,827 | ||||||

Adobe, Inc. * | 5,025 | 2,997,915 | ||||||

Alphabet, Inc. - Class A * | 27,790 | 3,881,985 | ||||||

Intuit, Inc. | 4,890 | 3,056,397 | ||||||

Microsoft Corp. | 44,700 | 16,808,988 | ||||||

Oracle Corp. | 35,425 | 3,734,858 | ||||||

|

| |||||||

| 34,076,970 | ||||||||

|

| |||||||

Transportation - 3.6% | ||||||||

FedEx Corp. | 13,725 | 3,472,013 | ||||||

TFI International, Inc. | 11,100 | 1,509,378 | ||||||

Union Pacific Corp. | 12,375 | 3,039,548 | ||||||

|

| |||||||

| 8,020,939 | ||||||||

|

| |||||||

Utilities - 3.9% | ||||||||

DTE Energy Co. | 22,875 | 2,522,198 | ||||||

NiSource, Inc. | 106,575 | 2,829,566 | ||||||

See accompanying notes to financial statements.

| 12 | SIT MUTUAL FUNDS SEMI-ANNUAL REPORT | |

| Name of Issuer | Quantity | Fair Value ($) | ||||||

PPL Corp. | 126,600 | 3,430,860 | ||||||

|

| |||||||

| 8,782,624 | ||||||||

|

| |||||||

Total Common Stocks | 222,797,016 | |||||||

|

| |||||||

Short-Term Securities - 1.0% | ||||||||

Fidelity Inst. Money Mkt. Gvt. Fund, 5.29% | 2,300,344 | 2,300,344 | ||||||

|

| |||||||

Total Investments in Securities - 99.8% | 225,097,360 | |||||||

Other Assets and Liabilities, net - 0.2% | 492,872 | |||||||

|

| |||||||

Net Assets - 100.0% | $ | 225,590,232 | ||||||

|

| |||||||

| * | Non-income producing security. |

ADR — American Depositary Receipt |

PLC — Public Limited Company |

Numeric footnotes not disclosed are not applicable to this Schedule of Investments.

A summary of the levels for the Fund’s investments as of December 31, 2023 is as follows (see Note 2 - significant accounting policies in the notes to financial statements):

| Investment in Securities | ||||||||||||||||

Level 1 Quoted Prices ($) | Level 2 Other significant | Level 3 Significant unobservable inputs ($) | Total ($) | |||||||||||||

Common Stocks** | 222,797,016 | — | — | 222,797,016 | ||||||||||||

Short-Term Securities | 2,300,344 | — | — | 2,300,344 | ||||||||||||

Total: | 225,097,360 | — | — | 225,097,360 | ||||||||||||

| ** | For equity securities categorized in a single level, refer to the detail above for further breakdown. |

There were no transfers into or out of level 3 during the reporting period.

See accompanying notes to financial statements.

| DECEMBER 31, 2023 | 13 | |

OBJECTIVE & STRATEGY

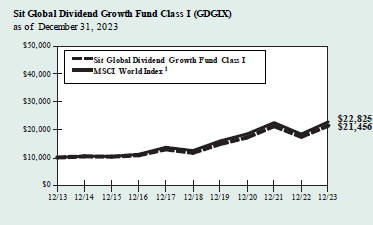

The objective of the Sit Global Dividend Growth Fund is to provide current income that exceeds the dividend yield of the MSCI World Index and that grows over a period of years. Secondarily, the Fund seeks long-term capital appreciation. The Fund seeks to achieve its objectives by investing, under normal market conditions, at least 80% of its net assets in dividend-paying common stocks issued by U.S. and foreign companies. The Fund may invest the balance of its assets in preferred stocks, convertible bonds, U.S. Treasury securities and closed-end investment companies.

Fund Performance

The Sit Global Dividend Growth Fund Class I shares provided a return of +8.23% during the 6-month period ended December 31, 2023, compared to the return of the MSCI World Index of +7.56%. The Fund’s gross dividend yield (before deducting Fund expenses) was 1.91% as of December 31, 2023, compared to 1.94% for the MSCI World Index.

Factors that Influenced the Fund’s Performance

The Fund recorded strong absolute returns during the 6-month period and outperformed the MSCI World Index. Strong overall stock selection was partially offset by a negative allocation effect, as the highest P/E stocks and the lowest yielding and non-yielding stocks outperformed, and these issues were underweighted in the Fund. The Fund’s holdings in the financial services sector performed well on an absolute basis, helped by an overweight position and positive returns relative to the benchmark sector. Here, strong stock performances in Partners Group Holdings AG and Goldman Sachs augmented returns. The technology sectors also contributed favorably to Fund returns during the period, led by Broadcom, Logitech International S.A., and Atlassian. Performance was also enhanced by stock selection in the capital goods sector, where the Fund held BAE Systems plc and Trane Technologies plc. The biggest detractor to the Fund’s performance during the period was holdings in the pharmaceuticals biotechnology & life sciences sector. The Fund did not hold stocks with exposure to GLP-1 drugs used to treat Type 2 diabetes and prescribed for weight loss, which outperformed during the period. Company-specific issues also hurt the Fund’s holdings in Lonza Group AG and Astellas Pharma. In addition, exposure to the food beverage & tobacco sector hurt returns, due to the “risk-on” investment mode that prevailed during much of the period. Geographically, the Fund’s exposure to Asia/Pacific ex Japan, Non-Euroland, and Euroland added value during the period due to strong stock selection, while its exposure to North America detracted from performance.

Outlook and Positioning

Still-high economic uncertainty, elevated policy/geopolitical risks, and “fair” equity valuations support our quality bias within a better environment for stock pickers in 2024. We generally maintain positions in the most attractive “Magnificent Seven” stocks but also see compelling opportunities in other technology segments, including semiconductors, software/services, and cybersecurity. Sentiment is also broadly improving for financial stocks. Given pent-up demand for initial public

HYPOTHETICAL GROWTH OF $10,000

The chart above illustrates the total value of a hypothetical $10,000 investment in the Fund over the past 10 years as compared to the performance of the MSCI World Index. Past performance does not guarantee future results. Returns include the reinvestment of distributions. The chart does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

1 The MSCI World Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets. It is not possible to invest directly in an index.

offerings, debt issuance, and M&A, we see the most attractive opportunities for a strong rebound in capital markets businesses. We also see an emerging backdrop that has historically led to solid relative performance for high-quality, dividend-paying growth stocks. In addition to the groups noted above, we see attractive growth and income opportunities in diverse areas, including energy, P&C insurance, drug distributors, and select pharmaceutical companies. Internationally, we remain positive on equities in China, South Korea, Singapore, India, Australia, Mexico, and Brazil. We favor high-quality industries with improving fundamentals, like life insurance, Macau gaming, and some internet names. At the same time, we are keeping defensive exposure in consumer staples, healthcare, and utilities.

Roger J. Sit Raymond E. Sit

Kent L. Johnson

Portfolio Managers

Information on this page is unaudited.

| 14 | SIT MUTUAL FUNDS SEMI-ANNUAL REPORT | |

|

COMPARATIVE RATES OF RETURNS

as of December 31, 2023 | ||||||

| Sit Global Dividend Growth Fund | ||||||||||||

| Class I | Class S | | MSCI World Index | 1 | ||||||||

Six Month | 8.23% | 8.14 | % | 7.56 | % | |||||||

One Year | 23.12 | 22.78 | 23.79 | |||||||||

Five Year | 12.88 | 12.60 | 12.80 | |||||||||

Ten Year | 7.93 | 7.66 | 8.60 | |||||||||

Since Inception (9/30/08) | 9.16 | 8.88 | 8.75 | |||||||||

Performance figures are historical and do not guarantee future results. Investment returns and principal value will vary, and you may have a gain or loss when you sell shares. Current performance may be lower or higher than the performance data quoted. Contact the Fund for performance data current to the most recent month-end. Returns include changes in share price as well as reinvestment of all dividends and capital gains. Returns do not reflect the deduction of the 2% redemption fee imposed if shares are redeemed or exchanged within 30 calendar days from their date of purchase. If imposed, the fee would reduce the performance quoted. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Management fees and administrative expenses are included in the Fund’s performance. Returns for periods greater than one year are compounded average annual rates of return.

1 The MSCI World Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets. It is not possible to invest directly in an index.

| PORTFOLIO SUMMARY | ||||||||

| Class I: | ||||||||

Net Asset Value 12/31/23: | $24.41 | Per Share | ||||||

Net Asset Value 6/30/23: | $22.75 | Per Share | ||||||

Net Assets: | $44.1 | Million | ||||||

| Class S: | ||||||||

Net Asset Value 12/31/23: | $24.39 | Per Share | ||||||

Net Asset Value 6/30/23: | $22.71 | Per Share | ||||||

Net Assets: | $4.2 | Million | ||||||

Weighted Average Market Cap: | $625.7 | Billion | ||||||

TOP 10 HOLDINGS

1. Microsoft Corp.

2. Apple, Inc.

3. Broadcom, Inc.

4. Shell, PLC, ADR

5. Applied Materials, Inc.

6. Alphabet, Inc. - Class A

7. JPMorgan Chase & Co.

8. Accenture, PLC

9. Johnson & Johnson

10. BAE Systems, PLC

Based on net assets as of December 31, 2023.

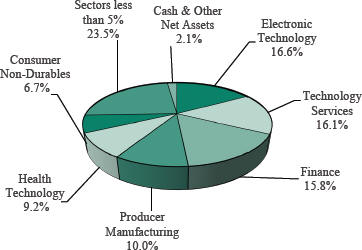

SECTOR ALLOCATION

Based on net assets as of December 31, 2023.

Information on this page is unaudited.

| DECEMBER 31, 2023 | 15 | |

SCHEDULE OF INVESTMENTS (Unaudited)

December 31, 2023

Sit Global Dividend Growth Fund

Investments are grouped by geographic region

| Name of Issuer | Quantity | Fair Value ($) | ||||||

Common Stocks - 97.9% | ||||||||

Asia - 6.2% | ||||||||

Australia - 3.5% | ||||||||

Atlassian Corp. * | 3,445 | 819,428 | ||||||

BHP Group, Ltd. ADR | 6,010 | 410,543 | ||||||

Macquarie Group, Ltd. | 3,810 | 476,763 | ||||||

|

| |||||||

| 1,706,734 | ||||||||

|

| |||||||

Japan - 1.7% | ||||||||

Astellas Pharma, Inc. | 29,200 | 349,157 | ||||||

Recruit Holdings Co., Ltd. | 10,600 | 448,282 | ||||||

|

| |||||||

| 797,439 | ||||||||

|

| |||||||

Singapore - 1.0% | ||||||||

Singapore Technologies Engineering, Ltd. | 155,000 | 456,867 | ||||||

|

| |||||||

Europe - 32.9% | ||||||||

France - 0.7% | ||||||||

Safran SA, ADR | 7,520 | 331,858 | ||||||

|

| |||||||

Germany - 5.7% | ||||||||

Allianz SE, ADR | 34,190 | 912,531 | ||||||

Deutsche Post AG | 3,960 | 196,090 | ||||||

Infineon Technologies AG | 6,275 | 261,851 | ||||||

Muenchener Rueckversicherungs AG | 1,470 | 608,715 | ||||||

Siemens AG | 4,250 | 797,229 | ||||||

|

| |||||||

| 2,776,416 | ||||||||

|

| |||||||

Ireland - 4.7% | ||||||||

Accenture, PLC | 3,285 | 1,152,739 | ||||||

Linde, PLC | 1,445 | 593,476 | ||||||

Trane Technologies, PLC | 2,125 | 518,288 | ||||||

|

| |||||||

| 2,264,503 | ||||||||

|

| |||||||

Spain - 1.6% | ||||||||

Iberdrola SA | 59,010 | 773,260 | ||||||

|

| |||||||

Switzerland - 6.4% | ||||||||

Chubb, Ltd. | 2,590 | 585,340 | ||||||

Logitech International SA | 4,150 | 394,499 | ||||||

Lonza Group AG | 930 | 391,107 | ||||||

Nestle SA | 5,935 | 688,094 | ||||||

Partners Group Holding AG | 705 | 1,016,783 | ||||||

|

| |||||||

| 3,075,823 | ||||||||

|

| |||||||

United Kingdom - 13.8% | ||||||||

AstraZeneca, PLC, ADR | 15,040 | 1,012,944 | ||||||

BAE Systems, PLC | 72,955 | 1,032,677 | ||||||

Compass Group, PLC | 14,170 | 387,606 | ||||||

Diageo, PLC, ADR | 4,125 | 600,848 | ||||||

Glencore, PLC, ADR | 24,620 | 294,948 | ||||||

London Stock Exchange Group, PLC | 6,715 | 793,787 | ||||||

Man Group, PLC | 216,290 | 641,264 | ||||||

RELX, PLC | 14,120 | 558,354 | ||||||

Shell, PLC, ADR | 20,055 | 1,319,619 | ||||||

|

| |||||||

| 6,642,047 | ||||||||

|

| |||||||

North America - 58.8% | ||||||||

United States - 58.8% | ||||||||

Abbott Laboratories | 7,230 | 795,806 | ||||||

Alphabet, Inc. - Class A * | 8,790 | 1,227,875 | ||||||

| Name of Issuer | Quantity | Fair Value ($) | ||||||

Apple, Inc. | 18,220 | 3,507,897 | ||||||

Applied Materials, Inc. | 7,985 | 1,294,129 | ||||||

Arthur J Gallagher & Co. | 3,685 | 828,683 | ||||||

Broadcom, Inc. | 1,785 | 1,992,506 | ||||||

Cheniere Energy, Inc. | 2,830 | 483,109 | ||||||

ConocoPhillips | 4,025 | 467,182 | ||||||

Constellation Brands, Inc. | 2,690 | 650,307 | ||||||

FedEx Corp. | 1,900 | 480,643 | ||||||

Gilead Sciences, Inc. | 2,665 | 215,892 | ||||||

Goldman Sachs Group, Inc. | 1,370 | 528,505 | ||||||

Home Depot, Inc. | 2,490 | 862,909 | ||||||

Honeywell International, Inc. | 3,130 | 656,392 | ||||||

Johnson & Johnson | 6,765 | 1,060,346 | ||||||

JPMorgan Chase & Co. | 7,180 | 1,221,318 | ||||||

Lockheed Martin Corp. | 1,525 | 691,191 | ||||||

McDonald’s Corp. | 1,820 | 539,648 | ||||||

Microsoft Corp. | 10,475 | 3,939,019 | ||||||

Mondelez International, Inc. | 6,940 | 502,664 | ||||||

NVIDIA Corp. | 1,150 | 569,503 | ||||||

Otis Worldwide Corp. | 3,785 | 338,644 | ||||||

PepsiCo, Inc. | 4,765 | 809,288 | ||||||

Salesforce, Inc. * | 705 | 185,514 | ||||||

Sherwin-Williams Co. | 1,835 | 572,336 | ||||||

Thermo Fisher Scientific, Inc. | 1,145 | 607,755 | ||||||

Union Pacific Corp. | 3,960 | 972,655 | ||||||

UnitedHealth Group, Inc. | 1,585 | 834,455 | ||||||

Waste Management, Inc. | 4,980 | 891,918 | ||||||

WEC Energy Group, Inc. | 6,010 | 505,862 | ||||||

Williams Cos., Inc. | 4,490 | 156,387 | ||||||

|

| |||||||

| 28,390,338 | ||||||||

|

| |||||||

Total Common Stocks | 47,215,285 | |||||||

|

| |||||||

Short-Term Securities - 2.0% | ||||||||

Fidelity Inst. Money Mkt. Gvt. Fund, 5.29% | 989,060 | 989,060 | ||||||

|

| |||||||

Total Investments in Securities - 99.9% | 48,204,345 | |||||||

Other Assets and Liabilities, net - 0.1% | 66,411 | |||||||

|

| |||||||

Net Assets - 100.0% | $ | 48,270,756 | ||||||

|

| |||||||

| * | Non-income producing security. |

ADR — American Depositary Receipt |

PLC — Public Limited Company |

Numeric footnotes not disclosed are not applicable to this Schedule of Investments.

See accompanying notes to financial statements.

| 16 | SIT MUTUAL FUNDS SEMI-ANNUAL REPORT | |

A summary of the levels for the Fund’s investments as of December 31, 2023 is as follows (see Note 2 - significant accounting policies in the notes to financial statements):

| Investment in Securities | ||||||||||||||||

| Level 1 | Level 2 | Level 3 | ||||||||||||||

| Quoted | Other significant | Significant | ||||||||||||||

| Prices ($) | observable inputs ($) | unobservable inputs ($) | Total ($) | |||||||||||||

Common Stocks | ||||||||||||||||

Australia | 1,706,734 | — | — | 1,706,734 | ||||||||||||

France | 331,858 | — | — | 331,858 | ||||||||||||

Germany | 2,776,416 | — | — | 2,776,416 | ||||||||||||

Ireland | 2,264,503 | — | — | 2,264,503 | ||||||||||||

Japan | 797,439 | — | — | 797,439 | ||||||||||||

Singapore | 456,867 | — | — | 456,867 | ||||||||||||

Spain | 773,260 | — | — | 773,260 | ||||||||||||

Switzerland | 3,075,823 | — | — | 3,075,823 | ||||||||||||

United Kingdom | 6,642,047 | — | — | 6,642,047 | ||||||||||||

United States | 28,390,338 | — | — | 28,390,338 | ||||||||||||

Short-Term Securities | 989,060 | — | — | 989,060 | ||||||||||||

Total: | 48,204,345 | — | — | 48,204,345 | ||||||||||||

Level 1 securities of foreign issuers are primarily American Depositary Receipts (ADRs), Public Limited Companies (PLCs) or Global Depositary Receipts (GDRs). There were no transfers into or out of level 3 during the reporting period.

See accompanying notes to financial statements.

| DECEMBER 31, 2023 | 17 | |

OBJECTIVE & STRATEGY

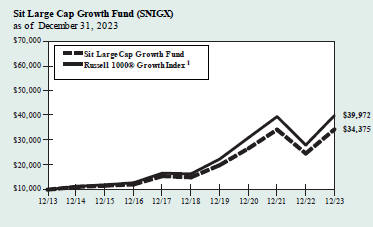

The objective of the Sit Large Cap Growth Fund is to maximize long-term capital appreciation. The Fund pursues this objective by investing, under normal market conditions, at least 80% of its net assets in the common stocks of domestic growth companies with capitalizations of $5 billion or more at the time of purchase.

Fund Performance

The Sit Large Cap Growth Fund’s return was +10.46% during the 6-month period ended December 31, 2023, compared to a +10.59% return for the Russell 1000® Growth Index. The S&P 500® Index return for the period was +8.04%.

Factors that Influenced the Fund’s Performance

The Fund posted strong, positive returns, that were in line with the Russell 1000® Growth Index during the period. The largest contributor to positive performance was an underweight allocation and stock selection in the consumer durables sector, where the Fund’s holdings (+27% sector return) outperformed the benchmark’s return (-5%). Key holdings here were Yeti and Activision Blizzard, which was acquired by Microsoft. The Fund was also helped by strong stock selection in the electronic technology sector. Its position in Broadcom, which benefited from increasing spending surrounding artificial intelligence, was a key holding. Palo Alto Networks was another important holding in this sector, as the company continues to benefit from strong cybersecurity spending. Finally, stock selection in the retail trade sector augmented returns. Holdings here were supported by a resilient consumer, with Lululemon representing one of the Fund’s strongest holdings during the period. While being underweight the health technology sector helped returns, stock selection in this sector detracted from performance. An overweight position in the consumer non-durables sector and stock selection within the sector also detracted from returns.

Outlook and Positioning

Investors entered 2023 in full “risk-on” mode, hopeful that the Federal Reserve would begin cutting rates by midyear and the economy would achieve a soft landing (or only a mild recession). Yet, stronger-than-expected inflation and jobs data dashed those hopes in February, and investors became fearful the Fed would continue tightening, which caused a rotation to “risk-off.” Equity investors repeated several iterations of this pattern during the year, but enthusiasm for artificial intelligence (AI) companies remained a prominent theme. The AI craze drove extraordinary gains for a handful of stocks dubbed the “Magnificent Seven” (M7) – Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla. These seven stocks generated a cap-weighted price return of +76.8% in 2023, while the other 493 stocks in the S&P 500® Index (as a group) returned +11.5%. Strong relative earnings growth explains much of the

HYPOTHETICAL GROWTH OF $10,000

The chart above illustrates the total value of a hypothetical $10,000 investment in the Fund over the past 10 years as compared to the performance of the Russell 1000® Growth Index. Past performance does not guarantee future results. Returns include the reinvestment of distributions. The chart does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

1 Russell 1000® Growth Index is an unmanaged index that measures the performance of those Russell 1000 Index companies with higher price-to-book ratios and higher forecasted growth values. It is not possible to invest directly in an index. This is the Fund’s primary index.

M7’s stock price outperformance in 2023, though valuation multiple expansion also played a role. However, given comparatively tepid earnings expectations and attractive valuations for many other companies, we believe the tide may shift in favor of the “other 493” in the S&P 500®. Still-high economic uncertainty, elevated policy/geopolitical risks, and “fair” equity valuations support our quality bias within a better environment for stock pickers in 2024. We generally maintain positions in the most attractive M7 stocks but also see compelling opportunities in other technology segments, including semiconductors, software/services, and cybersecurity. In addition to technology, early cycle and rate-sensitive sectors should fare well in the year ahead. Transportation companies, for example, have been struggling with excess customer inventories and cost pressures, but pricing has remained solid and the freight backdrop is set to rebound in 2024. Sentiment is also broadly improving for financial stocks. We see the most attractive opportunities for a strong rebound in capital markets businesses, given pent-up demand for initial public offerings, debt issuance, and M&A.

Roger J. Sit

Ronald D. Sit

Portfolio Managers

| 18 | SIT MUTUAL FUNDS SEMI-ANNUAL REPORT | |

|

COMPARATIVE RATES OF RETURNS

as of December 31, 2023

| Sit Large Cap Growth Fund | Russell 1000® Growth Index1 | Russell 1000® Index2 | ||||||||||

Six Month | 10.46 | % | 10.59% | 8.44 | % | |||||||

One Year | 39.69 | 42.68 | 26.53 | |||||||||

Five Year | 18.06 | 19.50 | 15.52 | |||||||||

Ten Year | 13.14 | 14.86 | 11.80 | |||||||||

Since Inception 3 | 10.78 | 12.00 | 11.92 | |||||||||

(9/2/82) | ||||||||||||

Performance figures are historical and do not guarantee future results. Investment returns and principal value will vary, and you may have a gain or loss when you sell shares. Current performance may be lower or higher than the performance data quoted. Contact the Fund for performance data current to the most recent month-end. Returns include changes in share price as well as reinvestment of all dividends and capital gains. Returns do not reflect the deduction of the 2% redemption fee imposed if shares are redeemed or exchanged within 30 calendar days from their date of purchase. If imposed, the fee would reduce the performance quoted. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Management fees and administrative expenses are included in the Fund’s performance. Returns for periods greater than one year are compounded average annual rates of return.

1 Russell 1000® Growth Index is an unmanaged index that measures the performance of those Russell 1000 Index companies with higher price-to-book ratios and higher forecasted growth values. It is not possible to invest directly in an index.

2 Russell 1000® Index is an unmanaged index that measures the performance of approximately 1,000 of the largest U.S. companies by market capitalization.

3 On 6/6/93, the Fund’s investment objective changed to allow for a portfolio of 100% stocks. Prior to that time, the portfolio was required to contain no more than 80% stocks.

PORTFOLIO SUMMARY

Net Asset Value 12/31/23: | $63.18 Per Share | |

Net Asset Value 6/30/23: | $58.26 Per Share | |

Net Assets: | $176.7 Million | |

Weighted Average Market Cap: | $1043.2 Billion |

TOP HOLDINGS

| 1. | Microsoft Corp. | |||

| 2. | Apple, Inc. | |||

| 3. | Alphabet, Inc. | |||

| 4. | NVIDIA Corp. | |||

| 5. | Amazon.com, Inc. | |||

| 6. | Broadcom, Inc. | |||

| 7. | UnitedHealth Group, Inc. | |||

| 8. | salesforce.com, Inc. | |||

| 9. | Adobe, Inc. | |||

| 10. | Applied Materials, Inc. | |||

Based on net assets as of December 31, 2023.

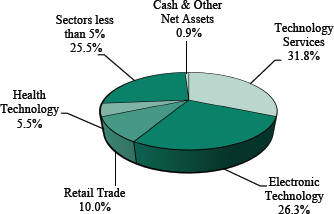

SECTOR ALLOCATION

Based on net assets as of December 31, 2023.

| DECEMBER 31, 2023 | 19 | |

SCHEDULE OF INVESTMENTS (Unaudited)

December 31, 2023

Sit Large Cap Growth Fund

Investments are grouped by economic sectors.

| Name of Issuer | Quantity | Fair Value ($) | ||||||

Common Stocks - 99.1% | ||||||||

Consumer Durables - 0.5% | ||||||||

YETI Holdings, Inc. * | 17,000 | 880,260 | ||||||

|

| |||||||

Consumer Non-Durables - 3.1% | ||||||||

Constellation Brands, Inc. | 7,425 | 1,794,994 | ||||||

Mondelez International, Inc. | 12,850 | 930,726 | ||||||

NIKE, Inc. | 9,050 | 982,558 | ||||||

PepsiCo, Inc. | 10,000 | 1,698,400 | ||||||

|

| |||||||