UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

(Amendment No. )

Filed by the Registrant ☒ Filed by a Party other than the Registrant ☐

Check the appropriate box:

| ☐ | Preliminary Proxy Statement | |

| ☐ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | |

| ☒ | Definitive Proxy Statement | |

| ☐ | Definitive Additional Materials | |

| ☐ | Soliciting Material Under §240.14a-12 | |

Nuveen Texas Quality Municipal Income Fund

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| ☒ | No fee required. | |||

| ☐ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | |||

| (1) | Title of each class of securities to which transaction applies:

| |||

| (2) | Aggregate number of securities to which transaction applies:

| |||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined):

| |||

| (4) | Proposed maximum aggregate value of transaction:

| |||

| (5) | Total fee paid:

| |||

| ☐ | Fee paid previously with preliminary materials. | |||

| ☐ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | |||

| (1) | Amount Previously Paid:

| |||

| (2) | Form, Schedule or Registration Statement No.:

| |||

| (3) | Filing Party:

| |||

| (4) | Date Filed:

| |||

IMPORTANT NOTICE TO SHAREHOLDERS OF

MUNIFUND PREFERRED SHARES OF

NUVEEN TEXAS QUALITY MUNICIPAL INCOME FUND (NTX)

AUGUST 9, 2019

Although we recommend that you read the complete Proxy Statement, for your convenience, we have provided a brief overview of the proposal to be voted on.

| Q. | Why am I receiving the enclosed Proxy Statement? |

| A. | You are receiving the Proxy Statement as a holder of MuniFund Preferred Shares (“MFP Shares”) of Nuveen Texas Quality Municipal Income Fund (the “Target Fund”) in connection with a special meeting of shareholders of the Target Fund (the “Special Meeting”). At the Special Meeting, shareholders of the Target Fund will be asked to vote on an Agreement and Plan of Reorganization (the “Proposal”) under which the Target Fund will transfer substantially all of its assets and liabilities to Nuveen Quality Municipal Income Fund (the “Acquiring Fund”) in exchange for newly issued common and preferred shares of the Acquiring Fund (the “Reorganization”). The Acquiring Fund and the Target Fund are collectively referred to herein as the “Funds,” and each, a “Fund.” |

The Target Fund’s Board of Trustees (the “Target Fund’s Board”), including the independent Board members, unanimously recommends that you vote FOR the Proposal. |

| Q. | Why has the Target Fund’s Board recommended the Proposal? |

| A. | Nuveen Fund Advisors, LLC (“Nuveen Fund Advisors”), a subsidiary of Nuveen, LLC (“Nuveen”) and the Funds’ investment adviser, recommended the proposed Reorganization as part of an ongoing initiative to rationalize the product offerings of Nuveen’s municipalclosed-end funds. Based on information provided by Nuveen Fund Advisors, the Target Fund’s Board believes that the proposed Reorganization may benefit common shareholders of the Target Fund in a number of ways, including, among other things: |

| • | The potential for higher common share net earnings, due in part to the Acquiring Fund’s larger exposure to lower rated securities (or “junk bonds”) which are subject to higher risk, as well as operating economies from the Acquiring Fund’s greater scale; |

| • | Greater secondary market liquidity and improved secondary market trading for common shares as a result of the combined fund’s greater share volume, which may lead to narrowerbid-ask spreads and smallertrade-to-trade price movements; |

| • | Increased portfolio and leverage management flexibility due to the significantly larger asset base of the combined fund and the Acquiring Fund’s national mandate with greater flexibility to invest in lower rated securities; and |

| • | Lower net operating expenses excluding the cost of leverage, as certain fixed costs are spread over a larger asset base and a lower management fee for Target Fund shareholders due to breakpoints in the Acquiring Fund’s fee schedule (as discussed in more detail below, total expenses including leverage are expected to be higher for the combined fund due to different amounts of leverage). |

With respect to holders of preferred shares of the Target Fund, the Target Fund’s Board considered that, upon the closing of the Reorganization, holders of the MFP Shares of the Target Fund will receive, on aone-for-one basis, newly issued MFP Shares of the Acquiring Fund having substantially similar terms, as of the closing of the Reorganization, as the MFP Shares exchanged therefor. |

For these reasons, the Target Fund’s Board has determined that the Reorganization would be in the best interests of the Target Fund and has approved the Reorganization. |

Based on information provided by Nuveen Fund Advisors, the Acquiring Fund’s Board considered that the Acquiring Fund may benefit in the near term from a modest increase in operating efficiencies and over the long term from increased investment capital, which allows the Acquiring Fund to pursue additional investment opportunities. With respect to holders of preferred shares of the Acquiring Fund, the Acquiring Fund’s Board considered that the outstanding preferred shares of the Acquiring Fund and the preferred shares of the Acquiring Fund to be issued in the Reorganization would have equal priority with each other as to the payment of dividends and distributions of assets upon dissolution, liquidation or winding up of the affairs of the Acquiring Fund. |

| Q. | How will holders of MFP Shares be affected by the Reorganization? |

| A. | The Acquiring Fund has one series of MFP Shares outstanding, two series of Adjustable Rate MuniFund Term Preferred Shares (“AMTP Shares��) and three series of Variable Rate Demand Preferred Shares (“VRDP Shares”) outstanding. The Target Fund has one series of MFP Shares outstanding. Upon the closing of the Reorganization, holders of MFP Shares of the Target Fund will receive, on aone-for-one basis, newly issued MFP Shares of the Acquiring Fund having substantially similar terms, as of the closing of the Reorganization, as the MFP Shares of the Target Fund exchanged therefor. The outstanding preferred shares of the Acquiring Fund and the preferred shares to be issued by the Acquiring Fund in the Reorganization will have equal priority with each other and with any other preferred shares that the Acquiring Fund may issue in the future as to the payment of dividends and the distribution of assets upon the dissolution, liquidation or winding up of the affairs of the Acquiring Fund. |

Following the Reorganization, holders of MFP Shares of the combined fund received in exchange for MFP Shares of the Target Fund will hold a smaller percentage of the outstanding preferred shares of the combined fund as compared to their percentage holdings of preferred shares of the Target Fund prior to the Reorganization. Additionally, the combined fund will have multiple series and types of preferred shares outstanding, while the Target Fund has one series of preferred shares outstanding. The different types of preferred shares have different characteristics and features, which are described in more detail in the Proxy Statement. See “Information About the Reorganization—Description of MFP Shares to Be Issued by the Acquiring Fund” beginning on page 31, “Additional Information About the Acquiring Fund—Description of Outstanding Acquiring Fund MFP Shares” beginning on page 46, “Additional |

ii

| Information the Acquiring Fund—Description of Outstanding Acquiring Fund AMTP Shares” beginning on page 48, and “Additional Information About the Acquiring Fund—Description of Outstanding Acquiring Fund VRDP Shares” beginning on page 50. In addition, the voting power of certain series of preferred shares may be more concentrated than others. |

| Q. | Will the terms of the MFP Shares to be issued by the Acquiring Fund as part of the Reorganization be substantially similar to the terms of the Target Fund’s MFP Shares outstanding as of immediately prior to the closing of the Reorganization? |

| A. | Yes. The terms of the MFP Shares to be issued by the Acquiring Fund as part of the Reorganization will be substantially similar, as of the closing of the Reorganization, to the terms of the Target Fund’s MFP Shares outstanding as of immediately prior to the closing of the Reorganization, including the same: |

| • | dividend rate and dividend determination method, including applicable spread adjustments, and dividend amount adjustment provisions; |

| • | mandatory and optional redemption terms, including the same term redemption date; |

| • | voting and consent rights; and |

| • | information delivery rights. |

| Q. | Do the Funds have similar investment objectives, policies and risks? |

| A. | Both Funds seek to providetax-exempt current income by investing primarily in municipal securities. However, there are material differences between the investment objectives, policies and risks of the Funds. The principal similarities and differences between the Funds’ investment objectives, policies and risks are as follows: |

| • | Both Funds seek current income exempt from regular federal income tax. |

| • | The Target Fund invests primarily in Texas municipal obligations and is subject to economic, political and other risks of a single state, while the Acquiring Fund may invest in municipal obligations of any U.S. state or territory. |

| • | Each Fund may invest up to 20% of its managed assets in municipal securities which pay interest that is subject to the federal alternative minimum tax applicable to individuals. |

| • | The Target Fund invests primarily in investment-grade securities, while the Acquiring Fund may invest up to 35% of its managed assets in securities rated, at the time of investment, below the three highest grades (Baa or BBB or lower) by at least one nationally recognized statistical rating organization. |

| • | Each Fund is a diversified,closed-end management investment company and currently employs leverage through the issuance of preferred shares and the use of inverse floating rate securities. |

iii

See “A. Synopsis—Comparison of the Acquiring Fund and the Target Fund—Investment Objectives and Policies” and “A. Synopsis—Comparative Risk Information” for more information. |

| Q. | Will holders of MFP Shares have to pay any fees or expenses in connection with the Reorganization? |

| A. | No. The Target Fund, and indirectly its common shareholders, will bear the costs of the Reorganization, whether or not the Reorganization is consummated. Preferred shareholders will not bear any costs of the Reorganization. The allocation of the costs of the Reorganization to the Target Fund is based on the expected benefits of the Reorganization, including forecasted increases to net earnings, improvements in the secondary trading market for common shares and operating expense savings, if any, to Target Fund shareholders following the Reorganization. |

The total costs of the Reorganization are estimated to be $475,000 (0.32% of average net assets attributable to the Target Fund’s common shares for thesix-month period ended April 30, 2019) and such costs will be reflected in the Target Fund’s net asset value at or before the close of trading on the business day immediately prior to the closing of the Reorganization. If the Reorganization is not consummated for any reason, including because the requisite shareholder approvals are not obtained, the Target Fund, and common shareholders of the Target Fund indirectly, will still bear the costs of the Reorganization. |

A Target Fund shareholder’s broker, dealer or other financial intermediary (each, a “Financial Intermediary”) may impose its own shareholder account fees for processing corporate actions, which could apply as a result of the Reorganization. These shareholder account fees, if applicable, are not paid or otherwise remitted to the Funds or the Funds’ investment adviser. The imposition of such fees is based solely on the terms of a shareholder’s account agreement with his, her or its Financial Intermediary and/or is in the discretion of the Financial Intermediary. Questions concerning any such shareholder account fees or other similar fees should be directed to a shareholder’s Financial Intermediary. |

| Q. | Does the Reorganization constitute a taxable event for the Target Fund’s shareholders? |

| A. | No. The Reorganization is intended to qualify as atax-free “reorganization” for federal income tax purposes. It is expected that Target Fund shareholders will recognize no gain or loss for federal income tax purposes as a direct result of the Reorganization, except to the extent that a Target Fund common shareholder receives cash in lieu of a fractional Acquiring Fund common share. Prior to the closing of the Reorganization, the Target Fund expects to declare a distribution of all of its net investment income and net capital gains, if any. All or a portion of such distribution may be taxable to the Target Fund’s shareholders for federal income tax purposes. Prior to the closing of the Reorganization, the Target Fund is expected to sell certain municipal securities in its portfolio. Such sales are not expected to be material (less than 5% of the assets of the Target Fund). To the extent that portfolio securities of the Target Fund are sold prior to the closing of the Reorganization, the Target Fund may realize gains or losses, which may increase or decrease the net capital gains or net investment income to be distributed by the Target Fund. |

iv

| Q. | What will happen if the required shareholder approvals are not obtained? |

| A. | The closing of the Reorganization is subject to the satisfaction or waiver of certain closing conditions, which include customary closing conditions. In order for the Reorganization to occur, all requisite shareholder approvals must be obtained, and certain other consents, confirmations and/or waivers from various third parties, including liquidity providers with respect to the outstanding VRDP Shares of the Acquiring Fund, also must be obtained. Because the closing of the Reorganization is contingent upon each of the Acquiring Fund and Target Fund obtaining such shareholder approvals and satisfying (or obtaining the waiver of) other closing conditions, it is possible that the Reorganization will not occur, even if shareholders of the Target Fund entitled to vote approve the Proposal and the Target Fund satisfies all of its closing conditions, if the Acquiring Fund does not obtain its requisite shareholder approvals or satisfy (or obtain the waiver of) its closing conditions. If the Reorganization is not consummated, each Fund’s Board may take such actions as it deems in the best interests of its Fund, including conducting additional solicitations with respect to the Proposal or, with respect to the Target Fund’s Board, continuing to operate the Target Fund as a standalone fund. |

Each series of preferred shares was issued on a private placement basis to one or a small number of institutional holders. To the extent that one or more preferred shareholders of a Fund owns, holds or controls, individually or in the aggregate, all or a significant portion of a Fund’s outstanding preferred shares, one or more shareholder approvals required for the Reorganization to occur may turn on the exercise of voting or consent rights by such particular shareholder(s) and its or their determination as to the favorable view of the Reorganization with respect to its or their interests. The Funds exercise no influence or control over the determinations of such shareholders with respect to the Proposal; there is no guarantee that such shareholders will approve the Proposal over which they may exercise effective disposition power. |

| Q. | What is the timetable for the Reorganization? |

| A. | If the shareholder approvals and other conditions to closing are satisfied (or waived), the Reorganization is expected to take effect on or about November 11, 2019 or as soon as practicable thereafter. |

| Q. | How does the Board recommend that shareholders vote on the Reorganization? |

| A. | After careful consideration, each Board has determined that the Reorganization is in the best interests of its Fund and recommends that holders of MFP Shares vote FOR the Proposal. |

| Q. | Who do I call if I have questions? |

| A. | If you need any assistance, or have any questions regarding the Proposal or how to vote your shares, please call Computershare Fund Services, the proxy solicitor hired by your Fund, at1-866-905-8143 weekdays during its business hours of 9:00 a.m. to 11:00 p.m. and Saturdays 12:00 p.m. to 6:00 p.m. Eastern time. Please have your proxy materials available when you call. |

v

| Q. | How do I vote my shares? |

| A. | You may vote by mail, by telephone or over the Internet: |

| • | To vote by mail, please mark, sign, date and mail the enclosed proxy card. No postage is required if mailed in the United States. |

| • | To vote by telephone, please call the toll-free number located on your proxy card and follow the recorded instructions, using your proxy card as a guide. |

| • | To vote over the Internet, go to the Internet address provided on your proxy card and follow the instructions, using your proxy card as a guide. |

| • | To vote in person, if you own shares directly with the Target Fund, you may attend the Special Meeting and vote in person, or you may execute a proxy designating a representative to attend the Special Meeting and vote on your behalf. If you own shares in “street name” through a broker or nominee, you may attend the Special Meeting and vote in person only if you obtain a proxy from your broker or nominee in advance of the Special Meeting and bring it with you to hand in along with the ballot that will be provided. The date, time and location of the Special Meeting is set forth on the enclosed notice of meeting for the Target Fund. |

| Q. | Will anyone contact me? |

| A. | You may receive a call from Computershare Fund Services, the proxy solicitor hired by the Target Fund, to verify that you received your proxy materials, to answer any questions you may have about the Proposal and to encourage you to vote your proxy. |

We recognize the inconvenience of the proxy solicitation process and would not impose on you if we did not believe that the matter being proposed was important. Once your vote has been registered with the proxy solicitor, your name will be removed from the solicitor’sfollow-up contact list. |

Your vote is very important. We encourage you as a shareholder to participate in your Fund’s governance by returning your vote as soon as possible. If enough shareholders fail to cast their votes, the Target Fund may not be able to hold the Special Meeting or the vote on the Proposal, and will be required to incur additional solicitation costs in order to obtain sufficient shareholder participation. |

vi

AUGUST 9, 2019

NUVEEN TEXAS QUALITY MUNICIPAL INCOME FUND (NTX)

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS

TO BE HELD ON SEPTEMBER 23, 2019

To the Holders of MuniFund Term Preferred Shares:

Notice is hereby given that a Special Meeting of Shareholders (the “Special Meeting”) of Nuveen Texas Quality Municipal Income Fund (the “Target Fund”) will be held at the offices of Nuveen, LLC, 333 West Wacker Drive, Chicago, Illinois 60606, on Monday, September 23, 2019 at 2:00 p.m. Central time, for the following purposes:

Agreement and Plan of Reorganization. The shareholders of the Target Fund voting as set forth below will vote on a proposal to approve an Agreement and Plan of Reorganization pursuant to which the Target Fund would: (i) transfer substantially all of its assets to Nuveen Quality Municipal Income Fund (the “Acquiring Fund”) in exchange solely for newly issued common shares and preferred shares of the Acquiring Fund and the Acquiring Fund’s assumption of substantially all of the liabilities of the Target Fund; (ii) distribute such newly issued shares of the Acquiring Fund to the common shareholders and preferred shareholders of the Target Fund; and (iii) liquidate, dissolve and terminate in accordance with applicable law. |

| (a) | The common and preferred shareholders voting together as a single class to approve the Agreement and Plan of Reorganization. |

| (b) | The preferred shareholders voting together as a single class to approve the Agreement and Plan of Reorganization. |

To transact such other business as may properly come before the Special Meeting.

Only shareholders of record of the Funds as of the close of business on June 25, 2019 are entitled to notice of and to vote at the Special Meeting and any and all adjournments or postponements thereof. The common shareholders of the Target Fund and the preferred shareholders of the Acquiring Fund are being solicited to vote on the proposal described above by means of a separate joint proxy statement/prospectus.

All Fund shareholders are cordially invited to attend the Special Meeting. In order to avoid delay and additional expense for the Funds and to assure that your shares are represented, please vote as promptly as possible, regardless of whether or not you plan to attend the Special Meeting. You may vote by mail, by telephone or over the Internet.

| • | To vote by mail, please mark, sign, date and mail the enclosed proxy card. No postage is required if mailed in the United States. |

| • | To vote by telephone, please call the toll-free number located on your proxy card and follow the recorded instructions, using your proxy card as a guide. |

| • | To vote over the Internet, go to the Internet address provided on your proxy card and follow the instructions, using your proxy card as a guide. |

1

If you intend to attend the Special Meeting in person and you are a record holder of Target Fund shares, in order to gain admission you must show photographic identification, such as your driver’s license. If you intend to attend the Special Meeting in person and you hold your shares through a bank, broker or other custodian, in order to gain admission you must show photographic identification, such as your driver’s license, and satisfactory proof of ownership of shares of the Fund, such as your voting instruction form (or a copy thereof) or broker’s statement indicating ownership as of a recent date. If you hold your shares in a brokerage account or through a bank or other nominee, you will not be able to vote in person at the Special Meeting unless you have previously requested and obtained a “legal proxy” from your broker, bank or other nominee and present it at the Special Meeting.

Gifford R. Zimmerman

Vice President and Secretary

The NuveenClosed-End Funds

2

NUVEEN FUNDS

333 WEST WACKER DRIVE

CHICAGO, ILLINOIS 60606

(800) 257-8787

PROXY STATEMENT

FOR HOLDERS OF MUNIFUND TERM PREFERRED SHARES

OF

NUVEEN TEXAS QUALITY MUNICIPAL INCOME FUND (NTX)

AUGUST 9, 2019

This Proxy Statement is being furnished by Nuveen Texas Quality Municipal Income Fund (the “Target Fund”) to holders of MuniFund Term Preferred Shares (“MFP Shares”) of the Target Fund in connection with the solicitation of proxies by the Board of Trustees (the “Target Fund’s Board,” and each of the Target Fund’s Board and the Board of Trustees of the Acquiring Fund (defined below) (the “Acquiring Fund’s Board”), a “Board” and together, the “Boards” and each trustee, a “Board Member”) of the Target Fund and Nuveen Quality Municipal Income Fund (the “Acquiring Fund”) (each a “Fund” and together, the “Funds”), for use at the Special Meeting of Shareholders of the Target Fund to be held at the offices of Nuveen, LLC (“Nuveen”), 333 West Wacker Drive, Chicago, Illinois 60606, on Monday, September 23, 2019 at 2:00 p.m. Central time, and at any and all adjournments or postponements thereof (the “Special Meeting”), to consider the proposal described below and discussed in greater detail elsewhere in this Proxy Statement. The Acquiring Fund and Target Fund are organized as Massachusetts business trusts. The enclosed proxy card and this Proxy Statement are first being sent to holders of MFP Shares on or about August 13, 2019. Shareholders of record of the Target Fund as of the close of business on June 25, 2019 are entitled to notice of and to vote at the Special Meeting and any and all adjournments or postponements thereof.

This Proxy Statement explains concisely what you should know before voting on the proposal described in this Proxy Statement or investing in the Acquiring Fund. Please read it carefully and keep it for future reference.

On the matter coming before the Special Meeting as to which a choice has been specified by shareholders on the accompanying proxy card, the shares will be voted accordingly where such proxy card is properly executed, timely received and not properly revoked (pursuant to the instructions below). If a proxy is returned and no choice is specified, the shares will be votedFOR the proposal. Shareholders of the Target Fund who execute proxies or provide voting instructions by telephone or by Internet may revoke them at any time before a vote is taken on the proposal by filing with the Fund a written notice of revocation, by delivering a duly executed proxy bearing a later date or by attending the Special Meeting and voting in person. A prior proxy can also be revoked by voting again through the toll-free number or the Internet address listed in the proxy card. However, merely attending the Special Meeting will not revoke any previously submitted proxy.

Pursuant to this Proxy Statement, holders of MFP Shares of the Target Fund are being solicited to vote on a proposal to approve an Agreement and Plan of Reorganization pursuant to which the Target Fund would: (i) transfer substantially all of its assets to the Acquiring Fund in exchange solely for newly issued common shares and preferred shares of the Acquiring Fund and the Acquiring Fund’s assumption of substantially all of the liabilities of the Target Fund; (ii) distribute such newly issued

shares of the Acquiring Fund to the common shareholders and preferred shareholders of the Target Fund; and (iii) liquidate, dissolve and terminate in accordance with applicable law (the “Reorganization”).

In addition to its common shares, each Fund has one or more series of preferred shares outstanding. The Acquiring Fund has one series of MFP Shares, three series of Variable Rate Demand Preferred Shares (“VRDP Shares”) and two series of Adjustable Rate MuniFund Term Preferred Shares (“AMTP Shares”) outstanding. The Target Fund has one series of MFP Shares outstanding.

To be approved, the proposal must be approved by the Funds’ common and preferred shareholders as follows:

| • | With respect to the Target Fund, the proposal must be approved by the Target Fund’s common and preferred shareholders voting together as a single class and by the Target Fund’s preferred shareholders voting separately. |

| • | With respect to the Acquiring Fund, the proposal must be approved by the Acquiring Fund’s preferred shareholders voting together as a single class. |

Only holders of MFP Shares of the Target Fund are being solicited to vote on the proposal described above pursuant to this Proxy Statement. The common shareholders of the Target Fund and preferred shareholders of the Acquiring Fund are being solicited to vote on the proposal described above by means of a separate joint proxy statement/prospectus.

A quorum of shareholders is required to take action at the Special Meeting. A majority of the shares entitled to vote at the Special Meeting, represented in person or by proxy, will constitute a quorum of shareholders at the Special Meeting. Votes cast in person or by proxy at the Special Meeting will be tabulated by the inspectors of election appointed for the Special Meeting. The inspectors of election will determine whether or not a quorum is present at the Special Meeting. “Brokernon-votes” are shares held by brokers or nominees, typically in “street name,” for which instructions have not been received from beneficial owners or persons entitled to vote and the broker or nominee returns a valid proxy but are not voted because the broker or nominee does not have discretionary authority to vote such shares on a particular matter. For purposes of voting on the proposal, abstentions and brokernon-votes, if any, will be counted as present for purposes of determining whether a quorum is present.

Broker-dealer firms holding shares of a Fund in “street name” for the benefit of their customers and clients will request the instructions of such customers and clients on how to vote their shares before the Fund’s Special Meeting. The Target Fund understands that, under the rules of the New York Stock Exchange (the “NYSE”), such broker-dealer firms may, for certain “routine” matters, grant discretionary authority to the proxies designated by each Board to vote without instructions from their customers and clients if no instructions have been received prior to the date specified in the broker-dealer firm’s request for voting instructions. The proposal described in this Proxy Statement is considered a“non-routine” matter for which, under the rules of the NYSE, uninstructed shares may not be voted by broker-dealers. Because the approval of the proposal requires that a minimum percentage of the Target Fund’s outstanding common shares and preferred shares and the Acquiring Fund’s preferred shares be voted in favor of the proposal, abstentions and brokernon-votes will have the same effect as a vote against the proposal.

ii

Those persons who were shareholders of record of MFP Shares of the Target Fund as of the close of business on June 25, 2019 will be entitled to one vote for each share held.

As of June 25, 2019, the shares of the Funds issued and outstanding are as follows:

Fund | Common Shares(1) | MFP Shares | VRDP Shares | AMTP Shares | ||||||

Acquiring Fund (NAD) | 201,864,367 | 6,070 (Series A) | 2,368 (Series 1) 2,675 (Series 2) 1,277 (Series 3) | 3,370 (Series 2028) 2,085 (Series 2028-1) | ||||||

Target Fund (NTX) | 9,958,610 | 720 (Series A) | — | — | ||||||

| (1) | The common shares of the Acquiring Fund and Target Fund are listed on the NYSE. Upon the closing of the Reorganization, it is expected that the common shares of the Acquiring Fund will continue to be listed on the NYSE. None of the preferred shares are currently listed on any exchange. |

The proposed Reorganization is part of an ongoing initiative to rationalize the product offerings of Nuveen’s municipalclosed-end funds. The Acquiring Fund and the Target Fund invest exclusively in municipal securities and other investments the income from which is exempt from regular federal income taxes; however, the Target Fund concentrates its investment portfolio in Texas state-specific, investment-grade municipal securities in comparison to the Acquiring Fund’s policy of investing in a nationally diversified portfolio of medium-credit municipal securities.

iii

PROXY STATEMENT

AUGUST 9, 2019

NUVEEN TEXAS QUALITY MUNICIPAL INCOME FUND (NTX)

iv

| Page | ||||||

| 60 | ||||||

| 61 | ||||||

| A-1 | ||||||

| B-1 | ||||||

v

PROPOSAL—REORGANIZATION OF THE TARGET FUND INTO THE ACQUIRING FUND

| A. | SYNOPSIS |

The following is a summary of certain information contained elsewhere in this Proxy Statement with respect to the proposed Reorganization. More complete information is contained elsewhere in this Proxy Statement and the appendices hereto and thereto. Shareholders should read the entire Proxy Statement carefully.

Background and Reasons for the Reorganization

The Target Fund’s Board has approved the Reorganization as part of an ongoing initiative to rationalize the product offerings of Nuveen funds. The Board considered the Reorganization in connection with this initiative and determined that the Reorganization would be in the best interests of the Target Fund. The Acquiring Fund and the Target Fund each invest exclusively in municipal securities and other investments the income from which is exempt from federal income tax; however, the Target Fund concentrates its investment portfolio in Texas state-specific, investment-grade municipal securities in comparison to the Acquiring Fund’s policy of investing in a nationally diversified portfolio of medium-credit municipal securities.

Based on information provided by Nuveen Fund Advisors, LLC (“Nuveen Fund Advisors” or the “Adviser”), the investment adviser to each Fund, the Target Fund’s Board believes that the Reorganization may benefit common shareholders in a number of ways, including, among other things:

| • | The potential for higher common share net earnings due in part to the Acquiring Fund’s larger exposure to lower rated securities (or “junk bonds”) which are subject to higher risk, as well as operating economies from the Acquiring Fund’s greater scale; |

| • | Greater secondary market liquidity and improved secondary market trading for common shares as a result of the combined fund’s greater share volume, which may lead to narrowerbid-ask spreads and smallertrade-to-trade price movements; |

| • | Increased portfolio and leverage management flexibility due to the significantly larger asset base of the combined fund and the Acquiring Fund’s national mandate with greater flexibility to invest in lower rated securities; and |

| • | Lower net operating expenses excluding the cost of leverage, as certain fixed costs are spread over a larger asset base and a lower management fee for Target Fund shareholders due to breakpoints in the Acquiring Fund’s fee schedule (however, total expenses including leverage are expected to be higher for the combined fund due to differences in the amounts of leverage). |

With respect to outstanding preferred shares of the Target Fund, the Target Fund’s Board considered that, upon the closing of the Reorganization, holders of the MFP Shares of the Target Fund will receive, on aone-for-one basis, newly issued MFP Shares of the Acquiring Fund having substantially similar terms, as of the closing of the Reorganization, as the MFP Shares exchanged therefor.

1

Based on information provided by Nuveen Fund Advisors, the Acquiring Fund’s Board considered that the Acquiring Fund may benefit in the near term from a modest increase in operating efficiencies and over the long term from increased investment capital, which allows the Acquiring Fund to pursue additional investment opportunities. With respect to holders of preferred shares of the Acquiring Fund, the Acquiring Fund’s Board considered that the outstanding preferred shares of the Acquiring Fund and the preferred shares of the Acquiring Fund to be issued in the Reorganization would have equal priority with each other as to the payment of dividends and distributions of assets upon dissolution, liquidation or winding up of the affairs of the Acquiring Fund.

The closing of the Reorganization is subject to the satisfaction or waiver of certain closing conditions, which include customary closing conditions. In order for the Reorganization to occur, all requisite shareholder approvals must be obtained, and certain other consents, confirmations and/or waivers must also be obtained from various third parties, including liquidity providers with respect to the outstanding VRDP Shares. Because the closing of the Reorganization is contingent upon each of the Target Fund and the Acquiring Fund obtaining such shareholder approvals and satisfying (or obtaining the waiver of) other closing conditions, it is possible that the Reorganization will not occur, even if shareholders of a Fund entitled to vote approve the Reorganization proposal and the Fund satisfies all of its closing conditions, if the other Fund does not obtain its requisite shareholder approvals or satisfy (or obtain the waiver of) its closing conditions.

Each series of MFP Shares, VRDP Shares and AMTP Shares was issued on a private placement basis to one or a small number of institutional holders. To the extent that one or more preferred shareholders of a Fund owns, holds or controls, individually or in the aggregate, all or a significant portion of a Fund’s outstanding preferred shares, one or more shareholder approvals required for the Reorganization may turn on the exercise of voting rights by such particular shareholder(s) and its or their determination as to the favorable view of the Reorganization with respect to its or their interests. The Funds exercise no influence or control over the determinations of such shareholders with respect to the proposal; there is no guarantee that such shareholders will approve the proposal over which they may exercise effective disposition power. If the Reorganization is not consummated, each Fund’s Board may take such actions as it deems in the best interests of its Fund including conducting additional solicitations with respect to the proposal or, with respect to the Target Fund’s Board, continuing to operate as a stand-alone fund. For a fuller discussion of the Boards’ considerations regarding the approval of the Reorganization, see “Information about the Reorganization—Reasons for the Reorganization.”

Material Federal Income Tax Consequences of the Reorganization

As a condition to closing, each Fund will receive an opinion of Vedder Price P.C., subject to certain representations, assumptions and conditions, substantially to the effect that the proposed Reorganization will qualify as atax-free reorganization under Section 368(a) of the Internal Revenue Code of 1986, as amended (the “Code”). Accordingly, it is expected that neither Fund will recognize gain or loss for federal income tax purposes as a direct result of the Reorganization. It is also expected that shareholders of the Target Fund who receive Acquiring Fund shares pursuant to the Reorganization will recognize no gain or loss for federal income tax purposes as a result of such exchange, except to the extent a common shareholder of the Target Fund receives cash in lieu of a fractional Acquiring Fund common share. Prior to the closing of the Reorganization, the Target Fund expects to declare a distribution to common shareholders of all of its net investment income and net

2

capital gains, if any. All or a portion of such a distribution may be taxable to the Target Fund’s shareholders for federal income tax purposes. If shareholders of the Funds approve the Reorganization, prior to the closing of the Reorganization, the Target Fund is expected to sell certain municipal securities in its portfolio. Such sales are not expected to be material (less than 5% of the assets of the Target Fund). To the extent that portfolio securities of the Target Fund are sold prior to the closing of the Reorganization, the Target Fund may realize gains or losses, which may increase or decrease the net capital gains or net investment income to be distributed by the Target Fund.

The foregoing discussion and the tax opinion discussed above to be received by the Funds regarding certain aspects of the Reorganization, including that the Reorganization will qualify as atax-free reorganization under the Code, will rely on the position that the Acquiring Fund preferred shares will constitute equity of the Acquiring Fund. In that regard, Sidley Austin LLP, as special tax counsel to the Acquiring Fund, will deliver an opinion to the Acquiring Fund, subject to certain representations, assumptions and conditions, substantially to the effect that the Acquiring Fund MFP Shares received in the Reorganization by the holders of MFP Shares of the Target Fund will qualify as equity of the Acquiring Fund for federal income tax purposes. As a result, distributions with respect to the preferred shares (other than distributions in redemption of preferred shares subject to Section 302(b) of the Code) will generally constitute dividends to the extent of the Acquiring Fund’s allocable current or accumulated earnings and profits, as calculated for federal income tax purposes. Because the treatment of a corporate security as debt or equity is determined on the basis of the facts and circumstances of each case, and no controlling precedent exists for the preferred shares issued in the Reorganization, there can be no assurance that the IRS will not question special tax counsel’s opinion and the Acquiring Fund’s treatment of the preferred shares as equity. If the IRS were to succeed in such a challenge, holders of preferred shares could be characterized as receiving taxable interest income rather than exempt-interest or other dividends, possibly requiring them to file amended income tax returns and retroactively to recognize additional amounts of ordinary income and pay additional tax, interest and penalties, and the tax consequences of the Reorganization could differ significantly from those described in this Proxy Statement. See “Information about the Reorganization—Material Federal Income Tax Consequences of the Reorganization.”

Comparison of the Acquiring Fund and the Target Fund

General. The Acquiring Fund and the Target Fund are diversified,closed-end management investment companies. Set forth below is certain comparative information about the organization, capitalization and operation of the Funds.

Fund | Organization Date | State of Organization | Entity Type | |||||||

Acquiring Fund | January 15, 1999 | Commonwealth of Massachusetts | business trust | |||||||

Target Fund | July 26, 1991 | Commonwealth of Massachusetts | business trust | |||||||

Capitalization—Common Shares(1) | ||||||||||||||

Fund | Authorized Shares | Shares Outstanding(1) | Par Value Per Share | Preemptive, Conversion or Exchange Rights | Rights to Cumulative Voting | Exchange on which Common Shares Are Listed | ||||||||

Acquiring Fund | Unlimited | 201,864,367 | $0.01 | None | None | NYSE | ||||||||

Target Fund | Unlimited | 9,958,610 | $0.01 | None | None | NYSE | ||||||||

| (1) | As of June 25, 2019. |

3

Each Fund’s common shares are listed for trading on the NYSE.

The Funds currently have outstanding the following series of preferred shares, with the Acquiring Fund’s MFP Shares, VRDP Shares and AMTP Shares remaining outstanding following the completion of the Reorganization:

Acquiring Fund—Preferred Shares | ||||||||||||

Series | Shares Outstanding | Par Value Per Share | Liquidation Preference Per Share | |||||||||

Series A MFP Shares | 6,070 | $ | 0.01 | $ | 100,000 | |||||||

Series 1 VRDP Shares | 2,368 | $ | 0.01 | $ | 100,000 | |||||||

Series 2 VRDP Shares | 2,675 | $ | 0.01 | $ | 100,000 | |||||||

Series 3 VRDP Shares | 1,277 | $ | 0.01 | $ | 100,000 | |||||||

Series 2028 AMTP Shares | 3,370 | $ | 0.01 | $ | 100,000 | |||||||

Series2028-1 AMTP Shares | 2,085 | $ | 0.01 | $ | 100,000 | |||||||

Target Fund—Preferred Shares | ||||||||||||

Series | Shares Outstanding | Par Value Per Share | Liquidation Preference Per Share | |||||||||

Series A MFP Shares | 720 | $ | 0.01 | $ | 100,000 | |||||||

Each Fund’s preferred shares are entitled to one vote per share. The MFP Shares of the Acquiring Fund to be issued in connection with the Reorganization will have equal priority with each other and the Acquiring Fund’s other outstanding preferred shares as to the payment of dividends and the distribution of assets upon dissolution, liquidation or winding up of the affairs of the Acquiring Fund. In addition, the preferred shares of the Acquiring Fund, including MFP Shares of the Acquiring Fund to be issued in connection with the Reorganization, will be senior in priority to the Acquiring Fund’s common shares as to payment of dividends and the distribution of assets upon dissolution, liquidation or winding up of the affairs of the Acquiring Fund. The MFP Shares of the Acquiring Fund to be issued in connection with the Reorganization will have rights and preferences, including liquidation preferences, that are substantially similar to those of the outstanding Target Fund preferred shares for which they are exchanged.

Investment Objectives and Policies. The Funds have similar investment objectives, policies and risks but there are material differences. Each Fund seeks to provide current income exempt from regular federal income tax and each Fund also seeks to enhance portfolio value relative to the municipal bond market by investing intax-exempt municipal securities that the Funds’ investment adviser believes are underrated or undervalued or that represent municipal market sectors that are undervalued. However, the Acquiring Fund is a national municipal bond fund, while the Target Fund is a state bond fund investing primarily in Texas municipal obligations.

4

The following summary compares the current principal investment policies and strategies of the Acquiring Fund to the current principal investment policies and strategies of the Target Fund as of the date of this Proxy Statement.

Acquiring Fund | Target Fund | Differences | ||

Principal Investment Strategy:

Under normal circumstances, the Fund will invest at least 80% of its Assets(1) in municipal securities and other related investments, the income from which is exempt from regular federal income taxes. | Principal Investment Strategy:

Under normal circumstances, the Fund will invest at least 80% of its Assets(1) in Texas municipal obligations, including municipal securities and other related investments, the income from which is exempt from regular federal income tax. |

The Acquiring Fund is a national municipal fund, while the Target Fund is a state-specific municipal fund. | ||

Credit Quality:

Under normal circumstances, the Fund may invest up to 35% of its Managed Assets(2) in securities that, at the time of investment, are rated below the three highest grades (Baa or BBB or lower) by at least one nationally recognized statistical rating organization (“NRSRO”) or are unrated but judged to be of comparable quality by the Fund’ssub-adviser. | Credit Quality

Under normal circumstances, the Fund will invest at least 80% of its Managed Assets(2) in securities that, at the time of investment, are rated within the four highest grades (Baa or BBB or better) by at least one NRSRO or are unrated but judged to be of comparable quality by Nuveen Asset Management. The Fund may invest up to 20% of its Managed Assets in municipal securities that at the time of investment are rated below investment grade or are unrated but judged to be of comparable quality by Nuveen Asset Management. No more than 10% of the Fund’s Managed Assets may be invested in municipal securities rated belowB3/B- or that are unrated but judged to be of comparable quality by Nuveen Asset Management. |

The Acquiring Fund may invest up to 35% of its Managed Assets in below-investment-grade or unrated securities. The Target Fund may invest up to 20% of its Managed Assets in municipal securities rated below investment grade, of which up to 10% of its Managed Assets may be rated belowB-/B3 or of comparable quality. | ||

Alternative Minimum Tax Policy:

The Fund may invest up to 20% of its Managed Assets in municipal securities that pay interest that is taxable under the federal alternative minimum tax. | Alternative Minimum Tax Policy:

The Fund may invest up to 20% of its Managed Assets in municipal securities that pay interest that is taxable under the federal alternative minimum tax. |

Identical. | ||

Leverage:

The Fund may use leverage to the extent permitted by the 1940 Act. The Fund may source leverage | Leverage:

The Fund may utilize the following forms of leverage: (a) portfolio investments that have |

Substantially similar. The Acquiring Fund may enter into reverse repurchase agreements. | ||

5

Acquiring Fund | Target Fund | Differences | ||

through a number of methods including the issuance of preferred shares, investments in inverse floating rate securities, entering into reverse repurchase agreements (effectively a secured borrowing) and borrowings (subject to certain investment restrictions). | the economic effect of leverage, including but not limited to investments in futures, options and inverse floating rate securities, and (b) the issuance of preferred shares. The Fund may invest up to 15% of its Managed Assets in inverse floating rate securities. | |||

Illiquid Securities:

The Fund may invest in illiquid securities (i.e., securities that are not readily marketable), including, but not limited to, restricted securities (securities the disposition of which is restricted under the federal securities laws), securities that may be resold only pursuant to Rule 144A under the Securities Act of 1933, as amended (the “Securities Act”), and repurchase agreements with maturities in excess of seven days. | Illiquid Securities:

The Fund may invest in illiquid securities (i.e., securities that are not readily marketable), including, but not limited to, restricted securities (securities the disposition of which is restricted under the federal securities laws), securities that may be resold only pursuant to Rule 144A under the Securities Act and repurchase agreements with maturities in excess of seven days. |

Substantially similar. | ||

Weighted Average Maturity Policy:

The Fund buys municipal securities with different maturities and intends to maintain an average portfolio maturity of 15 to 30 years, although this may be shortened depending on market conditions. | Weighted Average Maturity Policy:

The Fund will invest primarily in municipal securities with long-term maturities in order to maintain an average effective maturity of 15 to 30 years, including the effects of leverage, but the average effective maturity of obligations held by the Fund may be lengthened or shortened as a result of portfolio transactions effected by the Investment Adviser and/or theSub-Adviser, depending on market conditions and on an assessment by the portfolio manager of which segments of the municipal securities markets offer the most favorable relative investment values and opportunities fortax-exempt income and total return. |

Substantially similar. | ||

6

Acquiring Fund | Target Fund | Differences | ||

Other Investment Companies:

The Fund may invest in securities of other open- orclosed-end investment companies (including exchange-traded funds (“ETFs”)) that invest primarily in municipal securities of the types in which the Fund may invest directly, to the extent permitted by the Investment Company Act of 1940, as amended (the “1940 Act”), the rules and regulations issued thereunder and applicable exemptive orders issued by the SEC. In addition, the Fund may invest a portion of its Managed Assets in pooled investment vehicles (other than investment companies) that invest primarily in municipal securities of the types in which the Fund may invest directly. | Other Investment Companies:

The Fund may invest in securities of other open- orclosed-end investment companies (including ETFs) that invest primarily in municipal securities of the types in which the Fund may invest directly, to the extent permitted by the 1940 Act, the rules and regulations issued thereunder and applicable exemptive orders issued by the SEC. |

Substantially similar. | ||

Defaulted Securities:

The Fund may not invest in defaulted securities or in the securities of an issuer that is in bankruptcy at the time of investment, except where, pursuant to theSub-Adviser’s policy regarding municipal workouts, the Fund may invest in defaulted securities from an issuer of a security it already owns, or some other party, to help facilitate a favorable resolution to a municipal workout. | Defaulted Securities:

The Fund may not invest in the securities of an issuer which, at the time of investment, is in default on its obligations to pay principal or interest thereon when due or that is involved in a bankruptcy proceeding (i.e., rated belowC-, at the time of investment); provided, however, that the Fund’s adviser may determine that it is in the best interest of shareholders in pursuing a workout arrangement with issuers of defaulted securities to make loans to the defaulted issuer or another party, or purchase a debt, equity or other interest from the defaulted issuer or another party, or take other related or similar steps involving the investment of additional monies, but only if that issuer’s securities are already held by the Fund. |

Substantially similar. | ||

7

Acquiring Fund | Target Fund | Differences | ||

Use of Derivatives:

The Fund may enter into certain derivative instruments in pursuit of its investment objectives. Such instruments include financial futures contracts, swap contracts (including credit default swaps and interest rate swaps), options on financial futures, options on swap contracts or other derivative instruments. The Fund may not enter into a futures contract or related options or forward contracts if more than 30% of the Fund’s net assets would be represented by futures contracts or more than 5% of the Fund’s net assets would be committed to initial margin deposits and premiums on future contracts or related options. | Use of Derivatives:

The Fund may invest in certain other derivative instruments in pursuit of its investment objectives. Such instruments include financial futures contracts, swap contracts (including interest rate and credit default swaps), options on financial futures, options on swap contracts or other derivative instruments whose prices, in the Adviser’s and/or theSub-Adviser’s opinion, correlate with the prices of the Fund’s investments. The Fund may not enter into futures contracts or related options or forward contracts, if more than 30% of the Fund’s net assets would be represented by futures contracts or more than 5% of the Fund’s net assets would be committed to initial margin deposits and premiums on futures contracts and related options. |

Substantially similar. |

| (1) | Each Fund defines “Assets” as the Fund’s net assets plus the amount of any borrowings for investment purposes. |

| (2) | Each Fund defines “Managed Assets” as the total assets of the Fund, minus the sum of its accrued liabilities (other than Fund liabilities incurred for the express purpose of creating leverage). Total assets for this purpose shall include assets attributable to the Fund’s use of leverage (whether or not those assets are reflected in the Fund’s financial statements for purposes of generally accepted accounting principles), and derivatives will be valued at their market value. |

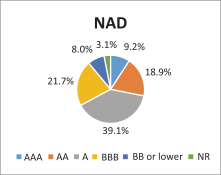

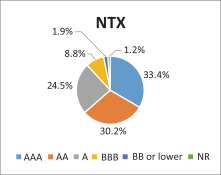

Credit Quality. A comparison of the credit quality(1) (as a percentage of total investment exposure, which includes the leveraged effect of the Funds’ investments in inverse floating rate securities of tender option bond trusts) of the portfolios of the Acquiring Fund and the Target Fund, as of May 31, 2019, is set forth below.

|  |

| (1) | Ratings shown are the highest rating given by one of the following national rating agencies: Standard and Poor’s Group (“S&P”), Moody’s Investors Service, Inc. (“Moody’s”) or Fitch Ratings, Inc. (“Fitch”). Credit ratings are subject to change. AAA, AA, A, and BBB are investment-grade ratings; BB or lower are below-investment-grade ratings. Certain bonds backed by U.S. government or agency securities are regarded as having an implied rating equal to the rating of such securities. Holdings designated N/R are not rated by these national rating agencies. |

8

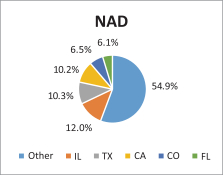

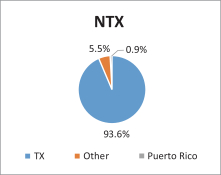

State Allocation.A comparison of the state allocation (as a percentage of total investment exposure, which includes the leveraged effect of the Funds’ investments in inverse floating rate securities of tender option bond trusts) of the portfolios of the Acquiring Fund and the Target Fund, as of May 31, 2019, is set forth below.

|  |

Leverage. Each Fund may utilize the following forms of leverage: the issuance of preferred shares and investments that have the economic effect of leverage, including but not limited to investments in futures, options and inverse floating rate securities (sometimes referred to as “inverse floaters”). The Acquiring Fund may also enter into reverse repurchase agreements. Each Fund currently employs leverage through the issuance of preferred shares and the use of inverse floaters. Certain important ratios related to each Fund’s use of leverage for the last three fiscal years are set forth below:

Acquiring Fund | 2018 | 2017 | 2016 | |||||||||

Asset Coverage Ratio(1) | 263.11 | % | 296.28 | % | 300.64 | % | ||||||

Regulatory Leverage Ratio(2) | 38.01 | % | 33.75 | % | 33.26 | % | ||||||

Effective Leverage Ratio(3) | 39.92 | % | 36.56 | % | 37.58 | % | ||||||

Target Fund | 2018 | 2017 | 2016 | |||||||||

Asset Coverage Ratio(1) | 307.38 | % | 308.18 | % | 311.03 | % | ||||||

Regulatory Leverage Ratio(2) | 32.53 | % | 32.45 | % | 32.15 | % | ||||||

Effective Leverage Ratio(3) | 37.08 | % | 36.99 | % | 34.49 | % | ||||||

| (1) | A Fund’s asset coverage ratio is defined under the 1940 Act as the ratio that the value of the total assets of the Fund, less all liabilities and indebtedness not represented by preferred shares or senior securities representing indebtedness, bears to the aggregate amount of preferred shares and senior securities representing indebtedness issued by the Fund. |

| (2) | Regulatory leverage consists of preferred shares issued or borrowings of a Fund. Both of these are part of a Fund’s capital structure. A Fund, however, may from time to time borrow on a typically transient basis in connection with itsday-to-day operations, primarily in connection with the need to settle portfolio trades. Such incidental borrowings are excluded from the calculation of a Fund’s regulatory leverage and effective leverage ratios. Regulatory leverage is subject to asset coverage limits set forth in the 1940 Act. |

| (3) | Effective leverage is a Fund’s effective economic leverage, and includes both regulatory leverage and the leverage effects of certain derivative and other investments in a Fund’s portfolio that increase the Fund’s investment exposure. Currently, the leverage effects of Tender Option Bond (TOB) inverse floater holdings are included in effective leverage ratios, in addition to any regulatory leverage. |

Board Members and Officers. The Acquiring Fund and the Target Fund have the same Board Members and officers. The management of each Fund, including general supervision of the duties performed by the Fund’s investment adviser under an investment management agreement between the investment adviser and such Fund (each, an “Investment Management Agreement”), is the responsibility of its Board. Each Fund currently has ten (10) Board Members, one (1) of whom is an “interested person,” as defined in the 1940 Act, and nine (9) of whom are not interested persons.

9

Pursuant to each Fund’sby-laws, the board of trustees of the Funds are divided into three classes (Class I, Class II and Class III) with staggered multi-year terms, such that only the members of one of the three classes stand for election each year; provided, however, that holders of preferred shares are entitled as a class to elect two trustees of the Acquiring Fund at all times. The staggered board structure could delay for up to two years the election of a majority of the Board of the Funds. To the extent the preferred shares are held by a small number of institutional holders, a few holders could exert influence on the selection of the Board as a result of the requirement that holders of preferred shares be entitled to elect two trustees of the Funds at all times. The Acquiring Fund’s board structure will remain in place following the closing of the Reorganization.

Investment Adviser. Nuveen Fund Advisors, LLC (previously defined as “Nuveen Fund Advisors” or the “Adviser”) is the investment adviser to each Fund and is responsible for overseeing each Fund’s overall investment strategy, including the use of leverage, and its implementation. Nuveen Fund Advisors also is responsible for the ongoing monitoring of anysub-adviser to the Funds, managing each Fund’s business affairs and providing certain clerical, bookkeeping and other administrative services to the Funds. Nuveen Fund Advisors is located at 333 West Wacker Drive, Chicago, Illinois 60606.

Nuveen Fund Advisors, a registered investment adviser, is a subsidiary of Nuveen, LLC (“Nuveen”), the investment management arm of Teachers Insurance and Annuity Association of America (“TIAA”). TIAA is a life insurance company founded in 1918 by the Carnegie Foundation for the Advancement of Teaching and is the companion organization of College Retirement Equities Fund. As of March 31, 2019, Nuveen managed approximately $989.2 billion in assets, of which approximately $143.6 billion was managed by Nuveen Fund Advisors.

Nuveen Fund Advisors has selected its wholly owned subsidiary, Nuveen Asset Management, LLC (“Nuveen Asset Management” or the“Sub-Adviser”), located at 333 West Wacker Drive, Chicago, Illinois 60606, to serve as asub-adviser to each of the Funds pursuant to asub-advisory agreement between Nuveen Fund Advisors and Nuveen Asset Management (the“Sub-Advisory Agreement”). Nuveen Asset Management, a registered investment adviser, overseesday-to-day operations and manages the investment of the Funds’ assets on a discretionary basis, subject to the supervision of Nuveen Fund Advisors. Pursuant to theSub-Advisory Agreement, Nuveen Asset Management is compensated for the services it provides to the Funds with a portion of the management fee Nuveen Fund Advisors receives from each Fund. Nuveen Fund Advisors and Nuveen Asset Management retain the right to reallocate investment advisory responsibilities and fees between themselves in the future.

Unless earlier terminated as described below, each Fund’s Investment Management Agreement with Nuveen Fund Advisors will remain in effect until August 1, 2020. Each Investment Management Agreement continues in effect from year to year so long as such continuation is approved at least annually by: (1) the Board or the vote of a majority of the outstanding voting securities of the Fund; and (2) a majority of the Board Members who are not interested persons of any party to the Investment Management Agreement, cast in person at a meeting called for the purpose of voting on such approval. Each Investment Management Agreement may be terminated at any time, without penalty, by either the Fund or Nuveen Fund Advisors upon 60 days’ written notice and is automatically terminated in the event of its assignment, as defined in the 1940 Act.

Pursuant to each Investment Management Agreement, each Fund has agreed to pay an annual management fee for the overall advisory and administrative services and general office facilities

10

provided by Nuveen Fund Advisors. Each Fund’s management fee consists of two components—a complex-level fee, based on the aggregate amount of all eligible fund assets of Nuveen-branded closed- andopen-end registered investment companies organized in the U.S., and a specific fund-level fee, based only on the amount of assets within such Fund. This pricing structure enables the Funds’ shareholders to benefit from growth in assets within each individual Fund as well as from growth of complex-wide assets managed by Nuveen Fund Advisors.

For thesix-month semi-annual period ended April 30, 2019 (annualized), the effective management fee rate of the Acquiring Fund, expressed as a percentage of average total daily net assets (including assets attributable to leverage), was approximately 0.5492%. For the fiscal year ended February 28, 2019, the effective management fee rate of the Target Fund, expressed as a percentage of average total daily net assets (including assets attributable to leverage), was approximately 0.6034%.

The annual fund-level fee rate for each Fund, payable monthly, is calculated according to the following schedule:

Current Fund-Level Fee Schedule for the Funds

Average Total Daily Managed Assets* | Fund-Level Fee Rate | |||

For the first $125 million | 0.4500 | % | ||

For the next $125 million | 0.4375 | % | ||

For the next $250 million | 0.4250 | % | ||

For the next $500 million | 0.4125 | % | ||

For the next $1 billion | 0.4000 | % | ||

For the next $3 billion | 0.3750 | % | ||

For managed assets over $5 billion | 0.3625 | % | ||

| * | For this purpose, managed assets means the total assets of the Fund, minus the sum of its accrued liabilities (other than Fund liabilities incurred for the express purpose of creating leverage). Total assets for this purpose shall include assets attributable to the Fund’s use of effective leverage (whether or not those assets are reflected in the Fund’s financial statements for purposes of U.S. generally accepted accounting principles). |

The management fee compensates the Adviser for overall investment advisory and administrative services and general office facilities. Each Fund pays all of its other costs and expenses of its operations, including compensation of its Board Members (other than those affiliated with the Adviser), custodian, transfer agency and dividend disbursing expenses, legal fees, expenses of independent auditors, expenses of repurchasing shares, expenses of issuing any preferred shares, expenses of preparing, printing and distributing shareholder reports, notices, proxy statements and reports to governmental agencies, listing fees and taxes, if any.

Each Fund also pays a complex-level fee to Nuveen Fund Advisors, which is payable monthly and is in addition to the fund-level fee. The complex-level fee is based on the aggregate daily amount of eligible assets for all Nuveen-brandedclosed-end andopen-end registered investment companies organized in the U.S., as stated in the table below. As of April 30, 2019, the complex-level fee rate for each Fund was 0.1580%.

11

The annual complex-level fee for each Fund, payable monthly, is calculated by multiplying the current complex-wide fee rate, determined according to the following schedule by a Fund’s daily managed assets:

Complex-Level Fee Rates

Complex-Level Managed Asset Breakpoint Level** | Effective Rate at Breakpoint Level | |||

$55 billion | 0.2000 | % | ||

$56 billion | 0.1996 | % | ||

$57 billion | 0.1989 | % | ||

$60 billion | 0.1961 | % | ||

$63 billion | 0.1931 | % | ||

$66 billion | 0.1900 | % | ||

$71 billion | 0.1851 | % | ||

$76 billion | 0.1806 | % | ||

$80 billion | 0.1773 | % | ||

$91 billion | 0.1691 | % | ||

$125 billion | 0.1599 | % | ||

$200 billion | 0.1505 | % | ||

$250 billion | 0.1469 | % | ||

$300 billion | 0.1445 | % | ||

| ** | For the fund-level and complex-level fees, managed assets includeclosed-end fund assets managed by the Adviser that are attributable to certain types of leverage. For these purposes, leverage includes the funds’ use of preferred stock and borrowings and certain investments in the residual interest certificates (also called inverse floating rate securities) in tender option bond (TOB) trusts, including the portion of assets held by a TOB trust that has been effectively financed by the trust’s issuance of floating rate securities, subject to an agreement by the Adviser as to certain funds to limit the amount of such assets for determining managed assets in certain circumstances. The complex-level fee is calculated based upon the aggregate daily managed assets of all Nuveen funds that constitute “eligible assets.” Eligible assets do not include assets attributable to investments in other Nuveen funds or assets in excess of $2 billion added to the Nuveen fund complex in connection with the Adviser’s assumption of the management of the former First American Funds effective January 1, 2011. |

Sub-Adviser.Nuveen Fund Advisors has selected its wholly owned subsidiary, Nuveen Asset Management, located at 333 West Wacker Drive, Chicago, Illinois 60606, to serve as thesub-adviser to each of the Funds pursuant to asub-advisory agreement between Nuveen Fund Advisors and Nuveen Asset Management (the“Sub-Advisory Agreement”). Nuveen Asset Management, a registered investment adviser, overseesday-to-day operations and manages the investment of the Funds’ assets on a discretionary basis, subject to the supervision of Nuveen Fund Advisors. Pursuant to eachSub-Advisory Agreement, Nuveen Asset Management is compensated for the services it provides to the Funds with a portion of the management fee Nuveen Fund Advisors receives from each Fund. Nuveen Fund Advisors and Nuveen Asset Management retain the right to reallocate investment advisory responsibilities and fees between themselves in the future.

For the services provided pursuant to each Fund’sSub-Advisory Agreement, Nuveen Fund Advisors pays Nuveen Asset Management a portfolio management fee, payable monthly, equal to 38.4615% of the management fee (net of applicable breakpoints, waivers and reimbursements) paid by the Fund to Nuveen Fund Advisors.

A discussion of the basis for the applicable Board’s most recent approval of each Fund’s current Investment Management Agreement andSub-Advisory Agreement will be included in the Acquiring Fund’s Annual Report for the fiscal year ending October 31, 2019 and the Target Fund’s semi-annual report to shareholders for the six months ended August 31, 2019.

12

Portfolio Management. Subject to the supervision of Nuveen Fund Advisors, Nuveen Asset Management is responsible for execution of specific investment strategies andday-to-day investment operations. Nuveen Asset Management manages the portfolios of the Funds using a team of analysts and a portfolio manager that focuses on a specific group of funds. Christopher L. Drahn, CFA, is the portfolio manager of the Acquiring Fund and Daniel J. Close, CFA, is the portfolio manager of the Target Fund. Mr. Drahn assumed portfolio management responsibility for the Acquiring Fund in 2016, and Mr. Close assumed portfolio management responsibility for the Target Fund in 2007. Christopher L. Drahn, CFA, will manage the combined fund upon completion of the Reorganization.

Christopher L. Drahn, CFA, is a Managing Director of Nuveen Asset Management. He manages several municipal funds and portfolios. He began working in the financial industry when he joined FAF Advisors in 1980. Mr. Drahn became a portfolio manager in 1988. He received a B.A. from Wartburg College and an M.B.A. in finance from the University of Minnesota. Mr. Drahn holds the Chartered Financial Analyst (CFA) designation.

Daniel J. Close, CFA, is a Managing Director of Nuveen Asset Management. Mr. Close is the lead portfolio manager for Nuveen Asset Management’s taxable municipal strategies. He manages several state-specific municipal bond strategies and related institutional portfolios. He also serves as portfolio manager for nationalclosed-end funds. He joined Nuveen Investments in 2000 as a member of Nuveen’s product management and development team. He then served as a research analyst for Nuveen’s municipal investing team, covering corporate-backed, energy, transportation and utility credits. He received his B.S. in Business from Miami University and his MBA from Northwestern University’s Kellogg School of Management. Mr. Close has earned the CFA designation.

Because each Fund invests primarily in municipal securities and other investments, the income from which is exempt from regular federal income taxes, the principal risks of an investment in each Fund are similar. However, there are material differences between the Funds’ investment objectives and policies that affect the comparative risk profile.The Target Fund is subject to single state risk, while the Acquiring Fund is not. The Acquiring Fund is subject to high yield securities risk to a greater degree than the Target Fund and is also subject to reverse repurchase agreement risk. The Funds are subject to various risks associated with investing primarily in a portfolio of municipal securities and employing leverage, which include:

| • | Municipal Securities Risk. Special factors may adversely affect the value of municipal securities and have a significant effect on the yield or value of a Fund’s investments in municipal securities. These factors include economic conditions, political or legislative changes, regulatory developments or enforcement actions, uncertainties related to the tax status of municipal securities, or the rights of investors. Federal income tax law changes that took effect in 2018 may affect the demand for and supply of municipal bonds, which may affect yields and other factors. |

| • | Municipal Bond Market Liquidity Risk. Inventories of municipal bonds held by brokers and dealers have decreased in recent years, lessening their ability to make a market in these securities. This reduction in market making capacity has the potential to decrease a Fund’s ability to buy or sell bonds, and increase bond price volatility and trading costs, particularly during periods of economic or market stress. In addition, changes to federal banking regulations may cause certain dealers to reduce their inventories of municipal |

13

bonds, which may further decrease a Fund’s ability to buy or sell bonds. As a result, a Fund may be forced to accept a lower price to sell a security, to sell other securities to raise cash, or to give up an investment opportunity, any of which could have a negative effect on performance. If a Fund needed to sell large blocks of bonds, those sales could further reduce the bonds’ prices and hurt performance. |

| • | High Yield Securities Risk. High yield securities, which are rated below investment grade and commonly referred to as “junk bonds,” are speculative and high risk investments that may cause income and principal losses for a Fund. They generally have greater credit risk, involve greater risks of default, downgrade, or price declines, are less liquid and have more volatile prices than investment-grade securities. Issuers of high yield securities are less financially strong, are more likely to encounter financial difficulties, and are more vulnerable to adverse market events and negative sentiments than issuers with higher credit ratings. While each Fund may currently invest in high yield securities, the Acquiring Fund expects to consistently allocate a greater percentage of its portfolio to lower rated municipal securities relative to the Target Fund. |

| • | Issuer Credit Risk. This is the risk that a security in a Fund’s portfolio will fail to make dividend or interest payments when due. Investments in lower rated securities are subject to higher risks than investments in higher rated securities. Because the Acquiring Fund may allocate a greater amount of its assets to lower rated municipal securities compared to the Target Fund, it is more susceptible to issuer credit risk. |

| • | Interest Rate Risk. Fixed-income securities such as bonds, preferred, convertible and other debt securities will decline in value if market interest rates rise. |

| • | Reinvestment Risk. If market interest rates decline, income earned from a Fund’s portfolio may be reinvested at rates below that of the original bond that generated the income. A decline in income could negatively affect the market price of a Fund’s shares or a shareholder’s returns. |

| • | Call Risk or Prepayment Risk. Issuers may exercise their option to prepay principal earlier than scheduled, forcing a Fund to reinvest in lower yielding securities. |

| • | Tax Risk. The tax treatment of the Funds and their distributions may be affected by new IRS interpretations of the Code and future changes in tax laws and regulations. In addition, because the interest income from the municipal securities held by the Funds is normally not subject to federal income tax, the attractiveness of municipal securities in relation to other investment alternatives is affected by changes in thetax-exempt status of interest income from municipal securities. Any proposed or actual changes in such exempt status, therefore, can significantly affect the demand for and supply, liquidity and marketability of municipal securities. This could, in turn, affect a Fund’s net asset value and ability to acquire and dispose of municipal securities at desirable yield and price levels. Additionally, neither Fund is a suitable investment for individual retirement accounts, othertax-exempt ortax-advantaged accounts or investors who are not sensitive to the federal income tax consequences of their investments. |

| • | Reverse Repurchase Agreement Risk. Reverse repurchase agreements involve the sale of securities held by a Fund with an agreement to repurchase the securities at an agreed-upon |

14

price, date and interest payment, and represent borrowings of the Fund. Reverse repurchase agreements involve the risk that the other party to the agreement may fail to return the securities in a timely manner or at all. A Fund could lose money if it is unable to recover the securities and the value of the collateral held by the Fund, including the value of investments made with cash collateral, is less than the value of the securities. These events could also trigger adverse tax consequences to the Fund. The use by a Fund of reverse repurchase agreements involves many of the same risks of leverage since the proceeds derived from such reverse repurchase agreements may be invested in additional securities. |