Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended June 29, 2007

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 0-19483

SWS GROUP, INC.

(Exact name of Registrant as specified in its charter)

| Delaware | 75-2040825 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| 1201 Elm Street, Suite 3500, Dallas, Texas | 75270 | |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code (214) 859-1800

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Name of Each Exchange on Which Registered | |

| Common Stock, par value $0.10 per share | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference inPart III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer ¨ Accelerated filer x Non-accelerated filer ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of voting and non-voting common equity held by non-affiliates on December 29, 2006, was $581,407,000 based on the closing price of the registrant’s common stock, $35.70 per share, reported on the New York Stock Exchange on December 29, 2006.

As of August 30, 2007, there were 27,720,256 shares of the Registrant’s common stock, $.10 par value, outstanding.

Table of Contents

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Proxy Statement to be used in connection with the solicitation of proxies to be voted at the Registrant’s Annual Meeting of Stockholders to be held November 29, 2007, which will be filed with the Securities and Exchange Commission pursuant to Regulations 240.14a(6) within 120 days after the Registrant’s fiscal year end, are incorporated by reference intoPart I andPart III of this Report on Form 10-K.

Table of Contents

SWS GROUP, INC. AND SUBSIDIARIES

INDEX TO 2007 ANNUAL REPORT ON FORM 10-K

Table of Contents

We are a full-service securities and banking firm delivering a broad range of investment, commercial banking and related financial services to individual, corporate and institutional investors, broker/dealers, governmental entities and financial intermediaries. We are a Delaware corporation and were incorporated in 1972.

For purposes of this report, references to “we,” “us,” “our,” “SWS” and the “company” mean SWS Group, Inc. collectively with all of our subsidiaries, and references to “SWS Group” mean solely SWS Group, Inc. as a single entity.

Our principal executive offices are located at 1201 Elm Street, Suite 3500, Dallas, Texas 75270. Our telephone number is (214) 859-1800 and our website is www.swsgroupinc.com. We do not intend for information contained on our website to be part of this Form 10-K. We file annual, quarterly and current reports, proxy statements and other information with the Securities and Exchange Commission (the “SEC”). You may read and copy any document we file with the SEC at the SEC’s public reference room at 100 F Street, N.E., Washington, DC 20549. Please call the SEC at 1-800-SEC-0330 for information on the public reference room.

The SEC also maintains an internet site that contains annual, quarterly and current reports, proxy and information statements and other information that we (together with other issuers) file electronically. The SEC’s internet site is www.sec.gov. We make available free of charge on or through our website our annual, quarterly and current reports as soon as reasonably practicable after we electronically file such material with or furnish it to the SEC. Additionally, we voluntarily will provide electronic or paper copies of our filings free of charge upon request.

Our principal brokerage subsidiary, Southwest Securities, Inc. (“Southwest Securities”), is a registered broker/dealer and a member of the New York Stock Exchange, Inc. (“NYSE”). It is also a member of the Financial Industry Regulatory Authority (“FINRA”), Securities Investor Protection Corporation (“SIPC”), and other regulatory and trade organizations. FINRA was formed in July 2007 through the consolidation of the National Association of Securities Dealers (“NASD”) and the member regulation, enforcement and arbitration functions of the NYSE.

Southwest Securities provides correspondent services to securities broker/dealers and other financial institutions in 33 states, Canada and Europe. Southwest Securities serves individual investors through its Private Client Group offices in Texas, New Mexico and Oklahoma and institutional investors nationwide. Southwest Securities executes and clears securities transactions for retail and institutional clients, extends margin credit and lends securities and manages and participates in underwriting equity and fixed income securities. For the year ended June 29, 2007, revenues from Southwest Securities accounted for approximately 73% of our consolidated revenues.

We operate one other broker/dealer subsidiary which is registered with the FINRA. SWS Financial Services, Inc. (“SWS Financial”) contracts with over 370 individual registered representatives (who are FINRA licensed salespersons) for the administration of their securities business. While these registered representatives must conduct all of their securities business through SWS Financial, they may conduct insurance, real estate brokerage or other business for others or for their own accounts. The registered representatives are responsible for all of their direct expenses and are paid higher commission rates than Southwest Securities’ registered representatives to compensate them for their added expenses. SWS Financial is a correspondent of Southwest Securities.

We provide clearing services to over 200 correspondent broker/dealers and registered investment advisors and over 370 independent registered representatives, as well as full-service brokerage services to individual and institutional investors. Clearing involves maintaining accounts, processing securities transactions, extending margin loans and performing a variety of administrative services as agent for our correspondent broker/dealers and their clients.

We offer full-service, traditional and Internet banking through Southwest Securities, FSB (the “Bank”). The Bank is a federally chartered savings bank organized and existing under the laws of the United States. Headquartered in Arlington, Texas, the Bank conducts business from its main office and its seven branch locations in North Texas and five loan production offices in Texas and Oklahoma. In 2003, SWS Banc Holding, Inc. (“SWS Banc”) was incorporated as a wholly owned subsidiary of SWS Group in the state of Delaware and became the sole shareholder of the Bank in 2004. The Bank’s one active subsidiary, FSB Development, LLC (“FSB Development”), participates in the development of single-family residential lots.

-1-

Table of Contents

PRODUCTS AND SERVICES

In fiscal 2007, we operated through four business segments grouped primarily by products and services. SeeNote 25 in the Notes to the Consolidated Financial Statements contained in this Report for information regarding the revenues and income (loss) of each of our business segments.

Clearing.We provide clearing and execution services for other broker/dealers (predominantly on a fully disclosed basis) including general securities broker/dealers, bank affiliated firms and firms specializing in high volume trading.

In a fully disclosed clearing transaction, the identity of the correspondent’s client is known to us and we physically maintain the client’s account and perform a variety of services as agent for the correspondent. We provide clearing and execution services for over 200 correspondents throughout the United States and Europe. Correspondent firms are charged fees based on their use of services according to a contractual schedule.

High-volume trading firms specialize in providing services to those customers who trade actively on a daily basis. As of June 29, 2007, Southwest Securities provided clearing services for eight high-volume firms. The nature of services provided to the customers of high-volume firms and the internal costs necessary to support them are substantially different from the standard correspondent costs and services. Accordingly, fees for services to these correspondents, on a per trade basis, are discounted 50-95% from the fees normally charged to other customers.

In addition to clearing trades, we provide other products and services to our correspondents such as recordkeeping, trade reporting, accounting, general back-office support, securities and margin lending, reorganization assistance and custody of securities.

The terms of our agreements with our correspondents define the allocation of financial, operational and regulatory responsibility arising from the clearing relationship. To the extent that the correspondent has available resources, we are protected against claims by customers of the correspondent arising from actions by the correspondent; however, if the correspondent is unable to meet its obligations, dissatisfied customers may attempt to recover from us.

Retail.The Retail segment includes retail securities, insurance and managed accounts.

Retail Securities. We act as securities broker through our employee registered representatives or through our independent contractor arrangements. As a securities broker, we act as agent in the purchase and sale of securities, options, commodities and futures contracts traded on various securities and commodities exchanges or in the over-the-counter market for retail investors. In most cases, we charge commissions to our clients, in accordance with our established commission schedule. In certain instances, varying discounts from the schedule are given, generally based upon the client’s level of business, the trade size and other relevant factors. Some of our registered representatives also maintain licenses to sell certain insurance products. Southwest Securities is registered with the Commodity Futures Trading Commission as a non-guaranteed introducing broker and is a member of the National Futures Association. Southwest Securities is a fully disclosed client of two of the largest futures commodity merchants in the United States.

At June 29, 2007, Southwest Securities had 12 retail brokerage offices (two located in Dallas and one each in Austin, Georgetown, Houston, Longview, Lufkin, Plano and San Antonio, Texas; Oklahoma City, Oklahoma; and Albuquerque and Santa Fe, New Mexico) and 94 registered representatives. At that date, SWS Financial had contracts with 376 independent retail representatives.

Insurance. Southwest Financial Insurance Agency, Inc. and Southwest Insurance Agency, Inc., together with its subsidiary, Southwest Insurance Agency of Alabama, Inc., hold insurance agency licenses in 46 states for the purpose of facilitating the sale of insurance and annuities for our registered representatives to the retail customer. We retain no risk of insurance related to the insurance and annuity products SWS Insurance sells.

Managed Accounts. Through the Managed Advisors and Accounts department of Southwest Securities, we provide advisors with a wide array of products and services to enhance and grow their advisory business. Each program can be tailored to the individual client-relationship, providing the flexibility that is key to an advisor’s success. Products available include “Premier Advisors,” which gives an investor access to more than 75 of the world’s

-2-

Table of Contents

leading institutional money managers at competitive rates; “Directed Mutual Fund Program,” which offers an array of predefined mutual fund portfolios with automatic rebalancing and due diligence; and “Partner,” which offers fee-based, advisor-directed account solutions that include monthly and quarterly performance reporting.

Institutional.The Institutional segment is comprised of businesses serving institutional customers in securities lending, investment banking and public finance, fixed income sales and trading and equity trading.

Securities Lending Activities. We engage in securities lending for other broker/dealers and lending institutions, as well as our own clearing and retail segments. These activities involve borrowing securities to cover short sales and to complete transactions in which clients have failed to deliver securities by the required settlement date and lending securities to other broker/dealers for similar purposes.

When borrowing securities, we are required to deposit cash or other collateral or to post a letter of credit with the lender, and we generally receive a rebate (based on the amount of cash deposited) or a fee calculated to yield a negotiated rate of return. When lending securities, we receive cash or similar collateral and generally pay interest (based on the amount of cash deposited) to the other party to the transaction. Generally, we earn net interest income based on the spread between the interest rate on cash or similar collateral we deposit and the interest rate paid on cash or similar collateral we receive.

Securities borrowing and lending transactions are executed pursuant to written agreements with counterparties which require that securities borrowed and loaned be marked-to-market on a daily basis, that excess collateral be refunded, and that deficit collateral be furnished. Collateral adjustments are usually made on a daily basis through the facilities of various clearinghouses. We are a principal in these securities borrowing and lending transactions and are liable for losses in the event of a failure of any other party to honor its contractual obligation. Our management sets credit limits with each counterparty and reviews these limits regularly to monitor the risk level with each counterparty.

The securities lending business is conducted primarily from Southwest Securities’ New Jersey office using a highly specialized sales force. Competition for these professionals is intense, and there can be no assurance that we will be able to retain these securities lending professionals.

Investment Banking and Public Finance. We earn investment banking revenues by assisting corporate and public entity clients in meeting their financial needs and advising them on the most advantageous means of raising capital. We manage or co-manage public offerings of securities or arrange private placements of securities with institutional or individual investors. In addition, we provide consulting services, including valuations of securities and companies, we arrange and evaluate mergers and acquisitions and we advise clients with respect to financing plans and related matters.

Our syndicate department coordinates the distribution of managed and co-managed corporate equity underwritings, accepts invitations to participate in competitive or negotiated underwritings managed by other investment banking firms, and allocates and merchandises our selling allotments to our branch office system, to institutional clients and to other broker/dealers.

Southwest Securities maintains a corporate finance branch office in Dallas, Texas and public finance branch offices in Austin, Dallas, Houston, Longview, Plano and San Antonio, Texas; Newport Beach, California; New York, New York; Boston, Massachusetts; and Albuquerque, New Mexico.

We are among the leaders in the Southwest in the origination, syndication and distribution of securities of municipalities and political subdivisions. The public finance department provides professional financial advisory and underwriting services to public bodies.

Participation in underwritings, both corporate and municipal, can expose us to material risk since the possibility exists that securities we have committed to purchase cannot be sold at the initial offering price. Federal and state securities laws and regulations also affect the activities of underwriters and impose substantial potential liabilities for violations in connection with sales of securities by underwriters to the public.

Fixed Income Sales and Trading and Equity Trading. Our Fixed Income Group trades fixed income securities primarily for and with institutional customers. These securities include U.S. government and agency bonds, corporate bonds, municipal bonds and mortgage and asset backed securities. We discount our commissions substantially on institutional transactions. Southwest Securities has Fixed Income offices in Dallas, Texas; Chicago, Illinois; Ft. Lauderdale, Florida; Mill Valley, California; Fairfield, Connecticut; Evergreen, Colorado; Bloomfield, New Jersey and New York, New York.

-3-

Table of Contents

Our Equity Trading Group focuses on providing best execution for equity and options orders for clients. We also execute institutional portfolio trades and make a limited number of markets in listed securities.

Banking. The Bank offers a full array of deposit products, including checking, savings, money market and certificates of deposit. As a full-service lender, the Bank offers competitive rates and terms on business loans, as well as a full line of consumer loans. Customers have access to comprehensive Internet banking services and online bill payment. The Bank provides interim construction lending to builders throughout the North Texas market. The Bank also provides factoring of commercial accounts. The Bank offers commercial and commercial real estate loans as well as residential mortgages through conventional and government loans, primarily in North Texas.

The Bank also purchases participations in newly originated residential loans (1-4 families), including sub-prime loans, from various mortgage bankers. The loans are pre-committed for sale to the secondary market and remain on the Bank’s books for an average of 17-20 days. As of the date of this Report, the Bank had 114 customer/originators with national coverage. Although the Bank is exposed to credit risk before the loans are sold, there is no recourse to the Bank once the sale has closed.

The Bank operates branch offices in Arlington, Garland, Granbury, Dallas and Fort Worth, Texas. The Bank also operates loan production offices in Hurst, Dallas, Fort Worth and Waxahachie, Texas and Oklahoma City, Oklahoma.

Margin Lending. We extend credit on a secured basis directly to our customers, both retail and institutional, the customers of correspondent firms and the correspondent firms themselves in order to facilitate customer and correspondent securities transactions. This credit, which earns interest income, is known as “margin lending” and is conducted across all of our brokerage segments. We extend margin credit to correspondent firms only to the extent that such firms pledge proprietary assets as collateral. Our correspondents indemnify us against margin losses on their customers’ accounts. Since we must rely on the guarantees and general creditworthiness of the correspondents, we may be exposed to significant risk of loss if correspondents are unable to meet their financial commitments should there be a substantial adverse change in the value of margined securities.

In customer margin transactions, the client borrows money from us to purchase securities or for other purposes. The loan is collateralized by the securities purchased or by other securities owned by the client. Interest is charged to clients on the amount borrowed to finance margin transactions at a floating rate. The rate charged is dependent on the average net debit balance in the client’s accounts, the activity level in the accounts and the applicable cost of funds. The amount of the loan is subject to the margin regulations (“Regulation T”) of the Board of Governors of the Federal Reserve System, FINRA margin requirements, and our internal policies. In most transactions, Regulation T limits the amount loaned to a customer for the purchase of a particular security to 50% of the purchase price. Furthermore, in the event of a decline in the value of the collateral, FINRA requirements regulate the percentage of client cash or securities that must be on deposit at all times as collateral for the loans.

In permitting clients to purchase on margin, we are subject to the risk of a market decline, which could reduce the value of our collateral below the client’s indebtedness. Agreements with margin account clients permit us to liquidate clients’ securities with or without prior notice in the event of an insufficient amount of margin collateral. Despite those agreements, we may be unable to liquidate clients’ securities for various reasons including a thin trading market, an excessive concentration or the issuance of a trading halt.

The primary source of funds to finance clients’ margin account balances is credit balances in clients’ accounts. We generally pay interest to clients on these credit balances at a rate determined periodically. Available credit balances are used to lend funds to our customers purchasing securities on margin. SEC regulations restrict the use of clients’ funds to the financing of clients’ activities including margin account balances. Excess customer credit balances, as defined by SEC regulations, are invested in short-term securities segregated for the exclusive benefit of customers as required by SEC regulations. We generate net interest income from the positive interest rate spread between the rate earned from margin lending and alternative short-term investments and the rate paid on customer credit balances.

-4-

Table of Contents

Revenues by Source

The following table shows our revenue by source for the last three fiscal years (dollars in thousands):

| 2007 | 2006 | 2005 | ||||||||||||||||

| Amount | Percent | Amount | Percent | Amount | Percent | |||||||||||||

Net revenues from clearing operations | $ | 12,451 | 3 | % | $ | 14,671 | 4 | % | $ | 14,078 | 4 | % | ||||||

Commissions: | ||||||||||||||||||

Listed equities | 11,856 | 3 | % | 10,212 | 3 | % | 10,701 | 3 | % | |||||||||

Over-the-counter equities | 35,461 | 8 | % | 35,905 | 9 | % | 28,942 | 9 | % | |||||||||

Corporate bonds | 11,004 | 2 | % | 9,360 | 2 | % | 13,615 | 4 | % | |||||||||

Government bonds and mortgage-backed securities | 6,802 | 1 | % | 5,252 | 1 | % | 5,393 | 2 | % | |||||||||

Municipal bonds | 8,223 | 2 | % | 8,815 | 2 | % | 9,866 | 3 | % | |||||||||

Options | 1,386 | — | 1,784 | — | 1,538 | — | ||||||||||||

Mutual funds | 13,328 | 3 | % | 11,907 | 3 | % | 11,179 | 4 | % | |||||||||

Other | 2,338 | — | 2,281 | 1 | % | 2,517 | 1 | % | ||||||||||

| 90,398 | 85,516 | 83,751 | ||||||||||||||||

Interest | 292,062 | 62 | % | 220,666 | 56 | % | 143,730 | 44 | % | |||||||||

Investment banking fees: | ||||||||||||||||||

Corporate | 4,629 | 1 | % | 1,331 | — | 1,805 | 1 | % | ||||||||||

Municipal | 15,742 | 3 | % | 15,567 | 4 | % | 13,392 | 4 | % | |||||||||

Taxable fixed income | 908 | — | 1,070 | — | 962 | — | ||||||||||||

Other (trading and other) | 289 | — | 463 | — | 702 | — | ||||||||||||

| 21,568 | 18,431 | 16,861 | ||||||||||||||||

Advisory and administrative fees: | ||||||||||||||||||

Money market funds | 4,697 | 1 | % | 4,884 | 1 | % | 4,769 | 1 | % | |||||||||

Managed account fees | 4,752 | 1 | % | 3,888 | 1 | % | 3,747 | 1 | % | |||||||||

Other | 2,394 | 1 | % | 2,578 | 1 | % | 2,618 | 1 | % | |||||||||

| 11,843 | 11,350 | 11,134 | ||||||||||||||||

Net gains on principal transactions: | ||||||||||||||||||

Equity securities | 2,115 | — | 2,177 | 1 | % | 4,420 | 1 | % | ||||||||||

Municipal securities | 1,297 | — | 784 | — | 1,842 | 1 | % | |||||||||||

Corporate bonds | 1,183 | — | 2,378 | 1 | % | 2,564 | 1 | % | ||||||||||

Government issues | 8,599 | 2 | % | 4,771 | 1 | % | 6,251 | 2 | % | |||||||||

Gain on delivery of Knight shares in settlement of DARTSSMobligation | — | — | — | — | 18,733 | 6 | % | |||||||||||

Other | 2,266 | 1 | % | 6,392 | 2 | % | 2,207 | 1 | % | |||||||||

| 15,460 | 16,502 | 36,017 | ||||||||||||||||

Other: | ||||||||||||||||||

Other fee revenue from clearing operations | 13,837 | 3 | % | 10,831 | 3 | % | 9,626 | 3 | % | |||||||||

Non-interest bank revenue | 3,135 | 1 | % | 2,672 | 1 | % | 3,241 | 1 | % | |||||||||

Floor brokerage | 1,126 | — | 570 | — | 536 | — | ||||||||||||

Regulatory fees | 2,680 | 1 | % | 3,437 | 1 | % | 3,029 | 1 | % | |||||||||

Other | 6,338 | 1 | % | 6,972 | 2 | % | 4,796 | 1 | % | |||||||||

| 27,116 | 24,482 | 21,228 | ||||||||||||||||

Total revenue | $ | 470,898 | 100 | % | $ | 391,618 | 100 | % | $ | 326,799 | 100 | % | ||||||

-5-

Table of Contents

COMPETITION

We encounter intense competition in our business. We compete directly with securities firms and banks, many of which have substantially greater capital and other resources. We also encounter competition from insurance companies and financial institutions in many elements of our business.

The brokerage entities compete principally on the basis of service, product selection, price, location and reputation. We operate at a price disadvantage to discount brokerage firms that do not offer equivalent services. We compete for the correspondent clearing business on the basis of service, reputation, price, technology and product selection.

Competition for successful securities traders, stock loan professionals and investment bankers among securities firms and other competitors is intense, as is competition for experienced financial advisors. We recognize the importance of hiring and retaining skilled professionals; we invest heavily in the recruiting process. The failure to attract and retain skilled professionals could have a material adverse effect on our business and on our performance.

The Bank also operates in an intensely competitive environment. This environment includes other banks, credit unions and insurance companies. There have been numerous new entrants into the Bank’s market area over the past few years. The competition ranges from small community banks to trillion dollar commercial banks. As with the securities industry the ability to attract and retain skilled professionals is critical to the Bank’s success. To enhance these activities the Bank utilizes SWS for assistance in recruiting and educational programs. The Bank competes for community banking products locally based on reputation, service, location and price. The Bank also competes nationally through its purchased mortgage loan division.

REGULATION

The securities industry in the United States is subject to extensive regulation under federal and state laws. The SEC administers the federal securities laws; much of the regulation of broker/dealers, however, has been delegated to self-regulatory organizations, principally FINRA. These self-regulatory organizations adopt rules (which are subject to approval by the SEC) for governing the industry and conduct periodic examinations of member broker/dealers. Securities firms are subject to regulation by state securities commissions in the states in which they conduct business. Southwest Securities and SWS Financial are registered in all 50 states. Southwest Securities is also registered in Puerto Rico.

The regulations to which broker/dealers are subject cover all aspects of the securities business, including sales methods, trade practices among broker/dealers, capital structure, record keeping and the conduct of directors, officers and employees. Additional legislation, changes in rules promulgated by the SEC and by self-regulatory organizations or changes in the interpretation or enforcement of existing laws and rules often directly affect the method of operation and profitability of broker/dealers. The SEC and the self-regulatory organizations may conduct administrative proceedings that can result in censure, fine, suspension or expulsion of a broker/dealer, its officers or employees. The principal purpose of regulation and discipline of broker/dealers is the protection of clients and the securities markets rather than protection of creditors and shareholders of broker/dealers.

Our broker/dealer subsidiaries are subject to the SEC’s net capital rule and the net capital requirements of various securities exchanges of which they are members. FINRA rules also impose limitations on the transfer of a broker/dealer’s assets. Compliance with the capital requirements may limit SWS’ operations requiring the intensive use of capital. Such requirements restrict SWS’ ability to withdraw capital from its broker/dealer subsidiaries, which in turn may limit its ability to pay dividends, repay debt or redeem or purchase shares of its own outstanding stock. Any change in such rules or the imposition of new rules affecting the scope, coverage, calculation or amount of capital requirements, or a significant operating loss or any unusually large charge against capital, could adversely affect SWS’ ability to pay dividends or to expand or maintain present business levels. In addition, such rules may require SWS to make substantial capital contributions into one or more of its broker/dealer subsidiaries in order for such subsidiaries to comply with such rules, either in the form of cash or subordinated loans made in accordance with the requirements of the SEC’s net capital rule.

Certain SWS subsidiaries are registered “introducing brokers” subject to the net capital requirements of, and their activities are regulated by, the Commodity Futures Trading Commission (the “CFTC”) and various commodity exchanges. SWS’ futures business is also regulated by the National Futures Association (the “NFA”), a registered futures association. Violation of the rules of the CFTC, the NFA or the commodity exchanges could result in remedial actions including fines, registration restrictions or terminations, trading prohibitions or revocations of commodity exchange memberships.

-6-

Table of Contents

The Bank, as a federal savings bank, is registered with the Office of Thrift Supervision (“OTS”) and is subject to OTS regulation, examination, supervision and reporting requirements. Regulations applicable to the Bank generally relate to lending and investment activities, payment of dividends and maintenance of appropriate levels of capital. Failure to comply with these regulations may be considered an unsafe and unsound practice and may result in the imposition by the OTS of various sanctions. Because the Bank’s deposits are insured by the Deposit Insurance Fund (“DIF”), the Federal Deposit Insurance Corporation (“FDIC”) also has the authority to conduct special examinations. The Bank is required to file periodic reports with the OTS describing its activities and financial condition. This supervision and regulation is intended to protect the depositors and preserve the safety and soundness of the financial markets.

The USA Patriot Act of 2001 (the “Patriot Act”) imposes significant obligations to detect and deter money laundering and terrorist financing activity, including requiring banks, broker-dealers and mutual funds to obtain specific identification on customers that maintain accounts. The Patriot Act also requires us to provide employees with anti-money laundering (“AML”) training, designate an AML compliance officer and undergo an annual, independent audit to assess the effectiveness of the AML program.

INSURANCE

Our broker/dealer subsidiaries are required by federal law to belong to the SIPC. SIPC provides protection for clients up to $500,000 each with a limitation of $100,000 for claims for cash balances. Southwest Securities purchases insurance which, when combined with the SIPC insurance, provides unlimited coverage in certain circumstances for securities held in clients’ accounts with a $100 million aggregate limit.

The Bank’s deposits are insured by the DIF, which is administered by the FDIC, up to applicable limits for each depositor.

EMPLOYEES

At June 29, 2007, we employed 899 individuals. Southwest Securities employed 693 of these individuals, 142 of whom were full-time registered representatives. In addition, 376 registered representatives were affiliated with Southwest Securities as independent contractors. The Bank employed 175 of these individuals at June 30, 2007.

CUSTOMERS

As of the date of this report, we provide full-service securities brokerage to approximately 28,300 client accounts and clearing services to approximately 166,000 additional client accounts. No single client constitutes a material percentage of our total business.

As of the date of this report, we provide deposit and loan services to approximately 73,300 customers through the Bank and its subsidiaries, which include 63,800 Southwest Securities’ customer accounts. No single customer constitutes a material percentage of the Bank’s total business.

TRADEMARKS

We own various registered trademarks and service marks, including “Southwest Securities,” “SWS,” “SWS Financial,” “Southwest Securities, FSB” and “SWS Group,” which are not material to our business. We also own various design marks related to logos for various business segments.

EXECUTIVE OFFICERS OF THE REGISTRANT

The following table lists our executive officers and their respective ages and positions, followed by a brief description of their business experience over the past five years. Each listed person has been elected to the indicated office by our board of directors.

-7-

Table of Contents

Name | Age | Position | ||

Donald W. Hultgren | 50 | Director and Chief Executive Officer | ||

William D. Felder | 49 | President | ||

Kenneth R. Hanks | 52 | Executive Vice President, Chief Financial Officer and Treasurer | ||

Stacy M. Hodges | 44 | Executive Vice President | ||

Daniel R. Leland | 46 | Executive Vice President | ||

Richard H. Litton | 60 | Executive Vice President | ||

James H. Ross | 57 | Executive Vice President | ||

W. Norman Thompson | 51 | Executive Vice President and Chief Information Officer | ||

Paul D. Vinton | 58 | Executive Vice President | ||

Richard J. Driscoll | 52 | Executive Vice President | ||

Allen R. Tubb | 53 | Vice President, General Counsel and Secretary |

Donald W. Hultgren was elected Director and Chief Executive Officer in August 2002. He served as Executive Vice President and Director of Capital Markets from March 2000 to August 2002. From 1989 to 2000, Mr. Hultgren was employed by Raymond James & Associates in various capacities including Managing Director in the Healthcare sector of Corporate Finance and Director of Research. He is a member of the Certified Financial Advisors (“CFA”) Institute and a member of the Advisory Committee for the University of Texas MBA Investment Fund. He formerly served as chairman of the board for the American Heart Association, Dallas, Texas Division, and is currently on the association’s Executive Committee. He also serves on the Strategic Advisory Board of the CFA Society of Dallas/Ft. Worth.

William D. Felder was elected President of SWS Group in August 2002 and President and Chief Executive Officer of Southwest Securities, Inc. in September 2004. He served as Executive Vice President of SWS Group from December 1995 to August 2002 and prior to that as Senior Vice President from 1993 to 1995. Mr. Felder has been associated with Southwest Securities in various other capacities since 1980, including Director since August 1993 and Senior Vice President in charge of Clearing Services from 1988 to 1998. Mr. Felder is a past Chairman of the District 6 Business Conduct Committee of the NASD and a past member of the Board of Governors of the Chicago Stock Exchange and Securities Industry Association’s Clearing Firms Committee. Mr. Felder is currently a member of the Securities Industry and Financial Markets Association’s (SIFMA) Board of Trustees for the Securities Industry Institute and a member of the NASD District 6 Nominating Committee. He also currently serves on the Board of Directors of the Options Clearing Corporation.

Kenneth R. Hankswas elected Treasurer and Chief Financial Officer in August 2002 and has served as Executive Vice President since June 1996. He served as Chief Operating Officer from August 1998 to August 2002. Mr. Hanks was the Chief Financial Officer from June 1996 to August 1998 and has been a Director of Southwest Securities since June 1997. Mr. Hanks served in various executive capacities at Rauscher Pierce Refsnes, Inc. from 1981 to 1996, including Executive Vice President and Chief Financial Officer. He serves as an arbitrator with the FINRA and formerly served as a member of the NASD’s District 6 Business Conduct Committee. Mr. Hanks also currently serves on the Board of Directors of Peerless, Mfg. Co., which designs and manufactures a wide range of separation filtration equipment and environmental systems for the reduction of air pollution.

Stacy M. Hodgeshas served as Executive Vice President since February 1999. She served as Treasurer and Chief Financial Officer from August 1998 to August 2002. Ms. Hodges was Controller from September 1994 to August 1998. Ms. Hodges served as Director of Southwest Securities from June 1997 to August 2002 and has served as Chief Financial Officer of Southwest Securities since June 1997. Prior to joining Southwest Securities, Ms. Hodges was a Senior Audit Manager in the Financial Services division of KPMG LLP. Ms. Hodges is a member of the American Institute of Certified Public Accountants and the Texas Society of CPAs.

Daniel R. Leland has served as Executive Vice President since May 2007. Mr. Leland was also Executive Vice President from February 1999 to September 2004. He served as President and Chief Executive Officer of Southwest Securities from August 2002 to September 2004. He also served as Executive Vice President of Southwest Securities from July 1995 to August 2002 and was re-elected in February 2006. Mr. Leland began his career at Barre & Company in June 1983 where he was employed in various capacities in fixed income sales and trading before becoming President of Barre & Company in 1993. Mr. Leland has been an arbitrator for the NASD and is a past Vice Chairman of the District 6 Business Conduct Committee.

-8-

Table of Contents

Richard H. Litton has served as Executive Vice President and Executive Vice President of Southwest Securities in charge of the Public Finance Division since July 1995. Previously, Mr. Litton was President of a regional investment bank and headed the Municipal Group in the Southwest for Merrill Lynch. Mr. Litton served on various advisory committees for the Texas House of Representatives’ Financial Institutions Committee, is past member and director of the Municipal Advisory Council of Texas and is a past member of the Marketing Committee of the Public Securities Association. He currently represents Southwest Securities on the Bond Market Association’s Legal and Legislative Committee.

James H. Rosswas elected Executive Vice President of SWS effective November 10, 2004. Mr. Ross was appointed the Director of the Private Client Group at Southwest Securities and Chief Executive Officer of SWS Financial Services effective March 9, 2004. Mr. Ross came to Southwest Securities January 5, 2004, to head the Private Client Group’s brokerage office in downtown Dallas. Prior to coming to Southwest Securities, Mr. Ross was with UBS Paine Webber, where, from April 1991 to December 2003, Mr. Ross held various positions from financial advisor to branch manager. He began his securities industry career in 1975.

W. Norman Thompson has served as Executive Vice President and Chief Information Officer since January 1995. Mr. Thompson was associated with Kenneth Leventhal & Co. (now a part of Ernst & Young LLP) in various capacities ranging from Audit Manager to Senior Consulting Manager from 1987 to 1994. Previously, Mr. Thompson was an auditor with KPMG LLP from 1981 to 1987. In the capacities he held with both Kenneth Leventhal & Co. and KPMG LLP, he was heavily involved in information technology auditing and consulting.

Paul D. Vinton has served as Executive Vice President since November 1998 and as Senior Vice President of Southwest Securities since June 1995. Mr. Vinton was associated with Stephens Inc. in various capacities from 1993 through 1995. Mr. Vinton has been employed within the securities industry since 1972 with various firms dealing primarily in operational, clearance and settlement activities. Mr. Vinton has served on various industry group boards including, most recently, the Depository Trust Company Settlement Advisory Board.

Richard J. Driscoll was elected Executive Vice President in August 2003. He has served as Chairman of the Board of Directors of the Bank since March 2002 and CEO of the Bank since 1991. He joined the Bank in 1991 as Chief Executive Officer and President and a member of the Board of Directors. Mr. Driscoll recently served as a Director of the Texas Savings and Community Banker’s Association and recently served as a member of the Federal Reserve Board Thrift Institutions Advisory Council. He currently serves on the Board of Directors of America’s Community Bankers.

Allen R. Tubb was elected Vice President, General Counsel and Secretary in August of 2002. He joined SWS as Corporate Counsel and Secretary in October 1999. From 1979 to 1999, Mr. Tubb was employed with Oryx Energy Company and its predecessor Sun Exploration and Production Company in various capacities including Chief Counsel, Worldwide Exploration and Production. Mr. Tubb is a member of the Texas Bar Association.

Our business, reputation, financial condition, operating results and cash flows can be impacted by a number of factors. Many of these factors are beyond our control and may increase during periods of market volatility or reduced liquidity. The potential harm from any one of these risks, or others, could cause our actual results to vary materially from recent results or from anticipated future results. Some risks may adversely impact not only our own operations, but the banking or securities industry in general which could also produce marked swings in the trading price of our securities.

WE ARE SUBJECT TO RISKS SPECIFIC TO OUR INDUSTRIES

Our revenues may decrease if securities transaction volumes decline. Our securities business depends upon the general volume of trading in the United States securities markets. If the volume of securities transactions should decline, revenues from our securities brokerage, securities lending and clearing businesses would decrease and our business, financial condition, results of operations and cash flow would be materially and adversely impacted.

Market fluctuations could adversely impact our securities business.We are subject to risks as a result of fluctuations in the securities markets. Our securities trading, market-making and underwriting activities involve the purchase and sale of securities as a principal, which subjects our capital to significant risks. Market conditions could limit our ability to sell securities purchased or to purchase securities sold in such transactions. If

-9-

Table of Contents

price levels for equity securities decline generally, the market value of equity securities that we hold in our inventory could decrease and trading volumes could decline. In addition, if interest rates increase, the value of debt securities we hold in our inventory would decrease. Rapid or significant market fluctuations could adversely affect our business, financial condition, results of operations and cash flow.

We are subject to risks relating to litigation and potential securities law liabilities.Many aspects of our business involve substantial risks of liability. In the normal course of our business, we have been subject to claims by clients dealing with matters such as unauthorized trading, churning, mismanagement, breach of fiduciary duty or other alleged misconduct by our employees. We are sometimes brought into lawsuits based on actions of our correspondents. As underwriters, we are subject to substantial potential liability for material misstatements and omissions in prospectuses and other communications with respect to underwritten offerings of securities. Prolonged litigation producing significant legal expenses or a substantial settlement or adverse judgment could have a material adverse effect on our business, financial condition, results of operations and cash flow.

Our securities business is subject to numerous operational risks.We must be able to consistently and reliably obtain securities pricing information, process client and investor transactions and provide reports and other customer service to our clients and investors. Any failure to keep current and accurate books and records can render us liable to disciplinary action by governmental and self-regulatory authorities, as well as to claims by our clients. If any of our financial, portfolio accounting or other data processing systems do not operate properly or are disabled, or if there are other shortcomings or failures in our internal processes, people or systems, we could suffer an impairment to our liquidity, a financial loss, a disruption of our businesses, liability to clients, regulatory problems or damage to our reputation. These systems may fail to operate properly or become disabled as a result of events that are wholly or partially beyond our control, including a disruption of electrical or communications services or our inability to occupy one or more of our buildings. In addition, our operations are dependent upon information from, and communications with, third parties, and operational problems at third parties may adversely affect our ability to carry on our business.

Failure to comply with the extensive state and federal laws governing our securities and banking operations, or the regulations adopted by several self-regulatory agencies having jurisdiction over us, could have material adverse consequences for us. Broker/dealers and banks are subject to regulation in almost every facet of their operations. Our ability to comply with these regulations depends largely on the establishment and maintenance of an effective compliance system as well as our ability to attract and retain qualified compliance personnel. We could be subject to disciplinary or other actions due to claimed non-compliance with these laws or regulations or possibly for the claimed non-compliance of our correspondents. If a claim of non-compliance is made by a regulatory authority, the efforts of our management could be diverted to responding to such claim and we could be subject to a range of possible consequences, including the payment of fines and the suspension of one or more portions of our business. Our clearing contracts generally include automatic termination provisions which are triggered in the event we are suspended from any of the national exchanges of which we are a member for failure to comply with the rules or regulations thereof. Compliance with capital requirements could limit our ability to pay dividends at SWS or may impede our ability to repurchase shares of our capital stock.

We depend on our computer and communications systems and an interruption in service would negatively affect our business.Significant malfunctions or failures of our computer systems or any other systems in the trading process (e.g., record retention and data processing functions performed by third parties, and third party software, such as Internet browsers) could cause delays in customer trading activity. Such delays could cause substantial losses for customers and could subject us to claims from customers for losses, including litigation claiming fraud or negligence. In addition, if our computer and communications systems fail to operate properly, regulations would restrict our ability to conduct business. Any such failure could prevent us from collecting funds relating to customer transactions, which would materially impact our cash flow. Any computer or communications system failure or decrease in computer system performance that causes interruptions in our operations could have a material adverse effect on our business, financial condition, results of operations and cash flow.

Our portfolio trading business is highly price competitive and serves a very limited market. Our business serves one small component of the portfolio trading execution market with a small customer base and a high service model, charging competitive commission rates. Consequently, growing or maintaining market share is very price sensitive. We rely upon a high level customer service and product customization to maintain our market share; however, should prevailing market prices fall, the size of our market segment decline or our customer base decline, our profitability would be adversely impacted.

-10-

Table of Contents

Our computer systems and network infrastructure could be vulnerable to security problems.Hackers may attempt to penetrate our network security which could have a material adverse effect on our business. A party who is able to penetrate our network security could misappropriate proprietary information. We rely on encryption and authentication technology licensed from third parties to provide the security and authentication necessary to effect secure transmission of confidential information. Advances in computer capabilities, discoveries in the field of cryptography and other discoveries, events or developments could lead to a compromise or breach of the algorithms that our licensed encryption and authentication technology uses to protect such confidential information. We may be required to expend significant capital and resources and engage the services of third parties to protect against the threat of such security, encryption and authentication technology breaches or to alleviate problems caused by such breaches. Security breaches or the inadvertent transmission of computer viruses could expose us to a risk of loss or litigation and possible liability which could have a material adverse affect on our business, financial condition, results of operations and cash flow

Our existing correspondents may choose to perform their own clearing services.As our correspondents’ operations grow, they often consider the option of performing clearing functions themselves, in a process referred to as “self clearing.” As the transaction volume of a broker/dealer grows, the cost of implementing the necessary infrastructure for self-clearing may be offset eventually by the elimination of per transaction processing fees that would otherwise be paid to a clearing firm. Additionally, performing their own clearing services allows self-clearing broker/dealers to retain their customers’ margin balances, free credit balances and securities for use in margin lending activities. Significant losses to self-clearing could have a material adverse affect on our business, financial condition, results of operations and cash flow.

WE ARE SUBJECT TO RISKS SPECIFIC TO OUR COMPANY

Our business is significantly dependent on net interest margins.The profitability of our margin lending business depends to a great extent on the difference between interest income earned on margin loans and investments of customer cash and the interest expense paid on customer cash balances and borrowings. The earnings and cash flows of the Bank are also dependent upon the difference between interest income earned on interest-earning assets such as loans and securities and interest expense paid on interest-bearing liabilities such as deposits and borrowed funds.

Interest rates are highly sensitive to many factors that are beyond our control, including general economic conditions and policies of various governmental and regulatory agencies and, in particular, the Board of Governors of the Federal Reserve System. Changes in monetary policy, including changes in interest rates, could influence the interest we receive on loans and securities and the amount of interest we pay on deposits and borrowings. Such changes could also affect our ability to originate loans and obtain deposits and the fair value of our financial assets and liabilities. If the interest rates paid on deposits and other borrowings increase at a faster rate than the interest rates received on loans and other investments, our net interest income, and therefore our earnings, could be adversely affected. Earnings could also be adversely affected if the interest rates received on loans and other investments fall more quickly than the interest rates paid on deposits and other borrowings.

Our margin lending, stock lending, securities execution, bank lending and mortgage purchase businesses are all subject to credit risk. Credit risk in all areas of our business increases if prices decline rapidly because the value of our collateral could fall below the amount of indebtedness it secures. In rapidly appreciating markets, credit risk increases due to short positions. Our securities lending business subjects us to credit risk if a counterparty fails to perform. In securities transactions we are subject to credit risk during the period between the execution of a trade and the settlement by the customer. While agreements with our clients permit us to liquidate or buy securities if the amount of our collateral becomes insufficient, we may be unable to liquidate or buy securities for various reasons.

Our banking group is exposed to the risk that our loan customers may not repay their loans in accordance with their terms, the collateral securing the loans may be insufficient, or our loan loss reserve may be inadequate, to fully compensate us for the outstanding balance of the loan plus the costs to dispose of the collateral. Our mortgage warehousing activities subject us to credit risk while mortgages are purchased and held for resale.

Significant failures by our customers or clients to honor their obligations, together with insufficient collateral and reserves, could have a material adverse affect on our business, financial condition, results of operations and cash flow.

-11-

Table of Contents

If our allowance for loan losses is not sufficient to cover actual loan losses, the profitability of our financial services segment could decrease.Our loan customers may fail to repay their loans according to the terms, and the collateral securing the payment of these loans may be insufficient to assure repayment. Such loan losses could have a material adverse effect on our operating results. We make various assumptions, estimates, and judgments about the collectibility of our loan portfolio, including the creditworthiness of our borrowers and the value of the real estate and other assets serving as collateral for the repayment of many of our loans. In determining the amount of the allowance for loan losses, we rely on a number of factors, including our own experience and our evaluation of economic conditions. If our assumptions prove to be incorrect, our current allowance for loan losses may not be sufficient to cover losses inherent in our loan portfolio, and adjustments may be necessary that would have a material adverse effect on our operating results.

The Bank’s mortgage and interim construction lending business is dependent on the general health of the North Texas economy.The Bank’s interim construction, commercial real estate, commercial and mortgage lending businesses are dependent on the general health of the North Texas economy. A significant downturn in the local North Texas economy could adversely affect these lines of business, and consequently our financial condition, results of operations and cash flow.

We depend on the highly skilled, and often specialized, individuals we employ, particularly certain personnel in our loan production, private client group, securities lending and trading businesses. Competition for the services of these employees is intense, and we cannot guarantee that our efforts to retain such personnel will be successful. We generally do not enter into employment agreements or noncompetition agreements with our employees. Our business, financial condition, operating results and cash flow could be materially impacted if we were to lose the services of certain of our loan production, private client group, securities lending or trading professionals.

We face liquidity risk, which is the potential inability to repay short-term borrowings with new borrowings or assets that can be quickly converted into cash while meeting other obligations and continuing to operate as a going concern. Our liquidity may be impaired due to circumstances that we may be unable to control, such as general market disruptions or an operational problem that affects our trading clients, third parties or ourselves. Our ability to sell assets may also be impaired if other market participants are seeking to sell similar assets at the same time. Our inability to borrow funds or sell assets to meet maturing obligations would have an adverse effect on our business, financial condition, results of operations and cash flow.

From time to time, we make statements (including some contained in this report) that predict or forecast future events, depend on future events for their accuracy, or otherwise contain “forward-looking” information. These statements may relate to anticipated changes in revenues or earnings per share, anticipated changes in our businesses or in anticipated expense levels, or in expectations regarding financial market conditions. We caution readers that any forward-looking information we provide is not a guarantee of future performance. Actual results may differ materially as a result of various factors, some of which are outside of our control.

Factors which may cause actual results to differ materially from forward-looking statements include those factors discussed in this report in the sections entitled “Business,” “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Overview,” “-Risk Management,” and “-Critical Accounting Policies and Estimates” and those discussed in our other reports filed with and available from the SEC. All forward-looking statements we make speak only as of the date on which they are made, and we undertake no obligations to update them to reflect events or circumstances occurring after the date on which they were made or to reflect the occurrence of unanticipated events.

We receive from time to time written comments from the staff of the SEC regarding our periodic or current reports under the Securities Exchange Act of 1934 (the “Exchange Act”). There are no comments that remain unresolved.

Our executive offices and primary operations are located in approximately 155,000 square-feet of leased space in an office building in Dallas, Texas. The lease expires in 2020. Our other office locations are leased and generally do not exceed 13,000 square feet of space. We conduct our clearing operations primarily at the Dallas headquarters, and our securities lending activities are primarily conducted from our office in New Jersey.

-12-

Table of Contents

We have 12 retail brokerage offices with nine in Texas, one in Oklahoma and two in New Mexico. In keeping with Management’s goal to become the leading brokerage firm in the Southwest, we plan to expand our offices throughout the region.

We have nine public finance branch offices, six in Texas, one in New Mexico, one in Massachusetts and one in California. (Public finance has one additional branch in New York for which SWS does not maintain an office.) We have eight fixed income branch offices with one branch in each of Illinois, Texas, Connecticut, Colorado, Florida, New Jersey, New York and California. Our corporate finance office is located in Dallas, Texas. We also have a disaster recovery site in Dallas, Texas.

The company has developed business continuity plans that are designed to permit continued operation of business critical functions in the event of disruptions to our Dallas, Texas headquarters facility as well as critical facilities used by our major subsidiaries. Our critical activities can be relocated among our normal operating facilities and our North Dallas business recovery and disaster recovery center. Our North Dallas facility houses redundant securities and bank processing facilities adequate to replace those found in our primary data center. Our plans are periodically tested, and we participate in the industry-wide tests within the securities industry.

The Bank leases its approximately 25,000 square-foot main office located in Arlington, Texas, leases branch offices in Arlington, Downtown Dallas, North Dallas, Fort Worth and Garland, Texas, and leases separate space in Hurst, Waxahachie, Fort Worth, and Dallas, Texas and Oklahoma City, Oklahoma for loan production offices. The Bank leases the land and owns the drive-in facilities located next to the main office. The Bank owns its banking facilities in Granbury, Texas and South Arlington.

Management believes that our present facilities and equipment are adequate for the foreseeable future, exclusive of expansion opportunities.

In the general course of our brokerage business and the business of clearing for other brokerage firms, we have been named as defendants in various pending lawsuits and arbitration proceedings. These claims allege violation of federal and state securities laws. The Bank is also involved in certain claims and legal actions arising in the ordinary course of business. We believe that resolution of these claims will not result in any material adverse effect on our business, consolidated financial condition, results of operations or cash flows.

SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS

None.

-13-

Table of Contents

MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND

ISSUER PURCHASES OF EQUITY SECURITIES

Our common stock trades on the NYSE under the symbol “SWS.” At August 30, 2007, there were 280 holders of record of our common stock and approximately 6,400 beneficial holders of our common stock. The following table sets forth for the periods indicated the high and low market prices for the common stock and the cash dividend declared per common share:

2007 | 1st Qtr. (1) | 2nd Qtr. (1) | 3rd Qtr. | 4th Qtr. | ||||||||

Cash dividend declared per common share | $ | 0.07 | $ | 0.07 | $ | 0.08 | $ | 1.08 | ||||

Stock price range | ||||||||||||

High | $ | 17.69 | $ | 24.95 | $ | 31.99 | $ | 28.22 | ||||

Low | $ | 14.45 | $ | 16.00 | $ | 22.54 | $ | 20.92 | ||||

2006 | 1st Qtr. (1) | 2nd Qtr. (1) | 3rd Qtr. (1) | 4th Qtr. (1) | ||||||||

Cash dividend declared per common share | $ | 0.07 | $ | 0.07 | $ | 0.07 | $ | 0.74 | ||||

Stock price range | ||||||||||||

High | $ | 12.64 | $ | 14.77 | $ | 17.54 | $ | 19.88 | ||||

Low | $ | 10.45 | $ | 10.10 | $ | 13.60 | $ | 14.60 | ||||

(1) | On November 30, 2006, our Board of Directors declared a 3-for-2 stock split effected in the form of a 50% stock dividend. All references to dividends and stock prices have been restated to give retroactive effect to the stock split. |

The following table provides information about purchases by SWS during the quarter ended June 29, 2007 of our equity securities registered pursuant to Section 12 of the Exchange Act:

ISSUER PURCHASES OF EQUITY SECURITIES

| Total Number of Shares Purchased | Average Price Paid per Share | Total Number of Shares Purchased as Part of Publicly Announced Plan | Maximum Number of Shares that May Yet Be Purchased Under the Plans(1) | |||||

3/31/07 to 4/27/07 | — | — | — | 500,000 | ||||

4/27/07 to 5/25/07 | — | — | — | 500,000 | ||||

5/26/07 to 6/29/07 | — | — | — | 500,000 | ||||

| — | — | — | ||||||

(1) | In November 2006, the Board of Directors approved a stock repurchase program effective January 1, 2007 and expires June 30, 2008. The program allows for the purchase of up to 500,000 shares of our common stock. |

-14-

Table of Contents

Equity Compensation Plan Information

Restricted Stock Plan.On November 12, 2003, our stockholders approved the adoption of the SWS Group, Inc. 2003 Restricted Stock Plan (“Restricted Stock Plan”). The Restricted Stock Plan allows for awards of up to 750,000 shares of our common stock to our directors, officers and employees. No more than 300,000 of the authorized shares may be newly issued shares of common stock. The Restricted Stock Plan terminates on August 21, 2013. The vesting period is determined on an individualized basis by the Compensation Committee of the Board of Directors. In general, restricted stock granted to employees under the Restricted Stock plan is fully vested after three years, and restricted stock granted to non-employee directors vests on the one year anniversary of the date of grant. At June 29, 2007, the total number of shares outstanding was 236,492 and the total number of securities available for future grants was 334,614.

Deferred Compensation Plan.In July 1999, we implemented a Deferred Compensation Plan (the “1999 Plan”) for eligible officers and employees to defer a portion of their bonus compensation and commissions. The 1999 Plan was amended and restated in 2003. On November 10, 2004, the shareholders of SWS Group approved the 2005 Deferred Compensation Plan (the “2005 Plan”), the effective date of which was January 1, 2005. With the approval of the 2005 Plan, no future deferrals may be made pursuant to the 1999 Plan after the effective date; however, amounts previously deferred will be paid in accordance with the terms of the 1999 Plan. The 2005 Plan was designed to comply with the American Jobs Creation Act of 2004 while continuing to allow eligible officers and employees to defer a portion of certain compensation. Contributions to the 2005 Plan, and previously the 1999 Plan, consist of employee pre-tax contributions and SWS’ matching contributions, in the form of SWS stock, up to a specified limit. The 2005 Plan limits the number of SWS shares that may be issued to 375,000 shares. The number of SWS shares available for future issuance under the plan is 143,804 at June 29, 2007.

The assets of the 2005 Plan include investments in SWS Group, Westwood Holdings Group, Inc. (“Westwood”), and company owned life insurance (“COLI”). Investments in SWS Group stock are carried at cost and are held as treasury stock with an offsetting deferred compensation liability in the equity section of the Consolidated Statement of Financial Condition. Investments in Westwood stock are carried at market value and recorded as marketable equity securities available for sale. Investments in COLI are carried at the cash surrender value of the insurance policies and recorded in Other Assets in the Consolidated Statements of Financial Condition. As of December 31, 2004, all investments in the 1999 Plan were liquidated, except for the investments in SWS Group and Westwood stock. Proceeds from the liquidation were invested in COLI.

For the fiscal year ended June 29, 2007, approximately $9,191,000, with a market value of $10,531,000, was invested in the 2005 Plan. At June 29, 2007, funds totaling $1,917,000 were invested in 129,964 shares of our common stock. During the second quarter of fiscal 2007, SWS received proceeds of $2,289,000 from company owned life insurance which were recorded in other revenue in the Consolidated Statement of Income and Comprehensive Income. Approximately $1,332,000 of compensation expense was recorded for participant contributions and employer matching contributions related to the 2005 Plan in fiscal year 2007.

The trustee of the 2005 Plan is Wilmington Trust Company.

Stock Option Plans. We have two expired stock option plans, the SWS Group, Inc. 1997 Stock Option Plan (the “1997 Plan”) which expired August 19, 2007 and the SWS Group, Inc. Stock Option Plan (the “1996 Plan”) which expired February 1, 2006. All options outstanding under the 1997 Plan and the 1996 Plan may still be exercised until their contracted expiration date occurs. Options granted under the 1996 and 1997 Plans have a maximum ten-year term, and the vesting period was determined on an individual basis by the Compensation Committee of the Board of Directors. However, options granted to non-employee directors under the 1996 Plan were fully vested six-months after grant and have a five-year term.

As of June 25, 2005, we began accounting for the plans under the recognition and measurement principles of the Financial Accounting Standards Board Statement of Financial Accounting Standards No. 123R, “Share-Based Payment.” For all periods prior to June 25, 2005, we accounted for the plans under the recognition and measurement principles of Accounting Principles Board Opinion No. 25, “Accounting for Stock Issued to Employees.” SeeNote 1(p) in the Notes to the Consolidated Financial Statements contained in this Report.

The following table sets forth certain information concerning all equity compensation plans approved by our stockholders and all equity compensation plans not approved by our stockholders as of June 29, 2007.

-15-

Table of Contents

EQUITY COMPENSATION PLAN INFORMATION AS OF JUNE 29, 2007

Plan category | Number of securities to be issued upon exercise of outstanding options and rights | Weighted-average exercise price of outstanding options | Number of securities remaining available for future issuance under equity compensation plans (excluding securities reflected in the first column) | |||||||

Equity compensation plans approved by stockholders | 755,509 | (1) | $ | 11.95 | (2) | 478,418 | (3) | |||

Equity compensation plans not approved by stockholders | 12,479 | (4) | $ | 10.72 | 253,641 | (4) | ||||

| 767,988 | $ | 11.93 | 732,059 | |||||||

(1) | Amount represents 625,545 shares issuable upon the exercise of options granted under the 1996 Plan and 129,964 stock units credited to participants’ accounts under the 2005 Plan (see descriptions above). The stock units credited to the participants’ accounts under the 2005 Plan are not included in the weighted average exercise price calculation. |

(2) | Calculation of weighted-average exercise price does not include stock units credited to participants’ accounts under the 2005 Plan. |

(3) | Amount represents 143,804 shares available for future issuance under the 2005 Plan and 334,614 shares available for future issuance under the Restricted Stock Plan. The 1996 Plan expired on February 1, 2006 thus there are no longer any shares available for issuance. All options outstanding under the 1996 Plan may still be exercised until their contracted expiration date occurs. |

(4) | Amounts represent share information with respect to the 1997 Plan. The 1997 Plan expired August 19, 2007 at which time there were no longer any shares available for issuance. |

-16-

Table of Contents

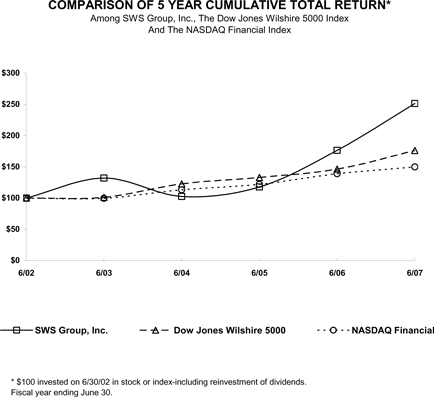

The following graph compares the cumulative total stockholder return on our common stock for the 60-month period from June 2002 through June 2007, with the cumulative total return of the Dow Jones Wilshire 5000 Index and the Nasdaq Financial Index over the same period. The graph depicts the results of investing $100 in our common stock, the Dow Jones Wilshire 5000 Index and the Nasdaq Financial Index in June 2002, including reinvestment of dividends.

| Cumulative Total Return | ||||||||||||

| 6/02 | 6/03 | 6/04 | 6/05 | 6/06 | 6/07 | |||||||

SWS GROUP, INC. | 100.00 | 132.07 | 102.65 | 117.86 | 176.31 | 251.27 | ||||||

DOW JONES WILSHIRE 5000 | 100.00 | 101.27 | 122.71 | 133.01 | 146.35 | 176.22 | ||||||

NASDAQ FINANCIAL | 100.00 | 99.67 | 113.23 | 122.02 | 139.05 | 149.87 | ||||||

-17-

Table of Contents

The selected financial data presented below for the five fiscal years ended June 29, 2007 have been derived from our Consolidated Financial Statements as audited by our independent registered public accounting firms. The historical financial data are qualified in their entirety by, and should be read in conjunction with, the Consolidated Financial Statements and the notes thereto, and other financial information contained in this report.

The following items, all of which impact the comparability of the data from year-to-year, should be considered: (i) the consolidation into our brokerage operations or discontinuance of the services provided by SWS Technologies Corporation (“SWS Technologies”) in the first quarter of fiscal 2003; (ii) the sale of the accounts of Mydiscountbroker in the fourth quarter of fiscal 2003; (iii) the maturation of the DARTSSM in the first quarter of fiscal 2004; (iv) the closure of May Financial in the second quarter of fiscal 2004; (v) the sale of certain assets of FSB Financial LTD (“FSB Financial”) in the third quarter of fiscal 2006 and (vi) the declaration on November 30, 2006 by our Board of Directors of a 3-for-2 stock split effected in the form of a 50% stock dividend. All references to amounts per share and the number of shares outstanding have been restated to give retroactive effect to the stock split. Additional items that should be considered are included in “Management’s Discussion and Analysis of Financial Condition and Results of Operations -Events and Transactions.” Results for 2003, 2004 and 2005 have been restated to reflect the operations of FSB Financial as discontinued operations. See additional discussion inNote 1(v) in the Notes to the Consolidated Financial Statements contained in this Report.

| Year Ended | ||||||||||||||||

(In thousands, except ratios and per share amounts) | June 29, 2007 | June 30, 2006 | June 24, 2005 | June 25, 2004 | June 27, 2003 | |||||||||||

Consolidated Operating Results: | ||||||||||||||||

Total revenue | $ | 470,898 | $ | 391,618 | $ | 326,799 | $ | 267,649 | $ | 260,019 | ||||||

Net revenue(1) | 273,615 | 252,944 | 249,692 | 235,006 | 220,359 | |||||||||||

Net income (loss) from continuing operations | 37,507 | 28,637 | 28,082 | (190 | ) | 242 | ||||||||||

Net income from discontinued operations | 102 | 12,696 | 3,250 | 3,035 | 2,797 | |||||||||||

Net income | 37,609 | 41,408 | 31,332 | 2,845 | 3,484 | |||||||||||

Earnings per share – basic | ||||||||||||||||

Income (loss) from continuing operations | $ | 1.39 | $ | 1.09 | $ | 1.09 | $ | (0.01 | ) | $ | 0.01 | |||||

Income from discontinued operations | — | 0.49 | 0.12 | 0.12 | 0.10 | |||||||||||

Extraordinary item and cumulative effect of change in accounting principles | — | — | — | — | 0.02 | |||||||||||

Net income | $ | 1.39 | $ | 1.58 | $ | 1.21 | $ | 0.11 | $ | 0.13 | ||||||

Earnings per share – diluted | ||||||||||||||||

Income (loss) from continuing operations | $ | 1.37 | $ | 1.08 | $ | 1.08 | $ | (0.01 | ) | $ | 0.01 | |||||

Income from discontinued operations | 0.01 | 0.49 | 0.12 | 0.12 | 0.10 | |||||||||||

Extraordinary item and cumulative effect of change in accounting principles | — | — | — | — | 0.02 | |||||||||||

Net income | $ | 1.38 | $ | 1.57 | $ | 1.20 | $ | 0.11 | $ | 0.13 | ||||||

Weighted average shares outstanding – basic | 26,972 | 26,162 | 25,819 | 25,653 | 25,524 | |||||||||||

Weighted average shares outstanding – diluted | 27,284 | 26,420 | 26,096 | 25,917 | 25,595 | |||||||||||

Cash dividends declared per common share | $ | 1.30 | $ | .95 | $ | 0.27 | $ | 0.27 | $ | 0 .27 | ||||||

-18-

Table of Contents

| Year Ended | ||||||||||||||||||||

| June 29, 2007 | June 30, 2006 | June 24, 2005 | June 25, 2004 | June 27, 2003 | ||||||||||||||||

Consolidated Financial Condition: | ||||||||||||||||||||

Total assets | $ | 5,074,585 | $ | 4,657,851 | $ | 4,631,144 | $ | 4,740,958 | $ | 4,090,464 | ||||||||||

Long-term debt(2) | 66,989 | 37,341 | 34,808 | 34,990 | 19,795 | |||||||||||||||

Stockholders’ equity | 306,447 | 289,472 | 265,770 | 250,782 | 252,781 | |||||||||||||||

Shares outstanding | 27,492 | 26,592 | 25,995 | 25,665 | 25,436 | |||||||||||||||

Book value per common share | $ | 11.15 | $ | 10.89 | $ | 10.23 | $ | 9.78 | $ | 9.94 | ||||||||||

Bank Performance Ratios: | ||||||||||||||||||||

Return on assets | 1.3 | % | 1.5 | % | 1.2 | % | 0.8 | % | 0.6 | % | ||||||||||

Return on equity | 15.3 | % | 16.1 | % | 13.6 | % | 9.6 | % | 7.1 | % | ||||||||||

Equity to assets ratio | 8.2 | % | 9.6 | % | 8.6 | % | 8.6 | % | 8.2 | % | ||||||||||

| (1) | Net revenue is equal to total revenues less interest expense. |

| (2) | Includes subordinated notes, capital leases and Federal Home Loan Bank advances with maturities in excess of one year. |

-19-

Table of Contents

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL

CONDITION AND RESULTS OF OPERATIONS

OVERVIEW