UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

________

FORM N-CSR

________

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act File Number 811-06400

The Advisors’ Inner Circle Fund

(Exact name of registrant as specified in charter)

________

SEI Investments

One Freedom Valley Drive

Oaks, PA 19456

(Address of principal executive offices) (Zip code)

SEI Investments

One Freedom Valley Drive

Oaks, PA 19456

(Name and address of agent for service)

Registrant’s telephone number, including area code: (877) 446-3863

Date of fiscal year end: October 31, 2024

Date of reporting period: October 31, 2024

| Item 1. | Reports to Stockholders. |

(a) A copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended (the “Act”) (17 CFR § 270.30e-1), is attached hereto.

The Advisors' Inner Circle Fund

LSV Emerging Markets Equity Fund

Institutional Class Shares - LSVZX

Annual Shareholder Report: October 31, 2024

This annual shareholder report contains important information about Institutional Class Shares of the LSV Emerging Markets Equity Fund (the "Fund") for the period from November 1, 2023 to October 31, 2024. You can find additional information about the Fund at https://www.lsvasset.com/emerging-markets-equity-fund/. You can also request this information by contacting us at 888-386-3578.

What were the Fund costs for the last year?

(based on a hypothetical $10,000 investment)

| Fund Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

|---|

| LSV Emerging Markets Equity Fund, Institutional Class Shares | $107 | 0.95% |

How did the Fund perform in the last year?

The global equity market as measured by the MSCI AC World Index was up 32.79% for the twelve months ended October 31, 2024. The U.S. stock market continued to lead global equities, with the S&P 500 up 38.02% over the past year. The U.S. market's dominance in global indices increased further, with its weight in the MSCI AC World Index rising to 64% as of October 31, 2024. Enthusiasm for fast-growing businesses, particularly in the technology sector, remained strong. While the market rewarded the mega-cap growth stocks in the period, value-oriented stocks, and emerging market stocks lagged behind. The MSCI Emerging Markets Index (Net) (USD) was up 25.32%. From a style perspective, emerging markets value stocks (as measured by the MSCI Indices) underperformed growth over the period—the MSCI Emerging Markets Value Index (Net) (USD) was up 22.58% while the MSCI Emerging Markets Growth Index (USD) was up 27.86%. From a sector perspective, Information Technology, Utilities, and Financials stocks outperformed while the Consumer Staples, Materials, and Health Care sectors lagged.

The LSV Emerging Markets Equity Fund Institutional Class Shares was up 25.46% for the period. The portfolio’s deep value bias had a muted impact on relative returns for the period while the portfolio’s smaller capitalization bias relative to the benchmark detracted as large cap stocks across Emerging markets outperformed during the trailing one year. Performance attribution further indicates that stock selection contributed positively to portfolio relative returns for the period while sector selection modestly detracted. Stock selection relative gains were primarily the result of the outperformance of deep value names within the Energy, Industrials, and Materials. Within Energy, holdings in Oil & Gas Exploration & Production, and Integrated Oil & Gas added to returns. Within Industrials, avoiding expensive stocks in Electrical Components & Equipment and holdings in Data Processing & Outsourced Services added to returns. Within Materials, avoiding expensive stocks in Commodity Chemicals, and holdings in Aluminum added to returns. From a sector perspective, relative losses were primarily the result of our underweight positions in the Information Technology sector coupled with an overweight position in the Energy and Materials sector. Top contributors for the year included our overweight positions in Oil India, Power Finance Corporation, REC Limited, Amara Raja Energy & Mobility, Gail, Oracle Financial Services Software, National Aluminum Company, Tencent Music Entertainment, Canara Bank, and Firstsource Solutions. Not owning Wuxi Biologics, NetEase, Samsung Electronics, Saudi Arabian Oil, LG Chem, Posco Holdings, Yum China Holdings, Wal Mart De Mexico, Samsung SDI, and Li Auto also added value. The main individual detractors included our overweight positions in Abu Qir Fertilizers & Chemical Industries, Chennai Petroleum Corporation, Zhongsheng Group, Origin Property, Kimberly-Clark De Mexico, Eastern Company, CSPC Pharmaceutical Group, China Medical System Holdings, China Resources Medical Holdings. Not owning Meituan, Xiaomi, SK Hynix, Bharti Airtel, Trip.Com, China Construction Bank, Mahindra & Mahindra, Trent Limited, ICICI Bank, and Zomato also contributed to losses. Additionally, underweights in Taiwan Semiconductor, Tencent, Hyundai Motor, KB Financial, Indian Oil, Fubon Financial, International Container Terminal Services, Gold Fields, China Railway and Tenaga Nasional Berhad contributed to losses.

The Fund continues to trade at a significant discount to the overall market as well as to the value benchmark. The Fund is trading at 8.5x forward earnings compared to 13.6x for the MSCI Emerging Markets Index (Net) (USD), 1.1x book value compared to 1.8x for the MSCI Emerging Markets Index (Net) (USD) and 6.2x cash flow compared to 11.0x for the MSCI Emerging Markets Index (Net) (USD). Sector weightings are a result of our bottom-up stock selection process, subject to constraints at the sector and industry levels. The Fund is currently overweight Energy, Financials, and Industrials while underweight Information Technology, Consumer Discretionary, and Health Care.

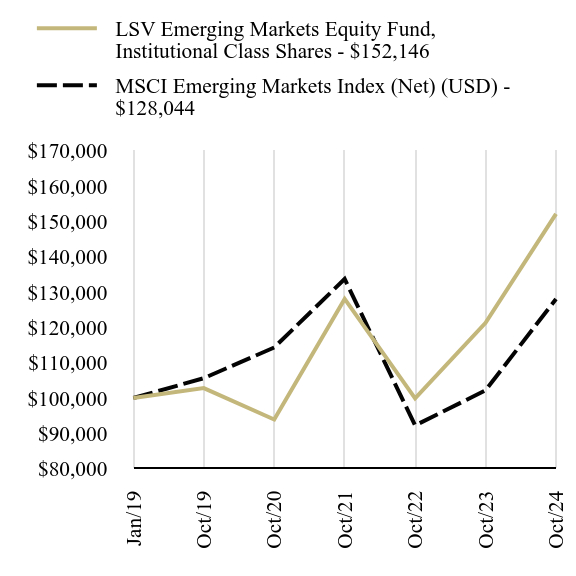

How did the Fund perform since inception?

Total Return Based on $100,000 Investment

| LSV Emerging Markets Equity Fund, Institutional Class Shares - $152146 | MSCI Emerging Markets Index (Net) (USD) - $128044 |

|---|

| Jan/19 | $100000 | $100000 |

| Oct/19 | $102800 | $105599 |

| Oct/20 | $93889 | $114313 |

| Oct/21 | $128042 | $133701 |

| Oct/22 | $99906 | $92218 |

| Oct/23 | $121273 | $102177 |

| Oct/24 | $152146 | $128044 |

Since its inception on January 17, 2019. The line graph represents historical performance of a hypothetical investment of $100,000 in the Fund since inception. Returns shown are total returns, which assume the reinvestment of dividends and capital gains. The table and graph presented above do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. Past performance is not indicative of future performance.Call 888-386-3578 or visit https://www.lsvasset.com/emerging-markets-equity-fund/ for current month-end performance.

Average Annual Total Returns as of October 31, 2024

| Fund/Index Name | 1 Year | 5 Years | Annualized Since Inception |

|---|

| LSV Emerging Markets Equity Fund, Institutional Class Shares | 25.46% | 8.16% | 7.51% |

| MSCI Emerging Markets Index (Net) (USD) | 25.32% | 3.93% | 4.36% |

Key Fund Statistics as of October 31, 2024

| Total Net Assets (000's) | Number of Holdings | Total Advisory Fees Paid (000's) | Portfolio Turnover Rate |

|---|

| $82,685 | 260 | $71 | 13% |

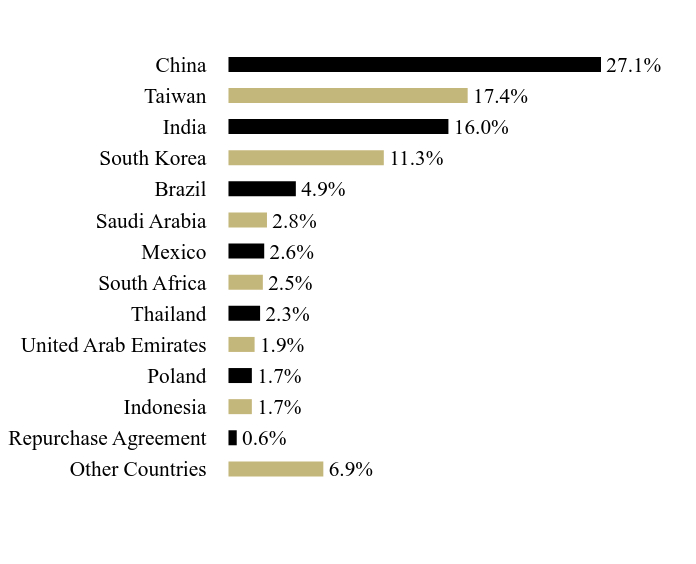

What did the Fund invest in?

Country WeightingsFootnote Reference*

| Value | Value |

|---|

| Other Countries | 6.9% |

| Repurchase Agreement | 0.6% |

| Indonesia | 1.7% |

| Poland | 1.7% |

| United Arab Emirates | 1.9% |

| Thailand | 2.3% |

| South Africa | 2.5% |

| Mexico | 2.6% |

| Saudi Arabia | 2.8% |

| Brazil | 4.9% |

| South Korea | 11.3% |

| India | 16.0% |

| Taiwan | 17.4% |

| China | 27.1% |

| Footnote | Description |

Footnote* | Percentages are calculated based on total net assets. |

| Holding Name | | | Percentage of Total Net Assets |

|---|

| Alibaba Group Holding | | | 3.1% |

| Taiwan Semiconductor Manufacturing | | | 3.0% |

| JD.com, Cl A | | | 1.8% |

| Tencent Holdings | | | 1.6% |

| Samsung Electronics | | | 1.5% |

| MediaTek | | | 1.5% |

| Hon Hai Precision Industry | | | 1.3% |

| CTBC Financial Holding | | | 1.2% |

| Oil & Natural Gas | | | 1.1% |

| Kia | | | 0.9% |

There were no material changes during the reporting period.

Changes in and Disagreements with Accountants

There were no changes in or disagreements with accountants during the reporting period.

For additional information about the Fund, including its prospectus, financial information, holdings, and proxy voting information, call or visit:

Rule 30e-1 of the Investment Company Act of 1940 permits funds to transmit only one copy of a proxy statement, annual report or semi-annual report to shareholders (who need not be related) with the same residential, commercial or electronic address, provided that the shareholders have consented in writing and the reports are addressed either to each shareholder individually or to the shareholders as a group. This process is known as “householding” and is designed to reduce the duplicate copies of materials that shareholders receive and to lower printing and mailing costs for funds. Once implemented, if you would like to discontinue householding for your accounts, please call toll-free at 888-386-3578 to request individual copies of these documents. Once the Fund receives notice to stop householding, we will begin sending individual copies 30 days after receiving your request.

The Advisors' Inner Circle Fund

LSV Emerging Markets Equity Fund / Institutional Class Shares - LSVZX

Annual Shareholder Report: October 31, 2024

LSV-AR-TSR-2024-3

The Advisors' Inner Circle Fund

LSV Emerging Markets Equity Fund

Investor Class Shares - LVAZX

Annual Shareholder Report: October 31, 2024

This annual shareholder report contains important information about Investor Class Shares of the LSV Emerging Markets Equity Fund (the "Fund") for the period from November 1, 2023 to October 31, 2024. You can find additional information about the Fund at https://www.lsvasset.com/emerging-markets-equity-fund/. You can also request this information by contacting us at 888-386-3578.

What were the Fund costs for the last year?

(based on a hypothetical $10,000 investment)

| Fund Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

|---|

| LSV Emerging Markets Equity Fund, Investor Class Shares | $135 | 1.20% |

How did the Fund perform in the last year?

The global equity market as measured by the MSCI AC World Index was up 32.79% for the twelve months ended October 31, 2024. The U.S. stock market continued to lead global equities, with the S&P 500 Index up 38.02% over the past year. The U.S. market's dominance in global indices increased further, with its weight in the MSCI AC World Index rising to 64% as of October 31, 2024. Enthusiasm for fast-growing businesses, particularly in the technology sector, remained strong. While the market rewarded the mega-cap growth stocks in the period, value-oriented stocks, and emerging market stocks lagged behind. The MSCI Emerging Markets Index (Net) (USD) was up 25.32%. From a style perspective, emerging markets value stocks (as measured by the MSCI Indices) underperformed growth over the period—the MSCI Emerging Markets Value Index (USD) was up 22.58% while the MSCI Emerging Markets Growth Index (USD) was up 27.86%. From a sector perspective, Information Technology, Utilities, and Financials stocks outperformed while the Consumer Staples, Materials, and Health Care sectors lagged.

The LSV Emerging Markets Equity Fund Investor Class Shares was up 25.30% for the period. The portfolio’s deep value bias had a muted impact on relative returns for the period while the portfolio’s smaller capitalization bias relative to the benchmark detracted as large cap stocks across Emerging markets outperformed during the trailing one year. Performance attribution further indicates that stock selection contributed positively to portfolio relative returns for the period while sector selection modestly detracted. Stock selection relative gains were primarily the result of the outperformance of deep value names within the Energy, Industrials, and Materials. Within Energy, holdings in Oil & Gas Exploration & Production, and Integrated Oil & Gas added to returns. Within Industrials, avoiding expensive stocks in Electrical Components & Equipment and holdings in Data Processing & Outsourced Services added to returns. Within Materials, avoiding expensive stocks in Commodity Chemicals, and holdings in Aluminum added to returns. From a sector perspective, relative losses were primarily the result of our underweight positions in the Information Technology sector coupled with an overweight position in the Energy and Materials sector. Top contributors for the year included our overweight positions in Oil India, Power Finance Corporation, REC Limited, Amara Raja Energy & Mobility, Gail, Oracle Financial Services Software, National Aluminum Company, Tencent Music Entertainment, Canara Bank, and Firstsource Solutions. Not owning Wuxi Biologics, NetEase, Samsung Electronics, Saudi Arabian Oil, LG Chem, Posco Holdings, Yum China Holdings, Wal Mart De Mexico, Samsung SDI, and Li Auto also added value. The main individual detractors included our overweight positions in Abu Qir Fertilizers & Chemical Industries, Chennai Petroleum Corporation, Zhongsheng Group, Origin Property, Kimberly-Clark De Mexico, Eastern Company, CSPC Pharmaceutical Group, China Medical System Holdings, China Resources Medical Holdings. Not owning Meituan, Xiaomi, SK Hynix, Bharti Airtel, Trip.Com, China Construction Bank, Mahindra & Mahindra, Trent Limited, ICICI Bank, and Zomato also contributed to losses. Additionally, underweights in Taiwan Semiconductor, Tencent, Hyundai Motor, KB Financial, Indian Oil, Fubon Financial, International Container Terminal Services, Gold Fields, China Railway and Tenaga Nasional Berhad contributed to losses.

The Fund continues to trade at a significant discount to the overall market as well as to the value benchmark. The Fund is trading at 8.5x forward earnings compared to 13.6x for the MSCI Emerging Markets Index (Net) (USD), 1.1x book value compared to 1.8x for the MSCI Emerging Markets Index(Net) (USD) and 6.2x cash flow compared to 11.0x for the MSCI Emerging Markets Index (Net) (USD). Sector weightings are a result of our bottom-up stock selection process, subject to constraints at the sector and industry levels. The Fund is currently overweight Energy, Financials, and Industrials while underweight Information Technology, Consumer Discretionary, and Health Care.

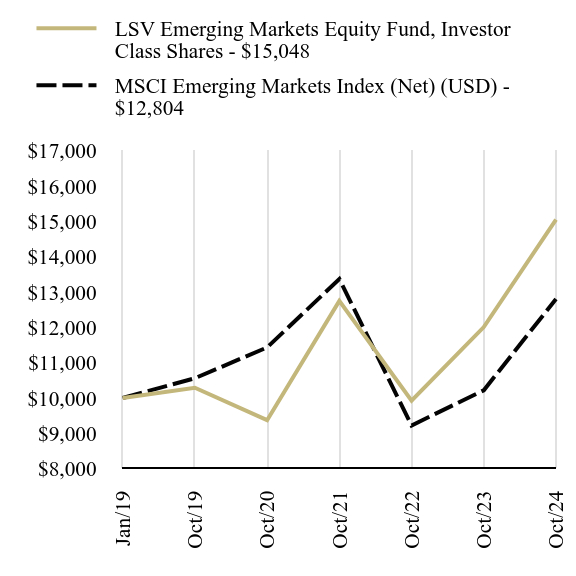

How did the Fund perform since inception?

Total Return Based on $10,000 Investment

| LSV Emerging Markets Equity Fund, Investor Class Shares - $15048 | MSCI Emerging Markets Index (Net) (USD) - $12804 |

|---|

| Jan/19 | $10000 | $10000 |

| Oct/19 | $10290 | $10560 |

| Oct/20 | $9372 | $11431 |

| Oct/21 | $12751 | $13370 |

| Oct/22 | $9923 | $9222 |

| Oct/23 | $12009 | $10218 |

| Oct/24 | $15048 | $12804 |

Since its inception on January 17, 2019. The line graph represents historical performance of a hypothetical investment of $10,000 in the Fund since inception. Returns shown are total returns, which assume the reinvestment of dividends and capital gains. The table and graph presented above do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. Past performance is not indicative of future performance.Call 888-386-3578 or visit https://www.lsvasset.com/emerging-markets-equity-fund/ for current month-end performance.

Average Annual Total Returns as of October 31, 2024

| Fund/Index Name | 1 Year | 5 Years | Annualized Since Inception |

|---|

| LSV Emerging Markets Equity Fund, Investor Class Shares | 25.30% | 7.90% | 7.31% |

| MSCI Emerging Markets Index (Net) (USD) | 25.32% | 3.93% | 4.36% |

Key Fund Statistics as of October 31, 2024

| Total Net Assets (000's) | Number of Holdings | Total Advisory Fees Paid (000's) | Portfolio Turnover Rate |

|---|

| $82,685 | 260 | $71 | 13% |

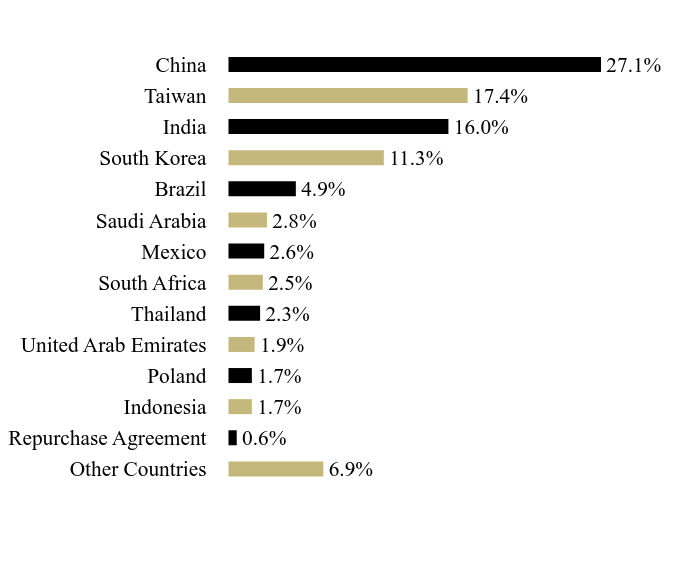

What did the Fund invest in?

Country WeightingsFootnote Reference*

| Value | Value |

|---|

| Other Countries | 6.9% |

| Repurchase Agreement | 0.6% |

| Indonesia | 1.7% |

| Poland | 1.7% |

| United Arab Emirates | 1.9% |

| Thailand | 2.3% |

| South Africa | 2.5% |

| Mexico | 2.6% |

| Saudi Arabia | 2.8% |

| Brazil | 4.9% |

| South Korea | 11.3% |

| India | 16.0% |

| Taiwan | 17.4% |

| China | 27.1% |

| Footnote | Description |

Footnote* | Percentages are calculated based on total net assets. |

| Holding Name | | | Percentage of Total Net Assets |

|---|

| Alibaba Group Holding | | | 3.1% |

| Taiwan Semiconductor Manufacturing | | | 3.0% |

| JD.com, Cl A | | | 1.8% |

| Tencent Holdings | | | 1.6% |

| Samsung Electronics | | | 1.5% |

| MediaTek | | | 1.5% |

| Hon Hai Precision Industry | | | 1.3% |

| CTBC Financial Holding | | | 1.2% |

| Oil & Natural Gas | | | 1.1% |

| Kia | | | 0.9% |

There were no material changes during the reporting period.

Changes in and Disagreements with Accountants

There were no changes in or disagreements with accountants during the reporting period.

For additional information about the Fund, including its prospectus, financial information, holdings, and proxy voting information, call or visit:

Rule 30e-1 of the Investment Company Act of 1940 permits funds to transmit only one copy of a proxy statement, annual report or semi-annual report to shareholders (who need not be related) with the same residential, commercial or electronic address, provided that the shareholders have consented in writing and the reports are addressed either to each shareholder individually or to the shareholders as a group. This process is known as “householding” and is designed to reduce the duplicate copies of materials that shareholders receive and to lower printing and mailing costs for funds. Once implemented, if you would like to discontinue householding for your accounts, please call toll-free at 888-386-3578 to request individual copies of these documents. Once the Fund receives notice to stop householding, we will begin sending individual copies 30 days after receiving your request.

The Advisors' Inner Circle Fund

LSV Emerging Markets Equity Fund / Investor Class Shares - LVAZX

Annual Shareholder Report: October 31, 2024

LSV-AR-TSR-2024-4

(b) Not applicable.

The Registrant (also referred to as the “Trust”) has adopted a code of ethics that applies to the Registrant’s principal executive officer, principal financial officer, controller or principal accounting officer, and any person who performs a similar function. There have been no amendments to or waivers granted to this code of ethics during the period covered by this report.

| Item 3. | Audit Committee Financial Expert. |

(a)(1) The Registrant’s board of trustees has determined that the Registrant has at least one audit committee financial expert serving on the audit committee.

(a)(2) The Registrant’s audit committee financial expert is Robert Mulhall. Mr. Mulhall is considered to be “independent”, as that term is defined in Form N-CSR Item 3(a)(2).

| Item 4. | Principal Accountant Fees and Services. |

Fees billed by PricewaterhouseCoopers LLP (“PwC”) related to the Trust.

PwC billed the Trust aggregate fees for services rendered to the Trust for the last two fiscal years as follows:

| | FYE October 31, 2024 | FYE October 31, 2023 |

| | | All fees and services to the Trust that were pre-approved | All fees and services to service affiliates that were pre-approved | All other fees and services to service affiliates that did not require pre-approval | All fees and services to the Trust that were pre-approved | All fees and services to service affiliates that were pre-approved | All other fees and services to service affiliates that did not require pre-approval |

| (a) | Audit Fees(1) | $91,274 | None | None | $72,710 | None | None |

| (b) | Audit-Related Fees | None | None | None | None | None | None |

| (c) | Tax Fees | None | None | None | None | None | $115,395(2) |

| (d) | All Other Fees | None | None | None | None | None | $47,411(3) |

Fees billed by Ernst & Young LLP (“E&Y”) related to the Trust.

E&Y billed the Trust aggregate fees for services rendered to the Trust for the last two fiscal years as follows:

| | FYE October 31, 2024 | FYE October 31, 2023 |

| | | All fees and services to the Trust that were pre-approved | All fees and services to service affiliates that were pre-approved | All other fees and services to service affiliates that did not require pre-approval | All fees and services to the Trust that were pre-approved | All fees and services to service affiliates that were pre-approved | All other fees and services to service affiliates that did not require pre-approval |

| (a) | Audit Fees(1) | $539,063 | None | None | $550,800 | None | None |

| (b) | Audit-Related Fees | None | None | None | None | None | None |

| (c) | Tax Fees | None | None | None | None | None | None |

| (d) | All Other Fees | None | None | None | None | None | None |

Fees billed by Cohen & Co. (“Cohen”) related to the Trust.

Cohen billed the Trust aggregate fees for services rendered to the Trust for the last two fiscal years as follows:

| | FYE October 31, 2024 | FYE October 31, 2023 |

| | | All fees and services to the Trust that were pre-approved | All fees and services to service affiliates that were pre-approved | All other fees and services to service affiliates that did not require pre-approval | All fees and services to the Trust that were pre-approved | All fees and services to service affiliates that were pre-approved | All other fees and services to service affiliates that did not require pre-approval |

| (a) | Audit Fees(1) | $43,700 | None | None | $61,000 | None | None |

| (b) | Audit-Related Fees | None | None | None | None | None | None |

| (c) | Tax Fees | None | None | None | None | None | None |

| (d) | All Other Fees | None | None | None | None | None | None |

Notes:

| (1) | Audit fees include amounts related to the audit of the Trust’s annual financial statements and services normally provided by the accountant in connection with statutory and regulatory filings. |

| (2) | Tax compliance services provided to service affiliates of the funds. |

| (3) | Non-audit assurance engagements for service affiliates of the funds. |

(e)(1) The Trust’s Audit Committee has adopted and the Board of Trustees has ratified an Audit and Non-Audit Services Pre-Approval Policy (the “Policy”), which sets forth the procedures and the conditions pursuant to which services proposed to be performed by the independent auditor of the Funds may be pre-approved.

The Policy provides that all requests or applications for proposed services to be provided by the independent auditor must be submitted to the Registrant’s Chief Financial Officer (“CFO”) and must include a detailed description of the services proposed to be rendered. The CFO will determine whether such services:

| (1) | require specific pre-approval; |

| (2) | are included within the list of services that have received the general pre-approval of the Audit Committee pursuant to the Policy; or |

| (3) | have been previously pre-approved in connection with the independent auditor’s annual engagement letter for the applicable year or otherwise. In any instance where services require pre-approval, the Audit Committee will consider whether such services are consistent with SEC’s rules and whether the provision of such services would impair the auditor’s independence. |

Requests or applications to provide services that require specific pre-approval by the Audit Committee will be submitted to the Audit Committee by the CFO. The Audit Committee will be informed by the CFO on a quarterly basis of all services rendered by the independent auditor. The Audit Committee has delegated specific pre-approval authority to either the Audit Committee Chair or financial expert, provided that the estimated fee for any such proposed pre-approved service does not exceed $100,000 and any pre-approval decisions are reported to the Audit Committee at its next regularly-scheduled meeting.

Services that have received the general pre-approval of the Audit Committee are identified and described in the Policy. In addition, the Policy sets forth a maximum fee per engagement with respect to each identified service that has received general pre-approval.

All services to be provided by the independent auditor shall be provided pursuant to a signed written engagement letter with the Registrant, the investment adviser, or applicable control affiliate (except that matters as to which an engagement letter would be impractical because of timing issues or because the matter is small may not be the subject of an engagement letter) that sets forth both the services to be provided by the independent auditor and the total fees to be paid to the independent auditor for those services.

In addition, the Audit Committee has determined to take additional measures on an annual basis to meet the Audit Committee’s responsibility to oversee the work of the independent auditor and to assure the auditor's independence from the Registrant, such as (a) reviewing a formal written statement from the independent auditor delineating all relationships between the independent auditor and the Registrant, and (b) discussing with the independent auditor the independent auditor’s methods and procedures for ensuring independence.

(e)(2) Percentage of fees billed applicable to non-audit services pursuant to waiver of pre-approval requirement were as follows (PwC):

| | 2024 | 2023 |

Audit-Related Fees | None | None |

| Tax Fees | None | None |

All Other Fees | None | None |

(e)(2) Percentage of fees billed applicable to non-audit services pursuant to waiver of pre-approval requirement were as follows (E&Y):

| | 2024 | 2023 |

Audit-Related Fees | None | None |

| Tax Fees | None | None |

All Other Fees | None | None |

(e)(2) Percentage of fees billed applicable to non-audit services pursuant to waiver of pre-approval requirement were as follows (Cohen):

| | 2024 | 2023 |

Audit-Related Fees | None | None |

| Tax Fees | None | None |

All Other Fees | None | None |

(f) Not applicable.

(g) The aggregate non-audit fees and services billed by PwC for services rendered to the Registrant, and rendered to the Registrant’s investment adviser (not including any sub-adviser whose role is primarily portfolio management and is subcontracted with or overseen by another investment adviser), and any entity controlling, controlled by, or under common control with the adviser that provides ongoing services to the Registrant for the last two fiscal-years-ended October 31st were $0 and $162,806 for 2024 and 2023, respectively.

(g) The aggregate non-audit fees and services billed by E&Y for services rendered to the Registrant, and rendered to the Registrant’s investment adviser (not including any sub-adviser whose role is primarily portfolio management and is subcontracted with or overseen by another investment adviser), and any entity controlling, controlled by, or under common control with the adviser that provides ongoing services to the Registrant for the last two fiscal-years-ended October 31st were $0 and $0 for 2024 and 2023, respectively.

(g) The aggregate non-audit fees and services billed by Cohen for services rendered to the Registrant, and rendered to the Registrant’s investment adviser (not including any sub-adviser whose role is primarily portfolio management and is subcontracted with or overseen by another investment adviser), and any entity controlling, controlled by, or under common control with the adviser that provides ongoing services to the Registrant for the last two fiscal-years-ended October 31st were $0 and $0 for 2024 and 2023, respectively.

(h) During the past fiscal year, all non-audit services provided by the Registrant’s principal accountant to either the Registrant’s investment adviser or to any entity controlling, controlled by, or under common control with the Registrant’s investment adviser that provides ongoing services to the Registrant were pre-approved by the Audit Committee of Registrant’s Board of Trustees. Included in the Audit Committee’s pre-approval of these non-audit service were the review and consideration as to whether the provision of these non-audit services is compatible with maintaining the principal accountant’s independence.

(i) Not Applicable. The Registrant has not retained, for the preparation of the audit report on the financial statements included in the Form N-CSR, a registered public accounting firm that has a branch or office that is located in a foreign jurisdiction and that the Public Company Accounting Oversight Board (the “PCAOB”) has determined that the PCAOB is unable to inspect or investigate completely because of a position taken by an authority in the foreign jurisdiction.

(j) Not applicable. The Registrant is not a “foreign issuer,” as defined in 17 CFR § 240.3b-4.

| Item 5. | Audit Committee of Listed Registrants. |

Not applicable to open-end management investment companies.

| Item 6. | Schedule of Investments. |

(a) The Schedule of Investments is included as part of the Financial Statements and Other Information filed under Item 7 of this form.

(b) Not applicable.

| Item 7. | Financial Statements and Financial Highlights for Open-End Management Investment Companies. |

Financial statements and financial highlights are filed herein.

THE ADVISORS’ INNER CIRCLE FUND

Emerging Markets Equity Fund

ANNUAL FINANCIALS AND OTHER INFORMATION

October 31, 2024

This information must be preceded or accompanied by a current prospectus. Investors should read the prospectus carefully before investing.

| THE ADVISORS’ INNER CIRCLE FUND | LSV

Emerging Markets Equity Fund

October 31, 2024 |

TABLE OF CONTENTS

| Financial Statements (Form N-CSR Item 7) | |

| Schedule of Investments | 1 |

| Statement of Assets and Liabilities | 6 |

| Statement of Operations | 7 |

| Statements of Changes in Net Assets | 8 |

| Financial Highlights | 9 |

| Notes to Financial Statements | 10 |

| Report of Independent Registered Public Accounting Firm | 17 |

| Notice to Shareholders (Unaudited) | 18 |

Schedule of Investments

October 31, 2024

| LSV Emerging Markets Equity Fund |

| | | Shares | | | Value (000) | |

| Foreign Common Stock (96.8%) |

| Brazil (3.0%) |

| Ambev | | | 140,200 | | | $ | 306 | |

| Banco do Brasil | | | 80,300 | | | | 365 | |

| Camil Alimentos | | | 44,100 | | | | 60 | |

| Cia de Saneamento de Minas Gerais Copasa MG | | | 88,900 | | | | 354 | |

| JBS S | | | 47,500 | | | | 297 | |

| Telefonica Brasil | | | 42,000 | | | | 383 | |

| Vale | | | 50,700 | | | | 543 | |

| Vibra Energia | | | 55,200 | | | | 213 | |

| | | | | | | | 2,521 | |

| | | | | | | | | |

| Chile (0.2%) |

| Cencosud | | | 67,000 | | | | 139 | |

| | | | | | | | | |

| China (27.1%) |

| 3SBio | | | 457,000 | | | | 343 | |

| Alibaba Group Holding | | | 210,100 | | | | 2,569 | |

| AviChina Industry & Technology, Cl H | | | 637,000 | | | | 342 | |

| BAIC Motor, Cl H | | | 305,500 | | | | 84 | |

| Baidu, Cl A* | | | 35,100 | | | | 401 | |

| Bank of China, Cl H | | | 934,000 | | | | 443 | |

| Bank of Communications, Cl H | | | 385,000 | | | | 292 | |

| Beijing Enterprises Holdings | | | 22,500 | | | | 74 | |

| Bosideng International Holdings | | | 496,000 | | | | 278 | |

| BYD Electronic International | | | 66,000 | | | | 283 | |

| China CITIC Bank, Cl H | | | 263,000 | | | | 164 | |

| China Coal Energy, Cl H | | | 289,000 | | | | 361 | |

| China Everbright Bank, Cl H | | | 817,000 | | | | 276 | |

| China Feihe | | | 589,000 | | | | 445 | |

| China Hongqiao Group | | | 291,500 | | | | 468 | |

| China Medical System Holdings | | | 124,000 | | | | 124 | |

| China Merchants Port Holdings | | | 96,000 | | | | 158 | |

| China Minsheng Banking, Cl H | | | 254,000 | | | | 94 | |

| China Nonferrous Mining | | | 141,000 | | | | 100 | |

| China Pacific Insurance Group, Cl H | | | 164,200 | | | | 570 | |

| China Petroleum & Chemical, Cl H | | | 446,000 | | | | 251 | |

| China Railway Signal & Communication, Cl H | | | 733,000 | | | | 302 | |

| China Suntien Green Energy, Cl H | | | 463,000 | | | | 211 | |

| China Tower, Cl H | | | 3,806,000 | | | | 514 | |

| China XLX Fertiliser | | | 128,000 | | | | 67 | |

| CSPC Pharmaceutical Group | | | 478,000 | | | | 354 | |

| LSV Emerging Markets Equity Fund |

| | | Shares | | | Value (000) | |

| China (continued) |

| Far East Horizon | | | 91,000 | | | $ | 64 | |

| First Tractor, Cl H | | | 384,000 | | | | 343 | |

| Great Wall Motor, Cl H | | | 191,000 | | | | 304 | |

| Guangzhou Baiyunshan Pharmaceutical Holdings, Cl H | | | 22,000 | | | | 52 | |

| Haier Smart Home, Cl H | | | 124,600 | | | | 452 | |

| Hello Group ADR | | | 46,900 | | | | 332 | |

| Hengan International Group | | | 97,000 | | | | 286 | |

| JD.com, Cl A | | | 72,400 | | | | 1,468 | |

| Jiangxi Copper, Cl H | | | 208,000 | | | | 350 | |

| JOYY ADR | | | 9,300 | | | | 317 | |

| Kunlun Energy | | | 360,000 | | | | 341 | |

| Lenovo Group | | | 416,000 | | | | 549 | |

| Lonking Holdings | | | 152,000 | | | | 29 | |

| New China Life Insurance, Cl H | | | 150,100 | | | | 507 | |

| Orient Overseas International | | | 19,000 | | | | 259 | |

| People's Insurance Group of China, Cl H | | | 886,000 | | | | 447 | |

| PetroChina, Cl H | | | 636,000 | | | | 478 | |

| PICC Property & Casualty, Cl H | | | 240,000 | | | | 364 | |

| Ping An Insurance Group of China, Cl H | | | 65,500 | | | | 406 | |

| Postal Savings Bank of China, Cl H | | | 561,000 | | | | 322 | |

| Shougang Fushan Resources Group | | | 210,000 | | | | 76 | |

| Sinopec Engineering Group, Cl H | | | 459,000 | | | | 319 | |

| Sinopharm Group, Cl H | | | 120,000 | | | | 299 | |

| Sinotrans, Cl H | | | 476,000 | | | | 213 | |

| Sinotruk Hong Kong | | | 172,000 | | | | 464 | |

| SITC International Holdings | | | 111,000 | | | | 314 | |

| TCL Electronics Holdings | | | 212,000 | | | | 150 | |

| Tencent Holdings | | | 26,000 | | | | 1,356 | |

| Vipshop Holdings ADR | | | 15,200 | | | | 219 | |

| Want Want China Holdings | | | 497,000 | | | | 309 | |

| Weichai Power, Cl H | | | 175,000 | | | | 264 | |

| Xtep International Holdings | | | 342,000 | | | | 254 | |

| Yangzijiang Shipbuilding Holdings | | | 143,600 | | | | 279 | |

| Zhengzhou Coal Mining Machinery Group, Cl H | | | 157,200 | | | | 210 | |

| Zhongsheng Group Holdings | | | 43,500 | | | | 67 | |

| ZTE, Cl H | | | 143,400 | | | | 357 | |

| | | | | | | 22,388 | |

| | | | | | | | | |

| Egypt (0.3%) |

| Abou Kir Fertilizers & Chemical Industries | | | 112,500 | | | | 131 | |

The accompanying notes are an integral part of the financial statements

Schedule of Investments

October 31, 2024

| LSV Emerging Markets Equity Fund |

| | | Shares | | | Value (000) | |

| Egypt (continued) |

| Eastern SAE | | | 157,533 | | | $ | 88 | |

| | | | | | | | 219 | |

| | | | | | | | | |

| Greece (1.1%) |

| Hellenic Telecommunications Organization | | | 19,000 | | | | 314 | |

| Motor Oil Hellas Corinth Refineries | | | 13,100 | | | | 280 | |

| National Bank of Greece | | | 35,100 | | | | 275 | |

| | | | | | | | 869 | |

| | | | | | | | | |

| Hong Kong (0.8%) |

| Dongfang Electric, Cl H | | | 191,800 | | | | 252 | |

| Grand Pharmaceutical Group | | | 400,000 | | | | 234 | |

| Kingboard Laminates Holdings | | | 66,000 | | | | 57 | |

| SSY Group | | | 224,000 | | | | 109 | |

| | | | | | | | 652 | |

| | | | | | | | | |

| Hungary (0.9%) |

| Magyar Telekom Telecommunications | | | 87,700 | | | | 269 | |

| MOL Hungarian Oil & Gas | | | 10,900 | | | | 76 | |

| OTP Bank Nyrt | | | 7,800 | | | | 387 | |

| | | | | | | | 732 | |

| | | | | | | | | |

| India (16.0%) |

| Amara Raja Energy & Mobility | | | 7,900 | | | | 130 | |

| Aurobindo Pharma | | | 2,998 | | | | 50 | |

| Bank of Baroda | | | 227,600 | | | | 677 | |

| Bank of India | | | 226,400 | | | | 291 | |

| Bharat Petroleum | | | 161,800 | | | | 597 | |

| Canara Bank | | | 484,000 | | | | 588 | |

| CESC | | | 101,200 | | | | 226 | |

| Chambal Fertilisers and Chemicals | | | 77,400 | | | | 443 | |

| Chennai Petroleum | | | 48,900 | | | | 370 | |

| Coal India | | | 133,500 | | | | 717 | |

| EID Parry India | | | 8,600 | | | | 82 | |

| Firstsource Solutions | | | 21,900 | | | | 88 | |

| GAIL India | | | 65,800 | | | | 156 | |

| General Insurance Corp of India | | | 46,700 | | | | 204 | |

| Great Eastern Shipping | | | 31,000 | | | | 473 | |

| Gujarat Narmada Valley Fertilizers & Chemicals | | | 11,800 | | | | 88 | |

| Gujarat State Fertilizers & Chemicals | | | 50,600 | | | | 125 | |

| HCL Technologies | | | 13,000 | | | | 272 | |

| Hindalco Industries | | | 57,100 | | | | 463 | |

| Indian Bank | | | 73,700 | | | | 519 | |

| Indian Oil | | | 152,700 | | | | 257 | |

| Jindal Saw | | | 45,400 | | | | 170 | |

| LSV Emerging Markets Equity Fund |

| | | Shares | | | Value (000) | |

| India (continued) |

| JK Paper | | | 58,700 | | | $ | 321 | |

| JK Tyre & Industries | | | 50,400 | | | | 237 | |

| LIC Housing Finance | | | 55,700 | | | | 417 | |

| Mahanagar Gas | | | 6,973 | | | | 119 | |

| Maharashtra Seamless | | | 31,800 | | | | 236 | |

| Manappuram Finance | | | 130,300 | | | | 242 | |

| National Aluminium | | | 150,500 | | | | 404 | |

| NMDC | | | 214,400 | | | | 563 | |

| NMDC Steel* | | | 44,900 | | | | 25 | |

| Oil & Natural Gas | | | 277,300 | | | | 876 | |

| Oil India | | | 56,900 | | | | 319 | |

| Petronet LNG | | | 130,500 | | | | 515 | |

| Power Finance | | | 44,400 | | | | 239 | |

| Power Grid Corp of India | | | 62,000 | | | | 236 | |

| PTC India | | | 99,100 | | | | 214 | |

| REC | | | 41,400 | | | | 256 | |

| Redington | | | 64,800 | | | | 149 | |

| Sun TV Network | | | 29,100 | | | | 260 | |

| Union Bank of India | | | 137,800 | | | | 191 | |

| Vedanta | | | 82,900 | | | | 456 | |

| | | | | | | 13,261 | |

| | | | | | | | | |

| Indonesia (1.7%) |

| Astra International | | | 1,335,000 | | | | 433 | |

| Bank Negara Indonesia Persero | | | 913,800 | | | | 305 | |

| Bukit Asam | | | 279,400 | | | | 53 | |

| Telkom Indonesia Persero | | | 1,803,100 | | | | 322 | |

| United Tractors | | | 186,100 | | | | 325 | |

| | | | | | | 1,438 | |

| | | | | | | | | |

| Kuwait (0.3%) |

| Mobile Telecommunications KSCP | | | 189,200 | | | | 281 | |

| | | | | | | | | |

| Malaysia (1.4%) |

| AMMB Holdings | | | 338,000 | | | | 392 | |

| CIMB Group Holdings | | | 222,400 | | | | 403 | |

| RHB Bank | | | 110,000 | | | | 161 | |

| Scientex | | | 64,200 | | | | 65 | |

| Sime Darby | | | 199,000 | | | | 105 | |

| | | | | | | 1,126 | |

| | | | | | | | | |

| Mexico (2.6%) |

| America Movil | | | 453,100 | | | | 358 | |

| Cemex | | | 208,200 | | | | 109 | |

| Coca-Cola Femsa | | | 26,300 | | | | 218 | |

| Fibra Uno Administracion‡ | | | 55,800 | | | | 64 | |

| Genomma Lab Internacional, Cl B | | | 230,400 | | | | 309 | |

| Grupo Financiero Banorte, Cl O | | | 18,700 | | | | 131 | |

| Grupo Mexico | | | 75,800 | | | | 397 | |

| Kimberly-Clark de Mexico, Cl A | | | 196,200 | | | | 283 | |

The accompanying notes are an integral part of the financial statements

Schedule of Investments

October 31, 2024

| LSV Emerging Markets Equity Fund |

| | | Shares | | | Value (000) | |

| Mexico (continued) |

| Megacable Holdings | | | 133,800 | | | $ | 295 | |

| | | | | | | | 2,164 | |

| | | | | | | | | |

| Philippines (0.7%) |

| DMCI Holdings | | | 460,100 | | | | 88 | |

| Metropolitan Bank & Trust | | | 391,300 | | | | 511 | |

| | | | | | | | 599 | |

| | | | | | | | | |

| Poland (1.7%) |

| Asseco Poland | | | 12,640 | | | | 284 | |

| Orange Polska | | | 146,000 | | | | 284 | |

| ORLEN | | | 10,400 | | | | 136 | |

| Powszechna Kasa Oszczednosci Bank Polski | | | 36,900 | | | | 512 | |

| Powszechny Zaklad Ubezpieczen | | | 23,100 | | | | 229 | |

| | | | | | | | 1,445 | |

| | | | | | | | | |

| Russia (–%) |

| Gazprom PJSC(A),(B)* | | | 11,300 | | | | — | |

| GMK Norilskiy Nickel PAO(A),(B) | | | 37,000 | | | | — | |

| LUKOIL PJSC(A),(B) | | | 2,300 | | | | — | |

| Magnit PJSC(A),(B) | | | 1,000 | | | | — | |

| Mobile TeleSystems PJSC(A),(B) | | | 13,800 | | | | — | |

| | | | | | | | — | |

| | | | | | | | | |

| Saudi Arabia (2.8%) |

| Al Babtain Power & Telecommunication | | | 25,600 | | | | 304 | |

| Arab National Bank | | | 103,300 | | | | 519 | |

| Banque Saudi Fransi | | | 33,300 | | | | 276 | |

| Etihad Etisalat | | | 33,400 | | | | 460 | |

| Saudi Awwal Bank | | | 57,300 | | | | 516 | |

| Saudi Investment Bank | | | 65,600 | | | | 230 | |

| | | | | | | | 2,305 | |

| | | | | | | | | |

| South Africa (2.5%) |

| Absa Group | | | 16,500 | | | | 158 | |

| African Rainbow Minerals | | | 9,700 | | | | 98 | |

| Astral Foods* | | | 2,135 | | | | 21 | |

| Exxaro Resources | | | 24,600 | | | | 232 | |

| Foschini Group | | | 19,200 | | | | 167 | |

| Gold Fields | | | 19,000 | | | | 313 | |

| Impala Platinum Holdings* | | | 23,500 | | | | 155 | |

| MTN Group | | | 19,400 | | | | 96 | |

| Nedbank Group | | | 19,600 | | | | 333 | |

| Oceana Group | | | 16,600 | | | | 64 | |

| Tiger Brands | | | 9,929 | | | | 134 | |

| Vodacom Group | | | 52,700 | | | | 330 | |

| | | | | | | | 2,101 | |

| | | | | | | | | |

| South Korea (11.3%) |

| BGF retail | | | 800 | | | | 67 | |

| LSV Emerging Markets Equity Fund |

| | | Shares | | | Value (000) | |

| South Korea (continued) |

| DB HiTek | | | 9,800 | | | $ | 273 | |

| DB Insurance | | | 4,300 | | | | 339 | |

| Doosan Bobcat | | | 10,700 | | | | 288 | |

| Hana Financial Group | | | 8,000 | | | | 345 | |

| Hankook Tire & Technology | | | 10,500 | | | | 267 | |

| Hyundai Glovis | | | 4,100 | | | | 361 | |

| Hyundai Marine & Fire Insurance | | | 11,900 | | | | 261 | |

| Hyundai Motor | | | 3,500 | | | | 539 | |

| JB Financial Group | | | 29,100 | | | | 378 | |

| KB Financial Group | | | 4,900 | | | | 319 | |

| Kia | | | 11,400 | | | | 754 | |

| KT | | | 12,600 | | | | 402 | |

| KT&G | | | 4,800 | | | | 381 | |

| LG | | | 2,800 | | | | 153 | |

| LG Innotek | | | 1,700 | | | | 216 | |

| Lotte Chilsung Beverage | | | 1,000 | | | | 88 | |

| LX INTERNATIONAL CORP | | | 2,700 | | | | 59 | |

| LX Semicon | | | 5,100 | | | | 225 | |

| PSK | | | 13,700 | | | | 202 | |

| Samsung Electronics | | | 29,500 | | | | 1,252 | |

| Samsung Fire & Marine Insurance | | | 1,100 | | | | 267 | |

| Samsung Life Insurance | | | 3,700 | | | | 271 | |

| Samsung SDS | | | 1,700 | | | | 175 | |

| Shinhan Financial Group | | | 10,300 | | | | 384 | |

| Shinsegae | | | 500 | | | | 56 | |

| SK Square* | | | 9,200 | | | | 556 | |

| SK Telecom | | | 8,800 | | | | 361 | |

| SNT Motiv | | | 2,000 | | | | 66 | |

| | | | | | | 9,305 | |

| | | | | | | | | |

| Taiwan (17.4%) |

| ASE Technology Holding | | | 51,000 | | | | 241 | |

| Asustek Computer | | | 31,000 | | | | 547 | |

| Cathay Financial Holding | | | 207,000 | | | | 437 | |

| Chicony Electronics | | | 20,000 | | | | 101 | |

| Chin-Poon Industrial | | | 193,000 | | | | 227 | |

| Chipbond Technology | | | 43,000 | | | | 84 | |

| ChipMOS Technologies | | | 274,000 | | | | 301 | |

| Compal Electronics | | | 135,000 | | | | 148 | |

| Compeq Manufacturing | | | 53,000 | | | | 100 | |

| CTBC Financial Holding | | | 873,000 | | | | 968 | |

| Eva Airways | | | 418,000 | | | | 483 | |

| Everlight Electronics | | | 141,000 | | | | 366 | |

| Getac Holdings | | | 89,000 | | | | 305 | |

| Global Brands Manufacture | | | 60,000 | | | | 108 | |

| Global Mixed Mode Technology | | | 8,000 | | | | 56 | |

| Hon Hai Precision Industry | | | 168,000 | | | | 1,077 | |

| KGI Financial Holding | | | 585,000 | | | | 301 | |

| King Yuan Electronics | | | 35,000 | | | | 132 | |

| King's Town Bank | | | 219,000 | | | | 336 | |

| MediaTek | | | 32,000 | | | | 1,246 | |

The accompanying notes are an integral part of the financial statements

Schedule of Investments

October 31, 2024

| LSV Emerging Markets Equity Fund |

| | | Shares | | | Value (000) | |

| Taiwan (continued) |

| Novatek Microelectronics | | | 10,000 | | | $ | 155 | |

| Pegatron | | | 165,000 | | | | 500 | |

| Pou Chen | | | 304,000 | | | | 355 | |

| Powertech Technology | | | 60,000 | | | | 234 | |

| Primax Electronics | | | 36,000 | | | | 90 | |

| Radiant Opto-Electronics | | | 56,000 | | | | 365 | |

| Sigurd Microelectronics | | | 41,000 | | | | 93 | |

| Simplo Technology | | | 27,000 | | | | 285 | |

| Sino-American Silicon Products | | | 65,000 | | | | 315 | |

| SinoPac Financial Holdings | | | 47 | | | | — | |

| Taiwan Semiconductor Manufacturing | | | 80,000 | | | | 2,508 | |

| Topco Scientific | | | 10,288 | | | | 99 | |

| Tripod Technology | | | 62,000 | | | | 366 | |

| Tung Ho Steel Enterprise | | | 127,000 | | | | 290 | |

| United Integrated Services | | | 14,000 | | | | 145 | |

| United Microelectronics | | | 488,000 | | | | 704 | |

| Yuanta Financial Holding | | | 289,680 | | | | 291 | |

| | | | | | | | 14,359 | |

| |

| Thailand (2.3%) |

| Bangkok Bank | | | 74,800 | | | | 326 | |

| Kasikornbank | | | 120,600 | | | | 523 | |

| Kiatnakin Phatra Bank | | | 78,100 | | | | 126 | |

| Krung Thai Bank | | | 851,700 | | | | 517 | |

| Supalai | | | 176,000 | | | | 102 | |

| Thai Beverage | | | 849,900 | | | | 340 | |

| | | | | | | | 1,934 | |

| |

| Türkiye (0.8%) |

| BIM Birlesik Magazalar | | | 14,700 | | | | 201 | |

| Coca-Cola Icecek | | | 152,000 | | | | 226 | |

| Haci Omer Sabanci Holding | | | 109,100 | | | | 265 | |

| | | | | | | | 692 | |

| |

| United Arab Emirates (1.9%) |

| Air Arabia PJSC | | | 436,900 | | | | 342 | |

| Emaar Properties PJSC | | | 208,500 | | | | 493 | |

| Emirates NBD Bank PJSC | | | 137,100 | | | | 708 | |

| | | | | | | | 1,543 | |

| |

| TOTAL FOREIGN COMMON STOCK |

| (Cost $76,379) | | | | | | | 80,073 | |

| | | | | | | | | |

| Foreign Preferred Stock (2.3%) |

| Brazil** (1.9%) |

| Banco do Estado do Rio Grande do Sul | | | 36,000 | | | | 70 | |

| Cia Energetica de Minas Gerais | | | 230,200 | | | | 452 | |

| Itausa | | | 206,100 | | | | 378 | |

| LSV Emerging Markets Equity Fund |

| | | Shares | | | Value (000) | |

| Brazil** (continued) |

| Petroleo Brasileiro | | | 110,000 | | | $ | 682 | |

| | | | | | | | 1,582 | |

| | | | | | | | | |

| Chile** (0.4%) |

| Embotelladora Andina | | | 107,400 | | | | 321 | |

| | | | | | | | | |

| TOTAL FOREIGN PREFERRED STOCK |

| (Cost $1,978) | | | | | | | 1,903 | |

| Warrants (0.0%)* |

| Thailand (0.0%) |

| Kiatnakin Phatra Bank 01/03/2027* | | | 3,642 | | | | — | |

| | | | | | | | | |

| TOTAL WARRANTS |

| (Cost $–) | | | | | | | — | |

| | | Face Amount (000) | | | | |

| Repurchase Agreement (0.6%) |

| South Street Securities |

| 4.500%, dated 10/31/2024, to be repurchased on 11/01/2024, repurchase price $470 (collateralized by various U.S. Treasury obligations, ranging in par value $0 - $452, 0.625% - 4.250%, 03/31/2025 - 02/15/2052; total market value $479) | | $ | 470 | | | | 470 | |

| | | | | | | | | |

| TOTAL REPURCHASE AGREEMENT |

| (Cost $470) | | | | | | | 470 | |

| | | | | | | | | |

| Total Investments – 99.7% |

| (Cost $78,827) | | | | | | $ | 82,446 | |

Percentages are based on Net Assets of $82,685 (000).

| ‡ | Real Estate Investment Trust. |

| * | Non-income producing security. |

| (A) | Security is Fair Valued. |

| (B) | Level 3 security in accordance with fair value hierarchy. |

ADR — American Depositary Receipt

Cl — Class

PJSC — Public Joint Stock Company

The accompanying notes are an integral part of the financial statements

Schedule of Investments

October 31, 2024

The following is a summary of the inputs used as of October 31, 2024, in valuing the Fund’s investments carried at value ($000):

| Investments in Securities | | Level 1 | | | Level 2 | | | Level 3(1) | | | Total | |

| Foreign Common Stock |

| Brazil | | $ | 2,521 | | | $ | – | | | $ | – | | | $ | 2,521 | |

| Chile | | | 139 | | | | – | | | | – | | | | 139 | |

| China | | | 1,241 | | | | 21,147 | | | | – | | | | 22,388 | |

| Egypt | | | 219 | | | | – | | | | – | | | | 219 | |

| Greece | | | – | | | | 869 | | | | – | | | | 869 | |

| Hong Kong | | | – | | | | 652 | | | | – | | | | 652 | |

| Hungary | | | – | | | | 732 | | | | – | | | | 732 | |

| India | | | – | | | | 13,261 | | | | – | | | | 13,261 | |

| Indonesia | | | – | | | | 1,438 | | | | – | | | | 1,438 | |

| Kuwait | | | – | | | | 281 | | | | – | | | | 281 | |

| Malaysia | | | – | | | | 1,126 | | | | – | | | | 1,126 | |

| Mexico | | | 2,164 | | | | – | | | | – | | | | 2,164 | |

| Philippines | | | – | | | | 599 | | | | – | | | | 599 | |

| Poland | | | – | | | | 1,445 | | | | – | | | | 1,445 | |

| Russia | | | – | | | | – | | | | – | ^ | | | – | ^ |

| Saudi Arabia | | | – | | | | 2,305 | | | | – | | | | 2,305 | |

| South Africa | | | 167 | | | | 1,934 | | | | – | | | | 2,101 | |

| South Korea | | | – | | | | 9,305 | | | | – | | | | 9,305 | |

| Taiwan | | | – | | | | 14,359 | | | | – | | | | 14,359 | |

| Thailand | | | – | | | | 1,934 | | | | – | | | | 1,934 | |

| Türkiye | | | 226 | | | | 466 | | | | – | | | | 692 | |

| United Arab Emirates | | | – | | | | 1,543 | | | | – | | | | 1,543 | |

| Total Foreign Common Stock | | | 6,677 | | | | 73,396 | | | | – | ^ | | | 80,073 | |

| Foreign Preferred Stock |

| Brazil | | | 1,582 | | | | – | | | | – | | | | 1,582 | |

| Chile | | | 321 | | | | – | | | | – | | | | 321 | |

| Total Foreign Preferred Stock | | | 1,903 | | | | – | | | | – | | | | 1,903 | |

| Total Warrants | | | – | | | | – | | | | – | | | | – | |

| Total Repurchase Agreement | | | – | | | | 470 | | | | – | | | | 470 | |

| Total Investments in Securities | | $ | 8,580 | | | $ | 73,866 | | | $ | – | ^ | | $ | 82,446 | |

| (1) | A reconciliation of Level 3 investments and disclosures of significant un-observable inputs are presented when the Fund has a significant amount of Level 3 investments at the end of the period in relation to Net Assets. Management has concluded that Level 3 investments are not material in relation to Net Assets. |

| ^ | Includes Securities in which the fair value is $0 or has been rounded to $0. |

Amounts designated as “—“ are $0 or have been rounded to $0.

For more information on valuation inputs, see Note 2 — Significant Accounting Policies in the Notes to Financial Statements.

The accompanying notes are an integral part of the financial statements

Statement of Assets and Liabilities (000)

October 31, 2024

| | | LSV Emerging Markets Equity Fund | |

| Assets: | | | | |

| Investments, at Value (Cost $78,827) | | $ | 82,446 | |

| Foreign Currency, at Value (Cost $336) | | | 334 | |

| Dividends and Interest Receivable | | | 178 | |

| Receivable for Capital Shares Sold | | | 56 | |

| Reclaims Receivable | | | 5 | |

| Prepaid Expenses | | | 12 | |

| Total Assets | | | 83,031 | |

| Liabilities: | | | | |

| Accrued Foreign Capital Gains Tax | | | 262 | |

| Payable for Custody Fees | | | 39 | |

| Payable for Fund Shares Redeemed | | | 16 | |

| Payable due to Administrator | | | 4 | |

| Payable due to Investment Adviser | | | 1 | |

| Payable due to Trustees | | | 1 | |

| Payable due to Distributor | | | 1 | |

| Payable due to Chief Compliance Officer | | | 1 | |

| Other Accrued Expenses | | | 21 | |

| Total Liabilities | | | 346 | |

| Net Assets | | $ | 82,685 | |

| Net Assets Consist of: | | | | |

| Paid-in Capital | | $ | 78,685 | |

| Total Distributable Earnings | | | 4,000 | |

| Net Assets | | $ | 82,685 | |

| Net Asset Value, Offering and Redemption Price Per Share — Institutional Class Shares ($79,386 ÷ 6,509,833 shares)(1) | | $ | 12.19 | * |

| Net Asset Value, Offering and Redemption Price Per Share — Investor Class Shares ($3,299 ÷ 271,259 shares)(1) | | $ | 12.16 | * |

| (1) | Shares have not been rounded. |

| * | Net Assets divided by Shares does not calculate to the stated NAV because Net Asset amounts are shown rounded. |

The accompanying notes are an integral part of the financial statements

Statement of Operations (000)

For the year ended October 31, 2024

| | | LSV Emerging

Markets Equity

Fund | |

| Investment Income: | | | | |

| Dividend Income | | $ | 1,760 | |

| Interest Income | | | 32 | |

| Foreign Taxes Withheld | | | (241 | ) |

| Total Investment Income | | | 1,551 | |

| Expenses: | | | | |

| Investment Advisory Fees | | | 388 | |

| Administration Fees | | | 23 | |

| Distribution Fees - Investor Class | | | 6 | |

| Trustees' Fees | | | 3 | |

| Chief Compliance Officer Fees | | | 2 | |

| Custodian Fees | | | 147 | |

| Registration and Filing Fees | | | 39 | |

| Transfer Agent Fees | | | 38 | |

| Professional Fees | | | 10 | |

| Printing Fees | | | 4 | |

| Insurance and Other Fees | | | 34 | |

| Total Expenses | | | 694 | |

| Less: Waiver of Investment Advisory Fees | | | (317 | ) |

| Less: Fees Paid Indirectly — (see Note 4) | | | (4 | ) |

| Net Expenses | | | 373 | |

| Net Investment Income | | | 1,178 | |

| Net Realized Gain on Investments | | | 614 | |

| Net Realized Loss on Foreign Currency Transactions | | | (154 | ) |

| Net Realized Loss on Foreign Capital Gains Tax | | | (67 | ) |

| Net Realized Gain | | | 393 | |

| Net Change in Unrealized Appreciation on Investments | | | 4,430 | |

| Net Change in Unrealized Depreciation on Foreign Capital Gains Tax on Appreciated Securities | | | (172 | ) |

| Net Change in Unrealized Depreciation on Foreign Currency Translation | | | (4 | ) |

| Net Unrealized Gain | | | 4,254 | |

| Net Realized and Unrealized Gain | | | 4,647 | |

| Net Increase in Net Assets Resulting from Operations | | $ | 5,825 | |

The accompanying notes are an integral part of the financial statements

Statements of Changes in Net Assets (000)

For the year ended October 31,

| | | LSV Emerging Markets Equity Fund | |

| | | 2024 | | | 2023 | |

| Operations: | | | | | | | | |

| Net Investment Income | | $ | 1,178 | | | $ | 768 | |

| Net Realized Gain (Loss) | | | 393 | | | | (396 | ) |

| Net Change in Unrealized Appreciation | | | 4,254 | | | | 3,162 | |

| Net Increase in Net Assets Resulting from Operations | | | 5,825 | | | | 3,534 | |

| Distributions | | | | | | | | |

| Institutional Class Shares | | | (1,027 | ) | | | (589 | ) |

| Investor Class Shares | | | (79 | ) | | | (31 | ) |

| Total Distributions | | | (1,106 | ) | | | (620 | ) |

| Capital Share Transactions: | | | | | | | | |

| Institutional Class Shares: | | | | | | | | |

| Issued | | | 58,130 | | | | 1,782 | |

| Reinvestment of Dividends and Distributions | | | 1,027 | | | | 588 | |

| Redeemed | | | (3,054 | ) | | | (1,961 | ) |

| Net Increase from Institutional Class Shares Transactions | | | 56,103 | | | | 409 | |

| Investor Class Shares: | | | | | | | | |

| Issued | | | 5,066 | | | | 756 | |

| Reinvestment of Dividends and Distributions | | | 79 | | | | 31 | |

| Redeemed | | | (3,569 | ) | | | (415 | ) |

| Net Increase from Investor Class Shares Transactions | | | 1,576 | | | | 372 | |

| Net Increase in Net Assets Derived from Capital Share Transactions | | | 57,679 | | | | 781 | |

| Total Increase in Net Assets | | | 62,398 | | | | 3,695 | |

| Net Assets: | | | | | | | | |

| Beginning of Year | | | 20,287 | | | | 16,592 | |

| End of Year | | $ | 82,685 | | | $ | 20,287 | |

| Shares Transactions: | | | | | | | | |

| Institutional Class: | | | | | | | | |

| Issued | | | 4,813 | | | | 178 | |

| Reinvestment of Dividends and Distributions | | | 93 | | | | 62 | |

| Redeemed | | | (259 | ) | | | (197 | ) |

| Total Institutional Class Share Transactions | | | 4,647 | | | | 43 | |

| Investor Class: | | | | | | | | |

| Issued | | | 434 | | | | 75 | |

| Reinvestment of Dividends and Distributions | | | 7 | | | | 3 | |

| Redeemed | | | (301 | ) | | | (41 | ) |

| Total Investor Class Share Transactions | | | 140 | | | | 37 | |

| Net Increase in Shares Outstanding | | | 4,787 | | | | 80 | |

The accompanying notes are an integral part of the financial statements

Financial Highlights

For a share outstanding throughout each year ended October 31,

| | | | Net Asset Value Beginning of Year | | | Net Investment Income(1) | | | Realized and Unrealized Gains (Losses) | | | Total from Operations | | | Dividends from Net Investment Income | | | Distributions from Realized Gains | | | Total Dividends and Distributions | | | Net Asset Value End of Year | | | Total Return† | | | Net Assets End of Year (000) | | | Ratio of Expenses to Average Net Assets | | | Ratio of Expenses to Average Net Assets (Excluding Waivers, Reimbursements and Fees Paid Indirectly) | | | Ratio of Net Investment Income to Average Net Assets | | | Portfolio Turnover Rate | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| LSV Emerging Markets Equity Fund | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Institutional Class Shares | |

| 2024 | | | $ | 10.18 | | | $ | 0.36 | | | $ | 2.18 | | | $ | 2.54 | | | $ | (0.53 | ) | | $ | – | | | $ | (0.53 | ) | | $ | 12.19 | | | | 25.46 | % | | $ | 79,386 | | | | 0.95 | % | | | 1.77 | % | | | 3.03 | % | | | 13 | % |

| 2023 | | | | 8.67 | | | | 0.39 | | | | 1.44 | | | | 1.83 | | | | (0.32 | ) | | | – | | | | (0.32 | ) | | | 10.18 | | | | 21.39 | | | | 18,960 | | | | 1.19 | | | | 1.85 | | | | 3.87 | | | | 17 | |

| 2022 | | | | 12.09 | | | | 0.45 | | | | (2.88 | ) | | | (2.43 | ) | | | (0.36 | ) | | | (0.63 | ) | | | (0.99 | ) | | | 8.67 | | | | (21.97 | ) | | | 15,780 | | | | 1.19 | | | | 2.45 | | | | 4.33 | | | | 38 | |

| 2021 | | | | 9.11 | | | | 0.37 | | | | 2.91 | | | | 3.28 | | | | (0.21 | ) | | | (0.09 | ) | | | (0.30 | ) | | | 12.09 | | | | 36.38 | | | | 13,451 | | | | 1.19 | | | | 2.68 | | | | 3.18 | | | | 19 | |

| 2020 | | | | 10.28 | | | | 0.26 | | | | (1.11 | ) | | | (0.85 | ) | | | (0.31 | ) | | | (0.01 | ) | | | (0.32 | ) | | | 9.11 | | | | (8.67 | ) | | | 6,384 | | | | 1.19 | | | | 3.20 | | | | 2.85 | | | | 19 | |

| Investor Class Shares |

| 2024 | | | $ | 10.15 | | | $ | 0.37 | | | $ | 2.15 | | | $ | 2.52 | | | $ | (0.51 | ) | | $ | – | | | $ | (0.51 | ) | | $ | 12.16 | | | | 25.30 | % | | $ | 3,299 | | | | 1.20 | % | | | 2.04 | % | | | 3.16 | % | | | 13 | % |

| 2023 | | | | 8.65 | | | | 0.37 | | | | 1.43 | | | | 1.80 | | | | (0.30 | ) | | | – | | | | (0.30 | ) | | | 10.15 | | | | 21.02 | | | | 1,327 | | | | 1.45 | | | | 2.09 | | | | 3.65 | | | | 17 | |

| 2022 | | | | 12.07 | | | | 0.43 | | | | (2.89 | ) | | | (2.46 | ) | | | (0.33 | ) | | | (0.63 | ) | | | (0.96 | ) | | | 8.65 | | | | (22.18 | ) | | | 812 | | | | 1.45 | | | | 2.63 | | | | 4.04 | | | | 38 | |

| 2021 | | | | 9.10 | | | | 0.37 | | | | 2.88 | | | | 3.25 | | | | (0.19 | ) | | | (0.09 | ) | | | (0.28 | ) | | | 12.07 | | | | 36.06 | | | | 1,031 | | | | 1.45 | | | | 2.95 | | | | 3.15 | | | | 19 | |

| 2020 | | | | 10.28 | | | | 0.25 | | | | (1.12 | ) | | | (0.87 | ) | | | (0.30 | ) | | | (0.01 | ) | | | (0.31 | ) | | | 9.10 | | | | (8.83 | ) | | | 350 | | | | 1.45 | | | | 3.50 | | | | 2.79 | | | | 19 | |

| † | Total return is for the period indicated and has not been annualized. Total return would have been lower had the Adviser not waived a portion of its fee. Total returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. |

| (1) | Per share data calculated using average shares method. |

Amounts designated as “—” are $0 or have been rounded to $0.

The accompanying notes are an integral part of the financial statements

Notes to Financial Statements

October 31, 2024

1. Organization:

The Advisors’ Inner Circle Fund (the “Trust”) is organized as a Massachusetts business trust under an Amended and Restated Agreement and Declaration of Trust dated February 18, 1997. The Trust is registered under the Investment Company Act of 1940, as amended, as an open-end management investment company with 26 funds. The financial statements herein are those of the LSV Emerging Markets Equity Fund, a diversified Fund (the “Fund”). The Fund seeks long-term growth of capital by investing in undervalued stocks which are out of favor in the market. The Fund commenced operations on January 17, 2019, offering Institutional Class Shares and Investor Class Shares. The financial statements of the remaining funds of the Trust are not presented herein, but are presented separately. The assets of each fund are segregated, and a shareholder’s interest is limited to the fund in which shares are held.

2. Significant Accounting Policies:

The accompanying financial statements have been prepared in conformity with U.S. generally accepted accounting principles (“U.S. GAAP”) and are presented in U.S. dollars which is the functional currency of the Fund. The Fund is an investment company and therefore applies the accounting and reporting guidance issued by the U.S. Financial Accounting Standards Board (“FASB”) in Accounting Standards Codification (“ASC”) Topic 946, Financial Services — Investment Companies. The following are significant accounting policies which are consistently followed in the preparation of the financial statements.

Use of Estimates — The preparation of financial statements requires management to make estimates and assumptions that affect the fair value of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates and such differences could be material.

Security Valuation — Securities listed on a securities exchange, market or automated quotation system for which quotations are readily available (except for securities traded on NASDAQ), including securities traded over the counter, are valued at the last quoted sale price on an exchange or market (foreign or domestic) on which they are traded on the valuation date (or at approximately 4:00 pm ET if a security’s primary exchange is normally open at that time), or, if there is no such reported sale on the valuation date, at

the most recent quoted bid price. For securities traded on NASDAQ, the NASDAQ Official Closing Price will be used. The prices for foreign securities are reported in local currency and converted to U.S. dollars using currency exchange rates.

Securities for which market prices are not “readily available” are valued in accordance with fair value procedures (the "Fair Value Procedures") established by the Adviser and approved by the Trust's Board of Trustees (the “Board”). Pursuant to Rule 2a-5 under the 1940 Act, the Board has designated the Adviser as the "valuation designee" to determine the fair value of securities and other instruments for which no readily available market quotations are available. The Fair Value Procedures are implemented through a Fair Value Committee (the “Committee”) of the Adviser.

Some of the more common reasons that may necessitate that a security be valued using Fair Value Procedures include: the security’s trading has been halted or suspended; the security has been de-listed from a national exchange; the security’s primary trading market is temporarily closed at a time when under normal conditions it would be open; the security has not been traded for an extended period of time; the security’s primary pricing source is not able or willing to provide a price; or trading of the security is subject to local government-imposed restrictions. When a security is valued in accordance with the Fair Value Procedures, the Committee will determine the value after taking into consideration relevant information reasonably available to the Committee. As of October 31, 2024, the total market value of securities that were fair valued by the Committee were $0 (000) or 0.0% of Net Assets.

For securities that principally trade on a foreign market or exchange, a significant gap in time can exist between the time of a particular security’s last trade and the time at which the Fund calculates its net asset value. The closing prices of such securities may no longer reflect their market value at the time the Fund calculates net asset value if an event that could materially affect the value of those securities (a “Significant Event”) has occurred between the time of the security’s last close and the time that the Fund calculates net asset value. A Significant Event may relate to a single issuer or to an entire market sector. If the adviser of the Fund becomes aware of a Significant Event that has occurred with respect to a security or group of securities after the closing of the exchange or market on which the security or securities principally trade, but before the time at which the Fund calculates net asset value, it may request that a Committee meeting be called. In addition, the Fund’s administrator monitors price movements among certain selected indices, securities and/or baskets of securities that may be an indicator that the closing prices received earlier from foreign exchanges or markets may not reflect market value at the time the Fund calculates net asset value. If price movements in a monitored index or security exceed levels established by the administrator, the administrator notifies the adviser that such limits have been exceeded. In such event, the adviser makes the determination whether a Committee meeting should be called based on the information provided.

Notes to Financial Statements

October 31, 2024

The Fund uses Intercontinental Exchange Data Pricing & Reference Data, LLC (“ICE”) as a third party fair valuation vendor when the fair value trigger is met. ICE provides a fair value for foreign securities in the Fund based on certain factors and methodologies (involving, generally, tracking valuation correlations between the U.S. market and each non-U.S. security) applied by ICE in the event that there is a movement in the U.S. market that exceeds a specific threshold established by the Committee. The Committee establishes a “confidence interval” which is used to determine the level of correlation between the value of a foreign security and movements in the U.S. market before a particular security is fair valued when the threshold is exceeded. In the event that the threshold established by the Committee is exceeded on a specific day, the Fund values its non-U.S. securities that exceed the applicable “confidence interval” based upon the fair values provided by ICE. In such event, it is not necessary to hold a Committee meeting. In the event that the Adviser believes that the fair values provided by ICE are not reliable, the Adviser contacts SEI Investments Global Fund Services (the “Administrator”) and may request that a meeting of the Committee be held. As of October 31, 2024, the total market value of securities were valued based on the fair value prices provided by ICE were $73,396 (000) or 89.0% of Net Assets. If a local market in which the Fund owns securities is closed for one or more days, the Fund shall value all securities held in that corresponding currency based on the fair value prices provided by ICE using the predetermined confidence interval discussed above.

In accordance with the authoritative guidance on fair value measurements and disclosure under U.S. GAAP, the Fund discloses fair value of its investments in a hierarchy that prioritizes the inputs to valuation techniques used to measure the fair value. The objective of a fair value measurement is to determine the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date (an exit price). Accordingly, the fair value hierarchy gives the highest priority to quoted prices (unadjusted) in active markets for identical assets or liabilities (Level 1) and the lowest priority to unobservable inputs (Level 3). The three levels of

the fair value hierarchy are described below:

Level 1 — Unadjusted quoted prices in active markets for identical, unrestricted assets or liabilities that the Fund has the ability to access at the measurement date;

Level 2 — Other significant observable inputs (includes quoted prices for similar securities, interest rates, prepayment speeds, credit risk, referenced indices, quoted prices in inactive markets, adjusted quoted prices in active markets, adjusted quoted prices on foreign equity securities that were adjusted in accordance with The Adviser’s pricing procedures,etc.); and

Level 3 — Prices, inputs or proprietary modeling techniques which are both significant to the fair value measurement and unobservable (supported by little or no market activity).

Investments are classified within the level of the lowest significant input considered in determining fair value. Investments classified within Level 3 whose fair value measurement considers several inputs may include Level 1 or Level 2 inputs as components of the overall fair value measurement.

Federal Income Taxes — It is the Fund’s intention to continue to qualify as a regulated investment company for Federal income tax purposes by complying with the appropriate provisions of Subchapter M of the Internal Revenue Code of 1986, as amended and to distribute substantially all of its income to shareholders. Accordingly, no provision for Federal income taxes has been made in the financial statements.

The Fund evaluates tax positions taken or expected to be taken in the course of preparing the Fund’s tax returns to determine whether it is “more-likely-than-not” (i.e., greater than 50-percent) that each tax position will be sustained upon examination by a taxing authority based on the technical merits of the position. Tax positions not deemed to meet the more-likely-than-not threshold are recorded as a tax benefit or expense in the current year. The Fund did not record any tax provision in the current period. However, management’s conclusions regarding tax positions taken may be subject to review and adjustment at a later date based on factors including, but not limited to, examination by tax authorities on open tax years (i.e. the last three open tax year ends, as applicable), on-going analysis of and changes to tax laws, regulations and interpretations thereof.

As of and during the year ended October 31, 2024, the Fund did not have a liability for any unrecognized tax benefits. The Fund recognizes interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the Statement of Operations. During the year ended October 31, 2024, the Fund did not incur any interest or penalties.

Notes to Financial Statements

October 31, 2024

Withholding taxes on foreign dividends, if any, have been provided for in accordance with the Funds’ understanding of the applicable country’s tax rules and rates. The Funds or their agent files withholding tax reclaims in certain jurisdictions to recover certain amounts previously withheld. The Funds may record a reclaim receivable based on collectability, which includes factors such as the jurisdiction’s applicable laws, payment history and market convention. Professional fees paid to those that provide assistance in receiving the tax reclaims, which generally are contingent upon successful receipt of reclaimed amounts, are recorded in Professional Fees on the Statements of Operations once the amounts are due. The professional fees related to pursuing these tax reclaims are not subject to the Adviser’s expense limitation agreement.

Security Transactions and Investment Income— Security transactions are accounted for on trade date for financial reporting purposes. Costs used in determining realized gains or losses on the sale of investment securities are based on the specific identification method. Dividend income is recorded on the ex-dividend date. Interest income is recognized on the accrual basis from settlement date.

Investments in Real Estate Investment Trusts (REITs) — With respect to the Fund, dividend income is recorded based on the income included in distributions received from the REIT investments using published REIT reclassifications including some management estimates when actual amounts are not available. Distributions received in excess of this estimated amount are recorded as a reduction of the cost of investments or reclassified to capital gains. The actual amounts of income, return of capital, and capital gains are only determined by each REIT after its fiscal year-end, and may differ from the estimated amounts.

Repurchase Agreements — In connection with transactions involving repurchase agreements, a third party custodian bank takes possession of the underlying securities (“collateral”), the value of which exceeds the principal amount of the repurchase transaction, including accrued interest. Such collateral will be cash, debt securities issued or guaranteed by the U.S. Government, securities that at the time the repurchase agreement is entered into are rated in the highest category by a nationally recognized statistical rating organization (“NRSRO”), as determined by the Adviser.

Provisions of the repurchase agreements and procedures adopted by the Board require that the market value of the collateral, including accrued interest thereon, is sufficient in the event of default by the counterparty. In the event of default or bankruptcy by the counterparty to the agreement, realization and/or retention of the collateral or proceeds may be subject to legal proceedings.

Repurchase agreements are entered into by the Fund under Master Repurchase Agreements (“MRA”) which permit the Fund, under certain circumstances including an event of default (such as bankruptcy or insolvency), to offset payables and/or receivables under the MRA with collateral held and/ or posted to the counterparty and create one single net payment due to or from the Fund.

At October 31, 2024, the open repurchase agreement by counterparty which is subject to a MRA on a net payment basis is as follows (000):

| Counterparty | | Repurchase Agreement | | | Fair Value of Non-Cash Collateral Received(1) | | | Cash Collateral Received(1) | | | Net Amount(2) | |

| South Street Securities | | $ | 470 | | | $ | 470 | | | $ | – | | | $ | – | |

| (1) | The amount of collateral reflected in the table does not include any over-collateralization received by the Fund. |

| (2) | Net amount represents the net amount receivable due from the counterparty in the event of default. |