UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act File Number 811-06400

The Advisors’ Inner Circle Fund

(Exact name of registrant as specified in charter)

SEI Investments

One Freedom Valley Drive

Oaks, PA 19456

(Address of principal executive offices) (Zip code)

SEI Investments

One Freedom Valley Drive

Oaks, PA 19456

(Name and address of agent for service)

Registrant’s telephone number, including area code: (877) 446-3863

Date of fiscal year end: October 31, 2024

Date of reporting period: October 31, 2024

Item 1. Reports to Stockholders.

(a) A copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended (the “Act”) (17 CFR § 270.30e-1), is attached hereto.

The Advisors' Inner Circle Fund

Institutional Class Shares - LSVEX

Annual Shareholder Report: October 31, 2024

This annual shareholder report contains important information about Institutional Class Shares of the LSV Value Equity Fund (the "Fund") for the period from November 1, 2023 to October 31, 2024. You can find additional information about the Fund at https://www.lsvasset.com/value-equity-fund/. You can also request this information by contacting us at 888-386-3578.

What were the Fund costs for the last year?

(based on a hypothetical $10,000 investment)

| Fund Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

|---|

| LSV Value Equity Fund, Institutional Class Shares | $77 | 0.67% |

How did the Fund perform in the last year?

The broad U.S. equity market as measured by the S&P 500 Index was up 38.02% for the twelve months ended October 31, 2024. The market's strong performance came despite various challenges, including concerns about inflation, geopolitical tensions, and uncertainties surrounding the US presidential election. The resilience of the US economy and corporate earnings growth were key factors supporting the positive returns. While the market rewarded the mega-cap growth stocks in the period, smaller stocks and value-oriented stocks once again lagged behind. Small cap stocks underperformed large caps over the period as the Russell 1000 Index (USD) was up 38.07% while the Russell 2000 Index (USD) was up 34.07%. From a style perspective, value stocks (as measured by the Russell Indices) underperformed growth—the Russell 1000 Value Index (USD) was up 30.98% while the Russell 1000 Growth Index (USD) was up 43.77%. The LSV Value Equity Fund, Institutional Class Shares was up 30.77% for the period. From a sector perspective, Financial, Industrial, Utility and Real Estate stocks outperformed while the Energy, Health Care and Consumer Staple sectors lagged.

The Fund’s deeper value bias had a muted impact over the period as cheaper stocks on an earnings and cash flow basis performed in line with the benchmark. Performance attribution further indicates that stock selection experienced a small positive contribution to portfolio relative returns while sector allocation detracted slightly from relative returns over the year. Stock selection relative gains were primarily the result of the outperformance of deep value names within the Utilities, Financials, and Communication Services. Within Utilities, holdings in Independent Power Producers & Energy Traders, added to returns. Within Financials, holdings in Regional Banks and Asset Management & Custody Banks added to returns. Within Communication Services, holdings in Interactive Media & Services and Integrated Telecommunication Services bolstered excess returns. From a sector perspective, relative losses were more modest and largely the result of our overweight to Health Care stocks combined with an underweight to the Industrials and Utilities sectors. Top contributors for the year included our overweight positions in Vistra, Allison Transmission, Dell, Mueller Industries, Bank of New York Mellon, Pulte Group, Meta Platforms, NRG Energy, General Motors, and Citigroup Inc. Not owning Chevron, Conoco Phillips, Procter & Gamble, Boeing, and Schlumberger also added value. Additionally, underweights in Johnson & Johnson, Intel, Biogen, Keycorp, and Qorvo contributed to returns. The main individual detractors included our overweight positions in Merck, HF Sinclair, APA Corp, Molson Coors, CVS Health Corp, Marathon Oil, and Jazz Pharmaceuticals. Not owning JP Morgan Chase, General Electric, Walmart, Constellation Energy, GE Vernova, Philip Morris, KKR & Co, American Express, Blackrock, and Eaton Corp also contributed to losses. Additionally, underweights in Bank of America Corp, Morgan Stanley, Intl Business Machines, and Western Digital Corp contributed to losses.

The Fund continues to trade at a significant discount to the overall market as well as to the value benchmark. The Fund is trading at 11.5x forward earnings compared to 18.0x for the Russell 1000 Value (USD), 2.0x book value compared to 2.7x for the Russell 1000 Value Index (USD) and 7.7x cash flow compared to 13.3x for the Russell 1000 Value Index (USD). Sector weightings are a result of our bottom-up stock selection process, subject to constraints at the sector and industry levels. The Fund is currently overweight the Communication Services, Information Technology, and Consumer Discretionary while underweight Real Estate, Utilities, and Industrials.

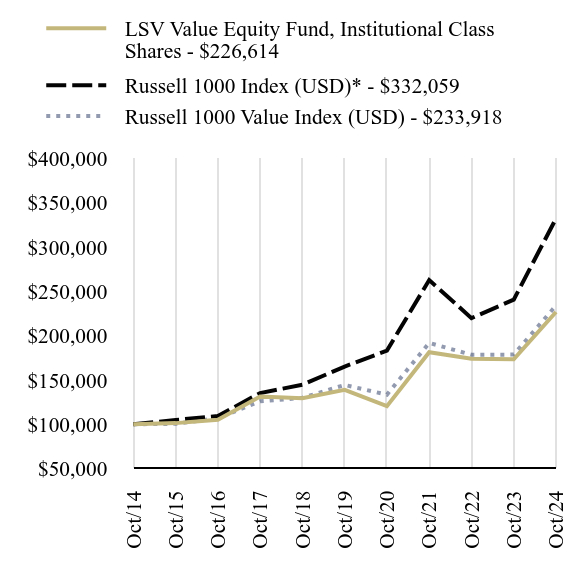

How did the Fund perform during the last 10 years?

Total Return Based on $100,000 Investment

| LSV Value Equity Fund, Institutional Class Shares - $226614 | Russell 1000 Index (USD)* - $332059 | Russell 1000 Value Index (USD) - $233918 |

|---|

| Oct/14 | $100000 | $100000 | $100000 |

| Oct/15 | $101304 | $104865 | $100529 |

| Oct/16 | $105061 | $109327 | $106934 |

| Oct/17 | $131265 | $135203 | $125948 |

| Oct/18 | $129270 | $144638 | $129770 |

| Oct/19 | $138771 | $165107 | $144321 |

| Oct/20 | $120422 | $183047 | $133403 |

| Oct/21 | $181291 | $262694 | $191776 |

| Oct/22 | $174032 | $219670 | $178357 |

| Oct/23 | $173287 | $240503 | $178595 |

| Oct/24 | $226614 | $332059 | $233918 |

The line graph represents historical performance of a hypothetical investment of $100,000 in the Fund during the last 10 years. Returns shown are total returns, which assume the reinvestment of dividends and capital gains. The table and graph presented above do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund Shares. Past performance is not indicative of future performance.Call 888-386-3578 or visit https://www.lsvasset.com/value-equity-fund/ for current month-end performance.

Footnote Reference*As of October 2024, pursuant to the new regulatory requirements, this index has been added to represent the broad-based securities market index.

Average Annual Total Returns as of October 31, 2024

| Fund/Index Name | 1 Year | 5 Years | 10 Years |

|---|

| LSV Value Equity Fund, Institutional Class Shares | 30.77% | 10.31% | 8.52% |

| Russell 1000 Index (USD)* | 38.07% | 15.00% | 12.75% |

| Russell 1000 Value Index (USD) | 30.98% | 10.14% | 8.87% |

Key Fund Statistics as of October 31, 2024

| Total Net Assets (000's) | Number of Holdings | Total Advisory Fees Paid (000's) | Portfolio Turnover Rate |

|---|

| $1,383,173 | 155 | $7,762 | 26% |

What did the Fund invest in?

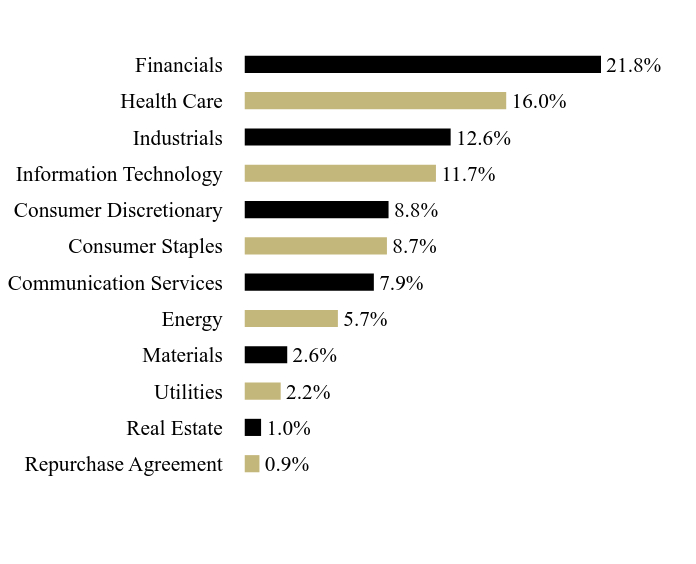

Sector WeightingsFootnote Reference*

| Value | Value |

|---|

| Repurchase Agreement | 0.9% |

| Real Estate | 1.0% |

| Utilities | 2.2% |

| Materials | 2.6% |

| Energy | 5.7% |

| Communication Services | 7.9% |

| Consumer Staples | 8.7% |

| Consumer Discretionary | 8.8% |

| Information Technology | 11.7% |

| Industrials | 12.6% |

| Health Care | 16.0% |

| Financials | 21.8% |

| Footnote | Description |

Footnote* | Percentages are calculated based on total net assets. |

| Holding Name | | | Percentage of Total Net Assets |

|---|

| Comcast, Cl A | | | 2.1% |

| AT&T | | | 2.0% |

| Wells Fargo | | | 1.8% |

| Bank of New York Mellon | | | 1.6% |

| Johnson & Johnson | | | 1.6% |

| State Street | | | 1.5% |

| Bristol-Myers Squibb | | | 1.5% |

| Kroger | | | 1.5% |

| Verizon Communications | | | 1.4% |

| Merck | | | 1.4% |

There were no material changes during the reporting period.

Changes in and Disagreements with Accountants

There were no changes in or disagreements with accountants during the reporting period.

For additional information about the Fund, including its prospectus, financial information, holdings, and proxy voting information, call or visit:

Rule 30e-1 of the Investment Company Act of 1940 permits funds to transmit only one copy of a proxy statement, annual report or semi-annual report to shareholders (who need not be related) with the same residential, commercial or electronic address, provided that the shareholders have consented in writing and the reports are addressed either to each shareholder individually or to the shareholders as a group. This process is known as “householding” and is designed to reduce the duplicate copies of materials that shareholders receive and to lower printing and mailing costs for funds. Once implemented, if you would like to discontinue householding for your accounts, please call toll-free at 888-386-3578 to request individual copies of these documents. Once the Fund receives notice to stop householding, we will begin sending individual copies 30 days after receiving your request.

The Advisors' Inner Circle Fund

LSV Value Equity Fund / Institutional Class Shares - LSVEX

Annual Shareholder Report: October 31, 2024

LSV-AR-TSR-2024-14

The Advisors' Inner Circle Fund

Investor Class Shares - LVAEX

Annual Shareholder Report: October 31, 2024

This annual shareholder report contains important information about Investor Class Shares of the LSV Value Equity Fund (the "Fund") for the period from November 1, 2023 to October 31, 2024. You can find additional information about the Fund at https://www.lsvasset.com/value-equity-fund/. You can also request this information by contacting us at 888-386-3578.

What were the Fund costs for the last year?

(based on a hypothetical $10,000 investment)

| Fund Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

|---|

| LSV Value Equity Fund, Investor Class Shares | $106 | 0.92% |

How did the Fund perform in the last year?

The broad U.S. equity market as measured by the S&P 500 Index was up 38.02% for the twelve months ended October 31, 2024. The market's strong performance came despite various challenges, including concerns about inflation, geopolitical tensions, and uncertainties surrounding the US presidential election. The resilience of the US economy and corporate earnings growth were key factors supporting the positive returns. While the market rewarded the mega-cap growth stocks in the period, smaller stocks and value-oriented stocks once again lagged behind. Small cap stocks underperformed large caps over the period as the Russell 1000 Index (USD) was up 38.07% while the Russell 2000 Index (USD) was up 34.07%. From a style perspective, value stocks (as measured by the Russell Indices) underperformed growth—the Russell 1000 Value Index (USD) was up 30.98% while the Russell 1000 Growth Index (USD) was up 43.77%. The LSV Value Equity Fund, Investor Class Shares was up 30.41% for the period. From a sector perspective, Financial, Industrial, Utility and Real Estate stocks outperformed while the Energy, Health Care and Consumer Staple sectors lagged.

The Fund’s deeper value bias had a muted impact over the period as cheaper stocks on an earnings and cash flow basis performed in line with the benchmark. Performance attribution further indicates that stock selection experienced a small positive contribution to portfolio relative returns while sector allocation detracted slightly from relative returns over the year. Stock selection relative gains were primarily the result of the outperformance of deep value names within the Utilities, Financials, and Communication Services. Within Utilities, holdings in Independent Power Producers & Energy Traders, added to returns. Within Financials, holdings in Regional Banks and Asset Management & Custody Banks added to returns. Within Communication Services, holdings in Interactive Media & Services and Integrated Telecommunication Services bolstered excess returns. From a sector perspective, relative losses were more modest and largely the result of our overweight to Health Care stocks combined with an underweight to the Industrials and Utilities sectors. Top contributors for the year included our overweight positions in Vistra, Allison Transmission, Dell, Mueller Industries, Bank of New York Mellon, Pulte Group, Meta Platforms, NRG Energy, General Motors, and Citigroup Inc. Not owning Chevron, Conoco Phillips, Procter & Gamble, Boeing, and Schlumberger also added value. Additionally, underweights in Johnson & Johnson, Intel, Biogen, Keycorp, and Qorvo contributed to returns. The main individual detractors included our overweight positions in Merck, HF Sinclair, APA Corp, Molson Coors, CVS Health Corp, Marathon Oil, and Jazz Pharmaceuticals. Not owning JP Morgan Chase, General Electric, Walmart, Constellation Energy, GE Vernova, Philip Morris, KKR & Co, American Express, Blackrock, and Eaton Corp also contributed to losses. Additionally, underweights in Bank of America Corp, Morgan Stanley, Intl Business Machines, and Western Digital Corp contributed to losses.

The Fund continues to trade at a significant discount to the overall market as well as to the value benchmark. The Fund is trading at 11.5x forward earnings compared to 18.0x for the Russell 1000 Value Index (USD), 2.0x book value compared to 2.7x for the Russell 1000 Value Index and 7.7x cash flow compared to 13.3x for the Russell 1000 Value (USD). Sector weightings are a result of our bottom-up stock selection process, subject to constraints at the sector and industry levels. The Fund is currently overweight the Communication Services, Information Technology, and Consumer Discretionary while underweight Real Estate, Utilities, and Industrials.

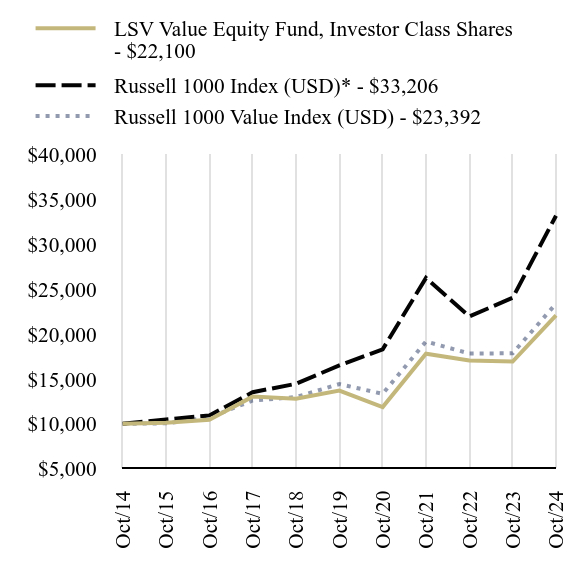

How did the Fund perform during the last 10 years?

Total Return Based on $10,000 Investment

| LSV Value Equity Fund, Investor Class Shares - $22100 | Russell 1000 Index (USD)* - $33206 | Russell 1000 Value Index (USD) - $23392 |

|---|

| Oct/14 | $10000 | $10000 | $10000 |

| Oct/15 | $10103 | $10486 | $10053 |

| Oct/16 | $10450 | $10933 | $10693 |

| Oct/17 | $13030 | $13520 | $12595 |

| Oct/18 | $12797 | $14464 | $12977 |

| Oct/19 | $13707 | $16511 | $14432 |

| Oct/20 | $11865 | $18305 | $13340 |

| Oct/21 | $17817 | $26269 | $19178 |

| Oct/22 | $17058 | $21967 | $17836 |

| Oct/23 | $16946 | $24050 | $17860 |

| Oct/24 | $22100 | $33206 | $23392 |

The line graph represents historical performance of a hypothetical investment of $10,000 in the Fund during the last 10 years. Returns shown are total returns, which assume the reinvestment of dividends and capital gains. The table and graph presented above do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund Shares. Past performance is not indicative of future performance.Call 888-386-3578 or visit https://www.lsvasset.com/value-equity-fund/ for current month-end performance.

Footnote Reference*As of October 2024, pursuant to the new regulatory requirements, this index has been added to represent the broad-based securities market index.

Average Annual Total Returns as of October 31, 2024

| Fund/Index Name | 1 Year | 5 Years | 10 Years |

|---|

| LSV Value Equity Fund, Investor Class Shares | 30.41% | 10.02% | 8.25% |

| Russell 1000 Index (USD)* | 38.07% | 15.00% | 12.75% |

| Russell 1000 Value Index (USD) | 30.98% | 10.14% | 8.87% |

Key Fund Statistics as of October 31, 2024

| Total Net Assets (000's) | Number of Holdings | Total Advisory Fees Paid (000's) | Portfolio Turnover Rate |

|---|

| $1,383,173 | 155 | $7,762 | 26% |

What did the Fund invest in?

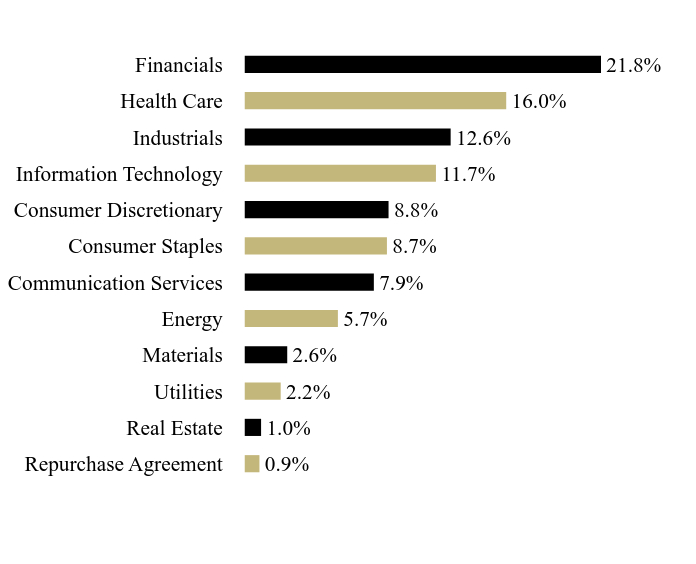

Sector WeightingsFootnote Reference*

| Value | Value |

|---|

| Repurchase Agreement | 0.9% |

| Real Estate | 1.0% |

| Utilities | 2.2% |

| Materials | 2.6% |

| Energy | 5.7% |

| Communication Services | 7.9% |

| Consumer Staples | 8.7% |

| Consumer Discretionary | 8.8% |

| Information Technology | 11.7% |

| Industrials | 12.6% |

| Health Care | 16.0% |

| Financials | 21.8% |

| Footnote | Description |

Footnote* | Percentages are calculated based on total net assets. |

| Holding Name | | | Percentage of Total Net Assets |

|---|

| Comcast, Cl A | | | 2.1% |

| AT&T | | | 2.0% |

| Wells Fargo | | | 1.8% |

| Bank of New York Mellon | | | 1.6% |

| Johnson & Johnson | | | 1.6% |

| State Street | | | 1.5% |

| Bristol-Myers Squibb | | | 1.5% |

| Kroger | | | 1.5% |

| Verizon Communications | | | 1.4% |

| Merck | | | 1.4% |

There were no material changes during the reporting period.

Changes in and Disagreements with Accountants

There were no changes in or disagreements with accountants during the reporting period.

For additional information about the Fund, including its prospectus, financial information, holdings, and proxy voting information, call or visit:

Rule 30e-1 of the Investment Company Act of 1940 permits funds to transmit only one copy of a proxy statement, annual report or semi-annual report to shareholders (who need not be related) with the same residential, commercial or electronic address, provided that the shareholders have consented in writing and the reports are addressed either to each shareholder individually or to the shareholders as a group. This process is known as “householding” and is designed to reduce the duplicate copies of materials that shareholders receive and to lower printing and mailing costs for funds. Once implemented, if you would like to discontinue householding for your accounts, please call toll-free at 888-386-3578 to request individual copies of these documents. Once the Fund receives notice to stop householding, we will begin sending individual copies 30 days after receiving your request.

The Advisors' Inner Circle Fund

LSV Value Equity Fund / Investor Class Shares - LVAEX

Annual Shareholder Report: October 31, 2024

LSV-AR-TSR-2024-13

(b) Not applicable.

Item 2. Code of Ethics.

The Registrant (also referred to as the “Trust”) has adopted a code of ethics that applies to the Registrant’s principal executive officer, principal financial officer, controller or principal accounting officer, and any person who performs a similar function. There have been no amendments to or waivers granted to this code of ethics during the period covered by this report.

Item 3. Audit Committee Financial Expert.

(a)(1) The Registrant’s board of trustees has determined that the Registrant has at least one audit committee financial expert serving on the audit committee.

(a)(2) The Registrant’s audit committee financial expert is Robert Mulhall. Mr. Mulhall is considered to be “independent”, as that term is defined in Form N-CSR Item 3(a)(2).

Item 4. Principal Accountant Fees and Services.

Fees billed by PricewaterhouseCoopers LLP (“PwC”) related to the Trust.

PwC billed the Trust aggregate fees for services rendered to the Trust for the last two fiscal years as follows:

| | FYE October 31, 2024 | FYE October 31, 2023 |

| | | All fees and services to the Trust that were pre-approved | All fees and services to service affiliates that were pre-approved | All other fees and services to service affiliates that did not require pre-approval | All fees and services to the Trust that were pre-approved | All fees and services to service affiliates that were pre-approved | All other fees and services to service affiliates that did not require pre-approval |

| (a) | Audit Fees(1) | $91,274 | None | None | $72,710 | None | None |

| (b) | Audit-Related Fees | None | None | None | None | None | None |

| (c) | Tax Fees | None | None | None | None | None | $115,395(2) |

| (d) | All Other Fees | None | None | None | None | None | $47,411(3) |

Fees billed by Ernst & Young LLP (“E&Y”) related to the Trust.

E&Y billed the Trust aggregate fees for services rendered to the Trust for the last two fiscal years as follows:

| | FYE October 31, 2024 | FYE October 31, 2023 |

| | | All fees and services to the Trust that were pre-approved | All fees and services to service affiliates that were pre-approved | All other fees and services to service affiliates that did not require pre-approval | All fees and services to the Trust that were pre-approved | All fees and services to service affiliates that were pre-approved | All other fees and services to service affiliates that did not require pre-approval |

| (a) | Audit Fees(1) | $539,063 | None | None | $550,800 | None | None |

| (b) | Audit-Related Fees | None | None | None | None | None | None |

| (c) | Tax Fees | None | None | None | None | None | None |

| (d) | All Other Fees | None | None | None | None | None | None |

Fees billed by Cohen & Co. (“Cohen”) related to the Trust.

Cohen billed the Trust aggregate fees for services rendered to the Trust for the last two fiscal years as follows:

| | FYE October 31, 2024 | FYE October 31, 2023 |

| | | All fees and services to the Trust that were pre-approved | All fees and services to service affiliates that were pre-approved | All other fees and services to service affiliates that did not require pre-approval | All fees and services to the Trust that were pre-approved | All fees and services to service affiliates that were pre-approved | All other fees and services to service affiliates that did not require pre-approval |

| (a) | Audit Fees(1) | $43,700 | None | None | $61,000 | None | None |

| (b) | Audit-Related Fees | None | None | None | None | None | None |

| (c) | Tax Fees | None | None | None | None | None | None |

| (d) | All Other Fees | None | None | None | None | None | None |

Notes:

| (1) | Audit fees include amounts related to the audit of the Trust’s annual financial statements and services normally provided by the accountant in connection with statutory and regulatory filings. |

| (2) | Tax compliance services provided to service affiliates of the funds. |

| (3) | Non-audit assurance engagements for service affiliates of the funds. |

(e)(1) The Trust’s Audit Committee has adopted and the Board of Trustees has ratified an Audit and Non-Audit Services Pre-Approval Policy (the “Policy”), which sets forth the procedures and the conditions pursuant to which services proposed to be performed by the independent auditor of the Funds may be pre-approved.

The Policy provides that all requests or applications for proposed services to be provided by the independent auditor must be submitted to the Registrant’s Chief Financial Officer (“CFO”) and must include a detailed description of the services proposed to be rendered. The CFO will determine whether such services:

| (1) | require specific pre-approval; |

| (2) | are included within the list of services that have received the general pre-approval of the Audit Committee pursuant to the Policy; or |

| (3) | have been previously pre-approved in connection with the independent auditor’s annual engagement letter for the applicable year or otherwise. In any instance where services require pre-approval, the Audit Committee will consider whether such services are consistent with SEC’s rules and whether the provision of such services would impair the auditor’s independence. |

Requests or applications to provide services that require specific pre-approval by the Audit Committee will be submitted to the Audit Committee by the CFO. The Audit Committee will be informed by the CFO on a quarterly basis of all services rendered by the independent auditor. The Audit Committee has delegated specific pre-approval authority to either the Audit Committee Chair or financial expert, provided that the estimated fee for any such proposed pre-approved service does not exceed $100,000 and any pre-approval decisions are reported to the Audit Committee at its next regularly-scheduled meeting.

Services that have received the general pre-approval of the Audit Committee are identified and described in the Policy. In addition, the Policy sets forth a maximum fee per engagement with respect to each identified service that has received general pre-approval.

All services to be provided by the independent auditor shall be provided pursuant to a signed written engagement letter with the Registrant, the investment adviser, or applicable control affiliate (except that matters as to which an engagement letter would be impractical because of timing issues or because the matter is small may not be the subject of an engagement letter) that sets forth both the services to be provided by the independent auditor and the total fees to be paid to the independent auditor for those services.

In addition, the Audit Committee has determined to take additional measures on an annual basis to meet the Audit Committee’s responsibility to oversee the work of the independent auditor and to assure the auditor's independence from the Registrant, such as (a) reviewing a formal written statement from the independent auditor delineating all relationships between the independent auditor and the Registrant, and (b) discussing with the independent auditor the independent auditor’s methods and procedures for ensuring independence.

(e)(2) Percentage of fees billed applicable to non-audit services pursuant to waiver of pre-approval requirement were as follows (PwC):

| | 2024 | 2023 |

Audit-Related Fees | None | None |

| Tax Fees | None | None |

All Other Fees | None | None |

(e)(2) Percentage of fees billed applicable to non-audit services pursuant to waiver of pre-approval requirement were as follows (E&Y):

| | 2024 | 2023 |

Audit-Related Fees | None | None |

| Tax Fees | None | None |

All Other Fees | None | None |

(e)(2) Percentage of fees billed applicable to non-audit services pursuant to waiver of pre-approval requirement were as follows (Cohen):

| | 2024 | 2023 |

Audit-Related Fees | None | None |

| Tax Fees | None | None |

All Other Fees | None | None |

(f) Not applicable.

(g) The aggregate non-audit fees and services billed by PwC for services rendered to the Registrant, and rendered to the Registrant’s investment adviser (not including any sub-adviser whose role is primarily portfolio management and is subcontracted with or overseen by another investment adviser), and any entity controlling, controlled by, or under common control with the adviser that provides ongoing services to the Registrant for the last two fiscal-years-ended October 31st were $0 and $162,806 for 2024 and 2023, respectively.

(g) The aggregate non-audit fees and services billed by E&Y for services rendered to the Registrant, and rendered to the Registrant’s investment adviser (not including any sub-adviser whose role is primarily portfolio management and is subcontracted with or overseen by another investment adviser), and any entity controlling, controlled by, or under common control with the adviser that provides ongoing services to the Registrant for the last two fiscal-years-ended October 31st were $0 and $0 for 2024 and 2023, respectively.

(g) The aggregate non-audit fees and services billed by Cohen for services rendered to the Registrant, and rendered to the Registrant’s investment adviser (not including any sub-adviser whose role is primarily portfolio management and is subcontracted with or overseen by another investment adviser), and any entity controlling, controlled by, or under common control with the adviser that provides ongoing services to the Registrant for the last two fiscal-years-ended October 31st were $0 and $0 for 2024 and 2023, respectively.

(h) During the past fiscal year, all non-audit services provided by the Registrant’s principal accountant to either the Registrant’s investment adviser or to any entity controlling, controlled by, or under common control with the Registrant’s investment adviser that provides ongoing services to the Registrant were pre-approved by the Audit Committee of Registrant’s Board of Trustees. Included in the Audit Committee’s pre-approval of these non-audit service were the review and consideration as to whether the provision of these non-audit services is compatible with maintaining the principal accountant’s independence.

(i) Not Applicable. The Registrant has not retained, for the preparation of the audit report on the financial statements included in the Form N-CSR, a registered public accounting firm that has a branch or office that is located in a foreign jurisdiction and that the Public Company Accounting Oversight Board (the “PCAOB”) has determined that the PCAOB is unable to inspect or investigate completely because of a position taken by an authority in the foreign jurisdiction.

(j) Not applicable. The Registrant is not a “foreign issuer,” as defined in 17 CFR § 240.3b-4.

Item 5. Audit Committee of Listed Registrants.

Not applicable to open-end management investment companies.

Item 6. Schedule of Investments.

(a) The Schedule of Investments is included as part of the Financial Statements and Other Information filed under Item 7 of this form.

(b) Not applicable.

Item 7. Financial Statements and Financial Highlights for Open-End Management Investment Companies.

Financial statements and financial highlights are filed herein.

THE ADVISORS’ INNER CIRCLE FUND

Value Equity Fund

ANNUAL FINANCIALS AND OTHER INFORMATION

October 31, 2024

This information must be preceded or accompanied by a current prospectus. Investors should read the prospectus carefully before investing.

| THE ADVISORS’ INNER CIRCLE FUND | LSV |

Value Equity Fund

October 31, 2024

TABLE OF CONTENTS

| Financial Statements (Form N-CSR Item 7) | |

| Schedule of Investments | 1 |

| Statement of Assets and Liabilities | 4 |

| Statement of Operations | 5 |

| Statements of Changes in Net Assets | 6 |

| Financial Highlights | 7 |

| Notes to Financial Statements | 8 |

| Report of Independent Registered Public Accounting Firm | 13 |

| Notice to Shareholders (Unaudited) | 14 |

Schedule of Investments

October 31, 2024

LSV Value Equity Fund

| | Shares | | | Value (000) | |

| Common Stock (99.0%) | | | |

| Communication Services (7.9%) | | | | | | | | |

| AT&T | | | 1,211,800 | | | $ | 27,314 | |

| Comcast, Cl A | | | 667,700 | | | | 29,159 | |

| Fox | | | 326,200 | | | | 13,700 | |

| Meta Platforms, Cl A | | | 15,100 | | | | 8,570 | |

| Nexstar Media Group, Cl A | | | 27,100 | | | | 4,768 | |

| Playtika Holding | | | 338,246 | | | | 2,648 | |

| TEGNA | | | 206,400 | | | | 3,391 | |

| Verizon Communications | | | 471,000 | | | | 19,843 | |

| | | | | | | | 109,393 | |

| Consumer Discretionary (8.8%) | | | | | | | | |

| Adtalem Global Education* | | | 48,100 | | | | 3,892 | |

| BorgWarner | | | 203,800 | | | | 6,854 | |

| Capri Holdings* | | | 66,800 | | | | 1,319 | |

| Carter's | | | 60,900 | | | | 3,331 | |

| Dick's Sporting Goods | | | 34,200 | | | | 6,695 | |

| eBay | | | 245,900 | | | | 14,142 | |

| Ford Motor | | | 476,300 | | | | 4,901 | |

| General Motors | | | 296,100 | | | | 15,030 | |

| Group 1 Automotive | | | 14,100 | | | | 5,137 | |

| H&R Block | | | 110,700 | | | | 6,612 | |

| Harley-Davidson | | | 188,800 | | | | 6,032 | |

| Macy's | | | 198,700 | | | | 3,048 | |

| MGM Resorts International* | | | 106,200 | | | | 3,916 | |

| Phinia | | | 30,840 | | | | 1,437 | |

| PulteGroup | | | 119,800 | | | | 15,518 | |

| PVH | | | 57,300 | | | | 5,642 | |

| Tri Pointe Homes* | | | 266,400 | | | | 10,770 | |

| Upbound Group, Cl A | | | 134,100 | | | | 3,921 | |

| Whirlpool | | | 38,300 | | | | 3,964 | |

| | | | | | | | 122,161 | |

| Consumer Staples (8.7%) | | | | | | | | |

| Altria Group | | | 327,200 | | | | 17,819 | |

| Bunge Global | | | 86,200 | | | | 7,242 | |

| Campbell Soup | | | 208,200 | | | | 9,713 | |

| Conagra Brands | | | 170,000 | | | | 4,920 | |

| Edgewell Personal Care | | | 130,600 | | | | 4,564 | |

| Energizer Holdings | | | 166,400 | | | | 5,336 | |

| General Mills | | | 113,100 | | | | 7,693 | |

| Ingredion | | | 79,200 | | | | 10,515 | |

| Kraft Heinz | | | 410,800 | | | | 13,745 | |

| Kroger | | | 374,200 | | | | 20,869 | |

| Molson Coors Beverage, Cl B | | | 246,300 | | | | 13,416 | |

| PriceSmart | | | 49,900 | | | | 4,146 | |

| | | | | | | | 119,978 | |

| Energy (5.7%) | | | | | | | | |

| APA | | | 185,700 | | | | 4,382 | |

| California Resources | | | 91,800 | | | | 4,771 | |

| ExxonMobil | | | 124,500 | | | | 14,539 | |

| Halliburton | | | 264,900 | | | | 7,348 | |

| Helmerich & Payne | | | 100,800 | | | | 3,387 | |

| HF Sinclair | | | 112,900 | | | | 4,359 | |

LSV Value Equity Fund

| | Shares | | | Value (000) | |

| Energy (continued) | | | | | | | | |

| Marathon Oil | | | 290,900 | | | $ | 8,058 | |

| Marathon Petroleum | | | 63,800 | | | | 9,281 | |

| Murphy Oil | | | 135,800 | | | | 4,275 | |

| Phillips 66 | | | 72,200 | | | | 8,796 | |

| Scorpio Tankers | | | 44,700 | | | | 2,605 | |

| Valero Energy | | | 57,500 | | | | 7,461 | |

| | | | | | | | 79,262 | |

| Financials (21.8%) | | | | | | | | |

| Aflac | | | 69,300 | | | | 7,262 | |

| Ally Financial | | | 148,800 | | | | 5,216 | |

| American International Group | | | 171,900 | | | | 13,044 | |

| Ameriprise Financial | | | 25,900 | | | | 13,217 | |

| Bank of America | | | 170,000 | | | | 7,109 | |

| Bank of New York Mellon | | | 298,000 | | | | 22,457 | |

| Blue Owl Capital | | | 331,600 | | | | 4,987 | |

| Capital One Financial | | | 38,100 | | | | 6,202 | |

| Citigroup | | | 300,500 | | | | 19,283 | |

| Citizens Financial Group | | | 205,900 | | | | 8,673 | |

| CNO Financial Group | | | 278,100 | | | | 9,567 | |

| Discover Financial Services | | | 26,000 | | | | 3,859 | |

| Everest Group | | | 24,100 | | | | 8,570 | |

| First Horizon | | | 542,100 | | | | 9,395 | |

| Goldman Sachs Group | | | 29,400 | | | | 15,223 | |

| Hartford Financial Services Group | | | 160,800 | | | | 17,759 | |

| Jackson Financial, Cl A | | | 43,300 | | | | 4,328 | |

| Lincoln National | | | 102,200 | | | | 3,551 | |

| MetLife | | | 61,800 | | | | 4,846 | |

| MGIC Investment | | | 447,800 | | | | 11,213 | |

| Navient | | | 222,860 | | | | 3,171 | |

| PayPal Holdings* | | | 199,600 | | | | 15,828 | |

| Popular | | | 31,000 | | | | 2,766 | |

| Radian Group | | | 256,700 | | | | 8,962 | |

| Regions Financial | | | 336,800 | | | | 8,039 | |

| State Street | | | 225,500 | | | | 20,926 | |

| Victory Capital Holdings, Cl A | | | 104,700 | | | | 6,275 | |

| Voya Financial | | | 65,500 | | | | 5,260 | |

| Wells Fargo | | | 373,200 | | | | 24,228 | |

| Western Union | | | 577,400 | | | | 6,213 | |

| Zions Bancorp | | | 104,000 | | | | 5,414 | |

| | | | | | | | 302,843 | |

| Health Care (16.0%) | | | | | | | | |

| Amgen | | | 13,300 | | | | 4,258 | |

| Baxter International | | | 137,100 | | | | 4,894 | |

| Bristol-Myers Squibb | | | 375,200 | | | | 20,925 | |

| Cardinal Health | | | 65,900 | | | | 7,151 | |

| Centene* | | | 186,000 | | | | 11,580 | |

| Cigna Group | | | 37,400 | | | | 11,774 | |

| CVS Health | | | 211,900 | | | | 11,964 | |

| DaVita* | | | 28,300 | | | | 3,957 | |

| Exelixis* | | | 283,900 | | | | 9,425 | |

| Gilead Sciences | | | 195,500 | | | | 17,364 | |

The accompanying notes are an integral part of the financial statements

Schedule of Investments

October 31, 2024

LSV Value Equity Fund

| | | Shares | | | Value (000) | |

| Health Care (continued) |

| HCA Healthcare | | | 28,400 | | | $ | 10,188 | |

| Incyte* | | | 122,300 | | | | 9,065 | |

| Jazz Pharmaceuticals* | | | 64,400 | | | | 7,086 | |

| Johnson & Johnson | | | 137,700 | | | | 22,013 | |

| McKesson | | | 11,500 | | | | 5,757 | |

| Merck | | | 189,500 | | | | 19,389 | |

| Organon | | | 376,100 | | | | 7,063 | |

| Pfizer | | | 418,400 | | | | 11,841 | |

| United Therapeutics* | | | 31,900 | | | | 11,930 | |

| Universal Health Services, Cl B | | | 29,400 | | | | 6,007 | |

| Viatris, Cl W | | | 517,700 | | | | 6,005 | |

| | | | | | | | 219,636 | |

| Industrials (12.6%) |

| AGCO | | | 82,900 | | | | 8,277 | |

| Allison Transmission Holdings | | | 144,200 | | | | 15,409 | |

| Brink's | | | 67,000 | | | | 6,887 | |

| CNH Industrial | | | 679,000 | | | | 7,625 | |

| CSG Systems International | | | 90,300 | | | | 4,209 | |

| Cummins | | | 46,600 | | | | 15,331 | |

| Delta Air Lines | | | 104,800 | | | | 5,997 | |

| Deluxe | | | 71,546 | | | | 1,342 | |

| FedEx | | | 48,600 | | | | 13,309 | |

| GMS* | | | 40,100 | | | | 3,605 | |

| Huntington Ingalls Industries | | | 11,100 | | | | 2,053 | |

| Lockheed Martin | | | 31,300 | | | | 17,091 | |

| ManpowerGroup | | | 55,100 | | | | 3,463 | |

| Mueller Industries | | | 184,500 | | | | 15,123 | |

| Oshkosh | | | 32,700 | | | | 3,343 | |

| Owens Corning | | | 57,210 | | | | 10,114 | |

| PACCAR | | | 33,700 | | | | 3,514 | |

| Ryder System | | | 82,100 | | | | 12,010 | |

| Snap-on | | | 12,800 | | | | 4,226 | |

| Textron | | | 172,910 | | | | 13,906 | |

| United Airlines Holdings* | | | 75,700 | | | | 5,924 | |

| | | | | | | | 172,758 | |

| Information Technology (11.7%) |

| Amdocs | | | 90,500 | | | | 7,941 | |

| Amkor Technology | | | 170,400 | | | | 4,337 | |

| Applied Materials | | | 42,400 | | | | 7,699 | |

| Arrow Electronics* | | | 84,600 | | | | 10,040 | |

| Cirrus Logic* | | | 52,600 | | | | 5,777 | |

| Cisco Systems | | | 282,400 | | | | 15,467 | |

| Dell Technologies, Cl C | | | 116,700 | | | | 14,428 | |

| Dropbox, Cl A* | | | 238,000 | | | | 6,152 | |

| DXC Technology* | | | 207,400 | | | | 4,119 | |

| Flex* | | | 311,100 | | | | 10,786 | |

| Gen Digital | | | 286,100 | | | | 8,328 | |

| Hewlett Packard Enterprise | | | 587,300 | | | | 11,447 | |

| HP | | | 464,000 | | | | 16,481 | |

| Intel | | | 140,200 | | | | 3,017 | |

| International Business Machines | | | 31,100 | | | | 6,429 | |

LSV Value Equity Fund

| | | Shares | | | Value (000) | |

| Information Technology (continued) | | | | | | | | |

| Jabil | | | 52,100 | | | $ | 6,413 | |

| QUALCOMM | | | 86,800 | | | | 14,128 | |

| Skyworks Solutions | | | 47,900 | | | | 4,195 | |

| Western Digital* | | | 77,300 | | | | 5,048 | |

| | | | | | | | 162,232 | |

| Materials (2.6%) | | | | | | | | |

| Berry Global Group | | | 181,300 | | | | 12,773 | |

| Graphic Packaging Holding | | | 246,200 | | | | 6,958 | |

| NewMarket | | | 7,300 | | | | 3,832 | |

| Steel Dynamics | | | 95,000 | | | | 12,398 | |

| | | | | | | | 35,961 | |

| Real Estate (1.0%) | | | | | | | | |

| Highwoods Properties‡ | | | 140,300 | | | | 4,706 | |

| Host Hotels & Resorts‡ | | | 196,000 | | | | 3,379 | |

| Piedmont Office Realty Trust, Cl A‡ | | | 206,087 | | | | 2,048 | |

| Simon Property Group‡ | | | 21,300 | | | | 3,602 | |

| | | | | | | | 13,735 | |

| Utilities (2.2%) | | | | | | | | |

| NRG Energy | | | 175,600 | | | | 15,874 | |

| UGI | | | 306,300 | | | | 7,324 | |

| Vistra | | | 62,600 | | | | 7,823 | |

| | | | | | | | 31,021 | |

| TOTAL COMMON STOCK | | | | | | | | |

| (Cost $1,104,732) | | | | | | | 1,368,980 | |

| | | Face Amount | | | | | | |

| | | | (000) | | | | | |

| Repurchase Agreement (0.9%) | | | | | | | | |

| South Street Securities 4.500%, dated 10/31/2024, to be repurchased on 11/01/2024, repurchase price $13,030 (collateralized by various U.S. Treasury obligations, ranging in par value $0 - $12,522, 0.625% - 4.250%, 03/31/2025 - 02/15/2052; total market value $13,289) | | $ | 13,029 | | | | 13,029 | |

| TOTAL REPURCHASE AGREEMENT | | | | | | | | |

| (Cost $13,029) | | | | | | | 13,029 | |

| | | | | | | | | |

| Total Investments – 99.9% | | | | | | | | |

| (Cost $1,117,761) | | | | | | $ | 1,382,009 | |

Percentages are based on Net Assets of $1,383,173(000).

| ‡ | Real Estate Investment Trust. |

| * | Non-income producing security. |

Cl — Class

The accompanying notes are an integral part of the financial statements

Schedule of Investments

October 31, 2024

The following is a summary of the inputs used as of October 31, 2024, in valuing the Fund’s investments carried at value ($ Thousands):

| Investments in Securities | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| Common Stock | | $ | 1,368,980 | | | $ | — | | | $ | — | | | $ | 1,368,980 | |

| Repurchase Agreement | | | — | | | | 13,029 | | | | — | | | | 13,029 | |

| Total Investments in Securities | | $ | 1,368,980 | | | $ | 13,029 | | | $ | — | | | $ | 1,382,009 | |

Amounts designated as “—“ are $0 or have been rounded to $0.

For more information on valuation inputs, see Note 2 — Significant Accounting Policies in the Notes to Financial Statements.

The accompanying notes are an integral part of the financial statements

Statement of Assets and Liabilities (000)

October 31, 2024

| | | LSV Value Equity | |

| | | Fund | |

| Assets: | | | | |

| Investments, at Value (Cost $1,117,761) | | $ | 1,382,009 | |

| Receivable for Capital Shares Sold | | | 1,662 | |

| Dividends and Interest Receivable | | | 1,556 | |

| Receivable for Investment Securities Sold | | | 557 | |

| Prepaid Expenses | | | 52 | |

| Total Assets | | | 1,385,836 | |

| Liabilities: | | | | |

| Payable for Fund Shares Redeemed | | | 1,570 | |

| Payable due to Investment Adviser | | | 667 | |

| Payable due to Administrator | | | 70 | |

| Payable due to Distributor | | | 66 | |

| Payable due to Trustees | | | 24 | |

| Payable due to Chief Compliance Officer | | | 12 | |

| Other Accrued Expenses | | | 254 | |

| Total Liabilities | | | 2,663 | |

| Net Assets | | $ | 1,383,173 | |

| Net Assets Consist of: | | | | |

| Paid-in Capital | | $ | 1,015,630 | |

| Total Distributable Earnings | | | 367,543 | |

| Net Assets | | $ | 1,383,173 | |

| Net Asset Value, Offering and Redemption Price Per Share — Institutional Class Shares ($1,076,076 ÷ 37,709,667 shares)(1) | | $ | 28.54 | * |

| Net Asset Value, Offering and Redemption Price Per Share — Investor Class Shares ($307,097 ÷ 10,833,944 shares)(1) | | $ | 28.35 | * |

| (1) | Shares have not been rounded. |

| * | Net Assets divided by Shares does not calculate to the stated NAV because Net Asset amounts are shown rounded |

The accompanying notes are an integral part of the financial statements

Statement of Operations (000)

For the year ended October 31, 2024

| | | LSV Value Equity | |

| | | Fund | |

| Investment Income: | | | | |

| Dividend Income | | $ | 38,103 | |

| Interest Income | | | 696 | |

| Foreign Taxes Withheld | | | (19 | ) |

| Total Investment Income | | | 38,780 | |

| Expenses: | | | | |

| Investment Advisory Fees | | | 7,762 | |

| Administration Fees | | | 829 | |

| Distribution Fees - Investor Class | | | 806 | |

| Trustees' Fees | | | 106 | |

| Chief Compliance Officer Fees | | | 15 | |

| Professional Fees | | | 209 | |

| Transfer Agent Fees | | | 152 | |

| Printing Fees | | | 126 | |

| Custodian Fees | | | 98 | |

| Registration and Filing Fees | | | 81 | |

| Insurance and Other Fees | | | 86 | |

| Total Expenses | | | 10,270 | |

| Less: Fees Paid Indirectly — (see Note 4) | | | (39 | ) |

| Net Expenses | | | 10,231 | |

| Net Investment Income | | | 28,549 | |

| Net Realized Gain on Investments | | | 81,724 | |

| Net Change in Unrealized Appreciation on Investments | | | 253,364 | |

| Net Realized and Unrealized Gain on Investments | | | 335,088 | |

| Net Increase in Net Assets Resulting from Operations | | $ | 363,637 | |

The accompanying notes are an integral part of the financial statements

Statements of Changes in Net Assets (000)

For the year ended October 31,

| | | LSV Value Equity Fund | |

| | | 2024 | | | 2023 | |

| Operations: | | | | | | |

| Net Investment Income | | $ | 28,549 | | | $ | 32,128 | |

| Net Realized Gain | | | 81,724 | | | | 66,519 | |

| Net Change in Unrealized Appreciation (Depreciation) | | | 253,364 | | | | (90,204 | ) |

| Net Increase in Net Assets Resulting from Operations | | | 363,637 | | | | 8,443 | |

| Distributions | | | | | | | | |

| Institutional Class Shares | | | (81,000 | ) | | | (159,277 | ) |

| Investor Class Shares | | | (15,327 | ) | | | (47,150 | ) |

| Total Distributions | | | (96,327 | ) | | | (206,427 | ) |

| Capital Share Transactions: | | | | | | | | |

| Institutional Class Shares: | | | | | | | | |

| Issued | | | 118,434 | | | | 119,376 | |

| Reinvestment of Dividends and Distributions | | | 79,941 | | | | 157,376 | |

| Redeemed | | | (344,233 | ) | | | (350,837 | ) |

| Net Decrease from Institutional Class Shares Transactions | | | (145,858 | ) | | | (74,085 | ) |

| Investor Class Shares: | | | | | | | | |

| Issued | | | 421,083 | | | | 124,194 | |

| Reinvestment of Dividends and Distributions | | | 15,291 | | | | 47,079 | |

| Redeemed | | | (423,068 | ) | | | (306,555 | ) |

| Net Increase (Decrease) from Investor Class Shares Transactions | | | 13,306 | | | | (135,282 | ) |

| Net Decrease in Net Assets Derived from Capital Share Transactions | | | (132,552 | ) | | | (209,367 | ) |

| Total Increase (Decrease) in Net Assets | | | 134,758 | | | | (407,351 | ) |

| Net Assets: | | | | | | | | |

| Beginning of Year | | | 1,248,415 | | | | 1,655,766 | |

| End of Year | | $ | 1,383,173 | | | $ | 1,248,415 | |

| Shares Transactions: | | | | | | | | |

| Institutional Class: | | | | | | | | |

| Issued | | | 4,476 | | | | 4,849 | |

| Reinvestment of Dividends and Distributions | | | 3,151 | | | | 6,498 | |

| Redeemed | | | (13,116 | ) | | | (14,154 | ) |

| Total Institutional Class Share Transactions | | | (5,489 | ) | | | (2,807 | ) |

| Investor Class: | | | | | | | | |

| Issued | | | 15,727 | | | | 5,121 | |

| Reinvestment of Dividends and Distributions | | | 606 | | | | 1,957 | |

| Redeemed | | | (15,553 | ) | | | (12,429 | ) |

| Total Investor Class Share Transactions | | | 780 | | | | (5,351 | ) |

| Net Decrease in Shares Outstanding | | | (4,709 | ) | | | (8,158 | ) |

The accompanying notes are an integral part of the financial statements

Financial Highlights

For a share outstanding throughout each year ended October 31,

| | | | Net Asset Value Beginning of Year | | | Net Investment Income(1) | | | Realized and Unrealized Gains (Losses) | | | Total from Operations | | | Dividends from Net Investment Income | | | Distributions from Realized Gains | | | Total Dividends and Distributions | | | Net Asset Value End of Year | | | Total Return† | | | Net Assets End of Year (000) | | | Ratio of Expenses to Average Net Assets | | | Ratio of Expenses to Average Net Assets (Excluding Waivers, Reimbursements and Fees Paid Indirectly) | | | Ratio of Net Investment Income to Average Net Assets | | | Portfolio Turnover Rate | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| LSV Value Equity Fund | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Institutional Class Shares | |

| 2024 | | | $ | 23.47 | | | $ | 0.55 | | | $ | 6.40 | | | $ | 6.95 | | | $ | (0.59 | ) | | $ | (1.29 | ) | | $ | (1.88 | ) | | $ | 28.54 | | | | 30.77 | % | | $ | 1,076,076 | | | | 0.67 | % | | | 0.67 | % | | | 2.08 | % | | | 26 | % |

| 2023 | | | | 27.01 | | | | 0.57 | | | | (0.65 | ) | | | (0.08 | ) | | | (0.60 | ) | | | (2.86 | ) | | | (3.46 | ) | | | 23.47 | | | | (0.43 | ) | | | 1,013,997 | | | | 0.68 | | | | 0.68 | | | | 2.28 | | | | 10 | |

| 2022 | | | | 31.86 | | | | 0.56 | | | | (1.63 | ) | | | (1.07 | ) | | | (0.59 | ) | | | (3.19 | ) | | | (3.78 | ) | | | 27.01 | | | | (4.00 | ) | | | 1,242,510 | | | | 0.66 | | | | 0.66 | | | | 2.00 | | | | 28 | |

| 2021 | | | | 22.35 | | | | 0.54 | | | | 10.39 | | | | 10.93 | | | | (0.62 | ) | | | (0.80 | ) | | | (1.42 | ) | | | 31.86 | | | | 50.55 | | | | 1,354,981 | | | | 0.66 | | | | 0.66 | | | | 1.83 | | | | 9 | |

| 2020 | | | | 27.03 | | | | 0.55 | | | | (3.87 | ) | | | (3.32 | ) | | | (0.59 | ) | | | (0.77 | ) | | | (1.36 | ) | | | 22.35 | | | | (13.22 | ) | | | 1,090,639 | | | | 0.65 | | | | 0.65 | | | | 2.29 | | | | 24 | |

| Investor Class Shares | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 2024 | | | $ | 23.32 | | | $ | 0.49 | | | $ | 6.35 | | | $ | 6.84 | | | $ | (0.52 | ) | | $ | (1.29 | ) | | $ | (1.81 | ) | | $ | 28.35 | | | | 30.41 | % | | $ | 307,097 | | | | 0.92 | % | | | 0.92 | % | | | 1.82 | % | | | 26 | % |

| 2023 | | | | 26.83 | | | | 0.52 | | | | (0.65 | ) | | | (0.13 | ) | | | (0.52 | ) | | | (2.86 | ) | | | (3.38 | ) | | | 23.32 | | | | (0.66 | ) | | | 234,418 | | | | 0.93 | | | | 0.93 | | | | 2.09 | | | | 10 | |

| 2022 | | | | 31.66 | | | | 0.50 | | | | (1.65 | ) | | | (1.15 | ) | | | (0.49 | ) | | | (3.19 | ) | | | (3.68 | ) | | | 26.83 | | | | (4.26 | ) | | | 413,256 | | | | 0.91 | | | | 0.91 | | | | 1.79 | | | | 28 | |

| 2021 | | | | 22.24 | | | | 0.46 | | | | 10.34 | | | | 10.80 | | | | (0.58 | ) | | | (0.80 | ) | | | (1.38 | ) | | | 31.66 | | | | 50.16 | | | | 671,772 | | | | 0.91 | | | | 0.91 | | | | 1.59 | | | | 9 | |

| 2020 | | | | 26.91 | | | | 0.42 | | | | (3.79 | ) | | | (3.37 | ) | | | (0.53 | ) | | | (0.77 | ) | | | (1.30 | ) | | | 22.24 | | | | (13.43 | ) | | | 725,566 | | | | 0.91 | | | | 0.91 | | | | 1.82 | | | | 24 | |

| † | Total return is for the period indicated and has not been annualized. Total return would have been lower had the Adviser not waived a portion of its fee. |

Total returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

| (1) | Per share data calculated using average shares method. |

The accompanying notes are an integral part of the financial statements

Notes to Financial Statements

October 31, 2024

1. Organization:

The Advisors’ Inner Circle Fund (the “Trust”) is organized as a Massachusetts business trust under an Amended and Restated Agreement and Declaration of Trust dated February 18, 1997. The Trust is registered under the Investment Company Act of 1940, as amended, as an open-end management investment company with 26 funds. The financial statements herein are those of the LSV Value Equity Fund, a diversified Fund (the “Fund”). The Fund seeks long-term growth of capital by investing in undervalued stocks which are out of favor in the market. The financial statements of the remaining funds of the Trust are not presented herein, but are presented separately. The assets of each fund are segregated, and a shareholder’s interest is limited to the fund in which shares are held.

2. Significant Accounting Policies:

The accompanying financial statements have been prepared in conformity with U.S. generally accepted accounting principles (“U.S. GAAP”) and are presented in U.S. dollars which is the functional currency of the Fund. The Fund is an investment company and therefore applies the accounting and reporting guidance issued by the U.S. Financial Accounting Standards Board (“FASB”) in Accounting Standards Codification (“ASC”) Topic 946, Financial Services — Investment Companies. The following are significant accounting policies which are consistently followed in the preparation of the financial statements.

Use of Estimates — The preparation of financial statements requires management to make estimates and assumptions that affect the fair value of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates and such differences could be material.

Security Valuation — Securities listed on a securities exchange, market or automated quotation system for which quotations are readily available (except for securities traded on NASDAQ), including securities traded over the counter, are valued at the last quoted sale price on an exchange or market (foreign or domestic) on which they are traded on the valuation date (or at approximately 4:00 pm ET if a security’s primary exchange is normally open at that time), or, if there is no such reported sale on the valuation date, at the most recent quoted bid price. For securities traded on NASDAQ, the NASDAQ Official Closing

Price will be used. The prices for foreign securities are reported in local currency and converted to U.S. dollars using currency exchange rates.

Securities for which market prices are not “readily available” are valued in accordance with fair value procedures (the "Fair Value Procedures") established by the Adviser and approved by the Trust's Board of Trustees (the “Board”). Pursuant to Rule 2a-5 under the 1940 Act, the Board has designated the Adviser as the "valuation designee" to determine the fair value of securities and other instruments for which no readily available market quotations are available. The Fair Value Procedures are implemented through a Fair Value Committee (the “Committee”) of the Adviser.

Some of the more common reasons that may necessitate that a security be valued using Fair Value Procedures include: the security’s trading has been halted or suspended; the security has been de-listed from a national exchange; the security’s primary trading market is temporarily closed at a time when under normal conditions it would be open; the security has not been traded for an extended period of time; the security’s primary pricing source is not able or willing to provide a price; or trading of the security is subject to local government-imposed restrictions. When a security is valued in accordance with the Fair Value Procedures, the Committee will determine the value after taking into consideration relevant information reasonably available to the Committee. As of October 31, 2024, there were no securities valued in accordance with the Fair Value Procedures.

In accordance with the authoritative guidance on fair value measurements and disclosure under U.S. GAAP, the Fund discloses fair value of its investments in a hierarchy that prioritizes the inputs to valuation techniques used to measure the fair value. The objective of a fair value measurement is to determine the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date (an exit price). Accordingly, the fair value hierarchy gives the highest priority to quoted prices (unadjusted) in active markets for identical assets or liabilities (Level 1) and the lowest priority to unobservable inputs (Level 3). The three levels of the fair value hierarchy are described below:

Level 1 — Unadjusted quoted prices in active markets for identical, unrestricted assets or liabilities that the Fund has the ability to access at the measurement date;

Level 2 — Other significant observable inputs (includes quoted prices for similar securities, interest rates, prepayment speeds, credit risk, referenced indices, quoted prices in inactive markets, adjusted quoted prices in active markets, adjusted quoted prices on foreign equity securities that were adjusted in accordance with The Adviser’s pricing procedures,etc.); and

Notes to Financial Statements

October 31, 2024

Level 3 — Prices, inputs or proprietary modeling techniques which are both significant to the fair value measurement and unobservable (supported by little or no market activity).

Investments are classified within the level of the lowest significant input considered in determining fair value. Investments classified within Level 3 whose fair value measurement considers several inputs may include Level 1 or Level 2 inputs as components of the overall fair value measurement.

Federal Income Taxes — It is the Fund’s intention to continue to qualify as a regulated investment company for Federal income tax purposes by complying with the appropriate provisions of Subchapter M of the Internal Revenue Code of 1986, as amended and to distribute substantially all of its income to shareholders. Accordingly, no provision for Federal income taxes has been made in the financial statements.

The Fund evaluates tax positions taken or expected to be taken in the course of preparing the Fund’s tax returns to determine whether it is “more-likely-than-not” (i.e., greater than 50-percent) that each tax position will be sustained upon examination by a taxing authority based on the technical merits of the position. Tax positions not deemed to meet the more-likely-than-not threshold are recorded as a tax benefit or expense in the current year. The Fund did not record any tax provision in the current period. However, management’s conclusions regarding tax positions taken may be subject to review and adjustment at a later date based on factors including, but not limited to, examination by tax authorities on open tax years (i.e. the last three open tax year ends, as applicable), on-going analysis of and changes to tax laws, regulations and interpretations thereof.

As of and during the year ended October 31, 2024, the Fund did not have a liability for any unrecognized tax benefits. The Fund recognizes interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the Statement of Operations. During the year ended October 31, 2024, the Fund did not incur any interest or penalties.

Withholding taxes on foreign dividends, if any, have been provided for in accordance with the Funds’ understanding of the applicable country’s tax rules and rates. The Funds or their agent files withholding tax reclaims in certain jurisdictions to recover certain amounts previously withheld. The Funds may record

a reclaim receivable based on collectability, which includes factors such as the jurisdiction’s applicable laws, payment history and market convention. Professional fees paid to those that provide assistance in receiving the tax reclaims, which generally are contingent upon successful receipt of reclaimed amounts, are recorded in Professional Fees on the Statements of Operations once the amounts are due. The professional fees related to pursuing these tax reclaims are not subject to the Adviser’s expense limitation agreement.

Security Transactions and Investment Income — Security transactions are accounted for on trade date for financial reporting purposes. Costs used in determining realized gains or losses on the sale of investment securities are based on the specific identification method. Dividend income is recorded on the ex-dividend date. Interest income is recognized on the accrual basis from settlement date.

Investments in Real Estate Investment Trusts (REITs) — With respect to the Fund, dividend income is recorded based on the income included in distributions received from the REIT investments using published REIT reclassifications including some management estimates when actual amounts are not available. Distributions received in excess of this estimated amount are recorded as a reduction of the cost of investments or reclassified to capital gains. The actual amounts of income, return of capital, and capital gains are only determined by each REIT after its fiscal year-end, and may differ from the estimated amounts.

Repurchase Agreements — In connection with transactions involving repurchase agreements, a third party custodian bank takes possession of the underlying securities (“collateral”), the value of which exceeds the principal amount of the repurchase transaction, including accrued interest. Such collateral will be cash, debt securities issued or guaranteed by the U.S. Government, securities that at the time the repurchase agreement is entered into are rated in the highest category by a nationally recognized statistical rating organization (“NRSRO”) or unrated category by an NRSRO, as determined by the Adviser. Provisions of the repurchase agreements and procedures adopted by the Board require that the market value of the collateral, including accrued interest thereon, is sufficient in the event of default by the counterparty. In the event of default on the obligation to repurchase, the Fund has the right to liquidate the collateral and apply the proceeds in satisfaction of the obligation. In the event of default or bankruptcy by the counterparty to the agreement, realization and/or retention of the collateral or proceeds may be subject to legal proceedings.

Notes to Financial Statements

October 31, 2024

Repurchase agreements are entered into by the Fund under Master Repurchase Agreements (“MRA”) which permit the Fund, under certain circumstances including an event of default (such as bankruptcy or insolvency), to offset payables and/or receivables under the MRA with collateral held and/or posted to the counterparty and create one single net payment due to or from the Fund.

At October 31, 2024, the open repurchase agreements by counterparty which are subject to a MRA on a net payment basis are as follows (000):

| Counterparty | | Repurchase Agreement | | | Fair Value of Non-Cash Collateral Received(1) | | | Cash Collateral Received(1) | | | Net Amount(2) | |

| South Street Securities | | $ | 13,029 | | | $ | 13,029 | | | $ | — | | | $ | — | |

| (1) | The amount of collateral reflected in the table does not include any over-collateralization received by the Fund. |

| (2) | Net amount represents the net amount receivable due from the counterparty in the event of default. |

Expenses— Expenses that are directly related to the Fund are charged to the Fund. Other operating expenses of the Trust are prorated to the Fund based on the number of funds and/or average daily net assets

Classes— Class specific expenses are borne by that class of shares. Income, realized and unrealized gains and losses and non-class specific expenses are allocated to the respective class on the basis of average daily net assets.

Dividends and Distributions to Shareholders— Dividends from net investment income, if any, are declared and paid to shareholders annually. Any net realized capital gains are distributed to shareholders at least annually.

3. Transactions with Affiliates:

Certain officers of the Trust are also employees of SEI Investments Global Funds Services (the “Administrator”), a wholly owned subsidiary of SEI Investments Company, and/or SEI Investments Distribution Co. (the “Distributor”). Such officers are paid no fees by the Trust for serving as officers of the Trust other than the Chief Compliance Officer (“CCO”) as described below.

A portion of the services provided by the CCO and his staff, whom are employees of the Administrator, are paid for by the Trust as incurred. The services include

regulatory oversight of the Trust’s Advisors and service providers as required by SEC regulations. The CCO’s services have been approved by and reviewed by the Board.

| 4. | Administration, Distribution, Transfer Agency and Custodian Agreements: |

The Fund, along with other series of the Trust advised by LSV Asset Management (the “Adviser”), and the Administrator are parties to an Administration Agreement, under which the Administrator provides administrative services to the Fund. For these services, the Administrator is paid an asset based fee, subject to certain minimums, which will vary depending on the number of share classes and the average daily net assets of the Fund. For the year October 31, 2024, the Fund incurred $828,889 for these services.

The Fund has adopted a distribution plan under the Rule 12b-1 under the 1940 Act for Investor Class Shares that allows the Fund to pay distribution and service fees for the sale and distribution of its shares, and for services provided to shareholders. The maximum annual distribution fee for Investor Class Shares of the Fund is 0.25% annually of the average daily net assets. For the year ended October 31, 2024, the Fund incurred $805,642 of distribution fees.

SS&C Global Investor & Distribution Solutions, Inc. serves as transfer agent and dividend disbursing agent for the Fund under the transfer agency agreement with the Trust. During the year ended October 31, 2024, the Fund earned $39,151 in cash management credits which were used to offset transfer agent expenses. This amount is labeled as “Fees Paid Indirectly” on the Statement of Operations.

U.S. Bank, N.A. acts as custodian (the “Custodian”) for the Fund. The Custodian plays no role in determining the investment policies of the Fund or which securities are to be purchased and sold by the Fund.

| 5. | Investment Advisory Agreement: |

The Trust and the Adviser are parties to an Investment Advisory Agreement, under which the Adviser receives an annual fee equal to 0.55% of the Fund’s average daily net assets.

| 6. | Investment Transactions: |

The cost of security purchases and the proceeds from security sales, other than short-term investments, for the year ended October 31, 2024, were as follows (000):

| Purchases | | | $ | 367,377 | |

| Sales | | | $ | 582,898 | |

Notes to Financial Statements

October 31, 2024

7. Federal Tax Information:

The amount and character of income and capital gain distributions to be paid, if any, are determined in accordance with Federal income tax regulations, which may differ from U.S. GAAP. As a result, net investment income (loss) and net realized gain (loss) on investment transactions for a reporting period may differ significantly from distributions during such period. These book/tax differences may be temporary or permanent. To the extent these differences are permanent in nature, they are charged or credited to distributable earnings or paid-in capital, as appropriate, in the period that the differences arise.

The permanent differences primarily consist of reclassification of long term capital gain distribution on REITs, reclass of Distributions and investments in publicly traded partnerships. There are no permanent differences that are credited or charged to Paid-in Capital and Distributable Earnings (Accumulated Losses) as of October 31, 2024.

The tax character of dividends and distributions paid during the year ended October 31, 2024 and 2023 was as follows (000):

| | | | Ordinary Income | | | Long-Term Capital Gain | | | Total | |

| 2024 | | | $ | 30,383 | | | $ | 65,944 | | | $ | 96,327 | |

| 2023 | | | | 41,356 | | | | 165,071 | | | | 206,427 | |

As of October 31, 2024, the components of distributable earnings (accumulated losses) on a tax basis were as follows (000):

| Undistributed Ordinary Income | | $ | 23,514 | |

| Undistributed Long-Term Capital Gain | | | 80,038 | |

| Other Temporary Differences | | | (6 | ) |

| Unrealized Appreciation | | | 263,997 | |

| Total Distributable Earnings | | $ | 367,543 | |

The fund has no capital loss carryforwards at October, 31, 2024.

During the year ended October 31, 2024, no capital loss carryforwards were utilized to offset capital gains.

The total cost of securities for Federal income tax purposes and the aggregate gross unrealized appreciation and depreciation on investments held by the Fund at October 31, 2024, were as follows (000):

Federal Tax Cost | | | Aggregated Gross Unrealized Appreciation | | | Aggregated Gross Unrealized Depreciation | | | Net Unrealized Appreciation | |

| $ | 1,118,012 | | | $ | 336,387 | | | $ | (72,390 | ) | | $ | 263,997 | |

For Federal income tax purposes, the difference between Federal tax cost and book cost primarily relates to wash sales.

| 8. | Concentration of Risks: |

Since the Fund purchases equity securities, the Fund is subject to the risk that stock prices will fall over short or extended periods of time. Historically, the equity markets have moved in cycles, and the value of the Fund’s equity securities may fluctuate drastically from day-to-day. Individual companies may report poor results or be negatively affected by industry and/or economic trends and developments. The prices of securities issued by such companies may suffer a decline in response. These factors contribute to price volatility, which is the principal risk of investing in the Fund.

Markets for securities in which the Fund invests may decline significantly in response to adverse issuer, political, regulatory, market, economic or other developments that may cause broad changes in market value, public perceptions concerning these developments, and adverse investor sentiment or publicity. Similarly, the impact of any epidemic, pandemic or natural disaster, or widespread fear that such events may occur, could negatively affect the global economy, as well as the economies of individual countries, the financial performance of individual companies and sectors, and the markets in general in significant and unforeseen ways. Any such impact could adversely affect the prices and liquidity of the securities and other instruments in which the Fund invests, which in turn could negatively impact the Fund’s performance and cause losses on your investment in the Fund.

The medium- and smaller-capitalization companies in which the Fund may invest may be more vulnerable to adverse business or economic events than larger, more established companies. In particular, investments in these medium- and small-sized companies may pose additional risks, including liquidity risk, because these companies tend to have limited product lines, markets and financial resources, and may depend upon a relatively small management group. Therefore, medium-and small-capitalization stocks may be more volatile than those of larger companies. These securities may be traded over-the-counter or listed on an exchange.

Since the Fund pursues a “value style” of investing, if the Adviser’s assessment of market conditions, or a company’s value or prospects for exceeding earnings expectations is wrong, the Fund could suffer losses or produce poor performance relative to other funds. In addition, “value stocks” can continue to be undervalued by the market for long periods of time.

Notes to Financial Statements

October 31, 2024

Because the Fund may, from time to time, be more heavily invested in particular sectors, the value of its shares may be especially sensitive to factors and economic risks that specifically affect those sectors. As a result, the Fund’s share price may fluctuate more widely

9. Concentration of Shareholders:

At October 31, 2024, 34% of total shares outstanding for the Institutional Class Shares were held by one record shareholder owning 10% or greater of the aggregate total shares outstanding. At October 31, 2024, 97% of total shares outstanding for the Investor Class Shares were held by one record shareholder owning 10% or greater of the aggregate total shares outstanding. These were comprised mostly of omnibus accounts which were held on behalf of various individual shareholders.

10. Indemnifications:

In the normal course of business, the Fund enters into contracts that provide general indemnifications. The Fund’s maximum exposure under these arrangements is dependent on future claims that may be made against the Fund and, therefore, cannot be estimated; however, based on experience, the risk of loss from such claims is considered remote.

11. New Accounting Pronouncement

In November 2023, the Financial Accounting Standards Board issued Accounting Standards Update No. 2023-07 (“ASU 2023-07”), Segment Reporting (“Topic 280”). ASU 2023-07 clarifies the guidance in Topic 280, which requires public entities to provide disclosures of significant segment expenses and other segment items. The guidance requires public entities to provide in interim periods all disclosures about a reportable segment’s profit or loss and assets that are currently required annually and also applies to public entities with a single reportable segment. Entities are permitted to disclose more than one measure of a segment’s profit or loss if such measures are used by the Chief Operating Decision Maker to allocate resources and assess performance, as long as at least one of those measures is determined in a way that is most consistent with the measurement principles used to measure the corresponding amounts in the consolidated financial statements. The amendments in ASU 2023-07 are effective for fiscal years beginning after December 15, 2023, and interim periods within fiscal years beginning after December 15, 2024. Early adoption is permitted. Management is currently evaluating the implications, if any, of the additional requirements and their impact on a Fund’s financial statements.

12. Subsequent Events:

The Fund has evaluated the need for additional disclosures and/or adjustments resulting from subsequent events through the date the financial statements were issued. Based on this evaluation, no additional disclosures or adjustments were required to the financial statements.

Report of Independent Registered Public Accounting Firm

To the Board of Trustees of The Advisors’ Inner Circle Fund and the Shareholders of LSV Value Equity Fund

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities of LSV Value Equity Fund (the “Fund”) (one of the funds constituting The Advisors’ Inner Circle Fund (the “Trust”)), including the schedule of investments, as of October 31, 2024, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, the financial highlights for each of the five years in the period then ended and the related notes (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund (one of the funds constituting The Advisors’ Inner Circle Fund) at October 31, 2024, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended and its financial highlights for each of the five years in the period then ended, in conformity with U.S. generally accepted accounting principles.

Basis for Opinion

These financial statements are the responsibility of the Trust’s management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) ("PCAOB") and are required to be independent with respect to the Trust in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Trust is not required to have, nor were we engaged to perform, an audit of the Trust’s internal control over financial reporting. As part of our audits, we are required to obtain an understanding of internal control over financial reporting but not for the purpose of expressing an opinion on the effectiveness of the Trust’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of October 31, 2024, by correspondence with the custodian and others. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

We have served as the auditor of one or more LSV Asset Management investment companies since 2005.

Philadelphia, Pennsylvania

December 23, 2024