| WSGR Wilson Sonsini Goodrich & Rosati PROFESSIONAL CORPORATION Date: May 26, 2010 To: Kathleen Krebs, Special Counsel Company: US Securities and Exchange Commission Fax: (202) 772-9205 Phone: (202) 551-3350 [ ] Use this fax number only [ ] Notify recipient before sending From: Robert Sanchez Phone: (202)973-8827 Return Fax: (202) 973-8899 Original: [ ] To follow via mail [ ] To follow via courier [ ] To follow via email [X] Original will not follow Fax Contains: 11 pages (including this sheet). If incomplete, call (202) 973-8827. Message: Re: infoGroup Inc. Revised Preliminary Proxy Statement on Schedule 14A, Filed May 18, 2010, File No, 001-34298 As discussed yesterday, attached are changed pages from infoGroup’s revised Preliminary Proxy Statement on Schedule 14A together with a draft letter in response to the Staffs May 24, 2010 comment letter. I look forward to speaking to you and/or Reid Hooper later this morning. If you have any questions, please contact me at (202) 973-8827. Thank you, Bob Sanchez 1700 K Street, N.W., Fifth Floor, Washington, D.C. 20006-3817 202.973.8800 Tel• 202.973.8899 Fax• www.wsgr.com This fax may contain confidential and privileged material for the sole use of the intended recipient. Any review or distribution by others is strictly prohibited. If you are not the intended recipient please contact the sender and destroy ail copies. Entire Transmission Copyright© 2003 Wilson Sonsini Goodrich & Rosati. All Rights Reserved. |

| WSGR Wilson Sonsini Goodrich & Rosati PROFESSIONAL CORPORATION Date: May 26,2010 To: Reid Hooper, Attorney-Advisor Company: US Securities and Exchange Commission Fax: (202) 772-9205 Phone: (202)551-3350 [ ] Use this fax number only [ ] Notify recipient before sending From: Robert Sanchez Phone: (202) 973-8827 Return Fax: (202) 973-8899 Original: [ ] To follow via mail [ ] To follow via courier [ ] To follow via email [X] Original will not follow Fax Contains: 11 pages (including this sheet). If incomplete, call (202) 973-8827. Message: Re: infoGroup Inc. Revised Preliminary Proxy Statement on Schedule 14A, Filed May 18, 2010, File No. 001•34298 As discussed with Kathleen Krebs yesterday, attached are changed pages from infoGroup’s revised Preliminary Proxy Statement on Schedule 14A together with a draft letter in response to the Staffs May 24, 2010 comment letter. I look forward to speaking to you and/or Kathleen later this morning. If you have any questions, please contact me at (202) 973-8827. Thank you, Bob Sanchez 1700 K Street, N.W., Fifth Floor, Washington, DC. 20006-3817 202.973.8800 Tel• 202.973.8899 Fax• www.wsgr.com This fax may contain confidential and privileged material for the sole use of the intended recipient. Any review or distribution by others is strictly prohibited. If you are not the intended recipient please contact the sender and destroy all copies. Entire Transmission Copyright© 2003 Wilson Sonsini Goodrich & Rosati. All Rights Reserved |

| infogroup Thomas J. McCusker Executive Vice President for Business Conduct and General Counsel 5711 S 86th Circle• Omaha, NE 68127-0347 Phone: (402) 593-4543 Fax: (402) 537-7833 tom.mccusker@infogroup.com May 26, 2010 U.S. Securities and Exchange Commission Division of Corporation Finance 3 00 F Street, N.E. Washington, DC 20549 Attn: Larry Spirgel Re: infoGroup, Inc. Revised Preliminary Proxy Statement on Schedule 14A Filed May 18, 2010 File No. 001-34928 Ladies and Gentlemen: We are writing in response to the comments contained in the Staffs letter, dated May 24, 2010, (the “Comment Letter”), with respect to the Revised Preliminary Proxy Statement on Schedule 14A of infoGroup Inc. (the “Company”), as filed with the SEC on May 18, 2010 (the “Proxy Statement”). We have filed with the SEC via EDGAR a revised Preliminary Proxy Statement on Schedule 14A. For your convenience, we have repeated your comments below in bold italic type before each of our responses. Background of the Merger, page 17 1. We note your response to comment six from our letter dated May J3, 2010. Please clarify your disclosure and provide additional context by discussing which principal business group or operating segment the company’s Small Business Group and interactive marketing solutions business unit are associated with. In addition, disclose the sales of each as a percentage of total net sales of the company. We note your disclosure that the company’s interactive marketing solutions business unit was expected to be the primary growth engine of the company’s digital data solutions. In response to the Staff’s comment, we have revised our disclosure on page 32 of the Proxy Statement to disclose that the Company’s Small Business Group is part of the Company’s Data Group, that the software solutions division of InfoGroup Interactive is part of the Company’s Services Group and the percentages of the Company’s revenue that each of these business units contributed in 2009. |

| U.S. Securities and Exchange Commission May 26, 2010 Page 2 Reasons for the Merger; Recommendation of the M&A Committee and Our Board of Directors, page 35 2. We note your response to comment nine from our letter dated May 13, 2010. Please disclose that the M&A Committee considered full first quarter results as well as the implication of those results on the 2010 full year results. Disclose the implications, including whether March 2010 results and the full first quarter results continued to reflect the trends noted regarding January and February 2010 financial performance. In response to the Staff’s comments, we have revised our disclosure on page 36 of the Proxy Statement to clarify that the Company did not adjust its internal budget as a result of the Company’s January and February 2010 financial performance. 3. We note your response to comment 10 from our letter dated May 13, 2010. Please revise your disclosure to specifically discuss why, based on updates from Evercore, the M&A Committee believed the financial and credit markets were becoming more supportive of merger and acquisition activity. In response to the Staff’s comments, we have revised our disclosure on page 29 of the Proxy Statement to disclose the material elements of Evercore’s updates that formed the basis for the M&A Committee’s belief that the financial and credit markets were becoming more supportive of merger and acquisition activity. Opinion of Evercore, page 39 4. We note your response to comment 11 from our letter dated May 13, 2010. Please confirm that you have disclosed the material projections provided to the third party bidders. Furthermore, please explain why the quarterly projections would not be material to shareholders when monthly projections appeared to be material to CCMP and resulted in CCMP lowering its proposed price per share. In response to the Staff’s comments, the Company hereby confirms that all material projections provided to third party bidders have been disclosed in the Proxy Statement. In this context, we supplementally advise the Staff that the basis upon which the Board of Directors analyzed and evaluated the CCMP offer was in comparison to implied values calculated by applying a number of customary valuation methodologies to the Company’s projected financial performance on an annual basis over a five-year period. Additionally, CCMP has advised us that their primary concern over the Company’s actual financial results for January and February 2010 was the potential impact of these results on the Company’s projected financial performance for the entire 2010 fiscal year. 5. With respect to Evercore’s selection of the two-year period ending March 5, 2010 for its historical trading analysis, please elaborate upon the “different industry environment within which the Company operated” in the past two years. |

| U.S. Securities and Exchange Commission May 26, 2010 Page 3 In response to the Staff’s comment, we have revised our disclosure on page 43 of the Proxy Statement to elaborate on the different industry environment within which the Company operated. 6. We note your response to our prior comment 12 in our letter dated May 13, 2010; yet, it is still unclear as to how Evercore selected specific multiples. For example, we note the range of selected multiples derived from the selected publicly-traded companies is below the mean and median for both the Marketing Services and Business Information companies listed in the table on page 44. In addition, we note the range of selected multiples derived from the selected precedent M&A transactions appears to be on the low end of the multiples disclosed in the table on page 46. Please revise your disclosure to explain in more specific detail why Evercore chose the particular range of selected multiples for the company. In response to the Staff’s comment, we have revised our disclosure on page 45 and page 47 of the Proxy Statement to provide more specific detail regarding the reasons that Evercore chose the particular range of selected multiples for the Company. * * * The Company hereby acknowledges the following:• we are responsible for the adequacy and accuracy of the disclosure in our filings;• Staff comments or changes to disclosure in response to Staff comments do not foreclose the Commission from taking any action with respect to the filing; and• the Company may not assert Staff comments as a defense in any proceeding initiated by the Commission or any person under the federal securities laws of the United States. |

| U.S. Securities and Exchange Commission May 26, 2010 Page 4 We appreciate the assistance the Staff has provided with its comments. Please direct your questions or comments regarding the Company’s response to the undersigned at (402) 593-4543. Thank you for your assistance. Sincerely, Thomas J. McCusker Executive Vice President for Business Conduct, General Counsel and Secretary cc: Bill L. Fairfield, infoGroup Inc. Tom Oberdorf, infoGroup Inc. Winston King, Esq., infoGroup Inc. Larry Sonsini, Wilson Sonsini Goodrich & Rosati, Professional Corporation Robert D. Sanchez, Wilson Sonsini Goodrich & Rosati, Professional Corporation |

| was merely an expression of interest in pursuing a PIPE transaction in the future rather than a firm proposal that could be evaluated and compared against the proposals from CCMP and Patty A. In its preliminary review of the terms of the proposal from Party A, the M&A Committee discussed that in addition to being inferior to the CCMP proposal on price, Party A’s proposal included a number of terms that greatly increased the risk that a transaction with Party A might not ultimately be completed. Party A’s proposal was conditioned, for example, on Party A’s completion of a substantial additional due diligence review of the Company and its business which Party A anticipated would require three additional weeks to complete and during which Party A proposed the Company would be bound to negotiate exclusively with Party A, Party A also proposed merger agreement terms that were much less favorable to the Company than CCMP’s proposed merger agreement terms, including significant conditions to Party A’s obligation to complete the transaction as well as lesser restrictions on Party A’s ability to refuse to close the transaction post signing. The M&A Committee also noted that the debt commitment from BofA submitted by Party A was much more preliminary in nature than the debt commitment from BofA submitted by CCMP and therefore would require considerably more work in order to determine whether such financing was in fact available. Between February 12, 2010 and February 16, 2010, representatives of both CCMP and Party A called representatives of Evercore to clarify their proposals and reiterate their strong interest in a transaction. No other party submitted proposals during this time. The 9 other parties that submitted preliminary proposals and performed additional due diligence on the Company but did not submit final proposals to acquire the Company (including the financial sponsor proposing the PIPE transaction) provided the following reasons, among others: (a) an inability to submit an offer at or above the market price at the time of such conversations (the closing share price of the Company on February 12, 2010, was $7.62), (b) a less favorable view relative to the Company management’s financial plan of the Company’s future growth prospects absent a material transformation of, and investment in, the business, with an associated high degree of execution risk, (c) a lack of comfort with the financial and strategic plans put forth by Company management given the perceived insufficient supporting detail for such plans and inadequate historical data regarding the business to benchmark and compare such future projections, (d) an increasingly competitive landscape with significantly reduced barriers to entry, (e) the disparate nature of the Company’s portfolio of products and services, (f) a perceived need for senior management changes, and (g) limited financing available for an acquisition of the Company. On February 16, 2010, the M&A Committee convened an in-person meeting at the San Mateo Marriott Hotel in San Mateo, California attended by representatives of WSGR and Evercore. As the first order of business, the Evercore team undertook an extensive presentation regarding various aspects and considerations related to the proposals received from CCMP, Party A and the financial sponsor proposing the PIPE transaction. Evercore’s presentation included an update on conditions in the equity, credit and mergers and acquisitions markets. Evercorenoted, among other things, that these markets had rebounded in the second half of 2009 and continued through year to date 2010, including improved equity market performance, a narrowing of interest rate spreads, an increase in high yield new issuance and an increase in leveraged buyout transaction volume. Evercore also noted, however, that there hud been a recent slowdown in the growth of the equity markets and increased volatility in the credit markets.Evercore also compared the proposals to the valuation analyses performed by Evercore in connection with the Company’s long term strategic plan. Following the Evercore presentation, WSGR presented to the M&A Committee a review of fiduciary duties, as well as a comparison of the legal terms of the CCMP and Party A proposals (including the terms and conditions of the merger agreements and collateral documents included with each of the proposals). The M&A Committee and its advisors discussed potential risks associated with the offers, including the need for completion by each of CCMP and Party A of substantial debt financing and the Company’s recourse under the proposed merger agreements if either CCMP or Party A were unable to obtain financing. On February 17, 2010, the Board of Directors convened an in-person meeting at the San Mateo Marriott Hotel in San Mateo, California attended by representatives of WSGR and Evercore. Representatives of Evercore gave a detailed presentation summarizing the transaction process to date, current mergers and acquisition and capital market conditions, and the terms and conditions of the proposals received from CCMP, Party A and the financial sponsor proposing the PIPE transaction. Evercore also compared the proposals to the valuation analyses performed by Evercore in connection with the Company’s long term strategic plan. Following the Evercore presentation, 29 |

| termination fee to Parent upon termination of the merger agreement. Representatives of WSGR also reported that the final terms of Mr. Gupta’s voting agreement had not yet been agreed upon and that these provisions continued to be negotiated. Next, it was noted that one of the conditions to funding of BofA’s debt commitment letter would be that the Company satisfy a stipulated minimum debt to EBITDA ratio. Mr. Oberdorf reviewed for the M&A Committee the requirements of this condition and the current expectations regarding the Company’s ability to satisfy this condition. On March 2, 2010, the Board of Directors convened a meeting attended by representatives of WSGR and Evercore. Representatives of Evercore updated the Board of Directors on the current status of negotiations with CCMP including the status of the proposed debt financing with BofA. Representatives of WSGR reviewed for the Board of Directors the terms and conditions of the proposed definitive agreements including the merger agreement, the equity and debt commitment letters, the guarantee and the voting agreements, highlighting the remaining unresolved legal and business issues. On March 3. 2010, management of the Company provided to representatives of CCMP preliminary revenue results for the month of February, which fell short of the revenue budget for February 2010 by approximately 2% and was 3% lower than prior year results. On March 4, 2010, representatives of CCMP held a conference call with members of Company’s management and representatives of Evercore to discuss February 2010 preliminary revenue results to evaluate the shortfalls in year-to-date financial results relative to budget and the implications for the financial forecast for the remainder of fiscal year 2010 as well as to discuss the significant underperformance of the Company’s Small Business Group, which is part of the Data Group, and what is now known as Infogroup Interactive, a subsidiary within the Company’s Services Group. In particular, with, respect to the software solutions division of Infogroup Interactive, which was expected to be the primary growth engine of the Company’s digitaldata solutions strategy, revenue growth slowed from 20% in 2008 to 4% in 2009. Management noted that this division’s year-to-date revenue results were 12% below budget for the first two months of 2010 and2-% below the same period in 2009. The Company’s Small Business Group had 2009 revenue representing 21% of the Company’s total 2009 revenue. The software solutions division of lnfogroup Interactive had 2009 revenue representing 10% of the Company’s total 2009 revenue. On March 4, 2010, representatives of WSGR had telephone conversations with representatives of O’Melveny & Myers in an effort to resolve the remaining unresolved issues on the merger agreement and the other transaction documents. Later that afternoon, representatives of CCMP called Evercore to inform them that they were lowering their proposed price to $7.60 per share. CCMP informed Evercore that the change in price was based on (i) year-to-date financial performance of the Company through February 2010 that was materially below budget, including the significant underperformance of the software solutions division of Infogroup Interactive with year-to-date revenue that was 12% below budget and 2% below the same period in 2009, (ii) limited evidence to support the Company’s ability to achieve the 2010 budget, (iii) feedback from BofA that indicated revised terms of the debt commitment would be less favorable to CCMP than provided for at the time of the original offer submitted on February 12, 2010, and (iv) additional liabilities of the Company discovered by CCMP during the course of its due diligence review. As context, the financing proposal provided for the original offer submitted on February 12, 2010 included $350 million of funded debt in the form of a secured term loan, whereas the verbal indication of a revised per share price of $7.60, pending BofA receiving final internal approval, provided on March 4, 2010 included a reduced debt commitment from BofA that included $315 million of funded debt in the form of a secured term loan. In addition, the terms of the debt commitment associated with the revised offer were also less favorable than those associated with the original offer. As a result of the above factors, CCMP stated that it could no longer support the previously proposed offer price of $8.60 per share and was, therefore, lowering its proposed price. That evening, the M&A Committee had a telephonic meeting attended by representatives of WSGR and Evercore. Representatives of Evercore informed the M&A Committee of the proposed price reduction. Representatives of Evercore also reported that BofA’s internal credit committee was scheduled to review and approve the BofA debt commitment letter to CCMP the following day. Representatives of Evercore and the M&A Committee discussed CCMP’s stated reasons for the proposed price reduction. The M&A Committee discussed the possibility and capability of Party A to improve upon its initial $8.00 per share proposal. Representatives of Evercore reported that in a telephone conversation with representatives of Party A earlier in the day, the representatives of Party A had indicated that Party A would still require an additional 2 to 3 weeks of diligence prior to being in a position to enter into an agreement for a transaction. Party A further indicated that they maintained their proposal at $8,00 and that should negotiations with 32 |

| • the fact that many of the Company’s newer and emerging competitors have a significant head start with providers and consumers of digital data and that the Company might not be able to compete as effectively in this market;• the need to consolidate the product development function from its historical decentralization among the Company’s smaller independent operating units to a more unified approach and the risk that the Company might not be able to effect such a consolidation efficiently or effectively;• the need to make changes to the management team at multiple levels to maximize the possibility of executing effectively on a stand-alone business strategy and the risk that the Company might not be successful in recruiting such qualified employees due to geographic limitations and the continuing risk Mr. Gupta would present as an activist shareholder with limited restrictions in the manner in which he could sell his shares;• the risk of continuous downward pressure on the Company’s stock price resulting from Mr. Gupta’s significant shareholdings, including his continued ability to sell into the market;• the risk that additional costs savings may be increasingly difficult to achieve and that without revenue growth, such reductions are the only avenue available for continued earnings growth;• the fact that management’s long-term strategic plan did not: include the level of investment the M&A Committee believed would be required to be made in connection with, nor the potential future impact of, new business strategies and initiatives not currently in development; or make adequate provisions for creating common technology platforms to be shared by the Company’s many separate business units to streamline data delivery to customers;• the slowing growth rates of the Company’s software solutions division of Infogroup Interactive business, which management expected to be the primary growth engine of the Company’s digital data solutions strategy, the underperformance of the Company’s software solutions division of Infogroup Interactive business revenue year-to-date relative to budget and prior year results, and the negative impact such performance could have on the Company’s organic growth prospects; and• the fact that product development within the Company was too decentralized, that efforts to enhance systems and customer solutions were being duplicated throughout the Company and the high level of risk and expense the M&A Committee believed would be required to address these inefficiencies;• the M&A Committee engaged in a full, thorough, complete process over a substantial period of time, engaging more than 50 potential counterparties to a transaction, inviting all remaining active participants to a second round, ultimately requesting final bids from all parties still involved in the process, and facilitating a go-shop process subsequent to the transaction announcement;• the transaction process was authorized by the Board of Directors to commence only after (i) a thorough review of the Company’s strategic alternatives was conducted over a 9-month period (ii) a significant increase in the Company’s share price was realized during this period due in some part to the unauthorized public disclosure of certain details of the Company’s sale process, and (iii) signs of stabilization and pending recovery in the business were evident in recent historical financial performance metrics including the favorable effects of Adjusted EBITDA due to cost reductions and the decrease in the rate of revenue declines;• the Company’s January and February 2010 financial performance, which fell short of the Company’s budgeted revenue by approximately $1.9 million, or 2%, and approximately $2,2 million, or 13%, in Adjusted EBITDA and, although the Company did not adjust its internal budget, the potential impl ications such shortfall may have on 2010 full-year results given that the Company’s budget was heavily back-end loaded such that an early year shortfall would extrapolate to a much larger shortfall in the full-year budget, including the fact that, since the formation of the M&A Committee in January 2009, the Company had missed its budgeted financial results during each reported fiscal period; 36 |

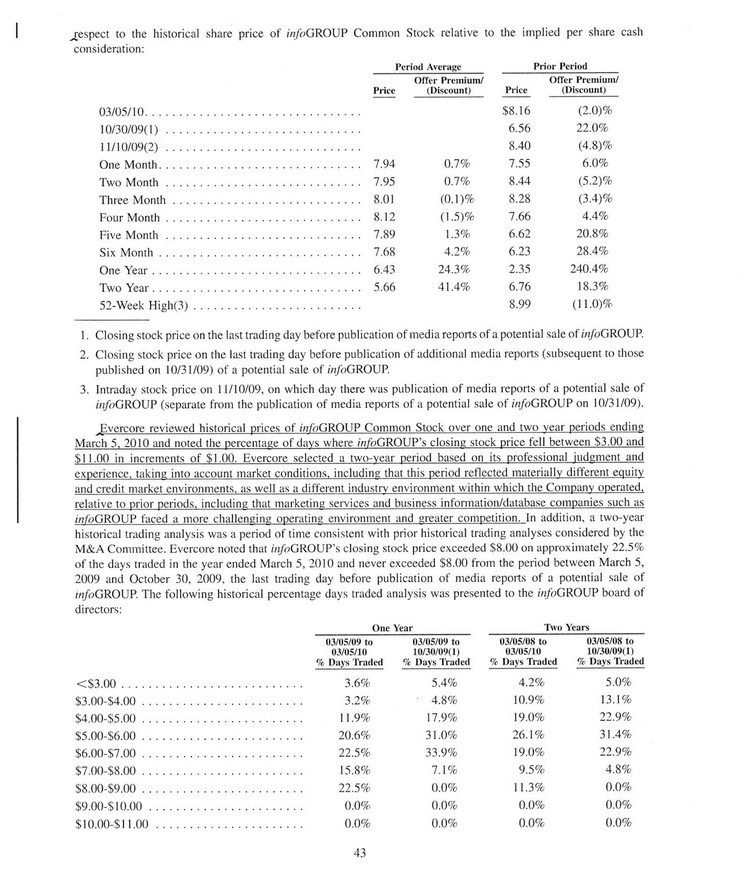

| respect to the historical share price of infoGROUP Common Stock relative to the implied per share cash consideration; Period Average Prior Period Offer Premium/ Offer Premium/ Price (Discount) Price (Discount) 03/05/10 ..... $8.16 (2.0)% 10/30/09(1) ...... 6.56 22.0% 11/10/09(2) ...... 8.40 (4.8)% One Month ........ 7.94 0.7% 7.55 6.0% Two Month ........ 7.95 0.7% 8.44 (5.2)% Three Month ...... 8.01 (0.1)% 8.28 (3.4)% Four Month ....... 8.12 (1.5)% 7.66 4.4% Five Month ....... 7.89 1.3% 6.62 20.8% Six Month ........ 7.68 4.2% 6.23 28.4% One Year ......... 6.43 24.3% 2.35 240.4% Two Year ......... 5.66 41.4% 6.76 18.3% 52-Week High(3) .. 8.99 (11.0)% 1. Closing stock price on the last trading day before publication of media reports of a potential sale of infoGROUP. 2. Closing stock price on the last trading day before publication of additional media reports (subsequent to those published on 10/31/09) of a potential sale of infoGROUP. 3. Intraday stock price on 11/10/09, on which day there was publication of media reports of a potential sale of infoGROUP (separate from the publication of media reports of a potential sale of infoGROUP on 10/31/09). Evercore reviewed historical prices of infoGROUP Common Stock over one and two year periods ending March 5. 2010 and noted the percentage of days where infoGROUP’s closing stock price fell between S3.00 and $11.00 in increments of $1.00, Evercore selected a two-year period based on its professional judgment and experience, taking into account market conditions, including that this period reflected materially different equity and credit market environments, as well as a different industry environment within which the Company operated.relative to prior periods, including that marketing services and business information/database companies such as infoGROUP faced a more challenging operating environment and greater competition. In addition, a two-year historical trading analysis was a period of time consistent with prior historical trading analyses considered by the M&A Committee. Evercore noted that infoGROUP’s closing stock price exceeded $8.00 on approximately 22.5% of the days traded in the year ended March 5, 2010 and never exceeded $8.00 from the period between March 5, 2009 and October 30, 2009, the last trading day before publication of media reports of a potential sale of infoGROUP. The following historical percentage days traded analysis was presented to the infoGROUP board of directors: One Year Two Years —— — 03/05/09 to 03/05/09 to 03/05/08 to 03/05/08 to 03/05/10 10/30/09(1) 03/05/10 10/30/09(l) % Days Traded % Days Traded % Days Traded % Days Traded <$3.00 .... 3.6% 5.4% 4.2% 5.0% $3.00-$4.00 ...... 3.2% 4.8% 10.9% 13.1% $4.00-$5.00 .. 11.9% 17.9% 19.0% 22.9% $5,00-$6.00 .. 20.6% 31.0% 26.1% 31.4% $6.00-$7.00 ...... 22.5% 33.9% 19.0% 22.9% $7.00-S8.00 ...... 15,8% 7.1% 9.5% 4.8% $8.00-$9.00 ...... 22,5% 0.0% 11.3% 0.0% $9.00-$10.00 ..... 0.0% 0.0% 0.0% 0.0% $10.00-$11.00 .... 0,0% 0.0% 0.0% 0.0% 43 |

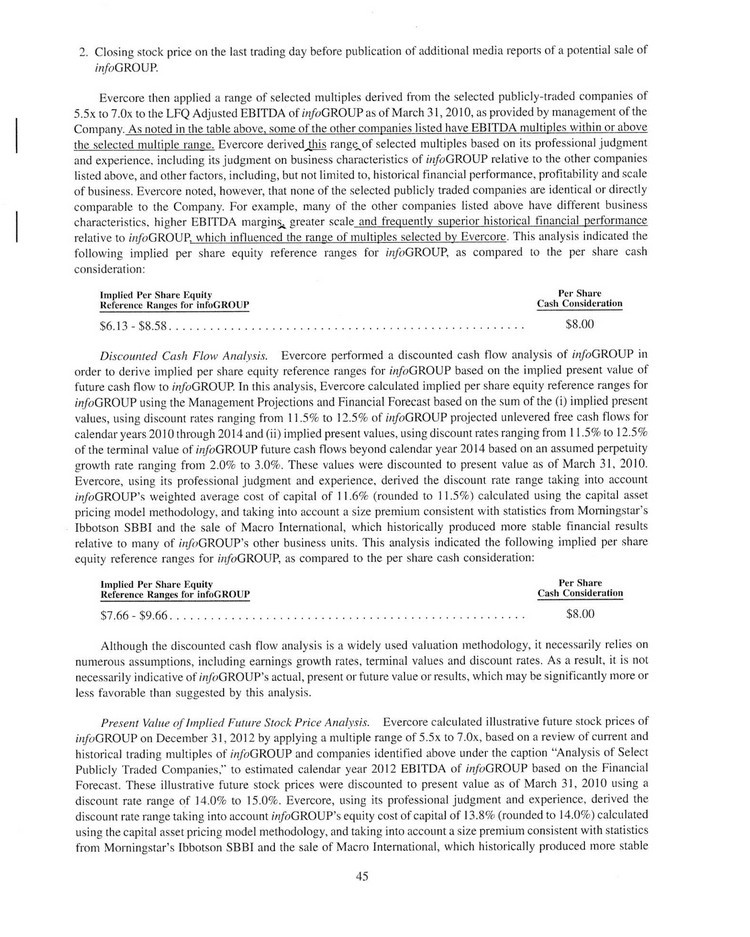

| 2. Closing stock price on the last trading day before publication of additional media reports of a potential sale of infoGROUP. Evercore then applied a range of selected multiples derived from the selected publicly-traded companies of 5.5x to 7.0x to the LFQ Adjusted EBITDA of infoGROUP as of March 31, 2010, as provided by management of the Company, As noted in the table above, some of the other companies listed have EBITDA multiples within or above the selected multiple range. Evercore derived this range of selected multiples based on its professional judgment and experience, including its judgment on business characteristics of infoGROUP relative to the other companies listed above, and other factors, including, but not limited to, historical financial performance, profitability and scale of business. Evercore noted, however, that none of the selected publicly traded companies are identical or directly comparable to the Company. For example, many of the other companies listed above have different business characteristics, higher EBITDA margin greater scale and frequently superior historical financial performancerelative to infoGROUP. which influenced the range of multiples selected by Evercore. This analysis indicated the following implied per share equity reference ranges for infoGROUP, as compared to the per share cash consideration: Implied Per Share Equity Per Share Reference Ranges for infoGROUP Cash Consideration —— — $6.13 — $8.58 ............ $8.00 Discounted Cash Flow Analysis. Evercore performed a discounted cash flow analysis of infoGROUP in order to derive implied per share equity reference ranges for infoGROUP based on the implied present value of future cash flow to infoGROUP. In this analysis, Evercore calculated implied per share equity reference ranges for infoGROUP using the Management Projections and Financial Forecast based on the sum of the (i) implied present values, using discount rates ranging from 11.5% to 12.5% of infoGROUP projected unlevered free cash flows for calendar years 2010 through 2014 and (ii) implied present values, using discount rates ranging from 11.5% to 12.5% of the terminal value of infoGROUP future cash flows beyond calendar year 2014 based on an assumed perpetuity growth rate ranging from 2.0% to 3.0%. These values were discounted to present value as of March 31, 2010. Evercore, using its professional judgment and experience, derived the discount rate range taking into account infoGROUP’s weighted average cost of capital of 11.6% (rounded to 11.5%) calculated using the capital asset pricing model methodology, and taking into account a size premium consistent with statistics from Morningstar’s Ibbotson SBBI and the sale of Macro International, which historically produced more stable financial results relative to many of infoGROUP’s other business units. This analysis indicated the following implied per share equity reference ranges for infoGROUP, as compared to the per share cash consideration: Implied Per Share Equity Per Share Reference Ranges tor infoGROUP Cash Consideration —— — $7.66 — $9.66 ............ $8.00 Although the discounted cash flow analysis is a widely used valuation methodology, it necessarily relies on numerous assumptions, including earnings growth rates, terminal values and discount rates. As a result, it is not necessarily indicative of infoGROUP’s actual, present or future value or results, which may be significantly more or less favorable than suggested by this analysis. Present Value of Implied Future Stock Price Analysis. Evercore calculated illustrative future stock prices of infoGROUP on December 31, 2012 by applying a multiple range of 5.5x to 7.0x, based on a review of current and historical trading multiple s of infoGROUP and companies identified above under the caption “Analysis of Select Publicly Traded Companies.” to estimated calendar year 2012 EBITDA of infoGROUP based on the Financial Forecast. These illustrative future stock prices were discounted to present value as of March 31, 2010 using a discount rate range of 14.0% to 15.0%. Evercore, using its professional judgment and experience, derived the discount rate range taking into account infoGROUP’s equity cost of capital of 13.8% (rounded to 14.0%) calculated using the capital asset pricing model methodology, and taking into account a size premium consistent with statistics from Morningstar’s Ibbotson SBBI and the sale of Macro International, which historically produced more stable 45 |

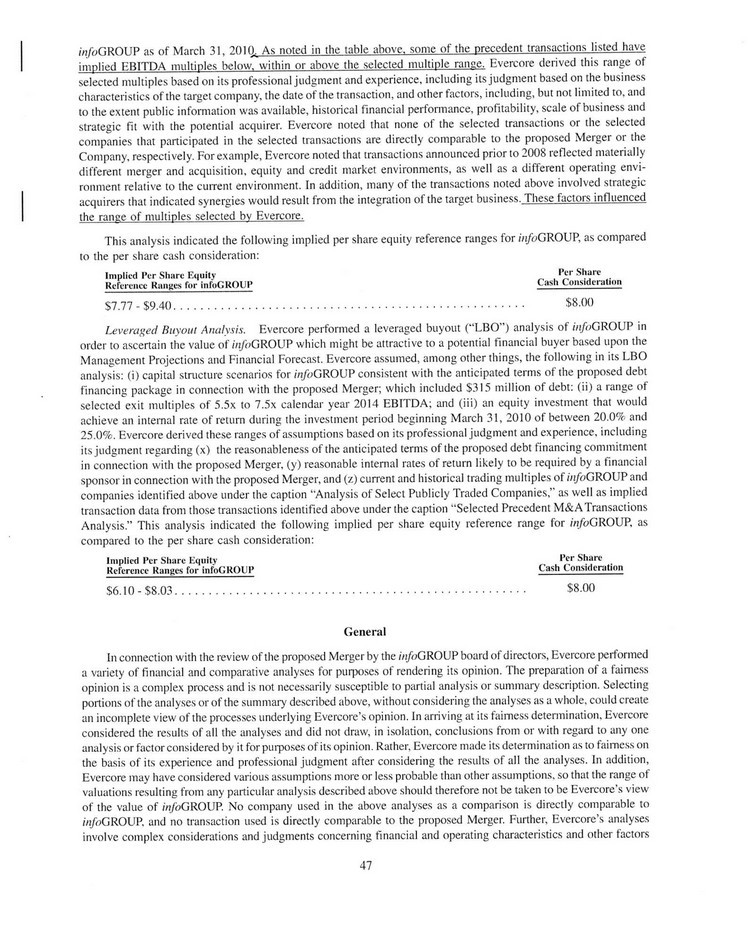

| infoGROUP as of March 31, 2010. As noted in the table above, some of the precedent transactions listed have implied EBITDA multiples below, within or above the selected multiple range. Evercore derived this range of selected multiples based on its professional judgment and experience, including its judgment based on the business characteristics of the target company, the date of the transaction, and other factors, including, but not limited to, and to the extent public information was available, historical financial performance, profitability, scale of business and strategic fit with the potential acquirer. Evercore nosed that none of the selected transactions or the selected companies that participated in the selected transactions are directly comparable to the proposed Merger or the Company, respectively. For example, Evercore noted that transactions announced prior to 2008 reflected materially different merger and acquisition, equity and credit market environments, as well as a different operating environment relative to the current environment. In addition, many of the transactions noted above involved strategic acquirers that indicated synergies would result from the integration of the target business. These factors influenced the range of multiples selected by Evercore. This analysis indicated the following implied per share equity reference ranges for infoGROUP, as compared to the per share cash consideration: Implied Per Share Equity Per Share Reference Ranges for infoGROUP Cash Consideration —— — $7.77 — $9.40 ............ $8.00 Leveraged Buyout Analysis. Evercore performed a leveraged buyout (“LBO”) analysis of infoGROUP in order to ascertain the value of infoGROUP which might be attractive to a potential financial buyer based upon the Management Projections and Financial Forecast. Evercore assumed, among other things, the following in its LBO analysis: (i) capital structure scenarios for infoGROUP consistent with the anticipated terms of the proposed debt financing package in connection with the proposed Merger; which included $315 million of debt: (ii) a range of selected exit multiples of 5.5s to 7.5x calendar year 2014 EBITDA; and (iii) an equity investment that would achieve an internal rate of return during the investment period beginning March 31, 2010 of between 20.0% and 25.0%. Evercore derived these ranges of assumptions based on its professional judgment and experience, including its judgment regarding (x) the reasonableness of the anticipated terms of the proposed debt financing commitment in connection with the proposed Merger, (y) reasonable internal rates of return likely to be required by a financial sponsor in connection with the proposed Merger, and (z) current and historical trading multiples of infoGROUP and companies identified above under the caption ‘“Analysis of Select Publicly Traded Companies,” as well as implied transaction data from those transactions identified above under the caption “Selected Precedent M&A Transactions Analysis.” This analysis indicated the following implied per share equity reference range for infoGROUP, as compared to the per share cash consideration: Implied Per Share Equity Per Share Reference Ranges ft>r infoGROUP Cash Consideration —— — $6.10 — $8.03 ................ $8.00 General In connection with the review of the proposed Merger by the infoGROUP board of directors, Evercore performed a variety of financial and comparative analyses for purposes of rendering its opinion. The preparation of a fairness opinion is a complex process and is not necessarily susceptible to partial analysis or summary description. Selecting portions of the analyses or of the summary described above, wi thout considering the analyses as a whole, could create an incomplete view of the processes underlying Evercore’s opinion. In arriving at its fairness determination, Evercore considered the results of all the analyses and did not draw, in isolation, conclusions from or with regard to any one analysis or factor considered by it for purposes of its opinion. Rather, Evercore made its determination as to fairness on the basis of its experience and professional judgment after considering the results of all the analyses. In addition, Evercore may have considered various assumptions more or less probable than other assumptions, so that the range of valuations resulting from any particular analysis described above should therefore not be taken to be Evercore’s view of the value of infoGROUP. No company used in the above analyses as a comparison is directly comparable to infoGROUP, and no transaction used is directly comparable to the proposed Merger. Further, Evercore’s analyses involve complex considerations and judgments concerning financial and operating characteristics and other factors 47 |