United States

Securities and Exchange Commission

Washington, D.C. 20549

Form N-CSR

Certified Shareholder Report of Registered Management Investment Companies

811-6447

(Investment Company Act File Number)

Federated Hermes Fixed Income Securities, Inc.

_______________________________________________________________

(Exact Name of Registrant as Specified in Charter)

Federated Hermes Funds

4000 Ericsson Drive

Warrendale, Pennsylvania 15086-7561

(Address of Principal Executive Offices)

(412) 288-1900

(Registrant's Telephone Number)

Peter J. Germain, Esquire

1001 Liberty Avenue

Pittsburgh, Pennsylvania 15222-3779

(Name and Address of Agent for Service)

(Notices should be sent to the Agent for Service)

Date of Fiscal Year End: 09/30/20

Date of Reporting Period: 09/30/20

| Item 1. | Reports to Stockholders |

Annual Shareholder Report

September 30, 2020

Federated Hermes Municipal Ultrashort Fund(formerly, Federated Municipal Ultrashort Fund)

Fund Established 2000

A Portfolio of Federated Hermes Fixed Income Securities, Inc.(formerly, Federated Fixed Income Securities, Inc.)

IMPORTANT NOTICE REGARDING REPORT DELIVERY

Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Fund’s shareholder reports like this one will no longer be sent by mail, unless you specifically request paper copies of the reports from the Fund or from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Fund or your financial intermediary electronically by contacting your financial intermediary (such as a broker-dealer or bank); other shareholders may call the Fund at 1-800-341-7400, Option 4.

You may elect to receive all future reports in paper free of charge. You can inform the Fund or your financial intermediary that you wish to continue receiving paper copies of your shareholder reports by contacting your financial intermediary (such as a broker-dealer or bank); other shareholders may call the Fund at 1-800-341-7400, Option 4. Your election to receive reports in paper will apply to all funds held with the Fund complex or your financial intermediary.

Not FDIC Insured ▪ May Lose Value ▪ No Bank Guarantee

J. Christopher

Donahue

President

Federated Hermes Municipal Ultrashort Fund

Letter from the President

Dear Valued Shareholder,

I am pleased to present the Annual Shareholder Report for your fund covering the period from October 1, 2019 through September 30, 2020.

As we all confront the unprecedented effects of the coronavirus and the challenges it presents to our families, communities, businesses and the financial markets, I want you to know that everyone at Federated Hermes is dedicated to helping you successfully navigate the markets ahead. You can count on us for the insights, investment management knowledge and client service that you have come to expect. Please refer to our website, FederatedInvestors.com, for timely updates on this and other economic and market matters.

Thank you for investing with us. I hope you find this information useful and look forward to keeping you informed.

Sincerely,

J. Christopher Donahue, President

Management’s Discussion of Fund Performance (unaudited)

The total return of Federated Hermes Municipal Ultrashort Fund (the “Fund”), based on net asset value for the 12-month reporting period ended September 30, 2020, was 1.14% for the Class A Shares, 1.35% for the Institutional Shares and 1.37% for the Class R6 Shares. The 1.37% total return for the Class R6 Shares for the reporting period consisted of 1.17% of tax-exempt dividend income and price appreciation of 0.20% in the net asset value of the shares.1,2 The total return of the Bloomberg Barclays 1-Year U.S. Municipal Bond Index (BB1MBI),3 the Fund’s broad-based securities market index, was 2.24% and the total return of the Lipper Short Municipal Debt Funds Average (LSMDFA),4 a peer group average of short-term bond funds with durations of less than three years, was 1.84% during the same period. The total return of a 50/50 blend (Blended Index)5 of the BB1MBI and the Lipper Tax-Exempt Money Market Funds Average, which would approximate a 0.75 year average duration, was 1.39% during the same period. The Fund’s and the LSMDFA’s total returns for the most recently completed fiscal year reflected actual cash flows, transaction costs and other expenses that were not reflected in the total return of the BB1MBI.

During the reporting period, the Fund’s investment strategy focused on: (a) the effective duration6 of its portfolio (which indicates the portfolio’s price sensitivity to interest rates); (b) the selection of securities with different maturities (expressed by a yield curve showing the relative yield of securities with different maturities); (c) the allocation of the portfolio among securities of similar issuers (referred to as “sectors”); and (d) the credit quality7 and ratings of the portfolio securities (which indicate the risk that securities may default). These were the most significant factors affecting the Fund’s performance relative to the BB1MBI during the reporting period.

The following discussion will focus on the performance of the Fund’s Class R6 Shares relative to the BB1MBI.

MARKET OVERVIEW

During the reporting period, the 10-year U.S. Treasury yield decreased from a high of 1.94% in November 2019 to a low of 0.51% in August 2020 and averaged 1.12%. The 10-year yield ended the period at 0.69%.

During most of the period, economic activity in the U.S. expanded at a moderate pace. The slope of the U.S. Treasury curve was unusually flat by historical standards, which in the past has often been associated with a deterioration in future macroeconomic performance. Inflation was showing signs of picking up during the reporting period; however, it continued to run below the 2% target inflation rate of the Federal Reserve (the “Fed”). Inflation readings had been held down in 2019 due to factors such as the decline in oil prices, softer inflation abroad and appreciation in the dollar despite strengthening labor market conditions and rising input costs for industry.

Annual Shareholder Report

The Fed’s decision to cut the federal funds target rate (FFTR) three times by ¼ of a percent each time during 2019 was mostly anticipated by the markets. In determining the size and timing of changes in the FFTR, changes in the Federal Open Market Committee’s (FOMC) indicators of maximum employment and a 2% inflation target were essential. The Fed reaffirmed that adjustments to the policy path would depend on assessments of how the economic outlook and risks to the outlook were evolving. Then, on March 3, 2020, with an unscheduled rate decision, the Fed reduced the FFTR by 1∕2 of a percent to a range of 1.0% to 1.25% and then again on March 16, 2020 by a full 1% to the lower bound of 0% to 0.25% in reaction to global developments concerning the Coronavirus (Covid-19) pandemic and its potential impacts on the economic outlook. The FOMC’s recent meeting minutes stated that the Coronavirus outbreak has harmed communities and disrupted economic activity in many countries, including in the U.S. Global financial conditions have also been significantly affected. The Fed has remained at the 0% lower FFTR boundary through September 2020.

The Fed made a substantial announcement in August when Chair Jerome Powell unveiled a significant change in monetary policy: a modification of its “Statement on Longer-Run Goals and Monetary Policy Strategy.” This document explains the Fed’s framework for its policy actions and is not updated often—the last major shift happened in 2012. The new framework puts an increased emphasis on fostering employment, one of the Fed’s two Congressional mandates. The other is to corral inflation, which the Fed has defined as 2%. Policymakers now say they will tolerate a temporary rise above that level if it is caused by a strong labor market. Expressed in their rate policy, they will refrain from raising the FFTR from the current target range of 0% to 0.25% until economic conditions are not just good, but robust.

Available economic data showed that the U.S. economy came into this challenging period on a strong footing. Given the sizeable downward revision for 2020 Gross Domestic Product (GDP) growth, Fund management is more cautious overall now on municipal credit for the intermediate-term. That is based on an expectation that these issuers–many already facing liquidity constraints and other financial issues–may face increased pressure over the coming months. Fund management believes that high-grade municipals7 should fare better, but will still likely be affected by such a sizeable GDP reduction, as it will factor into funding sources for most issuers in the municipal market.

Annual Shareholder Report

Fund management believes that state and local governments will experience sizeable tax collection declines–especially from sales and income taxes–and at the same time will see increased spending, particularly on public health. Some analysts expect state tax collections to decline on the order of 16%. We believe that revenues beyond taxes will decline in nearly all sectors for nearly all issuers. Of all the outstanding municipal securities, approximately 30% are general obligation (GO) bonds and 70% are revenue bonds. We believe that total funding shortfalls could be far higher than for general obligation issuers alone as many revenue sectors have experienced increased pandemic costs and revenue declines due to economic closure.

State and local governments, hospitals, airports and mass transit agencies were among the entities that received some $400 billion of funding under the CARES Act signed into law by President Trump. We believe that still more funding may be needed–somewhere on the order of $150 billion to $300 billion for municipal market issuers to help weather the effects of economic shutdown and closure of operations. The $150 billion that state and local governments are specifically set to receive from the CARES Act’s Coronavirus Relief Fund is meant to be largely used for Coronavirus expense reimbursement rather than for budget gap purposes.

Some municipal issuers have also benefited from the $454 billion economic stabilization fund–anticipated to be leveraged by the Fed–established under the CARES Act. Under these provisions, the Fed is allowed, though not required, to purchase municipal debt directly from issuers, in the secondary market, or to make direct loans or loan guarantees. The Fed is not authorized to provide free, direct funding to municipal issuers. We believe, absent further direct aid for the municipal debt market, that state and local government budgets would be further stressed at the most inopportune time, particularly as revenues decline as a result of business closures and rising unemployment.

During the reporting period, credit was generally stable and the municipal bond market’s technical (net supply and demand) position was mostly favorable. The issuance of municipal debt in 2019 had been relatively comparable to previous periods, even though the ability to advance refund existing debt became disallowed. Flows from investors into short, intermediate, long and high-yield municipal bond funds were positive for a significant portion of the period but turned sharply negative in March and April once the Coronavirus and its impact on the world economy became apparent. Flows have since rebounded from May through September as investor confidence returned due to the various governmental responses.

Annual Shareholder Report

As a result of the Coronavirus pandemic, municipal credit quality is expected to be negatively impacted within every sector of the municipal bond market by the federal and state governments’ decisions to bring the U.S. economy to a virtual halt. State and local governments’ income and sales tax revenues will likely be reduced as a result of the layoffs and business closures throughout the country. Municipal transportation, health care, higher education and dedicated tax debt may be impaired to varying degrees by the virus’ impacts. We believe that a large number of credit downgrades can be expected within the municipal market. However, credit defaults are not anticipated to occur to any significant degree as social distancing recommendations and business closures are expected to be curtailed as the Coronavirus subsides.

Over the reporting period, the municipal yield curve declined significantly and steepened as yields for short maturity securities (1 to 5 years) fell more than those on intermediate and longer maturities (5 to 30 years). Short-term high grade (“AAA”-rated) municipal yields (1-to-5-year maturities) decreased meaningfully over the first six months of the reporting period amid multiple Fed eases in 2019, reaching a low of 0.50% in early March 2020 before the Covid-19 shutdown began. In March, high grade short-term municipal yields spiked from 0.50% to 2.80% in 10 trading days amid liquidity constraints, heavy shareholder redemptions, and the uncertainty of the impact of the shutdown on the economy and many municipal credit sectors. As the market began to stabilize in early April, yields then began to fall rapidly in April and May and stabilized to end the period at lows of 0.15% to 0.30%.

DURATION

The Fund is an ultrashort tax-exempt municipal bond fund and pursues a low price volatility strategy. As such, the Fund’s typical dollar-weighted average duration is constrained by its prospectus to one year or less with the typical operating range from four months to one year. As determined at the end of the reporting period, the Fund’s dollar-weighted duration was 0.87 years. The duration of the BB1MBI (which contains only bonds with maturities from one to two years) was 1.38 years at the end of the reporting period.

The seven-day SIFMA rate, a proxy for weekly municipal variable-rate demand note (MVRDN) yields held in the Fund and the base coupon index for many municipal floating-rate notes (MFRNs) held in the Fund, averaged 0.83% over the reporting period but ranged from 0.08% to 5.20%. The 1-month ICE LIBOR Index, a base index for some of the MFRNs in the Fund, averaged 0.94% over the reporting period but moved from 2.01% at the start to 0.15% at the end.

Annual Shareholder Report

Amid all of the volatility in the market in March and into April, Fund management focused primarily on maintaining liquidity during that brief period. However, with short-term interest rates sharply declining over the reporting period and considering the Fed’s actions, we opportunistically lengthened the Fund’s duration from 0.74 years at the end of March to 0.87 years at the end of the period in order to seek to capture more total return performance and lock in higher fixed-rate yields before they declined following the Fed rate cuts and subsequent credit spread tightening. This decision helped the total return performance of the Fund versus the BB1MBI, but with the structural duration differential of the index versus the Fund and the significant decline in rates, the Fund lagged in price performance versus the BB1MBI.

As part of the duration positioning of the Fund and with strong cash inflows into the Fund from May through September, the floating-rate/variable-rate percentage of the Fund was maintained at 30% to 50% over the period. However, the Fund’s holdings of MVRDNs and MFRNs produced above average income over the period. For example, MFRNs, which comprised about 25% to 30% of the Fund, had an average coupon rate of 0.74% at the end of the reporting period. This coupon income was significantly higher than comparable maturity fixed-rate yields in the market over the period.

Maturity/Yield Curve

During the reporting period, the municipal yield curve steepened as yields on shorter maturities (one to five years) fell more than intermediate and longer maturity bonds (five years and longer).

Because the Fund pursues an ultrashort duration strategy to seek to provide income exempt from federal regular income tax, the Fund was managed during the reporting period with an intention of maintaining a barbell structure consisting of: 35% to 55% weighting in very short-term maturity securities such as tax-exempt weekly reset MVRDNs and weekly and monthly reset MFRNs combined with 45% to 65% weighting in tender option bonds, tax-exempt fixed-rate municipal notes and fixed-rate municipal bonds with durations generally from three months to five years.

The BB1MBI contains only bonds with maturities greater than one year but less than two years, and it does not contain any bonds with less than one year remaining to maturity nor does it include MVRDNs and MFRNs. The Fund’s portfolio of 25% to 30% in MFRNs and 10% to 25% in MVRDNs underperformed the longer maturity bonds contained in the BB1MBI (1-to-2-year maturities) during the reporting period, but contributed to lower price volatility within the portfolio, especially in March.

Annual Shareholder Report

SECTOR ALLOCATION

During the reporting period, the Fund received a positive contribution from sector allocation relative to the BB1MBI. The Fund maintained a higher portfolio allocation, relative to the BB1MBI, to securities issued by industrial development and pollution control revenue entities (corporate obligors and investor-owned electric and gas utilities), and hospitals. These allocations helped the Fund’s performance due to the outperformance of these sectors relative to the BB1MBI.

The Fund was significantly underweight, compared to the BB1MBI, in pre-refunded bonds (which are bonds for which the principal and interest payments are secured or guaranteed by cash or U.S. Treasury securities held in an escrow account), and since this sector was a slight underperformer and a 37% weight within the BB1MBI, this decision positively affected Fund performance relative to the BB1MBI during the reporting period.

Overall, security selection had a negative impact on the Fund’s performance relative to the BB1MBI during the reporting period. FRNs lagged the price performance of fixed-rate bonds in the BB1MBI over the reporting period, and the Fund’s need to maintain liquidity and sell fixed-rate securities in a volatile March period when investors had a strong preference for stable value U.S. Treasury-backed cash compared to risk based sectors such as municipals also detracted from performance.

CREDIT QUALITY

During the reporting period, investor appetite for yield in the low interest rate environment along with strong municipal bond fund inflows, the exception being significant outflows in March and April, resulted in outperformance of bonds rated “A” and “BBB” (or unrated bonds of comparable quality) relative to bonds rated in the higher rating categories (“AA” and “AAA”) (or unrated bonds of comparable quality). This credit allocation had a significant and positive effect on performance.

The Fund’s overweight position, relative to the BB1MBI, in “A”, “BBB” debt (or unrated bonds of comparable quality) during the reporting period had a significant and positive impact on the Fund’s performance. The Fund’s underweight position in bonds rated “AAA” and “AA” (or unrated bonds of comparable quality) also made a positive contribution to performance as bonds in these ratings categories underperformed within the BB1MBI.

Annual Shareholder Report

1

Bond prices are sensitive to changes in interest rates, and a rise in interest rates can cause a decline in their prices. The Fund is not a “money market” mutual fund. Some money market mutual funds attempt to maintain a stable net asset value through compliance with relevant Securities and Exchange Commission (SEC) rules. The Fund is not governed by those rules, and its shares will fluctuate in value.

2

Income may be subject to the federal alternative minimum tax, as well as state and local taxes.

3

Please see the footnotes to the line graphs under “Fund Performance and Growth of a $10,000 Investment” below for the definition of, and more information about, the BB1MBI.

4

Please see the footnotes to the line graphs under “Fund Performance and Growth of a $10,000 Investment” below for the definition of, and more information about, the LSMDFA.

5

Please see the footnotes to the line graphs under “Fund Performance and Growth of a $10,000 Investment” below for the definition of, and more information about, the Blended Index.

6

Duration is a measure of a security’s price sensitivity to changes in interest rates. Securities with longer durations are more sensitive to changes in interest rates than securities with shorter durations. For purposes of this Management’s Discussion of Fund Performance, duration is determined using a third-party analytical system.

7

Investment-grade securities and noninvestment-grade securities may either be: (a) rated by a nationally recognized statistical ratings organization or rating agency; or (b) unrated securities that the Fund’s investment adviser (“Adviser”) believes are of comparable quality. The rating agencies that provided the ratings for rated securities include Standard & Poor’s, Moody’s Investor Services, Inc. and Fitch Rating Service. When ratings vary, the highest rating is used. Credit ratings of “AA” or better are considered to be high credit quality; credit ratings of “A” are considered high or medium/good quality; and credit ratings of “BBB” are considered to be medium/good credit quality, and the lowest category of investment-grade securities; credit ratings of “BB” and below are lower-rated, noninvestment-grade securities or junk bonds; and credit ratings of “CCC” or below are noninvestment-grade securities that have high default risk. Any credit quality breakdown does not give effect to the impact of any credit derivative investments made by the Fund. Credit ratings are an indication of the risk that a security will default. They do not protect a security from credit risk. Lower-rated bonds typically offer higher yields to help compensate investors for the increased risk associated with them. Among these risks are lower creditworthiness, greater price volatility, more risk to principal and income than with higher rated securities and increased possibilities of default.

Annual Shareholder Report

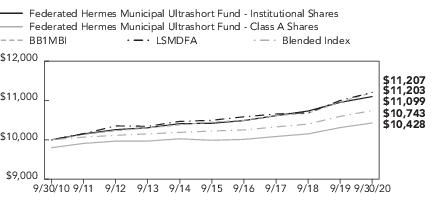

FUND PERFORMANCE AND GROWTH OF A $10,000 INVESTMENT

The graph below illustrates the hypothetical investment of $10,0001 in the Federated Hermes Municipal Ultrashort Fund (the “Fund”) from September 30, 2010 to September 30, 2020, compared to the Bloomberg Barclays 1-Year U.S. Municipal Bond Index (BB1MBI),2 the Lipper Short Municipal Debt Funds Average (LSMDFA)3 and a 50/50 blended index (Blended Index) of the BB1MBI and Lipper Tax-Exempt Money Market Funds Average.2,3 The Average Annual Total Return table below shows returns for each class averaged over the stated periods.

Growth of a $10,000 Investment

Growth of $10,000 as of September 30, 2020

■ Total returns shown for Class A include the maximum sales charge of 2.00% ($10,000 investment minus $200 sales charge = $9,800).

The Fund offers multiple share classes whose performance may be greater than or less than its other share class(es) due to differences in sales charges and expenses. See the Average Annual Return table below for the returns of additional classes not shown in the line graph above.

Average Annual Total Returns for the Period Ended 9/30/2020

(returns reflect all applicable sales charges as specified below in footnote #1)

Annual Shareholder Report

Performance data quoted represents past performance which is no guarantee of future results. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Mutual fund performance changes over time and current performance may be lower or higher than what is stated. For current to the most recent month-end performance and after-tax returns, visit FederatedInvestors.com or call 1-800-341-7400. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Mutual funds are not obligations of or guaranteed by any bank and are not federally insured.

1

Represents a hypothetical investment of $10,000 in the Fund after deducting applicable sales charge. For Class A Shares, the maximum sales charge of 2.00% ($10,000 investment minus $200 sales charge = $9,800). The Fund’s performance assumes the reinvestment of all dividends and distributions. The BB1MBI, the LSMDFA and the Blended Index have been adjusted to reflect reinvestment of dividends on securities in the index and the average.

2

The BB1MBI is the one-year (1-2) component of the Bloomberg Barclays U.S. Municipal Bond Index. The Bloomberg Barclays U.S. Municipal Bond Index covers the USD-denominated long-term tax-exempt bond market. The index has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds and prerefunded bonds. The BB1MBI is not adjusted to reflect sales charges, expenses or other fees that the SEC requires to be reflected in the Fund’s performance. The Fund is not a money market fund and is not subject to the special regulatory requirements (including maturity and credit quality constraints) designed to enable money market funds to maintain a stable share price. The BB1MBI is unmanaged, and unlike the Fund, is not affected by cash flows. It is not possible to invest directly in an index.

3

Lipper figures represent the average of the total returns reported by all funds designated by Lipper, Inc., as falling into the respective category and are not adjusted to reflect any sales charges. The Lipper figures in the Growth of $10,000 line graph are based on historical return information published by Lipper and reflect the return of the funds comprising the category in the year of publication. Because the funds designated by Lipper as falling into the category can change over time, the Lipper figures in the line graph may not match the Lipper figures in the Average Annual Total Returns table, which reflect the return of the funds that currently comprise the category.

4

The Fund’s Class R6 Shares commenced operations on May 29, 2019. For the period prior to the commencement of operations of the Class R6 Shares, the Class R6 Shares performance information shown is for the Fund’s Institutional Shares. The performance of the Institutional Shares has not been adjusted to reflect the expenses of the Class R6 Shares since the Class R6 Shares have a lower expense ratio than the expense ratio of the Institutional Shares.

Annual Shareholder Report

Portfolio of Investments Summary Table (unaudited)

At September 30, 2020, the Fund’s sector composition1 was as follows:

| Percentage of

Total Net Assets |

Industrial Development Bond/Pollution Control Revenue | |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

Other Assets and Liabilities—Net3 | |

| |

1

Sector classifications, and the assignment of holdings to such sectors, are based upon the economic sector and/or revenue source of the underlying obligor, as determined by the Fund’s Adviser. For securities that have been enhanced by a third-party guarantor, such as bond insurers and banks, sector classifications are based upon the economic sector and/or revenue source of the underlying obligor, as determined by the Fund’s Adviser.

2

For purposes of this table, sector classifications constitute 83.0% of the Fund’s total net assets. Remaining sectors have been aggregated under the designation “Other.”

3

Assets, other than investments in securities, less liabilities. See Statement of Assets and Liabilities.

Annual Shareholder Report

Portfolio of Investments

September 30, 2020

| | | |

| | | |

| | | |

| | Black Belt Energy Gas District, AL, Gas Prepay Revenue Bonds Project No. 4 (Series 2019A-1), (Morgan Stanley GTD), 4.000%, 6/1/2021 | |

| | Black Belt Energy Gas District, AL, Gas Prepay Revenue Bonds Project No. 4 (Series 2019A-1), (Morgan Stanley GTD), 4.000%, 6/1/2022 | |

| | Black Belt Energy Gas District, AL, Gas Prepay Revenue Bonds Project No. 4 (Series 2019A-1), (Morgan Stanley GTD), 4.000%, 6/1/2023 | |

| | Black Belt Energy Gas District, AL, Gas Prepay Revenue Bonds Project No.3 (Series 2018B-1) FRNs, (Goldman Sachs Group, Inc. GTD), 1.004% (1-month USLIBOR x 0.67 +0.900%), Mandatory Tender 12/1/2023 | |

| | Lower Alabama Gas District, Gas Project Revenue Bonds Project No.2 (Series 2020A) TOBs, (Goldman Sachs Group, Inc. GTD), 4.000%, Mandatory Tender 12/1/2025 | |

| | Selma, AL IDB (International Paper Co.), Gulf Opportunity Zone Revenue Refunding Bonds (Series 2019A) TOBs, 2.000%, Mandatory Tender 10/1/2024 | |

| | Selma, AL IDB (International Paper Co.), Gulf Opportunity Zone Revenue Refunding Bonds (Series 2020A) TOBs, 1.375%, Mandatory Tender 6/16/2025 | |

| | Southeast Alabama Gas Supply District, Gas Supply Revenue Bonds Project No. 2 (Series 2018B) FRNs, (Morgan Stanley GTD), 0.954% (1-month USLIBOR x 0.67 +0.850%), Mandatory Tender 6/1/2024 | |

| | | |

| | | |

| | Chandler, AZ IDA (Intel Corp.), Industrial Development Revenue Bonds (Series 2019) TOBs, 4.918%, Mandatory Tender 6/3/2024 | |

| | Coconino County, AZ Pollution Control Corp. (Nevada Power Co.), Pollution Control Refunding Revenue Bonds (Series 2017A) TOBs, 1.875%, Mandatory Tender 3/31/2023 | |

| | Maricopa County, AZ Pollution Control Corp. (Public Service Co., NM), Pollution Control Revenue Refunding Bonds Palo Verde Project (Series 2003A) TOBs, 1.050%, Mandatory Tender 6/1/2022 | |

| | Tempe, AZ IDA (Mirabella at ASU), Revenue Bonds (Series 2017B), 4.000%, 10/1/2023 | |

Annual Shareholder Report

| | | |

| | MUNICIPAL BONDS—continued | |

| | | |

| | Yavapai County, AZ IDA Solid Waste Disposal (Waste Management, Inc.), Solid Waste Disposal Revenue Bonds (Series 2002) TOBs, 2.800%, Mandatory Tender 6/1/2021 | |

| | | |

| | | |

| | Bay Area Toll Authority, CA, San Francisco Bay Area Toll Bridge Revenue Bonds (Index Rate Bonds Series 2017D) FRNs, 0.757% (3-month USLIBOR x 0.70 +0.550%), Mandatory Tender 4/1/2021 | |

| | California Infrastructure & Economic Development Bank (California Academy of Sciences), Revenue Bonds (Series 2018B) FRNs, 0.483% (1-month USLIBOR x 0.70 +0.380%), Mandatory Tender 8/1/2021 | |

| | California Infrastructure & Economic Development Bank (DesertXpress Enterprises, LLC), (Series 2020A: Brightline West Passenger Rail) TOBs, (United States Treasury GTD), 0.450%, Mandatory Tender 7/1/2021 | |

| | California Infrastructure & Economic Development Bank (J Paul Getty Trust), Variable Rate Refunding Revenue Bonds (Series 2011A-1) FRNs, 0.309% (1-month USLIBOR x 0.70 +0.200%), Mandatory Tender 4/1/2021 | |

| | California Infrastructure & Economic Development Bank (Los Angeles County Museum of Art), Revenue Refunding Bonds (Series 2017B) FRNs, 0.754% (1-month USLIBOR x 0.70 +0.650%), Mandatory Tender 2/1/2021 | |

| | California PCFA (Republic Services, Inc.), (Series A-2) TOBs, 0.600%, Mandatory Tender 10/15/2020 | |

| | California PCFA (Republic Services, Inc.), Solid Waste Refunding Revenue Bonds (Series 2010A) TOBs, 0.500%, Mandatory Tender 11/2/2020 | |

| | California State Pollution Control Financing Authority (American Water Capital Corp.), Revenue Refunding Bonds (Series 2020) TOBs, 0.600%, Mandatory Tender 9/1/2023 | |

| | California State, UT GO Bonds (Index Floating Rate Bonds Series 2013D) FRNs, 0.370% (SIFMA 7-day +0.290%), Mandatory Tender 12/1/2020 | |

| | California State, UT GO Various Purpose Bonds, 5.000%, 3/1/2029 | |

| | California State, UT GO Various Purpose Refunding Bonds, 5.000%, 3/1/2025 | |

| | California State, Various Purpose GO Bonds (Series 2020-1), 5.000%, 11/1/2024 | |

| | California State, Various Purpose GO Bonds (Series 2020-1), 5.000%, 11/1/2025 | |

| | Southern California Public Power Authority (Power Projects), Windy Point/Windy Flats Project Revenue Refunding Bonds (Series 2020-1) Green Bonds, 5.000%, 4/1/2024 | |

Annual Shareholder Report

| | | |

| | MUNICIPAL BONDS—continued | |

| | | |

| | Western Placer, CA Unified School District, Community Facilities District No. 1 2020 Bond Anticipation Notes, 2.000%, 6/1/2025 | |

| | Western Placer, CA Unified School District, Community Facilities District No.2 2020 Bond Anticipation Notes, 2.000%, 6/1/2025 | |

| | | |

| | | |

| | Colorado School of Mines Board of Trustees (Colorado School of Mines, CO), Institutional Enterprise Revenue Refunding Bonds (Series 2018A) FRNs, 0.604% (1-month USLIBOR x 0.67 +0.500%), 2/1/2023 | |

| | Denver, CO City & County Department of Aviation, Airport System Revenue Refunding Bonds (Series 2019D) TOBs, 5.000%, Mandatory Tender 11/15/2022 | |

| | E-470 Public Highway Authority, CO, Senior Revenue Bonds (LIBOR Index Series 2017B) FRNs, 1.151% (1-month USLIBOR x 0.67 +1.050%), Mandatory Tender 9/1/2021 | |

| | E-470 Public Highway Authority, CO, Senior Revenue Bonds (LIBOR Index Series 2019A) FRNs, 0.517% (1-month USLIBOR x 0.67 +0.420%), Mandatory Tender 9/1/2021 | |

| | | |

| | | |

| | Connecticut State Health & Educational Facilities (Yale-New Haven Hospital), Revenue Bonds (Series 2019B) TOBs, 1.800%, Mandatory Tender 7/1/2024 | |

| | Connecticut State Special Transportation Fund, Special Tax Obligation Bonds Transportation Infrastructure Purposes (Series 2020A), 4.000%, 5/1/2021 | |

| | Connecticut State Special Transportation Fund, Special Tax Obligation Bonds Transportation Infrastructure Purposes (Series 2020A), 5.000%, 5/1/2022 | |

| | Connecticut State Special Transportation Fund, Special Tax Obligation Bonds Transportation Infrastructure Purposes (Series 2020A), 5.000%, 5/1/2023 | |

| | Connecticut State Special Transportation Fund, Special Tax Obligation Bonds Transportation Infrastructure Purposes (Series 2020A), 5.000%, 5/1/2024 | |

| | Connecticut State Special Transportation Fund, Special Tax Obligation Bonds Transportation Infrastructure Purposes (Series 2020A), 5.000%, 5/1/2025 | |

| | Connecticut State Special Transportation Fund, Special Tax Obligation Bonds Transportation Infrastructure Purposes (Series 2020A), 5.000%, 5/1/2026 | |

| | Connecticut State Special Transportation Fund, Special Tax Obligation Bonds Transportation Infrastructure Purposes (Series 2020A), 5.000%, 5/1/2027 | |

Annual Shareholder Report

| | | |

| | MUNICIPAL BONDS—continued | |

| | | |

| | Connecticut State, UT GO SIFMA Index Bonds (Series 2013A) FRNs, 0.870% (SIFMA 7-day +0.750%), 3/1/2021 | |

| | Connecticut State, UT GO SIFMA Index Bonds (Series 2013A) FRNs, 0.970% (SIFMA 7-day +0.850%), 3/1/2022 | |

| | Connecticut State, UT GO SIFMA Index Bonds (Series 2013A) FRNs, 1.020% (SIFMA 7-day +0.900%), 3/1/2023 | |

| | Griswold, CT BANs, 2.000%, 10/20/2020 | |

| | West Haven, CT, (Series B) BANs, 2.000%, 9/30/2021 | |

| | | |

| | | |

| | Delaware Economic Development Authority (Delmarva Power and Light Co.), Gas Facilities Revenue Refunding Bonds (Series 2020A) TOBs, 1.050%, Mandatory Tender 7/1/2025 | |

| | | |

| | Escambia County, FL (International Paper Co.), Environmental Improvement Revenue Refunding Bonds (Series 2019B) TOBs, 2.000%, Mandatory Tender 10/1/2024 | |

| | Jacksonville, FL EDC (JEA, FL Electric System), (Series 2000-A), CP, (U.S. Bank, N.A. LIQ), 0.210%, Mandatory Tender 10/1/2020 | |

| | Miami-Dade County, FL IDA (Waste Management, Inc.), (Series 2011) TOBs, 1.600%, Mandatory Tender 11/2/2020 | |

| | Orlando, FL Utilities Commission, Utility System Revenue Refunding Bonds (Series 2017A) TOBs, 3.000%, Mandatory Tender 10/1/2020 | |

| | Orlando, FL Utilities Commission, Utility System Revenue Refunding Bonds (Series 2017A) TOBs, 5.000%, Mandatory Tender 10/1/2020 | |

| | Pasco County, FL School Board, Variable Rate Refunding Certificates of Participation (Series 2020B) FRNs, 0.870% (SIFMA 7-day +0.750%), Mandatory Tender 8/2/2023 | |

| | | |

| | | |

| | Atlanta, GA (Atlantic Station Project), Tax Allocation Refunding Bonds (Series 2017), 5.000%, 12/1/2020 | |

| | Atlanta, GA (Atlantic Station Project), Tax Allocation Refunding Bonds (Series 2017), 5.000%, 12/1/2021 | |

| | Bartow County, GA Development Authority (Georgia Power Co.), Bowen Project Pollution Control Revenue Bonds (First Series 1997) TOBs, 2.050%, Mandatory Tender 11/19/2021 | |

| | Burke County, GA Development Authority (Georgia Power Co.), Vogtle Project Pollution Control Revenue Bonds (Fifth Series 1994) TOBs, 2.150%, Mandatory Tender 6/13/2024 | |

Annual Shareholder Report

| | | |

| | MUNICIPAL BONDS—continued | |

| | | |

| | Burke County, GA Development Authority (Georgia Power Co.), Vogtle Project Pollution Control Revenue Bonds (First Series 2012) TOBs, 1.550%, Mandatory Tender 8/19/2022 | |

| | Burke County, GA Development Authority (Georgia Power Co.), Vogtle Project Pollution Control Revenue Bonds (Second Series 2012) TOBs, 1.700%, Mandatory Tender 8/22/2024 | |

| | Main Street Natural Gas, Inc., GA, Gas Supply Revenue Bonds (Series 2018B) FRNs, (Royal Bank of Canada GTD), 0.854% (1-month USLIBOR x 0.67 +0.750%), Mandatory Tender 9/1/2023 | |

| | Main Street Natural Gas, Inc., GA, Gas Supply Revenue Bonds (Series 2019B) TOBs, (Toronto Dominion Bank GTD), 4.000%, Mandatory Tender 12/2/2024 | |

| | Monroe County, GA Development Authority Pollution Control (Georgia Power Co.), Scherer Project Pollution Control Revenue Bonds (First Series 2009) TOBs, 2.050%, Mandatory Tender 11/19/2021 | |

| | Private Colleges & Universities Facilities of GA (Emory University), Revenue Bonds (Series 2020B), 5.000%, 9/1/2025 | |

| | | |

| | | |

| | Chicago, IL Water Revenue, Second Lien Water Revenue Refunding Bonds (Series 2004), 5.000%, 11/1/2020 | |

| | Chicago, IL Water Revenue, Second Lien Water Revenue Refunding Bonds (Series 2004), 5.000%, 11/1/2021 | |

| | Illinois Finance Authority (Admiral at the Lake), Revenue Refunding Bonds (Series 2017), 5.000%, 5/15/2021 | |

| | Illinois Finance Authority (OSF Health Care Systems), Revenue Bonds (Series 2020A) TOBs, 5.000%, Mandatory Tender 11/15/2024 | |

| | Illinois State Solid Waste Development Authority (Waste Management, Inc.), (Series 2019) TOBs, 1.600%, Mandatory Tender 11/2/2020 | |

| | Illinois State, GO Bonds (Series 2017D), 5.000%, 11/1/2020 | |

| | Illinois State, GO Bonds (Series 2017D), 5.000%, 11/1/2021 | |

| | Illinois State, GO Bonds (Series 2017D), 5.000%, 11/1/2022 | |

| | Illinois State, GO Bonds (Series 2017D), 5.000%, 11/1/2024 | |

| | Illinois State, UT GO Bonds (Series 2020B), 5.375%, 5/1/2023 | |

| | Illinois State, UT GO Refunding Bonds (Series 2018A), 5.000%, 10/1/2021 | |

| | Illinois State, UT GO Refunding Bonds (Series 2018A), 5.000%, 10/1/2022 | |

| | | |

Annual Shareholder Report

| | | |

| | MUNICIPAL BONDS—continued | |

| | | |

| | Bartholomew Consolidated School Corp., IN TANs, 4.000%, 12/31/2020 | |

| | Beech Grove, IN CSD BANs, 2.000%, 7/15/2021 | |

| | Indiana Health Facility Financing Authority (Ascension Health Alliance Senior Credit Group), Revenue Bonds (Series 2001A-2) TOBs, (United States Treasury PRF), 2.000%, Mandatory Tender 2/1/2023 | |

| | Indiana Health Facility Financing Authority (Ascension Health Alliance Senior Credit Group), Revenue Bonds (Series 2001A-2) TOBs, 2.000%, Mandatory Tender 2/1/2023 | |

| | Indiana State EDA (Republic Services, Inc.), (Series A) TOBs, 0.650%, Mandatory Tender 12/1/2020 | |

| | Rockport, IN PCR (American Electric Power Co., Inc.), Pollution Control Revenue Refunding Bonds (Series 1995A) TOBs, 1.350%, Mandatory Tender 9/1/2022 | |

| | Rockport, IN PCR (American Electric Power Co., Inc.), Pollution Control Revenue Refunding Bonds (Series 1995B) TOBs, 1.350%, Mandatory Tender 9/1/2022 | |

| | | |

| | | |

| | Iowa Finance Authority, Single Family Mortgage Bonds (Series 2018B) FRNs, 0.420% (SIFMA 7-day +0.300%), Mandatory Tender 5/3/2021 | |

| | | |

| | Holton, KS (Holton Community Hospital), Hospital Loan Anticipation Revenue Bonds (Series 2019), 2.500%, 7/1/2021 | |

| | | |

| | Kentucky Housing Corp. (BTT Development III Portfolio), Multifamily Rental Housing Revenue Bonds (Series 2019) TOBs, (United States Treasury GTD), 1.400%, Mandatory Tender 6/1/2022 | |

| | Kentucky State Rural Water Finance Corp., Public Project Construction Notes (Series E-2019-1), 1.450%, 6/1/2021 | |

| | Louisville & Jefferson County, KY Metropolitan Government (Louisville Gas & Electric Co.), Revenue Refunding Bonds Series 2013A (Remarketing 4/1/19) TOBs, 1.850%, Mandatory Tender 4/1/2021 | |

| | Louisville & Jefferson County, KY Metropolitan Government (Norton Healthcare, Inc.), Health System Revenue Bonds (Series 2020B) TOBs, 5.000%, Mandatory Tender 10/1/2023 | |

| | Owen County, KY (American Water Capital Corp.), Revenue Refunding Bonds (Series 2020) TOBs, 0.700%, Mandatory Tender 9/1/2023 | |

Annual Shareholder Report

| | | |

| | MUNICIPAL BONDS—continued | |

| | | |

| | Public Energy Authority of Kentucky, Gas Supply Revenue Bonds (Series 2018B) TOBs, (BP PLC GTD), 4.000%, Mandatory Tender 1/1/2025 | |

| | Public Energy Authority of Kentucky, Gas Supply Revenue Bonds (Series 2019A-1) TOBs, (Morgan Stanley GTD), 4.000%, Mandatory Tender 6/1/2025 | |

| | Public Energy Authority of Kentucky, Gas Supply Revenue Bonds (Series 2020A) TOBs, (BP PLC GTD), 4.000%, Mandatory Tender 6/1/2026 | |

| | | |

| | | |

| | Louisiana Local Government Environmental Facilities Community Development Authority (East Baton Rouge Sewerage Commission), Subordinate Lien Multi-Modal Revenue Refunding Bonds (Series 2020B) TOBs, 0.875%, Mandatory Tender 2/1/2025 | |

| | St. John the Baptist Parish, LA (Marathon Oil Corp.), Revenue Refunding Bonds (Series 2017B-1) TOBs, 2.125%, Mandatory Tender 7/1/2024 | |

| | St. John the Baptist Parish, LA (Marathon Oil Corp.), Revenue Refunding Bonds (Series 2019 A-1) TOBs, 2.000%, Mandatory Tender 4/1/2023 | |

| | | |

| | | |

| | Massachusetts Department of Transportation, Subordinated Metropolitan Highway System Revenue Refunding Bonds (Series 2019A) TOBs, 5.000%, Mandatory Tender 1/1/2023 | |

| | Massachusetts Development Finance Agency (Mass General Brigham), Index Floating Rate Bonds (Series 2017S) FRNs, 0.540% (SIFMA 7-day +0.420%), Mandatory Tender 1/27/2022 | |

| | Massachusetts Development Finance Agency (Mass General Brigham), Index Floating Rate Bonds (Series 2017S) FRNs, 0.620% (SIFMA 7-day +0.500%), Mandatory Tender 1/26/2023 | |

| | Massachusetts Development Finance Agency (Mass General Brigham), Revenue Bonds (Series 2017 S-4) TOBs, 5.000%, Mandatory Tender 1/25/2024 | |

| | Massachusetts HEFA (University of Massachusetts), Revenue Bonds (Series A) TOBs, 1.819%, Mandatory Tender 4/1/2022 | |

| | Massachusetts State HFA (Massachusetts State HFA SFH Revenue), Single Family Housing Revenue Bonds (Series 196) FRNs, 0.459% (1-month USLIBOR x 0.70 +0.350%), Mandatory Tender 6/1/2021 | |

| | Massachusetts State HFA (Massachusetts State HFA SFH Revenue), Single Family Housing Revenue Bonds (Series 212) TOBs, 1.450%, Mandatory Tender 12/1/2022 | |

Annual Shareholder Report

| | | |

| | MUNICIPAL BONDS—continued | |

| | | |

| | Orange, MA BANs, 1.250%, 8/27/2021 | |

| | | |

| | | |

| | Michigan State Hospital Finance Authority (Ascension Health Alliance Senior Credit Group), Refunding and Project Revenue Bonds (Series 2010F-2) TOBs, 1.900%, Mandatory Tender 4/1/2021 | |

| | Michigan State Hospital Finance Authority (McLaren Health Care Corp.), Hospital Revenue Refunding Floating Rate Bonds (Series 2015D-1) FRNs, 0.503% (1-month USLIBOR x 0.68 +0.400%), Mandatory Tender 10/15/2021 | |

| | Michigan State Housing Development Authority, Rental Housing Revenue Bonds (Series 2016E) FRNs, 1.207% (3-month USLIBOR x 0.70 +1.000%), Mandatory Tender 10/1/2021 | |

| | University of Michigan (The Regents of), General Revenue Bonds (Series 2019C) TOBs, 3.934%, Mandatory Tender 4/1/2024 | |

| | | |

| | | |

| | Brooklyn Center, MN (Sonder House Apartments), Multifamily Housing Revenue Refunding Bonds (Series 2019) TOBs, 1.350%, Mandatory Tender 7/1/2022 | |

| | Minnesota State HFA, Residential Housing Finance Bonds (Series 2018D) FRNs, 0.550% (SIFMA 7-day +0.430%), Mandatory Tender 7/3/2023 | |

| | | |

| | | |

| | Mississippi Business Finance Corp. (Mississippi Power Co.), Revenue Bonds (First Series 2010) TOBs, 2.750%, Mandatory Tender 12/9/2021 | |

| | | |

| | Missouri State Environmental Improvement & Energy Resources Authority (Union Electric Co.), Environmental Improvement Revenue Refunding Bonds (Series 1992), 1.600%, 12/1/2022 | |

| | Missouri State Public Utilities Commission, Interim Construction Notes (Series 2020), 0.500%, 3/1/2022 | |

| | | |

| | | |

| | Montana Facility Finance Authority (Billings Clinic Obligated Group), Variable Rate Revenue Bonds (Series 2018C) FRNs, 0.670% (SIFMA 7-day +0.550%), Mandatory Tender 8/15/2023 | |

| | Montana State University (The Board of Regents of), Facilities Refunding Revenue Bonds (Series 2018F) FRNs, 0.570% (SIFMA 7-day +0.450%), Mandatory Tender 9/1/2023 | |

| | | |

Annual Shareholder Report

| | | |

| | MUNICIPAL BONDS—continued | |

| | | |

| | BB&T Muni Trust, Tax-Exempt Pool Certificates (Series 2016 Class D) FRNs, (Cooperatieve Rabobank UA LOC), 1.370% (SIFMA 7-day +1.250%), 12/31/2021 | |

| | BB&T Muni Trust, Tax-Exempt Pool Certificates (Series 2018 Class C) FRNs, (Cooperatieve Rabobank UA LOC), 1.020% (SIFMA 7-day +0.800%), 11/30/2021 | |

| | | |

| | | |

| | Clark County, NV Airport System, Airport System Junior Subordinate Lien Revenue Notes (Series 2017C), 5.000%, 7/1/2021 | |

| | Clark County, NV Airport System, Airport System Subordinate Lien Revenue Refunding Bonds (Series 2019A), 5.000%, 7/1/2025 | |

| | Clark County, NV Pollution Control (Nevada Power Co.), Pollution Control Refunding Revenue Bonds (Series 2017) TOBs, 1.650%, Mandatory Tender 3/31/2023 | |

| | Clark County, NV School District, LT GO Building Bonds (Series 2020A), (Assured Guaranty Municipal Corp. INS), 3.000%, 6/15/2023 | |

| | Clark County, NV School District, LT GO Building Bonds (Series 2020A), (Assured Guaranty Municipal Corp. INS), 3.000%, 6/15/2025 | |

| | Clark County, NV School District, LT GO Building Bonds (Series 2020A), (Assured Guaranty Municipal Corp. INS), 5.000%, 6/15/2026 | |

| | Director of the State of Nevada Department of Business and Industry (DesertXpress Enterprises, LLC), (Series 2020A: Brightline West Passenger Rail) TOBs, (United States Treasury GTD), 0.500%, Mandatory Tender 7/1/2021 | |

| | Director of the State of Nevada Department of Business and Industry (Republic Services, Inc.) TOBs, 0.875%, Mandatory Tender 12/1/2020 | |

| | Humboldt County, NV (Idaho Power Co.), PCR Refunding Bonds (Series 2003), 1.450%, 12/1/2024 | |

| | | |

| | | |

| | National Finance Authority, NH (Waste Management, Inc.), (Series A-2) TOBs, 0.400%, Mandatory Tender 12/1/2020 | |

| | National Finance Authority, NH (Waste Management, Inc.), (Series A-3) TOBs, 0.400%, Mandatory Tender 12/1/2020 | |

| | National Finance Authority, NH (Waste Management, Inc.), Solid Waste Disposal Refunding Revenue Bonds (Series 2018A) FRNs, 0.870% (SIFMA 7-day +0.750%), Mandatory Tender 10/1/2021 | |

Annual Shareholder Report

| | | |

| | MUNICIPAL BONDS—continued | |

| | | |

| | National Finance Authority, NH (Waste Management, Inc.), Solid Waste Disposal Refunding Revenue Bonds (Series 2019A-1) TOBs, 2.150%, Mandatory Tender 7/1/2024 | |

| | National Finance Authority, NH (Waste Management, Inc.), Solid Waste Disposal Refunding Revenue Bonds (Series 2019A-3) TOBs, 2.150%, Mandatory Tender 7/1/2024 | |

| | National Finance Authority, NH (Waste Management, Inc.), Solid Waste Disposal Refunding Revenue Bonds (Series 2019A-4) TOBs, 2.150%, Mandatory Tender 7/1/2024 | |

| | | |

| | | |

| | Asbury Park, NJ BANs, 1.500%, 1/22/2021 | |

| | Bridgeton, NJ BANs, 1.250%, 5/25/2021 | |

| | Englewood Cliffs, NJ BANs, 2.000%, 2/19/2021 | |

| | New Jersey EDA (New Jersey-American Water Co., Inc.), Water Facilities Refunding Revenue Bonds (Series 2020B) TOBs, 1.200%, Mandatory Tender 6/1/2023 | |

| | New Jersey Turnpike Authority, Revenue Refunding Bonds (Series 2017 C-2) FRNs, 0.589% (1-month USLIBOR x 0.70 +0.480%), 1/1/2022 | |

| | New Jersey Turnpike Authority, Revenue Refunding Bonds (Series 2017 C-5) FRNs, 0.569% (1-month USLIBOR x 0.70 +0.460%), Mandatory Tender 1/1/2021 | |

| | New Jersey Turnpike Authority, Revenue Refunding Bonds (Series 2017 C-6) FRNs, 0.859% (1-month USLIBOR x 0.70 +0.750%), Mandatory Tender 1/1/2023 | |

| | Newark, NJ BANs, 3.500%, 7/27/2021 | |

| | Newark, NJ, (Series B) BANs, 2.000%, 10/5/2021 | |

| | Newark, NJ, (Series C) BANs, 2.000%, 10/5/2021 | |

| | Newark, NJ, UT GO Qualified General Improvement Refunding Bonds (Series 2020A), (Assured Guaranty Municipal Corp. INS), 5.000%, 10/1/2023 | |

| | Newark, NJ, UT GO Qualified General Improvement Refunding Bonds (Series 2020A), (Assured Guaranty Municipal Corp. INS), 5.000%, 10/1/2024 | |

| | Newark, NJ, UT GO Qualified General Improvement Refunding Bonds (Series 2020A), 5.000%, 10/1/2021 | |

| | Newark, NJ, UT GO Qualified General Improvement Refunding Bonds (Series 2020A), 5.000%, 10/1/2022 | |

| | Newark, NJ, UT GO Qualified School Refunding Bonds (Series 2020B), (Assured Guaranty Municipal Corp. INS), 5.000%, 10/1/2023 | |

| | Newark, NJ, UT GO Qualified School Refunding Bonds (Series 2020B), 5.000%, 10/1/2021 | |

Annual Shareholder Report

| | | |

| | MUNICIPAL BONDS—continued | |

| | | |

| | Newark, NJ, UT GO Qualified School Refunding Bonds (Series 2020B), 5.000%, 10/1/2022 | |

| | Riverdale Borough, NJ BANs, 1.500%, 9/10/2021 | |

| | Roseland, NJ BANs, 2.000%, 4/30/2021 | |

| | Roselle, NJ BANs, 2.000%, 11/18/2020 | |

| | South Hackensack, NJ BANs, 1.500%, 2/18/2021 | |

| | Spring Lake Heights, NJ BANs, 1.000%, 10/7/2021 | |

| | Tobacco Settlement Financing Corp., NJ, Tobacco Settlement Asset-Backed Refunding Bonds (Series 2018A), 5.000%, 6/1/2021 | |

| | Tobacco Settlement Financing Corp., NJ, Tobacco Settlement Asset-Backed Refunding Bonds (Series 2018A), 5.000%, 6/1/2022 | |

| | Union Beach, NJ BANs, 1.500%, 2/19/2021 | |

| | Weehawken Township, NJ BANs, 1.750%, 2/12/2021 | |

| | West Orange Township, NJ BANs, 2.000%, 5/6/2021 | |

| | | |

| | | |

| | Farmington, NM (Public Service Co., NM), Pollution Control Revenue Refunding Bonds (Series 2010B) TOBs, 2.125%, Mandatory Tender 6/1/2022 | |

| | Farmington, NM (Public Service Co., NM), Pollution Control Revenue Refunding Bonds (Series 2016B) TOBs, 1.875%, Mandatory Tender 10/1/2021 | |

| | Farmington, NM (Public Service Co., NM), Pollution Control Revenue Refunding Bonds San Juan Project (Series 2010C) TOBs, 1.150%, Mandatory Tender 6/4/2024 | |

| | Farmington, NM (Public Service Co., NM), Pollution Control Revenue Refunding Bonds San Juan Project (Series 2010D) TOBs, 1.100%, Mandatory Tender 6/1/2023 | |

| | New Mexico Municipal Energy Acquisition Authority, Gas Supply Revenue Refunding and Acquisition Bonds (Series 2019A) TOBs, (Royal Bank of Canada GTD), 5.000%, Mandatory Tender 5/1/2025 | |

| | New Mexico Municipal Energy Acquisition Authority, Gas Supply Revenue Refunding and Acquisition Bonds (Series 2019A), (Royal Bank of Canada GTD), 4.000%, 11/1/2021 | |

| | New Mexico Municipal Energy Acquisition Authority, Gas Supply Revenue Refunding and Acquisition Bonds (Series 2019A), (Royal Bank of Canada GTD), 4.000%, 11/1/2022 | |

| | New Mexico Municipal Energy Acquisition Authority, Gas Supply Revenue Refunding and Acquisition Bonds (Series 2019A), (Royal Bank of Canada GTD), 4.000%, 11/1/2023 | |

| | New Mexico Municipal Energy Acquisition Authority, Gas Supply Revenue Refunding and Acquisition Bonds (Series 2019A), (Royal Bank of Canada GTD), 4.000%, 11/1/2024 | |

Annual Shareholder Report

| | | |

| | MUNICIPAL BONDS—continued | |

| | | |

| | New Mexico Municipal Energy Acquisition Authority, Gas Supply Revenue Refunding and Acquisition Bonds (Series 2019A), (Royal Bank of Canada GTD), 4.000%, 5/1/2021 | |

| | New Mexico Municipal Energy Acquisition Authority, Gas Supply Revenue Refunding and Acquisition Bonds (Series 2019A), (Royal Bank of Canada GTD), 4.000%, 5/1/2022 | |

| | New Mexico Municipal Energy Acquisition Authority, Gas Supply Revenue Refunding and Acquisition Bonds (Series 2019A), (Royal Bank of Canada GTD), 4.000%, 5/1/2023 | |

| | New Mexico Municipal Energy Acquisition Authority, Gas Supply Revenue Refunding and Acquisition Bonds (Series 2019A), (Royal Bank of Canada GTD), 4.000%, 5/1/2024 | |

| | New Mexico Municipal Energy Acquisition Authority, Gas Supply Revenue Refunding and Acquisition Bonds (Series 2019A), (Royal Bank of Canada GTD), 4.000%, 5/1/2025 | |

| | | |

| | | |

| | Attica, NY Central School District BANs, 2.000%, 6/23/2021 | |

| | Auburn City School District, NY BANs, 1.500%, 6/23/2021 | |

| | Belfast, NY Central School District, (Series 2019A) BANs, 2.000%, 12/4/2020 | |

| | Campbell-Savona, NY, Central School District BANs, 1.500%, 6/25/2021 | |

| | Chautauqua County, NY Capital Resource Corporation (NRG Energy, Inc.), Exempt Facilities Revenue Refunding Bonds (Series 2020) TOBs, 1.278%, Mandatory Tender 4/3/2023 | |

| | Cortland, NY BANs, 1.750%, 11/25/2020 | |

| | Dalton-Nunda, NY Central School District BANs, 1.500%, 6/24/2021 | |

| | Elba, NY BANs, 1.750%, 11/24/2020 | |

| | Elmira, NY City School District BANs, 1.500%, 6/25/2021 | |

| | Endicott, NY BANs, 1.000%, 8/26/2021 | |

| | Fort Plain, NY CSD BANs, 1.500%, 6/30/2021 | |

| | Greater Southern Tier Board of Cooperative Educational Services, NY RANs, 1.500%, 6/30/2021 | |

| | Hempstead, NY Union Free School District RANs, 1.750%, 12/15/2020 | |

| | Honeoye, NY Central School District BANs, 1.500%, 6/30/2021 | |

| | Island Park Village, NY BANs, 2.000%, 3/4/2021 | |

| | Jamestown, NY BANs, 2.000%, 3/4/2021 | |

Annual Shareholder Report

| | | |

| | MUNICIPAL BONDS—continued | |

| | | |

| | Long Island Power Authority, NY, Electric System General Revenue Bonds (Series 2014C) (LIBOR Floating Rate Tender Notes) FRNs, 0.859% (1-month USLIBOR x 0.70 +0.750%), Mandatory Tender 10/1/2023 | |

| | Long Island Power Authority, NY, Electric System General Revenue Bonds (Series 2019B) TOBs, 1.650%, Mandatory Tender 9/1/2024 | |

| | Long Island Power Authority, NY, Electric System General Revenue Bonds (Series 2020B) TOBs, 0.850%, Mandatory Tender 9/1/2025 | |

| | Metropolitan Transportation Authority, NY (MTA Dedicated Tax Fund), Dedicated Tax Fund Variable Rate Bonds (Series 2008A-2A) FRNs, 0.570% (SIFMA 7-day +0.450%), Mandatory Tender 6/1/2022 | |

| | Metropolitan Transportation Authority, NY (MTA Transportation Revenue), Transportation Revenue Variable Rate Refunding Bonds (Series 2002D-A2) FRNs, (Assured Guaranty Municipal Corp. INS), 0.787% (1-month USLIBOR x 0.69 +0.680%), Mandatory Tender 4/6/2021 | |

| | Metropolitan Transportation Authority, NY (MTA Transportation Revenue), Transportation Revenue Variable Rate Refunding Bonds (Series 2011B) FRNs, 0.654% (1-month USLIBOR x 0.67 +0.550%), Mandatory Tender 11/1/2022 | |

| | Montgomery County, NY BANs, 2.000%, 10/8/2021 | |

| | New York City Housing Development Corp., Sustainable Development Bonds (Series 2016C-2) TOBs, 0.850%, Mandatory Tender 4/29/2021 | |

| | New York State Board of Cooperative Educational Services (Jefferson Lewis Hamilton Counties, NY) RANs, 1.250%, 6/17/2021 | |

| | New York State Board of Cooperative Educational Services (Orange and Ulster Counties, NY CSD) RANs, 1.000%, 7/22/2021 | |

| | New York State Dormitory Authority State Personal Income Tax Revenue, (Series B), 5.000%, 3/31/2021 | |

| | New York State Environmental Facilities Corp. (Waste Management, Inc.), Solid Waste Disposal Refunding Revenue Bonds (Series 2012) TOBs, 0.450%, Mandatory Tender 11/2/2020 | |

| | Newark Valley, NY Central School District BANs, 1.000%, 6/25/2021 | |

| | North West Fire District, NY, (Series A) BANs, 1.500%, 4/27/2021 | |

| | Oneida, NY Public Library District BANs, 1.500%, 7/9/2021 | |

| | Oneonta, NY City School District BANs, 1.500%, 6/25/2021 | |

| | Portville, NY Central School District BANs, 1.500%, 7/30/2021 | |

| | Romulus, NY Central School District BANs, 1.500%, 6/25/2021 | |

| | Rose, NY BANs, 1.250%, 9/16/2021 | |

Annual Shareholder Report

| | | |

| | MUNICIPAL BONDS—continued | |

| | | |

| | Sackets Harbor, NY CSD BANs, 2.000%, 6/18/2021 | |

| | Schenectady, NY TANs, 1.000%, 9/30/2021 | |

| | Scio, NY Central School District BANs, 1.250%, 6/25/2021 | |

| | Southwestern, NY Central School District BANs, 1.500%, 6/24/2021 | |

| | Stillwater, NY BANs, 1.500%, 6/4/2021 | |

| | Syracuse, NY BANs, 2.000%, 7/30/2021 | |

| | Warrensburg, NY CSD BANs, 1.500%, 6/25/2021 | |

| | Watson, NY BANs, 1.500%, 4/23/2021 | |

| | Wayne, NY Central School District BANs, 1.500%, 6/30/2021 | |

| | | |

| | | |

| | Columbus County, NC Industrial Facilities & Pollution Control Financing Authority (International Paper Co.), Recovery Zone Facility Revenue Refunding Bonds (Series 2019B) TOBs, 2.000%, Mandatory Tender 10/1/2024 | |

| | Columbus County, NC Industrial Facilities & Pollution Control Financing Authority (International Paper Co.), Recovery Zone Facility Revenue Refunding Bonds (Series 2020A) TOBs, 1.375%, Mandatory Tender 6/16/2025 | |

| | North Carolina Capital Facilities Finance Agency (Republic Services, Inc.), (Series 2013) TOBs, 0.280%, Mandatory Tender 12/15/2020 | |

| | North Carolina Capital Facilities Finance Agency (Republic Services, Inc.), (Series B) TOBs, 0.280%, Mandatory Tender 12/1/2020 | |

| | University of North Carolina at Chapel Hill, General Revenue Refunding Bonds (Series 2019A) FRNs, 0.454% (1-month USLIBOR x 0.67 +0.350%), Mandatory Tender 12/1/2021 | |

| | | |

| | | |

| | Chillicothe, OH BANs, 1.000%, 9/29/2021 | |

| | Harrison, OH BANs, 3.000%, 10/28/2020 | |

| | Lancaster, OH Port Authority, Gas Supply Revenue Refunding Bonds (Series 2019) TOBs, (Royal Bank of Canada GTD), 5.000%, Mandatory Tender 2/1/2025 | |

| | Lorain County, OH, (Series A) BANs, 3.000%, 2/6/2021 | |

| | Obetz Village, OH, (Series B) BANs, 2.000%, 11/20/2020 | |

| | Ohio State Higher Educational Facility Commission (Case Western Reserve University, OH), Revenue Refunding Bonds (Series 2019A) FRNs, 0.529% (1-month USLIBOR x 0.70 +0.420%), Mandatory Tender 4/1/2022 | |

Annual Shareholder Report

| | | |

| | MUNICIPAL BONDS—continued | |

| | | |

| | Ohio State Hospital Revenue (University Hospitals Health System, Inc.), Hospital Revenue Bonds (Series 2020B) TOBs, 5.000%, Mandatory Tender 1/15/2025 | |

| | Ohio Waste Development Authority Solid Waste (Waste Management, Inc.), Revenue Bonds (Series 2002), 3.250%, 11/1/2022 | |

| | Trenton, OH BANs, 2.125%, 11/12/2020 | |

| | | |

| | | |

| | Cleveland County, OK Educational Facilities Authority (Norman Public Schools), Education Facilities Lease Revenue Bonds (Series 2019), 5.000%, 6/1/2022 | |

| | Cleveland County, OK Educational Facilities Authority (Norman Public Schools), Educational Facilities Lease Revenue Bonds (Series 2019), 5.000%, 6/1/2021 | |

| | Cleveland County, OK Educational Facilities Authority (Norman Public Schools), Educational Facilities Lease Revenue Bonds (Series 2019), 5.000%, 6/1/2024 | |

| | | |

| | | |

| | Clackamas County, OR Hospital Facilities Authority (Rose Villa, Inc.), Senior Living Revenue Bonds TEMPS-50 (Series 2020B-2), 2.750%, 11/15/2025 | |

| | Clackamas County, OR Hospital Facilities Authority (Rose Villa, Inc.), Senior Living Revenue Bonds TEMPS-85 (Series 2020B-1), 3.250%, 11/15/2025 | |

| | | |

| | | |

| | Bethlehem, PA Area School District Authority, Revenue Refunding Bonds (Series 2018) FRNs, 0.586% (1-month USLIBOR x 0.70 +0.480%), Mandatory Tender 11/1/2021 | |

| | Bethlehem, PA Area School District Authority, Revenue Refunding Bonds (Series 2018A) FRNs, 0.586% (1-month USLIBOR x 0.70 +0.480%), Mandatory Tender 11/1/2021 | |

| | Lehigh County, PA General Purpose Authority (Muhlenberg College), College Revenue Bonds (Series 2019) FRNs, 0.700% (SIFMA 7-day +0.580%), Mandatory Tender 11/1/2024 | |

| | Lehigh County, PA IDA (PPL Electric Utilities Corp.), Pollution Control Revenue Refunding Bonds (Series 2016B) TOBs, 1.800%, Mandatory Tender 8/15/2022 | |

| | Manheim Township, PA School District, GO LIBOR Notes (Series 2017A) FRNs, 0.425% (1-month USLIBOR x 0.68 +0.320%), 5/3/2021 | |

Annual Shareholder Report

| | | |

| | MUNICIPAL BONDS—continued | |

| | | |

| | Manheim Township, PA School District, GO LIBOR Notes (Series 2017A) FRNs, 0.525% (1-month USLIBOR x 0.68 +0.420%), 11/1/2021 | |

| | Manheim Township, PA School District, GO LIBOR Notes (Series 2017A) FRNs, 0.575% (1-month USLIBOR x 0.68 +0.470%), Mandatory Tender 11/1/2021 | |

| | Montgomery County, PA Higher Education & Health Authority Hospital (Thomas Jefferson University), Revenue Bonds (Series 2018C) FRNs, 0.840% (SIFMA 7-day +0.720%), Mandatory Tender 9/1/2023 | |

| | North Penn, PA Water Authority, SIFMA Index Rate Water Revenue Refunding Bonds (Series 2019) FRNs, 0.380% (SIFMA 7-day +0.260%), 11/1/2021 | |

| | North Penn, PA Water Authority, SIFMA Index Rate Water Revenue Refunding Bonds (Series 2019) FRNs, 0.580% (SIFMA 7-day +0.460%), 11/1/2023 | |

| | Northampton County, PA General Purpose Authority (St. Luke’s University Health Network), Variable Rate Hospital Revenue Bonds (Series 2018B) FRNs, 1.149% (1-month USLIBOR x 0.70 +1.040%), Mandatory Tender 8/15/2024 | |

| | Pennsylvania Economic Development Financing Authority (PPL Electric Utilities Corp.), Pollution Control Revenue Refunding Bonds (Series 2008), 0.400%, 10/1/2023 | |

| | Pennsylvania Economic Development Financing Authority (Republic Services, Inc.), (Series 2014) TOBs, 0.650%, Mandatory Tender 1/4/2021 | |

| | Pennsylvania Economic Development Financing Authority (Republic Services, Inc.), (Series B-1) TOBs, 0.600%, Mandatory Tender 10/15/2020 | |

| | Pennsylvania Economic Development Financing Authority (Waste Management, Inc.), (Series 2013) TOBs, 0.450%, Mandatory Tender 11/2/2020 | |

| | Pennsylvania Economic Development Financing Authority (Waste Management, Inc.), Solid Waste Disposal Revenue Bonds (Series 2017A) TOBs, 0.700%, Mandatory Tender 8/2/2021 | |

| | Pennsylvania HFA, SFM Revenue Bonds (Series 2018-127C) FRNs, 0.676% (1-month USLIBOR x 0.70 +0.570%), Mandatory Tender 10/1/2023 | |

| | Pennsylvania State Turnpike Commission, Variable Rate Turnpike Revenue Bonds (Series 2018B) FRNs, 0.620% (SIFMA 7-day +0.500%), 12/1/2021 | |

| | Pennsylvania State Turnpike Commission, Variable Rate Turnpike Revenue Bonds (Series 2018B) FRNs, 0.820% (SIFMA 7-day +0.700%), 12/1/2023 | |

| | Pennsylvania State Turnpike Commission, Variable Rate Turnpike Revenue Bonds (SIFMA Index Bonds)(Series 2018A-1) FRNs, 0.720% (SIFMA 7-day +0.600%), 12/1/2023 | |

Annual Shareholder Report

| | | |

| | MUNICIPAL BONDS—continued | |

| | | |

| | Philadelphia, PA, GO Bonds (Series 2019B), 5.000%, 2/1/2023 | |

| | Philadelphia, PA, GO Bonds (Series 2019B), 5.000%, 2/1/2024 | |

| | Pittsburgh, PA Water & Sewer Authority, First Lien Revenue Refunding Bonds (Series 2018C) FRNs, (Assured Guaranty Municipal Corp. INS), 0.765% (1-month USLIBOR x 0.70 +0.640%), Mandatory Tender 12/1/2020 | |

| | Scranton, PA School District, GO Notes (Series 2014) (LIBOR Floating Rate Tender Notes) FRNs, (Pennsylvania School District Intercept Program GTD), 0.955% (1-month USLIBOR x 0.68 +0.850%), Mandatory Tender 4/1/2021 | |

| | Southcentral PA, General Authority (Wellspan Health Obligated Group), Revenue Bonds (Series 2019A) FRNs, 0.720% (SIFMA 7-day +0.600%), Mandatory Tender 6/1/2024 | |

| | University of Pittsburgh, Pitt Asset Notes—Higher Education Registered Series of 2019 FRNs, 0.480% (SIFMA 7-day +0.360%), 2/15/2024 | |

| | | |

| | | |

| | Charleston, SC Waterworks and Sewer System, Capital Improvement Revenue Bonds (Series 2006B) FRNs, 0.474% (3-month USLIBOR x 0.70 +0.370%), Mandatory Tender 1/1/2022 | |

| | Patriots Energy Group Financing Agency, Gas Supply Revenue Bonds (Series 2018B) FRNs, (Royal Bank of Canada GTD), 0.960% (1-month USLIBOR x 0.67 +0.860%), Mandatory Tender 2/1/2024 | |

| | South Carolina Transportation Infrastructure Bank, Revenue Refunding Bonds (Series 2003B) FRNs, 0.554% (1-month USLIBOR x 0.67 +0.450%), Mandatory Tender 10/1/2022 | |

| | | |

| | | |

| | Lewisburg, TN IDB (Waste Management, Inc.), (Series 2012) TOBs, 0.450%, Mandatory Tender 11/2/2020 | |

| | Memphis, TN Health, Educational and Housing Facility Board (Chickasaw Place Apartments), Collateralized Multifamily Housing Bonds (Series 2020) TOBs, 0.625%, Mandatory Tender 6/1/2022 | |

| | Tennergy Corp., TN Gas Revenue, Gas Supply Revenue Bonds (Series 2019A) TOBs, (Royal Bank of Canada GTD), 5.000%, Mandatory Tender 10/1/2024 | |

| | | |

| | | |

| | Alvin, TX Independent School District, Variable Rate Unlimited Tax Schoolhouse Bonds (Series 2014B) TOBs, (Texas Permanent School Fund Guarantee Program GTD), 0.450%, Mandatory Tender 8/15/2023 | |

| | Austin, TX Airport System, Revenue Refunding Bonds (Series 2019), 5.000%, 11/15/2020 | |

Annual Shareholder Report

| | | |

| | MUNICIPAL BONDS—continued | |

| | | |

| | Austin, TX Airport System, Revenue Refunding Bonds (Series 2019), 5.000%, 11/15/2021 | |

| | Austin, TX Airport System, Revenue Refunding Bonds (Series 2019), 5.000%, 11/15/2022 | |

| | Austin, TX Airport System, Revenue Refunding Bonds (Series 2019), 5.000%, 11/15/2023 | |

| | Austin, TX Airport System, Revenue Refunding Bonds (Series 2019), 5.000%, 11/15/2024 | |

| | Central Texas Regional Mobility Authority, Senior Lien Revenue & Refunding Bonds (Series 2015B) TOBs, 5.000%, Mandatory Tender 1/7/2021 | |

| | Cypress-Fairbanks, TX Independent School District, Variable Rate UT School Building Bonds (Series 2017A-2) TOBs, (Texas Permanent School Fund Guarantee Program GTD), 1.250%, Mandatory Tender 8/15/2022 | |

| | Dickinson, TX Independent School District, Variable Rate Unlimited Tax Refunding Bonds (Series 2013) TOBs, (Texas Permanent School Fund Guarantee Program GTD), 1.350%, Mandatory Tender 8/2/2021 | |

| | Eagle Mountain-Saginaw, TX Independent School District, Variable Rate Unlimited Tax School Building Bonds (Series 2011) TOBs, (Texas Permanent School Fund Guarantee Program GTD), 2.000%, Mandatory Tender 8/1/2024 | |

| | Eanes, TX Independent School District, Variable Rate UT School Building Bonds (Series 2019B) TOBs, (Texas Permanent School Fund Guarantee Program GTD), 1.750%, Mandatory Tender 8/1/2025 | |

| | Fort Bend, TX Independent School District, UT GO Refunding Bonds (Series 2019A) TOBs, (Texas Permanent School Fund Guarantee Program GTD), 1.950%, Mandatory Tender 8/1/2022 | |

| | Fort Bend, TX Independent School District, Variable Rate Unlimited Tax School Building and Refunding Bonds (Series 2020B) TOBs, (Texas Permanent School Fund Guarantee Program GTD), 0.875%, Mandatory Tender 8/1/2025 | |

| | Georgetown, TX Independent School District, Variable Rate Unlimited Tax School Building Bonds (Series 2019B) TOBs, (Texas Permanent School Fund Guarantee Program GTD), 2.750%, Mandatory Tender 8/1/2022 | |

| | Goose Creek, TX ISD, Variable Rate UT School Building Bonds (Series 2019B) TOBs, (Texas Permanent School Fund Guarantee Program INS), 3.000%, Mandatory Tender 10/1/2020 | |

| | Harris County, TX Cultural Education Facilities Finance Corp. (Memorial Hermann Health System), Hospital Revenue Refunding Bonds (Series 2013B) FRNs, 0.950% (SIFMA 7-day +0.830%), 6/1/2021 | |

Annual Shareholder Report

| | | |

| | MUNICIPAL BONDS—continued | |

| | | |

| | Harris County, TX Education Facilities Finance Corp. (Memorial Hermann Health System), Hospital Revenue Bonds (Series 2019B-1) TOBs, 5.000%, Mandatory Tender 12/1/2022 | |

| | Harris County, TX Education Facilities Finance Corp. (Memorial Hermann Health System), Hospital Revenue Bonds (Series 2019C-1) FRNs, 0.540% (SIFMA 7-day +0.420%), Mandatory Tender 12/1/2022 | |

| | Harris County, TX Education Facilities Finance Corp. (Memorial Hermann Health System), Hospital Revenue Bonds (Series 2019C-2) FRNs, 0.690% (SIFMA 7-day +0.570%), Mandatory Tender 12/4/2024 | |

| | Harris County, TX Education Facilities Finance Corp. (Memorial Hermann Health System), Variable Rate Hospital Revenue Refunding Bonds (Series 2020C-1) TOBs, 5.000%, Mandatory Tender 12/1/2022 | |

| | Harris County, TX Education Facilities Finance Corp. (Memorial Hermann Health System), Variable Rate Hospital Revenue Refunding Bonds (Series 2020C-2) TOBs, 5.000%, Mandatory Tender 12/1/2024 | |

| | Harris County, TX Education Facilities Finance Corp. (Memorial Hermann Health System), Variable Rate Hospital Revenue Refunding Bonds (Series 2020C-3) TOBs, 5.000%, Mandatory Tender 12/1/2026 | |

| | Houston, TX Combined Utility System, First Lien Revenue Refunding Bonds (Series 2018C) FRNs, 0.466% (1-month USLIBOR x 0.70 +0.360%), Mandatory Tender 8/1/2021 | |

| | Hutto, TX Independent School District, Unlimited Tax School Building Bonds (Series 2017) TOBs, (Texas Permanent School Fund Guarantee Program GTD), 2.000%, Mandatory Tender 8/1/2025 | |

| | Katy, TX Independent School District, Variable Rate Unlimited Tax Refunding Bonds (Series 2015C) FRNs, (Texas Permanent School Fund Guarantee Program GTD), 0.380% (1-month USLIBOR x 0.67 +0.280%), Mandatory Tender 8/16/2021 | |

| | Lower Colorado River Authority, TX (LCRA Transmission Services Corp.), Transmission Contract Refunding Revenue Bonds (Series 2019A), 5.000%, 5/15/2021 | |

| | Lower Colorado River Authority, TX (LCRA Transmission Services Corp.), Transmission Contract Refunding Revenue Bonds (Series 2019A), 5.000%, 5/15/2022 | |

| | Lower Colorado River Authority, TX (LCRA Transmission Services Corp.), Transmission Contract Refunding Revenue Bonds (Series 2019A), 5.000%, 5/15/2023 | |

| | Lower Colorado River Authority, TX (LCRA Transmission Services Corp.), Transmission Contract Refunding Revenue Bonds (Series 2019A), 5.000%, 5/15/2024 | |

Annual Shareholder Report

| | | |

| | MUNICIPAL BONDS—continued | |

| | | |

| | Lower Colorado River Authority, TX (LCRA Transmission Services Corp.), Transmission Contract Refunding Revenue Bonds (Series 2019A), 5.000%, 5/15/2025 | |

| | Lower Colorado River Authority, TX (LCRA Transmission Services Corp.), Transmission Contract Refunding Revenue Bonds (Series 2020), 5.000%, 5/15/2021 | |

| | Lower Colorado River Authority, TX (LCRA Transmission Services Corp.), Transmission Contract Refunding Revenue Bonds (Series 2020), 5.000%, 5/15/2022 | |

| | Mansfield, TX Independent School District, UT GO School Building Bonds (Series 2012) TOBs, (Texas Permanent School Fund Guarantee Program GTD), 2.500%, Mandatory Tender 8/1/2021 | |

| | Matagorda County, TX Navigation District No. 1 (AEP Texas, Inc.), PCR Refunding Bonds (Central Power and Light Company Project) (Series 1996) TOBs, 0.900%, Mandatory Tender 9/1/2023 | |

| | Midlothian, TX Independent School District, Variable Rate Unlimited Tax School Building Bonds (Series 2017B) TOBs, (Texas Permanent School Fund Guarantee Program GTD), 2.000%, Mandatory Tender 8/1/2023 | |

| | Mission, TX Economic Development Corp. (Republic Services, Inc.) TOBs, 0.500%, Mandatory Tender 11/2/2020 | |

| | Mission, TX Economic Development Corp. (Republic Services, Inc.), (Series 2020 A) TOBs, 0.500%, Mandatory Tender 11/2/2020 | |

| | Mission, TX Economic Development Corp. (Waste Management, Inc.), (Series B) TOBs, 0.400%, Mandatory Tender 12/1/2020 | |

| | Mission, TX Economic Development Corp. (Waste Management, Inc.), Solid Waste Disposal Revenue Bonds (Series 2018) FRNs, 0.920% (SIFMA 7-day +0.800%), Mandatory Tender 11/1/2021 | |

| | Northside, TX Independent School District, Variable Rate Unlimited Tax School Building Bonds (Series 2020) TOBs, (Texas Permanent School Fund Guarantee Program GTD), 0.700%, Mandatory Tender 6/1/2025 | |

| | Pflugerville, TX Independent School District, Variable Rate Unlimited Tax School Building Bonds (Series 2014) TOBs, (Texas Permanent School Fund Guarantee Program GTD), 2.250%, Mandatory Tender 8/15/2022 | |

| | San Antonio, TX Water System, Water System Variable Rate Junior Lien Revenue Bonds (Series 2019A) TOBs, 2.625%, Mandatory Tender 5/1/2024 | |

| | Spring Branch, TX Independent School District, Unlimited Tax Schoolhouse Bonds (Series 2013) TOBs, (Texas Permanent School Fund Guarantee Program GTD), 1.550%, Mandatory Tender 6/15/2021 | |

| | Texas State TRANs, 4.000%, 8/26/2021 | |

Annual Shareholder Report

| | | |

| | MUNICIPAL BONDS—continued | |

| | | |

| | Tomball, TX Independent School District, Variable Rate Unlimited Tax School Building Bonds (Series 2014B-1) TOBs, 0.450%, Mandatory Tender 8/15/2023 | |

| | | |

| | | |

| | Utah County, UT Hospital Revenue (IHC Health Services, Inc.), Revenue Bonds (Series 2020 B-1) TOBs, 5.000%, Mandatory Tender 8/1/2024 | |

| | Utah State, UT GO Bonds (Series 2020B), 5.000%, 7/1/2023 | |

| | Utah State, UT GO Bonds (Series 2020B), 5.000%, 7/1/2024 | |

| | | |

| | | |

| | Chesapeake Bay Bridge & Tunnel District, VA, First Tier General Resolution Revenue Bonds Anticipation Notes (Series 2019), 5.000%, 11/1/2023 | |

| | Chesapeake, VA EDA (Virginia Electric & Power Co.), PCR Refunding Bonds (Series 2008A) TOBs, 1.900%, Mandatory Tender 6/1/2023 | |

| | Louisa, VA IDA (Virginia Electric & Power Co.), PCR Refunding Bonds (Series 2008A) TOBs, 1.800%, Mandatory Tender 4/1/2022 | |

| | Virginia Peninsula Port Authority (Dominion Terminal Associates), Coal Terminal Revenue Refunding Bonds (Series 2003) TOBs, 1.700%, Mandatory Tender 10/1/2022 | |

| | Virginia State Public Building Authority Public Facilities, Public Facilities Revenue Refunding Bonds (Series 2020B), 5.000%, 8/1/2022 | |

| | Virginia State Public Building Authority Public Facilities, Public Facilities Revenue Refunding Bonds (Series 2020B), 5.000%, 8/1/2023 | |

| | Wise County, VA IDA (Virginia Electric & Power Co.), (Series 2010A) TOBs, 1.200%, Mandatory Tender 5/31/2024 | |

| | Wise County, VA IDA (Virginia Electric & Power Co.), Solid Waste and Sewage Disposal Revenue Bonds (Series 2009A) TOBs, 0.750%, Mandatory Tender 9/2/2025 | |

| | York County, VA EDA (Virginia Electric & Power Co.), PCR Refunding Bonds (Series 2009A) TOBs, 1.900%, Mandatory Tender 6/1/2023 | |

| | | |

| | | |

| | Seattle, WA Municipal Light & Power, Refunding Revenue Bonds—SIFMA Index (Series 2018C) FRNs, 0.610% (SIFMA 7-day +0.490%), Mandatory Tender 11/1/2023 | |

Annual Shareholder Report

| | | |

| | MUNICIPAL BONDS—continued | |

| | | |

| | Washington State Health Care Facilities Authority (CommonSpirit Health), Revenue Bonds (Series 2019B-1) TOBs, 5.000%, Mandatory Tender 8/1/2024 | |

| | Washington State Health Care Facilities Authority (Fred Hutchinson Cancer Research Center), Variable Rate LIBOR Index Revenue Bonds (Series 2017B) FRNs, 1.201% (1-month USLIBOR x 0.67 +1.100%), Mandatory Tender 7/1/2022 | |

| | Washington State Health Care Facilities Authority (Fred Hutchinson Cancer Research Center), Variable Rate SIFMA Index Revenue Bonds (Series 2017C) FRNs, 1.170% (SIFMA 7-day +1.050%), Mandatory Tender 7/3/2023 | |

| | | |

| | | |

| | Roane County, WV Building Commission (Roane General Hospital), Lease Revenue Bond Anticipation Notes (Series 2019), 2.550%, 11/1/2021 | |

| | West Virginia EDA Solid Waste Disposal Facilities (Appalachian Power Co.), Revenue Bonds (Series 2011A) TOBs, 1.000%, Mandatory Tender 9/1/2025 | |

| | | |

| | | |

| | Wisconsin State Public Finance Authority (Waste Management, Inc.), (Series A) TOBs, 0.450%, Mandatory Tender 11/2/2020 | |

| | Wisconsin State Public Finance Authority (Waste Management, Inc.), (Series A-2) TOBs, 0.450%, Mandatory Tender 11/2/2020 | |

| | Wisconsin State Public Finance Authority (Waste Management, Inc.), (Series A-3) TOBs, 0.450%, Mandatory Tender 11/2/2020 | |

| | | |

| | TOTAL MUNICIPAL BONDS