IPSCO Inc.

CIBC World Markets

Institutional Investor Conference

February 16, 2006

Information contained in this document other than historical information, may be considered forward-looking.

Forward-looking statements can be identified by the use of forward-looking words such as “believes,”

“expects,” “may,” “will,” “should,” “seeks,” “approximately,” “intends,” “plans,” “estimates” or “anticipates”

or the negative of these terms or other comparable words, or by discussions of strategy, plans or intentions.

Forward-looking information reflects management’s current views of future events and financial performance

that involve a number of risks and uncertainties. The factors that could cause actual results to differ

materially include, but are not limited to, the following: (1) general economic conditions; (2) changes in

financial markets; (3) political conditions and developments, including conflict in the Middle East and the war

on terrorism; (4) changes in the supply and demand for steel and our specific steel products; (5) the level of

demand outside of North America for steel and steel products; (6) equipment performance at our

manufacturing facilities; (7) the occurrence of any material lawsuits; (8) the availability of capital; (9) our

ability to properly and efficiently staff our manufacturing facilities; (10) domestic and international

competitive factors, including the level of steel imports into the Canadian and U.S. markets; (11) economic

conditions in steel exporting nations; (12) trade sanction activities and the enforcement of trade sanction

remedies; (13) supply and demand for scrap steel and iron, alloys and other raw materials; (14) supply,

demand and pricing for the electricity and natural gas that we use; (15) changes in environmental and other

regulations, including regulations arising from the Canadian Parliament’s ratification of the Kyoto Protocol,

and the magnitude of future environmental expenditures; (16) inherent uncertainties in the development and

performance of new or modified equipment or technologies; (17) North American interest rates; and (18)

exchange rates.

This list is not exhaustive of the factors which may impact our forward-looking statements. These and other

factors should be considered carefully and users should not place undue reliance on our forward-looking

statements. As a result of the foregoing and other factors, no assurance can be given as to any such future

results, levels of activity or achievements and neither we nor any other person assumes responsibility for the

accuracy and completeness of these forward-looking statements. We undertake no obligation to update

forward-looking statements contained in this presentation.

Special Note Regarding

Forward-Looking Statements

IPSCO At A Glance

One of North America’s leading steel plate and pipe

producers. IPSCO is a $4+ billion market capitalization stock,

dual-listed as “IPS” on the NYSE and TSX.

Uniquely positioned to capitalize on cyclical trends, employing

a “steel short” strategy to optimize pricing, production and

margins based on current demand across its markets -

industrial, transportation and energy.

A company with modern, state of the art facilities,

management depth and experience, and focus on low-cost

production and profitable growth - propelling the company to

record sales, record production and record earnings of $11.96

per diluted share in 2005

3

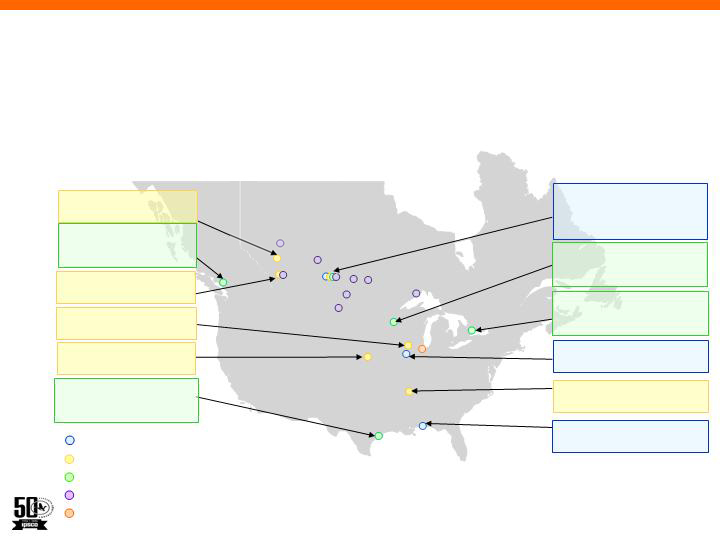

Thunder Bay

Minot

Dickinson

Saskatoon

Edmonton

Lisle

Winnipeg

Brandon

Surrey

Calgary

Red Deer

Regina

Geneva

Montpelier

Camanche

St. Paul

Toronto

Houston

Mobile

Blytheville

Note: Capacity in Tons

Houston, Texas

Temper Mill and

Cut-to-Length Line 300,000

Geneva, Nebraska

Pipe Mill 120,000

Camanche, Iowa

Pipe Mill 250,000

Calgary, Alberta

Pipe Mill 300,000

Red Deer, Alberta

Pipe Mill 155,000

Surrey, British Columbia

Cut-to-Length Line

150,000

Toronto, Ontario

Temper Mill and

Cut-to-Length Line 300,000

St. Paul, Minnesota

Temper Mill and

Cut-to-Length Line 300,000

Regina, Saskatchewan

Steelworks 1,000,000

Pipe Mills 650,000

Cut-to-Length Line 150,000

Montpelier, Iowa

Steelworks 1,250,000

Mobile, Alabama

Steelworks 1,250,000

Blytheville, Arkansas

Pipe Mill 300,000

Steel Products

Tubular Products

Coil Processing

Scrap Processing Centers

Operational Headquarters

Diverse Production And Geographic Capacity

4

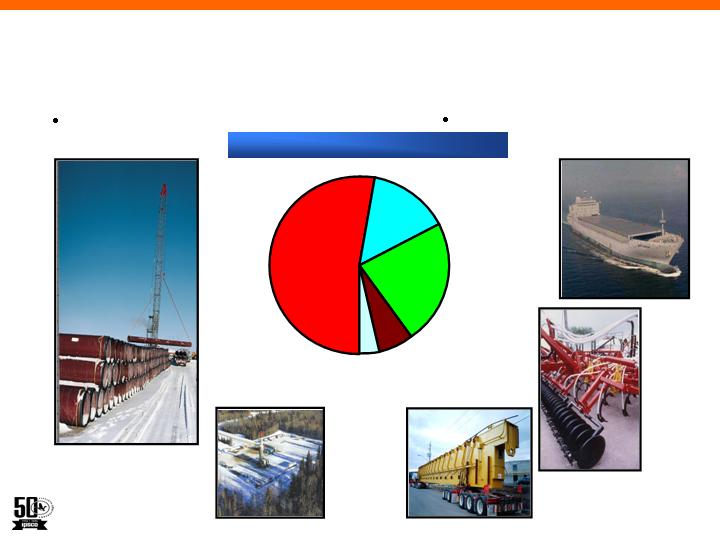

IPSCO’s Products

Tubular Products

Steel Mill Products

2005 Sales Distribution

Energy

Tubulars

22%

Cut-to-Length

15%

Discrete

Plate Coil

54%

Large

Diameter

Tubulars 2%

Non-Energy Tubulars

6%

5

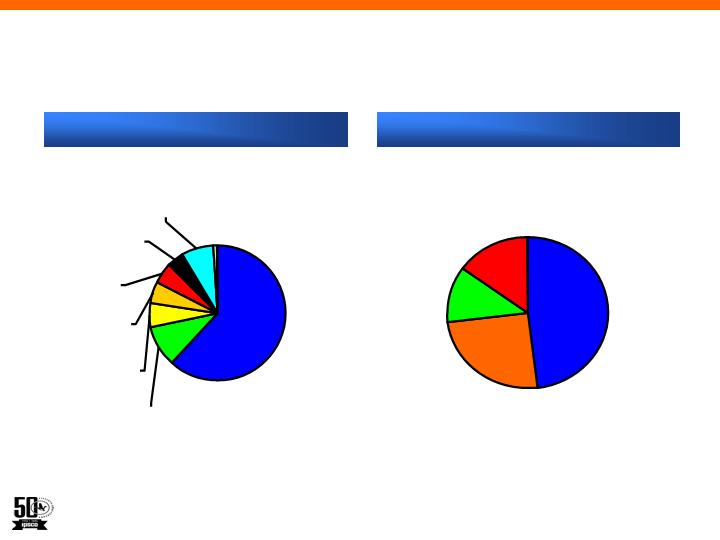

Sales Distribution by End Markets

2005 All Products

2005 Steel Mill Products

Oil & Gas

Industry

5%

Construction

Products

5%

Machinery &

Industrial

Equipment

6%

Pipe & Tube

Manufacturing

10%

Rail

Transportation

4%

Shipbuilding/

Marine

Equipment

7%

Service

Centers/

Distributors

62%

Other

1%

Energy

48%

Transportation

25%

Construction

12%

Machinery &

Industrial

Equipment

15%

6

IPSCO’s Energy Exposure

IPSCO is leveraged to the energy sector through

multiple channels:

Direct exposure through pipe business

Exploration and development - OCTG

Gathering and distribution – line pipe

Transmission – large diameter line pipe

Direct exposure through plate to energy fabricators

Wind Towers, Offshore Platforms, Oilfield Tanks, etc

Indirect exposure through sales to pipe making customers

Two of top ten customers are major energy pipe producers

Indirect exposure through suppliers of equipment to

operators in energy sector

Construction equipment, transportation (rail and barge)

7

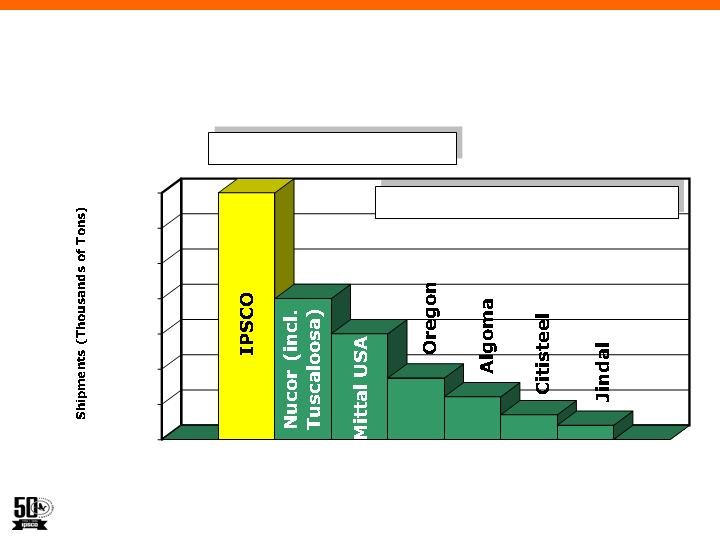

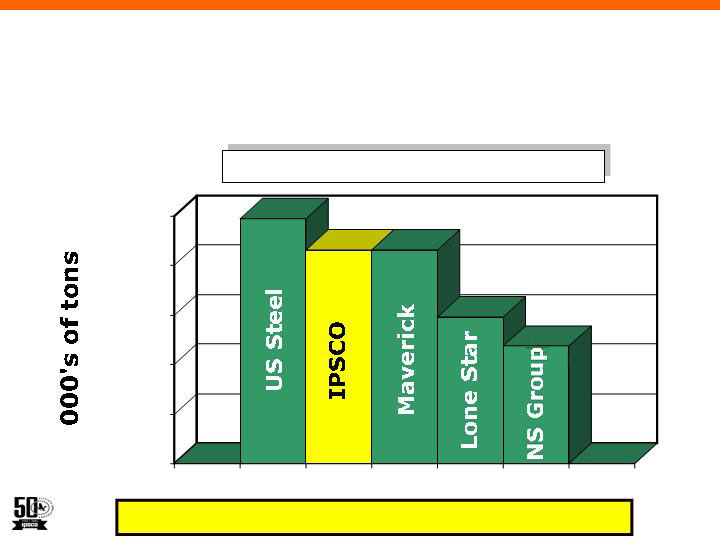

Top Plate Producer in North America

Full Year 2004

Oregon/Jindal = No/partial melt

Top 3 > 75% of shipments

Source: Estimated from Company filings & First River

Note: Includes Plate in Coil Form

Source: Estimated from Company filings & First River

0

500

1,000

1,500

2,000

2,500

3,000

3,500

8

Plate Consumers – Late-Cycle Performers

9

Plate Production is Cost

Competitive Globally

IPSCO utilizes latest technology

North America mills relative to other

nations have availability and cost

advantage to scrap

Man-hours per ton are best-in-class

10

Growth Driver: Expansion of Value

Add Plate Products

Normalized Plate

Quench Temper Plate

Heavier Gauge Plate

Higher Strength As Rolled Plate

Blast & Painted Plate

11

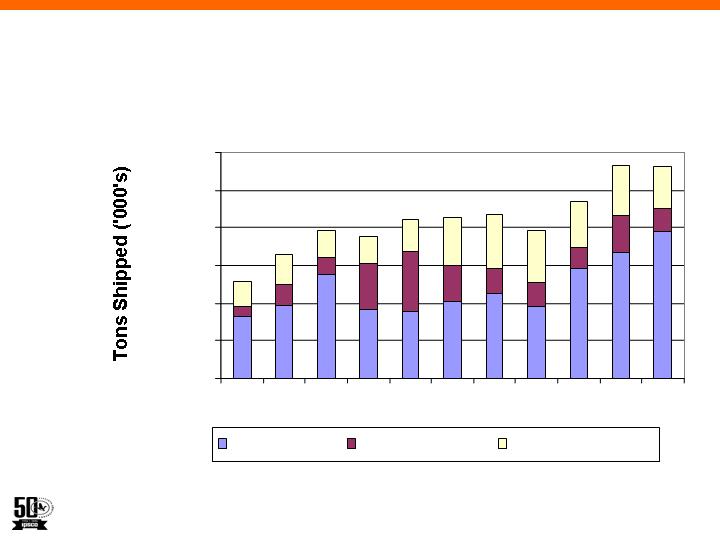

Strong Position in North American Tubes

Top 3 > 40% of North American Capacity

Energy tubulars represent 80% of tubular shipments

0

200

400

600

800

1,000

2004 Energy Tubular Shipments

12

Tubular Shipments

-

200.0

400.0

600.0

800.0

1,000.0

1,200.0

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

Energy Tubulars

LD Energy Tubulars

Non-Energy Tubulars

13

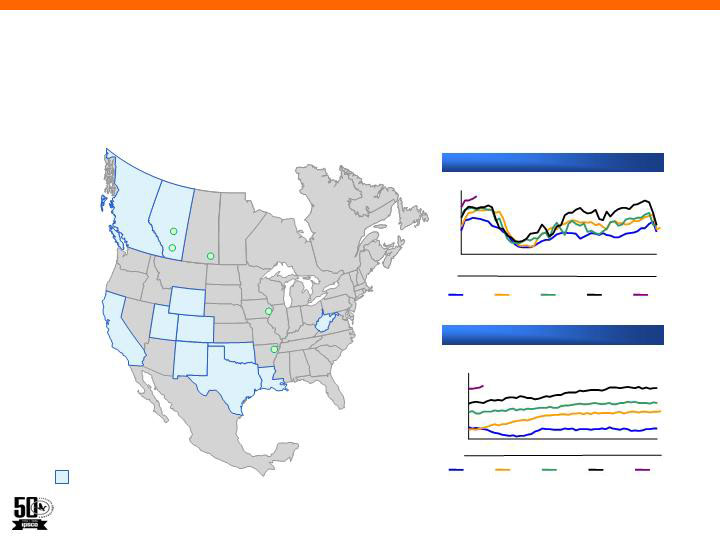

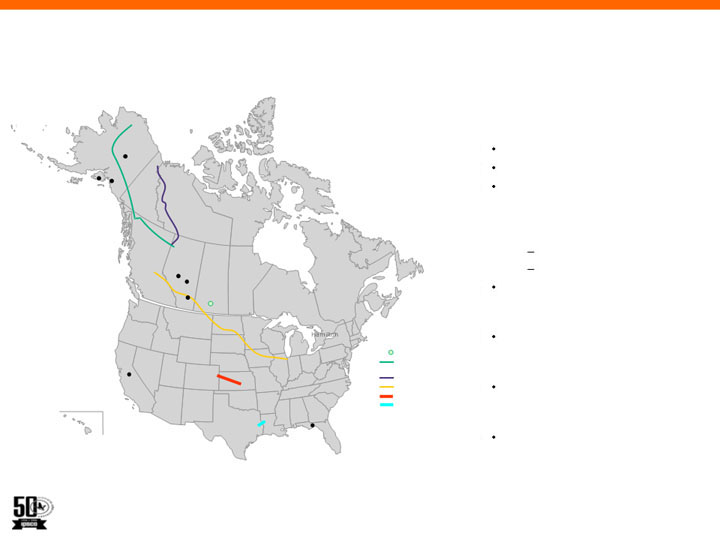

Growth Driver: Energy Tubular

Regina

Red Deer

Camanche

Calgary

Blytheville

= High drilling activity areas

Rig Count – Canada

Rig Count – US

High natural gas prices are expected to drive higher rig counts, which

in turn will drive consumption of energy tubulars

Source – Baker Hughes

700

900

1,100

1,300

1,500

1,700

1

7

12

18

24

29

35

41

46

52

2002

2003

2004

2005

2006

Week

Current (Week 5)

Rig Count =1,513

0

200

400

600

800

1

7

12

18

24

29

35

41

46

52

2002

2003

2004

2005

2006

Week

Current (Week 5)

Rig Count = 727

14

Growth Driver: Large Diameter Pipe

Drivers

Project-based orders

Gaining market share

Need for large pipelines to

bring natural gas from Alaska

and Northern Canada to

markets

Mackenzie Pipeline

Alaska Pipeline

Expanding core competency

with Frontier Pipe Research

Unit

Production facilities located to

capitalize on eventual

construction

Additional infrastructure will

be required around northern

pipelines

2006 looks very promising

Berg

Cheyenne Plains

East Texas Expansion

Prudhoe Bay

Alaska

Fairbanks

Kenai

Valdez

Mackenzie

Delta

Yukon

Northwest

Territories

British

Columbia

Alberta

Edmonton

Saskatchewan

Camrose

Portland

Calgary

Regina

Ontario

Nunavut

Hamilton

NAPA

IPSCO LDP Mill

Alaska Natural Gas

Transportation System

Mackenzie Valley Pipeline

Alliance Pipeline

15

The Outlook For IPSCO’s Pipe Is Strong

High energy prices driving hydrocarbon exploration,

development, transportation together with the

development of alternative energy sources

Exploration and development drilling (OCTG) is at a

high level

Steel intensive oil sands development

Numerous large diameter transmission lines in

development stage:

Oil from Alberta to markets on West Coast or US refineries

Multiple transmission lines in the US

The Northern lines

16

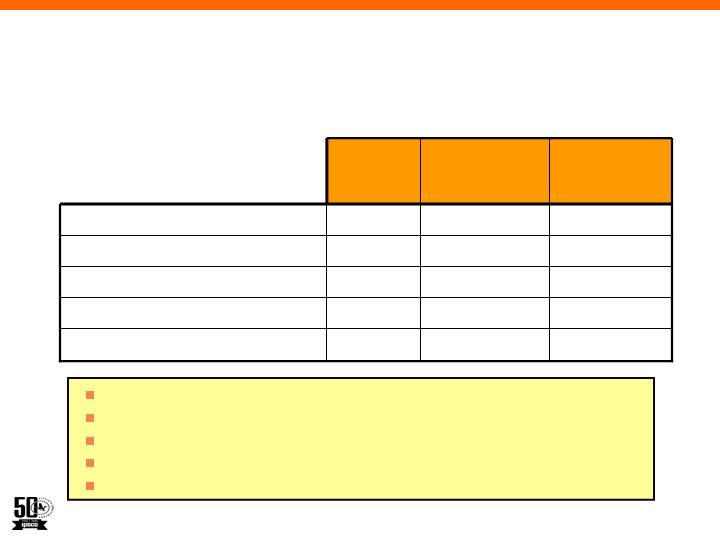

Full Year 2005

Operating Performance

+38

$8.69

$11.96

Diluted EPS

+29

455

586

Net Income

+43

619

884

Income Before Tax

+36

663

898

Operating Income

+20

$2,531

$3,033

Sales

B/(W)

% Chg.

2004

2005

Fourth consecutive record year of sales and production

Record operating profit per ton of $259

Record full year earnings

Record coil and plate production of 3.4M tons

Record energy tubular shipments of 775,000 tons

$ millions except EPS

17

Industry-Leading Profitability

* Full Year 2004, Q4 2005 and Full Year 2005

Include Benefit Corridor and other charges

Operating Income % to Sales

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

Algoma

Dofasco

U.S. Steel

AK

Mittal

IPSCO

Steel

Dynamics

Nucor

Maverick

LoneStar

NS Group

Grant

Prideco

Full Year 2004

Q1 2005

Q2 2005

Q3 2005

Q4 2005

Full Year 2005

l-------------------Integrated---------------------l

l-----------Mini-mills------------l

l----------------Tubular---------------l

*

18

* Full Year 2004, Q4 2005 and Full Year 2005

Include Benefit Corridor and other charges

Integrated

Mini-mills

Industry-Leading Profitability

Operating income per ton

-$50

$0

$50

$100

$150

$200

$250

$300

Algoma

Dofasco

U.S. Steel

AK *

IPSCO

Steel Dynamics

Nucor

Full Year 2004

Q1 2005

Q2 2005

Q3 2005

Q4 2005

Full Year 2005

19

Employee Incentives Aligned

with Shareholder Interest

Incentives based on

productivity, safety, and/or

corporate profitability

All Other Employees

Rewarded for achieving

Budget Goals and Return on

Equity

Key Managers

Rewarded for Return on

Capital and Performance

Relative to Peers

Senior Officers

20

Growth Strategy: Strategic Capital

Expenditures

Increase Heat Treating Capabilities – Expanding production

capacities in higher value heat treat, quench and tempered pipe in

Calgary, Alberta and plate in Mobile, Alabama

Eliminate Bottlenecks – Rebalancing processes and executing Six

Sigma programs within each facility that will unlock added capacity and

improve asset utilization

Expand Finishing Processes – Investing in new value-added

processes that improve the mix and margins of our product lines

Broaden Product Offerings – Expand pipe diameter offerings in

casing to include larger popular diameters in high collapse grades of

steel

Strategic Synergies – Invest in projects that create synergies with our

core business strategies

21

Outlook

Believe end-user demand for steel mill products will

remain relatively stable in 2006

Expect high oil and gas prices will continue to drive high

rig counts and demand for OCTG products

Expect spiral pipe mill will run at near capacity

throughout 2006

Anticipate that higher costs of steel making inputs will

result in some margin compression in 1Q06

22

Conclusion

IPSCO:

Is Globally Competitive on cost and quality

Has Significant Market Share in the plate and pipe

markets it serves with complimentary product lines

Leads in New Technologies necessary to make value-

added steel and energy pipe for the oil & gas industry

Employs a “Steel Short” strategy across

complementary product lines which enables IPSCO to

optimize production and profitability

Possesses Financial Flexibility to support an

opportunistic expansion/acquisition strategy

Positioned to outperform our peers through the cycle -

creating long-term SHAREHOLDER VALUE

23

Thank You

David Sutherland

President and Chief Executive Officer

Dave Sutherland has been President and CEO of IPSCO Inc. since January, 2002. He

joined IPSCO in 1977. Early in his career he held senior managerial positions in the

staff areas of Employee and Industrial Relations in Regina. In April, 2000 Sutherland

moved to the company’s newly formed operational headquarters in Lisle, Illinois, a

suburb of Chicago. He was promoted to Executive Vice President and Chief Operating

Officer in April, 2001, and to President and CEO just nine months later.

Dave Sutherland’s IPSCO career has seen him work in all aspects of the company’s

business – steel, tubulars, and coil processing. He has held important line and staff

positions and has been deeply involved in both manufacturing and sales. During Dave

Sutherland’s tenure with IPSCO the company has grown from a relatively small

Western Canadian steel and pipe company to a NAFTA – based bi-national multi

location developer and producer of high quality steel and tubular products. IPSCO sales

have increased over 360% since 1997 to nearly $2.5 billion US in 2004.

In addition to his broad experience in all aspects of IPSCO’s business, Dave Sutherland

possesses a Bachelor of Commerce degree from the University of Saskatchewan and a

Masters of Business Administration from the Katz Graduate School of Business at the

University of Pittsburgh.

Mr. Sutherland also holds directorships with the Steel Manufacturers Association (SMA)

where he is Treasurer, the American Iron & Steel Institute (AISI) where he is the Vice

Chair, the Canadian Steel Producers Association (CSPA) where he is Chair, the

International Iron & Steel Institute (IISI), National Association of Manufacturers (NAM)

and the C.D. Howe Institute. He is a member of the Canadian Council of Chief

Executives and of the Council’s North American Security and Prosperity Initiative.

25

Thomas Filstrup

Director of Investor Relations

Mr. Filstrup joined IPSCO in August 2005 after more than 20 years of investor

relations and financial experience with Whirlpool Corporation, where he was most

recently Director, Investor Relations.

Mr. Filstrup joined Whirlpool at its corporate headquarters in Benton Harbor,

Michigan in 1983 and held various positions in the internal audit department. In

1988 Mr. Filstrup was named Director of Investor Relations where he developed

Whirlpool’s first investor relations marketing program. From 1988 to 1997 Mr.

Filstrup was also responsible for managing the assets of the company’s $2 billion

Pension and 401(k) plans. Prior to joining Whirlpool, he was self-employed and

owned and operated three restaurants in the Austin, Texas area.

Mr. Filstrup earned his MBA from Northwestern University and his B.S. in

Mechanical Engineering from the University of Michigan. He has been active with

the National Investor Relations Institute (NIRI) as both a member of the National

Board of Directors and Chair of the Audit Committee. Mr. Filstrup is also a

member of the NIRI Senior Roundtable and MAPI Investor Relations Council.

26