driving

NEW LEVELS OF

At CSB, we’re responsive to the fast changing landscape of channel delivery options. We are committed to ensuring that customers can bank with us in the ways they prefer. During 2014, the CSB team pictured above conducted significant research and developed important insights and strategies to reachnew levels of success and customer service in our markets.

Virtual Channel Development Team (vCDT) members shown above. Standing, Left to Right: Jennifer Deam, Brett Gallion, Alyssa Waller and Marc Harvey. Seated, Left to Right: Molly Mohr and Misty Obringer.

2014 FINANCIAL HIGHLIGHTS

| | | | | | | | | | | | |

| FOR THE YEAR ENDED DECEMBER 31 | | 2014 | | | 2013 | | | % CHANGE | |

| |

| (Dollars in thousands, except per share data) | | | | | | | | | |

| | | |

CONSOLIDATED RESULTS | | | | | | | | | | | | |

Net interest income | | $ | 19,927 | | | $ | 18,883 | | | | 6 | % |

Net interest income – fully taxable-equivalent (“FTE”) basis | | | 20,212 | | | | 19,190 | | | | 5 | |

Noninterest income | | | 4,250 | | | | 4,318 | | | | -2 | |

Provision for loan losses | | | 643 | | | | 840 | | | | -23 | |

Noninterest expense | | | 15,082 | | | | 14,848 | | | | 2 | |

Net income | | | 5,884 | | | | 5,240 | | | | 12 | |

| | | |

AT YEAR-END | | | | | | | | | | | | |

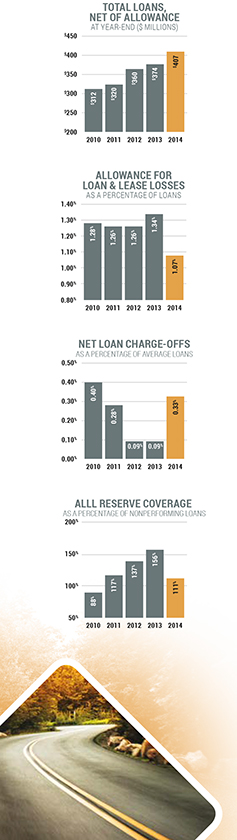

Loans, net | | $ | 406,522 | | | $ | 374,040 | | | | 9 | % |

Assets | | | 620,981 | | | | 596,465 | | | | 4 | |

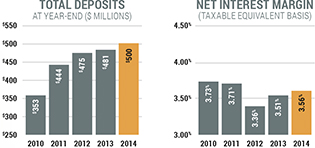

Deposits | | | 500,075 | | | | 480,933 | | | | 4 | |

Shareholders’ equity | | | 57,450 | | | | 52,411 | | | | 10 | |

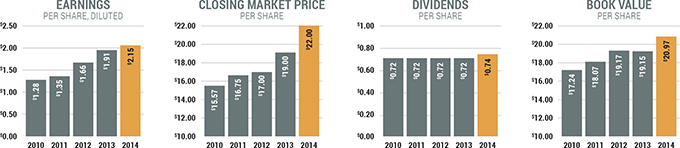

Cash dividends declared | | | 0.74 | | | | 0.72 | | | | 3 | |

Book value | | | 20.97 | | | | 19.15 | | | | 10 | |

Tangible book value | | | 19.02 | | | | 17.15 | | | | 11 | |

Market price | | | 22.00 | | | | 19.00 | | | | 16 | |

Basic and diluted earnings per share | | | 2.15 | | | | 1.91 | | | | 13 | |

| | | |

FINANCIAL PERFORMANCE | | | | | | | | | | | | |

Return on average assets | | | 0.97 | % | | | 0.90 | % | | | | |

Return on average equity | | | 10.60 | | | | 9.93 | | | | | |

Net interest margin, FTE | | | 3.56 | | | | 3.51 | | | | | |

Efficiency ratio | | | 61.46 | | | | 63.01 | | | | | |

| | | |

CAPITAL RATIOS | | | | | | | | | | | | |

Risk-based capital: | | | | | | | | | | | | |

Tier 1 | | | 12.51 | % | | | 12.31 | % | | | | |

Total | | | 13.56 | | | | 13.56 | | | | | |

Leverage | | | 8.51 | | | | 8.21 | | | | | |

2014 Report to Shareholders | CSB Bancorp, Inc. 3

LETTER TO SHAREHOLDERS

DEAR FELLOW SHAREHOLDER:

2014 was another year of growth, improved financial performance and progress in key strategic initiatives. We are larger than we have ever been, generating record income, and building forward momentum in our markets.

The Company’s average balance sheet size exceeded $600 million for the first time in its history. Net income of $5.9 million established a third consecutive record high. Our technology and talent development efforts continue to increase our effectiveness in the marketplace. In short, the CSB team is actively engaged in supporting our vision of building a company of enduring greatness.

CSB’s stock delivered a total return of 20% during 2014, including dividend reinvestment and price appreciation. Our dividend remains very attractive, with an average yield of 3.67% when dividing total cash dividends paid by the average 2014 daily closing stock price. The dividend yield has been above 3.5% since before the financial crisis of 2007-08 and remains substantially stronger than state and national averages for financial stocks. Dividends are one reflection of our commitment to work hard at continually enhancing shareholder value.

HOW WE DO BUSINESS

Our business model remains community centric. The rural and urban areas in which we operate are at the core of our mission and strategy. Everything we do is intended in some way to enhance the well-being of these communities. We provide products and services that help customers accomplish their financial goals. We seek, hire and grow leadership from within the local markets. We keep the interests of our shareholders, many of whom are local investors, in mind as we conduct our operations.

Our six core values continue to guide our efforts. Profit Responsibility, Customer Service, Valued Employees, Honesty and Integrity, Enjoyment of Life and the privilege to work in the communities in which we live, and Growth as part of the lifeblood of our future provide the time-tested framework for all that we do. As the industry continues to change, these core values will continue to guide our journey.

We have built a strong culture of effective risk management and compliance to sustain the safety and soundness of the Bank. We diligently focus on protecting our customers from cybersecurity threats and fraud risks, as well as conducting our operations in accordance with increasing regulatory requirements. We continually evaluate our policies and procedures, systems and technology as we work to reduce risks to our customers and protect the reputation and trust that we have established.

MARKETS

Most of our business activities are conducted in Holmes, Tuscarawas, Wayne and Stark counties of Ohio. These markets exhibit relatively stable populations, a wide range of manufacturing, distribution, service and agriculture enterprises, and solid educational and advancement opportunities for citizens.

The economy in each of these counties has been slowly expanding for several years. Business investments are increasing, and home prices and construction levels are generally improving. Unemployment rates have declined to levels below those that existed prior to the severe recession of 2007-2009, and are presently below U.S. and Ohio average rates. We are fortunate to be able to call these markets home.

OVERVIEW OF BANKING ACTIVITY

Our business model provides effective intermediary services that facilitate the flow of funds within the communities we serve. We safeguard deposit and investment monies entrusted to us, we put a significant amount of depositor funds to work by lending prudently in the broader community, and we provide access to reliable payment channels for debit and credit card processing, internet and mobile banking and check clearing.

Lending is the primary revenue generating activity in our business model, accounting for 71% of gross revenue in the past year. As a commercial bank, we provide loans to businesses and individuals alike. Average loan balances increased 8% during the year to

4 2014 Report to Shareholders | CSB Bancorp, Inc.

LETTER TO SHAREHOLDERS

more than $400 million in average loans outstanding. Commercial real estate loans, many of which reflect owner-occupied businesses, comprised about 34% of our outstanding loan balances at the end of the year, while business loans and home residence loans each comprised about 30% of our loan portfolio. This mix has been little-changed in recent years, and each of these major categories of average loan balances grew by more than 5% during 2014.

Income from our securities portfolio amounted to 11% of revenue in 2014. Service charges, interchange income on card transactions, and trust and brokerage revenue accounted for 5%, 4% and 3% of revenues, respectively.

Average deposit balances increased for the eighth consecutive year, growing by 2% and establishing a sixth consecutive high water mark. A little over one-fourth of our total deposits are in non-interest bearing accounts, largely business related with the remainder in savings, time deposits and interest-bearing demand accounts.

| | | | |

SENIOR MANAGEMENT |

| STEVEN BAILEY | | PAULA MEILER | | EDDIE STEINER |

| Executive Vice President, | | Senior Vice President, | | President, |

| Chief Operations/ | | Chief Financial Officer | | Chief Executive Officer |

| Chief Information Officer | | | | |

TRENDS IN THE INDUSTRY

The financial services sector is undergoing fairly significant changes with a number of macro factors at play. New adaptations of technology for banking and payments processing and new forms of competition are all having major impact on the banking landscape. Consumers are increasingly demonstrating a preference for direct electronic access to financial services and the omnipresent mobile device appears poised to become a primary banking channel. A complex and active regulatory climate requires significant resource utilization. Data integrity and the protection of sensitive customer information have become primary concerns and are requiring increased attention and resources.

We believe the above factors create opportunities for us to grow and strengthen our position in the marketplace. Maintaining financial strength and stability are requisite to thrive in such circumstances and we carefully steward our capital, liquidity, credit quality and expense management in order to maintain the base fitness required to respond to changing conditions and seize opportunities.

CHANNEL DELIVERY

We continue to work at enhancing our customers’ experience. We recognize the fundamental importance of providing services in ways that customers find most convenient. Some customers highly value in-person transactions at our retail locations. Other customers prefer one or more electronic channels to handle transactions, such as our website or mobile banking applications. Our commitment is to provide noticeably different service The CSB Way regardless of which delivery channel a customer prefers or uses for any particular interaction. We are working toward a consistent CSB look and feel across all channels of customer engagement, whether in person or by digital means. Our customer service call center is one example of a channel that we significantly enhanced over the past year. These CSB team members are shining stars when it comes to customer service.

2014 Report to Shareholders | CSB Bancorp, Inc. 5

LETTER TO SHAREHOLDERS

LEADERSHIP DEVELOPMENT

Perpetuating meaningful contributions to the well-being of the communities we serve relies on the continuous development of CSB’s outstanding employees. For the past four years, we have devoted considerable energy to reengineering our leadership development initiatives. Our leadership program is guided by our training board and administered by an in-house team of training and professional development staff. We supplement these efforts with select use of outside leadership development programs and could not be more pleased with the results to date.

IN APPRECIATION

For more than 35 years, Dr. Daniel J. Miller has served on CSB’s Board of Directors. His market and business knowledge, his steadfast commitment to the greater Holmes County area, and his counsel have been invaluable in helping the Bank grow assets fifteen fold during his tenure. Dan is retiring from the CSB Board as of our April 22, 2015 annual meeting. It is with deep appreciation and gratitude that we thank Dan for his contributions.

Collectively, CSB’s employees strive to provide excellence in financial services to each customer. The team’s considerable talent, commitment and adaptability bode well for the continued success of the Company. We are proud of their accomplishments in helping make the Company what it is today and what it will be tomorrow.

To our shareholders, who help provide capital to sustain our mission, we continue to pledge attentiveness to the responsibilities that we have on your behalf. Thank you for your support.

| | | | |

| |  | |  |

| | EDDIE STEINER | | JOHN WALTMAN |

| | President and | | Chairman of the |

| | Chief Executive Officer | | Board of Directors |

BOARD OF DIRECTORS

| | | | | | | | |

Standing, Left to Right |

| | | | |

| J. THOMAS LANG | | RONALD E. HOLTMAN | | EDDIE L. STEINER | | ROBERT K. BAKER | | JOHN R. WALTMAN |

| Veterinarian, | | Attorney, Of Counsel, | | President, | | Co-Owner and Controller, | | Attorney, Of Counsel, |

| Dairy Farmer, | | Logee, Hostetler, | | Chief Executive Officer, | | Bakerwell, Inc. | | Critchfield, Critchfield |

| Spring Hill Farms, Inc. | | Stutzman & Lehman | | CSB Bancorp, Inc. | | | | & Johnston |

| | | | | | | | Chairman, |

| | | | | | | | CSB Bancorp, Inc. |

|

Seated, Left to Right |

| | | | | |

| | DANIEL J. MILLER | | | | JEFFERY A. ROBB, SR. | | |

| | Retired Physician, | | | | President, | | |

| | East Holmes Family Care, Inc. | | Robb Companies, Inc. | | |

| | | | |

| | Chairman of the Board, | | | | | | |

| | Dutchman Hospitality Group, Inc. | | | | |

2014 Report to Shareholders | CSB Bancorp, Inc. 7

2014 FINANCIAL REVIEW

INTRODUCTION

CSB Bancorp, Inc. (the “Company” or “CSB”) was incorporated under the laws of the State of Ohio in 1991 and is a registered bank holding company. The Company’s wholly-owned subsidiaries are The Commercial and Savings Bank (the “Bank”) and CSB Investment Services, LLC which is inactive. The Bank is chartered under the laws of the State of Ohio and was organized in 1879. The Bank is a member of the Federal Reserve System, with deposits insured by the Federal Deposit Insurance Corporation, and its primary regulators are the Ohio Division of Financial Institutions and the Federal Reserve Board.

The Company, through the Bank, provides retail and commercial banking services to its customers including checking and savings accounts, time deposits, cash management, safe deposit facilities, personal loans, commercial loans, real estate mortgage loans, installment loans, IRAs, night depository facilities and trust and brokerage services. Its customers are located primarily in Holmes, Tuscarawas, Wayne, Stark and portions of surrounding counties in Ohio.

In 2014, the Company’s market area demonstrated increasing economic activity following five years of modest gains. Unemployment levels in Holmes County, reported at 2.9% in December 2014, have generally been among the lowest in the State of Ohio, while the balance of the Company’s market area reported unemployment levels below the state average for 2014 and 2013. Residential real estate property values have slowly recovered with low mortgage rates and high affordability. Auto sales also grew, helped by job growth, available financing and the near record age of existing vehicle stock. Ohio’s growth activity continues to be reported in manufacturing and energy-related industries. If oil prices were to experience a sustained decline, mining and manufacturing jobs in the oil and gas business, which had been expanding in the previous two years may decline. The Company’s market is adjacent to areas of primary shale activity.

FORWARD-LOOKING STATEMENTS

Certain statements contained in Management’s Discussion and Analysis of Financial Condition and Results of Operations are not related to historical results, but are forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These statements involve a number of risks and uncertainties. Any forward-looking statements made by the Company herein and in future reports and statements are not guarantees of future performance, and actual results may differ materially from those in forward-looking statements because of various risk factors as discussed in this annual report and the Company’s Annual Report on Form 10-K. The Company does not undertake, and specifically disclaims, any obligation to publicly release the result of any revisions to any forward-looking statements to reflect the occurrence of unanticipated events or circumstances after the date of such statements.

8 2014 Report to Shareholders | CSB Bancorp, Inc.

2014 FINANCIAL REVIEW

SELECTED FINANCIAL DATA

The following table sets forth certain selected consolidated financial information:

| | | | | | | | | | | | | | | | | | | | |

(Dollars in thousands, except per share data) | | 2014 | | | 2013 | | | 2012 | | | 2011 | | | 2010 | |

| |

| | | | | |

Statements of income: | | | | | | | | | | | | | | | | | | | | |

Total interest income | | $ | 21,656 | | | $ | 21,138 | | | $ | 20,584 | | | $ | 20,018 | | | $ | 20,390 | |

Total interest expense | | | 1,729 | | | | 2,255 | | | | 2,978 | | | | 3,678 | | | | 4,820 | |

| | | | | | | | | | | | | | | | | | | | |

Net interest income | | | 19,927 | | | | 18,883 | | | | 17,606 | | | | 16,340 | | | | 15,570 | |

Provision for loan losses | | | 643 | | | | 840 | | | | 823 | | | | 950 | | | | 1,235 | |

| | | | | | | | | | | | | | | | | | | | |

Net interest income after provision for loan losses | | | 19,284 | | | | 18,043 | | | | 16,783 | | | | 15,390 | | | | 14,335 | |

Noninterest income | | | 4,250 | | | | 4,318 | | | | 4,204 | | | | 3,508 | | | | 3,275 | |

Noninterest expense | | | 15,082 | | | | 14,848 | | | | 14,450 | | | | 13,609 | | | | 12,546 | |

| | | | | | | | | | | | | | | | | | | | |

Income before income taxes | | | 8,452 | | | | 7,513 | | | | 6,537 | | | | 5,289 | | | | 5,064 | |

Income tax provision | | | 2,568 | | | | 2,273 | | | | 1,990 | | | | 1,602 | | | | 1,568 | |

| | | | | | | | | | | | | | | | | | | | |

Net income | | $ | 5,884 | | | $ | 5,240 | | | $ | 4,547 | | | $ | 3,687 | | | $ | 3,496 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Per share of common stock: | | | | | | | | | | | | | | | | | | | | |

Basic income per share | | $ | 2.15 | | | $ | 1.91 | | | $ | 1.66 | | | $ | 1.35 | | | $ | 1.28 | |

Diluted income per share | | | 2.15 | | | | 1.91 | | | | 1.66 | | | | 1.35 | | | | 1.28 | |

Dividends | | | 0.74 | | | | 0.72 | | | | 0.72 | | | | 0.72 | | | | 0.72 | |

Book value | | | 20.97 | | | | 19.15 | | | | 19.17 | | | | 18.07 | | | | 17.24 | |

Average basic common shares outstanding | | | 2,737,636 | | | | 2,736,473 | | | | 2,734,889 | | | | 2,734,799 | | | | 2,734,799 | |

Average diluted common shares outstanding | | | 2,739,078 | | | | 2,738,477 | | | | 2,735,141 | | | | 2,734,838 | | | | 2,734,799 | |

| | | | | |

Year-end balances: | | | | | | | | | | | | | | | | | | | | |

Loans, net | | $ | 406,522 | | | $ | 374,040 | | | $ | 360,000 | | | $ | 320,100 | | | $ | 311,616 | |

Securities | | | 143,038 | | | | 151,535 | | | | 134,754 | | | | 128,489 | | | | 80,667 | |

Total assets | | | 620,981 | | | | 596,465 | | | | 586,900 | | | | 551,233 | | | | 457,056 | |

Deposits | | | 500,075 | | | | 480,933 | | | | 475,443 | | | | 443,553 | | | | 353,491 | |

Borrowings | | | 61,580 | | | | 61,130 | | | | 56,664 | | | | 56,234 | | | | 54,927 | |

Shareholders’ equity | | | 57,450 | | | | 52,411 | | | | 52,453 | | | | 49,429 | | | | 47,154 | |

| | | | | |

Average balances: | | | | | | | | | | | | | | | | | | | | |

Loans, net | | $ | 400,876 | | | $ | 369,889 | | | $ | 338,441 | | | $ | 314,670 | | | $ | 309,121 | |

Securities | | | 145,065 | | | | 138,976 | | | | 132,567 | | | | 93,851 | | | | 77,967 | |

Total assets | | | 604,605 | | | | 581,150 | | | | 564,875 | | | | 471,329 | | | | 445,649 | |

Deposits | | | 479,330 | | | | 468,395 | | | | 453,526 | | | | 367,865 | | | | 334,073 | |

Borrowings | | | 67,657 | | | | 57,882 | | | | 57,735 | | | | 52,717 | | | | 62,951 | |

Shareholders’ equity | | | 55,529 | | | | 52,787 | | | | 51,384 | | | | 48,674 | | | | 47,081 | |

| | | | | |

Select ratios: | | | | | | | | | | | | | | | | | | | | |

Net interest margin, tax equivalent basis | | | 3.56 | % | | | 3.51 | % | | | 3.36 | % | | | 3.71 | % | | | 3.73 | % |

Return on average total assets | | | 0.97 | | | | 0.90 | | | | 0.80 | | | | 0.78 | | | | 0.78 | |

Return on average shareholders’ equity | | | 10.60 | | | | 9.93 | | | | 8.85 | | | | 7.57 | | | | 7.43 | |

Average shareholders’ equity as a percent of average total assets | | | 9.18 | | | | 9.08 | | | | 9.10 | | | | 10.33 | | | | 10.56 | |

Net loan charge-offs as a percent of average loans | | | 0.33 | | | | 0.09 | | | | 0.09 | | | | 0.28 | | | | 0.40 | |

Allowance for loan losses as a percent of loans at year-end | | | 1.07 | | | | 1.34 | | | | 1.26 | | | | 1.26 | | | | 1.28 | |

Shareholders’ equity as a percent of total year-end assets | | | 9.25 | | | | 8.79 | | | | 8.94 | | | | 8.97 | | | | 10.32 | |

Dividend payout ratio | | | 34.42 | | | | 37.60 | | | | 43.30 | | | | 53.40 | | | | 56.32 | |

2014 Report to Shareholders | CSB Bancorp, Inc. 9

2014 FINANCIAL REVIEW

RESULTS OF OPERATIONS

Net Income

CSB’s 2014 net income was $5.9 million compared to $5.2 million for 2013, representing an increase of 12%. Basic and diluted earnings per share were $2.15, up 13% from the prior year. The increased net income improved the return on average assets to 0.97% in 2014 from 0.90% in 2013 and return on average equity rose to 10.60% in 2014 from 9.93% in 2013.

Net income for 2013 was $5.2 million while basic and diluted earnings per share were $1.91, as compared to $4.5 million or $1.66 per share, for the year ended December 31, 2012. Net income increased 15% during 2013 as compared to 2012, due primarily to a $1.3 million increase in total net interest income and a $114 thousand increase in noninterest income. Partially offsetting the higher revenue were increases in noninterest expenses and federal income taxes. Return on average assets was 0.90% in 2013 compared to 0.80% in 2012, and return on average shareholders’ equity was 9.93% in 2013 as compared to 8.85% in 2012.

Net Interest Income

| | | | | | | | | | | | |

| (Dollars in thousands) | | 2014 | | | 2013 | | | 2012 | |

| |

Net interest income | | $ | 19,927 | | | $ | 18,883 | | | $ | 17,606 | |

Taxable equivalent1 | | | 285 | | | | 307 | | | | 290 | |

| | | | | | | | | | | | |

Net interest income, fully taxable equivalent | | $ | 20,212 | | | $ | 19,190 | | | $ | 17,896 | |

| | | | | | | | | | | | |

Net interest yield | | | 3.51 | % | | | 3.46 | % | | | 3.31 | % |

Taxable equivalent adjustment1 | | | 0.05 | | | | 0.05 | | | | 0.05 | |

| | | | | | | | | | | | |

Net interest yield-taxable equivalent | | | 3.56 | % | | | 3.51 | % | | | 3.36 | % |

| | | | | | | | | | | | |

1Taxable equivalent adjustments have been computed assuming a 34% tax rate.

Net interest income is the largest source of the Company’s revenue and consists of the difference between interest income generated on earning assets and interest expense incurred on liabilities (deposits and short-term and long-term borrowings). Volumes, interest rates and composition of interest-earning assets and interest-bearing liabilities affect net interest income.

Net interest income increased $1.0 million or 6%, in 2014 compared to 2013, partially due to a 4% increase in average earning assets, and a favorable mix of increased average loan balances and decreased cash balances. Additionally, the net interest margin increased to 3.51%, from 3.46% last year. The margin improvement was primarily due to lower funding costs resulting from a 2% increase in total average deposits, with average balance increases in lower cost demand, savings and maturing time deposits repricing at lower rates. Net discount and accretion of purchase accounting adjustments for loans, time deposits and borrowings acquired decreased the net interest margin by 1 basis point in 2014 after having improved the net interest margin by 5 basis points during 2013 and 2 basis points in 2012.

Interest income increased $518 thousand or 2% in 2014 compared to 2013 due to the $31 million increase in average loan balances, partially offset by lower yields. Rates decreased on loans and tax exempt asset categories from reduced rates on new and repriced assets due to lending competition and the lower interest rate environment. Repricing of loans and lower rates to quality borrowers caused a decline in loan yields of 28 basis points in 2014 as compared to 2013. The increase in average loan volume helped mitigate the low interest rate environment. In 2014, average loan balances to average gross earning assets rose to 71%, compared to 69% in 2013. Securities yields continued to decline in 2014 with new and reinvestment cash flows being deployed at lower rates.

Interest income increased $554 thousand or 3% in 2013 compared to 2012 due to the $32 million increase in average loan balances, partially offset by lower yields. Rates decreased on all significant earning asset categories from reduced rates on new and repriced assets due to lending competition and the lower interest rate environment. Repricing of loans and lower rates to quality borrowers caused a decline in loan yields of 26 basis points in 2013 as compared to 2012. The increase in average loan volume helped mitigate the low interest rate environment. In 2013, average loan balances to average gross earning assets rose to 69%, compared to 64% in 2012.

Interest expense decreased $526 thousand or 23% in 2014 as compared to 2013 due to decreases in the cost of all categories of interest-bearing liabilities and a continued shift in the liability mix towards less expensive, noninterest-bearing demand deposits and savings accounts. Total average time deposits continue to decline with an emphasis on growing customers with multiple banking relationships, as opposed to single service time deposit customers.

Interest expense decreased $723 thousand or 24% in 2013 as compared to 2012 due to decreases in the cost of all categories of interest-bearing liabilities and a continued shift in the liability mix towards less expensive, noninterest-bearing demand deposits and savings accounts. Total average time deposits continue to decline due to an emphasis on growing customers with multiple banking relationships, as opposed to single service time deposit customers.

10 2014 Report to Shareholders | CSB Bancorp, Inc.

2014 FINANCIAL REVIEW

The following table provides detailed analysis of changes in average balances, yield and net interest income:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | AVERAGE BALANCE SHEETS AND NET INTEREST MARGIN ANALYSIS |

| | | | |

| | | 2014 | | 2013 | | | | 2012 |

| | | |

(Dollars in thousands) | | Average

Balance1 | | | Interest | | | Average

Rate2 | | | | | | Average

Balance1 | | | Interest | | | Average

Rate2 | | | | | | | Average

Balance1 | | | Interest | | | Average

Rate2 |

|

| | | | | | | | | | | | | |

Interest-earning assets | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Federal funds sold | | $ | 546 | | | $ | 1 | | | 0.22% | | | | | | $ | 188 | | | $ | 0 | | | | 0.16 | % | | | | | | $ | 148 | | | $ | 0 | | | 0.12% |

Interest-earning deposits | | | 16,356 | | | | 42 | | | 0.26 | | | | | | | 32,127 | | | | 90 | | | | 0.28 | | | | | | | | 56,422 | | | | 147 | | | 0.26 |

Securities: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Taxable | | | 128,973 | | | | 2,857 | | | 2.22 | | | | | | | 122,314 | | | | 2,572 | | | | 2.10 | | | | | | | | 118,867 | | | | 2,672 | | | 2.25 |

Tax exempt | | | 16,092 | | | | 466 | | | 2.89 | | | | | | | 16,662 | | | | 513 | | | | 3.08 | | | | | | | | 13,700 | | | | 486 | | | 3.55 |

Loans3 | | | 405,973 | | | | 18,290 | | | 4.51 | | | | | | | 374,821 | | | | 17,963 | | | | 4.79 | | | | | | | | 342,868 | | | | 17,279 | | | 5.05 |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total interest-earning assets | | | 567,940 | | | | 21,656 | | | 3.81% | | | | | | | 546,112 | | | | 21,138 | | | | 3.87 | % | | | | | | | 532,005 | | | | 20,584 | | | 3.87% |

Noninterest-earning assets | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Cash and due from banks | | | 13,663 | | | | | | | | | | | | | | 12,911 | | | | | | | | | | | | | | | | 12,399 | | | | | | | |

Bank premises and equipment, net | | | 8,494 | | | | | | | | | | | | | | 9,222 | | | | | | | | | | | | | | | | 8,630 | | | | | | | |

Other assets | | | 19,605 | | | | | | | | | | | | | | 17,837 | | | | | | | | | | | | | | | | 16,268 | | | | | | | |

Allowance for loan losses | | | (5,097 | ) | | | | | | | | | | | | | (4,932 | ) | | | | | | | | | | | | | | | (4,427 | ) | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total assets | | $ | 604,605 | | | | | | | | | | | | | $ | 581,150 | | | | | | | | | | | | | | | $ | 564,875 | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | |

Interest-bearing liabilities | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Demand deposits | | $ | 73,307 | | | | 36 | | | 0.05% | | | | | | $ | 70,648 | | | | 42 | | | | 0.06 | % | | | | | | $ | 63,346 | | | | 50 | | | 0.08% |

Savings deposits | | | 151,822 | | | | 130 | | | 0.09 | | | | | | | 141,638 | | | | 144 | | | | 0.10 | | | | | | | | 135,035 | | | | 230 | | | 0.17 |

Time deposits | | | 129,676 | | | | 1,000 | | | 0.77 | | | | | | | 149,340 | | | | 1,534 | | | | 1.03 | | | | | | | | 163,997 | | | | 2,043 | | | 1.25 |

Borrowed funds | | | 67,657 | | | | 563 | | | 0.83 | | | | | | | 57,882 | | | | 535 | | | | 0.92 | | | | | | | | 57,735 | | | | 655 | | | 1.13 |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total interest-bearing liabilities | | | 422,462 | | | | 1,729 | | | 0.41% | | | | | | | 419,508 | | | | 2,255 | | | | 0.54 | % | | | | | | | 420,113 | | | | 2,978 | | | 0.71% |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Noninterest-bearing liabilities and shareholders’ equity | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Demand deposits | | | 124,525 | | | | | | | | | | | | | | 106,769 | | | | | | | | | | | | | | | | 91,148 | | | | | | | |

Other liabilities | | | 2,089 | | | | | | | | | | | | | | 2,086 | | | | | | | | | | | | | | | | 2,230 | | | | | | | |

Shareholders’ equity | | | 55,529 | | | | | | | | | | | | | | 52,787 | | | | | | | | | | | | | | | | 51,384 | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total liabilities and equity | | $ | 604,605 | | | | | | | | | | | | | $ | 581,150 | | | | | | | | | | | | | | | $ | 564,875 | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Net interest income | | | | | | $ | 19,927 | | | | | | | | | | | | | $ | 18,883 | | | | | | | | | | | | | | | $ | 17,606 | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Net interest margin | | | | | | | | | | 3.51% | | | | | | | | | | | | | | | 3.46 | % | | | | | | | | | | | | | | 3.31% |

Net interest spread | | | | | | | | | | 3.40% | | | | | | | | | | | | | | | 3.33 | % | | | | | | | | | | | | | | 3.16% |

1Average balances have been computed on an average daily basis.

2Average rates have been computed based on the amortized cost of the corresponding asset or liability.

3Average loan balances include nonaccrual loans.

2014 Report to Shareholders | CSB Bancorp, Inc. 11

2014 FINANCIAL REVIEW

The following table compares the impact of changes in average rates and changes in average volumes on net interest income:

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | RATE/VOLUME ANALYSIS OF CHANGES | |

| | | | | | IN INCOME AND EXPENSE1 | |

| | | |

| | | 2014 v. 2013 | | | | | 2013 v. 2012 | |

| | | | | | | |

| | | Net Increase | | | | | | | | | | | Net Increase | | | | | | | |

(Dollars in thousands) | | (Decrease) | | | Volume | | | Rate | | | | | (Decrease) | | | Volume | | | Rate | |

| |

| | | | | | | |

Increase (decrease) in interest income: | | | | | | | | | | | | | | | | | | | | | | | | | | |

Federal funds | | $ | 1 | | | $ | 1 | | | $ | – | | | | | $ | – | | | $ | – | | | $ | – | |

Interest-earning deposits | | | (48 | ) | | | (40 | ) | | | (8 | ) | | | | | (57 | ) | | | (68 | ) | | | 11 | |

Securities: | | | | | | | | | | | | | | | | | | | | | | | | | | |

Taxable | | | 285 | | | | 147 | | | | 138 | | | | | | (100 | ) | | | 72 | | | | (172 | ) |

Tax exempt | | | (47 | ) | | | (16 | ) | | | (31 | ) | | | | | 27 | | | | 91 | | | | (64 | ) |

Loans | | | 327 | | | | 1,403 | | | | (1,076 | ) | | | | | 684 | | | | 1,531 | | | | (847 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

Total interest income change | | | 518 | | | | 1,495 | | | | (977 | ) | | | | | 554 | | | | 1,626 | | | | (1,072 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

Increase (decrease) in interest expense: | | | | | | | | | | | | | | | | | | | | | | | | | | |

Demand deposits | | | (6 | ) | | | 1 | | | | (7 | ) | | | | | (8 | ) | | | 4 | | | | (12 | ) |

Savings deposits | | | (14 | ) | | | 9 | | | | (23 | ) | | | | | (86 | ) | | | 7 | | | | (93 | ) |

Time deposits | | | (534 | ) | | | (152 | ) | | | (382 | ) | | | | | (509 | ) | | | (151 | ) | | | (358 | ) |

Other borrowed funds | | | 28 | | | | 81 | | | | (53 | ) | | | | | (120 | ) | | | 1 | | | | (121 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

Total interest expense change | | | (526 | ) | | | (61 | ) | | | (465 | ) | | | | | (723 | ) | | | (139 | ) | | | (584 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

Net interest income | | $ | 1,044 | | | $ | 1,556 | | | $ | (512 | ) | | | | $ | 1,277 | | | $ | 1,765 | | | $ | (488 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

1Changes attributable to both volume and rate, which cannot be segregated, have been allocated based on the absolute value of the change due to volume and the change due to rate.

Provision For Loan Losses

The provision for loan losses is determined by management as the amount required to bring the allowance for loan losses to a level considered appropriate to absorb probable future net charge-offs inherent in the loan portfolio as of period end. The provision for loan losses was $643 thousand in 2014, $840 thousand for 2013 and $823 thousand for 2012. Lower provision expense in 2014 reflects improving economic conditions which have led to a decrease in classified loans. See “Financial Condition – Allowance for Loan Losses” below for additional discussion and information relative to the provision for loan losses.

Noninterest Income

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | YEAR ENDED DECEMBER 31 | | | | |

| | |

| | | Change from 2013 | | | Change from 2012 | |

| | | | | | | |

(Dollars in thousands) | | 2014 | | | Amount | | | % | | | 2013 | | | Amount | | | % | | | 2012 | |

| |

| | | | | | | |

Service charges on deposit accounts | | $ | 1,269 | | | $ | (80 | ) | | | (5.9 | )% | | $ | 1,349 | | | $ | 44 | | | | 3.4 | % | | $ | 1,305 | |

Trust services | | | 811 | | | | (15 | ) | | | (1.8 | ) | | | 826 | | | | 155 | | | | 23.1 | | | | 671 | |

Debit card interchange fees | | | 910 | | | | 131 | | | | 16.8 | | | | 779 | | | | (18 | ) | | | (2.3 | ) | | | 797 | |

Securities gains | | | 133 | | | | (26 | ) | | | (16.4 | ) | | | 159 | | | | 159 | | | | 100.0 | | | | – | |

Gain on sale of loans, including MSR’s | | | 198 | | | | (149 | ) | | | (42.9 | ) | | | 347 | | | | (244 | ) | | | (41.3 | ) | | | 591 | |

Other | | | 929 | | | | 71 | | | | 8.3 | | | | 858 | | | | 18 | | | | 2.1 | | | | 840 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total noninterest income | | $ | 4,250 | | | $ | (68 | ) | | | (1.6 | )% | | $ | 4,318 | | | $ | 114 | | | | 2.7 | % | | $ | 4,204 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

12 2014 Report to Shareholders | CSB Bancorp, Inc.

2014 FINANCIAL REVIEW

Noninterest income decreased $68 thousand, or 2% in 2014 compared to the same period in 2013. Net gains on sales of mortgage loans including mortgage servicing rights (“MSRs”) decreased 43% due to the continuing slowdown in mortgage refinance activity during 2014. The Bank originated and sold $6 million in mortgage loans in 2014 as compared to the sale of $12 million of loans in 2013. Service charges on deposits which are primarily customer overdraft fees, decreased 6% in 2014, with an 11% decrease in overdraft fees due to increasing health of consumer deposit balances. Trust fees increased 11% as assets under management increased from overall market improvements and customer development initiatives. The average market value of trust assets under management in 2014 was $95 million compared to $86 million in 2013. However, brokerage fees contained within trust services decreased $80 thousand in 2014 contributing to the net decrease of 2%. With interest rates declining during 2014, available-for-sale securities with gains of $133 thousand were sold as net loan demand increased during 2014.

Noninterest income increased $114 thousand, or 3% in 2013 compared to the same period in 2012. Trust and brokerage fees increased 23% as assets under management increased from overall market improvements and customer development initiatives. The average market value of trust assets under management in 2013 was $86 million as compared to $76 million in 2012. Brokerage fees increased $86 thousand in 2013 as customers returned to stock and annuity investments to increase their returns. Service charges on deposits which are primarily customer overdraft fees, increased 3% in 2013 due to growth in deposits. Net gains on sales of mortgage loans including MSRs decreased 41% due to a significant slowdown in mortgage refinance activity during 2013. The Bank originated and sold $12 million in mortgage loans in 2013 as compared to the sale of $20 million of loans in 2012. With historical low interest rates during the first half of 2013, available-for-sale securities with gains of $159 thousand were sold as net loan demand increased.

Noninterest Expenses

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | YEAR ENDED DECEMBER 31 | | | | |

| | |

| | | Change from 2013 | | | Change from 2012 | |

| | | | | | | |

(Dollars in thousands) | | 2014 | | | Amount | | | % | | | 2013 | | | Amount | | | % | | | 2012 | |

| |

| | | | | | | |

Salaries and employee benefits | | $ | 8,321 | | | $ | 60 | | | | 0.7 | % | | $ | 8,261 | | | $ | 301 | | | | 3.8 | % | | $ | 7,960 | |

Occupancy expense | | | 1,014 | | | | (12 | ) | | | (1.2 | ) | | | 1,026 | | | | 1 | | | | 0.1 | | | | 1,025 | |

Equipment expense | | | 715 | | | | (4 | ) | | | (0.6 | ) | | | 719 | | | | 101 | | | | 16.3 | | | | 618 | |

Professional and director fees | | | 725 | | | | 97 | | | | 15.4 | | | | 628 | | | | (186 | ) | | | (22.9 | ) | | | 814 | |

Franchise tax expense | | | 361 | | | | (220 | ) | | | (37.9 | ) | | | 581 | | | | 39 | | | | 7.2 | | | | 542 | |

Marketing and public relations | | | 378 | | | | (17 | ) | | | (4.3 | ) | | | 395 | | | | 3 | | | | 0.8 | | | | 392 | |

Software expense | | | 727 | | | | 197 | | | | 37.2 | | | | 530 | | | | 139 | | | | 35.5 | | | | 391 | |

Debit card expense | | | 421 | | | | 130 | | | | 44.7 | | | | 291 | | | | (40 | ) | | | (12.1 | ) | | | 331 | |

Amortization of intangible assets | | | 130 | | | | (5 | ) | | | (4.4 | ) | | | 135 | | | | (5 | ) | | | (3.6 | ) | | | 140 | |

FDIC insurance | | | 358 | | | | (1 | ) | | | (0.3 | ) | | | 359 | | | | 31 | | | | 9.5 | | | | 328 | |

Branch acquisition expense | | | – | | | | – | | | | – | | | | – | | | | (8 | ) | | | (100.0 | ) | | | 8 | |

Other real estate expenses | | | – | | | | (9 | ) | | | N.M. | | | | 9 | | | | (24 | ) | | | N.M. | | | | 33 | |

Other | | | 1,932 | | | | 18 | | | | (0.2 | ) | | | 1,914 | | | | 46 | | | | 2.2 | | | | 1,868 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total noninterest expenses | | $ | 15,082 | | | $ | 234 | | | | 1.6 | % | | $ | 14,848 | | | $ | 398 | | | | 2.8 | % | | $ | 14,450 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

N.M., not a meaningful value

Noninterest expense increased $234 thousand, or 2% in 2014 compared to 2013. Salaries and employee benefits increased $60 thousand due to base compensation increasing $185 thousand as a result of additional full time employees and annual adjustments. Capitalization of employee costs of loan origination and benefit decreases amounted to $125 thousand. Software expense increased $197 thousand in 2014 due to a full year increase of the cost of new core processing and loan documentation software. Equipment expense decreased $4 thousand in 2014 as compared to 2013. Franchise tax expense decreased $220 thousand in 2014, to $361 thousand, with the implementation of the new Ohio Financial Institutions Tax. Debit card expense increased $130 thousand in 2014, a result of one time charges of $40 thousand to convert to a new third party processor, $26 thousand additional fraud losses and increased customer usage. Professional and director fees increased $97 thousand, a result of the increase in legal fees surrounding loan collections of $118 thousand primarily incurred in the disposition of two commercial loan relationships.

2014 Report to Shareholders | CSB Bancorp, Inc. 13

2014 FINANCIAL REVIEW

Noninterest expense increased $398 thousand, or 3% in 2013 as compared to 2012. Salaries and employee benefits increased $301 thousand due to annual adjustments to compensation of $211 thousand and benefit increases of $90 thousand due to higher payroll taxes and retirement benefits. Software expense rose $139 thousand in 2013 due to the acquisition of new core processing and loan documentation software. Equipment expense increased $101 thousand in 2013 as compared to 2012 with the acquisition of a new core processor, new telephone system and new ATMs in the branch network. Franchise tax expense increased $39 thousand in 2013 to $581 thousand but is expected to decrease in 2014.

Income Taxes

The provision for income taxes amounted to $2.6 million in 2014, $2.3 million in 2013 and $2.0 million in 2012, resulting in an effective rate of 30.4% in 2014, 30.3% in 2013 and 30.4% in 2012. The slight increase in the effective tax rate during 2014 as compared to 2013 is due primarily to increased income.

FINANCIAL CONDITION

Total assets of the Company were $621 million at December 31, 2014, compared to $596 million at December 31, 2013, representing an increase of $25 million, or 4%. Net loans increased $32 million, or 9%, while investment securities decreased $8 million, or 6% and interest-earning deposits with other banks increased $2 million. Deposits increased $19 million, or 4%, while other borrowings from the FHLB increased by $2 million, or 20%.

Securities

Total investment securities decreased $8 million, or 6% to $143 million at year-end 2014. CSB’s portfolio is primarily comprised of agency mortgage-backed securities, other government agencies’ debt, and obligations of state and political subdivisions. Restricted securities consist primarily of FHLB stock.

The Company has no exposure to government-sponsored enterprise preferred stocks, collateralized debt obligations or trust preferred securities. The Company’s municipal bond portfolio consists of both taxable and tax-exempt general obligation and revenue bonds. As of December 31, 2014, $15.9 million, or 87%, held an S&P or Moody’s investment grade rating and $2.4 million or 13% were non-rated. The municipal portfolio includes a broad spectrum of counties, towns, universities and school districts with 98% of the portfolio originating in Ohio and 2% in Pennsylvania. Total gross unrealized security losses within the portfolio were 0.3% of total available-for-sale securities at December 31, 2014, reflecting interest rate fluctuations, not credit downgrades.

During the third quarter 2013, the Company reclassified $39 million of U.S. Agency and U.S. Agency collateralized mortgage-backed obligations from available-for-sale to held-to-maturity. The Company considers the held-to-maturity classification to be more appropriate in a rising interest rate environment as other comprehensive income is no longer negatively impacted by the decline in value on specific bonds. The Company has the ability and the intent to hold the longer-term Agency debt securities and the mortgage-backed securities to maturity. On the date of transfer, the $1.9 million gross unrealized loss became a discount to the carrying value of the bonds while the net of tax unrealized loss remained in shareholders’ equity in other comprehensive income. The effect on interest income of the accretion of the discount on the bonds is basically offset by the amortization of the other comprehensive loss over the life of the bonds.

One of the primary functions of the securities portfolio is to provide a source of liquidity and it is structured such that maturities and cash flows satisfy the Company’s liquidity needs and asset/liability management requirements.

Loans

Total loans increased $32 million, or 8% during 2014. Volume increases were recognized in commercial and commercial real estate loans of $16 million, or 7%, and residential real estate loans of $10 million, or 9%. Construction loans increased $4 million, or 30%. During 2014, business expansion continued in the Company’s newly expanded markets. Aided by low interest rates, commercial and commercial real estate loans continued to increase in 2014.

As investment spreads tightened in the mortgage-backed securities market, the Company developed marketing campaigns for fifteen year, lower fee, fixed-rate, owner occupied loans which drove the $10 million increase in residential real estate loans. Attractive interest rates in the secondary market continued to drive consumer demand for longer-term 1-4 family fixed rate residential mortgages during 2014 and the Company sold $6 million of originated mortgages into the secondary market as compared to $12 million in 2013. This demand for low fixed-rate mortgages included some refinancing of the Company’s in-house mortgage portfolio. Demand for home equity loans flattened in 2014, with balances decreasing $114 thousand as many consumers rewrote their floating rate equity line and first mortgage into a lower rate fixed rate mortgage. Installment lending improved with consumer loans increasing 18% on a year-over-year basis to $7.9 million at December 31, 2014.

14 2014 Report to Shareholders | CSB Bancorp, Inc.

2014 FINANCIAL REVIEW

Management anticipates the Company’s local service areas will continue to exhibit modest economic growth in line with the past three years. Commercial and commercial real estate loans comprise approximately 64% and 65% of the total loan portfolio at year-end 2014 and 2013, respectively. Residential real estate loans increased from 29% to approximately 30% between December 31, 2013 and December 31, 2014. Construction and land development loans remained stable at 4% of the total portfolio between 2013 and 2014. The Company is well within the respective regulatory guidelines for investment in construction development and investment property loans that are not owner occupied.

Most of the Company’s lending activity is with customers primarily located within Holmes, Tuscarawas, Wayne and Stark counties in Ohio. Credit concentrations, including commitments, as determined using North American Industry Classification Codes (NAICS), to the four largest industries compared to total loans at December 31, 2014 included $30 million, or 7% of total loans to lessors of non-residential buildings or dwellings; $19 million, or 5% of total loans to logging, sawmills and timber tract operations; $18 million, or 4% of total loans to lessors of residential real estate and $16 million, or 4% of total loans to borrowers in the hotel, motel and lodging business. These loans are generally secured by real property and equipment, and repayment is expected from operational cash flow. Credit evaluation is based on an evaluation of cash flow coverage of principal and interest payments and the adequacy of the collateral received.

Nonperforming Assets, Impaired Loans and Loans Past Due 90 Days or More

Nonperforming assets consist of nonaccrual loans, loans past due 90 days and still accruing and other real estate acquired through or in lieu of foreclosure. Other impaired loans include certain loans that are internally classified as substandard or doubtful. Loans are placed on nonaccrual status when they become past due 90 days or more, or when mortgage loans are past due as to principal and interest 120 days or more, unless they are both well secured and in the process of collection.

NONPERFORMING ASSETS

| | | | | | | | |

| | | DECEMBER 31 | |

(Dollars in thousands) | | 2014 | | | 2013 | |

| |

| | |

Nonaccrual loans: | | | | | | | | |

Commercial | | $ | 1,071 | | | $ | 84 | |

Commercial real estate | | | 1,734 | | | | 1,108 | |

Residential real estate | | | 863 | | | | 1,042 | |

Construction & land development | | | – | | | | – | |

Loans past due 90 days and still accruing: | | | | | | | | |

Commercial | | | 1 | | | | – | |

Commercial real estate | | | – | | | | 40 | |

Residential real estate | | | 280 | | | | 46 | |

Construction & land development | | | – | | | | 950 | |

| | | | | | | | |

Total nonperforming loans | | | 3,949 | | | | 3,270 | |

Other real estate owned | | | – | | | | – | |

| | | | | | | | |

Total nonperforming assets | | $ | 3,949 | | | $ | 3,270 | |

| | | | | | | | |

Nonperforming assets as a percentage of loans plus other real estate | | | 0.96 | % | | | 0.86 | % |

Allowance for Loan Losses

The allowance for loan losses is maintained at a level considered by management to be adequate to cover loan losses that are currently anticipated based on past loss experience, general economic conditions, changes in mix and size of the loan portfolio, information about specific borrower situations and other factors and estimates which are subject to change over time. Management periodically reviews selected large loans, delinquent and other problem loans and selected other loans. Collectability of these loans is evaluated by considering the current financial position and performance of the borrower, estimated market value of the collateral, the Company’s collateral position in relationship to other creditors, guarantees and other potential sources of repayment. Management forms judgments, which are in part subjective, as to the probability of loss and the amount of loss on these loans as well as other loans taken together. The Company’s Allowance for Loan Losses Policy includes, among other items, provisions for classified loans and a provision for the remainder of the portfolio based on historical data, including past charge-offs.

2014 Report to Shareholders | CSB Bancorp, Inc. 15

2014 FINANCIAL REVIEW

| | | | | | | | |

| ALLOWANCE FOR LOAN LOSSES | | FOR THE YEAR ENDED | |

(Dollars in thousands) | | 2014 | | | 2013 | |

| |

Beginning balance of allowance for loan losses | | $ | 5,085 | | | $ | 4,580 | |

Provision for loan losses | | | 643 | | | | 840 | |

Charge-offs: | | | | | | | | |

Commercial | | | 985 | | | | 149 | |

Commercial real estate | | | 379 | | | | 108 | |

Residential real estate & home equity | | | 27 | | | | 82 | |

Construction & land development | | | – | | | | – | |

Consumer | | | 11 | | | | 48 | |

Deposit accounts | | | 20 | | | | 35 | |

Credit cards | | | – | | | | 6 | |

| | | | | | | | |

Total charge-offs | | | 1,422 | | | | 428 | |

Recoveries: | | | | | | | | |

Commercial | | | 21 | | | | 15 | |

Commercial real estate | | | 8 | | | | – | |

Residential real estate & home equity | | | 25 | | | | 18 | |

Construction & land development | | | – | | | | – | |

Consumer | | | 14 | | | | 50 | |

Deposit accounts | | | 7 | | | | 10 | |

Credit cards | | | – | | | | – | |

| | | | | | | | |

Total recoveries | | | 75 | | | | 93 | |

| | | | | | | | |

Net charge-offs | | | 1,347 | | | | 335 | |

| | | | | | | | |

Ending balance of allowance for loan losses | | $ | 4,381 | | | $ | 5,085 | |

| | | | | | | | |

Net charge-offs as a percentage of average total loans | | | 0.33 | % | | | 0.09 | % |

Allowance for loan losses as a percentage of total loans | | | 1.07 | | | | 1.34 | |

Allowance for loan losses to total nonperforming loans | | | 1.11 | x | | | 1.56 | x |

Components of the allowance for loan losses: | | | | | | | | |

General reserves | | $ | 4,197 | | | $ | 4,301 | |

Specific reserve allocations | | | 184 | | | | 784 | |

| | | | | | | | |

Total allowance for loan losses | | $ | 4,381 | | | $ | 5,085 | |

| | | | | | | | |

The allowance for loan losses totaled $4.4 million, or 1.07%, of total loans at year-end 2014 as compared to $5.1 million, or 1.34% of total loans at year-end 2013. Net charge-offs for 2014 totaled $1.3 million as compared to net charge-offs of $335 thousand in 2013. The majority of the charge-offs were attributed to one commercial relationship which had been specifically reserved for during 2014.

The Company maintains an internal watch list on which it places loans where management’s analysis of the borrower’s operating results and financial condition indicates that the borrower’s cash flows are inadequate to meet its debt service requirements and loans where there exists an increased risk that such a shortfall may occur. Nonperforming loans, which consist of loans past due 90 days or more and nonaccrual loans aggregated $3.9 million, or 1.0% of loans at year-end 2014 as compared to $3.3 million, or 0.9% of loans at year-end 2013. Impaired loans were $9.2 million at year-end 2014 as compared to $10.7 million at year-end 2013. Impaired loans as a percentage of total loans declined from 2013 to 2014 and reflect economic stabilization in the Company’s market area with decreasing unemployment levels. Management has assigned loss allocations to absorb the estimated losses on these impaired loans, and these allocations are included in the total allowance for loan losses balance.

16 2014 Report to Shareholders | CSB Bancorp, Inc.

2014 FINANCIAL REVIEW

Other Assets

Net premises and equipment decreased $404 thousand to $8.3 million at year-end 2014 primarily because depreciation expense exceeded the purchase of equipment and furniture in 2014. There was no other real estate owned at December 31, 2014 or 2013. Bank-owned life insurance of $1 million was purchased on the life of a senior management member during 2013. At December 31, 2014 the Company recognized a net deferred tax asset of $377 thousand as compared to a net deferred tax asset of $1.2 million at December 31, 2013. The change in the Company’s net deferred tax position resulted primarily from the decrease in the net deferred tax asset related to the unrealized loss on securities available for sale.

Deposits

The Company’s deposits are obtained primarily from individuals and businesses located in its market area. For deposits, the Company must compete with products offered by other financial institutions as well as alternative investment options. Demand and savings deposits increased for the year ended 2014, due to focused retail and business banking strategies to obtain more account relationships as well as customers reflecting their preference for shorter maturities.

| | | | | | | | | | | | | | | | |

| | | December 31 | | | Change from 2013 | |

(Dollars in thousands) | | 2014 | | | 2013 | | | Amount | | | % | |

| |

Noninterest-bearing demand | | $ | 139,251 | | | $ | 120,325 | | | $ | 18,926 | | | | 15.7 | % |

Interest-bearing demand | | | 77,725 | | | | 76,327 | | | | 1,398 | | | | 1.8 | |

Traditional savings | | | 84,548 | | | | 76,630 | | | | 7,918 | | | | 10.3 | |

Money market savings | | | 70,788 | | | | 73,307 | | | | (2,519 | ) | | | (3.4 | ) |

Time deposits in excess of $100,000 | | | 43,130 | | | | 42,562 | | | | 568 | | | | 1.3 | |

Other time deposits | | | 84,633 | | | | 91,782 | | | | (7,149 | ) | | | (7.8 | )�� |

| | | | | | | | | | | | | | | | |

Total deposits | | $ | 500,075 | | | $ | 480,933 | | | $ | 19,142 | | | | 4.0 | % |

| | | | | | | | | | | | | | | | |

Other Funding Sources

The Company obtains additional funds through securities sold under repurchase agreements, overnight borrowings from the FHLB or other financial institutions and advances from the FHLB. Short-term borrowings, which consist of securities sold under repurchase agreements, decreased $2 million; while other borrowings, which consist of FHLB advances, increased $2 million as the result of borrowing $5 million in a long-term amortizing advance to partially offset the interest rate risk of booking fifteen-year fixed-rate mortgages.

CAPITAL RESOURCES

Total shareholders’ equity increased to $57.5 million at December 31, 2014 as compared to $52.4 million at December 31, 2013. This increase was primarily due to $5.9 million of net income and $1.2 million other comprehensive income, which were offset by the payment of $2.0 million cash dividends in 2014. The Board of Directors approved a Stock Repurchase Program on July 7, 2005 that would allow the repurchase of up to 10% of the Company’s then-outstanding common shares. Repurchased shares are to be held as treasury stock and would be available for general corporate purposes. At December 31, 2014, approximately forty-one thousand shares could still be repurchased under the current authorized program. No shares were repurchased in 2014 or 2013.

In July 2013, the Federal Reserve adopted final rules effective on January 1, 2015 to implement the Basel III and regulatory capital changes required by the Dodd-Frank Act. These changes will apply to the Company and the Bank. Among other things, the rules include new minimum risk-based and leverage capital requirements for all banking organizations and removal of references to credit ratings. A new capital conservation buffer of 2.5% of risk-weighted assets is being phased-in over a transition period ending January 1, 2019. Failure to maintain the required ratios will restrict or prohibit dividends, share repurchases and discretionary bonuses. Management has evaluated the new rules and their effects on the Company and the Bank, and believes the Company and the Bank will remain “well-capitalized” under the new rules.

Banking regulations have established minimum capital ratios for banks and bank holding companies. Therefore, the Company and the Bank must meet a risk-based capital requirement, which defines two tiers of capital and compares each to the Company’s “risk-weighted assets.” The Company’s assets and certain off-balance-sheet items, such as loan commitments, are each assigned a risk factor such that assets with potentially higher credit risk will require more capital support than assets with lower risk. These regulations require the Company to have a minimum total risk-based capital ratio of 8%, at least half of which must be Tier 1 capital. The Company’s Tier 1 capital is its shareholders’ equity before any unrealized gain or loss on securities available for sale, while total risk-based capital includes Tier 1 capital and a limited amount of the allowance for loan losses. In addition, a bank or bank holding company’s leverage ratio (which for the Company equals its shareholders’ equity before any unrealized gain or loss on securities available-for-sale, divided by average assets) must be maintained at a minimum of 4%. The Company and Bank’s actual and required capital amounts are disclosed in Note 12 to the consolidated financial statements.

2014 Report to Shareholders | CSB Bancorp, Inc. 17

2014 FINANCIAL REVIEW

Dividends paid by the Bank to CSB are the primary source of funds available to the Company for payment of dividends to shareholders and for other working capital needs. The payment of dividends by the Bank to the Company is subject to restrictions by regulatory authorities, which generally limit dividends to current year net income and the prior two years net retained earnings, as defined by regulation. In addition, dividend payments generally cannot reduce regulatory capital levels below the minimum regulatory guidelines discussed above.

LIQUIDITY

| | | | | | | | | | | | | | | | |

| | | December 31 | | | | | | | |

(Dollars in millions) | | 2014 | | | 2013 | | | Change

from 2013 | |

| |

Cash and cash equivalents | | $ | 44 | | | $ | 43 | | | | | | | $ | 1 | |

Unused lines of credit | | | 46 | | | | 42 | | | | | | | | 4 | |

Unpledged securities at fair market value | | | 48 | | | | 42 | | | | | | | | 6 | |

| | | | | | | | | | | | | | | | |

| | $ | 138 | | | $ | 127 | | | | | | | $ | 11 | |

| | | | | | | | | | | | | | | | |

Net deposits and short-term liabilities | | $ | 497 | | | $ | 473 | | | | | | | $ | 24 | |

| | | | | | | | | | | | | | | | |

Liquidity ratio | | | 27.9 | % | | | 26.9 | % | | | | | | | | |

Minimum board approved liquidity ratio | | | 20.0 | % | | | 20.0 | % | | | | | | | | |

Liquidity refers to the Company’s ability to generate sufficient cash to fund current loan demand, meet deposit withdrawals, pay operating expenses and meet other obligations. Liquidity is monitored by CSB’s Asset Liability Committee. The Company was within all Board-approved limits at December 31, 2014 and 2013. Additional sources of liquidity include net income, loan repayments, the availability or borrowings and adjustments of interest rates to attract deposit accounts.

As summarized in the consolidated statements of cash flows, the most significant investing activities for the Company in 2014 included net loan originations of $33 million and the maturities and repayments of securities totaling $45 million, offset by $38 million in securities purchases. The Company’s financing activities included a $19 million increase in deposits, a $2 million decrease in securities sold under agreements to repurchase and a $2 million net increase in FHLB advances.

QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

The most significant market risk to which the Company is exposed is interest rate risk. The business of the Company and the composition of its balance sheet consist of investments in interest-earning assets (primarily loans and securities), which are funded by interest-bearing liabilities (deposits and borrowings). These financial instruments have varying levels of sensitivity to changes in the market rates of interest, resulting in market risk. None of the Company’s financial instruments are held for trading purposes.

The Board of Directors establishes policies and operating limits with respect to interest rate risk. The Company manages interest rate risk regularly through its Asset Liability Committee. The Committee meets on a monthly basis and reviews various asset and liability management information including, but not limited to, the Company’s liquidity position, projected sources and uses of funds, interest rate risk position and economic conditions.

Interest rate risk is monitored primarily through the use of an earnings simulation model. The model is highly dependent on various assumptions, which change regularly as the balance sheet and market interest rates change. The earnings simulation model projects changes in net interest income resulting from the effect of changes in interest rates. The analysis is performed quarterly over a twenty-four month horizon. The analysis includes two balance sheet models, one based on a static balance sheet and one on a dynamic balance sheet with projected growth in assets and liabilities. This analysis is performed by estimating the expected cash flows of the Company’s financial instruments using interest rates in effect at year-end 2014 and 2013. Interest rate risk policy limits are tested by measuring the anticipated change in net interest income over a two-year period. The tests assume a quarterly ramped 100, 200, 300 and 400 basis point increase and a 100 basis point decrease in 2014 in market interest rates as compared to a stable rate environment or base model.

18 2014 Report to Shareholders | CSB Bancorp, Inc.

2014 FINANCIAL REVIEW

The following table reflects the change to interest income for the first twelve month period of the twenty-four month horizon.

Net Interest Income at Risk

| | | | | | | | | | |

| | | December 31, 2014 |

| (Dollars in thousands) | | Change In

Interest Rates

(Basis Points) | | Net

Interest

Income | | Dollar

Change | | Percentage

Change | | Board

Policy

Limits |

| | + 400 | | $ 21,408 | | $ 1,144 | | 5.6% | | ± 25% |

| | + 300 | | 21,082 | | 818 | | 4.0 | | ± 15 |

| | + 200 | | 20,766 | | 502 | | 2.5 | | ± 10 |

| | + 100 | | 20,454 | | 190 | | 0.9 | | ± 5 |

| | 0 | | 20,264 | | – | | – | | |

| | – 100 | | 20,022 | | (242) | | (1.1) | | ± 5 |

| |

| | | December 31, 2013 |

| | + 400 | | $ 20,812 | | $ 962 | | 4.8% | | ± 25% |

| | + 300 | | 20,507 | | 657 | | 3.3 | | ± 15 |

| | + 200 | | 20,217 | | 367 | | 1.8 | | ± 10 |

| | + 100 | | 19,966 | | 116 | | 0.6 | | ± 5 |

| | 0 | | 19,850 | | – | | – | | |

| | – 100 | | 19,644 | | (206) | | (1.0) | | ± 5 |

Management reviews Net Interest Income at Risk with the Board on a periodic basis. The Company was within all Board-approved limits at December 31, 2014 and 2013.

Economic Value of Equity at Risk

| | | | |

| December 31, 2014 |

Change In Interest Rates (Basis Points) | | Percentage Change | | Board Policy Limits |

+ 400 | | 17.7% | | ± 35% |

| + 300 | | 15.7 | | ± 30 |

| + 200 | | 13.0 | | ± 20 |

| + 100 | | 8.3 | | ± 15 |

| – 100 | | (8.8) | | ± 15 |

|

| December 31, 2013 |

+ 400 | | 9.8% | | ± 35% |

| + 300 | | 8.8 | | ± 30 |

| + 200 | | 7.4 | | ± 20 |

| + 100 | | 4.7 | | ± 15 |

| – 100 | | (7.6) | | ± 15 |

2014 Report to Shareholders | CSB Bancorp, Inc. 19

2014 FINANCIAL REVIEW

The economic value of equity is calculated by subjecting the period-end balance sheet to changes in interest rates and measuring the impact of the changes on the values of the assets and liabilities. Hypothetical changes in interest rates are then applied to the financial instruments, and the cash flows and fair values are again estimated using these hypothetical rates. For the net interest income estimates, the hypothetical rates are applied to the financial instruments based on the assumed cash flows.

Management periodically measures and reviews the Economic Value of Equity at Risk with the Board. At December 31, 2014, the market value of equity as a percent of base in a 400 basis point rising rate environment indicates an increase of 17.7%, as compared to an increase of 9.8% as of December 31, 2013. The Company added the review of a -100 basis change in interest rates during 2013 as rates had risen at December 31, 2013 in comparison with 2012. The Company was within all Board-approved limits at December 31, 2014 and 2013.

SIGNIFICANT ASSUMPTIONS AND OTHER CONSIDERATIONS

The above analysis is based on numerous assumptions, including relative levels of market interest rates, loan prepayments and reactions of depositors to changes in interest rates, and should not be relied upon as being indicative of actual results. Furthermore, the analysis does not necessarily contemplate all actions the Company may undertake in response to changes in interest rates.

U.S. Treasury securities, obligations of U.S. Government corporations and agencies and obligations of states and political subdivisions will generally repay at their stated maturity, or if callable prior to their final maturity date. Mortgage-backed security payments increase when interest rates are low and decrease when interest rates rise. Most of the Company’s loans permit the borrower to prepay the principal balance prior to maturity without penalty. The likelihood of prepayment depends on a number of factors, including current interest rate and interest rate index (if any) on the loan, the financial ability of the borrower to refinance, the economic benefit to be obtained from refinancing, availability of refinancing at attractive terms, as well as economic and other factors in specific geographic areas which affect the sales and price levels of residential and commercial property. In a changing interest rate environment, prepayments may increase or decrease on fixed and adjustable rate loans depending on the current relative levels and expectations of future short-term and long-term interest rates. Prepayments on adjustable rate loans generally increase when long-term interest rates fall or are at historically low levels relative to short-term interest rates, thus making fixed rate loans more desirable. While savings and checking deposits generally may be withdrawn upon the customer’s request without prior notice, a continuing relationship with customers resulting in future deposits and withdrawals is generally predictable, resulting in a dependable and uninterrupted source of funds. Time deposits generally have early withdrawal penalties, which discourage customer withdrawal prior to maturity. Short-term borrowings have fixed maturities. Certain advances from the FHLB carry prepayment penalties and are expected to be repaid in accordance with their contractual terms.

FAIR VALUE MEASUREMENTS

The Company discloses the estimated fair value of its financial instruments at December 31, 2014 and 2013 in Note 15 to the consolidated financial statements.

OFF-BALANCE SHEET ARRANGEMENTS, CONTRACTUAL OBLIGATIONS, AND CONTINGENT LIABILITIES AND COMMITMENTS

The following table summarizes the Company’s loan commitments, including letters of credit, as of December 31, 2014:

| | | | | | | | | | | | | | | | | | | | |

| | | Amount of Commitment to Expire Per Period | |

| | | | | |

| (Dollars in thousands) | | Total | | | Less than | | | 1 to 3 | | | 3 to 5 | | | Over 5 | |

Type of Commitment | | Amount | | | 1 year | | | Years | | | Years | | | Years | |

| |

| | | | | |

Commercial lines-of-credit | | $ | 77,799 | | | $ | 69,904 | | | $ | 1,750 | | | $ | 1,223 | | | $ | 4,922 | |

Real estate lines-of-credit | | | 37,580 | | | | 2,491 | | | | 5,101 | | | | 5,456 | | | | 24,532 | |

Consumer lines-of-credit | | | 881 | | | | 881 | | | | – | | | | – | | | | – | |

Credit cards lines-of-credit | | | 3,493 | | | | 3,493 | | | | – | | | | – | | | | – | |

Overdraft privilege | | | 6,634 | | | | 6,634 | | | | – | | | | – | | | | – | |

Commercial real estate loan commitments | | | – | | | | – | | | | – | | | | – | | | | – | |

Letters of credit | | | 1,778 | | | | 1,778 | | | | – | | | | – | | | | – | |

| | | | | | | | | | | | | | | | | | | | |

Total commitments | | $ | 128,165 | | | $ | 85,181 | | | $ | 6,851 | | | $ | 6,679 | | | $ | 29,454 | |

| | | | | | | | | | | | | | | | | | | | |

20 2014 Report to Shareholders | CSB Bancorp, Inc.

2014 FINANCIAL REVIEW

As indicated in Note 10 to the consolidated financial statements, the Company had $128 million in total loan commitments at the end of 2014, with $85 million of that amount expiring within one year. All lines-of-credit represent either fee-paid or legally binding loan commitments for the loan categories noted. Letters of credit are also included in the amounts noted in the table since the Company requires that each letter of credit be supported by a loan agreement. The commercial and consumer lines represent both unsecured and secured obligations. The real estate lines are secured by mortgages on residential and nonresidential property. It is anticipated that a significant portion of these lines will expire without being drawn upon.

The following table summarizes the Company’s other contractual obligations, exclusive of interest, as of December 31, 2014:

| | | | | | | | | | | | | | | | | | | | |

| | | | | | Payment Due by Period | | | | |

(Dollars in thousands) Contractual Obligations | | Total

Amount | | | Less than

1 year | | | 1 to 3

Years | | | 3 to 5

Years | | | Over 5

Years | |

| |

Total time deposits | | $ | 127,763 | | | $ | 66,964 | | | $ | 41,065 | | | $ | 19,712 | | | $ | 22 | |

Short-term borrowings | | | 46,627 | | | | 46,627 | | | | – | | | | – | | | | – | |

Other borrowings | | | 14,953 | | | | 1,488 | | | | 11,809 | | | | 923 | | | | 733 | |

Operating leases | | | 498 | | | | 294 | | | | 204 | | | | – | | | | – | |

| | | | | | | | | | | | | | | | | | | | |

Total obligations | | $ | 189,841 | | | $ | 115,373 | | | $ | 53,078 | | | $ | 20,635 | | | $ | 755 | |

| | | | | | | | | | | | | | | | | | | | |

The other borrowings noted in the preceding table represent borrowings from the FHLB of Cincinnati. The notes require payment of interest on a monthly basis with principal due in monthly installments or at maturity, depending upon the issue. The obligations bear stated fixed interest rates and stipulate a prepayment penalty if the note’s interest rate exceeds the current market rate for similar borrowings at the time of repayment. As the notes mature, the Company evaluates the liquidity and interest rate circumstances, at that time, to determine whether to pay off or renew the note. The evaluation process typically includes the strength of current and projected customer loan demand, the Company’s federal funds sold or purchased position, projected cash flows from maturing investment securities, the current and projected market interest rate environment, local and national economic conditions and customer demand for the Company’s deposit product offerings.

CRITICAL ACCOUNTING POLICIES

The Company’s consolidated financial statements are prepared in accordance with U.S. generally accepted accounting principles and follow general practices within the commercial banking industry. Application of these principles requires management to make estimates, assumptions and judgments that affect the amounts reported in the financial statements. These estimates, assumptions and judgments are based upon the information available as of the date of the financial statements.

The most significant accounting policies followed by the Company are presented in the Summary of Significant Accounting Policies. These policies, along with the other disclosures presented in the Notes to Consolidated Financial Statements and the 2014 Financial Review, provide information about how significant assets and liabilities are valued in the financial statements and how those values are determined. Management has identified the allowance for loan losses and the fair value of financial investments as the accounting areas that require the most subjective and complex estimates, assumptions and judgments and, as such, could be the most subject to revision as new information becomes available.

Securities are evaluated periodically to determine whether a decline in their value is other-than-temporary. Management utilizes criteria such as the magnitude and duration of the decline, in addition to the reasons underlying the decline, to determine whether the loss in value is other-than-temporary. The term “other-than-temporary” is not intended to indicate that the decline is permanent, but indicates that the prospect for a near-term recovery of value is not necessarily favorable, or that there is a lack of evidence to support a realizable value equal to or greater than the carrying value of the investment. Once a decline in value is determined to be other-than-temporary, the value of the security is reduced and a corresponding charge to earnings is recognized.

As previously noted in the section entitled Allowance for Loan Losses, management performs analysis to assess the adequacy of its allowance for loan losses. This analysis encompasses a variety of factors including the potential loss exposure for individually reviewed loans, the historical loss experience, the volume of nonperforming loans (i.e., loans in nonaccrual status or past due 90 days or more), the volume of loans past due, any significant changes in lending or loan review staff, an evaluation of current and future local and national economic conditions, any significant changes in the volume or mix of loans within each category, a review of the significant concentrations of credit and any legal, competitive or regulatory concerns.

2014 Report to Shareholders | CSB Bancorp, Inc. 21

2014 FINANCIAL REVIEW

The Company accounts for business combinations using the acquisition method of accounting. Goodwill and intangible assets with indefinite useful lives are not amortized. Intangible assets with finite useful lives, consisting of core deposit intangibles, are amortized using accelerated methods over their estimated weighted-average useful lives, approximating ten years. Additional information is presented in Note 5, Core Deposit Intangible Assets.

IMPACT OF INFLATION AND CHANGING PRICES