Table of Contents

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended September 30, 2002

or

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 000-19654

VITESSE SEMICONDUCTOR

CORPORATION

(Exact name of registrant as specified in its charter)

Delaware | No. 77-0138960 | |

(State or other jurisdiction | (I.R.S. Employer | |

incorporation or organization) | Identification No.) |

741 Calle Plano, Camarillo, CA 93012

(Address of principal executive offices)

Registrant’s telephone number, including area code: (805) 388-3700

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, $0.01 Par Value

(Title of Class)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

The aggregate market value of the voting stock held by non-affiliates of the registrant, based upon the closing sale price of the Common Stock on September 30, 2002 as reported on the Nasdaq National Market, was approximately $134,681,055. Shares of Common Stock held by each officer and director and by each person who owns 5% or more of the outstanding Common Stock have been excluded in that such persons may be deemed to be affiliates. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

As of December 2, 2002, the registrant had outstanding 202,673,727 shares of Common Stock.

DOCUMENTS INCORPORATED BY REFERENCE

Definitive Proxy Statement relating to the Company’s Annual Meeting of Stockholders to be held on January 28, 2003 (incorporated into Part III hereof).

Registration Statement on Form S-1 effective December 10, 1991 (incorporated into Part IV hereof).

Table of Contents

VITESSE SEMICONDUCTOR CORPORATION

2002 ANNUAL REPORT ON FORM 10-K

Page | ||||

PART I. | ||||

| Item 1. | 1 | |||

| Item 2. | 15 | |||

| Item 3. | 15 | |||

| Item 4. | 15 | |||

PART II. | ||||

| Item 5. | 17 | |||

| Item 6. | 17 | |||

| Item 7. | 18 | |||

| Item 7a. | 32 | |||

| Item 8. | 34 | |||

| Item 9. | 63 | |||

PART III. | ||||

| Item 10. | 64 | |||

| Item 11. | 64 | |||

| Item 12. | 64 | |||

| Item 13. | 64 | |||

| Item 14. | 64 | |||

PART IV. | ||||

| Item 15. | 65 | |||

| 68 | ||||

| 69 | ||||

Table of Contents

FORWARD-LOOKING STATEMENTS

This report contains forward-looking statements that involve risks and uncertainties. These statements relate to our future plans, objectives, expectations and intentions. These statements may be identified by the use of words such as “expects”, “anticipates”, “intends”, “plans” and similar expressions. Our actual results could differ materially from those discussed in these statements. Factors that could contribute to these differences include those discussed under “Risk Factors”, “Management’s Discussion and Analysis of Financial Condition and Results of Operations”, and elsewhere in this report. The cautionary statements made in this report should be read as being applicable to all forward-looking statements wherever they appear in this report.

PART I

Vitesse Semiconductor Corporation (“Vitesse” or the “Company”) was incorporated in the State of Delaware in 1987. Our principal offices are located at 741 Calle Plano, Camarillo, California, and our phone number is (805) 388-3700. Our Internet address is www.vitesse.com. Our SEC filings are available through our website. Our Common Stock trades on the Nasdaq National Market under the symbol “VTSS”.

We are a leading supplier of high-performance integrated circuits (“ICs”) and optical modules, principally targeted at systems manufacturers in the communications and storage industries. Over the past few years, the proliferation of the Internet and the rapid growth in volume of data being sent over local and wide area networks placed a tremendous strain on the networking infrastructure. The resulting demand for increased bandwidth created a need for both faster as well as more expansive networks. There has also been a growing trend by systems companies towards the outsourcing of IC design and manufacture to suppliers such as Vitesse. Additionally, due to increasing needs for moving, managing and storing mission-critical data, the market for storage equipment has been growing significantly. Since the end of 2000, the communications industry has been experiencing a severe downturn due to the overbuilding of the networking infrastructure and excess inventories, among other reasons. In spite of these recent adverse conditions, we believe that the long-term prospects for the communications market remain strong. Our customers include leading communications and storage original equipment manufacturers (“OEMs”) such Alcatel, Cisco, EMC, Fujitsu, IBM, Lucent, McData, Nortel, Sun Microsystems, and Tellabs.

We are also a supplier of ICs to other markets such as the automatic test equipment (“ATE”) market. Over the past three years, revenues from this market have become less important as we have focused our business and operations on the communications market.

Background

Over the past decade, public communications networks, such as those used by long-distance and local exchange carriers, and specialized networks, such as those used by Internet service providers, experienced dramatic growth in traffic. This was driven by rapid growth of data intensive applications, such as Internet access, e-commerce, e-mail, video conferencing and the movement of large blocks of stored data across networks. This in turn spurred demand for high-speed interconnectivity between wide area networks (“WANs”), metropolitan area networks (“MANs”) and local area networks (“LANs”). The network protocols, particularly in the WAN, were designed to optimize voice communications rather than data transmission, which had started to account for the majority of traffic. As a result, service providers were forced to upgrade their infrastructure to provide high-speed data services to customers in addition to providing standard telephone services. At the same time, the abundance of capital available in the private and public markets in the late 1990’s and 2000 accelerated the build out of the infrastructure, leading to a significant increase in capital spending on networking equipment.

During this period of rapid expansion, our customers began increasing orders for semiconductor devices in anticipation of continued growth in demand for communications equipment. With device manufacturers such as

1

Table of Contents

Vitesse running at full capacity at that time, OEMs often ordered more devices than necessary in an effort to secure component deliveries. This resulted in a significant increase in inventory levels in the entire supply chain.

At the end of 2000, business conditions changed suddenly. As the supply of capital started to slow down and the overall economy began to weaken, many carriers as well as enterprises, faced with extreme financial hardship, either scaled back their expenditures or in some cases, ceased operations. Additionally, as it became evident that the infrastructure had been built out in excess of true end-user demand, capital spending on networking equipment across the industry dropped sharply. Due to this widespread market downturn, we experienced a significant decline in sales of our products, which was further exacerbated by the high inventory levels in the supply chain. In response to the decreased demand for our products and the continuing disruption in our industry, we implemented three restructuring plans during fiscal 2001 and 2002. These restructuring plans, which included the termination of employees, office closures, cancellation of certain development projects and the write down of certain assets, have significantly lowered our operating costs going forward. For a detailed description of these restructuring plans see “Restructuring Costs” in the Management’s Discussion and Analysis section and Note 4 to the Consolidated Financial Statements of this report.

In spite of these adverse conditions that have affected our business, we believe that for several reasons, the long-term prospects for the communications market and for Vitesse remain strong.

First, the demand for additional bandwidth continues to grow, driven primarily by increased traffic on the Internet, as more households and enterprises increase their utilization of the Internet. Further, the emergence of new data-intensive applications such as video-on-demand and next-generation wireless services is expected to drive additional traffic through the communications infrastructure. Finally, we believe that the build out of the infrastructure in developing countries will lead to increased demand for communications equipment.

Second, even as carriers and service providers are faced with a shortage of capital, to remain competitive they will find it necessary to upgrade their existing networks not only to offer additional services that their customers are demanding, but to do so more efficiently and at a lower cost. We believe this trend will spur demand for systems that augment, rather than replace existing equipment in the infrastructure.

Third, some MANs are experiencing traffic bottlenecks due to a lack of prior investment in equipment servicing the MAN as well as the interface between the MAN and the WAN. We believe this represents an opportunity for OEMs to supply equipment to carriers who wish to mitigate any bottlenecks.

Fourth, over the past few years, OEMs have been focusing their efforts on providing superior software and services as a means of differentiating themselves from their competition. This, in conjunction with rising costs of maintaining component design teams and developing custom integrated circuits, has led to OEMs outsourcing their IC development efforts to companies such as Vitesse. The reductions in workforce that many OEMs have recently implemented have accelerated this trend. As a result, even though capital expenditures for communications equipment have declined significantly and are expected to further decline in fiscal 2003, we believe that the available market for our products has increased.

Finally, over the past five years, through a combination of acquisitions and internal development efforts, we have expanded our product line beyond our traditional products that served the core telecommunications infrastructure. Specifically, we have enhanced our product offerings that serve the storage, enterprise and metro markets. We believe that these markets will recover faster from the current downturn than the telecommunications markets.

Infrastructure improvements to networks have most prominently included a dramatic increase in the deployment of fiber optic technology to replace conventional copper wire. Optical fiber offers substantially greater capacity, is less error prone and is easier to administer than copper wire. SONET (Synchronous Optical Network) in the United States and Japan and the equivalent SDH (Synchronous Digital Hierarchy) in the rest of

2

Table of Contents

the world are the primary standards for high-speed transmission of communication over optical fiber. The SONET/SDH standards facilitate high-data integrity and improved performance in terms of network reliability and reduced maintenance and other operations costs by standardizing interoperability among different vendors’ equipment.

More recently, the demand for system bandwidth is being addressed by a technique called wavelength division multiplexing (“WDM”). WDM is a technique that allows several optical signals, each of a different wavelength, to be transmitted simultaneously on a single optical fiber. The adoption of WDM has enabled system operators to significantly increase system bandwidth without having to deploy additional fiber cables, a long and costly process. While WDM increases the bandwidth carried by each optical fiber, it does not reduce the number of electronic components required. Instead, WDM has accelerated the growth of SONET/SDH deployment by eliminating fiber installation as a growth limiter.

There are two primary protocols being utilized today on top of the SONET optical base to ensure that routing and switching of information occurs accurately. They are Asynchronous Transfer Mode (“ATM”) and Internet Protocol (“IP”). ATM is based on fixed-size packets, called cells, and is designed to efficiently integrate voice, data and video and easily scale bandwidth. IP is a packet-based protocol that is generally accepted as the industry standard for LAN data transfer and is being increasingly used in MANs and WANs as well. Both ATM and IP packet switching network technologies are being deployed over optical networks based on the complementary SONET/SDH standards, known as ATM over SONET and Packet over SONET (“POS”). Fiber optic transmission systems that adhere to the SONET/SDH and ATM standards use data transmission rates of 155 Megabit per second (“Mb/s”), 622 Mb/s, 2.5 Gigabit per second (“Gb/s”) or 10 Gb/s today, with 40Gb/s in development. Additionally, new protocols such as multi-protocol label switching (“MPLS”) have emerged, which are better suited for data traffic while providing for the low latency and quality of service needs of voice and video traffic.

Most present day LANs use the Ethernet transmission protocol, which operates at 10 Mb/s, 100 Mb/s and 1Gb/s. The increasing bandwidth needs of network users have prompted manufacturers to begin developing networking systems with per-port transmission speeds of 10Gb/s. The scalability and migration capability built into the Gigabit Ethernet protocol allows OEMs to leverage their experience with this standard to transition to the higher data rate.

The proliferation of the Internet and the resulting need for managing, moving and storing increasing amounts of mission-critical data has led to significant growth in the market for storage equipment. Changes in storage topologies from Direct Attached Storage to architectures such as Network Attached Storage and Storage Area Networks (“SANs”) have spawned the need for inter-connecting high-performance computers, peripheral equipment, storage devices and networks at very high speeds. Most present day storage networks use a standard interface protocol known as small computer systems interface, or SCSI. For newer SANs, which require networking at high speeds over long distances, SCSI has become a limiting technology. To address the limitations of SCSI-based storage systems, the Fibre Channel standard was developed in the early 1990s. Fibre Channel is a practical, inexpensive, yet expandable method for achieving high-speed data transfer among workstations, mainframes, data storage devices and other peripherals. We have been a leading provider of Fibre Channel based ICs since the inception of this standard over ten years ago.

To address the demanding needs of communications networks and the various protocols that they must handle, OEMs are developing increasingly sophisticated systems. In order to achieve the performance and functionality required by such systems, these OEMs must utilize more complex ICs, which account for a larger portion of the cost of such systems. As a result of the rapid pace of new product introductions, the variety of standards to be accommodated and the difficulty of designing and producing the required ICs, OEMs are increasingly outsourcing these ICs to semiconductor firms with specialized expertise. These trends have created a significant opportunity for IC suppliers that can design cost-effective solutions for the next generation systems. These OEMs require IC vendors that possess both circuit design and system-level expertise and can quickly bring to market reliable, high-performance and power-efficient ICs.

3

Table of Contents

Strategy

Our objective is to be the leading supplier of high-performance IC and module solutions for the global communications market. In order to attain this goal, our corporate strategy encompasses the following elements:

Target Growing Markets

We target emerging high-growth areas in the communications infrastructure such as products delivering services based on SONET/SDH, ATM, IP, MPLS, Fibre Channel and Gigabit Ethernet, which typically require ICs that are capable of high-bandwidth data transmission. We strive to provide solutions that adhere to the major networking protocols and perform common networking functions required by the most widely deployed communications equipment.

Provide Complete Solutions

To be a leader in our market segment, we must not only address the current needs of our customers, but we also need to be aware of how these requirements are evolving. Over the past few years we recognized a trend among our customers to rely on standard products for a majority of their semiconductor needs, which they could purchase from component suppliers. Accordingly, our objective is to evolve from being solely the supplier of the highest speed physical layer ICs to being the supplier of all the critical high-performance components in our customers’ systems. These components range from the analog electronics used in the conversion between optical and electrical signals, our legacy physical layer products, as well as framers, network processors, and switch fabrics. Through our acquisition of Versatile Optical Networks, Inc. (“Versatile”), we have extended our reach into optical modules and switches. We believe that the complete solution strategy results in better interoperability and provides our customers with cost-effective and faster time-to-market solutions. It also enables us to build defensible barriers against competitors who offer only a partial or single circuit solution. Additionally, we continually strive to integrate multiple functions on a single chip, thereby reducing device cost and improving performance.

Develop “Technology Transparent” Products

The broad range of products that comprises the “complete solution” strategy requires a variety of semiconductor process technologies. We endeavor to offer solutions to our customers using the most appropriate process technology for the particular application. While most functions can be implemented in state-of-the-art complementary metal-oxide-silicon (“CMOS”) technology available through relationships with commercial foundries, the very highest speed functions, particularly at 10 Gb/s and 40 Gb/s, still require proprietary technologies such as Gallium Arsenide (“GaAs”) and Indium Phosphide (“InP”), which we possess internally.

Establish Close Relationships with Customers’ Engineering Management

One of the key elements of our strategy is to work closely with our customers’ systems design teams. We believe that these relationships enable us to better understand the customers’ needs and win designs for existing and new systems.

4

Table of Contents

Products and Customers

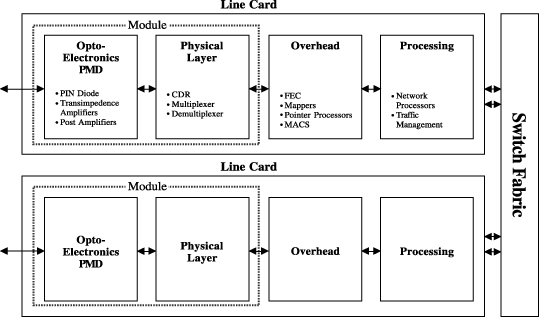

In order to meet our objective of being a provider of complete solutions to the high-performance communications equipment market, we offer several products that perform a variety of functions. The following functional block diagram shows the flow of data through a typical optical communications system.

Physical Media Devices (Optoelectronics)

The physical media device (“PMD”) serves as the actual physical connection to the fiber optic cable and is responsible for converting the incoming optical signal into an electric signal. Similarly, for data flowing in the opposite direction, the PMD converts electric signals into optical signals. Some of the PMDs that we offer are laser drivers, transimpedance amplifiers and post amplifiers operating at speeds ranging from 1.25 Gb/s to 10.7 Gb/s.

Physical Layer Devices

The physical layer (“PHY”) devices perform various functions, such as converting high-speed analog signals from the PMD to digital signals, clock and data regeneration (“CDR”) and multiplexing/demultiplexing (“MUX/DMUX”). The CDR cleans and re-times the signal to synchronize it with the overall system clock, while the MUX/DMUX converts low-speed parallel data into higher speed serial data and vice versa. We offer a broad line of PHY products for the SONET, DWDM, ATM, IP, Fibre Channel and Gigabit Ethernet markets at the 622Mb/s, 1.0 Gb/s, 1.25 Gb/s, 2.5Gb/s and 10 Gb/s data rates.

Optical Modules and Switches

Over the past few years, there has been a trend toward integrating optical components such as lasers and detectors with PMDs and PHY components on a single module. This optoelectronic integration provides OEMs with a compact, power-efficient and lower cost solution that they can obtain from a single vendor. Optical transponder modules streamline the supply chain further and improve time to market for OEMs. These “super components” interface with the fiber on one end and with the parallel data to and from the rest of the system at the other end, thus relieving the OEM from the engineering task of dealing with the opto-electrical interfaces as

5

Table of Contents

well as difficult to handle ultra high speed serial signals. During fiscal 2001, we expanded our reach into the optical part of communication systems through the acquisition of Versatile. We believe that since OEMs have begun to view the module as a component, the addition of these sub-systems to our product portfolio gives us a significant competitive edge over other semiconductor suppliers. Our products in this area include a 10 Gb/s optical transponder module and an 8x8 and 64x64 all optical switch utilizing proprietary opto-mechanical technology. We believe our products offer several advantages over competing products, including smaller size, the ability to transmit data over longer distances and extremely low insertion loss. To date, we have shipped only small quantities of optical modules and optical switches. Our ability to ship these products in larger volumes in the future will be subject to several factors including customer acceptance of these products, the timing of customer order patterns and our ability to manufacture the products in production volumes at acceptable yields.

Framing, Mapping & Other Overhead Processing Functions

Framers are devices that take incoming data traffic from the PHY or optical module and strip (or add) the framing information used for transporting data. Mappers convert data from one protocol to another. Some of the other critical functions within this block are FEC, Performance Monitoring and Pointer Processing. We offer a complete line of these products, principally for the SONET market as well MACs for the Gigabit Ethernet market.

Network Processors and Traffic Managers

A network processor is a software-programmable microprocessor that is optimized for networking and communications functions such as classification, filtering, policing, grooming, forwarding and routing. In recent years, OEMs have been increasingly outsourcing this function to semiconductor vendors such as Vitesse since an off-the-shelf product presents a faster time-to-market alternative to designing a custom application specific integrated circuit (“ASIC”). Traffic management ICs reside on a line card between the network processor and the switch fabric and perform the policing, queuing and buffering functions. Vitesse offers the IQ2000 and the IQ2200 family of network processors that is designed to deliver programmable high-performance deep-packet processing solutions at speeds up to 2.5 Gb/s. We also offer the Pacemaker line of traffic management products that is targeted at packet processing solutions within multi-service and ATM core switches, digital cross connects and high-speed routers

Switch Fabrics

The switch fabric is responsible for receiving data from a line card and routing it to the proper destination. As in the case of the network processor, this is a function that is primarily served by internally developed and manufactured ASIC solutions today. However, OEMs have increasingly begun to outsource the fabric to semiconductor suppliers. Our most current switch fabric solution is GigaStream, which integrates advanced queuing and scheduling, a serial crossbar and multiple channels of high-speed serial link technology in a two-component fabric chip set. GigaStream’s flexible architecture allows systems designers to scale system bandwidth up to 80 Gb/s. This chip set is ideally suited for access, edge and metro area routers and multiservice switches at data rates up to 2.5 Gb/s. We have also announced the TeraStream switch fabric, a two component chipset that supports 2.5 Gb/s and 10 Gb/s port speeds with a maximum aggregate user bandwidth of 160 Gb/s.

Through our acquisition of Exbit Technology in fiscal 2001, we have expanded our product line to include switches that address Gigabit Ethernet applications in the LAN. Vitesse also supplies a family of time slot interchange (“TSI”) and crosspoint switches for use in SONET and WDM equipment in the MAN and within the core of the network. The TSI switches provide aggregate bandwidth up to 160Gb/s. The crosspoint switches are available in a broad range of sizes from 2x2 to 144x144 matrices.

6

Table of Contents

Storage and Serial Backplane Products

We supply a number of different products for the enterprise storage and serial backplane markets. Our products target various systems such as host bus adaptors, switches, servers, hubs, disk arrays and RAID (redundant array of inexpensive disks) subsystems using Fibre Channel, SCSI and Serial ATA interfaces. Our offerings consist of physical layer devices such as serializers and deserializers (“SerDes”), transceivers, and port bypass circuits, as well as more integrated products such as switches and enclosure management controllers.

Process Technology

The majority of our products make use of state-of-the-art CMOS technology that is readily available through commercial foundries. These foundries produce wafers using feature sizes down to 0.13 microns. In the internal manufacturing of our products, we principally use GaAs as the substrate.

We have recently introduced a new InP process in our Camarillo wafer fabrication facility targeted at high-speed applications at 40Gb/s and higher. This process is based on a vertical NPN bipolar transistor and offers up to three layers of aluminum interconnect. Indium Phosphide based products also enable optical integration in the form of on-chip photo detectors, thereby reducing the number of components required in an optical receiver. We believe that this InP process offers customers performance that is not available in silicon germanium (“SiGe”), CMOS or any other commercially available processes.

Manufacturing

Wafer Fabrication

We outsource the wafer fabrication for the majority of our products to outside foundries such as IBM, LSI Logic, Taiwan Semiconductor Manufacturing Corporation and United Microelectronics Corporation. The typical time required to produce wafers is about 12-16 weeks. After fabrication, the wafers must be probed to separate usable and unusable die. We perform all of our probing internally using advanced probers and testers.

We fabricate a limited amount of GaAs and InP wafers at our two wafer fabrication facilities in Camarillo, California, and Colorado Springs, Colorado. The Camarillo plant has a 6,000 square foot clean room with a rating of Class 10, (meaning there are fewer than ten particles larger than 0.5 micron per cubic foot of air) while the Colorado Springs plant has a 10,000 square foot Class 1 clean room.

We have recently established a manufacturing operation for our optical modules and switches in a new facility in San Jose. This operation includes commercially available equipment such as wire bonders, die attach machines and opto-mechanical equipment for the precision alignment of lasers and detectors to optical fibers. To maximize production yield and minimize production costs, our manufacturing process includes extensive quality assurance systems and performance testing.

IC Assembly and Test

We outsource our IC packaging to multiple assembly subcontractors in the United States and Asia. Following assembly, the packaged parts are returned to us for final testing prior to shipment to customers. For final test we utilize advanced automated testers as well as high-performance bench test equipment.

Components and Raw Materials

We manufacture our products using a variety of wafers and other components procured from third-party suppliers. All of our integrated circuits are packaged by third parties. Certain components, materials and services

7

Table of Contents

are available from only a limited number of sources. GaAs and InP substrates and other raw materials used in the internal production of our ICs are available from several suppliers. Although lead times are occasionally extended in the industry, we have not experienced any material difficulty in obtaining raw materials, wafers or assembly services.

Engineering, Research and Development

The market for our products is characterized by continually evolving industry standards, rapid changes in process technologies and increasing levels of functional integration. We believe that our future success will depend largely on our ability to continue to improve our products and our process technologies, to develop new technologies and to adopt emerging industry standards.

Product Research and Development

Our product development efforts are focused on designing new products for the high-performance communications and storage markets based on understanding the evolving needs of our customers. We are expending considerable design effort to increase the speed and complexity and to reduce the power dissipation of our products and to create new, value added functionality. We have, and will continue to develop, cores and standard blocks that can be reused in multiple products, thereby reducing design cycle time and increasing first-time design correctness.

Process Development

Currently, our process development is directed at refining and enhancing a new InP process that we have recently implemented in our Camarillo facility. In addition to developing this process to maturity, this effort is focused on increasing yields and improving the speed, complexity and power dissipation of the underlying products.

Our engineering, research and development expenses in fiscal 2002, 2001 and 2000, excluding the amortization of deferred stock-based compensation and purchased in-process research and development (“IPR&D”), were $137.2 million, $86.2 million and $57.3 million, respectively.

Competition

The markets for our products are intensely competitive and subject to rapid technological advancement in design tools, wafer manufacturing techniques, process tools and alternate networking technologies. We must identify and capture future market opportunities to offset the rapid price erosion that characterizes our industry. We may not be able to develop new products at competitive pricing and performance levels. Even if we are able to do so, we may not complete a new product and introduce it to market in a timely manner. Our customers may substitute use of our products in their next generation equipment with those of current or future competitors. Our competitors include Agere Systems, Applied Micro Circuit Corporation, Broadcom, Conexant Systems, IBM, Intel, Infineon, Marvell, Maxim Integrated Products and PMC Sierra. We also compete with the internal ASIC design units of systems companies such as Cisco and Nortel. Over the next few years, we expect additional competitors, some of which may have greater financial and other resources, to enter the market with new products. In addition, we are aware of smaller privately held companies that focus on specific portions of our range of products. These companies, individually or collectively, could represent future competition for many design wins and subsequent product sales.

We typically face competition at the design stage, where customers evaluate alternative design approaches that require integrated circuits. Our competitors have increasingly frequent opportunities to supplant our products in next generation systems because of shortened product life and design-in cycles in many of our customers’ products.

8

Table of Contents

Competition is particularly strong in the market for communications ICs, in part due to the market’s growth rate, which attracts larger competitors, and in part due to the number of smaller companies focused on this area. These companies, individually and collectively, represent strong competition for many design wins, and subsequent product sales. Larger competitors in our market have acquired both mature and early stage companies with advanced technologies. These acquisitions could enhance the ability of larger competitors to obtain new business that Vitesse might have otherwise won.

Sales and Customer Support

We sell our products principally through direct sales to system manufacturers by our sales force. Because of the significant engineering support required in connection with the sale of high-performance ICs, we provide our customers with field engineering support as well as engineering support from our headquarters. Our sales cycle is typically lengthy and requires the continued participation of salespersons, field engineers, engineers based at our headquarters and senior management.

We augment this direct sales approach with domestic and foreign distributors that work under the direction of our sales force and service smaller accounts purchasing application specific standard products.

Our sales headquarters is located in Camarillo, California. We have 9 additional sales and field application support offices in the United States, two in Canada, three in China, three in Europe and one in Japan.

We generally warrant our products against defects in materials and workmanship for a period of one year.

Licenses and Patents

We have been awarded 37 U.S. patents for various aspects of design and process innovations used in the design and manufacture of our products. We have 101 patent applications pending in the U.S. and 13 patent applications pending in Europe and are preparing to file several more patent applications. We believe that patents are of less significance in our industry than such factors as technical expertise, innovative skills and the abilities of our personnel.

As is typical in the semiconductor industry, we have, from time to time, received, and may receive in the future, letters from third parties asserting patent rights, mask work rights or copyrights on certain of our products and processes. None of the claims to date has resulted in the commencement of any litigation against us nor have we to date believed it is necessary to license any of the patent rights referred to in such letters.

Backlog

Vitesse’s sales are made primarily pursuant to standard purchase orders for delivery of products. Quantities of our products to be delivered and delivery schedules are frequently revised to reflect changes in customer needs. For these reasons, our backlog as of any particular date is not representative of actual sales for any succeeding period, and we therefore do not believe that backlog is a good indicator of future revenue.

Environmental Matters

We are subject to a variety of federal, state and local governmental regulations related to the use, storage, discharge and disposal of toxic, volatile or otherwise hazardous chemicals used in our manufacturing process. Any failure to comply with present or future regulations could result in the imposition of fines on us, the suspension of production or a cessation of operations. In addition, such regulations could restrict our ability to operate or expand any of our manufacturing facilities or could require us to acquire costly equipment or incur other significant expenses to comply with environmental regulations or clean up prior discharges.

9

Table of Contents

Employees

As of September 30, 2002, we had 936 employees, including 537 in engineering, research and development, 110 in marketing and sales, 251 in operations and 38 in finance and administration. Our ability to attract and retain qualified personnel is essential to our continued success. None of our employees are represented by a collective bargaining agreement, nor have we ever experienced any work stoppage. We believe our employee relations are good.

Risk Factors

We Have Experienced Continuing Losses From Operations Since March 31, 2001, and We Expect That Our Operating Results Will Fluctuate in The Future Due to Reduced Demand in Our Markets

Since our quarterly revenues and earnings per share (excluding acquisition related and non-recurring charges) peaked in the quarter ended December 31, 2000, our revenues have declined substantially and we have experienced continuing losses from operations. While our revenues have improved slightly in the current fiscal year’s quarters, they are still not sufficient to cover our operating expenses. Further, in the first and third quarters of fiscal 2002 our operating results were materially and adversely affected by an inventory write-down, restructuring charges and impairment charges. If we are required to take additional charges such as these in the future, the adverse effect on our operating results may again be material. Due to general economic conditions and slowdowns in purchases of networking equipment, it has become increasingly difficult for us to predict the purchasing activities of our customers and we expect that our operating results will fluctuate substantially in the future. We cannot predict when we will again achieve profitability, if at all. Future fluctuations in operating results may also be caused by a number of factors, many of which are outside our control. Additional factors that could affect our future operating results include the following:

| • | The loss of major customers; |

| • | Variations, delays or cancellations of orders and shipments of our products; |

| • | Reduction in the selling prices of our products; |

| • | Significant changes in the type and mix of products being sold; |

| • | Delays in introducing new products; |

| • | Design changes made by our customers; |

| • | Our failure to manufacture and ship products on time; |

| • | Changes in manufacturing capacity, the utilization of this capacity and manufacturing yields; |

| • | Variations in product development costs; |

| • | Changes in inventory levels; and |

| • | Expenses or operational disruptions resulting from acquisitions. |

In the quarters ended June 30, 2002 and December 31, 2001, we implemented significant cost reductions. We do not expect that these measures will be sufficient to offset lower revenues prior to the later half of fiscal 2003, if at all, and as such, we expect to continue to incur net losses at least in the first half of the upcoming year. In the past, we have recorded significant new product and process development costs because our policy is to expense these costs at the time that they are incurred. We may incur these types of expenses in the future. These additional expenses will have a material and adverse effect on our results in future periods. The occurrence of any of the above-mentioned factors could have a material adverse effect on our business and on our financial results.

10

Table of Contents

The Market Price for Our Common Stock Has Been Volatile and Future Volatility Could Cause the Value of Your Investment in Our Company to Decline.

Our stock price has experienced significant volatility recently. In particular, our stock price declined significantly in the context of announcements made by us and other semiconductor suppliers of reduced revenue expectations and of a general slowdown in the technology sector, particularly the optical networking equipment sector. Given these general economic conditions and the reduced demands for our products that we have experienced recently, we expect that our stock price will continue to be volatile. In addition, the value of your investment could decline due to the impact of any of the following factors, among others, upon the market price of our common stock:

| • | Additional changes in financial analysts’ estimates of our revenues and operating results; |

| • | Our failure to meet financial analysts’ performance expectations; and |

| • | Changes in market valuations of other companies in the semiconductor or networking industries. |

In addition, many of the risks described elsewhere in this section could materially and adversely affect our stock price, as discussed in those risk factors. The stock markets have recently experienced substantial price and volume volatility. Fluctuations such as these have affected and are likely to continue to affect the market price of our common stock.

In the past, securities class action litigation has often been instituted against companies following periods of volatility and decline in the market price of such companies’ securities. If instituted against us, regardless of the outcome, such litigation could result in substantial costs and diversion of our management’s attention and resources and have a material adverse effect on our business, financial condition and results of operations. We could be required to pay substantial damages, including punitive damages, if we were to lose such a lawsuit.

If We are Unable to Develop and Introduce New Products Successfully or to Achieve Market Acceptance of Our New Products, Our Operating Results would be Adversely Affected.

Our future success will depend on our ability to develop new high-performance integrated circuits and optical modules for existing and new markets, introduce these products in a cost-effective and timely manner and convince leading equipment manufacturers to select these products for design into their own new products. Our quarterly results in the past have been, and are expected in the future to continue to be, dependent on the introduction of a relatively small number of new products and the timely completion and delivery of those products to customers. The development of new integrated circuits is highly complex, and from time to time we have experienced delays in completing the development and introduction of new products. In addition, we only introduced optical modules since our acquisition of Versatile Optical Networks, Inc., in July 2001, and have only begun to see significant sales of these products in the last two quarters. Our ability to develop and deliver new products successfully will depend on various factors, including our ability to:

| • | Accurately predict market requirements and evolving industry standards; |

| • | Accurately define new products; |

| • | Timely complete and introduce new products; |

| • | Timely qualify and obtain industry interoperability certification of our products and our customers’ products into which our products will be incorporated; |

| • | Achieve high manufacturing yields; and |

| • | Gain market acceptance of our products and our customers’ products. |

If we are not able to develop and introduce new products successfully, our business, financial condition and results of operations will be materially and adversely affected.

11

Table of Contents

We are Dependent on a Small Number of Customers in a Few Industries

We intend to continue focusing our sales effort on a small number of customers in the communications and storage markets that require high-performance integrated circuits. Some of these customers are also our competitors. For the year ended September 30, 2002, no single customer accounted for greater than 10% of total revenues. If any of our major customers delays orders of our products or stops buying our products, our business and financial condition would be severely affected.

There Are Risks Associated with Recent and Future Acquisitions

Since the beginning of fiscal 2000, we made four significant acquisitions. In March 2000, we completed the acquisition of Orologic, Inc. (“Orologic”) in exchange for approximately 4.5 million shares of our common stock. In May 2000, we completed the acquisition of SiTera Incorporated (“SiTera”) for approximately 14.7 million shares of our common stock. In June 2001, we acquired Exbit Technology A/S (“Exbit”) for up to approximately 2.7 million shares of our common stock and may be required to issue an additional 2.4 million shares upon the attainment of certain internal future retention and performance goals. In July 2001, we completed the acquisition of Versatile for approximately 8.8 million shares of our common stock. Also since the beginning of fiscal 2000, we completed four smaller acquisitions for an aggregate of approximately $61.7 million consisting of approximately 0.8 million shares of common stock issued and stock options assumed and approximately $44.6 million in cash. These acquisitions may result in the diversion of management’s attention from the day-to-day operations of the Company’s business. Risks of making these acquisitions include difficulties in the integration of acquired operations, products and personnel. If we fail in our efforts to integrate recent and future acquisitions, our business and operating results could be materially and adversely affected.

Our management frequently evaluates strategic opportunities available. In the future, we may pursue additional acquisitions of complementary products, technologies or businesses. Acquisitions we make in the future could result in dilutive issuances of equity securities, substantial debt and amortization expenses related to intangible assets. In particular, in connection with our acquisition of Orologic, we were required to record an IPR&D charge of $45.6 million in the three months ended March 31, 2000. In addition, under the new FASB Standard No. 142, which we adopted as of October 1, 2001, certain intangible assets relating to acquired businesses, including goodwill, are maintained on the balance sheet rather than being amortized. These assets must be tested at least annually for impairment, and in the year ended September 30, 2002, we recorded impairment charges of $403.0 million associated with goodwill and other intangible assets related to past acquisitions. As of September 30, 2002 and after accounting for these impairment charges, we have an aggregate of $179.6 million of goodwill and other intangible assets on our balance sheet. These assets may eventually be written down to the extent they are deemed to be impaired and any such write-downs would adversely affect our results.

Our Industry is Highly Competitive

The markets for our products are intensely competitive and subject to rapid technological advancement in design tools, wafer-manufacturing techniques, process tools and alternate networking technologies. We must identify and capture future market opportunities to offset the rapid price erosion that characterizes our industry. We may not be able to develop new products at competitive pricing and performance levels. Even if we are able to do so, we may not complete a new product and introduce it to market in a timely manner. Our customers may substitute use of our products in their next generation equipment with those of current or future competitors. Our competitors include Agere, Applied Micro Circuits Corporation, Broadcom, Conexant Systems, IBM, Intel, Infineon, Marvell, Maxim Integrated Products and PMC Sierra. We also compete with internal ASIC design units of systems companies such as Cisco and Nortel. Over the next few years, we expect additional competitors, some of which may have greater financial and other resources, to enter the market with new products. In addition, we are aware of venture-backed companies that focus on specific portions of our product line. These companies, individually or collectively, could represent future competition for many design wins and subsequent product sales.

12

Table of Contents

We typically face competition at the design stage, where customers evaluate alternative design approaches that require integrated circuits. Our competitors have increasingly frequent opportunities to supplant our products in next generation systems because of shortened product life and design-in cycles in many of our customer’s products.

Competition is particularly strong in the market for optical networking chips, in part due to the market’s past growth rate, which attracts larger competitors, and in part due to the number of smaller companies focused on this area. These companies, individually and collectively, represent strong competition for many design wins and subsequent product sales. Larger competitors in our market have acquired both mature and early stage companies with advanced technologies. These acquisitions could enhance the ability of larger competitors to obtain new business that Vitesse might have otherwise won.

There are Risks Associated with Doing Business in Foreign Countries

In fiscal 2002, 2001 and 2000 international sales accounted for 22%, 23% and 24%, respectively, of our total revenues, and we expect international sales to constitute a substantial portion of our total revenues for the foreseeable future. International sales involve a variety of risks and uncertainties, including risks related to:

| • | Reliance on strategic alliance partners; |

| • | Compliance with foreign regulatory requirements; |

| • | Variability of foreign economic conditions; |

| • | Changing restrictions imposed by U.S. export laws; and |

| • | Competition from U.S. based companies that have firmly established significant international operations. |

Failure to successfully address these risks and uncertainties could adversely affect our international sales, which could in turn have a material and adverse effect on our results of operations and financial condition.

We Must Keep Pace with Product and Process Development and Technological Change

The market for our products is characterized by rapid changes in both product and process technologies. We believe that our success to a large extent depends on our ability to continue to improve our product and process technologies and to develop new products and technologies in order to maintain our competitive position. Further, we must adapt our products and processes to technological changes and adopt emerging industry standards. Our failure to accomplish any of the above could have a negative impact on our business and financial results.

We Are Dependent on Key Suppliers

We manufacture our products using a variety of components procured from third-party suppliers. All of our high-performance integrated circuits are packaged by third parties. Other components and materials used in our manufacturing process are available from only a limited number of sources. Further, we are increasingly relying on third-party semiconductor foundries for our supply of silicon-based products. Any difficulty in obtaining sole- or limited-sourced parts or services from third parties could affect our ability to meet scheduled product deliveries to customers. This in turn could have a material adverse effect on our customer relationships, business and financial results.

Our Manufacturing Yields Are Subject to Fluctuation

Semiconductor fabrication is a highly complex and precise process. Defects in masks, impurities in the materials used, contamination of the manufacturing environment and equipment failures can cause a large

13

Table of Contents

percentage of wafers or die to be rejected. Manufacturing yields vary among products, depending on a particular high-performance integrated circuit’s complexity and on our experience in manufacturing it. In the past, we have experienced difficulties in achieving acceptable yields on some high-performance integrated circuits, which has led to shipment delays. Our overall yields are lower than yields obtained in a mature silicon process because we manufacture a large number of different products in limited volume and our process technology is less developed. We anticipate that many of our current and future products may never be produced in volume.

Since a majority of our manufacturing costs are relatively fixed, maintaining a number of shippable die per wafer is critical to our operating results. Yield decreases can result in higher unit costs and may adversely affect gross profit and net income. We use estimated yields for valuing work-in-process inventory. If actual yields are materially different than these estimates, we may need to revalue work-in-process inventory. Consequently, if any of our current or future products experience yield problems, our financial results may be adversely affected.

Our Business Is Subject to Environmental Regulations

We are subject to various governmental regulations related to toxic, volatile and other hazardous chemicals used in our manufacturing process. If we fail to comply with these regulations, this failure could result in the imposition of fines or in the suspension or cessation of our operations. Additionally, we may be restricted in our ability to expand operations at our present locations or we may be required to incur significant expenses to comply with these regulations.

Our Failure to Manage Growth of Operations May Adversely Affect Us

The management of our growth requires qualified personnel, systems and other resources. We have recently established several product design centers worldwide and have acquired Orologic in March 2000, SiTera in May 2000, Exbit in June 2001, Versatile in July 2001 and completed seven other smaller acquisitions since the fall of 1998. We have only limited experience in integrating the operations of acquired businesses. Failure to manage our growth or to successfully integrate new and future facilities or newly acquired businesses could have a material adverse effect on our business and financial results.

We Are Dependent on Key Personnel

Due to the specialized nature of our business, our success depends in part upon attracting and retaining the services of qualified managerial and technical personnel. The competition for qualified personnel is intense. The loss of any of our key employees or the failure to hire additional skilled technical personnel could have a material adverse effect on our business and financial results.

Our Ability to Repurchase Our Debentures, If Required, with Cash, upon a Change of Control May Be Limited

In certain circumstances involving a change of control or the termination of public trading of our common stock, holders of our 4% convertible subordinated debentures may require us to repurchase some or all of the debentures. We cannot assure that we will have sufficient financial resources at such time or will be able to arrange financing to pay the repurchase price of the debentures.

Our ability to repurchase the debentures in such event may be limited by law, by the indenture, by the terms of other agreements relating to our senior debt and by such indebtedness and agreements as may be entered into, replaced, supplemented or amended from time to time. We may be required to refinance our senior debt in order to make such payments. We may not have the financial ability to repurchase the debentures if payment of our senior debt is accelerated.

14

Table of Contents

Our executive offices and principal research and development and fabrication facility is located in Camarillo, California, and is being leased under a noncancellable operating lease that expires in 2009. The total space occupied in this building is approximately 111,000 square feet. We have a second wafer fabrication facility in Colorado Springs, Colorado that is under a lease until November 2002. This facility includes a 10,000 square foot clean room for wafer fabrication and a product development center. We have opted to purchase this facility upon expiration of the lease. We lease an additional 62,000 square feet in Camarillo for product development. In March 2001, we purchased an additional facility, located in Camarillo, for product development. This building is approximately 52,000 square feet. In San Jose, California, we lease an 80,000 square foot facility for the manufacturing of our optical modules and switches. We also lease space for 14 other product development centers in California, Colorado, Denmark, Florida, Massachusetts, Minnesota, New Hampshire, North Carolina, Oregon, and Texas, and 18 sales and field application support offices (9 in the United States, 2 in Canada, 3 in Europe, 3 in China and 1 in Japan).

We are currently involved in several legal proceedings; however, we believe that resolution of these matters, if resolved against us, would not have a material and adverse effect on us.

No matters were submitted to a vote of security holders during the fourth quarter of the fiscal year covered by this report.

Executive Officers of the Registrant

The executive officers of the Company are as follows:

Name | Age | Position | ||

| Louis Tomasetta | 53 | President and Chief Executive Officer, Director | ||

| Ira Deyhimy | 62 | Vice President, Business Development | ||

| Christopher Gardner | 42 | Vice President, General Manager of Transport Division | ||

| Eugene Hovanec | 50 | Vice President, Finance & Chief Financial Officer | ||

| Yatin Mody | 39 | Vice President, Finance | ||

| Richard Riker | 47 | Vice President, Sales and Marketing |

Louis Tomasetta, a co-founder of the Company, has been President, Chief Executive Officer and a Director since the Company’s inception in February 1987. From 1984 to 1987, he served as President of the integrated circuits division of Vitesse Electronics Corporation. Prior to that he was the director of the Advanced Technology Implementation department at Rockwell International Corporation. Dr. Tomasetta has over 25 years experience in the management and development of GaAs based businesses, products, and technology. Dr Tomasetta received his B.S., M.S., and Ph.D. degrees in electrical engineering from the Massachusetts Institute of Technology.

Ira Deyhimy, a co-founder of the Company, was Vice President of Product Development since the Company’s inception in February 1987 and became Vice President, Business Development in fiscal 2001. From 1984 to 1987, he was Vice President, Engineering at Vitesse Electronics Corporation. Prior to that, Mr. Deyhimy was manager of Integrated Circuit Engineering at Rockwell International Corporation. Mr. Deyhimy has over 25 years experience in GaAs electronics. Mr. Deyhimy holds a B.S. degree in physics from the University of California at Los Angeles and a M.S. degree in physics from the California State University at Northridge.

Christopher Gardner joined Vitesse in 1986, became Director of ASIC Products in 1992, Vice President and General Manager of ATE Products in 1996, and was appointed Vice President and General Manager of the

15

Table of Contents

Telecom Division in 1999. Mr. Gardner served as Vice President and Chief Operating Officer from November 2000 to June 2002. In June 2002, Mr. Gardner became Vice President and General Manager of the Transport Division. Prior to joining Vitesse, he was a member of the technical staff at AT&T Bell Laboratories, which later became part of Lucent Technologies. Mr. Gardner received his BSEE from Cornell University and his MSEE from the University of California at Berkeley.

Eugene Hovanec joined the Company as Vice President, Finance and Chief Financial Officer in December 1993. From 1989 to 1993, Mr. Hovanec served as Vice President, Finance & Administration, and Chief Financial Officer at Digital Sound Corporation. Prior to that, from 1984 to 1989, he served as Vice President and Controller at Micropolis Corporation. Mr. Hovanec holds a Bachelor of Business Administration degree from Pace University, New York. Mr. Hovanec also serves as a director of Interlink Electronics, Inc.

Yatin Mody joined the Company in March 1992 as Manager of Budgeting and Cost Accounting, became Controller in August 1993, Vice President and Controller in November 1998, and Vice President, Finance in July 2002. Prior to that, Mr. Mody was at Deloitte and Touche, most recently as a manager. Mr. Mody holds a Bachelor of Technology degree in electrical engineering from the Indian Institute of Technology, Madras and an M.B.A degree from the University of California at Los Angeles.

Richard Riker joined Vitesse in June 2001 as Vice President, Sales and Marketing. He has over 21 years of experience in the semiconductor industry and related fields. From 2000 to 2001, Mr. Riker was Vice President, Sales and Business Development at Stargen. From 1994 to 2000, Mr. Riker was Director of Sales at Intel and Vice President Worldwide Sales, Digital Semiconductors, a business unit of Digital Equipment Corporation. Mr. Riker holds a BSEE from California State University at Long Beach and an MBA from Pepperdine University.

16

Table of Contents

PART II

Our common stock is traded in the Nasdaq National Market System under the symbol VTSS. Our common stock has been trading on the Nasdaq National Market since December 11, 1991. The table below presents the quarterly high and low closing prices on the Nasdaq National Market during the past two fiscal years, adjusted for stock splits.

Fiscal Year Ended September 30, 2001 | High | Low | ||||

| First Quarter | $ | 92.25 | $ | 43.13 | ||

| Second Quarter | 75.88 | 23.81 | ||||

| Third Quarter | 37.77 | 15.94 | ||||

| Fourth Quarter | 22.20 | 7.03 | ||||

Fiscal Year Ended September 30, 2002 | ||||||

| First Quarter | $ | 14.84 | $ | 7.27 | ||

| Second Quarter | 14.16 | 7.02 | ||||

| Third Quarter | 10.23 | 2.59 | ||||

| Fourth Quarter | 3.41 | 0.68 | ||||

As of September 30, 2002, there were approximately 2,356 shareholders of record. We have never paid cash dividends and presently intend to retain any future earnings for business development. Further, our bank line of credit agreement and lease agreements prohibit the payment of dividends without the banks’ consent.

The selected financial data presented below was derived from the consolidated financial statements of the Company and should be read in conjunction with the audited consolidated financial statements, the notes thereto and the other financial data included therein.

As of and for the years ended September 30, | |||||||||||||||||

2002 | 2001 | 2000 | 1999 | 1998 | |||||||||||||

(in thousands except per share amounts) | |||||||||||||||||

Statement of operations data: | |||||||||||||||||

| Revenues | $ | 162,357 | $ | 384,143 | $ | 441,694 | $ | 281,669 | $ | 181,169 | |||||||

| Income (loss) from operations | (821,467 | ) | (174,218 | ) | 60,802 | 79,454 | 46,992 | ||||||||||

| Income (loss) before extraordinary gain | (949,793 | ) | (130,842 | ) | 27,889 | 61,151 | 48,634 | ||||||||||

| Net income (loss) | (883,526 | ) | (111,875 | ) | 27,889 | 61,151 | 48,634 | ||||||||||

| Extraordinary gain per share—diluted | 0.33 | 0.10 | — | — | — | ||||||||||||

| Net income (loss) per share—basic | (4.45 | ) | (0.60 | ) | 0.16 | 0.37 | 0.32 | ||||||||||

| Net income (loss) per share—diluted(1) | (4.45 | ) | (0.60 | ) | 0.15 | 0.34 | 0.29 | ||||||||||

| Shares used in per-share calculation—basic | 198,608 | 185,853 | 176,147 | 164,602 | 153,735 | ||||||||||||

| Shares used in per-share calculation—diluted(1) | 198,608 | 185,853 | 189,828 | 178,312 | 166,847 | ||||||||||||

Balance sheet data: | |||||||||||||||||

| Cash and short-term investments | $ | 312,161 | $ | 219,785 | $ | 699,556 | $ | 200,186 | $ | 176,773 | |||||||

| Working capital, net | 269,526 | 227,329 | 806,571 | 295,463 | 295,463 | ||||||||||||

| Total assets | 827,259 | 1,932,782 | 1,901,066 | 543,069 | 543,069 | ||||||||||||

| Long-term debt, less current portion | 195,915 | 469,031 | 723,587 | 1,636 | 701 | ||||||||||||

| Total shareholder’s equity | 482,705 | 1,329,005 | 1,105,402 | 502,381 | 361,646 | ||||||||||||

Note 1: Diluted net income per share is computed using the weighted-average number of common shares and dilutive potential common shares outstanding during the period. Diluted net loss per share is computed using the weighted-average number of common shares and excludes dilutive potential common shares, as their effect is antidilutive. The dilutive potential common shares which were antidilutive for fiscal 2002 totaled approximately 26.6 million shares.

17

Table of Contents

The following discussion of the financial condition and results of operations of Vitesse should be read in conjunction with the Consolidated Financial Statements and Notes thereto included elsewhere in this report.

Overview

We are a leading supplier of high-performance integrated circuits and optical modules, principally targeted at systems manufacturers in the communications and storage industries. Our customers include leading communications and storage OEMs such Alcatel, Cisco, EMC, Fujitsu, IBM, Lucent, McData, Nortel, Sun Microsystems, and Tellabs. Over the past few years, the proliferation of the Internet and the rapid growth in volume of data being sent over local and wide area networks placed a tremendous strain on the networking infrastructure. The resulting demand for increased bandwidth created a need for both faster as well as more expansive networks. There has also been a growing trend by systems companies towards the outsourcing of IC design and manufacture to suppliers such as Vitesse. Additionally, due to increasing needs for moving, managing and storing mission-critical data, the market for storage equipment has been growing significantly.

During this period of rapid expansion, our customers began increasing orders for our products in anticipation of continued growth in demand for communications equipment. At the end of fiscal 2000, business conditions changed suddenly. As credit tightened and the economy slipped into a recession, many carriers and service providers, faced with financial hardship, either scaled back their expenditures or in some cases, ceased operations. Additionally, as it became evident that the infrastructure had been built out in excess of true end-user demand, capital spending on networking equipment across the industry dropped sharply. Due to this widespread market downturn, we experienced a significant decline in sales. In response to these arduous conditions, we implemented three restructuring plans during fiscal 2001 and 2002 as detailed below.

In spite of the difficult environment confronting the communications industry today, we believe that the long-term prospects for the markets that we participate in remain strong.

Restructuring Costs Fiscal 2001

In the third quarter of fiscal 2001, we announced a restructuring plan as a result of the decreased demand for our products and to align our cost structure with the business environment at that time. This restructuring plan included a reduction of our workforce by 12% and consolidation of excess facilities, which resulted in impairment of goodwill and intangible assets. As a result of implementing the restructuring plan, we incurred a charge of $26.6 million in fiscal 2001.

Included in the restructuring charge were workforce reduction costs of $2.0 million, primarily related to severance and fringe benefits. The termination of these 165 employees was completed in the quarter ended June 30, 2001, primarily within our manufacturing and research and development operations. We began to realize annual payroll and benefits savings in the amount of approximately $9.5 million commencing June 2001 as a result of this action.

The consolidation of excess facilities resulted in a charge of $1.7 million, which represents lease terminations, non-cancelable lease costs and write-off of leasehold improvements and equipment and will be paid over the respective lease terms through October 2003. The facilities that were closed or consolidated were as follows:

Location | Description | |

| Clark, NJ | Design center, 3,917 sq. ft. | |

| Framingham, MA | Design center, 20,000 sq. ft. | |

| Santa Clara, CA | Design center, 21,842 sq. ft. | |

| Santa Clara, CA | Sales and design office, 4,297 sq. ft. |

18

Table of Contents

The four facilities listed above were closed between May and September 2001. The individuals affected were primarily engineers working in projects that we decided to curtail or terminate. Our charge of $1.7 million was approximately 64% of the estimated future obligations for those sites. Depending on our ability to sublease the excess facilities, we will realize annualized savings in the form of lower rent expense of approximately $0.5 million in fiscal 2003.

We also performed a review of our product development efforts, which involved comparing the time and costs required to bring the products to completion and considered the estimated amount of revenues that these products could generate. Based on our assessment, we decided to cease development of those products that were not expected to yield an adequate return on investment. We also decided to augment resources allocated to products that we expect would generate the highest revenues in the near-term. Specifically, we decided to terminate the development of certain products targeted at long-haul SONET applications within the telecommunications core and to supplement our efforts on products targeting the metro, storage and enterprise markets. Many of these products that were cancelled were being developed by the design of two companies that we had previously acquired—Vermont Scientific Technologies, Inc. (“VTEK”) and Kalman Saffran Associates, Inc. (“KSA”). In light of the cancellation of these products and our plan to discontinue further development of portions of the technology acquired in the purchase of VTEK and KSA, we recorded a charge of $22.9 million related to the impairment of goodwill and intangible assets associated with those acquisitions. The charge was measured as the amount by which the carrying amount exceeded the present value of operating cash flows expected to be generated by these assets. As a result of the significant reduction in headcount of these two acquired businesses, we placed the remaining employees under common management and closed one of the two KSA facilities. Additionally, we realigned the design efforts of the combined team to focus on a narrower set of products that we believed would generate a high return on investment. Failure to achieve the revised levels of revenues and net income will negatively impact the revised return on investment and may result in further impairment of goodwill and intangible assets related to VTEK and KSA. The charge that we recorded for impairment of goodwill and intangible assets resulted in a $2.3 million annualized reduction in amortization costs starting June 2001.

Restructuring Costs Fiscal 2002

In the first quarter of fiscal 2002, we announced a restructuring plan as a result of the continued decrease in demand for our products, a shift in the industry’s technology and the need to align our cost structure with significantly reduced revenue levels. In the third quarter of fiscal 2002, we announced additional steps to restructure our operations as a result of continued adverse business conditions, a faster shift in technology away from our internal manufacturing process toward advanced outsourced CMOS-based processes, and a slower than previously expected trend in the outsourcing of products to semiconductor vendors such as Vitesse. This restructuring plan included the termination of certain product lines, curtailment of certain research and development projects, a resulting workforce reduction, and the consolidation of excess facilities. In connection with this restructuring, we also wrote down certain fixed assets which were deemed to be impaired, and accrued costs associated with non-cancelable equipment and software contracts. The summary of restructuring costs for fiscal 2002 are outlined as follows (in thousands) :

Total Charge | Noncash Charges | Cash Payments | Balance at September 30, 2002 | |||||||||

| Workforce reduction | $ | 4,058 | — | (3,455 | ) | $ | 603 | |||||

| Consolidation of excess facilities | 3,855 | — | (947 | ) | 2,908 | |||||||

| Impairment of assets | 170,363 | (170,363 | ) | — | — | |||||||

| Contract settlement costs | 34,221 | — | (2,714 | ) | 31,507 | |||||||

| Total | $ | 212,497 | (170,363 | ) | (7,116 | ) | $ | 35,018 | ||||

19

Table of Contents

Workforce reduction includes the cost of severance and related benefits of 130 employees affected by the November 2001 restructuring and the related costs for 183 employees affected by the July 2002 restructuring. The remaining benefits are expected to be paid out in the quarter ending December 31, 2002. We began to realize annual payroll and benefits savings in the amount of approximately $29.7 million commencing in August 2002 as a result of these actions.

The excess facilities charge includes lease termination payments, non-cancelable lease costs and write off of leasehold improvements and office equipment related to these leases. The consolidation of our excess facilities resulted in a charge of $3.9 million in fiscal 2002. These costs will be paid over the respective lease terms through February 2004. The facilities that were closed or consolidated are as follows:

Location | Description | |

| Frederick, MD | Sales office, 625 sq. ft. | |

| Wayzata, MN | Sales office, 711 sq. ft. | |

| Lake Oswego, OR | Sales office, 3,565 sq. ft. | |

| Woodstock, VT | Design center, 2,632 sq. ft. | |

| San Jose, CA | Design center, 20,100 sq. ft. | |

| Camarillo, CA | Warehouse space, 18,950 sq. ft. | |

| Longmont, CO | Design center, 24,588 sq. ft. | |

| Morrisville, NC | Design center and sales office, 12,341 sq. ft. |

The eight facilities listed above were closed between November 2001 and November 2002. The individuals affected were primarily engineers working in projects that we decided to curtail or terminate. Our charge of $3.9 million was approximately 95% of the estimated future obligations for those sites. Depending on our ability to sublease the excess facilities, we will realize annualized savings in the form of lower rent expense of approximately $1.8 million.

The impairment of assets charge includes the write down of certain excess manufacturing equipment, including fabrication and test equipment, and prepaid maintenance contracts associated with that equipment. This charge also included the write off of certain software licenses and future software license purchase commitments under non-cancelable agreements associated with research and development employment positions which were eliminated as a result of the cancellation of non-strategic and unprofitable projects. The impairment of assets resulted in a charge of $170.4 million in fiscal 2002.

In the first quarter of 2002, we recorded an asset impairment charge of $63.2 million for the following reasons. First, the evolution of our products from the legacy GaAs process to mainstream processes such as CMOS, as well as emerging technologies such as Indium Phosphide was making much of our internal fabrication equipment obsolete faster than we had anticipated. As a result of this technology shift, we converted a majority of the fabrication equipment in our Camarillo facility to run the InP process, with the expectation that we would not run a GaAs process in Camarillo after the third quarter of fiscal 2002. Second, the Colorado fabrication facility has several pieces of equipment that were put in place for a significantly higher level of capacity. As we scaled down manufacturing of GaAs based products from the already low levels, the likelihood that we would ever use this equipment was remote. Additionally, our test facilities had planned for annual revenue levels in excess of $750.0 million, compared to the current expected revenue of $200.0 million per year. Therefore, we decided to close the Colorado test facility and transfer some of the equipment to Camarillo. The remaining equipment is likely to remain idle for an indefinite period of time. Finally, we reduced our engineering work force and discontinued the development of certain products, which resulted in the impairment of software, tooling and masks associated with these products.

The asset impairment charge of $63.2 million was determined based on the held for disposal or abandonment model. Under this model, all long-lived assets and certain identifiable intangibles to be disposed of,

20

Table of Contents