| (3) | Preliminary goodwill arising from the ETFS Acquisition represents the value of expected synergies created from combining the operations of ETFS and the Company. The goodwill is not deductible for tax purposes as the transaction was structured as a stock acquisition occurring in the United Kingdom. |

The Company has until August 31, 2018 to satisfy itself with the opening balance sheet delivered by ETFS Capital. Pursuant to Clause 4.2 of the Share Sale Agreement, if the Completion Working Capital Amount (as defined) is greater than the Target Working Capital Amount (as defined), then the Company will owe ETFS Capital the excess amount. At June 30, 2018, this excess is $7,033 which is recorded as a payable to ETFS Capital on the Company’s consolidated balance sheet. Any changes to the opening balance sheet may result in an adjustment to the amount owed to ETFS Capital, or alternatively, goodwill. All other elements of the purchase price allocation are finalized.

Acquisition-Related Costs

During the three and six months ended June 30, 2018, the Company incurred acquisition-related costs associated with the ETFS Acquisition of $7,928 and $9,990, respectively, which included professional advisor fees, severance and other compensation costs, awrite-off of the Company’s office lease and other integration costs.

Operating Results of ETFS

The Company’s Consolidated Statements of Operations include the following operating results of ETFS since the acquisition date of April 11, 2018 through June 30, 2018:

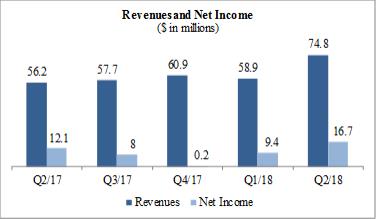

Revenues: $22,934

Income before taxes: $18,102 (including a gain on revaluation of deferred consideration of $9,898)

Supplemental Unaudited Pro Forma Financial Information

The following table presents unaudited pro forma financial information of the Company as if the ETFS Acquisition had been consummated on January 1, 2017. The information was derived from the historical financial results of the Company and ETFS for all periods presented and was adjusted to give effect to pro forma events that are directly attributable to the acquisition, factually supportable and expected to have a continuing impact on the combined results following the acquisition.

| | | | | | | | | | | | | | | | |

| | | Three Months Ended June 30, | | | Six Months Ended June 30, | |

| | | 2018 | | | 2017 | | | 2018 | | | 2017 | |

Revenues | | $ | 78,025 | | | $ | 76,718 | | | $ | 157,796 | | | $ | 149,410 | |

Net income | | $ | 23,274 | | | $ | 15,554 | | | $ | 34,517 | | | $ | 17,451 | |

Included within the proforma financial information above is a gain/(loss) on revaluation of deferred consideration of $8,326 and $319 for the three months ended June 30, 2018 and 2017, respectively, and $5,771 and ($8,039) for the six months ended June 30, 2018 and 2017, respectively. Significant adjustments to the unaudited pro forma financial information above include the recognition of interest expense associated with the Credit Facility for the periods presented, eliminating acquisition-related costs directly attributable to the acquisition and adjusting consolidated income tax expense based upon the Company’s anticipated normalized consolidated effective tax rate.

The unaudited pro forma financial information above is not necessarily indicative of what the combined results of the Company would have been had the acquisition been completed as of January 1, 2017 and does not purport to project the future results of the combined company. In addition, the unaudited pro forma financial information does not reflect any future planned cost savings initiatives following the completion of the acquisition.

4. Cash and Cash Equivalents

Cash and cash equivalents of approximately $31,805 and $24,103 at June 30, 2018 and December 31, 2017, respectively, were held at one financial institution. At June 30, 2018 and December 31, 2017, cash equivalents were approximately $4,701 and $26,548, respectively.

5. Fair Value Measurements

Securities owned and securities sold, but not yet purchased are measured at fair value. The fair value of securities is defined as the price that would be received to sell an asset or paid to transfer a liability (i.e., “the exit price”) in an orderly transaction between market participants at the measurement date. Accounting Standards Codification (“ASC”) 820,Fair Value Measurements, establishes a hierarchy for inputs used in measuring fair value that maximizes the use of observable inputs and minimizes the use of unobservable inputs by requiring that the most observable inputs be used when available. Observable inputs are inputs that market participants would use in pricing the asset or liability developed based on market data obtained from independent sources. Unobservable inputs reflect assumptions that market participants would use in pricing the asset or liability developed based on the best information available in the circumstances. The hierarchy is broken down into three levels based on the transparency of inputs as follows:

15