Exhibit 99.1

Valassis

Investor Presentation

September 2007

Safe Harbor

Certain statements found in this document constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Such forward-looking statements involve known and unknown risks and uncertainties and other factors which may cause the actual results, performance or achievements of the Company to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. Such factors include, among others, the following: price competition from the Company’s existing competitors; new competitors in any of the Company’s businesses; a shift in customer preference for different promotional materials, strategies or coupon delivery methods; an unforeseen increase in the Company’s paper or postal costs; changes which affect the businesses of the Company’s customers and lead to reduced sales promotion spending; challenges and costs of achieving synergies and cost savings in connection with the ADVO acquisition and integrating ADVO’s operations may be greater than expected; the Company’s substantial indebtedness, and its ability to incur additional indebtedness, may affect the Company’s financial health; certain covenants in the Company’s debt documents could adversely restrict the Company’s financial and operating flexibility; fluctuations in the amount, timing, pages and weight, and kinds of advertising pieces from period to period, due to a change in the Company’s customers’ promotional needs, inventories and other factors; the Company’s failure to attract and retain qualified personnel may affect its business and results of operations; a rise in interest rates could increase the Company’s borrowing costs; the outcome of ADVO’s pending shareholder lawsuits; possible governmental regulation or litigation affecting aspects of the Company’s business; and general economic conditions, whether nationally or in the market areas in which the Company conducts its business, may be less favorable than expected. These and other risks and uncertainties related to the Company’s business are described in greater detail in its filings with the United States Securities and Exchange Commission, including the Company’s reports on Forms 10-K and 10-Q, and the foregoing information should be read in conjunction with these filings. The Company disclaims any intention or obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

Slide 1

Valassis delivers…

Customers need…

• Targeted communications

• Scalability

• Multi-product solutions

• Measurability of results

• Favorable ROI

Consumers want…

Control

• To block unwanted marketing

• To opt-in to relevant media messages

Value

• Financial

• Informational

• Entertainment

• Social/community

Consumer Marketing Spend

Public Relations

General Advertising

DIRECT MARKETING SOLUTIONS

Objective: Revenue Generation

• Newspaper-delivered Solutions

• Solo Direct Mail

• In-store

• Direct-to-Door/Consumer

• Direct Marketing Services

• Shared Mail

• Electronic

Slide 2

Customer Relationships & Value-oriented Content

®

As consumer preferences change, we will repurpose content to match their preferences

Valassis is the leader in delivering value-oriented content to consumers how, when and where they want.

Slide 3

Delivering value to consumers - how, when and where they want

In-store

Industry Size: $1 billion Strategy: Growth

Direct Mail

Industry Size: $33 billion

Valassis-ADVO Revenue*: $1.5 billion Strategy: Growth and Grow Share

Interactive

Industry Size: $18 billion Strategy: Growth

Sampling

Industry Size: $2 billion Valassis-ADVO Revenue*: $57 million Strategy: Grow Share

Newspaper

Industry Size/Valassis-ADVO Revenue*: ROP: $25 billion/$117 million FSI: $1 billion/$441 million Preprint: $14 billion/$258 million Strategy: Grow Share

*Revenue figures based on Valassis and ADVO 2006 calendar year revenue.

Slide 4

Sales Initiatives - Recognizing Revenue Synergies

Completed:

Integrated New Account Development, Direct Response and six Strategic Account sales teams

More powerful value proposition to drive new customer acquisition

Integrated Sales Planning and Development

Harmonize communications and accelerate training & development

Defined customer value proposition

Targeting, scalability, broad product portfolio and consumer insight

Conducted “Sales Roadshow”

Met with 700 sales people and 25+ key customers

Launched short-term compensation plan for the second half of 2007

Focus on lead generation, up-selling, collaboration and wrap sales

Slide 5

Sales Initiatives - Recognizing Revenue Synergies

Now and Ongoing:

Refocus ADVO field sales on local accounts

Profitable, defendable, consumer relevancy

Execute ADVO market share initiatives

Market-specific sales strategies to increase shared mail market share

Leverage immediate cross-selling opportunities

Supplement newspaper distribution with shared mail

Use ADVO grocery relationships to enhance in-store networks

Insert the FSI into ADVO shared mail packages

Create differentiation and lower costs

Slide 6

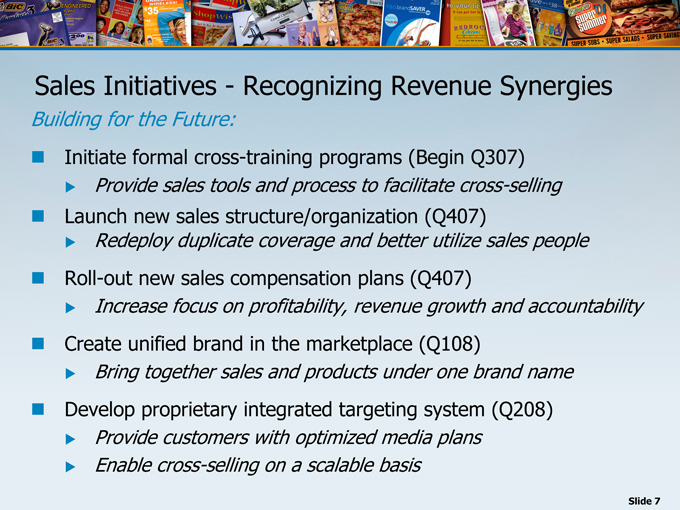

Sales Initiatives - Recognizing Revenue Synergies

Building for the Future:

Initiate formal cross-training programs (Begin Q307)

Provide sales tools and process to facilitate cross-selling

Launch new sales structure/organization (Q407)

Redeploy duplicate coverage and better utilize sales people

Roll-out new sales compensation plans (Q407)

Increase focus on profitability, revenue growth and accountability

Create unified brand in the marketplace (Q108)

Bring together sales and products under one brand name

Develop proprietary integrated targeting system (Q208)

Provide customers with optimized media plans

Enable cross-selling on a scalable basis

Slide 7

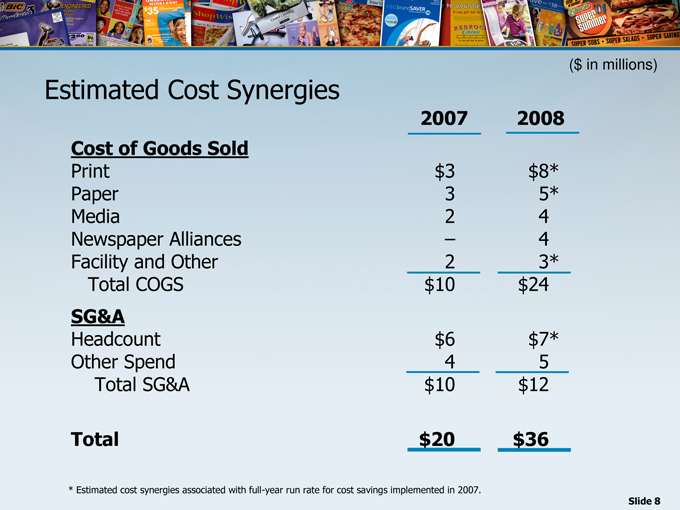

($ in millions)

Estimated Cost Synergies

2007 2008

Cost of Goods Sold

Print $ 3 $8*

Paper 3 5*

Media 2 4

Newspaper Alliances – 4

Facility and Other 2 3*

Total COGS $ 10 $ 24

SG&A

Headcount $ 6 $7*

Other Spend 4 5

Total SG&A $ 10 $ 12

Total $ 20 $ 36

* Estimated cost synergies associated with full-year run rate for cost savings implemented in 2007.

Slide 8

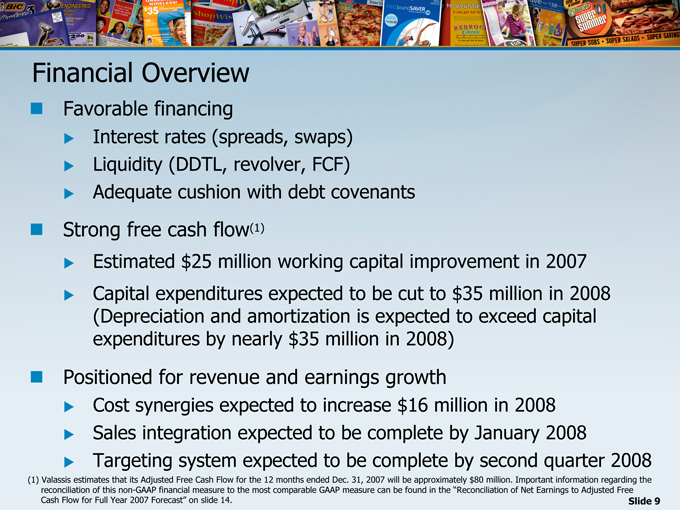

Financial Overview

Favorable financing

Interest rates (spreads, swaps)

Liquidity (DDTL, revolver, FCF)

Adequate cushion with debt covenants

Strong free cash flow(1)

Estimated $25 million working capital improvement in 2007

Capital expenditures expected to be cut to $35 million in 2008 (Depreciation and amortization is expected to exceed capital expenditures by nearly $35 million in 2008)

Positioned for revenue and earnings growth

Cost synergies expected to increase $16 million in 2008

Sales integration expected to be complete by January 2008

Targeting system expected to be complete by second quarter 2008

(1) Valassis estimates Adjusted Free Cash Flow for the 12 months ended Dec. 31, 2007 will be approximately $80 million. Important information regarding the reconciliation of this non-GAAP financial measure to the most comparable GAAP measure can be found in the “Reconciliation of Net Earnings to Adjusted Free Cash Flow for Full Year 2007 Forecasts” that its on slide 14. Slide 9

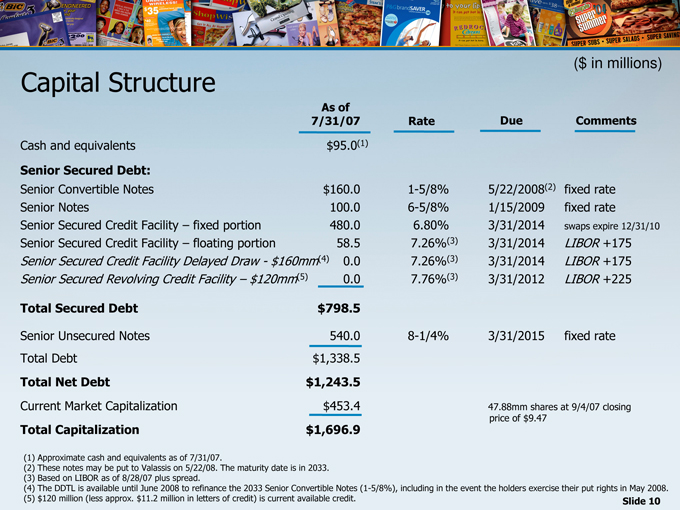

($ in millions)

Capital Structure

As of

7/31/07 Rate Due Comments

Cash and equivalents $ 95.0(1)

Senior Secured Debt:

Senior Convertible Notes $ 160.0 1-5/8% 5/22/2008(2) fixed rate

Senior Notes 100.0 6-5/8% 1/15/2009 fixed rate

Senior Secured Credit Facility – fixed portion 480.0 6.80% 3/31/2014 swaps expire 12/31/10

Senior Secured Credit Facility – floating portion 58.5 7.26%(3) 3/31/2014 LIBOR +175

Senior Secured Credit Facility Delayed Draw - $160mm (4) 0.0 7.26%(3) 3/31/2014 LIBOR +175

Senior Secured Revolving Credit Facility – $120mm(5) 0.0 7.76%(3) 3/31/2012 LIBOR +225

Total Secured Debt $ 798.5

Senior Unsecured Notes 540.0 8-1/4% 3/31/2015 fixed rate

Total Debt $ 1,338.5

Total Net Debt $ 1,243.5

Current Market Capitalization $ 453.4 47.88mm shares at 9/4/07 closing

price of $ 9.47

Total Capitalization $ 1,696.9

(1) Approximate cash and equivalents as of 7/31/07.

(2) These notes may be put to Valassis on 5/22/08. The maturity date is in 2033. (3) Based on LIBOR as of 8/28/07 plus spread.

(4) The DDTL is available until June 2008 to refinance the 2033 Senior Convertible Notes (1-5/8%), including in the event the holders exercise their put rights in May 2008. (5) $120 million (less approx. $11.2 million in letters of credit) is current available credit. Slide 10

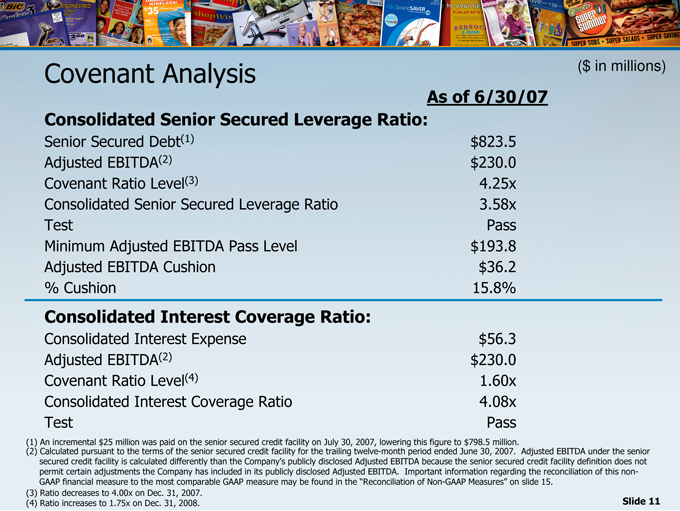

($ in millions)

Covenant Analysis

As of 6/30/07

Consolidated Senior Secured Leverage Ratio:

Senior Secured Debt(1) $ 823.5

Adjusted EBITDA(2) $ 230.0

Covenant Ratio Level(3) 4.25x

Consolidated Senior Secured Leverage Ratio 3.58x

Test Pass

Minimum Adjusted EBITDA Pass Level $ 193.8

Adjusted EBITDA Cushion $ 36.2

% Cushion 15.8%

Consolidated Interest Coverage Ratio:

Consolidated Interest Expense $ 56.3

Adjusted EBITDA(2) $ 230.0

Covenant Ratio Level(4) 1.60x

Consolidated Interest Coverage Ratio 4.08x

Test Pass

(1) An incremental $25 million was paid on the senior secured credit facility on July 30, 2007, lowering this figure to $798.5 million.

(2) Calculated pursuant to the terms of the senior secured credit facility for the trailing twelve-month period ended June 30, 2007. Adjusted EBITDA under the senior secured credit facility is calculated differently than the Company’s publicly disclosed Adjusted EBITDA because the senior secured credit facility definition does not permit certain adjustments the Company has included in its publicly disclosed Adjusted EBITDA. Important information regarding the reconciliation of this non-GAAP financial measure to the most comparable GAAP measure may be found in the “Reconciliation of Non-GAAP Measures” on slide 15.

(3) Ratio decreases to 4.00x on Dec. 31, 2007.

(4) Ratio increases to 1.75x on Dec. 31, 2008. Slide 11

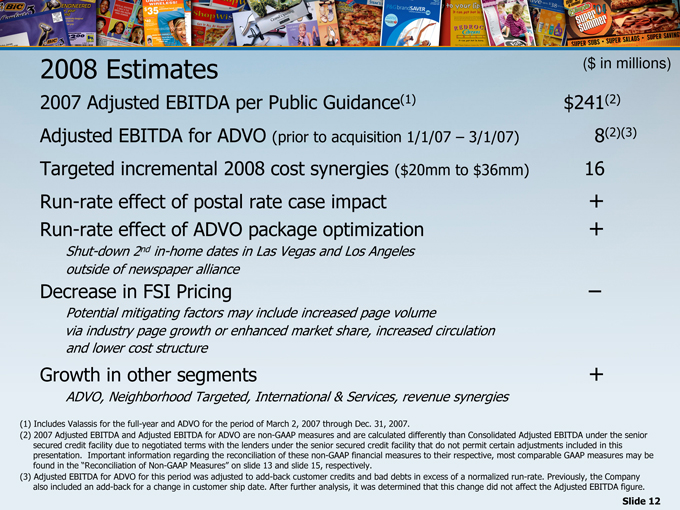

2008 Estimates ($ in millions)

2007 Adjusted EBITDA per Public Guidance(1) $ 241(2)

Adjusted EBITDA for ADVO (prior to acquisition 1/1/07 – 3/1/07) 8(2)(3)

Targeted incremental 2008 cost synergies ($20mm to $36mm) 16

Run-rate effect of postal rate case impact +

Run-rate effect of ADVO package optimization +

Shut-down 2nd in-home dates in Las Vegas and Los Angeles

outside of newspaper alliance

Decrease in FSI Pricing /

Potential mitigating factors may include increased page volume

via industry page growth or enhanced market share, increased circulation

and lower cost structure

Growth in other segments +

ADVO, Neighborhood Targeted, International & Services, revenue synergies

(1) Includes Valassis for the full-year and ADVO for the period of March 2, 2007 through Dec. 31, 2007.

(2) 2007 Adjusted EBITDA and Adjusted EBITDA for ADVO are non-GAAP measures and are calculated differently than Consolidated Adjusted EBITDA under the senior secured credit facility due to negotiated terms with the lenders under the senior secured credit facility that do not permit certain adjustments included in this presentation. Important information regarding the reconciliation of these non-GAAP financial measures to their respective, most comparable GAAP measures may be found in the “Reconciliation of Non-GAAP Measures” on slide 13 and slide 15, respectively. (3) Adjusted EBITDA for ADVO for this period was adjusted to add-back customer credits and bad debts in excess of a normalized run-rate. Previously, the Company also included an add-back for a change in customer ship date. After further analysis, it was determined that this change did not affect the Adjusted EBITDA figure.

Slide 12

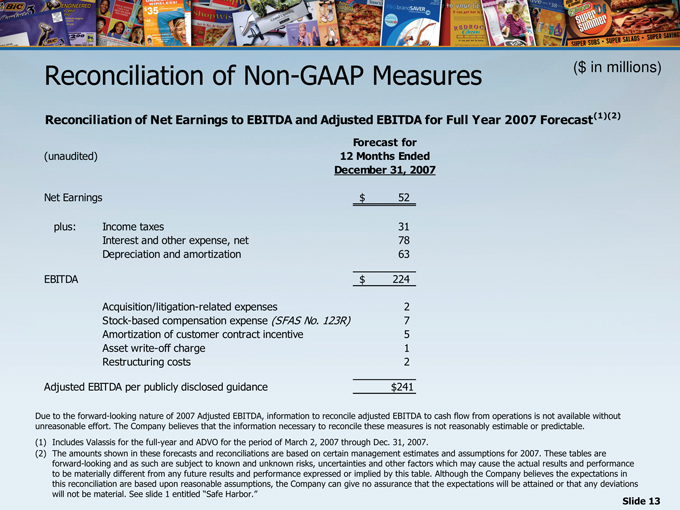

Reconciliation of Non-GAAP Measures($ in millions)

Reconciliation of Net Earnings to EBITDA and Adjusted EBITDA for Full Year 2007 Forecast(1)(2)

Forecast for

(unaudited) 12 Months Ended

December 31, 2007

Net Earnings $ 52

plus: Income taxes 31

Interest and other expense, net 78

Depreciation and amortization 63

EBITDA $ 224

Acquisition/litigation-related expenses 2

Stock-based compensation expense (SFAS No. 123R) 7

Amortization of customer contract incentive 5

Asset write-off charge 1

Restructuring costs 2

Adjusted EBITDA per publicly disclosed guidance $ 241

Due to the forward-looking nature of 2007 Adjusted EBITDA, information to reconcile adjusted EBITDA to cash flow from operations is not available without unreasonable effort. The Company believes that the information necessary to reconcile these measures is not reasonably estimable or predictable.

(1) Includes Valassis for the full-year and ADVO for the period of March 2, 2007 through Dec. 31, 2007.

(2) The amounts shown in these forecasts and reconciliations are based on certain management estimates and assumptions for 2007. These tables are forward-looking and as such are subject to known and unknown risks, uncertainties and other factors which may cause the actual results and performance to be materially different from any future results and performance expressed or implied by this table. Although the Company believes the expectations in this reconciliation are based upon reasonable assumptions, the Company can give no assurance that the expectations will be attained or that any deviations will not be material. See slide 1 entitled “Safe Harbor.”

Slide 13

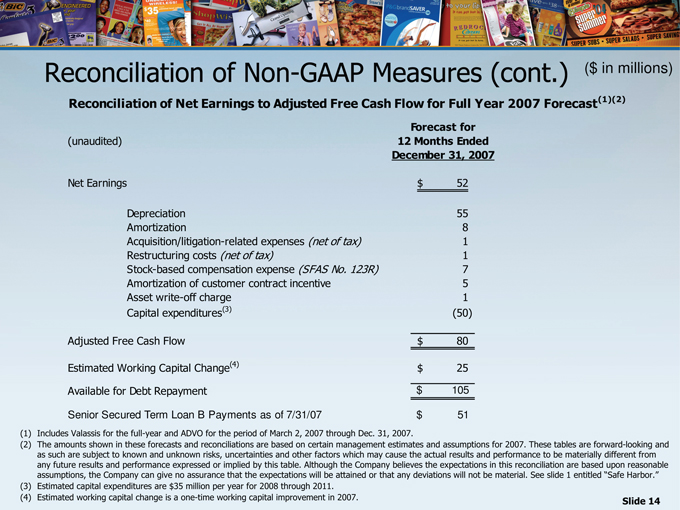

Reconciliation of Non-GAAP Measures (cont.) ($ in millions)

Reconciliation of Net Earnings to Adjusted Free Cash Flow for Full Year 2007 Forecast(1)(2)

Forecast for

(unaudited) 12 Months Ended

December 31, 2007

Net Earnings $ 52

Depreciation 55

Amortization 8

Acquisition/litigation-related expenses (net of tax) 1

Restructuring costs (net of tax) 1

Stock-based compensation expense (SFAS No. 123R) 7

Amortization of customer contract incentive 5

Asset write-off charge 1

Capital expenditures(3) (50)

Adjusted Free Cash Flow $ 80

Estimated Working Capital Change(4) $ 25

Available for Debt Repayment $ 105

Senior Secured Term Loan B Payments as of 7/31/07 $ 51

(1) Includes Valassis for the full-year and ADVO for the period of March 2, 2007 through Dec. 31, 2007.

(2) The amounts shown in these forecasts and reconciliations are based on certain management estimates and assumptions for 2007. These tables are forward-looking and as such are subject to known and unknown risks, uncertainties and other factors which may cause the actual results and performance to be materially different from any future results and performance expressed or implied by this table. Although the Company believes the expectations in this reconciliation are based upon reasonable assumptions, the Company can give no assurance that the expectations will be attained or that any deviations will not be material. See slide 1 entitled “Safe Harbor.” (3) Estimated capital expenditures are $35 million per year for 2008 through 2011.

(4) Estimated working capital change is a one-time working capital improvement in 2007.

Slide 14

($ in millions)

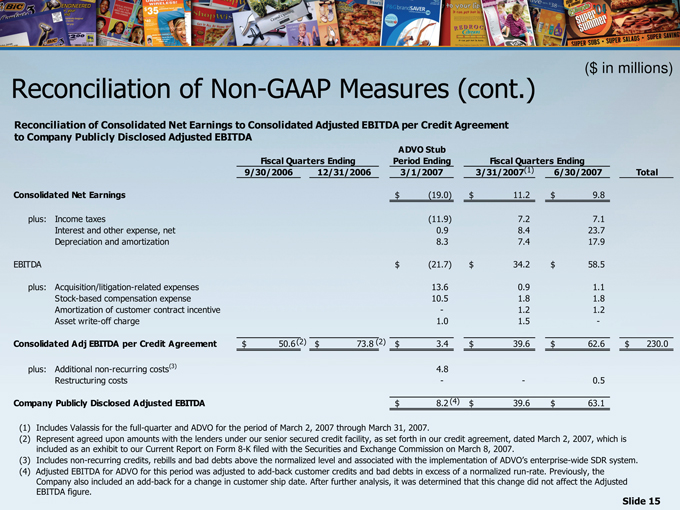

Reconciliation of Non-GAAP Measures (cont.)

Reconciliation of Consolidated Net Earnings to Consolidated Adjusted EBITDA per Credit Agreement to Company Publicly Disclosed Adjusted EBITDA

ADVO Stub

Fiscal Quarters Ending Period Ending Fiscal Quarters Ending

9/30/2006 12/31/2006 3/1/2007 3/31/2007(1) 6/30/2007 Total

Consolidated Net Earnings $ (19.0) $ 11.2 $ 9.8

plus: Income taxes (11.9) 7.2 7.1

Interest and other expense, net 0.9 8.4 23.7

Depreciation and amortization 8.3 7.4 17.9

EBITDA $ (21.7) $ 34.2 $ 58.5

plus: Acquisition/litigation-related expenses 13.6 0.9 1.1

Stock-based compensation expense 10.5 1.8 1.8

Amortization of customer contract incentive—1.2 1.2

Asset write-off charge 1.0 1.5 -

Consolidated Adj EBITDA per Credit Agreement $ 50.6(2) $ 73.8 (2) $ 3.4 $ 39.6 $ 62.6 $ 230.0

plus: Additional non-recurring costs(3) 4.8

Restructuring costs—- 0.5

Company Publicly Disclosed Adjusted EBITDA $ 8.2(4) $ 39.6 $ 63.1

(1) Includes Valassis for the full-quarter and ADVO for the period of March 2, 2007 through March 31, 2007.

(2) Represent agreed upon amounts with the lenders under our senior secured credit facility, as set forth in our credit agreement, dated March 2, 2007, which is included as an exhibit to our Current Report on Form 8-K filed with the Securities and Exchange Commission on March 8, 2007.

(3) Includes non-recurring credits, rebills and bad debts above the normalized level and associated with the implementation of ADVO’s enterprise-wide SDR system. (4) Adjusted EBITDA for ADVO for this period was adjusted to add-back customer credits and bad debts in excess of a normalized run-rate. Previously, the Company also included an add-back for a change in customer ship date. After further analysis, it was determined that this change did not affect the Adjusted EBITDA figure.

Slide 15

Reconciliation of Non-GAAP Measures (cont.)

We define adjusted EBITDA as net earnings before net interest and other related expenses, income taxes, depreciation, amortization, acquisition/litigation-related expenses, stock-based compensation expense associated with SFAS No. 123R, amortization of a customer contract incentive and other non-cash and non-recurring charges. We define adjusted free cash flow as net earnings plus depreciation, amortization, stock-based compensation expense, acquisition/litigation-related expenses and other non-cash and non-recurring items, less capital expenditures. Adjusted EBITDA and adjusted free cash flow are non-GAAP financial measures commonly used by financial analysts, investors, rating agencies and other interested parties in evaluating companies, including marketing services companies. Accordingly, management believes that adjusted EBITDA and adjusted free cash flow may be useful in assessing our operating performance and our ability to meet our debt service requirements. However, these non-GAAP financial measures have limitations as analytical tools and should not be considered in isolation from, or as an alternative to, operating income, cash flow or other income or cash flow data prepared in accordance with GAAP. Some of these limitations are:

3 adjusted EBITDA does not reflect our cash expenditures for capital equipment or other contractual commitments;

3 although depreciation and amortization are non-cash charges, the assets being depreciated or amortized may have to be replaced in the future, and adjusted EBITDA does not reflect cash capital expenditure requirements for such replacements; 3 adjusted EBITDA does not reflect changes in, or cash requirements for, our working capital needs; 3 adjusted EBITDA does not reflect the significant interest expense or the cash requirements necessary to service interest or principal payments on our indebtedness; 3 adjusted EBITDA does not reflect income tax expense or the cash necessary to pay income taxes; 3 adjusted EBITDA does not reflect the impact of earnings or charges resulting from matters we consider not to be indicative of our ongoing operations; 3 adjusted free cash flow does not represent our residual cash flow available for discretionary expenditures since we have mandatory debt service requirements and other required expenditures that are not deducted from adjusted free cash flow; 3 adjusted free cash flow does not capture debt repayment and/or the receipt of proceeds from the issuance of debt; and 3 other companies, including companies in our industry, may calculate these measures differently and as the number of differences in the way two different companies calculate these measures increases, the degree of their usefulness as a comparative measure correspondingly decreases.

Because of these limitations, adjusted EBITDA and adjusted free cash flow should not be considered as measures of discretionary cash available to us to invest in the growth of our business or reduce indebtedness. We compensate for these limitations by relying primarily on our GAAP results and using these non-GAAP financial measures only as a supplement.

Slide 16

Investment Considerations

Leader in Value-oriented Content

Unmatched Product Offering

Unparalleled Coverage

Flexible Targeting Capabilities

Diversified Blue Chip Customer Base

Leading Capabilities and Services

Experienced Operating Management Team

Balanced Capital Structure

Valassis

Slide 17

QUESTIONS?