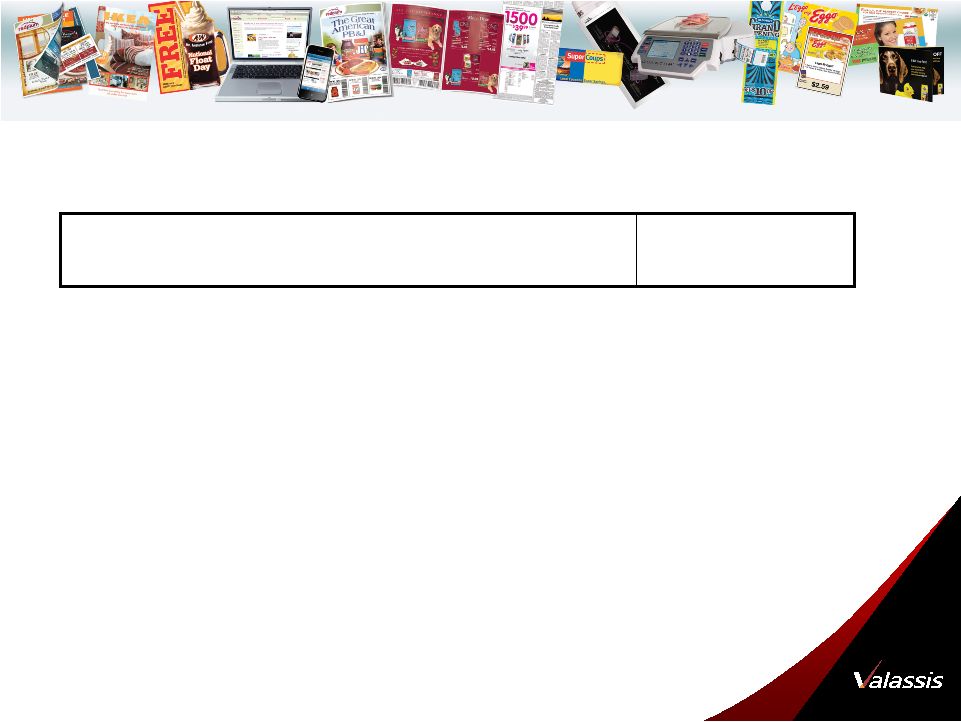

16 ® Reconciliation of Non-GAAP Measure Non-GAAP Financial Measures *We define adjusted EBITDA as earnings before net interest expense, other non-cash expenses (income), net, income taxes, depreciation, amortization, stock-based compensation expense associated with SFAS No. 123R, non-recurring restructuring and severance costs and amortization of a client contract incentive. Adjusted EBITDA is a non-GAAP financial measure commonly used by financial analysts, investors, rating agencies and other interested parties in evaluating companies, including marketing services companies. Accordingly, management believes that adjusted EBITDA may be useful in assessing our operating performance and our ability to meet our debt service requirements. In addition, adjusted EBITDA is used by management to measure and analyze our operating performance and, along with other data, as our internal measure for setting annual operating budgets, assessing financial performance of business segments and as a performance criteria for incentive compensation. However, this non-GAAP financial measure has limitations as an analytical tool and should not be considered in isolation from, or as an alternative to, operating income, cash flow or other income or cash flow data prepared in accordance with GAAP. Some of these limitations are: adjusted EBITDA does not reflect our cash expenditures for capital equipment or other contractual commitments; although depreciation and amortization are non-cash charges, the assets being depreciated or amortized may have to be replaced in the future, and adjusted EBITDA does not reflect cash capital expenditure requirements for such replacements; adjusted EBITDA does not reflect changes in, or cash requirements for, our working capital needs; adjusted EBITDA does not reflect the significant interest expense or the cash requirements necessary to service interest or principal payments on our indebtedness; adjusted EBITDA does not reflect income tax expense or the cash necessary to pay income taxes; adjusted EBITDA does not reflect the impact of earnings or charges resulting from matters we consider not to be indicative of our ongoing operations; and other companies, including companies in our industry, may calculate this measure differently and as the number of differences in the way two different companies calculate this measure increases, the degree of its usefulness as a comparative measure correspondingly decreases. Because of these limitations, adjusted EBITDA should not be considered as a measure of discretionary cash available to us to invest in the growth of our business or reduce indebtedness. We compensate for these limitations by relying primarily on our GAAP results and using this non-GAAP financial measure only supplementally. Further important information regarding operating results and reconciliations of this non-GAAP financial measure to the most comparable GAAP measures can be found below. |