UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number

(Exact name of registrant as specified in charter)

610 Market Street

Philadelphia, PA 19106

Registrant's telephone number, including area code:

Date of reporting period:

Item 1. Report to Stockholders.

(a) The registrant’s annual report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 is as follows:

Delaware Ivy Multi-Asset Income Fund

Class A: IMAAX

Annual shareholder report | September 30, 2024

This annual shareholder report contains important information about Delaware Ivy Multi-Asset Income Fund (Fund) for the period of October 1, 2023, to September 30, 2024. You can find additional information about the Fund at delawarefunds.com/literature. You can also request this information by contacting us at 800 523-1918, weekdays from 8:30am to 6:00pm ET.

This report describes changes to the Fund that occurred during the reporting period.

What were the Fund's costs for the last 12 months?

(Based on a hypothetical $10,000 investment)

| Class | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

| Class A | $109 | 1.00% |

Management’s discussion of Fund performance

Performance highlights

Delaware Ivy Multi-Asset Income Fund (Class A) returned 17.33% (excluding sales charge) for the 12 months ended September 30, 2024. During the same period, the MSCI ACWI (All Country World Index) Index (net), MSCI ACWI Index (gross), and Bloomberg US Aggregate Index, the Fund's broad-based securities market indices, returned 31.76%, 32.35%, and 11.57%, respectively, while the current blended benchmark*, the Fund's narrowly based securities market index, returned 23.54%.

The Delaware Ivy Multi-Asset Income Fund is a real assets portfolio that aims to provide capital appreciation and income, inflation protection, and diversification with a dynamic, multi-asset allocation framework built on market assessments using pairwise views by an experienced multi-asset allocation team with specialized experts in each asset class.

During the period, the asset classes in scope for the Fund that delivered the highest returns were:

Global equities

Global listed infrastructure

Global real estate

The asset classes in scope for the Fund with the lowest returns during the period were:

Global natural resources

Investment grade fixed income

High yield fixed income

The largest detractor from performance relative to the blended benchmark of the Fund was an underweight to global equities combined with a negative selection effect within global equities primarily due to the extremely strong performance from US equities, particularly within the growth style cohort and mega-cap technology stocks. Additional detractors to relative performance included the underperformance of global natural resources and both investment grade and high yield fixed income relative to global equities.

These headwinds were partially offset by the positive effects of overweight allocations to global real estate and global listed infrastructure, which provided very strong returns more in-line with global equities during the period.

*The blended benchmark is computed using a combination of 50% MSCI ACWI Index (net) / 50% ICE BofA US High Yield Index.

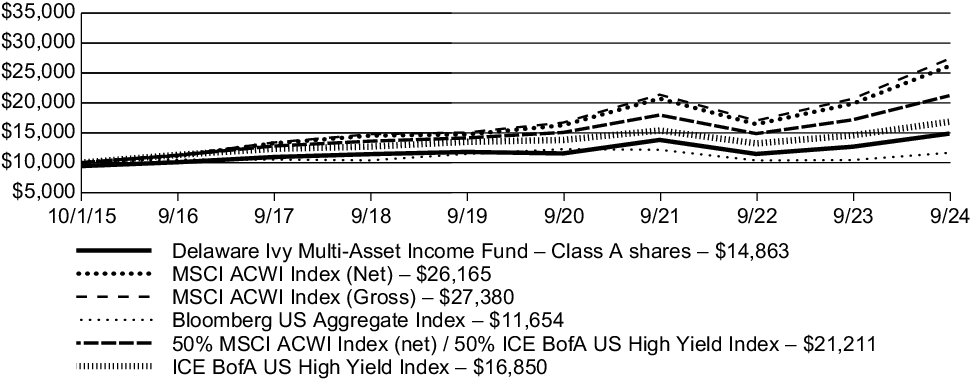

Fund performance

The following graph compares the initial and subsequent account values at the end of each of the most recently completed fiscal years (or period) of the Class for the life of the Class. It also assumes a $10,000 initial investment at the Class's inception date in multiple broad-based securities market indices and multiple narrowly based securities market indices for the same period and the deduction of the maximum applicable sales charge for Class A shares.

Growth of $10,000 investment

For the period October 1, 2015 (Class A's inception), through September 30, 2024

| Average annual total returns (as of September 30, 2024) | 1 year | 5 year | Since inception

(10/1/15) |

| Delaware Ivy Multi-Asset Income Fund (Class A) – including sales charge | 10.53 | % | 3.49 | % | 4.50 | % |

| Delaware Ivy Multi-Asset Income Fund (Class A) – excluding sales charge | 17.33 | % | 4.73 | % | 5.19 | % |

| MSCI ACWI Index (net) | 31.76 | % | 12.19 | % | 11.27 | % |

| MSCI ACWI Index (gross) | 32.35 | % | 12.72 | % | 11.83 | % |

| Bloomberg US Aggregate Index | 11.57 | % | 0.33 | % | 1.72 | % |

| 50% MSCI ACWI Index / 50% ICE BofA US High Yield Index | 23.54 | % | 8.45 | % | 8.71 | % |

| ICE BofA US High Yield Index | 15.66 | % | 4.55 | % | 5.97 | % |

Keep in mind that the Fund's past performance is not a good predictor of how the Fund will perform in the future.

Visit delawarefunds.com/performance for the most recent performance information. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. Performance results reflect any expense caps in effect during these periods. All results shown assume reinvestment of distributions.

In connection with new regulatory requirements, effective the date of this report, the Fund changed its broad-based securities market benchmark index to the MSCI ACWI Index and the Bloomberg US Aggregate Index. Although the MSCI ACWI Index and the Bloomberg US Aggregate Index can be considered broadly representative of the overall securities market applicable to the Fund, the Fund will continue to show the performance of the blended benchmark for comparative purposes because Delaware Management Company, the Fund's manager, believes it is more representative of the Fund’s investment universe.

Fund statistics (as of September 30, 2024)

| Fund net assets | $82,514,992 |

| Total number of portfolio holdings | 491 |

| Total advisory fees paid | $155,934 |

| Portfolio turnover rate | 53% |

Fund holdings (as of September 30, 2024)

The tables below show the investment makeup of the Fund, with each category representing a percentage of the total net assets of the Fund.

| Common Stocks | 53.38% |

| Corporate Bonds | 29.81% |

| Exchange-Traded Funds | 7.94% |

| Agency Mortgage-Backed Securities | 3.92% |

| Convertible Bond | 1.26% |

| Non-Agency Commercial Mortgage-Backed Securities | 1.11% |

| Preferred Stocks | 0.76% |

| Short-Term Investments | 0.48% |

| Loan Agreements | 0.37% |

| US Treasury Obligations | 0.08% |

| Diageo | 0.95% |

| Koninklijke Ahold Delhaize | 0.94% |

| SAP | 0.94% |

| Visa Class A | 0.90% |

| Equinix | 0.88% |

| Nestle | 0.87% |

| Unilever | 0.86% |

| Welltower | 0.86% |

| Smith & Nephew | 0.86% |

| Securitas Class B | 0.80% |

For the fiscal year ended September 30, 2024, the Fund’s total annual operating expenses for Class A decreased from 1.06% to 1.00%. In addition, effective February 29, 2024, the Fund modified its principal investment strategies to reflect that Macquarie Investment Management Austria Kapitalanlage AG (MIMAK), the Fund's sub-advisor that is primarily responsible for the day-to-day management of the portfolio, will also manage a tactical / completion sleeve of the Fund and such sleeve will typically vary from 0% to 20% of the Fund's total assets and primarily hold derivatives and exchange-traded funds. Effective February 29, 2024, the Fund also added "Exchange-traded fund risk" as an additional principal investment risk of the Fund.

This is a summary of certain changes to the Fund since the beginning of the reporting period. For more complete information, you may review the Fund's next prospectus, which we expect to be available by January 29, 2025, at delawarefunds.com/literature or upon request at 800 523-1918, weekdays from 8:30am to 6:00pm ET.

Availability of additional information

You can find additional information about the Fund, such as the prospectus, financial information, holdings, and proxy voting information, at delawarefunds.com/literature. You can also request this information by contacting us at 800 523-1918, weekdays from 8:30am to 6:00pm ET, or by contacting your financial intermediary.

Householding

In order to reduce expenses, we will deliver a single copy of prospectuses, proxies, financial reports, and other communication to shareholders with the same residential address, provided they have the same last name or we reasonably believe them to be members of the same family. Unless we are notified otherwise, we will continue to send recipients only one copy of these materials for as long as they remain a shareholder of the Fund. If you would like to receive individual mailings, please call 800 523-1918 or contact your financial intermediary. Your instructions will typically be effective within 30 days of receipt by Delaware Funds by Macquarie® or your financial intermediary. If you choose, you may receive these documents through electronic delivery.

For more information, please scan the QR code at left to navigate to additional hosted material at delawarefunds.com/literature.

Delaware Ivy Multi-Asset Income Fund

Class C: IMACX

Annual shareholder report | September 30, 2024

This annual shareholder report contains important information about Delaware Ivy Multi-Asset Income Fund (Fund) for the period of October 1, 2023, to September 30, 2024. You can find additional information about the Fund at delawarefunds.com/literature. You can also request this information by contacting us at 800 523-1918, weekdays from 8:30am to 6:00pm ET.

This report describes changes to the Fund that occurred during the reporting period.

What were the Fund's costs for the last 12 months?

(Based on a hypothetical $10,000 investment)

| Class | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

| Class C | $189 | 1.75% |

Management’s discussion of Fund performance

Performance highlights

Delaware Ivy Multi-Asset Income Fund (Class C) returned 16.38% (excluding sales charge) for the 12 months ended September 30, 2024. During the same period, the MSCI ACWI (All Country World Index) Index (net), MSCI ACWI Index (gross), and Bloomberg US Aggregate Index, the Fund's broad-based securities market indices, returned 31.76%, 32.35%, and 11.57%, respectively, while the current blended benchmark*, the Fund's narrowly based securities market index, returned 23.54%.

The Delaware Ivy Multi-Asset Income Fund is a real assets portfolio that aims to provide capital appreciation and income, inflation protection, and diversification with a dynamic, multi-asset allocation framework built on market assessments using pairwise views by an experienced multi-asset allocation team with specialized experts in each asset class.

During the period, the asset classes in scope for the Fund that delivered the highest returns were:

Global equities

Global listed infrastructure

Global real estate

The asset classes in scope for the Fund with the lowest returns during the period were:

Global natural resources

Investment grade fixed income

High yield fixed income

The largest detractor from performance relative to the blended benchmark of the Fund was an underweight to global equities combined with a negative selection effect within global equities primarily due to the extremely strong performance from US equities, particularly within the growth style cohort and mega-cap technology stocks. Additional detractors to relative performance included the underperformance of global natural resources and both investment grade and high yield fixed income relative to global equities.

These headwinds were partially offset by the positive effects of overweight allocations to global real estate and global listed infrastructure, which provided very strong returns more in-line with global equities during the period.

*The blended benchmark is computed using a combination of 50% MSCI ACWI Index (net) / 50% ICE BofA US High Yield Index.

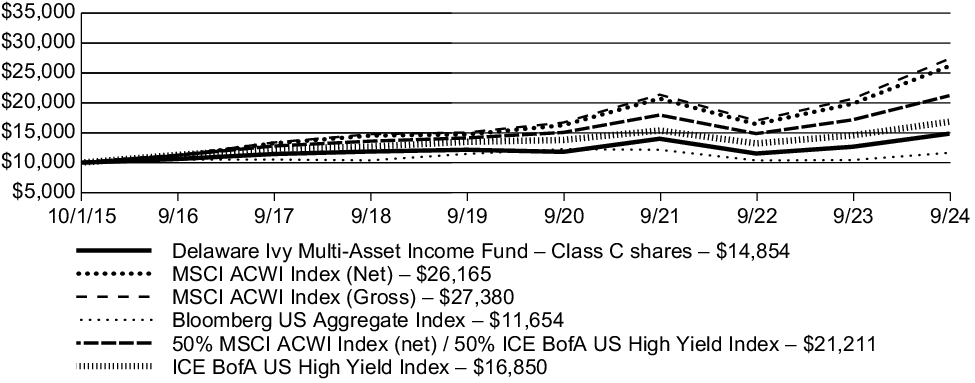

Fund performance

The following graph compares the initial and subsequent account values at the end of each of the most recently completed fiscal years (or period) of the Class for the life of the Class. It also assumes a $10,000 initial investment at the Class's inception date in multiple broad-based securities market indices and multiple narrowly based securities market indices for the same period.

Growth of $10,000 investment

For the period October 1, 2015 (Class C's inception), through September 30, 2024

| Average annual total returns (as of September 30, 2024) | 1 year | 5 year | Since inception

(10/1/15) |

| Delaware Ivy Multi-Asset Income Fund (Class C) – including sales charge | 15.38 | % | 3.92 | % | 4.49 | % |

| Delaware Ivy Multi-Asset Income Fund (Class C) – excluding sales charge | 16.38 | % | 3.92 | % | 4.49 | % |

| MSCI ACWI Index (net) | 31.76 | % | 12.19 | % | 11.27 | % |

| MSCI ACWI Index (gross) | 32.35 | % | 12.72 | % | 11.83 | % |

| Bloomberg US Aggregate Index | 11.57 | % | 0.33 | % | 1.72 | % |

| 50% MSCI ACWI Index / 50% ICE BofA US High Yield Index | 23.54 | % | 8.45 | % | 8.71 | % |

| ICE BofA US High Yield Index | 15.66 | % | 4.55 | % | 5.97 | % |

Keep in mind that the Fund's past performance is not a good predictor of how the Fund will perform in the future.

Visit delawarefunds.com/performance for the most recent performance information. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. Performance results reflect any expense caps in effect during these periods. All results shown assume reinvestment of distributions.

In connection with new regulatory requirements, effective the date of this report, the Fund changed its broad-based securities market benchmark index to the MSCI ACWI Index and the Bloomberg US Aggregate Index. Although the MSCI ACWI Index and the Bloomberg US Aggregate Index can be considered broadly representative of the overall securities market applicable to the Fund, the Fund will continue to show the performance of the blended benchmark for comparative purposes because Delaware Management Company, the Fund's manager, believes it is more representative of the Fund’s investment universe.

Fund statistics (as of September 30, 2024)

| Fund net assets | $82,514,992 |

| Total number of portfolio holdings | 491 |

| Total advisory fees paid | $155,934 |

| Portfolio turnover rate | 53% |

Fund holdings (as of September 30, 2024)

The tables below show the investment makeup of the Fund, with each category representing a percentage of the total net assets of the Fund.

| Common Stocks | 53.38% |

| Corporate Bonds | 29.81% |

| Exchange-Traded Funds | 7.94% |

| Agency Mortgage-Backed Securities | 3.92% |

| Convertible Bond | 1.26% |

| Non-Agency Commercial Mortgage-Backed Securities | 1.11% |

| Preferred Stocks | 0.76% |

| Short-Term Investments | 0.48% |

| Loan Agreements | 0.37% |

| US Treasury Obligations | 0.08% |

| Diageo | 0.95% |

| Koninklijke Ahold Delhaize | 0.94% |

| SAP | 0.94% |

| Visa Class A | 0.90% |

| Equinix | 0.88% |

| Nestle | 0.87% |

| Unilever | 0.86% |

| Welltower | 0.86% |

| Smith & Nephew | 0.86% |

| Securitas Class B | 0.80% |

For the fiscal year ended September 30, 2024, the Fund’s total annual operating expenses for Class C decreased from 1.82% to 1.75%. In addition, effective February 29, 2024, the Fund modified its principal investment strategies to reflect that Macquarie Investment Management Austria Kapitalanlage AG (MIMAK), the Fund's sub-advisor that is primarily responsible for the day-to-day management of the portfolio, will also manage a tactical / completion sleeve of the Fund and such sleeve will typically vary from 0% to 20% of the Fund's total assets and primarily hold derivatives and exchange-traded funds. Effective February 29, 2024, the Fund also added "Exchange-traded fund risk" as an additional principal investment risk of the Fund.

This is a summary of certain changes to the Fund since the beginning of the reporting period. For more complete information, you may review the Fund's next prospectus, which we expect to be available by January 29, 2025, at delawarefunds.com/literature or upon request at 800 523-1918, weekdays from 8:30am to 6:00pm ET.

Availability of additional information

You can find additional information about the Fund, such as the prospectus, financial information, holdings, and proxy voting information, at delawarefunds.com/literature. You can also request this information by contacting us at 800 523-1918, weekdays from 8:30am to 6:00pm ET, or by contacting your financial intermediary.

Householding

In order to reduce expenses, we will deliver a single copy of prospectuses, proxies, financial reports, and other communication to shareholders with the same residential address, provided they have the same last name or we reasonably believe them to be members of the same family. Unless we are notified otherwise, we will continue to send recipients only one copy of these materials for as long as they remain a shareholder of the Fund. If you would like to receive individual mailings, please call 800 523-1918 or contact your financial intermediary. Your instructions will typically be effective within 30 days of receipt by Delaware Funds by Macquarie® or your financial intermediary. If you choose, you may receive these documents through electronic delivery.

For more information, please scan the QR code at left to navigate to additional hosted material at delawarefunds.com/literature.

Delaware Ivy Multi-Asset Income Fund

Class I: IMAIX

Annual shareholder report | September 30, 2024

This annual shareholder report contains important information about Delaware Ivy Multi-Asset Income Fund (Fund) for the period of October 1, 2023, to September 30, 2024. You can find additional information about the Fund at delawarefunds.com/literature. You can also request this information by contacting us at 800 523-1918, weekdays from 8:30am to 6:00pm ET.

This report describes changes to the Fund that occurred during the reporting period.

What were the Fund's costs for the last 12 months?

(Based on a hypothetical $10,000 investment)

| Class | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

| Class I | $82 | 0.75% |

Management’s discussion of Fund performance

Performance highlights

Delaware Ivy Multi-Asset Income Fund (Class I) returned 17.57% (excluding sales charge) for the 12 months ended September 30, 2024. During the same period, the MSCI ACWI (All Country World Index) Index (net), MSCI ACWI Index (gross), and Bloomberg US Aggregate Index, the Fund's broad-based securities market indices, returned 31.76%, 32.35%, and 11.57%, respectively, while the current blended benchmark*, the Fund's narrowly based securities market index, returned 23.54%.

The Delaware Ivy Multi-Asset Income Fund is a real assets portfolio that aims to provide capital appreciation and income, inflation protection, and diversification with a dynamic, multi-asset allocation framework built on market assessments using pairwise views by an experienced multi-asset allocation team with specialized experts in each asset class.

During the period, the asset classes in scope for the Fund that delivered the highest returns were:

Global equities

Global listed infrastructure

Global real estate

The asset classes in scope for the Fund with the lowest returns during the period were:

Global natural resources

Investment grade fixed income

High yield fixed income

The largest detractor from performance relative to the blended benchmark of the Fund was an underweight to global equities combined with a negative selection effect within global equities primarily due to the extremely strong performance from US equities, particularly within the growth style cohort and mega-cap technology stocks. Additional detractors to relative performance included the underperformance of global natural resources and both investment grade and high yield fixed income relative to global equities.

These headwinds were partially offset by the positive effects of overweight allocations to global real estate and global listed infrastructure, which provided very strong returns more in-line with global equities during the period.

*The blended benchmark is computed using a combination of 50% MSCI ACWI Index (net) / 50% ICE BofA US High Yield Index.

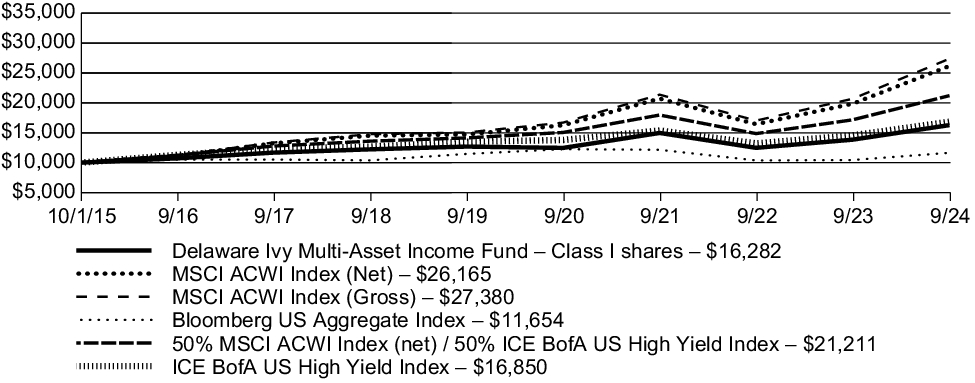

Fund performance

The following graph compares the initial and subsequent account values at the end of each of the most recently completed fiscal years (or period) of the Class for the life of the Class. It also assumes a $10,000 initial investment at the Class's inception date in multiple broad-based securities market indices and multiple narrowly based securities market indices for the same period.

Growth of $10,000 investment

For the period October 1, 2015 (Class I's inception), through September 30, 2024

| Average annual total returns (as of September 30, 2024) | 1 year | 5 year | Since inception

(10/1/15) |

| Delaware Ivy Multi-Asset Income Fund (Class I) – including sales charge | 17.57 | % | 5.11 | % | 5.57 | % |

| Delaware Ivy Multi-Asset Income Fund (Class I) – excluding sales charge | 17.57 | % | 5.11 | % | 5.57 | % |

| MSCI ACWI Index (net) | 31.76 | % | 12.19 | % | 11.27 | % |

| MSCI ACWI Index (gross) | 32.35 | % | 12.72 | % | 11.83 | % |

| Bloomberg US Aggregate Index | 11.57 | % | 0.33 | % | 1.72 | % |

| 50% MSCI ACWI Index / 50% ICE BofA US High Yield Index | 23.54 | % | 8.45 | % | 8.71 | % |

| ICE BofA US High Yield Index | 15.66 | % | 4.55 | % | 5.97 | % |

Keep in mind that the Fund's past performance is not a good predictor of how the Fund will perform in the future.

Visit delawarefunds.com/performance for the most recent performance information. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. Performance results reflect any expense caps in effect during these periods. All results shown assume reinvestment of distributions.

In connection with new regulatory requirements, effective the date of this report, the Fund changed its broad-based securities market benchmark index to the MSCI ACWI Index and the Bloomberg US Aggregate Index. Although the MSCI ACWI Index and the Bloomberg US Aggregate Index can be considered broadly representative of the overall securities market applicable to the Fund, the Fund will continue to show the performance of the blended benchmark for comparative purposes because Delaware Management Company, the Fund's manager, believes it is more representative of the Fund’s investment universe.

Fund statistics (as of September 30, 2024)

| Fund net assets | $82,514,992 |

| Total number of portfolio holdings | 491 |

| Total advisory fees paid | $155,934 |

| Portfolio turnover rate | 53% |

Fund holdings (as of September 30, 2024)

The tables below show the investment makeup of the Fund, with each category representing a percentage of the total net assets of the Fund.

| Common Stocks | 53.38% |

| Corporate Bonds | 29.81% |

| Exchange-Traded Funds | 7.94% |

| Agency Mortgage-Backed Securities | 3.92% |

| Convertible Bond | 1.26% |

| Non-Agency Commercial Mortgage-Backed Securities | 1.11% |

| Preferred Stocks | 0.76% |

| Short-Term Investments | 0.48% |

| Loan Agreements | 0.37% |

| US Treasury Obligations | 0.08% |

| Diageo | 0.95% |

| Koninklijke Ahold Delhaize | 0.94% |

| SAP | 0.94% |

| Visa Class A | 0.90% |

| Equinix | 0.88% |

| Nestle | 0.87% |

| Unilever | 0.86% |

| Welltower | 0.86% |

| Smith & Nephew | 0.86% |

| Securitas Class B | 0.80% |

Effective February 29, 2024, the Fund modified its principal investment strategies to reflect that Macquarie Investment Management Austria Kapitalanlage AG (MIMAK), the Fund's sub-advisor that is primarily responsible for the day-to-day management of the portfolio, will also manage a tactical / completion sleeve of the Fund and such sleeve will typically vary from 0% to 20% of the Fund's total assets and primarily hold derivatives and exchange-traded funds. Effective February 29, 2024, the Fund also added "Exchange-traded fund risk" as an additional principal investment risk of the Fund.

This is a summary of certain changes to the Fund since the beginning of the reporting period. For more complete information, you may review the Fund's next prospectus, which we expect to be available by January 29, 2025, at delawarefunds.com/literature or upon request at 800 523-1918, weekdays from 8:30am to 6:00pm ET.

Availability of additional information

You can find additional information about the Fund, such as the prospectus, financial information, holdings, and proxy voting information, at delawarefunds.com/literature. You can also request this information by contacting us at 800 523-1918, weekdays from 8:30am to 6:00pm ET, or by contacting your financial intermediary.

Householding

In order to reduce expenses, we will deliver a single copy of prospectuses, proxies, financial reports, and other communication to shareholders with the same residential address, provided they have the same last name or we reasonably believe them to be members of the same family. Unless we are notified otherwise, we will continue to send recipients only one copy of these materials for as long as they remain a shareholder of the Fund. If you would like to receive individual mailings, please call 800 523-1918 or contact your financial intermediary. Your instructions will typically be effective within 30 days of receipt by Delaware Funds by Macquarie® or your financial intermediary. If you choose, you may receive these documents through electronic delivery.

For more information, please scan the QR code at left to navigate to additional hosted material at delawarefunds.com/literature.

Delaware Ivy Multi-Asset Income Fund

Class R6: IMURX

Annual shareholder report | September 30, 2024

This annual shareholder report contains important information about Delaware Ivy Multi-Asset Income Fund (Fund) for the period of October 1, 2023, to September 30, 2024. You can find additional information about the Fund at delawarefunds.com/literature. You can also request this information by contacting us at 800 523-1918, weekdays from 8:30am to 6:00pm ET.

This report describes changes to the Fund that occurred during the reporting period.

What were the Fund's costs for the last 12 months?

(Based on a hypothetical $10,000 investment)

| Class | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

| Class R6 | $73 | 0.67% |

Management’s discussion of Fund performance

Performance highlights

Delaware Ivy Multi-Asset Income Fund (Class R6) returned 17.65% (excluding sales charge) for the 12 months ended September 30, 2024. During the same period, the MSCI ACWI (All Country World Index) Index (net), MSCI ACWI Index (gross), and Bloomberg US Aggregate Index, the Fund's broad-based securities market indices, returned 31.76%, 32.35%, and 11.57%, respectively, while the current blended benchmark*, the Fund's narrowly based securities market index, returned 23.54%.

The Delaware Ivy Multi-Asset Income Fund is a real assets portfolio that aims to provide capital appreciation and income, inflation protection, and diversification with a dynamic, multi-asset allocation framework built on market assessments using pairwise views by an experienced multi-asset allocation team with specialized experts in each asset class.

During the period, the asset classes in scope for the Fund that delivered the highest returns were:

Global equities

Global listed infrastructure

Global real estate

The asset classes in scope for the Fund with the lowest returns during the period were:

Global natural resources

Investment grade fixed income

High yield fixed income

The largest detractor from performance relative to the blended benchmark of the Fund was an underweight to global equities combined with a negative selection effect within global equities primarily due to the extremely strong performance from US equities, particularly within the growth style cohort and mega-cap technology stocks. Additional detractors to relative performance included the underperformance of global natural resources and both investment grade and high yield fixed income relative to global equities.

These headwinds were partially offset by the positive effects of overweight allocations to global real estate and global listed infrastructure, which provided very strong returns more in-line with global equities during the period.

*The blended benchmark is computed using a combination of 50% MSCI ACWI Index (net) / 50% ICE BofA US High Yield Index.

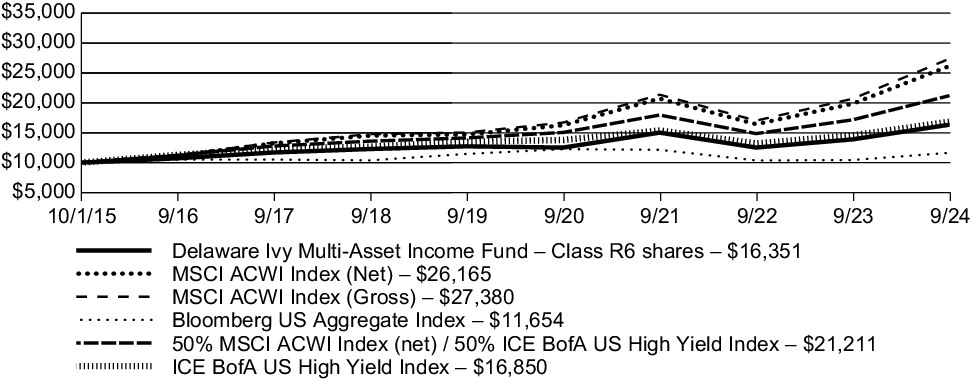

Fund performance

The following graph compares the initial and subsequent account values at the end of each of the most recently completed fiscal years (or period) of the Class for the life of the Class. It also assumes a $10,000 initial investment at the Class's inception date in multiple broad-based securities market indices and multiple narrowly based securities market indices for the same period.

Growth of $10,000 investment

For the period October 1, 2015 (Class R6's inception), through September 30, 2024

| Average annual total returns (as of September 30, 2024) | 1 year | 5 year | Since inception

(10/1/15) |

| Delaware Ivy Multi-Asset Income Fund (Class R6) – including sales charge | 17.65 | % | 5.12 | % | 5.62 | % |

| Delaware Ivy Multi-Asset Income Fund (Class R6) – excluding sales charge | 17.65 | % | 5.12 | % | 5.62 | % |

| MSCI ACWI Index (net) | 31.76 | % | 12.19 | % | 11.27 | % |

| MSCI ACWI Index (gross) | 32.35 | % | 12.72 | % | 11.83 | % |

| Bloomberg US Aggregate Index | 11.57 | % | 0.33 | % | 1.72 | % |

| 50% MSCI ACWI Index / 50% ICE BofA US High Yield Index | 23.54 | % | 8.45 | % | 8.71 | % |

| ICE BofA US High Yield Index | 15.66 | % | 4.55 | % | 5.97 | % |

Keep in mind that the Fund's past performance is not a good predictor of how the Fund will perform in the future.

Visit delawarefunds.com/performance for the most recent performance information. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. Performance results reflect any expense caps in effect during these periods. All results shown assume reinvestment of distributions.

In connection with new regulatory requirements, effective the date of this report, the Fund changed its broad-based securities market benchmark index to the MSCI ACWI Index and the Bloomberg US Aggregate Index. Although the MSCI ACWI Index and the Bloomberg US Aggregate Index can be considered broadly representative of the overall securities market applicable to the Fund, the Fund will continue to show the performance of the blended benchmark for comparative purposes because Delaware Management Company, the Fund's manager, believes it is more representative of the Fund’s investment universe.

Fund statistics (as of September 30, 2024)

| Fund net assets | $82,514,992 |

| Total number of portfolio holdings | 491 |

| Total advisory fees paid | $155,934 |

| Portfolio turnover rate | 53% |

Fund holdings (as of September 30, 2024)

The tables below show the investment makeup of the Fund, with each category representing a percentage of the total net assets of the Fund.

| Common Stocks | 53.38% |

| Corporate Bonds | 29.81% |

| Exchange-Traded Funds | 7.94% |

| Agency Mortgage-Backed Securities | 3.92% |

| Convertible Bond | 1.26% |

| Non-Agency Commercial Mortgage-Backed Securities | 1.11% |

| Preferred Stocks | 0.76% |

| Short-Term Investments | 0.48% |

| Loan Agreements | 0.37% |

| US Treasury Obligations | 0.08% |

| Diageo | 0.95% |

| Koninklijke Ahold Delhaize | 0.94% |

| SAP | 0.94% |

| Visa Class A | 0.90% |

| Equinix | 0.88% |

| Nestle | 0.87% |

| Unilever | 0.86% |

| Welltower | 0.86% |

| Smith & Nephew | 0.86% |

| Securitas Class B | 0.80% |

Material Fund changes

Effective January 29, 2024, the Fund introduced a revised fee waiver for Class R6 shares of 0.63% (excluding certain items), which resulted in a decrease in the net annual operating expenses for Class R6 from 0.75% to 0.67%. In addition, effective February 29, 2024, the Fund modified its principal investment strategies to reflect that Macquarie Investment Management Austria Kapitalanlage AG (MIMAK), the Fund's sub-advisor that is primarily responsible for the day-to-day management of the portfolio, will also manage a tactical / completion sleeve of the Fund and such sleeve will typically vary from 0% to 20% of the Fund's total assets and primarily hold derivatives and exchange-traded funds. Effective February 29, 2024, the Fund also added "Exchange-traded fund risk" as an additional principal investment risk of the Fund.

This is a summary of certain changes to the Fund since the beginning of the reporting period. For more complete information, you may review the Fund's next prospectus, which we expect to be available by January 29, 2025, at delawarefunds.com/literature or upon request at 800 523-1918, weekdays from 8:30am to 6:00pm ET.

Availability of additional information

You can find additional information about the Fund, such as the prospectus, financial information, holdings, and proxy voting information, at delawarefunds.com/literature. You can also request this information by contacting us at 800 523-1918, weekdays from 8:30am to 6:00pm ET, or by contacting your financial intermediary.

Householding

In order to reduce expenses, we will deliver a single copy of prospectuses, proxies, financial reports, and other communication to shareholders with the same residential address, provided they have the same last name or we reasonably believe them to be members of the same family. Unless we are notified otherwise, we will continue to send recipients only one copy of these materials for as long as they remain a shareholder of the Fund. If you would like to receive individual mailings, please call 800 523-1918 or contact your financial intermediary. Your instructions will typically be effective within 30 days of receipt by Delaware Funds by Macquarie® or your financial intermediary. If you choose, you may receive these documents through electronic delivery.

For more information, please scan the QR code at left to navigate to additional hosted material at delawarefunds.com/literature.

Delaware Ivy Multi-Asset Income Fund

Class Y: IMAYX

Annual shareholder report | September 30, 2024

This annual shareholder report contains important information about Delaware Ivy Multi-Asset Income Fund (Fund) for the period of October 1, 2023, to September 30, 2024. You can find additional information about the Fund at delawarefunds.com/literature. You can also request this information by contacting us at 800 523-1918, weekdays from 8:30am to 6:00pm ET.

This report describes changes to the Fund that occurred during the reporting period.

What were the Fund's costs for the last 12 months?

(Based on a hypothetical $10,000 investment)

| Class | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

| Class Y | $109 | 1.00% |

Management’s discussion of Fund performance

Performance highlights

Delaware Ivy Multi-Asset Income Fund (Class Y) returned 17.32% (excluding sales charge) for the 12 months ended September 30, 2024. During the same period, the MSCI ACWI (All Country World Index) Index (net), MSCI ACWI Index (gross), and Bloomberg US Aggregate Index, the Fund's broad-based securities market indices, returned 31.76%, 32.35%, and 11.57%, respectively, while the current blended benchmark*, the Fund's narrowly based securities market index, returned 23.54%.

The Delaware Ivy Multi-Asset Income Fund is a real assets portfolio that aims to provide capital appreciation and income, inflation protection, and diversification with a dynamic, multi-asset allocation framework built on market assessments using pairwise views by an experienced multi-asset allocation team with specialized experts in each asset class.

During the period, the asset classes in scope for the Fund that delivered the highest returns were:

Global equities

Global listed infrastructure

Global real estate

The asset classes in scope for the Fund with the lowest returns during the period were:

Global natural resources

Investment grade fixed income

High yield fixed income

The largest detractor from performance relative to the blended benchmark of the Fund was an underweight to global equities combined with a negative selection effect within global equities primarily due to the extremely strong performance from US equities, particularly within the growth style cohort and mega-cap technology stocks. Additional detractors to relative performance included the underperformance of global natural resources and both investment grade and high yield fixed income relative to global equities.

These headwinds were partially offset by the positive effects of overweight allocations to global real estate and global listed infrastructure, which provided very strong returns more in-line with global equities during the period.

*The blended benchmark is computed using a combination of 50% MSCI ACWI Index (net) / 50% ICE BofA US High Yield Index.

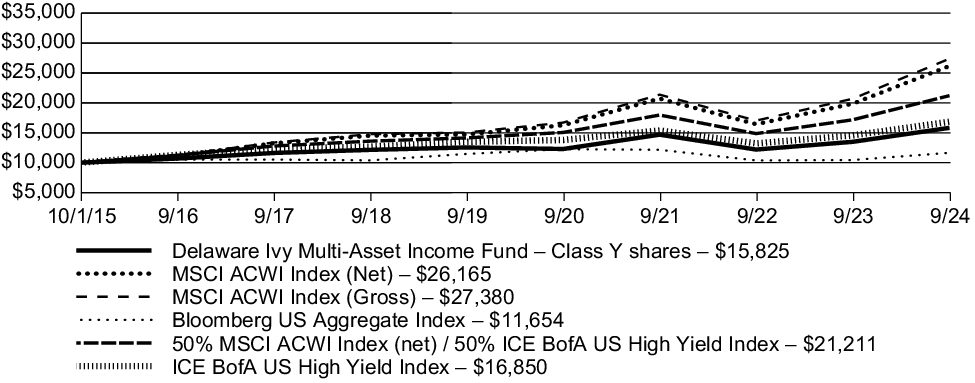

Fund performance

The following graph compares the initial and subsequent account values at the end of each of the most recently completed fiscal years (or period) of the Class for the life of the Class. It also assumes a $10,000 initial investment at the Class's inception date in multiple broad-based securities market indices and multiple narrowly based securities market indices for the same period.

Growth of $10,000 investment

For the period October 1, 2015 (Class Y's inception), through September 30, 2024

| Average annual total returns (as of September 30, 2024) | 1 year | 5 year | Since inception

(10/1/15) |

| Delaware Ivy Multi-Asset Income Fund (Class Y) – including sales charge | 17.32 | % | 4.75 | % | 5.23 | % |

| Delaware Ivy Multi-Asset Income Fund (Class Y) – excluding sales charge | 17.32 | % | 4.75 | % | 5.23 | % |

| MSCI ACWI Index (net) | 31.76 | % | 12.19 | % | 11.27 | % |

| MSCI ACWI Index (gross) | 32.35 | % | 12.72 | % | 11.83 | % |

| Bloomberg US Aggregate Index | 11.57 | % | 0.33 | % | 1.72 | % |

| 50% MSCI ACWI Index / 50% ICE BofA US High Yield Index | 23.54 | % | 8.45 | % | 8.71 | % |

| ICE BofA US High Yield Index | 15.66 | % | 4.55 | % | 5.97 | % |

Keep in mind that the Fund's past performance is not a good predictor of how the Fund will perform in the future.

Visit delawarefunds.com/performance for the most recent performance information. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. Performance results reflect any expense caps in effect during these periods. All results shown assume reinvestment of distributions.

In connection with new regulatory requirements, effective the date of this report, the Fund changed its broad-based securities market benchmark index to the MSCI ACWI Index and the Bloomberg US Aggregate Index. Although the MSCI ACWI Index and the Bloomberg US Aggregate Index can be considered broadly representative of the overall securities market applicable to the Fund, the Fund will continue to show the performance of the blended benchmark for comparative purposes because Delaware Management Company, the Fund's manager, believes it is more representative of the Fund’s investment universe.

Fund statistics (as of September 30, 2024)

| Fund net assets | $82,514,992 |

| Total number of portfolio holdings | 491 |

| Total advisory fees paid | $155,934 |

| Portfolio turnover rate | 53% |

Fund holdings (as of September 30, 2024)

The tables below show the investment makeup of the Fund, with each category representing a percentage of the total net assets of the Fund.

| Common Stocks | 53.38% |

| Corporate Bonds | 29.81% |

| Exchange-Traded Funds | 7.94% |

| Agency Mortgage-Backed Securities | 3.92% |

| Convertible Bond | 1.26% |

| Non-Agency Commercial Mortgage-Backed Securities | 1.11% |

| Preferred Stocks | 0.76% |

| Short-Term Investments | 0.48% |

| Loan Agreements | 0.37% |

| US Treasury Obligations | 0.08% |

| Diageo | 0.95% |

| Koninklijke Ahold Delhaize | 0.94% |

| SAP | 0.94% |

| Visa Class A | 0.90% |

| Equinix | 0.88% |

| Nestle | 0.87% |

| Unilever | 0.86% |

| Welltower | 0.86% |

| Smith & Nephew | 0.86% |

| Securitas Class B | 0.80% |

For the fiscal year ended September 30, 2024, the Fund’s total annual operating expenses for Class Y decreased from 1.06% to 1.00%. In addition, effective February 29, 2024, the Fund modified its principal investment strategies to reflect that Macquarie Investment Management Austria Kapitalanlage AG (MIMAK), the Fund's sub-advisor that is primarily responsible for the day-to-day management of the portfolio, will also manage a tactical / completion sleeve of the Fund and such sleeve will typically vary from 0% to 20% of the Fund's total assets and primarily hold derivatives and exchange-traded funds. Effective February 29, 2024, the Fund also added "Exchange-traded fund risk" as an additional principal investment risk of the Fund.

This is a summary of certain changes to the Fund since the beginning of the reporting period. For more complete information, you may review the Fund's next prospectus, which we expect to be available by January 29, 2025, at delawarefunds.com/literature or upon request at 800 523-1918, weekdays from 8:30am to 6:00pm ET.

Availability of additional information

You can find additional information about the Fund, such as the prospectus, financial information, holdings, and proxy voting information, at delawarefunds.com/literature. You can also request this information by contacting us at 800 523-1918, weekdays from 8:30am to 6:00pm ET, or by contacting your financial intermediary.

Householding

In order to reduce expenses, we will deliver a single copy of prospectuses, proxies, financial reports, and other communication to shareholders with the same residential address, provided they have the same last name or we reasonably believe them to be members of the same family. Unless we are notified otherwise, we will continue to send recipients only one copy of these materials for as long as they remain a shareholder of the Fund. If you would like to receive individual mailings, please call 800 523-1918 or contact your financial intermediary. Your instructions will typically be effective within 30 days of receipt by Delaware Funds by Macquarie® or your financial intermediary. If you choose, you may receive these documents through electronic delivery.

For more information, please scan the QR code at left to navigate to additional hosted material at delawarefunds.com/literature.

Item 2. Code of Ethics.

| | (a) | The registrant has adopted a code of ethics that applies to the registrant’s principal executive officer, principal financial officer, principal accounting officer or controller, or persons performing similar functions, regardless of whether these individuals are employed by the registrant or a third party. A copy of the registrant’s Code of Business Ethics has been posted on the Delaware Funds by Macquarie® Internet Web site at www.delawarefunds.com. Any amendments to the Code of Business Ethics, and information on any waiver from its provisions granted by the registrant, will also be posted on this Web site within five business days of such amendment or waiver and will remain on the Web site for at least 12 months. |

Item 3. Audit Committee Financial Expert.

The registrant’s Board of Trustees has determined that certain members of the registrant’s Audit Committee are audit committee financial experts, as defined below. For purposes of this item, an “audit committee financial expert” is a person who has the following attributes:

a. An understanding of generally accepted accounting principles and financial statements;

b. The ability to assess the general application of such principles in connection with the accounting for estimates, accruals, and reserves;

c. Experience preparing, auditing, analyzing, or evaluating financial statements that present a breadth and level of complexity of accounting issues that are generally comparable to the breadth and complexity of issues that can reasonably be expected to be raised by the registrant’s financial statements, or experience actively supervising one or more persons engaged in such activities;

d. An understanding of internal controls and procedures for financial reporting; and

e. An understanding of audit committee functions.

An “audit committee financial expert” shall have acquired such attributes through:

a. Education and experience as a principal financial officer, principal accounting officer, controller, public accountant, or auditor or experience in one or more positions that involve the performance of similar functions;

b. Experience actively supervising a principal financial officer, principal accounting officer, controller, public accountant, auditor, or person performing similar functions;

c. Experience overseeing or assessing the performance of companies or public accountants with respect to the preparation, auditing, or evaluation of financial statements; or

d. Other relevant experience.

The registrant’s Board of Trustees has also determined that each member of the registrant’s Audit Committee is independent. In order to be “independent” for purposes of this item, the Audit Committee member may not, other than in his or her capacity as a member of the Board of Trustees or any committee thereof, (i) accept directly or indirectly any consulting, advisory or other compensatory fee from the issuer; or (ii) be an “interested person” of the registrant as defined in Section 2(a)(19) of the Investment Company Act of 1940.

The names of the audit committee financial experts on the registrant’s Audit Committee are set forth below:

Ann Borowiec

H. Jeffrey Dobbs

Frances Sevilla-Sacasa, Chair

Christianna Wood

Item 4. Principal Accountant Fees and Services.

Audit Fees

| | (a) | The aggregate fees billed for each of the last two fiscal years for professional services rendered by the principal accountant for the audit of the registrant’s annual financial statements or services that are normally provided by the accountant in connection with statutory and regulatory filings or engagements for those fiscal years are $47,500 for 2024 and $223,864 for 2023. |

Audit-Related Fees

| | (b) | The aggregate fees billed in each of the last two fiscal years for assurance and related services by the principal accountant that are reasonably related to the performance of the audit of the registrant’s financial statements and are not reported under paragraph (a) of this Item are $1,374,878 for 2024 and $1,362,878 for 2023. These audit-related services were as follows: year end audit procedures; group reporting and subsidiary statutory audits. |

Tax Fees

| | (c) | The aggregate fees billed in each of the last two fiscal years for professional services rendered by the principal accountant for tax compliance, tax advice, and tax planning are $7,828 for 2024 and $36,942 for 2023. These tax-related services were as follows: review of income tax returns and review of annual excise distribution calculations. |

All Other Fees

| | (d) | The aggregate fees billed in each of the last two fiscal years for products and services provided by the principal accountant, other than the services reported in paragraphs (a) through (c) of this Item are $0 for 2024 and $0 for 2023. |

| (e)(1) | The registrant’s Audit Committee has established pre-approval policies and procedures as permitted by Rule 2-01(c)(7)(i)(B) of Regulation S-X (the “Pre-Approval Policy”) with respect to services provided by the registrant’s independent auditors. Pursuant to the Pre-Approval Policy, the Audit Committee has pre-approved the services set forth in the table below with respect to the registrant up to the specified fee limits. |

Certain fee limits are based on aggregate fees to the registrant and other registrants within the Delaware Funds® by Macquarie.

| | |

Service | | Range of Fees |

Audit Services | | |

Statutory audits or financial audits for new Funds | | up to $50,000 per Fund |

Services associated with SEC registration statements (e.g., Form N-1A, Form N-14, etc.), periodic reports and other documents filed with the SEC or other documents issued in connection with securities offerings (e.g., comfort letters for closed-end Fund offerings, consents), and assistance in responding to SEC comment letters | | up to $10,000 per Fund |

Consultations by Fund management as to the accounting or disclosure treatment of transactions or events and/or the actual or potential impact of final or proposed rules, standards or interpretations by the SEC, FASB, or other regulatory or standard-setting bodies (Note: Under SEC rules, some consultations may be considered “audit-related services” rather than “audit services”) | | up to $25,000 in the aggregate |

Audit-Related Services | | |

Consultations by Fund management as to the accounting or disclosure treatment of transactions or events and /or the actual or potential impact of final or proposed rules, standards or interpretations by the SEC, FASB, or other regulatory or standard-setting bodies (Note: Under SEC rules, some consultations may be considered “audit services” rather than “audit-related services”) | | up to $25,000 in the aggregate |

Tax Services | | |

U.S. federal, state and local and international tax planning and advice (e.g., consulting on statutory, regulatory or administrative developments, evaluation of Funds’ tax compliance function, etc.) | | up to $25,000 in the aggregate |

| U.S. federal, state and local tax compliance (e.g., excise distribution reviews, etc.) | | up to $5,000 per Fund |

| Review of federal, state, local and international income, franchise and other tax returns | | up to $5,000 per Fund |

Under the Pre-Approval Policy, the Audit Committee has also pre-approved the services set forth in the table below with respect to the registrant’s investment adviser and other entities controlling, controlled by or under common control with the investment adviser that provide ongoing services to the registrant (the “Control Affiliates”) up to the specified fee limit. This fee limit is based on aggregate fees to the investment adviser and its Control Affiliates.

| | |

Service | | Range of Fees |

Non-Audit Services | | |

Services associated with periodic reports and other documents filed with the SEC and assistance in responding to SEC comment letters | | up to $10,000 in the aggregate |

The Pre-Approval Policy requires the registrant’s independent auditors to report to the Audit Committee at each of its regular meetings regarding all services initiated since the last such report was rendered, including those services authorized by the Pre-Approval Policy.

| (e)(2) | The percentage of services described in each of paragraphs (b) through (d) of this Item that were approved by the audit committee pursuant to paragraph (c)(7)(i)(C) of Rule 2-01 of Regulation S-X are as follows: |

(b) 0%

(c) 0%

(d) 0%

| | (g) | The aggregate non-audit fees billed by the registrant’s accountant for services rendered to the registrant, and rendered to the registrant’s investment adviser (not including any sub-adviser whose role is primarily portfolio management and is subcontracted with or overseen by another investment adviser), and any entity controlling, controlled by, or under common control with the adviser that provides ongoing services to the registrant for each of the last two fiscal years of the registrant was $9,688,403 for 2024 and $24,428,000 for 2023. |

| | (h) | The audit committee of the registrant’s board of trustees has considered whether the provision of non-audit services that were rendered to the registrant’s investment adviser (not including any sub-adviser whose role is primarily portfolio management and is subcontracted with or overseen by another investment adviser), and any entity controlling, controlled by, or under common control with the investment adviser that provides ongoing services to the registrant that were not pre-approved pursuant to paragraph (c)(7)(ii) of Rule 2-01 of Regulation S-X is compatible with maintaining the principal accountant’s independence. |

Item 5. Audit Committee of Listed Registrants.

Not applicable.

Item 6. Investments.

| (a) | Schedule of Investments in securities of unaffiliated issuers as of the close of the reporting period is included as part of the Financial Statements filed under Item 7 of this form. |

Item 7. Financial Statements and Financial Highlights for Open-End Management Investment Companies.

| | (a) | An open-end management investment company registered on Form N-1A [17 CFR 239.15A and 17 CFR 274.11A] must file its most recent annual or semi-annual financial statements required, and for the periods specified, by Regulation S-X. |

The annual financial statements are attached herewith.

| | (b) | An open-end management investment company registered on Form N-1A [17 CFR 239.15A and 17 CFR 274.11A] must file the information required by Item 13 of Form N-1A. |

The Financial Highlights are attached herewith.

Alternative / specialty mutual fund

Delaware Ivy Multi-Asset Income Fund

Financial statements and other information

For the year ended September 30, 2024

This report and the financial statements contained herein are submitted for the general information of the shareholders of the Fund. This report is not authorized for distribution to prospective investors in the Fund unless preceded or accompanied by an effective prospectus.

Form N-PORT and proxy voting information

The Fund files its complete schedule of portfolio holdings with the Securities and Exchange Commission (SEC) for the first and third quarters of each fiscal year on Form N-PORT. The Fund’s Form N-PORT, as well as a description of the policies and procedures that the Fund uses to determine how to vote proxies (if any) relating to portfolio securities, is available without charge (i) upon request, by calling 800 523-1918; and (ii) on the SEC’s website at sec.gov. In addition, a description of the policies and procedures that the Fund uses to determine how to vote proxies (if any) relating to portfolio securities and the Schedule of Investments included in the Fund’s most recent Form N-PORT are available without charge on the Fund’s website at delawarefunds.com/literature.

Information (if any) regarding how the Fund voted proxies relating to portfolio securities during the most recently disclosed 12-month period ended June 30 is available without charge (i) through the Fund’s website at delawarefunds.com/proxy; and (ii) on the SEC’s website at sec.gov.

Schedule of investments

| Delaware Ivy Multi-Asset Income Fund | September 30, 2024 |

| | | Principal

amount° | Value (US $) |

| Agency Mortgage-Backed Securities — 3.92% |

| Fannie Mae S.F. 15 yr | | | |

| 2.00% 8/1/36 | | 50,042 | $ 46,012 |

| 2.50% 8/1/36 | | 44,280 | 41,566 |

| 3.00% 11/1/33 | | 13,203 | 12,819 |

|

|

Fannie Mae S.F. 20 yr

4.00% 9/1/42 | | 53,448 | 52,517 |

| Fannie Mae S.F. 30 yr | | | |

| 2.00% 3/1/51 | | 122,798 | 101,710 |

| 2.00% 9/1/51 | | 40,430 | 33,511 |

| 2.50% 2/1/52 | | 48,777 | 42,556 |

| 3.00% 1/1/50 | | 250,595 | 228,980 |

| 3.00% 6/1/52 | | 51,167 | 46,249 |

| 3.50% 6/1/51 | | 242,263 | 227,196 |

| 3.50% 6/1/52 | | 139,838 | 130,312 |

| 4.00% 5/1/51 | | 40,621 | 39,511 |

| 4.50% 1/1/50 | | 109,973 | 111,231 |

| 4.50% 10/1/52 | | 285,896 | 281,168 |

| 4.50% 2/1/53 | | 22,905 | 22,526 |

| 5.50% 8/1/52 | | 114,715 | 116,534 |

| 5.50% 11/1/52 | | 223,971 | 228,738 |

| 6.00% 5/1/53 | | 21,783 | 22,463 |

| 6.00% 6/1/53 | | 92,571 | 94,790 |

| 6.00% 9/1/53 | | 31,632 | 32,335 |

| Freddie Mac S.F. 20 yr | | | |

| 2.00% 8/1/42 | | 116,378 | 101,458 |

| 2.50% 3/1/42 | | 47,582 | 42,675 |

| 2.50% 9/1/42 | | 32,710 | 29,379 |

| 3.00% 5/1/40 | | 242,696 | 229,294 |

| Freddie Mac S.F. 30 yr | | | |

| 2.00% 3/1/52 | | 154,996 | 128,318 |

| 2.50% 7/1/50 | | 309,873 | 270,897 |

| 4.00% 8/1/52 | | 95,797 | 92,490 |

| 4.00% 9/1/52 | | 41,518 | 39,935 |

| 4.50% 10/1/52 | | 36,999 | 36,371 |

| 5.00% 7/1/52 | | 29,538 | 30,110 |

| 5.00% 9/1/52 | | 136,897 | 138,862 |

| 5.00% 6/1/53 | | 105,044 | 105,042 |

| 5.50% 9/1/52 | | 27,473 | 28,213 |

| 5.50% 10/1/52 | | 39,587 | 40,109 |

Schedule of investments

Delaware Ivy Multi-Asset Income Fund

| | | Principal

amount° | Value (US $) |

| Agency Mortgage-Backed Securities (continued) |

| Freddie Mac S.F. 30 yr | | | |

| 5.50% 6/1/53 | | 9,011 | $ 9,119 |

Total Agency Mortgage-Backed Securities

(cost $3,296,680) | 3,234,996 |

|

|

|

| Convertible Bond — 1.26% |

| New Cotai PIK 5.00% exercise price $0.40, maturity date 2/2/27 =, >>, π | | 383,301 | 1,036,225 |

Total Convertible Bond

(cost $376,334) | 1,036,225 |

| | | | |

| Corporate Bonds — 29.81% |

| Banking — 2.23% |

| Bank of America | | | |

| 5.819% 9/15/29 μ | | 15,000 | 15,790 |

| 6.204% 11/10/28 μ | | 95,000 | 100,301 |

|

|

| Bank of Montreal 7.70% 5/26/84 μ | | 200,000 | 211,556 |

| Bank of New York Mellon 4.70% 9/20/25 μ, ψ | | 40,000 | 39,788 |

| Barclays 9.625% 12/15/29 μ, ψ | | 200,000 | 225,683 |

| Citigroup | | | |

| 5.61% 9/29/26 μ | | 25,000 | 25,225 |

| 7.00% 8/15/34 μ, ψ | | 20,000 | 21,452 |

|

|

| Deutsche Bank 6.00% 10/30/25 μ, ψ | | 200,000 | 196,044 |

| Fifth Third Bancorp 6.361% 10/27/28 μ | | 43,000 | 45,303 |

| Goldman Sachs Group | | | |

| 5.727% 4/25/30 μ | | 30,000 | 31,535 |

| 5.851% 4/25/35 μ | | 35,000 | 37,622 |

| 6.125% 11/10/34 μ, ψ | | 25,000 | 25,171 |

| 6.484% 10/24/29 μ | | 30,000 | 32,312 |

| JPMorgan Chase & Co. | | | |

| 5.012% 1/23/30 μ | | 170,000 | 174,390 |

| 5.571% 4/22/28 μ | | 40,000 | 41,248 |

| 6.254% 10/23/34 μ | | 27,000 | 30,040 |

|

|

| KeyBank 5.85% 11/15/27 | | 30,000 | 31,114 |

| Morgan Stanley | | | |

| 5.831% 4/19/35 μ | | 50,000 | 53,727 |

| 6.296% 10/18/28 μ | | 33,000 | 34,896 |

| 6.407% 11/1/29 μ | | 70,000 | 75,238 |

| 6.627% 11/1/34 μ | | 55,000 | 62,234 |

| | | Principalamount° | Value (US $) |

| Corporate Bonds (continued) |

| Banking (continued) |

| PNC Financial Services Group | | | |

| 5.676% 1/22/35 μ | | 35,000 | $ 37,120 |

| 6.875% 10/20/34 μ | | 35,000 | 40,091 |

|

|

| Regions Financial 5.502% 9/6/35 μ | | 30,000 | 30,541 |

| State Street 4.993% 3/18/27 | | 45,000 | 46,070 |

| SVB Financial Group 4.57% 4/29/33 ‡ | | 74,000 | 43,359 |

| US Bancorp | | | |

| 4.653% 2/1/29 μ | | 56,000 | 56,555 |

| 5.384% 1/23/30 μ | | 15,000 | 15,581 |

| 5.678% 1/23/35 μ | | 35,000 | 37,115 |

| 6.787% 10/26/27 μ | | 25,000 | 26,257 |

| | 1,843,358 |

| Basic Industry — 1.56% |

| Cleveland-Cliffs 144A 7.00% 3/15/32 # | | 165,000 | 167,020 |

| FMG Resources August 2006 144A 5.875% 4/15/30 # | | 285,000 | 288,934 |

| Freeport-McMoRan 5.45% 3/15/43 | | 90,000 | 90,474 |

| LYB International Finance III | | | |

| 3.625% 4/1/51 | | 40,000 | 29,839 |

| 5.50% 3/1/34 | | 100,000 | 104,087 |

|

|

| NOVA Chemicals 144A 8.50% 11/15/28 # | | 35,000 | 37,404 |

| Novelis 144A 4.75% 1/30/30 # | | 295,000 | 286,259 |

| Olympus Water US Holding 144A 9.75% 11/15/28 # | | 200,000 | 213,702 |

| Sherwin-Williams 3.30% 5/15/50 | | 90,000 | 66,319 |

| | 1,284,038 |

| Brokerage — 0.18% |

| Focus Financial Partners 144A 6.75% 9/15/31 # | | 106,000 | 107,081 |

| Jefferies Financial Group 5.875% 7/21/28 | | 36,000 | 37,565 |

| | 144,646 |

| Capital Goods — 3.04% |

| Amphenol | | | |

| 2.20% 9/15/31 | | 15,000 | 12,971 |

| 5.05% 4/5/27 | | 20,000 | 20,478 |

| 5.25% 4/5/34 | | 10,000 | 10,452 |

|

|

| Ardagh Metal Packaging Finance USA 144A 3.25% 9/1/28 # | | 150,000 | 137,445 |

| Boeing 144A 6.858% 5/1/54 # | | 50,000 | 54,917 |

| Bombardier | | | |

| 144A 7.25% 7/1/31 # | | 60,000 | 63,506 |

| 144A 8.75% 11/15/30 # | | 55,000 | 60,463 |

|

|

| Clydesdale Acquisition Holdings 144A 8.75% 4/15/30 # | | 115,000 | 116,891 |

Schedule of investments

Delaware Ivy Multi-Asset Income Fund

| | | Principalamount° | Value (US $) |

| Corporate Bonds (continued) |

| Capital Goods (continued) |

|

| CP Atlas Buyer 144A 7.00% 12/1/28 # | | 135,000 | $ 125,130 |

| Esab 144A 6.25% 4/15/29 # | | 125,000 | 128,538 |

| GFL Environmental 144A 6.75% 1/15/31 # | | 90,000 | 94,507 |

| Manitowoc 144A 9.25% 10/1/31 # | | 55,000 | 56,444 |

| Mauser Packaging Solutions Holding | | | |

| 144A 7.875% 4/15/27 # | | 175,000 | 181,025 |

| 144A 9.25% 4/15/27 # | | 65,000 | 66,710 |

|

|

| Northrop Grumman 5.20% 6/1/54 | | 65,000 | 66,248 |

| Resideo Funding 144A 6.50% 7/15/32 # | | 98,000 | 100,721 |

| Sealed Air | | | |

| 144A 5.00% 4/15/29 # | | 90,000 | 88,729 |

| 144A 6.50% 7/15/32 # | | 45,000 | 46,520 |

|

|

| Standard Building Solutions 144A 6.50% 8/15/32 # | | 115,000 | 119,174 |

| Standard Industries | | | |

| 144A 3.375% 1/15/31 # | | 90,000 | 80,256 |

| 144A 4.375% 7/15/30 # | | 30,000 | 28,417 |

| 144A 4.75% 1/15/28 # | | 28,000 | 27,450 |

|

|

| Teledyne Technologies 2.25% 4/1/28 | | 25,000 | 23,352 |

| Terex 144A 6.25% 10/15/32 # | | 100,000 | 100,000 |

| TransDigm | | | |

| 144A 6.625% 3/1/32 # | | 55,000 | 57,343 |

| 144A 6.875% 12/15/30 # | | 170,000 | 178,180 |

|

|

| Wesco Aircraft Holdings 144A 8.50% 11/15/24 #, ‡ | | 492,000 | 71,340 |

| White Cap Buyer 144A 6.875% 10/15/28 # | | 245,000 | 247,499 |

| White Cap Parent 144A PIK 8.25% 3/15/26 #, > | | 143,000 | 143,223 |

| | 2,507,929 |

| Communications — 5.60% |

| Advantage Sales & Marketing 144A 6.50% 11/15/28 # | | 116,000 | 110,227 |

| AMC Networks 4.25% 2/15/29 | | 165,000 | 119,486 |

| American Tower | | | |

| 2.30% 9/15/31 | | 30,000 | 25,829 |

| 5.20% 2/15/29 | | 75,000 | 77,487 |

| 5.45% 2/15/34 | | 40,000 | 41,836 |

|

|

| AT&T 3.50% 9/15/53 | | 35,000 | 25,734 |

| CCO Holdings | | | |

| 144A 4.50% 8/15/30 # | | 336,000 | 304,822 |

| 144A 5.375% 6/1/29 # | | 175,000 | 168,784 |

|

|

| Charter Communications Operating 3.85% 4/1/61 | | 55,000 | 33,760 |

| CMG Media 144A 8.875% 12/15/27 # | | 230,000 | 136,275 |

| | | Principalamount° | Value (US $) |

| Corporate Bonds (continued) |

| Communications (continued) |

| Connect Finco | | | |

| 144A 6.75% 10/1/26 # | | 200,000 | $ 200,000 |

| 144A 9.00% 9/15/29 # | | 200,000 | 193,797 |

| Consolidated Communications | | | |

| 144A 5.00% 10/1/28 # | | 2,000 | 1,843 |

| 144A 6.50% 10/1/28 # | | 350,000 | 331,347 |

|

|

| CSC Holdings 144A 4.50% 11/15/31 # | | 200,000 | 145,763 |

| Cumulus Media New Holdings 144A 8.00% 7/1/29 # | | 399,000 | 160,720 |

| Directv Financing 144A 5.875% 8/15/27 # | | 113,000 | 111,027 |

| Frontier Communications Holdings | | | |

| 5.875% 11/1/29 | | 60,847 | 60,460 |

| 144A 6.00% 1/15/30 # | | 225,000 | 224,817 |

| 144A 6.75% 5/1/29 # | | 99,000 | 99,769 |

| Gray Television | | | |

| 144A 4.75% 10/15/30 # | | 15,000 | 9,556 |

| 144A 5.375% 11/15/31 # | | 340,000 | 212,895 |

|

|

| Iliad Holding 144A 8.50% 4/15/31 # | | 200,000 | 215,295 |

| Matterhorn Telecom 3.125% 9/15/26 ■ | EUR | 69,000 | 76,042 |

| McGraw-Hill Education 144A 7.375% 9/1/31 # | | 81,000 | 84,107 |

| Meta Platforms | | | |

| 4.30% 8/15/29 | | 20,000 | 20,313 |

| 4.55% 8/15/31 | | 10,000 | 10,227 |

| 4.75% 8/15/34 | | 20,000 | 20,422 |

| 5.40% 8/15/54 | | 20,000 | 20,969 |

|

|

| Midcontinent Communications 144A 8.00% 8/15/32 # | | 110,000 | 112,097 |

| Netflix 4.90% 8/15/34 | | 70,000 | 72,432 |

| Rogers Communications | | | |

| 5.00% 2/15/29 | | 60,000 | 61,247 |

| 5.30% 2/15/34 | | 65,000 | 66,153 |

|

|

| Sable International Finance 144A 5.75% 9/7/27 # | | 240,000 | 239,615 |

| Sirius XM Radio 144A 4.125% 7/1/30 # | | 240,000 | 217,817 |

| Sprint Capital 6.875% 11/15/28 | | 30,000 | 32,778 |

| Stagwell Global 144A 5.625% 8/15/29 # | | 120,000 | 116,111 |

| T-Mobile USA | | | |

| 5.25% 6/15/55 | | 45,000 | 44,814 |

| 5.75% 1/15/34 | | 75,000 | 80,572 |

|

|

| Univision Communications 144A 7.375% 6/30/30 # | | 75,000 | 72,648 |

| Verizon Communications 2.875% 11/20/50 | | 35,000 | 23,760 |

| Vmed O2 UK Financing I 144A 4.75% 7/15/31 # | | 265,000 | 236,150 |

| | 4,619,803 |

Schedule of investments

Delaware Ivy Multi-Asset Income Fund

| | | Principalamount° | Value (US $) |

| Corporate Bonds (continued) |

| Consumer Cyclical — 4.64% |

| Arches Buyer 144A 6.125% 12/1/28 # | | 74,000 | $ 63,426 |

| Asbury Automotive Group | | | |

| 144A 4.625% 11/15/29 # | | 3,000 | 2,863 |

| 4.75% 3/1/30 | | 170,830 | 163,645 |

|

|

| Bath & Body Works 6.875% 11/1/35 | | 270,000 | 281,642 |

| Boyd Gaming 144A 4.75% 6/15/31 # | | 140,000 | 133,773 |

| Caesars Entertainment | | | |

| 144A 6.50% 2/15/32 # | | 85,000 | 87,978 |

| 144A 7.00% 2/15/30 # | | 275,000 | 287,480 |

| Carnival | | | |

| 144A 5.75% 3/1/27 # | | 71,000 | 71,950 |

| 144A 6.00% 5/1/29 # | | 335,000 | 339,631 |

| Carvana | | | |

| PIK 144A 13.00% 6/1/30 #, >> | | 42,600 | 46,358 |

| PIK 144A 14.00% 6/1/31 #, >> | | 37,450 | 44,145 |

|

|

| Dana 4.50% 2/15/32 | | 90,000 | 79,874 |

| Garrett Motion Holdings 144A 7.75% 5/31/32 # | | 163,000 | 166,937 |

| General Motors | | | |

| 5.40% 4/1/48 | | 12,000 | 11,041 |

| 5.95% 4/1/49 | | 14,000 | 13,888 |

| General Motors Financial | | | |

| 5.60% 6/18/31 | | 15,000 | 15,410 |

| 5.95% 4/4/34 | | 63,000 | 65,226 |

| Home Depot | | | |

| 4.85% 6/25/31 | | 10,000 | 10,369 |

| 4.875% 6/25/27 | | 15,000 | 15,393 |

| 4.95% 6/25/34 | | 45,000 | 46,801 |

|

|

| Hyundai Capital America 144A 5.275% 6/24/27 # | | 20,000 | 20,455 |

| Light & Wonder International 144A 7.25% 11/15/29 # | | 100,000 | 103,536 |

| Murphy Oil USA 4.75% 9/15/29 | | 45,000 | 43,780 |

| PetSmart 144A 7.75% 2/15/29 # | | 340,000 | 335,968 |

| Phinia 144A 6.625% 10/15/32 # | | 51,000 | 51,458 |

| Royal Caribbean Cruises 144A 5.50% 4/1/28 # | | 211,000 | 213,807 |

| S&S Holdings 144A 8.375% 10/1/31 # | | 75,000 | 75,570 |

| Scientific Games Holdings 144A 6.625% 3/1/30 # | | 300,000 | 297,927 |

| Six Flags Entertainment 144A 6.625% 5/1/32 # | | 120,000 | 124,358 |

| Staples 144A 10.75% 9/1/29 # | | 120,000 | 116,586 |

| Uber Technologies 5.35% 9/15/54 | | 20,000 | 19,848 |

| VICI Properties 4.95% 2/15/30 | | 75,000 | 75,506 |

| Victra Holdings 144A 8.75% 9/15/29 # | | 125,000 | 131,356 |

| Wand NewCo 3 144A 7.625% 1/30/32 # | | 115,000 | 121,232 |

| | | Principalamount° | Value (US $) |

| Corporate Bonds (continued) |

| Consumer Cyclical (continued) |

|

| ZF North America Capital 144A 6.75% 4/23/30 # | | 150,000 | $ 151,378 |

| | 3,830,595 |

| Consumer Non-Cyclical — 1.55% |

| AbbVie 5.35% 3/15/44 | | 10,000 | 10,557 |

| Bunge Limited Finance 4.20% 9/17/29 | | 65,000 | 64,853 |

| CHS 144A 5.25% 5/15/30 # | | 210,000 | 193,436 |

| DaVita | | | |

| 144A 3.75% 2/15/31 # | | 115,000 | 103,826 |

| 144A 4.625% 6/1/30 # | | 70,000 | 66,783 |

| Fiesta Purchaser | | | |

| 144A 7.875% 3/1/31 # | | 52,000 | 55,218 |

| 144A 9.625% 9/15/32 # | | 80,000 | 83,011 |

| HCA | | | |

| 5.45% 4/1/31 | | 30,000 | 31,267 |

| 6.00% 4/1/54 | | 85,000 | 89,874 |

|

|

| Legacy LifePoint Health 144A 4.375% 2/15/27 # | | 95,000 | 93,244 |

| MajorDrive Holdings IV 144A 6.375% 6/1/29 # | | 239,000 | 232,707 |

| Royalty Pharma 3.35% 9/2/51 | | 175,000 | 121,063 |

| Surgery Center Holdings 144A 7.25% 4/15/32 # | | 130,000 | 135,853 |

| | 1,281,692 |

| Electric — 1.66% |

| Berkshire Hathaway Energy 2.85% 5/15/51 | | 35,000 | 23,712 |

| Calpine | | | |

| 144A 5.00% 2/1/31 # | | 60,000 | 58,146 |

| 144A 5.125% 3/15/28 # | | 55,000 | 54,275 |

|

|

| Constellation Energy Generation 5.75% 3/15/54 | | 45,000 | 47,656 |

| Dominion Energy 6.875% 2/1/55 μ | | 35,000 | 37,181 |

| DTE Energy 5.10% 3/1/29 | | 45,000 | 46,357 |

| Duke Energy 6.45% 9/1/54 μ | | 20,000 | 20,816 |

| Duke Energy Carolinas 4.95% 1/15/33 | | 110,000 | 113,456 |

| Lightning Power 144A 7.25% 8/15/32 # | | 135,000 | 142,074 |

| NextEra Energy Capital Holdings | | | |

| 5.55% 3/15/54 | | 60,000 | 62,744 |

| 5.749% 9/1/25 | | 20,000 | 20,208 |

| Oglethorpe Power | | | |

| 3.75% 8/1/50 | | 35,000 | 26,997 |

| 6.20% 12/1/53 | | 10,000 | 10,957 |

| Pacific Gas & Electric | | | |

| 3.30% 8/1/40 | | 40,000 | 31,089 |

| 4.95% 7/1/50 | | 95,000 | 86,450 |

Schedule of investments

Delaware Ivy Multi-Asset Income Fund

| | | Principalamount° | Value (US $) |

| Corporate Bonds (continued) |

| Electric (continued) |

| PacifiCorp | | | |

| 5.10% 2/15/29 | | 10,000 | $ 10,336 |

| 5.80% 1/15/55 | | 5,000 | 5,251 |

|

|

| Southern California Edison 5.20% 6/1/34 | | 105,000 | 108,902 |

| Vistra 144A 7.00% 12/15/26 #, μ, ψ | | 380,000 | 388,228 |

| Vistra Operations 144A 6.95% 10/15/33 # | | 65,000 | 73,333 |

| | 1,368,168 |

| Energy — 4.30% |

| Archrock Partners 144A 6.625% 9/1/32 # | | 105,000 | 107,751 |

| Ascent Resources Utica Holdings 144A 5.875% 6/30/29 # | | 120,000 | 118,647 |

| BP Capital Markets America 5.227% 11/17/34 | | 25,000 | 26,038 |

| Cheniere Energy Partners | | | |

| 4.50% 10/1/29 | | 95,000 | 93,760 |

| 144A 5.75% 8/15/34 # | | 21,000 | 21,893 |

|

|

| Civitas Resources 144A 8.625% 11/1/30 # | | 130,000 | 137,842 |

| Diamondback Energy | | | |

| 5.40% 4/18/34 | | 88,000 | 89,875 |

| 5.75% 4/18/54 | | 79,000 | 79,662 |

|

|

| Enbridge 5.75% 7/15/80 μ | | 15,000 | 14,745 |

| Energy Transfer | | | |

| 5.75% 2/15/33 | | 135,000 | 141,299 |

| 5.95% 5/15/54 | | 60,000 | 61,455 |

| Enterprise Products Operating | | | |

| 4.95% 2/15/35 | | 30,000 | 30,478 |

| 5.55% 2/16/55 | | 25,000 | 25,844 |

| Genesis Energy | | | |

| 7.75% 2/1/28 | | 95,000 | 96,265 |

| 7.875% 5/15/32 | | 30,000 | 30,568 |

|

|

| Gulfport Energy Operating 144A 6.75% 9/1/29 # | | 110,000 | 111,424 |

| Hilcorp Energy I | | | |

| 144A 6.00% 2/1/31 # | | 25,000 | 24,362 |

| 144A 6.25% 4/15/32 # | | 250,000 | 243,545 |

| Kinder Morgan | | | |

| 5.00% 2/1/29 | | 15,000 | 15,327 |

| 5.20% 6/1/33 | | 25,000 | 25,318 |

|

|

| Matador Resources 144A 6.25% 4/15/33 # | | 75,000 | 73,930 |

| Murphy Oil 6.00% 10/1/32 | | 40,000 | 39,496 |

| | | Principalamount° | Value (US $) |

| Corporate Bonds (continued) |

| Energy (continued) |

| Nabors Industries | | | |

| 144A 8.875% 8/15/31 # | | 45,000 | $ 42,847 |

| 144A 9.125% 1/31/30 # | | 90,000 | 92,896 |

|

|

| NGL Energy Operating 144A 8.375% 2/15/32 # | | 125,000 | 128,913 |

| Noble Finance II 144A 8.00% 4/15/30 # | | 85,000 | 87,767 |

| NuStar Logistics 6.00% 6/1/26 | | 146,000 | 146,982 |

| Occidental Petroleum | | | |

| 5.375% 1/1/32 | | 20,000 | 20,291 |

| 5.55% 10/1/34 | | 15,000 | 15,239 |

| 6.05% 10/1/54 | | 15,000 | 15,241 |

| 6.125% 1/1/31 | | 48,000 | 50,684 |

|

|

| ONEOK 5.65% 11/1/28 | | 20,000 | 20,914 |

| SM Energy | | | |

| 144A 6.75% 8/1/29 # | | 40,000 | 40,197 |

| 144A 7.00% 8/1/32 # | | 49,000 | 49,223 |

|

|

| Sunoco 144A 7.25% 5/1/32 # | | 70,000 | 74,259 |

| Targa Resources Partners 5.00% 1/15/28 | | 20,000 | 20,011 |

| Transocean | | | |

| 144A 8.00% 2/1/27 # | | 168,000 | 168,029 |

| 144A 8.50% 5/15/31 # | | 120,000 | 119,315 |

| USA Compression Partners | | | |

| 6.875% 9/1/27 | | 140,000 | 141,294 |

| 144A 7.125% 3/15/29 # | | 20,000 | 20,615 |

| Venture Global LNG | | | |

| 144A 7.00% 1/15/30 # | | 115,000 | 117,572 |

| 144A 8.375% 6/1/31 # | | 175,000 | 184,906 |

|

|

| Vital Energy 144A 7.875% 4/15/32 # | | 155,000 | 150,265 |

| Weatherford International 144A 8.625% 4/30/30 # | | 225,000 | 234,618 |

| | 3,551,602 |

| Finance Companies — 1.05% |

| AerCap Holdings 5.875% 10/10/79 μ | | 225,000 | 225,136 |

| AerCap Ireland Capital DAC 3.65% 7/21/27 | | 150,000 | 147,158 |

| Air Lease 4.65% 6/15/26 μ, ψ | | 130,000 | 127,048 |

| Apollo Debt Solutions BDC 144A 6.70% 7/29/31 # | | 30,000 | 30,919 |

| Aviation Capital Group | | | |

| 144A 3.50% 11/1/27 # | | 105,000 | 101,334 |

| 144A 5.375% 7/15/29 # | | 35,000 | 35,770 |

|

|

| Blue Owl Credit Income 144A 5.80% 3/15/30 # | | 70,000 | 69,356 |

Schedule of investments

Delaware Ivy Multi-Asset Income Fund

| | | Principalamount° | Value (US $) |

| Corporate Bonds (continued) |

| Finance Companies (continued) |

|

| Fortress Transportation and Infrastructure Investors 144A 7.00% 6/15/32 # | | 120,000 | $ 126,072 |

| | 862,793 |

| Industrials — 0.07% |

| Arcosa 144A 6.875% 8/15/32 # | | 55,000 | 57,607 |

| | 57,607 |

| Insurance — 2.14% |

| Aon 2.90% 8/23/51 | | 25,000 | 16,631 |

| Aon North America | | | |

| 5.30% 3/1/31 | | 45,000 | 46,970 |

| 5.75% 3/1/54 | | 10,000 | 10,602 |

|

|

| Ardonagh Finco 144A 7.75% 2/15/31 # | | 200,000 | 206,916 |

| Athene Global Funding 144A 1.985% 8/19/28 # | | 30,000 | 27,255 |

| Elevance Health 5.15% 6/15/29 | | 50,000 | 51,895 |

| Howden UK Refinance | | | |

| 144A 7.25% 2/15/31 # | | 200,000 | 207,708 |

| 144A 8.125% 2/15/32 # | | 200,000 | 205,767 |

| HUB International | | | |

| 144A 5.625% 12/1/29 # | | 130,000 | 127,615 |

| 144A 7.375% 1/31/32 # | | 120,000 | 123,986 |

| Jones Deslauriers Insurance Management | | | |

| 144A 8.50% 3/15/30 # | | 205,000 | 219,509 |

| 144A 10.50% 12/15/30 # | | 102,000 | 111,011 |

|

|

| New York Life Global Funding 144A 5.45% 9/18/26 # | | 60,000 | 61,701 |

| Panther Escrow Issuer 144A 7.125% 6/1/31 # | | 125,000 | 131,212 |

| UnitedHealth Group | | | |

| 4.90% 4/15/31 | | 40,000 | 41,392 |

| 5.375% 4/15/54 | | 35,000 | 36,412 |

| 5.50% 7/15/44 | | 40,000 | 42,357 |

|

|

| USI 144A 7.50% 1/15/32 # | | 90,000 | 93,348 |

| | 1,762,287 |

| Natural Gas — 0.08% |

| Sempra 6.40% 10/1/54 μ | | 65,000 | 65,285 |

| | 65,285 |

| Real Estate Investment Trusts — 0.09% |

| Extra Space Storage 5.40% 2/1/34 | | 75,000 | 77,510 |

| | 77,510 |

| | | Principalamount° | Value (US $) |

| Corporate Bonds (continued) |

| Technology — 1.39% |

| Amentum Escrow 144A 7.25% 8/1/32 # | | 40,000 | $ 41,782 |

| Block 144A 6.50% 5/15/32 # | | 90,000 | 93,831 |

| Broadcom | | | |

| 5.05% 7/12/29 | | 30,000 | 30,914 |

| 5.15% 11/15/31 | | 20,000 | 20,764 |

|

|

| CDW 3.276% 12/1/28 | | 45,000 | 42,653 |

| Cloud Software Group 144A 6.50% 3/31/29 # | | 205,000 | 204,141 |

| Entegris 144A 4.75% 4/15/29 # | | 75,000 | 73,976 |

| NCR Voyix 144A 5.00% 10/1/28 # | | 78,000 | 76,624 |

| Oracle | | | |

| 3.60% 4/1/50 | | 77,000 | 58,671 |

| 4.20% 9/27/29 | | 20,000 | 19,973 |

| 4.65% 5/6/30 | | 70,000 | 71,415 |

| 5.375% 9/27/54 | | 20,000 | 20,003 |

|

|

| Roper Technologies 4.90% 10/15/34 | | 30,000 | 30,222 |

| Seagate HDD Cayman | | | |

| 5.75% 12/1/34 | | 88,000 | 88,779 |