Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Searchable text section of graphics shown above

[GRAPHIC}

International Investor Day

June 12, 2003

[LOGO]

1

[GRAPHIC]

[LOGO]

David Banks, SVP Investor Relations

Welcome & Opening Comments

2

Statements in this presentation regarding First Data Corporation’s business which are not historical facts are “forward-looking statements.” All forward-looking statements are inherently uncertain as they are based on various expectations and assumptions concerning future events and they are subject to numerous known and unknown risks and uncertainties which could cause actual events or results to differ materially from those projected. Please refer to the company’s meaningful cautionary statements contained on the last slide of this presentation and the company’s 2002 Annual Report on Form 10-K for a more detailed list of risks and uncertainties.

3

This communication is not a solicitation of a proxy from any security holder of First Data Corporation or Concord EFS, Inc., and First Data Corporation and Concord EFS, Inc. will be filing with the Securities and Exchange Commission a definitive joint proxy statement/prospectus to be mailed to security holders and other relevant documents concerning the planned merger of Concord EFS, Inc. with a subsidiary of First Data Corporation. WE URGE INVESTORS TO READ THE DEFINITIVE VERSION OF THE JOINT PROXY STATEMENT / PROSPECTUS AND ANY OTHER RELEVANT DOCUMENTS TO BE FILED WITH THE SEC, BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. Investors will be able to obtain the documents free of charge at the SEC’s website, www.sec.gov. In addition, documents filed with the SEC by First Data Corporation will be available free of charge from First Data Investor Relations, 6200 S. Quebec St., Suite 340, Greenwood Village, CO, 80111. Documents filed with the SEC by Concord EFS, Inc. will be available free of charge from Concord Investor Relations, 2525 Horizon Lake Drive, Suite 120, Memphis, TN, 38133.

First Data Corporation and its directors and executive officers and other members of its management and employees, may be deemed to be participants in the solicitation of proxies from the stockholders of First Data Corporation in connection with the merger. Information about the directors and executive officers of First Data Corporation and their ownership of First Data Corporation stock is set forth in the proxy statement for First Data Corporation’s 2003 annual meeting of stockholders.

4

• First Data Overview

• Western Union International

• First Data International

• Questions & Answers

[LOGO]

5

[GRAPHIC]

• Real time

• Pre-paid

• Pay later

6

[LOGO]

Well Positioned in High Growth Markets

7

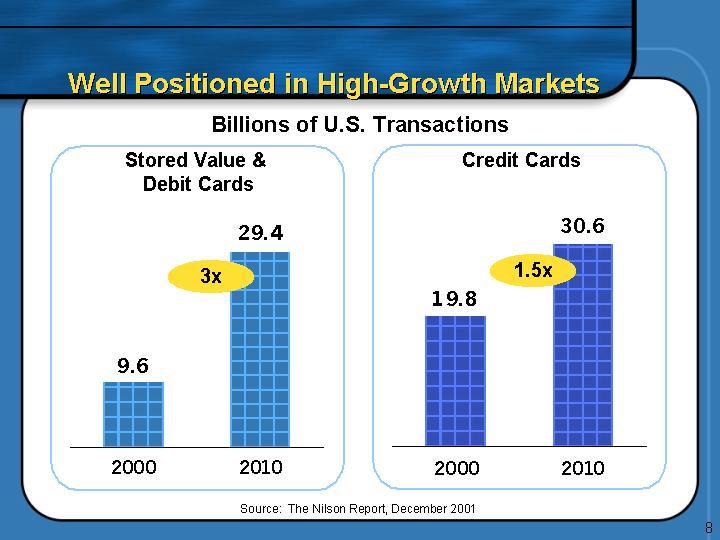

Well Positioned in High-Growth Markets

Billions of U.S. Transactions

Stored Value & Debit Cards

[CHART]

Credit Cards

[CHART]

Source: The Nilson Report, December 2001

8

Well Positioned in Huge Markets

Estimated Remittance Market = $138B

[CHART] [LOGO]

Huge market opportunity

Source: International Monetary Fund, 2002

9

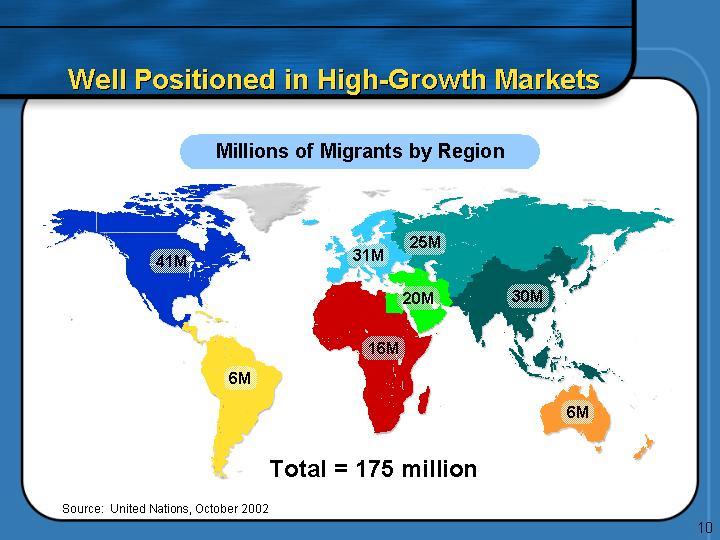

Well Positioned in High-Growth Markets

Millions of Migrants by Region

[GRAPHIC]

Total = 175 million

Source: United Nations, October 2002

10

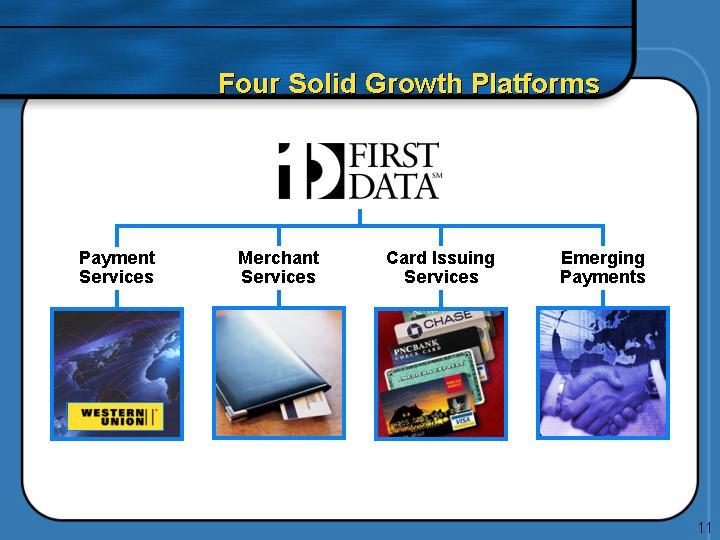

Four Solid Growth Platforms

[LOGO]

Payment |

| Merchant |

| Card Issuing |

| Emerging |

[GRAPHIC] |

| [GRAPHIC] |

| [GRAPHIC] |

| [GRAPHIC] |

11

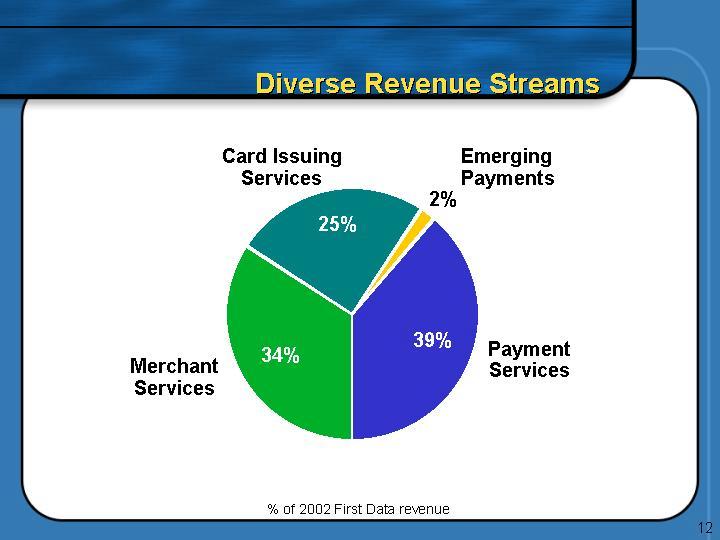

[CHART]

% of 2002 First Data revenue

12

[GRAPHIC]

• 2002 revenues $3.2B

• 80% Western Union money transfer

• 159,000 worldwide locations

• Driven by millions of transactions

• Moved $700B in face value in 2002

Sales and Distribution Powerhouse

13

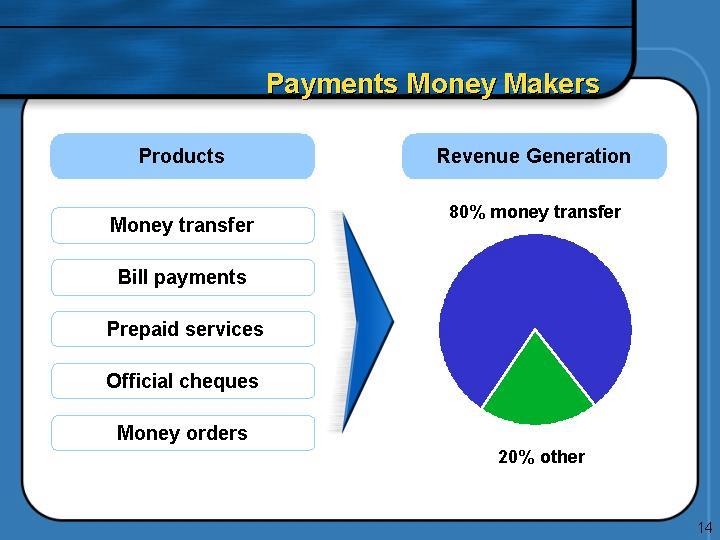

Products

Money transfer

Bill payments

Prepaid services

Official cheques

Money orders

[GRAPHIC]

Revenue Generation

[CHART]

14

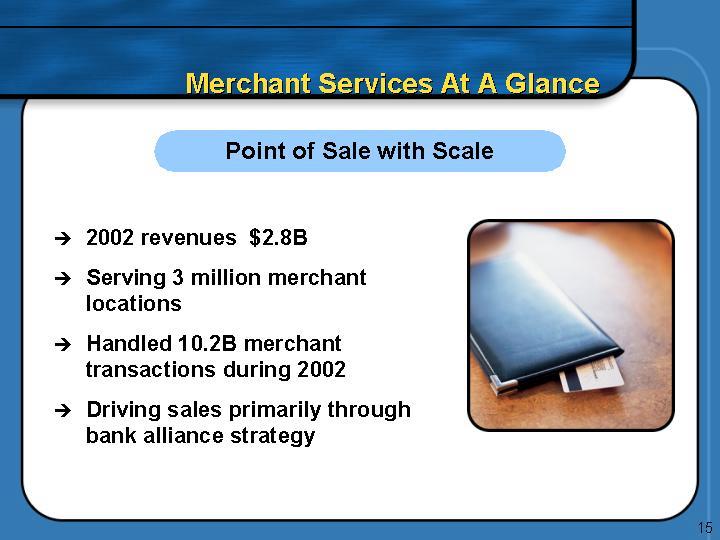

Point of Sale with Scale

• 2002 revenues $2.8B

• Serving 3 million merchant locations

• Handled 10.2B merchant transactions during 2002

• Driving sales primarily through bank alliance strategy

[GRAPHIC]

15

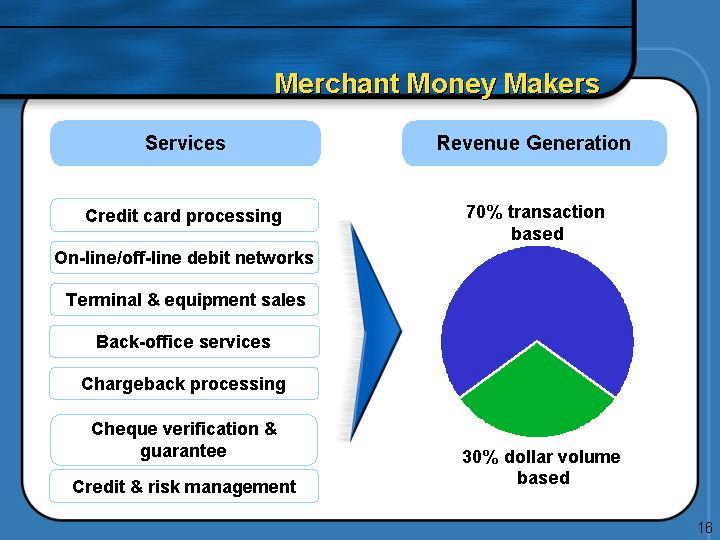

Services

Credit card processing

On-line/off-line debit networks

Terminal & equipment sales

Back-office services

Chargeback processing

Cheque verification & guarantee

Credit & risk management

[GRAPHIC]

Revenue Generation

[CHART]

16

Card Issuing Services At A Glance

• 2002 revenues $1.9B

• Servicing 324M card accounts

• nearly 90M cards in conversion pipeline

• Providing support to 1,400 card issuers

[GRAPHIC]

First Data’s Outsourcing Segment

17

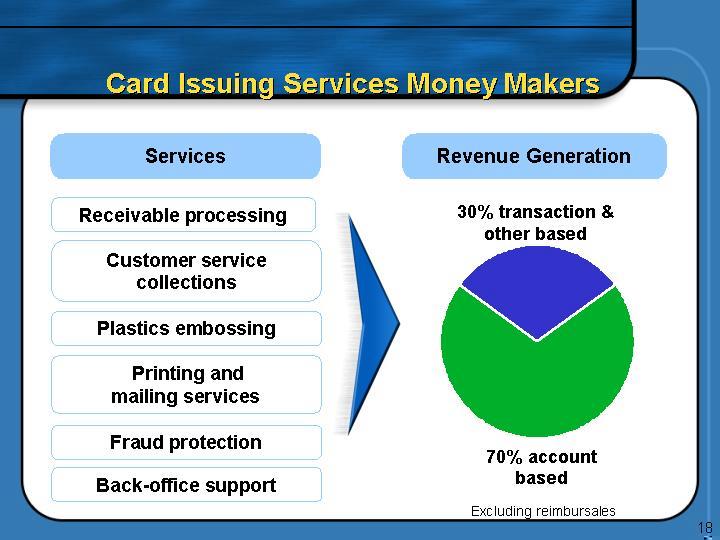

Card Issuing Services Money Makers

Services

Receivable processing

Customer Service Collections

Plastics embossing

Printing and mailing services

Fraud protection

Back-office support

[GRAPHIC]

Revenue Generation

[CHART]

Excluding reimbursales

18

• About $200M +/- annual revenue run rate

• Providing business-to- government tax payments

• Laying groundwork for future of cell phones as payment devices

[GRAPHIC]

Payments of the Future

19

[LOGO]

[GRAPHIC]

20

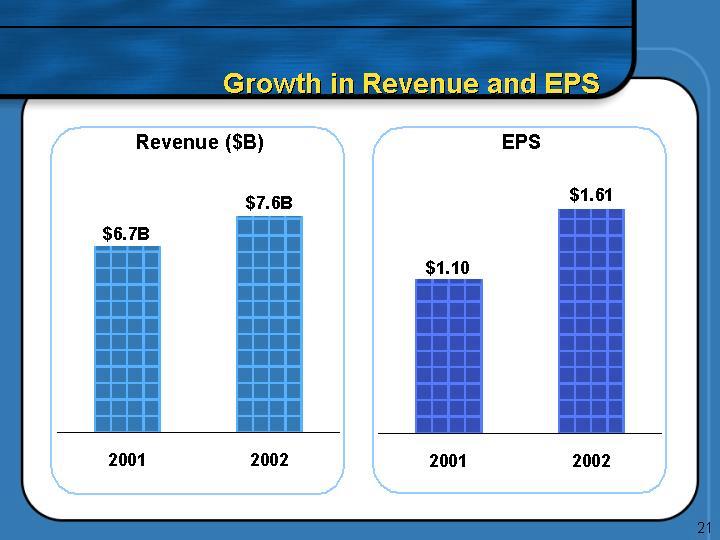

Revenue ($B)

[CHART]

EPS

[CHART]

21

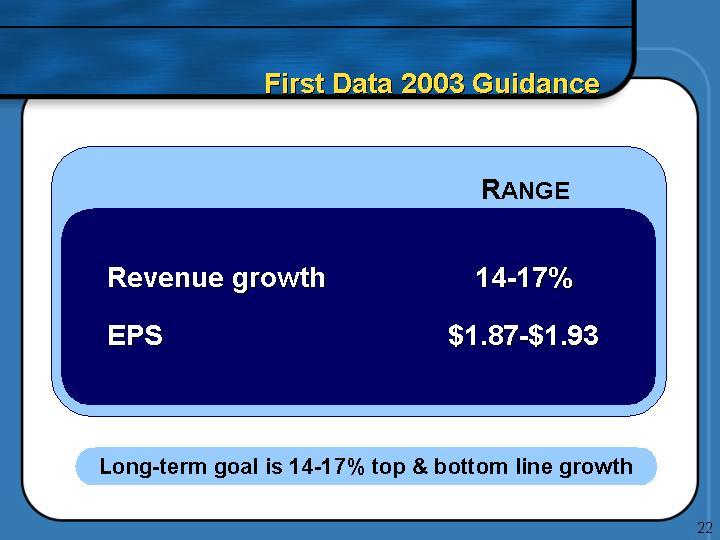

|

| RANGE |

|

|

|

|

|

Revenue growth |

| 14-17 | % |

EPS |

| $1.87-$1.93 |

|

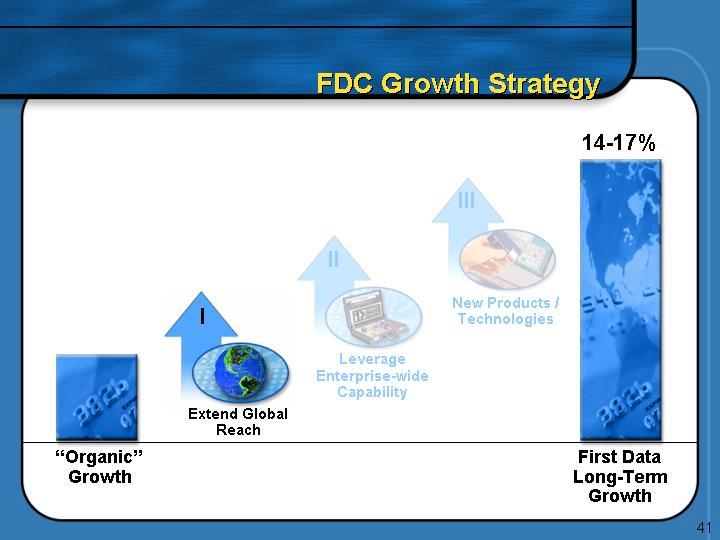

Long-term goal is 14-17% top & bottom line growth

22

Charlie Fote

Chairman and CEO

23

[GRAPHIC]

Christina Gold

President

Western Union

[GRAPHIC]

Scott Betts

President

Merchant Services

24

[GRAPHIC]

Kim Patmore

Chief Financial

Officer

[GRAPHIC]

Mike Whealy

Chief Administrative

Officer

25

[GRAPHIC]

Mike Yerington

President

WU North America

[GRAPHIC]

Bill Thomas

President

WU International

26

[GRAPHIC]

Pam Patsley

President

First Data International

[GRAPHIC]

Garen Staglin

President & CEO

eONE Global

27

First Data - A Leader by Design

[GRAPHIC]

• Makes commerce more secure, efficient and convenient

• Leveraging extraordinary infrastructure and distribution channels

• Record of flawless execution

• Developing the next generation of payment services

28

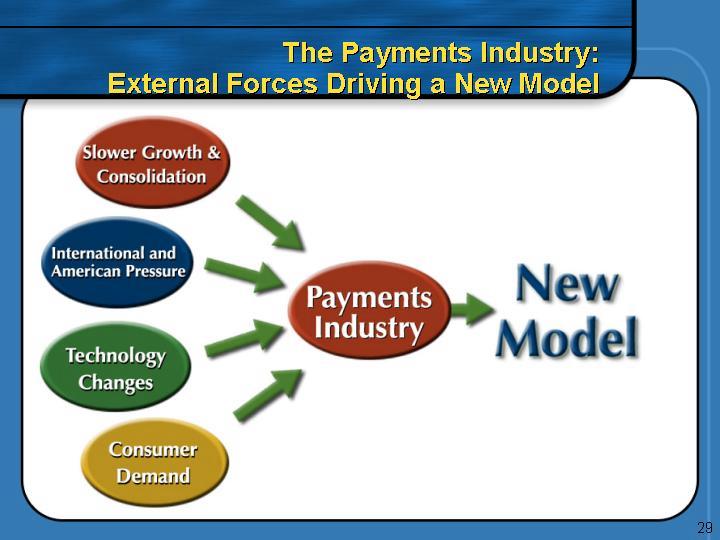

The Payments Industry:

External Forces Driving a New Model

[GRAPHIC]

29

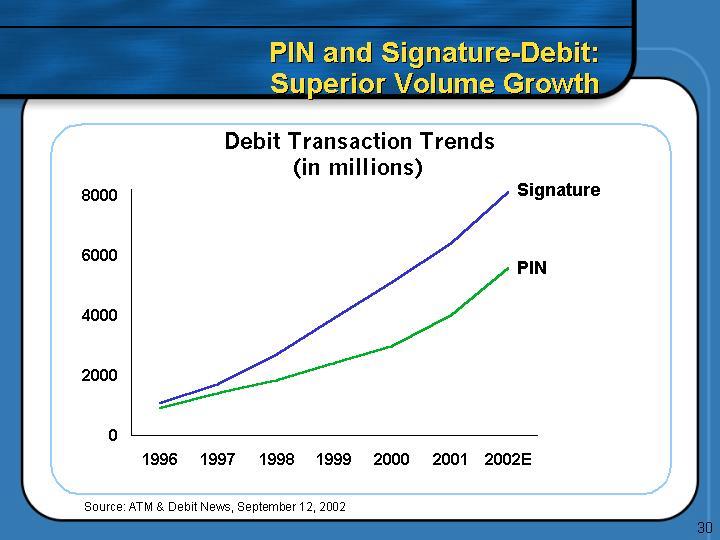

PIN and Signature-Debit:

Superior Volume Growth

Debit Transaction Trends

(in millions)

[CHART]

Source: ATM & Debit News, September 12, 2002

30

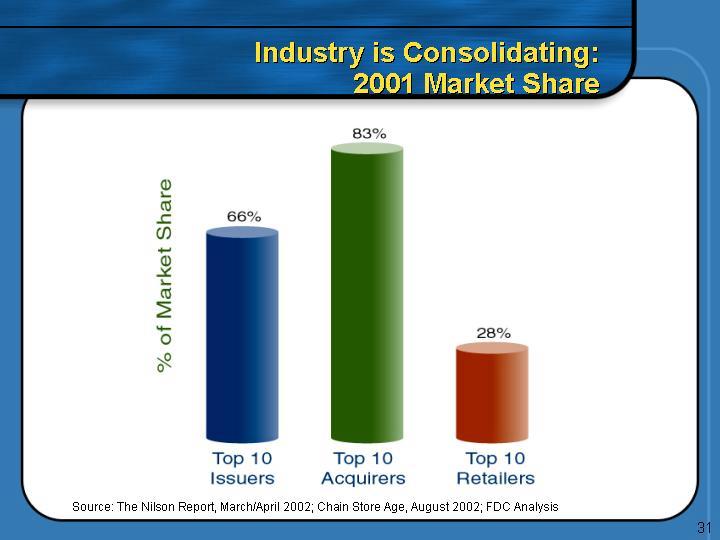

Industry is Consolidating:

2001 Market Share

[CHART]

Source: The Nilson Report, March/April 2002; Chain Store Age, August 2002; FDC Analysis

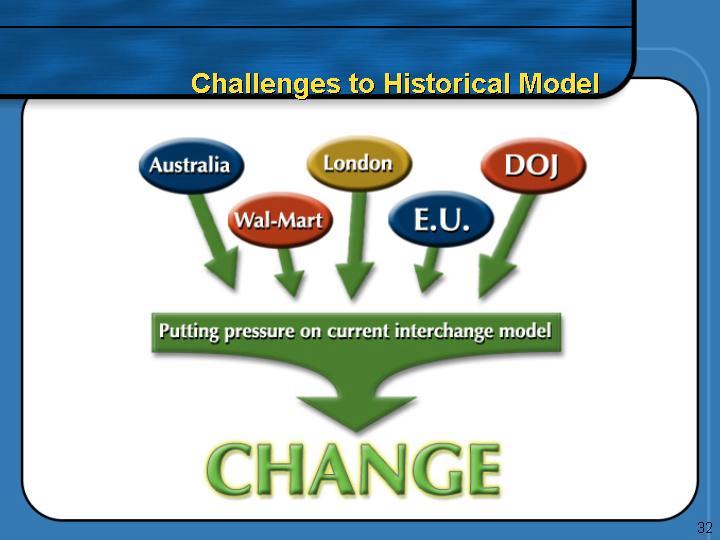

31

Challenges to Historical Model

[GRAPHIC]

32

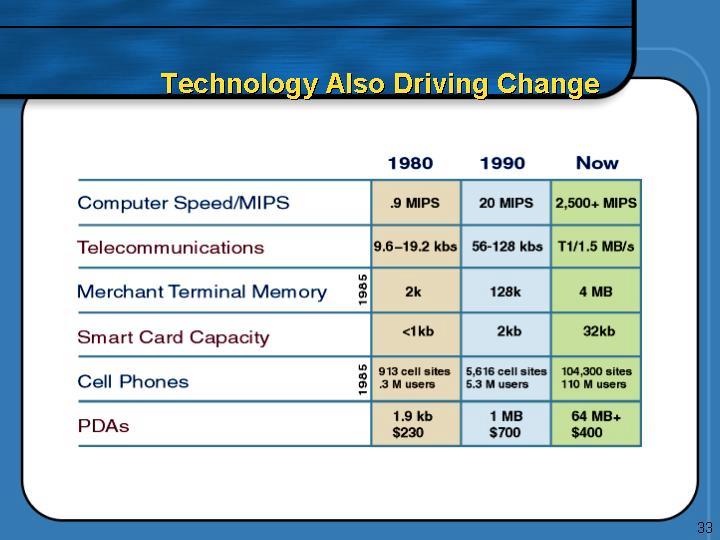

Technology Also Driving Change

|

| 1980 |

| 1990 |

| Now |

|

Computer Speed/MIPS |

| .9MIPS |

| 20MIPS |

| 2,500+MIPS |

|

Telecommunications |

| 9.6-19.2 kbs |

| 56-128 kbs |

| T1/1.5 MB/s |

|

Merchant Terminal Memory 1985 |

| 2k |

| 128k |

| 4 MB |

|

Smart Card Capacity |

| <1kb |

| 2kb |

| 32kb |

|

Cell Phones 1985 |

| 913 cell sites |

| 5,616 cell sites |

| 104,300 sites |

|

PDAs |

| 1.9kb |

| 1 Mb |

| 64 MB+ |

|

33

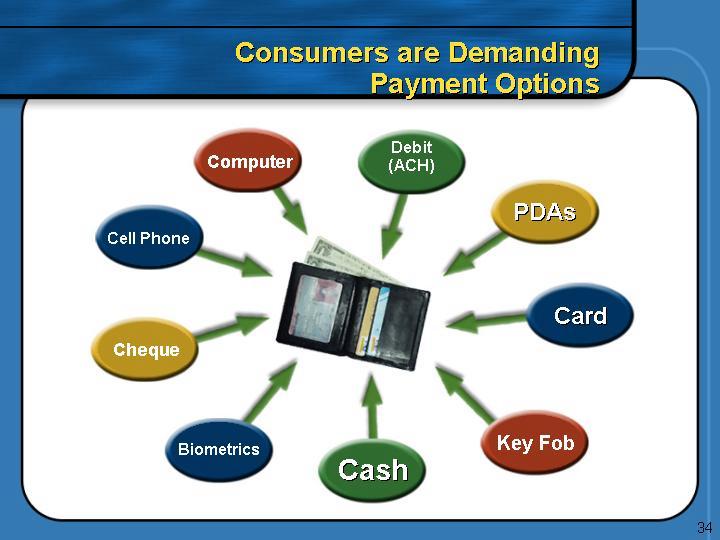

Consumers are Demanding Payment Options

[GRAPHIC]

34

[GRAPHIC]

35

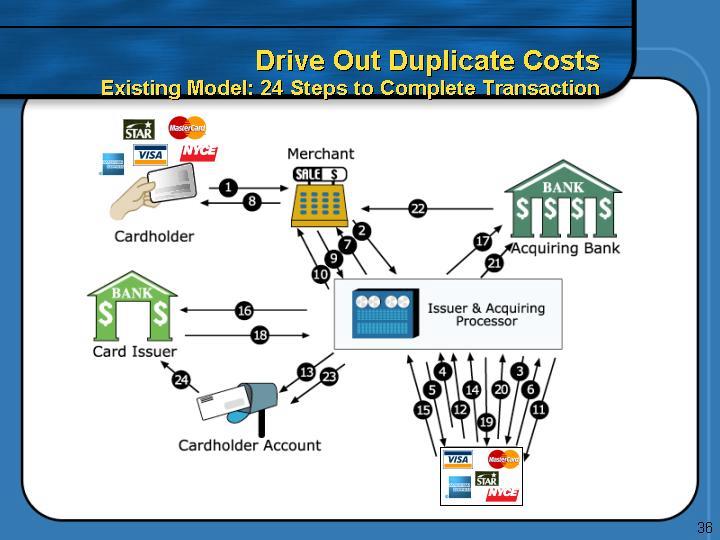

Drive Out Duplicate Costs

Existing Model: 24 Steps to Complete Transaction

[GRAPHIC]

36

Drive Out Duplicate Costs

New Model: 14 Steps to Complete Transaction

[GRAPHIC]

37

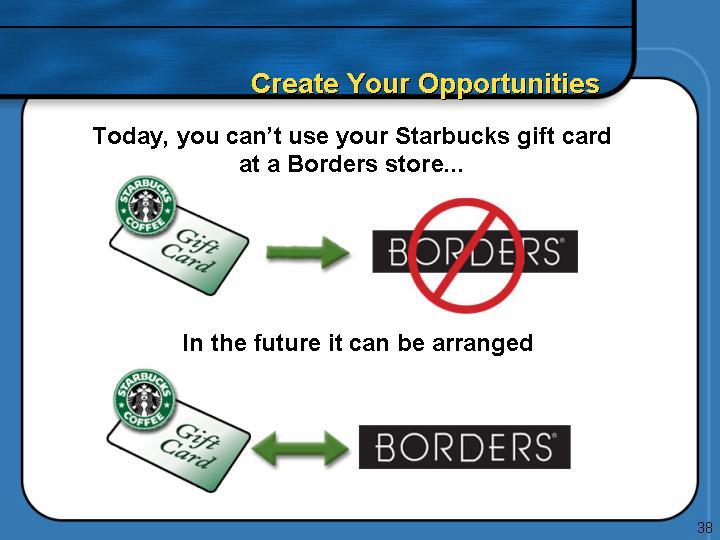

Today, you can’t use your Starbucks gift card at a Borders store...

[GRAPHIC]

In the future it can be arranged

[GRAPHIC]

38

[GRAPHIC]

Your Customer’s Satisfaction

39

What’s Driving the New Model?

[GRAPHIC]

40

[CHART]

41

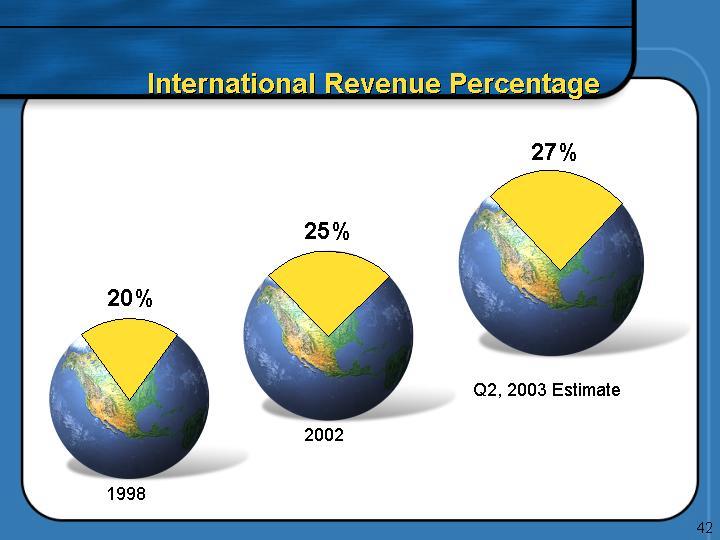

International Revenue Percentage

1998

[CHART]

2002

[CHART]

Q2, 2003 Estimate

[CHART]

42

Our International Revenue Goal in 2007

Pre-Concord

[CHART]

Post-Concord

[CHART]

43

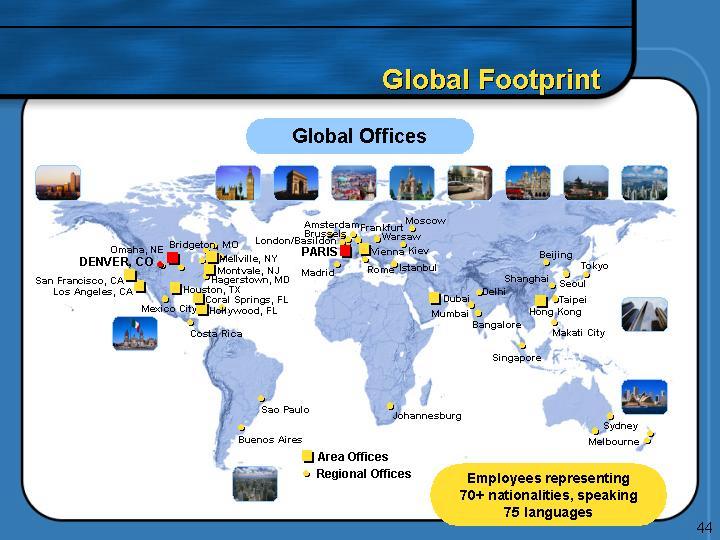

Global Offices

[GRAPHIC]

Employees representing 70+ nationalities, speaking 75 languages

44

Agenda

• First Data Overview

• Western Union International

• First Data International

• Questions & Answers

[LOGO]

45

[LOGO]

President, Western Union International

46

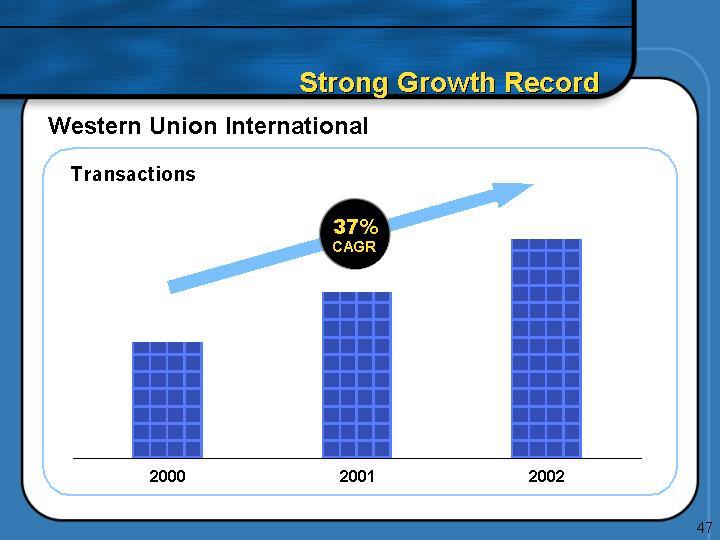

Western Union International

Transactions

[CHART]

47

[GRAPHIC]

48

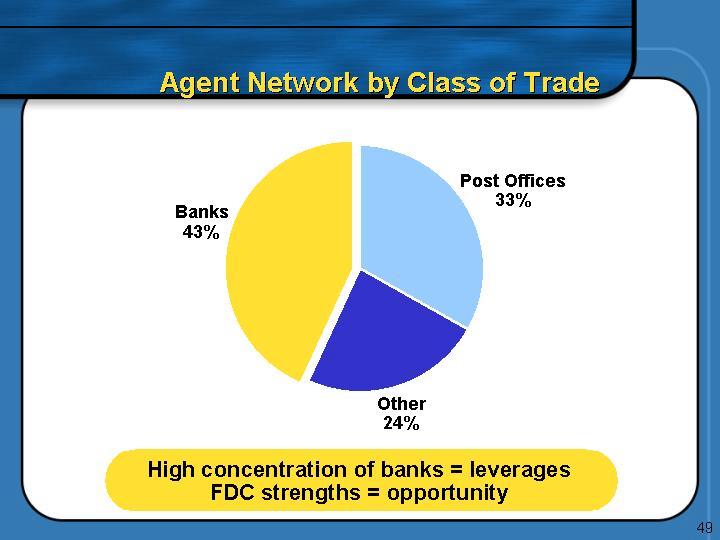

Agent Network by Class of Trade

[CHART]

High concentration of banks = leverages

FDC strengths = opportunity

49

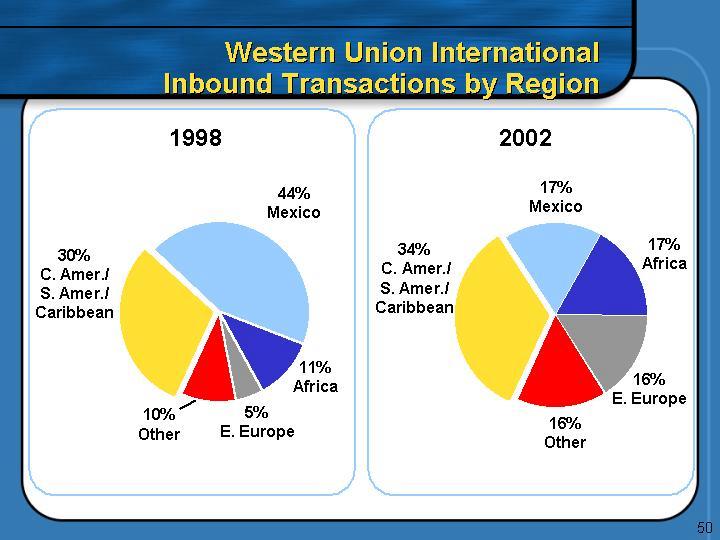

Western Union International

Inbound Transactions by Region

1998

[CHART]

2002

[CHART]

50

• Sharing relationships to bring expanded product offerings to key partners around the globe

• offering card issuing and merchant services to existing bank partners and agent base

• utilising Western Union agent outlets to distribute First Data products

• introducing Western Union products through Card and Merchant business channels

[GRAPHIC]

51

• First Data Overview

• Western Union International

• First Data International

• Questions & Answers

[LOGO]

52

[GRAPHIC]

Pam Patsley

President, First Data International

53

Our International Revenue Goal in 2007

[CHART]

Pre-Concord

[CHART]

Post-Concord

54

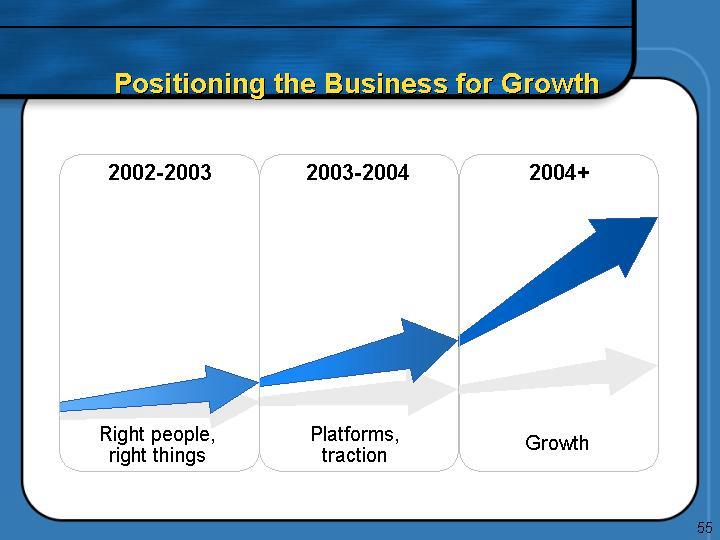

Positioning the Business for Growth

[CHART]

55

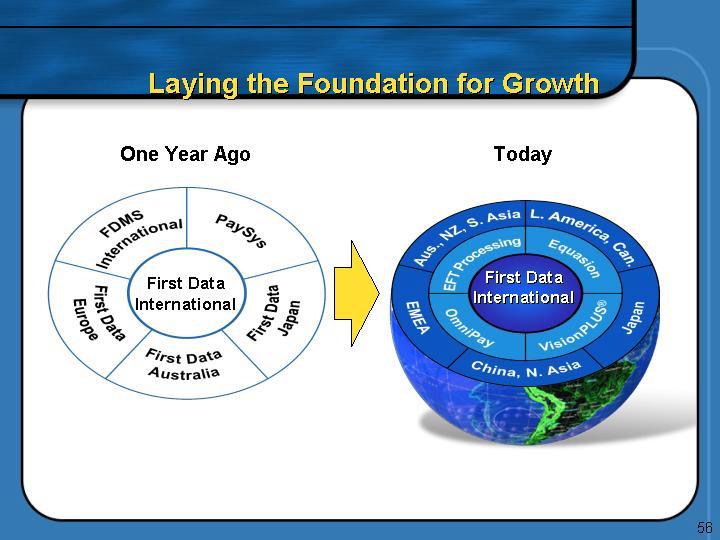

Laying the Foundation for Growth

[Chart]

56

Key Takeaways

[GRAPHIC] Strong organisation

[GRAPHIC] Large worldwide opportunity

[GRAPHIC] A global strategy

[GRAPHIC] Strategy at work – World Tour

57

Key Takeaways

[GRAPHIC] Strong organisation

[GRAPHIC] Large worldwide opportunity

[GRAPHIC] A global Strategy

[GRAPHIC] Strategy at work — World Tour

58

First Data International

• Formed May 2002

• Leverage capabilities of existing businesses:

• Card issuing services

• Merchant services

• VisionPLUSâ transaction software

• Payment card and electronic banking services

• Western Union International

• Strong infrastructure, worldwide leadership team

• Single source provider of end-to-end solutions

[GRAPHIC]

59

Worldwide Presence

Headquarters: Paris, France

[GRAPHIC]

60

Strong Regional Leaders

[GRAPHIC]

Peter Harrington

President

Latin America

& Canada

[GRAPHIC]

Gerald Hawkins

President

Europe, the Middle

East & Africa

[GRAPHIC]

Henry Tsuei

President

China & North Asia

[GRAPHIC]

Greg Nash

President

Australia, New Zealand

& South Asia

[GRAPHIC]

Kozo Watanabe

President

Japan

[GRAPHIC]

An international team of 3,800 people

61

Key Takeways

[GRAPHIC] Strong organisation

[GRAPHIC] Large worldwide opportunity

[GRAPHIC] A global strategy

[GRAPHIC] Strategy at work – World Tour

62

Factors Driving Growth

• Increased use of electronic payments

• Migration to EMV smart cards*

• Global commerce

• eCommerce

[GRAPHIC]

* Europay, MasterCard, Visa interoperable smart card standard

63

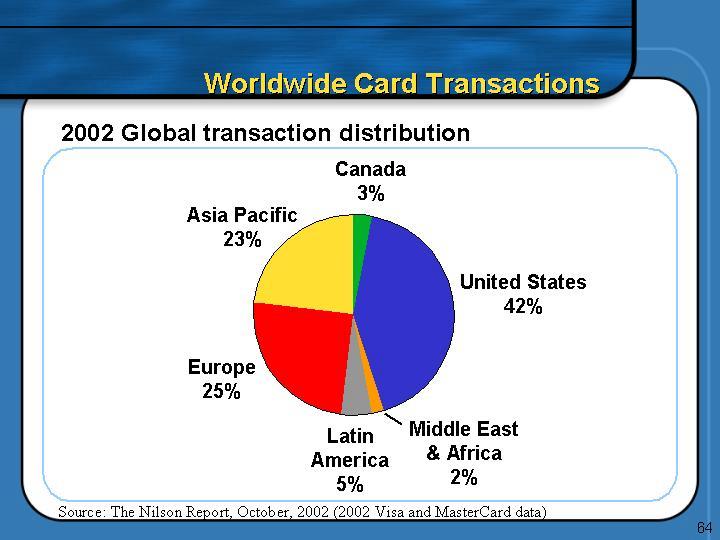

Worldwide Card Transactions

2002 Global transaction distribution

[CHART]

Source: The Nilson Report, October, 2002 (2002 Visa and MasterCard data)

64

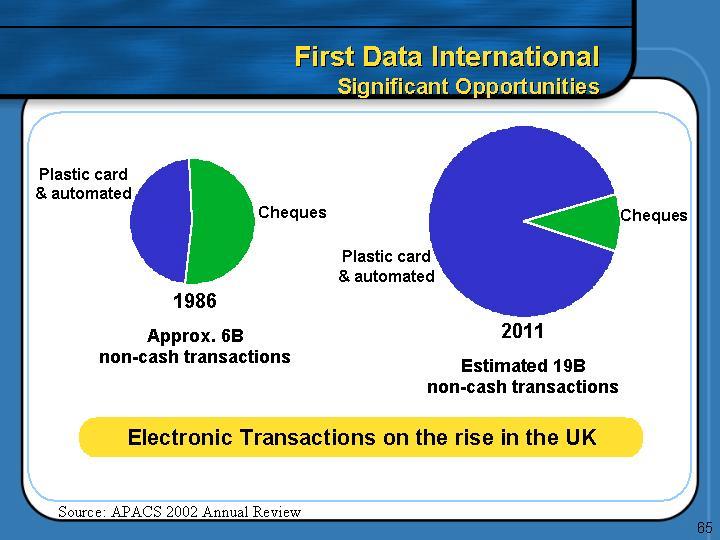

First Data International

Significant Opportunities

[Chart]

Approx. 6B

non-cash transactions

[Chart]

Estimated 19B

non-cash transactions

Electronic Transactions of the rise in the UK

Source: APACS 2002 Annual Review

65

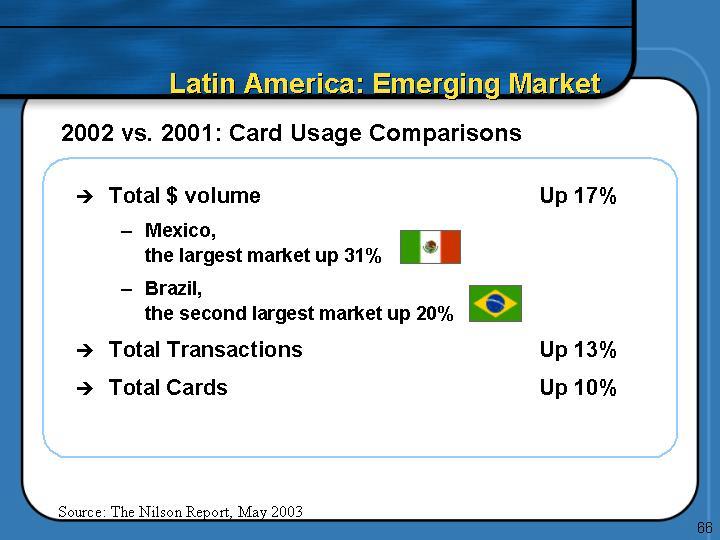

Latin America: Emerging Market

2002 vs. 2001: Card Usage Comparisons

• | Total $ Volume | Up 17% | |

| • | Mexico, | [GRAPHIC] |

|

|

|

|

| • | Brazil, | [GRAPHIC] |

|

|

|

|

• | Total Transactions | Up 13% | |

• | Total Cards | Up 10% | |

Source: The Nilson Report, May 2003

66

Key Takeaways

[GRAPHIC] Strong organisation

[GRAPHIC] Large worldwide opportunity

[GRAPHIC] A global strategy

[GRAPHIC] Strategy at work – World Tour

67

Our Strategy

• Aggressively grow the business as one company

• Attract / retain best-in-class talent

• Innovate new products and enter new geographies

• Grow existing customers through superior service

• Leverage existing platforms and capabilities

68

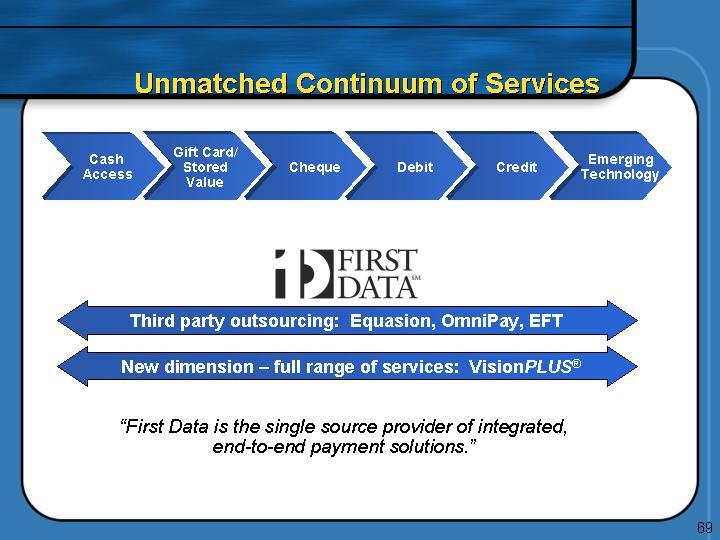

Unmatched Continuum of Services

[GRAPHIC]

Cash | Gift Card/ | Cheque | Debit | Credit | Emerging |

[LOGO]

Third party outsourcing: Equasion, OmniPay, EFT

New dimension – full range of services: VisionPLUSâ

“First Data is the single source provider of integrated,

end-to-end payment solutions.”

69

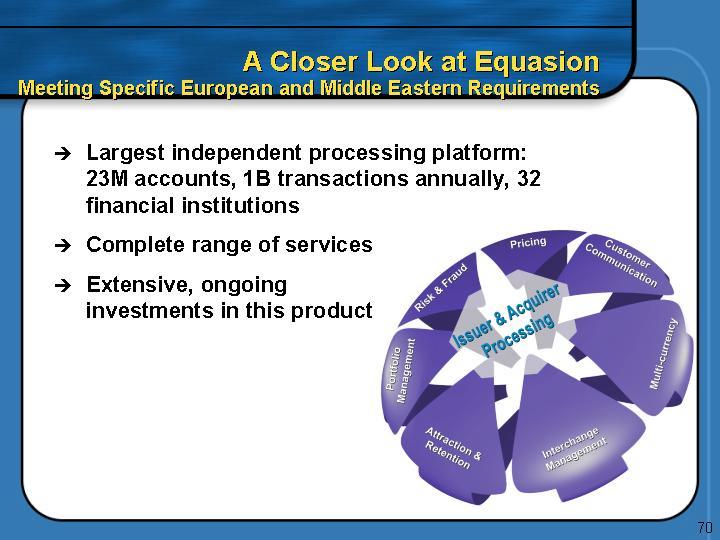

A Closer Look at Equasion

Meeting Specific European and Middle Eastern Requirements

• Largest independent processing platform:

23M accounts, 1B transactions annually, 32 financial institutions

• Complete range of services

• Extensive, ongoing

investments in this product

[GRAPHIC]

70

A Closer Look at Equasion

Blue Chip Client Base

[GRAPHIC]

71

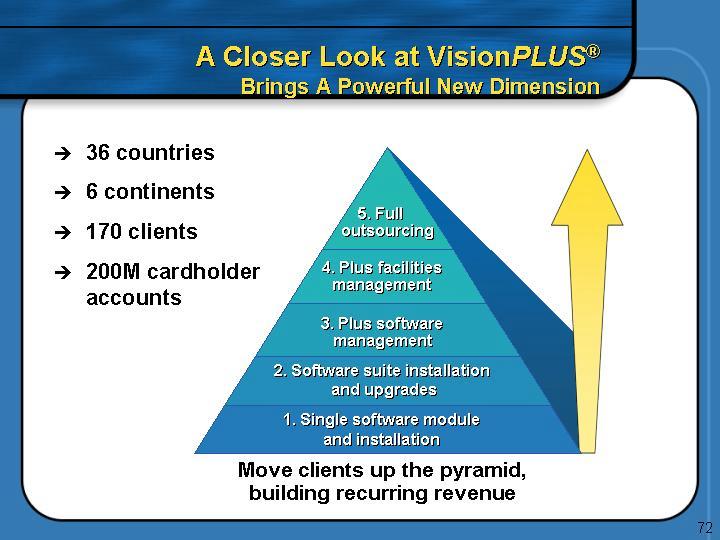

A Closer Look at VisionPLUSâ

Brings A Powerful New Dimension

• 36 countries

• 6 continents

• 170 clients

• 200M cardholder accounts

[GRAPHIC]

5. Full outsourcing

4. Plus facilities management

3. Plus software management

2. Software suite installation and upgrades

1. Single software module and installation

Move clients up the pyramid, building recurring revenue

72

A Closer Look at VisionPLUSâ

Strong Client Base

[GRAPHIC]

73

A Closer Look at OmniPay

Global Merchant Platform

• Global application, key advantages

• currency

• language

• international and domestic capabilities

• cost effective

• speed to market

[GRAPHIC]

[LOGO]

74

A Closer Look at OmniPay

Blue Chip Client Base

‘Global Choice’ clients:

[GRAPHIC]

Customers enjoying Central Acquiring benefits:

[GRAPHIC]

Customers enjoying DCC benefits:

[GRAPHIC]

75

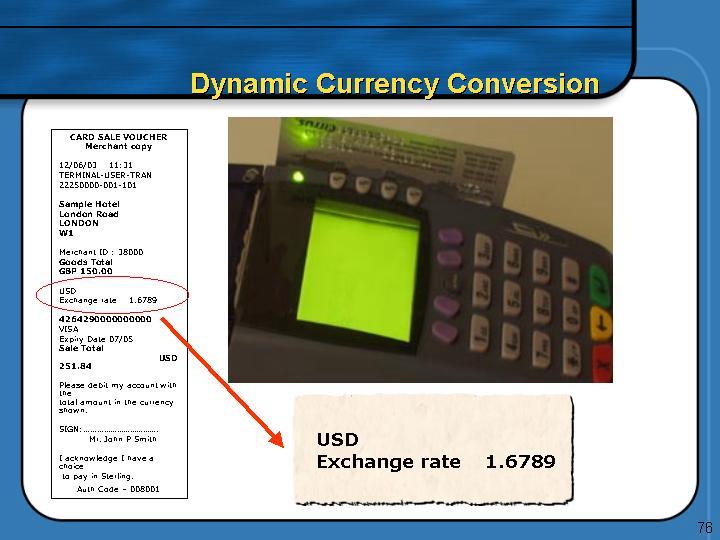

Dynamic Currency Conversion

CARD SALE VOUCHER

Merchant copy

12/06/03 11:31

TERMINAL-USER-TRAN

22250000-001-101

Sample Hotel

London Road

LONDON

W1

Merchant ID: 38000

Goods Total

GBP 150.00

USD

Exchange rate 1.6789

4264290000000000

VISA

Expiry Date 07/05

Sale Total

USD

251.84

Please debit my account with the total amount in the currency shown.

Sign:____________________

M. John P. Smith

I ackowledge I have a choice to pay in Sterling.

Auto Code - DD8DD1

[GRAPHIC]

76

Dynamic Currency Conversion

[GRAPHIC]

77

Key Takeaways

[GRAPHIC] Strong organisation

[GRAPHIC] Large worldwide opportunity

[GRAPHIC] A global Strategy

[GRAPHIC] Strategy at work – World Tour

78

[GRAPHIC]

Europe, the Middle East & Africa

79

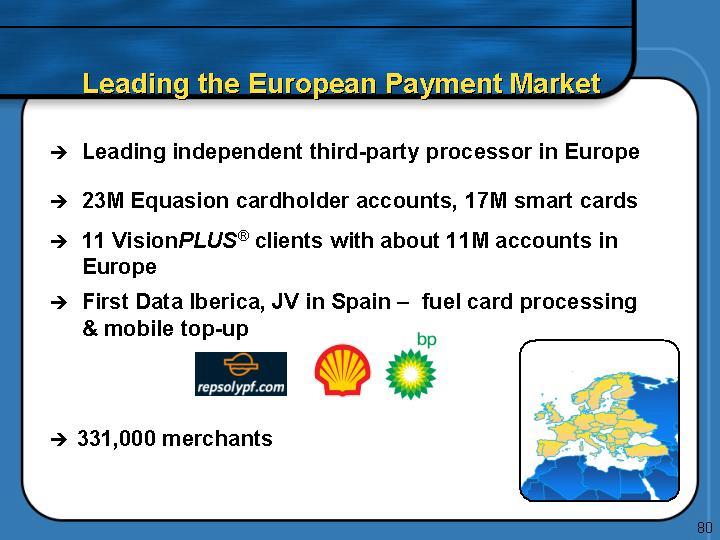

Leading the European Payment Market

• Leading independent third-party processor in Europe

• 23M Equasion cardholder accounts, 17M smart cards

• 11 VisionPLUSâ clients with about 11M accounts in europe

• First Data lberica, JV in Spain – fuel card processing & mobile top-up

[GRAPHIC]

• 331,000 merchants

[GRAPHIC]

80

Spotlight – France

In-House Processing Dominates

• Significant market – 68M cards, 25M private label

• Strong domestic deferred debit

• Growth drivers

• cheques to cards

• private label to branded

• new market entrants

[GRAPHIC]

Source: Data Monitor July 202, European Card Review, 2001-02

81

Spotlight – Germany

Largest European Market

• Largest European market

• total cards in issue 108M

• 91M debit

• 3.8M transactions

• Nearly 70% of POS purchases are cash vs. 44% in the U.S.

• Growth drivers

• credit card acceptance

• consolidation of networks

• debit card usage at POS

• migration to EMV chip cards

• Acquired TeleCash

[GRAPHIC]

Source: Lafferty Electronic Payments June 22, Data Monitor July 2002, Electronic Payments International June 22, Nilson Report April 2002.

82

Establishing a Presence in the

Middle East & Africa

• 4 Middle East card processing services clients

• 11 VisionPLUSâ accounts

• About 16M VisionPLUSâ accounts

• Optional in-house or third-party processing

• New agreements

[GRAPHIC]

83

Spotlight – South Africa

Significant Processing Potential

• VisionPLUSâ is the leading provider of Software for private label processing

• About 14M VisionPLUSâ accounts

• Migrate to outsourcing; partnerships key

[GRAPHIC]

84

[LOGO]

China & North Asia

85

China & North Asia

Investment for the Long Term

• 5 VisionPLUSâ in-region clients

• Regional HQ in Shanghai; data centre operational

• Focus; 1st outsourcing client

[GRAPHIC]

86

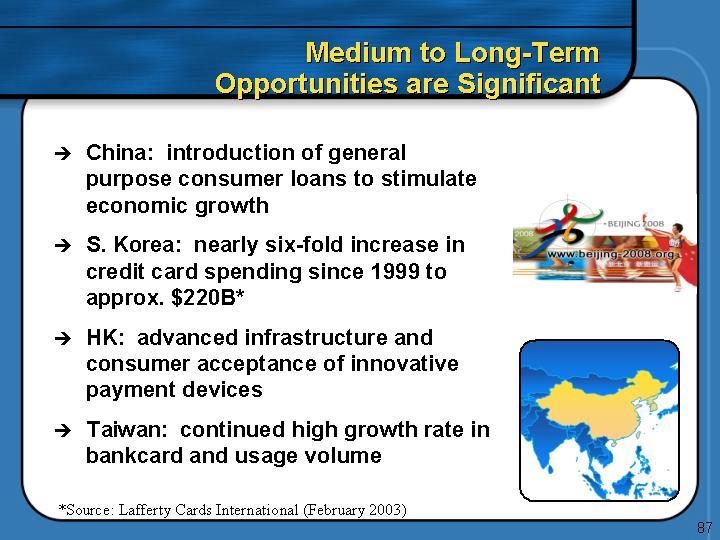

Medium to Long-Term

Opportunities are Significant

• China: introduction of general purpose consumer loans to stimulate economic growth

• S. Korea: nearly six-fold increase in credit card spending since 1999 to approx. $220B*

• HK: advanced infrastructure and consumer acceptance of innovative payment devices

• Taiwan: continued high growth rate in bankcard and usage volume

[GRAPHIC]

* Source: Lafferty Cards International (February 2003)

87

[LOGO]

88

Spotlight – Japan

Building Relationships

• Partnership Nihon Card Processing Co., Ltd. (NICAP)

[GRAPHIC]

• May 2003 established First Data Japan K.K.

• Significant long-term opportunities

• Success with ValueLINK for Starbucks

[GRAPHIC]

89

[LOGO]

Australia, New Zealand & South Asia

90

Spotlight – Australia, New Zealand & South Asia

Significant, Diverse Market Opportunity

• Full range of payment card and electronic banking services

• Largest regional independent EFT payments network, 400 clients, 500M + transactions annually

• Strong VisionPLUSâ recognition, 9 major clients including:

[GRAPHIC]

• Westpac Banking Corporation, 1st VisionPLUSâ processing client

• Pursue regional acquisitions

[GRAPHIC]

91

[LOGO]

Latin America & Canada

92

Enabling Commerce in

Latin America & Canada

• A leading merchant acquirer processor with 186,000 locations services

• VisionPLUSâ leads the card market with more than 57M accounts

• 9 processing customers

[GRAPHIC]

93

Latin America & Canada – Achievements

• Signed agreements:

[GRAPHIC]

• Successfully completed largest migration to VisionPLUSâ 8.0 for C&A, one of the largest retailers in S. America

• 6 additional VisionPLUSâ conversions to be completed 2003

[GRAPHIC]

94

Latin America & Canada

New Discussions Underway

• Detailed discussions with WU Agents to explore First Data additional products and services

[GRAPHIC]

• Leverage WU relationship to expand

[GRAPHIC]

95

In Summary

[GRAPHIC]

• Large and growing international opportunity

• Organisation, platforms and strategy now in place

• Gaining traction, building momentum

96

[GRAPHIC]

97

[GRAPHIC]

June 12, 2003

[LOGO]

98

Cautionary Information Regarding Forward-Looking Statements

Statements in this presentation regarding First Data Corporation’s business which are not historical facts, including the revenue and earnings projections, are “forward-looking statements.” All forward-looking statements are inherently uncertain as they are based on various expectations and assumptions concerning future events and they are subject to numerous known and unknown risks and uncertainties which could cause actual events or results to differ materially from those projected. Important factors upon which the Company’s forward-looking statements are premised include: (a) continued growth at rates approximating recent levels for card-based payment transactions, consumer money transfer transactions and other product markets; (b) successful conversions under service contracts with major clients; (c) renewal of material contracts in the Company’s business units consistent with past experience; (d) timely, successful and cost-effective implementation of processing systems to provide new products, improved functionally and increased efficiencies, particularly in the card issuing services segment; (e) successful and timely integration of significant businesses and technologies acquired by the Company and realisation of anticipated synergies; (f) continuing development and maintenance of appropriate business continuity plans for the Company’s processing systems based on the needs and risks relative to each such system; (g) absence of consolidation among client financial institutions or other client groups which has a significant impact on FDC client relationships and no material loss of business from significant customers of the Company; (h) achieving planned revenue growth throughout the Company, including in the merchant alliance program which involves several joint ventures not under the sole control of the Company and each of which acts independently of the others, and successful management of pricing pressures through cost efficiencies and other cost management initiatives; (i) successfully managing the credit and fraud risks in the Company’s business units and the merchant alliances, particularly in the context of the developing e-commerce markets; (j) anticipation of and response to technological changes, particularly with respect to e-commerce; (k) attracting and retaining qualified key employees; (l) no unanticipated changes in laws, regulations, credit card association rules or other industry standards affecting FDC’s businesses which require significant product redevelopment efforts, reduce the market for or value of its products or render products obsolete; (m) continuation of the existing interest rate environment so as to avoid increases in agent fees related to Payment Services’ products and increases in interest on the Company’s borrowings; (n) absence of significant changes in foreign exchange spreads on retail money transfer transactions, particularly in high-volume corridors, without a corresponding increase in volume or consumer fees; (o) continued political stability in countries in which Western Union has material operations; (p) implementation of Western Union agent agreements with governmental entities according to schedule and no interruption of relations with countries in which Western Union has or is implementing material agent agreements; (q) no unanticipated developments relating to previously disclosed lawsuits, investigations or similar matters; (r) successful management of any impact from slowing economic conditions or consumer spending; (s) no catastrophic events that could impact the Company’s or its major customer’s operating facilities, communication systems and technology or that has a material negative impact on current economic conditions or levels of consumer spending; (t) no material breach of security of any of our systems; and (u) successfully managing the potential both for patent protection and patent liability in the context of rapidly developing legal framework for expansive software patent protection.

99

[GRAPHIC]

International Investor Day

June 12, 2003

[LOGO]

100