UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-6563

CALVERT WORLD VALUES FUND, INC.

(Exact name of registrant as specified in charter)

4550 Montgomery Avenue

Suite 1000N

Bethesda, Maryland 20814

(Address of Principal Executive Offices)

Ivy Wafford Duke, Esq.

4550 Montgomery Avenue

Suite 1000N

Bethesda, Maryland 20814

(Name and Address of Agent for Service)

Registrant's telephone number, including area code: (301) 951-4800

Date of fiscal year end: September 30

Date of reporting period: Six months ended March 31, 2015

Item 1. Report to Stockholders.

[Calvert International Equity Fund Semi-Annual Report to Shareholders]

and

[Calvert Capital Accumulation Fund Semi-Annual Report to Shareholders]

and

[Calvert International Opportunities Fund Semi-Annual Report to Shareholders]

and

[Calvert Emerging Markets Equity Fund Semi-Annual Report to Shareholders]

|

| | |

| | |

| | | |

| Calvert International Equity Fund | | |

| | | |

| | |

|

| |

Semi-Annual Report March 31, 2015

E-Delivery Sign-Up — Details Inside | |

Choose Planet-friendly E-delivery!

Sign up now for on-line statements, prospectuses, and fund reports. In less than five minutes you can help reduce paper mail and lower fund costs.

Just go to www.calvert.com. If you already have an online account at Calvert, click on Login, to access your Account, and select the documents you would like to receive via e-mail.

If you’re new to online account access, click on Login, then Register to create your user name and password. Once you’re in, click on the E-delivery sign-up on the Account Portfolio page and follow the quick, easy steps.

Note: if your shares are not held directly at Calvert but through a brokerage firm, you must contact your broker for electronic delivery options available through their firm.

|

| | | |

| TABLE OF CONTENTS |

| | | | |

| | | | President's Letter |

| | | | Portfolio Management Discussion |

| | | | Shareholder Advocacy Update |

| | | | Shareholder Expense Example |

| | | | Statement of Net Assets |

| | | | Statement of Operations |

| | | | Statements of Changes in Net Assets |

| | | | Notes to Financial Statements |

| | | | Financial Highlights |

| | | | Explanation of Financial Tables |

| | | | Proxy Voting |

| | | | Availability of Quarterly Portfolio Holdings |

| | | | Basis for Board’s Approval of Investment Advisory Contracts |

|

| |

| John Streur President and Chief Executive Officer, Calvert Investments, Inc. |

Dear Calvert Shareowner,

The United States economy improved throughout 2014 and into the first quarter of 2015, while major economies in other regions of the world struggled to regain momentum or saw slowing growth. It is still too early to declare victory, but one may say that while the United States led the world into financial crisis nearly eight years ago, the innovative and aggressive responses to the crisis by our policymakers are allowing the United States to recover more quickly. Granted, the United States has the benefit of possessing the world’s reserve currency and our monetary maneuvers in our self-interest are not without cost to economies in other regions.

As 2014 drew to a close, the United States was winding down the quantitative easing portion of its post-crisis monetary policy while the European and Japanese central banks were finding it necessary to increase their own forms of quantitative easing in efforts to support asset prices and spur economic growth.

The impact of modestly improving economic activity in the U.S. and ongoing low global interest rates on financial assets in 2014 created positive returns for most stocks and bonds for the previous 12 months, a condition that gave benefit to most Calvert Funds. The exceptions are assets tied to the price of oil, which collapsed during the second half of the year. Energy industries and natural resource based companies, including renewable energy companies and water related companies, saw their stock valuations drop in reaction.

Across our fixed income and equity strategies, Calvert finds more utility in conducting fundamental research in order to find relative values in securities of individual companies than we do in attempting to anticipate or time changes in global economic indicators. Broadly, we are mindful of the fact that stocks and bonds have benefitted substantially from the easy monetary policies and ultra-low interest rates of the post-crisis era. We believe markets are more or less fairly valued and we have taken steps seeking to moderate the risk across our portfolios.

As I take the helm at Calvert and look back at the 39 years since the firm’s founding in 1976, I note the substantial growth in the world’s population, the massive increase in the industrialization of our global society, and the associated change in the role of corporations in societal and environmental outcomes for our future.

4 www.calvert.com CALVERT INTERNATIONAL EQUITY FUND SEMI-ANNUAL REPORT (UNAUDITED)

Public companies have created tremendous net benefits to society through advances in health care, food systems, energy efficiency, communications and technology, and access to finance and other products and services too vast to detail. Hundreds of millions of people throughout the world have seen their standard of living increased through benefits created by corporate activity.

Along with the obvious net benefits to society, we are aware of the substantial stresses placed upon society and the environment from corporate behaviors. At the same time, society has awarded corporations an increasingly prominent role in the day-to-day outcomes of our lives and in the societal and environmental outcomes that will determine the future direction of the world.

Calvert, as a global investment management firm and a steward of client assets, has a growing and evolving role as a leader in responsible investing. Calvert has a rich history as a socially responsible investor and has made many contributions to public policy and corporate governance. Today we are bringing Calvert’s deep expertise in socially responsible investing, public and private policy work, and investment management to a new level with a focus on developing principles and setting standards for use in our investment management processes, our active ownership and engagement discipline and within our investment risk management processes.

As a long-term investor with unique insights into environmental, social, and governance activities of companies throughout the world, Calvert is able to develop a holistic view of companies’ operations. Our ability to use our insights for the benefit of the stewardship of client assets, both to produce desirable investment outcomes for our clients and to assist companies in evolving their role in society along a responsible path has never been more important.

As fellow shareowners of Calvert Funds, you and I know that it is essential to pursue the type of enduring value that Calvert seeks to create, through excellence in financial results balanced with the evolving needs of society and the environment.

Thank you for your share ownership in Calvert Funds; all of us at Calvert Investments, Inc. appreciate the confidence and trust you have placed in us.

John Streur

April 2015

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND SEMI-ANNUAL REPORT (UNAUDITED) 5

|

| |

| PORTFOLIO MANAGEMENT DISCUSSION |

|

| |

| Natalie A. Trunow Senior Vice President and Chief Investment Officer, Equities |

Equity market returns over the six-month reporting period largely reflected macroeconomic trends, with solid gains for U.S. stocks relative to international equity markets. Improving economic conditions in the United States remained in stark contrast to the sluggish growth outlook in much of the rest of the world, particularly in Europe. However, U.S. equity markets faced several headwinds at the start of 2015 as another harsh winter weighed on economic activity and the stronger dollar contributed to negative earnings revisions for companies deriving larger portions of their earnings from overseas. International equity markets underperformed for the period, but recouped some of their losses in the first quarter of 2015 as central banks in Europe and Japan maintained quantitative-easing programs and emerging markets were buoyed by stimulus announcements from China.

For the six-month period ended March 31, 2015, the Standard and Poor’s (S&P) 500, Russell 1000, Russell 2000, MSCI EAFE, and MSCI Emerging Markets Indices returned 5.93%, 6.55%, 14.46%, 1.29%, and -2.26%, respectively.

From an investment-style perspective, growth stocks outperformed value stocks, and domestic small-cap stocks, which have less exposure to foreign markets and are less dependent on global growth, outperformed their large-cap counterparts. Looking at sector performance, Health Care, Consumer Discretionary, and Consumer Staples were the top-performing sectors within the Russell 1000 Index during the period, while the Energy, Telecommunication Services, and Materials sectors lagged.

U.S. Economic Recovery Hits Soft Patch, but Outpaces Rest of Developed World

The U.S. economy continued to outperform other developed countries, with U.S. gross domestic product (GDP) growing at a 2.2% annualized rate in the fourth quarter of 2014. More recent U.S. macroeconomic data has been weaker, however, with the slowdown largely attributed to poor weather and the strength of the dollar. A labor dispute between West Coast ports and dockworkers also resulted in a modest drag on economic activity. The U.S. ISM Manufacturing Purchasing Manufacturers Index (PMI)1 ended the period at 51.5, firmly in expansion territory, but has declined for five consecutive months. Housing activity, while remaining on an upward trend, has been disappointing of late.

Although the most recent jobs report for March was less than stellar, the job market has continued to improve, adding an average of 260,000 jobs per month over the last year. This helped push the unemployment rate down to 5.5% from 6.6% this time a year ago, though this has been aided by a drop in the labor-force participation rate. Wage growth is taking longer to materialize than in past recoveries, but recent data has been encouraging, showing modest gains in average hourly earnings and the Employment Cost Index.

6 www.calvert.com CALVERT INTERNATIONAL EQUITY FUND SEMI-ANNUAL REPORT (UNAUDITED)

|

| | | | |

| | | | |

| | CALVERT INTERNATIONAL EQUITY FUND |

| | MARCH 31, 2015 | |

| | | | |

| | ECONOMIC SECTORS | % OF TOTAL INVESTMENTS | |

| | Consumer Discretionary | 15.0 | % | |

| | Consumer Staples | 7.4 | % | |

| | Energy | 4.6 | % | |

| | Financials | 24.4 | % | |

| | Health Care | 14.4 | % | |

| | Industrials | 7.8 | % | |

| | Information Technology | 3.1 | % | |

| | Limited Partnership Interest | 0.4 | % | |

| | Materials | 4.1 | % | |

| | Short-Term Investments | 8.6 | % | |

| | Telecommunication Services | 7.0 | % | |

| | Utilities | 2.9 | % | |

| | Venture Capital | 0.3 | % | |

| | Total | 100 | % | |

| | | | |

Consumer confidence reached a nine-year high during the reporting period, due in part to lower gasoline prices, which should lead to a pick-up in consumer spending and housing activity over the remainder of the year.

Decline in Oil Prices a Positive for U.S. Economy Overall

The price of crude oil fell nearly 50% over the six-month reporting period. Weakening demand due to slowing global growth and a strategic decision by Saudi Arabia, the world’s largest oil producer, to not cut oil production in the face of increased U.S. supplies, were key drivers of the dramatic price decline.

Some economies and sectors stand to benefit from the significant price decline in oil while others will undoubtedly continue to come under pressure. Countries which import a large portion of their energy are the clear winners, with the United States, Europe, Japan, and China benefiting.

|

| | | | | | |

| | | | | |

| | CALVERT INTERNATIONAL EQUITY FUND | |

| | MARCH 31, 2015 | |

| | | | | |

| | INVESTMENT PERFORMANCE | |

| | (TOTAL RETURN AT NAV*) | |

| | | 6 MONTHS ENDED 3/31/15 | 12 MONTHS ENDED 3/31/15

| |

| | Class A | 1.56 | % | -2.06 | % | |

| | Class B | 0.90 | % | -3.38 | % | |

| | Class C | 1.12 | % | -2.96 | % | |

| | Class I | 1.91 | % | -1.43 | % | |

| | Class Y | 1.72 | % | -1.72 | % | |

| | | | | |

| | MSCI EAFE Investable Market Index (IMI) | 1.54 | % | -0.74 | % | |

| | | | | |

| | Lipper International Multi-Cap Growth Funds Average | 2.40 | % | -0.17 | % | |

| | | | | |

| | TEN LARGEST STOCK HOLDINGS | % OF NET ASSETS | |

| | Statoil ASA (ADR) | 2.8 | % | |

| | Sanofi SA (ADR) | 2.8 | % | |

| | Toyota Motor Corp. | 2.5 | % | |

| | Unilever NV (CVA) | 2.1 | % | |

| | Novartis AG (ADR) | 2.0 | % | |

| | Roche Holding AG | 2.0 | % | |

| | AIA Group Ltd. | 1.9 | % | |

| | Allianz SE (ADR) | 1.7 | % | |

| | Prudential plc | 1.6 | % | |

| | Astellas Pharma, Inc. | 1.5 | % | |

| | Total | 20.9 | % | |

| | | |

| | * Investment performance/return at NAV does not reflect the deduction of the Fund’s maximum 4.75% front-end sales charge or any deferred sales charge. | |

| | | | | |

Within the U.S., states such as North Dakota and Texas will be hurt by lower oil prices; however energy capital expenditure (CapEx) represents less than 2% of GDP and we believe the overall impact of lower

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND SEMI-ANNUAL REPORT (UNAUDITED) 7

energy prices is positive for the U.S. economy as a whole due to the significant cost savings its creates in a majority of sectors and the multiplier effect it has throughout the economy.

Global Easing Continues Amid Low Inflation and Stronger Dollar

The U.S. dollar strengthened throughout the period, hitting a 7-year high vs. the Japanese Yen and a 12-year high against the euro. Since most commodities are priced globally in U.S. dollars, a stronger dollar relative to foreign currencies typically correlates with lower commodity prices, which has kept a lid on inflation.

More than half the central banks in the G20 economies implemented some type of monetary easing policy during the period, which provided additional support for global equities. Most notably, the Bank of Japan announced a massive stimulus policy and the European Central Bank (ECB) followed with a strong quantitative easing (QE) program of its own.

Interest Rate Hikes by the Fed on the Horizon

With the U.S. economy improving, both market sentiment and Federal Reserve officials seem divided on the optimal timing of the Fed’s interest-rate increases. However, consistently low inflation and recent softness in U.S. macroeconomic data—as well as the rapid increase in the dollar’s strength, which has hurt U.S. exports and the manufacturing sector—makes it more likely that the Fed will delay raising rates until later in the year or possibly even next year.

Eurozone Economic Struggles Continue but QE Offers Some Respite

Economic conditions continued to deteriorate in the eurozone through the end of 2014 as inflation turned negative, prompting the ECB to launch its massive QE program. The program has been successful thus far in decreasing the value of the euro in an attempt to stimulate exports and eurozone economies.

|

| | | | |

| | | | |

| | CALVERT INTERNATIONAL EQUITY FUND | |

| | MARCH 31, 2015 | |

| | | | |

| | AVERAGE ANNUAL TOTAL RETURNS | |

| | | | |

| | CLASS A SHARES | (WITH MAX. LOAD) | |

| | One year | -6.69 | % | |

| | Five year | 3.69 | % | |

| | Ten year | 1.39 | % | |

| | | | |

| | CLASS B SHARES | (WITH MAX. LOAD) | |

| | One year | -8.21 | % | |

| | Five year | 3.25 | % | |

| | Ten year | 0.74 | % | |

| | | | |

| | CLASS C SHARES | (WITH MAX. LOAD) | |

| | One year | -3.93 | % | |

| | Five year | 3.78 | % | |

| | Ten year | 1.00 | % | |

| | | | |

| | CLASS I SHARES | | |

| | One year | -1.43 | % | |

| | Five year | 5.45 | % | |

| | Ten year | 2.61 | % | |

| | | | |

| | CLASS Y SHARES* | | |

| | One year | -1.72 | % | |

| | Five year | 5.12 | % | |

| | Ten year | 2.15 | % | |

| | | | |

| | * Calvert International Equity Fund first offered Class Y shares on October 31, 2008. Performance prior to that date reflects the performance of Class A shares at net asset value (NAV). Actual Class Y share performance would have been different. | |

| | | | |

Manufacturing PMIs, credit demand, and consumer confidence all have been showing signs of modest improvement, indicating a potential positive effect from QE as well as a potential bottoming out of eurozone economic malaise. Despite these marginally positive developments, we are skeptical that central bankers’ efforts will meaningfully reinvigorate those economies unless accompanied by structural economic

8 www.calvert.com CALVERT INTERNATIONAL EQUITY FUND SEMI-ANNUAL REPORT (UNAUDITED)

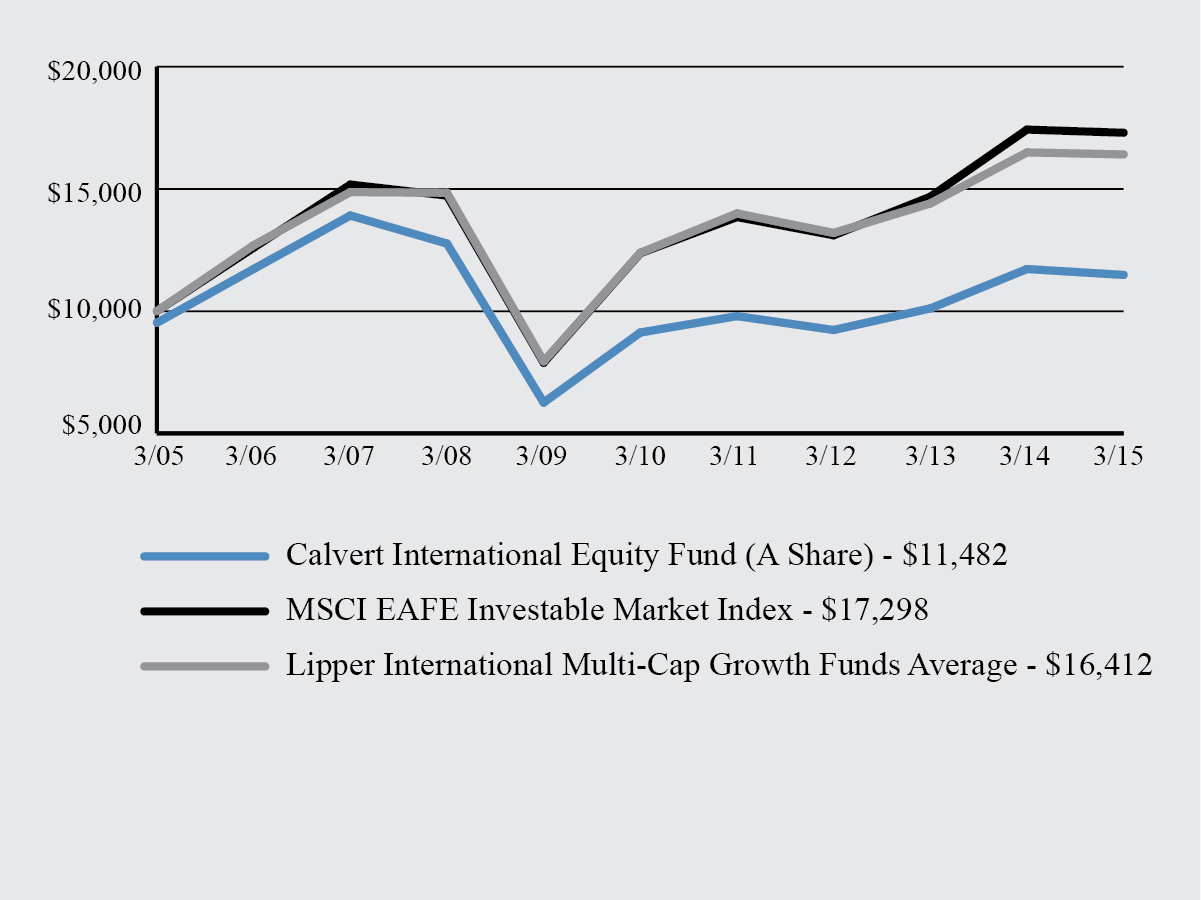

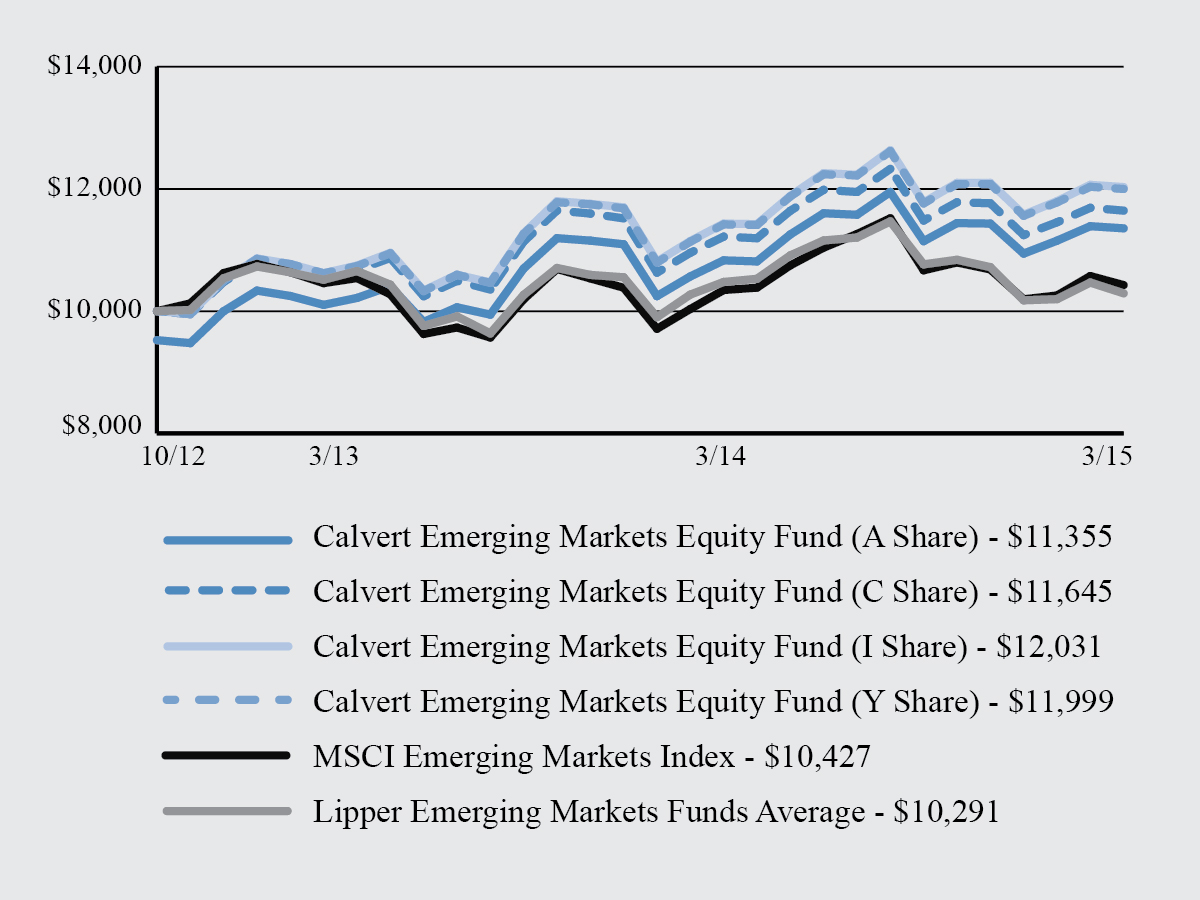

Growth of $10,000

The graph below shows the value of a hypothetical $10,000 investment in the Fund over the past 10 fiscal year periods. The results shown are for Class A shares and reflect the deduction of the maximum front-end Class A sales charge of 4.75%, and assume the reinvestment of dividends. The result is compared with benchmarks that include a broad based market index and a Lipper peer group average. Market indexes are unmanaged and their results do not reflect the effect of expenses or sales charges. The Lipper average reflects the deduction of the category’s average front-end sales charge. The value of an investment in a different share class would be different.

All performance data shown, including the graph above and the adjacent table, represents past performance, does not guarantee future results, assumes reinvestment of dividends and distributions and does not reflect the deduction of taxes that a shareholder would pay on the Fund’s distributions or the redemption of the Fund shares. All performance data reflects fee waivers and/or expense limitations, if any are in effect; in their absence performance would be lower. See Note B in Notes to Financial Statements. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted; for current performance data visit www.calvert.com. The gross expense ratio from the current prospectus for Class A shares is 1.68%. This number may differ from the expense ratio shown elsewhere in this report because it is based on a different time period and, if applicable, does not include fee or expense waivers. Performance data quoted already reflects the deduction of the Fund’s operating expenses.

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND SEMI-ANNUAL REPORT (UNAUDITED) 9

reforms. Possible risks from Greece exiting the eurozone and political turmoil emerging in other euro-area countries also remain a lingering concern and may re-surface later in the year.

Stimulus Measures Boost Chinese Stocks but Economic Challenges Remain

Despite Manufacturing PMI weakening throughout the period, Chinese equities rallied on the back of several stimulus measures and investor expectations that the government would continue stimulus measures to offset slowing, though still robust, economic growth. China is also benefiting from cheaper oil, which essentially acts as another form of stimulus. The Services PMI held up better than expected, indicating some very modest progress in transitioning away from an investment-driven economy to a more consumer-oriented one. However, structural improvements in social welfare programs, such as health care and retirement planning, will be needed in order to encourage Chinese consumers to spend more and bring down their notoriously high savings rate. Given these challenges, as well as ongoing concerns regarding a potential property-bubble burst, stimulus does not mean the Chinese economy is out of the woods. A hard economic landing remains a possibility down the road.

Outlook

While we may see some continued softness in U.S. macroeconomic data during the first half of the year, we believe U.S. economic growth will continue to exceed growth from other developed countries and we remain positive on the U.S. economy longer-term. We believe the significant positive multiplier effect from lower gas prices hasn’t yet been fully reflected in U.S. economic data, and we are likely to see the additional positive impact in the coming quarters.

In our view, U.S. stocks can still post decent performance, but probably not as good as what we saw in the past couple of years because of higher valuations, slower earnings growth, and potentially having reached peak margins. The stronger dollar, combined with lower commodity prices, tends to benefit consumers and hurt industrial companies, especially those with heavy sales outside the United States, or those directly involved in the energy sector. This is one reason why we continue to favor small-cap stocks on the domestic front.

With lower commodity prices, a stronger dollar, and little wage growth, inflation in the United States will likely remain low for some time to come, while deflationary threats are very real in other parts of the world. This may lead the Federal Reserve to raise interest rates less quickly than currently expected, since challenging global economic conditions can have a significant impact on the U.S. economy. Our position remains that when the Fed does decide to raise rates, the tightening process will be slow and gradual, with the Fed keeping a close eye on interest-rate volatility and its impact on mortgage rates. Even with a gradual tightening, monetary policy should still remain accommodative for an extended period of time. That said, we expect market volatility to increase as we grow closer to the inevitability of higher interest rates.

Calvert Investment Management, Inc.

April 2015

1. The Institute for Supply Management (ISM) Manufacturing PMI is published monthly and shows business conditions in the U.S. manufacturing sector, and is considered a significant indicator of overall economic conditions. The ISM index includes prices paid for all purchases including import purchases and purchases of food and energy, excluding crude oil. A result above 50 indicates that the manufacturing economy is generally expanding; below 50 indicates that it is generally declining.

10 www.calvert.com CALVERT INTERNATIONAL EQUITY FUND SEMI-ANNUAL REPORT (UNAUDITED)

SHAREHOLDER ADVOCACY UPDATE

2014 Corporate Diversity Report Findings Released

In March, Calvert published its 2014 survey findings on the corporate diversity practices of the largely multinational companies that make up the Standard & Poor’s 100 Index (S&P 100), in follow-up to reports published in 2012 and 2010. Calvert believes companies that fully commit to providing a fair and equitable working environment will recognize gains in both the workplace and marketplace.

Key findings from the 2014 survey include:

| |

| • | Milestone for women in the board room. In 2014, every company in the S&P 100 had at least one woman on its board of directors. In addition, there was a 17% increase in companies with three or more women and/or minorities on their boards. |

| |

| • | Diversity commitment on the rise. In the past two years, top scores related to overall corporate commitment have increased by 45%.This stems primarily from greater board oversight of diversity initiatives and increased CEO and/or chair involvement. |

| |

| • | LGBT policies have advanced overall. However, initiatives for persons with disabilities continue to fall behind other groups. |

Overall, in 2014, we saw growing commitment to women and minority employees, momentum around family-friendly work environments, and accelerated progress in support of LGBT employees. Looking ahead, we hope to see enhanced corporate diversity commitments, greater representation of women and minorities on boards, improved EEO1-disclosure, and expanded diversity initiatives for persons with disabilities.

To learn the highest- and lowest-rated companies in the report, A Survey of Corporate Diversity Practices of the S&P 100, and to find out more about the report’s methodology and findings, visit www.calvert.com.

2015 Shareholder Resolutions

Building on our initiatives from 2014, Calvert was the lead filer on 38 shareholder resolutions for the 2015 proxy season, and co-filer on another 18 proposals. Key topics include “big data” and civil rights issues, sustainability reporting, board of director oversight of environmental and social matters, water risk, climate change and greenhouse gas emissions reductions, supply chain labor issues, and board diversity.

Specifically, Calvert asked 14 companies to set a goal and a timeline for reducing their greenhouse gas emissions and filed seven proposals asking companies to issue a sustainability report describing their environmental, social and governance (ESG) performance and goals. To push for improved boardroom diversity, Calvert filed six proposals with companies requesting they report on their plans to increase minority and women Board representation and assess the effectiveness of these efforts. We also filed seven proposals requesting that companies assess and manage the civil rights’ risks related to their use of big data, which refers to data sets so large or complex that traditional data processing applications are inadequate. We also filed proposals on water risk in the agricultural supply chain and on developing a sustainable agriculture policy.

To keep abreast of the outcomes of these 2015 shareholder resolutions, as well as Calvert’s proxy voting and public policy initiatives, visit the “Resources” section on www.calvert.com.

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND SEMI-ANNUAL REPORT (UNAUDITED) 11

SHAREHOLDER EXPENSE EXAMPLE

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) and redemption fees; and (2) ongoing costs, including management fees; distribution (12b-1) fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

This Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (October 1, 2014 to March 31, 2015).

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled "Expenses Paid During Period" to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare the 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), or redemption fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

12 www.calvert.com CALVERT INTERNATIONAL EQUITY FUND SEMI-ANNUAL REPORT (UNAUDITED)

|

| | | |

| | BEGINNING ACCOUNT VALUE 10/1/14 | ENDING ACCOUNT VALUE 3/31/15 | EXPENSES PAID DURING PERIOD* 10/1/14 - 3/31/15 |

CLASS A | | | |

| Actual | $1,000.00 | $1,015.56 | $8.44 |

| Hypothetical | $1,000.00 | $1,016.56 | $8.44 |

| (5% return per year before expenses) | | | |

| | | | |

CLASS B | | | |

| Actual | $1,000.00 | $1,009.00 | $14.88 |

| Hypothetical | $1,000.00 | $1,010.12 | $14.88 |

| (5% return per year before expenses) | | | |

| | | | |

CLASS C | | | |

| Actual | $1,000.00 | $1,010.50 | $13.08 |

| Hypothetical | $1,000.00 | $1,011.92 | $13.09 |

| (5% return per year before expenses) | | | |

| | | | |

| | | | |

CLASS I | | | |

| Actual | $1,000.00 | $1,019.15 | $5.17 |

| Hypothetical | $1,000.00 | $1,019.81 | $5.18 |

| (5% return per year before expenses) | | | |

| | | | |

CLASS Y | | | |

| Actual | $1,000.00 | $1,017.16 | $6.62 |

| Hypothetical | $1,000.00 | $1,018.37 | $6.62 |

| (5% return per year before expenses) | | | |

| | | | |

| | | | |

* Expenses are equal to the Fund’s annualized expense ratio of 1.68%, 2.97%, 2.61%, 1.03%, and 1.32% for Class A, Class B, Class C, Class I, and Class Y, respectively, multiplied by the average account value over the period, multiplied by 182/365 (to reflect the one-half year period).

|

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND SEMI-ANNUAL REPORT (UNAUDITED) 13

STATEMENT OF NET ASSETS

MARCH 31, 2015

|

| | | |

EQUITY SECURITIES - 91.5% | SHARES | VALUE |

| Australia - 2.2% | | |

| Macquarie Group Ltd. | 36,560 |

| $2,126,225 |

| Westpac Banking Corp. | 14,549 |

| 435,674 |

| Westpac Banking Corp. (ADR) | 87,222 |

| 2,608,810 |

| Woolworths Ltd. | 128,731 |

| 2,885,816 |

| | | 8,056,525 |

| | | |

| Austria - 1.0% | | |

| OMV AG (ADR) | 723 |

| 19,911 |

| Voestalpine AG | 97,015 |

| 3,543,301 |

| | | 3,563,212 |

| | | |

| Belgium - 0.2% | | |

| Ageas (ADR) | 16,568 |

| 594,377 |

| | | |

| Canada - 0.4% | | |

| Lululemon Athletica, Inc.* | 20,813 |

| 1,332,448 |

| | | |

| China - 1.1% | | |

| BOC Hong Kong Holdings Ltd. (ADR) | 15,012 |

| 1,069,155 |

| China Construction Bank Corp. | 3,834,000 |

| 3,180,635 |

| | | 4,249,790 |

| | | |

| Denmark - 0.0% | | |

| H Lundbeck A/S (ADR) | 5,080 |

| 108,026 |

| | | |

| Finland - 0.1% | | |

| Sampo Oyj (ADR) | 10,009 |

| 252,627 |

| | | |

| France - 7.2% | | |

| AXA SA (ADR) | 103,724 |

| 2,617,994 |

| BNP Paribas SA (ADR) | 52,375 |

| 1,588,272 |

| Casino Guichard Perrachon SA (ADR) | 370 |

| 6,597 |

| Credit Agricole SA (ADR) | 72,354 |

| 528,184 |

| Kering SA | 23,121 |

| 4,515,098 |

| Orange SA | 6,279 |

| 100,928 |

| Orange SA (ADR) | 201,354 |

| 3,223,678 |

| Sanofi SA | 24,075 |

| 2,366,802 |

| Sanofi SA (ADR) | 205,399 |

| 10,154,927 |

| Suez Environnement Co. (ADR) | 12,411 |

| 105,494 |

| Valeo SA (ADR) | 8,067 |

| 601,516 |

| Veolia Environnement SA (ADR) | 32,156 |

| 606,784 |

| | | 26,416,274 |

| | | |

| Germany - 6.2% | | |

| Allianz SE | 7,885 |

| 1,368,837 |

| Allianz SE (ADR) | 361,651 |

| 6,294,536 |

| Brenntag AG | 26,536 |

| 1,589,370 |

| Celesio AG (ADR) | 2,134 |

| 12,377 |

14 www.calvert.com CALVERT INTERNATIONAL EQUITY FUND SEMI-ANNUAL REPORT (UNAUDITED)

|

| | | | | |

EQUITY SECURITIES - CONT'D | SHARES | VALUE |

| | | |

| Germany - Cont'd | | |

| Commerzbank AG (ADR)* | 2 |

| $28 |

| Continental AG (ADR) | 76 |

| 3,589 |

| Deutsche Post AG | 141,953 |

| 4,436,514 |

| Deutsche Post AG (ADR) | 68,078 |

| 2,132,203 |

| Dialog Semiconductor plc* | 66,219 |

| 2,991,943 |

| Hugo Boss AG | 28,000 |

| 3,406,324 |

| K+S AG (ADR) | 2,275 |

| 37,196 |

| Merck KGaA (ADR) | 4,215 |

| 156,398 |

| Muenchener Rueckversicherungs-Gesellschaft AG (ADR) | 18,721 |

| 403,531 |

| | | 22,832,846 |

| | | |

| Hong Kong - 3.2% | | |

| AIA Group Ltd. | 1,094,600 |

| 6,852,232 |

| Hang Seng Bank Ltd. (ADR) | 53,867 |

| 965,297 |

| PCCW Ltd. | 7,000 |

| 4,265 |

| PCCW Ltd. (ADR) | 4,416 |

| 26,496 |

| Samsonite International SA* | 1,157,100 |

| 4,017,651 |

| The Bank of East Asia Ltd. (ADR) | 7,835 |

| 31,027 |

| | | 11,896,968 |

| | | |

| Ireland - 1.1% | | |

| Kerry Group plc | 61,021 |

| 4,094,673 |

| | | |

| Israel - 1.5% | | |

| Check Point Software Technologies Ltd.* | 65,600 |

| 5,377,232 |

| | | |

| Italy - 3.8% | | |

| GTECH SpA (ADR) | 1,136 |

| 22,640 |

| Intesa Sanpaolo SpA, Milano Stock Exchange | 1,589,554 |

| 5,389,059 |

| Intesa Sanpaolo SpA (ADR) | 15,917 |

| 324,388 |

| Mediobanca SpA | 501,526 |

| 4,804,019 |

| Prysmian SpA | 161,645 |

| 3,326,944 |

| Snam SpA (ADR) | 4,650 |

| 45,058 |

| Terna Rete Elettrica Nazionale SpA (ADR) | 3,886 |

| 51,315 |

| | | 13,963,423 |

| | | |

| Japan - 17.8% | | |

| Astellas Pharma, Inc. | 346,000 |

| 5,668,354 |

| Eisai Co. Ltd. (ADR) | 436 |

| 31,196 |

| Isuzu Motors Ltd. | 418,900 |

| 5,570,965 |

| JSR Corp. | 192,800 |

| 3,343,877 |

| Mitsui Fudosan Co. Ltd. | 154,256 |

| 4,532,369 |

| Mizuho Financial Group, Inc. | 2,696,200 |

| 4,741,289 |

| Mizuho Financial Group, Inc. (ADR) | 477,960 |

| 1,696,758 |

| MS&AD Insurance Group Holdings (ADR) | 51,806 |

| 725,543 |

| Nippon Telegraph & Telephone Corp. | 10,100 |

| 622,219 |

| Nippon Telegraph & Telephone Corp. (ADR) | 119,596 |

| 3,685,949 |

| Nissan Motor Co. Ltd. | 408,000 |

| 4,159,372 |

| Nissan Motor Co. Ltd. (ADR) | 86,568 |

| 1,759,927 |

| Nomura Holdings, Inc. | 40,600 |

| 238,662 |

| Nomura Holdings, Inc. (ADR) | 246,548 |

| 1,447,237 |

| ORIX Corp. | 360,400 |

| 5,067,829 |

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND SEMI-ANNUAL REPORT (UNAUDITED) 15

|

| | | | | |

EQUITY SECURITIES - CONT'D | SHARES | VALUE |

| | | |

| Japan - Cont'd | | |

| Softbank Corp. | 83,500 |

| $4,852,601 |

| Sony Corp.* | 9,700 |

| 259,261 |

| Sony Corp. (ADR)* | 57,644 |

| 1,543,706 |

| Takeda Pharmaceutical Co. Ltd. (ADR) | 14,813 |

| 370,918 |

| Tokyo Gas Co. Ltd. | 621,118 |

| 3,910,785 |

| Toyota Motor Corp. (t) | 129,900 |

| 9,063,656 |

| Toyota Motor Corp. (ADR) | 14,920 |

| 2,087,159 |

| | | 65,379,632 |

| | | |

| Luxembourg - 1.3% | | |

| Ipsen SA (ADR) | 47,534 |

| 556,623 |

| ProSiebenSat.1 Media AG | 84,472 |

| 4,147,270 |

| | | 4,703,893 |

| | | |

| Malaysia - 0.2% | | |

| AirAsia Bhd. | 1,433,600 |

| 921,109 |

| | | |

| Mexico - 0.1% | | |

| FINAE, Series D, Preferred (b)(i)* | 1,962,553 |

| 226,071 |

| | | |

| Netherlands - 4.5% | | |

| Koninklijke Ahold NV, Amsterdam Stock Exchange | 13,249 |

| 261,128 |

| Koninklijke Ahold NV (ADR) | 80,500 |

| 1,582,630 |

| Koninklijke Philips NV: | | |

| Common | 13,830 |

| 392,494 |

| NY Shares | 82,615 |

| 2,341,309 |

| Unilever NV, NY Shares | 100,971 |

| 4,216,549 |

| Unilever NV (CVA) | 183,493 |

| 7,669,073 |

| | | 16,463,183 |

| | | |

| New Zealand - 0.1% | | |

| Spark New Zealand Ltd. | 26,473 |

| 58,840 |

| Spark New Zealand Ltd. (ADR) | 32,193 |

| 356,537 |

| | | 415,377 |

| | | |

| Norway - 4.5% | | |

| DNB ASA | 187,819 |

| 3,022,131 |

| DNB ASA (ADR) | 377 |

| 60,350 |

| Statoil ASA (ADR) | 589,938 |

| 10,377,009 |

| StatoilHydro ASA | 133,032 |

| 2,349,759 |

| Yara International ASA (ADR) | 12,176 |

| 617,932 |

| | | 16,427,181 |

| | | |

| Peru - 1.1% | | |

| Credicorp Ltd. | 28,503 |

| 4,008,377 |

| | | |

| Philippines - 0.9% | | |

| Philippine Long Distance Telephone Co. | 7,910 |

| 502,839 |

| Philippine Long Distance Telephone Co. (ADR) | 48,217 |

| 3,013,080 |

| | | 3,515,919 |

| | | |

16 www.calvert.com CALVERT INTERNATIONAL EQUITY FUND SEMI-ANNUAL REPORT (UNAUDITED)

|

| | | | | |

EQUITY SECURITIES - CONT'D | SHARES | VALUE |

| | | |

| Singapore - 0.3% | | |

| Singapore Telecommunications Ltd. (ADR) | 29,605 |

| $943,363 |

| | | |

| South Africa - 2.2% | | |

| Aspen Pharmacare Holdings Ltd.* | 105,170 |

| 3,327,072 |

| MTN Group Ltd. (ADR) | 31,566 |

| 538,358 |

| Naspers Ltd. | 26,867 |

| 4,121,565 |

| Nedbank Group Ltd. (ADR) | 5,888 |

| 115,140 |

| Tiger Brands Ltd. (ADR) | 2,952 |

| 73,844 |

| | | 8,175,979 |

| | | |

| South Korea - 0.5% | | |

| LG Household & Health Care Ltd. | 2,347 |

| 1,777,389 |

| | | |

| Spain - 2.3% | | |

| Banco Bilbao Vizcaya Argentaria SA: | | |

| Common | 28,740 |

| 289,771 |

| Rights* | 28,740 |

| 4,137 |

| Banco Bilbao Vizcaya Argentaria SA (ADR) | 173,673 |

| 1,741,940 |

| Banco Santander SA | 37,296 |

| 280,243 |

| Banco Santander SA (ADR) | 225,996 |

| 1,683,670 |

| Enagas SA (ADR) | 2,626 |

| 37,460 |

| Ferrovial SA (ADR) | 442 |

| 9,286 |

| Inditex SA | 136,945 |

| 4,386,664 |

| | | 8,433,171 |

| | | |

| Sweden - 2.0% | | |

| Atlas Copco AB | 2,755 |

| 89,066 |

| Atlas Copco AB (ADR): | | |

| A Shares | 42,356 |

| 1,371,699 |

| B Shares | 17,932 |

| 529,622 |

| Sandvik AB | 358,977 |

| 4,009,030 |

| Sandvik AB (ADR) | 5,564 |

| 61,872 |

| Svenska Handelsbanken AB (ADR) | 12,848 |

| 289,787 |

| Swedbank AB (ADR) | 14,941 |

| 357,463 |

| Tele2 AB (ADR) | 121,443 |

| 722,586 |

| | | 7,431,125 |

| | | |

| Switzerland - 7.5% | | |

| Clariant AG* | 264,132 |

| 5,279,208 |

| Novartis AG | 15,624 |

| 1,545,362 |

| Novartis AG (ADR) | 76,156 |

| 7,509,743 |

| Roche Holding AG | 27,020 |

| 7,452,101 |

| Roche Holding AG (ADR) | 131,390 |

| 4,517,188 |

| Swiss Re AG (ADR) | 4,079 |

| 394,011 |

| Zurich Insurance Group AG (ADR)* | 30,490 |

| 1,028,885 |

| | | 27,726,498 |

| | | |

| United Kingdom - 17.2% | | |

| Admiral Group plc (ADR) | 3,494 |

| 80,904 |

| ARM Holdings plc | 192,278 |

| 3,151,058 |

| AstraZeneca plc | 4,551 |

| 312,312 |

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND SEMI-ANNUAL REPORT (UNAUDITED) 17

|

| | | | | |

EQUITY SECURITIES - CONT'D | SHARES | VALUE |

| | | |

| United Kingdom - Cont'd | | |

| AstraZeneca plc (ADR) | 75,725 |

| $5,181,862 |

| Barclays plc | 1,320,992 |

| 4,744,443 |

| Barclays plc (ADR) | 218,811 |

| 3,188,076 |

| BG Group plc | 324,390 |

| 3,988,775 |

| BT Group plc | 76,870 |

| 498,499 |

| BT Group plc (ADR) | 45,852 |

| 2,988,175 |

| Bunzl plc (ADR) | 21,554 |

| 584,113 |

| Capita plc | 159,059 |

| 2,631,920 |

| Catlin Group Ltd. (ADR) | 2,231 |

| 46,739 |

| GlaxoSmithKline plc | 14,334 |

| 328,558 |

| GlaxoSmithKline plc (ADR) | 43,218 |

| 1,994,511 |

| Howden Joinery Group plc | 274,685 |

| 1,807,212 |

| Indivior plc (ADR)* | 1,064 |

| 14,970 |

| Inmarsat plc | 298,192 |

| 4,094,844 |

| J Sainsbury plc (ADR) | 11,183 |

| 173,001 |

| Johnson Matthey plc | 54,055 |

| 2,714,569 |

| Legal & General Group plc (ADR) | 907 |

| 18,816 |

| Man Group plc (ADR) | 55,991 |

| 164,614 |

| Meggitt plc | 504,745 |

| 4,104,671 |

| Old Mutual plc (ADR) | 1,346 |

| 35,503 |

| Persimmon plc* | 147,203 |

| 3,632,987 |

| Prudential plc | 233,225 |

| 5,780,153 |

| Reckitt Benckiser Group plc (ADR) | 26,602 |

| 455,160 |

| Sage Group plc (ADR) | 91 |

| 2,518 |

| SSE plc | 155,983 |

| 3,467,827 |

| SSE plc (ADR) | 89,854 |

| 1,998,353 |

| The British Land Co. plc (ADR) | 5,664 |

| 69,739 |

| Unilever plc | 9,203 |

| 384,204 |

| Unilever plc (ADR) | 97,067 |

| 4,048,665 |

| United Utilities Group plc (ADR) | 26,500 |

| 731,798 |

| | | 63,419,549 |

| | | |

| United States - 1.0% | | |

| Applied Industrial Technologies, Inc. | 13,914 |

| 630,861 |

| Bioceptive, Inc., Series A, Preferred (a)(b)(i)* | 582,574 |

| 299,967 |

| Bristol-Myers Squibb Co. | 35,316 |

| 2,277,882 |

|

| Powerspan Corp., Contingent Deferred Distribution (b)(i)* | 1 |

| — |

|

| Unit Corp.* | 17,325 |

| 484,754 |

| | | 3,693,464 |

| | | |

| Total Equity Securities (Cost $315,884,230) | | 336,399,701 |

| | | |

VENTURE CAPITAL LIMITED PARTNERSHIP INTEREST - 0.4% | ADJUSTED BASIS | |

| Mainstream Brazil Impact Investing Fund (b)(i)* |

| $18,422 |

| 941 |

| BFSE Holding, BV (b)(i)* | 612,966 |

| 292,833 |

| Africa Renewable Energy Fund (b)(i)* | 102,623 |

| 70,845 |

| Blackstone Clean Technology Partners (b)(i)* | 76,276 |

| 26,513 |

| China Environment Fund 2004 (b)(i)* | — |

| 123,854 |

| Emerald Sustainability Fund I (b)(i)* | 433,916 |

| 140,859 |

| gNet Defta Development Holdings LLC (a)(b)(i)* | 400,000 |

| 313,827 |

18 www.calvert.com CALVERT INTERNATIONAL EQUITY FUND SEMI-ANNUAL REPORT (UNAUDITED)

|

| | | | | |

VENTURE CAPITAL LIMITED PARTNERSHIP INTEREST - CONT'D | ADJUSTED BASIS | VALUE |

| | | |

| SEAF Central and Eastern European Growth Fund LLC (a)(b)(i)* |

| $327,254 |

| $429,009 |

| SEAF India International Growth Fund (b)(i)* | 274,667 |

| 120,146 |

| ShoreCap International LLC (b)(i)* | — |

| — |

|

| Terra Capital (b)(i)* | 469,590 |

| 1 |

| | | |

Total Venture Capital Limited Partnership Interest (Cost $2,715,714) | | 1,518,828 |

| | | |

VENTURE CAPITAL DEBT OBLIGATIONS - 0.3% | PRINCIPAL AMOUNT | |

| AFIG LLC, 6.00%, 10/17/17 (b)(i) | 450,953 |

| 338,214 |

| FINAE: | | |

| Note I, 6.50%, 12/1/15 (b)(i) | 187,500 |

| 187,500 |

| Note II, 6.50%, 12/1/15 (b)(i) | 375,000 |

| 375,000 |

| Windhorse International-Spring Health Water Ltd., 1.00%, 3/14/18 (b)(i)(u) | 70,000 |

| 52,500 |

| | | |

| Total Venture Capital Debt Obligations (Cost $1,083,453) | | 953,214 |

| | | |

HIGH SOCIAL IMPACT INVESTMENTS - 1.2% | | |

| Calvert Social Investment Foundation Notes, 0.25%, 7/1/17 (b)(i)(r) | 4,431,583 |

| 4,393,480 |

| | | |

| Total High Social Impact Investments (Cost $4,431,583) | | 4,393,480 |

| | | |

TIME DEPOSIT - 8.8% | | |

| State Street Bank Time Deposit, 0.088%, 4/1/15 | 32,317,328 |

| 32,317,328 |

| | | |

| Total Time Deposit (Cost $32,317,328) | | 32,317,328 |

| | | |

| | | |

| TOTAL INVESTMENTS (Cost $356,432,308) - 102.2% | | 375,582,551 |

| Other assets and liabilities, net - (2.2%) | | (8,025,970) |

NET ASSETS - 100% | | $367,556,581 |

| | | |

| See notes to financial statements. |

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND SEMI-ANNUAL REPORT (UNAUDITED) 19

|

| | | |

NET ASSETS CONSIST OF: | |

| Paid-in capital applicable to the following shares of common stock with 250,000,000 shares of $0.01 par value shares authorized: | |

| Class A: 13,811,555 shares outstanding |

| $311,828,948 |

|

| Class B: 96,469 shares outstanding | 7,754,331 |

|

| Class C: 1,177,554 shares outstanding | 31,331,711 |

|

| Class I: 5,575,232 shares outstanding | 134,018,975 |

|

| Class Y: 1,119,226 shares outstanding | 18,106,336 |

|

| Undistributed net investment income | 53,640 |

|

| Accumulated net realized gain (loss) on investments and foreign currency transactions | (154,639,088 | ) |

| Net unrealized appreciation (depreciation) on investments, foreign currencies, and assets and liabilities denominated in foreign currencies | 19,101,728 |

|

| | |

NET ASSETS |

| $367,556,581 |

|

| | |

NET ASSET VALUE PER SHARE | |

| Class A (based on net assets of $230,144,776) |

| $16.66 |

|

| Class B (based on net assets of $1,406,427) |

| $14.58 |

|

| Class C (based on net assets of $16,993,809) |

| $14.43 |

|

| Class I (based on net assets of $99,286,078) |

| $17.81 |

|

| Class Y (based on net assets of $19,725,491) |

| $17.62 |

|

| | |

| |

|

| | | | |

RESTRICTED SECURITIES | ACQUISITION DATES | COST |

| AFIG LLC, 6.00%, 10/17/17 | 10/11/12 |

| $450,953 |

|

| Africa Renewable Energy Fund LP | 4/17/14 - 11/10/14 | 102,623 |

|

| BFSE Holding, BV LP | 1/12/06 - 6/11/14 | 612,966 |

|

| Bioceptive, Inc., Series A, Preferred | 10/26/12 - 12/18/13 | 252,445 |

|

| Blackstone Clean Technology Partners LP | 7/29/10 - 2/10/15 | 76,276 |

|

| Calvert Social Investment Foundation Notes, 0.25%, 7/1/17 | 7/1/14 | 4,431,583 |

|

| China Environment Fund 2004 LP | 9/15/05 - 4/1/09 | — |

|

| Emerald Sustainability Fund I LP | 7/19/01 - 5/17/11 | 433,916 |

|

| FINAE: | | |

| Series D, Preferred | 2/28/11 | 252,686 |

|

| Note I, 6.50%, 12/1/15 | 12/10/10 | 187,500 |

|

| Note II, 6.50%, 12/1/15 | 2/24/11 | 375,000 |

|

| gNet Defta Development Holdings LLC, LP | 8/30/05 | 400,000 |

|

| Mainstream Brazil Impact Investing Fund LP | 12/12/14 - 3/25/15 | 18,422 |

|

| Powerspan Corp., Contingent Deferred Distribution | 7/11/14 | — |

|

| SEAF Central and Eastern European Growth Fund LLC, LP | 8/10/00 - 8/26/11 | 327,254 |

|

| SEAF India International Growth Fund LP | 3/22/05 - 5/24/10 | 274,667 |

|

| ShoreCap International LLC, LP | 8/12/04 - 12/15/08 | — |

|

| Terra Capital LP | 11/23/98 - 3/14/06 | 469,590 |

|

| Windhorse International-Spring Health Water Ltd., 1.00%, 3/14/18 | 2/12/14 | 70,000 |

|

| See notes to financial statements. |

20 www.calvert.com CALVERT INTERNATIONAL EQUITY FUND SEMI-ANNUAL REPORT (UNAUDITED)

|

| | |

(a) Affiliated company. (b) This security was valued under the direction of the Board of Directors. See Note A. (i) Restricted securities represent 2.0% of net assets of the Fund. (r) The coupon rate shown on floating or adjustable rate securities represents the rate at period end. (t) 90,000 shares of Toyota Motor Corp. have been soft segregated in order to cover outstanding commitments to certain limited partnerships investments within the Fund. There are no restrictions on the trading of this security. (u) Security defaulted as to principal and interest in March 2013. It has been restructured at a 9% rate maturing on March 14, 2018 with 1% to be paid annually and the remaining interest due at maturity. This security is currently accruing at 1%. * Non-income producing security Abbreviations: ADR: American Depositary Receipts CVA: Certificaten Van Aandelen LLC: Limited Liability Corporation plc: Public Limited Company See notes to financial statements. |

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND SEMI-ANNUAL REPORT (UNAUDITED) 21

STATEMENT OF OPERATIONS

SIX MONTHS ENDED MARCH 31, 2015

|

| | | |

NET INVESTMENT INCOME | |

| Investment Income: | |

| Dividend income (net of foreign taxes withheld of $285,992) |

| $3,515,406 |

|

| Interest income |

| $50,791 |

|

| Total investment income | 3,566,197 |

|

| | |

| Expenses: | |

| Investment advisory fee | 1,411,723 |

|

| Transfer agency fees and expenses | 341,244 |

|

| Administrative fees | 573,204 |

|

| Distribution Plan expenses: | |

| Class A | 314,002 |

|

| Class B | 8,718 |

|

| Class C | 83,521 |

|

| Directors' fees and expenses | 21,216 |

|

| Custodian fees | 87,403 |

|

| Registration fees | 31,078 |

|

| Reports to shareholders | 27,716 |

|

| Professional fees | 29,707 |

|

| Miscellaneous | 28,877 |

|

| Total expenses | 2,958,409 |

|

| Reimbursement from Advisor: | |

| Class B | (7,474 | ) |

| Net expenses | 2,950,935 |

|

| | |

NET INVESTMENT INCOME | 615,262 |

|

| | |

REALIZED AND UNREALIZED GAIN (LOSS) | |

| Net realized gain (loss) on: | |

| Investments | 8,272,351 |

|

| Foreign currency transactions | (424,076 | ) |

| | 7,848,275 |

|

| Change in unrealized appreciation (depreciation) on: | |

| Investments and foreign currencies | (1,222,998 | ) |

| Assets and liabilities denominated in foreign currencies | (19,522 | ) |

| | (1,242,520 | ) |

| | |

NET REALIZED AND UNREALIZED GAIN (LOSS) | 6,605,755 |

|

| | |

INCREASE (DECREASE) IN NET ASSETS RESULTING FROM OPERATIONS |

| $7,221,017 |

|

| | |

| See notes to financial statements. |

22 www.calvert.com CALVERT INTERNATIONAL EQUITY FUND SEMI-ANNUAL REPORT (UNAUDITED)

STATEMENTS OF CHANGES IN NET ASSETS

|

| | | | | | | |

INCREASE (DECREASE) IN NET ASSETS | SIX MONTHS ENDED MARCH 31, 2015 | | YEAR ENDED SEPTEMBER 30, 2014 |

| Operations: | | | |

| Net investment income |

| $615,262 |

| |

| $3,856,887 |

|

| Net realized gain (loss) | 7,848,275 |

| | 38,182,047 |

|

| Change in unrealized appreciation (depreciation) | (1,242,520 | ) | | (39,050,285 | ) |

| | | | |

INCREASE (DECREASE) IN NET ASSETS RESULTING FROM OPERATIONS | 7,221,017 |

| | 2,988,649 |

|

| | | | |

| Distributions to shareholders from: | | | |

| Net investment income: | | | |

| Class A shares | (1,631,424 | ) | | (1,441,168 | ) |

| Class I shares | (1,067,547 | ) | | (1,465,772 | ) |

| Class Y shares | (128,897 | ) | | (125,098 | ) |

| Total distributions | (2,827,868 | ) | | (3,032,038 | ) |

| | | | |

| Capital share transactions: | | | |

| Shares sold: | | | |

| Class A shares | 33,874,439 |

| | 58,755,990 |

|

| Class B shares | 16,461 |

| | 22,810 |

|

| Class C shares | 1,311,205 |

| | 2,254,459 |

|

| Class I shares | 8,481,853 |

| | 15,405,740 |

|

| Class Y shares | 4,390,097 |

| | 9,173,420 |

|

| Reinvestment of distributions: | | | |

| Class A shares | 1,180,437 |

| | 1,068,320 |

|

| Class I shares | 878,598 |

| | 1,195,493 |

|

| Class Y shares | 88,086 |

| | 72,616 |

|

| Redemption fees: | | | |

| Class A shares | 388 |

| | 3,602 |

|

| Class C shares | 20 |

| | 227 |

|

| Shares redeemed: | | | |

| Class A shares | (71,858,315 | ) | | (38,938,256 | ) |

| Class B shares | (631,923 | ) | | (1,205,154 | ) |

| Class C shares | (1,662,924 | ) | | (2,857,013 | ) |

| Class I shares | (3,163,763 | ) | | (6,486,688 | ) |

| Class Y shares | (2,439,207 | ) | | (1,959,045 | ) |

| Total capital share transactions | (29,534,548 | ) | | 36,506,521 |

|

| | | | |

TOTAL INCREASE (DECREASE) IN NET ASSETS | (25,141,399 | ) | | 36,463,132 |

|

| | | | |

NET ASSETS | | | |

| Beginning of period | 392,697,980 |

| | 356,234,848 |

|

| End of period (including undistributed net investment income of $53,640 and $2,266,246, respectively) |

| $367,556,581 |

| |

| $392,697,980 |

|

| | | | |

| See notes to financial statements. |

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND SEMI-ANNUAL REPORT (UNAUDITED) 23

STATEMENTS OF CHANGES IN NET ASSETS

|

| | | | | |

CAPITAL SHARE ACTIVITY | SIX MONTHS ENDED MARCH 31, 2015 | | YEAR ENDED SEPTEMBER 30, 2014 |

| Shares sold: | | | |

| Class A shares | 2,082,393 |

| | 3,451,461 |

|

| Class B shares | 1,117 |

| | 1,517 |

|

| Class C shares | 92,523 |

| | 152,718 |

|

| Class I shares | 484,303 |

| | 846,818 |

|

| Class Y shares | 253,817 |

| | 510,073 |

|

| Reinvestment of distributions: | | | |

| Class A shares | 73,138 |

| | 62,658 |

|

| Class I shares | 51,022 |

| | 65,795 |

|

| Class Y shares | 5,163 |

| | 4,041 |

|

| Shares redeemed: | | | |

| Class A shares | (4,316,558 | ) | | (2,290,221 | ) |

| Class B shares | (43,778 | ) | | (80,280 | ) |

| Class C shares | (118,058 | ) | | (193,947 | ) |

| Class I shares | (181,682 | ) | | (355,259 | ) |

| Class Y shares | (141,613 | ) | | (108,621 | ) |

| Total capital share activity | (1,758,213 | ) | | 2,066,753 |

|

| | | | |

| See notes to financial statements. |

24 www.calvert.com CALVERT INTERNATIONAL EQUITY FUND SEMI-ANNUAL REPORT (UNAUDITED)

NOTES TO FINANCIAL STATEMENTS

NOTE A — SIGNIFICANT ACCOUNTING POLICIES

General: Calvert International Equity Fund (the “Fund”), a series of Calvert World Values Fund, Inc., is registered under the Investment Company Act of 1940 as a diversified, open-end management investment company. Calvert World Values Fund, Inc. is comprised of four separate series. The operations of each series are accounted for separately. The Fund offers five classes of shares of capital stock - Classes A, B, C, I, and Y. Class A shares are sold with a maximum front-end sales charge of 4.75%. Class B shares are sold without a front-end sales charge and, with certain exceptions, will be charged a deferred sales charge at the time of redemption, depending on how long investors have owned the shares. Class B shares are no longer offered for purchase, except through reinvestment of dividends and/or distributions and through certain exchanges. Class B shares were closed effective April 20, 2015. Class C shares are sold without a front-end sales charge and, with certain exceptions, will be charged a deferred sales charge on shares sold within one year of purchase. Class B and Class C shares have higher levels of expenses than Class A shares. Class I shares require a minimum account balance of $1,000,000. The $1 million minimum initial investment is waived for retirement plans that trade through omnibus accounts and may be waived for certain other institutional accounts where it is believed to be in the best interest of the Fund and its shareholders. Class I shares have no front-end or deferred sales charge and have lower levels of expenses than Class A shares. Class Y shares are generally only available to wrap or similar fee-based programs offered by financial intermediaries, foundations, and endowments that have entered into an agreement with the Fund’s Distributor to offer Class Y shares. Class Y shares have no front-end or deferred sales charge and have lower levels of expenses than Class A shares. Each class has different: (a) dividend rates, due to differences in Distribution Plan expenses and other class-specific expenses, (b) exchange privileges and (c) class-specific voting rights.

Security Valuation: Net asset value per share is determined every business day as of the close of the regular session of the New York Stock Exchange (generally 4:00 p.m. Eastern time). The Fund uses independent pricing services approved by the Board of Directors (“the Board”) to value its investments wherever possible. Investments for which market quotations are not available or deemed not reliable are fair valued in good faith under the direction of the Board.

The Board has adopted Valuation Procedures (the “Procedures”) to determine the fair value of securities and other financial instruments for which market prices are not readily available or which may not be reliably priced. The Board has delegated the day-to-day responsibility for determining the fair value of assets of the Fund, except Special Equities investments, to Calvert Investment Management, Inc. (the “Advisor” or “Calvert”) and has provided these Procedures to govern Calvert in its valuation duties. Special Equities investments, as described in the Fund’s prospectus and statement of additional information, are fair valued by the Board’s Audit Committee (prior to January 1, 2015, by the Special Equities Committee).

Calvert has chartered an internal Valuation Committee to oversee the implementation of these Procedures and to assist it in carrying out the valuation responsibilities that the Board has delegated.

The Valuation Committee meets on a regular basis to review illiquid securities and other investments which may not have readily available market prices. The Valuation Committee’s fair valuation determinations are subject to review, approval and ratification by the Board at its next regularly scheduled meeting covering the calendar quarter in which the fair valuation was determined.

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND SEMI-ANNUAL REPORT (UNAUDITED) 25

The Valuation Committee utilizes various methods to measure the fair value of the Fund’s investments. Generally Accepted Accounting Principles (GAAP) establishes a disclosure hierarchy that categorizes the inputs to valuation techniques used to value assets and liabilities at measurement date. These inputs are summarized in the three broad levels listed below:

Level 1 - quoted prices in active markets for identical securities

Level 2 - other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.)

Level 3 - significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments)

The inputs or methodologies used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

Changes in valuation techniques may result in transfers in or out of an investment’s assigned level within the hierarchy during the period. At March 31, 2015, $206,991,697 transferred out of Level 1 into Level 2. Valuation techniques used to value the Fund's investments by major category are as follows:

Equity securities, including restricted securities and venture capital securities, for which market quotations are readily available, are valued at the last reported sale price or official closing price as reported by an independent pricing service on the primary market or exchange on which they are traded and are categorized as Level 1 in the hierarchy. In the event there were no sales during the day or closing prices are not available, securities are valued at the last quoted bid price or using the last available price and are categorized as Level 2 in the hierarchy. Foreign securities are valued based on quotations from the principal market in which such securities are normally traded. If events occur after the close of the principal market in which foreign securities are traded, and before the close of business of the Fund, that are expected to materially affect the value of those securities, then they are valued at their fair value taking these events into account. The Fund has retained a third party fair value pricing service to quantitatively analyze the price movement of its holdings on foreign exchanges and to automatically fair value if the variation from the prior day’s closing price exceeds specified parameters. Such securities would be categorized as Level 2 in the hierarchy in these circumstances. Utilizing this technique may result in transfers between Level 1 and Level 2. For restricted securities and private placements where observable inputs are limited, assumptions about market activity and risk are used and such securities are categorized as Level 3 in the hierarchy.

Venture capital securities for which market quotations are not readily available are fair valued by the Fund’s Board of Directors and are categorized as Level 3 in the hierarchy. Venture capital direct equity securities are generally valued using the most appropriate and applicable method to measure fair value in light of each company’s situation. Methods may include market, income or cost approaches with discounts as appropriate based on assumptions of liquidation or exit risk. Examples of the market approach are subsequent rounds of financing, comparable transactions, and revenue times an industry multiple. An example of the income approach is the discounted cash flow. Examples of the cost approach are replacement cost, salvage value, or net asset percentage. Venture capital limited partnership (“LP”) securities are valued at the fair value reported by the general partner of the partnership adjusted as necessary to reflect subsequent capital calls and distributions and any other available information, as a practical expedient. In the absence of a reported LP unit value, fair value may be estimated based on the Fund’s percentage equity in the partnership and/or other balance sheet information and portfolio value for the

26 www.calvert.com CALVERT INTERNATIONAL EQUITY FUND SEMI-ANNUAL REPORT (UNAUDITED)

most recently available period reported by the general partner. In some cases adjustments may be made to account for daily pricing of material public holdings within the partnership. Venture capital debt securities are valued based on assumptions of credit and market risk. For venture capital securities denominated in foreign currency, the fair value is marked to the daily exchange rate.

Debt securities, including restricted securities, are valued based on evaluated prices received from independent pricing services or from dealers who make markets in such securities and are generally categorized as Level 2 in the hierarchy. Short-term securities of sufficient credit quality with remaining maturities of sixty days or less for which quotations are not readily available are valued at amortized cost, which approximates fair value, and are categorized as Level 2 in the hierarchy.

When independent prices are unavailable or unreliable, debt securities may be valued utilizing pricing matrices which consider similar factors that would be used by independent pricing services. These are generally categorized as Level 2 in the hierarchy but may be Level 3 depending on the circumstances.

If a market value cannot be determined for a security using the methodologies described above, or if, in the good faith opinion of the Advisor, the market value does not constitute a readily available market quotation, or if a significant event has occurred that would materially affect the value of the security, the security will be fair valued as determined in good faith by the Valuation Committee or with respect to Special Equities investments, by the Audit Committee using the venture capital methodologies described above.

The Valuation Committee considers a number of factors, including significant unobservable valuation inputs when arriving at fair value. It considers all significant facts that are reasonably available and relevant to the determination of fair value.

The Valuation Committee primarily employs a market-based approach which may use related or comparable assets or liabilities, recent transactions, market multiples, book values, and other relevant information for the investment to determine the fair value of the investment. When more appropriate, the fund may employ an income-based or cost approach. An income-based valuation approach discounts anticipated future cash flows of the investment to calculate a present amount (discounted). The measurement is based on the value indicated by current market expectations about those future amounts. Discounts may also be applied due to the nature or duration of any restrictions on the disposition of the investments. A cost based approach is based on the amount that currently would be required to replace the service capacity of an asset (current replacement cost). From the seller’s perspective, the price that would be received for the asset is determined based on the cost to a buyer to acquire or construct a substitute asset of comparable utility, adjusted for obsolescence.

The values assigned to fair value investments are based on available information and do not necessarily represent amounts that might ultimately be realized. Further, due to the inherent uncertainty of valuations of such investments, the fair values may differ significantly from the values that would have been used had an active market existed, and the differences could be material. The Valuation Committee employs various methods for calibrating these valuation approaches including a regular review of key inputs and assumptions, transactional back-testing or disposition analysis and reviews of any related market activity.

At March 31, 2015, securities valued at $7,391,560, or 2.0% of net assets, were fair valued in good faith under the direction of the Board.

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND SEMI-ANNUAL REPORT (UNAUDITED) 27

The following table summarizes the market value of the Fund’s holdings as of March 31, 2015, based on the inputs used to value them:

|

| | | | | | | | | | | | | | | |

| | VALUATION INPUTS |

INVESTMENTS IN SECURITIES | LEVEL 1 | | LEVEL 2 | | LEVEL 3 | | TOTAL |

| Equity securities* |

| $128,881,966 |

| |

| $206,991,697 | ** | | — |

| | $335,873,663*** |

|

| Other debt obligations | — |

| | 36,710,808 |

| | — |

| | 36,710,808 |

|

| Venture capital | — |

| | 226,071 |

| | $2,772,009 | | 2,998,080 |

|

| TOTAL |

| $128,881,966 |

| |

| $243,928,576 |

| |

| $2,772,009 | **** | |

| $375,582,551 |

|

| | | | | | | | |

* For further breakdown of equity securities by country, please refer to the Statement of Net Assets. ** Includes certain securities trading primarily outside the U.S. whose value was adjusted as a result of significant market movements following the close of local trading. On March 31, 2015, price movements exceeded specified parameters and the third party fair value pricing service quantitatively fair valued the affected securities. *** Exclusive of $526,038 venture capital equity shown in venture capital heading. **** Level 3 securities represent 0.8% of net assets. |

At March 31, 2015, a significant transfer out of Level 1 and into Level 2 occurred.

On March 31, 2015, price movements exceeded specified parameters and the third party fair value pricing service quantitatively fair valued the affected securities.

Restricted Securities: The Fund may invest in securities that are subject to legal or contractual restrictions on resale. Generally, these securities may only be sold publicly upon registration under the Securities Act of 1933 or in transactions exempt from such registration. Information regarding restricted securities is included at the end of the Fund’s Statement of Net Assets.

Security Transactions and Net Investment Income: Security transactions are accounted for on trade date. Realized gains and losses are recorded on an identified cost basis and may include proceeds from litigation. Dividend income is recorded on the ex-dividend date or, in the case of dividends on certain foreign securities, as soon as the Fund is informed of the ex-dividend date. Withholding taxes on foreign dividends have been provided for in accordance with the Fund’s understanding of the applicable country’s tax rules and rates. Distributions received on securities that represent a return of capital or capital gain are recorded as a reduction of cost of investments and/or as a realized gain. Interest income, which includes amortization of premium and accretion of discount on debt securities, is accrued as earned. Investment income and realized and unrealized gains and losses are allocated to separate classes of shares based upon the relative net assets of each class. Expenses arising in connection with a specific class are charged directly to that class. Expenses common to the classes are allocated to each class in proportion to their relative net assets.

Foreign Currency Transactions: The Fund’s accounting records are maintained in U.S. dollars. For valuation of assets and liabilities on each date of net asset value determination, foreign denominations are converted into U.S. dollars using the current exchange rate. Security transactions, income and expenses are translated at the prevailing rate of exchange on the date of the event. The effect of changes in foreign exchange rates on securities and foreign currencies is included in the net realized and unrealized gain or loss on securities and foreign currencies.

28 www.calvert.com CALVERT INTERNATIONAL EQUITY FUND SEMI-ANNUAL REPORT (UNAUDITED)

Distributions to Shareholders: Distributions to shareholders are recorded by the Fund on ex-dividend date. Dividends from net investment income and distributions from net realized capital gains, if any, are paid at least annually. Distributions are determined in accordance with income tax regulations which may differ from generally accepted accounting principles; accordingly, periodic reclassifications are made within the Fund’s capital accounts to reflect income and gains available for distribution under income tax regulations.

Estimates: The preparation of the financial statements in conformity with accounting principles generally accepted in the United States requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of income and expenses during the reported period. Actual results could differ from those estimates.

Redemption Fees: The Fund charges a 2% redemption fee on redemptions, including exchanges, made within 30 days of purchase in the same Fund (within seven days for Class I shares). The redemption fee is accounted for as an addition to paid-in capital and is intended to discourage market-timers by ensuring that short-term trading costs are borne by the investors making the transactions and not the shareholders already in the Fund. This fee was eliminated effective February 2, 2015.

Federal Income Taxes: No provision for federal income or excise tax is required since the Fund intends to continue to qualify as a regulated investment company under the Internal Revenue Code and to distribute substantially all of its taxable earnings.

Management has analyzed the Fund’s tax positions taken for all open federal income tax years and has concluded that no provision for federal income tax is required in the Fund’s financial statements. A Fund’s federal tax return is subject to examination by the Internal Revenue Service for a period of three years.

NOTE B — RELATED PARTY TRANSACTIONS

Calvert Investment Management, Inc. (the “Advisor”) is wholly-owned by Calvert Investments, Inc., which is indirectly wholly-owned by Ameritas Mutual Holding Company. The Advisor provides investment advisory services and pays the salaries and fees of officers and Directors of the Fund who are employees of the Advisor or its affiliates. For its services, the Advisor receives a monthly fee based on the following annual rates of average daily net assets: .75% on the first $250 million, .725% on the next $250 million, and .675% on the excess of $500 million. Under the terms of the agreement, $231,340 was payable.

The Advisor has contractually agreed to limit net annual fund operating expenses through January 31, 2016 for Class I and Class Y. The contractual expense cap is 1.10% and 1.39%, respectively. For the purpose of this expense limit, operating expenses do not include interest expense, brokerage commissions, taxes, and extraordinary expenses. This expense limitation does not limit any acquired fund fees and expenses, if any. At period end, $838 was receivable from the Advisor. The Advisor voluntarily reimbursed Class B shares for expenses of $7,474 for the six months ended March 31, 2015.

Calvert Investment Administrative Services, Inc., an affiliate of the Advisor, provides administrative services to the Fund for an annual fee, payable monthly, of .35% for Classes A, B, C, and Y, and .15% for Class I, based on their average daily net assets. Under the terms of the agreement, $92,349 was payable at period end.

Calvert Investment Distributors, Inc. (“CID”), an affiliate of the Advisor, is the distributor and principal underwriter for the Fund. Pursuant to Rule 12b-1 under the Investment Company Act

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND SEMI-ANNUAL REPORT (UNAUDITED) 29

of 1940, the Fund has adopted a Distribution Plan that permits the Fund to pay certain expenses associated with the distribution and servicing of its shares. The expenses paid may not exceed .35%, 1.00% and 1.00% annually of average daily net assets of Class A, B, and C, respectively. The amount actually paid by the Fund is an annualized fee, payable monthly, of .25%, 1.00% and 1.00% of the Fund’s average daily net assets of Class A, B, and C, respectively. Class I and Class Y shares do not have Distribution Plan expenses. Under the terms of agreement, $64,699 was payable at period end.

CID received $17,482 as its portion of commissions charged on sales of the Fund’s Class A shares for the six months ended March 31, 2015.

Calvert Investment Services, Inc. (“CIS”), an affiliate of the Advisor, is the shareholder servicing agent for the Fund. For its services, CIS received a fee of $48,191 for the period ended March 31, 2015. Under the terms of the agreement, $7,940 was payable at period end. Boston Financial Data Services, Inc. is the transfer and dividend disbursing agent.

The Fund invests in Community Investment Notes issued by the Calvert Social Investment Foundation (the “CSI Foundation”). The CSI Foundation is a 501(c)(3) non-profit organization that receives in-kind support from Calvert and its subsidiaries. The Fund has received an exemptive order from the Securities and Exchange Commission permitting the Fund to make investments in these notes under certain conditions.

Each Director of the Funds who is not an employee of the Advisor or its affiliates receives an annual retainer of $52,000 ($48,000 prior to January 1, 2015) plus a meeting fee of up to $3,000 for each Board meeting attended. Additional fees of up to $6,000 ($5,000 prior to January 1, 2015) annually may be paid to the Committee chairs ($10,000 for the Board chair and the Special Equities Committee chair) and $2,500 annually may be paid to Committee members, plus a Committee meeting fee of $500 for each Committee meeting attended. Directors’ fees are allocated to each of the Funds served.

NOTE C — INVESTMENT ACTIVITY AND TAX INFORMATION

During the period, the cost of purchases and proceeds from sales of investments, other than short-term securities, were $104,310,312, and $148,482,648, respectively.

The Fund may purchase securities, typically short-term variable rate demand notes, from or sell to other funds managed by the Advisor. These interportfolio transactions are primarily used for cash management purposes and are made pursuant to Rule 17a-7 of the Investment Company Act of 1940. For the six months ended March 31, 2015, such sales transactions were $201,633. The realized loss on sales transactions was $92,252.

|

| | | |

CAPITAL LOSS CARRYFORWARD | |

| |

EXPIRATION DATE | |

| 30-Sep-17 |

| ($44,177,301 | ) |

| 30-Sep-18 | (105,942,268 | ) |

| 30-Sep-19 | (10,386,632 | ) |