Table of Contents

Filed Pursuant to Rule 424(b)(5)

File Number 333-112132

PROSPECTUS SUPPLEMENT TO PROSPECTUS DATED MARCH 15, 2004

7,500,000 Shares

Common Stock

We are selling 7,500,000 shares of our common stock.

Our common stock is listed on the New York Stock Exchange and the Philadelphia Stock Exchange under the symbol “UGI.” The last reported sale price of our common stock on the New York Stock Exchange on March 18, 2004 was $32.10 per share.

The underwriters have an option to purchase a maximum of 1,125,000 additional shares to cover over-allotments of shares.

Investing in our common stock involves risk. See “Risk Factors” beginning on page S-9 of this prospectus supplement.

Price to Public | Underwriting Discounts and Commissions | Proceeds to UGI | |||||||

Per Share | $ | 32.10 | $ | 1.4044 | $ | 30.6956 | |||

Total | $ | 240,750,000 | $ | 10,533,000 | $ | 230,217,000 | |||

Delivery of the shares of common stock will be made on or about March 23, 2004.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus supplement is truthful or complete. Any representation to the contrary is a criminal offense.

Credit Suisse First Boston

Citigroup

Wachovia Securities

Janney Montgomery Scott LLC

The date of this Prospectus Supplement is March 18, 2004.

Table of Contents

| Page | ||

| S-1 | ||

| S-1 | ||

| S-9 | ||

| S-15 | ||

| S-16 | ||

| S-16 | ||

| S-17 | ||

| S-18 | ||

| Page | ||

CERTAIN UNITED STATES FEDERAL TAX CONSEQUENCES TO NON-U.S. HOLDERS | S-19 | |

| S-21 | ||

| S-23 | ||

| S-23 | ||

| S-23 | ||

| S-24 | ||

| S-25 | ||

You should rely only on the information contained in, or incorporated by reference into, this document or to which we have referred you. We have not authorized anyone to provide you with information that is different. This document may only be used where it is legal to sell these securities. The information in this document may only be accurate on the date of this document.

i

Table of Contents

You should read the following summary together with the more detailed information regarding our company, our common stock, the financial statements and notes to those statements incorporated herein by reference from our other filings with the Securities and Exchange Commission (the “SEC”) and the AGZ Holding financial statements and notes to those statements included herein. We urge you to read the entire prospectus supplement carefully, especially the risks of investing in our common stock, which are discussed under “Risk Factors,” before making an investment decision. All references to “we,” “our” or “us” in this prospectus supplement refer to UGI Corporation and, where appropriate, its consolidated subsidiaries, unless the context otherwise requires.

UGI Corporation is a distributor and marketer of energy products and services serving nearly 2 million customers principally in North America and Europe through subsidiaries and joint venture affiliates, including:

| • | AmeriGas Partners, L.P. (“AmeriGas Partners”)—the largest retail propane marketer in the United States based on retail volume, distributing more than one billion retail gallons in its fiscal year ended September 30, 2003. As of September 30, 2003, AmeriGas Partners served approximately 1.3 million customers from approximately 650 locations in 46 states. On October 1, 2003, AmeriGas Partners acquired the assets of Horizon Propane LLC. Giving effect to the Horizon Propane acquisition, AmeriGas Partners has over 700 locations. The common units of AmeriGas Partners, representing limited partnership interests in the limited partnership, trade on the New York Stock Exchange under the symbol “APU.” We have an effective 48% ownership interest in AmeriGas Partners. The remaining interest is publicly held. |

| • | UGI Utilities, Inc. (“UGI Utilities”)—a regulated gas and electric distribution utility serving over 300,000 customers in eastern Pennsylvania as of September 30, 2003. UGI Utilities is regulated by the Pennsylvania Public Utility Commission. |

| • | UGI Enterprises, Inc. (“UGI Enterprises”)—a company that conducts domestic and international energy related-businesses through subsidiaries and joint ventures. UGI Enterprises’ principal operating business is UGI Energy Services, Inc. (“ESI”), which markets natural gas, oil and electricity in the eastern region of the United States under the trade name GASMARK® and served approximately 5,000 customers as of September 30, 2003. ESI also owns and operates liquefied natural gas and propane plants which are used to meet peak energy needs. UGI Development Company, a subsidiary of ESI, owns interests in and operates Pennsylvania-based electric generation assets. UGI HVAC Enterprises, Inc. operates a heating and cooling installation and service business in the Mid-Atlantic region. |

| UGI Enterprises conducts its international liquefied petroleum gases (“LPG”) distribution business through wholly-owned subsidiaries and joint ventures. It owns FLAGA GmbH, the largest retail LPG distributor in Austria and one of the largest suppliers in the Czech Republic and Slovakia, distributing approximately 33 million gallons of LPG during the fiscal year ended September 30, 2003. UGI Enterprises also participates in a propane distribution joint venture in China. As discussed more fully below, UGI Enterprises currently holds, through UGI France, Inc., an approximate 19.5% interest in AGZ Holding, a French corporation (société anonyme) and the parent holding company of Antargaz, one of the largest distributors of LPG in France. We expect to acquire the remaining approximate 80.5% interest in AGZ Holding in the transaction that is intended to be funded, in part, through this offering. |

S-1

Table of Contents

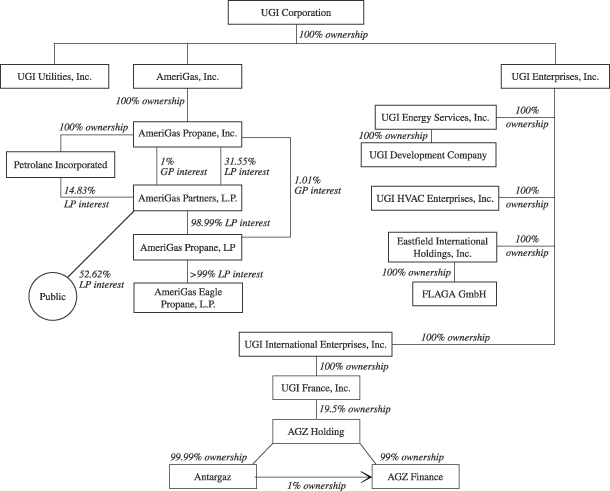

The following chart depicts the current ownership structure of our principal subsidiaries:

S-2

Table of Contents

Our Competitive Strengths

We believe that our competitive strengths include the following:

| • | Operational and managerial expertise in the U.S. and international propane markets and a proven ability to maintain propane margins in warm weather periods. |

| • | An experienced management team with a successful track record of growing the regulated gas utility operations within its service territory. |

| • | A disciplined pursuit of acquisition opportunities focused in the propane and retail energy market sectors. |

| • | A demonstrated ability to integrate acquisitions and achieve operating efficiencies. |

Our Business Strategy

In the late 1990s, we undertook an evaluation of our businesses and their prospects. Following that evaluation, we decided to focus on being a distributor and marketer of energy products and services both nationally and internationally.

In pursuing our energy distribution and marketing strategy, we seek to leverage our asset base, our geographic reach and our intellectual capital. We employ our core competencies from our existing businesses, and use our national scope, international experience, extensive asset base, access to customers and operating expertise to accelerate growth in related and complementary businesses, both domestic and international. During fiscal year 2003, we completed a number of transactions in pursuit of this strategy.

We have identified the international LPG distribution business as one area for potential growth. This area is of particular interest to us because (1) through it, we can leverage our substantial intellectual capital and operating expertise in propane distribution, (2) international LPG markets include both mature markets, which meet our need for income, and developing markets, which are consistent with our desire for growth, and (3) we believe this strategy provides greater potential to achieve economies of scale over time.

Our wholly-owned subsidiary, UGI Enterprises, Inc., currently participates in the international LPG distribution business in Austria, the Czech Republic and Slovakia, and through joint ventures in France (through its holdings in AGZ Holding) and China. Our management philosophy in the international LPG distribution business consists of three elements:

| • | Ensure that each business has strong “in country” expertise to ensure proper regard is given to local cultural and market differences. This “in country” expertise is gained through a strong local management team, board or partner. |

| • | Transfer the best practices of our U.S. propane distribution business to our international LPG distribution businesses. |

| • | Transfer the best practices of our international LPG distribution businesses to our U.S. propane distribution business. |

We believe that our intended acquisition of the remaining interests in AGZ Holding is consistent with our focus on the international LPG distribution business and our commitment to remain a superior, balanced growth and income investment for our shareholders.

S-3

Table of Contents

Planned Acquisition of Antargaz

We hold, through our indirect, wholly-owned subsidiary, UGI France, Inc., approximately 19.5% of the issued and outstanding shares of the capital stock of AGZ Holding. AGZ Holding owns 99.99% of Antargaz, a French corporation (société anonyme), which, through its wholly- and partially-owned subsidiaries, is engaged in the business of marketing, selling and distributing LPG in mainland France and the French island of Corsica. We expect to acquire the ownership interests in AGZ Holding that we do not already own as of April 1, 2004.

Antargaz is one of the four leading distributors of LPG in France. During its fiscal year ended March 31, 2003, Antargaz sold approximately 350 million gallons of LPG and had an approximate 24% market share in France. The French LPG market is mature, with limited future growth expected. Antargaz serves over 220,000 customers using a logistical system that includes five primary storage facilities and 26 secondary storage facilities. Antargaz’s customer base consists of residential, commercial, agricultural and motor fuel accounts that use LPG for space heating, cooking, water heating, process heat and transportation. As of September 30, 2003, Antargaz had approximately 1,350 employees.

We expect to realize a number of significant economic and strategic benefits as a result of our planned acquisition of Antargaz. We anticipate that the planned transaction will:

| • | Contribute to our earnings growth strategy; |

| • | Provide significant financial resources to grow our earnings per share; |

| • | Provide a larger platform for growth in Europe; |

| • | Provide an experienced management team in Europe; and |

| • | Enhance the opportunities for a sharing of best practices. |

On February 17, 2004 and February 20, 2004, we executed a share purchase agreement and a joinder agreement, respectively, to effect the acquisition of the ownership interests in AGZ Holding that we do not already own by purchasing, through UGI France, Inc., or another of our wholly-owned subsidiaries, (1) approximately 78.3% of the issued and outstanding capital stock of AGZ Holding, approximately 68.5% of which is currently owned by privately-held, French-based investment funds that are managed by PAI partners, a French corporation (société par actions simplifiée) (“PAI”), and approximately 9.8% of which is currently owned by Medit Mediterranea GPL S.r.L., a company organized under the laws of Italy (“Medit”), and (2) approximately 99.99% of the shares of the issued and outstanding capital stock of Financière AGZ, a French corporation (société par actions simplifiée) which owns approximately 2.2% of the issued and outstanding capital stock of AGZ Holding. Financière AGZ has nominal assets and conducts no business operations; its shareholders are currently comprised of AGZ Holding, PAI, Medit, UGI France and certain individuals, including officers and managers of AGZ Holding, Antargaz, Antargaz subsidiaries or their affiliates.

In the anticipated transaction, we have agreed to pay approximately €258.5 million ($320.2 million based on an exchange rate of $1.2387 per euro on March 18, 2004), based upon estimates of working capital and pre- and post-closing adjustments, for the ownership interests in AGZ Holding that we do not already own. We expect to fund the purchase price with approximately $100 million of existing cash balances and the proceeds of this offering.

UGI Corporation has made an offer to acquire, upon completion of the transaction, the outstanding 10% Senior Notes due 2011 of AGZ Finance (the “AGZ Notes”), a wholly-owned subsidiary of AGZ Holding, at the purchase price of 101% of the principal amount of the notes tendered plus accrued and unpaid interest thereon and specified additional amounts, if any, as provided for in the trust deed governing the AGZ Notes. Although, at this time, we do not expect significant amounts of AGZ Notes to be tendered in such offer, we have executed agreements with certain affiliates of Credit Suisse First Boston to enable us to finance the purchase of any AGZ Notes tendered pursuant to such offer.

S-4

Table of Contents

Under AGZ Holding’s senior facilities agreement, dated June 26, 2003, as amended, with Credit Lyonnais as mandated lead arranger, facility agent and security agent, our acquisition of Antargaz will constitute a “change of control” and result in an acceleration of all amounts borrowed and outstanding under such agreement, unless our subsidiary, UGI France, Inc., or any of its affiliates obtains, within six months of the consummation of the acquisition, a corporate rating from Standard & Poor’s Ratings Group of at least BBB. AGZ Holding will not be able to make any restricted payments under the senior facilities agreement during such six-month period prior to obtaining such rating. As of December 31, 2003, there were term loans of €211,000,000 outstanding under AGZ Holding’s senior facilities agreement. We expect to seek an amendment of the senior facilities agreement to provide that our acquisition of AGZ Holding does not constitute a “change of control” under the agreement.

Additional Information

We were incorporated in Pennsylvania in 1991. UGI Corporation is not subject to regulation by the Pennsylvania Public Utility Commission. We are also exempt from registration as a holding company and not otherwise subject to the Public Utility Holding Company Act of 1935, except for Section 9(a)(2), which regulates the acquisition of voting securities of an electric or gas utility company.

Our executive offices are located at 460 North Gulph Road, King of Prussia, Pennsylvania 19406, and our telephone number is (610) 337-1000. Our website is http://www.ugicorp.com. The information on our website is not incorporated into, and does not constitute a part of, this prospectus supplement.

Recent Events

On January 27, 2004, we announced our intention to increase the annual dividend rate on our common stock to $1.25 per share from $1.14 per share effective with the regularly scheduled July dividend payment, assuming the completion of the anticipated acquisition of the shares in AGZ Holding that we do not already own.

S-5

Table of Contents

The Offering

Unless otherwise indicated, all of the information in this prospectus supplement assumes no exercise of any underwriters’ over-allotment option to purchase additional shares of common stock from us.

Common stock offered by us | 7,500,000 shares | |

Common stock to be outstanding after the offering | 50,278,798 shares | |

Use of proceeds | To pay the purchase price for the ownership interests that we do not already own in AGZ Holding, the parent holding company of Antargaz. To the extent any proceeds remain after paying such purchase price or we do not complete such transaction, we will use the proceeds for general corporate purposes. | |

New York Stock Exchange Symbol | UGI | |

Philadelphia Stock Exchange Symbol | UGI | |

The number of shares of common stock to be outstanding after this offering is based on 42,778,798 shares outstanding as of December 31, 2003, and excludes:

| • | 2,950,288 shares of common stock underlying options as of March 1, 2004, at an average option exercise price of $21.877 per share; |

| • | a maximum of 507,854 shares of common stock that may be issued pursuant to grants of phantom units as of March 1, 2004; and |

| • | 2,712,096 shares available for future grants under all equity compensation plans as of March 1, 2004. |

S-6

Table of Contents

Summary Financial Data

The following data (except pro forma data), insofar as they relate to each of the years in the three-year period ended September 30, 2003, have been derived from our audited annual financial statements, including the consolidated balance sheets at September 30, 2002 and 2003 and the related consolidated statements of operations and cash flows for the three years ended September 30, 2003 and the notes thereto, incorporated herein by reference. The unaudited pro forma income statement data give effect to the acquisition of the ownership interests in AGZ Holding that we do not already own as if the acquisition had been consummated on October 1, 2002. The unaudited pro forma balance sheet data give effect to the acquisition as if it had been consummated on December 31, 2003. The selected unaudited pro forma financial data are not necessarily indicative of operating results or financial position that would have been achieved had the acquisition of the ownership interests in AGZ Holding that we do not already own been consummated and should not be construed as representative of future operating results or financial position. The following data should be read in conjunction with our historical financial statements, and the related notes thereto, which are incorporated herein by reference, the Unaudited Pro Forma Condensed Combined Financial Statements beginning on page P-1, and the historical financial statements and the related notes of AGZ Holding beginning on page F-1.

| Year Ended September 30, | Three Months Ended December 31, | ||||||||||||||||||||

| 2001(a) | 2002 | 2003 | 2003 Pro Forma (b) (c) | 2002 | 2003 | 2003 Pro Forma(b) | |||||||||||||||

| (Millions of dollars, except per share amounts) | |||||||||||||||||||||

Income Statement Data: | |||||||||||||||||||||

Revenues | $ | 2,468.1 | $ | 2,213.7 | $ | 3,026.1 | $ | 3,725.0 | $ | 739.9 | $ | 893.7 | $ | 1,108.0 | |||||||

Income before accounting changes | $ | 52.0 | $ | 75.5 | $ | 98.9 | $ | 36.7 | $ | 38.8 | |||||||||||

Cumulative effect of accounting changes (d) | 4.5 | — | — | — | — | ||||||||||||||||

Net income (e) | $ | 56.5 | $ | 75.5 | $ | 98.9 | $ | 119.4 | $ | 36.7 | $ | 38.8 | $ | 57.5 | |||||||

Earnings per common share - basic (c) (f) | |||||||||||||||||||||

Income before accounting changes | $ | 1.28 | $ | 1.83 | $ | 2.34 | $ | 0.88 | $ | 0.91 | |||||||||||

Cumulative effect of accounting changes, net (d) | 0.11 | — | — | — | — | ||||||||||||||||

Net income - basic | $ | 1.39 | $ | 1.83 | $ | 2.34 | $ | 2.40 | $ | 0.88 | $ | 0.91 | $ | 1.14 | |||||||

Earnings per common share - diluted (c) (f) | |||||||||||||||||||||

Income before accounting changes | $ | 1.27 | $ | 1.80 | $ | 2.29 | $ | 0.86 | $ | 0.88 | |||||||||||

Cumulative effect of accounting changes, net (d) | 0.11 | — | — | — | — | ||||||||||||||||

Net income - diluted (e) | $ | 1.38 | $ | 1.80 | $ | 2.29 | $ | 2.35 | $ | 0.86 | $ | 0.88 | $ | 1.12 | |||||||

Cash dividends declared per common share | $ | 1.05 | $ | 1.083 | $ | 1.13 | $ | 1.13 | $ | 0.275 | $ | 0.285 | $ | 0.285 | |||||||

S-7

Table of Contents

| As of September 30, | As of December 31, | |||||||||||||||||||||||

| 2001(a) | 2002 | 2003 | 2002 | 2003 | 2003 Pro Forma (b) | |||||||||||||||||||

| (Millions of dollars) | ||||||||||||||||||||||||

Balance Sheet Data: | ||||||||||||||||||||||||

Total assets | $ | 2,550.2 | $ | 2,610.9 | $ | 2,781.3 | $ | 2,870.6 | $ | 3,027.0 | $ | 4,432.7 | ||||||||||||

Capitalization: | ||||||||||||||||||||||||

Debt: | ||||||||||||||||||||||||

Bank loans - AmeriGas Propane | $ | — | $ | 10.0 | $ | — | 37.0 | 36.0 | 36.0 | |||||||||||||||

Bank loans - UGI Utilities | 57.8 | 37.2 | 40.7 | 78.3 | 72.2 | 72.2 | ||||||||||||||||||

Bank loans - other | 10.0 | 8.6 | 15.9 | 11.2 | 18.1 | 18.1 | ||||||||||||||||||

Long-term debt (including current maturities): | ||||||||||||||||||||||||

AmeriGas Propane | 1,005.9 | 945.8 | 927.3 | 1,035.7 | 926.0 | 926.0 | ||||||||||||||||||

UGI Utilities | 208.4 | 248.4 | 217.3 | 222.3 | 217.2 | 217.2 | ||||||||||||||||||

AGZ Holding (g) | — | — | — | — | — | 510.6 | ||||||||||||||||||

Other | 80.9 | 81.5 | 78.9 | 85.3 | 83.7 | 83.7 | ||||||||||||||||||

Total debt | $ | 1,363.0 | $ | 1,331.5 | $ | 1,280.1 | $ | 1,469.8 | $ | 1,353.2 | $ | 1,863.8 | ||||||||||||

Minority interests | 246.2 | 276.0 | 134.6 | 122.9 | 149.8 | 164.9 | ||||||||||||||||||

UGI Utilities preferred shares subject to mandatory redemption | 20.0 | 20.0 | 20.0 | 20.0 | 20.0 | 20.0 | ||||||||||||||||||

Common stockholders’ equity | 255.6 | 313.8 | 569.4 | 503.3 | 608.6 | 838.8 | ||||||||||||||||||

Total capitalization | $ | 1,884.8 | $ | 1,941.3 | $ | 2,004.1 | $ | 2,116.0 | $ | 2,131.6 | $ | 2,887.5 | ||||||||||||

Ratio of Capitalization: | ||||||||||||||||||||||||

Total debt | 72.3 | % | 68.6 | % | 63.9 | % | 69.5 | % | 63.5 | % | 64.5 | % | ||||||||||||

Minority interests | 13.1 | % | 14.2 | % | 6.7 | % | 5.8 | % | 7.0 | % | 5.7 | % | ||||||||||||

UGI Utilities preferred shares subject to mandatory redemption | 1.1 | % | 1.0 | % | 1.0 | % | 0.9 | % | 0.9 | % | 0.7 | % | ||||||||||||

Common stockholders’ equity | 13.5 | % | 16.2 | % | 28.4 | % | 23.8 | % | 28.6 | % | 29.1 | % | ||||||||||||

| (a) | Arthur Andersen LLP audited our consolidated financial statements for 2001. You should refer to the final risk factor under “Risk Factors—Risks Related to our Common Stock” on page S-14 of this prospectus supplement. |

| (b) | The pro forma income statement data assume that our acquisition of the ownership interests in AGZ Holding that we do not already own was completed on October 1, 2002 and are based on the average currency exchange rate of $1.19 per euro and $1.08 per euro for the three months ended December 31, 2003 and the fiscal year ended September 30, 2003, respectively. The pro forma balance sheet data assume that the acquisition was completed on December 31, 2003 and are based on a currency exchange rate of $1.26 per euro as of December 31, 2003. |

| (c) | Pro forma net income and earnings per diluted share include (1) the write-down of goodwill related to AGZ Holding’s investment in an equity investee of $4.8 million and $0.09, respectively, (2) the after-tax write-off of debt issuance costs of $3.2 million and $0.06, respectively, associated with AGZ Holding’s issuance and subsequent refinancing of the AGZ Notes, and (3) the after-tax write-off of an interest rate swap of $4.0 million and $0.08, respectively, associated with AGZ Holding’s senior debt redeemed in July 2003. |

| (d) | Includes the cumulative effect of accounting changes associated with (1) AmeriGas Partners’ changes in accounting for tank fee revenues and tank installation costs and (2) our adoption of Statement of Financial Accounting Standards No. 133, “Accounting for Derivative Instruments and Hedging Activities.” See Notes 1 and 15 to our Consolidated Financial Statements, incorporated herein by reference. |

| (e) | Statement of Financial Accounting Standards No. 142, “Goodwill and Other Intangible Assets,” was adopted effective October 1, 2001. Net income and net income per diluted share adjusted to reflect the impact of SFAS No. 142 as if it had been adopted at the beginning of the 2001 fiscal year would have been $70.5 million and $1.72, respectively. |

| (f) | Earnings per share for all periods presented reflect the effects of our 3-for-2 common stock split distributed on April 1, 2003 to stockholders of record on February 28, 2003. |

| (g) | Includes €165 million aggregate principal amount of AGZ Notes, reflected at fair market value on December 31, 2003. |

S-8

Table of Contents

Investing in our common stock involves a high degree of risk. You should carefully consider the following risk factors, in addition to the other information in this prospectus supplement, before making an investment decision. Each of these risk factors could adversely affect our business, operating results and financial condition, and the value of an investment in our common stock. Generally, each of the following risk factors that relates to our propane operations is also a risk factor that is applicable to Antargaz’s LPG operations.

Risks Related to Our Business

Decreases in the demand for our energy products and services because of warmer weather adversely affect our results of operations.

Because many of our customers rely on our energy products and services to heat their homes and businesses, our results of operations are adversely affected by warmer weather. Weather conditions have a significant impact on the demand for our energy products and services for both heating and agricultural purposes. Accordingly, the volume of our energy products sold is at its highest during the five-month peak heating season of November through March and is directly affected by the severity of the winter weather. For example, historically, approximately 55% to 60% of AmeriGas Partners’ annual retail propane volume has been sold during these months and approximately 60% of our natural gas throughput (the total volume of gas sold to or transported for customers within our distribution system) occurs during these months. In certain prior years, warmer-than-normal weather in our service territories reduced demand for our energy products and services for heating purposes below normal levels, which had an adverse effect on our operating results. There can be no assurance that normal winter weather in our service territories will occur in the future.

Our holding company structure could limit our ability to pay dividends or debt service.

We are a holding company whose material assets are the stock of our subsidiaries and interests in joint ventures. Accordingly, we conduct all of our operations through our subsidiaries and joint venture affiliates. Our ability to pay dividends on our common stock and to pay principal and accrued interest on our debt, if any, depends on the payment of dividends or distributions to us by our principal operating subsidiaries, AmeriGas Partners, L.P., UGI Utilities, Inc. and UGI Enterprises, Inc. Payments to us by those subsidiaries, in turn, depends upon their results of operations and cash flows and, in the case of AmeriGas Partners, the provisions of its partnership agreement. The operations of those subsidiaries are affected by conditions beyond our control, including weather, competition in markets we serve, the costs and availability of propane, natural gas, electricity and other energy sources and changes in capital market conditions. The ability of our subsidiaries, including AGZ Holding after completion of the proposed acquisition, to make payments to us is also affected by the level of indebtedness of such subsidiaries, which is substantial, and the restrictions on payments to us imposed under the terms of such indebtedness.

Our profitability is subject to propane pricing and inventory risk.

The retail propane business is a “margin-based” business in which gross profits are dependent upon the excess of the sales price over the propane supply costs. Propane is a commodity, and, as such, its unit price is subject to volatile fluctuations in response to changes in supply or other market conditions. We have no control over these market conditions. Consequently, the unit price of the propane that our subsidiaries and other marketers purchase can change rapidly over a short period of time. Most of our propane product supply contracts permit suppliers to charge posted prices at the time of delivery or the current prices established at major U.S. storage points such as Mont Belvieu, Texas or Conway, Kansas. Because our subsidiaries’ profitability is sensitive to changes in wholesale propane supply costs, it will be adversely affected if we cannot pass on increases in the cost of propane to our customers. Due to competitive pricing in the propane industry, our subsidiaries may not be able to pass on product cost increases to our customers when product costs rise rapidly,

S-9

Table of Contents

or when our competitors do not raise their product prices. In addition, high propane product prices may lead to customer conservation, resulting in reduced demand. Finally, market volatility may cause our subsidiaries to sell propane at less than the price at which they purchased it, which could adversely affect our operating results.

Our operations may be adversely affected by competition from other energy sources.

Our energy products and services face competition from other energy sources, some of which are less costly for equivalent energy value. In addition, we cannot predict the effect that the development of alternative energy sources might have on our operations.

Our propane business competes for customers against suppliers of electricity, fuel oil and natural gas. Electricity is a major competitor of propane, but propane generally enjoys a competitive price advantage over electricity for space heating, water heating and cooking. Fuel oil is also a major competitor of propane and is generally less expensive than propane. Furnaces and appliances that burn propane will not operate on fuel oil and vice versa, however, so a conversion from one fuel to the other requires the installation of new equipment. Our customers generally have an incentive to switch to fuel oil only if fuel oil becomes significantly less expensive than propane. Except for certain industrial and commercial applications, propane is generally not competitive with natural gas in areas where natural gas pipelines already exist because natural gas is generally a less expensive source of energy than propane. The gradual expansion of natural gas distribution systems in our service areas has resulted in the availability of natural gas in some areas that previously depended upon propane. As long as natural gas remains a less expensive energy source than propane, our propane business will lose customers in each region into which natural gas distribution systems are expanded. In France, the state-owned natural gas monopoly, Gaz de France, has in the past extended France’s natural gas grid.

Our natural gas business competes primarily with electricity and fuel oil, and, to a lesser extent, with propane and coal. Competition among these fuels is primarily a function of their comparative price and the relative cost and efficiency of fuel utilization equipment. Electric utilities within the areas served by our natural gas business are seeking new customers, primarily in the new construction market. Fuel oil dealers compete with us for customers in all areas, including industrial customers. There can be no assurance that our natural gas revenues will not be adversely affected by this competition.

Our ability to increase revenues is adversely affected by the maturity of the retail propane industry.

The retail propane industry in the United States is mature, with only modest growth in total demand for the product foreseen. Given this limited growth, we expect that year-to-year industry volumes will be principally affected by weather patterns. Therefore, our ability to grow within the propane industry is dependent on our ability to acquire other retail distributors and to achieve internal growth, which includes expansion of the PPX® program (through which consumers can exchange an empty propane grill cylinder for a filled one) and the strategic accounts program (through which we encourage large, multi-location propane users to enter into a supply agreement with us rather than with many small suppliers), as well as the success of our sales and marketing programs designed to attract and retain customers. Any failure to retain and grow our customer base would have an adverse effect on our results.

Our ability to grow our businesses will be adversely affected if we are not successful in making acquisitions or in integrating the acquisitions we have made.

Given the mature nature of the U.S. propane market, one of our strategies is to grow through acquisitions in the United States and in international markets. We may choose to finance future acquisitions with debt, equity, cash or a combination of the three. There is significant competition for acquisitions in the U.S. propane industry, specifically among publicly-traded master limited partnerships. We believe that there are numerous potential acquisition candidates in the U.S. propane industry, some of which represent acquisition opportunities that would be material to us. We cannot assure you that we will find attractive acquisition candidates in the future, that we will be able to acquire such candidates on economically acceptable terms, that any acquisitions will not be dilutive to earnings or that any additional debt incurred to finance an acquisition will not affect our ability to pay dividends.

S-10

Table of Contents

In addition, the restructuring of the energy markets in the United States and internationally, including the privatization of government-owned utilities and the sale of utility-owned assets, is creating opportunities for, and competition from, well-capitalized competitors, which may affect our ability to achieve our business strategy.

To the extent we are successful in making acquisitions, such acquisitions, including the anticipated acquisition of Antargaz, involve a number of risks, including, but not limited to, the assumption of material liabilities, the diversion of management’s attention from the management of daily operations to the integration of operations, difficulties in the assimilation and retention of employees and difficulties in the assimilation of different cultures and practices, as well as in the assimilation of broad and geographically dispersed personnel and operations. The failure to successfully integrate acquisitions could have an adverse affect on our business, financial condition and results of operations.

The U.S. propane retail distribution business is highly competitive.

We compete in the U.S. propane retail distribution business with other large propane marketers, including other full-service marketers, and thousands of small independent operators. In recent years, some rural electric cooperatives and fuel oil distributors have expanded their businesses to include propane distribution, and we compete with them as well. The ability to compete effectively depends on providing satisfactory customer service, maintaining competitive retail prices and controlling operating expenses.

We are dependent on our principal propane suppliers, which increases the risks from an interruption in supply and transportation.

During the year ended September 30, 2003, AmeriGas Partners purchased approximately 79% of its propane needs in the United States from ten suppliers. If supplies from these sources were interrupted, the cost of procuring replacement supplies and transporting those supplies from alternative locations might be materially higher and, at least on a short-term basis, our earnings could be affected. Additionally, in certain market areas, some of AmeriGas Partners’ suppliers provide 70% to 80% of its propane requirements. Disruptions in supply in these areas could also have an adverse impact on our earnings. Antargaz is similarly dependent upon its suppliers. Significant amounts of propane must be imported to meet demand in France. There is no assurance that Antargaz will be able to continue to acquire sufficient supplies of propane to meet demand at prices or within time periods that would allow it to remain competitive.

The expansion of our international business means that we will face increased risks, which may negatively affect our business results.

Our intended acquisition of Antargaz will significantly increase our international presence. As we continue to grow as a multi-national corporation, with subsidiaries around the world, we face risks in doing business abroad that we do not face domestically. Certain aspects inherent in transacting business internationally could negatively impact our operating results, including:

| • | costs and difficulties in staffing and managing international operations; |

| • | regulatory requirements and changes in regulatory requirements, including French and EU competition laws that may adversely affect the terms of contracts with customers, and new environmental requirements that have led to stricter regulations of LPG storage sites in France; |

| • | tariffs and other trade barriers; |

| • | difficulties in enforcing contractual rights; |

| • | longer payment cycles; |

| • | local political and economic conditions; |

| • | potentially adverse tax consequences, including restrictions on repatriating earnings and the threat of “double taxation”; and |

| • | fluctuations in currency exchange rates. |

S-11

Table of Contents

We are subject to operating and litigation risks that may not be covered by insurance.

Our business’ operations and those of Antargaz are subject to all of the operating hazards and risks normally incidental to the handling, storage and delivery of combustible products, such as LPG and natural gas, and the generation of electricity. These risks could result in substantial losses due to personal injury and/or loss of life, severe damage to and destruction of property and equipment and pollution or other environmental damage. As a result, we are sometimes a defendant in legal proceedings and litigation arising in the ordinary course of business. We maintain insurance policies with insurers in such amounts and with such coverages and deductibles as we believe are reasonable and prudent. We cannot assure you, however, that such insurance will be adequate to protect us from all material expenses related to potential future claims for personal and property damage or that such levels of insurance will be available in the future at economical prices.

Moreover, our acquisition of the remaining interests in AGZ Holding will expose us to additional litigation risks at Antargaz. Specifically, in connection with its 2001 acquisition of its propane business, AGZ Holding entered into a guarantee agreement with Elf Antar France, now Total France, and Elf Aquitaine pursuant to which Total France and Elf Aquitaine agreed to indemnify AGZ Holding for all payments which would have been due from Antargaz in respect of certain matters, including a business tax related to AGZ Holding’s propane tanks for the period from January 1, 1997 through December 31, 2000, and certain potential environmental/safety liabilities. If Total France and Elf Aquitaine were to reject their indemnity obligations or if such obligations were found to be unenforceable, AGZ Holding may not have recourse against any third party with respect to any such liabilities, which, in turn, could have an adverse effect on our ability to receive distributions of cash from AGZ Holding.

If energy conservation and efficiency and technology trends continue to decrease demand for our energy products and services, our revenues will decrease.

Retail customers primarily use our energy products and services for home heating, water heating and cooking purposes. Energy conservation and efficiency measures and advances in heating, conservation and other devices have begun to decrease demand for our energy products. Should that decrease continue, and not be offset by colder weather, our revenues will decrease. Additionally, new technologies and alternative sources of energy may be developed that could negatively affect the competitiveness of our operating subsidiaries and therefore, our revenues.

We may be unable to respond effectively to competition, which may adversely affect our operating results.

We may be unable to timely respond to changes within the energy and utility sectors that may result from regulatory initiatives to further increase competition within our industry. Such regulatory initiatives may create opportunities for additional competitors to enter our markets, and, as a result, we may be unable to maintain our revenues or continue to pursue our current business strategy.

The loss of key personnel would have an adverse effect on our business, financial results and results of operations.

Our continued success is dependent upon the efforts and abilities of our executive officers and other key employees and our ability to continue to attract, motivate and retain highly-qualified personnel. Our ability to effectively integrate acquired businesses, including Antargaz, will also depend on the efforts and abilities of the officers or key employees we retain in those acquisitions. The loss of key personnel or the failure to attract and motivate key personnel could have an adverse effect on our business, financial condition and results of operations.

Our net income will decrease if we are required to incur additional costs to comply with existing and new governmental safety, health, transportation and environmental regulation.

We are subject to extensive and changing international, federal, state and local safety, health, transportation and environmental laws and regulations governing the storage, distribution and transportation of our energy products.

S-12

Table of Contents

New regulations, or a change in the interpretation of existing regulations, could result in increased expenditures. For example, the explosion at Grande Pariosse S.A.’s chemical factory in Toulouse, France in September 2001 gave rise to new regulations relating to the safety risks of operations such as Antargaz’s, which involve the storage of large amounts of flammable substances. In addition, for many of our operations, we are required to obtain permits from regulatory authorities. Failure to comply with these permits or applicable laws could result in civil and criminal fines or the cessation of the operations in violation.

We are investigating and remediating contamination at a number of present and former operating sites in the United States, including former sites where we or our former subsidiaries operated manufactured gas plants. We have also received claims from third parties that allege that we are responsible for costs to clean up properties where we or our former subsidiaries operated a manufactured gas plant or conducted other operations. Costs we incur to remediate sites outside of Pennsylvania cannot be recovered in future utility rate proceedings, and insurance may not cover all or even part of these costs. Our actual costs to clean up these sites may exceed our current estimates due to factors beyond our control, such as:

| • | the discovery of presently unknown conditions; |

| • | changes in environmental laws and regulations; |

| • | judicial rejection of our legal defenses to the third-party claims; or |

| • | the insolvency of other responsible parties at the sites at which we are involved. |

In addition, if we discover additional contaminated sites, we could be required to incur material costs, which would reduce our net income.

Under certain conditions, if the credit rating of UGI Utilities’ long-term debt is downgraded, FLAGA’s lenders may accelerate repayment of FLAGA’s debt, which could adversely affect our ability to pay dividends on our common stock.

FLAGA has a€15 million working capital loan commitment from a European bank expiring in November 2004. As of December 31, 2003, borrowings under this working capital facility totaled€14.4 million ($18.1 million U.S. dollar equivalent). We guarantee the debt issued under this agreement, as well as $78.0 million of acquisition and special purpose debt of FLAGA. In the event that the credit rating of UGI Utilities’ long-term debt is downgraded from A3 to Baa2 by Moody’s Investors Service and from BBB+ to BBB by Standard & Poor’s, FLAGA’s lenders may accelerate the repayment of this debt, which could require us to refinance FLAGA’s debt immediately. On January 29, 2004, Standard & Poor’s Ratings Services placed its BBB+ corporate credit and other ratings on UGI Utilities on CreditWatch with negative implications. If we were unable to refinance the debt, we could be unable to pay dividends on our common stock.

Current economic and political conditions may harm our business.

U.S. and international economic conditions and the effects of ongoing military actions against terrorists may cause significant disruptions to commerce throughout the world. To the extent that such conditions and disruptions result in delays or cancellations of customer orders, impair our ability to effectively market our energy products or services or acquire our sources of supply for our energy products, or cause or prolong an economic recession, we would have lower consolidated revenues, and, therefore, lower consolidated net income. In addition, our ability to raise capital for acquisitions, capital expenditures and ongoing operations is dependent upon ready access to capital markets. During times of adverse economic and political conditions, investor confidence in and accessibility to capital markets could decrease. If capital markets are not available to us over an extended period of time, we could be unable to make acquisitions, refinance debt, invest in capital expenditures and fund operations.

S-13

Table of Contents

Risks Related to Our Common Stock

The price of our securities may be affected by the general perception of the energy and utility sectors of the economy.

Events, such as the blackout in parts of the United States on August 14, 2003, those involving Enron Corporation, political unrest in oil-producing countries and the energy crisis in California, could adversely affect investors’ perceptions of the energy and utility sectors. A negative perception of our industry by investors could adversely affect the equity prices of companies within the energy and utility sectors. We cannot predict what news or events might affect the perceptions of investors in our industry or how such news or events might affect the market price of our common stock, but fluctuations in the market price of our common stock could be severe and any effects could be long-term.

Your ability to seek potential recoveries from our former independent public accountants, Arthur Andersen LLP, is limited.

Arthur Andersen LLP audited our financial statements and schedules as of and for the year ended September 30, 2001, which are incorporated by reference into this prospectus supplement. Arthur Andersen LLP has not reissued their report on our financial statements in this prospectus supplement, and we have relied on Rule 437a under the Securities Act in filing this registration statement without such a consent. On June 15, 2002, Arthur Andersen LLP was convicted of obstruction of justice by a federal jury in Houston, Texas in connection with Arthur Andersen LLP’s work for Enron Corporation. On September 15, 2002, a federal judge upheld this conviction. Arthur Andersen LLP ceased its audit practice before the SEC on August 31, 2002. In May 2002, we terminated our engagement of Arthur Andersen LLP as our independent accountants and engaged PricewaterhouseCoopers LLP to serve as our independent accountants for the fiscal year ending September 30, 2002. Because Arthur Andersen has not consented to the incorporation by reference of their reports on our financial statements in this prospectus and because of the circumstances affecting Arthur Andersen LLP, as a practical matter, it may not be able to satisfy any claims arising from the provision of auditing services to us, including claims you may have that are available to securities holders under federal and state securities law.

S-14

Table of Contents

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

The information in this prospectus supplement, including the information incorporated by reference into this prospectus supplement, includes “forward-looking statements” within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and Section 27A of the Securities Act as enacted by the Private Securities Litigation Reform Act of 1995. Such statements use forward-looking words such as “believe,” “plan,” “anticipate,” “continue,” “estimate,” “expect,” “may,” “will,” or other similar words. These statements discuss plans, strategies, events or developments that we expect or anticipate will or may occur in the future.

A forward-looking statement may include a statement of the assumptions or bases underlying the forward-looking statement. We believe that we have chosen these assumptions or bases in good faith and that they are reasonable. However, we caution you that actual results almost always vary from assumed facts or bases, and the differences between actual results and assumed facts or bases can be material, depending on the circumstances. When considering forward-looking statements, you should keep in mind the following important factors which could affect our future results and could cause those results to differ materially from those expressed in our forward-looking statements:

| • | adverse weather conditions resulting in reduced demand; |

| • | price volatility and availability of propane, fuel oil, electricity and natural gas and the capacity to transport them to our market areas; |

| • | changes in laws and regulations, including safety, tax, competition, environmental and accounting matters; |

| • | competitive pressures from the same and alternative energy sources; |

| • | failure to acquire new customers, thereby reducing or limiting any increase in revenues; |

| • | liability for environmental claims; |

| • | customer conservation measures and improvements in energy efficiency and technology resulting in reduced demand; |

| • | adverse labor relations; |

| • | large customer, counterparty or supplier defaults; |

| • | liability for personal injury and property damage arising from explosions and other catastrophic events, including acts of terrorism, resulting from operating hazards and risks incidental to generating and distributing electricity and transporting, storing and distributing natural gas and propane, including liability in excess of insurance coverage; |

| • | political, regulatory and economic conditions in the United States and in foreign countries; |

| • | interest rate fluctuations and other capital market conditions, including foreign currency rate fluctuations; |

| • | reduced distributions or dividends from subsidiaries; |

| • | the timing of the completion of our proposed acquisition of the ownership interests that we do not already own in AGZ Holding; and |

| • | the timing and success of our efforts to develop new business opportunities. |

These factors are not necessarily all of the important factors that could cause actual results to differ materially from those expressed in any of our forward-looking statements. Other unknown or unpredictable factors could also have material adverse effects on future results. We undertake no obligation to update publicly any forward-looking statement whether as a result of new information or future events except as required by federal securities laws.

S-15

Table of Contents

Our net proceeds from the sale of the 7,500,000 shares of common stock will be approximately $229.1 million, or approximately $263.6 million if the underwriters exercise their over-allotment option in full, based on a price to the public of $32.10 per share and after deducting the underwriting discount and the estimated offering expenses payable by us.

We intend to use all of the net proceeds from this offering to acquire the ownership interests in AGZ Holding, the parent holding company of Antargaz, that we do not already own. You should refer to the section in this prospectus supplement entitled “Who We Are — Planned Acquisition of Antargaz,” for a description of that transaction. To the extent any proceeds remain after paying the purchase price for the ownership interests in AGZ Holding that we do not already own or such transaction is not completed, we will use the proceeds for general corporate purposes.

We paid quarterly dividends on our common stock as set forth in the following table. On January 27, 2004, we announced our intention to increase the annual dividend rate on our common stock to $1.25 per share from $1.14 per share effective with the regularly scheduled July dividend payment, assuming the completion of the anticipated acquisition of the shares in AGZ Holding that we do not already own.

| Amount* | |||

2004 Fiscal Year | |||

Second Quarter | $ | 0.285 | |

First Quarter | 0.285 | ||

2003 Fiscal Year | |||

Fourth Quarter | $ | 0.285 | |

Third Quarter | 0.285 | ||

Second Quarter | 0.275 | ||

First Quarter | 0.275 | ||

2002 Fiscal Year | |||

Fourth Quarter | $ | 0.275 | |

Third Quarter | 0.267 | ||

Second Quarter | 0.267 | ||

First Quarter | 0.267 | ||

| * | On January 28, 2003, our Board of Directors approved a 3-for-2 split of our common stock, effective April 1, 2003. Dividends paid are reflected on a post-split basis. |

S-16

Table of Contents

PRICE RANGE OF OUR COMMON STOCK

Our common stock is traded on the New York and Philadelphia stock exchanges under the symbol “UGI.” The following table sets forth, for the periods indicated, the high and low sales prices for our common stock on The New York Stock Exchange Composite Transactions tape as reported in The Wall Street Journal.

| High* | Low* | |||||

2004 Fiscal Year | ||||||

Second Quarter (through March 18, 2004) | $ | 34.35 | $ | 31.40 | ||

First Quarter | 34.20 | 28.85 | ||||

2003 Fiscal Year | ||||||

Fourth Quarter | $ | 33.45 | $ | 28.86 | ||

Third Quarter | 35.05 | 29.00 | ||||

Second Quarter | 30.57 | 24.93 | ||||

First Quarter | 26.99 | 23.27 | ||||

2002 Fiscal Year | ||||||

Fourth Quarter | $ | 24.51 | $ | 17.11 | ||

Third Quarter | 22.14 | 19.60 | ||||

Second Quarter | 20.99 | 18.06 | ||||

First Quarter | 21.02 | 17.79 | ||||

| * | On January 28, 2003, our Board of Directors approved a 3-for-2 split of our common stock, effective April 1, 2003. Sales prices for the periods presented are reflected on a post-split basis. |

S-17

Table of Contents

The following table shows our capitalization as of December 31, 2003, (i) on an actual basis and (ii) on a pro forma and as adjusted basis giving effect to the consummation of the acquisition of the ownership interests in AGZ Holding that we do not already own and the sale of 7,500,000 shares of our common stock in this offering (assuming no exercise of the underwriters’ over-allotment option). You should read this table in conjunction with our financial statements and the notes to those financial statements incorporated by reference into this prospectus supplement and the Unaudited Pro Forma Condensed Combined Financial Statements beginning on page P-1.

| December 31, 2003 | ||||||||

| Actual | Pro Forma and As Adjusted | |||||||

| (in millions) | ||||||||

Cash, cash equivalents and short-term investments (a) | $ | 193.5 | $ | 157.0 | ||||

Total debt | $ | 1,353.2 | $ | 1,863.8 | (b) | |||

Minority interests | $ | 149.8 | $ | 164.9 | ||||

UGI Utilities preferred shares subject to mandatory redemption, without par value | $ | 20.0 | $ | 20.0 | ||||

Total common stockholders’ equity | ||||||||

Common Stock, without par value; 150,000,000 shares authorized; 42,778,798 outstanding as of December 31, 2003; and 50,278,798 outstanding as adjusted | $ | 582.9 | $ | 813.1 | ||||

Retained earnings | 117.5 | 117.5 | ||||||

Accumulated other comprehensive income | 15.6 | 15.6 | ||||||

Notes receivable from employees | (0.4 | ) | (0.4 | ) | ||||

Less treasury stock, at cost | (107.0 | ) | (107.0 | ) | ||||

Total common stockholders’ equity | 608.6 | 838.8 | ||||||

Total capitalization | $ | 2,131.6 | $ | 2,887.5 | ||||

| (a) | $23.3 million of which is held by AmeriGas Partners, L.P., which currently makes distributions pursuant to the terms of its partnership agreement. |

| (b) | Includes €165 million aggregate principal amount of AGZ Notes, reflected at fair market value on December 31, 2003. |

The number of shares of common stock to be outstanding after this offering is based on 42,778,798 shares outstanding as of December 31, 2003, and excludes:

| • | 2,950,288 shares of common stock underlying options as of March 1, 2004, at an average option exercise price of $21.877 per share; |

| • | a maximum of 507,854 shares of common stock that may be issued pursuant to grants of phantom units as of March 1, 2004; and |

| • | 2,712,096 shares available for future grants under all equity compensation plans as of March 1, 2004. |

S-18

Table of Contents

CERTAIN UNITED STATES FEDERAL TAX CONSEQUENCES TO NON-U.S. HOLDERS

This discussion describes the material United States federal income and estate tax consequences of the ownership and disposition of shares of our common stock by a non-U.S. holder. When we refer to a non-U.S. holder, we mean a beneficial owner of our common stock that, for U.S. federal income tax purposes, is other than:

| • | a citizen or resident of the United States; |

| • | a corporation (including for this purpose any other entity treated as a corporation for U.S. federal income tax purposes) created or organized in or under the laws of the United States or any political subdivision thereof; |

| • | an estate the income of which is subject to U.S. federal income taxation regardless of its source; or |

| • | a trust that is subject to the primary supervision of a U.S. court and to the control of one or more U.S. persons, or that has a valid election in effect under applicable U.S. Treasury regulations to be treated as a U.S. person. |

If a partnership (including for this purpose any other entity, either organized within or without the United States, treated as a partnership for U.S. federal income tax purposes) holds the shares, the tax treatment of a partner as a beneficial owner of the shares generally will depend upon the status of the partner and the activities of the partnership. Foreign partnerships also generally are subject to special U.S. tax documentation requirements.

This discussion does not consider the specific facts and circumstances that may be relevant to a particular non-U.S. holder and does not address the treatment of a non-U.S. holder under the laws of any state, local or foreign taxing jurisdiction. This section is based on the tax laws of the United States, including the Internal Revenue Code of 1986, as amended, which we refer to as the Code, existing and proposed regulations, and administrative and judicial interpretations, all as currently in effect. These laws are subject to change, possibly on a retroactive basis. You should consult a tax advisor regarding the U.S. federal tax consequences of acquiring, holding and disposing of our common stock in your particular circumstances, as well as any tax consequences that may arise under the laws of any state, local or foreign taxing jurisdiction.

Dividends

We pay dividends with respect to our common stock. Dividends paid to a non-U.S. holder, except as described below, are subject to withholding of U.S. federal income tax at a 30% rate or at a lower rate if the holder is eligible for the benefits of an income tax treaty that provides for a lower rate (and you have furnished to us a valid Internal Revenue Service Form W-8BEN or an acceptable substitute form).

If dividends paid to a non-U.S. holder are “effectively connected” with your conduct of a trade or business within the United States, and, if required by a tax treaty, the dividends are attributable to a permanent establishment that the non-U.S. holder maintains in the United States, we generally are not required to withhold tax from the dividends, provided that the non-U.S. holder has furnished to us a valid Internal Revenue Service Form W-8ECI or an acceptable substitute form. Instead, “effectively connected” dividends are taxed at rates applicable to United States persons. If a non-U.S. holder is a corporation, “effectively connected” dividends that it receives may, under certain circumstances, be subject to an additional “branch profits tax” at a 30% rate or at a lower rate if the holder is eligible for the benefits of an income tax treaty that provides for a lower rate.

S-19

Table of Contents

Gain on Disposition of Common Stock

Non-U.S. holders generally will not be subject to United States federal income tax on gain that they recognize on a disposition of our common stock unless:

| • | the holder is an individual who is present in the United States for 183 days or more in the taxable year of disposition and certain other conditions are met; |

| • | such gain is effectively connected with the holder’s conduct of a trade or business within the United States and, if certain tax treaties apply, is attributable to a U.S. permanent establishment maintained by the holder; |

| • | the holder is subject to the Code provisions applicable to certain U.S. expatriates; or |

| • | we are or have been a “U.S. real property holding corporation” for U.S. federal income tax purposes and, assuming that our common stock is deemed to be “regularly traded on an established securities market,” the holder held, directly or indirectly at any time during the five-year period ending on the date of disposition or such shorter period that such shares were held, more than five percent of our common stock. We have not been, are not and do not anticipate becoming, a United States real property holding corporation for United States federal income tax purposes. |

Federal Estate Taxes

If our common stock is held by a non-U.S. holder at the time of death, such stock will be included in the holder’s gross estate for U.S. federal estate tax purposes, unless an applicable estate tax treaty provides otherwise.

Backup Withholding and Information Reporting

Backup withholding and information reporting requirements will not apply to dividends paid on our common stock to a non-U.S. holder, provided the non-U.S. holder provides a valid Internal Revenue Service Form W-8BEN (or satisfies certain documentary evidence requirements for establishing that such holder is a non-U.S. person) or otherwise establishes an exemption. Information reporting and backup withholding also generally will not apply to a payment of the proceeds of a sale of common stock effected outside the United States by a foreign office of a foreign broker.

However, a sale of our common stock will be subject to information reporting if it is effected at a foreign office of a broker that is:

| • | a U.S. person; |

| • | a controlled foreign corporation for U.S. tax purposes; |

| • | a foreign person 50% or more of whose gross income is effectively connected with the conduct of a U.S. trade or business for a specified three-year period; or |

| • | a foreign partnership, if at any time during its tax year one or more of its partners are “U.S. persons,” as defined in U.S. Treasury regulations, who in the aggregate hold more than 50% of the income or capital interest in the partnership, or such foreign partnership is engaged in the conduct of a U.S. trade or business; |

unless the documentation requirements described above are met or you otherwise establish an exemption and the broker does not have actual knowledge or reason to know that you are a United States person. Backup withholding will apply if the sale is subject to information reporting and the broker has actual knowledge that the holder is a U.S. person.

A non-U.S. holder generally may obtain a refund of any amounts withheld under the backup withholding rules that exceed its income tax liability by filing a refund claim with the Internal Revenue Service.

S-20

Table of Contents

UNDERWRITING

Under the terms and subject to the conditions contained in an underwriting agreement dated March 18, 2004, we have agreed to sell to the underwriters named below, for whom Credit Suisse First Boston (Europe) Limited is acting as representative, the following respective numbers of shares of common stock:

| Underwriter | Number of Shares | |

Credit Suisse First Boston (Europe) Limited | 4,500,000 | |

Citigroup Global Markets Inc. | 1,875,000 | |

Wachovia Capital Markets, LLC | 750,000 | |

Janney Montgomery Scott LLC | 375,000 | |

Total | 7,500,000 | |

Credit Suisse First Boston (Europe) Limited will make offers and sales in the United States through Credit Suisse First Boston LLC, which is acting as selling agent for Credit Suisse First Boston (Europe) Limited.

The underwriting agreement provides that the underwriters are obligated to purchase all the shares of common stock in the offering if any are purchased, other than those shares covered by the over-allotment option described below. The underwriting agreement also provides that if an underwriter defaults, the purchase commitments of non-defaulting underwriters may be increased or the offering may be terminated.

We have granted to the underwriters a 30-day option to purchase on a pro rata basis up to 1,125,000 additional shares at the initial public offering price less the underwriting discounts and commissions. The option may be exercised only to cover any over-allotments of common stock.

The underwriters propose to offer the shares of common stock initially at the public offering price on the cover page of this prospectus and to selling group members at that price less a selling concession of $0.8426 per share. The underwriters and selling group members may allow a discount of $0.100 per share on sales to other broker/dealers. After the initial public offering the representatives may change the public offering price and concession and discount to broker/dealers.

The following table summarizes the compensation and estimated expenses we will pay:

| Per Share | Total | |||||||||||

| Without Over-allotment | With Over-allotment | Without Over-allotment | With Over-allotment | |||||||||

Underwriting discounts and commissions paid by us | $ | 1.4044 | $ | 1.4044 | $ | 10,533,000 | $ | 12,112,950 | ||||

Expenses payable by us | $ | 0.1467 | $ | 0.1275 | $ | 1,100,000 | $ | 1,100,000 | ||||

We have agreed that we will not offer, sell, contract to sell, pledge or otherwise dispose of, directly or indirectly, or file with the SEC a registration statement under the Securities Act relating to, any shares of our common stock or securities convertible into or exchangeable or exercisable for any shares of our common stock, or publicly disclose the intention to make any offer, sale, pledge, disposition or filing, without the prior written consent of Credit Suisse First Boston (Europe) Limited for a period of 90 days after the date of this prospectus supplement (other than shares of our common stock or options to acquire shares of our common stock issued pursuant to our equity compensation and savings plans, shares of our common stock issued pursuant to our dividend reinvestment plan, shares of our common stock issued in connection with options or warrants outstanding as of the date of this prospectus supplement or shares of our common stock issued as consideration for any acquisition).

Our executive officers have agreed that they will not offer, sell, contract to sell, pledge or otherwise dispose of, directly or indirectly, any shares of our common stock or securities convertible into or exchangeable or exercisable for any shares of our common stock, enter into a transaction that would have the same effect, or enter into any swap, hedge or other arrangement that transfers, in whole or in part, any of the economic consequences

S-21

Table of Contents

of ownership of our common stock, whether any of these transactions are to be settled by delivery of our common stock or other securities, in cash or otherwise, or publicly disclose the intention to make any offer, sale, pledge or disposition, or to enter into any transaction, swap, hedge or other arrangement, without, in each case, the prior written consent of Credit Suisse First Boston (Europe) Limited for a period of 45 days after the date of this prospectus supplement.

We have agreed to indemnify the underwriters against liabilities under the Securities Act, or to contribute to payments which the underwriters may be required to make in that respect.

Our common stock is listed on the New York Stock Exchange and the Philadelphia Stock Exchange under the symbol “UGI”.

In connection with the offering, the underwriters may engage in stabilizing transactions, over-allotment transactions, syndicate covering transactions and penalty bids in accordance with Regulation M under the Securities Exchange Act of 1934.

| • | Stabilizing transactions permit bids to purchase the underlying security so long as the stabilizing bids do not exceed a specified maximum. |

| • | Over-allotment involves sales by the underwriters of shares in excess of the number of shares the underwriters are obligated to purchase, which creates a syndicate short position. The short position may be either a covered short position or a naked short position. In a covered short position, the number of shares over-allotted by the underwriters is not greater than the number of shares that they may purchase in the over-allotment option. In a naked short position, the number of shares involved is greater than the number of shares in the over-allotment option. The underwriters may close out any short position by either exercising their over-allotment option and/or purchasing shares in the open market. |

| • | Syndicate covering transactions involve purchases of the common stock in the open market after the distribution has been completed in order to cover syndicate short positions. In determining the source of shares to close out the short position, the underwriters will consider, among other things, the price of shares available for purchase in the open market as compared to the price at which they may purchase shares through the over-allotment option. If the underwriters sell more shares than could be covered by the over-allotment option, a naked short position, the position can only be closed out by buying shares in the open market. A naked short position is more likely to be created if the underwriters are concerned that there could be downward pressure on the price of the shares in the open market after pricing that could adversely affect investors who purchase in the offering. |

| • | Penalty bids permit the representatives to reclaim a selling concession from a syndicate member when the common stock originally sold by the syndicate member is purchased in a stabilizing or syndicate covering transaction to cover syndicate short positions. |

These stabilizing transactions, syndicate covering transactions and penalty bids may have the effect of raising or maintaining the market price of our common stock or preventing or retarding a decline in the market price of the common stock. As a result, the price of our common stock may be higher than the price that might otherwise exist in the open market. These transactions may be effected on the New York Stock Exchange or otherwise and, if commenced, may be discontinued at any time.

In the ordinary course of business, certain of the underwriters and their affiliates have provided and may in the future provide financial advisory, investment banking and general financing and banking services for us and our affiliates for customary fees.

A prospectus in electronic format may be made available on the websites maintained by one or more of the underwriters or selling group members, if any, participating in this offering. The representatives may agree to allocate a number of shares to underwriters and selling group members for sale to their online brokerage account holders. Internet distributions will be allocated by the underwriters and selling group members that will make internet distributions on the same basis as other allocations.

S-22

Table of Contents

WHERE YOU CAN FIND MORE INFORMATION

We file annual, quarterly and current reports, proxy statements and other information with the SEC. You may read and copy any document we file with the SEC at the SEC’s public reference room at 450 Fifth Street, N.W., Washington, D.C. 20549. Please call the SEC at 1-800-SEC-0330 for further information on the public reference room. The SEC maintains a website at http://www.sec.gov that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC. In addition, we maintain a website at http://www.ugicorp.com and make available free of charge on this website our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC. The information on our website, other than the documents incorporated by reference into this prospectus supplement pursuant to the section entitled “Incorporation of Certain Documents By Reference” below, is not incorporated into, and does not constitute a part of, this prospectus supplement.

INCORPORATION OF CERTAIN DOCUMENTS BY REFERENCE

The SEC allows us to “incorporate by reference” the information we file with them, which means that we can disclose important information to you by referring you to those documents. Statements made in this prospectus supplement as to the contents of any contract, agreement or other documents are not necessarily complete, and, in each instance, we refer you to a copy of such document filed as an exhibit to the registration statement, of which this prospectus supplement is a part, or otherwise filed with the SEC. The information incorporated by reference is considered to be part of this prospectus supplement. When we file information with the SEC in the future, that information will automatically update and supersede this information. We incorporate by reference herein our documents listed below and any future filings we make with the SEC under Sections 13(a), 13(c), 14 or 15(d) of the Exchange Act until all of the shares of common stock that we have registered are sold (other than Current Reports on Form 8-K containing disclosure furnished under Item 9 or Item 12 of Form 8-K and exhibits relating to such disclosures, unless otherwise specifically stated in any such Current Report or Form 8-K):

| • | our annual report on Form 10-K for the fiscal year ended September 30, 2003, filed on December 23, 2003, except to the extent superseded by the current report on Form 8-K filed on March 11, 2004; |

| • | our quarterly report on Form 10-Q for the fiscal quarter ended December 31, 2003, filed on February 13, 2004; |

| • | our current report on Form 8-K filed on March 11, 2004; and |

| • | the description of our common stock contained in our registration statement on Form 8-B, dated March 23, 1992, as amended by Amendment No. 1 to Form 8-B, dated April 10, 1992, and on Form 8-A, dated June 24, 1996, and any amendments or reports filed after the date hereof for the purpose of updating such description. |

We will provide, upon written or oral request, to each person to whom a prospectus supplement is delivered, a copy of any or all of the information that has been incorporated by reference into the prospectus supplement but not delivered with the prospectus supplement. You may request a copy of these filings, at no cost, by writing us at UGI Corporation, 460 North Gulph Road, King of Prussia, Pennsylvania 19406, Attention: Vice President and Treasurer. Our telephone number is (610) 337-1000.

The validity of the shares of common stock offered hereby will be passed upon for us by Morgan, Lewis & Bockius LLP. The underwriters have been represented by Cravath, Swaine & Moore LLP, New York, N.Y.

S-23

Table of Contents

The audited consolidated financial statements incorporated into this prospectus supplement by reference to the current report on Form 8-K dated March 11, 2004 have been so incorporated in reliance on the report of PricewaterhouseCoopers LLP, independent accountants, given on the authority of said firm as experts in auditing and accounting.

The consolidated financial statements of AGZ Holding at March 31, 2003 and for the year then ended, appearing in this prospectus supplement have been audited by PricewaterhouseCoopers Audit and Barbier Frinault & Autres, Ernst & Young, independent auditors, as set forth in their report thereon appearing elsewhere herein, and are included in reliance upon such report given on the authority of such firms as experts in accounting and auditing.

The audited consolidated financial statements and schedules for the period ended September 30, 2001, which are incorporated by reference in this prospectus supplement, were audited by Arthur Andersen LLP, our former independent accountants, as indicated in their reports with respect thereto. Copies of such reports are incorporated by reference herein, but Arthur Andersen LLP has not reissued such reports or consents to the incorporation of such reports into this prospectus supplement and has ceased operations.

S-24

Table of Contents

INDEX TO FINANCIAL STATEMENTS