UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

| |

☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2024

or

| |

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission File Number: 000-19961

ORTHOFIX MEDICAL INC.

(Exact name of registrant as specified in its charter)

| | |

Delaware |

| 98-1340767 |

(State or other jurisdiction of incorporation or organization) |

| (I.R.S. Employer Identification No.) |

| |

3451 Plano Parkway, Lewisville, Texas |

| 75056 |

(Address of principal executive offices) |

| (Zip Code) |

(214) 937-2000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| | | | |

Common Stock, $0.10 par value |

| OFIX | | Nasdaq Global Select Market |

(Title of Class) |

| (Trading Symbol) | | (Name of Exchange on Which Registered) |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | |

Large accelerated filer |

| ☐ |

| Accelerated filer |

| ☒ | | Emerging Growth Company | | ☐ |

Non-accelerated filer |

| ☐ |

| Smaller reporting company |

| ☐ | | | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. §7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The aggregate market value of registrant’s common stock held by non-affiliates, based upon the closing price of the common stock on the last business day of the fiscal quarter ended June 30, 2024, as reported by the Nasdaq Global Select Market, was approximately $504.4 million.

As of February 21, 2025, 39,022,492 shares of common stock were issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Certain sections of the registrant’s definitive proxy statement to be filed with the Commission in connection with the Orthofix Medical Inc. 2025 Annual Meeting of Shareholders are incorporated by reference in Part III of this Annual Report.

Orthofix Medical Inc.

Form 10-K for the Year Ended December 31, 2024

Table of Contents

Forward-Looking Statements

This Annual Report contains forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended ("the Exchange Act"), and Section 27A of the Securities Act of 1933, as amended, relating to our business and financial outlook, which are based on our current beliefs, assumptions, expectations, estimates, forecasts, and projections. In some cases, you can identify forward-looking statements by terminology such as "may," "will," "should," "expects," "plans," "anticipates," "believes," "estimates," "projects," "intends," "predicts," "potential," "continue," or other comparable terminology. Forward-looking statements include, but are not limited to, statements about:

•our intentions, beliefs, and expectations regarding our operations, sales, expenses, and future financial performance;

•our intentions, beliefs, and expectations regarding the anticipated benefits of the merger with SeaSpine Holdings Corporation ("SeaSpine"), including the anticipated cross-selling opportunities from the merger;

•our plans for future products and enhancements of existing products;

•anticipated growth and trends in our business;

•the timing of and our ability to maintain and obtain regulatory clearances or approvals;

•our belief that our cash and cash equivalents, investments, and access to our credit facilities will be sufficient to satisfy our anticipated cash requirements;

•our expectations regarding our revenues, customers, and distributors;

•our expectations regarding our costs, suppliers, and manufacturing abilities;

•our beliefs and expectations regarding our market penetration and expansion efforts;

•our anticipated trends and challenges in the markets in which we operate; and

•our expectations and beliefs regarding and the impact of investigations, claims, and litigation.

These forward-looking statements are not guarantees of future performance and involve risks, uncertainties, estimates, and assumptions that are difficult to predict. Any or all forward-looking statements that we make may turn out to be wrong (due to inaccurate assumptions that we make or otherwise) and our actual outcomes and results may differ materially from those expressed in these forward-looking statements. Potential risks and uncertainties that could cause actual results to differ materially include, but are not limited to, those set forth in Part I, Item 1A under the heading "Risk Factors", Part II, Item 7 "Management’s Discussion and Analysis of Financial Condition and Results of Operations" and elsewhere throughout this Annual Report and in any other documents incorporated by reference to this Annual Report. You should not place undue reliance on any of these forward-looking statements. Further, any forward-looking statement speaks only as of the date hereof, unless it is specifically otherwise stated to be made as of a different date. We undertake no obligation to update, and expressly disclaim any duty to update, our forward-looking statements, whether as a result of circumstances or events that arise after the date hereof, new information, or otherwise.

Summary of Risk Factors

The section provides a summary of many of the risks we are exposed to in the normal course of our business activities. The summary does not contain all of the information that may be important to you, and you should read the summary together with the more detailed discussion of risks set forth following this section as well as elsewhere in this report.

•Integration of the SeaSpine business is still ongoing. We may not be able to successfully complete remaining integration activities and/or realize all anticipated benefits of the merger.

•We are subject to a wide range of requirements, regulations, and laws due to our international operations and related to the medical device industry in which we operate, the violation of any of which could subject us to adverse consequences.

•Ongoing healthcare reform initiatives and changes in third-party reimbursement policies and in the healthcare industry aimed at cost containment may adversely impact our business.

•We and certain of our suppliers are subject to extensive government regulation that increases our costs and could limit our ability to market or sell our products.

•Oversight of the medical device industry might affect the way we sell medical devices and compete in the marketplace.

•A FDA panel recommended that bone growth stimulator devices be reclassified by the FDA from Class III to Class II devices, which could increase future competition for us in this product category and negatively affect our future sales of such products.

•We are subject to requirements relating to hazardous materials which may impose significant compliance or other costs on us.

•Pandemics, wars and armed conflicts, terrorist attacks, and other such global events, and the related effects thereof, could materially adversely affect, our operations, supply chain, manufacturing, product demand, product distribution, customers, and other business activities.

•Our business may be adversely affected if consolidation in the healthcare industry leads to demand for price concessions or if a group purchasing organization ("GPO") or similar entity excludes us from being a supplier.

•The industry in which we operate is highly competitive. New product developments and improvements by our competitors could make our products or technologies non-competitive or obsolete. Similarly, unless clinical studies demonstrate the safety and efficacy of our products, alone and relative to competitive products, our sales may be adversely affected.

•Our ability to market products successfully depends, in part, upon the acceptance of the products not only by consumers, but also by independent third parties, including physicians, hospitals, and third-party payors.

•Clinical development is a lengthy and expensive process with an inherently uncertain outcome. Failure to successfully complete clinical trials and obtain regulatory approval for our product candidates within our anticipated timelines at reasonable costs to us, or at all, could have a material adverse effect on our business, operating results, and financial condition.

•If the third parties on which we rely to conduct our clinical studies do not perform as contractually required or expected, we may not obtain required approvals for or commercialize our products.

•Unfavorable negative publicity concerning both alleged improper methods of tissue recovery from donors and disease transmission from donated tissue could limit widespread acceptance of some of our products.

•We may not be able to successfully introduce new products to the market and, if we do, market acceptance or the market size for our products may not be as we expect.

•There is no guarantee that regulatory authorities, U.S. or foreign, will grant clearance or premarket approval of our future products, or that we will be able to maintain such clearances or approvals for current products.

•Our success depends on our ability to successfully educate and train surgeons and their staff on the benefits, safety, cost-effectiveness, and proper use of our products.

•Security breaches, cyber-attacks, loss of data, misappropriation of PHI or personal identifiable information ("PII"), and other disruptions to our information technology systems could compromise sensitive information and/or adversely affect our business.

•Our business could be harmed if any of our manufacturing, development, or research facilities are damaged and/or our manufacturing processes are interrupted, including as the result of natural disasters and other catastrophic events outside our control.

•We depend on a limited number of third-party manufacturers and suppliers for manufacturing and processing activities, components, and raw materials. Failure of these third parties to perform as expected could result in substantial delays, increased costs or failures of our product development programs, or delayed or unsuccessful commercialization of our products.

•We may not maintain or grow our revenue if we are unable to maintain and expand our network of independent sales representatives and distributors.

•Our success depends on the services of key members of our senior management and other key employees.

•Our business is subject to economic, political, regulatory, and other risks associated with international sales and operations.

•Our failure to adequately protect or enforce our intellectual property rights could harm our position in the marketplace or prevent or impede the commercial protection of our products.

•We may be subject to third party claims and litigation for infringement or misappropriation of their intellectual property, which are inherently costly, divert significant time and other resources, and have unpredictable outcomes.

•We may have significant product or other liability exposure, some of which may not be covered by insurance, and if covered by insurance, such coverage may not cover all claims, which could require us to pay substantial sums.

•Ongoing litigation and arbitration matters could negatively affect our business operations.

•Our efforts to identify, pursue, and implement new business opportunities (including acquisitions) may be unsuccessful.

•Our sales volumes and our operating results may fluctuate.

•Our goodwill, intangible assets, and fixed assets are subject to potential impairment which could adversely affect our future financial results.

•We maintain a $275.0 million credit agreement secured by a pledge of substantially all of our property. Our failure to comply with the facility’s covenants could result in an event of default, which could adversely affect our future.

•We must maintain high levels of inventory, which could consume a significant amount of our resources and reduce our cash flows.

•Our future capital needs are uncertain and we may need to raise additional funds in the future, and such funds may not be available on acceptable terms or at all.

•Our business could be negatively impacted by corporate citizenship and environmental, social, and governance ("ESG") matters and/or our reporting of such matters.

Trademarks

Solely for convenience, our trademarks and trade names in this Annual Report are referred to without the ® and ™ symbols, but such references should not be construed as any indicator that we will not assert, to the fullest extent under applicable law, our rights thereto.

PART I

Item 1. Business

In this Annual Report, the terms "we," "us," "our," "Orthofix," and "the Company" refer to the combined operations of Orthofix Medical Inc. and its consolidated subsidiaries and affiliates, unless the context requires otherwise.

Company Overview

Orthofix is a global medical technology company headquartered in Lewisville, Texas. By providing medical technologies that heal musculoskeletal pathologies, we deliver exceptional experiences and life-changing solutions to patients around the world. Orthofix offers a comprehensive portfolio of spinal hardware, bone growth therapies, specialized orthopedic solutions, biologics, and enabling technologies, including the 7D FLASH navigation system.

The Company was founded in Verona, Italy in 1980 and formally incorporated in 1987 in Curaçao as "Orthofix International N.V." In 2018, we completed a change in our jurisdiction of organization from Curaçao to the State of Delaware (the "Domestication") and changed our name to "Orthofix Medical Inc." As a result, we are a corporation existing under the laws of the State of Delaware.

In January 2023 we completed a "merger of equals" transaction with SeaSpine whereby SeaSpine became a wholly owned subsidiary of the Company via an all-stock merger (the "Merger"). As a result of the Merger, each share of SeaSpine common stock issued and outstanding immediately prior to the closing of the Merger was converted into 0.4163 shares of Orthofix common stock. The shares of common stock of Orthofix, as the corporate parent entity in the combined company structure, continue following the Merger to trade on NASDAQ under the symbol "OFIX".

Available Information and Orthofix Website

Our filings with the Securities and Exchange Commission ("SEC"), including our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, Proxy Statements for Meetings of Shareholders, registration statements, and amendments to those reports, are available free of charge on our website as soon as reasonably practicable after they are filed with, or furnished to, the SEC. Information contained on our website or connected to our website is not incorporated by reference into this Annual Report. Our website is located at www.orthofix.com. Our SEC filings are also available on the SEC website at www.sec.gov.

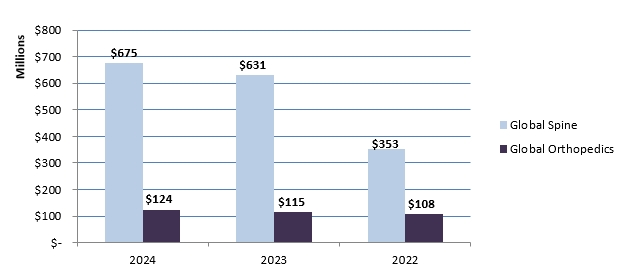

Business Segments

Orthofix manages the business by two reporting segments, Global Spine and Global Orthopedics, which accounted for 84% and 16% of our total net sales in 2024, respectively. The chart below presents reported net sales, which includes product sales and marketing service fees, by reporting segment for each of the years ended December 31, 2024, 2023, and 2022.

Financial information regarding our reportable business segments and certain geographic information is included in Part II, Item 7 of this Annual Report under the heading "Management’s Discussion and Analysis of Financial Condition and Results of Operations," and Note 16 of the Notes to the Consolidated Financial Statements in Item 8 of this Annual Report.

Global Spine

Within the Global Spine segment, we provide implantable medical devices, biologics, enabling technologies, and other regenerative solutions which aim to restore the quality of life of patients suffering from diseases and traumas of the spine. We offer a variety of treatment solutions that uniquely incorporate multiple treatment modalities, such as mechanical, biological, and electromagnetic modes, to achieve desired clinical outcomes.

Global Spine Strategy

Our strategy for the Global Spine segment is to drive business growth through organic and inorganic innovation, physician collaboration, and partnerships with dedicated and high-performing commercial sales channels. Growth initiatives include:

•A regular cadence of new and differentiated product launches supporting our spine implant and enabling technologies, biologics, and bone growth therapies portfolios;

•Ongoing, global sales channel optimization and expansion;

•Reinforcement of our bone growth stimulation business through the collection and dissemination of clinical evidence, and the delivery of new and novel value-added services;

•Conducting clinical research to support and broaden our spine implant, biologics, and bone growth stimulation portfolios;

•Acquiring or licensing products, technologies, and companies to further expand and enhance our spine portfolio;

•Investing in the further development of our pre-clinical and clinical programs designed to generate peer-reviewed scientific evidence in support of our products; and

•Attracting, developing, and retaining key talent.

Global Spine Principal Products

The Global Spine reporting segment is largely represented by two principal product categories, (i) Bone Growth Therapies and (ii) Spinal Implants, Biologics, and Enabling Technologies. Each of these product categories, and their significant components, are further described below.

Bone Growth Therapies

Within the Bone Growth Therapies product category, we manufacture, distribute, and provide support services for market-leading bone growth stimulation devices that enhance bone fusion. These Class III medical devices are indicated as an adjunctive, noninvasive treatment to improve fusion success rates in the cervical and lumbar spine as well as a therapeutic treatment for non-spinal, appendicular fractures, treating both fresh fractures or fractures that have not healed ("nonunions"). Several devices in our portfolio utilize our patented pulsed electromagnetic field ("PEMF") technology, the safety and efficacy of which is supported by basic mechanism of action data in the scientific literature, as well as published data from level one randomized controlled clinical trials. A new addition to our stimulation portfolio utilizes our low intensity pulsed ultrasound ("LIPUS"), a technology also supported by strong basic science and published clinical literature. Orthofix is the only manufacturer which offers both PEMF and LIPUS technologies. We sell these products almost exclusively in the United States ("U.S."), using distributors and direct sales representatives to provide our devices to healthcare providers and their patients.

Spinal Implants

Within Spinal Implants, we design, develop, and market a portfolio of spine fixation implant products for broad spectrum use throughout the entire spinal column. Such products are typically used to facilitate fusion in degenerative, minimally invasive, and complex spinal deformity procedures throughout the lumbar, thoracic, sacral, and cervical regions of the spine. We distribute these products globally through a network of distributors and sales representatives to sell spine products to facilities that conduct spine care, including hospitals, ambulatory surgery centers ("ASC"), and out-patient hospitals.

Enabling Technologies

Within Enabling Technologies, we design, develop, and market a portfolio of navigation technologies including tracked surgical tools, intelligent software and imaging equipment based on Machine-Vision and optical innovations. Specifically, our 7D FLASH

Navigation System has redefined image guided surgery, delivering a navigation platform with meaningful benefits in spine and cranial procedures. The speed, accuracy, workflow efficiency, and intraoperative radiation-free safety profile of the 7D FLASH Navigation System delivers significant economic value, while eliminating the long-standing frustrations and challenges of traditional image guided navigation systems. We distribute these products globally through a network of direct sales representatives and distributors to facilitate pediatric, adolescent, and adult procedures in hospitals, ASCs, and out-patient facilities.

Biologics

Within the Biologics product category, we offer a portfolio of bone graft substitutes intended to address the key elements of bone regeneration that allow physicians to successfully treat a variety of spinal, orthopedic, and dental conditions. Our Biologics portfolio includes fiber-based and particulate demineralized bone matrices ("DBMs"), cellular bone allografts, collagen ceramic matrices, and synthetic bone void fillers in various forms with supporting graft delivery solutions to address a wide range of clinical applications. Distributed globally through a network of distributors and sales representatives, our portfolio is a mix of internally manufactured tissues and products as well as marketed tissue forms provided by MTF Biologics. The breadth of the product offering and data-supported product lines position us with greater access to facilities, including group purchasing organizations ("GPOs")/integrated delivery networks ("IDNs"), hospitals, and ASCs.

The following table and discussion identify our principal Global Spine products by trade name and describe their primary applications:

| | |

Bone Growth Therapies Products | | |

| | |

Product | | Primary Application |

| | |

CervicalStim Spinal Fusion Therapy | | PEMF non-invasive cervical spinal fusion therapy used to enhance bone growth. |

| |

SpinalStim Spinal Fusion Therapy | | PEMF non-invasive lumbar spinal fusion therapy used to enhance bone growth. |

| |

PhysioStim Bone Healing Therapy | | PEMF non-invasive appendicular skeleton healing therapy used to enhance bone growth in nonunion fractures. |

| | |

AccelStim | | LIPUS healing therapy used to enhance bone growth in certain fresh, distal radius, and tibial diaphysis fractures and nonunion fractures. |

| | |

Spinal Implants and Enabling Technologies Products | | |

| | |

Primary Application | | Product |

| | |

Posterior Thoracolumbar Fixation Procedures | | Pedicle screw systems for open and minimally invasive surgery ("MIS") procedures and adult deformity procedures featuring modular technology and accompanying instrumentation designed to reduce the number of trays needed for surgery and that provides surgeons with multiple intra-operative options to facilitate posterior thoracolumbar fixation. We also provide powerful instrumented compression and distraction of the spine. Products include our Mariner, Firebird, Firebird NXG, Janus, Daytona, Newport, and Phoenix product lines. These brands also include several different screw types including, cannulated, fenestrated, hydroxyapatite ("HA") coated, and cortical cancellous. These options give surgeons a full portfolio of choices for their patients without having to utilize several different screw systems. |

| | |

Artificial Cervical Disc Replacement Procedures | | Our next-generation artificial disc, M6-C artificial cervical disc, developed to replace an intervertebral disc damaged by cervical disc degeneration is the only artificial cervical disc that mimics the anatomic structure of a natural disc by incorporating an artificial viscoelastic nucleus and fiber annulus into its design. In February 2025, the Company announced the discontinuation of the M6 line of products. |

| | |

| | |

Artificial Lumbar Disc Replacement Procedures | | Our next-generation artificial disc, M6-L artificial lumbar disc, developed to replace an intervertebral disc damaged by lumbar disc degeneration; the only artificial lumbar disc that mimics the anatomic structure of a natural disc by incorporating an artificial viscoelastic nucleus and fiber annulus into its design. (Not available in the U.S.) In February 2025, the Company announced the discontinuation of the M6 line of products. |

| | |

Anterior Lumbar Interbody Fusion ("ALIF") Procedures | | A complete portfolio of ALIF products, including interbody spacers, disc preparation instruments, access systems, and plating/fixation options. Our spacers come in a variety of material options including polyetheretherketone ("PEEK"), PEEK Titanium composite ("PTC"), and 3D printed Titanium. Some of our products also contain U.S. Food and Drug Administration ("FDA") cleared Nano surface technology ("Nanovate") that is scientifically proven to upregulate osteogenic factors in vitro. The multiple material types allow surgeons to select the material best for their patients. These products also come in a variety of footprints and lordotic options. The interbodies come with a large graft area to accommodate the addition of biologics to aid in the fusion process. Some of our interbodies include integrated fixation to eliminate the need for additional fixation. These variations provide a complete list of options for the ALIF procedural category. Our main contributors to this category include Meridian, Waveform A, Reef A, and Pillar SA PTC. |

| | |

Posterior Cervical Fixation Procedures | | We provide spinal fixation systems with novel instrumentation and anatomically designed implants to provide a safe and effective solution designed to improve surgical flow when navigating through complex posterior cervical procedures. These products include a wide array of screws, rods, and instruments to aid surgeons in performing these procedures. These products include Northstar occipital cervical thoracic ("OCT") and Centurion. |

| | |

Posterior Lumbar Interbody Fusion ("PLIF")/ Transforaminal Lumbar Interbody Fusion ("TLIF") Procedures | | Our PLIF/TLIF portfolio includes a variety of interbodies, as well as several disc prep and access options. The interbodies come in both straight and curved footprints to accommodate surgeons in placement of the interbodies, and a choice of materials from PEEK, PEEK Titanium Composite, and 3D printed Titanium. Some of our product also contain FDA-cleared Nanovate that is scientifically proven to upregulate osteogenic factors in vitro. Our main products in the static PLIF/TLIF interbodies are Waveform TA/TO, Reef TA/TO, and Forza. Our straight product category contains both traditional static interbodies as well as expandable options. These options include both our Forza XP and Explorer TO product lines. These expandable options allow surgeons to minimize their exposure and expand the interbody in-situ to the preferred height and lordosis that best suits their patient. To aid in access we also offer several retractor options with our latest screw-based retractor called Fathom. |

| | |

Lateral Lumbar Interbody Fusion ("LLIF") Procedures | | The LLIF portfolio includes a full portfolio of interbodies, additional fixation options, retractor access systems, and disc prep instrumentation. Our interbodies come in a variety of footprint and lordotic options, and in a number of material types, including PEEK, PEEK Titanium composite, and 3D printed Titanium. Our main LLIF interbody brands are Regatta Lateral and Waveform L. These interbodies can be paired with the Regatta plate to provide auxiliary fixation during the LLIF procedure. The Lattus Retractor is our newest market-leading access retractor providing surgeons the ability to access the disc space and conduct the LLIF procedure. This pairs seamlessly with several lateral disc prep options that aid surgeons in completing their discectomy prior to interbody placement. |

| | |

| | |

Anterior Cervical Discectomy and Fusion ("ACDF") Procedures | | The ACDF portfolio includes interbodies with and without integrated fixation and plating systems to provide fixation of the anterior cervical spine. Our cervical interbodies come in a wide variety of footprints and lordotic options, as well as material options, giving surgeons the ability of choice to accommodate their patient populations. Our top producing cervical interbodies include Waveform C, and our Construx brands. The Shoreline product brand provides the ability to turn interbodies without integrated fixation into fixated spacers, reducing time surgeons spend in the operating room and making it seamless to fixate interbodies into the disc space. When selecting an interbody without fixation an anterior cervical plate is needed. Our top brands of cervical plates are Admiral and Cetra. In addition to these options, we also offer several different disc and endplate preparation options to satisfy the ACDF procedure. |

| | |

Revision Surgical Procedures | | As an adjunct to our posterior lumbar fixation portfolio, we offer two main products, Mariner Outrigger and Connectors, that are designed to help surgeons tackle difficult revision cases. These sets are constructed with an industry-leading number of connectors, specially designed rods, and instruments to aid in these cases. Giving surgeons a tremendous number of options is the key to the success of these sets. |

| |

Sacroiliac ("SI") Joint Fusion Procedures | | Firebird SI is a minimally invasive screw system that is intended for fixation of sacroiliac joint disruptions in skeletally mature patients. This has been, and continues to be, a product differentiator, as many competitors do not offer SI fixation options. Firebird SI is one of the only 3D printed Titanium products on the market and the only 3D printed product that also has nanotechnology claims with our Nanovate technology. |

| | |

Other procedures: Corpectomy, Laminoplasty, Jazz Bands | | Outside of the main spinal procedural categories, we also offer several products in areas such as corpectomy (VuMesh), laminoplasty (Newbridge), and a unique product, Jazz Bands. Jazz Bands provide a temporary short-term stabilization as a bond anchor to aid in the repair of bone fractures. |

| | |

7D FLASH Navigation System (Spine) | | A machine-vision navigation platform for use in open and mini-open posterior spinal procedures that uses proprietary visible light technology coupled with advanced software algorithms to deliver a fast, efficient, cost-effective, and radiation free solution for spine surgery. |

| |

7D FLASH Navigation System (Percutaneous) | | A valuable enhancement to the 7D FLASH Navigation System to address percutaneous spinal procedures; the camera-based technology, coupled with 7D Machine Vision algorithms, maintains the same fast, accurate, and efficient surgical workflow as the Spine platform, while also providing an imaging agnostic solution to percutaneous posterior spine surgery. |

| |

7D FLASH Navigation System (Cranial) |

| A module on the 7D FLASH Navigation System that utilizes 7D Machine Vision Technology for cranial surgery; the visible light technology allows for a completely contactless workflow, acquires hundreds of thousands of virtual fiducials using the patient’s own anatomy, and results in nearly instantaneous cranial registrations to the skin or skull in almost any surgical position. |

| | |

FLASH External Ventricular Drain ("EVD") System (Cranial) | | The FLASH EVD system leverages proprietary LiveTrack Machine Vision hardware and software to generate high-resolution three-dimensional images embedded with hundreds of thousands of virtual fiducials. This advanced navigation system enables a fully contactless workflow by seamlessly tracking disposable surgical instruments via integrated LiveTrack tile markers, ensuring precise surgical navigation for external ventricular drain bedside procedures. |

| | |

| | |

Biologics Technologies | | |

| | |

Product Categories | | Products |

| | |

Proprietary Technology | | Accell Bone Matrix ("ABM") An open structured, dispersed form of DBM, which increases the bioavailability of bone proteins at an earlier time in the healing cascade; when combined with traditional DBM, both fibers and particulate forms, provides a biphasic release of growth factors to promote healing. Accell is a technology featured in several key DBM products, including but not limited to, Strand Plus and Evo3. |

| | |

Demineralized Bone Fibers ("DBF") | | Strand, Strand Plus, Fiberfuse DBFs are designed to facilitate and aid in fusion by maximizing osteoinductive content while providing an improved conductive matrix. Multiple compositions include 100% fibers, fibers with ABM, and fibers mixed with cancellous bone. Provided in both putty and strip formulations. |

| | |

Demineralized Bone Putty | | Evo3/Evo3c, Torrent/Torrent C, DynaGraft II, OrthoBlast II, Legacy Flowable DBMs designed with putty-like handling characteristics to ease graft placement and conform to any bony anatomy to aid in bone fusion. Provided in multiple compositions of DBM particulate and carrier with and without Accell Bone Matrix or with and without cancellous bone. |

| | |

Cellular Bone Matrixes ("CBM") | | Trinity Elite, Virtuos Lyograft Comprised of demineralized cortical bone fibers and cancellous bone with retained cells, cellular allografts are used during surgery that is designed to aid in the success of a spinal fusion or bone fusion procedure. Provided in either a cryopreserved or shelf-stable form. |

| | |

Synthetics | | Cove, Mozaik To address the synthetic market segment, this portfolio includes an advanced bioactive synthetic and a value-based offering to meet different customer profiles. Provided in both putty and strip formulations. |

| | |

Procedure specific solutions | | Market-differentiated products focused on solving clinical problems tied to specific procedure techniques in spine for fusion. Ballast, Ballast MT Resorbable mesh filled with 100% DBM, or provided empty; aids in simplifying graft placement and prevents graft migration for posterolateral fusion. NorthStar Facet Fusion, Flash Facet Fusion Novel procedural solution for reproducible biologic placement within the facet joint for cervical and lumbar spine. Systems includes pre-shaped demineralized bone fibers with single-use instrumentation for facet prep and biologic delivery. RAPID, O-Genesis Reusable and sterile, single use options to aid in bone graft delivery to the surgical site. |

| | |

Other | | Versashield A thin hydrophilic amniotic membrane designed to serve as a wound covering and protective barrier for a variety of surgical demands. |

Bone Growth Therapies — Spinal Therapy

Our bone growth therapy devices used in spinal applications are designed to enhance bone growth and improve the success rate of certain spinal fusion procedures by stimulating the body’s own natural healing mechanism post-surgically. These non-invasive portable devices are intended to be used as part of a home treatment program prescribed by a physician.

We offer two spinal fusion therapy devices: the SpinalStim and CervicalStim devices. Our stimulation products use a PEMF technology designed to enhance the growth of bone tissue following surgery and are placed externally over the site to be healed. Research data shows that our PEMF signal induces mineralization and results in a process that stimulates new regeneration at the spinal fusion site. Some spine fusion patients are at greater risk of not achieving a solid fusion of new bone around the fusion site. These patients typically have one or more risk factors, such as smoking, obesity, or diabetes, or their surgery involves the revision of a failed fusion or the fusion of multiple levels of vertebrae in one procedure. For these patients, post-surgical bone growth therapy has been shown to significantly increase the probability of fusion success.

The SpinalStim device is a non-invasive spinal fusion stimulator system designed for the treatment of the lumbar region of the spine. The device uses proprietary technology and a wavelength to generate a PEMF signal. The FDA has approved the SpinalStim system as a spinal fusion adjunct to increase the probability of fusion success and as a non-operative treatment for salvage of failed spinal fusion at least nine months post-operatively.

Our CervicalStim product remains the only FDA-approved bone growth stimulator on the market indicated for use as an adjunct to cervical spine fusion surgery. It is indicated for patients at high-risk for non-fusion.

The SpinalStim and CervicalStim systems are accompanied by an application for mobile devices called STIM onTrack. The mobile app includes a first-to-market feature that enables physicians to remotely view patient adherence to prescribed treatment protocols and patient reported outcome measures. Designed for use with smartphones and other mobile devices, the STIM onTrack tool helps patients follow their prescription with daily treatment reminders and a device usage calendar. The app is free and available through the Android and Apple App Stores.

Bone Growth Therapies — Orthopedic Therapy

Our PhysioStim bone healing therapy products use PEMF technology similar to that used in our spine stimulators. The primary difference is that the PhysioStim devices are designed for use on the appendicular skeleton.

A bone’s regenerative power results in most fractures healing naturally within a few months. However, in the presence of certain risk factors, some fractures do not heal or heal slowly, resulting in nonunions. Traditionally, orthopedists have treated such nonunion conditions surgically, often by means of a bone graft with fracture fixation devices, such as bone plates, screws, or intramedullary rods. These are examples of "invasive" treatments. Our patented PhysioStim bone healing therapy products are designed to use a low level of PEMF signals to noninvasively activate the body’s natural healing process. The devices are anatomically designed, allowing ease of placement, patient mobility, and the ability to cover a large treatment area.

Similar to our SpinalStim and CervicalStim systems, the PhysioStim device is also accompanied by the STIM onTrack mobile app, enabling physicians treating patients with nonunion fractures to remotely view and assess patient adherence to prescribed treatment protocols and patient reported outcome measures.

The AccelStim device provides a safe and effective nonsurgical treatment to improve nonunion fracture healing and accelerate the healing of indicated fresh fractures. The device stimulates the bone’s natural healing process through LIPUS waves to the fracture site.

Spinal Implants — Motion Preservation Solutions

The M6-C cervical and M6-L lumbar artificial discs are used to treat patients suffering from degenerative disc disease of the spine. In February 2025, the Company announced that the M6 line of products is being discontinued.

Spinal Implants — Spinal Fixation Solutions

We provide a wide range of implants and fixation products for use in spinal surgery, and we cover the entire spine from occiput to sacrum. See below for a discussion of our portfolio based on the segmentation of our internal franchise groups:

Cervical

Our cervical portfolio includes fixation, interbodies, and plates. Our interbody spacer brands and materials include PTC, Waveform, Reef, and Nanovate 3D printed titanium surface technologies. Each comes with different material, clinical, and handling characteristics that can be options for clinicians to make the proper choice for their patients. Some of our spacers also have the option for integrated fixation which eliminates the necessity for additional fixation. In addition to our spacers, our surgical grade titanium plating systems, Admiral and Cetra, allow for anterior fixation of the cervical spine. Lastly, for posterior fixation we offer two systems, Northstar OCT and Centurion, as well as a laminoplasty system, Newbridge. These systems are comprehensive systems comprised of rods, connectors, and screws that are implanted for posterior fixation.

Interbody

Our robust interbody group has options for every approach vector, including anterior lumbar, posterior lumbar, and lateral. Within each group there are several material types, including a thermoplastic compound called PEEK, 3D printed titanium with FDA approved Nanotechnology claims, and two different composites, Nanometalene and PTC, comprised of both PEEK and titanium. Our anterior lumbar portfolio has several different footprints and lordotic options as well as options for integrated fixation or plating. These brands include Waveform A, Reef A, Pillar SA PTC, Unity Lumbosacral Plating, and Meridian. Our lateral portfolio takes full advantage of our top-of-the-line retractor systems to gain access to the disc space. The lateral portfolio is complete with highly competitive footprints and plating options as well. These brands include Skyhawk, Regatta L, and Waveform L, which are utilized in direct lateral, prone lateral, and anterior to the psoas procedures. Our posterior portfolio, utilized for PLIF and TLIF procedures, has two key segmentations, static and expandable. Our expandable posterior interbodies allow for a smaller incision and smaller exposure that then expands to create or fill the space of the disc space. Our expandable brands are Forza XP, our top performing interbody implant, and Explorer TO. In the static posterior interbodies, we have several brands serving all material types and offering both straight and curved footprints to aid in posterior procedures. Our brands are Forza, Forza PTC, Forza Ti, Waveform TA/TO, and Reef TA/TO.

Thoracolumbar

In our thoracolumbar franchise we have a complete line of fixation products for degenerative spinal conditions, as well as for complex deformity, midline, and revision cases. Our posterior brands are all modular, meaning surgeons have the option to select from several different screw shank varieties including, cannulated, fenestrated, HA coated, cortical cancellous, and a traditional dual lead option. This allows the surgeon to maintain the instrumentation of the parent system, but then select the proper screw shank for the patient, offering maximum clinical value. The Firebird/Firebird NXG, Phoenix, and Mariner brands are available for open or minimally invasive procedures and have options such as connectors, mono axial screws, and many more instrumentation options to aid in a variety of cases. Also within this franchise group is our SI fixation product, Firebird SI, the first 3D printed SI fixation product and one of the only such products with Nanotechnology claims.

Enabling Technologies

Our machine vision 7D FLASH Navigation System is used in a variety of posterior spinal procedures, including degenerative, deformity, tumor, trauma, and revision surgery. The system can be utilized in MIS/percutaneous, mini-open, or open techniques. The technology also offers a comprehensive cranial platform for use in cranial neurosurgery.

Our innovative 7D FLASH Navigation System delivers a comprehensive navigation platform that utilizes visible light, machine-vision cameras, and intelligent software algorithms to create a 3D image within seconds for surgical navigation. The novel technology allows for a fast image reconstruction for surgical navigation with no disruption to surgeon workflow and eliminates radiation exposure during the procedure to the patient, surgeon, and operating room staff.

Our Spine Module is our leading product in the FLASH Navigation Portfolio. In 2024, we further enhanced the 7D FLASH Navigation System with the release of our 7D MRVision utilizing MRIguidance’s BoneMRI software to generate a synthetic CT from an MRI scan that can be used for surgical planning and spinal navigation with the 7D FLASH Navigation System Spine Module. Traditional spine navigation requires a preoperative CT or intraoperative radiation for image acquisition and registration. 7D MRVision is the

first and only solution that eliminates radiation from the entire navigation workflow. Further enhancements and new features to the Spine Module and Percutaneous Module are in development and are expected to launch in 2025.

In addition to these new products focused on spine, the FLASH Navigation Portfolio also includes our Cranial Module for use in cranial surgeries. The technology uses a completely contactless workflow, acquiring hundreds of thousands of virtual fiducials using the patient’s own anatomy, and results in nearly instantaneous cranial registrations to the skin or skull in almost any surgical position. In 2025, we anticipate the commercial launch of FLASH EVD, a new mobile bed-side navigational system leveraging 7D FLASH Technology designed for fast and reliable EVD placement. Cadaveric testing has been completed and FLASH EVD achieved FDA 510K clearance in December 2024.

Biologics — Regenerative Solutions

Our biologics portfolio is focused on best-in-class bone grafting solutions from each of the major bone grafting categories - demineralized bone, cellular allografts, and synthetics. The breadth of the portfolio within each segment allows for a consultative approach with both physicians and hospitals to determine the best product based on clinical performance and price.

Our largest portfolio of products is within DBMs, which includes both putty and fiber-based forms that provide different handling and performance based on clinical applications. Leading this portfolio are Strand Plus, 100% DBM Fiber with Accell, Evo3/Evo3c, and DBM putty with Accell. ABM is a key differentiator within the DBM market. This internally processed, proprietary technology is an open structured, dispersed form of DBM, which increases the bioavailability of bone proteins at an earlier time in the healing cascade. When combined with traditional DBM, it provides a biphasic release of growth factors to promote healing.

Our cellular allografts portfolio features a market-leading graft with Trinity Elite and recently released Virtuous Lyograft, both co-branded with MTF Biologics. Trinity Elite, an allograft with viable cells, has maintained position as a market leader with over a decade of clinical evidence and a series of peer-reviewed publications. Virtuous Lyograft is particularly unique in that it is a first-of-its-kind, shelf-stable cellular allograft for spine and orthopedic procedures provided in a room-temperature, ready-to-use, moldable form.

Regarding synthetic solutions, our focus products are Cove and Mozaik. Cove, an advanced bioactive synthetic, is the newest introduction into this segment. Cove has a unique surface topography of the β-TCP and HA granule and has demonstrated the ability to grow bone in a muscle pouch. Additionally, Cove has handling characteristics ideal for ensuring graft placement remains where it is needed. The combination of Cove and Mozaik provides different value options within this portfolio to meet varying customer needs.

In addition to each of the major categories, we have continued to invest in products that address specific procedural and clinical needs. Our solutions address many of the issues that physicians see with graft delivery and containment within the surgical site. Several of our solutions address this through handling characteristics of product, shape and design, instrumentation to aid delivery, or even added materials to aid in graft containment. All of these solutions are to improve the ease of use and consistency of our products while driving better clinical outcomes.

We receive marketing fees through our collaboration with MTF Biologics for Virtuous, Trinity Elite, FiberFuse, and certain other tissues. MTF Biologics processes the tissues, maintains inventory, and invoices hospitals, surgery centers, and other points of care for service fees, which are submitted by customers via purchase orders. We have exclusive worldwide rights to market the Virtuous and Trinity Elite, and exclusive rights to market the FiberFuse tissues in the U.S.

Our other leading tissue forms and synthetics such as, Strand Plus, Strand, Evo3, Evo3c, Ballast, Cove, and Mozaik are all processed internally through IsoTis Orthobiologics. This completely integrated business unit allows for a continuous feedback cycle with research and development, marketing, manufacturing, and quality to ensure high-quality products delivered with consistent customer fulfillment.

To date, our Biologics products are offered primarily in the U.S. market, due in part to restrictions on providing U.S. human donor tissue and bovine collagen in certain countries.

Global Spine Future Product Applications

We remain very active with multiple internal developments to support new technology commercialization efforts. These new technologies apply to both the cervical and thoracolumbar spinal anatomy. We expect that the contribution of new, internally developed technologies and any future external acquisitions will be the primary driver of future growth.

Regarding our Bone Growth Therapy business, we have participated in research at the Wake Forest University Health Sciences, Chinese University of Hong Kong, and University of California San Francisco, where scientists conducted animal and cellular studies

to identify the mechanisms of action of our PEMF signals on bone, cartilage, meniscus, nerve, and efficacy of healing. From these efforts, some studies have been published in peer-reviewed journals. Among other insights, the studies illustrate positive effects of PEMF on callus formation and bone strength, meniscus and nerve injury repair, as well as proliferation and differentiation of cells involved in tissue regeneration and healing. Furthermore, we believe that the previous research work with Cleveland Clinic, the Chinese University of Hong Kong, and the University of Pennsylvania, allowing for characterization and demonstration of the Orthofix new PEMF waveform, is paving the way for signal optimization for a variety of new applications and indications. This collection of pre-clinical data, along with additional clinical data, could represent new clinical indication opportunities for our regenerative stimulation solutions.

Global Orthopedics

The Global Orthopedics reporting segment offers products and solutions for the underserved limb reconstruction market that encompasses four pillars: deformity correction, limb lengthening, complex fracture management, and limb preservation. This reporting segment specializes in the design, development, and marketing of external and internal fixation orthopedic products that are coupled with enabling digital technologies to serve the complete patient treatment pathway. We sell these products through a global network of distributors and sales representatives to hospitals, healthcare organizations, and healthcare providers.

Global Orthopedics Strategy

Our strategy for the Global Orthopedics reporting segment has recently evolved to specifically focus on providing unrivaled limb reconstruction procedural solutions coupled with first-in-class service and support.

Our key strategies in this segment are:

•Expand our position as the worldwide leader in limb reconstruction, including both internal and external solutions, through a patient-centric approach and digital treatment journey;

•Leverage our cross-product OrthoNext digital platform, a uniquely developed pre and post planning, software that allows our clinicians to pre-plan surgery for patients so they can start surgeries with a greater degree of confidence, reduce surgical times, enable better outcomes, and follow up post operatively to evaluate the success of the chosen surgical plan;

•Build on our historical position as a company at the forefront of innovation in the management of Charcot foot and ankle conditions by further investing into limb preservation technology advancements that address challenging conditions associated with diabetic foot;

•Promote and invest in our Fitbone intramedullary limb lengthening platform, including the newly released Transport and Lengthening System – the only all internal bone transport intramedullary nail available in the U.S.;

•Continue to be market leaders in deformity correction with our flagship TrueLok system, comprised of the most comprehensive external ring fixation solutions, and focusing on delivering enabling technology solutions to improve surgeons' ability to effectively treat their patients;

•Continue to focus on complex fracture management in select global markets, with the Galaxy Fixation System and by providing single-use sterile pack procedural solutions to reduce costs and drive surgical efficiencies;

•Collaborate with physicians and healthcare partners to improve patients’ lives through digitally transformative technology, clinical evidence, and our industry-leading medical education program, Orthofix Academy;

•Continue the strong pace of new product launches; and

•Acquire or license products, technologies, and companies to support these market opportunities.

Global Orthopedics Focus Products

Global Orthopedics offers a comprehensive line of limb reconstruction technologies that address the most complex patient conditions within deformity correction, limb lengthening, complex fracture management, and limb preservation. We provide innovative external and internal solutions to help surgeons improve the quality of life for patients of all ages.

The following table identifies the principal Global Orthopedics products by trade name and describes their primary applications:

| | |

Products and Software | | Primary Application |

| |

TrueLok | | A surgeon-designed, lightweight external fixation system for complex fracture management, limb lengthening, limb preservation, and deformity correction, which consists of circular rings and semi-circular external supports centered on the patient’s limb and secured to the bone by crossed, tensioned wires and half pins. |

| | |

TrueLok Hexapod System ("TL-HEX") | | A hexapod external fixation system for deformity correction with associated software newly integrated into the OrthoNext platform, designed as a three-dimensional bone segment reposition module to augment the previously developed TrueLok frame. The system consists of circular and semi-circular external supports, secured to the bones by wires and half pins and interconnected by six struts, which allows multi-planar adjustment of the external supports. The rings’ positions are adjusted either rapidly or gradually in precise increments to perform bone segment repositioning in three-dimensional space. |

| | |

TrueLok EVO | | A modular circular external fixation system, available pre-assembled in sterile kits for complex fracture management, deformity correction, and limb preservation; it is the only circular fixation system to feature both radiolucent rings and struts that provides surgeons with clear radiographic visualization to better assess bone anatomy both during surgery and in post-operative care. |

| | |

Fitbone Intramedullary Limb-Lengthening System | | An intramedullary lengthening system intended for limb lengthening of the femur and tibia, surgically implanted in the bone through a minimally invasive procedure; it includes an external telemetry control set that manages the distraction process, and is the only intramedullary limb lengthening system with an FDA-cleared pediatric indication. |

| | |

Galaxy Fixation System | | A pin-to-bar system for temporary and definitive fracture fixation, in the upper and lower limbs. Available in sterile kits, the system incorporates a streamlined combination of clamps, with both pin-to-bar and bar-to-bar coupling capabilities, offering a complete range of applications, including specific anatomic units for the shoulder, elbow, and wrist. The latest version, Galaxy Gemini, includes a universal clamp and other updates to better streamline surgical procedures. |

| | |

Galaxy Fixation Shoulder | | A unique solution for the treatment of proximal humeral fractures. |

| | |

Ankle Hindfoot Nail ("AHN") | | A differentiated solution for hindfoot fusions that includes a revision option to address larger bone defects and more complex hindfoot pathologies. |

| | |

G-BEAM Fusion Beaming System | | A system designed to address the specific demands of advanced deformity and trauma reconstructions of foot and ankle applications, such as Charcot, requiring fusion of the medial and/or lateral columns, with or without corrective osteotomies, as well as for joint fusions within the mid- and hindfoot. |

| | |

OSCAR | | An ultrasonic powered surgical system for revision hip and knee arthroplasty. |

| | |

External Fixators | | External fixation, including our limb-lengthening systems, ProCallus, XCaliber, Pennig, Radiolucent Wrist Fixators, and Calcaneal Fixator. |

| |

LRS Advanced Limb Reconstruction System | | An external fixation solution for limb lengthening and deformity correction, that uses callus distraction to lengthen bone in a variety of procedures, |

| | |

| | including bone transport, simultaneous compression and distraction at different sites, bifocal lengthening, and correction of deformities with shortening. |

| | |

OrthoNext Digital Platform | | A digital software platform developed specifically to enable surgeons to perform deformity analysis, plan out the correction, and template the appropriate implant to use. The platform includes modules for the JuniOrtho Plating System, Fitbone Intramedullary Limb Lengthening System, and more recently added TL-Hex system. |

External Fixation

External fixation devices are used to correct bone deformities, stabilize fractures, and offer an ideal treatment in patients with known risk factors or co-morbidities. The treatment is minimally invasive and allows external manipulation of the bone to obtain and maintain final bone alignment (reduction). The bone is fixed in this way until healing occurs. External fixation allows small degrees of micromotion (dynamization), which promotes blood flow at the fracture or fusion site and accelerates the bone healing process. External fixation devices may also be used temporarily in complex fracture cases to stabilize the fracture prior to treating it definitively. In these situations, the device offers rapid fracture stabilization, which is important in life-saving and limb-salvaging procedures.

We offer most of our products in sterile packaged procedural kits, which fulfills the need of a streamlined and ready-to-use set of products, particularly in trauma applications or the military setting, where timing is crucial.

Examples of our external fixation devices include the TrueLok, TL-HEX, TrueLok Evo, the Galaxy and Galaxy Gemini Fixation Systems, and the LRS Advanced Limb Reconstruction System.

Internal Fixation

Internal fixation devices consist of either long rods, commonly referred to as nails, or plates that are attached to the bone with the use of screws. Nails and plates come in various sizes, depending on the bone that requires treatment. A nail is inserted into the medullary canal of a fractured long bone of the human arm or leg (e.g., humerus, femur, or tibia). Alternatively, a plate is attached by screws to an area such as a broken wrist, hip, or foot. Examples of our internal fixation devices include Chimaera, AHN, and the G-BEAM Fusion Beaming System.

The Fitbone Intramedullary Limb Lengthening System provides an internal option for limb lengthening of the femur and tibia and together with our external fixation solutions, provides Orthofix with the most complete limb reconstruction portfolio on the market. The portfolio was recently expanded with the release of the Fitbone Transport and Lengthening System specifically developed for bone defect management applications. We are continuing to invest in the Fitbone technology platform in order to offer surgeons more innovative solutions to meet both their needs to treat limb length discrepancies and complex deformities.

In addition, we also design, manufacture, and distribute devices intended to treat congenital bone conditions, such as angular deformities (e.g., bowed legs in children), degenerative diseases, and conditions resulting from a previous trauma. An example of a product offered in this area is the eight-Plate Plus Guided Growth System.

Product Development

Our primary research and development facilities are located in Lewisville, Texas; Carlsbad, California; Toronto, Canada; and Verona, Italy.

We have a research and development organization dedicated to advancing our portfolio of spinal implants, biologics, orthopedic devices, and machine vision image guidance innovations through product development and clinical affairs programs. Our product development efforts employ an integrated team approach that involves collaboration between surgeons, our engineers, our machinists, and our regulatory personnel. We also work with leading hospital research institutions, surgeons, consultants, and certain non-profit organizations, such as MTF Biologics, on the long-term scientific planning and evolution of our products and therapies. Several of the products that we market have been developed through these collaborations. In addition, we periodically receive suggestions for new products and product enhancements from the scientific and medical community, some of which result in us entering into assignment or license agreements with physicians and third parties.

For our spine and orthopedics products, our product development teams, in consultation with design surgeons, formulate a design for the product and then our machinists build prototypes for testing our prototyping development and testing operation at our

facilities. We use a broad scope of technologies designed to allow us to meet the complex engineering requirements of customers. As part of the development process, surgeons test the implantation of the products in our in-house cadaveric laboratories, which aids in the design of new products intended to meet the needs of both the surgeon, the patient, and the healthcare ecosystem. Our team refines or redesigns the prototype as necessary based on the results of the product testing, allowing our team to perform rapid iterations of the design-prototype-test development cycle. Our clinical and regulatory personnel work in parallel with our product engineering personnel to facilitate regulatory clearances of our products. We believe that these product development efforts allow our team to provide solutions that respond to the needs of our surgeon customers and their patients.

Like the spine and orthopedics product development process, our software engineers, product managers, and design surgeons are working towards the full integration of our spinal implants and biologics product lines with our machine vision 7D FLASH Navigation System. This includes the design of specific software modules, features, and tracked instruments designed to meet the needs of a wide range of procedures including, degenerative, complex, revision, minimally invasive and deformity spine procedures. In addition, we are also exploring opportunities to integrate the 7D FLASH Technology into a variety of orthopedic applications to treat patients of all ages.

For biologics, we plan to develop line extensions for our innovative biologics technologies that will continue to improve bone forming potential while addressing specific procedural requirements, both in the spine field and in general orthopedic applications. We are investigating new product formulations in DBM, while continuously looking at process improvements within tissue processing. Our Biologics research and development team has experience in biomaterial sciences and bringing next generation technologies to market.

In 2024, 2023, and 2022, we incurred research and development expenses of $73.6 million, $80.2 million, and $49.1 million, respectively.

Patents, Trade Secrets, Assignments and Licenses

We rely on a combination of patents, trade secrets, assignment and license agreements, and non-disclosure agreements to protect our proprietary intellectual property. We possess numerous U.S. and foreign patents, have numerous pending patent applications, and have license rights under patents held by third parties. Many of our products are covered by patents in the major markets in which they are sold. We do not believe that the expiration of any single patent is likely to significantly affect our intellectual property position. The medical device industry is characterized by the existence of a large number of patents and frequent litigation based on allegations of patent infringement. Patent litigation can involve complex factual and legal questions and its outcome is uncertain. Our success is dependent, in part, on us not infringing upon patents issued to others, including our competitors, potential competitors, and other third parties. While we make extensive efforts to ensure that our products do not infringe other parties’ patents and proprietary rights, our products and methods may be found by a court to be covered by patents held by our competitors or other third parties. For a further discussion of these risks, please see Item 1A of this Annual Report under the heading "Risk Factors."

We rely on confidentiality and non-disclosure agreements with employees, consultants, and other parties to protect, in part, trade secrets and other proprietary technology.

We obtain assignments or licenses of varying durations for certain of our products from third parties. We typically acquire rights under such assignments or licenses in exchange for lump-sum payments or arrangements under which we pay a percentage of sales to the licensor. However, while assignments or licenses to us generally are irrevocable, no assurance can be given that these arrangements will continue to be made available to us on terms that are acceptable to us, or at all. The terms of our license and assignment agreements vary in length from a specified number of years, to the life of the patents, or for the economic life of the product. These agreements generally provide for royalty payments and termination rights in the event of a material breach.

Compliance and Ethics Program

It is our fundamental policy to conduct business in accordance with the highest ethical and legal standards. We have a comprehensive compliance and ethics program, which is overseen by a Chief Compliance and Risk Officer, who reports directly to our Chief Executive Officer and the Compliance and Ethics Committee of the Board of Directors. The program is intended to promote lawful and ethical business practices throughout our domestic and international businesses. It is designed to prevent and detect violations of applicable federal, state, and local laws in accordance with the standards set forth in guidance issued by the U.S. Department of Justice ("U.S. DOJ") ("Evaluation of Corporate Compliance Programs" (updated March 2023)), the Office of

Inspector General (HCCA-OIG "General Compliance Program Guidance" (November 2023)), and the U.S. Sentencing Commission ("Effective Compliance and Ethics Programs" (November 2014)). Key elements of the program include:

•Organizational oversight by senior-level personnel responsible for the compliance function within the Company;

•Written standards and procedures, including a Corporate Code of Conduct;

•Methods for communicating compliance concerns, including anonymous reporting mechanisms;

•Investigation and remediation measures to ensure a prompt response to reported matters and timely corrective action;

•Compliance education and training for employees and contracted business associates;

•Auditing and monitoring controls to promote compliance with applicable laws and to assess program effectiveness;

•Disciplinary guidelines to enforce compliance and address violations;

•Due diligence reviews of high-risk intermediaries and exclusion lists screening of employees and contracted business associates; and

•Risk assessments to identify areas of compliance risk.

Government Regulation

Classification and Approval of Products by the FDA and other Regulatory Authorities

Our research, development, clinical programs, and our manufacturing and marketing operations, are subject to extensive regulation in the U.S. and other countries. Most notably, all of our products sold in the U.S. are subject to the Federal Food, Drug, and Cosmetic Act (the "FDCA") and the Public Health Services Act as implemented and enforced by the FDA. The regulations that cover our products and facilities vary widely from country to country. The amount of time required to obtain approvals or clearances from regulatory authorities also differs from country to country.

Unless an exemption applies, each medical device we commercially distribute in the U.S. is covered by premarket notification ("510(k)") clearance, letter to file, or approval of a premarket approval application ("PMA"). The FDA classifies medical devices into one of three classes, which generally determine the type of FDA approval required. Devices deemed to pose low risk are placed in Class I, devices deemed to pose moderate risk are placed in Class II, and devices deemed to pose the greatest risks, requiring more regulatory controls to provide a reasonable assurance of safety and effectiveness, or devices deemed not substantially equivalent to a device that previously received 510(k) clearance (as described below), are placed in Class III. Our Spinal Implants and Global Orthopedics products are, for the most part, classified as Class II devices and the instruments used with these products are generally classified as Class I. Our 7D FLASH Navigation System is classified as Class II and certain accessories thereto are classified as Class I. Our Bone Growth Therapies products and the M6-C artificial cervical disc are currently classified as Class III, and have been approved for commercial distribution in the U.S. through the PMA process. However, an FDA panel recommended that bone growth stimulator devices be reclassified by the FDA from Class III to Class II devices with special controls. For additional discussion of this development, see Item 1A of this Annual Report under the heading "Risk Factors."

The medical devices we develop, manufacture, distribute, and market are subject to rigorous regulation by the FDA and numerous other federal, state, and foreign governmental authorities. The process of obtaining FDA clearance and other regulatory approvals to develop and market a medical device, particularly from the FDA, can be costly and time-consuming, and there can be no assurance such approvals will be granted on a timely basis, if at all. While we believe we have obtained all necessary clearances and approvals for the manufacture and sale of our products and that they are in material compliance with applicable FDA and other material regulatory requirements, there can be no assurance that we will be able to continue such compliance.

In 2017, the European Union ("E.U.") adopted the E.U. Medical Device Regulation ("MDR") (Council Regulations 2017/745), which imposes strict requirements for the marketing and sale of medical devices, including new quality system and post-market surveillance requirements. The regulation, as amended in March 2023, provides a transition period for all currently approved medical devices prior to May 2021 (under the European Medical Device Directive) to meet the additional requirements, and for higher risk devices, this transition period was extended until December 2027 and until December 2028 for medium-and-lower risk devices. After this transition period, all medical devices marketed in the E.U. will require certification according to these new requirements. This regulation has required us to incur, and we expect to continue to incur, significant costs through the transition period and beyond to maintain compliance with the additional requirements. Failure to meet the requirements of the regulation could adversely impact our business in the E.U. and other countries that utilize or rely on E.U. requirements for medical device registrations.

In the E.U., our products that contain human-derived tissue, including demineralized bone material, are not medical devices as defined in the MDR. They are also not medicinal products as defined in Directive 2001/83/EC of the European Parliament and of the Council of the E.U. Today, the regulations in the E.U. governing products that contain human-derived tissue, if applicable, vary from one E.U. member state to the next. Because of the absence of a harmonized regulatory framework and the proposed regulation for advanced therapy medicinal products in the E.U., the approval process for human-derived cell or tissue-based medical products in the E.U. may be extensive, lengthy, expensive, and unpredictable.

Certain countries, as well as the E.U., have issued regulations that govern products that contain materials derived from animal sources. Regulatory authorities are particularly concerned with materials infected with the agent that causes bovine spongiform encephalopathy ("BSE"). These regulations affect our biomaterial products for the spine, which contain material derived from bovine tissue. Although we take steps designed to provide that our products are safe and free of agents that can cause disease, products that contain materials derived from animals, including our products, may become subject to additional regulation, or even be banned in certain countries, because of concern over the potential for prion transmission. Significant new regulations, a ban of our products, or a movement away from bovine-derived products because of an outbreak of BSE could have a material and adverse effect on our business or our ability to expand our business.

Within our Biologics product category, we market tissue for bone repair and reconstruction, an allogeneic bone matrix comprised of cancellous bone containing viable cells and a demineralized cortical bone component, as well as, demineralized cortical fibers, structural allografts, and an amniotic membrane, which is a natural tissue barrier. These allografts are regulated under the FDA’s Human Cell, Tissues and Cellular and Tissue-Based Products ("HCT/P") regulatory paradigm and not as a medical device, biologic, or a drug. These tissues are regulated by the FDA as minimally-manipulated tissue and are covered by the FDA’s "Good Tissues Practices" regulations, which cover all stages of allograft processing. There can be no assurance our suppliers will continue to meet applicable regulatory requirements or that those requirements will not be changed in ways that could adversely affect our business. Further, there can be no assurance these products will continue to be made available to us or that applicable regulatory standards will be met or remain unchanged. Moreover, products derived from human tissue or bones are from time to time subject to recall for certain administrative or safety reasons and we may be affected by one or more such recalls.

In addition to our allograft solutions (HCT/Ps), we market and distribute additional demineralized bone putties, resorbable mesh with demineralized particulates, and synthetic putties and strips that are regulated by the FDA as medical devices. We also provide ancillary technologies regulated by the FDA as medical devices that aid in the delivery of our bone grafting options clinically. These products are sourced from third party manufacturers, which we believe maintain an adequate inventory to avoid disruptions in product supply.