UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811- 01136

Security Equity Fund

(Exact name of registrant as specified in charter)

805 King Farm Boulevard, Suite 600

Rockville, Maryland 20850

(Address of principal executive offices) (Zip code)

Donald C. Cacciapaglia, President

Security Equity Fund

805 King Farm Boulevard, Suite 600

Rockville, Maryland 20850

(Name and address of agent for service)

Registrant's telephone number, including area code: 1-301-296-5100

Date of fiscal year end: September 30

Date of reporting period: September 30, 2012

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. §3507.

Item 1. Reports to Stockholders.

FUNDAMENTAL ALPHA

LARGE CAP CORE FUND

ALL CAP VALUE FUND

MID CAP VALUE FUND

MID CAP VALUE INSTITUTIONAL FUND

SMALL CAP GROWTH FUND

SMALL CAP VALUE FUND

LARGE CAP CONCENTRATED GROWTH FUND

MSCI EAFE EQUAL WEIGHT FUND

OPPORTUNISTIC

ALPHA OPPORTUNITY FUND

GO GREEN!

ELIMINATE MAILBOX CLUTTER

Go paperless with Guggenheim Investments eDelivery—a service giving you full online access to account information and documents. Save time, cut down on mailbox clutter and be a friend to the environment with eDelivery.

With Guggenheim Investments eDelivery you can:

| · | View online confirmations and statements at your convenience. |

| | |

| · | Receive email notifications when your most recent confirmations, statements and other account documents are available for review. |

| | |

| · | Access prospectuses, annual reports and semiannual reports online. |

If you have questions about Guggenheim Investments eDelivery services, contact one of our Shareholder Service Representatives at 800.820.0888.

This report and the financial statements contained herein are submitted for the general information of our shareholders. The report is not authorized for distribution to prospective investors unless preceded or accompanied by an effective prospectus.

Distributed by Rydex Distributors, LLC.

| the GUGGENHEIM FUNDS annual report | 1 |

September 30, 2012

Dear Shareholder:

Security Investors, LLC (the “Investment Adviser”) is pleased to present the annual shareholder report for nine of our mutual funds (the “Funds”).

The Investment Adviser is a part of Guggenheim Investments, which represents the investment management businesses of Guggenheim Partners, LLC, a global, diversified financial services firm.

This report covers performance of the following Funds for the annual period ended September 30, 2012, with the name of each Fund followed by its ticker symbol:

– Large Cap Core Fund (SECEX)*

– All Cap Value Fund (SESAX)*

– Mid Cap Value Fund (SEVAX)*

– Mid Cap Value Institutional Fund (SVUIX)

– Small Cap Growth Fund (SSCAX)*

– Small Cap Value Fund (SSUAX)*

– Large Cap Concentrated Growth Fund (SEFAX)*

– MSCI EAFE Equal Weight Fund (SEQAX)*

– Alpha Opportunity Fund (SAOAX)*

Rydex Distributors, LLC, the distributor of the Funds, is committed to providing investors with innovative investment solutions; as of the date of this report, we offer a wide range of domestic and global themes in our funds and a distinctive ETF line-up.

To learn more about economic and market conditions over the 12 months ended September 30, 2012 and the objective and performance of each Fund, we encourage you to read the Economic and Market Overview section of the report, which follows this letter, and the Manager’s Commentary for each Fund.

Sincerely,

Donald C. Cacciapaglia

President

October 31, 2012

* Ticker symbol is for A-Class shares.

Read each fund’s prospectus and summary prospectus (if available) carefully before investing. It contains the fund’s investment objectives, risks, charges, expenses and other information, which should be considered carefully before investing. Obtain a prospectus and summary prospectus (if available) at guggenheiminvestments.com or call 800.820.0888.

2 | THE GUGGENHEIM FUNDS ANNUAL REPORT

| ECONOMIC AND MARKET OVERVIEW | September 30, 2012 |

Amidst the negative headlines concerning the potential fiscal cliff in the U.S., further turmoil in Europe and worsening economic data from China, the U.S. economy has shown surprising resilience, with signs of rising consumer sentiment and a recovery in housing. The U.S. housing market appears to have passed its bottom and real estate prices have begun to pick up. Our expectation is that a period of continued low interest rates will likely reinforce the rise in home prices and sales. Rising home prices will increase household net worth, which will translate into greater consumption via the wealth effect, and is supportive of overall economic growth. The recent rise in headline inflation, led by increases in energy and food prices, is likely to be transitory. Inflationary pressures should remain muted in the medium-term given the substantial slack in the economy.

The U.S. economy continues to press forward despite the current headwinds, and we believe the current macroeconomic environment remains constructive for risk assets, especially in the U.S. Stocks in the U.S. appear to be undervalued by most measures, and should benefit from continued capital inflow and the Federal Reserve’s accommodative monetary policy. We continue to see attractive value in credit products on a relative basis. This positive outlook for fixed income, however, is limited to spread (or non-government) sectors. Treasury prices, particularly in the ten-year segment, appear rich. As a result, Treasuries are not a significant holding in the portfolios.

On the international front, uncertainty continues to weigh on European markets. European policymakers appear to be coming closer to a consensus on the need for a fiscal union, albeit at a glacial pace. This would be a positive development in our view and is necessary for a resolution of the current crisis. In China, a recent batch of economic data suggests that the odds of a hard landing have increased materially. We expect an announcement of additional stimulus measures after the government transition next year, but not on the scale of the previous round of stimulus from 2009. Although a stimulus would be supportive of economic growth, we expect China’s headline growth to slow from its breakneck pace of the past decade.

Beginning in October 2011, the U.S. stock market moved up fairly consistently, except for a second-quarter pullback caused by lower earnings and GDP, with the Standard & Poor’s 500 Index* (the “S&P 500”) closing on its highest level since early 2008 late in the period. (All returns cited are for the 12-month period ended September 30, 2012.) The S&P 500, which is generally regarded as an indicator of the broad U.S. stock market, returned 30.20%. Most foreign equity markets were also strong. The Morgan Stanley Capital International (“MSCI”) Europe-Australasia-Far East (“EAFE”) Index*, which is composed of approximately 1,100 companies in 20 developed countries in Europe and the Pacific Basin, returned 13.75%. The MSCI Emerging Markets Index*, which measures stock market performance in global emerging markets, returned 16.93%.

The search for yield continued to attract investors to the U.S. bond markets, helping performance, with lower-rated bonds outperforming higher-quality issues. The return of the Barclays U.S. Aggregate Bond Index*, which is a proxy for the U.S. investment grade bond market, returned 5.14%, while return of the Barclays U.S. Corporate High Yield Index* was 19.37%.

Reflecting the Federal Reserve’s continuing accommodative monetary policy, interest rates on short-term securities remained at their lowest levels in many years; the return of the Bank of America Merrill Lynch 3-Month U.S. Treasury Bill Index* was 0.07%.

The opinions and forecasts expressed may not actually come to pass. This information is subject to change at any time, based on market and other conditions, and should not be construed as a recommendation of any specific security or strategy.

THE GUGGENHEIM FUNDS ANNUAL REPORT | 3

| ECONOMIC AND MARKET OVERVIEW | September 30, 2012 |

*Index Definitions:

The following indices are referenced throughout this report. Indices are unmanaged and not available for direct investment. Index performance does not reflect transaction cost, fees, or expenses.

Barclays U.S. Aggregate Bond Index is a broad-based benchmark that measures the investment grade, U.S. dollar denominated, fixed-rate taxable bond market, including U.S. Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS, and CMBS.

Barclays U.S. Corporate High Yield Index measures the market of USD-denominated, non-investment grade, fixed-rate, taxable corporate bonds. Securities are classified as high yield if the middle rating of Moody’s, Fitch, and S&P is Ba1/BB+/BB+ or below.

Bank of America Merrill Lynch 3-Month U.S. Treasury Bill Index is an unmanaged market index of U.S. Treasury securities maturing in 90 days that assumes reinvestment of all income.

MSCI EAFE Index is a capitalization weighted measure of stock markets in Europe, Australasia and the Far East.

MSCI Emerging Markets Index is a free float-adjusted market capitalization weighted index that is designed to measure equity market performance in the global emerging markets.

MSCI EAFE Equal Weighted Index equally weights the issuers in the MSCI EAFE Index, which is a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the U.S. and Canada. The MSCI EAFE Equal Weighted Index is rebalanced quarterly so that each issuer has the same weight on each rebalancing date. The MSCI EAFE Index consists of the following 22 developed market country indices: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Greece, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland and the United Kingdom.

Standard & Poor’s 500 Index (the “S&P 500”) is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad economy, representing all major industries and is considered a representation of the U.S. stock market.

Russell 3000® Value Index measures the performance of the broad value segment of the U.S. equity value universe. It includes those Russell 3000 companies with lower price-to-book ratios and lower forecasted growth values.

Russell 2500® Value Index measures the performance of the small- to mid-cap value segment of the U.S. equity universe. It includes those Russell 2500 companies with lower price-to-book ratios and lower forecasted growth values.

Russell 2000® Growth Index measures the performance of the small-cap growth segment of the U.S. equity universe. It includes those Russell 2000 companies with higher price-to-book ratios and higher forecasted growth values.

Russell 2000® Value Index measures the performance of the small-cap value segment of the U.S. equity universe. It includes those Russell 2000 companies with lower price-to-book ratios and lower forecasted growth values.

Russell 1000® Growth Index measures the performance of the large-cap growth segment of the U.S. equity universe. It includes those Russell 1000 companies with higher price-to-book ratios and higher forecasted growth value.

4 | THE GUGGENHEIM FUNDS ANNUAL REPORT

ABOUT SHAREHOLDERS’ FUND EXPENSES (Unaudited)

All mutual funds have operating expenses and it is important for our shareholders to understand the impact of costs on their investments. Shareholders of a Fund incur two types of costs: (i) transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, or other distributions; and exchange fees; and (ii) ongoing costs, including management fees, administrative services, and shareholder reports, among others. These ongoing costs, or operating expenses, are deducted from a fund’s gross income and reduce the investment return of the fund.

A fund’s expenses are expressed as a percentage of its average net assets, which is known as the expense ratio. The following examples are intended to help investors understand the ongoing costs (in dollars) of investing in a Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The examples are based on an investment of $1,000 made at the beginning of the period and held for the entire six-month period beginning March 31, 2012 and ending September 30, 2012.

The following tables illustrate a Fund’s costs in two ways:

Table 1. Based on actual Fund return. This section helps investors estimate the actual expenses paid over the period. The “Ending Account Value” shown is derived from the Fund’s actual return, and the fourth column shows the dollar amount that would have been paid by an investor who started with $1,000 in the Fund. Investors may use the information here, together with the amount invested, to estimate the expenses paid over the period. Simply divide the Fund’s account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number provided under the heading “Expenses Paid During Period.”

Table 2. Based on hypothetical 5% return. This section is intended to help investors compare a Fund’s cost with those of other mutual funds. The table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses paid during the period. The example is useful in making comparisons because the U.S. Securities and Exchange Commission (the “SEC”) requires all mutual funds to calculate expenses based on the 5% return. Investors can assess a Fund’s costs by comparing this hypothetical example with the hypothetical examples that appear in shareholder reports of other funds.

The calculations illustrated above assume no shares were bought or sold during the period. Actual costs may have been higher or lower, depending on the amount of investment and the timing of any purchases or redemptions.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) on purchase payments, and contingent deferred sales charges (“CDSC”) on redemptions, if any. Therefore, the second table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

More information about a Fund’s expenses, including annual expense ratios for the past five years, can be found in the Financial Highlights section of this report. For additional information on operating expenses and other shareholder costs, please refer to the appropriate Fund prospectus.

THE GUGGENHEIM FUNDS ANNUAL REPORT | 5

ABOUT SHAREHOLDERS’ FUND EXPENSES (Unaudited) (continued)

| | | | | | | | | Beginning | | | Ending | | | Expenses | |

| | | Expense | | | Fund | | | Account Value | | | Account Value | | | Paid During | |

| | | Ratio1 | | | Return | | | March 31, 2012 | | | September 30, 2012 | | | Period2 | |

| Table 1. Based on actual Fund return3 | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| Large Cap Core Fund | | | | | | | | | | | | | | | | | | | | |

| A-Class | | | 2.09 | % | | | (0.38 | %) | | $ | 1,000.00 | | | $ | 996.20 | | | $ | 10.43 | |

| B-Class | | | 4.02 | % | | | (1.10 | %) | | | 1,000.00 | | | | 989.00 | | | | 19.99 | |

| C-Class | | | 3.37 | % | | | (0.85 | %) | | | 1,000.00 | | | | 991.50 | | | | 16.78 | |

| Institutional Class | | | 1.18 | % | | | (0.23 | %) | | | 1,000.00 | | | | 997.70 | | | | 5.89 | |

| | | | | | | | | | | | | | | | | | | | | |

| All Cap Value Fund | | | | | | | | | | | | | | | | | | | | |

| A-Class | | | 1.28 | % | | | (0.34 | %) | | | 1,000.00 | | | | 996.60 | | | | 6.39 | |

| C-Class | | | 2.03 | % | | | (0.70 | %) | | | 1,000.00 | | | | 993.00 | | | | 10.11 | |

| Institutional Class | | | 1.02 | % | | | (0.17 | %) | | | 1,000.00 | | | | 998.30 | | | | 5.10 | |

| | | | | | | | | | | | | | | | | | | | | |

| Mid Cap Value Fund | | | | | | | | | | | | | | | | | | | | |

| A-Class | | | 1.49 | % | | | (0.69 | %) | | | 1,000.00 | | | | 993.10 | | | | 7.42 | |

| B-Class | | | 2.44 | % | | | (1.18 | %) | | | 1,000.00 | | | | 988.20 | | | | 12.13 | |

| C-Class | | | 2.15 | % | | | (1.04 | %) | | | 1,000.00 | | | | 989.60 | | | | 10.69 | |

| | | | | | | | | | | | | | | | | | | | | |

| Mid Cap Value Institutional Fund | | | 1.05 | % | | | (0.18 | %) | | | 1,000.00 | | | | 998.20 | | | | 5.25 | |

| | | | | | | | | | | | | | | | | | | | | |

| Small Cap Growth Fund | | | | | | | | | | | | | | | | | | | | |

| A-Class | | | 2.15 | % | | | (2.86 | %) | | | 1,000.00 | | | | 971.40 | | | | 10.60 | |

| B-Class | | | 4.31 | % | | | (3.92 | %) | | | 1,000.00 | | | | 960.80 | | | | 21.13 | |

| C-Class | | | 2.89 | % | | | (3.20 | %) | | | 1,000.00 | | | | 968.00 | | | | 14.22 | |

| Institutional Class | | | 1.70 | % | | | (2.66 | %) | | | 1,000.00 | | | | 973.40 | | | | 8.39 | |

| | | | | | | | | | | | | | | | | | | | | |

| Small Cap Value Fund | | | | | | | | | | | | | | | | | | | | |

| A-Class | | | 1.30 | % | | | (1.44 | %) | | | 1,000.00 | | | | 985.60 | | | | 6.45 | |

| C-Class | | | 2.05 | % | | | (1.76 | %) | | | 1,000.00 | | | | 982.40 | | | | 10.16 | |

| Institutional Class | | | 1.05 | % | | | (1.36 | %) | | | 1,000.00 | | | | 986.40 | | | | 5.21 | |

| | | | | | | | | | | | | | | | | | | | | |

| Large Cap Concentrated Growth Fund | | | | | | | | | | | | | | | | | | | | |

| A-Class | | | 1.36 | % | | | (1.37 | %) | | | 1,000.00 | | | | 986.30 | | | | 6.75 | |

| B-Class | | | 2.11 | % | | | (1.75 | %) | | | 1,000.00 | | | | 982.50 | | | | 10.46 | |

| C-Class | | | 2.11 | % | | | (1.74 | %) | | | 1,000.00 | | | | 982.60 | | | | 10.46 | |

| Institutional Class | | | 1.07 | % | | | (1.16 | %) | | | 1,000.00 | | | | 988.40 | | | | 5.32 | |

| | | | | | | | | | | | | | | | | | | | | |

| MSCI EAFE Equal Weight Fund | | | | | | | | | | | | | | | | | | | | |

| A-Class | | | 1.65 | % | | | (3.74 | %) | | | 1,000.00 | | | | 962.60 | | | | 8.10 | |

| B-Class4 | | | 1.40 | % | | | (3.66 | %) | | | 1,000.00 | | | | 963.40 | | | | 6.87 | |

| C-Class | | | 2.40 | % | | | (4.05 | %) | | | 1,000.00 | | | | 959.50 | | | | 11.76 | |

| Institutional Class | | | 1.26 | % | | | (3.76 | %) | | | 1,000.00 | | | | 962.40 | | | | 6.18 | |

| | | | | | | | | | | | | | | | | | | | | |

| Alpha Opportunity Fund | | | | | | | | | | | | | | | | | | | | |

| A-Class | | | 2.22 | % | | | 2.62 | % | | | 1,000.00 | | | | 1,026.20 | | | | 11.25 | |

| B-Class | | | 2.98 | % | | | 2.18 | % | | | 1,000.00 | | | | 1,021.80 | | | | 15.06 | |

| C-Class | | | 2.96 | % | | | 2.18 | % | | | 1,000.00 | | | | 1,021.80 | | | | 14.96 | |

| Institutional Class | | | 1.96 | % | | | 3.35 | % | | | 1,000.00 | | | | 1,033.50 | | | | 9.96 | |

6 | THE GUGGENHEIM FUNDS ANNUAL REPORT

ABOUT SHAREHOLDERS’ FUND EXPENSES (Unaudited) (concluded)

| | | | | | | | | Beginning | | | Ending | | | Expenses | |

| | | Expense | | | Fund | | | Account Value | | | Account Value | | | Paid During | |

| | | Ratio1 | | | Return | | | March 31, 2012 | | | September 30, 2012 | | | Period2 | |

| Table 2. Based on hypothetical 5% return (before expenses) | | | | | | | | | |

| | | | | | | | | | |

| Large Cap Core Fund | | | | | | | | | | | | | | | | | | | | |

| A-Class | | | 2.09 | % | | | 5.00 | % | | $ | 1,000.00 | | | $ | 1,014.55 | | | $ | 10.53 | |

| B-Class | | | 4.02 | % | | | 5.00 | % | | | 1,000.00 | | | | 1,004.90 | | | | 20.15 | |

| C-Class | | | 3.37 | % | | | 5.00 | % | | | 1,000.00 | | | | 1,008.15 | | | | 16.92 | |

| Institutional Class | | | 1.18 | % | | | 5.00 | % | | | 1,000.00 | | | | 1,019.10 | | | | 5.96 | |

| | | | | | | | | | | | | | | | | | | | | |

| All Cap Value Fund | | | | | | | | | | | | | | | | | | | | |

| A-Class | | | 1.28 | % | | | 5.00 | % | | | 1,000.00 | | | | 1,018.60 | | | | 6.46 | |

| C-Class | | | 2.03 | % | | | 5.00 | % | | | 1,000.00 | | | | 1,014.85 | | | | 10.23 | |

| Institutional Class | | | 1.02 | % | | | 5.00 | % | | | 1,000.00 | | | | 1,019.90 | | | | 5.15 | |

| | | | | | | | | | | | | | | | | | | | | |

| Mid Cap Value Fund | | | | | | | | | | | | | | | | | | | | |

| A-Class | | | 1.49 | % | | | 5.00 | % | | | 1,000.00 | | | | 1,017.55 | | | | 7.52 | |

| B-Class | | | 2.44 | % | | | 5.00 | % | | | 1,000.00 | | | | 1,012.80 | | | | 12.28 | |

| C-Class | | | 2.15 | % | | | 5.00 | % | | | 1,000.00 | | | | 1,014.25 | | | | 10.83 | |

| | | | | | | | | | | | | | | | | | | | | |

| Mid Cap Value Institutional Fund | | | 1.05 | % | | | 5.00 | % | | | 1,000.00 | | | | 1,019.75 | | | | 5.30 | |

| | | | | | | | | | | | | | | | | | | | | |

| Small Cap Growth Fund | | | | | | | | | | | | | | | | | | | | |

| A-Class | | | 2.15 | % | | | 5.00 | % | | | 1,000.00 | | | | 1,014.25 | | | | 10.83 | |

| B-Class | | | 4.31 | % | | | 5.00 | % | | | 1,000.00 | | | | 1,003.45 | | | | 21.59 | |

| C-Class | | | 2.89 | % | | | 5.00 | % | | | 1,000.00 | | | | 1,010.55 | | | | 14.53 | |

| Institutional Class | | | 1.70 | % | | | 5.00 | % | | | 1,000.00 | | | | 1,016.50 | | | | 8.57 | |

| | | | | | | | | | | | | | | | | | | | | |

| Small Cap Value Fund | | | | | | | | | | | | | | | | | | | | |

| A-Class | | | 1.30 | % | | | 5.00 | % | | | 1,000.00 | | | | 1,018.50 | | | | 6.56 | |

| C-Class | | | 2.05 | % | | | 5.00 | % | | | 1,000.00 | | | | 1,014.75 | | | | 10.33 | |

| Institutional Class | | | 1.05 | % | | | 5.00 | % | | | 1,000.00 | | | | 1,019.75 | | | | 5.30 | |

| | | | | | | | | | | | | | | | | | | | | |

| Large Cap Concentrated Growth Fund | | | | | | | | | | | | | | | | | | | | |

| A-Class | | | 1.36 | % | | | 5.00 | % | | | 1,000.00 | | | | 1,018.20 | | | | 6.86 | |

| B-Class | | | 2.11 | % | | | 5.00 | % | | | 1,000.00 | | | | 1,014.45 | | | | 10.63 | |

| C-Class | | | 2.11 | % | | | 5.00 | % | | | 1,000.00 | | | | 1,014.45 | | | | 10.63 | |

| Institutional Class | | | 1.07 | % | | | 5.00 | % | | | 1,000.00 | | | | 1,019.65 | | | | 5.40 | |

| | | | | | | | | | | | | | | | | | | | | |

| MSCI EAFE Equal Weight Fund | | | | | | | | | | | | | | | | | | | | |

| A-Class | | | 1.65 | % | | | 5.00 | % | | | 1,000.00 | | | | 1,016.75 | | | | 8.32 | |

| B-Class4 | | | 1.40 | % | | | 5.00 | % | | | 1,000.00 | | | | 1,018.00 | | | | 7.06 | |

| C-Class | | | 2.40 | % | | | 5.00 | % | | | 1,000.00 | | | | 1,013.00 | | | | 12.08 | |

| Institutional Class | | | 1.26 | % | | | 5.00 | % | | | 1,000.00 | | | | 1,018.70 | | | | 6.36 | |

| | | | | | | | | | | | | | | | | | | | | |

| Alpha Opportunity Fund | | | | | | | | | | | | | | | | | | | | |

| A-Class | | | 2.22 | % | | | 5.00 | % | | | 1,000.00 | | | | 1,013.90 | | | | 11.18 | |

| B-Class | | | 2.98 | % | | | 5.00 | % | | | 1,000.00 | | | | 1,010.10 | | | | 14.98 | |

| C-Class | | | 2.96 | % | | | 5.00 | % | | | 1,000.00 | | | | 1,010.20 | | | | 14.88 | |

| Institutional Class | | | 1.96 | % | | | 5.00 | % | | | 1,000.00 | | | | 1,015.20 | | | | 9.87 | |

| 1 | Annualized and excludes expenses of the underlying funds in which the Funds invest. This ratio represents net expenses, which includes dividends on short sales and prime broker interest expenses. Excluding these expenses, the operating expense ratio of the Alpha Opportunity Fund would be 0.10%, 0.10%, 0.10%, and 0.10% lower for the A-Class, B-Class, C-Class and Institutional Class, respectively. |

| 2 | Expenses are equal to the Fund’s annualized expense ratio, net of any applicable fee waivers, multiplied by the average account value over the period, multiplied by 183/366 (to reflect the one-half year period). |

| 3 | Actual cumulative return at net asset value for the period March 31, 2012 to September 30, 2012. |

| 4 | B-Class shares did not charge 12b-1 fees during the period. |

THE GUGGENHEIM FUNDS ANNUAL REPORT | 7

| MANAGER’S COMMENTARY (Unaudited) | September 30, 2012 |

To Our Shareholders:

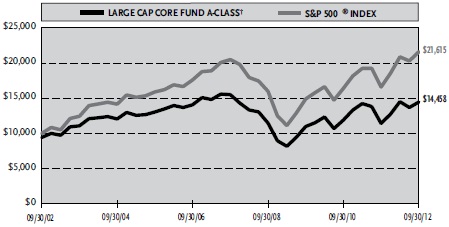

For the fiscal year ended September 30, 2012, the Large Cap Core Fund returned 26.71%1, while the benchmark, the S&P 500® Index, gained 30.20%. The Fund pursues its objective by investing 50% of its total assets according to a large cap growth strategy and approximately 50% to a large cap value strategy. The managers rebalance if either strategy equals or exceeds 60% of total assets. The managers use a blended approach, investing in growth stocks and value stocks, and may invest in a limited number of industries and sectors.

The large cap growth manager chooses growth-oriented companies through a combination of a qualitative top-down approach in reviewing growth trends that are based on several fixed-income factors, along with a quantitative fundamental bottom-up approach. The large cap value manager chooses securities of companies that appear to be undervalued relative to assets, growth potential and cash flow. The managers sell a security when the reasons for buying it no longer apply or when the company begins to show deteriorating fundamentals or poor performance.

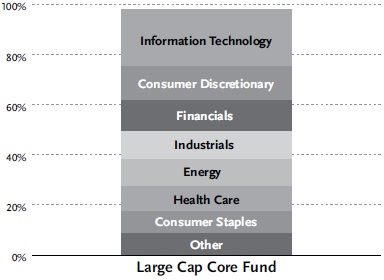

Contributing to the portfolio return were stock selection in the Consumer Discretionary sector, which was the best-performing sector in the Fund and the benchmark, and both stock selection and an overweight in the Financials sector. However, this was not enough to offset poor stock selection in both the Health Care and Information Technology sectors.

The holdings contributing most to return were Apple, Inc., Wells Fargo & Co. and Equifax, Inc. Leading detractors from performance were Caterpillar, Inc., Anadarko Petroleum Corp. and DeVry, Inc.

From the growth perspective, our fixed income indicators, including the slope of the yield curve and corporate bond spreads, alternated during the fiscal year, but in the third quarter of 2012 turned positive, which led us to add beta back into the portfolio relative to the benchmark. We believe equity markets can build on strong performance in the third quarter and move higher before the end of 2012. We will focus our attention on secular growth names in the year to come, with an eye towards more cyclical names if the global economy can find firmer footing.

In the value side of the portfolio, we remain focused on searching for companies we think have good long-term fundamental prospects and attractive valuations that are likely to generate strong performance relative to the broader market, regardless of macroeconomic events.

We appreciate your business and the trust you place in us.

Sincerely,

Mark Bronzo, CFA, Portfolio Manager

Mark A. Mitchell, CFA, Portfolio Manager

Performance displayed represents past performance which is no guarantee of future results.

1 Performance figures are based on A-Class shares and do not reflect deduction of the sales charges or taxes that a shareholder would pay on distributions or the redemption of shares.

This fund may not be suitable for all investors. • Value stocks are subject to the risk that the intrinsic value of the stock may never be realized by the market or that the stocks price will decline in value. • Growth stocks may be more volatile than other stocks because they are more sensitive to investor perceptions regarding the growth potential of the issuing company.

The opinions and forecasts expressed may not actually come to pass. This information is subject to change at any time, based on market and other conditions, and should not be construed as a recommendation of any specific security or strategy.

8 | THE GUGGENHEIM FUNDS ANNUAL REPORT

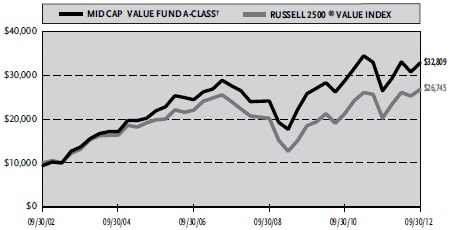

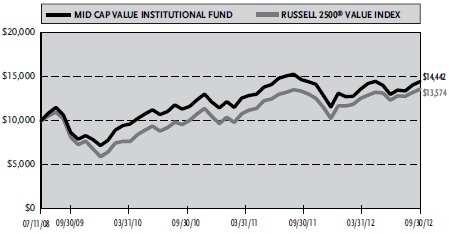

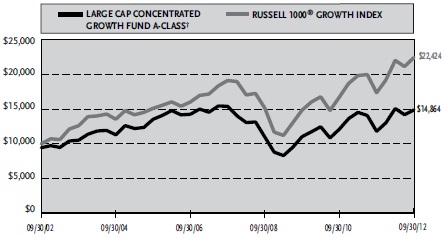

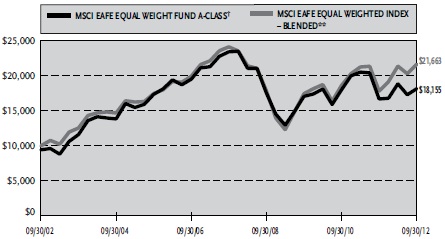

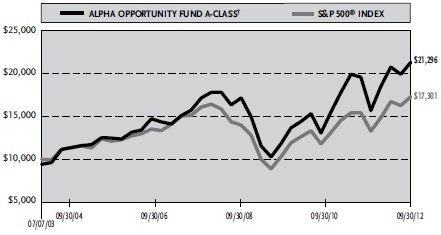

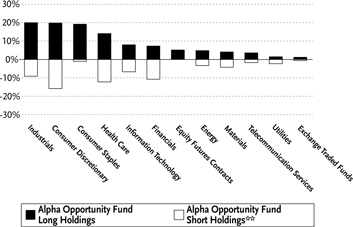

| PERFORMANCE REPORT AND FUND PROFILE (Unaudited) | September 30, 2012 |

LARGE CAP CORE FUND

OBJECTIVE: Seeks long-term growth of capital.

Cumulative Fund Performance*

Average Annual Returns*

Periods Ended 09/30/12

| | | 1 Year | | | 5 Year | | | 10 Year | |

| A-Class Shares | | | 26.71 | % | | | -1.42 | % | | | 4.37 | % |

| A-Class Shares with sales charge† | | | 20.68 | % | | | -2.58 | % | | | 3.76 | % |

| B-Class Shares | | | 25.13 | % | | | -2.23 | % | | | 3.76 | % |

| B-Class Shares with CDSC‡ | | | 20.13 | % | | | -2.55 | % | | | 3.76 | % |

| C-Class Shares | | | 25.59 | % | | | -2.15 | % | | | 3.60 | % |

| C-Class Shares with CDSC§ | | | 24.59 | % | | | -2.15 | % | | | 3.60 | % |

| S&P 500 Index | | | 30.20 | % | | | 1.05 | % | | | 8.01 | % |

| | | | | | | | | | | | | |

| | | Since Inception | |

| | | (03/01/12) | |

| Institutional Class Shares | | | 2.11 | % |

| S&P 500 Index | | | 6.17 | % |

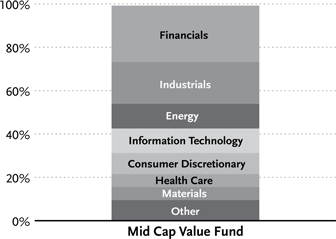

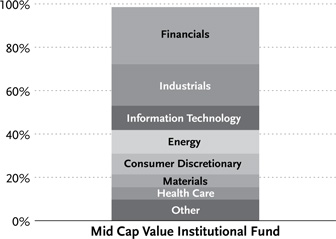

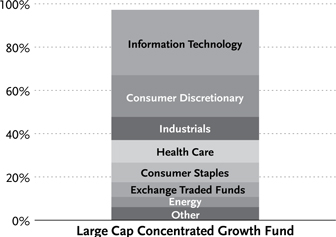

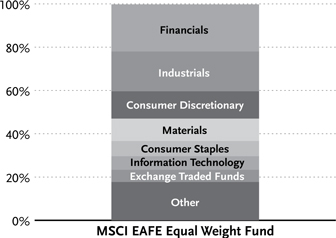

Holdings Diversification (Market Exposure as % of Net Assets)

“Holdings Diversification (Market Exposure as % of Net Assets)” excludes any temporary cash investments.

| Inception Dates: | |

| A-Class | September 10, 1962 |

| B-Class | October 19, 1993 |

| C-Class | January 29, 1999 |

| Institutional Class | March 1, 2012 |

| Ten Largest Holdings (% of Total Net Assets) |

| Apple, Inc. | 4.6% |

| Wells Fargo & Co. | 3.4% |

| Covidien plc | 3.0% |

| Mondelez International, Inc. — Class A | 2.7% |

| Google, Inc. — Class A | 2.6% |

| iShares Russell 1000 Growth Index Fund | 2.3% |

| Microsoft Corp. | 2.2% |

| Costco Wholesale Corp. | 2.0% |

| Express Scripts Holding Co. | 1.9% |

| Chevron Corp. | 1.9% |

| Top Ten Total | 26.6% |

“Ten Largest Holdings” exclude any temporary cash or derivative investments.

| * | The performance data above represents past performance that is not predictive of future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Returns are historical and include changes in principal and reinvested dividends and capital gains and do not reflect the effect of taxes. The S&P 500 Index is an unmanaged index and, unlike the Fund, has no management fees or operating expenses to reduce its reported return. |

| † | Effective February 22, 2011, the maximum sales charge decreased from 5.75% to 4.75%. A 5.75% maximum sales charge is used in the calculation of the 5 Year and 10 Year Average Annual Returns (based on subscriptions made prior to February 22, 2011), and a 4.75% maximum sales charge will be used to calculate performance for periods based on subscriptions made on or after February 22, 2011. |

| ‡ | Fund returns include a CDSC of up to 5% if redeemed within 5 years of purchase. |

| § | Fund returns include a CDSC of 1% if redeemed within 12 months of purchase. |

THE GUGGENHEIM FUNDS ANNUAL REPORT | 9

| SCHEDULE OF INVESTMENTS | September 30, 2012 |

| LARGE CAP CORE FUND |

| | | Shares | | | Value | |

| COMMON STOCKS† - 93.8% | | | | | | | | |

| | | | | | | | | |

| INFORMATION TECHNOLOGY - 22.7% | | | | | | | | |

| Apple, Inc. | | | 12,350 | | | $ | 8,240,660 | |

| Google, Inc. — Class A* | | | 6,035 | | | | 4,553,407 | |

| Microsoft Corp. | | | 129,750 | | | | 3,863,955 | |

| International Business Machines Corp. | | | 14,850 | | | | 3,080,633 | |

| eBay, Inc.* | | | 63,550 | | | | 3,076,456 | |

| Western Union Co. | | | 155,900 | | | | 2,840,498 | |

| EMC Corp.* | | | 90,700 | | | | 2,473,389 | |

| Broadcom Corp. — Class A | | | 68,760 | | | | 2,377,721 | |

| TE Connectivity Ltd. | | | 66,700 | | | | 2,268,467 | |

| Computer Sciences Corp. | | | 70,200 | | | | 2,261,142 | |

| Oracle Corp. | | | 60,800 | | | | 1,914,592 | |

| Cisco Systems, Inc. | | | 86,900 | | | | 1,658,921 | |

| Hewlett-Packard Co. | | | 63,816 | | | | 1,088,701 | |

| NetApp, Inc.* | | | 19,090 | | | | 627,679 | |

| Mercury Computer Systems, Inc.* | | | 19,190 | | | | 203,798 | |

| Total Information Technology | | | | | | | 40,530,019 | |

| CONSUMER DISCRETIONARY - 13.6% | | | | | | | | |

| Home Depot, Inc. | | | 51,750 | | | | 3,124,148 | |

| Walt Disney Co. | | | 59,656 | | | | 3,118,815 | |

| Comcast Corp. — Class A | | | 83,300 | | | | 2,979,641 | |

| Target Corp. | | | 44,700 | | | | 2,837,109 | |

| Nordstrom, Inc. | | | 51,150 | | | | 2,822,457 | |

| Time Warner, Inc. | | | 59,566 | | | | 2,700,127 | |

| Lowe’s Companies, Inc. | | | 72,000 | | | | 2,177,280 | |

| Starwood Hotels & | | | | | | | | |

| Resorts Worldwide, Inc. | | | 35,100 | | | | 2,034,396 | |

| BorgWarner, Inc.* | | | 28,700 | | | | 1,983,457 | |

| DeVry, Inc. | | | 24,100 | | | | 548,516 | |

| Total Consumer Discretionary | | | | | | | 24,325,946 | |

| FINANCIALS - 12.4% | | | | | | | | |

| Wells Fargo & Co. | | | 173,278 | | | | 5,983,289 | |

| Aon plc | | | 50,100 | | | | 2,619,729 | |

| U.S. Bancorp | | | 69,326 | | | | 2,377,882 | |

| Berkshire Hathaway, Inc. — Class A* | | | 16 | | | | 2,123,200 | |

| American International Group, Inc.* | | | 55,652 | | | | 1,824,829 | |

| JPMorgan Chase & Co. | | | 41,770 | | | | 1,690,850 | |

| Allstate Corp. | | | 40,300 | | | | 1,596,283 | |

| State Street Corp. | | | 34,200 | | | | 1,435,032 | |

| BB&T Corp. | | | 42,012 | | | | 1,393,118 | |

| Progressive Corp. | | | 53,000 | | | | 1,099,220 | |

| Total Financials | | | | | | | 22,143,432 | |

| INDUSTRIALS - 11.1% | | | | | | | | |

| Honeywell International, Inc. | | | 50,190 | | | | 2,998,852 | |

| Caterpillar, Inc. | | | 33,250 | | | | 2,860,830 | |

| CSX Corp. | | | 127,550 | | | | 2,646,663 | |

| AMETEK, Inc. | | | 56,550 | | | | 2,004,698 | |

| Republic Services, Inc. — Class A | | | 61,700 | | | | 1,697,367 | |

| Equifax, Inc. | | | 35,810 | | | | 1,668,030 | |

| URS Corp. | | | 47,104 | | | | 1,663,242 | |

| United Technologies Corp. | | | 21,000 | | | | 1,644,089 | |

| Quanta Services, Inc.* | | | 52,200 | | | | 1,289,340 | |

| Parker Hannifin Corp. | | | 14,070 | | | | 1,175,971 | |

| GeoEye, Inc.* | | | 2,930 | | | | 77,440 | |

| Total Industrials | | | | | | | 19,726,522 | |

| ENERGY - 10.7% | | | | | | | | |

| Chevron Corp. | | | 28,940 | | | | 3,373,246 | |

| Williams Companies, Inc. | | | 76,100 | | | | 2,661,217 | |

| Schlumberger Ltd. | | | 33,150 | | | | 2,397,741 | |

| Ensco plc — Class A | | | 40,800 | | | | 2,226,048 | |

| McDermott International, Inc.* | | | 152,138 | | | | 1,859,126 | |

| Apache Corp. | | | 19,335 | | | | 1,671,897 | |

| Halliburton Co. | | | 39,400 | | | | 1,327,386 | |

| Exxon Mobil Corp. | | | 14,240 | | | | 1,302,248 | |

| ConocoPhillips | | | 14,400 | | | | 823,392 | |

| Chesapeake Energy Corp. | | | 35,400 | | | | 667,998 | |

| WPX Energy, Inc.* | | | 25,366 | | | | 420,822 | |

| Phillips 66 | | | 7,200 | | | | 333,864 | |

| Total Energy | | | | | | | 19,064,985 | |

| HEALTH CARE - 10.0% | | | | | | | | |

| Covidien plc | | | 90,200 | | | | 5,359,684 | |

| Express Scripts Holding Co.* | | | 55,200 | | | | 3,459,384 | |

| Biogen Idec, Inc.* | | | 20,200 | | | | 3,014,446 | |

| Aetna, Inc. | | | 68,300 | | | | 2,704,680 | |

| Forest Laboratories, Inc.* | | | 33,800 | | | | 1,203,618 | |

| UnitedHealth Group, Inc. | | | 20,700 | | | | 1,146,987 | |

| Teva Pharmaceutical Industries Ltd. ADR | | | 21,420 | | | | 887,002 | |

| Total Health Care | | | | | | | 17,775,801 | |

| CONSUMER STAPLES - 8.7% | | | | | | | | |

| Mondelez International, Inc. — Class A | | | 115,400 | | | | 4,771,790 | |

| Costco Wholesale Corp. | | | 35,900 | | | | 3,594,487 | |

| PepsiCo, Inc. | | | 40,900 | | | | 2,894,493 | |

| CVS Caremark Corp. | | | 45,880 | | | | 2,221,510 | |

| Wal-Mart Stores, Inc. | | | 27,700 | | | | 2,044,260 | |

| Total Consumer Staples | | | | | | | 15,526,540 | |

| MATERIALS - 2.6% | | | | | | | | |

| EI du Pont de Nemours & Co. | | | 59,000 | | | | 2,965,930 | |

| Dow Chemical Co. | | | 59,300 | | | | 1,717,328 | |

| Total Materials | | | | | | | 4,683,258 | |

| UTILITIES - 1.6% | | | | | | | | |

| Edison International | | | 61,800 | | | | 2,823,642 | |

| TELECOMMUNICATION SERVICES - 0.4% | | | | | | | | |

| Windstream Corp. | | | 75,500 | | | | 763,305 | |

| Total Common Stocks | | | | | | | | |

| (Cost $143,792,044) | | | | | | | 167,363,450 | |

| 10 | THE GUGGENHEIM FUNDS ANNUAL REPORT | SEE NOTES TO FINANCIAL STATEMENTS. |

| SCHEDULE OF INVESTMENTS (concluded) | September 30, 2012 |

| LARGE CAP CORE FUND |

| | | Shares | | | Value | |

| EXCHANGE TRADED FUNDS† - 4.2% | | | | | | | | |

| iShares Russell 1000 Growth Index Fund | | | 61,450 | | | $ | 4,098,715 | |

| Financial Select Sector SPDR Fund | | | 162,050 | | | | 2,527,980 | |

| iShares Russell 1000 Value Index Fund | | | 11,370 | | | | 820,687 | |

| Total Exchange Traded Funds | | | | | | | | |

| (Cost $7,003,421) | | | | | | | 7,447,382 | |

| Total Investments - 98.0% | | | | | | | | |

| (Cost $150,795,465) | | | | | | $ | 174,810,832 | |

| Other Assets & Liabilities, net - 2.0% | | | | | | | 3,489,961 | |

| Total Net Assets - 100.0% | | | | | | $ | 178,300,793 | |

| * | Non-income producing security. |

| † | Value determined based on Level 1 inputs — See Note 4. |

| | ADR — American Depositary Receipt |

| | plc — Public Limited Company |

| SEE NOTES TO FINANCIAL STATEMENTS. | THE GUGGENHEIM FUNDS ANNUAL REPORT | 11 |

STATEMENT OF ASSETS

AND LIABILITIES

September 30, 2012

| Assets: | | | | |

| Investments, at value | | | | |

| (cost $150,795,465) | | $ | 174,810,832 | |

| Cash | | | 3,713,667 | |

| Prepaid expenses | | | 26,991 | |

| Receivables: | | | | |

| Dividends | | | 206,502 | |

| Fund shares sold | | | 11,234 | |

| Total assets | | | 178,769,226 | |

| Liabilities: | | | | |

| Payable for: | | | | |

| Fund shares redeemed | | | 133,348 | |

| Management fees | | | 112,453 | |

| Securities purchased | | | 60,290 | |

| Distribution and service fees | | | 41,468 | |

| Transfer agent/maintenance fees | | | 26,398 | |

| Fund accounting/administration fees | | | 14,244 | |

| Directors’ fees* | | | 9,930 | |

| Miscellaneous | | | 70,302 | |

| Total liabilities | | | 468,433 | |

| Net assets | | $ | 178,300,793 | |

| Net assets consist of: | | | | |

| Paid in capital | | $ | 167,090,453 | |

| Undistributed net investment income | | | 317,574 | |

| Accumulated net realized loss on investments | | | (13,122,601 | ) |

| Net unrealized appreciation on investments | | | 24,015,367 | |

| Net assets | | $ | 178,300,793 | |

| A-Class: | | | | |

| Net assets | | $ | 171,906,977 | |

| Capital shares outstanding | | | 8,088,533 | |

| Net asset value per share | | $ | 21.25 | |

| Maximum offering price per share | | | | |

| (Net asset value divided by 95.25%) | | $ | 22.31 | |

| B-Class: | | | | |

| Net assets | | $ | 4,714,333 | |

| Capital shares outstanding | | | 275,202 | |

| Net asset value per share | | $ | 17.13 | |

| C-Class: | | | | |

| Net assets | | $ | 1,669,271 | |

| Capital shares outstanding | | | 89,738 | |

| Net asset value per share | | $ | 18.60 | |

| Institutional Class: | | | | |

| Net assets | | $ | 10,212 | |

| Capital shares outstanding | | | 480 | |

| Net asset value per share | | $ | 21.28 | |

STATEMENT OF

OPERATIONS

Year Ended September 30, 2012

| Investment Income: | | | | |

| Dividends | | $ | 3,070,554 | |

| Interest | | | 1,258 | |

| Total investment income | | | 3,071,812 | |

| | | | | |

| Expenses: | | | | |

| Management fees | | | 1,372,286 | |

| Transfer agent/maintenance fees | | | | |

| A-Class | | | 309,822 | |

| B-Class | | | 33,608 | |

| C-Class | | | 4,976 | |

| Institutional Class | | | 10 | |

| Distribution and service fees: | | | | |

| A-Class | | | 440,201 | |

| B-Class | | | 51,560 | |

| C-Class | | | 17,294 | |

| Fund accounting/administration fees | | | 173,821 | |

| Directors’ fees* | | | 23,920 | |

| Custodian fees | | | 9,901 | |

| Miscellaneous | | | 131,811 | |

| Total expenses | | | 2,569,210 | |

| Net investment income | | | 502,602 | |

| | | | | |

| Net Realized and Unrealized Gain (Loss): | | | | |

| Net realized gain (loss) on: | | | | |

| Investments | | | 5,620,024 | |

| Options written | | | 21,833 | |

| Net realized gain | | | 5,641,857 | |

| Net change in unrealized appreciation | | | | |

| (depreciation) on: | | | | |

| Investments | | | 36,163,920 | |

| Options written | | | (4,934 | ) |

| Net change in unrealized appreciation | | | | |

| (depreciation) | | | 36,158,986 | |

| Net realized and unrealized gain | | | 41,800,843 | |

| Net increase in net assets resulting | | | | |

| from operations | | $ | 42,303,445 | |

* Relates to Directors not deemed “interested persons” within the meaning of Section 2(a)(19) of the 1940 Act.

| 12 | THE GUGGENHEIM FUNDS ANNUAL REPORT | SEE NOTES TO FINANCIAL STATEMENTS. |

STATEMENTS OF CHANGES IN NET ASSETS

| | | Year Ended | | | Year Ended | |

| | | September 30, | | | September 30, | |

| | | 2012 | | | 2011 | |

| Increase (Decrease) In Net Assets From Operations: | | | | | | | | |

| Net investment income | | $ | 502,602 | | | $ | 54,220 | |

| Net realized gain on investments | | | 5,641,857 | | | | 15,933,509 | |

| Net change in unrealized appreciation (depreciation) on investments | | | 36,158,986 | | | | (21,397,112 | ) |

| Net increase (decrease) in net assets resulting from operations | | | 42,303,445 | | | | (5,409,383 | ) |

| | | | | | | | | |

| Distributions to shareholders from: | | | | | | | | |

| Net investment income | | | | | | | | |

| A-Class | | | (200,274 | ) | | | (546,823 | ) |

| Total distributions to shareholders | | | (200,274 | ) | | | (546,823 | ) |

| | | | | | | | | |

| Capital share transactions: | | | | | | | | |

| Proceeds from sale of shares | | | | | | | | |

| A-Class | | | 3,926,067 | | | | 9,715,889 | |

| B-Class | | | 147,411 | | | | 1,180,154 | |

| C-Class | | | 118,320 | | | | 177,237 | |

| Institutional Class1 | | | 10,000 | | | | — | |

| Distributions reinvested | | | | | | | | |

| A-Class | | | 187,685 | | | | 502,041 | |

| Cost of shares redeemed | | | | | | | | |

| A-Class | | | (28,967,385 | ) | | | (22,520,161 | ) |

| B-Class | | | (1,734,071 | ) | | | (2,775,354 | ) |

| C-Class | | | (443,550 | ) | | | (716,944 | ) |

| Institutional Class1 | | | — | | | | — | |

| Net decrease from capital share transactions | | | (26,755,523 | ) | | | (14,437,138 | ) |

| Net increase (decrease) in net assets | | | 15,347,648 | | | | (20,393,344 | ) |

| | | | | | | | | |

| Net assets: | | | | | | | | |

| Beginning of year | | | 162,953,145 | | | | 183,346,489 | |

| End of year | | $ | 178,300,793 | | | $ | 162,953,145 | |

| Undistributed net investment income at end of year | | $ | 317,574 | | | $ | 13,084 | |

| | | | | | | | | |

| Capital share activity: | | | | | | | | |

| Shares sold | | | | | | | | |

| A-Class | | | 200,433 | | | | 493,303 | 2 |

| B-Class | | | 9,082 | | | | 73,162 | 2 |

| C-Class | | | 7,018 | | | | 10,210 | 2 |

| Institutional Class1 | | | 480 | | | | — | |

| Shares issued from reinvestment of distributions | | | | | | | | |

| A-Class | | | 10,201 | | | | 26,342 | 2 |

| Shares redeemed | | | | | | | | |

| A-Class | | | (1,425,434 | ) | | | (1,144,274 | )2 |

| B-Class | | | (108,033 | ) | | | (172,978 | )2 |

| C-Class | | | (25,344 | ) | | | (40,853 | )2 |

| Institutional Class1 | | | — | | | | — | |

| Net decrease in shares | | | (1,331,597 | ) | | | (755,088 | ) |

| 1 | Since the commencement of operations: March 1, 2012. |

| 2 | The share activity for the period October 1, 2010 through April 8, 2011 has been restated to reflect a 1:4 reverse share split effective April 8, 2011. |

| SEE NOTES TO FINANCIAL STATEMENTS. | THE GUGGENHEIM FUNDS ANNUAL REPORT | 13 |

FINANCIAL HIGHLIGHTS

This table is presented to show selected data for a share outstanding throughout each period and to assist shareholders in evaluating a Fund’s performance for the periods presented.

| | | Year Ended | | | Year Ended | | | Year Ended | | | Year Ended | | | Year Ended | |

| | | September 30, | | | September 30, | | | September 30, | | | September 30, | | | September 30, | |

| A-Class | | 2012 | | | 2011e | | | 2010e | | | 2009e | | | 2008e | |

| Per Share Data | | | | | | | | | | | | | | | | | | | | |

| Net asset value, beginning of period | | $ | 16.79 | | | $ | 17.56 | | | $ | 16.20 | | | $ | 17.04 | | | $ | 27.36 | |

| Income (loss) from investment operations: | | | | | | | | | | | | | | | | | | | | |

| Net investment incomea | | | .06 | | | | .01 | | | | .04 | | | | .04 | | | | .04 | |

| Net gain (loss) on investments | | | | | | | | | | | | | | | | | | | | |

| (realized and unrealized) | | | 4.42 | | | | (.74 | ) | | | 1.32 | | | | (.80 | ) | | | (6.44 | ) |

| Total from investment operations | | | 4.48 | | | | (.73 | ) | | | 1.36 | | | | (.76 | ) | | | (6.40 | ) |

| Less distributions from: | | | | | | | | | | | | | | | | | | | | |

| Net investment income | | | (.02 | ) | | | (.04 | ) | | | — | | | | (.04 | ) | | | — | |

| Net realized gains | | | — | | | | — | | | | — | | | | — | | | | (3.88 | ) |

| Return of capital | | | — | | | | — | | | | — | | | | (.04 | ) | | | (.04 | ) |

| Total distributions | | | (.02 | ) | | | (.04 | ) | | | — | | | | (.08 | ) | | | (3.92 | ) |

| Net asset value, end of period | | $ | 21.25 | | | $ | 16.79 | | | $ | 17.56 | | | $ | 16.20 | | | $ | 17.04 | |

| | | | | | | | | | | | | | | | | | | | | |

| Total Returnb | | | 26.71 | % | | | (4.11 | %) | | | 8.40 | % | | | (4.32 | %) | | | (26.12 | %) |

| Ratios/Supplemental Data | | | | | | | | | | | | | | | | | | | | |

| Net assets, end of period (in thousands) | | $ | 171,907 | | | $ | 156,232 | | | $ | 174,371 | | | $ | 175,404 | | | $ | 205,908 | |

| Ratios to average net assets: | | | | | | | | | | | | | | | | | | | | |

| Net investment income | | | 0.32 | % | | | 0.06 | % | | | 0.31 | % | | | 0.28 | % | | | 0.15 | % |

| Total expensesc | | | 1.36 | % | | | 1.35 | % | | | 1.43 | % | | | 1.49 | % | | | 1.36 | % |

| Portfolio turnover rate | | | 101 | % | | | 92 | % | | | 100 | % | | | 69 | % | | | 111 | % |

| | | Year Ended | | | Year Ended | | | Year Ended | | | Year Ended | | | Year Ended | |

| | | September 30, | | | September 30, | | | September 30, | | | September 30, | | | September 30, | |

| B-Class | | 2012 | | | 2011e | | | 2010e | | | 2009e | | | 2008e | |

| Per Share Data | | | | | | | | | | | | | | | | | | | | |

| Net asset value, beginning of period | | $ | 13.69 | | | $ | 14.40 | | | $ | 13.36 | | | $ | 14.12 | | | $ | 23.56 | |

| Income (loss) from investment operations: | | | | | | | | | | | | | | | | | | | | |

| Net investment lossa | | | (.15 | ) | | | (.11 | ) | | | (.08 | ) | | | (.04 | ) | | | (.12 | ) |

| Net gain (loss) on investments | | | | | | | | | | | | | | | | | | | | |

| (realized and unrealized) | | | 3.59 | | | | (.60 | ) | | | 1.12 | | | | (.68 | ) | | | (5.40 | ) |

| Total from investment operations | | | 3.44 | | | | (.71 | ) | | | 1.04 | | | | (.72 | ) | | | (5.52 | ) |

| Less distributions from: | | | | | | | | | | | | | | | | | | | | |

| Net realized gains | | | — | | | | — | | | | — | | | | — | | | | (3.88 | ) |

| Return of capital | | | — | | | | — | | | | — | | | | (.04 | ) | | | (.04 | ) |

| Total distributions | | | — | | | | — | | | | — | | | | (.04 | ) | | | (3.92 | ) |

| Net asset value, end of period | | $ | 17.13 | | | $ | 13.69 | | | $ | 14.40 | | | $ | 13.36 | | | $ | 14.12 | |

| | | | | | | | | | | | | | | | | | | | | |

| Total Returnb | | | 25.13 | % | | | (4.93 | %) | | | 7.78 | % | | | (4.96 | %) | | | (26.69 | %) |

| Ratios/Supplemental Data | | | | | | | | | | | | | | | | | | | | |

| Net assets, end of period (in thousands) | | $ | 4,714 | | | $ | 5,121 | | | $ | 6,817 | | | $ | 7,784 | | | $ | 10,621 | |

| Ratios to average net assets: | | | | | | | | | | | | | | | | | | | | |

| Net investment loss | | | (0.92 | %) | | | (0.70 | %) | | | (0.48 | %) | | | (0.46 | %) | | | (0.61 | %) |

| Total expensesc | | | 2.59 | % | | | 2.10 | % | | | 2.17 | % | | | 2.24 | % | | | 2.11 | % |

| Portfolio turnover rate | | | 101 | % | | | 92 | % | | | 100 | % | | | 69 | % | | | 111 | % |

| 14 | THE GUGGENHEIM FUNDS ANNUAL REPORT | SEE NOTES TO FINANCIAL STATEMENTS. |

FINANCIAL HIGHLIGHTS (concluded)

This table is presented to show selected data for a share outstanding throughout each period and to assist shareholders in evaluating a Fund’s performance for the periods presented.

| | | Year Ended | | | Year Ended | | | Year Ended | | | Year Ended | | | Year Ended | |

| | | September 30, | | | September 30, | | | September 30, | | | September 30, | | | September 30, | |

| C-Class | | 2012 | | | 2011e | | | 2010e | | | 2009e | | | 2008e | |

| Per Share Data | | | | | | | | | | | | | | | | | | | | |

| Net asset value, beginning of period | | $ | 14.81 | | | $ | 15.56 | | | $ | 14.48 | | | $ | 15.24 | | | $ | 25.12 | |

| Income (loss) from investment operations: | | | | | | | | | | | | | | | | | | | | |

| Net investment lossa | | | (.10 | ) | | | (.12 | ) | | | (.08 | ) | | | (.04 | ) | | | (.12 | ) |

| Net gain (loss) on investments | | | | | | | | | | | | | | | | | | | | |

| (realized and unrealized) | | | 3.89 | | | | (.63 | ) | | | 1.16 | | | | (.68 | ) | | | (5.84 | ) |

| Total from investment operations | | | 3.79 | | | | (.75 | ) | | | 1.08 | | | | (.72 | ) | | | (5.96 | ) |

| Less distributions from: | | | | | | | | | | | | | | | | | | | | |

| Net realized gains | | | — | | | | — | | | | — | | | | — | | | | (3.88 | ) |

| Return of capital | | | — | | | | — | | | | — | | | | (.04 | ) | | | (.04 | ) |

| Total distributions | | | — | | | | — | | | | — | | | | (.04 | ) | | | (3.92 | ) |

| Net asset value, end of period | | $ | 18.60 | | | $ | 14.81 | | | $ | 15.56 | | | $ | 14.48 | | | $ | 15.24 | |

| | | | | | | | | | | | | | | | | | | | | |

| Total Returnb | | | 25.59 | % | | | (4.82 | %) | | | 7.46 | % | | | (4.60 | %) | | | (26.79 | %) |

| Ratios/Supplemental Data | | | | | | | | | | | | | | | | | | | | |

| Net assets, end of period (in thousands) | | $ | 1,669 | | | $ | 1,600 | | | $ | 2,158 | | | $ | 2,244 | | | $ | 2,915 | |

| Ratios to average net assets: | | | | | | | | | | | | | | | | | | | | |

| Net investment loss | | | (0.55 | %) | | | (0.70 | %) | | | (0.44 | %) | | | (0.47 | %) | | | (0.60 | %) |

| Total expensesc | | | 2.22 | % | | | 2.10 | % | | | 2.18 | % | | | 2.24 | % | | | 2.11 | % |

| Portfolio turnover rate | | | 101 | % | | | 92 | % | | | 100 | % | | | 69 | % | | | 111 | % |

| | | Period Ended | | | | | | | | | | | | | |

| | | September 30, | | | | | | | | | | | | | |

| Institutional Class | | 2012d | | | | | | | | | | | | | |

| Per Share Data | | | | | | | | | | | | | | | | | | | | |

| Net asset value, beginning of period | | $ | 20.84 | | | | | | | | | | | | | | | | | |

| Income (loss) from investment operations: | | | | | | | | | | | | | | | | | | | | |

| Net investment incomea | | | .07 | | | | | | | | | | | | | | | | | |

| Net gain on investments | | | | | | | | | | | | | | | | | | | | |

| (realized and unrealized) | | | .37 | | | | | | | | | | | | | | | | | |

| Total from investment operations | | | .44 | | | | | | | | | | | | | | | | | |

| Net asset value, end of period | | $ | 21.28 | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| Total Returnb | | | 2.11 | % | | | | | | | | | | | | | | | | |

| Ratios/Supplemental Data | | | | | | | | | | | | | | | | | | | | |

| Net assets, end of period (in thousands) | | $ | 10 | | | | | | | | | | | | | | | | | |

| Ratios to average net assets: | | | | | | | | | | | | | | | | | | | | |

| Net investment income | | | 0.59 | % | | | | | | | | | | | | | | | | |

| Total expensesc | | | 1.12 | % | | | | | | | | | | | | | | | | |

| Portfolio turnover rate | | | 101 | % | | | | | | | | | | | | | | | | |

| a | Net investment income (loss) per share was computed using average shares outstanding throughout the period. |

| b | Total return does not reflect the impact of any applicable sales charges and has not been annualized. |

| c | Does not include expenses of the underlying funds in which the Fund invests. |

| d | Since commencement of operations: March 1, 2012. Percentage amounts for the period, except total return and portfolio turnover rate, have been annualized. The portfolio turn-over rate stated is for the entire fiscal year of the Fund, not since commencement of operations of the Class. |

| e | Per share amounts for years ended September 30, 2008 – September 30, 2010 and the period October 1, 2010 through April 8, 2011 have been restated to reflect a 1:4 reverse share split effective April 8, 2011. |

| SEE NOTES TO FINANCIAL STATEMENTS. | THE GUGGENHEIM FUNDS ANNUAL REPORT | 15 |

| MANAGER’S COMMENTARY (Unaudited) | September 30, 2012 |

To Our Shareholders:

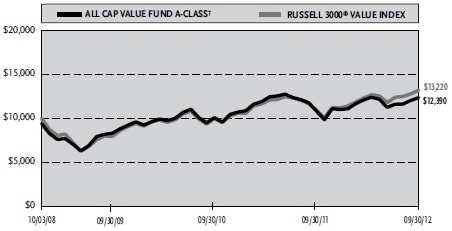

For the fiscal year ended September 30, 2012, the All Cap Value Fund returned 25.61%1, while the benchmark, the Russell 3000® Value Index, returned 31.05%.

Guggenheim Investments decided in August 2012, after a review of its mutual fund offerings, to close and subsequently liquidate the All Cap Value Fund. The liquidation was approved by the Board of Directors and the Fund ceased operations, liquidated its assets, and distributed the liquidation proceeds to shareholders of record on October 16, 2012.

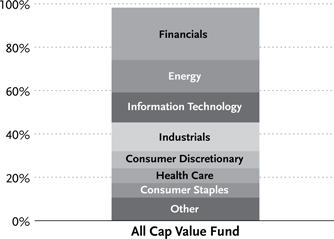

The portfolio’s performance was helped by stock selection in the Consumer Discretionary sector, which was the best-performing sector in both the portfolio and the index, and an underweight in the Utilities sector. Utilities have a rich valuation, and the underweight has benefited the portfolio over the period. These benefits were not enough, however, to offset poor stock selection in Information Technology and Industrials, and poor stock selection and an underweight in the Financials sector. The drag from holding cash was also a factor in the underperformance versus the benchmark, as the Fund prepared for liquidation.

The holdings contributing most to portfolio performance over the period were Equifax, Inc., Williams Companies, Inc. and Lowe’s Companies, Inc. The top three detractors were Maxwell Technologies, Inc., DeVry, Inc. and MGIC Investment Corp.

Sincerely,

James Schier, CFA, Portfolio Manager

Mark A. Mitchell, CFA, Portfolio Manager

Performance displayed represents past performance which is no guarantee of future results.

1 Performance figures are based on A-Class shares and do not reflect deduction of the sales charges or taxes that a shareholder would pay on distributions or the redemption of shares. Fee waivers and/or reimbursements reduce Fund expenses and in the absence of such waivers, the performance quoted would be reduced.

This fund may not be suitable for all investors. • An investment in the fund will fluctuate and is subject to investment risks, which means investors could lose money. • The intrinsic value of the underlying stocks may never be realized or the stock may decline in value. • Investments in small- and/or mid-sized company securities may present additional risks such as less predictable earnings, higher volatility and less liquidity than larger, more established companies.

The opinions and forecasts expressed may not actually come to pass. This information is subject to change at any time, based on market and other conditions, and should not be construed as a recommendation of any specific security or strategy.

16 | THE GUGGENHEIM FUNDS ANNUAL REPORT

| PERFORMANCE REPORT AND FUND PROFILE (Unaudited) | September 30, 2012 |

| | |

| ALL CAP VALUE FUND |

OBJECTIVE: Seeks long-term growth of capital.

Cumulative Fund Performance*

Average Annual Returns*

Periods Ended 09/30/12

| | | | | | Since Inception | |

| | | 1 Year | | | (10/03/08) | |

| A-Class Shares | | | 25.61 | % | | | 7.09 | % |

| A-Class Shares with sales charge† | | | 19.69 | % | | | 5.52 | % |

| C-Class Shares | | | 24.61 | % | | | 6.30 | % |

| C-Class Shares with CDSC‡ | | | 23.61 | % | | | 6.30 | % |

| Institutional Class Shares | | | 25.94 | % | | | 7.36 | % |

| Russell 3000 Value Index | | | 31.05 | % | | | 7.24 | % |

Holdings Diversification (Market Exposure as % of Net Assets)

“Holdings Diversification (Market Exposure as % of Net Assets)” excludes any temporary cash investments.

| Inception Dates: |

| A-Class | October 3, 2008 |

| C-Class | October 3, 2008 |

| Institutional Class | October 3, 2008 |

| Ten Largest Holdings (% of Total Net Assets) |

| Western Union Co. | 2.8% |

| iShares Russell 1000 Value Index Fund | 2.7% |

| Chevron Corp. | 2.7% |

| TE Connectivity Ltd. | 2.5% |

| Wells Fargo & Co. | 2.5% |

| Aon plc | 2.3% |

| Computer Sciences Corp. | 2.2% |

| Berkshire Hathaway, Inc. — Class B | 2.2% |

| Lowe’s Companies, Inc. | 2.1% |

| Time Warner, Inc. | 2.1% |

| Top Ten Total | 24.1% |

“Ten Largest Holdings” exclude any temporary cash or derivative investments.

| * | The performance data above represents past performance that is not predictive of future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Returns are historical and include changes in principal and reinvested dividends and capital gains and do not reflect the effect of taxes. The Russell 3000 Value Index is an unmanaged index and, unlike the Fund, has no management fees or operating expenses to reduce its reported return. |

| † | Effective February 22, 2011, the maximum sales charge decreased from 5.75% to 4.75%. A 5.75% maximum sales charge is used in the calculation of since inception Average Annual Returns (based on subscriptions made prior to February 22, 2011), and a 4.75% maximum sales charge will be used to calculate performance for periods based on subscriptions made on or after February 22, 2011. |

| ‡ | Fund returns include a CDSC of 1% if redeemed within 12 months of purchase. |

THE GUGGENHEIM FUNDS ANNUAL REPORT | 17

| SCHEDULE OF INVESTMENTS (In Liquidation) | September 30, 2012 |

| ALL CAP VALUE FUND |

| | | Shares | | | Value | |

| COMMON STOCKS† - 94.3% | | | | | | | | |

| | | | | | | | | |

| FINANCIALS - 24.1% | | | | | | | | |

| Wells Fargo & Co. | | | 1,883 | | | $ | 65,020 | |

| Aon plc | | | 1,111 | | | | 58,094 | |

| Berkshire Hathaway, Inc. — Class B* | | | 638 | | | | 56,271 | |

| U.S. Bancorp | | | 1,379 | | | | 47,300 | |

| American International Group, Inc.* | | | 1,162 | | | | 38,102 | |

| Allstate Corp. | | | 906 | | | | 35,887 | |

| BB&T Corp. | | | 1,068 | | | | 35,414 | |

| JPMorgan Chase & Co. | | | 799 | | | | 32,344 | |

| Hanover Insurance Group, Inc. | | | 860 | | | | 32,044 | |

| State Street Corp. | | | 715 | | | | 30,001 | |

| WR Berkley Corp. | | | 736 | | | | 27,593 | |

| Progressive Corp. | | | 1,111 | | | | 23,042 | |

| Reinsurance Group of America, | | | | | | | | |

| Inc. — Class A | | | 326 | | | | 18,866 | |

| Ocwen Financial Corp.* | | | 651 | | | | 17,844 | |

| American Financial Group, Inc. | | | 423 | | | | 16,032 | |

| Alleghany Corp.* | | | 45 | | | | 15,522 | |

| Employers Holdings, Inc. | | | 571 | | | | 10,466 | |

| Endurance Specialty Holdings Ltd. | | | 245 | | | | 9,433 | |

| RenaissanceRe Holdings Ltd. | | | 109 | | | | 8,397 | |

| Huntington Bancshares, Inc. | | | 1,122 | | | | 7,742 | |

| Synovus Financial Corp. | | | 2,120 | | | | 5,024 | |

| First Niagara Financial Group, Inc. | | | 540 | | | | 4,369 | |

| Zions Bancorporation | | | 210 | | | | 4,338 | |

| First Midwest Bancorp, Inc. | | | 339 | | | | 4,254 | |

| SVB Financial Group* | | | 70 | | | | 4,232 | |

| Wintrust Financial Corp. | | | 110 | | | | 4,133 | |

| City National Corp. | | | 80 | | | | 4,121 | |

| Citizens Republic Bancorp, Inc.* | | | 197 | | | | 3,812 | |

| Old National Bancorp | | | 215 | | | | 2,926 | |

| Total Financials | | | | | | | 622,623 | |

| ENERGY - 15.0% | | | | | | | | |

| Chevron Corp. | | | 606 | | | | 70,636 | |

| Williams Companies, Inc. | | | 1,537 | | | | 53,749 | |

| McDermott International, Inc.* | | | 3,481 | | | | 42,538 | |

| Apache Corp. | | | 454 | | | | 39,256 | |

| ConocoPhillips | | | 521 | | | | 29,791 | |

| Halliburton Co. | | | 839 | | | | 28,266 | |

| Gulfport Energy Corp.* | | | 640 | | | | 20,006 | |

| Plains Exploration & Production Co.* | | | 470 | | | | 17,611 | |

| Exxon Mobil Corp. | | | 191 | | | | 17,467 | |

| Chesapeake Energy Corp. | | | 680 | | | | 12,832 | |

| SandRidge Energy, Inc.* | | | 1,760 | | | | 12,267 | |

| Phillips 66 | | | 260 | | | | 12,056 | |

| WPX Energy, Inc.* | | | 515 | | | | 8,544 | |

| Resolute Energy Corp.* | | | 950 | | | | 8,427 | |

| Goodrich Petroleum Corp.* | | | 566 | | | | 7,154 | |

| Whiting Petroleum Corp.* | | | 150 | | | | 7,107 | |

| Total Energy | | | | | | | 387,707 | |

| INFORMATION TECHNOLOGY - 13.8% | | | | | | | | |

| Western Union Co. | | | 3,977 | | | | 72,462 | |

| TE Connectivity Ltd. | | | 1,924 | | | | 65,436 | |

| Computer Sciences Corp. | | | 1,778 | | | | 57,269 | |

| Cisco Systems, Inc. | | | 2,042 | | | | 38,982 | |

| IXYS Corp.* | | | 3,004 | | | | 29,799 | |

| Hewlett-Packard Co. | | | 1,489 | | | | 25,402 | |

| Cree, Inc.* | | | 547 | | | | 13,965 | |

| NetApp, Inc.* | | | 390 | | | | 12,823 | |

| Maxwell Technologies, Inc.* | | | 1,328 | | | | 10,783 | |

| Symmetricom, Inc.* | | | 1,442 | | | | 10,051 | |

| RF Micro Devices, Inc.* | | | 2,130 | | | | 8,414 | |

| Power-One, Inc.* | | | 1,179 | | | | 6,602 | |

| Mercury Computer Systems, Inc.* | | | 370 | | | | 3,929 | |

| Total Information Technology | | | | | | | 355,917 | |

| INDUSTRIALS - 13.3% | | | | | | | | |

| Equifax, Inc. | | | 1,126 | | | | 52,449 | |

| Republic Services, Inc. — Class A | | | 1,516 | | | | 41,706 | |

| URS Corp. | | | 1,068 | | | | 37,711 | |

| Quanta Services, Inc.* | | | 1,470 | | | | 36,309 | |

| United Technologies Corp. | | | 401 | | | | 31,395 | |

| Parker Hannifin Corp. | | | 335 | | | | 27,999 | |

| Covanta Holding Corp. | | | 1,184 | | | | 20,317 | |

| GeoEye, Inc.* | | | 619 | | | | 16,360 | |

| Saia, Inc.* | | | 700 | | | | 14,098 | |

| Aegion Corp. — Class A* | | | 698 | | | | 13,374 | |

| Orbital Sciences Corp.* | | | 861 | | | | 12,536 | |

| Navigant Consulting, Inc.* | | | 989 | | | | 10,928 | |

| Atlas Air Worldwide Holdings, Inc.* | | | 138 | | | | 7,125 | |

| United Stationers, Inc. | | | 206 | | | | 5,360 | |

| Trex Company, Inc.* | | | 135 | | | | 4,606 | |

| DryShips, Inc.* | | | 1,693 | | | | 3,962 | |

| ICF International, Inc.* | | | 159 | | | | 3,196 | |

| General Cable Corp.* | | | 93 | | | | 2,732 | |

| Total Industrials | | | | | | | 342,163 | |

| CONSUMER DISCRETIONARY - 7.9% | | | | | | | | |

| Lowe’s Companies, Inc. | | | 1,826 | | | | 55,218 | |

| Time Warner, Inc. | | | 1,190 | | | | 53,943 | |

| Cabela’s, Inc.* | | | 270 | | | | 14,764 | |

| Chico’s FAS, Inc. | | | 773 | | | | 13,999 | |

| DeVry, Inc. | | | 598 | | | | 13,610 | |

| Brown Shoe Company, Inc. | | | 834 | | | | 13,369 | |

| Scholastic Corp. | | | 344 | | | | 10,932 | |

| Jack in the Box, Inc.* | | | 378 | | | | 10,626 | |

| Maidenform Brands, Inc.* | | | 467 | | | | 9,564 | |

| Jones Group, Inc. | | | 646 | | | | 8,314 | |

| Total Consumer Discretionary | | | | | | | 204,339 | |

| 18 | THE GUGGENHEIM FUNDS ANNUAL REPORT | SEE NOTES TO FINANCIAL STATEMENTS. |

| SCHEDULE OF INVESTMENTS (In Liquidation) (concluded) | September 30, 2012 |

| ALL CAP VALUE FUND |

| | | Shares | | | Value | |

| HEALTH CARE - 6.8% | | | | | | | | |

| Covidien plc | | | 643 | | | $ | 38,207 | |

| Aetna, Inc. | | | 862 | | | | 34,136 | |

| UnitedHealth Group, Inc. | | | 364 | | | | 20,169 | |

| MEDNAX, Inc.* | | | 255 | | | | 18,985 | |

| Teva Pharmaceutical Industries Ltd. ADR | | | 440 | | | | 18,220 | |

| Forest Laboratories, Inc.* | | | 495 | | | | 17,627 | |

| Community Health Systems, Inc.* | | | 310 | | | | 9,033 | |

| Universal Health Services, Inc. — Class B | | | 168 | | | | 7,683 | |

| Hologic, Inc.* | | | 309 | | | | 6,254 | |

| Kindred Healthcare, Inc.* | | | 474 | | | | 5,394 | |

| Total Health Care | | | | | | | 175,708 | |

| CONSUMER STAPLES - 6.7% | | | | | | | | |

| CVS Caremark Corp. | | | 957 | | | | 46,338 | |

| Mondelez International, Inc. — Class A | | | 1,001 | | | | 41,391 | |

| Wal-Mart Stores, Inc. | | | 550 | | | | 40,590 | |

| Ralcorp Holdings, Inc.* | | | 239 | | | | 17,447 | |

| Hormel Foods Corp. | | | 317 | | | | 9,269 | |

| Darling International, Inc.* | | | 506 | | | | 9,255 | |

| JM Smucker Co. | | | 72 | | | | 6,216 | |

| Post Holdings, Inc.* | | | 73 | | | | 2,194 | |

| Total Consumer Staples | | | | | | | 172,700 | |

| UTILITIES - 3.2% | | | | | | | | |

| Edison International | | | 1,169 | | | | 53,412 | |

| Black Hills Corp. | | | 395 | | | | 14,050 | |

| Great Plains Energy, Inc. | | | 392 | | | | 8,726 | |

| MDU Resources Group, Inc. | | | 222 | | | | 4,893 | |

| Total Utilities | | | | | | | 81,081 | |

| MATERIALS - 2.9% | | | | | | | | |

| Dow Chemical Co. | | | 1,308 | | | | 37,880 | |

| Owens-Illinois, Inc.* | | | 840 | | | | 15,758 | |

| Sonoco Products Co. | | | 413 | | | | 12,799 | |

| Zoltek Companies, Inc.* | | | 635 | | | | 4,883 | |

| Globe Specialty Metals, Inc. | | | 271 | | | | 4,125 | |

| Total Materials | | | | | | | 75,445 | |

| TELECOMMUNICATION SERVICES - 0.6% | | | | | | | | |

| Windstream Corp. | | | 1,556 | | | | 15,731 | |

| Total Common Stocks | | | | | | | | |

| (Cost $2,122,374) | | | | | | | 2,433,414 | |

| EXCHANGE TRADED FUNDS† - 3.9% | | | | | | | | |

| iShares Russell 1000 Value Index Fund | | | 980 | | | | 70,736 | |

| iShares Russell Midcap Value Index Fund | | | 625 | | | | 30,450 | |

| Total Exchange Traded Funds | | | | | | | | |

| (Cost $99,876) | | | | | | | 101,186 | |

| Total Investments - 98.2% | | | | | | | | |

| (Cost $2,222,250) | | | | | | $ | 2,534,600 | |

| Other Assets & Liabilities, net - 1.8% | | | | | | | 45,964 | |

| Total Net Assets - 100.0% | | | | | | $ | 2,580,564 | |

| * | Non-income producing security. |

| † | Value determined based on Level 1 inputs — See Note 4. |

| | ADR — American Depositary Receipt |

| | plc — Public Limited Company |

| SEE NOTES TO FINANCIAL STATEMENTS. | THE GUGGENHEIM FUNDS ANNUAL REPORT | 19 |

STATEMENT OF ASSETS

AND LIABILITIES (In Liquidation)

September 30, 2012

| Assets: | | | | |

| Investments, at value | | | | |

| (cost $2,222,250) | | $ | 2,534,600 | |

| Cash | | | 57,672 | |

| Prepaid expenses | | | 23,271 | |

| Receivables: | | | | |

| Investment advisor | | | 7,068 | |

| Dividends | | | 3,933 | |

| Fund shares sold | | | 6 | |

| Total assets | | | 2,626,550 | |

| Liabilities: | | | | |

| Payable for: | | | | |

| Fund shares redeemed | | | 27,085 | |

| Professional fees | | | 9,436 | |

| Management fees | | | 1,518 | |

| Distribution and service fees | | | 1,129 | |

| Transfer agent/maintenance fees | | | 479 | |

| Securities purchased | | | 338 | |

| Fund accounting/administration fees | | | 206 | |

| Directors’ fees* | | | 193 | |

| Miscellaneous | | | 5,602 | |

| Total liabilities | | | 45,986 | |

| Net assets | | $ | 2,580,564 | |

| Net assets consist of: | | | | |

| Paid in capital | | $ | 2,146,601 | |

| Undistributed net investment income | | | 5,259 | |

| Accumulated net realized gain on investments | | | 116,354 | |

| Net unrealized appreciation on investments | | | 312,350 | |

| Net assets | | $ | 2,580,564 | |

| A-Class: | | | | |

| Net assets | | $ | 1,144,766 | |

| Capital shares outstanding | | | 97,856 | |

| Net asset value per share | | $ | 11.70 | |

| Maximum offering price per share | | | | |

| (Net asset value divided by 95.25%) | | $ | 12.28 | |

| C-Class: | | | | |

| Net assets | | $ | 1,057,579 | |

| Capital shares outstanding | | | 92,922 | |

| Net asset value per share | | $ | 11.38 | |

| Institutional Class: | | | | |

| Net assets | | $ | 378,219 | |

| Capital shares outstanding | | | 32,266 | |

| Net asset value per share | | $ | 11.72 | |

STATEMENT OF

OPERATIONS (In Liquidation)

Year Ended September 30, 2012

| Investment Income: | | | | |

| Dividends | | $ | 52,567 | |

| Interest | | | 9 | |

| Total investment income | | | 52,576 | |

| Expenses: | | | | |

| Management fees | | | 21,336 | |

| Transfer agent/maintenance fees | | | | |

| A-Class | | | 3,799 | |

| C-Class | | | 3,010 | |

| Institutional Class | | | 391 | |

| Distribution and service fees: | | | | |

| A-Class | | | 3,613 | |

| C-Class | | | 12,485 | |

| Fund accounting/administration fees | | | 2,895 | |

| Registration fees | | | 38,902 | |

| Custodian fees | | | 6,986 | |

| Printing expenses | | | 6,387 | |

| Professional fees | | | 5,647 | |

| Directors’ fees* | | | 310 | |

| Miscellaneous | | | 2,553 | |

| Total expenses | | | 108,314 | |

| Less: | | | | |

| Expenses waived/reimbursed by Advisor | | | (60,997 | ) |

| Net expenses | | | 47,317 | |

| Net investment income | | | 5,259 | |

| Net Realized and Unrealized Gain (Loss): | | | | |

| Net realized gain (loss) on: | | | | |

| Investments | | | 152,569 | |

| Options written | | | 2,504 | |

| Net realized gain | | | 155,073 | |

| Net change in unrealized appreciation | | | | |

| (depreciation) on: | | | | |

| Investments | | | 501,666 | |

| Options written | | | (116 | ) |

| Net change in unrealized appreciation | | | | |

| (depreciation) | | | 501,550 | |

| Net realized and unrealized gain | | | 656,623 | |

| Net increase in net assets resulting | | | | |

| from operations | | $ | 661,882 | |

* Relates to Directors not deemed “interested persons” within the meaning of Section 2(a)(19) of the 1940 Act.

| 20 | THE GUGGENHEIM FUNDS ANNUAL REPORT | SEE NOTES TO FINANCIAL STATEMENTS. |

STATEMENTS OF CHANGES IN NET ASSETS

| | | Year Ended | | | Year Ended | |

| | | September 30, 2012 | | | September 30, | |

| | | (In Liquidation) | | | 2011 | |

| Increase (Decrease) In Net Assets From Operations: | | | | | | | | |

| Net investment income | | $ | 5,259 | | | $ | 2,892 | |

| Net realized gain on investments | | | 155,073 | | | | 186,457 | |

| Net change in unrealized appreciation (depreciation) on investments | | | 501,550 | | | | (392,697 | ) |

| Net increase (decrease) in net assets resulting from operations | | | 661,882 | | | | (203,348 | ) |

| | | | | | | | | |

| Distributions to shareholders from: | | | | | | | | |

| Net investment income | | | | | | | | |

| A-Class | | | (1,457 | ) | | | (2,929 | ) |

| Institutional Class | | | (1,267 | ) | | | (1,040 | ) |

| Net realized gains | | | | | | | | |

| A-Class | | | (97,073 | ) | | | (89,465 | ) |

| C-Class | | | (65,107 | ) | | | (51,878 | ) |

| Institutional Class | | | (19,564 | ) | | | (18,694 | ) |

| Total distributions to shareholders | | | (184,468 | ) | | | (164,006 | ) |

| | | | | | | | | |

| Capital share transactions: | | | | | | | | |

| Proceeds from sale of shares | | | | | | | | |

| A-Class | | | 792,840 | | | | 509,310 | |

| C-Class | | | 1,221,188 | | | | 500,554 | |

| Institutional Class | | | 373,000 | | | | 23,672 | |

| Distributions reinvested | | | | | | | | |

| A-Class | | | 98,113 | | | | 92,394 | |

| C-Class | | | 64,307 | | | | 51,833 | |

| Institutional Class | | | 20,831 | | | | 19,734 | |

| Cost of shares redeemed | | | | | | | | |

| A-Class | | | (1,492,824 | ) | | | (547,992 | ) |

| C-Class | | | (1,419,806 | ) | | | (166,421 | ) |

| Institutional Class | | | (372,828 | ) | | | (25,872 | ) |

| Net increase (decrease) from capital share transactions | | | (715,179 | ) | | | 457,212 | |

| Net increase (decrease) in net assets | | | (237,765 | ) | | | 89,858 | |

| | | | | | | | | |

| Net assets: | | | | | | | | |

| Beginning of year | | | 2,818,329 | | | | 2,728,471 | |

| End of year | | $ | 2,580,564 | | | $ | 2,818,329 | |

| Undistributed net investment income at end of year | | $ | 5,259 | | | $ | 2,724 | |

| | | | | | | | | |

| Capital share activity: | | | | | | | | |

| Shares sold | | | | | | | | |

| A-Class | | | 70,114 | | | | 44,039 | |

| C-Class | | | 111,516 | | | | 42,478 | |

| Institutional Class | | | 32,266 | | | | 1,966 | |

| Shares issued from reinvestment of distributions | | | | | | | | |

| A-Class | | | 9,544 | | | | 7,993 | |

| C-Class | | | 6,392 | | | | 4,547 | |

| Institutional Class | | | 2,026 | | | | 1,706 | |

| Shares redeemed | | | | | | | | |

| A-Class | | | (131,878 | ) | | | (46,034 | ) |

| C-Class | | | (131,066 | ) | | | (14,749 | ) |

| Institutional Class | | | (32,251 | ) | | | (2,076 | ) |

| Net increase (decrease) in shares | | | (63,337 | ) | | | 39,870 | |

| SEE NOTES TO FINANCIAL STATEMENTS. | THE GUGGENHEIM FUNDS ANNUAL REPORT | 21 |

FINANCIAL HIGHLIGHTS

This table is presented to show selected data for a share outstanding throughout each period and to assist shareholders in evaluating a Fund’s performance for the periods presented.

| | | Year Ended | | | Year Ended | | | Year Ended | | | Period Ended | |

| | | September 30, 2012 | | | September 30, | | | September 30, | | | September 30, | |

| A-Class | | (In Liquidation) | | | 2011 | | | 2010 | | | 2009a | |

| Per Share Data | | | | | | | | | | | | | | | | |

| Net asset value, beginning of period | | $ | 9.91 | | | $ | 11.11 | | | $ | 10.21 | | | $ | 10.00 | |

| Income (loss) from investment operations: | | | | | | | | | | | | | | | | |

| Net investment incomeb | | | .05 | | | | .04 | | | | .03 | | | | .04 | |

| Net gain (loss) on investments | | | | | | | | | | | | | | | | |