UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

|

| Investment Company Act file number 811-01136 |

SECURITY EQUITY FUND

|

| (Exact name of registrant as specified in charter) |

| | |

| ONE SECURITY BENEFIT PLACE, TOPEKA, KANSAS | | 66636-0001 |

| (Address of principal executive offices) | | (Zip code) |

RICHARD M. GOLDMAN, PRESIDENT

SECURITY EQUITY FUND

ONE SECURITY BENEFIT PLACE

TOPEKA, KANSAS 66636-0001

|

| (Name and address of agent for service) |

Registrant’s telephone number, including area code: (785) 438-3000

Date of fiscal year end: September 30

Date of reporting period: September 30, 2008

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. §3507.

| Item 1. | Reports to Stockholders. |

Security Equity Fund

Security Large Cap Value Fund

Security Mid Cap Growth Fund

September 30, 2008

Annual Report

Table of Contents

Security Global Investors refers to the asset management arm of Security Benefit Corporation (“Security Benefit”) that consists of Security Investors, LLC, and for global investing, Security Global Investors, LLC. Security Distributors, Inc., Security Investors, LLC and Security Global Investors, LLC are subsidiaries of Security Benefit.

| | |

Managers’ Commentary November 14, 2008 | | Security Equity Fund Alpha Opportunity Series (unaudited) |

| |

| |

To Our Shareholders:

Performance

Although returns were down the performance of the Security Equity Fund - Alpha Opportunity Series was strong on a relative basis in the 12 months ended September 30, 2008, returning –15.99%1 compared to

–21.98% for the S&P 500 Index. For the five-year period ending September 30, 2008, the Series has outperformed the benchmark by more than 400 basis points, 9.19% to 5.17% on an annualized basis.

Investment Philosophy

We are active managers as we believe that style and approach plays well to our strengths of portfolio management experience and discipline. Our fundamental philosophy rests first upon the belief that it is critical to identify the long-term investment theme governing the equity markets. These themes may persist for 15 to 20 years. Second, while we also believe that valuation adds important perspective to investment decisions, it is not an efficient means of timing purchase and sale decisions. Those decisions are best made using technical analysis, a practice that uses the movement of security prices to indicate possible future price behavior. The third tenet of our philosophy is that changes in stock prices can lead changes in fundamental corporate developments.

Sector Performance

The favorable comparisons to the S&P 500 Index can be primarily attributed to the Series’ use of cash, emphasis on the energy and materials sectors of the market in the

first nine months of the fiscal year, and the timely reduction of those same sectors beginning in the third fiscal quarter. Short positions during the period added to performance.

Our secular investment theme reflects the need for global infrastructure where energy and materials stocks provide leadership. When using the performance of the S&P 500 sectors as an indicator, both sectors performed extremely well in the first nine months of the year. Where the S&P 500 Index was down –15% in that period, energy stocks were up 13% and materials experienced a slight decline of –0.2%. With the S&P 500 Index declining –8% in the fourth fiscal quarter, our reductions of those sectors in the prior period mitigated losses as the energy and materials sectors experienced losses of –25% and –23%, respectively.

Although our secular theme could last 15 to 20 years, there will be periods where its favored sectors, such as energy and materials, will trail the S&P 500 Index and others will lead. We are in one of those periods now. It is our belief that financial and consumer-oriented stocks provide the best return opportunities during this counter-cyclical period, a period that may last through most of 2009. For that reason, we have an overweight position in both sectors versus the index.

Market Outlook

In brief, with the S&P 500 Index more than 25% off its October 2007 highs, we believe there is a lot of bad news priced in the market. Although the statistics may not have confirmed it yet, we are probably in a recession that may last well into 2009. However, we do not believe that means the financial markets cannot recover over the intermediate term.

| | |

Managers’ Commentary November 14, 2008 | | Security Equity Fund Alpha Opportunity Series (unaudited) |

| |

| |

Numerous actions by the U.S. Congress, Treasury Department, and the Federal Reserve Bank have been an effort to stabilize securities markets and shore up the financial system. Other institutions and governments around the world have taken similar actions. While the results will not be known for some time, it is an indication of the commitment from various leaders around the globe to return normalcy to the financial system.

However, events such as the bankruptcy of Lehman Brothers, which froze credit markets, and the federal government intervention of Fannie Mae, Freddie Mac, and AIG, have resulted in extreme volatility in the equity markets. The credit market freeze has made it difficult to find counterparties with which to trade, making Series management more challenging. In addition, as a result of a previous brokerage relationship with Lehman Brothers International Europe (“LIBE”) (which was placed into administration on September 15, 2008), the Series has certain short sale positions that it is currently unable to settle and certain long positions held by its custodian that are pledged to LIBE which the Series currently cannot access. Because of the market environment, the Series is currently unable to pursue part of its investment objective because the Series is unable to invest according to a long/short strategy with an emphasis on securities of non-U.S. issuers. The Series is unable to determine when it will resume its full investment program.

We thank you for your investment and appreciate the trust and confidence you have placed in us.

Sincerely,

Bill Jenkins, Portfolio Manager

(Mainstream Investment Advisers)

John Boich, Portfolio Manager (Security Investors)

David Whittall, Portfolio Manager (Security Investors)

Scott Klimo, Portfolio Manager (Security Global Investors)

Mark Lamb, Portfolio Manager (Security Investors)

Steve Bowser, Portfolio Manager (Security Investors)

1 Performance figures are based on Class A shares and do not reflect deduction of the sales charges or taxes that a shareholder would pay on distributions or the redemption of shares. Fee waivers and/or reimbursements reduce Series expenses and in the absence of such waivers, the performance quoted would be reduced.

| | |

Performance Summary September 30, 2008 | | Security Equity Fund Alpha Opportunity Series (unaudited) |

| |

| |

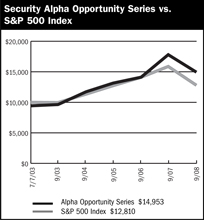

$10,000 Since Inception

This chart assumes a $10,000 investment in Class A shares of Alpha Opportunity Series on July 7, 2003 (date of inception), reflects deduction of the 5.75% sales load and assumes all dividends reinvested. The chart does not reflect the deduction of taxes that a shareholder would pay on distributions or the redemption of fund shares. The S&P 500 Index is a capitalization weighted index composed of 500 selected common stocks that represent the broad domestic economy and is a widely recognized unmanaged index of market performance.

| | | | | | |

Average Annual Returns |

Periods Ended 9-30-08 | | 1 Year | | 5 Years | | Since Inception

(7-07-03) |

A Shares | | (15.99%) | | 9.19% | | 9.22% |

A Shares with sales charge | | (20.82%) | | 7.92% | | 7.99% |

B Shares | | (16.66%) | | 8.36% | | 8.38% |

B Shares with CDSC | | (19.96%) | | 8.11% | | 8.38% |

C Shares | | (16.63%) | | 8.39% | | 8.41% |

C Shares with CDSC | | (17.29%) | | 8.39% | | 8.41% |

The performance data above represents past performance that is not predictive of future results. The investment return and principal value of an investment in the Series will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The figures above do not reflect deduction of the maximum front-end sales charge of 5.75% for Class A shares or the contingent deferred sales charge of 5% for Class B shares and 1% for Class C shares, as applicable, except where noted. The figures do not reflect the deduction of taxes that a shareholder would pay on distributions or redemption of shares. Such figures would be lower if the maximum sales charge and any applicable taxes were deducted. Fee waivers and/or reimbursements reduced expenses of the Series and in the absence of such waiver, the performance quoted would be reduced. |

| | | | | | | | |

| | | Portfolio Composition by Sector as of 9-30-08* | | |

| | | Consumer Discretionary | | 8.74% | | | | |

| | | Consumer Staples | | 6.25 | | | | |

| | | Energy | | 1.90 | | | | |

| | | Financials | | 15.30 | | | | |

| | | Health Care | | 4.39 | | | | |

| | | Industrials | | 11.83 | | | | |

| | | Information Technology | | 4.38 | | | | |

| | | Materials | | (0.80) | | | | |

| | | Telecommunication Services | | 0.22 | | | | |

| | | Utilities | | (0.30) | | | | |

| | | Exchange Traded Funds | | 0.06 | | | | |

| | | U.S. Government Sponsored Agencies | | 25.61 | | | | |

| | | Short Term Investments | | 4.65 | | | | |

| | | Cash & Other Assets, Less Liabilities | | 17.77 | | | | |

| | | Total Net Assets | | 100.00% | | | | |

| | | | | | | | | |

| | | | | | | | | |

*Securities sold short are netted with long positions in common stocks in the appropriate sectors.

| | | | |

| | 4 | | The accompanying notes are an integral part of the financial statements |

| | |

Performance Summary September 30, 2008 | | Security Equity Fund Alpha Opportunity Series (unaudited) |

| |

| |

Information About Your Series Expenses

Calculating your ongoing Series expenses

Example

As a shareholder of the Series, you incur two types of costs: (1) transaction costs, which may include sales charges (loads) on purchase payments; contingent deferred sales charges on redemptions; and redemption fees, if any; and (2) ongoing costs, including management fees; distribution and/or service fees (12b-1); and other Series expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Series and to compare these costs with ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period April 1, 2008 through September 30, 2008.

Actual Expenses

The first line for each class of shares in the table provides information about actual account values and actual expenses. You may use the information in this table, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the table under the heading entitled “Expenses Paid During the Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line for each class of shares in the table provides information about hypothetical account values and hypothetical expenses based on the Series actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Series actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Series and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other mutual funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) on purchase payments, contingent deferred sales charges on redemptions, and redemption fees, if any. Therefore, the second line for each class of shares is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | | | | | |

Series Expenses | | | | |

| | | Beginning

Account

Value

4/1/2008 | | Ending

Account

Value

9/30/2008 1 | | Expenses

Paid

During

Period 2 |

Alpha Opportunity | | | | |

Series - Class A | | | | | | |

Actual | | $1,000.00 | | $914.96 | | $14.65 |

Hypothetical | | 1,000.00 | | 1,009.70 | | 15.37 |

Alpha Opportunity | | | | |

Series - Class B | | | | | | |

Actual | | 1,000.00 | | 910.49 | | 18.05 |

Hypothetical | | 1,000.00 | | 1,006.10 | | 18.96 |

Alpha Opportunity | | | | |

Series - Class C | | | | | | |

Actual | | 1,000.00 | | 910.59 | | 18.29 |

Hypothetical | | 1,000.00 | | 1,005.85 | | 19.21 |

1 The actual ending account value is based on the actual total return of the Series for the period April 1, 2008 to September 30, 2008 after actual expenses and will differ from the hypothetical ending account value which is based on the Series expense ratio and a hypothetical annual return of 5% before expenses. The actual cumulative return at net asset value for the period April 1, 2008 to September 30, 2008 was (8.50%), (8.95%) and (8.94%), for Class A, B, and C shares, respectively.

2 Expenses are equal to the Series annualized expense ratio (3.06%, 3.78% and 3.83% for Class A, B, and C shares, respectively), including performance fees and net of any applicable fee waivers or earnings credits, multiplied by the average account value over the period, multiplied by 183/366 (to reflect the one-half year period).

| | |

Schedule of Investments September 30, 2008 | | Security Equity Fund Alpha Opportunity Series |

| |

| | | | |

| | | Shares | | Value |

COMMON STOCKS - 57.9% | | | | |

Aerospace & Defense - 1.2% | | | | |

Lockheed Martin Corporation 1,2 | | 3,753 | | $411,592 |

Northrop Grumman Corporation 1,2 | | 1,100 | | 66,594 |

| | | | |

| | | | 478,186 |

| | | | |

Airlines - 1.8% | | | | |

AMR Corporation * | | 25,133 | | 246,806 |

Southwest Airlines Company | | 34,121 | | 495,096 |

| | | | |

| | | | 741,902 |

| | | | |

Apparel Retail - 2.9% | | | | |

Childrens Place Retail Stores, Inc. * | | 669 | | 22,311 |

Gap, Inc. 1,2 | | 6,000 | | 106,680 |

Gymboree Corporation 1,2* | | 3,000 | | 106,500 |

Ltd. Brands, Inc. 1,2 | | 5,100 | | 88,332 |

Ross Stores, Inc. 1,2 | | 7,391 | | 272,063 |

TJX Companies, Inc. 1,2 | | 3,600 | | 109,872 |

Urban Outfitters, Inc. * | | 13,453 | | 428,747 |

| | | | |

| | | | 1,134,505 |

| | | | |

Apparel, Accessories & Luxury Goods - 0.3% | | | | |

Phillips-Van Heusen Corporation 1,2 | | 800 | | 30,328 |

Polo Ralph Lauren Corporation | | 1,222 | | 81,434 |

| | | | |

| | | | 111,762 |

| | | | |

Asset Management & Custody Banks - 1.8% | | | | |

BlackRock, Inc. 4 | | 3,151 | | 612,870 |

T. Rowe Price Group, Inc. | | 1,690 | | 90,770 |

| | | | |

| | | | 703,640 |

| | | | |

Auto Parts & Equipment - 0.4% | | | | |

Fuel Systems Solutions, Inc. * | | 4,738 | | 163,224 |

| | | | |

Biotechnology - 0.9% | | | | |

Amgen, Inc. 1,2,* | | 1,800 | | 106,686 |

Biogen Idec, Inc. * | | 2,500 | | 125,725 |

OSI Pharmaceuticals, Inc. * | | 2,600 | | 128,154 |

| | | | |

| | | | 360,565 |

| | | | |

Coal & Consumable Fuels - 0.5% | | | | |

Consol Energy, Inc. | | 4,623 | | 212,149 |

Uranium Energy Corporation * | | 4,504 | | 4,279 |

| | | | |

| | | | 216,428 |

| | | | |

Communications Equipment - 0.9% | | |

Harmonic, Inc. 1,2* | | 11,000 | | 92,950 |

Research In Motion, Ltd. * | | 3,889 | | 265,619 |

| | | | |

| | | | 358,569 |

| | | | |

Computer & Electronics Retail - 0.6% | | | | |

Best Buy Company, Inc. | | 4,291 | | 160,913 |

RadioShack Corporation 1,2 | | 5,100 | | 88,128 |

| | | | |

| | | | 249,041 |

| | | | |

Computer Hardware - 0.6% | | | | |

Apple, Inc. * | | 2,145 | | 243,801 |

| | | | |

Construction & Engineering - 2.1% | | |

Foster Wheeler, Ltd. * | | 10,575 | | 381,863 |

Pike Electric Corporation * | | 6,743 | | 99,324 |

Quanta Services, Inc. * | | 14,163 | | 382,543 |

| | | | |

| | | | 863,730 |

| | | | |

| | | Shares | | Value |

COMMON STOCKS (continued) | | | | |

| Construction & Farm Machinery & Heavy Trucks - 1.6% | | | | |

Joy Global, Inc. 1,2 | | 9,080 | | $409,871 |

Trinity Industries, Inc. 1,2 | | 10,200 | | 262,446 |

| | | | |

| | | | 672,317 |

| | | | |

Diversified Banks - 0.9% | | | | |

Wachovia Corporation | | 13,328 | | 46,648 |

Wells Fargo & Company | | 8,295 | | 311,311 |

| | | | |

| | | | 357,959 |

| | | | |

Diversified Real Estate Activities - 0.9% | | | | |

St. Joe Company | | 9,458 | | 369,713 |

| | | | |

Education Services - 0.1% | | | | |

ITT Educational Services, Inc. * | | 429 | | 34,710 |

| | | | |

Electrical Components & Equipment - 0.4% | | | | |

AO Smith Corporation 1,2 | | 2,800 | | 109,732 |

Thomas & Betts Corporation * | | 1,597 | | 62,395 |

| | | | |

| | | | 172,127 |

| | | | |

Electronic Equipment & Instruments - 0.4% | | | | |

Agilent Technologies, Inc. * | | 6,006 | | 178,138 |

| | | | |

Electronic Manufacturing Services - 0.1% | | | | |

Celestica, Inc. * | | 5,700 | | 36,708 |

| | | | |

Exchange Traded Funds - 1.0% | | | | |

Claymore | | 7,871 | | 129,651 |

PowerShares DB US Dollar Index Bullish Fund | | 4,860 | | 118,778 |

SPDR KBW Regional Banking ETF | | 4,072 | | 146,511 |

| | | | |

| | | | 394,940 |

| | | | |

Food Retail - 0.2% | | | | |

Safeway, Inc. 1,2 | | 3,900 | | 92,508 |

| | | | |

General Merchandise Stores - 0.2% | | | | |

Family Dollar Stores, Inc. 1,2 | | 3,700 | | 87,690 |

| | | | |

Health Care Distributors - 0.3% | | | | |

Owens & Minor, Inc. 1,2 | | 2,700 | | 130,950 |

| | | | |

Health Care Equipment - 0.3% | | | | |

Baxter International, Inc. 1,2 | | 1,800 | | 118,134 |

Smith & Nephew plc ADR | | 73 | | 3,876 |

| | | | |

| | | | 122,010 |

| | | | |

Health Care Facilities - 0.3% | | | | |

Kindred Healthcare, Inc. 1,2,* | | 3,900 | | 107,523 |

| | | | |

Health Care Services - 0.3% | | | | |

Lincare Holdings, Inc. 1,2,* | | 3,800 | | 114,342 |

| | | | |

| | | | |

| | | 6 | | The accompanying notes are an integral part of the financial statements |

| | |

Schedule of Investments September 30, 2008 | | Security Equity Fund Alpha Opportunity Series |

| |

| | | | |

| | | Shares | | Value |

COMMON STOCKS (continued) | | |

Home Entertainment Software - 0.9% | | | | |

Shanda Interactive Entertainment, Ltd. ADR 1,2,* | | 15,100 | | $385,805 |

| | | | |

| Home Improvement Retail - 0.1% | | |

Lowe’s Companies, Inc. | | 2,508 | | 59,415 |

| | | | |

| Homebuilding - 2.2% | | | | |

M.D.C. Holdings, Inc. | | 11,856 | | 433,811 |

NVR, Inc. * | | 822 | | 470,184 |

| | | | |

| | | | 903,995 |

| | | | |

| Homefurnishing Retail - 0.0% | | | | |

Haverty Furniture Companies, Inc. | | 959 | | 10,971 |

| | | | |

Housewares & Specialties - 0.9% | | | | |

Jarden Corporation * | | 16,296 | | 382,141 |

| | | | |

| Human Resource & Employment Services - 0.3% | | | | |

Watson Wyatt Worldwide, Inc. 1,2 | | 2,200 | | 109,406 |

| | | | |

Hypermarkets & Super Centers - 1.0% | | | | |

BJ’s Wholesale Club, Inc. * | | 7,108 | | 276,217 |

Wal-Mart Stores, Inc. 1,2 | | 2,200 | | 131,758 |

| | | | |

| | | | 407,975 |

| | | | |

Independent Power Producers & Energy Traders - 0.2% | | | | |

Constellation Energy Group, Inc. 1,2 | | 2,999 | | 72,876 |

| | | | |

| Industrial Conglomerates - 0.3% | | |

General Electric Company 1,2 | | 4,200 | | 107,100 |

| | | | |

| Industrial Machinery - 0.4% | | | | |

Lincoln Electric Holdings, Inc. | | 847 | | 54,471 |

Pentair, Inc. | | 1,279 | | 44,215 |

Watts Water Technologies, Inc. 1,2 | | 2,800 | | 76,580 |

| | | | |

| | | | 175,266 |

| | | | |

| Insurance Brokers - 0.2% | | | | |

Marsh & McLennan Companies, Inc. | | 2,921 | | 92,771 |

| | | | |

| Integrated Oil & Gas - 0.3% | | | | |

ConocoPhillips 1,2 | | 1,500 | | 109,875 |

| | | | |

Integrated Telecommunication Services - 0.7% | | | | |

AT&T, Inc. 1,2 | | 10,600 | | 295,952 |

| | | | |

Internet Software & Services - 0.3% | | | | |

Netease.com ADR * | | 994 | | 22,663 |

Sohu.com, Inc. * | | 1,629 | | 90,817 |

| | | | |

| | | | 113,480 |

| | | | |

| | | | |

| | | Shares | | Value |

COMMON STOCKS (continued) | | |

| Investment Banking & Brokerage - 1.6% | | | | |

KBW, Inc. * | | 6,885 | | $226,791 |

Lazard, Ltd. | | 2,521 | | 107,798 |

Raymond James Financial, Inc. | | 5,312 | | 175,190 |

TD Ameritrade Holding Corporation * | | 8,968 | | 145,282 |

| | | | |

| | | | 655,061 |

| | | | |

IT Consulting & Other Services -0.4% | | | | |

Accenture, Ltd. | | 4,200 | | 159,600 |

| | | | |

| Leisure Products - 0.2% | | | | |

Polaris Industries, Inc. | | 1,554 | | 70,691 |

| | | | |

| Life & Health Insurance - 0.8% | | | | |

Prudential Financial, Inc. | | 4,550 | | 327,600 |

| | | | |

Life Sciences Tools & Services - 1.6% | | | | |

Charles River Laboratories International, Inc. 1,2,* | | 2,000 | | 111,060 |

Icon plc ADR * | | 571 | | 21,841 |

Illumina, Inc. * | | 8,144 | | 330,076 |

Invitrogen Corporation 1,2,* | | 2,800 | | 105,840 |

Millipore Corporation 1,2,* | | 1,800 | | 123,840 |

| | | | |

| | | | 692,657 |

| | | | |

| Managed Health Care - 0.4% | | | | |

Magellan Health Services, Inc. * | | 1,800 | | 73,908 |

WellCare Health Plans, Inc. 1,2* | | 2,300 | | 82,800 |

| | | | |

| | | | 156,708 |

| | | | |

| Movies & Entertainment - 0.5% | | | | |

Imax Corporation * | | 4,280 | | 25,338 |

Marvel Entertainment, Inc. 1,2,* | | 5,400 | | 184,356 |

| | | | |

| | | | 209,694 |

| | | | |

| Multi-Line Insurance - 0.1% | | | | |

Genworth Financial, Inc. 1,2 | | 4,000 | | 34,440 |

| | | | |

| Multi-Utilities - 0.2% | | | | |

TECO Energy, Inc. | | 5,200 | | 81,796 |

| | | | |

| Oil & Gas Equipment & Services - 1.3% | | | | |

Dresser-Rand Group, Inc. * | | 8,978 | | 282,538 |

Oil States International, Inc. * | | 3,100 | | 109,585 |

Superior Well Services, Inc. * | | 4,146 | | 104,935 |

WSP Holdings, Ltd. ADR * | | 2,375 | | 14,963 |

| | | | |

| | | | 512,021 |

| | | | |

| Oil & Gas Exploration & Production - 0.6% | | | | |

Anadarko Petroleum Corporation 1,2 | | 2,755 | | 133,645 |

Canadian Natural Resources, Ltd. | | 1,747 | | 119,600 |

| | | | |

| | | | 253,245 |

| | | | |

| Oil & Gas Refining & Marketing - 0.2% | | | | |

Clean Energy Fuels Corporation * | | 6,349 | | 89,838 |

| | | | |

| | | | |

| | 7 | | The accompanying notes are an integral part of the financial statements |

| | |

Schedule of Investments September 30, 2008 | | Security Equity Fund Alpha Opportunity Series |

| |

| | | | |

| | | Shares | | Value |

COMMON STOCKS (continued) | | |

| Other Diversified Financial Services - 0.3% | | | | |

JPMorgan Chase & Company | | 2,432 | | $113,574 |

| | | | |

| Packaged Foods & Meats - 0.3% | | |

Tyson Foods, Inc. | | 9,652 | | 115,245 |

| | | | |

| Paper Products - 0.3% | | | | |

International Paper Company | | 4,406 | | 115,349 |

| | | | |

| Personal Products - 0.2% | | | | |

Herbalife, Ltd. 1,2 | | 2,500 | | 98,800 |

| | | | |

| Pharmaceuticals - 1.4% | | | | |

Forest Laboratories, Inc. 1,2,* | | 3,400 | | 96,152 |

Johnson & Johnson 1,2 | | 5,000 | | 346,400 |

Matrixx Initiatives, Inc. * | | 613 | | 11,028 |

Viropharma, Inc. 1,2,* | | 9,900 | | 129,888 |

| | | | |

| | | | 583,468 |

| | | | |

Property & Casualty Insurance - 1.1% | | | | |

ACE, Ltd. | | 6,568 | | 355,525 |

Amtrust Financial Services, Inc. 1,2 | | 6,000 | | 81,540 |

White Mountains Insurance Group, Ltd. | | 58 | | 27,246 |

| | | | |

| | | | 464,311 |

| | | | |

| Railroads - 1.0% | | | | |

Burlington Northern Santa Fe Corporation | | 2,395 | | 221,370 |

Canadian National Railway Company | | 4,056 | | 193,998 |

| | | | |

| | | | 415,368 |

| | | | |

| Regional Banks - 1.4% | | | | |

Commerce Bancshares, Inc. | | 6,364 | | 295,289 |

National City Corporation | | 38,718 | | 67,757 |

Old National Bancorp | | 809 | | 16,196 |

PNC Financial Services Group, Inc. | | 2,123 | | 158,588 |

Synovus Financial Corporation 4 | | 4,006 | | 41,462 |

| | | | |

| | | | 579,292 |

| | | | |

| Reinsurance - 0.5% | | | | |

Endurance Specialty Holdings, Ltd. 1,2 | | 3,000 | | 92,760 |

Reinsurance Group of America, Inc. | | 2,300 | | 124,200 |

| | | | |

| | | | 216,960 |

| | | | |

| Residential REIT’s - 0.8% | | | | |

Equity Residential | | 7,664 | | 340,358 |

| | | | |

| Restaurants - 2.4% | | | | |

Bob Evans Farms, Inc. | | 4,100 | | 111,889 |

Jack in the Box, Inc. 1,2* | | 4,000 | | 84,400 |

Panera Bread Company 4,* | | 13,016 | | 662,515 |

Papa John’s International, Inc. * | | 5,057 | | 137,348 |

| | | | |

| | | | 996,152 |

| | | | |

| Retail REIT’s - 0.1% | | | | |

National Retail Properties, Inc. | | 1,839 | | 44,044 |

| | | | |

| | | | |

| | | Shares | | Value |

COMMON STOCKS (continued) | | |

Semiconductor Equipment - 0.1% | | | | |

Amkor Technology, Inc. 1,2* | | 9,200 | | $58,604 |

| | | | |

| Semiconductors - 0.0% | | | | |

ARM Holdings plc ADR | | 1,729 | | 8,991 |

| | | | |

| Soft Drinks - 0.3% | | | | |

Fomento Economico Mexicano SAB de CV ADR | | 2,748 | | 104,809 |

| | | | |

| Specialized REIT’s - 2.6% | | | | |

Plum Creek Timber Company, Inc. | | 9,094 | | 453,428 |

Potlatch Corporation | | 6,846 | | 317,586 |

Rayonier, Inc. | | 5,571 | | 263,787 |

| | | | |

| | | | 1,034,801 |

| | | | |

| Specialty Stores - 0.3% | | | | |

Signet Jewelers, Ltd. | | 2,172 | | 50,781 |

Staples, Inc. | | 2,950 | | 66,375 |

| | | | |

| | | | 117,156 |

| | | | |

| Steel - 0.4% | | | | |

Schnitzer Steel Industries, Inc. | | 4,617 | | 181,171 |

| | | | |

| Systems Software - 1.6% | | | | |

CA, Inc. 1,2 | | 19,362 | | 386,465 |

Check Point Software Technologies * | | 6,636 | | 150,902 |

Symantec Corporation 1,2,* | | 5,900 | | 115,522 |

| | | | |

| | | | 652,889 |

| | | | |

| Technology Distributors - 0.4% | | |

Arrow Electronics, Inc. 1,2* | | 2,600 | | 68,172 |

Avnet, Inc. 1,2* | | 3,100 | | 76,353 |

| | | | |

| | | | 144,525 |

| | | | |

Thrifts & Mortgage Finance - 1.5% | | | | |

Hudson City Bancorp, Inc. | | 29,899 | | 551,636 |

Sovereign Bancorp, Inc. | | 18,868 | | 74,529 |

| | | | |

| | | | 626,165 |

| | | | |

| Tobacco - 2.0% | | | | |

Altria Group, Inc. 1,2 | | 16,700 | | 331,328 |

Philip Morris International, Inc. 1,2 | | 9,800 | | 471,379 |

| | | | |

| | | | 802,707 |

| | | | |

| Trading Companies & Distributors - 0.8% | | | | |

Fastenal Company | | 3,684 | | 181,952 |

W.W. Grainger, Inc. | | 1,609 | | 139,935 |

| | | | |

| | | | 321,887 |

| | | | |

| Trucking - 1.4% | | | | |

Con-way, Inc. 1,2 | | 3,496 | | 154,209 |

Heartland Express, Inc. | | 5,029 | | 78,050 |

Knight Transportation, Inc. * | | 8,686 | | 147,401 |

Old Dominion Freight Line, Inc. * | | 1,597 | | 45,259 |

YRC Worldwide, Inc. * | | 10,865 | | 129,945 |

| | | | |

| | | | 554,864 |

TOTAL COMMON STOCKS (cost $26,665,292) | | | | $23,658,857 |

| | Shares | | Value |

FOREIGN STOCKS - 13.1% | | | | |

| Austria - 0.3% | | | | |

Erste Group Bank AG | | 2,418 | | $120,291 |

| | | | |

| | | | |

| | 8 | | The accompanying notes are an integral part of the financial statements |

| | |

Schedule of Investments September 30, 2008 | | Security Equity Fund Alpha Opportunity Series |

| |

| | | | |

| | | Shares | | Value |

FOREIGN STOCKS (continued) | | |

Brazil - 0.6% | | | | |

BM&F BOVESPA S.A. | | 54,215 | | $238,525 |

| | | | |

China - 0.5% | | | | |

ZTE Corporation 3 | | 58,300 | | 220,823 |

| | | | |

France - 0.1% | | | | |

UBISOFT Entertainment 3,* | | 500 | | 34,757 |

| | | | |

Germany - 1.7% | | | | |

Adidas AG 3 | | 2,361 | | 126,031 |

Kloeckner & Company SE 3 | | 2,400 | | 55,052 |

Volkswagen AG 3 | | 1,300 | | 509,027 |

| | | | |

| | | | 690,110 |

| | | | |

Hong Kong - 1.1% | | | | |

Link REIT 3,5 | | 210,000 | | 436,527 |

| | | | |

Indonesia - 0.4% | | | | |

Bumi Resources Tbk PT 3 | | 459,746 | | 152,930 |

| | | | |

Ireland - 0.3% | | | | |

Anglo Irish Bank Corporation plc 3 | | 18,672 | | 105,843 |

| | | | |

Italy - 1.0% | | | | |

Maire Tecnimont SpA 3 | | 29,100 | | 103,173 |

Unione di Banche Italiane SCPA 3 | | 14,706 | | 321,923 |

| | | | |

| | | | 425,096 |

| | | | |

Japan - 1.5% | | | | |

Astellas Pharma, Inc. 3 | | 2,800 | | 117,532 |

JGC Corporation 3 | | 22,288 | | 357,205 |

K’s Holdings Corporation 3 | | 7,000 | | 128,259 |

Mediceo Paltac Holdings Company, Ltd. 3 | | 8,100 | | 98,992 |

| | | | |

| | | | 701,988 |

| | | | |

Norway - 0.3% | | | | |

Orkla ASA 3 | | 11,900 | | 109,439 |

| | | | |

Portugal - 0.7% | | | | |

BRISA 3 | | 15,796 | | 157,000 |

Jeronimo Martins SGPS S.A. 3 | | 14,700 | | 125,277 |

| | | | |

| | | | 282,277 |

| | | | |

South Africa - 0.7% | | | | |

Aveng, Ltd. 3 | | 38,418 | | 292,391 |

| | | | |

Switzerland - 1.2% | | | | |

Actelion, Ltd. 3,* | | 1,800 | | 92,718 |

Lonza Group AG 3 | | 2,916 | | 365,745 |

| | | | |

| | | | 458,463 |

| | | | |

United Kingdom - 2.7% | | | | |

AstraZeneca plc 3 | | 2,600 | | 113,766 |

Cadbury plc 3 | | 35,200 | | 355,837 |

GlaxoSmithKline plc 3 | | 5,200 | | 112,591 |

Imperial Tobacco Group plc 3 | | 16,105 | | 517,019 |

| | | | |

| | | | | 1,099,213 |

TOTAL FOREIGN STOCKS | | | | |

(cost $5,996,267) | | | | $5,368,673 |

| | | | | | |

| | | Principal

Amount | | | Value | |

| U.S. GOVERNMENT SPONSORED AGENCY BONDS & NOTES - 25.6% | |

Federal Home Loan Bank | | | | | | |

2.35%, 10/15/20084 | | $575,000 | | | $574,475 | |

2.42%, 10/28/20084 | | 300,000 | | | 299,456 | |

2.03%, 10/31/20084 | | 300,000 | | | 299,493 | |

2.40%, 11/3/20084 | | 1,800,000 | | | 1,796,782 | |

2.12%, 11/14/20084 | | 1,100,000 | | | 1,097,379 | |

2.08%, 11/21/20084 | | 650,000 | | | 648,204 | |

2.44%, 11/25/20084 | | 200,000 | | | 199,254 | |

2.40%, 12/10/20084 | | 400,000 | | | 398,056 | |

| Federal Home Loan Mortgage Corporation | | | | | | |

2.45%, 10/1/20081 | | 775,000 | | | 775,000 | |

2.52%, 10/7/20084 | | 275,000 | | | 274,977 | |

2.10%, 12/12/20084 | | 600,000 | | | 597,000 | |

| Federal National Mortgage Association | | | | | | |

2.30%, 10/10/20084 | | 1,000,000 | | | 999,425 | |

2.36%, 10/15/20084 | | 225,000 | | | 224,956 | |

2.25%, 10/20/20084 | | 2,000,000 | | | 1,999,472 | |

2.02%, 11/7/20084 | | 300,000 | | | 299,399 | |

TOTAL U.S. GOVERNMENT SPONSORED AGENCY BONDS & NOTES (cost $10,480,670) | | | $10,483,328 | |

| | Principal

Amount |

| | Value | |

SHORT TERM INVESTMENTS - 4.6% | |

State Street General Acount Prime Money Market Fund | | $600,000 | | | $600,000 | |

State Street Treasury Money Market Fund | | 1,302,590 | | | 1,302,590 | |

TOTAL SHORT TERM INVESTMENTS (cost $1,902,590) | | | $1,902,590 | |

Total Investments - 101.2% | | | | |

(cost $45,044,819) | | | | | $41,413,448 | |

Liabilities, Less Cash & Other Assets - (1.2)% | | | (473,279 | ) |

| | | | | | |

Total Net Assets - 100.0% | | | $40,940,169 | |

| | | | | | |

|

| Schedule of Securities Sold Short | |

| | |

| | Shares | | | Value | |

COMMON STOCKS - (10.1)% | |

Advertising - (0.2)% | | | | | | |

Focus Media Holding, Ltd. ADR 6,* | | (2,130 | ) | | $(61,943) | |

| | | | | | |

| Alternative Carriers - (0.1)% | | | | |

Global Crossing, Ltd. 6,* | | (1,800 | ) | | (32,286 | ) |

| | | | | | |

Biotechnology - (1.4)% | | | | | | |

Acorda Therapeutics, Inc. 6,* | | (2,800 | ) | | (78,288 | ) |

Alnylam Pharmaceuticals, Inc. 6,* | | (2,900 | ) | | (81,460 | ) |

Cepheid, Inc. 6,* | | (5,300 | ) | | (92,667 | ) |

Regeneron Pharmaceuticals, Inc. 6,* | | (3,180 | ) | | (71,734 | ) |

Rigel Pharmaceuticals, Inc. 6,* | | (3,050 | ) | | (66,677 | ) |

Savient Pharmaceuticals, Inc. 6,* | | (2,420 | ) | | (55,707 | ) |

| | | | |

| | 9 | | The accompanying notes are an integral part of the financial statements |

| | |

Schedule of Investments September 30, 2008 | | Security Equity Fund Alpha Opportunity Series |

| |

| | | | |

| | | Shares | | Value |

COMMON STOCKS (continued) |

| Biotechnology (continued) | | | | |

Vertex Pharmaceuticals, Inc. 6,* | | (2,600) | | $(73,539) |

| | | | |

| | | | (520,072) |

| | | | |

| Building Products - (0.3)% | | | | |

USG Corporation 6,* | | (4,940) | | (136,112) |

| | | | |

Communications Equipment - (0.1)% | | | | |

Riverbed Technology, Inc. 6,* | | (3,280) | | (58,202) |

| | | | |

| Computer Storage & Peripherals - (0.1)% | | | | |

Intermec, Inc. 6,* | | (2,740) | | (57,614) |

| | | | |

| Diversified Banks - (0.8)% | | | | |

Wachovia Corporation | | (13,328) | | (46,648) |

Wells Fargo & Company 6 | | (9,730) | | (305,943) |

| | | | |

| | | | (352,591) |

| | | | |

Diversified Metals & Mining - (0.1)% | | | | |

Ivanhoe Mines, Ltd. 6,* | | (4,440) | | (45,774) |

| | | | |

| Electric Utilities - (0.7)% | | | | |

Korea Electric Power Corporation ADR 6 | | (18,310) | | (276,071) |

| | | | |

Exchange Traded Funds - (0.9)% | | |

SPDR Gold Trust * | | (3,384) | | (287,877) |

United States Oil Fund, LP * | | (1,015) | | (83,230) |

| | | | |

| | | | (371,107) |

| | | | |

| Gold - (0.3)% | | | | |

Newmont Mining Corporation | | (3,045) | | (118,025) |

Yamana Gold, Inc. | | (1,721) | | (14,336) |

| | | | |

| | | | (132,361) |

| | | | |

| Health Care Equipment - (0.1)% | | |

Intuitive Surgical, Inc. 6,* | | (200) | | (59,799) |

| | | | |

| Health Care Services - (0.2)% | | | | |

athenahealth, Inc. 6,* | | (2,500) | | (80,274) |

| | | | |

| Health Care Supplies - (0.2)% | | | | |

Align Technology, Inc. 6,* | | (6,100) | | (81,155) |

| | | | |

Home Entertainment Software - (0.1)% | | | | |

Electronic Arts, Inc. 6,* | | (900) | | (42,957) |

| | | | |

| Integrated Oil & Gas - (0.2)% | | | | |

Exxon Mobil Corporation | | (1,015) | | (78,824) |

| | | | |

Internet Software & Services - (0.7)% | | | | |

Baidu.com ADR 6,* | | (200) | | (62,667) |

Equinix, Inc. 6,* | | (1,000) | | (77,801) |

SAVVIS, Inc. 6,* | | (5,700) | | (79,275) |

VeriSign, Inc. 6,* | | (1,200) | | (38,030) |

| | | | |

| | | | (257,773) |

| | | | |

| Leisure Products - (0.6)% | | | | |

Pool Corporation 6 | | (11,639) | | (276,585) |

| | | | |

| | | | |

| | | Shares | | Value |

COMMON STOCKS (continued) |

| Life Sciences Tools & Services - (0.6)% | | | | |

AMAG Pharmaceuticals, Inc. 6* | | (1,900) | | $(79,315) |

Exelixis, Inc. 6,* | | (4,500) | | (29,463) |

Luminex Corporation 6,* | | (2,500) | | (61,285) |

Sequenom, Inc. 6,* | | (3,810) | | (79,465) |

| | | | |

| | | | (249,528) |

| | | | |

| Oil & Gas Drilling - (0.1)% | | | | |

Noble Corporation | | (1,015) | | (44,559) |

| | | | |

| Oil & Gas Exploration & Production - (0.2)% | | | | |

BPZ Resources, Inc. 6* | | (5,700) | | (77,382) |

| | | | |

| Pharmaceuticals - (0.4)% | | | | |

Auxilium Pharmaceuticals, Inc. 6,* | | (1,540) | | (63,962) |

Sepracor, Inc. 6,* | | (1,400) | | (25,724) |

XenoPort, Inc. 6,* | | (1,376) | | (67,247) |

| | | | |

| | | | (156,933) |

| | | | |

| Regional Banks - (0.2)% | | | | |

PrivateBancorp, Inc. 6 | | (2,390) | | (75,975) |

| | | | |

Semiconductor Equipment - (0.1)% | | | | |

Varian Semiconductor Equipment Associates, Inc. 6,* | | (1,260) | | (43,137) |

| | | | |

| Semiconductors - (0.3)% | | | | |

Cree, Inc. 6,* | | (4,000) | | (81,002) |

Rambus, Inc. 6,* | | (3,600) | | (55,453) |

| | | | |

| | | | (136,455) |

| | | | |

| Soft Drinks - (0.2)% | | | | |

Hansen Natural Corporation 6,* | | (3,250) | | (94,200) |

| | | | |

| Specialty Chemicals - (0.1)% | | |

Zoltek Companies, Inc. 6,* | | (2,700) | | (44,530) |

| | | | |

| Systems Software - (0.4)% | | | | |

Red Hat, Inc. 6,* | | (2,610) | | (58,601) |

VMware, Inc. 6,* | | (2,400) | | (88,322) |

| | | | |

| | | | (146,923) |

| | | | |

| Wireless Telecommunication Services - (0.4)% | | |

Clearwire Corporation 6,* | | (2,530) | | (27,183) |

Leap Wireless International, Inc. 6,* | | (1,500) | | (63,847) |

SBA Communications Corporation 6,* | | (2,400) | | (82,713) |

| | | | |

| | | | (173,743) |

TOTAL COMMON STOCKS SOLD SHORT (proceeds $4,328,575) | | $(4,164,865) |

| | | Shares | | Value |

FOREIGN STOCKS - (8.8)% |

| Australia - (0.7)% | | | | |

Aquila Resources, Ltd. 6,* | | (2,500) | | $(26,744) |

Arrow Energy, Ltd. 6,* | | (8,900) | | (24,300) |

Ausenco, Ltd. 6 | | (2,100) | | (21,319) |

Queensland Gas Company, Ltd. 6,* | | (12,800) | | (48,691) |

Riversdale Mining, Ltd. 6,* | | (6,700) | | (49,992) |

Sino Gold Mining, Ltd. 5,6* | | (8,600) | | (30,946) |

| | | | |

| | 10 | | The accompanying notes are an integral part of the financial statements |

| | |

Schedule of Investments September 30, 2008 | | Security Equity Fund Alpha Opportunity Series |

| |

| | | | |

| | | Shares | | Value |

FOREIGN STOCKS (continued) |

| Australia (continued) | | | | |

Western Areas NL 6,* | | (6,200) | | $(42,462) |

| | | | |

| | | | (244,454) |

| | | | |

Austria - (0.9)% | | | | |

bwin Interactive Entertainment AG 6,* | | (1,600) | | (41,006) |

Erste Group Bank AG 6 | | (5,200) | | (274,278) |

Intercell AG 6,* | | (1,900) | | (83,910) |

| | | | |

| | | | (399,194) |

| | | | |

Bermuda - 0.0% | | | | |

C C Land Holdings, Ltd. 6 | | (50,000) | | (19,707) |

| | | | |

Canada - (0.4)% | | | | |

Agnico-Eagle Mines, Ltd. 6 | | (1,800) | | (89,744) |

Silver Wheaton Corporation 6,* | | (6,100) | | (64,389) |

Trican Well Service, Ltd. 6 | | (2,000) | | (38,332) |

| | | | |

| | | | (192,465) |

| | | | |

China - (0.6)% | | | | |

Anhui Conch Cement Company, Ltd. 6 | | (4,500) | | (19,499) |

Beijing Capital International Airport Company, Ltd. 6 | | (218,000) | | (153,368) |

China Communications Construction Company, Ltd. 6 | | (15,000) | | (24,388) |

China National Building Material Company, Ltd. 6 | | (14,700) | | (19,087) |

China National Materials Company, Ltd. 6,* | | (34,400) | | (23,282) |

| | | | |

| | | | (239,624) |

| | | | |

Germany - (1.5)% | | | | |

Premiere AG 6,* | | (4,000) | | (69,097) |

Volkswagen AG 3 | | (1,300) | | (509,025) |

| | | | |

| | | | (578,122) |

| | | | |

Gibraltar - (0.2)% | | | | |

PartyGaming plc 6,* | | (15,200) | | (60,009) |

| | | | |

Hong Kong - (0.2)% | | | | |

China Merchants Holdings International Company, Ltd. 6 | | (3,100) | | (10,738) |

Franshion Properties China, Ltd. 6 | | (79,400) | | (27,023) |

Fushan International Energy Group, Ltd. 6,* | | (66,000) | | (34,202) |

| | | | |

| | | | (71,963) |

| | | | |

Ireland - (0.1)% | | | | |

Ryanair Holdings plc 6,* | | (9,600) | | (39,530) |

| | | | |

Isle Of Man - (0.1)% | | | | |

Genting International plc 6,* | | (124,900) | | (44,635) |

| | | | |

| Japan - (1.4)% | | | | |

Access Company, Ltd. 6,* | | (17) | | (26,715) |

Aeon Mall Company, Ltd. 6 | | (1,700) | | (46,256) |

Aozora Bank, Ltd. 6 | | (16,300) | | (34,871) |

Japan Steel Works, Ltd. 6 | | (1,500) | | (24,128) |

Marui Group Company, Ltd. 6 | | (29,100) | | (220,049) |

Mizuho Financial Group, Inc. 6 | | (11) | | (46,597) |

Mizuho Trust & Banking Company, Ltd. 6 | | (17,700) | | (24,821) |

Modec, Inc. 6 | | (900) | | (25,626) |

Monex Group, Inc. 6 | | (78) | | (36,852) |

Tokyo Broadcasting System, Inc. 6 | | (1,300) | | (20,263) |

| | | | |

| | | Shares | | Value |

FOREIGN STOCKS (continued) |

Japan (continued) | | | | |

Toyo Tanso Company, Ltd. 6 | | (500) | | $(26,446) |

| | | | |

| | | | (532,624) |

| | | | |

Norway - (0.1)% | | | | |

Sevan Marine ASA 6,* | | (5,900) | | (58,326) |

| | | | |

Portugal - (1.0)% | | | | |

BRISA 6 | | (44,400) | | (431,595) |

| | | | |

Spain - (0.1)% | | | | |

Zeltia S.A. 6 | | (8,000) | | (58,423) |

| | | | |

Sweden - (1.0)% | | | | |

Electrolux AB 6 | | (30,100) | | (393,257) |

| | | | |

Switzerland - (0.3)% | | | | |

Basilea Pharmaceutica 6,* | | (500) | | (81,308) |

Meyer Burger Technology AG 6,* | | (200) | | (54,522) |

| | | | |

| | | | (135,830) |

| | | | |

| United Kingdom - (0.2)% | | | | |

Imperial Energy Corporation plc 6* | | (3,900) | | (84,652) |

| | | | |

| | | | |

TOTAL FOREIGN STOCKS SOLD SHORT (proceeds $3,495,580) | | $(3,584,410) |

TOTAL SECURITIES SOLD SHORT - (18.9%) | | |

(proceeds $7,824,155) | | $(7,749,275) |

| | | | |

For federal income tax purposes the identified cost of investments owned at September 30, 2008 was $45,363,271.

| | |

ADR | | American Depositary Receipt |

plc | | Public Limited Company |

* Non-income producing security

1 Security is segregated as collateral for open short positions.

2 Security is deemed illiquid. The total market value of illiquid securities is $7,570,226 (cost $8,657,054), or 18.5% of total net assets.

3 Security is subject to the fair value trigger at September 30, 2008. The total market value of securities subject to the fair value trigger amounts to $4,500,832, (cost $5,132,486) or 11.0% of total net assets.

4 Security is segregated as collateral for open futures contracts.

5 Security is a PFIC (Passive Foreign Investment Company).

6 Security is fair valued by the Valuation Committee at September 30, 2008. The total market value of fair valued securities amounts to ($6,566,751) (cost $(6,574,873)), or (16.0%) of total net assets.

| | | | |

| | | 11 | | The accompanying notes are an integral part of the financial statements |

Security Equity Fund

Alpha Opportunity Series

| | |

Statement of Assets and Liabilities |

September 30, 2008 |

Assets: | | |

Investments, at value* | | $41,413,448 |

Cash | | 2,607,198 |

Cash denominated in a foreign currency, at value*** | | 106,780 |

Restricted cash | | 857,066 |

Restricted cash denominated in a foreign currency, at value**** | | 3,279,694 |

Receivables: | | |

Fund shares sold | | 123,122 |

Securities sold | | 709,814 |

Interest | | 3,636 |

Dividends | | 28,866 |

Variation margin | | 455,895 |

Security Investors | | 6,965 |

Prepaid expenses | | 14,555 |

| | |

Total assets | | 49,607,039 |

| | |

Liabilities: | | |

Securities sold short, at value** | | 7,749,275 |

Payable for: | | |

Securities purchased | | 759,299 |

Fund shares redeemed | | 57,482 |

Dividends on short sales | | 4,166 |

Management fees | | 45,313 |

Transfer agent/maintenance fees | | 8,056 |

Administration fees | | 6,788 |

Professional fees | | 17,704 |

12b-1 distribution plan fees | | 16,030 |

Directors’ fees | | 790 |

Other | | 1,967 |

| | |

Total liabilities | | 8,666,870 |

| | |

Net assets | | $40,940,169 |

| | |

Net assets consist of: | | |

Paid in capital | | $48,851,137 |

Accumulated net investment loss | | (35,571) |

Accumulated net realized loss on sale of investments and foreign currency transactions | | (3,323,597) |

Net unrealized depreciation in value of investments and translation of assets and liabilities in foreign currencies | | (4,551,800) |

| | |

Net assets | | $40,940,169 |

| | |

Class A: | | |

Capital shares outstanding (unlimited number of shares authorized) | | 3,267,374 |

Net assets | | $30,614,532 |

Net asset value and redemption price per share | | $9.37 |

| | |

Maximum offering price per share (net asset value divided by 94.25%) | | $9.94 |

| | |

Class B: | | |

Capital shares outstanding (unlimited number of shares authorized) | | 607,814 |

Net assets | | $5,390,668 |

Net asset value, offering and redemption price per share (excluding any applicable contingent deferred sales charge) | | $8.87 |

| | |

Class C: | | |

Capital shares outstanding (unlimited number of shares authorized) | | 556,443 |

Net assets | | $4,934,969 |

Net asset value, offering and redemption price per share (excluding any applicable contingent deferred sales charge) | | $8.87 |

| | |

| |

*Investments, at cost | | $45,044,819 |

**Securities sold short, proceeds | | 7,824,155 |

***Cash denominated in a foreign currency, at cost | | 109,535 |

| ****Restricted cash denominated in a foreign currency, at cost | | 3,364,461 |

| | |

Statement of Operations |

For the Year Ended September 30, 2008 |

Investment Income: | | |

Dividends (net of foreign withholding tax of $546) | | $204,413 |

Interest | | 460,629 |

| | |

Total investment income | | 665,042 |

| | |

| |

Expenses: | | |

Management fees | | 891,663 |

Transfer agent/maintenance fees | | 84,349 |

Administration fees | | 62,487 |

Custodian fees | | 62,473 |

Directors’ fees | | 2,684 |

Professional fees | | 36,545 |

Reports to shareholders | | 3,653 |

Registration fees | | 31,171 |

Other expenses | | 3,375 |

Dividends on short sales | | 41,976 |

12b-1 distribution fees - Class A | | 71,980 |

12b-1 distribution fees - Class B | | 44,068 |

12b-1 distribution fees - Class C | | 54,221 |

| | |

Total expenses | | 1,390,645 |

Less: | | |

Reimbursement of expenses - Class A | | (26,619) |

Reimbursement of expenses - Class B | | (4,996) |

Reimbursement of expenses - Class C | | (4,134) |

Earnings credits applied | | (59,184) |

| | |

Net expenses | | 1,295,712 |

| | |

Net investment loss | | (630,670) |

| | |

Net Realized and Unrealized Gain (Loss): |

Net realized gain (loss) during the year on: | | |

Investments | | 350,161 |

Securities sold short | | 592,568 |

Foreign currency transactions | | (35,571) |

Futures | | (2,807,480) |

| | |

Net realized loss | | (1,900,322) |

| | |

Net unrealized appreciation (depreciation) during the year on: | | |

Investments | | (3,741,089) |

Securities sold short | | 72,495 |

Futures | | (1,446,840) |

Translation of assets and liabilities in foreign currencies | | (87,811) |

| | |

Net unrealized depreciation | | (5,203,245) |

| | |

Net loss | | (7,103,567) |

| | |

Net decrease in net assets resulting from operations | | $(7,734,237) |

| | |

| | | | |

| | 12 | | The accompanying notes are an integral part of the financial statements |

| | |

Statement of Changes in Net Assets | | Security Equity Fund Alpha Opportunity Series |

| |

| | | | | | | | |

| | | Year Ended

September 30, 2008 | | | Year Ended

September 30, 2007 | |

| | |

Increase (decrease) in net assets from operations: | | | | | | | | |

Net investment loss | | $ | (630,670 | ) | | $ | (98,282 | ) |

Net realized gain (loss) during the year on investments and foreign currency transactions | | | (1,900,322 | ) | | | 6,873,561 | |

Net unrealized appreciation (depreciation) during the year on investments and translation of assets and liabilities in foreign currencies | | | (5,203,245 | ) | | | 898,061 | |

| | | | | | | | |

Net increase (decrease) in net assets resulting from operations | | | (7,734,237 | ) | | | 7,673,340 | |

| | | | | | | | |

| | |

Distributions to shareholders from: | | | | | | | | |

Net realized gain | | | | | | | | |

Class A | | | (4,624,275 | ) | | | (2,136,563 | ) |

Class B | | | (730,879 | ) | | | (523,991 | ) |

Class C | | | (959,211 | ) | | | (617,311 | ) |

Return of capital | | | | | | | | |

Class A | | | (508,721 | ) | | | – | |

Class B | | | (80,405 | ) | | | – | |

Class C | | | (105,524 | ) | | | – | |

| | | | | | | | |

Total distributions to shareholders | | | (7,009,015 | ) | | | (3,277,865 | ) |

| | | | | | | | |

| | |

Capital share transactions: | | | | | | | | |

Proceeds from sale of shares | | | | | | | | |

Class A | | | 20,613,127 | | | | 10,352,391 | |

Class B | | | 5,409,786 | | | | 1,279,776 | |

Class C | | | 3,698,851 | | | | 1,430,285 | |

Distributions reinvested | | | | | | | | |

Class A | | | 5,033,793 | | | | 2,077,296 | |

Class B | | | 802,594 | | | | 522,694 | |

Class C | | | 960,779 | | | | 556,963 | |

Cost of shares redeemed | | | | | | | | |

Class A | | | (9,305,440 | ) | | | (11,078,834 | ) |

Class B | | | (2,099,606 | ) | | | (4,098,624 | ) |

Class C | | | (1,872,076 | ) | | | (4,012,623 | ) |

| | | | | | | | |

Net increase (decrease) from capital share transactions | | | 23,241,808 | | | | (2,970,676 | ) |

| | | | | | | | |

Net increase in net assets | | | 8,498,556 | | | | 1,424,799 | |

| | | | | | | | |

| | |

Net assets: | | | | | | | | |

Beginning of year | | | 32,441,613 | | | | 31,016,814 | |

| | | | | | | | |

End of year | | $ | 40,940,169 | | | $ | 32,441,613 | |

| | | | | | | | |

| | |

Accumulated net investment loss at end of year | | $ | (35,571 | ) | | $ | – | |

| | | | | | | | |

| | |

Capital share activity: | | | | | | | | |

Shares sold | | | | | | | | |

Class A | | | 1,869,043 | | | | 802,495 | |

Class B | | | 505,963 | | | | 104,269 | |

Class C | | | 335,936 | | | | 114,901 | |

Shares reinvested | | | | | | | | |

Class A | | | 463,090 | | | | 174,124 | |

Class B | | | 77,545 | | | | 45,216 | |

Class C | | | 92,829 | | | | 48,180 | |

Shares redeemed | | | | | | | | |

Class A | | | (863,491 | ) | | | (862,512 | ) |

Class B | | | (210,696 | ) | | | (321,701 | ) |

Class C | | | (186,349 | ) | | | (317,535 | ) |

| | | | |

| | 13 | | The accompanying notes are an integral part of the financial statements |

| | |

Financial Highlights Selected data for each share of capital stock outstanding throughout each year | | Security Equity Fund

Alpha Opportunity Series |

| |

| | | | | | | | | | |

| Class A | | 2008a | | 2007 | | 2006 | | 2005 | | Year Ended

September 30,

2004 |

Per Share Data | | | | | | | | | | |

Net asset value, beginning of period | | $13.94 | | $12.23 | | $12.37 | | $11.79 | | $10.21 |

Income (loss) from investment operations: | | | | | | | | | | |

Net investment lossb | | (0.16) | | (0.01) | | (0.06) | | (0.10) | | (0.16) |

Net gain (loss) on securities (realized and unrealized) | | (1.68) | | 2.99 | | 0.93 | | 1.50 | | 2.33 |

| | |

Total from investment operations | | (1.84) | | 2.98 | | 0.87 | | 1.40 | | 2.17 |

Less distributions: | | | | | | | | | | |

Distributions from realized gains | | (2.57) | | (1.27) | | (1.01) | | (0.82) | | (0.59) |

Return of capital | | (0.16) | | – | | – | | – | | – |

| | |

Total distributions | | (2.73) | | (1.27) | | (1.01) | | (0.82) | | (0.59) |

Net asset value, end of period | | $9.37 | | $13.94 | | $12.23 | | $12.37 | | $11.79 |

| | |

| | | | | | | | | | |

Total Return c | | (15.99%) | | 26.10% | | 7.39% | | 12.26% | | 21.68% |

Ratios/Supplemental Data | | | | | | | | | | |

Net assets, end of period (in thousands) | | $30,615 | | $25,072 | | $20,595 | | $14,622 | | $6,556 |

Ratios to average net assets: | | | | | | | | | | |

Net investment loss | | (1.44%) | | (0.08%) | | (0.50%) | | (0.83%) | | (1.48%) |

Total expensesd | | 2.96% | | 2.88% | | 3.20% | | 2.94% | | 3.57% |

Net expensese | | 2.75% | | 2.68% | | 3.01% | | 2.86% | | 2.78% |

Net expenses prior to custodian earning credits and net of expense waivers | | 2.88% | | 2.88% | | 3.10% | | 2.86% | | 2.79% |

Net expenses prior to performance fee adjustmentf | | 2.39% | | 2.77% | | 2.82% | | 2.78% | | 2.78% |

Portfolio turnover rate | | 1,248% | | 1,697% | | 1,302% | | 1,502% | | 1,175% |

| | | | | |

| Class B | | 2008a | | 2007 | | 2006 | | 2005 | | Year Ended

September 30,

2004 |

Per Share Data | | | | | | | | | | |

Net asset value, beginning of period | | $13.42 | | $11.90 | | $12.15 | | $11.68 | | $10.20 |

Income (loss) from investment operations: | | | | | | | | | | |

Net investment lossb | | (0.23) | | (0.09) | | (0.15) | | (0.18) | | (0.25) |

Net gain (loss) on securities (realized and unrealized) | | (1.59) | | 2.88 | | 0.91 | | 1.47 | | 2.32 |

| | |

Total from investment operations | | (1.82) | | 2.79 | | 0.76 | | 1.29 | | 2.07 |

Less distributions: | | | | | | | | | | |

Distributions from realized gains | | (2.57) | | (1.27) | | (1.01) | | (0.82) | | (0.59) |

Return of capital | | (0.16) | | – | | – | | – | | – |

| | |

Total distributions | | (2.73) | | (1.27) | | (1.01) | | (0.82) | | (0.59) |

Net asset value, end of period | | $8.87 | | $13.42 | | $11.90 | | $12.15 | | $11.68 |

| | |

| | | | | | | | | | |

Total Return c | | (16.66%) | | 25.14% | | 6.56% | | 11.39% | | 20.68% |

Ratios/Supplemental Data | | | | | | | | | | |

Net assets, end of period (in thousands) | | $5,391 | | $3,154 | | $4,846 | | $4,106 | | $2,324 |

Ratios to average net assets: | | | | | | | | | | |

Net investment loss | | (2.18%) | | (0.77%) | | (1.24%) | | (1.60%) | | (2.25%) |

Total expensesd | | 3.13% | | 3.59% | | 3.95% | | 3.69% | | 4.29% |

Net expensese | | 2.93% | | 3.39% | | 3.76% | | 3.61% | | 3.53% |

Net expenses prior to custodian earning credits and net of expense waivers | | 3.04% | | 3.59% | | 3.85% | | 3.61% | | 3.53% |

Net expenses prior to performance fee adjustmentf | | 2.62% | | 3.51% | | 3.57% | | 3.53% | | 3.53% |

Portfolio turnover rate | | 1,248% | | 1,697% | | 1,302% | | 1,502% | | 1,175% |

| | | | |

| | 14 | | The accompanying notes are an integral part of the financial statements |

| | |

| Financial Highlights | | Security Equity Fund |

Selected data for each share of capital stock outstanding throughout each year | | Alpha Opportunity Series |

| | | | | | | | | | |

| Class C | | 2008a | | 2007 | | 2006 | | 2005 | | Year Ended

September 30,

2004 |

Per Share Data | | | | | | | | | | |

Net asset value, beginning of period | | $13.43 | | $11.90 | | $12.15 | | $11.68 | | $10.20 |

Income (loss) from investment operations: | | | | | | | | | | |

Net investment lossb | | (0.23) | | (0.10) | | (0.15) | | (0.18) | | (0.25) |

Net gain (loss) on securities (realized and unrealized) | | (1.60) | | 2.90 | | 0.91 | | 1.47 | | 2.32 |

| | |

Total from investment operations | | (1.83) | | 2.80 | | 0.76 | | 1.29 | | 2.07 |

Less distributions: | | | | | | | | | | |

Distributions from realized gains | | (2.57) | | (1.27) | | (1.01) | | (0.82) | | (0.59) |

Return of capital | | (0.16) | | – | | – | | – | | – |

| | |

Total distributions | | (2.73) | | (1.27) | | (1.01) | | (0.82) | | (0.59) |

Net asset value, end of period | | $8.87 | | $13.43 | | $11.90 | | $12.15 | | $11.68 |

| | |

| | | | | | | | | | |

Total Return c | | (16.63%) | | 25.24% | | 6.56% | | 11.39% | | 20.68% |

Ratios/Supplemental Data | | | | | | | | | | |

Net assets, end of period (in thousands) | | $4,935 | | $4,216 | | $5,576 | | $7,813 | | $3,143 |

Ratios to average net assets: | | | | | | | | | | |

Net investment loss | | (2.21%) | | (0.77%) | | (1.18%) | | (1.58%) | | (2.24%) |

Total expensesd | | 4.02% | | 3.60% | | 3.95% | | 3.68% | | 4.30% |

Net expensese | | 3.80% | | 3.40% | | 3.75% | | 3.61% | | 3.53% |

Net expenses prior to custodian earning credits and net of expense waivers | | 3.95% | | 3.60% | | 3.83% | | 3.61% | | 3.53% |

Net expenses prior to performance fee adjustmentf | | 3.40% | | 3.51% | | 3.57% | | 3.53% | | 3.53% |

Portfolio turnover rate | | 1,248% | | 1,697% | | 1,302% | | 1,502% | | 1,175% |

a Security Global Investors, LLC (SGI) became the sub-adviser of 37.5% of the assets of the Alpha Opportunity Series effective August 18, 2008. Also effective August 18, 2008, Mainstream Investment Advisers, LLC (Mainstream) sub-advises 37.5% of the assets and Security Investors, LLC (SI) manages 25% of the assets. Prior to August 18, 2008, SI paid Mainstream sub-advisory fees for 60% of the assets. SI managed the remaining 40% of the assets.

b Net investment income (loss) was computed using average shares outstanding throughout the period.

c Total return information does not reflect deduction of any sales charges imposed at the time of purchase for Class A shares or upon redemption for Class B and C shares.

d Total expense information reflects expense ratios absent expense reductions by the Investment Manager and custodian earnings credits, as applicable.

e Net expense information reflects the expense ratios after voluntary expense waivers, reimbursements and custodian earnings credits, as applicable.

f Net expenses prior to performance fee adjustment reflect ratios after voluntary expense waivers, reimbursements, custodian earnings credits, and before performance fees adjustments, as applicable.

| | | | |

| | 15 | | The accompanying notes are an integral part of the financial statements |

This page left blank intentionally.

| | |

Manager’s Commentary November 14, 2008 | | Security Equity Fund Equity Series (unaudited) |

| |

| |

| | |

| | To Our Shareholders: Security Equity Fund Equity Series returned –26.12%1 in the period, lagging the benchmark S&P 500 Index’s return of –21.98% and the Series’ peer group median return of –22.36%. |

Our strategy is to buy companies that are trading at a significant discount to their intrinsic value. Our investment approach is a defined and disciplined process of three clear philosophical tenets focus, a long-term perspective and an opportunistic approach.

This investment process is fundamentally driven and quantitatively aided. We use proprietary screens to identify potential companies for investment and then perform rigorous fundamental analysis to identify the best ideas. Through this fundamental research, we determine an estimate of intrinsic value and a valuation target for each potential investment. We construct the portfolios based on the level of conviction generated by this bottom-up analysis and the upside/downside profile associated with each company.

Health Care and Materials Top Performers

The health care sector of the portfolio benefited from superior stock selection relative to the S&P 500 Index allowing the Series to post a break-even return for the period compared to a –12% loss for the S&P 500 Index. The portfolio positioned the sector as a slight underweight. Leading holdings in the Series included Celgene Corporation, Gilead Sciences, Inc., and Covidien, Ltd.

Relative performance against the S&P 500 Index, in the materials sector helped performance, as the portfolio holdings lost only –4%, versus –21% for the benchmark. The portfolio was slightly overweight in the relatively small overall weighted sector. Adding positive returns for the Series were Rohm & Haas Company, Allegheny Technologies, Inc., and Vulcan Materials Company.

Over the difficult 12-month period, the consumer staples sector was able to produce a positive contribution to the return. While an even weight with the benchmark, the sector gained 9% for the portfolio, compared to 1% for the S&P 500 Index. Wal-Mart Stores, Inc. was the biggest contributor.

Financials and Industrials Disappoint

By far, the largest detractor from portfolio performance was the financials sector. The portfolio had an equal weight position with the benchmark, but stock selection fell short, even in this most battered sector. While financials in the benchmark dropped 39%, holdings in the portfolio lost –51%. Financial holdings that caused the most damage were in First Marblehead Corporation and American International Group, Inc. Both were significant holdings in the portfolio over the period and each lost more than 90% of its value.

The portfolio was significantly overweight in industrials, accounting for 18% of total assets. While the sector in the benchmark lost –25%, poor stock selection sent the portfolio down –30%. General Electric Company was the portfolio’s largest loser in the sector. Deere & Company, Textron, Inc., and McDermott International, Inc. also pulled performance down.

Stock selection in the energy sector hurt the portfolio. The largest detractors in the sector were Evergreen Energy, Inc. and Nabors Industries, Ltd.

2009 Market Outlook

Our bottom-up approach looks at market uncertainty in the context of the potential long-term impact on individual companies. Our focus is on identifying companies with the ability to be substantially better over the next three to five years or have the potential to maintain their return on capital at current levels in a difficult economic environment. During these uncertain times and volatile market conditions, we are confident in our ability to find these companies by consistently applying our disciplined process to individual stock evaluations.

We believe that investing is a long-term pursuit that requires patience and a consistent approach. We thank you for your business and the confidence you place in us.

Sincerely,

Mark Bronzo

Senior Portfolio Manager

1 Performance figures are based on Class A shares and do not reflect deduction of the sales charges or taxes that a shareholder would pay on distributions or the redemption of shares.

| | |

Performance Summary September 30, 2008 | | Security Equity Fund Equity Series (unaudited) |

| |

| |

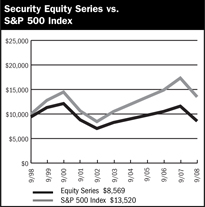

$10,000 Over Ten Years

This chart assumes a $10,000 investment in Class A shares of Equity Series on September 30, 1998, reflects deduction of the 5.75% sales load and assumes all dividends reinvested. The chart does not reflect the deduction of taxes that a shareholder would pay on distributions or the redemption of fund shares. The S&P 500 Index is a capitalization weighted index composed of 500 selected common stocks that represent the broad domestic economy and is a widely recognized unmanaged index of market performance.

| | | | | | | | |

Average Annual Returns |

| | | | | |

Periods Ended 9-30-08 | | 1 Year | | 5 Years | | 10 Years | | Since Inception |

| | | | | (1-29-99) |

A Shares | | (26.12%) | | 0.71% | | (0.95%) | | – |

A Shares with sales charge | | (30.39%) | | (0.46%) | | (1.53%) | | – |

B Shares | | (26.69%) | | (0.06%) | | (1.65%) | | – |

B Shares with CDSC | | (29.69%) | | (0.32%) | | (1.65%) | | – |

C Shares | | (26.79%) | | (0.06%) | | – | | (3.92%) |

C Shares with CDSC | | (27.39%) | | (0.06%) | | – | | (3.92%) |

The performance data above represents past performance that is not predictive of future results. The investment return and principal value of an investment in the Series will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The figures above do not reflect deduction of the maximum front-end sales charge of 5.75% for Class A shares or the contingent deferred sales charge of 5% for Class B shares and 1% for Class C shares, as applicable, except where noted. The figures do not reflect the deduction of taxes that a shareholder would pay on distributions or redemption of shares. Such figures would be lower if the maximum sales charge and any applicable taxes were deducted. |

| | | | | | |

| | | Portfolio Composition by Sector as of 9-30-08 |

| | | Consumer Discretionary | | 10.35% | | |

| | | Consumer Staples | | 11.50 | | |

| | | Energy | | 8.93 | | |

| | | Financials | | 8.07 | | |

| | | Health Care | | 11.34 | | |

| | | Industrials | | 18.07 | | |

| | | Information Technology | | 16.64 | | |

| | | Materials | | 7.04 | | |

| | | Exchange Traded Funds | | 1.00 | | |

| | | Telecommunication Services | | 0.96 | | |

| | | Utilities | | 1.09 | | |

| | | U.S. Government Sponsored Agencies | | 1.82 | | |

| | | Repurchase Agreement | | 3.45 | | |

| | | Liabilities, Less Cash & Other Assets | | (0.26) | | |

| | | Total Net Assets | | 100.00% | | |

| | | | | | | |

| | | | | | | |

| | | | |

| | 18 | | The accompanying notes are an integral part of the financial statements |

| | |

Performance Summary September 30, 2008 | | Security Equity Fund Equity Series (unaudited) |

| |

| |

Information About Your Series Expenses

Calculating your ongoing Series expenses

Example

As a shareholder of the Series, you incur two types of costs: (1) transaction costs, which may include sales charges (loads) on purchase payments; contingent deferred sales charges on redemptions; and redemption fees, if any; and (2) ongoing costs, including management fees; distribution and/or service fees (12b-1); and other Series expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Series and to compare these costs with ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period April 1, 2008 through September 30, 2008.

Actual Expenses

The first line for each class of shares in the table provides information about actual account values and actual expenses. You may use the information in this table, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the table under the heading entitled “Expenses Paid During the Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line for each class of shares in the table provides information about hypothetical account values and hypothetical expenses based on the Series actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Series actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Series and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other mutual funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) on purchase payments, contingent deferred sales charges on redemptions, and redemption fees, if any. Therefore, the second line for each class of shares is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | | | | | |

Series Expenses |

| | | Beginning

Account

Value

4/1/2008 | | Ending

Account

Value

9/30/2008 1 | | Expenses

Paid

During

Period 2 |

Equity Series - | | | | | | |

Class A | | | | | | |

Actual | | $1,000.00 | | $860.61 | | $6.28 |

Hypothetical | | 1,000.00 | | 1,018.25 | | 6.81 |

Equity Series - | | | | | | |

Class B | | | | | | |

Actual | | 1,000.00 | | 856.80 | | 9.75 |

Hypothetical | | 1,000.00 | | 1,014.50 | | 10.58 |

Equity Series - | | | | | | |

Class C | | | | | | |

Actual | | 1,000.00 | | 856.18 | | 9.74 |

Hypothetical | | 1,000.00 | | 1,014.50 | | 10.58 |

1 The actual ending account value is based on the actual total return of the Series for the period April 1, 2008 to September 30, 2008 after actual expenses and will differ from the hypothetical ending account value which is based on the Series expense ratio and a hypothetical annual return of 5% before expenses. The actual cumulative return at net asset value for the period April 1, 2008 to September 30, 2008 was (13.94%), (14.32%) and (14.38%), for Class A, B, and C shares, respectively.

2 Expenses are equal to the Series annualized expense ratio (1.35%, 2.10% and 2.10% for Class A, B, and C shares, respectively), net of any applicable fee waivers or earnings credits, multiplied by the average account value over the period, multiplied by 183/366 (to reflect the one-half year period).

| | |

| Schedule of Investments | | Security Equity Fund |

September 30, 2008 | | Equity Series |

| | | | |

| | | Shares | | Value |

| COMMON STOCKS - 95.0% |

| Aerospace & Defense - 3.4% | | | | |

Honeywell International, Inc. | | 77,770 | | $3,231,344 |

United Technologies Corporation | | 68,900 | | 4,138,134 |

| | | | |

| | | | 7,369,478 |

| | | | |

| Air Freight & Logistics - 1.8% | | | | |

FedEx Corporation | | 49,200 | | 3,888,768 |

| | | | |

| Asset Management & Custody Banks - 1.5% | | | | |

Bank of New York Mellon Corporation | | 102,935 | | 3,353,622 |

| | | | |

| Biotechnology - 3.7% | | | | |

Celgene Corporation * | | 53,290 | | 3,372,191 |

Gilead Sciences, Inc. * | | 101,735 | | 4,637,081 |

| | | | |

| | | | 8,009,272 |

| | | | |

Broadcasting - 0.3% | | | | |

CBS Corporation | | 47,000 | | 687,610 |

| | | | |

| | |

Building Products - 1.8% | | | | |

USG Corporation * | | 151,800 | | 3,886,080 |

| | | | |

| | |

Cable & Satellite - 1.0% | | | | |

Comcast Corporation | | 117,200 | | 2,300,636 |

| | | | |

Communications Equipment - 4.2% | | | | |

Cisco Systems, Inc. * | | 105,895 | | 2,388,991 |

Corning, Inc. | | 151,755 | | 2,373,448 |

Qualcomm, Inc. | | 63,895 | | 2,745,568 |

Research In Motion, Ltd. * | | 25,225 | | 1,722,868 |

| | | | |

| | | | 9,230,875 |

| | | | |

Computer Hardware - 5.0% | | | | |

Apple, Inc. * | | 35,660 | | 4,053,116 |

Hewlett-Packard Company | | 150,085 | | 6,939,930 |

| | | | |

| | | | 10,993,046 |

| | | | |

Construction & Farm Machinery & Heavy Trucks - 1.3% | | | | |

Deere & Company | | 59,420 | | 2,941,290 |

| | | | |

| Construction Materials - 0.8% | | |

Vulcan Materials Company | | 24,900 | | 1,855,050 |

| | | | |

| Consumer Finance - 1.3% | | | | |

Capital One Financial Corporation | | 38,800 | | 1,978,800 |

First Marblehead Corporation | | 334,900 | | 833,901 |

| | | | |

| | | | 2,812,701 |

| | | | |

| | | | |

| Data Processing & Outsourced Services - 2.9% | | | | |

Visa, Inc. | | 44,910 | | 2,757,025 |

Western Union Company | | 145,300 | | 3,584,551 |

| | | | |

| | | | 6,341,576 |

| | | | |

Department Stores - 1.1% | | | | |

JC Penney Company, Inc. | | 71,700 | | 2,390,478 |

| | | | |

| Diversified Banks - 1.2% | | | | |

Wells Fargo & Company | | 68,700 | | 2,578,311 |

| | | | |

| Diversified Chemicals - 0.7% | | | | |

Dow Chemical Company | | 49,600 | | 1,576,288 |

| | | | |

| | | | |

| | | Shares | | Value |

| COMMON STOCKS (continued) |

| Drug Retail - 3.3% | | | | |

CVS Caremark Corporation | | 216,885 | | $7,300,349 |

| | | | |

| Electric Utilities - 1.1% | | | | |

Edison International | | 60,000 | | 2,394,000 |

| | | | |

| Electrical Components & Equipment - 2.0% | | | | |

Emerson Electric Company | | 105,330 | | 4,296,411 |

| | | | |

| Electronic Manufacturing Services - 0.4% | | | | |

Tyco Electronics, Ltd. | | 32,800 | | 907,248 |

| | | | |

Exchange Traded Funds - 1.0% | | | | |

iShares Russell 1000 Value Index Fund | | 17,100 | | 1,092,519 |

iShares S&P 500 Value Index Fund | | 18,300 | | 1,095,255 |

| | | | |

| | | | 2,187,774 |

| | | | |

Fertilizers & Agricultural | | | | |

Chemicals - 3.1% | | | | |

Monsanto Company | | 33,980 | | 3,363,340 |

Mosaic Company | | 50,485 | | 3,435,000 |

| | | | |

| | | | 6,798,340 |

| | | | |

| Footwear - 1.8% | | | | |

Nike, Inc. (Cl.B) | | 58,195 | | 3,893,246 |

| | | | |

| Health Care Equipment - 1.7% | | | | |

Covidien, Ltd. | | 33,800 | | 1,817,088 |