V

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2017

OR

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 000-50039

OLD DOMINION ELECTRIC COOPERATIVE

(Exact name of Registrant as specified in its charter)

VIRGINIA | | 23-7048405 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. employer identification no.) |

| | |

4201 Dominion Boulevard, Glen Allen, Virginia | | 23060 |

(Address of principal executive offices) | | (Zip code) |

(804) 747-0592

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act: NONE

Securities registered pursuant to Section 12(g) of the Act: NONE

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act? Yes ☐ No ☒

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Securities Exchange Act (the “Exchange Act”). Yes ☒ No ☐

Indicate by check mark whether the Registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☐ No ☒

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405) is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this form 10-K. ☒

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ☐ | | Accelerated filer | ☐ |

Non-accelerated filer | ☒ | | Smaller reporting company | ☐ |

Emerging growth company | ☐ | | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the Registrant is a shell company (as defined in Exchange Act Rule 12b-2). Yes ☐ No ☒

State the aggregate market value of the voting and non-voting common equity held by non-affiliates of the Registrant. NONE

Indicate the number of shares outstanding of each of the Registrant’s classes of common stock. The Registrant is a membership corporation and has no authorized or outstanding equity securities.

Documents incorporated by reference: NONE

OLD DOMINION ELECTRIC COOPERATIVE

2017 ANNUAL REPORT ON FORM 10-K

GLOSSARY OF TERMS

The following abbreviations or acronyms used in this Form 10-K are defined below:

Abbreviation or Acronym | Definition |

ACES | Alliance for Cooperative Energy Services Power Marketing, LLC |

Alstom | Alstom Power, Inc. |

Bear Island | Bear Island Paper WB LLC |

CAA | Clean Air Act |

CCRs | Coal combustion residuals |

CEC | Choptank Electric Cooperative, Inc. |

CEO | Chief Executive Officer |

CFO | Chief Financial Officer |

Clover | Clover Power Station |

CO2 | Carbon dioxide |

CSAPR | Cross-State Air Pollution Rule |

D.C. Circuit | U.S. Court of Appeals for the District of Columbia Circuit |

DEC | Delaware Electric Cooperative, Inc. |

DPSC | Delaware Public Service Commission |

DOE | U.S. Department of Energy |

EGU | Electric generating unit |

EPA | Environmental Protection Agency |

EPACT | Energy Policy Act of 2005, as amended |

EPC | Engineering, procurement, and construction |

FERC | Federal Energy Regulatory Commission |

Fitch | Fitch Ratings, Inc. |

GAAP | Accounting principles generally accepted in the United States |

GHG | Greenhouse gases |

Indenture | Second Amended and Restated Indenture of Mortgage and Deed of Trust, dated January 1, 2011, of ODEC with Branch Banking and Trust Company, as trustee, as amended and supplemented |

IRC | Internal Revenue Code of 1986, as amended |

kV | Kilovolt |

LIBOR | London Interbank Offered Rate |

MATS | Mercury and Air Toxics Standards |

Mitsubishi | Mitsubishi Hitachi Power Systems Americas, Inc. |

Moody’s | Moody’s Investors Service |

MPSC | Maryland Public Service Commission |

MW | Megawatt(s) |

MWh | Megawatt hour(s) |

NAAQS | National Ambient Air Quality Standards |

NERC | North American Electric Reliability Corporation |

North Anna | North Anna Nuclear Power Station |

North Anna Unit 3 | A potential additional nuclear-powered generating unit at North Anna |

|

NOVEC | Northern Virginia Electric Cooperative |

NOx | Nitrogen oxide |

NRC | U.S. Nuclear Regulatory Commission |

NRECA | National Rural Electric Cooperative Association |

NYMEX | New York Mercantile Exchange |

ODEC, We, Our, Us | Old Dominion Electric Cooperative |

PJM | PJM Interconnection, LLC |

PPA | Pension Protection Act |

RCRA | Resource Conservation and Recovery Act, as amended |

REC | Rappahannock Electric Cooperative |

2

Abbreviation or Acronym | Definition |

RICE | Reciprocating Internal Combustion Engine National Emissions Standards for Hazardous Air Pollutants |

RGGI | Regional Greenhouse Gas Initiative |

RPM | Reliability Pricing Model |

RPS | Renewable portfolio standards |

RTO | Regional transmission organization |

RUS | U.S. Department of Agriculture Rural Utilities Service |

S&P | Standard & Poor’s Ratings Services |

SEPA | Southeastern Power Administration |

SIP | State Implementation Plan |

SO2 | Sulfur dioxide |

SVEC | Shenandoah Valley Electric Cooperative |

TEC | TEC Trading, Inc. |

VDEQ | Virginia Department of Environmental Quality |

Virginia Power | Virginia Electric and Power Company |

VMDAEC | Virginia, Maryland, and Delaware Association of Electric Cooperatives |

VSCC | Virginia State Corporation Commission |

Wildcat Point | Wildcat Point Generation Facility |

WOPC | White Oak Power Constructors |

XBRL | Extensible Business Reporting Language |

3

PART I

ITEM 1. BUSINESS

OVERVIEW

Old Dominion Electric Cooperative was incorporated under the laws of the Commonwealth of Virginia in 1948 as a not-for-profit power supply cooperative. We are organized for the purpose of supplying the power our member distribution cooperatives require to serve their customers on a cost-effective basis. We serve their power requirements pursuant to long-term, all-requirements wholesale power contracts. Through our member distribution cooperatives, we served approximately 580,000 retail electric customers (meters), representing a total population of approximately 1.4 million people in 2017.

We supply our member distribution cooperatives’ power requirements, consisting of demand requirements and energy requirements, through a portfolio of resources including generating facilities, power purchase contracts, and spot market energy purchases. Our generating facilities are fueled by a mix of coal, nuclear, natural gas, and fuel oil. We are a member of a regional transmission organization, PJM, and we participate in its energy, capacity, and transmission services markets to serve our member distribution cooperatives. See “Power Supply Resources” below and “Properties” in Item 2 for a description of these resources.

We are owned entirely by our members, which are the primary purchasers of the power we sell. We have two classes of members. Our Class A members are customer-owned electric distribution cooperatives that are engaged in the retail sale of power to their customers. Our sole Class B member is TEC, a taxable corporation owned by our member distribution cooperatives. Our member distribution cooperatives primarily serve rural, suburban, and recreational areas of the mid-Atlantic region. See “Members—Service Territories and Customers” below.

We are a power supply cooperative. In general, a cooperative is a business organization owned by its members, which are also either the cooperative’s wholesale or retail customers. Cooperatives are designed to give their members the opportunity to satisfy their collective needs in a particular area of business more effectively than if the members acted independently. As not-for-profit organizations, cooperatives are intended to provide services to their members on a cost-effective basis, in part by eliminating the need to produce profits or a return on equity in excess of required margins. Margins not distributed to members constitute patronage capital, a cooperative’s principal source of equity. Patronage capital is held for the account of the members without interest and returned when the board of directors of the cooperative deems it appropriate to do so.

Electric distribution cooperatives form power supply cooperatives to acquire power supply resources, typically through the construction of generating facilities or the development of other power purchase arrangements, at a lower cost than if they were acquiring those resources alone.

Our Class A members are electric distribution cooperatives. Electric distribution cooperatives own and operate electric distribution systems to supply the power requirements of their retail customers. Electric distribution cooperatives own and maintain nearly half of the distribution lines in the United States and serve almost three-quarters of the United States’ land mass.

We are a not-for-profit electric cooperative and currently are exempt from federal income taxation under IRC Section 501(c)(12).

We are not a party to any collective bargaining agreement. We had 136 employees as of March 1, 2018.

Our principal executive office is located at 4201 Dominion Boulevard, Glen Allen, Virginia 23060. Our telephone number is (804) 747-0592.

4

MEMBERS

Member Distribution Cooperatives

General

Our member distribution cooperatives provide electric services, consisting of power supply, transmission services, and distribution services (including metering and billing services) to residential, commercial, and industrial customers. We have eleven member distribution cooperatives that serve customers in 70 counties in Virginia, Delaware, and Maryland. The member distribution cooperatives’ distribution business involves the operation of substations, transformers, and electric lines that deliver power to their customers.

Eight of our member distribution cooperatives provide electric services on the Virginia mainland:

BARC Electric Cooperative

Community Electric Cooperative

Mecklenburg Electric Cooperative

Northern Neck Electric Cooperative

Prince George Electric Cooperative

Rappahannock Electric Cooperative

Shenandoah Valley Electric Cooperative

Southside Electric Cooperative

Three of our member distribution cooperatives provide electric services on the Delmarva Peninsula:

A&N Electric Cooperative in Virginia

Choptank Electric Cooperative, Inc. in Maryland

Delaware Electric Cooperative, Inc. in Delaware

The member distribution cooperatives are not our subsidiaries, but rather our owners. We have no interest in their assets, liabilities, equity, revenues, or margins.

Revenues from our member distribution cooperatives and the percentage each contributed to total revenues from sales to our member distribution cooperatives in 2017 are as follows:

Member Distribution Cooperatives | | Revenues | |

| | (in millions) | | | |

Rappahannock Electric Cooperative | | $ | 217.7 | | 29.8 | % |

Shenandoah Valley Electric Cooperative | | | 146.8 | | 20.0 | |

Delaware Electric Cooperative, Inc. | | | 97.5 | | 13.3 | |

Choptank Electric Cooperative, Inc. | | | 69.7 | | 9.5 | |

Southside Electric Cooperative | | | 58.4 | | 8.0 | |

A&N Electric Cooperative | | | 46.0 | | 6.3 | |

Mecklenburg Electric Cooperative | | | 36.7 | | 5.0 | |

Prince George Electric Cooperative | | | 20.6 | | 2.8 | |

Northern Neck Electric Cooperative | | | 18.2 | | 2.5 | |

Community Electric Cooperative | | | 11.4 | | 1.6 | |

BARC Electric Cooperative | | | 8.6 | | 1.2 | |

Total | | $ | 731.6 | | 100.0 | % |

In 2017, there was no individual customer of our member distribution cooperatives that constituted 1% or more of our revenues from our member distribution cooperatives.

5

Service Territories and Customers

The territories served by our member distribution cooperatives cover large portions of Virginia, Delaware, and Maryland. These service territories range from the extended suburbs of Washington, D.C. to the North Carolina border and from the Atlantic shores of Virginia, Delaware, and Maryland to the Appalachian Mountains.

Our member distribution cooperatives’ service territories encompass primarily rural, suburban, and recreational areas. Our member distribution cooperatives’ customers’ requirements for capacity and energy generally are seasonal and increase in winter and summer as home heating and cooling needs increase and then decline in the spring and fall as the weather becomes milder. Our member distribution cooperatives also serve major industries which include manufacturing, poultry, telecommunications, agriculture, forestry and wood products, health care, and recreation.

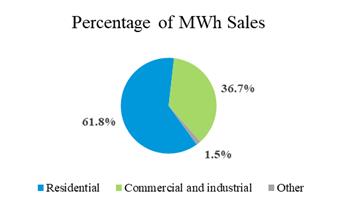

Our member distribution cooperatives’ sales of energy in 2017 totaled approximately 11,600,000 MWh. These sales were divided by customer class as follows:

From 2012 through 2017, our eleven member distribution cooperatives experienced a compound annual growth rate of 0.9% in the number of customers (meters) and energy sales measured in MWh were relatively flat.

Our eleven member distribution cooperatives’ average number of customers per mile of energized line has been relatively unchanged from 2012 to 2017 at approximately 9.5 customers per mile. System densities of our member distribution cooperatives in 2017 ranged from 6.3 customers per mile in the service territory of BARC Electric Cooperative to 14.4 customers per mile in the service territory of A&N Electric Cooperative. In 2017, the average service density for all electric distribution cooperatives in the United States was approximately 7.4 customers per mile.

Delaware and Maryland each currently grant all retail customers the right to choose their power supplier. Virginia currently grants a limited number of large retail customers the right to choose their power suppliers and then only in very limited circumstances. The laws of each state grant utilities, including our member distribution cooperatives, the exclusive right to provide transmission and distribution (including metering and billing) services and to be the default providers of power to their customers in service territories certified by their respective state public service commissions. See “Regulation of Member Distribution Cooperatives” and “Competition” below.

Wholesale Power Contracts

Our financial relationships with our member distribution cooperatives are based primarily on our contractual arrangements for the supply of power and related transmission and ancillary services. These arrangements are set forth in our wholesale power contracts with our member distribution cooperatives which are effective until January 1, 2054, and beyond this date unless either party gives the other at least three years notice of termination. The wholesale power contracts are all-requirements contracts. Each contract obligates us to sell and deliver to our member distribution cooperative, and obligates our member distribution cooperative to purchase and receive from us, all power that it requires for the operation of its system, with limited exceptions, to the extent that we have the power and facilities available to do so.

6

An exception to the all-requirements obligations of our member distribution cooperatives relates to the ability of our eight mainland Virginia member distribution cooperatives to purchase hydroelectric power allocated to them from SEPA, a federal power marketing administration. Purchases under this exception constituted less than 2% of our member distribution cooperatives’ total energy requirements in 2017.

There are two additional limited exceptions to the all-requirements nature of the contract. One exception permits each of our member distribution cooperatives, with 180 days prior written notice, to receive up to the greater of 5% of its demand and associated energy or 5 MW and associated energy from its owned generation or from other suppliers. The other exception permits our member distribution cooperatives to purchase additional power from other suppliers in limited circumstances following approval by our board of directors.

If all of our member distribution cooperatives elected to utilize the 5% or 5 MW exception, we estimate the current impact would be a reduction of approximately 175 MW of demand and associated energy. As of May 1, 2018, there will be approximately 66 MW remaining that can be utilized under this exception. The following table summarizes the cumulative removal of load requirements under this exception since January 1, 2016.

Date | | MW | |

January 1, 2016 | | | 9 | |

May 1, 2016 | | | 60 | |

June 1, 2017 | | | 65 | |

May 1, 2018 | | | 109 | |

We do not anticipate that either the current or potential full utilization of this exception will have a material impact on our financial condition, results of operations, or cash flows.

As of December 31, 2017, none of our member distribution cooperatives had utilized the other exception noted above.

Each member distribution cooperative is required to pay us monthly for power furnished under its wholesale power contract in accordance with our formula rate. We review our formula rate design at least every three years to consider whether it is appropriately achieving its intended results. The formula rate, which has been filed with and accepted by FERC, is designed to recover our total cost of service and create a firm equity base. See “Regulation—Rate Regulation” below, "Legal Proceedings—FERC Proceeding Related to Formula Rate" in Item 3, and “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Factors Affecting Results—Formula Rate” in Item 7.

More specifically, the formula rate is intended to meet all of our costs, expenses, and financial obligations associated with our ownership, operation, maintenance, repair, replacement, improvement, modification, retirement, and decommissioning of our generating plants, transmission system, or related facilities, services provided to the member distribution cooperatives, and the acquisition and transmission of power or related services, including:

| • | payments of principal and premium, if any, and interest on all indebtedness issued by us (other than payments resulting from the acceleration of the maturity of the indebtedness); |

| • | any additional cost or expense, imposed or permitted by any regulatory agency; and |

| • | additional amounts necessary to meet the requirement of any rate covenant with respect to coverage of principal and interest on our indebtedness contained in any indenture or contract with holders of our indebtedness. |

The rates established under the wholesale power contracts are designed to enable us to comply with financing, regulatory, and governmental requirements, which apply to us from time to time.

Regulation of Member Distribution Cooperatives

Of our 11 member distribution cooperatives, eight currently participate in RUS loan or guarantee programs. These member distribution cooperatives have entered into loan documents with RUS that we understand contain affirmative and

7

negative covenants, including with respect to matters such as accounting, issuances of securities, rates and charges for the sale of power, construction or acquisition of facilities, and the purchase and sale of power. In addition, we understand financial covenants in these member distribution cooperatives’ loan documents require them to design rates to achieve an interest coverage ratio and a debt service coverage ratio. Finally, we understand that the principal loan documentation of our member distribution cooperatives that do not participate in RUS loan or guarantee programs contains similar covenants.

Our member distribution cooperatives in Virginia are subject to rate regulation by the VSCC in the provision of electric services to their customers, but they have the ability to pass through changes in their wholesale power costs, including the demand and energy costs we charge our member distribution cooperatives, to their customers. Our Virginia member distribution cooperatives also may adjust their rates for distribution service by a maximum net increase or decrease of 5%, on a cumulative basis, in any three-year period without approval by the VSCC. Additionally, they may make adjustments to their rates to collect fixed costs through a new or modified fixed monthly charge rather than through volumetric charges associated with energy usage, so long as such adjustments are revenue neutral.

The MPSC regulates the rates and services offered by our Maryland member distribution cooperative, CEC, other than wholesale power costs, which are a pass-through to CEC’s customers. Our Delaware member distribution cooperative, DEC, is not regulated by the DPSC, including with respect to wholesale power costs which are a pass-through to its customers.

We are not subject to any RPS; however DEC is subject to RPS. DEC meets the RPS through purchases of renewable energy credits, and owned and purchased resources pursuant to the 5% or 5 MW exception in its wholesale power contract with us. See “Wholesale Power Contracts” above.

Competition

Delaware and Maryland each have laws unbundling the power component (also known as the generation component) of electric service to retail customers, while maintaining regulation of transmission and distribution services. All retail customers in Delaware, including customers of DEC, are currently permitted to purchase power from a registered supplier only after DEC approves the supplier’s ability to do business in its service territory. All retail customers in Maryland, including customers of CEC, are currently permitted to purchase power from the registered supplier of their choice. As of March 1, 2018, no retail customer of DEC or CEC has switched to an alternative power supplier.

In Virginia, retail choice in the selection of a power supplier is available to customers that consume at least 5 MW of power individually or in the aggregate (with aggregation subject to the approval of the VSCC) and that do not account for more than 1% of the incumbent utility's peak load during the past year. Currently, no customer of our member distribution cooperatives has elected to choose an alternate supplier under this provision. Retail choice is also available to any customer whose noncoincident peak demand exceeds 90 MW. Beginning June 1, 2016, Bear Island, an industrial customer of REC and the only customer of any of our member distribution cooperatives that has noncoincident peak demand that exceeds 90 MW, elected to purchase its power requirements from an alternate supplier. Additionally, all Virginia retail customers are permitted to select an alternative power supplier that provides 100% renewable energy if their incumbent utility, such as one of our member distribution cooperatives, does not offer this same option. As of December 31, 2017, eight of our nine Virginia member distribution cooperatives provided this option.

Currently, we do not anticipate that any of these limited rights to retail choice of our member distribution cooperatives’ customers, individually or in the aggregate, will have a material impact on our financial condition, results of operations, or cash flows.

TEC

TEC is owned by our member distribution cooperatives and currently is our only Class B member. We have a power sales contract with TEC under which we may sell to TEC power that we do not need to meet the needs of our member distribution cooperatives. TEC then sells this power to the market under market-based rate authority granted by FERC. Additionally, we have a separate contract under which we may purchase natural gas from TEC. TEC does not

8

engage in speculative trading. To facilitate TEC’s participation in the power and natural gas markets, we have agreed to provide a maximum of $200 million in credit support to TEC. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources—Uses—Significant Contingent Obligations—TEC Guarantees” in Item 7.

POWER SUPPLY RESOURCES

General

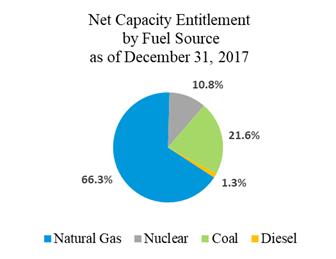

We provide power to our members through a combination of our interests in Clover, a coal-fired generating facility; North Anna, a nuclear power station; our three natural gas-fired combustion turbine facilities – Louisa, Marsh Run, and Rock Springs; diesel-fired distributed generation facilities; and physically-delivered forward power purchase contracts and spot market energy purchases. Our energy supply resources for the past three years were as follows:

| | Year Ended December 31, |

| | 2017 | | 2016 | | 2015 |

| | (in MWh and percentages) |

Generated: | | | | | | | | | | | | | |

Clover | | 1,616,377 | | 13.6 | % | 2,714,966 | | 21.3 | % | 2,734,519 | | 19.6 | % |

North Anna | | 1,870,626 | | 15.7 | | 1,766,491 | | 13.9 | | 1,887,395 | | 13.5 | |

Louisa | | 262,797 | | 2.2 | | 366,274 | | 2.9 | | 403,489 | | 2.9 | |

Marsh Run | | 472,447 | | 4.0 | | 553,597 | | 4.3 | | 689,713 | | 4.9 | |

Rock Springs | | 143,571 | | 1.2 | | 362,738 | | 2.8 | | 297,610 | | 2.1 | |

Distributed Generation | | 605 | | — | | 1,066 | | — | | 1,388 | | — | |

Total Generated | | 4,366,423 | | 36.7 | | 5,765,132 | | 45.2 | | 6,014,114 | | 43.0 | |

Purchased: | | | | | | | | | | | | | |

Other than renewable: | | | | | | | | | | | | | |

Long-term and short-term | | 4,913,333 | | 41.3 | | 5,211,045 | | 40.9 | | 6,554,835 | | 46.8 | |

Spot market | | 1,849,489 | | 15.5 | | 993,413 | | 7.8 | | 677,836 | | 4.8 | |

Total Other than renewable | | 6,762,822 | | 56.8 | | 6,204,458 | | 48.7 | | 7,232,671 | | 51.6 | |

Renewable (1) | | 777,505 | | 6.5 | | 782,871 | | 6.1 | | 751,458 | | 5.4 | |

Total Purchased | | 7,540,327 | | 63.3 | | 6,987,329 | | 54.8 | | 7,984,129 | | 57.0 | |

Total Available Energy | | 11,906,750 | | 100.0 | % | 12,752,461 | | 100.0 | % | 13,998,243 | | 100.0 | % |

| (1) | Related to our contracts from renewable facilities from which we obtain renewable energy credits. We sell these renewable energy credits to our member distribution cooperatives and non-members. |

In 2017, our generating facilities satisfied approximately 73.4% of our PJM capacity obligation. For a description of our generating facilities, see “Properties” in Item 2. In 2017, we obtained the remainder of our PJM capacity obligation through the PJM RPM capacity auction process and purchased capacity contracts. See “PJM” below. The energy requirements not met by our owned generating facilities were obtained from multiple suppliers under various long-term and short-term physically-delivered forward power purchase contracts and spot market purchases. See “Power Purchase Contracts” below.

In 2017, our peak demand obligation to our member distribution cooperatives occurred in January and was 2,911 MW.

We plan to continue purchasing energy into the future by utilizing a combination of physically-delivered forward power purchase contracts, as well as spot market purchases. As we have done in the past, we expect to adjust our portfolio of power supply resources to reflect our projected power requirements and changes in the market. To assist us in these efforts, we engage ACES, an energy trading and risk management company. Specifically, ACES assists us in negotiating power purchase contracts, evaluating the credit risk of counterparties, modeling our power requirements, bidding and dispatch of the generating facilities that we operate, and executing and settling energy transactions. See “Quantitative and Qualitative Disclosures About Market Risk” in Item 7A.

9

Power Supply Planning

By utilizing various long-term and short-term planning processes and models, we continually evaluate power supply options available to us to meet the needs of our member distribution cooperatives. We have policies that establish targets that define how our projected power needs will be met, and one of the ways we manage these targets is the utilization of hedging. We use hedging instruments, including forwards, futures, financial transmission rights, and options, to manage our power market price risks. These hedging instruments have varying time periods ranging from one month to multiple years in advance. Additionally, we evaluate other power supply options including the acquisition, development, or disposition of generating facilities.

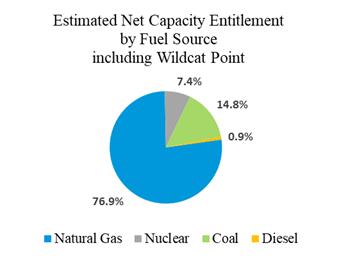

Wildcat Point

We are the sole owner of an approximate 1,000 MW natural gas-fueled combined cycle generation facility, named Wildcat Point, in Cecil County, Maryland. Wildcat Point's major equipment consists of two Mitsubishi combustion turbines, two Alstom heat recovery steam generators, and one Alstom steam turbine generator. While the facility was scheduled to become operational in mid-2017, we currently anticipate that Wildcat Point will achieve substantial completion in the spring of 2018. The majority of construction has been completed; however some additional construction work and testing is required before Wildcat Point becomes commercially operable and available for dispatch by PJM to meet a portion of our member distribution cooperatives’ power requirements. WOPC, the EPC contractor, claims that the delay was associated with the incurrence of additional work and other matters, including alleged misrepresentation under the EPC contract, for which it will seek recovery, in whole or in part, from its subcontractors and us. See “Item 3 – Legal Proceedings.”

PJM

PJM is an RTO that coordinates the transmission of wholesale electricity in all or parts of 13 states and the District of Columbia. As a federally regulated RTO, PJM must act independently and impartially in managing the regional transmission system and the wholesale electricity market. PJM is primarily responsible for ensuring the reliability of the largest centrally dispatched energy market in North America. PJM coordinates the continuous buying, selling, and delivery of wholesale electricity throughout its members’ service territories. PJM system operators continuously conduct dispatch operations and monitor the status of the transmission grid of its participants. PJM also oversees a regional planning process for transmission expansion to ensure the continued reliability of the PJM electric system. PJM coordinates and establishes policies for the generation, purchase, and sale of capacity and energy in the control areas of its members.

All of our member distribution cooperatives’ service territories are in PJM. As a member of PJM, we are subject to the operations of PJM, and our generating facilities are under dispatch control of PJM. We transmit power to our member distribution cooperatives through the transmission facilities subject to operational control of PJM. We have agreements with PJM that provide us with access to transmission facilities under PJM’s operational control as necessary to deliver energy to our member distribution cooperatives. We own a limited amount of transmission facilities. See “Properties—Transmission” in Item 2.

PJM balances its participants’ power requirements with the power resources available to supply those requirements. Based on this evaluation of supply and demand, PJM schedules and dispatches available generating facilities throughout its region in a manner intended to meet the demand for energy in the most reliable and cost-effective manner. Thus PJM directs the dispatch of these facilities even though it does not own them. When PJM cannot dispatch the most economical generating facilities due to transmission constraints, PJM will dispatch more expensive generating facilities to meet the required power requirements. PJM participants whose power requirements cause the redispatch are obligated to pay the additional costs to dispatch the more expensive generating facilities. These additional costs are commonly referred to as congestion costs. PJM conducts the auction of financial transmission rights for future periods to provide market participants an opportunity to hedge these congestion costs.

The PJM energy market consists of day-ahead and real-time markets. PJM’s day-ahead market is a forward market in which hourly locational marginal prices are calculated for the following day based on the prices at which the owners of

10

generating facilities, including ODEC, offer to run their facilities to meet the requirements of energy customers. PJM’s real-time market is a spot market in which current locational marginal prices are calculated at five-minute intervals.

PJM rules require that load serving entities, such as ODEC, meet certain minimum capacity obligations. These obligations can be met through a combination of owned generation resources and purchases under bilateral agreements and from forward capacity auctions under PJM’s capacity construct, known as RPM. The purpose of PJM’s capacity construct is to develop a longer-term pricing program for capacity resources, to provide localized pricing for capacity, and to reduce the resulting investment risk to owners of generating resources, thus encouraging new investment in generating facilities. The value of capacity resources can vary by location and RPM provides for the recognition of the locational value. To date, PJM has conducted capacity auctions for capacity to be supplied through May 31, 2021. Each annual auction is held 36 months before each subsequent delivery year, and incremental auctions may be held at prescribed dates after the base residual auction for each delivery year to adjust for changes to the load forecast and the availability of capacity.

Concurrent with the PJM delivery year beginning June 1, 2016, the PJM tariff provides for a new component referred to as capacity performance, which is intended to improve the reliability of the power grid by increasing the availability of generating units, especially during emergency conditions. Generation owners, such as ODEC, could earn increased compensation for capacity for some of their generating units and will be exposed to significantly higher charges if their generation units do not perform during emergency conditions. For the PJM delivery year beginning June 1, 2016, qualifying generating units were allowed to be voluntarily offered into PJM’s capacity auction as a capacity performance unit. A unit not offered as a capacity performance unit, known as a base capacity unit, will be excluded from the assessment of the charges for non-performance during the winter months. Starting with the delivery year beginning June 1, 2020, PJM will require the majority of generating resources to be offered as capacity performance units, eliminating the base capacity option. We continue to evaluate our bidding strategy for our generating units for the PJM capacity auctions.

Power Purchase Contracts

We purchase significant amounts of power in the market from investor-owned utilities and power marketers through long-term and short-term physically-delivered forward power purchase contracts. We also purchase power in the spot energy market. This approach to meeting our member distribution cooperatives’ energy requirements is not without risks. See “Risk Factors” in Item 1A. below. To mitigate these risks, we attempt to match our energy purchases with our energy needs to reduce our spot market purchases of energy and sales of excess energy. Additionally, we utilize policies, procedures, and various hedging instruments to manage our power market risks. These policies and procedures, developed in consultation with ACES, are designed to strike an appropriate balance between minimizing costs and reducing energy cost volatility. See “Quantitative and Qualitative Disclosures About Market Risk” in Item 7A.

Renewables

We have contracts with companies that own and operate wind, solar, and landfill gas facilities. These contracts allow us to buy output, including renewable energy credits, from the renewable facilities at a predetermined price. We sell these renewable energy credits to our member distribution cooperatives and non-members. We do not own or operate any of these facilities and are not responsible for their operational costs or performance.

Fuel Supply

Coal

Virginia Power, as operating agent of Clover, has the sole authority and responsibility to procure coal for the facility. Virginia Power advises us that it uses both long-term contracts and short-term spot agreements to acquire the low sulfur bituminous coal used to fuel the facility. We are not a direct party to any of these procurement contracts and we do not control their terms or duration. As of December 31, 2017 and December 31, 2016, there was a 55-day and a 61-day supply of coal at Clover, respectively. We anticipate that sufficient supplies of coal will be available in the future to operate the facility when dispatched by PJM. See “Quantitative and Qualitative Disclosures About Market Risk” in Item 7A.

11

Nuclear

Virginia Power, as operating agent of North Anna, has the sole authority and responsibility to procure nuclear fuel for the facility. Virginia Power advises us that it primarily uses long-term contracts to support North Anna’s nuclear fuel requirements and that worldwide market conditions are continuously evaluated to ensure a range of supply options at reasonable prices, which are dependent upon the market environment. We are not a direct party to any of these procurement contracts and we do not control their terms or duration. Virginia Power advises us that current agreements, inventories, and spot market availability are expected to support North Anna’s current and planned fuel supply needs for the near term and that additional fuel is purchased as required to attempt to ensure optimal cost and inventory levels.

Under the Nuclear Waste Policy Act of 1982, the DOE is required to provide for the permanent disposal of spent nuclear fuel produced by nuclear facilities, such as North Anna, in accordance with contracts executed with the DOE. The DOE did not begin accepting spent fuel in 1998 as specified in its contract. As a result, Virginia Power sought reimbursement for certain spent nuclear fuel-related costs incurred and in 2012 signed a settlement agreement with the DOE. See Note 1 of the Notes to Consolidated Financial Statements in Item 8.

Natural Gas

Our three combustion turbine facilities and Wildcat Point are fueled by natural gas and are located adjacent to natural gas transmission pipelines. We are responsible for procuring the natural gas to be used by all of our units at these facilities and have developed and utilize a natural gas supply strategy for providing natural gas. The strategy includes securing transportation contracts and incorporating the ability to use No. 2 distillate fuel oil as a backup fuel for Louisa and Marsh Run, as needed, to minimize natural gas pipeline transportation costs. We have identified our primary natural gas suppliers and have negotiated the contracts needed for procurement of physical natural gas. We have put in place strategies and mechanisms to financially hedge our natural gas needs. We anticipate that sufficient supplies of natural gas will be available in the future to support the operation of our combustion turbine facilities and Wildcat Point, but significant price volatility may occur. See “Quantitative and Qualitative Disclosures About Market Risk” in Item 7A.

REGULATION

General

We are subject to regulation by FERC and, to a limited extent, state public service commissions. Some of our operations also are subject to regulation by the VDEQ, the Maryland Department of the Environment, the DOE, the NRC, and other federal, state, and local authorities. Compliance with future laws or regulations may increase our operating and capital costs by requiring, among other things, changes in the design or operation of our generating facilities.

Rate Regulation

We establish our rates for power furnished to our member distribution cooperatives pursuant to our formula rate, which has been accepted by FERC. The VSCC, the DPSC, and the MPSC do not have jurisdiction over our rates, charges, and services.

Our formula rate is intended to permit us to collect revenues, which, together with revenues from all other sources, are equal to all of our costs and expenses, plus a targeted amount equal to 20% of our total interest charges, plus additional equity contributions as approved by our board of directors. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Factors Affecting Results—Formula Rate” in Item 7. Our current formula rate was accepted by FERC and became effective January 1, 2014, subject to refund, pending a final order from FERC. See “FERC Proceeding Related to Formula Rate” in “Legal Proceedings” in Item 3.

FERC may review our rates upon its own initiative or upon complaint and order a reduction of any rates determined to be unjust, unreasonable, or otherwise unlawful and order a refund for amounts collected during such proceedings in excess of the just, reasonable, and lawful rates.

Our charges to TEC are established under our market-based sales tariff filed with FERC.

12

Other Regulation

In addition to its jurisdiction over rates, FERC also regulates the issuance of securities and assumption of liabilities by us, as well as mergers, consolidations, the acquisition of securities of other utilities, and the disposition of property under FERC jurisdiction. Under FERC regulations, we are prohibited from selling, leasing, or otherwise disposing of the whole of our facilities subject to FERC jurisdiction, or any part of such facilities having a value in excess of $10 million without FERC approval. We are also required to seek FERC approval prior to merging or consolidating our facilities with those of any other entity having a value in excess of $10 million.

The VSCC, the DPSC, and the MPSC oversee the siting of our utility facilities in their respective jurisdictions.

Environmental

We are subject to federal, state, and local laws and regulations, and permits designed to both protect human health and the environment and to regulate the emission, discharge, or release of pollutants into the environment. We believe that we are in material compliance with all current requirements of such environmental laws and regulations and permits. However, as with all electric utilities, the operation of our generating units could be affected by future changes in environmental laws or new environmental regulations. We continue to monitor activity related to changes in environmental laws and regulations, including new requirements. Capital expenditures and increased operating costs required to comply with any future regulations could be significant. See “Risk Factors” in Item 1A. Our capital expenditures for environmental improvements at our generating facilities were approximately $3.8 million and $6.0 million in 2017 and 2016, respectively.

Clean Air Act (“CAA”)

Currently, the most significant environmental law affecting our operations is the CAA. The CAA requires, among other things, that owners and operators of fossil fuel-fired power stations limit emissions of SO2, particulate matter, mercury, and NOx. Additionally, regulatory programs are in place for new units and are being proposed for existing units to limit emissions of CO2 and other GHG. Discussed below are certain standards and regulations under the CAA that impact us.

| • | Cross-State Air Pollution Rule |

| • | Mercury and Air Toxics Standards |

| • | National Ambient Air Quality Standards |

| • | CO2 New Source Performance Standards for EGUs |

| • | Greenhouse Gas Prevention of Significant Deterioration Permitting |

Cross-State Air Pollution Rule (“CSAPR”)

CSAPR requires 27 states and the District of Columbia to significantly improve air quality by reducing power plant SO2 and NOx emissions that contribute to ozone and fine particle pollution in other states. Phase 2 emissions budgets were applicable beginning in 2017. Based upon published allocations/new source set-aside allowances for Virginia and Maryland, we anticipate that we will have to purchase a large number of NOx and a limited number of SO2 CSAPR allowances for Clover. We anticipate that we will have to purchase the majority of emissions allowances required for Wildcat Point and will apply for new source set-aside NOX allowances from Maryland. Wildcat Point will need to purchase allowances for any emissions that exceed the number of new source set-aside allowances received. Currently, there is an adequate supply of NOx allowances available for purchase for Wildcat Point. The number of set-aside allowances available for Wildcat Point will depend on the number of new sources requesting the allowances. Because the CSAPR allowance market is relatively new, we cannot predict the potential financial impacts of such purchases.

13

Acid Rain Program

Under the CAA’s Acid Rain Program, each of our fossil fuel-fired plants must have SO2 allowances equal to the number of tons of SO2 they emit into the atmosphere annually. The total number of SO2 allowances for all facilities is capped, and individual allowances are issued to facilities on the basis of past utilization and other factors. SO2 allowances issued to individual sources can be traded. As a facility that was built before the Acid Rain Program, Clover receives an annual allocation of SO2 allowances at no cost based upon its baseline operations. Our newer facilities, Louisa, Marsh Run, Rock Springs, and Wildcat Point, need to obtain allowances under the Acid Rain Program. Because they are primarily gas-fired generating facilities, the number of SO2 allowances these newer facilities must obtain is typically minimal and can be supplied from any excess SO2 allowances allocated to Clover.

Mercury and Air Toxics Standards (“MATS”)

MATS regulates mercury, acid gases, and other air toxic organic compounds from coal and oil-fired power plants. Coal and oil-fired power plants were required to meet maximum achievable control technology standards to control the pollutants regulated by MATS by April 16, 2015. Clover has demonstrated compliance with this rule and continues to submit periodic reports. We do not anticipate that any additional emissions control measures will be required to continue to comply with MATS due to the existing pollution control equipment, which removes greater than 90% of the mercury emitted from the facility.

National Ambient Air Quality Standards (“NAAQS”)

As part of the NAAQS, states will be required to develop and implement plans to address sources emitting pollutants which contribute to the formation of ozone. In November 2016, the EPA published the proposed designations and SIP requirements for implementation. We anticipate that the EPA will finalize designations of the ozone NAAQS in the future. Compliance requirements are dependent upon the attainment designation and we currently anticipate that compliance may begin in 2020 and go through 2027. We currently do not anticipate any emissions control requirement changes for our existing facilities. The EPA is still developing the implementation guidance related to the NAAQS. We will continue to follow this rulemaking in order to determine potential impacts related to our facilities.

CO2 New Source Performance Standards for EGUs

In 2015, the EPA finalized the national standards for CO2 emissions from new fossil fuel-fired electric generating units under 111(b) of the CAA. The standards limit CO2 emissions from new fossil fuel-fired electric generating units, newly constructed and reconstructed fossil fuel-fired stationary combustion turbines, and baseload natural gas-fired units. This rule would affect permitting and operational requirements applicable to new, fossil fuel-fired facilities. We do not currently know the cost of compliance or the extent of control requirements that might be applicable to any future facilities.

CO2 Emissions Guidelines for Existing EGUs (“Clean Power Plan”)

In 2015, the EPA issued final emission guidelines for CO2 from existing electric utility generating units under 111(d) of the CAA. The final regulations, referred to as the Clean Power Plan, took effect December 23, 2015. The final rule established rate-based and mass-based goals for each state, with interim goals during years 2022 to 2029, and final goals for target year 2030. The primary legal challenge to the Clean Power Plan is pending in the D.C. Circuit. On February 9, 2016, the U.S. Supreme Court granted a stay of the implementation of the Clean Power Plan, pending resolution of the challenge pending before the D.C. Circuit, including any review of that court’s decision by the Supreme Court.

On October 16, 2017, the EPA proposed a rule to repeal the Clean Power Plan. The comment period related to this proposal extends to April 26, 2018, and a number of hearings are scheduled across the country. We are monitoring the rulemaking, and are utilizing stakeholder processes to provide comments. We currently cannot predict the impact of the Clean Power Plan on our existing facilities due to the uncertainties and complexities of the regulations and the unclear status of efforts to repeal the plan.

14

Greenhouse Gas Prevention of Significant Deterioration Permitting

In 2010, the EPA issued the Tailoring Rule to address GHG emissions from stationary sources under the CAA permitting programs. The final rule set thresholds for GHG emissions that define when permits under the New Source Review Prevention of Significant Deterioration and Title V Operating Permit programs are required for new and existing industrial facilities. In late 2010, the EPA issued a series of rules that provide the necessary regulatory framework for permitting of both new and existing large stationary sources. Regulation of GHG emissions may affect the future renewal of Title V Operating Permits for Clover, Louisa, Marsh Run, and Rock Springs, as the rules will require that existing facilities quantify their GHGs emissions and may establish limits in their reissued operating permits.

Regional Greenhouse Gas Initiative (“RGGI”)

RGGI provides for a cap-and-trade program to regulate CO2 emissions among participating northeastern and Mid-Atlantic States, including Delaware and Maryland. We are required to purchase RGGI CO2 allowances for each ton of CO2 emitted by our Rock Springs units and Wildcat Point. We anticipate that Wildcat Point will apply for and be awarded a portion of the allowances from the Maryland clean generation set-aside account through the year 2022. We continue to project that there will be an adequate quantity of CO2 allowances available for purchase to support both Rock Springs and Wildcat Point.

Virginia CO2 Regulation

The governor of the Commonwealth of Virginia issued an executive directive on May 16, 2017, directing VDEQ to develop a proposed regulation by the end of 2017 to abate, control, or limit CO2 emissions from electric power facilities. The proposed rule was presented to the Virginia Air Pollution Control Board for approval and was subsequently published in the Virginia Register of Regulations on January 8, 2018, with a 90-day public comment period. The major implementation component of the regulation is the linkage to RGGI. There is considerable uncertainty as to the impact on ODEC’s Virginia facilities given (1) the proposed consignment auction approach has never been used before under the RGGI model, (2) all other participating RGGI states have deregulated electric markets, and (3) the stringency of the Virginia budget cap in relation to the overall RGGI cap. We will be providing significant comment on this proposed rule and will be following the process closely.

Clean Water Act

The Clean Water Act and applicable state laws regulate water intake structures, discharges of cooling water, storm water runoff, and other wastewater discharges at our generating facilities. Our permits are subject to periodic review and renewal proceedings, and can be made more restrictive over time. Limitations on the thermal discharges in cooling water, or withdrawal of cooling water during low flow conditions, can restrict our operations. In 2013, the EPA proposed revising limits on certain toxic pollutants that would require most steam electric (including coal and combined cycle, natural gas) facilities to strengthen existing, or implement new, controls to manage water discharges from their sites. The final rule was published in the Federal Register on November 3, 2015, with an implementation date of January 4, 2016. The final rule, known as the Steam Electric Effluent Limitation Guidelines revised the guidelines to set the first limits on the levels of toxic metals in wastewater that can be discharged from power plants. The final rule sets new or additional requirements for wastewater streams from flue gas desulfurization, fly ash, bottom ash, flue gas mercury control, and gasification of fuels such as coal and petroleum coke.

On December 5, 2016, several industry parties represented by the Utility Water Act Group filed opening briefs against the final rule. The briefs alleged several instances where it is believed that the EPA violated standards and procedures in producing the guidelines. On September 13, 2017, a final rule was issued postponing compliance dates for “best available technology economically achievable” effluent limitations and pretreatment standards for two waste streams of existing sources, bottom ash transport water and flue-gas desulfurization wastewater, for a period of two years. In the interim EPA is working to revise the 2015 ruling after further input from stakeholders.

We do not currently expect there to be a significant impact on facility operations. We are currently in compliance and will continue to follow this rulemaking in order to determine potential future impacts related to our facilities.

15

Resource Conservation and Recovery Act, as amended (“RCRA”)

The EPA regulates CCRs under the RCRA to address the risks from disposal of CCRs generated by coal combustion at electric generating facilities. In 2014, the EPA proposed regulations governing the “Disposal of Coal Combustion Residuals for Electric Utilities,” which addressed risks related to coal ash disposal, such as leaking of contaminants into groundwater, blowing of contaminants into the air as dust, and the catastrophic failure of coal ash surface impoundments. The final rule was published in 2015, and established technical requirements for CCR landfills and surface impoundments, and for monitoring and cleanup of affected soil or groundwater. Virginia Power, as operator of Clover, is currently making modifications to Clover to comply with RCRA. Also, under the final rule, facilities are subject to recordkeeping requirements, requirements to notify the state, and a requirement to develop and maintain a publicly available internet site containing information on its actions to comply with the elements of the final rule.

On September 14, 2017, the EPA announced that it had granted two petitions to reconsider substantive provisions of the final rule. The EPA has yet to announce any rulings related to its reconsideration of the final rule. We continue to monitor these regulations and the potential impact on the operations at Clover.

Future Regulation

New legislative and regulatory proposals are frequently introduced on both the federal level and state level that would modify the environmental regulatory programs applicable to our facilities. Changing regulatory requirements can increase our capital and operating costs and adversely affect the ability to operate our existing facilities, as well as restrict construction of new facilities.

ITEM 1A. – RISK FACTORS

RISK FACTORS

The following risk factors and all other information contained in this report should be considered carefully when evaluating ODEC. These risk factors could affect our actual results and cause these results to differ materially from those expressed in any forward-looking statements of ODEC. Other risks and uncertainties, in addition to those that are described below, may also impair our business operations. We consider the risks listed below to be material, but you may view risks differently than we do and we may omit a risk that we consider immaterial but you consider important. An adverse outcome of any of the following risks could materially affect our business or financial condition. These risk factors should be read in conjunction with the other detailed information set forth elsewhere in this report, including “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in Item 7, including “Caution Regarding Forward-looking Statements,” and the notes to Consolidated Financial Statements.

Changes in fuel and purchased power costs could increase our operating costs.

We are subject to changes in fuel costs, which could increase the cost of generating power and purchased power costs. Increases in fuel costs and purchased power costs increase the cost to our member distribution cooperatives. The market prices for fuel may fluctuate over relatively short periods of time. Factors that could influence fuel and purchased power costs are:

| • | the availability of competitively priced alternative energy sources; |

| • | constraints related to the transportation of fuels; |

| • | price competition among fuels used to produce electricity, including natural gas, coal, and oil; |

| • | energy transmission capacity constraints; |

| • | the impact of implementation of new technologies in the power industry, such as batteries; |

16

| • | federal, state, and local energy and environmental regulation and legislation, including increased regulation of the extraction of natural gas and coal; and |

| • | natural disasters, war, terrorism, and other catastrophic events. |

We rely substantially on purchases of energy from other power suppliers which exposes us to market price risk.

We supply our member distribution cooperatives with all of their power (energy and demand) requirements, with limited exceptions. Our costs to provide this energy and demand are passed through to our member distribution cooperatives under our wholesale power contracts. We obtain the power to serve their requirements from generating facilities in which we have an interest and purchases of power from other power suppliers.

Historically, our power supply strategy has relied substantially on purchases of energy from other power suppliers. In 2017, we purchased approximately 63.3% of our energy resources. These purchases consisted of a combination of purchases under physically-delivered forward contracts and purchases of energy in the spot market. Our reliance on purchases of energy from other suppliers will continue into the future. Our reliance on energy purchases could also increase because the operation of our generating facilities is subject to many risks, including changes in their dispatch, shutdown, or breakdown or failure of equipment.

Purchasing power helps us mitigate high fixed costs related to the ownership of generating facilities but exposes us to significant market price risk because energy prices can fluctuate substantially. When we enter into long-term power purchase contracts or agree to purchase energy at a date in the future, we utilize our judgment and assumptions in our models. These judgments and assumptions relate to factors such as future demand for power and market prices of energy and the price of commodities, such as natural gas, used to generate electricity. Our models cannot predict what will actually occur and our results may vary from what our models predict, which may in turn impact our resulting costs to our members. Our models become less reliable the further into the future that the estimates are made. Although we have developed strategies to attempt to meet our power requirements in an economical manner and we have implemented a hedging strategy to limit our exposure to variability in the market, we still may purchase energy at a price which is higher than other utilities’ costs of generating energy or future market prices of energy. For further discussion of our market price risk, see “Quantitative and Qualitative Disclosures About Market Risk” in Item 7A.

Environmental regulation may limit our operations or increase our costs or both.

We are required to comply with numerous federal, state, and local laws and regulations, relating to the protection of the environment. We believe that we have obtained all material environmental approvals currently required to own and operate our existing facilities or that necessary approvals have been applied for and will be issued in a timely manner. We may incur significant additional costs because of compliance with these requirements. Failure to comply with environmental laws and regulations could have a material effect on us, including potential civil or criminal liability and the imposition of fines or expenditures of funds to bring our facilities into compliance. Delay in obtaining, or failure to obtain and maintain in effect, any environmental approvals, or the delay or failure to satisfy any applicable environmental regulatory requirements related to the operation of our existing facilities or the sale of energy from these facilities could result in significant additional cost to us.

The Clean Power Plan, which took effect December 23, 2015, was stayed on February 9, 2016, by the courts and on October 16, 2017, the EPA proposed a rule to repeal the Clean Power Plan. If implemented, the Clean Power Plan requires that each state implement plans to meet state-specific carbon emissions reductions. We have ownership interests in generating facilities in Virginia and Maryland and are exposed to the impact of inconsistent standards between states as well as the uncertainty of the implementation plans. We are closely monitoring the rulemaking related to the Clean Power Plan. We currently cannot predict the impact of the Clean Power Plan on our existing facilities due to the uncertainties and complexities of the regulations and the unclear status of efforts to repeal the plan.

17

The governor of the Commonwealth of Virginia issued an executive directive on May 16, 2017, directing VDEQ to develop a proposed regulation by the end of 2017 to abate, control, or limit CO2 emissions from electric power facilities. The proposed rule was presented to the Virginia Air Pollution Control Board for approval and was subsequently published in the Virginia Register of Regulations on January 8, 2018, with a 90-day public comment period. The major implementation component of the regulation is the linkage to RGGI. We have ownership interests in generating facilities in Virginia and could be potentially exposed to higher costs to dispatch these facilities under the proposed rule.

We cannot predict the cost or the effect of any future environmental legislation or regulation. New environmental laws or regulations, the revision or reinterpretation of existing environmental laws or regulations, or penalties imposed for non-compliance with existing environmental laws or regulations may require us to incur additional expenses and could have a material adverse effect on the cost of power we supply our member distribution cooperatives. See “Regulation—Environmental” in Item 1.

Our financial condition is largely dependent upon our member distribution cooperatives.

Our financial condition is largely dependent upon our member distribution cooperatives satisfying their obligations to us under the wholesale power contract that each has executed with us. The wholesale power contracts require our member distribution cooperatives to pay us for power furnished to them in accordance with our FERC formula rate. Our board of directors, which is composed of representatives of our members, can approve changes in the rates we charge to our member distribution cooperatives without seeking FERC approval, with limited exceptions. In 2017, 63.1% of our revenues from sales to our member distribution cooperatives were received from our three largest members, REC, SVEC, and DEC.

Our member distribution cooperatives’ ability to collect their costs from their members may have an impact on our financial condition. Economic conditions may make it difficult for some customers of our member distribution cooperatives to pay their power bills in a timely manner, which could ultimately affect the timeliness of our member distribution cooperatives’ payments to us.

Technological advancements and other changes impacting power requirements of our member distribution cooperatives’ customers may reduce demand for power from us.

Technological advancements are occurring in the electric industry, including advancements related to self-generation and distributed energy technologies. Distributed energy technologies include fuel cells, batteries, micro turbines, wind turbines and solar cells. The increased adoption of these technologies and a greater degree of the adoption of energy efficiency technology and conservation by our member distribution cooperatives’ customers, along with the impact of regional economic conditions, could reduce our member distribution cooperatives’ demand for power from us and cause our long-term load expectations to be materially different than planned.

We are subject to risks associated with owning an interest in a nuclear generating facility.

We have an 11.6% undivided ownership interest in North Anna, which provided approximately 15.7% of our energy requirements in 2017. Ownership of an interest in a nuclear generating facility involves risks, including:

| • | potential liabilities relating to harmful effects on the environment and human health resulting from the operation of the facility and the storage, handling, and disposal of radioactive materials; |

| • | significant capital expenditures relating to maintenance, operation, and repair of the facility, including repairs required by the NRC; |

| • | limitations on the amounts and types of insurance commercially available to cover losses that might arise in connection with operation of the facility; and |

| • | uncertainties regarding the technological and financial aspects of decommissioning a nuclear plant at the end of its licensed life. |

The NRC has broad authority under federal law to impose licensing and safety-related requirements for the operation of North Anna. If the facility is not in compliance, the NRC may impose fines or shut down the units until compliance is achieved, or both depending upon its assessment of the situation. Revised safety requirements issued by the

18

NRC have, in the past, necessitated substantial capital expenditures at other nuclear generating facilities. North Anna’s operating and safety procedures may be subject to additional federal or state regulatory scrutiny as a result of worldwide events related to nuclear facilities. In addition, if a serious nuclear incident at North Anna did occur, it could have a material but presently indeterminable adverse effect on our operations or financial condition. Further, any unexpected shut down at North Anna as a result of regulatory non-compliance or unexpected maintenance will require us to purchase replacement energy.

We may not complete generating facility construction projects that we commence, or we may complete such projects on materially different terms or timing than initially anticipated and we may not be able to achieve the intended benefits of any such projects, if completed.

Construction projects, such as investments in generation assets, carry with them the risk that decisions made today can have implications well into the future. Failure to anticipate market, technology, and regulatory risks regarding particular capital assets can impact their cost to operate and value in the future. We anticipate that we will need to seek additional financing in the future to fund these construction and expansion projects and we may not be able to secure such financing on favorable terms. Construction carries with it risks relating to timely completion and operational effectiveness. We may not be able to complete the construction or expansion projects on time or at all as a result of weather conditions, delays in obtaining or failure to obtain regulatory approvals, delays in obtaining key materials, labor difficulties, other construction delays, difficulties with partners, contractors, or suppliers, or other factors beyond our control. Even if the construction and expansion projects are completed, the total costs of the construction and expansion projects may be higher than anticipated and the performance of our business following the construction and expansion projects may not meet expectations. Further, we may not be able to timely and effectively integrate the construction and expansion projects into our operations, or the integration may result in unforeseen operating difficulties or unanticipated costs. Any of these or other factors could adversely affect our ability to realize the anticipated benefits from construction and expansion projects.

We may have operational deficiencies or catastrophic events related to our generating facilities.

The operation of our generation or transmission facilities involves risks, including the breakdown or failure of power generation equipment, transmission lines, pipes or other equipment or processes, fuel supply delivery, and performance below expected levels of output or efficiency. The occurrence of any of these events could result in:

| • | substantial charges assessed by PJM as a result of the expectation that generation facilities would be available if called upon to be dispatched; |

| • | significant additional capital expenditures to repair or replace the affected facilities; or |

| • | the purchase of potentially more costly replacement power on the open market. |

Counterparties under power purchase and natural gas arrangements may fail to perform their obligations to us.

Because we rely substantially on the purchase of energy and natural gas from other suppliers, we are exposed to the risk that counterparties will default in performance of their obligations to us. On an on-going basis we analyze and monitor the default risks of counterparties and other credit issues related to these purchases, and we may require our counterparties to post collateral with us; however, defaults may still occur. Defaults may take the form of failure to physically deliver the purchased energy or natural gas. If a default occurs, we may be forced to enter into alternative contractual arrangements or purchase energy or natural gas in the forward or spot markets at then-current market prices that may exceed the prices previously agreed upon with the defaulting counterparty.

The use of hedging instruments could impact our liquidity.

We use various hedging instruments, including forwards, futures, financial transmission rights, and options, to manage our power market price risks. These hedging instruments generally include collateral requirements that require us to deposit funds or post letters of credit with counterparties when a counterparty’s credit exposure to us is in excess of agreed upon credit limits. When commodity prices decrease to levels below the levels where we have hedged future costs, we may be required to use a material portion of our cash or liquidity facilities to cover these collateral requirements.

19

Additionally, existing or new regulations related to the use of hedging instruments may impact our access to and use of hedging instruments.

Adverse changes in our credit ratings may require us to provide credit support for some of our obligations and could negatively impact our liquidity and our ability to access capital.

S&P, Moody’s, and Fitch currently rate our outstanding obligations issued under our Indenture at “A+,” “A2,” and “A,” respectively. Additionally, we have an issuer credit rating of “A+” from S&P, and an implied senior unsecured rating of “A” from Fitch. If these agencies were to downgrade our ratings, particularly below investment grade, we may be required to deposit funds or post letters of credit related to our power purchase arrangements, which may reduce our available liquidity and impact our access to future liquidity resources. To the extent that we would have to provide additional credit support as a result of a downgrade in our credit ratings, our ability to access additional credit may be limited and our liquidity may be materially impaired. Also, we may be required to pay higher interest rates on our revolving credit facility and financings that we may need to undertake in the future, and our potential pool of investors and funding sources could decrease.

War, acts and threats of terrorism, sabotage, cyber security breach, natural disaster, and other significant events could adversely affect our operations.

We cannot predict the impact that any future terrorist attack, sabotage, cyber security breach, or natural disaster may have on the energy industry in general, or on our business in particular. Infrastructure facilities, such as electric generation, transmission, and distribution facilities, and RTOs, could be direct targets of, or indirect casualties of, an act of terror, sabotage, or cyber security breach. The physical or cyber security compromise of our facilities could adversely affect our ability to operate or manage our facilities effectively. Additionally, any military strikes or sustained military campaign may affect the operation of our facilities in unpredictable ways, such as changes in financial markets, and disruptions of fuel supplies and energy markets. We also use third-party vendors to electronically process certain of our business transactions. Information systems, both ours and those of third-party information processors, are vulnerable to cyber security breach. Cyber security incidents could impact the ability to operate our generation and transmission assets, delay the development and construction of new facilities or capital improvement projects to existing facilities, and result in unauthorized disclosure of personal information regarding employees and their dependents, contractors, and other individuals. Instability in financial markets as a result of terrorism, war, sabotage, cyber security breach, natural disasters, pandemic, credit crises, recession, or other factors could have a significant negative effect on the U.S. economy, and in the increased cost of financing and insurance coverage, which could negatively impact our results of operations and financial condition.

Failure to comply with regulatory reliability standards, and other regulatory requirements could subject us to substantial monetary penalties.

As a result of EPACT, owners, operators, and users of bulk electric systems, including ODEC, are subject to mandatory reliability standards enacted by NERC and its regional entities, and enforced by FERC. We must follow these standards, which are in place to require that proper functions are performed to ensure the reliability of the bulk power system. Although the standards are developed by the NERC Standards Committee, which includes representatives of various electric energy sectors, and must be just and reasonable, the standards are legally binding and compliance may require increased capital expenditures and costs to provide electricity to our member distribution cooperatives under our wholesale power contracts. If we are found to be in non-compliance with any mandatory reliability standards we could be subject to sanctions, including potentially substantial monetary penalties. New, revised or reinterpreted laws or regulations related to reliability standards and/or participation in wholesale power markets could also result in substantial monetary penalties if ODEC is found to have violated or failed to comply with applicable standards, laws and regulations.

Poor market performance will affect the asset values in our nuclear decommissioning trust and our defined benefit retirement plans, which may increase our costs.

We are required to maintain a funded trust to satisfy our future obligation to decommission North Anna. A decline in the market value of those assets due to poor investment performance or other factors may increase our funding requirements for these obligations which may increase our costs.

20