Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

SCHEDULE 14A

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

(Amendment No. )

| Filed by the Registrant ☒ | Filed by a Party other than the Registrant ☐ |

Check the appropriate box:

☐ | Preliminary Proxy Statement. | |

☐ | Confidential, for use of the Commission Only (as permitted by Rule 14a-6(e)(2)). | |

☒ | Definitive Proxy Statement. | |

☐ | Definitive Additional Materials. | |

☐ | Soliciting Material Pursuant to §240.14a-12. | |

Avon Products, Inc.

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement, if Other Than the Registrant)

Payment of Filing Fee (Check the appropriate box):

☒ | No fee required. | |

☐ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | |

(1) | Title of each class of securities to which transaction applies:

| |

(2) | Aggregate number of securities to which transaction applies:

| |

(3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined):

| |

(4) | Proposed maximum aggregate value of transaction:

| |

(5) | Total fee paid:

| |

☐ | Fee paid previously with preliminary materials. | |

☐ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the form or schedule and the date of its filing. | |

(1) | Amount Previously Paid:

| |

(2) | Form, Schedule or Registration Statement No.:

| |

(3) | Filing Party:

| |

(4) | Date Filed:

| |

Table of Contents

Table of Contents

April 4, 2018

Dear Shareholders:

It is my pleasure to invite you to join me, the Board of Directors, senior leaders, and current and former employees at the 2018 Annual Meeting of Shareholders in White Plains, New York. Details regarding admission to the meeting and the business to be conducted are more fully described in the accompanying Notice of Annual Meeting of Shareholders and Proxy Statement.

We hope that you will join us in person, but whether or not you plan to attend the Annual Meeting, your vote is important. I encourage you to vote by telephone, by internet or by signing, dating, and returning your proxy card by mail. Voting instructions are found on page 5 of the Proxy Statement.

On behalf of the Board of Directors and Avon management, thank you for your investment and interest in Avon.

| Sincerely yours, | ||

| ||

| Jan Zijderveld | ||

| Chief Executive Officer | ||

Table of Contents

AVON PRODUCTS, INC.

Building 6, Chiswick Park

London W4 5HR

United Kingdom

YOUR VOTE IS IMPORTANT – YOU CAN VOTE IN ONE OF FOUR WAYS:

|  |  |  | |||

VIA THE INTERNET Visit the website listed on your proxy card |

BY TELEPHONE Call the telephone number on your proxy card |

BY MAIL Sign, date and return your proxy card in the enclosed envelope |

IN PERSON Attend the Annual Meeting | |||

If your shares are held in a stock brokerage account or by a bank or other record holder, follow the voting instructions on the form that you receive from them. The availability of telephone and internet voting will depend on their voting process. | ||||||

Meeting Agenda

1 Elect as directors the eight nominees named in the Proxy Statement;

|

2 Hold anon-binding, advisory vote to approve compensation of our named executive officers;

|

3 Ratify the appointment of PricewaterhouseCoopers LLP, United Kingdom, as our independent registered public accounting firm for 2018; and

|

4 Transact such other business as may properly come before the meeting.

|

NOTICE OF ANNUAL MEETING OF SHAREHOLDERS

Wednesday, May 16, 2018

9:00 a.m.

The Ritz-Carlton

New York, Westchester

3 Renaissance Square

White Plains, NY 10601

Salon III | How to Attend the Meeting

| |||||

If you plan to attend the meeting in person, please see page 5 for admission requirement.

| ||||||

The record date for the meeting is March 27, 2018. This means that you are entitled to receive notice of meeting and vote your shares at the meeting if you were a shareholder of record as of the close of business on March 27, 2018.

| ||||||

| By order of the Board of Directors, | ||||||

| ||||||

Ginny Edwards Vice President & Corporate Secretary

| ||||||

April 4, 2018

| ||||||

Important notice regarding the availability of proxy materials for the shareholder meeting to be held on May 16, 2018:

Our Proxy Statement and Annual Report to Shareholders are available atwww.edocumentview.com/avp

|

Table of Contents

| 1 | |||||

| 5 | |||||

| 9 | |||||

| INFORMATION CONCERNING THE BOARD OF DIRECTORS | 15 | ||||

| 15 | |||||

| 15 | |||||

| 15 | |||||

| 16 | |||||

| 17 | |||||

| 18 | |||||

| 18 | |||||

| Director Nomination Process & Shareholder Nominations | 18 | ||||

| 19 | |||||

| 19 | |||||

| Compensation and Management Development Committee Interlocks and Insider Participation | 19 | ||||

| 20 | |||||

| 22 | |||||

| 24 | |||||

| 28 | |||||

Table of Contents

This summary highlights information contained elsewhere in the Proxy Statement and in Avon Products, Inc.’s (“Avon,” the “Company,” “we,” “us,” or “our”) Annual Report on Form10-K for the year ended December 31, 2017. This summary is not a complete description and you should read the entire Proxy Statement carefully before voting. Proxy materials were first sent to shareholders on or about April 4, 2018.

Meeting Agenda

Matter

|

Board Vote Recommendation

|

Page Reference (for more detail)

| ||||

| PROPOSAL 1 | Election of the eight Director Nominees named in this Proxy Statement

| FOR EACH NOMINEE

| 9

| |||

| PROPOSAL 2 | AnnualNon-Binding, Advisory Vote to Approve Compensation of our Named Executive Officers

| FOR | 73 | |||

| PROPOSAL 3 | Ratification of PricewaterhouseCoopers LLP, United Kingdom, as Independent Registered Public Accounting Firm for 2018 | FOR | 77 | |||

Board and Governance Highlights

The Company has adopted many leading governance practices that establish strong independent leadership in our boardroom and provide our shareholders with meaningful rights. Highlights include:

• Since 2016, over 60% Board member refreshment including new Chief Executive Officer in 2018

• Annual election of directors

• Non-executive Chairman of the Board and Lead Independent Director

• All directors are independent other than CEO

• Proxy Access

• Majority vote standard with resignation policy for election of directors in uncontested elections

• Directors may serve on limited number of other public boards

• Regular Executive Sessions of independent directors

• Annual board and committee evaluations

• No supermajority voting with respect to common stock, except as provided under New York Business Corporation law

• Compensation: Several compensation best practices, including double-triggerchange-in-control benefits, no excise tax reimbursements forchange-in-control payments, prohibition against hedging common stock, claw-back policy, stock ownership guidelines and certain holding period requirements |

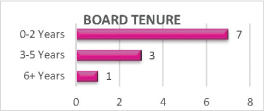

TENURE AVERAGE: 3 Years AVERAGE AGE: 60

The above charts reflect information regarding Andrew G. McMaster, Jr. and James A. Mitarotonda, who have been nominated to our Board but are not currently directors of the Company. For more details regarding them, please see page 9.

|

BOARD INDEPENDENCE Independent 10Non-Independent 1 BOARD GENDER Women 3 27% Men 8 73% BOARD RACE, ETHNICITY & GEOGRAPHIC DIVERSITY Diverse 3 27% Other 8 73% BOARD TENURE 0-2 Years 3-5 Years 6+ Years

| AVON 2018 Proxy Statement | 1 |

Table of Contents

Board Nominees and Designees

The following table provides summary information about each director nominated for election by our Board of Directors (the “Board”) to the Board at the 2018 Annual Meeting (collectively, the “Director Nominees”) and each director elected to the Board by holders of our Series C Preferred Stock (collectively, the “Series C Designees”). Director Nominees are elected annually by a majority of the votes cast by our shareholders, voting together as a single class. The Series C Designees have been elected by the holders of our Series C Preferred Stock, voting separately as a class.

Nominees and Designees

| Committee Membership

| |||||||||||||

| Names | Director Since | Independent1 | Other Public Boards | Audit Committee | Compensation and Management Development Committee

| Finance Committee | Nominating and Corporate Governance Committee

| |||||||

Jose Armario

|

2016

|

I

|

1

|

|

| |||||||||

W. Don Cornwell2

|

2002

|

I

|

2

|

|

|

| ||||||||

Chan W. Galbato3,4

|

2016

|

I

|

1

|

|

| |||||||||

Nancy Killefer

|

2013

|

I

|

2

|

|

| |||||||||

Susan J. Kropf

|

2015

|

I

|

3

|

| ||||||||||

Helen McCluskey

|

2014

|

I

|

2

|

| ||||||||||

Andrew G. McMaster, Jr. 5

|

-----

|

I

|

0

| |||||||||||

James A. Mitarotonda5

|

-----

|

I

|

3

| |||||||||||

Michael F. Sanford4

|

2016

|

I

|

0

|

| ||||||||||

Lenard B. Tessler4

|

2018

|

I

|

1

| |||||||||||

Jan Zijderveld6 |

2018 |

0 | ||||||||||||

1 Independent in accordance with NYSE listing standards, SEC regulations, and our Corporate Governance Guidelines

2 Lead Independent Director

3 Non-executive Chairman of the Board

4 Series C Designee

5 Not currently a director of the Company

6 CEO |

| |

- Member

- Member*Charles H. Noski advised the Company on March 24, 2018 that he had chosen not to stand for re-election at the 2018 Annual Meeting. The Company had previously been advised by Cathy D. Ross that she preferred not to stand for election as well.

Attendance

Each Director Nominee and each Series C Designee other than Messrs. McMaster and Mitarotonda are current directors of the Company and each Director Nominee and Series C Designee that served on the Board in 2017 attended at least 75% of the aggregate number of 2017 meetings of the Board and each Board Committee on which he or she served.

| 2 | AVON 2018 Proxy Statement |

Table of Contents

Business and Strategy Highlights

At its core, Avon is an organization with a clear and compelling purpose with a rich130-year history, operating in the beauty and personal care categories across the globe skewed toward developing and growing markets. Through our 6 million direct selling Representatives, we empower millions of micro-entrepreneurs globally. Avon’s opportunity to modernize and enable them to be more competitive and to service their consumers better is powerful, and is at the heart of Avon’s value proposition.

During 2017, Avon continued to face ongoing revenue growth challenges while continuing to make progress against key initiatives such as cost savings and cash generation. Our focus on profitability and exceeding our cost savings target contributed to improved operating margin as we ended the year. For 2017 cash flow from operations increased $143 million compared with the prior year, primarily due to improvements in working capital.

Avon ended the year with $882 million of cash, ahead of our 2017 expectations. This represents substantial improvement in our cash conversion metric during 2017, and we expect this rate of conversion to continue. We have further supported our financial flexibility by renegotiating the covenant levels in our $400 million secured credit facility. In addition, in 2018, we expect to repay the $238 million remaining due on our 2019 bonds and retain the financial flexibility to fund investments.

Total revenue was disappointing in 2017, relatively unchanged but down 2% in constant dollars as compared to the prior year, driven by declines in Brazil, Russia and the UK. Overall Avon did not keep pace with industry growth in the global beauty category which grew by roughly3-4% in 2017. The number of active Representatives declined more than anticipated, largely due to a decrease in Brazil as we tightened credit policies. The competitive environment continues to intensify in many of our key markets. The revenue shortfall highlights the need and urgency to sharpen our focus on sales forecasting, data and analytics, and to deepen Avon’s insights from our Representatives to inform pricing as well as promotional and discount strategies locally.

Throughout the year the Board of Directors (the “Board”) has focused on strengthening Avon’s leadership team, recruiting seasoned and skilled senior executives. The process of putting in place the leadership team to accelerate change and grow profits sustainably culminated with the recruitment of a new Chief Executive Officer (“CEO”), Jan Zijderveld, who joined Avon in February 2018. Mr. Zijderveld was selected following an extensive search and assessment of a strong list of seasoned global executives. Mr. Zijderveld emerged as the clear choice that Avon needs to accelerate our transformation and growth. In addition, Mr. Zijderveld’s focus on strategic and operational excellence, while putting our direct selling Representatives and consumers front and center, make him ideally suited to lead Avon. Before joining Avon, Mr. Zijderveld was a senior executive and30-year veteran of Unilever N.V./PLC with a track record as a proven global leader driving profitable growth in large, multi-channel, complex consumer businesses across emerging, developing and developed markets.

Avon is operating in a dramatically changing consumer and competitive environment. Business as usual is not an option. The Board has given Mr. Zijderveld a clear mandate to lead a deep and comprehensive strategic and operating review of all facets of the business and evaluate ways to significantly accelerate Avon’s path to profitable growth, taking a critical look with a high sense of urgency.

Shareholder Engagement & 2017 Compensation Highlights

We remain focused on shareholder engagement and value shareholder insights. During recent years, the Chair of the Compensation and Management Development Committee (the “Committee”) conducted significant shareholder outreach to ensure shareholder perspectives and concerns were heard and well understood. During this time, we reviewed our compensation program changes, and discussed the Company’s transformation status and financial and strategic priorities. These discussions culminated in the changes we have made to our compensation programs since 2016.

During 2017, we continued our practice of deeply engaging with our shareholders and soliciting feedback. We reached out to our top 25 shareholders who collectively own over 65% of our common shares outstanding as of December 31, 2017. Of the top 25 shareholders, 36% are passive investors and therefore do not generally engage and 64% are actively managed. We directly interacted with over 65% of the active top 25 shareholders of our stock.

The feedback received from our shareholders continues to be tremendously valuable and was incorporated into the Committee’s determination of compensation program changes in recent years. In 2018, we will continue to ensure the alignment of our compensation programs with our shareholders’ interests with a strong pay for performance alignment and payouts of incentive plans based on business performance and stock price appreciation.

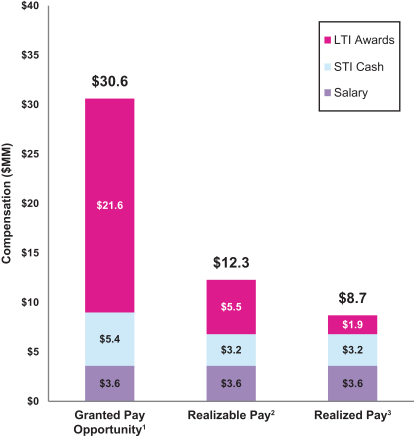

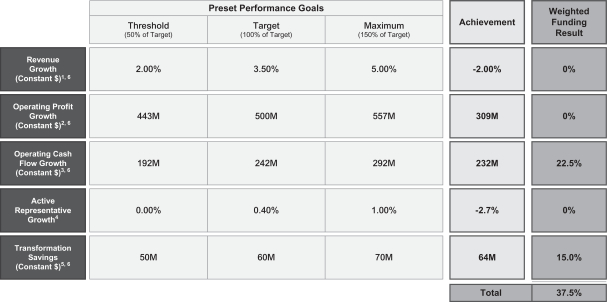

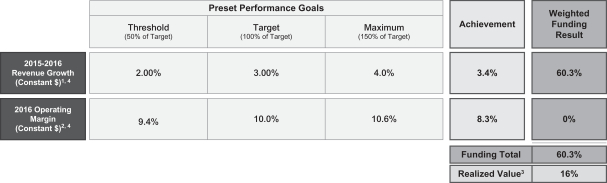

As a result of disappointing operating results, the 2017 annual incentive plan paid out at 37.5% of target, and the 2015-2017 Performance RSUs delivered a realized value of approximately only 16% of the targeted award value. The low performance results and loss of value for shareholders is reflected in very low annual and long-term incentive payouts and thus low realized pay for our executives and managers. In addition, the Committee continued to demonstrate a commitment to dynamic, shareholder-aligned pay plans through:

| • | Providing no increase in CEO 2017 target compensation opportunity over 2016 targeted pay. |

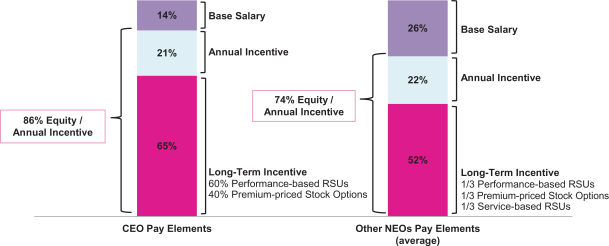

| • | Designing an executive compensation structure that remains strongly focused on performance-based compensation. For 2017, each executive had most of their compensation (70%+) at risk, which strongly aligns their interests to those of our shareholders. |

| AVON 2018 Proxy Statement | 3 |

Table of Contents

| • | Ensuring our 2017 executive annual incentive program continued to be 100% tied to objective measures of financial and operational success (including revenue growth, operating profit, operating cash flow, active Representative growth and transformation savings) and setting challenging goals for these measures to ensure alignment with shareholders in light of the headwinds facing our company. |

Our Say on Pay Proposal is found on page 73 and our Board recommends that our shareholders vote “For” this proposal. The following factors support this recommendation:

| • | Our programs are designed to support anddrive short- and long-term, externally communicated business objectives. Further, an analysis of our programs demonstrates astrong and direct link between realizable pay and performance (see page 43). |

| • | Ourprogram design incorporates shareholder feedback received during outreach campaigns. |

| • | Our long-term incentive plan design isaligned with shareholder value, requiring significant stock price appreciation before target awards are realized. As a result, we have delivered long-term incentive compensation for our named executive officers well below target. |

| • | We have also maintained a focus onlimiting shareholder dilution. |

| • | We benchmark our executives’ pay against apeer group that better reflects Avon’s business following the separation of our North America business. |

2018 Compensation Highlights

For 2018, the Committee has maintained its commitment to the strong alignment of our executive pay programs with our shareholders’ interests, while ensuring we can attract and retain key talent in the organization. As such, the Committee believes the 2017 design remains appropriate as it has strong performance elements that support our externally communicated business goals and requires significant stock price appreciation for executives to realize target compensation. As a result, the details of our compensation programs for 2018 are not significantly different from 2017, as shown on page 38. The Committee has also redefined the peer group for 2018 against which we benchmark executive pay to reflect our current lower revenues and geographic footprint (see page 46).

In addition, in recruiting a new CEO in 2018, we are providing him with a compensation opportunity in line with our newly developed peer group. His total target compensation is below our former CEO’s 2017 compensation target consistent with our reduced scale, and he has the opportunity for a significant upside wealth creation tied to company and share price performance. (see page 44)

Governance and Related Materials

The Company has established strong policies, practices and procedures which provide a framework for effective governance. Our Corporate Governance Guidelines describe our Board of Directors’ governance policies and practices, including standards for director independence, qualifications for Board and Board Committee membership, Board and Board Committee responsibilities, and Board and CEO evaluations. Highlighted below are some of our key governance and related materials:

| • | Corporate Governance Guidelines |

| • | Charters of Each Board Committee |

| • | Code of Conduct |

| • | Corporate Responsibility Report |

The Corporate Governance Guidelines, charters of each Board Committee, and Corporate Responsibility Report are available on our investor website (www.avoninvestor.com) and may be accessed by clicking on “Corporate Governance” or, in the case of our Corporate Responsibility Report, by clicking on “Corporate Responsibility.” The Code of Conduct is available atwww.avoncompany.com and may be accessed by clicking on “Ethics & Compliance” under the “About Avon” heading.

| 4 | AVON 2018 Proxy Statement |

Table of Contents

VOTING AND MEETING INFORMATION

Purpose of Materials

| ||

We are providing these proxy materials in connection with the solicitation by the Board of Directors of Avon Products, Inc. (“Avon,” the “Company,” “we,” “us,” or “our”) of proxies to be voted at our Annual Meeting of Shareholders, which will take place on Wednesday, May 16, 2018. | ||

This Proxy Statement describes the matters to be voted on at the Annual Meeting and contains other required information. | ||

Distribution of Proxy Materials

| ||

We are providing access to our proxy materials over the internet. Accordingly, on or about April 4, 2018, we mailed our shareholders a Notice of Internet Availability of Proxy Materials (“proxy notice”), which contains instructions on how to access our proxy materials over the internet and vote online. If you received a proxy notice, you will not receive a printed copy of our proxy materials by mail unless you request one by following the instructions provided on the proxy notice. We mailed the proxy materials to participants in our Avon Personal Savings Account Plan. | ||

Shareholders Entitled to Vote

| ||

Shareholders of our common stock and of our Series C Preferred Stock as of the close of business on March 27, 2018, the record date, are entitled to vote. There were approximately 440,947,715 shares of our common stock outstanding on March 27, 2018 for an aggregate vote of approximately 440,947,715 (or one vote per share) and 435,000 shares of our Series C Preferred Stock outstanding on March 27, 2018 for an aggregate vote of 87,051,524 (on anas-converted basis). Shareholders of our common stock and of our Series C Preferred Stock will vote together as a single class on all matters being presented in this Proxy Statement, for up to an aggregate 527,999,239 votes. We refer to the holders of shares of our common stock and of shares of our Series C Preferred Stock (which are convertible into shares of our common stock) as “shareholders” throughout this Proxy Statement. | ||

How to Vote

| ||

Shareholders can vote in one of several ways: | ||

• Via the Internet—Visit the website on the proxy notice or proxy card | ||

• By Telephone—Call the telephone number on the proxy card | ||

• By Mail—Sign, date and return your proxy card in the enclosed envelope | ||

• In Person—Attend the Annual Meeting (follow instructions below) | ||

If your shares are held in a stock brokerage account or by a bank or other record holder, follow the voting instructions on the form that you receive from them. The availability of telephone and internet voting will depend on their voting process. If you do not give instructions to the broker, bank or other record holder holding your shares, it will not be authorized to vote with respect to Proposals 1 or 2. We therefore urge you to provide instructions so that your shares may be voted. | ||

Attending the Annual Meeting

| ||

Shareholders who would like to attend the Annual Meeting in person are asked to follow the guidelines below. Anyone who arrives without an admission ticket orpre-registration will not be admitted to the Annual Meeting unless it can be verified that the individual was a shareholder as of March 27, 2018. | ||

| AVON 2018 Proxy Statement | 5 |

Table of Contents

| Shareholders of Record (shares are registered directly in your name with our transfer agent, Computershare Trust Company, N.A.) | ||

• Please bring the admission ticket that is attached to your proxy notice and/or proxy card and photo identification. If you vote in advance of the Annual Meeting, please keep a copy of your admission ticket and bring it with you. | ||

• If you do not have your admission ticket at the Annual Meeting, you must bring other proof of your Avon share ownership as of March 27, 2018 and photo identification. | ||

| Beneficial Owners (shares are held in a stock brokerage account, in the Avon Personal Savings Account, or by a bank or other record holder) | ||

• We recommend that youpre-register to attend the meeting by sending a written request, along with proof of ownership (such as a current brokerage statement), to our Investor Relations Department, Avon Products, Inc., 601 Midland Avenue, Rye, New York 10580, by mail, by email at avoninvestorrelations@icrinc.com or by fax203-724-1610. We must receive your request at least one week prior to the Annual Meeting to have time to process your request. In addition, please bring photo identification to the Annual Meeting. | ||

• You may attend withoutpre-registration; however, you must bring proof of your Avon share ownership as of March 27, 2018 and photo identification. | ||

Shares held in a stock brokerage account or by a bank or other record holder may be voted in person at the Annual Meeting only if you obtain a legal proxy from such broker, bank or other record holder giving you the right to vote the shares. Shares held through the Avon Personal Savings Account Plan (the Plan) must be voted through the Plan Trustee as described below. | ||

Voting Instructions

| ||

Your proxy, when properly signed and returned to us, or processed by telephone or via the internet, and not revoked, will be voted in accordance with your instructions. We are not aware of any other matter that may be properly presented at the meeting. If any other matter is properly presented, the persons named as proxies on the proxy card will have discretion to vote in their best judgment. | ||

Unless you give other instructions on your proxy card, or unless you give other instructions when you cast your vote by telephone or via the internet, the persons named as proxies will vote in accordance with the recommendations of the Board of Directors as follows:for the election of each Director Nominee,for the approval of the compensation of our named executive officers, andfor the ratification of the appointment of our independent registered public accounting firm. | ||

Revoking Your Proxy or Changing Your Vote

| ||

Shareholders are entitled to revoke their Proxies at any time before their shares are voted at the Annual Meeting. To revoke a Proxy, you must file a written notice of revocation with the Company’s Corporate Secretary at 601 Midland Avenue, Rye, NY 10580, deliver a duly executed Proxy bearing a later date than the original submitted Proxy, submit voting instructions again by telephone or via the Internet, or attend the Annual Meeting and vote in person. Attendance at the Annual Meeting will not, by itself, revoke your Proxy. | ||

If your shares are held in a stock brokerage account or by a bank or other record holder, you may submit new voting instructions by contacting your broker, bank or other record holder or, if you have obtained a legal proxy from your broker, bank or other record holder giving you the right to vote your shares, by attending the meeting and voting in person. | ||

| 6 | AVON 2018 Proxy Statement |

Table of Contents

Quorum Requirements

| ||

The presence at the meeting, in person or by proxy, of the holders of a majority of the outstanding shares entitled to vote at the Annual Meeting will constitute a quorum, permitting the meeting to conduct its business. | ||

Abstentions and “brokernon-votes” are counted as present and entitled to vote for purposes of determining a quorum. A brokernon-vote occurs when a broker or other record holder holding shares for a beneficial owner does not vote on a particular proposal because that holder does not have discretionary voting power and has not received instructions from the beneficial owner. If you do not give instructions to the broker, bank or other record holder holding your shares, it will not be authorized to vote your shares with respect to Proposals 1 or 2. We therefore urge you to provide instructions so that your shares held in a stock brokerage account or by a bank or other record holder may be voted.

| ||

Approval of a Proposal

| ||

Each of the Proposals requires the affirmative vote of a majority of the votes cast at the Annual Meeting. “Votes cast” means the votes actually cast “for” or “against” a particular proposal, whether in person or by proxy.

| ||

Avon Associates—Personal Savings Account Plan

| ||

The trustee of the Avon Personal Savings Account Plan (the “Plan”), as record holder of the shares held in the Plan, will vote the shares allocated to your account in accordance with your instructions. Unless your vote is received by 11:59 P.M. (New York time) on May 11, 2018 and unless you have specified your instructions, your shares cannot be voted by the trustee.

| ||

Voting Deadline

| ||

If your shares are registered directly in your name with our transfer agent, Computershare Trust Company, N.A. and if you vote by telephone or the internet, your vote must be received by 1:00 A.M. (New York time) on May 16, 2018. If you do not prefer to vote by telephone or internet, you should complete and return the proxy card as soon as possible, so that it is received no later than the closing of the polls at the Annual Meeting. | ||

| If your shares are held in a stock brokerage account or by a bank or other record holder, you should return your voting instructions in accordance with the instructions provided by the broker, bank or other record holder who holds the shares on your behalf. | ||

If you hold shares in the Avon Products, Inc. Personal Savings Account Plan, your voting instructions must be received by 11:59 P.M. (New York time) on May 11, 2018.

| ||

Tabulation of Votes

| ||

Representatives of our transfer agent, Computershare Trust Company, N.A., will tabulate the votes and act as inspectors of election.

| ||

Vote Results

| ||

We intend to announce preliminary voting results at the Annual Meeting and to publish final results in a Current Report on Form8-K within four business days of the Annual Meeting. | ||

All proxies, ballots and voting materials that identify the votes of specific shareholders will generally be kept confidential, except as necessary to meet applicable legal requirements, to allow for the tabulation and certification of votes, and to facilitate a successful proxy solicitation. | ||

| AVON 2018 Proxy Statement | 7 |

Table of Contents

Householding

| ||

Beneficial owners who share a single address may receive only one copy of the proxy notice or the proxy materials, as the case may be, unless their broker, bank or other nominee has received contrary instructions from any beneficial owner at that address. This practice, known as “householding,” is designed to reduce printing and mailing costs. If any beneficial owner(s) sharing a single address wish to discontinue householding and/or receive a separate copy of the proxy notice or the proxy materials, as the case may be, or wish to enroll in householding, they should contact their broker, bank or other nominee directly. Alternatively, if any such beneficial owners wish to receive a separate copy of the proxy materials, we will deliver them promptly upon written or oral request to Investor Relations Department, Avon Products, Inc., 601 Midland Avenue, Rye, New York 10580, by mail, email at avoninvestorrelations@icrinc.com or fax203-724-1610 (telephone number203-682-8200). We currently do not “household” for our registered shareholders. |

| 8 | AVON 2018 Proxy Statement |

Table of Contents

PROPOSAL 1—ELECTION OF DIRECTORS

The Board of Directors has fixed the number of directors at 11. The Board has nominated Jose Armario, W. Don Cornwell, Nancy Killefer, Susan J. Kropf, Helen McCluskey, Andrew G. McMaster, Jr., James A. Mitarotonda, and Jan Zijderveld (the “Director Nominees”) for election to the Board and Cerberus Investor, as the holder of the Company’s Series C Preferred Stock, has elected Chan W. Galbato, Michael F. Sanford and Lenard B. Tessler, (the “Series C Designees”) to serve as directors commencing immediately upon the conclusion of the 2018 Annual Meeting. All nominees other than Messrs. McMaster and Mitarotonda are current members of our Board. There are no family relationships among our directors or executive officers.

As set forth in further detail on page 19, on March 26, 2018, the Company entered into an agreement with certain shareholders (the “Nomination Agreement”), pursuant to which the Company agreed to nominate Mr. Mitarotonda for election to the Board at the 2018 Annual Meeting.

Each of the Series C Designees will hold office until the next succeeding Annual Meeting or until his successor is elected and qualified. Each of the Director Nominees, if elected as a director at the 2018 Annual Meeting, will generally hold office until the next succeeding Annual Meeting or until his or her successor is elected and qualified. As set forth in further detail on page 30, Cerberus Investor is required to vote its shares in favor of each Director Nominee. Each Director Nominee has consented to being named as a nominee in our proxy materials and to serve as a director, if elected. We have no reason to believe that any of the Director Nominees will be unable or unwilling to serve as a director.

Each Director Nominee who receives a majority of the votes cast will be elected to the Board. If a Director Nominee is an incumbent director and he or she receives a greater number of votes “withheld” from his or her election than votes “for” such election, he or she is required to tender his or her resignation in accordance with our Corporate Governance Guidelines, as described under “Information Concerning The Board Of Directors—Board Policy Regarding Voting for Directors” on page 18.

THE BOARD OF DIRECTORS RECOMMENDS

that you vote FOR the election of each of the Director Nominees listed below.

JOSE ARMARIO

|

Director Nominee

| |||

| Jose Armario served as Corporate Executive Vice President of Worldwide Supply Chain, Development, and Franchising of McDonald’s Corporation from August 2011 until his retirement in October 2015. He served as Group President, McDonald’s Canada and Latin America of McDonald’s Corporation from February 2008 to August 2011. Prior to this, Mr. Armario was President, McDonald’s Latin America from 2004 to July 2008. Earlier in his career, Mr. Armario held operating roles of increasing responsibility at Lenscrafters, Inc. and Burger King Corporation. Mr. Armario is currently a director of USG Corporation. He also serves on the President’s Council of the University of Miami, Florida and the Governing Council of Advocate Good Samaritan Hospital, director of Golden State Foods and Receptions for Research: The Greg Olsen Foundation. | Directorsince:2016

Age:58

COMMITTEES Audit Committee Compensation and Management Development Committee | ||

SKILLS & EXPERIENCE OF PARTICULAR RELEVANCE TO AVON:

Having served in a variety of key leadership positions in nearly two decades with McDonald’s Corporation, Mr. Armario brings to the Board substantial experience leading large complex operations in global marketing, branding, supply chain, franchising and strategic planning. His first-hand consumer experience and global responsibilities with McDonald’s Corporation, particularly in Latin America, provide him with valuable insights to guide Avon in its key geographies.

| AVON 2018 Proxy Statement | 9 |

Table of Contents

W. DON CORNWELL

|

Director Nominee

| |||

|

Mr. Cornwell was Chairman and Chief Executive Officer of Granite Broadcasting Corporation from 1988 until his retirement in August 2009, and served as Vice Chairman until December 2009. Previously, Mr. Cornwell was Chief Operating Officer for the Corporate Finance Department at Goldman, Sachs & Co. from 1980 to 1988 and Vice President of the Investment Banking Division of Goldman Sachs from 1976 to 1988. He is a member of the joint diversity advisory council of Comcast and NBCUniversal, a trustee of Big Brothers Big Sisters of New York and a director of the Edna McConnell Clark Foundation. Mr. Cornwell is a director of Pfizer, Inc. and American International Group, Inc. |

Directorsince:2002

Age:70

COMMITTEES Audit Committee Finance Committee (Chair) Nominating and Corporate Governance Committee

Lead Independent Director | ||

SKILLS & EXPERIENCE OF PARTICULAR RELEVANCE TO AVON:

Through Mr. Cornwell’s career as an entrepreneur driving the growth of a consumer focused-media company, an executive in the investment banking industry and as a director of several significant consumer product and health care companies, he has accumulated valuable business, leadership, and management experience and brings important perspectives on the issues facing the Company. Mr. Cornwell founded and built Granite Broadcasting Corporation, a consumer-focused media company, through acquisitions and operating growth, enabling him to provide insight and guidance on the Company’s strategic direction and growth. Mr. Cornwell’s strong financial background, including his work at Goldman Sachs prior toco-founding Granite and his service on the audit and investment committees of other companies’ boards, also provides financial expertise to the Board, including an understanding of financial statements, corporate finance, accounting, and capital markets.

NANCY KILLEFER

|

Director Nominee

| |||

|

Ms. Killefer served as a Senior Partner at McKinsey & Company, an international management consulting firm, until her retirement in August 2013. She joined McKinsey in 1979 and held a number of leadership roles, including as a member of the firm’s governing board. Ms. Killefer led the firm’s recruiting and chaired several of the firm’s personnel committees. From 2000 to 2007, she ran McKinsey’s Washington, D.C. office. From 1997 to 2000, Ms. Killefer served as Assistant Secretary for Management, Chief Financial Officer and Chief Operating Officer at the U.S. Department of Treasury. In 2000, she returned to McKinsey to establish and lead the firm’s Public Sector Practice. She also served as a member of the IRS Oversight Board from 2000 to 2005 and as chair of that body from 2002 to 2004. Ms. Killefer is currently a director of Cardinal Health and Chair of the board of directors of CSRA. She also serves as a vice chair of the Defense Business Board, an advisory body to the Secretary of Defense. |

Directorsince:2013

Age:64

COMMITTEES Compensation and Management Development Committee Nominating and Corporate Governance Committee (Chair) | ||

SKILLS & EXPERIENCE OF PARTICULAR RELEVANCE TO AVON:

Having served in key leadership positions in both the public and private sectors and having provided strategic counsel to consumer-based companies during her 30 years with McKinsey & Partners, Ms. Killefer brings to the Board substantial experience in the areas of strategic planning, including sales, marketing and brand building. Her experience as a partner of a global management consulting firm and as Chief Financial Officer and Chief Operating Officer of a government agency provides valuable expertise in the areas of executive leadership and finance. Ms. Killefer’s corporate governance experience as a director of other public companies, including as chair of the board of directors of CSRA, are also highly valuable to the Board.

| 10 | AVON 2018 Proxy Statement |

Table of Contents

SUSAN J. KROPF

| Director Nominee

| |||

|

Ms. Kropf served as President and Chief Operating Officer of Avon Products, Inc. from January 2001 until her retirement in 2006. She also served as Avon’s Executive Vice President and Chief Operating Officer, North America and Global Business Operations from 1999 to 2001 and Executive Vice President and President, North America from 1998 to 1999. Ms. Kropf was a member of Avon’s Board of Directors from 1998 to 2006. Ms. Kropf is currently a director of Tapestry (formerly Coach, Inc.), The Kroger Co., New Avon LLC and The Sherwin-Williams Company. Ms. Kropf also served as a director of Mead Westvaco Inc. until 2015.

|

Director since: 2015

Age:69

COMMITTEES Finance Committee | ||

SKILLS & EXPERIENCEOF PARTICULAR RELEVANCE TO AVON:

Having held various senior management positions during the course of her37-year career at Avon, including fullprofit-and-loss responsibility for all of Avon’s worldwide operations as its President and Chief Operating Officer, Ms. Kropf has extensive operational skills, a deep understanding of direct selling, and significant experience in marketing, research and development, product development, customer service, supply chain operations and manufacturing. Ms. Kropf has a strong financial background gained through her career at Avon and from her service on the boards of various public companies, including their compensation, audit, and corporate governance committees.

HELEN MCCLUSKEY

| Director Nominee

| |||

|

Ms. McCluskey was President, Chief Executive Officer and a member of the Board of Directors of The Warnaco Group, Inc. from February 2012 to February 2013, when it was acquired by PVH Corp., and she then served on the board of directors of PVH Corp. until June 2014. Ms. McCluskey also served in other leadership roles at Warnaco, including Chief Operating Officer from September 2010 to February 2012 and Group President from July 2004 to September 2010. Prior to joining Warnaco, Ms. McCluskey held positions of increasing responsibility at Liz Claiborne, Inc. from August 2001 to June 2004. Previously, she spent 18 years in Sara Lee Corporation’s intimate apparel units, where she held executive positions in marketing, operations and general management, including President of Playtex Apparel from 1999 to 2001. Ms. McCluskey is a director of Dean Foods Company and Signet Jewelers Limited.

|

Director since: 2014

Age:63

COMMITTEES Compensation and Management Development Committee (Chair) | ||

SKILLS & EXPERIENCEOF PARTICULAR RELEVANCE TO AVON:

Ms. McCluskey has a broad background in strategy, business planning and operations derived from a career spanning over 30 years with leading consumer goods companies. Having built women’s brands globally for sale through all channels of distribution worldwide, she brings a valuable blend of branding, merchandising, marketing and international expertise to the Board. Ms. McCluskey’s experience as a Chief Executive Officer of a global public company provides her with significant expertise in global business matters, corporate leadership and management which enables her to make important contributions to the oversight of the Company’s strategic direction and growth, and management development.

| AVON 2018 Proxy Statement | 11 |

Table of Contents

ANDREW G. MCMASTER, JR.

| Director Nominee

| |||

|

Mr. McMaster served as Deputy Chief Executive Officer and Vice Chairman at Deloitte & Touche LLP from 2002 until his retirement in May 2015. He joined Deloitte in 1976 and held a number of leadership roles, including National Managing Partner of Deloitte’s Office of the CEO client programs and of Deloitte’s U.S. and Global Forensic and Dispute Consulting practice. Mr. McMaster is currently a director of Black & Veatch Holding Company and UBS Americas Holding LLC, a subsidiary of UBS AG. Mr. McMaster also currently serves as Chairman of the Financial Accounting Standards Advisory Council (FASAC), an advisory body to the Financial Accounting Standards Board (FASB), and as Vice Chair of the Hobart and William Smith Colleges Board of Trustees.

|

Age: 65 | ||

SKILLS & EXPERIENCEOF PARTICULAR RELEVANCE TO AVON:

Mr. McMaster has substantial experience in the areas of finance, audit and accounting, having served as a senior executive during a39-year career with Deloitte & Touche LLP, as the current Chair of the audit committees of Black & Veatch Holding Company and UBS Americas Holding LLC, and as the current Chairman of the Financial Accounting Standards Advisory Council. He also gained experience in a variety of operational, client service and firm leadership roles at Deloitte, serving many of the firm’s largest, most complex global clients as both a Lead Engagement partner and an Advisory Partner across diverse industries.

JAMES A. MITAROTONDA

| Director Nominee

| |||

|

Mr. Mitarotonda has served as the Chairman of the Board, President and Chief Executive Officer of Barington Capital Group, L.P. (“Barington”), an investment firm that heco-founded, since 1991. He has also served as the Chairman of the Board, President and Chief Executive Officer of Barington Companies Investors, LLC, the general partner of Barington Companies Equity Partners, L.P., a value-added activist investment fund, since 1999. Mr. Mitarotonda is currently a director of A. Schulman Inc, OMNOVA Solutions, Inc. and The Eastern Company, where he is the Chairman. He also serves as a member of the Board of Trustees for Queens College. Mr. Mitarotonda previously served as a director of The Pep Boys-Manny, Moe & Jack until 2016, Ebix, Inc. until 2015, and The Jones Group Inc. until 2014. He also served as a director of Barington/Hilco Acquisition Corp. until January 2018, as its Chief Executive Officer until 2015, and as its Chairman until 2017.

|

Age: 63 | ||

SKILLS & EXPERIENCEOF PARTICULAR RELEVANCE TO AVON:

Through his over twenty-five years as Chairman of the Board, President and Chief Executive Officer of Barington Capital Group, L.P., Mr. Mitarotonda brings to the Board extensive financial, investment banking and executive leadership experience. He also has significant board of director and corporate governance experience through his service on numerous public company boards across diverse industries, including consumer-focused companies such as The Jones Group and Pep Boys-Manny, Moe & Jack.

| 12 | AVON 2018 Proxy Statement |

Table of Contents

JAN ZIJDERVELD

|

Director Nominee

| |||

| Mr. Zijderveld joined Avon as Chief Executive Officer and was appointed to the Board of Directors in February 2018. He joined Avon after 30 years with Unilever N.V./PLC, where he rose to serve as a member of the Executive Committee and President of Unilever’s European business in 2011. In this position, Mr. Zijderveld oversaw 25,000 employees and operations in 34 countries. Prior to that, he served in a number of leadership roles, including Executive Vice President of Unilever, South East Asia & Australasia from 2008 to 2011, while also acting asNon-Executive Chairman of Unilever’s listed Indonesian business, and CEO of Unilever, Middle East and North Africa (MENA) from 2005 to 2008. Earlier in his career, he served in numerous leadership positions across Europe, Australia and New Zealand in general management, marketing, sales and distribution. | Directorsince:2018

Age:53

CEO | ||

SKILLS & EXPERIENCE OF PARTICULAR RELEVANCE TO AVON:

Having spent 30 years with Unilever, a transnational consumer goods company, during which time he lived and worked in seven countries across three continents, Mr. Zijderveld possesses deep operating experience in multi-channel, complex consumer businesses across emerging, developing and developed markets. His particular experience in Europe, the Middle East and Asia enable him to provide insights and understanding into these areas and help guide the Company’s strategic decisions in these markets. His leadership positions at Unilever provide him with vast experience in marketing, sales and distribution, and make him uniquely qualified in making necessary decisions for the Company’s long-term growth, business goals and managing challenging market conditions.

CHAN W. GALBATO

|

Series C Designee

| |||

| Mr. Galbato was appointednon-executive Chairman of Avon’s Board of Directors in March 2016. Mr. Galbato is Chief Executive Officer of Cerberus Operations and Advisory Company, LLC. Prior to joining Cerberus in 2009, he owned and managed CWG Hillside Investments LLC, a consulting business, from 2007 to 2009. From 2005 to 2007, he served as President and CEO of the Controls Group of businesses for Invensys plc and President of Services for The Home Depot. Mr. Galbato previously served as President and Chief Executive Officer of Armstrong Floor Products and Chief Executive Officer of Choice Parts. He spent 14 years with General Electric Company, holding several operating and finance leadership positions within their various industrial divisions as well as holding the role of President and CEO of Coregis Insurance Company, a G.E. Capital company. Mr. Galbato currently serves on the Board of Directors of Blue Bird Corporation, DynCorp International, FirstKey Homes LLC, Iron Horse Acquisition Corporation, Staples Solutions B.V. and Steward Health Care, LLC, and on the Board of Managers of New Avon LLC. Mr. Galbato had previously served as lead director of the Brady Corporation, director of Tower International and Chairman of YP Holdings, LLC.

On April 2, 2018, Mr. Galbato wasre-elected to the Board of Directors commencing immediately upon the conclusion of the 2018 Annual Meeting by the holders of our Series C Preferred Stock, voting separately as a single class, and is not up for election by our shareholders at the 2018 Annual Meeting. | Directorsince:2016

Age:55

COMMITTEES Audit Committee(non-voting Observer) Nominating and Corporate Governance Committee

Non-executive Chairman of the Board | ||

SKILLS & EXPERIENCE OF PARTICULAR RELEVANCE TO AVON:

Through his 30 years of experience as an executive at public and private companies across a range of industries, including consumer products, Mr. Galbato has broad operational and business strategy expertise and significant skills in corporate leadership including as a Chief Executive Officer. Mr. Galbato is recognized for his experience in corporate turnarounds, which enables him to help guide the Company’s strategic direction and growth.

| AVON 2018 Proxy Statement | 13 |

Table of Contents

MICHAEL F. SANFORD

|

Series C Designee

| |||

| Mr. Sanford is a Senior Managing Director,Co-Head of North American Private Equity, and a member of the Global Private Equity Investment Committee at private investment firm Cerberus Capital Management, L.P. Prior to joining Cerberus in 2006, Mr. Sanford was at The Blackstone Group in its Restructuring and Reorganization Advisory Group from 2004 to 2006, where he advised companies and creditors on a variety of restructuring transactions. Prior to joining Blackstone, from 2003 to 2004, Mr. Sanford worked at Banc of America Securities in its Consumer and Retail Investment Banking Group, where he executed various financing, M&A and leveraged recapitalization transactions. He serves on the Board of Directors of DynCorp International Inc. and Tier 1 Group LLC and on the Board of Managers of New Avon LLC.

On April 2, 2018, Mr. Sanford wasre-elected to the Board of Directors commencing immediately upon the conclusion of the 2018 Annual Meeting by the holders of our Series C Preferred Stock, voting separately as a single class, and is not up for election by our shareholders at the 2018 Annual Meeting. | Directorsince:2016

Age:37

COMMITTEES Finance Committee | ||

SKILLS & EXPERIENCE OF PARTICULAR RELEVANCE TO AVON:

Through his career in various roles with finance and private equity firms, Mr. Sanford has extensive experience in financing matters and private equity investments. Mr. Sanford’s insights into capital management, restructuring, and capital markets are highly valuable to the Board.

LENARD B. TESSLER

|

Series C Designee

| |||

| Mr. Tessler is currently Vice Chairman and Senior Managing Director of private investment firm Cerberus Capital Management, L.P., where he is a member of the Cerberus Capital Management Investment Committee. Prior to joining Cerberus in 2001, Mr. Tessler served as Managing Partner of TGV Partners from 1990 to 2001, a private equity firm which he founded. Earlier in his career, he was a founding partner of Levine, Tessler, Leichtman & Co., and a founder, Director and Executive Vice President of Walker Energy Partners. Mr. Tessler is currently Lead Director of Albertsons Companies, and a director of Keane Group, Inc. He is also a Trustee of the New York-Presbyterian Hospital where he is a member of the Investment Committee and the Budget and Finance Committee.

On April 2, 2018, Mr. Tessler was re-elected to the Board of Directors commencing immediately upon the conclusion of the 2018 Annual Meeting by the holders of our Series C Preferred Stock, voting separately as a single class, and is not up for election by our shareholders at the 2018 Annual Meeting. | Directorsince:2018

Age:65 | ||

SKILLS & EXPERIENCE OF PARTICULAR RELEVANCE TO AVON:

Through his senior executive positions held during the course of over 30 years at private investment firms and his service on boards of directors of operating companies, Mr. Tessler has an extensive background in financing and private equity investments, which provides critical skills to the Board in its oversight of strategic planning and operations.

| 14 | AVON 2018 Proxy Statement |

Table of Contents

INFORMATION CONCERNING THE BOARD OF DIRECTORS

Our Board of Directors held seven meetings in 2017. Directors are expected to attend all meetings of the Board and the Board Committees on which they serve and to attend the Annual Meeting of Shareholders. In 2017, all directors then serving on the Board attended at least 75% of the aggregate number of 2017 meetings of the Board and of each Board Committee on which he or she served. All directors then serving on the Board attended the 2017 Annual Meeting. In addition to participation at Board and Committee meetings and the Annual Meeting of Shareholders, our directors discharge their duties throughout the year through communications with senior management.

Non-employee directors meet in regularly scheduled executive sessions, as needed, without the CEO or other members of management.

The Board currently separates the positions of Chairman, Lead Independent Director and CEO. Mr. Galbato serves as ournon-executive Chairman of the Board, Mr. Cornwell serves as our Lead Independent Director and Mr. Zijderveld serves as our CEO.

The Board evaluates its leadership structure periodically and believes that separating the Chairman, Lead Independent Director and CEO roles is important as the Company focuses on its transformation and growth efforts. Per the Company’sBy-Laws, the Chairman presides at all meetings of the Board, including executive sessions, at which the Chairman is present, and the Lead Independent Director presides at all meetings of the Board at which the Chairman is not present. Additional rights, duties and responsibilities of the Chairman and the Lead Independent Director are set forth in theBy-Laws and the Corporate Governance Guidelines. Pursuant to the Investor Rights Agreement, so long as Cerberus Investor maintains a certain ownership level in the Company (as described in more detail on page 30 of this Proxy Statement), Cerberus Investor has the right to select the director to be appointed as our Chairman.

The Board administers its risk oversight function primarily through the Audit Committee, which oversees the Company’s risk management practices. The Audit Committee is responsible for, among other things, discussing with management on a regular basis the Company’s guidelines and policies that govern the process for risk assessment and risk management. Management is responsible for assessing and managing the Company’s various risk exposures ona day-to-day basis. In connection with this, the Audit Committee has oversight of the Company’s enterprise risk management (“ERM”) program, which includes a risk management committee composed of certain key executives. The cross-functional group of key executives who comprise the risk management committee identify, on a periodic basis, the top current and future risks facing the Company, including, but not limited to, strategic, operational, financial and compliance risks, and the associated risk owners are responsible for managing and mitigating these risks. The Board may assign certain ERM risks to a specific Board Committee to examine in detail if such Board Committee is in the best position to review and assess the risk. In line with this, the Company provides regular ERM updates to the Audit Committee on several risks, including cybersecurity and data privacy, and to other Board Committees, as appropriate. The Audit Committee also periodically reports to the full Board on the Company’s ERM program.

While the Board has overall responsibility for overseeing risk management, Board Committees oversee risk within their areas of responsibility, as appropriate. For example, as set forth in further detail on page 55, our Compensation and Management Development Committee, with support and advice from its independent consultant, reviews the risk and reward structure of executive compensation plans, policies and practices at least annually to confirm that there are no compensation-related risks that are reasonably likely to have a material adverse effect on the Company. As set forth in its charter, the Finance Committee is responsible for, among other things, reviewing periodically the Company’s strategy for and use of derivatives for hedging risks such as interest rate and foreign exchange risks.

For certain risks, oversight is conducted by the full Board, such as during the Board’s annual review of the Company’s strategic goals and initiatives and other significant issues that are expected to affect the Company in the future. We believe that the Chairman, Lead Independent Director, CEO, and roles of the Board and the Board Committees provide the appropriate leadership to help ensure effective risk oversight.

| AVON 2018 Proxy Statement | 15 |

Table of Contents

The Board has the following regular standing committees: Audit Committee, Compensation and Management Development Committee, Nominating and Corporate Governance Committee, and Finance Committee. The charters of each Committee and our Corporate Governance Guidelines are available on our investor website (www.avoninvestor.com). Our Code of Conduct (which applies to the Company’s directors, officers and employees) is available atwww.avoncompany.com.

Audit Committee

|

Primary Responsibilities

|

2017 Meetings: 10

| ||

Charles H. Noski (Chair) Jose Armario W. Don Cornwell Cathy D. Ross Chan W. Galbato* *non-voting Observer |

• Assists the Board in fulfilling its responsibility to oversee the integrity of our financial statements, controls and disclosures, our compliance with legal and regulatory requirements, the qualifications and independence of our independent registered public accounting firm, and the performance of our internal audit function and independent registered public accounting firm. The Committee has the authority to conduct any investigation appropriate to fulfilling its purpose and responsibilities.

| |||

• The Board has determined that Mr. Noski, Mr. Cornwell and Ms. Ross are “audit committee financial experts,” under the rules of the Securities and Exchange Commission and that all of the Committee members are independent and financially literate under the listing standards of the New York Stock Exchange. | ||||

• A further description of the role of the Audit Committee is set forth on pages 75 through 78 under “Audit Committee Report” and “Proposal 3—Ratification of Appointment of Independent Registered Public Accounting Firm.”

| ||||

Compensation and Management Development Committee

|

Primary Responsibilities

|

2017 Meetings: 9

| ||

Helen McCluskey (Chair) Jose Armario Nancy Killefer |

• Discharges the responsibilities of the Board relating to executive compensation, including reviewing and establishing our overall executive compensation and benefits philosophy, including review of the risk and reward structure of executive compensation plans, policies and practices, as appropriate. In addition, the Committee, in consultation with the independent members of the Board, reviews and approves the goals and objectives relevant to the compensation of the CEO and determines the compensation of the CEO. It also determines the compensation of all senior officers and oversees incentive compensation plans, including establishing performance measures and evaluating and approving any incentive payouts thereunder. | |||

• Reviews and evaluates the Company’s talent management and succession planning approach, philosophy, and key processes, and is responsible for development and succession plans for members of the Company’s Executive Management Committee and their potential successors. | ||||

• The Committee may delegate responsibilities to a subcommittee composed of one or more members of the Committee, provided that any action taken shall be reported to the full Committee as soon as practicable, but in no event later than at the Committee’s next meeting. In addition, the Committee may delegate certain other responsibilities, as described in the Committee charter. For example, the Committee has delegated to Mr. Zijderveld in his capacity as a director the authority to approve annual andoff-cycle equity awards to employees who are not senior officers. | ||||

• A description of the role of the compensation consultant engaged by the Committee, scope of authority of the Committee and the role of executive officers in determining executive compensation is set forth on page 45 under “Compensation Discussion and Analysis—Roles in Executive Compensation.” | ||||

| 16 | AVON 2018 Proxy Statement |

Table of Contents

Nominating and Corporate Governance Committee

|

Primary Responsibilities

|

2017 Meetings: 5

| ||

Nancy Killefer (Chair) W. Don Cornwell Chan W. Galbato Charles H. Noski |

• Identifies individuals qualified to become Board members, consistent with criteria approved by the Board, and recommends to the Board the candidates for directorships to be filled by the Board. A description of the Committee’s process for identifying and evaluating nominees for directorships is set forth on page 18 under “Director Nomination Process & Shareholder Nominations.”

| |||

• Develops and recommends to the Board corporate governance principles, monitors developments in corporate governance, and makes recommendations to the Board regarding changes in governance policies and practices. | ||||

• Oversees the evaluation of the Board, including conducting an annual evaluation of the performance of the Board and Board committees. | ||||

• Reviews and recommends to the Board policies regarding the compensation ofnon-employee directors. | ||||

• A description of the compensation ofnon-employee directors and the Committee’s scope of authority with respect to such matters is set forth on page 21 under “Director Compensation—Role of Nominating and Corporate Governance Committee.”

| ||||

Finance Committee

|

Primary Responsibilities

|

2017 Meetings: 4

| ||

W. Don Cornwell (Chair) Susan J. Kropf Michael F. Sanford |

• Assists the Board in fulfilling its responsibilities to oversee our financial management, including oversight of our capital structure and financial strategies, investment strategies, banking relationships, and funding of the employee benefit plans. | |||

• Responsible for the oversight of the deployment and management of our capital, including the oversight of certain key business initiatives. | ||||

The Board has concluded that eachnon-employee director, Director Nominee and Series C Designee is independent.

The Board assesses the independence of itsnon-employee members at least annually in accordance with the listing standards of the New York Stock Exchange, the regulations of the Securities and Exchange Commission, and our Corporate Governance Guidelines. As part of its assessment, the Board determines whether or not any such director has a material relationship with the Company, either directly or indirectly as a partner, shareholder or officer of an organization that has a relationship with the Company. The Board broadly considers all relevant facts and circumstances and considers this issue not merely from the standpoint of the director, but also from that of persons or organizations with which the director has an affiliation. This consideration includes:

| • | the nature of the relationship; |

| • | the significance of the relationship to Avon, the other organization and the individual director; |

| • | whether or not the relationship is solely a business relationship in the ordinary course of Avon’s and the other organization’s businesses and does not afford the director any special benefits; and |

| • | any commercial, industrial, banking, consulting, legal, accounting, charitable, familial and other relationships;provided, that ownership of a significant amount of our stock is not, by itself, a bar to independence. |

In assessing the independence of directors and the materiality of any relationship with Avon and the other organization, the Board has determined that a relationship in the ordinary course of business involving the sale, purchase or leasing of property or services will not be deemed material if the amounts involved, on an annual basis, do not exceed the greater of (i) $1,000,000 or (ii) one percent (1%) of Avon’s revenues or one percent (1%) of the revenues of the other organization involved.

In the ordinary course of business, the Company has business relationships with certain companies on which Avon directors also serve on the board of directors, including for example, advertising arrangements, software services, and insurance coverage. The Company also has ongoing business relationships with affiliates of Cerberus Investor, of which the Series C Designees serve as directors, officers or employees, as described in “Transactions with Related Persons” on page 28. Based on the standards described above, the Board has determined that none of these transactions or relationships, nor the associated amounts paid to the parties, was material such that it would impede the exercise of independent judgment.

| AVON 2018 Proxy Statement | 17 |

Table of Contents

Board Policy Regarding Voting for Directors

Our Corporate Governance Guidelines provide that any incumbent director who receives a greater number of votes “withheld” than votes “for” his or her election in an uncontested election of directors will promptly tender his or her resignation. The Nominating and Corporate Governance Committee (the “Committee”) will recommend to the Board whether to accept or reject the tendered resignation, or whether other action should be taken. The Committee will consider any factors or other information that it considers appropriate or relevant. The Board, taking into account the Committee’s recommendation, will act on the tendered resignation and publicly disclose its decision and the rationale within 90 days from the date of the certification of the election results.

Board and Committee Self-Evaluations

Pursuant to the Company’s Corporate Governance Guidelines and each committee’s charter, the Board and each of its committees annually conducts a self-assessment. The Nominating and Corporate Governance Committee oversees the process. In recent years, the Board has used the Corporate Secretary or a third-party facilitator to interview each Director to obtain his or her feedback regarding the Board’s and each committee’s effectiveness, as well as feedback on each individual Director and the Chairman, Lead Independent Director and each committee chair in their respective roles. Self-evaluation topics generally include, among other matters, Board and committee composition and structure; effectiveness of the Board and committees; meeting topics and process; and Board interaction with management. The Board discusses the results of each annual self-evaluation and, based on the results, implements enhancements and other modifications as appropriate. Similarly, the results of each committee evaluation are discussed at subsequent committee meetings for the relevant committee. Individual feedback is provided to Directors by the Chairman and the Lead Independent Director.

Director Nomination Process & Shareholder Nominations

The Nominating and Corporate Governance Committee is responsible for identifying individuals qualified to become Board members, consistent with criteria approved by the Board, and for making recommendations to the Board regarding: (i) nominees for Board membership to fill vacancies and newly created positions, and (ii) the persons to be nominated by the Board for election at the Company’s annual meeting of shareholders. The Committee actively considers potential director candidates on an ongoing basis as part of its director succession planning efforts.

The Committee’s process for considering all candidates for election as directors, including shareholder-recommended candidates, is designed to ensure that the Committee fulfills its responsibility to recommend candidates that are properly qualified and are not serving any special interest groups, but rather the best interest of all of the shareholders.

In making its recommendations, the Committee evaluates each candidate based on the independence standards described above and other qualification standards described below. For example, our Corporate Governance Guidelines and the charter of the Nominating and Corporate Governance Committee require that our directors possess the highest standards of personal and professional ethics, character and integrity and meet the standards set forth in our Corporate Governance Guidelines. In identifying candidates for membership on the Board, the Committee takes into account all factors it considers appropriate, consistent with criteria approved by the Board, which may include professional experience, knowledge, independence, diversity of backgrounds, and the extent to which the candidate would fill a present or evolving need on the Board. There is not a formal diversity policy; however, the Board values diversity in its broadest sense, including differences of viewpoint, personal and professional experience, skill, gender, race, ethnicity, geography, and other individual characteristics, and the Committee endeavors to include women, minority, and geographically diverse candidates in the qualified pool from which Board candidates are chosen.

The Board takes an active and thoughtful approach to refreshment and strives to maintain a balance of longer-tenured directors and newer directors with fresh ideas and viewpoints to achieve an appropriate balance of continuity and refreshment. The Board does not believe in limiting the number of terms that a director may serve, as term limits could deprive the Company and its shareholders of valuable director experience and familiarity with the Company and its operations, however, there-nomination of incumbent directors is not automatic. In accordance with the Company’s Corporate Governance Guidelines, all directors serveone-year terms and anynon-employee director who will be age 72 or older at the time of the election may not stand for reelection unless requested by the Board. The composition of our Board, as contemplated by our current slate of nominees, includes six new independent directors since 2016. In addition, in 2018, Jan Zijderveld joined the Board in connection with his appointment as the Company’s Chief Executive Officer. As a result of these Board changes, tenure on the Board currently ranges from less than one year to 16 years, with an average Board tenure of 3 years.

The Committee has retained a third-party search firm to locate candidates who may meet the needs of the Board. The firm typically provides information on a number of candidates for review and discussion by the Committee. As appropriate, the Committee chair and other members of the Committee and the Board interview potential candidates. If the Committee determines that a potential candidate meets the needs of the Board, possesses the relevant qualifications, and meets the standards set forth in our Corporate Governance Guidelines, the Committee will vote to recommend to the Board the election of the candidate as a director. Following the completion of this process with respect to Mr. McMaster, members of the Committee determined that Mr. McMaster met these standards and, therefore, recommended to the Board the election of this candidate as a director.

| 18 | AVON 2018 Proxy Statement |

Table of Contents

On March 26, 2018, the Company and certain of its shareholders entered into an agreement (the “Nomination Agreement”), pursuant to which the Company agreed to nominate Mr. Mitarotonda for election to the Board at the 2018 Annual Meeting. The shareholders party to the Nomination Agreement consist of Shah Capital Management, Inc., NuOrion Advisors, LLC, Barington Capital Group, L.P. and certain of their respective affiliates (collectively, the “Barington Group”). In connection with the Nomination Agreement, the Barington Group withdrew its notice of nomination for the 2018 Annual Meeting. The Nomination Agreement requires each member of the Barington Group to abide by certain customary voting and standstill provisions, subject to certain exceptions, through Mr. Mitarotonda’s service on the Board, including that at the 2018 Annual Meeting it will vote all of its shares of the Company’s common stock that it or its affiliates have the right to vote in favor of the election of directors nominated by the Board and refrain from soliciting proxies or participating in any “withhold” or similar campaign. The foregoing is not a complete description of the terms of the Nomination Agreement and the associated Confidentiality Agreement. For copies of, and more information concerning, the Nomination Agreement and the Confidentiality Agreement, please see the Company’s Current Report on Form8-K filed with the Securities and Exchange Commission (the “SEC”) on March 26, 2018 and Exhibits 10.1 and 10.2 thereto.

The Committee will consider director candidates recommended by shareholders if properly submitted to the Committee in accordance with ourBy-Laws and our Corporate Governance Guidelines. Shareholders wishing to recommend persons for consideration by the Committee as nominees for election to the Board can do so by writing to the Nominating and Corporate Governance Committee, c/o Corporate Secretary, Avon Products, Inc., 601 Midland Avenue, Rye, NY 10580. Recommendations must include the proposed nominee’s name, detailed biographical data, work history, qualifications and corporate and charitable affiliations. A written statement from the proposed nominee consenting to be named as a nominee and, if nominated and elected, to serve as a director is also required. The Committee will then consider the candidate and the candidate’s qualifications using the criteria as set forth above. The Committee may discuss with the shareholder making the nomination the reasons for making the nomination and the qualifications of the candidate. The Committee may then interview the candidate and may also use the services of a search firm to provide additional information about the candidate prior to making a recommendation to the Board.

Shareholders of record may also nominate candidates for election to the Board by following the procedures set forth in ourBy-Laws. The Company’sBy-laws include proxy access provisions whereby a shareholder, or a group of up to 20 shareholders, who owns 3% or more of the Company’s common stock continuously for at least three years, may nominate and include in the Company’s proxy materials candidates for election as directors of the Company. Such shareholder(s) or group(s) of shareholders may nominate up to the greater of two individuals or 20% of the Board, provided that the shareholder(s) and the nominee(s) satisfy the requirements specified in theBy-Laws and comply with the other procedural requirements of our Corporate Governance Guidelines. Please also see Section 14(a) of Article 3 of ourBy-Laws for details regarding the nomination of a Director candidate through the Advance Notice Process which is separate from a proxy access nomination. Information regarding these procedures for nominations by shareholders will be provided upon request to our Corporate Secretary.

A shareholder or other interested person who wishes to contact the Chairman, the Lead Independent Director or thenon-employee or independent directors as a group may do so by addressing his or her correspondence to the Chairman, the Lead Independent Director or such directors, c/o Corporate Secretary, Avon Products, Inc., 601 Midland Avenue, Rye, NY 10580. All correspondence addressed to a director or group of directors will be forwarded to that director or group of directors.