UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d) of the

Securities Exchange Act of 1934

Date of Report (Date of earliest event reported): May 15, 2007

Kronos Incorporated

(Exact name of registrant as specified in charter)

Massachusetts |

| 000-20109 |

| 04-2640942 |

(State or other juris- |

| (Commission |

| (IRS Employer |

diction of incorporation) |

| File Number) |

| Identification No.) |

297 Billerica Road, Chelmsford, Massachusetts |

| 01824 |

(Address of principal executive offices) |

| (Zip Code) |

Registrant’s telephone number, including area code: (978) 250-9800

N/A

(Former name or former address, if changed since last report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instruction A.2. below):

o Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425)

o Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12)

o Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b))

o Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c))

Item 7.01. Regulation FD Disclosure.

Kronos Incorporated (the “Company”) is hereby furnishing the following information, which was provided to potential lenders in connection with the syndication of a new credit facility intended to be used to finance the merger and related transactions described in the Company’s definitive proxy statement on Schedule 14A filed with the Securities and Exchange Commission on May 4, 2007. The following presentation contains certain Non-GAAP financial measures. Please see below for a reconciliation of such measures to their most comparable GAAP measure.

This current report on Form 8-K contains forward-looking statements. Generally, you can identify these statements because they contain words like “anticipates,” “believes,” “estimates,” “expects,” “forecasts,” “future,” “intends,” “plans” and similar terms. These statements reflect the Company’s current expectations. Forward-looking statements include statements concerning its plans, objectives, goals, strategies, future events, capital expenditures, future results, its competitive strengths, its business strategy, the trends in its industry, and the benefits of its recent acquisitions.

Although the Company does not make forward-looking statements unless it believes that it has a reasonable basis for doing so, the Company does not guarantee their accuracy, and actual results may differ materially from those the Company anticipated due to a number of uncertainties, including, among others, the risks the Company faces as described under the “Risk Factors” section of its quarterly report on Form 10-Q for the quarter ended March 31, 2007. You should not place undue reliance on these forward-looking statements. These forward-looking statements are within the meaning of Section 27A of the Securities Act and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and are intended to be covered by the safe harbors created thereby. To the extent that such statements are not recitations of historical fact, such statements constitute forward-looking statements that, by definition, involve risks and uncertainties. In any forward-looking statement where the Company expresses an expectation or belief as to future results or events, such expectation or belief is expressed in good faith and is believed to have a reasonable basis, but there can be no assurance that such future results or events expressed by the statement of expectation or belief will be achieved or accomplished. The Company’s actual results, performance or achievements could differ materially from those expressed in, or implied by, forward-looking statements. The Company can give you no assurance that any of the events anticipated by forward-looking statements will occur or, if any of them do, what impact they will have on the Company’s results of operations and financial condition.

The Company cautions you that in light of the risks and uncertainties described in the “Risk Factors” section of its quarterly report on Form 10-Q for the quarter ended March 31, 2007, the matters referred to in the forward-looking statements contained in this current report on Form 8-K may not in fact occur. The Company undertakes no obligation to update or revise any forward-looking statement as a result of new information, future events or otherwise, except as otherwise required by law.

As provided in General Instruction B.2 of Form 8-K, the information contained in this current report on Form 8-K shall not be deemed to be “filed” for purposes of Section 18 of the Exchange Act, nor shall it be deemed to be incorporated by reference in any filing under the Securities Act of 1933, as amended, except as shall be expressly set forth by specific reference in such a filing. Furnishing this information, the Company makes no admission as to the materiality of any information in this report that is required to be disclosed solely by reason of Regulation FD.

Introduction

On March 22, 2007, the Company entered into an Agreement and Plan of Merger (the “Merger Agreement”) with Seahawk Acquisition Corporation, a Delaware corporation (“Parent”), and Seahawk Merger Sub Corporation, a Massachusetts corporation and a wholly-owned subsidiary of Parent (the “Merger Sub”). Under the Merger Agreement, the Merger Sub will be merged with and into the Company (the “Merger”), with the Company continuing after the Merger as the surviving corporation and a wholly-owned subsidiary of Parent. Parent and Merger Sub are entities affiliated with Hellman & Friedman LLC, a private equity investment firm. Under the terms of the Merger Agreement, the Company’s shareholders will receive $55.00 in cash for each share of the Company’s common stock (the “Transaction”). The acquisition of Kronos will be financed with $1,055.0 million of funded

1

senior secured credit facilities, $719.5 million of cash equity and $101.7 million of cash from the Company (the “Financing”).

A. Transaction Summary

The Transaction, which is expected to close in early June, values the Company at approximately $1.8 billion, or 12.5x (including fees and expenses) pro forma LTM 3/31/07 adjusted EBITDA(1) of $141.8 million.

For the twelve months ended March 31, 2007, Kronos generated pro forma revenue(2) and pro forma adjusted EBITDA(1) of $637.5 million, and $141.8 million, respectively.

Pro forma for the Financing, the Company will have first lien and total debt to pro forma LTM 3/31/07 adjusted EBITDA of 4.7x and 7.4x, respectively.

(1) Pro forma for deferred revenue adjustments and one-time, non-recurring items; pro forma for Unicru Inc., (“Unicru”) acquisition in August 2006.

(2) Pro forma for deferred revenue adjustments and for Unicru acquisition in August 2006.

B. Company Overview

For the twelve months ended March 31, 2007, Kronos generated pro forma revenue(1) of $637.5 million and pro forma adjusted EBITDA(2) of $141.8 million.

Revenue (1) | Adjusted EBITDA (2) |

($ in millions) | ($ in millions) |

|

|

|

|

(1) Pro forma for deferred revenue adjustments and Unicru acquisition in August 2006.

(2) Pro forma for deferred revenue adjustments and one-time, non-recurring items; pro forma for Unicru acquisition.

2

Revenue (1) | Adjusted EBITDA (2) |

($ in millions) | ($ in millions) |

|

|

|

|

(1) 2004-LTM 3/31/07 pro forma for Unicru acquisition. 2005-LTM 3/31/07 pro forma for deferred revenue adjustments.

(2) 2005-LTM 3/31/07 pro forma for deferred revenue adjustments and one-time, non-recurring items. 2004-LTM 3/31/07 pro forma for Unicru acquisition.

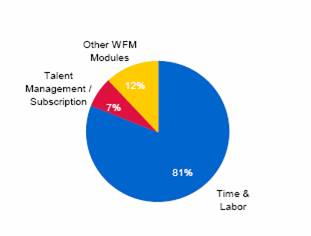

Summary of Kronos’ Software Offerings

|

| Kronos | ||||||||||||||

|

|

|

|

|

|

|

|

|

| Talent Management | ||||||

|

| Workforce Management |

| (Unicru) | ||||||||||||

|

|

|

|

|

| Absence |

| Labor Analytics/ |

| Recruiting/ | ||||||

|

| Time & Labor |

| Scheduling |

| Management |

| Activities |

| Screening | ||||||

|

|

|

|

|

|

|

|

|

|

| ||||||

PF FYE 2006 License Revenue(1) |

| · $104 million |

| · $10 million |

| · $11 million |

| · $12 million |

| · $43 million | ||||||

% of Total Software Revenue ($180 million)(2) |

| · 58% |

| · 6% |

| · 6% |

| · 6% |

| · 24% | ||||||

Description |

| · Automates the management and collection of timesheet data · Integrates with Kronos’ Time and labor hardware terminals · Serves as the platform for all other WFM add-on modules (e.g., scheduling, etc.) |

| · Plans and optimizes scheduling of staff resources · Able to forecast labor needs based on real-time info (e.g., POS data) |

| · Administers and enforces attendance policies · Manages leave time for employees |

| · Analyzes performance of labor against productivity benchmarks · Administers HR benefits, payroll, and compensation planning |

| · Allows candidates to apply for jobs online

· Evaluates applications and recommends candidates to hiring managers | ||||||

Product Names |

| · Workforce TimekeeperTM |

| · Workforce SchedulerTM

· Workforce Operation Planner TM |

| · Workforce LeaveTM · Workforce AttendanceTM · Work AccrualsTM |

| · Workforce AnalyticsTM · Workforce ActivitiesTM · VisionwareTM |

| · Workforce AcquisitionTM | ||||||

Competitive Position |

| · #1 vendor with ~60% market share in the WFM solutions market · Significant revenue opportunity from capacity additions for existing customers and upgrades |

| · Leverage existing Kronos large, installed Time & Labor customer base for cross-selling opportunities |

| · 3rd largest pure play in a fragmented market | ||||||||||

(1) Pro forma for Unicru acquisition in August 2006.

(2) Total software revenue is defined as software revenue plus Unicru revenue.

3

2006 PF FYE Revenue by Type |

| 2006 PF FYE Revenue by Industry |

($ in millions) |

|

|

|

|

|

PF FYE 9/30/06 Revenues: $619 million (1) |

| PF FYE 9/30/06 Revenues: $619 million (1) |

PF FYE 9/30/06 Revenues: $619 million (1)

(1) Pro forma for deferred revenue adjustments and for Unicru acquisition in August 2006.

C. Key Investment Considerations

The Company has achieved 10 year (1996-2006) pro forma revenue CAGR of 15.8% and pro forma adjusted EBITDA CAGR of 19.3%.

Kronos has a loyal and stable customer base comprised of multinationals, small and mid-market companies and blue chip companies. Over 50% of existing customers have been with the Company for 10+ years. The stability of the customer base is enhanced by the stickiness of the product and the high vendor switching costs. Time and labor products are usually tied to employee compensation, which creates greater customer stickiness as customers are wary of new systems and potential risk of failure. Moreover, switching vendors is both cost and resource prohibitive. It requires time to train personnel on a new software system, and there are additional expenses associated with switching hardware and software. Finally, Kronos’ suite of solutions has demonstrated quantifiable cost savings and enhanced ROI for its customers. Management estimates that these factors have led to Kronos achieving annual maintenance retention rates in excess of 90%.

4

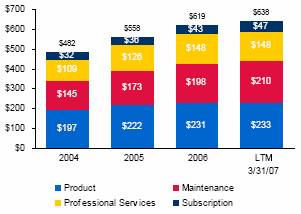

D. Historical Financial Performance

|

| Fiscal Year Ended September 30, |

| LTM |

| ||||||||

($ in millions) |

| 2004A |

| 2005A |

| 2006A |

| 3/31/2007 |

| ||||

Revenues (1) |

|

|

|

|

|

|

|

|

| ||||

Product |

| $ | 196.7 |

| $ | 221.6 |

| $ | 230.9 |

| $ | 232.3 |

|

Maintenance |

| 145.0 |

| 173.2 |

| 197.7 |

| 210.3 |

| ||||

Professional Services |

| 109.0 |

| 126.4 |

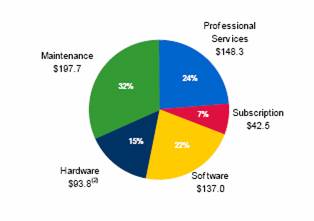

| 148.3 |

| 148.4 |

| ||||

Subscription |

| 31.6 |

| 36.3 |

| 42.5 |

| 46.5 |

| ||||

Total Revenue |

| $ | 482.3 |

| $ | 557.5 |

| $ | 619.4 |

| $ | 637.5 |

|

|

|

|

|

|

|

|

|

|

| ||||

Gross Profit (2) |

|

|

|

|

|

|

|

|

| ||||

Product |

| $ | 153.9 |

| $ | 173.6 |

| $ | 185.1 |

| $ | 187.9 |

|

Maintenance |

| 103.6 |

| 126.6 |

| 142.9 |

| 157.3 |

| ||||

Professional Services |

| 17.2 |

| 22.1 |

| 30.5 |

| 28.6 |

| ||||

Subscription |

| 12.4 |

| 24.6 |

| 28.3 |

| 18.6 |

| ||||

Total Gross Profit |

| $ | 287.1 |

| $ | 347.0 |

| $ | 386.8 |

| $ | 392.4 |

|

|

|

|

|

|

|

|

|

|

| ||||

Adjusted EBITDA (2) |

| $ | 95.0 |

| $ | 117.1 |

| $ | 136.7 |

| $ | 141.8 |

|

|

|

|

|

|

|

|

|

|

| ||||

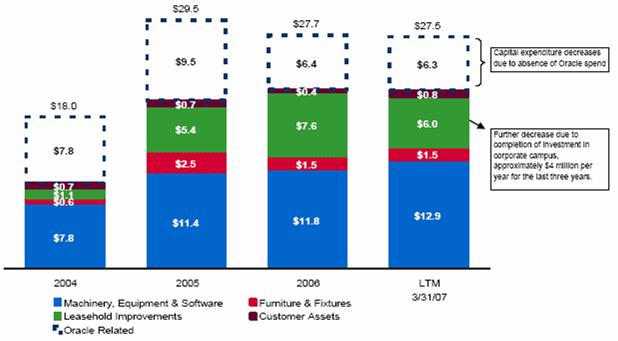

Capital Expenditures (3) |

| $ | 18.0 |

| $ | 29.5 |

| $ | 27.7 |

| $ | 27.5 |

|

|

|

|

|

|

|

|

|

|

| ||||

Capitalized Software Development Costs |

| $ | 12.8 |

| $ | 13.9 |

| $ | 13.5 |

| $ | 14.4 |

|

|

|

|

|

|

|

|

|

|

| ||||

|

|

|

|

|

|

|

|

|

| ||||

% Growth |

|

|

|

|

|

|

|

|

| ||||

Revenues |

|

|

|

|

|

|

|

|

| ||||

Product |

| — |

| 12.6 | % | 4.2 | % | — |

| ||||

Maintenance |

| — |

| 19.5 | % | 14.2 | % | — |

| ||||

Professional Services |

| — |

| 16.0 | % | 17.3 | % | — |

| ||||

Subscription |

| — |

| 14.9 | % | 17.1 | % | — |

| ||||

Total Revenue |

| — |

| 15.6 | % | 11.1 | % | — |

| ||||

|

|

|

|

|

|

|

|

|

| ||||

Adjusted EBITDA |

| — |

| 23.2 | % | 16.8 | % | — |

| ||||

|

|

|

|

|

|

|

|

|

| ||||

% Margin |

|

|

|

|

|

|

|

|

| ||||

Gross Profit |

|

|

|

|

|

|

|

|

| ||||

Product |

| 78.2 | % | 78.3 | % | 80.1 | % | 80.9 | % | ||||

Maintenance |

| 71.4 | % | 73.1 | % | 72.3 | % | 74.8 | % | ||||

Professional Services |

| 15.8 | % | 17.5 | % | 20.6 | % | 19.2 | % | ||||

Subscription |

| 39.4 | % | 67.8 | % | 66.7 | % | 40.0 | % | ||||

Total Gross Profit |

| 59.5 | % | 62.2 | % | 62.4 | % | 61.5 | % | ||||

|

|

|

|

|

|

|

|

|

| ||||

Adjusted EBITDA |

| 19.7 | % | 21.0 | % | 22.1 | % | 22.2 | % | ||||

|

|

|

|

|

|

|

|

|

| ||||

Capital Expenditures |

| 3.7 | % | 5.3 | % | 4.5 | % | 4.3 | % | ||||

|

|

|

|

|

|

|

|

|

| ||||

Capitalized Software Development Costs |

| 2.6 | % | 2.5 | % | 2.2 | % | 2.3 | % | ||||

(1) 2004-LTM 3/31/07 pro forma for Unicru acquisition. 2005-LTM 3/31/07 pro forma for deferred revenue adjustments.

(2) 2005-LTM 3/31/07 pro forma for deferred revenue adjustments and one-time, non-recurring items. 2004-LTM 3/31/07 pro forma for Unicru acquisition.

(3) 2004-LTM 3/31/07 pro forma for Unicru acquisition.

5

LTM 3/31/07 EBITDA Bridge

($ in millions)

| Fiscal Year Ended September 30, |

| LTM |

| |||||||||

($ in millions) |

| 2004A (1) |

| 2005A |

| 2006A |

| 3/31/2007 |

| ||||

Reported Revenue |

| $ | 450.7 |

| $ | 518.7 |

| $ | 578.2 |

| $ | 599.0 |

|

% Growth |

| — |

| 15.1 | % | 11.5 | % | — |

| ||||

|

|

|

|

|

|

|

|

|

| ||||

Revenue Adjustments |

|

|

|

|

|

|

|

|

| ||||

Deferred Revenue Adjustment |

| — |

| $ | 2.5 |

| $ | 5.2 |

| $ | 5.4 |

| |

Pro Forma Unicru |

| 31.6 |

| 36.3 |

| 36.0 |

| 33.1 |

| ||||

Total Adjustments |

| $ | 31.6 |

| $ | 38.8 |

| $ | 41.2 |

| $ | 38.5 |

|

|

|

|

|

|

|

|

|

|

| ||||

Adjusted Revenue |

| $ | 482.3 |

| $ | 557.5 |

| $ | 619.4 |

| $ | 637.5 |

|

% Growth |

| — |

| 15.6 | % | 11.1 | % | — |

| ||||

|

|

|

|

|

|

|

|

|

| ||||

Reported EBITDA |

| $ | 92.6 |

| $ | 109.1 |

| $ | 96.7 |

| $ | 105.3 |

|

% Margin |

| 19.2 | % | 19.6 | % | 15.6 | % | 16.5 | % | ||||

|

|

|

|

|

|

|

|

|

| ||||

EBITDA Adjustments |

|

|

|

|

|

|

|

|

| ||||

Stock Based Compensation |

| — |

| — |

| $ | 16.8 |

| $ | 17.4 |

| ||

Deferred Revenue Adjustment |

| — |

| 2.5 |

| 5.2 |

| 5.4 |

| ||||

One-Time Expenses |

| — |

| 0.1 |

| 2.5 |

| 0.7 |

| ||||

Severance Cost |

| — |

| — |

| 1.3 |

| 2.3 |

| ||||

Wage Savings |

| — |

| 0.8 |

| 8.0 |

| 7.0 |

| ||||

Pro Forma Unicru |

| (0.5 | ) | 2.0 |

| 4.1 |

| 1.6 |

| ||||

Public Company Cost Savings |

| 2.6 |

| 2.6 |

| 2.0 |

| 2.1 |

| ||||

Total Adjustments |

| $ | 94.7 |

| $ | 8.0 |

| $ | 40.0 |

| $ | 36.4 |

|

|

|

|

|

|

|

|

|

|

| ||||

Adjusted EBITDA |

| $ | 95.0 |

| $ | 117.1 |

| $ | 136.7 |

| $ | 141.8 |

|

% Margin |

| 19.7 | % | 21.0 | % | 22.1 | % | 22.2 | % | ||||

(1) 2004 not adjusted for deferred revenue adjustments and one-time, non-recurring items.

6

· Stock Based Compensation: Relates to the non-cash compensation expense that Kronos must take in accordance with FAS 123R. Kronos includes all non-cash share-based payments, including non-cash grants of stock options, restricted stock and employee stock purchase plan, in its income statement as an operating expense.

· Deferred Revenue Write-down: Corrects write-downs Kronos incurred with regard to various acquired companies. Kronos has acquired several companies in recent years and has accounted for these acquisitions using purchase accounting. As a result of purchase accounting rules, the Company has been required to write down a substantial portion of the deferred revenues attributable to these acquired companies. This add-back is meant to correct for this write-down so that EBITDA reflects an amount as if the revenue that was written down has actually been realized.

· One-time Expenses: Reflects the add-back for the custom contract losses related to contracts with Air France/KLM Royal Dutch Airline (“Air France/KLM”). The Company signed a contract with Air France/KLM to provide them with highly customized scheduling solutions. The Company provided the products and services to Air France/KLM at a loss.

· Severance Cost: Reflects the add-back of severance costs associated with the job elimination. In September 2006, Kronos restructured and realigned various business units to improve efficiency, which led to 66 position eliminations (33 in service, 26 in sales and 6 in marketing and G&A). In December 2006, the Company reduced 16 heads in its Altitude Division, a division focused on providing industry-specific solutions for the airline sector. In March 2007, the Company eliminated 45 positions in the profession services group.

· Wage Savings: Refers to wage savings arising from the Company’s restructuring and realignment initiative (see above), which took place in FYE 2006 and FYE 2007. The add-backs are taken net of any EBITDA that would have otherwise been contributed by the employees affected by the restructuring cuts. In addition, during FYE 2006, the Company eliminated the Service Account Management Program (“AMO”). The AMO program was a customer service group that interacted with clients. Kronos has reallocated the duties of this division and eliminated 26 people. The adjustments reflect the cost savings from the headcount elimination, net of any additional costs due to reallocation of services.

· Pro Forma Unicru Adjustment: Reflects the additional EBITDA the Company would have received from Unicru had it acquired the business at the beginning of the fiscal year. In reality, Kronos acquired Unicru in August 2006, during Kronos’ fiscal fourth quarter.

· Public Company Cost Savings: Reflects certain costs related to operating a public company, such as maintaining compliance with Sarbanes-Oxley and with the SEC, filing fees/dues, costs associated with investor relations and increased Directors & Officers insurance as a result of being a public company, which will no longer be incurred by the Company.

|

| Quarter Ended, |

| PF |

| Quarter Ended, |

| PF |

| ||||||||||||||||||||||

($ in millions) |

| 12/31/04 |

| 3/31/05 |

| 6/30/05 |

| 9/30/05 |

| FYE 2005 |

| 12/31/05 |

| 3/31/06 |

| 6/30/06 |

| 9/30/06 |

| FYE 2006 |

| ||||||||||

Revenues (1) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||

Product |

| $ | 53.3 |

| $ | 46.3 |

| $ | 53.4 |

| $ | 68.6 |

| $ | 221.6 |

| $ | 48.0 |

| $ | 59.0 |

| $ | 53.6 |

| $ | 69.1 |

| $ | 229.8 |

|

Services |

| 26.3 |

| 31.9 |

| 32.7 |

| 35.4 |

| 126.4 |

| 34.0 |

| 37.5 |

| 38.8 |

| 38.0 |

| 148.3 |

| ||||||||||

Subscription |

| 8.5 |

| 8.5 |

| 9.5 |

| 9.6 |

| 36.3 |

| 10.2 |

| 10.4 |

| 10.9 |

| 12.1 |

| 43.6 |

| ||||||||||

Maintenance |

| 39.5 |

| 42.8 |

| 44.7 |

| 46.3 |

| 173.2 |

| 47.6 |

| 48.3 |

| 49.9 |

| 51.9 |

| 197.7 |

| ||||||||||

Total Revenue |

| $ | 127.6 |

| $ | 129.5 |

| $ | 140.3 |

| $ | 160.0 |

| $ | 557.5 |

| $ | 139.7 |

| $ | 155.2 |

| $ | 153.3 |

| $ | 171.2 |

| $ | 619.4 |

|

% Growth |

|

|

|

|

|

|

|

|

|

|

| 9.5 | % | 19.9 | % | 9.2 | % | 7.0 | % | 11.1 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||

Gross Profit (2) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||

Product |

| $ | 41.9 |

| $ | 34.7 |

| $ | 41.6 |

| $ | 55.4 |

| $ | 173.6 |

| $ | 37.8 |

| $ | 46.5 |

| $ | 43.4 |

| $ | 57.5 |

| $ | 185.1 |

|

Services |

| 2.7 |

| 5.8 |

| 5.9 |

| 7.7 |

| 22.1 |

| 4.8 |

| 8.0 |

| 9.3 |

| 8.4 |

| 30.5 |

| ||||||||||

Subscription |

| 6.6 |

| 5.8 |

| 6.1 |

| 6.0 |

| 24.6 |

| 5.7 |

| 5.6 |

| 6.1 |

| 11.0 |

| 28.3 |

| ||||||||||

Maintenance |

| 28.4 |

| 31.8 |

| 33.5 |

| 33.0 |

| 126.6 |

| 34.3 |

| 34.5 |

| 36.3 |

| 37.7 |

| 142.9 |

| ||||||||||

Total Gross Profit |

| $ | 79.6 |

| $ | 78.0 |

| $ | 87.1 |

| $ | 102.2 |

| $ | 347.0 |

| $ | 82.7 |

| $ | 94.6 |

| $ | 95.2 |

| $ | 114.6 |

| $ | 386.8 |

|

% Growth |

|

|

|

|

|

|

|

|

|

|

| 3.9 | % | 21.3 | % | 9.3 | % | 12.1 | % | 11.5 | % | ||||||||||

% Margin |

| 62.3 | % | 60.2 | % | 62.1 | % | 63.9 | % | 62.2 | % | 59.2 | % | 61.0 | % | 62.1 | % | 66.9 | % | 62.5 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||

Adjusted EBITDA (2) |

| $ | 24.3 |

| $ | 24.8 |

| $ | 29.0 |

| $ | 38.9 |

| $ | 117.1 |

| $ | 25.5 |

| $ | 33.4 |

| $ | 33.0 |

| $ | 44.8 |

| $ | 136.7 |

|

% Margin |

| 19.1 | % | 19.2 | % | 20.7 | % | 24.3 | % | 21.0 | % | 18.3 | % | 21.5 | % | 21.5 | % | 26.2 | % | 22.1 | % | ||||||||||

(1) 2004-2006 pro forma for Unicru acquisition. 2005-2006 pro forma for deferred revenue adjustments.

(2) 2004-2006 pro forma for deferred revenue adjustments and one-time, non-recurring items; pro forma for Unicru acquisition in August 2006.

7

E. Unparalleled Track Record of Growth in Revenue and EBITDA

The Company has achieved 10 year (1996-2006) pro forma revenue CAGR of 15.8% and pro forma adjusted EBITDA CAGR of 19.3%.

($ in millions) |

| FYE 2006 REVENUE |

| IPO YEAR |

| YEARS OF |

| |

|

|

|

|

|

|

|

| |

|

| $ | 44,282 |

| 1986 |

| 25 |

|

|

|

|

|

|

|

|

| |

|

| $ | 619 | (1) | 1992 |

| 20 |

|

|

|

|

|

|

|

|

| |

|

| $ | 289 |

| 1998 |

| 16 |

|

|

|

|

|

|

|

|

| |

|

| $ | 1,254 |

| 1994 |

| 13 |

|

Source: Cap Horn Strategies, Inc. 2006

(1) Pro forma for deferred revenue adjustments and for Unicru acquisition in August 2006.

As illustrated below, the Company has achieved superior revenue and EBITDA growth over the last 10 years, with a 15.8% pro forma revenue CAGR and a 19.3% pro forma adjusted EBITDA CAGR.

Strong Revenue and EBITDA Growth

($ in millions)

% Revenue Growth |

| — |

| 19 | % | 19 | % | 26 | % | 7 | % | 9 | % | 16 | % | 16 | % | 22 | % | 16 | % | 11 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

% EBITDA Growth |

| — |

| 12 | % | 31 | % | 27 | % | (4 | %) | 13 | % | 30 | % | 24 | % | 21 | % | 18 | % | 25 | % |

Note: 2004-2006 revenue pro forma for Unicru acquisition; 2005-2006 pro forma for deferred revenue adjustments. 2005-2006 EBITDA pro forma for deferred revenue adjustments and one-time, non-recurring items; 2004-2006 pro forma for Unicru acquisition.

8

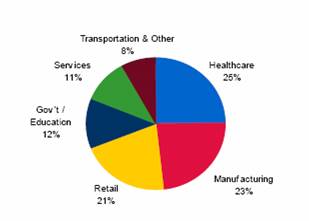

F. Diversified Revenue Base

PF FYE 9/30/06

Revenue(1) By Geography

PF FYE 9/30/06 Revenue: $619 million(1) |

(1) Pro forma for deferred revenue adjustments and for Unicru acquisition in August 2006.

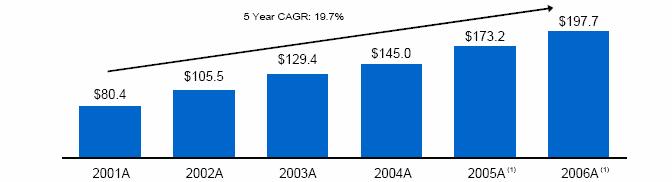

G. Strong, Recurring Revenue Base

Maintenance and Subscription Revenue

($ in millions)

% of Total Revenue (2) |

| 27 | % | 31 | % | 33 | % | 32 | % | 33 | % | 39 | % |

% Growth |

| – |

| 31 | % | 23 | % | 12 | % | 20 | % | 39 | % |

(1) Pro forma for deferred revenue adjustments.

(2) 2005-2006 pro forma for deferred revenue adjustment and one-time, non-recurring items. 2004-2006 pro forma for Unicru acquisition.

9

H. Strong Free Cash Flow

Trailing Twelve Month Unlevered Free Cash Flow

($ in millions)

% of PF Adj. EBITDA |

| 60 | % | 66 | % | 71 | % | 62 | % | 63 | % | 61 | % |

Note: Pro forma for deferred revenue adjustments and one-time, non-recurring items; pro forma for Unicru acquisition in August 2006.

Declining Capital Expenditure Requirements

($ in millions)

Note: Pro forma for Unicru acquisition in August 2006.

10

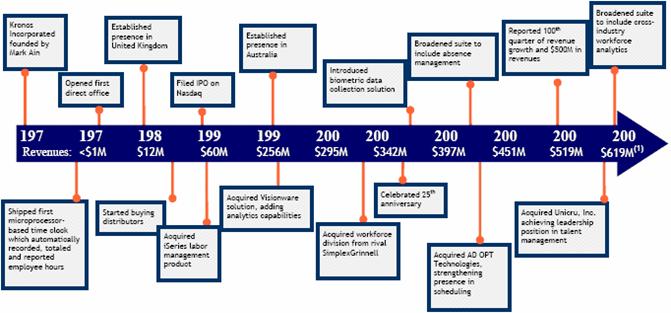

I. History

A summary of the Company’s significant milestones are as follows:

Note: Revenues are for FYE September 30.

(1) Pro forma for deferred revenue adjustments and for Unicru acquisition in August 2006.

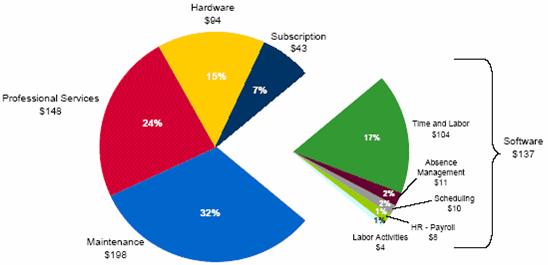

J. Products and Services

PF FYE 2006 Revenue by Type (1)

($ in millions)

(1) Pro forma for deferred revenue adjustments and for Unicru acquisition in August 2006.

11

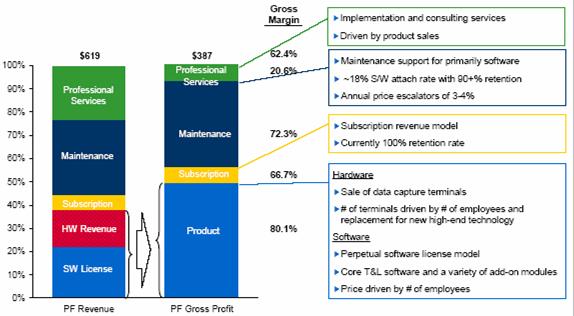

FYE 2006 Revenue and Gross Profit Streams

($ in millions)

Note: Revenue pro forma for Unicru acquisition; pro forma for deferred revenue adjustments. Gross profit pro forma for deferred revenue adjustments and one-time, non-recurring items; pro forma for Unicru acquisition.

Maintenance Revenue

($ in millions)

% of Total Revenue (2) |

| 27 | % | 31 | % | 33 | % | 32 | % | 33 | % | 32 | % |

% Growth |

| — |

| 31 | % | 23 | % | 12 | % | 20 | % | 14 | % |

(1) Pro forma for deferred revenue adjustments.

(2) 2005-2006 pro forma for deferred revenue adjustment and one-time, non-recurring items. 2004-2006 pro forma for Unicru acquisition.

12

K. Product Development

R&D Spend (1)

($ in millions)

(1) 2004-LTM 3/31/07 pro forma for Unicru R&D expense; excludes capitalized R&D costs. 2006 and LTM 3/31/07 excludes FAS 123R stock-based compensation cost allocated to R&D.

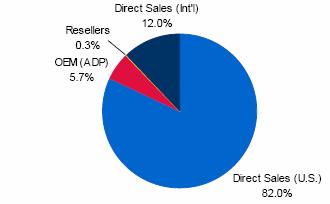

L. Sales and Marketing

FYE 2006 Sales By Channel

PF FYE 9/30/06 Revenue: $619 million (1)

(1) Pro forma for deferred revenue adjustments and for Unicru acquisition in August 2006.

13

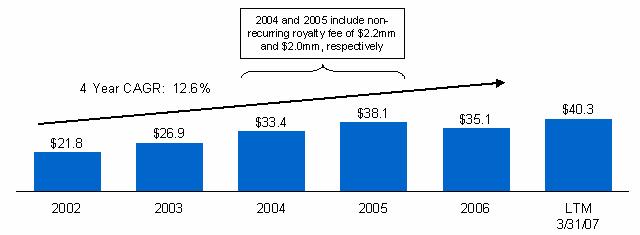

Revenue From ADP

($ in millions)

M. Growth Strategy

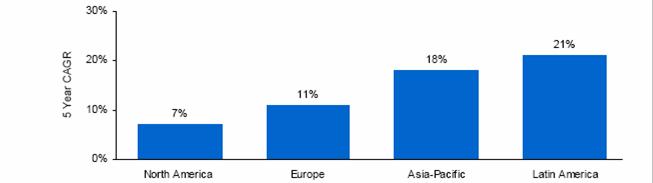

Kronos% of PF FYE 2006 Revenues (1) |

| 93% |

| 3% |

| 3% |

| 1% |

|

|

|

|

|

|

|

|

|

Competitive Position: |

| · Established market leader · Strong direct sales force · Established presence in Canada & Mexico |

| · #1 Provider in the UK · Valuating opportunities in continental Europe |

| · #1 Provider in Australia · Recently established presence in China and Singapore · Beginning to establish presence in India |

| · Sales via partners / distributors · Long-term focus market |

Source: AMR Research

(1) Pro forma for deferred revenue adjustments and for Unicru acquisition in August 2006.

14

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

| KRONOS INCORPORATED | |||

|

|

| ||

|

|

| ||

Date: May 15, 2007 | By: | /s/ Mark V. Julien | ||

| Name: | Mark V. Julien | ||

| Title: | Chief Financial Officer | ||

15