Free Writing Prospectus pursuant to Rule 433 dated June 24, 2024

Registration Statement No. 333-269296

loac

| Market Linked Securities — Autocallable with Contingent Coupon with Memory Feature and Contingent Downside Principal at Risk Securities Linked to an ordinary share of monday.com Ltd. due July 1, 2027 |

Summary of Terms |

| Underwriting discount: | up to 2.325% of the face amount*; Wells Fargo Securities, LLC (“WFS”) is the agent for the distribution of the securities. WFS will receive the underwriting discount of up to 2.325% of the aggregate face amount of the securities sold. The agent may resell the securities to Wells Fargo Advisors (“WFA”) at the original issue price of the securities less a concession of 1.75% of the aggregate face amount of the securities. In addition to the selling concession received by WFA, WFS advises that WFA may also receive out of the underwriting discount a distribution expense fee of 0.075% for each $1,000 face amount of a security WFA sells. | |

Company (Issuer) and Guarantor: | GS Finance Corp. (issuer) and The Goldman Sachs Group, Inc. (guarantor) |

| ||

Market Measure (the “underlying stock”): | an ordinary share of monday.com Ltd. (current Bloomberg ticker: “MNDY UW”) |

| ||

Pricing date: | expected to be June 28, 2024 |

| ||

Issue date: | expected to be July 3, 2024 |

| ||

Final calculation day: | expected to be June 28, 2027 |

| ||

Stated maturity date: | expected to be July 1, 2027 |

| ||

Starting price: | the stock closing price of the underlying stock on the pricing date |

| ||

Ending price: | the stock closing price of the underlying stock on the final calculation day |

| ||

Performance factor: | the ending price divided by the starting price (expressed as a percentage) |

| CUSIP: | 40058AXJ8 |

Automatic call: | If the stock closing price of the underlying stock on any call date is greater than or equal to the starting price, the securities will be automatically called, and on the related call settlement date you will be entitled to receive a cash payment per security in U.S. dollars equal to the face amount plus a final contingent coupon payment and any previously unpaid contingent coupon payments. The securities will not be subject to automatic call until the September 2024 calculation day. |

| Tax consequences: | See “Supplemental Discussion of U.S. Federal Income Tax Considerations” in the accompanying preliminary pricing supplement |

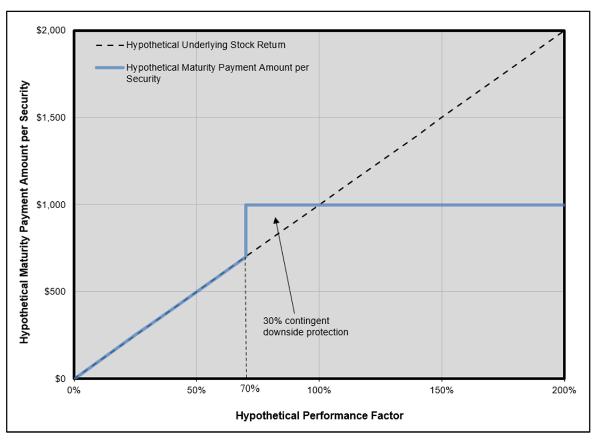

| * In addition, in respect of certain securities sold in this offering, GS&Co. may pay a fee of up to 0.35% of the aggregate face amount of the securities sold to selected securities dealers in consideration for marketing and other services in connection with the distribution of the securities to other securities dealers. Hypothetical Payout Profile (Maturity Payment Amount)

If the securities are not automatically called prior to stated maturity and the ending price is less than the downside threshold price, you will lose more than 30%, and possibly all, of the face amount of your securities at stated maturity. Any return on the securities will be limited to the sum of your contingent coupon payments, if any. You will not participate in any appreciation of the underlying stock, but you will have full downside exposure to the underlying stock if the ending price is less than the downside threshold price. You should read the accompanying preliminary pricing supplement dated June 24, 2024, which we refer to herein as the accompanying preliminary pricing supplement, to better understand the terms and risks of your investment, including the credit risk of GS Finance Corp. and The Goldman Sachs Group, Inc. The securities are part of the Medium-Term Notes, Series F program of GS Finance Corp. and are fully and unconditionally guaranteed by The Goldman Sachs Group, Inc. This document should be read in conjunction with the following:

The estimated value of your securities at the time the terms of your securities are set on the pricing is expected to be between $925 and $955 per $1,000 face amount. See the accompanying preliminary pricing supplement for a further discussion of the estimated value of your securities. | |||

| ||||

Downside threshold price: | 70% of the starting price |

| ||

Contingent coupon payment: | Subject to the automatic call, on each contingent coupon payment date, for each $1,000 of the outstanding face amount, you will receive a contingent coupon payment equal to at least $44.00 (equivalent to a contingent coupon rate of at least 17.60% per annum) (set on the pricing date) if, and only if, the stock closing price of the underlying stock on the related calculation day is greater than or equal to the coupon threshold price. In addition, if the stock closing price of the underlying stock on one or more calculation days is less than the coupon threshold price and, on a subsequent calculation day, the stock closing price of the underlying stock is greater than or equal to the coupon threshold price, on the contingent coupon payment date related to such subsequent calculation day you will receive the contingent coupon payment due for that subsequent calculation day plus all previously unpaid contingent coupon payments (without interest on amounts previously unpaid) |

| ||

Coupon threshold price: | 70% of the starting price |

| ||

Call dates: | each calculation day commencing in September 2024 and ending in March 2027 |

| ||

Call settlement date: | the contingent coupon payment date immediately following the applicable call date |

| ||

Calculation days: | quarterly, on the 28th day of each March, June, September and December, commencing in September 2024 and ending in March 2027, and the final calculation day |

| ||

Contingent coupon payment dates: | quarterly, on the third business day following each calculation day; provided that the contingent coupon payment date with respect to the final calculation day will be the stated maturity date |

| ||

Maturity payment amount (for each $1,000 face amount of your securities): | • if the ending price is greater than or equal to the downside threshold price: $1,000; or • if the ending price is less than the downside threshold price: $1,000 × performance factor |

| ||

|

|

| ||

|

|

| ||

|

|

| ||

The securities have more complex features than conventional debt securities and involve risks not associated with conventional debt securities. See “Risk Factors” in this term sheet and in the accompanying preliminary pricing supplement. This document does not provide all of the information that an investor should consider prior to making an investment decision. You should not invest in the securities without reading the accompanying preliminary pricing supplement and related documents for a more detailed description of the underlying stock, the terms of the securities and certain risks. |

About Your Securities |

GS Finance Corp. and The Goldman Sachs Group, Inc. have filed a registration statement (including a prospectus, as supplemented by the prospectus supplement, WFS product supplement no. 3 and preliminary pricing supplement listed below) with the Securities and Exchange Commission (SEC) for the offering to which this communication relates. Before you invest, you should read the prospectus, prospectus supplement, WFS product supplement no. 3 and preliminary pricing supplement, and any other documents relating to this offering that GS Finance Corp. and The Goldman Sachs Group, Inc. have filed with the SEC for more complete information about us and this offering. You may get these documents without cost by visiting EDGAR on the SEC web site at sec.gov. Alternatively, we will arrange to send you the prospectus, prospectus supplement, WFS product supplement no. 3 and preliminary pricing supplement if you so request by calling (212) 357-4612.

Risk Factors |

An investment in the securities is subject to risks. Many of the risks are described in the accompanying preliminary pricing supplement, accompanying WFS product supplement no. 3, accompanying prospectus supplement and accompanying prospectus. Below we have provided a list of risk factors discussed in the accompanying preliminary pricing supplement (but not those discussed in the accompanying WFS product supplement no. 3, accompanying prospectus supplement and accompanying prospectus). In addition to the below, you should read in full “Selected Risk Considerations” in the accompanying preliminary pricing supplement, “Risk Factors” in the accompanying WFS product supplement no. 3, as well as the risks and considerations described in the accompanying prospectus supplement and accompanying prospectus.

The following risk factors are discussed in greater detail in the accompanying preliminary pricing supplement:

Risks Related to Structure, Valuation and Secondary Market Sales ▪ The Estimated Value of Your Securities At the Time the Terms of Your Securities Are Set On the Pricing Date (as Determined By Reference to Pricing Models Used By GS&Co.) Is Less Than the Original Offering Price Of Your Securities ▪ The Securities Are Subject to the Credit Risk of the Issuer and the Guarantor ▪ You May Lose Your Entire Investment in the Securities ▪ The Return on Your Securities May Change Significantly Despite Only a Small Change in the Price of the Underlying Stock ▪ You May Not Receive a Contingent Coupon on Any Contingent Coupon Payment Date ▪ A Higher Contingent Coupon, a Lower Coupon Threshold Price and/or a Lower Downside Threshold Price May Reflect Greater Expected Volatility of the Underlying Stock, and Greater Expected Volatility Generally Indicates An Increased Risk of Declines in the Price of the Underlying Stock and, Potentially, a Significant Loss at Maturity ▪ Your Securities Are Subject to Automatic Redemption ▪ The Contingent Coupon Does Not Reflect the Actual |

| Performance of the Underlying Stock from the Pricing Date to Any Calculation Day or from Calculation Day to Calculation Day ▪ The Market Value of Your Securities May Be Influenced by Many Unpredictable Factors ▪ We Will Not Hold Shares of the Underlying Stock for Your Benefit ▪ You Have No Shareholder Rights or Rights to Receive the Underlying Stock Additional Risks Related to the Underlying Stock ▪ The Underlying Stock Has a Very Limited Trading History

Risks Related to Tax ▪ Certain Considerations for Insurance Companies and Employee Benefit Plans ▪ The Tax Consequences of an Investment in Your Securities Are Uncertain ▪ Foreign Account Tax Compliance Act (FATCA) Withholding May Apply to Payments on Your Securities, Including as a Result of the Failure of the Bank or Broker Through Which You Hold the Securities to Provide Information to Tax Authorities |

Wells Fargo Advisors is a trade name used by Wells Fargo Clearing Services, LLC and Wells Fargo Advisors Financial Network, LLC, members SIPC, separate registered broker-dealers and non-bank affiliates of Wells Fargo & Company.

This document does not provide all of the information that an investor should consider prior to making an investment decision. You should not invest in the securities without reading the accompanying preliminary pricing supplement and related documents for a more detailed description of the underlying stock, the terms of the securities and certain risks.

2