UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2012

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number: 000-20201

HAMPSHIRE GROUP, LIMITED

(Exact name of registrant as specified in its charter)

| Delaware | 06-0967107 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| | |

| 114 W. 41st Street, New York, New York | 10036 |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: (212) 840-5666

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act:

(Title of Class)

Common Stock, $0.10 par value

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted to its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to file such reports). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| | Large accelerated filer ¨ | Accelerated filer ¨ |

| | Non-accelerated filer ¨ | Smaller Reporting Company x |

| | (Do not check if Smaller Reporting Company) | |

Indicate by check mark whether registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

As of June 30, 2012, the aggregate market value of the voting and non-voting Common Stock held by non-affiliates of the registrant was $15,209,466. Such aggregate market value was computed by reference to the closing sale price of the Common Stock as reported on the OTC Markets, a centralized quotation service that collects and publishes market maker quotes for over-the-counter securities, on such date. For purposes of making this calculation only, the Registrant has defined “affiliates” as including all directors and executive officers, but excluding any institutional stockholders owning more than ten percent of the Registrant’s Common Stock.

Number of shares of Common Stock outstanding as of March 2, 2013: 7,472,457

DOCUMENTS INCORPORATED BY REFERENCE

Certain portions of the Registrant’s Definitive Proxy Statement, relative to our 2013 Annual Meeting of Stockholders to be filed with the Securities and Exchange Commission not later than 120 days after the end of the fiscal year, are incorporated by reference into Part III of this Annual Report on Form 10-K.

HAMPSHIRE GROUP, LIMITED

ANNUAL REPORT ON FORM 10-K

For the Fiscal Year Ended December 31, 2012

| "SAFE HARBOR” STATEMENT | ii |

PART I. | | 1 |

| Item 1. | Business | 1 |

| Item 1A. | Risk Factors | 6 |

| Item 1B. | Unresolved Staff Comments | 11 |

| Item 2. | Properties | 11 |

| Item 3. | Legal Proceedings | 12 |

| Item 4. | Mine Safety Disclosures | 12 |

PART II. | | 13 |

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 13 |

| Item 6. | Selected Financial Data. | 14 |

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 15 |

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 25 |

| Item 8. | Financial Statements and Supplementary Data | 26 |

| Item 9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | 56 |

| Item 9A. | Controls and Procedures | 56 |

| Item 9B. | Other Information | 56 |

PART III. | | 57 |

| Item 10. | Directors, Executive Officers and Corporate Governance | 57 |

| Item 11. | Executive Compensation | 57 |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 57 |

| Item 13. | Certain Relationships and Related Transactions and Director Independence | 57 |

| Item 14. | Principal Accounting Fees and Services | 57 |

| PART IV. | | 58 |

| Item 15. | Exhibits, Financial Statement Schedules | 58 |

“SAFE HARBOR” STATEMENT

UNDER THE PRIVATE SECURITIES LITIGATION REFORM ACT OF 1995

From time to time, we make oral and written statements that may constitute “forward looking statements” (rather than historical facts) as defined in the Private Securities Litigation Reform Act of 1995 or by the Securities and Exchange Commission (the “SEC”) in its rules, regulations and releases, including Section 27A of the Securities Act of 1933, as amended (the “Securities Act”) and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). We desire to take advantage of the “safe harbor” provisions in the Private Securities Litigation Reform Act of 1995 for forward looking statements made from time to time, including, but not limited to, the forward looking statements made in this Annual Report on Form 10-K (the “Annual Report”), as well as those made in other filings with the SEC.

Forward looking statements can be identified by our use of forward looking terminology such as “may,” “will,” “expect,” “anticipate,” “estimate,” “believe,” “continue,” “forecast,” “foresee” or other similar words. Such forward looking statements are based on our management’s current plans and expectations and are subject to risks, uncertainties and changes in plans that could cause actual results to differ materially from those described in the forward looking statements. Important factors that could cause actual results to differ materially from those anticipated in our forward looking statements include, but are not limited to, those described under “Risk Factors” set forth in Item 1A of this Annual Report.

We expressly disclaim any obligation to release publicly any updates or any changes in our expectations or any changes in events, conditions or circumstances on which any forward-looking statement is based.

As used herein, except as otherwise indicated by the context, the terms “Hampshire,” “Company,” “we” and “us” are used to refer to Hampshire Group, Limited and our wholly-owned subsidiaries.

ii

PART I.

Item 1. Business.

Company Overview

General

Hampshire Group, Limited is a provider of fashion apparel across a broad range of product categories, channels of distribution and price points. As a holding company, we operate through our wholly-owned subsidiaries, Hampshire Brands, Inc., Rio Garment S.A. and scott james, LLC. We were established in 1976 and are incorporated in the state of Delaware.

Hampshire Brands designs and markets men’s sportswear to department stores, chain stores and mass market retailers under licensed brands, our own proprietary brands and the private labels of our customers. Among others, we offer a full tops assortment under the Dockers® brand and a t-shirt and board short assortment under the Panama Jack® brand, both of which are licensed, as well as private label t-shirt and sweater offerings to retailers under their private labels.

The scott james® brand is a designer apparel collection for men, which includes a full sportswear offering. It is sold primarily through upscale department and specialty stores, scott james® retail shops and online at www.scottjamesonline.com.

Rio Garment S.A. (“Rio”), acquired August 25, 2011, is a Honduras-based apparel manufacturer, designing, sourcing and manufacturing knit tops for men, women and children, which are sold to retailers and distributors, primarily in the United States. Rio’s manufacturing platform primarily supports the vertical specialty store channel. Our manufacturing operations begin with the purchase of fabric and other raw materials from third party suppliers. The fabrics are ultimately sewn into finished garments at our textile facility or at the facilities of third party contractors located in Honduras. Rio also purchases yarn and outsources fabric production to third parties, where upon completion, the fabric returns to the Rio facility for production. Our garments may also be embellished and prepared for retail (with any combination of services, including ticketing, hang tags and hangers).

Recent Initiatives

The economic environment over the past several years has been challenging and has been characterized by, among other things, restrained consumer spending, weak credit market conditions and inflationary pressures on our cost of goods. In an effort to preserve gross margin dollars in the face of rising costs of goods and stagnant out the door prices, during the past two years we have taken significant steps to reposition our Company for growth and profitability, including:

| ▪ | Disposition of the women’s businesses. In May 2011, we announced a significant shift in our growth strategy with the disposition of our underperforming women’s businesses. The disposition of these businesses allowed us to focus on leveraging our operating platform in the men’s business and actively pursue other strategic opportunities. On May 5, 2011, in connection with this new strategic direction, we sold our women’s businesses, Hampshire Designers and Item-Eyes, in two separate transactions for a total purchase price of $12.3 million plus inventory before consideration of certain transaction costs and assets and liabilities that were not sold. |

| ▪ | Integration of Rio. On August 25, 2011, we reached a significant milestone with the acquisition of Rio. Rio has provided us an opportunity to grow our core business into the fast-growing vertical specialty store channel and has allowed us to leverage our existing operating platforms to expand Rio’s business into the department and chain store channels. Rio has the ability to produce for a variety of apparel categories including performance and fashion. Since completing the acquisition we have augmented Rio’s infrastructure in place to support growth. We are realizing the benefits of our strategy for Rio as we continue to develop a more robust product offering, grow its capacity within its current physical footprint and improve the efficiency of its operations. |

| ▪ | Added Dockers® and Panama Jack® licenses while phasing out legacy licenses with declining sales. We entered into a multi-year licensing agreement with Dockers® for its men’s “good” category tops in the United States. As part of this agreement, we oversee the design, production, sales and distribution of the line, to certain chain and department stores including Kohl’s Department Stores, Inc., J.C. Penney Company, Inc. and Sears Holding Corporation. The woven and knit line includes button down shirts, polos, fleece tops and t-shirts. We believe that these additional categories complement and strengthen the marketability of our Dockers® sweater offering and, taken together, help to ensure we have a compelling international brand to offer to retailers. We also entered into a licensing agreement with Panama Jack® to provide a new line of lifestyle apparel for men, including a full tops and board short assortment. The Dockers® and Panama Jack® licenses are well-recognized growing brands that have allowed us to phase out legacy licenses with declining sales. |

| ▪ | Broadening and diversifying our customer base. We remain focused on exploring opportunities to grow our sales and expand our retail relationships. We continued through 2012 to build brand recognition and market presence, as demonstrated by a new customer relationship with Bloomingdale’s. Further, we have begun new customer relationships with Wal-Mart and Kmart through our Panama Jack business. |

| ▪ | Restructuring and cost savings plan. In 2012, we implemented a cost savings plan, primarily through workforce reduction, that has allowed us to operate our business more efficiently and reduce costs. |

| ▪ | Reorganization plan. On January 15, 2013 Heath L. Golden resigned as chief executive officer of the Company. At the time of the resignation the Board of Directors of the Company (the “Board”) appointed Paul Buxbaum to serve as the Company’s new chief executive officer. Additionally, on January 28, 2013, the Company entered into an agreement with Buxbaum Group to provide certain restructuring and advisory consulting services. Pursuant to the agreement, Buxbaum Group is tasked with providing specific recommendations to the Board concerning the organization, operations and expenses to better support the Company’s business model and sales levels. Additionally, under the agreement Buxbaum Group is responsible for the implementation of such recommendations to the extent adopted by the Board. |

Our ProductsWe have continued to enhance and diversify our product lines in 2012. Our expanded product line and capabilities through the acquisition of Rio and development of scott james® permit us to supply many more departments of our existing customers and helps us attract new customers.

The emphasis with every garment we offer is a compelling product that features high quality and good value. The recent diversification and expansion of our product offerings allows us to participate in a range of retail price points from "main floor" traditional styles to fashion forward designer styles.

Our Strengths

We believe that we occupy a strong competitive position in a consolidating industry. We plan to further solidify our position through:

Business Focus. We continually review our portfolio of labels, business lines and divisions to evaluate whether they meet profitability and performance requirements and are in line with our business focus. During 2012, we expanded the product categories under our Dockers® license and entered into a Panama Jack® license. In 2011, we discontinued and sold the women’s businesses and acquired Rio.

Solid Infrastructure. We are recognized by leading retailers for our compelling product design, high quality value proposition, sourcing expertise and commitment to customer service. Our international sourcing abilities permit us to deliver trend right, quality product to each of the tiers of distribution we supply, which are primarily located within the United States. The quality of our garments is assured in a variety of ways. Each garment is manufactured using fine quality yarns and undergoes rigorous quality assurance checks. We utilize our own personnel, as well as factory personnel, independent inspection agencies and independent test labs to ensure that our products meet the high quality standards required for our brands. Extensive and Diverse Retail Relationships. Our relationships with major retailers range from national and regional department stores such as Macy’s, Inc. and Belk, Inc., to upscale department stores such as Bloomingdale’s, to national chain stores such as J.C. Penney Company, Inc. and Kohl’s Department Stores, Inc., to vertical specialty stores such as Aeropostale, Inc., to off-price retailers such as TJ Maxx, a division of The TJX Companies, Inc., and Ross Stores, Inc. These relationships enable our products to reach a large consumer base both in number and in geographical area.

Our Strategy

Hampshire’s strategies for the future include leveraging our:

Experienced Design and Sourcing Capabilities. We have and continue to invest in high quality design talent and resources. Our investments are aimed at further strengthening our design and sourcing efficiencies to ensure our brands fulfill the demand for high quality, value and trend right product.

Strong Competitive Position. As our retail customers seek to differentiate their assortments from competitors, they are increasingly turning to select designer and exclusive labels. We have demonstrated our value to retailers by offering such well known licensed brands as Dockers® and Panama Jack® lines. In addition, we are continuing to develop our owned scott james® brand. Also, Rio provides dependable and optimal pricing for the vertical specialty store customers. As we continue to integrate Rio into our business, we believe that we can benefit from considerable cross-selling opportunities and that our acquisition of Rio positions us well with respect to the strong industry trend toward migrating production to the western hemisphere.

Constant Improvement of our Infrastructure. As efficient systems and technologies are critical to meeting our retail customers’ needs, we are constantly re-evaluating our infrastructure to obtain additional synergies and efficiencies. During 2012 we were able to successfully integrate Rio onto certain reporting and operating platforms. Also, the Company is in the process of implementing a state-of-the-art production and planning system that will further enhance and improve Rio’s operating capabilities.

Growth Opportunities in Existing and New Channels. We are focused both on growing our sales to retailers in the moderate department and chain store channel, as well as actively exploring new sales channels including international, vertical specialty stores and direct-to-consumer. Our efforts with scott james® and Rio have been critical to achieving growth in this respect.

Organization

We have a long history of supplying men's branded and private label apparel to the department stores and national chains throughout the United States. We utilize our own sales force and contract third party salespersons to sell our products. With our established international sourcing relationships, we have the ability to respond quickly to changing fashion trends. Our acquisition of Rio has allowed us to continue to build upon our product diversification, sales force and agility within the apparel industry.

Customers

We have long term relationships with many of our customers. Hampshire Brands sells products principally into the moderate price sector of most major department and chain stores in the United States. scott james® sells products primarily to upscale specialty stores. Rio sells primarily to the vertical specialty store channel. Sales to our three largest customers in 2012, Aeropostale, Kohl's Department Stores, Inc. and J.C. Penney Company, Inc. represented 52%, 14% and 12%, respectively, of total annual sales. These same three customers represented 30%, 16% and 28%, respectively, of total sales during 2011. The growth in sales from Aeropostale from 2011 to 2012 was primarily due to a full year of sales in 2012 as compared to 2011 as Rio was acquired on August 25, 2011 and represents sales from that date forward. For each of the last two years, more than 99% of our sales from continuing operations were to customers located in the United States.

Suppliers

Hampshire Brands and scott james® primarily use foreign suppliers for their raw materials and product manufacturing. During 2012, the majority of our products were produced by independent manufacturers located in Southeast Asia. Keynote Services, Limited, our subsidiary based in China, assists with our sourcing needs and provides quality control. Rio primarily purchases raw materials, including yarn and fabric, from suppliers in the United States. Fabric is also purchased locally in Honduras. Purchased fabric is used in the manufacturing process at our facility located in Honduras. We outsource the fabric production to third party manufacturers.

Competition

The apparel market remains highly competitive. Competition is primarily based on design, price, quality and service. While we face competition from domestic manufacturers and distributors, our primary competition comes from private label programs of the internal sourcing organizations of many of our customers and factories located in Southeast Asia.

Our ability to compete is enhanced by our in-house design capabilities and our international sourcing relationships. Our launches of both Dockers® and Panama Jack® in additional categories and of scott james®, as well as the acquisition of Rio are the most recent examples of our ongoing efforts to deploy our financial resources in a manner that helps develop a competitive advantage by broadening our apparel offerings and product lines to reach multiple tiers of distribution.

Seasonality

In the past our business was highly seasonal as a result of our product mix including a high concentration of sweaters. Although not as significant as in prior years, our business continues to maintain a fairly high degree of seasonality with approximately 65% of our sales during 2012 occurring in the third and fourth quarters. As a result of such seasonality, inventory begins to rise in the second quarter and typically peaks during the third quarter before descending to its cyclical low in the fourth quarter. Trade receivable balances rise commensurately with sales. Cash balances follow this cycle as inventory is purchased, product is sold, and trade receivables are collected. Funding inventory and pending trade receivable collections deplete cash balances and may require draws from our revolving credit facility in the third or fourth quarters. Our income or loss from continuing operations has generally been correlated with revenue, as a large percentage of our profits have historically been generated in the third and fourth fiscal quarters.

Seasonality in 2012 declined largely as a result of Rio’s more even distribution of sales throughout the year as compared to our other subsidiaries. In 2013 and beyond, we expect this seasonality to decline further as a result of the Dockers® and Panama Jack® licenses which we believe will increase our sales during the spring season.

Rio’s manufacturing platform primarily supports the vertical specialty store channel. Our manufacturing operations begin with the purchase of fabric and other raw materials from third party suppliers. The fabrics are ultimately sewn into finished garments at our textile facility or at third party contractors located in Honduras. Rio also purchases yarn and outsources fabric production to third parties, where upon completion, the fabric returns to the Rio facility for production. Our garments may also be embellished and prepared for retail (with any combination of services, including ticketing, hang tags and hangers). For a description of risks associated with our operations located outside the United States, see Item 1A. Risk Factors.

Effects of Changing Prices

We are subject to increased prices for the products we source. We have historically managed our gross margin by achieving sourcing efficiencies, controlling costs in other parts of our operation and, when appropriate, passing along a portion of our cost increases to our customers through higher selling prices. We confront inflationary pressures in transportation costs, labor and materials.

Backlog

Our sales order backlog as of March 2, 2013 was approximately $71.5 million compared to approximately $67.7 million as of March 2, 2012. The sales order backlog as of March 2, 2012 included $20.4 million of orders related to license agreements that expired in 2012. The timing of the placement of seasonal orders by customers affects the backlog; accordingly, a comparison of backlog from year to year is not necessarily indicative of a trend in sales for the year. The backlog as of March 2, 2013 is expected to be filled during 2013.

Trademarks and Licenses

We consider our owned trademarks to have significant value in the marketing of our products. In addition, we have entered into licensing agreements to manufacture and market apparel under certain labels for which we pay royalties based on the volume of sales. The licensing agreements are generally for three year terms. We do not own any patents.

Electronic Information Systems

In order to schedule production, fill customer orders, transmit shipment data to our customers' distribution centers and invoice electronically, we have developed a number of integrated electronic information systems applications. Approximately 40% of our customer orders for 2012 were received electronically. In some instances, our customers' computer systems generate these orders based on sales and inventory levels. We electronically send advance shipment notices and invoices to our customers, which result in the timely update of their inventory levels.

Credit and Collection

We manage our credit and collection functions by approving and monitoring our customers' credit limits. Credit limits are determined by past payment history and financial information obtained from credit agencies and other sources. The majority of high risk accounts are factored without recourse, if possible, with financial institutions to reduce our credit risk exposure. We believe that our review procedures and our credit and collection staff have contributed significantly toward minimizing our losses from bad debt.

Governmental Regulation and Trade Agreements

The apparel industry and our business are subject to a wide variety of international trade agreements as well as federal, state and local regulations. We believe we are in compliance in all material respects with these agreements and regulations.

International trade agreements in particular can have a significant impact on the apparel industry and consequently on our business. These agreements generally provide for tariffs, which impose a duty charge on the product being imported, and quotas, which limit the amount of a product that may be imported from a specific country, both of which increase the cost of importing a product.

Primary among the trade agreements existing between the United States and certain foreign countries is the World Trade Organization (“WTO”), which is the governing body for international trade among the 151 originating member countries, including the United States. Effective January 1, 2005, all such quota restrictions involving trade with WTO member countries were terminated. In addition to the WTO, apparel imports into the United States are affected by other trade agreements and legislation, including the Dominican Republic – Central American Free Trade Agreement and the North American Free Trade Agreement, which has eliminated all apparel tariffs and quotas between the member countries and legislation granting similar trade benefits to 23 Caribbean countries. Further, Congress passed the African Growth and Opportunity Act in 2000, which gave 38 countries in sub-Saharan Africa similar trade privileges on apparel and certain other products exported to the United States.

Rio is authorized to operate under the Honduran Free Trade Zone Regime (“FTZ”). Therefore, Rio qualifies for exemption from Honduran customs duties, charges and surcharges, internal consumption, production sales tax and other excise taxes on imported and exported goods. Rio is also exempt from municipal taxes, asset taxes and income taxes, provided that Rio does not benefit from income tax exemption granted in another country. In order to maintain the FTZ exemption, Rio must export at least 95% of its annual production. Rio currently exports 99% of its production.

Compliance with Environmental Laws

We believe that we are in compliance with applicable environmental laws and that such compliance will not have a major adverse financial impact on us. We further believe that there are no environmental matters that are likely to have a significant financial impact on us. There can be no assurance, however, that future changes in federal, state or local regulations, interpretations of existing regulations or the discovery of currently unknown problems or conditions will not require substantial additional expenditures. Similarly, while we are not currently aware of any violations, the extent of our liability, if any, for past failures to comply with laws, regulations and permits applicable to our operations cannot be determined and could have a material adverse effect on our operations, financial condition or liquidity.

Employees

As of March 2, 2013, we employed approximately 979 full-time employees in Honduras, 76 full-time employees in the United States and 18 full-time employees in China. We believe our relationship with our employees is good. We have invested significant time and resources in ensuring that the working conditions in our Honduras facility meet or exceed the standards imposed by the relevant governing laws. In addition, we have proactive programs to promote workplace safety, personal health and employee wellness.

Available Information

Our periodic and current reports, including amendments to such reports as filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, are available, free of charge, on our website, www.hamp.com, as soon as reasonably practicable after such material is electronically filed with, or furnished to, the SEC. Information contained on our website is not and should not be deemed a part of this Annual Report or a part of any other report or filing with the SEC.

Item 1A. Risk Factors.

In addition to the risks that are described below, there may be risks that we do not yet know of or that we currently think are immaterial that may also impair our business. If any of the events or circumstances described as risks below or elsewhere in this report actually occur, our business, results of operations or financial condition could be materially and adversely affected. The following risks, as well as other information contained herein, including our consolidated financial statements and notes thereto, should be carefully considered in evaluating our business and any investment in our common stock.

The apparel industry is heavily influenced by general economic cycles that affect consumer spending. A prolonged period of depressed consumer spending would have a material adverse effect on us.

The apparel industry has historically been subject to cyclical variations, recessions in the general economy and uncertainties regarding future economic prospects that affect consumer spending habits, which could negatively impact our business. The success of our operations depends on a number of factors impacting discretionary consumer spending, including general economic conditions, consumer confidence, wages and unemployment, housing prices, consumer debt, interest rates, fuel and energy costs, taxation and political conditions. A downturn in the economy may affect consumer purchases of our products and adversely impact our growth and profitability.

We use foreign suppliers for our raw materials and the manufacture of products for our men’s division and our operations include a manufacturing facility based in Honduras, which poses risks to our business operations.

During 2012, the majority of our production took place in Honduras, and a significant portion of our products were also produced by independent manufacturers located outside the United States. Although no single supplier is critical to our production needs, any of the following could adversely affect the production and delivery of our products and, as a result, have an adverse effect on our business, financial condition and results of operations:

| · | political or labor instability in countries where contractors and suppliers are located; |

| · | political or military conflict involving the United States; |

| · | heightened terrorism security concerns, which could subject imported goods to additional, more frequent or more thorough inspections, leading to delays in deliveries or impoundment of goods for extended periods; |

| · | a significant decrease in availability or increase in cost of labor or raw materials, particularly in petroleum based synthetic fabrics; |

| · | impact of the global economic downturn on third party factories and their viability; |

| · | disease epidemics and health related concerns which could result in closed factories, reduced workforces and scrutiny or embargo of goods produced in infected areas; |

| · | imposition of regulations, quotas or duties relating to imports, which, among other things, could limit our ability to produce products in cost effective countries that have the labor force and expertise required; |

| · | any action that may change the foreign currency exchange rate against the dollar or permit the exchange rate to float; and |

| · | significant fluctuation of the value of the dollar as compared to other foreign currencies. |

The occurrence of any, some, or all of these events could have a material adverse impact on our business, operating results and financial condition. There can be no assurance that if a disruption occurred we could replace our manufacturing capacity and/or find other manufacturing resources.

There may not be an established public trading market for the Company’s common stock.

There is currently no established public trading market for our common stock. Our common stock is currently quoted on the OTC Markets (formerly known as “Pink Sheets”) under the symbol “HAMP”. The OTC Markets is a centralized quotation service that collects and publishes market maker quotes for over-the-counter securities in real time. Over-the-counter market quotations, like those on the OTC Markets, reflect inter-dealer prices, without retail mark-up, mark-down or commission and may not necessarily represent actual transactions. Currently, we are not actively seeking to become listed on the Nasdaq Global Market or any other exchange. There can be no assurance that our common stock will again be listed on a national exchange, or that a trading market for our common stock will be established.

We rely on our key customers, and a significant decrease in business from or the loss of any one of these key customers would substantially reduce our revenues and adversely affect our business.

Aeropostale, Kohl’s Department Stores, Inc. and J.C. Penney Company Inc. account for a significant portion of our revenues. We do not have long term agreements with any of our customers and purchases generally occur on an order by order basis. A decision by any of our major customers, whether motivated by marketing strategy, competitive conditions, financial difficulties or otherwise, to decrease significantly the amount of merchandise purchased from us or to change their manner of doing business with us, could substantially reduce our revenues and have a material adverse effect on our profitability.

The retail industry has, in the past several years, experienced a great deal of consolidation and other ownership changes and we expect such changes to be ongoing. In the future, retailers may further consolidate, undergo restructurings or reorganizations, realign their affiliations or re-position their stores' target markets. Any of these types of actions could decrease the number of stores that carry our products or increase the ownership concentration within the retail industry. These changes could decrease our opportunities in the market, increase our reliance on a smaller number of customers and decrease our negotiating strength with them.

Our business has been and could continue to be adversely affected by financial instability experienced by our customers. During the past several years, various retailers have experienced significant financial difficulties, which have resulted in bankruptcies, liquidations and store closings. Over the last few years, several of our customers, including Goody’s, Mervyns, Gottschalks and Boscov’s, either reorganized or liquidated. We sell our product primarily to national and regional department stores, and vertical specialty stores in the United States on credit and evaluate each customer's financial condition on a regular basis in order to determine the credit risk we take in selling goods to them. The financial difficulties of a customer could cause us to curtail business with that customer and we may be unable to shift sales to another customer at comparable margins. We may also assume more credit risk relating to receivables of a customer experiencing financial instability. Should these circumstances arise with respect to our customers, our inability to shift sales or to collect on our trade accounts receivable from any one of our customers could substantially reduce our revenues and have a material adverse effect on our financial condition and results of operations.

Chargebacks and margin support payments may have a material adverse effect on our business.

Consistent with industry practice, we may allow customers to deduct agreed upon amounts from the purchase price for sales allowances, co-op advertising, new store opening discounts and other marketing development funds, which in the opinion of management promotes brand awareness. In addition, margin support payments may be required due to lower than anticipated sell through rates, which may be caused by uncontrollable factors, such as general economic conditions, changing fashion trends and weather conditions, as well as controllable factors, such as wholesale prices, design, merchandising and the quality of our goods. These deductions have a dilutive effect on our business and results of operations since they reduce overall gross profit margins on sales. If our efforts to reduce our margin support are unsuccessful, we will likely continue to experience significant levels of chargebacks and margin support payments, which may further reduce our profitability resulting in a material adverse effect on our business.

We are dependent upon the revenues generated by our licensing alliances and the loss or inability to renew certain licenses could reduce our revenue and consequently reduce our net income.

We license brands from third parties for specific products. The term of each of our licenses is generally three years and we typically have the opportunity to renew or extend the licenses, which are sometimes conditioned upon our meeting certain sales targets. We may not be able to renew or extend these licenses on favorable terms, if at all. If we are unable to renew or extend any one of these licenses, we could experience a decrease in net sales.

We may not be able to anticipate consumer preferences and fashion trends, which could negatively affect acceptance of our products by retailers and consumers and result in a significant decrease in net sales.

Our failure to anticipate, identify and respond effectively to changing consumer demands and fashion trends could adversely affect acceptance of our products by retailers and consumers and may result in a significant decrease in net sales or leave us with a substantial amount of unsold inventory. Our products must appeal to a broad range of consumers whose preferences cannot be predicted with certainty and are subject to rapid change. We may not be able to continue to develop appealing styles or successfully meet constantly changing consumer demands in the future. In addition, any new products or brands that we introduce may not be received successfully by retailers and consumers. If our products are not received successfully by retailers and consumers and we are left with a substantial amount of unsold inventory, we may be forced to rely on markdowns or promotional sales to dispose of excess inventory. If this occurs, our business, financial condition and results of operations could be materially adversely affected.

If our manufacturers fail to use acceptable ethical business practices, our business could be adversely affected. We require our manufacturers to operate in compliance with applicable laws, rules and regulations regarding working conditions, employment practices and environmental compliance. However, we do not control the labor and other business practices of the independent manufacturers of our products. If one of our manufacturers violates labor or other laws or implements labor or other business practices that are generally regarded as unethical in the United States, the shipment of products to us could be interrupted and our reputation could be damaged. Any of these events could have a material adverse effect on our results of operations.

Our business could be harmed if we do not deliver quality products in a timely manner.

Our sourcing, logistics and technology functions operate within substantial production and delivery requirements and subject us to the risks associated with unaffiliated manufacturers, transportation and other factors. If we do not comply with customer product requirements or meet their delivery requirements, our customers could seek reduced purchase prices, require significant margin support, reduce the amount of business they do with us or cease to do business with us, all of which would adversely affect our business.

If we encounter problems with our distribution system, our ability to deliver our products to the market would be adversely affected.

We rely on third party distribution facilities to warehouse and to ship product to our customers. Due to the fact that substantially all of our product is distributed from a relatively small number of locations, our operations could be interrupted by earthquakes, floods, fires or other natural disasters near our distribution centers. We maintain business interruption insurance, but it may not adequately protect us from the loss of customers. In addition, our distribution capacity is dependent on the timely performance of services by third parties, including transportation of product to and from distribution facilities. If we encounter problems with our distribution system, our inability to meet customer expectations on managing inventory, complete sales and achieve objectives for operating efficiencies could have a material adverse effect on our business.

Labor disruptions at ports or our suppliers’ facilities, manufacturers’ facilities or distribution facilities may adversely affect our business.

Our business depends on our ability to source and distribute product in a timely manner. As a result, we rely on the free flow of goods on a consistent basis from our suppliers and manufacturers. Labor disputes at various ports or at our suppliers, manufacturers or our distribution facilities create significant risks for our business, particularly if these disputes result in work slowdowns, lockouts, strikes or other disruptions during our peak importing or manufacturing seasons. An interruption in the flow of goods could have a material adverse effect on our business, potentially resulting in cancelled orders by customers, unanticipated inventory accumulation or shortages and reduced net sales and net income.

We rely significantly on information technology and any failure, inadequacy, interruption or security lapse of that technology could adversely affect our ability to effectively operate our business.

Our ability to manage and maintain our inventory and internal reports and to ship products to customers and invoice them on a timely basis depends significantly on our internally developed enterprise resource planning system, as approximately 40% of our orders are received electronically. The failure of this system to operate effectively or to integrate with other systems or a breach in security of this system could cause delays in product fulfillment and reduced efficiency of our operations, and it could require significant capital investments to remedy any such failure, problem or breach.

We operate in a highly competitive and fragmented industry and our failure to compete successfully could result in a loss of one or more significant customers.

The apparel industry is highly competitive and fragmented. Our competitors include numerous apparel designers, manufacturers, retailers, importers and licensors, many of which have greater financial and marketing resources than we possess. We believe that the principal competitive factors in the apparel industry are:

| | · | brand name and brand identity; |

| | · | timeliness, reliability and quality of product and services provided; |

| | · | market share and visibility; |

| | · | the ability to anticipate customer and consumer demands. |

The level of competition and the nature of our competitors vary by product segment with low margin manufacturers being our main competitors in the less expensive segment of the market and with domestic and foreign designers and licensors competing with us in the more upscale segment of the market. Increasingly, we experience competition from our customers' in-house private labels. If we do not maintain our brand names and identities and continue to provide high quality and reliable services on a timely basis at competitive prices, our ability to compete in our industry will be adversely affected. If we are unable to compete successfully, we could lose one or more of our significant customers, which could have a material adverse effect on our sales and financial performance.

We may face challenges in the management of the sales and profitability of any acquisitions that we may make, as well as in integrating the acquired businesses, any of which may negatively impact our business.

As part of our growth strategy, we have acquired and licensed, and in the future, may acquire or license new brands and product categories. We may also make strategic acquisitions in addition to Rio. Acquisitions have inherent risks, including the risk that the projected sales and net income from the acquisition may not be generated, the risk that the integration of the acquired business is more costly and takes longer than anticipated, the risk of diversion of the attention and resources of management, risks associated with additional customer concentration and related credit risk, risks of retaining key personnel and risks associated with unanticipated events and unknown legal liabilities despite the due diligence efforts that we undertake. Any of these risks could have a material adverse effect on our business.

We may be subject to the impairment of acquired intangible assets.

When we acquire a business, a portion of the purchase price of the acquisition may be allocated to goodwill and other identifiable intangible assets. At December 31, 2012 and 2011, our goodwill and intangible assets were approximately $17.2 million and $18.6 million, respectively. We conduct an annual review, and more frequent reviews if events or circumstances dictate, to determine whether goodwill is impaired. We also determine whether impairment indicators are present related to our identifiable intangible assets. If we determine that goodwill or other intangible assets are impaired, we would be required to write down the value of these assets.

The ultimate resolution of income and other possible tax liabilities may require us to incur expense beyond amounts reserved on our balance sheet or make cash payments beyond those that we anticipated.

The ultimate resolution of income and other possible tax liabilities may require us to incur expense beyond amounts reserved on our balance sheet or make cash payments beyond those that we anticipated. Our historic income and other tax positions may be challenged by the appropriate taxing authorities. We believe that we have provided adequate reserves for these tax positions for all periods open under the applicable statutes of limitations, but a challenge by a taxing authority could prove costly to defend as well as to resolve. If the actual liability for taxes exceeds our reserves, earnings could be materially adversely affected, and we may be required to make cash payments beyond what we anticipated.

Utilization of our net operating losses and tax credit carry-forwards may be subject to substantial annual limitations due to the ownership change limitations provided by the Internal Revenue Code (the “Code”) Section 382. Such annual limitations could result in the expiration of the net operating loss and tax credit carryforwards before their utilization. The events that may cause ownership changes include, but are not limited to, a cumulative stock ownership change of greater than 50% over a three year period. Calculating whether an ownership change has occurred is subject to uncertainty, both because of the complexity of Section 382 of the Code and because of limitations on a publicly-traded company's knowledge as to the ownership of, and transactions in, its securities. Therefore, the calculation of the amount of our net operating loss carryforwards may be changed as a result of a challenge by a governmental authority or our learning of new information about the ownership of, and transactions in, our securities. Our ability to fully utilize our net operating losses could be limited if there are future ownership changes that, together with certain ownership changes in our common stock that have occurred during any prior three year period (including, as of the date hereof, any shares issued in connection with the Rio transaction), result in a “change of control” for the purposes of Section 382.

Rio is authorized to operate under the Honduran Free Trade Zone Regime (“FTZ”). Therefore, Rio qualifies for exemption from Honduran customs duties, charges and surcharges, internal consumption, production sales tax and other excise taxes on imported and exported goods. Rio is also exempt from municipal taxes, asset taxes and income taxes, provided that Rio does not benefit from income tax exemption granted in another country. In order to maintain the FTZ exemption, Rio must export at least 95% of its annual production. Rio currently exports 99% of its production. Although the FTZ is indefinite by nature, subsequent repeal or modification of the FTZ, or any failure to qualify for the aforementioned exemptions, could materially adversely affect our results of operations.

Significant changes to international trade regulations could adversely affect our results of operations.

A large portion of our products are manufactured in Honduras. We therefore benefit from the Dominican Republic – Central America Free Trade Agreement (“DR-CAFTA”). Our claims for duty free or reduced duty treatment under DR-CAFTA and other available programs are largely conditioned on our ability to produce or obtain accurate records, some of which are provided to us by third parties, about production processes and sources of raw materials. Subsequent repeal or modification of DR-CAFTA, or the inadequacy or unavailability of supporting records, could materially adversely affect our results of operations. In addition, our products are subject to foreign competition, which in the past has been faced with significant U.S. government import restrictions. The extent of import protection afforded to domestic apparel producers has been, and is likely to remain, subject to political considerations. The elimination of import protections for domestic apparel producers could significantly increase global competition, which could adversely affect our business. In addition, any failure to comply with international trade regulations could cause us to become subject to investigation resulting in significant penalties or claims or an inability to conduct our business, adversely affecting our results of operations.

We are dependent on certain key personnel, the loss of whom could negatively impact our ability to manage our business and thereby adversely affect our business.

Our future success depends to a significant extent on retaining the services of key executive officers, other key members of management and directors. The loss of the services of any one of these individuals, or any other key member of management, could have a material adverse effect on our business.

The stockholders’ rights plan adopted by the Board of Directors in 2008 may inhibit takeovers and may adversely affect the market price of our common stock.

In 2008, our Board of Directors (“Board”) approved the creation of our Series A Preferred Stock and adopted a stockholders’ rights plan pursuant to which it declared a dividend of one Series A Preferred Stock purchase right for each share of our common stock held by stockholders of record. The preferred share purchase rights will also attach to any additional shares of common stock issued. Initially, these rights will not be exercisable and will trade with the shares of our common stock. Under the rights plan, these rights will generally be exercisable only if a person or group acquires, or commences a tender or exchange offer, for 15% or more of our common stock. If the rights become exercisable, each right will permit its holder to purchase one one-thousandth of a share of Series A Preferred Stock for the exercise price of $33.00 per right. The rights plan also contains customary “flip-in” and “flip-over” provisions such that if a person or group acquires beneficial ownership of fifteen percent or more of our common stock, each right will permit its holder, other than the acquiring person or group, to purchase shares of our common stock for a price equal to the quotient obtained by dividing $33.00 per right by one-half the then current market price of our common stock. In addition, if, after a person acquires such ownership, we are later acquired in a merger or similar transaction, each right will permit its holder, other than the acquiring person or group, to purchase shares of the acquiring corporation’s stock for a price equal to the quotient obtained by dividing $33.00 per right by one-half of the then current market price of the acquiring company’s common stock, based on the market price of the acquiring corporation’s stock prior to such merger.

The stockholders’ rights plan and the associated Series A Preferred Stock purchase rights may discourage a hostile takeover and prevent our stockholders from receiving a premium over the prevailing market price for the shares of our common stock.

Global economic, political and social conditions may harm our ability to do business, increase our costs and negatively affect our stock price.

Global credit and financial markets have experienced extreme disruptions in recent years, including severely diminished liquidity and credit availability, declines in consumer confidence, declines in economic growth, increases in unemployment rates and uncertainty about economic stability. While the decline in consumer spending has recently moderated, these economic conditions could still lead to continued declines in consumer spending and may have resulted in a resetting of consumer spending habits that makes it unlikely that such spending will return to prior levels for the foreseeable future which in turn may lead to further decreases in our net sales or a material adverse effect on our operating results, financial position and cash flows. Economic conditions have also led to a highly promotional environment and strong discounting pressure from our customers, which have had a negative effect on our revenues and profitability. This promotional environment may continue even after economic growth returns, as we expect that consumer spending trends are likely to remain below historical levels for the foreseeable future.

The price of purchased yarn and other raw materials used by us or our suppliers is prone to significant fluctuations and volatility.

Fluctuations in the price, availability and quality of the fabrics or other raw materials used to manufacture our products could have a material adverse effect on our cost of goods sold or our ability to meet our customers’ demands. The prices for fabrics depend largely on the market prices for the raw materials used to produce them. The price and availability of such raw materials may fluctuate significantly, depending on many factors. At times in the past we have experienced significant upward pressure on each of the foregoing cost inputs, which resulted in pressure on our gross margin. Whenever possible, we pass along these cost increases to our customers through higher selling prices. Should our customers not accept such increases or should they accept them in the first instance, but fail to achieve higher average unit retails thereby increasing their need for margin support from us, our profitability may be materially adversely affected.

The price of energy and fuel costs are prone to significant fluctuations and volatility which could adversely affect our results of operations.

Our manufacturing operations and those of our suppliers require high inputs of energy, and therefore changes in energy prices directly impact our gross profits. In addition, we incur significant shipping and freight costs to transport goods from our offshore facility and suppliers’ offshore facilities to the United States. The cost of energy and fuel fluctuate due to a number of factors outside our control, including government policy and regulation and weather conditions. We continue to focus on manufacturing methods that will reduce the amount of energy used in the production of our products to mitigate risks of fluctuations in the cost of energy. However, significant increases in energy and fuel prices may make us less competitive as compared to others in the industry, which may have a material adverse effect on our results of operations.

We may be restricted in our ability to borrow under our revolving credit facility.

Significant operating losses or significant uses of cash in our operations could cause us to default on our asset-based revolving credit facility. Our ability to borrow under the credit facility depends on our accounts receivable and inventory levels. A significant deterioration in our accounts receivable or inventory levels could restrict our ability to borrow funds. In addition, the credit facility includes customary conditions to funding, representations and warranties, covenants and events of default. The covenants include, among other things, limitations on asset sales, consolidations, mergers, liens, indebtedness, loans, investments, guaranties, acquisitions, dividends, stock repurchases and transactions with affiliates. An event of default under the credit facility could result in an acceleration of our obligations under the agreement, in the foreclosure on any assets subject to liens in favor of the credit facility’s lenders, and in our inability to borrow additional amounts under the credit facility.

We may be unable to realize expected benefits from our restructuring and cost savings plan

In order to operate more efficiently and control costs, we announce from time to time restructuring and cost savings plans, such as our ongoing cost savings plan implemented in 2012, which may include workforce reductions and other cost reduction initiatives. These plans are intended to generate operating expense savings through selling, general and administrative expense reductions as well as other savings. We may undertake further workforce reductions or restructuring actions in the future. These types of cost reduction and restructuring activities are complex. If we do not successfully manage our current restructuring activities, or any other restructuring activities that we may undertake in the future, expected efficiencies and benefits might be delayed or not realized, and our operations and business could be disrupted. Risks associated with these actions include delays in implementation of anticipated workforce reductions, additional unexpected costs and the failure to meet operational targets due to the loss of employees, any of which may impair our ability to achieve anticipated cost reductions or may otherwise harm our business, which could have a material adverse effect on our competitive position, results of operations, cash flows or financial condition.

Item 1B. Unresolved Staff Comments.

Not Applicable.

Item 2. Properties.

We lease our manufacturing facility, administrative offices, operations center, sales offices, sourcing offices, showrooms and a retail store. Rio’s manufacturing facility is located in San Pedro Sula, Honduras. Our sales offices and showrooms are in New York, New York. Our scott james® retail store is in Boston, Massachusetts, and our scott james® outlet store is in Minneapolis, Minnesota. We have administrative offices in Anderson, South Carolina, operations centers in New York, New York and Minneapolis, Minnesota, and sourcing offices in Dongguan, China and Hong Kong. We believe that all of our properties are well maintained and suitable for their intended use, with the exception of our New York office. See Item 3. Legal Proceedings.

Item 3. Legal Proceedings.

New York Office Lease

In July 2007, the Company entered into a lease (the “New York Lease”) for corporate office space located at 114 West 41st Street, New York, NY 10036 (the “New York Office”). As part of the New York Lease, the landlord (“Landlord”) agreed to commence and substantially complete major capital improvements to the common areas of the New York Office by June 2008. After June 2008, if such capital improvements have not been substantially completed, the New York Lease provides, among other things, for a reduction in rent by one half for each day beyond June 30, 2008 that the capital improvements remain incomplete and are not being diligently prosecuted toward completion.

On February 16, 2011, the Company filed a complaint in the Supreme Court, New York County, with respect to the New York Lease. The Company asserted claims against the Landlord of the New York Office and the receiver of such property appointed in connection with a foreclosure action commenced against Landlord by its lender. The complaint sought (i) a judgment declaring (a) that the Company is not in default under the New York Lease and (b) that the rent previously paid by the Company represents the full amount of rent; and (ii) for rescission of the New York Lease as of June 30, 2008 by reason of default by the Landlord with respect to a material provision under the New York Lease requiring prompt completion of major capital improvements of the New York Office’s common areas. The Supreme Court action was dismissed on December 16, 2011 without prejudice to renew the action if complete relief is not afforded in the Civil Court action.

On February 23, 2011, the court appointed Receiver of the subject property commenced a non-payment proceeding in the Civil Court of the City of New York against the Company. The Receiver seeks payment of allegedly past due and unpaid rent and additional rent under the New York Lease. The Company vigorously denies that any rent or additional rent is due and owing under the New York Lease and has moved for an order removing this action to the Supreme Court, New York County, and consolidating it with the previously commenced action described above. The motion for removal and consolidation was denied by the Supreme Court and the matter has been proceeding in Civil Court. The Company has filed its answer, affirmative defenses and counterclaims and has moved for discovery in that action dated June 16, 2011. The motion and subsequent cross-motion were argued before the court on July 18, 2011. On October 5, 2011, that court granted the Company’s motion for discovery. On July 30, 2012 the Civil Court commenced a trial on the matter. The trial was concluded on December 19, 2012 and the respective parties filed post trial briefs and reply briefs with the Court on January 23 and February 5, 2013, respectively. A decision by the trial court is expected during the second quarter of 2013. See Item 8. Financial Statements and Supplementary Data Note 7 – Accrued Expenses and Other Liabilities and Note 13 – Commitments and Contingencies to the audited consolidated financial statements.

The Company is from time to time involved in other litigation incidental to the conduct of its business, none of which is expected to be material to its business, financial condition or operations.

Item 4. Mine Safety Disclosures.

Not applicable.

PART II.

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

There is currently no established public trading market for our common stock. Our common stock is currently quoted on the OTC Markets under the symbol “HAMP”. The OTC Markets is a centralized quotation service that collects and publishes market maker quotes for over-the-counter securities in real time. Over-the-counter market quotations, like those on the OTC Markets, reflect inter-dealer prices, without retail mark-up, mark-down or commission and may not necessarily represent actual transactions.

As of March 2, 2013, the Company had 37 stockholders of record of our common stock, although we believe there are a significantly larger number of beneficial owners. The following table sets forth the low and high sales prices of shares of our common stock for each of the quarters of 2012 and 2011 as reported by the OTC Markets:

| | | 2012 | | | 2011 | |

| | | Low | | | High | | | Low | | | High | |

| First Quarter | | $ | 2.05 | | | $ | 2.69 | | | $ | 3.35 | | | $ | 5.00 | |

| Second Quarter | | | 1.90 | | | | 3.20 | | | | 3.05 | | | | 4.25 | |

| Third Quarter | | | 2.65 | | | | 3.50 | | | | 2.26 | | | | 3.93 | |

| Fourth Quarter | | | 2.50 | | | | 3.45 | | | | 1.85 | | | | 3.20 | |

The closing stock price on March 2, 2013 was $3.00.

Any determination to pay dividends will be made by our Board and will be dependent upon our financial condition, results of operations, capital requirements and such other factors as our Board may deem relevant. Our revolving credit facility contains restrictive covenants placing limitations on payment of cash dividends. We did not pay dividends on our outstanding stock during the years ended December 31, 2012 and 2011.

On March 31, 2012 and 2011, shares of Hampshire common stock in the amount of 6,518 and 2,881, respectively, were returned to the Hampshire Group, Limited 2009 Stock Incentive Plan which allows employees to satisfy their applicable withholding tax obligations by using shares of common stock that would otherwise be deliverable upon the vesting of the restricted stock.

In connection with the adoption of the Hampshire Group, Limited 2009 Stock Incentive Plan (the “Stock Plan”), the Board authorized 880,000 shares of common stock under the Stock Plan and initially approved grants totaling 862,500 shares, which consisted of grants to certain employees, managers, named executive officers and directors. Ten percent of each award of restricted stock was subject to time-based vesting with the remaining 90% of each award subject to performance-based vesting. During 2012, 459,000 shares of non-vested restricted stock previously granted to certain employees who were participants in the Stock Plan were surrendered for cancellation by such employees pursuant to transactions that, with respect to each such employee, provided that such employee would be granted options to purchase Hampshire Common Stock in consideration for the cancellation of such shares of restricted stock held by it. In connection with such transactions, a total of 331,250 options were granted. In addition, during 2012, certain other employees who were participants in the Stock Plan were granted, in the aggregate, 375,750 options to purchase Hampshire Common Stock. Twenty-five percent (25%) of such options vested and became exercisable on December 31, 2012 and another twenty-five percent (25%) will vest and become exercisable on December 31st of each of 2013, 2014 and 2015, and the options will expire on March 30, 2022.

On October 1, 2012, 10,455 shares of Hampshire common stock were returned to the Company by Heath L. Golden pursuant to a net issuance in connection with the settlement of certain Restricted Stock Units in order to satisfy applicable withholding tax obligations.

See Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Shareholder Matters for information regarding our equity compensation plan.

Item 6. Selected Financial Data.

The following selected consolidated financial data should be read in conjunction with Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations and the consolidated financial statements, including the related notes, included herein in Item 8. Financial Statements and Supplementary Data. The selected consolidated financial data under the captions Statement of Operations Data and Balance Sheet Data as of and for the end of each of the years in the five year period ended December 31, 2012 are derived from our consolidated financial statements. The statement of operations data includes results from continuing operations, which excludes the discontinued operations of Hampshire Designers, Item-Eyes, Marisa Christina, Shane Hunter and David Brooks in each year presented. Our historical results are not necessarily indicative of results to be expected in any future period.

| | | Year Ended December 31, | |

| (in thousands, except per share data) | | 2012 | | | 2011 | | | 2010 | | | 2009 | | | 2008 | |

| | | | | | | | | | | | | | | | |

| Statement of Operations Data: | | | | | | | | | | | | | | | |

| Net sales | | $ | 117,560 | | | $ | 86,148 | | | $ | 57,318 | | | $ | 64,820 | | | $ | 69,752 | |

| | | | | | | | | | | | | | | | | | | | | |

| Gross profit | | | 23,454 | | | | 14,560 | | | | 9,879 | | | | 15,030 | | | | 15,147 | |

| Selling, general and administrative expenses | | | 33,965 | | | | 27,977 | | | | 16,871 | | | | 15,910 | | | | 20,337 | |

| Loss on lease obligation | | | — | | | | 6,306 | | | | — | | | | — | | | | — | |

| Restructuring costs | | | 644 | | | | 179 | | | | — | | | | 4,175 | | | | 215 | |

| Goodwill impairment loss | | | — | | | | 1,204 | | | | — | | | | — | | | | — | |

| Special costs | | | — | | | | — | | | | 4,481 | | | | 4,547 | | | | 3,761 | |

| Tender offer related costs | | | — | | | | — | | | | — | | | | 2,053 | | | | 386 | |

| Loss from operations | | $ | (11,155 | ) | | $ | (21,106 | ) | | $ | (11,473 | ) | | $ | (11,655 | ) | | $ | (9,552 | ) |

| Loss from continuing operations | | $ | (12,522 | ) | | $ | (20,301 | ) | | $ | (9,471 | ) | | $ | (5,826 | ) | | $ | (13,134 | ) |

| Basic loss per share from continuing operations | | $ | (1.72 | ) | | $ | (3.41 | ) | | $ | (1.70 | ) | | $ | (1.06 | ) | | $ | (1.91 | ) |

| Diluted loss per share from continuing operations | | $ | (1.72 | ) | | $ | (3.41 | ) | | $ | (1.70 | ) | | $ | (1.06 | ) | | $ | (1.91 | ) |

| Basic weighted average common shares outstanding | | | 7,271 | | | | 5,941 | | | | 5,554 | | | | 5,482 | | | | 6,884 | |

| Diluted weighted average common shares outstanding | | | 7,271 | | | | 5,941 | | | | 5,554 | | | | 5,482 | | | | 6,884 | |

| | | | 2012 | | | | 2011 | | | | 2010 | | | | 2009 | | | | 2008 | |

Balance Sheet Data: | | | | | | | | | | | | | | | | | | | | |

| Cash and short term investments | | $ | 12,500 | | | $ | 25,801 | | | $ | 33,720 | | | $ | 33,365 | | | $ | 35,098 | |

| Restricted cash | | | — | | | | — | | | | 2,725 | | | | — | | | | — | |

Working capital (1) | | | 24,926 | | | | 35,922 | | | | 48,098 | | | | 52,883 | | | | 51,324 | |

Total assets (1) | | | 72,085 | | | | 89,035 | | | | 78,553 | | | | 86,929 | | | | 98,706 | |

| Long-term liabilities | | | 16,277 | | | | 21,588 | | | | 13,948 | | | | 14,656 | | | | 14,076 | |

| Total stockholders’ equity | | | 34,339 | | | | 42,407 | | | | 49,402 | | | | 58,849 | | | | 64,797 | |

| Book value per share outstanding | | | 4.57 | | | | 5.95 | | | | 7.81 | | | | 9.32 | | | | 11.85 | |

(1) Excludes discontinued operations

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

The following discussion contains statements that are forward-looking. These statements are based on expectations and assumptions that are subject to risks and uncertainties. Actual results could differ materially because of, among other reasons, factors discussed in the “Safe Harbor” statement on page ii of this report and Item 1A – Risk Factors and elsewhere in this report. The commentary should be read in conjunction with the consolidated financial statements and related notes and other statistical information included in this report.

OVERVIEW

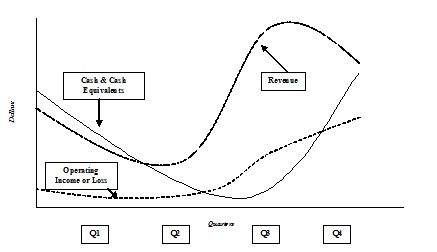

The following is a graphical illustration (it does not represent an actual time period, actual revenues, actual cash balances, etc.) of the historical seasonal nature of our business.

In the past our business was highly seasonal as a result of our product mix including a high concentration of sweaters. Although not as significant as in prior years, our business continues to maintain a fairly high degree of seasonality with approximately 65% of our sales during 2012 occurring in the third and fourth quarters. As a result of such seasonality, inventory begins to rise in the second quarter and typically peaks during the third quarter before descending to its cyclical low in the fourth quarter. Trade receivable balances rise commensurately with sales. Cash balances follow this cycle as inventory is purchased, product is sold and trade receivables are collected. Funding inventory and pending trade receivable collections deplete cash balances and may require draws from our revolving credit facility in the third or fourth quarters. Our income or loss from continuing operations has generally been correlated with revenue, as a large percentage of our profits have historically been generated in the third and fourth fiscal quarters.

Seasonality in 2012 declined as a result of Rio’s more even distribution of sales throughout the year as compared to our other subsidiaries. In 2013 and beyond, we expect this seasonality to decline further as a result of the Dockers® and Panama Jack® licenses which we believe will increase our sales during the spring season.

We are a provider of fashion apparel across a broad range of product categories, channels of distribution and price points. As a holding company, we operate through our wholly-owned subsidiaries, Hampshire Brands, Inc., Rio Garment S.A. and scott james, LLC. We were established in 1976 and are incorporated in the state of Delaware.

Hampshire Brands designs and markets men’s sportswear to department stores, chain stores and mass market retailers under licensed brands, our own proprietary brands and the private labels of our customers. Among others, we offer a full tops assortment under the Dockers® brand and a t-shirt and board short assortment under the Panama Jack® brand, both of which are licensed, as well as private label t-shirt and sweater offerings to retailers under their private labels.

The scott james® brand is a designer apparel collection for men, which includes a full sportswear offering. It is sold primarily through upscale department and specialty stores, scott james® retail shops and online at www.scottjamesonline.com.

Rio, acquired on August 25, 2011, is a Honduras-based apparel manufacturer, designing, sourcing and manufacturing knit tops for men, women and children, which are sold to retailers and distributors, primarily in the United States. Rio’s manufacturing platform primarily supports the vertical specialty store channel. Our manufacturing operations begin with the purchase of fabric and other raw materials from third party suppliers. The fabrics are ultimately sewn into finished garments at our textile facility or at the facilities of third party contractors located in Honduras. Rio also purchases yarn and outsources fabric production to third parties, where upon completion, the fabric returns to the Rio facility for production. Our garments may also be embellished and prepared for retail (with any combination of services, including ticketing, hang tags and hangers).

Our primary strength is our ability to design, develop, source and deliver quality products within a given price range, while providing superior levels of customer service. Our diversification of product lines allows for vertical integration through Rio, multi-category licensing through Hampshire Brands and owned lifestyle ways through scott james®. We have developed international sourcing abilities that permit us to deliver quality merchandise at competitive prices to our customers.

The apparel market is highly competitive. Competition is primarily based on product design, price, quality and service. We face competition from apparel designers, manufacturers, importers, licensors and our own customers’ private label programs, many of which are larger and have greater financial and marketing resources than we have available to us.

The economic environment over the past several years has been challenging and has been characterized by, among other things, restrained consumer spending, weak credit market conditions and inflationary pressures on our cost of goods. In an effort to preserve gross margin dollars in the face of rising costs of goods and stagnant out the door prices, during the past two years we have taken significant steps to reposition our Company for growth and profitability, including: