| Ethics Office | MyCompliance.fmr.com |

2021

Rules for

Employee Investing

CODE OF ETHICS FOR PERSONAL INVESTING

Fund Access Version

GLOBAL POLICY ON INSIDE INFORMATION

RULES FOR BROKER-DEALER EMPLOYEES

The Rules for Employee Investing are fairly comprehensive. They cover most of the personal investing situations a Fidelity employee is likely to experience. Yet it’s always possible you will encounter a situation that isn’t fully addressed by the rules. If that happens, you need to know what to do. The easiest way to make sure you are making the right decision is to follow these three principles:

1. Know the policy.

If you think your situation isn’t covered, check again. It never hurts to take a second look at the rules.

2. Seek guidance.

Asking questions is always appropriate. Talk with your manager or the Ethics Office if you’re not sure about the policy requirements or how they apply to your situation.

Additionally, resources are available at MyCompliance to assist you with your questions.

3. Use sound judgment.

Analyze the situation and weigh the options. Think about how your decision would look to an outsider.

Understanding and following the Rules for Employee Investing is one of the most important ways we can ensure our customers’ interests always come first.

Rules for Employee Investing

These Rules for Employee Investing contain the Code of Ethics for Personal Investing and the Global Policy on Inside Information.

The Fund Access Version of the Code of Ethics for Personal Investing contains rules about owning and trading securities for personal benefit. This version applies to officers, directors, and employees of Fidelity companies that are involved in the management and operations of Fidelity’s funds, or have access to non-public information about the funds, including investment advisors to the funds, the principal underwriter of the funds, and anyone designated by the Ethics Office. Keep in mind that if you change jobs within Fidelity, a different version of the Code of Ethics may apply to you.

The Global Policy on Inside Information, which applies to every Fidelity employee, contains rules on inside information and how to prevent its unauthorized use or dissemination.

| 1 | Code of Ethics for Personal Investing | 4 |

| Rules for All Employees Subject to This Code of Ethics | 4 |

Acknowledging that you understand the rules

Complying with securities laws

Reporting violations to the Ethics Office

Disclosing securities accounts and holdings in covered securities

Moving covered accounts to Fidelity

Moving holdings in Fidelity funds to Fidelity

Disclosing transactions of covered securities

Disclosing gifts and transfers of ownership of covered securities

Getting approval before engaging in private securities transactions

Clearing trades in advance (pre-clearance)

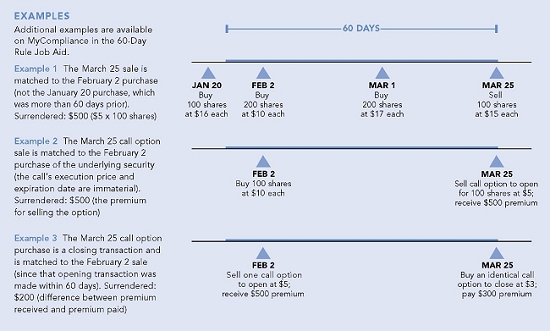

Surrendering 60-day gains (60-Day Rule)

Participating in an investment club

Buying securities of certain broker-dealers

Profiting from knowledge of fund transactions

Influencing a fund to benefit yourself or others

Attempting to defraud a client or fund

Using a derivative to get around a rule

| Additional Rules for Traders, Research Analysts, and Portfolio Managers | 12 |

All rules listed above plus the rules in this section

Notification of your ownership of covered securities in a research note

Disclosing trading opportunities to the funds before personally trading

Trading within seven days of a fund you manage

| CONTACT INFORMATION | |

Ethics Office

Phone (001) 617-563-5566

Fax (001) 617-385-0939

ethics.office@fmr.com

Mail zone WG3D

Web MyCompliance.fmr.com | Pre-Clearance

Web Internal preclear.fmr.com

External preclear.fidelity.com

Phone (001) 617-563-6109

To call the phone numbers from outside the United States or Canada, dial “001” before the number. |

| CODE OF ETHICS — FUND ACCESS VERSION | 2 |

Other policies you should be aware of

There are other policies that you need to be familiar with, including:

| ● | Professional Conduct Policies, Global Policy on Conflicts of Interest, and other Fidelity-wide policies (available at Policy.fmr.com) |

| ● | Equal Employment Opportunity, Prohibiting Discrimination & Harassment Corporate Policy (available at Policy.fmr.com) |

| ● | Electronic Communications, Social Media & Systems Usage Policy (available at Policy.fmr.com) |

| ● | Information security practices (available at InfoSecurity.fmr.com) |

| ● | Anti-Money Laundering Policies and Procedures (available at MyCompliance.fmr.com) |

| ● | Corporate Policy on Business Entertainment and Workplace Gifts (available at MyCompliance.fmr.com) |

| ● | Global Policy on Outside Business Activities (available at MyCompliance.fmr.com) |

| ● | Global Anti-Corruption Policy and applicable Supplements to the Global Anti-Corruption Policy (available at MyCompliance.fmr.com) |

| 2 | Global Policy on Inside Information | 15 |

Policy Requirements

Call your MNPI Designated Contact if you think you may have become aware of inside information

Refrain from sharing inside information with anyone else

Refrain from trading or transferring any security of the issuer to which the inside information relates

Comply with any information barriers to which you are made subject

| 3 | Rules for Broker-Dealer Employees | 19 |

Placing trades and trade adjustments through approved Fidelity channels

Do not misuse trading information

Do not make certain transactions

Do not trade in an account you do not own

Do not view or access an account you do not own

Do not act as a broker or make trade adjustments for your accounts

Do not use fictitious or nominee accounts or engage in prearranged trades

| CODE OF ETHICS — FUND ACCESS VERSION | 3 |

| CODE OF ETHICS — FUND ACCESS VERSION | 4 |

| CODE OF ETHICS — FUND ACCESS VERSION | 5 |

| CODE OF ETHICS — FUND ACCESS VERSION | 6 |

| CODE OF ETHICS — FUND ACCESS VERSION | 7 |

| CODE OF ETHICS — FUND ACCESS VERSION | 8 |

| CODE OF ETHICS — FUND ACCESS VERSION | 9 |

| CODE OF ETHICS — FUND ACCESS VERSION | 10 |

| HOW WE ENFORCE THE CODE OF ETHICS | |||||||

The Ethics Office regularly reviews the forms and reports it receives. If these reviews turn up information that is incomplete, questionable, or potentially in violation of the Code of Ethics, the Ethics Office will investigate the matter and may contact you.

If it is determined that you or any of your covered persons has violated the Code of Ethics, the Ethics Office or another appropriate party may take action. Among other things, subject to applicable law, potential actions may include:

• an informational memorandum

• a written warning

• a fine, a deduction from wages, disgorgement of profit, or other payment

• a limitation or ban on personal trading | • referral of the matter to Human Resources

• dismissal from employment

• referral of the matter to civil or criminal authorities

• disclosure of the matter to a regulator as required by law or regulation

Fidelity takes all Code of Ethics violations seriously, and, at least once a year, provides the funds’ trustees with a summary of actions taken in response to material violations of the Code of Ethics. You should be aware that other securities laws and regulations not addressed by the Code of Ethics may also apply to you, depending on your role at Fidelity.

The Chief Ethics Officer or designee retains the discretion to interpret and grant

| exceptions to the Code of Ethics and to decide how the rules apply to any given situation for the purpose of protecting the funds and being consistent with the general principles and objectives of the Code of Ethics.

Exceptions In cases where exceptions to the Code of Ethics are noted and you may qualify for them, you need to get prior written approval from the Ethics Office. The way to request any particular exception is discussed in the text of the relevant rule. If you believe that you have a situation that warrants an exception that is not discussed in the Code of Ethics, you may submit a written request to the Ethics Office. Your request will be considered by the Ethics Office, and you will be notified of the outcome.

| Appeals If you believe a request of yours has been incorrectly denied or that an action is not warranted, you may appeal the decision. To make an appeal, you need to provide the Ethics Office with a written explanation of your reasons for appeal within 30 days of when you were informed of the decision. Be sure to include any extenuating circumstances or other factors not previously considered. During the review process, you may, at your own expense, engage an attorney to represent you. The Ethics Office may arrange for senior management or other parties to be part of the review process. The Ethics Office will notify you in writing about the outcome of your appeal. | ||||

| CODE OF ETHICS — FUND ACCESS VERSION | 11 |

| CODE OF ETHICS — FUND ACCESS VERSION | 12 |

Legal Information The Code of Ethics for Personal Investing constitutes the code of ethics required by Rule 17j-1 under the Investment Company Act of 1940 and by Rule 204A-1 under the Investment Advisers Act of 1940 for the Fidelity funds, investment advisers or principal underwriters, and any other entity designated by the Ethics Office.

| CODE OF ETHICS — FUND ACCESS VERSION | 13 |

These definitions encompass broad categories, and the examples given are not all inclusive. If you have any questions regarding these definitions or application of these rules to a person, security, or account that is not addressed in this section, you can contact the Ethics Office for additional guidance.

Covered person

Fidelity is concerned not only that you observe the requirements of the Code of Ethics, but also that those in whose affairs you are actively involved observe the Code of Ethics. This means that the Code of Ethics can apply to persons owning assets over which you have control or influence or in which you have an opportunity to directly or indirectly profit or share in any profit derived from a securities transaction. This includes:

• you

• your spouse or domestic partner who shares your household

• any other immediate family member who shares your household and (a) is under 18 or (b) is supported financially by you or who financially supports you

• anyone else the Ethics Office has designated as a covered person

This is not an exclusive list, and a covered person may include, for example, immediate family members who live with you but whom you do not financially support, or whom you financially support or who financially support you but who do not live with you. If you have any doubt as to whether a person would be considered a “covered person” under the Code of Ethics, contact the Ethics Office.

Immediate family member

Your spouse or domestic partner who shares your household, and anyone who is related to you in any of the following ways, whether by blood, adoption, or marriage:

• children, stepchildren, and grandchildren

• parents, stepparents, and grandparents

• siblings

• parents-, children-, and siblings-in-law

Covered account

The term “covered account” encompasses a fairly wide range of accounts. Important factors to consider are:

• your actual or potential investment control over an account, including whether you have trading authority, power of attorney, or investment control over an account

| Specifically, a covered account is a brokerage account or any other type of account that holds, or is capable of holding, a covered security, and that belongs to, or is controlled by (including trading discretion or investment control), any of the following:

• a covered person

• any corporation or similar entity where a covered person is a controlling shareholder or participates in investment decisions by the entity

• any trust of which you or any of your covered persons:

– participates in making investment decisions for the trust

– is a trustee of the trust

– is a settlor who can independently revoke the trust and participate in making investment decisions for the trust

Exception

With prior written approval from the Ethics Office, a covered account may qualify for an exception from these rules where:

• it is the account of a nonprofit organization and a covered person is a member of a board or committee responsible for the investments of the organization, provided that the covered person does not participate in investment decisions with respect to covered securities

• it is an educational institution’s account that is used in connection with an investment course that is part of an MBA or other educational program, and a covered person participates in investment decisions with respect to the account

Fidelity fund

The terms “fund” and “Fidelity fund” mean any investment company or pool of assets that is advised or subadvised by any Fidelity entity.

Issuer

An entity, including its wholly owned bank branch, foreign office, or term note program that offers securities or other financial instruments to investors.

Discretionary Managed Account

A covered account may be eligible for certain exceptions, as specified in the Code of Ethics, with prior written approval of the Ethics Office

| validating that the covered account is managed by a third-party investment advisor who has discretionary trading authority over that covered account. To qualify for this exception, the third-party investment advisor must exercise all trading discretion over the covered account and will not accept any order to buy or sell specific securities from the employee or any other covered person. An approved discretionary managed account will still be subject to the Code of Ethics and all provisions in the Code of Ethics unless otherwise stated in a specific exception.

Covered security

This definition applies to all persons subject to this version of the Code of Ethics.

Covered securities include securities in which a covered person has the opportunity, directly or indirectly, to profit or share in any profit derived from a transaction in such securities, and encompasses most types of securities, including, but not limited to:

• shares of Fidelity mutual funds (except money market funds), including shares of Fidelity funds in a 529 plan

• shares of another company’s mutual fund if it is advised by Fidelity (check the prospectus to see if this is the case)

• interests in a variable annuity or life insurance product in which any of the underlying assets are held in funds advised by Fidelity, such as Fidelity VIP Funds (check the prospectus to see if this is the case)

• interests in Fidelity’s deferred compensation plan reflecting hypothetical investments in Fidelity funds

• interests in Fidelity’s deferred bonus plan (ECI) reflecting hypothetical investments in Fidelity funds

• shares of stock (of both public and private companies)

• ownership units in a private company or partnership

• corporate and municipal bonds

• bonds convertible into stock

• options on securities (including options on stocks and stock indexes)

• security futures (futures on covered securities)

| • shares of exchange-traded funds (ETFs)

• shares of closed-end funds

Exceptions

The following are not considered covered securities (please note that securities accounts holding non-covered securities still require disclosure):

• shares of money market funds (including Fidelity money market funds)

• shares of non-Fidelity open-end mutual funds (including shares of funds in non-Fidelity 529 plans)

• shares, debentures, or other securities issued by FMR LLC to you as compensation or a benefit associated with your employment

• U.S. Treasury securities

• obligations of U.S. government agencies with remaining maturities of one year or less

• money market instruments, such as certificates of deposit, banker’s acceptances, and commercial paper

• currencies

• commodities (such as agricultural products or metals), and options and futures on commodities that are traded on a commodities exchange

|

| US-COEFA-2021 | ||

| 1.908020.108 | CODE OF ETHICS — FUND ACCESS VERSION | 14 |

| Enterprise Compliance | MyCompliance.fmr.com |

Remember – your MNPI Designated Contact is here to help you with these issues!

How You May Encounter Inside Information

There are a number of ways you may encounter inside information, either at work or outside of Fidelity. For example:

Clients and Colleagues

• You may learn inside information from a conversation with a client in the course of providing business support, such as handling a trade request.

• You may be exposed to inside information about a mutual fund that may have an impact on the fund’s net asset value in the future, such as non-public information about a fund’s decision to reconsider the value of certain assets in its portfolio.

Brokers and Company Employees

• Brokers may share inside information when contacting you about securities offerings.

• You may receive inside information when meeting with employees of public companies, such as CEOs, CFOs, or Investor Relations representatives.

Consultants and Other Vendors

• In the course of providing consulting services to Fidelity, a third-party consultant may reveal inside information to you (knowingly or unknowingly), such as non-public information about another of the consultant’s public company clients.

• You may be negotiating a vendor contract, and inside information might be shared with you in the contract or the negotiations.

Outside the Workplace

• You may hear inside information from personal sources, such as a spouse, significant other, family member or friend who works at a company that issues publicly-traded securities.

• You may overhear conversations that reveal inside information in elevators, restaurants, public transportation or from speaker and mobile phones, or you may encounter written information that has been left out in public, such as on a copy machine or train seat. | • Associates participating in an outside business activity may encounter inside information while serving on a corporate board or from serving as a consultant or advisor to an outside business.

Please note that these are only examples, and you may receive inside information from other sources or in other circumstances.

What You Should Do If You Believe You May Have Received Inside Information

Contact Your MNPI Designated Contact

While this policy requires you to understand what inside information could be, and be aware of the circumstances in which you may receive it, you should never make any decisions about inside information on your own – for example, whether information you have received is material or non-public, or what steps you should take as a result.

Instead, if you think you may have received inside information, you must call your MNPI Designated Contact (telephone numbers are provided on pages 1 and 4). While it may seem contrary to normal protocol, it is important that you not share the information with anyone else, including your manager. By not sharing the information, you are protecting not only yourself and the information, but also other associates and Fidelity.

When you talk to your MNPI Designated Contact, reveal the details of the information as your contact asks for them, and follow the instructions you receive. Your contact will then determine whether the information requires an information barrier (which are described below) and inform you of that decision.

The possession of inside information is not in itself unlawful or an indication of wrongdoing. However, our goal as a firm is to limit the distribution of inside information only to those associates who have a business need to know and are subject to an information barrier. By assisting us in limiting the distribution of such information, you can best protect the information and yourself, and reduce the number of people who are subject to additional compliance protocols and restrictions.

Comply with Information Barriers

After you contact your MNPI Designated Contact, he or she will determine whether an information barrier is required. Information barriers are established as a way of helping the firm and its associates control inside information and avoid improper communication and potential compliance violations. If you are made | ||

| Fidelity Internal Information | Global Policy on Inside Information Page 2 of 4 |

subject to an information barrier, the Ethics Office will contact you, provide you with a document explaining the terms of the barrier, and require you to acknowledge and agree to abide by those terms.

Information barriers are established by identifying individual associates and groups of people who have received inside information. The information is then protected by employing a combination of information handling, storage protocols, and physical or technical barriers around the associates and the information they possess. Information barriers are monitored to detect possible gaps, including reviews of communications (such as emails), enhanced physical access and access designations, and additions of associates to the information barrier. Surveillance is conducted of associates’ personal trading to detect potential misuse of inside information.

Do Not Trade in the Security or the Issuer

If you have received inside information, you are prohibited from trading any security of the issuer to which the information relates. This is known as “insider trading” or “insider dealing,” which is a serious violation of law. You may not buy, sell, transfer, gift, loan or pledge these securities, even if you have a reason to trade that is independent of the inside information. You also may not modify, suspend, or cancel an automatic investment plan of the security or the issuer of the security or make any recommendations to anyone to deal in the security in any way. These prohibitions apply:

• Not only to your covered accounts, but also to any account you manage, including accounts at Fidelity;

• Regardless of whether you receive any financial or other benefit from the account or the trade; and

• Regardless of whether your trade is in a different direction than the inside information may indicate (e.g., a sale where the inside information indicates you should buy).

Remember that shares of mutual funds are also securities subject to these restrictions. You may not trade or transfer shares of mutual funds, whether advised by Fidelity or not, if you believe that you may have become aware of inside information about the mutual fund.

Protect Inside Information

It is critical that you keep inside information to yourself. You should refrain from discussing inside information in public, including elevators, restaurants, public transportation, on speaker and mobile phones, | or on social media (such as Twitter, LinkedIn, or Facebook). You should also store any documents containing or reflecting the inside information in a secure place in accordance with the document-handling procedures of Fidelity’s Global Policy on Information Protection (“SP2I”) Policy.

Do Not “Tip” or Improperly Disclose Inside Information

The prohibition on communicating with others about inside information extends to recommending investments or expressing opinions to anyone, or soliciting orders from Fidelity clients, on the basis of inside information. This is known as “tipping” or “tipping off,” which is a serious violation of law. You may become liable for any transactions by anyone to whom you have improperly disclosed inside information, or to whom they have made investment recommendations or expressed opinions on the basis of that information.

Reporting Potential Violations

You should report known or suspected violations of this policy to your MNPI Designated Contact or call the Chairman’s Line at 800-242-4762 to speak anonymously on an unrecorded line.

| ||

| Fidelity Internal Information | Global Policy on Inside Information Page 3 of 4 |

MNPI Designated Contacts

Asset Management associates:

Asset Management MNPI Hotline

(001) 617-563-3630

India associates:

FBS India Ethics Office

8-691-7373

+91-80-6691-7373

All other associates:

Ethics Office

(001) 617-563-5566

(001) 800-580-8780 | Business Unit, Regional or Supplemental Policies on Inside Information

Personal Investing – Corporate Issues: Insider Trading

Fidelity Capital Markets – Equity Origination Information Barriers

Fidelity Institutional Online Reference – Inside Information | ||

Contacts and Web Resources

General Policy Issues or Violations Ethics Office 800-580-8780

Chairman’s Line 800-242-4762

Compliance and Regulatory Issues Your MNPI Designated Contact

(See above) | Other Related Policies

Corporate Global Anti-Corruption Policy

Corporate Policy on Business Entertainment and Workplace Gifts

Global Policy on Personal Conflicts of Interest

Global Policy on Outside Business Activities

Global Policy on Information Protection

| ||

| Fidelity Internal Information | Global Policy on Inside Information Page 4 of 4 |

| RULES FOR BROKER-DEALER EMPLOYEES | 19 |

| RELATED POLICIES AND PROCEDURES | ||||

| Other Fidelity policies and guidelines governing employee conduct also apply, and may require pre-clearance by the Ethics Office before an employee takes any action. For example, Fidelity’s Corporate Policy on Business Entertainment and Workplace Gifts (BEWG) requires broker-dealer employees to pre-clear all gifts to business partners, and all gifts and business entertainment to government officials, public sector employees, labor unions and union employees. Fidelity’s Corporate Policy on Political Contributions and Activity requires all Fidelity employees to pre-clear all political contributions and fundraising activities to federal, state or local candidates or office holders. Other Fidelity policies may also require pre-clearance. Employees should be familiar with these policies, including the following located on the Policy Portal: | ||||

Code of Ethics for Personal Investing

Global Policy on Outside Business Activities

Corporate Policy on Business Entertainment and Workplace Gifts

Global Anti-Corruption Policy

Global Policy on Personal Conflicts of Interest

Professional Conduct and Reporting of Criminal Matters and Other Events Policy

| Global Policy on Inside Information

Information Protection Policy (SP2I/CS-601)

Electronic Communications, Social Media and Systems Usage Policy

Political Contributions and Activity Policy

Corporate Policy on Personal Political Contributions and Activities | |||

| RULES FOR BROKER-DEALER EMPLOYEES | 20 |

| RULES FOR BROKER-DEALER EMPLOYEES | 21 |

| are not reported in a timely manner, the employee could be subject to sanctions. Disclosures provided by registered employees will be updated on their Form U4 as required, and therefore it is important that all information listed on the registered employee’s Form U4 is accurate and complete. This includes administrative information such as full legal name (including middle name), home address (cannot be a P.O. box number) and outside business activities. Registered employees must also update answers to any disclosure questions involving customer complaints, criminal disclosures, regulatory disciplinary actions, civil judicial actions, terminations, or financial judgments.

Registration requirements You cannot perform a registered function if you are not registered. Your registration profile is available at MyCompliance.fmr.com If you change positions from one Fidelity broker-dealer to another and your new position requires registration, you must complete and sign a Request for Broker-Dealer Registration found at MyCompliance.fmr.com. You may not function in a registered capacity with your new Fidelity broker-dealer until the Registration and Licensing Group provides written notification to you and your supervisory principal that your registration has been transferred. If your job changes or your job responsibilities change and you require additional registrations or are no longer required or permitted to be registered, you must work with your supervisory principal or business unit Compliance Officer to complete the appropriate registration request form. Contact the Registration and Licensing Group (800-237-8132) if you have any questions regarding your disclosure obligations or registrations. | Employee Compliance Questionnaires All broker-dealer employees must promptly complete an online Employee Compliance Questionnaire (ECQ) as instructed when it becomes available on your To-Do List at MyCompliance.fmr.com. The ECQ lists prior disclosures, which may include covered accounts, outside business activities, political activities, business entertainment and workplace gifts, and reportable disclosure events. It also includes questions concerning compliance with various other policies referenced in these Rules. You must carefully complete this form and submit any comments or updates needed to make your information complete and accurate.

Continuing education All registered employees must complete all required continuing education, including regulatory element training and firm element training.

Annual compliance meeting All registered employees must participate in a meeting where compliance matters that are relevant to registered employees are discussed.

HOW WE ENFORCE THESE RULES Violation of any company policy, and any other form of misconduct, may lead to disciplinary or corrective action up to and including dismissal. |

| USFUND-2021 1.905642.108 | RULES FOR BROKER-DEALER EMPLOYEES | 22 |