Blackrock Muniyield California Quality Fund (MCA)

Filed: 22 Dec 21, 4:09pm

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

Filed by the Registrant ☒ Filed by a Party other than the Registrant ☐

Check the appropriate box:

| ☐ | Preliminary Proxy Statement | |

| ☐ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | |

| ☒ | Definitive Proxy Statement | |

| ☐ | Definitive Additional Materials | |

| ☐ | Soliciting Material Pursuant to § 240.14a-12 | |

BLACKROCK MUNIYIELD CALIFORNIA FUND, INC.

BLACKROCK MUNIYIELD CALIFORNIA QUALITY FUND, INC.

BLACKROCK MUNIHOLDINGS CALIFORNIA QUALITY FUND, INC.

(Exact Name of Registrant as Specified in Charter)

(Name of Person(s) Filing Proxy Statement, if Other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| ☒ | No fee required. | |||

| ☐ | Fee computed on table below per Exchange Act Rules 14a-6(i)(4) and 0-11. | |||

| (1) | Title of each class of securities to which transaction applies:

| |||

| (2) | Aggregate number of securities to which transaction applies:

| |||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined):

| |||

| (4) | Proposed maximum aggregate value of transaction:

| |||

| (5) | Total fee paid:

| |||

| ☐ | Fee paid previously with preliminary materials. | |||

| ☐ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | |||

| (1) | Amount Previously Paid:

| |||

| (2) | Form, Schedule or Registration Statement No.:

| |||

| (3) | Filing Party:

| |||

| (4) | Date Filed:

| |||

BLACKROCK MUNIYIELD CALIFORNIA FUND, INC.

BLACKROCK MUNIYIELD CALIFORNIA QUALITY FUND, INC.

BLACKROCK MUNIHOLDINGS CALIFORNIA QUALITY FUND, INC.

100 Bellevue Parkway

Wilmington, Delaware 19809

(800) 882-0052

December 22, 2021

Dear Preferred Shareholder:

You are cordially invited to attend a joint special shareholder meeting (the “Special Meeting”) of BlackRock MuniYield California Fund, Inc. (“MYC”), BlackRock MuniYield California Quality Fund, Inc. (“MCA”), BlackRock MuniHoldings California Quality Fund, Inc. (“MUC” or the “Acquiring Fund” and collectively with MYC and MCA, the “Funds,” and each, a “Fund”), to be held on February 4, 2022 at 11:00 a.m. (Eastern time). Because of our concerns regarding the coronavirus disease (COVID-19) pandemic, the Special Meeting will be held in a virtual meeting format only. Shareholders will not have to travel to attend the Special Meeting, but will be able to view the Special Meeting live, have a meaningful opportunity to participate, including the ability to ask questions of management, and cast their votes by accessing a web link. Before the Special Meeting, I would like to provide you with additional background information and ask for your vote on important proposals affecting the Funds.

Preferred Shareholders of MYC: You and the common shareholders of MYC are being asked to vote as a single class on a proposal to approve an Agreement and Plan of Reorganization between MYC and the Acquiring Fund (the “MYC Reorganization Agreement”) and the transactions contemplated therein, including the termination of MYC’s registration under the Investment Company Act of 1940, as amended (the “1940 Act”), and the dissolution of MYC under Maryland law (the “MYC Reorganization”). The Acquiring Fund has a similar investment objective and similar investment strategies, policies and restrictions as MYC, although there are some differences. In addition, you are being asked to vote as a separate class on a proposal to approve the MYC Reorganization Agreement and the MYC Reorganization.

Preferred Shareholders of MCA: You and the common shareholders of MCA are being asked to vote as a single class on a proposal to approve an Agreement and Plan of Reorganization between MCA and the Acquiring Fund (the “MCA Reorganization Agreement” and together with the MYC Reorganization Agreement, the “Reorganization Agreements”) and the transactions contemplated therein, including the termination of MCA’s registration under the 1940 Act and the dissolution of MCA under Maryland law (the “MCA Reorganization”). The Acquiring Fund has a similar investment objective and similar investment strategies, policies and restrictions as MCA, although there are some differences. In addition, you are being asked to vote as a separate class on a proposal to approve the MCA Reorganization Agreement and the MCA Reorganization.

Common Shareholders of the Acquiring Fund: You and the common shareholders of the Acquiring Fund are being asked to vote as a single class on a proposal to approve the issuance of additional common shares of the Acquiring Fund in connection with the MYC Reorganization and the MCA Reorganization (each, a “Reorganization”). In addition, you are being asked to vote as a separate class on a proposal to approve each Reorganization Agreement and the transactions contemplated therein.

The enclosed Proxy Statement is only being delivered to the Funds’ preferred shareholders. The common shareholders of each Fund are also being asked to attend the Special Meeting and to vote with respect to the proposals described above that require the vote of the common shareholders and preferred shareholders as a single class. Each Fund is delivering to its common shareholders a separate joint proxy statement/prospectus with respect to the proposals described above.

- 1 -

The Board of Directors of each Fund believes that the proposal that the preferred shareholders of its Fund are being asked to vote upon is in the best interests of its respective Fund and its shareholders and unanimously recommends that you vote “FOR” such proposal.

Your vote is important. Attendance at the Special Meeting will be limited to each Fund’s shareholders as of December 7, 2021, the record date for the Special Meeting.

If your shares in a Fund are registered in your name, you may attend and participate in the Special Meeting at https://meetnow.global/M5YSR7R by entering the control number found in the shaded box on your proxy card on the date and time of the Special Meeting. You may vote during the Special Meeting by following the instructions that will be available on the Special Meeting website during the Special Meeting.

If you are a beneficial shareholder of a Fund (that is if you hold your shares of a Fund through a bank, broker, financial intermediary or other nominee) and want to attend the Special Meeting you must register in advance of the Special Meeting. To register, you must submit proof of your proxy power (legal proxy), which you can obtain from your financial intermediary or other nominee, reflecting your Fund holdings along with your name and email address to Georgeson LLC, each Fund’s tabulator. You may email an image of your legal proxy to shareholdermeetings@computershare.com. Requests for registration must be received no later than 5:00 p.m. (Eastern time) three business days prior to the Special Meeting date. You will receive a confirmation email from Georgeson LLC of your registration and a control number and security code that will allow you to vote at the Special Meeting.

Even if you plan to attend the Special Meeting, please promptly follow the enclosed instructions to submit voting instructions by telephone or via the Internet. Alternatively, you may submit voting instructions by signing and dating each proxy card or voting instruction form you receive, and if received by mail, returning it in the accompanying postage-paid return envelope.

We encourage you to carefully review the enclosed materials, which explain the proposals in more detail. As a shareholder, your vote is important, and we hope that you will respond today to ensure that your shares will be represented at the meeting. You may vote using one of the methods below by following the instructions on your proxy card or voting instruction form(s):

| • | By touch-tone phone; |

| • | By internet; |

| • | By signing, dating and returning the enclosed proxy card or voting instruction form(s) in the postage-paid envelope; or |

| • | By participating at the Special Meeting as described above. |

If you do not vote using one of the methods described above, you may be called by Georgeson LLC, the Funds’ proxy solicitor, to vote your shares.

If you have any questions about the proposals to be voted on or the virtual Special Meeting, please call Georgeson LLC, the firm assisting us in the solicitation of proxies, toll free at 1-866-821-2614.

As always, we appreciate your support.

Sincerely,

JOHN M. PERLOWSKI

President and Chief Executive Officer of the Funds

- 2 -

Please vote now. Your vote is important.

To avoid the wasteful and unnecessary expense of further solicitation(s), we urge you to indicate your voting instructions on the enclosed proxy card, date and sign it and return it promptly in the postage-paid envelope provided, or record your voting instructions by telephone or via the internet, no matter how large or small your holdings may be. If you submit a properly executed proxy but do not indicate how you wish your preferred shares to be voted, your preferred shares will be voted “FOR” the proposal. If your preferred shares are held through a broker, you must provide voting instructions to your broker about how to vote your preferred shares in order for your broker to vote your preferred shares as you instruct at the Special Meeting.

- 3 -

December 22, 2021

IMPORTANT NOTICE

TO PREFERRED SHAREHOLDERS OF

BLACKROCK MUNIYIELD CALIFORNIA FUND, INC.

BLACKROCK MUNIYIELD CALIFORNIA QUALITY FUND, INC.

BLACKROCK MUNIHOLDINGS CALIFORNIA QUALITY FUND, INC.

QUESTIONS & ANSWERS

Although we urge you to read the entire Proxy Statement, we have provided for your convenience a brief overview of some of the important questions concerning the joint special shareholder meeting (the “Special Meeting”) of BlackRock MuniYield California Fund, Inc. (“MYC”) and BlackRock MuniYield California Quality Fund, Inc. (“MCA”) (together, the “Target Funds”) and BlackRock MuniHoldings California Quality Fund, Inc. (“MUC” or the “Acquiring Fund” and collectively with MYC and MCA, the “Funds,” and each, a “Fund”) and the proposals to be voted on. It is expected that the effective dates (collectively, the “Closing Date”) of the Reorganizations will be sometime during the second quarter of 2022, but they may be at a different time as described in the Proxy Statement.

The enclosed Proxy Statement is being sent only to (i) the holders of Variable Rate Muni Term Preferred Shares (“VMTP Shares” and the holders thereof, “VMTP Holders”) of the Acquiring Fund and (ii) the holders of Variable Rate Demand Preferred Shares (“VRDP Shares” and the holders thereof, “VRDP Holders”) of each Target Fund. Each Fund is separately soliciting the votes of its holders of shares of common stock (together with the VRDP Shares or VMTP Shares of each Fund, as applicable, the “Shares”) through a separate joint proxy statement/prospectus.

| Q: | Why is a shareholder meeting being held? |

| A: | Preferred Shareholders of BlackRock MuniYield California Fund, Inc. (NYSE Ticker: MYC): You and the common shareholders of MYC are being asked to vote as a single class on a proposal to approve an Agreement and Plan of Reorganization between MYC and the Acquiring Fund (the “MYC Reorganization Agreement”) and the transactions contemplated therein, including (i) the acquisition by the Acquiring Fund of substantially all of MYC’s assets and the assumption by the Acquiring Fund of substantially all of MYC’s liabilities in exchange solely for newly issued common shares and VMTP Shares of the Acquiring Fund, which will be distributed to the common shareholders (although cash may be distributed in lieu of fractional common shares) and VMTP Holders, respectively, of MYC, and which shall constitute the sole consideration to be distributed or paid to the common shareholders (although cash may be distributed in lieu of fractional common shares) and the VMTP Holders in respect of their common shares and VMTP Shares, respectively, and (ii) the termination by MYC of its registration under the Investment Company Act of 1940, as amended (the “1940 Act”), and the liquidation, dissolution and termination of MYC in accordance with its charter and Maryland law (the “MYC Reorganization”). If the MYC Reorganization Agreement is approved, prior to the Closing Date of the MYC Reorganization, it is expected that MYC will issue VMTP Shares, with terms substantially identical to the terms of the outstanding Acquiring Fund’s VMTP Shares and use the proceeds from such issuance to redeem all of MYC’s outstanding VRDP Shares (the “MYC VRDP Refinancing”). If the MYC VRDP Refinancing is not completed prior to the Closing Date of the MYC Reorganization, then the MYC Reorganization will not be consummated. |

You are also being asked to vote as a separate class on a proposal to approve the MYC Reorganization Agreement and the MYC Reorganization.

Preferred Shareholders of BlackRock MuniYield California Quality Fund (NYSE Ticker: MCA): You and the common shareholders of MCA are being asked to vote as a single class on a proposal to approve an Agreement and Plan of Reorganization between MCA and the Acquiring Fund (the “MCA Reorganization Agreement” and together with the MYC Reorganization Agreement, the “Reorganization Agreements”) and

i

the transactions contemplated therein, including (i) the acquisition by the Acquiring Fund of substantially all of MCA’s assets and the assumption by the Acquiring Fund of substantially all of MCA’s liabilities in exchange solely for newly issued common shares and VMTP Shares of the Acquiring Fund, which will be distributed to the common shareholders (although cash may be distributed in lieu of fractional common shares) and VMTP Holders, respectively, of MCA, and which shall constitute the sole consideration to be distributed or paid to the common shareholders (although cash may be distributed in lieu of fractional common shares) and the VMTP Holders in respect of their common shares and VMTP Shares, respectively, and (ii) the termination by MCA of its registration under the 1940 Act, and the liquidation, dissolution and termination of MCA in accordance with its charter and Maryland law (the “MCA Reorganization” and together with the MYC Reorganization, the “Reorganizations”). If the MCA Reorganization Agreement is approved, prior to the Closing Date of the MCA Reorganization, it is expected that MCA will issue VMTP Shares, with terms substantially identical to the terms of the outstanding Acquiring Fund’s VMTP Shares and use the proceeds from such issuance to redeem all of MCA’s outstanding VRDP Shares (the “MCA VRDP Refinancing” and together with the MYC VRDP Refinancing, the “VRDP Refinancings”). If the MCA VRDP Refinancing is not completed prior to the Closing Date of the MCA Reorganization, then the MCA Reorganization will not be consummated.

You are also being asked to vote as a separate class on a proposal to approve the MCA Reorganization Agreement and the MCA Reorganization.

Preferred Shareholders of BlackRock MuniHoldings California Quality Fund, Inc. (NYSE Ticker: MUC): You and the common shareholders of the Acquiring Fund are being asked to vote as a single class on a proposal to approve the issuance of additional common shares of the Acquiring Fund in connection with each Reorganization Agreement (each, an “Issuance” and collectively, the “Issuances”).

You are also being asked to vote as a separate class on a proposal to approve each Reorganization Agreement and the transactions contemplated therein, including amendments to the Articles Supplementary of Variable Rate Muni Term Preferred Shares of the Acquiring Fund (the “MUC Articles Supplementary”) in connection with the issuance of additional Acquiring Fund VMTP Shares. Such amendments to the MUC Articles Supplementary will include only changes related to the issuance of additional Acquiring Fund VMTP Shares in the Reorganizations.

The term “Combined Fund” refers to the Acquiring Fund as the surviving Fund after the consummation of each of the Reorganizations.

Each Reorganization is contingent upon the completion of the Target Fund’s respective VRDP Refinancing. If the respective VRDP Refinancing is not completed prior to the Closing Date of a Reorganization, then the Reorganization will not be consummated.

Neither Reorganization is contingent upon the approval of the other Reorganization. If a Reorganization is not consummated, the Fund for which such Reorganization(s) was not consummated would continue to exist and operate on a standalone basis.

| Q: | Why has each Fund’s Board recommended these proposals? |

| A: | The Board of Directors (each, a “Board” and each member thereof, a “Board Member”) of each Fund has determined that its Reorganization(s) is in the best interests of its Fund and that the interests of existing common shareholders and preferred shareholders of its Fund will not be diluted with respect to net asset value (“NAV”) and liquidation preference, respectively, as a result of the Reorganization. The Reorganizations seek to achieve certain economies of scale and other operational efficiencies by combining three funds that have similar investment objectives and similar investment strategies, policies and restrictions and are managed by the same investment adviser, BlackRock Advisors, LLC (the “Investment Advisor”). |

In light of these similarities, the Reorganizations are intended to reduce fund redundancies and create a single, larger fund that may benefit from anticipated operating efficiencies and economies of scale. The Reorganizations are intended to result in the following potential benefits to common shareholders:

| (i) | lower net total expenses per Common Share for common shareholders of each Fund (as common shareholders of the Combined Fund following the Reorganizations) due to economies of scale resulting from the larger size of the Combined Fund; |

ii

| (ii) | improved net earnings yield on NAV for common shareholders of each Fund other than MCA; |

| (iii) | improved secondary market trading of the common shares of the Combined Fund; and |

| (iv) | operating and administrative efficiencies for the Combined Fund, including the potential for the following: |

| (a) | greater investment flexibility and investment options; |

| (b) | greater diversification of portfolio investments; |

| (c) | the ability to trade portfolio securities in larger positions and more favorable transaction terms; |

| (d) | additional sources of leverage or more competitive leverage terms and more favorable transaction terms; |

| (e) | benefits from having fewer closed-end funds offering similar products in the market, including an increased focus by investors on the remaining funds in the market (including the Combined Fund) and additional research coverage; and |

| (f) | benefits from having fewer similar funds in the same fund complex, including a simplified operational model and a reduction in risk of operational, legal and financial errors. |

The Board of each Fund, including Board Members thereof who are not “interested persons” (as defined in the 1940 Act), approved its Reorganization Agreement(s) and the Issuances, as applicable, concluding that the Reorganization(s) is in the best interests of its Fund and that the interests of existing common shareholders and preferred shareholders of its Fund will not be diluted with respect to NAV and liquidation preference, respectively, as a result of the Reorganization(s). As a result of the Reorganizations, however, common and preferred shareholders of each Fund may hold a reduced percentage of ownership in the larger Combined Fund than they did in any of the individual Funds before the Reorganizations. Each Board’s conclusion was based on each Board Member’s business judgment after consideration of all relevant factors taken as a whole with respect to its Fund and the Fund’s common and preferred shareholders, although individual Board Members may have placed different weight on various factors and assigned different degrees of materiality to various factors.

Because the shareholders of each Fund will vote separately on the Fund’s respective Reorganization(s) or Issuances, as applicable, and each Reorganization is contingent upon the completion of the Target Fund’s respective VRDP Refinancing, there are multiple potential combinations of Reorganizations. To the extent either Reorganization is not completed, any expected expense savings by the Combined Fund, or other potential benefits resulting from the Reorganizations, may be reduced.

If a Reorganization is not consummated, then the Investment Advisor may, in connection with ongoing management of the Fund for which such Reorganization(s) was not consummated and its product line, recommend alternative proposals to the Board of that Fund.

| Q: | How will holders of preferred shares be affected by the Reorganizations? |

| A: | As of the date of the enclosed Proxy Statement, the Acquiring Fund has VMTP Shares outstanding and MYC and MCA each have VRDP Shares outstanding. As of December 6, 2021, MYC had 1,059 Series W-7 VRDP Shares outstanding, MCA had 1,665 Series W-7 VRDP Shares outstanding and the Acquiring Fund had 2,540 Series W-7 VMTP Shares outstanding. Pursuant to each VRDP Refinancing, it is expected that prior to the applicable Reorganization, all of the VRDP Shares of the Target Fund will be refinanced into Target Fund VMTP Shares, with terms substantially identical to those of the Acquiring Fund’s VMTP Shares. The dividend rate of the Target Fund VMTP Shares to be issued in each VRDP Refinancing will be based on a variable rate set weekly at a fixed rate spread to the Securities Industry and Financial Markets Association (SIFMA) Municipal Swap Index, whereas the dividend rate of the currently outstanding Target Fund VRDP Shares is set weekly by the remarketing agent for such VRDP Shares. See “Information About the Preferred Shares of the Funds” in the Proxy Statement for additional information about the preferred shares of each Fund. |

iii

In connection with the Reorganizations, and assuming that each VRDP Refinancing is completed prior to the Closing Date of the applicable Reorganization, the Acquiring Fund expects to issue 1,059 additional VMTP Shares to MYC VMTP Holders and 1,665 additional VMTP Shares to MCA VMTP Holders. Following the completion of the Reorganizations, the Combined Fund is expected to have 5,264 VMTP Shares outstanding. If the respective VRDP Refinancing is not completed prior to a Reorganization, then the Reorganization will not be consummated.

Assuming all of the Reorganizations are approved by shareholders, and each VRDP Refinancing is completed prior to the Closing Date of the Reorganizations, upon the Closing Date of the Reorganizations, MYC and MCA VMTP Holders will receive on a one-for-one basis one newly issued Acquiring Fund VMTP Share, par value $0.10 per share and with a liquidation preference of $100,000 per share (plus any accumulated and unpaid dividends that have accrued on the MYC or MCA VMTP Shares up to and including the day immediately preceding the Closing Date of the Reorganizations if such dividends have not been paid prior to the Closing Date), in exchange for each MYC or MCA VMTP Share held by the MYC or MCA VMTP Holders immediately prior to the Closing Date. The newly issued Acquiring Fund VMTP Shares may be of the same series as the Acquiring Fund’s outstanding VMTP Shares or a substantially identical series. No fractional Acquiring Fund VMTP Shares will be issued. The terms of the Acquiring Fund VMTP Shares to be issued in connection with the Reorganizations will be substantially identical to the terms of the Acquiring Fund’s outstanding VMTP Shares and will rank on parity with the Acquiring Fund’s outstanding VMTP Shares as to the payment of dividends and the distribution of assets upon dissolution, liquidation or winding up of the affairs of the Acquiring Fund. The newly issued Acquiring Fund VMTP Shares will have the same term redemption date applicable to the outstanding Acquiring Fund VMTP Shares as of the Closing Date of the Reorganization. Such term redemption date is March 30, 2023, unless extended. The Reorganizations will not result in any changes to the terms of the Acquiring Fund’s VMTP Shares currently outstanding.

The newly issued Acquiring Fund VMTP Shares will have terms that are substantially identical to the terms of the currently outstanding MYC and MCA VMTP Shares to be issued in connection with the VRDP Refinancings, including the same term redemption date of March 30, 2023 and the same dividend rate based on a variable rate set weekly at a fixed rate spread to the SIFMA Municipal Swap Index.

None of the expenses of the Reorganizations are expected to be borne by the VMTP Holders or the VRDP Holders, as applicable, of the Funds.

Following the Reorganizations, the VMTP Holders of each Fund will be VMTP Holders of the larger Combined Fund that will have a larger asset base and more VMTP Shares outstanding than any Fund individually before the Reorganizations. With respect to matters requiring all preferred shareholders to vote separately or common and preferred shareholders to vote together as a single class, following the Reorganizations, VMTP Holders of the Combined Fund may hold a smaller percentage of the outstanding preferred shares of the Combined Fund as compared to their percentage holdings of outstanding preferred shares of their respective Fund prior to the Reorganizations.

| Q: | How similar are the Funds? |

| A: | The Funds have the same investment adviser, officers and directors. MYC, MCA and the Acquiring Fund are each formed as a Maryland corporation. |

Each of the Acquiring Fund, MYC and MCA has its common shares listed on the NYSE. The Acquiring Fund has privately placed VMTP Shares outstanding. MYC and MCA each have privately placed VRDP Shares outstanding. MYC is managed by a team of investment professionals led by Theodore R. Jaeckel, Jr., CFA, Walter O’Connor, CFA and Michael Perilli. MCA is managed by a team of investment professionals led by Walter O’Connor, CFA and Michael Perilli. The Acquiring Fund is managed by a team of investment professionals lead by Walter O’Connor, CFA, Phillip Soccio, Michael Perilli and Kevin Maloney. Following the Reorganizations, it is expected that the Combined Fund will be managed by a team of investment professionals led by Michael Perilli and Kevin Maloney.

iv

The investment objective, significant investment strategies and operating policies, and investment restrictions of the Combined Fund will be those of the Acquiring Fund, which are similar to those of MYC and MCA, although there are some differences.

Investment Objective:

MYC | MCA | Acquiring Fund (MUC) | ||

| The Fund’s investment objective is to provide stockholders with as high a level of current income exempt from U.S. federal and California income taxes as is consistent with its investment policies and prudent investment management. | The Fund’s investment objective is to provide stockholders with as high a level of current income exempt from U.S. federal and California income taxes as is consistent with its investment policies and prudent investment management. | The Fund’s investment objective is to provide stockholders with current income exempt from regular federal income taxes and California personal income taxes. |

Municipal Bonds: Below is a comparison of each Fund’s investment policy with respect to municipal obligations issued by or on behalf of the State of California, its political subdivisions, agencies and instrumentalities and by other qualifying issuers that pay interest which, in the opinion of bond counsel to the issuer, is exempt from federal and California income taxes (except that the interest may be includable in taxable income for purposes of the federal alternative minimum tax) (“California Municipal Bonds”) and municipal obligations issued by or on behalf of states, territories and possessions of the United States and their political subdivisions, agencies or instrumentalities, each of which pays interest that is excludable from gross income for federal income tax purposes, in the opinion of bond counsel to the issuer, but is not excludable from gross income for California income tax purposes (“Municipal Bonds”). Unless otherwise noted, the term “Municipal Bonds” also includes California Municipal Bonds.

MYC | MCA | Acquiring Fund (MUC) | ||

| The Fund seeks to achieve its investment objective by investing, as a fundamental policy, at least 80% of an aggregate of the Fund’s net assets (including proceeds from the issuance of any preferred stock) and the proceeds of any borrowings for investment purposes, in a portfolio of California Municipal Bonds. The Fund also may invest in Municipal Bonds. | The Fund seeks to achieve its investment objective by investing, as a fundamental policy, at least 80% of an aggregate of the Fund’s net assets (including proceeds from the issuance of any preferred stock) and the proceeds of any borrowings for investment purposes, in a portfolio of California Municipal Bonds. The Fund also may invest in Municipal Bonds. | The Fund’s investment policies provide that the Fund will seek to achieve its investment objective by seeking to invest substantially all (a minimum of 80%) of its assets in California Municipal Bonds, except at times when, in the judgment of the Investment Advisor, California Municipal Bonds of sufficient quality and quantity are unavailable for investment at suitable prices by the Fund. The Fund’s investment policies provide that at all times, except during temporary defensive periods, the Fund will invest at least 65% of its assets in California Municipal Bonds and at least 80% of its assets in California Municipal Bonds and other long-term Municipal Bonds. |

Investment Grade and Non-Investment Grade Securities: Below is a comparison of each Fund’s policy with respect to investment in investment grade quality securities and non-investment grade quality securities. Investment grade quality means that such bonds are rated, at the time of investment, within the four highest

v

grades (Baa or BBB or better by Moody’s Investor Service, Inc. (“Moody’s”), S&P Global Ratings (“S&P) or Fitch Ratings (“Fitch”)) or are unrated but judged to be of comparable quality by the Investment Advisor. Below investment grade quality means securities rated at the time of purchase Ba or below by Moody’s, BB or below by S&P or Fitch, or securities determined by the Investment Advisor to be of comparable quality. Below investment grade quality is regarded as predominantly speculative with respect to the issuer’s capacity to pay interest and repay principal. Such securities commonly are referred to as “high yield” or “junk” bonds.

MYC | MCA | Acquiring Fund (MUC) | ||

| Under normal market conditions, the Fund expects to invest primarily in a portfolio of long-term Municipal Bonds that are commonly referred to as “investment grade” securities. The Fund may invest up to 20% of its total assets in securities that are rated below investment grade. | Under normal market conditions, the Fund expects to invest primarily in a portfolio of long-term Municipal Bonds that are commonly referred to as “investment grade” securities. The Fund may invest up to 20% of its managed assets in securities that are rated below investment grade. | The Fund’s investment policies provide that it will invest primarily in a portfolio of long-term, investment grade California Municipal Bonds. The Fund may invest up to 20% of its managed assets in securities that are rated below investment grade, subject to the Fund’s other investment policies. |

Bond Maturity: Below is a comparison of each Fund’s policy with respect to bond maturity.

MYC | MCA | Acquiring Fund (MUC) | ||

| The average maturity of the Fund’s portfolio securities varies from time to time based upon an assessment of economic and market conditions by the Investment Advisor. The Fund’s portfolio at any given time may include long-term, intermediate-term and short-term Municipal Bonds. | The average maturity of the Fund’s portfolio securities varies from time to time based upon an assessment of economic and market conditions by the Investment Advisor. The Fund’s portfolio at any given time may include long-term, intermediate-term and short-term Municipal Bonds. | The average maturity of the Fund’s portfolio securities varies from time to time based upon an assessment of economic and market conditions by the Investment Advisor. The Fund’s portfolio at any given time may include both long-term, intermediate-term and short-term California Municipal Bonds and Municipal Bonds. |

Leverage: Each Fund utilizes leverage through the issuance of either VMTP Shares or VRDP Shares and TOBs. See “The Acquiring Fund’s Investments—Leverage;” “General Risks of Investing in the Acquiring Fund—Leverage Risk;” and “General Risks of Investing in the Acquiring Fund—Tender Option Bond Risk.” Each of MYC and MCA currently leverages its assets through the use of VRDP Shares and TOBs. The Acquiring Fund currently leverages its assets through the use of VMTP Shares and TOBs. The Acquiring Fund is expected to continue to leverage its assets after the Closing Date of the Reorganizations through the use of VMTP Shares and TOBs. Please see “Information about the Preferred Shares of the Funds” in the Proxy Statement for additional information about the preferred shares of each Fund.

The annualized dividend rates for the preferred shares for each Fund’s most recent fiscal year ended July 31, 2021 were as follows:

Fund | Preferred Shares | Rate | ||||||

MYC | VRDP Shares | 0.14 | % | |||||

MCA | VRDP Shares | 0.14 | % | |||||

Acquiring Fund (MUC) | VMTP Shares | 0.82 | % | |||||

Please see below a comparison of certain important ratios related to (i) each Fund’s use of leverage as of December 6, 2021, (ii) the Combined Fund’s estimated use of leverage, assuming only the Reorganization of MYC into the Acquiring Fund had taken place as of December 6, 2021, (iii) the Combined Fund’s

vi

estimated use of leverage, assuming only the Reorganization of MCA into the Acquiring Fund had taken place as of December 6, 2021, and (iv) the Combined Fund’s estimated use of leverage, assuming the Reorganizations of all the Funds had taken place as of December 6, 2021.

Ratios | MYC | MCA | Acquiring Fund (MUC) | Pro forma Combined Fund (MYC into MUC) | Pro forma Combined Fund (MCA into MUC) | Pro forma Combined Fund (MYC and MCA into MUC) | ||||||||||||||||||

Asset Coverage Ratio | 429.7 | % | 432.8 | % | 355.2 | % | 377.1 | % | 385.9 | % | 394.7 | % | ||||||||||||

Regulatory Leverage Ratio(1) | 23.3 | % | 23.1 | % | 28.2 | % | 26.5 | % | 25.9 | % | 25.3 | % | ||||||||||||

Effective Leverage Ratio(2) | 37.7 | % | 39.7 | % | 37.4 | % | 37.5 | % | 38.5 | % | 38.3 | % | ||||||||||||

| (1) | Regulatory leverage consists of preferred shares issued by the Fund, which is a part of the Fund’s capital structure. Regulatory leverage is sometimes referred to as “1940 Act Leverage” and is subject to asset coverage limits set forth in the 1940 Act. |

| (2) | Effective leverage is a Fund’s effective economic leverage, and includes both regulatory leverage and the leverage effects of certain derivative investments in the Fund’s portfolio. Currently, the leverage effects of TOB inverse floater holdings, in addition to any regulatory leverage, are included in effective leverage ratios. |

| Q: | How will the Reorganizations be effected? |

| A: | Assuming a Reorganization receives the requisite shareholder approvals, as well as certain consents, confirmations and/or waivers from various third parties, including the liquidity provider with respect to the outstanding MYC and MCA VRDP Shares, and assuming the respective VRDP Refinancing is completed prior to the Closing Date of each Reorganization, the Acquiring Fund will acquire substantially all of a Target Fund’s assets and assume substantially all of such Target Fund’s liabilities in exchange solely for newly issued common shares and VMTP Shares of the Acquiring Fund, which will be distributed to the shareholders of the Target Fund (although cash will be distributed in lieu of fractional common shares). A Target Fund will then terminate its registration under the 1940 Act and liquidate, dissolve and terminate in accordance with its respective charter and Maryland law. If the respective VRDP Refinancing is not completed prior to the Closing Date of a Reorganization, the Reorganization will not be consummated. |

Shareholders of MYC and MCA will become shareholders of the Acquiring Fund. Common shareholders of MYC and MCA will receive newly issued common shares of the Acquiring Fund, par value $0.10 per share, the aggregate NAV (not the market value) of which will equal the aggregate NAV (not the market value) of the common shares of MYC and MCA such shareholders held immediately prior to the Closing Date (although common shareholders of MYC and MCA may receive cash for fractional common shares). The aggregate NAV of each Fund immediately prior to the applicable Reorganization will reflect accrued expenses associated with such Reorganization. The NAV of MYC and MCA common shares will not be diluted as a result of the Reorganizations. The common shareholders of each Fund have substantially similar voting rights and rights with respect to the payment of dividends and distribution of assets upon liquidation of their respective Fund and have no preemptive, conversion or exchange rights.

On the Closing Date of the Reorganizations, MYC and MCA VMTP Holders will receive on a one-for-one basis one newly issued Acquiring Fund VMTP Share, par value $0.10 per share and with a liquidation preference of $100,000 per share (plus any accumulated and unpaid dividends that have accrued on the MYC or MCA VMTP Shares up to and including the day immediately preceding the Closing Date of the Reorganizations if such dividends have not been paid prior to the Closing Date), in exchange for each MYC or MCA VMTP Share held by the MYC or MCA VMTP Holders immediately prior to the Closing Date. The newly issued Acquiring Fund VMTP Shares may be of the same series as the Acquiring Fund’s outstanding VMTP Shares or a substantially identical series. No fractional Acquiring Fund VMTP Shares will be issued. The terms of the Acquiring Fund VMTP Shares to be issued in connection with the Reorganizations will be substantially identical to the terms of the Acquiring Fund’s outstanding VMTP Shares and will rank on parity with the Acquiring Fund’s outstanding VMTP Shares as to the payment of dividends and the distribution of assets upon dissolution, liquidation or winding up of the affairs of the

vii

Acquiring Fund. The newly issued Acquiring Fund VMTP Shares will have the same term redemption date applicable to the outstanding Acquiring Fund VMTP Shares as of the Closing Date of the Reorganization. Such term redemption date is March 30, 2023, unless extended. The Reorganizations will not result in any changes to the terms of the Acquiring Fund’s VMTP Shares currently outstanding.

The newly issued Acquiring Fund VMTP Shares will have terms that are substantially identical to the terms of the outstanding MYC and MCA VMTP Shares to be issued in connection with the VRDP Refinancings, including the same term redemption date of March 30, 2023.

Shareholders of the Acquiring Fund will remain shareholders of the Acquiring Fund, which will have additional common shares and VMTP Shares outstanding after the Reorganizations.

| Q: | Will I have to pay any U.S. federal income taxes as a result of the Reorganizations? |

| A: | Each Reorganization is intended to qualify as a “reorganization” within the meaning of Section 368(a) of the Code. If a Reorganization so qualifies, in general, shareholders of MYC and MCA will recognize no gain or loss for U.S. federal income tax purposes upon the exchange of their common shares for Acquiring Fund Shares pursuant to their Reorganization (except with respect to cash received in lieu of fractional common shares). Additionally, each of MYC and MCA will recognize no gain or loss for U.S. federal income tax purposes by reason of its Reorganization. Neither the Acquiring Fund nor its shareholders will recognize any gain or loss for U.S. federal income tax purposes pursuant to the Reorganizations. |

As discussed above, shareholders of each Fund may receive distributions prior to, or after, the consummation of the Reorganizations, including distributions attributable to their proportionate share of each Fund’s undistributed net investment income declared prior to the consummation of the Reorganizations or the Combined Fund built-in gains, if any, recognized after the Reorganizations, when such income and gains are eventually distributed by the Combined Fund. To the extent that such a distribution is not an “exempt interest dividend” (as defined in the Code), the distribution may be taxable to shareholders for U.S. federal income tax purposes.

The Funds’ shareholders should consult their own tax advisers regarding the U.S. federal income tax consequences of the Reorganizations, as well as the effects of state, local and non-U.S. tax laws, including possible changes in tax laws.

| Q: | Will I have to pay any sales load, commission or other similar fees in connection with the Reorganizations? |

| A: | You will pay no sales loads or commissions in connection with the Reorganizations. Regardless of whether the Reorganizations are completed, however, the costs associated with the Reorganizations, including the costs associated with the Special Meeting, will be borne directly by each of the respective Funds incurring the expense as discussed more fully in the Proxy Statement. |

Common shareholders of each Fund will indirectly bear all or a portion of the costs of the Reorganizations. The expenses of the Reorganizations of MYC and MCA into the Acquiring Fund are estimated to be approximately $345,553 and $383,333, respectively, of which the Investment Advisor will bear approximately $60,009 and $42,974, respectively. For each of MYC and MCA, the costs of its Reorganization include estimated VRDP Refinancing costs of $79,450 and $79,450, respectively, which are expected to be amortized over one year by the Combined Fund. For the Acquiring Fund, the expenses of the applicable Reorganizations are estimated to be approximately $375,545, of which the Investment Advisor will bear approximately $110,355. The actual costs associated with the Reorganizations may be more or less than the estimated costs discussed herein.

VMTP Holders and VRDP Holders, as applicable, are not expected to bear any costs of the Reorganizations.

Neither the Funds nor the Investment Advisor will pay any direct expenses of shareholders arising out of or in connection with the Reorganizations (e.g., expenses incurred by the shareholder as a result of attending the Special Meeting, voting on the Reorganizations or other action taken by the shareholder in connection with the Reorganizations).

viii

| Q: | What shareholder approvals are required to complete the Reorganizations? |

| A: | The MYC Reorganization is contingent upon the following approvals: |

| 1. | The approval of the MYC Reorganization Agreement and the transactions contemplated therein, including the termination of MYC’s registration under the 1940 Act and the dissolution of MYC under Maryland law, by MYC’s common shareholders and VMTP Holders voting as a single class; |

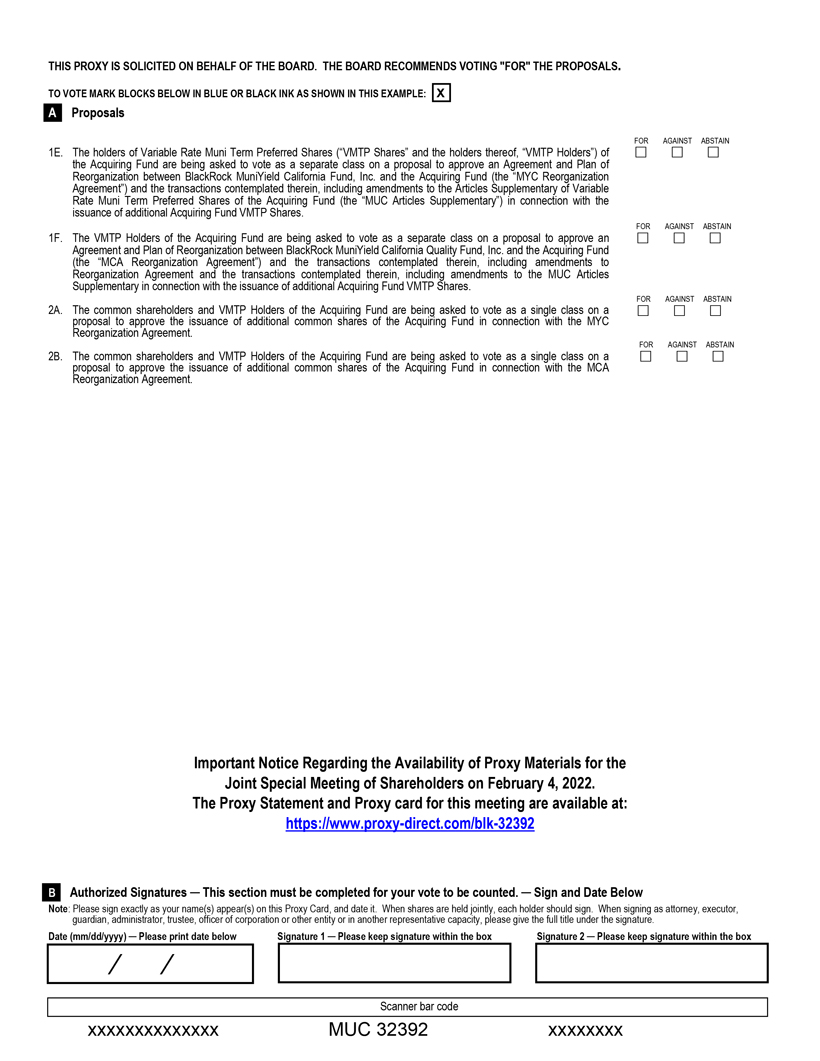

| 2. | The approval of the MYC Reorganization Agreement and the transactions contemplated therein, including the termination of MYC’s registration under the 1940 Act and the dissolution of MYC under Maryland law, by MYC’s VMTP Holders voting as a separate class; |

| 3. | The approval of the MYC Reorganization Agreement and the transactions contemplated therein, including amendments to MUC Articles Supplementary in connection with the issuance of additional Acquiring Fund VMTP Shares, by Acquiring Fund VMTP Holders voting as a separate class; and |

| 4. | The approval of the Issuance with respect to the MYC Reorganization by the Acquiring Fund’s common shareholders and Acquiring Fund VMTP Holders voting as a single class. |

The MCA Reorganization is contingent upon the following approvals:

| 1. | The approval of the MCA Reorganization Agreement and the transactions contemplated therein, including the termination of MCA’s registration under the 1940 Act and the dissolution of MCA under Maryland law, by MCA’s common shareholders and VMTP Holders voting as a single class; |

| 2. | The approval of the MCA Reorganization Agreement and the transactions contemplated therein, including the termination of MCA’s registration under the 1940 Act and the dissolution of MCA under Maryland law, by MCA’s VMTP Holders voting as a separate class; |

| 3. | The approval of the MCA Reorganization Agreement and the transactions contemplated therein, including amendments to the MUC Articles Supplementary in connection with the issuance of additional Acquiring Fund VMTP Shares, by Acquiring Fund VMTP Holders voting as a separate class; and |

| 4. | The approval of the Issuance with respect to the MCA Reorganization by the Acquiring Fund’s common shareholders and Acquiring Fund VMTP Holders voting as a single class. |

Each Reorganization is contingent upon the Target Fund’s VRDP Refinancing. If the respective VRDP Refinancing is not completed prior to the Closing Date of a Reorganization, then the Reorganization will not be consummated.

Neither Reorganization is contingent upon the approval of the other Reorganization. If a Reorganization is not consummated, the Fund for which such Reorganization(s) was not consummated would continue to exist and operate on a standalone basis.

If the requisite shareholder approvals for a Reorganization are not obtained, the VRDP Refinancing is not completed or a Reorganization is not otherwise consummated, the Board of the Fund for which such Reorganization(s) were not consummated may take such actions as it deems in the best interests of the Fund, including conducting additional solicitations with respect to the Reorganization(s) or continuing to operate the Fund as a standalone Maryland corporation registered under the 1940 Act as a closed-end management investment company advised by the Investment Advisor. The Investment Advisor may, in connection with the ongoing management of the Fund and its product line, recommend alternative proposals to the Board of the Fund.

In order for the Reorganizations to occur, each Fund must obtain all requisite shareholder approvals with respect to the Reorganizations, as well as certain consents, confirmations and/or waivers from various third parties, including the liquidity provider with respect to the outstanding VRDP Shares of the Target Funds. Because the closing of each Reorganization is contingent upon the applicable Fund and the Acquiring Fund

ix

obtaining the requisite shareholder approvals and third-party consents and satisfying (or obtaining the waiver of) other closing conditions, it is possible that a Reorganization will not occur, or that only one of MYC or MCA will be reorganized into the Acquiring Fund, even if shareholders of a Fund entitled to vote on the Reorganization approve the Reorganization and such Fund satisfies all of its closing conditions, if the other Fund does not obtain its requisite shareholder approvals or satisfy its closing conditions.

The preferred shares were issued on a private placement basis to one or a small number of institutional holders. Please see “Information about the Preferred Shares of the Funds” for additional information. To the extent that one or more preferred shareholder of MYC, MCA or the Acquiring Fund owns, holds or controls, individually or in the aggregate, all or a significant portion of such Fund’s outstanding preferred shares, the preferred shareholder approval required for a Reorganization may turn on the exercise of voting rights by such particular preferred shareholder(s) and its (or their) determination as to the favorability of the Reorganization with respect to its (or their) interests. The Funds exercise no influence or control over the determinations of such preferred shareholder(s) with respect to the Reorganizations; there is no guarantee that such preferred shareholder(s) will approve the Reorganizations, over which it (or they) may exercise effective disposition power.

| Q: | Why is the vote of shareholders of the Acquiring Fund being solicited in connection with the Reorganizations? |

| A: | The rules of the New York Stock Exchange (on which the Acquiring Fund common shares are listed) require the Acquiring Fund’s shareholders to approve each Issuance with respect to a Reorganization. If the Issuance with respect to a Reorganization is not approved, then the corresponding Reorganization will not occur. |

We are also seeking the approval of each Reorganization Agreement and the transactions contemplated therein, including amendments to the MUC Articles Supplementary in connection with the issuance of additional Acquiring Fund VMTP Shares, by the Acquiring Fund VMTP Holders voting as a separate class pursuant to the governing document of the Acquiring Fund VMTP Shares. If Acquiring Fund VMTP Holders do not approve a Reorganization Agreement as a separate class, then the corresponding Reorganization will not occur.

| Q: | How does the Board of my Fund suggest that I vote? |

| A: | After careful consideration, the Board of your Fund unanimously recommends that you vote “FOR” the proposal(s) relating to your Fund. |

| Q: | When and where will the Special Meeting be held? |

| A: | The Special Meeting will be held on February 4, 2022 at 11:00 a.m. (Eastern time). Because of our concerns regarding the coronavirus disease (COVID-19) pandemic, the Special Meeting will be held in virtual meeting format only. Shareholders will not have to travel to attend the Special Meeting, but will be able to view the Special Meeting live and cast their votes by accessing a web link. The Special Meeting will provide shareholders with a meaningful opportunity to participate, including the ability to ask questions of management. To support these efforts, the Funds will: |

| • | Provide for shareholders to begin logging into the Special Meeting at 10:30 a.m. (Eastern time) on February 4, 2022, thirty minutes in advance of the Special Meeting. |

| • | Permit shareholders attending the Special Meeting to submit questions via live webcast during the Special Meeting by following the instructions available on the meeting website during the Special Meeting. Questions relevant to Special Meeting matters will be answered during the Special Meeting, subject to time constraints. |

| • | Engage with and respond to shareholders who ask questions relevant to Special Meeting matters that are not answered during the Special Meeting due to time constraints. |

x

| Q: | How do I vote my proxy? |

| A: | Shareholders of record of each Fund as of the close of business on December 7, 2021 (the “Record Date”) are entitled to notice of and to vote at the Special Meeting or any adjournment or postponement thereof. You may cast your vote by mail, phone, internet or by participating at the Special Meeting as described below. |

To vote by mail, please mark your vote on the enclosed proxy card and sign, date and return the card in the postage-paid envelope provided.

If you choose to vote by phone or internet, please refer to the instructions found on the proxy card accompanying the Proxy Statement. To vote by phone or internet, you will need the “control number” that appears on the proxy card. In addition, we ask that you please note the following:

If your shares in a Fund are registered in your name, you may attend and participate in the Special Meeting at https://meetnow.global/M5YSR7R by entering the control number found in the shaded box in your proxy card on the date and timing of the Special Meeting. You may vote during the Special Meeting by following the instructions that will be available on the Special Meeting website during the Special Meeting.

Also, if you are a beneficial shareholder of a Fund, you will not be able to vote at the virtual Special Meeting unless you have registered in advance to attend the Special Meeting. To register, you must submit proof of your proxy power (legal proxy), which you can obtain from your financial intermediary or other nominee, reflecting your Fund holdings along with your name and email address to Georgeson LLC (“Georgeson”), each Fund’s tabulator. You may email an image of your legal proxy to shareholdermeetings@computershare.com. Requests for registration must be received no later than 5:00 p.m. (Eastern time) three business days prior to the Special Meeting date. You will receive a confirmation email from Georgeson of your registration and a control number and security code that will allow you to vote at the Special Meeting.

Even if you plan to attend the Special Meeting, please promptly follow the enclosed instructions to submit voting instructions by telephone or via the Internet. Alternatively, you may submit voting instructions by signing and dating each proxy card you receive, and if received by mail, returning it in the accompanying postage-paid return envelope.

| Q: | Whom do I contact for further information? |

| A: | You may contact your financial advisor for further information. You may also call Georgeson, the Funds’ proxy solicitor, at 1-866-821-2614. |

| Q: | Will anyone contact me? |

| A: | You may receive a call from Georgeson, the proxy solicitor hired by the Funds, to verify that you received your proxy materials, to answer any questions you may have about the proposals and to encourage you to vote your proxy. |

We recognize the inconvenience of the proxy solicitation process and would not impose on you if we did not believe that the matters being proposed were important. Once your vote has been registered with the proxy solicitor, your name will be removed from the solicitor’s follow-up contact list.

Your vote is very important. We encourage you as a shareholder to participate by returning your vote as soon as possible. If enough shareholders fail to cast their votes, a Fund may not be able to hold the Special Meeting or the vote on the applicable proposals, and will be required to incur additional solicitation costs in order to obtain sufficient shareholder participation.

Important additional information about the Reorganizations is set forth

in the accompanying Proxy Statement.

Please read it carefully.

xi

BLACKROCK MUNIYIELD CALIFORNIA FUND, INC.

BLACKROCK MUNIYIELD CALIFORNIA QUALITY FUND, INC.

BLACKROCK MUNIHOLDINGS CALIFORNIA QUALITY FUND, INC.

100 Bellevue Parkway

Wilmington, Delaware 19809

(800) 882-0052

NOTICE OF JOINT SPECIAL MEETING OF SHAREHOLDERS

TO BE HELD ON FEBRUARY 4, 2022

Notice is hereby given that a joint special meeting of shareholders (the “Special Meeting”) of BlackRock MuniYield California Fund, Inc. (NYSE Ticker: MYC) (“MYC”), BlackRock MuniYield California Quality Fund, Inc. (NYSE Ticker: MCA) (“MCA”) and BlackRock MuniHoldings California Quality Fund, Inc. (NYSE Ticker: MUC) (“MUC” or the “Acquiring Fund,” and collectively with MYC and MCA, the “Funds,” and each, a “Fund”) will be held on February 4, 2022 at 11:00 a.m. (Eastern time) for the following purposes:

Proposal 1: The Reorganizations of the Funds

For Shareholders of MYC:

Proposal 1(A): The common shareholders and holders of Variable Rate Demand Preferred Shares (“VRDP Shares” and the holders thereof, “VRDP Holders”) of MYC are being asked to vote as a single class on a proposal to approve an Agreement and Plan of Reorganization between MYC and the Acquiring Fund (the “MYC Reorganization Agreement”) and the transactions contemplated therein, including (i) the acquisition by the Acquiring Fund of substantially all of MYC’s assets and the assumption by the Acquiring Fund of substantially all of MYC’s liabilities in exchange solely for newly issued common shares and Variable Rate Muni Term Preferred Shares (“VMTP Shares” and the holders thereof, “VMTP Holders”) of the Acquiring Fund, which will be distributed to the common shareholders (although cash may be distributed in lieu of fractional common shares) and VMTP Holders, respectively, of MYC, and which shall constitute the sole consideration to be distributed or paid to the common shareholders (although cash may be distributed in lieu of fractional common shares) and the VMTP Holders in respect of their common shares and VMTP Shares, respectively, and (ii) the termination by MYC of its registration under the Investment Company Act of 1940, as amended (the “1940 Act”), and the liquidation, dissolution and termination of MYC in accordance with its charter and Maryland law (the “MYC Reorganization”). If the MYC Reorganization Agreement is approved, prior to the effective date of the MYC Reorganization, it is expected that MYC will issue VMTP Shares, with terms substantially identical to the terms of the outstanding Acquiring Fund’s VMTP Shares and use the proceeds from such issuance to redeem all of MYC’s outstanding VRDP Shares (the “MYC VRDP Refinancing”). If the MYC VRDP Refinancing is not completed prior to the effective date of the MYC Reorganization, then the MYC Reorganization will not be consummated.

Proposal 1(B): The VRDP Holders of MYC are being asked to vote as a separate class on a proposal to approve the MYC Reorganization Agreement and the MYC Reorganization.

For Shareholders of MCA:

Proposal 1(C): The common shareholders and VRDP Holders of MCA are being asked to vote as a single class on a proposal to approve an Agreement and Plan of Reorganization between MCA and the Acquiring Fund (the “MCA Reorganization Agreement” and together with the MYC Reorganization Agreement, the “Reorganization Agreements”) and the transactions contemplated therein, including (i) the acquisition by the Acquiring Fund of substantially all of MCA’s assets and the assumption by the Acquiring Fund of substantially all of MCA’s liabilities in exchange solely for newly issued common shares and VMTP Shares of the Acquiring

i

Fund, which will be distributed to the common shareholders (although cash may be distributed in lieu of fractional common shares) and VMTP Holders, respectively, of MCA, and which shall constitute the sole consideration to be distributed or paid to the common shareholders (although cash may be distributed in lieu of fractional common shares) and the VMTP Holders in respect of their common shares and VMTP Shares, respectively, and (ii) the termination by MCA of its registration under the 1940 Act, and the liquidation, dissolution and termination of MCA in accordance with its charter and Maryland law (the “MCA Reorganization” and together with the MYC Reorganization, the “Reorganizations”). If the MCA Reorganization Agreement is approved, prior to the effective date of the MCA Reorganization, it is expected that MCA will issue VMTP Shares, with terms substantially identical to the terms of the outstanding Acquiring Fund’s VMTP Shares and use the proceeds from such issuance to redeem all of MCA’s outstanding VRDP Shares (the “MCA VRDP Refinancing” and together with the MYC VRDP Refinancing, the “VRDP Refinancings”). If the MCA VRDP Refinancing is not completed prior to the effective date of the MCA Reorganization, then the MCA Reorganization will not be consummated.

Proposal 1(D): The VRDP Holders of MCA are being asked to vote as a separate class on a proposal to approve the MCA Reorganization Agreement and the MCA Reorganization.

For Shareholders of the Acquiring Fund:

Proposal 1(E): The VMTP Holders of the Acquiring Fund are being asked to vote as a separate class on a proposal to approve the MYC Reorganization Agreement and the transactions contemplated therein, including amendments to the Articles Supplementary of Variable Rate Muni Term Preferred Shares of the Acquiring Fund (the “MUC Articles Supplementary”) in connection with the issuance of additional Acquiring Fund VMTP Shares.

Proposal 1(F): The VMTP Holders of the Acquiring Fund are being asked to vote as a separate class on a proposal to approve the MCA Reorganization Agreement and the transactions contemplated therein, including amendments to the MUC Articles Supplementary in connection with the issuance of additional Acquiring Fund VMTP Shares.

Proposal 2: The Issuance of Additional Acquiring Fund Common Shares

Proposal 2(A): The common shareholders and VMTP Holders of the Acquiring Fund are being asked to vote as a single class on a proposal to approve the issuance of additional common shares of the Acquiring Fund in connection with the MYC Reorganization Agreement (the “MYC Issuance”).

Proposal 2(B): The common shareholders and VMTP Holders of the Acquiring Fund are being asked to vote as a single class on a proposal to approve the issuance of additional common shares of the Acquiring Fund in connection with the MCA Reorganization Agreement (the “MCA Issuance” and together with the MYC Issuance, the “Issuances”).

Each Reorganization is contingent upon the completion of the Target Fund’s respective VRDP Refinancing. If the respective VRDP Refinancing is not completed prior to the closing date of a Reorganization, then the Reorganization will not be consummated.

Neither Reorganization is contingent upon the approval of the other Reorganization. If a Reorganization is not consummated, the Fund for which such Reorganization(s) was not consummated would continue to exist and operate on a standalone basis.

Shareholders of record of each Fund as of the close of business on February 4, 2022 are entitled to notice of and to vote at the Special Meeting or any adjournment or postponement thereof.

ii

The Funds are soliciting the vote of their common shareholders on Proposal 1(A), Proposal 1(C), Proposal 2(A) and Proposal 2(B) through the joint proxy statement/prospectus.

Each Fund is separately soliciting the votes of its respective preferred shareholders on each proposal through a separate proxy statement and not through the joint proxy statement/prospectus.

Because of our concerns regarding the coronavirus disease (COVID-19) pandemic, the Special Meeting will be held in a virtual meeting format only. Shareholders will not have to travel to attend the Special Meeting but will be able to view the meeting live, have a meaningful opportunity to participate, including the ability to ask questions of management, and cast their votes by accessing a web link.

All shareholders are cordially invited to attend the Special Meeting. In order to avoid delay and additional expense for the Funds and to assure that your shares are represented, please vote as promptly as possible, regardless of whether or not you plan to attend the Special Meeting. You may vote by mail, by telephone or over the Internet. To vote by mail, please mark, sign, date and mail the enclosed proxy card or voting instruction form. No postage is required if mailed in the United States. To vote by telephone, please call the toll-free number located on your proxy card or voting instruction form and follow the recorded instructions. To vote over the Internet, go to the Internet address provided on your proxy card or voting instruction form and follow the instructions.

If your shares in a Fund are registered in your name, you may attend and participate in the Special Meeting at https://meetnow.global/M5YSR7R by entering the control number found in the shaded box on your proxy card on the date and time of the Special Meeting. You may vote during the Special Meeting by following the instructions that will be available on the Special Meeting website during the Special Meeting.

If you are a beneficial shareholder of a Fund (that is if you hold your Fund shares through a bank, broker, financial intermediary or other nominee) and want to attend the Special Meeting you must register in advance of the Special Meeting. To register, you must submit proof of your proxy power (legal proxy), which you can obtain from your financial intermediary or other nominee, reflecting your Fund holdings along with your name and email address to Georgeson LLC, each Fund’s tabulator. You may email an image of your legal proxy to shareholdermeetings@computershare.com. Requests for registration must be received no later than 5:00 p.m. (Eastern time) three business days prior to the Special Meeting date. You will receive a confirmation email from Georgeson LLC of your registration and a control number and security code that will allow you to vote at the Special Meeting.

Even if you plan to attend the Special Meeting, please promptly follow the enclosed instructions to submit voting instructions by telephone or via the Internet. Alternatively, you may submit voting instructions by signing and dating each proxy card or voting instruction form you receive, and if received by mail, returning it in the accompanying postage-paid return envelope.

The officers or directors of each Fund named as proxies by shareholders may participate in the Special Meeting by remote communications, including, without limitation, by means of a conference telephone or similar communications equipment by means of which all persons participating in the Special Meeting can hear and be heard by each other, and the participation of such officers or directors in the Special Meeting pursuant to any such communications system shall constitute presence at the Special Meeting.

THE BOARD OF DIRECTORS (EACH, A “BOARD”) OF EACH OF THE FUNDS RECOMMENDS THAT YOU VOTE YOUR SHARES BY INDICATING YOUR VOTING INSTRUCTIONS ON THE ENCLOSED PROXY CARD, DATING AND SIGNING SUCH PROXY CARD AND RETURNING IT IN THE ENVELOPE PROVIDED, WHICH IS ADDRESSED FOR YOUR CONVENIENCE AND NEEDS NO POSTAGE IF MAILED IN THE UNITED STATES, OR BY RECORDING YOUR VOTING INSTRUCTIONS BY TELEPHONE OR VIA THE INTERNET.

iii

THE BOARD OF EACH FUND UNANIMOUSLY RECOMMENDS THAT YOU CAST YOUR VOTE FOR THE APPLICABLE REORGANIZATION AGREEMENT AND FOR THE ISSUANCE OF ADDITIONAL COMMON SHARES OF THE ACQUIRING FUND, AS APPLICABLE, IN EACH CASE, AS DESCRIBED IN THE JOINT PROXY STATEMENT/PROSPECTUS FOR COMMON SHAREHOLDERS OR THE PROXY STATEMENT FOR PREFERRED SHAREHOLDERS, AS APPLICABLE.

IN ORDER TO AVOID THE ADDITIONAL EXPENSE OF FURTHER SOLICITATION, WE ASK THAT YOU MAIL YOUR PROXY CARD OR RECORD YOUR VOTING INSTRUCTIONS BY TELEPHONE OR VIA THE INTERNET PROMPTLY.

For the Board of each Fund

JOHN M. PERLOWSKI

President and Chief Executive Officer of the Funds

December 22, 2021

YOUR VOTE IS IMPORTANT.

PLEASE VOTE PROMPTLY BY SIGNING AND RETURNING THE ENCLOSED PROXY CARD OR BY RECORDING YOUR VOTING INSTRUCTIONS BY TELEPHONE OR VIA THE INTERNET, NO MATTER HOW MANY SHARES YOU OWN.

IMPORTANT NOTICE REGARDING THE AVAILABILITY OF PROXY MATERIALS FOR THE JOINT SPECIAL MEETING OF SHAREHOLDERS TO BE HELD ON FEBRUARY 4, 2022.

THE PROXY STATEMENT FOR THIS MEETING IS AVAILABLE AT:

www.proxy-direct.com/blk-32392

iv

PROXY STATEMENT

Dated December 22, 2021

BLACKROCK MUNIYIELD CALIFORNIA FUND, INC.

BLACKROCK MUNIYIELD CALIFORNIA QUALITY FUND, INC.

BLACKROCK MUNIHOLDINGS CALIFORNIA QUALITY FUND, INC.

100 Bellevue Parkway

Wilmington, Delaware 19809

(800) 882-0052

This Proxy Statement is furnished to you as a holder of (i) Variable Rate Demand Preferred Shares (“VRDP Shares” and the holders thereof “VRDP Holders”) of BlackRock MuniYield California Fund, Inc. (NYSE Ticker: MYC) (“MYC”); and/or VRDP Shares of BlackRock MuniYield California Quality Fund, Inc. (NYSE Ticker: MCA) (“MCA”); and/or Variable Rate Muni Term Preferred Shares (“VMTP Shares” and the holders thereof, “VMTP Holders”) of BlackRock MuniHoldings California Quality Fund, Inc. (NYSE Ticker: MUC) (“MUC” or the “Acquiring Fund” and collectively with MYC and MCA, the “Funds,” and each, a “Fund”) in connection with the solicitation of proxies by each Fund’s Board of Directors (the “Board,” the members of which are referred to as “Board Members”). Each of MYC and MCA may be referred to herein individually as a “Target Fund” or collectively as the “Target Funds.” The proxies will be voted at the joint special meeting of the shareholders of each Fund and at any and all adjournments, postponements and delays thereof (the “Special Meeting”). The Special Meeting will be held on February 4, 2022 at 11:00 a.m. (Eastern time) to consider the proposals set forth below and discussed in greater detail elsewhere in this Proxy Statement. Because of our concerns regarding the coronavirus disease (COVID-19) pandemic, the Special Meeting will be held in a virtual meeting format only. Shareholders will not have to travel to attend the Special Meeting, but will be able to view the meeting live, have a meaningful opportunity to participate, including the ability to ask questions of management, and cast their votes by accessing a web link. If you are unable to attend the Special Meeting or any adjournment or postponement thereof, the Board of your Fund recommends that you vote your preferred shares, by completing and returning the enclosed proxy card or by recording your voting instructions by telephone or via the internet. The approximate mailing date of this Proxy Statement and accompanying form of proxy is December 22, 2021.

The purposes of the Special Meeting are:

Proposal 1: The Reorganizations of the Funds

For Shareholders of MYC:

Proposal 1(A): The common shareholders and VRDP Holders of MYC are being asked to vote as a single class on a proposal to approve an Agreement and Plan of Reorganization between MYC and the Acquiring Fund (the “MYC Reorganization Agreement”) and the transactions contemplated therein, including (i) the acquisition by the Acquiring Fund of substantially all of MYC’s assets and the assumption by the Acquiring Fund of substantially all of MYC’s liabilities in exchange solely for newly issued common shares and VMTP Shares of the Acquiring Fund, which will be distributed to the common shareholders (although cash may be distributed in lieu of fractional common shares) and VMTP Holders, respectively, of MYC, and which shall constitute the sole consideration to be distributed or paid to the common shareholders (although cash may be distributed in lieu of fractional common shares) and the VMTP Holders in respect of their common shares and VMTP Shares, respectively, and (ii) the termination by MYC of its registration under the Investment Company Act of 1940, as amended (the “1940 Act”), and the liquidation, dissolution and termination of MYC in accordance with its charter and Maryland law (the “MYC Reorganization”). If the MYC Reorganization Agreement is approved, prior to the effective date of the MYC Reorganization, it is expected that MYC will issue VMTP Shares, with terms substantially identical to the terms of the outstanding Acquiring Fund’s VMTP Shares and use the proceeds

i

from such issuance to redeem all of MYC’s outstanding VRDP Shares (the “MYC VRDP Refinancing”). If the MYC VRDP Refinancing is not completed prior to the effective date of the MYC Reorganization, then the MYC Reorganization will not be consummated.

Proposal 1(B): The VRDP Holders of MYC are being asked to vote as a separate class on a proposal to approve the MYC Reorganization Agreement and the MYC Reorganization.

For Shareholders of MCA:

Proposal 1(C): The common shareholders and VRDP Holders of MCA are being asked to vote as a single class on a proposal to approve an Agreement and Plan of Reorganization between MCA and the Acquiring Fund (the “MCA Reorganization Agreement” and together with the MYC Reorganization Agreement, the “Reorganization Agreements”) and the transactions contemplated therein, including (i) the acquisition by the Acquiring Fund of substantially all of MCA’s assets and the assumption by the Acquiring Fund of substantially all of MCA’s liabilities in exchange solely for newly issued common shares and VMTP Shares of the Acquiring Fund, which will be distributed to the common shareholders (although cash may be distributed in lieu of fractional common shares) and VMTP Holders, respectively, of MCA, and which shall constitute the sole consideration to be distributed or paid to the common shareholders (although cash may be distributed in lieu of fractional common shares) and the VMTP Holders in respect of their common shares and VMTP Shares, respectively, and (ii) the termination by MCA of its registration under the 1940 Act, and the liquidation, dissolution and termination of MCA in accordance with its charter and Maryland law (the “MCA Reorganization” and together with the MYC Reorganization, the “Reorganizations”). If the MCA Reorganization Agreement is approved, prior to the effective date of the MCA Reorganization, it is expected that MCA will issue VMTP Shares, with terms substantially identical to the terms of the outstanding Acquiring Fund’s VMTP Shares and use the proceeds from such issuance to redeem all of MCA’s outstanding VRDP Shares (the “MCA VRDP Refinancing” and together with the MYC VRDP Refinancing, the “VRDP Refinancings”). If the MCA VRDP Refinancing is not completed prior to the effective date of the MCA Reorganization, then the MCA Reorganization will not be consummated.

Proposal 1(D): The VRDP Holders of MCA are being asked to vote as a separate class on a proposal to approve the MCA Reorganization Agreement and the MCA Reorganization.

For Shareholders of the Acquiring Fund:

Proposal 1(E): The VMTP Holders of the Acquiring Fund are being asked to vote as a separate class on a proposal to approve the MYC Reorganization Agreement and the transactions contemplated therein, including amendments to the Articles Supplementary of Variable Rate Muni Term Preferred Shares of the Acquiring Fund (the “MUC Articles Supplementary”) in connection with the issuance of additional Acquiring Fund VMTP Shares.

Proposal 1(F): The VMTP Holders of the Acquiring Fund are being asked to vote as a separate class on a proposal to approve the MCA Reorganization Agreement and the transactions contemplated therein, including amendments to the MUC Articles Supplementary in connection with the issuance of additional Acquiring Fund VMTP Shares.

Proposal 2: The Issuance of Additional Acquiring Fund Common Shares

Proposal 2(A): The common shareholders and VMTP Holders of the Acquiring Fund are being asked to vote as a single class on a proposal to approve the issuance of additional common shares of the Acquiring Fund in connection with the MYC Reorganization Agreement (the “MYC Issuance”).

Proposal 2(B): The common shareholders and VMTP Holders of the Acquiring Fund are being asked to vote as a single class on a proposal to approve the issuance of additional common shares of the Acquiring Fund in connection with the MCA Reorganization Agreement (the “MCA Issuance” and together with the MYC Issuance, the “Issuances”).

ii

It is expected that the effective dates (collectively, the “Closing Date”) of the Reorganizations will be sometime during the second quarter of 2022, but they may be at a different time as described herein. The term “Combined Fund” refers to the Acquiring Fund as the surviving Fund after the consummation of each of the Reorganizations.

Each Reorganization is contingent upon the completion of the Target Fund’s respective VRDP Refinancing. If the respective VRDP Refinancing is not completed prior to the Closing Date of a Reorganization, then the Reorganization will not be consummated.

Neither Reorganization is contingent upon the approval of the other Reorganization. If a Reorganization is not consummated, the Fund for which such Reorganization(s) was not consummated would continue to exist and operate on a standalone basis.

The Board of each Fund has determined that including these proposals applicable to preferred shareholders of the Funds in one Proxy Statement will reduce costs and is in the best interest of each Fund’s shareholders.

Distribution to the shareholders of this Proxy Statement and the accompanying materials will commence on or about December 22, 2021.

Shareholders of record of each Fund as of the close of business on December 7, 2021 (the “Record Date”) are entitled to notice of and to vote at the Special Meeting or any adjournment or postponement thereof.

Shareholders of each Fund are entitled to one vote for each common share or VMTP Share or VRDP Share, as applicable (each, a “Share”), held, with no Shares having cumulative voting rights. Preferred shareholders of each Fund will have equal voting rights with the common shareholders of such Fund with respect to the proposals that require the vote of the Fund’s VMTP Shares or VRDP Shares, as applicable, and common shares as a single class. The quorum and voting requirements for each Fund are described in the section herein entitled “Vote Required and Manner of Voting Proxies.”

This Proxy Statement is only being delivered to the preferred shareholders of each Fund. Each Fund is separately soliciting the votes of its respective common shareholders on each of the foregoing proposals that require the vote of the common shareholders and preferred shareholders as a single class through a separate joint proxy statement/prospectus and not through this Proxy Statement.