UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

X ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2015

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES

EXCHANGE ACT OF 1934

OR

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES

EXCHANGE ACT OF 1934

Date of event requiring this shell company report _____________

For the transition period from _____________ to _____________

Commission file number 0-20486

COMPAÑIA CERVECERIAS UNIDAS S.A.

(Exact name of Registrant as specified in its charter)

UNITED BREWERIES COMPANY, INC.

(Translation of Registrant's name into English)

Republic of Chile

(Jurisdiction of incorporation or organization)

Vitacura 2670, Twenty-Third Floor, Santiago, Chile

(Address of principal executive offices)

Felipe Dubernet, (562-24273536),fdubern@ccu.cl Vitacura 2670, Twenty-Third Floor, Santiago, Chile

(Name, Telephone, Email and/or Facsimile number and Address of Company Contact Person)

_________________________________________

Securities registered or to be registered pursuant to section 12(b) of the Act.

Name of each exchange

Title of each class on which registered

American Depositary Shares New York Stock Exchange

Representing Common Stock

Common Stock, without par value New York Stock Exchange*

__________

* Not for trading, but only in connection with the registration of American Depositary Shares which are evidenced by American Depositary Receipts

Securities registered or to be registered pursuant to Section 12(g) of the Act.

Not applicable

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

Not applicable

Indicate the number of outstanding shares of each of the issuer's classes of capital or common stock as of the close of the period covered by the annual report.

Common stock, with no par value: 369,502,872

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

YES X NO____

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

YES NO X

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

YES X NO_____

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

YES NO__

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer X Accelerated filer Non-accelerated filer____

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

U.S. GAAP International Financial Reporting Standards as issued Other____

by the International Accounting Standards Board X

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

ITEM 17 ITEM 18__

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

YES NO X

Introduction

In this annual report on Form 20-F, all references to “we,” “us,” “Company” or “CCU” are to Compañía Cervecerías Unidas S.A., an open stock corporation (sociedad anónima abierta) organized under the laws of the Republic of Chile, and its consolidated subsidiaries. Chile is divided into regions, each of which is known by its roman number (e.g. “Region XI”). Our fiscal year ends on December 31st. The expression “last three years’’ means the years ended December 31, 2013, 2014 and 2015. Unless otherwise specified, all references to “U.S. dollars” “dollars” “USD” or “US$” are to United States dollars, and references to “Chilean pesos” “pesos” “Ch$” or “CLP” are to Chilean pesos. We prepare our financial statements in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”). See the notes to our consolidated financial statements included in pages F-1 through F-104 of this annual report. We use the metric system of weights and measures in calculating our operating and other data. The United States equivalent units of the most common metric units used by us are as shown below:

1 liter = 0.2642 gallons | 1 gallon = 3.7854 liters |

1 liter = 0.008522 US beer barrels | 1 US beer barrel = 117.34 liters |

1 liter = 0.1761 soft drink unit cases (8 oz cans) | 1 soft drink unit case (8 oz cans) = 5.6775 liters |

1 liter = 0.1174 beer unit cases (12 oz cans). | 1 beer unit case (12 oz cans) = 8.5163 liters |

1 hectoliter = 100 liters | 1 liter = 0.01 hectoliters |

1 US beer barrel = 31 gallons | 1 gallon = 0.0323 US beer barrels |

1 hectare = 2.4710 acres | 1 acre = 0.4047 hectares |

1 mile = 1.6093 kilometers | 1 kilometer = 0.6214 miles |

i

Forward Looking Statements

This annual report contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, which we refer to as the “Securities Act,” and Section 21E of the Securities and Exchange Act of 1934, which we refer to as the “Exchange Act.” These statements relate to analyses and other information, which are based on forecasts of future results and estimates of amounts not yet determinable. They also relate to our future prospects, development and business strategies.

These forward-looking statements are identified by the use of terms and phrases such as “anticipate;” “believes;” “could;” “expects;” “intends;” “may;” “plans;” “predicts;” “projects;” “will” and similar terms and phrases. We caution you that actual results could differ materially from those expected by us, depending on the outcome of certain factors, including, without limitation:

· our success in implementing our investment and capital expenditure program;

· the nature and extent of future competition in our principal marketing areas;

· the nature and extent of a global financial disruption and its consequences;

· political and economic developments in Chile, Argentina and other countries where we currently conduct business or may conduct business in the future, including other Latin American countries; and

· other factors discussed under “Item 3: Key Information – Risk Factors,” “Item 4: Information on the Company” and “Item 5: Operating and Financial Review and Prospects.”

You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this annual report. We undertake no obligation to publically update any of these forward-looking statements to reflect events or circumstances after the date of this annual report, including, without limitation, changes in our business strategy or planned capital expenditures, or to reflect the occurrence of unanticipated events.

ii

PART I

ITEM 1: Identity of Directors, Senior Management and Advisers

Not applicable.

ITEM 2: Offer Statistics and Expected Timetable

Not applicable.

ITEM 3: Key Information

Selected Financial Data

The following table presents selected consolidated financial data as of and for the years ended December 31, 2015, 2014 and 2013 which has been derived from our consolidated financial statements prepared in accordance with IFRS and included elsewhere in this annual report, and as of and for the years ended December 31, 2012 and 2011 which has been derived from our consolidated financial statements prepared in accordance with IFRS and not included in this annual report. The financial data set forth below should be read in conjunction with the consolidated financial statements and related notesand “Item 5: Operating and Financial Review and Prospects” included elsewhere in this annual report.

| | | Year ended December 31, |

| IFRS | | 2011 | 2012 | 2013 | 2014 | 2015 |

1. Income Statement Data: | (million of CLP)(1) |

| Net sales | | 969,551 | 1,075,690 | 1,197,227 | 1,297,966 | 1,498,372 |

| Gross margin | 521,689 | 582,603 | 660,530 | 693,429 | 813,296 |

| Operating Result(2) | 192,818 | 181,188 | 188,266 | 179,920 | 204,937 |

| Other gains (losses) | 3,010 | -4,478 | 959 | 4,037 | 8,512 |

| Net financing expenses | -7,324 | -9,362 | -15,830 | -10,821 | -15,256 |

| Results as per adjustment units | -6,728 | -5,058 | -1,802 | -4,159 | -3,283 |

| Foreign currency exchange differences | -1,079 | -1,003 | -4,292 | -613 | 958 |

| Income taxes | | -45,196 | -37,133 | -34,705 | -46,674 | -50,115 |

| | | | | | | |

| Net income for the year: | 134,802 | 123,977 | 132,905 | 120,792 | 140,526 |

| Attributable to: | | | | | |

| Equity holders of the Parent Company | 122,752 | 114,433 | 123,036 | 106,238 | 120,808 |

| Non-controlling interests | 12,051 | 9,544 | 9,869 | 14,553 | 19,717 |

| | | | | | | |

| Basic and Diluted Income per share | 385.40 | 359.28 | 370.81 | 287.52 | 326.95 |

| Basic and Diluted Income per ADS(3) | 770.80 | 718.57 | 741.61 | 575.04 | 653.90 |

| Dividend per share (4) | 192.7 | 179.6 | 166.5 | 161.8 | 163.5 |

| Dividend per ADS in US$(3)(4) | 0.78 | 0.76 | 0.61 | 0.52 | 0.47 |

| Weighted average shares outstanding (000) | 318,503 | 318,503 | 331,806 | 369,503 | 369,503 |

| Shares outstanding as of December 31 (000) | 318,503 | 318,503 | 369,503 | 369,503 | 369,503 |

3

| | | Year ended December 31, |

| IFRS | | 2011 | 2012 | 2013 | 2014 | 2015 |

2. Balance Sheet Data: | (Million of CLP) (1) |

| | | | | | | |

| Total assets | | 1,298,365 | 1,328,710 | 1,727,720 | 1,768,901 | 1,823,357 |

| Total non-current liabilities | 251,026 | 303,662 | 234,347 | 242,070 | 247,144 |

| Total Financial debt (5) | 258,969 | 263,997 | 263,251 | 199,853 | 180,901 |

| Capital stock | | 231,020 | 231,020 | 562,693 | 562,693 | 562,693 |

| Subtotal Equity attributable to equity holders of the parent company | 568,976 | 613,220 | 988,676 | 1,025,588 | 1,057,816 |

| Total shareholders' equity | 684,786 | 710,518 | 1,084,244 | 1,148,500 | 1,187,522 |

3. Other Data | | | | | | |

| Sales volume (in millions of liters): | | | | | |

| Total volume | 1,839.7 | 1,990.9 | 2,191.6 | 2,289.8 | 2,391.0 |

| Chile Operating segment(6) | 1,260.4 | 1,384.4 | 1,557.0 | 1,621.6 | 1,686.5 |

| International Business Operating segment(7) | 458.1 | 478.9 | 507.1 | 537.5 | 569.7 |

| Wine Operating segment(8) | 121.2 | 127.6 | 127.4 | 130.6 | 134.8 |

(1) | Except for the number of shares outstanding, per share and per ADS amounts and sales volume. |

(2) | Defined, for management purposes, as earnings before other gains (losses), net financial expenses, equity and income of joint ventures, foreign currency exchange differences, results as per adjustment units and income taxes. Please see “Item 5: Operating and Financial Review and Prospects—OPERATING RESULT” for more details regarding Operating Result and a reconciliation of the most directly applicable IFRS measure to Operating Result. |

(3) | Per ADS amounts are determined by multiplying per share amounts by 2. As of December 20, 2012, there was an ADR ratio change from 1 ADR to 5 common shares, to a new ratio of 1 ADR to 2 common shares. |

(4) | Dividends per share are expressed in Chilean pesos as of payment dates, with charge to prior year's net income. Dividends per ADS are expressed in U.S. dollars at the conversion rate in effect on the date on which payment is made. |

(5) | Includes short-term and long-term financial debt (mainly bank loans, bonds and financial leasing). |

(6) | Includes sales of beer, non-alcoholic beverages and spirits in Chile. |

(7) | Includes sales of beer, non-alcoholic beverages and spirits in Argentina, Paraguay and Uruguay. |

(8) | Includes domestic and export sales to more than 80 countries. Excludes bulk wine sales. |

Exchange Rates.Prior to 1989, Chilean law permitted the purchase and sale of foreign currency only in those cases explicitly authorized by the Central Bank of Chile. The Central Bank Act, which was enacted in 1989, liberalized the rules that govern the ability to buy and sell foreign currency. Currently, pursuant to the Central Bank Act, the Central Bank of Chile has the authority to mandate that certain purchases and sales of foreign currency specified by law are to be carried out in the formal exchange market. The formal exchange market is formed by banks and other entities authorized by the Central Bank of Chile. All payments and distributions made to our holders of ADSs must be transacted in the formal exchange market.

In order to keep fluctuations in the average exchange rate within certain limits, the Central Bank of Chile has in the past intervened by buying or selling foreign currency on the formal exchange market. In September 1999, the Central Bank of Chile decided to limit its formal commitment to intervene and decided to exercise it only under extraordinary circumstances, which are to be announced in advance. The Central Bank of Chile also committed to provide periodic information about the levels of its international reserves.

The observed exchange rate is the average exchange rate at which commercial banks conduct authorized transactions on a given date, as certified by the Central Bank of Chile. The Central Bank of Chile generally carries out its transactions at the spot market rate. Authorized transactions by banks are now generally conducted at the spot market rate.

Purchases and sales of foreign currencies effectuated outside the formal exchange market are carried out in theMercado Cambiario Informal (the informal exchange market). The informal exchange market reflects the supply and demand for foreign currency. There are no limits imposed on the extent to which the rate of exchange in the informal exchange market can fluctuate above or below the observed exchange rate. On April 1, 2016 the U.S. dollar observed exchange rate relating to March 31, 2016 was CLP 669.80 per U.S. dollar.

4

The following table sets forth the low, high, average and period-end observed exchange rates for U.S. dollars for each of the indicated periods starting in 2011 as reported by the Central Bank of Chile. The Federal Reserve Bank of New York does not report a noon buying rate for Chilean pesos.

| Daily Observed Exchange Rate(1) |

| (CLP per USD) |

| Low(2) | High (2) | Average(3) | Period-end(4) |

| | | | |

2011 | 455.91 | 533.74 | 483.57 | 519.20 |

2012 | 469.65 | 519.69 | 486.58 | 479.96 |

2013 | 466.50 | 533.95 | 495.53 | 524.61 |

2014 | 524.61 | 621.41 | 570.50 | 606.75 |

2015 | 597.10 | 715.66 | 654.79 | 710.16 |

October 2015 | 673.91 | 695.53 | 684.48 | 690.32 |

November 2015 | 688.94 | 715.66 | 705.00 | 711.20 |

December 2015 | 693.72 | 711.52 | 704.39 | 710.16 |

January 2016 | 710.16 | 730.31 | 721.40 | 710.37 |

February 2016 | 689.18 | 715.41 | 703.31 | 694.17 |

March 2016 | 669.80 | 694.82 | 681.02 | 669.80 |

Source: Bloomberg | | | | |

(1) Historical pesos. | | | | |

(2) Rates shown are the actual low and high, on a day-by-day basis for each period. | | |

(3) For yearly data, the average of monthly average rates during the period reported, and for monthly data, the average of daily average rates during the period reported. |

(4) Published on the first day after month(year) end. |

The exchange rate on April 22, 2016, the latest practicable date, was CLP 666.80per U.S. dollar.

Capitalization and Indebtedness

Not applicable.

Reasons for the Offer and Use of Proceeds

Not applicable.

5

Risk Factors

RISKS RELATING TO CHILE

We are substantially dependent on economic conditions in Chile, which may adversely impact the results of our operations and financial condition.

We are predominantly engaged in business in Chile.60% of our sales revenues in 2015 was generated from our Chile Operating segment,27% came from the International Business Operating segment, which includes Argentina, Paraguay and Uruguay, and13% came from the Wine Operating segment. Thus, the results of our operations and financial condition are dependent to a large extent on the overall level of economic activity in Chile. The Chilean economy has experienced an average annual growth rate of3.8% between 2010 and 2015, and2.1% in 2015. In the past, slower economic growth in Chile has slowed down the rate of consumption of our products and adversely affected our profitability. Chile’s economic performance was affected by the disruption in the global financial markets in 2009 and catastrophic events such as earthquakes in the years 2010 and 2015. Therefore growth rates of past periods cannot be extrapolated to future performance.

Furthermore, Chile, as an emerging market economy, is more exposed to unfavorable conditions in the international markets which could have a negative impact on the demand for our products as well as products of third parties with whom we conduct business. Any combination of lower consumer confidence, disrupted global capital markets and/or reduced international economic conditions could have a negative impact on the Chilean economy and consequently on our business.

The relative liquidity and volatility of Chilean securities markets may increase the price volatility of our American Depositary Shares (“ADSs”) and adversely impact a holder’s ability to sell any shares of our common stock withdrawn from our American Depositary Receipt (“ADR”) facility.

The Chilean securities markets are substantially smaller, less liquid and more volatile than major securities markets in the United States. For example, the Santiago Stock Exchange, which is Chile’s principal stock exchange, had a market capitalization of approximately US$ 190.6 billion as of December 31, 2015, while The New York Stock Exchange (“NYSE”) had a market capitalization of approximately US$24.5 trillion and the NASDAQ National Market (“NASDAQ”) had a market capitalization of approximately US$7.90 trillion as of the same date. In addition, the Chilean securities markets can be materially affected by developments in other emerging markets, particularly other countries in Latin America.

The lower liquidity and greater volatility of the Chilean markets relative to markets in the United States could increase the price volatility of the ADSs and may impair a holder’s ability to sell in the Chilean market shares of our common stock withdrawn from the ADR facility in the amount and at the price and time the holder wishes to do so. See “Item 9: The Offer and Listing.”

We are subject to different corporate disclosure requirements and accounting standards than U.S. companies.

Although the securities laws of Chile which govern open stock corporations and publicly listed companies such as us have as a principal objective promoting disclosure of all material corporate information to the public, Chilean disclosure requirements differ from those in the United States in certain important respects. In addition, although Chilean law imposes restrictions on insider trading and price manipulation, the Chilean securities market is not as highly regulated and supervised as the U.S. securities market. We have been subject to the periodic reporting requirements of the Exchange Act since our initial public offering of ADSs in September 1992.

6

RISKS RELATING TO ARGENTINA

We have operations in Argentina, and economic conditions there have adversely affected the results of our operations in the past and may do so in the future.

We have significant assets in Argentina and we have generated significant income from our operations in this country.

As demand for alcoholic and non-alcoholic beverages is usually correlated with economic conditions prevailing in the local market, which in turn is dependent on the macroeconomic condition of the country, the financial condition and results of our operations in Argentina are, to a considerable extent, dependent upon political and economic conditions prevailing in Argentina. From 1999 through 2002, Argentina suffered a prolonged recession, which culminated in an economic crisis. Although the economic situation in Argentina has improved since the economic crisis of 2002, we have been observing a slowdown of the economy, and therefore, cannot assure you that economic conditions in Argentina will continue to improve or that our business will not be materially affected if Argentine economic conditions were to deteriorate.

The Argentine peso is subject to volatility which could adversely affect our results.

A devaluation of the Argentine peso may adversely affect our operating results. In 2015 Argentina experienced an average devaluation of the Argentine peso versus the dollar of14% year over year. We cannot assure you that the Argentine economy will recover or that it will not face a recession, nor can we predict what effect such a recession would have on our operations in Argentina. In 2009, the Company first reported its financial statements under IFRS, using the Argentine peso as the functional currency for our Argentine subsidiaries. The results are calculated in Argentine pesos and then translated into Chilean pesos for consolidation purposes.

Argentina’s legal regime and economy are susceptible to changes that could adversely affect our Argentine operations.

The measures taken by the previous Argentine government to address the country’s economic crisis of 2002 severely affected the Argentine financial system’s stability and have had a materially negative impact on the country´s economy. Recently, the Argentine government lifted restrictions on foreign exchange transactions for obligations entered into after December 17, 2015. Restrictions on obligations entered into before December 17, 2015 will remain in effect until May 2016. If Argentina were to experience a new fiscal and economic crisis, the Argentine government could implement economic and political measures, which could adversely impact our business.

Since January 2006, the Argentine government has adopted different methods to directly and indirectly regulate the prices of various consumer goods, including bottled beer, in an effort to slow inflation. Additionally, measures taken by the previous Argentine government to control the country’s trade balance and to limit the access to foreign currencies have negatively impacted the free import of goods and royalty payments by the Company, and also the repatriation of profits. This situation has recently changed following the installation of the new government in December 2015. We cannot assure you that the current Argentine government will not implement this type of measures and that these will not have an adverse effect on our operations in Argentina.

RISKS RELATING TO OUR BUSINESS

Potential changes to Chilean tax rules may result in an increase in the prices of our products and a corresponding decline in sales volumes.

7

Changes such as the new Chilean tax reform (the “Tax Reform Act”) that became effective on October 1, 2014, and implemented a series of changes to the tax rates and tax policies, increasing among other things the excise tax for alcoholic and sugar-containing beverages in Chile, forced us to implement price increases for certain categories, leading to a possible decline in volume.

Furthermore, the Tax Reform Act establishes two different systems: “The Partially Integrated System” and the “Attributed Income Regime”. The "Partially Integrated System" provides for a gradual increase in the First Category Income tax rate, going from 20% to 21% for the 2014 business year, to 22.5% for the 2015 business year, to 24% for the 2016 business year, to 25.5% for the 2017 business year and to 27% starting in the 2018 business year. The Tax Reform Act provides that corporations will apply by default the "Partially Integrated System", unless a future Extraordinary Shareholders Meeting agrees to opt for the "Attributed Income Regime”.

Implementation of these or similar future reforms that we are not aware of nor foresee, might adversely affect our business, our operating result and our financial position.

Fluctuations in the cost of our raw materials may adversely impact our profitability if we are unable to pass those costs on to our customers.

We purchase malt, rice and hops for beer, sugar for soft drinks, grapes for wine, pisco and cocktails, and packaging material from local producers or in the international market. The prices of those materials are subject to volatility caused by market conditions, and have experienced significant fluctuations over time and are determined by the global supply and demand for commodities as well as other factors, such as fluctuations in exchange rates, over which we have no control.

Although we historically have been able to implement price increases in response to increases in raw material costs, we cannot assure you that our ability to recover increases in the cost of raw materials will continue in the future. In particular, where raw material price fluctuations do not keep pace with market conditions in the markets in which we operate, we may have limited capacity to raise prices to offset increases in costs. If we are unable to increase prices in response to increases in raw material costs, any future increases in raw material costs may reduce our margins and profitability if we are not able to offset such cost increases through efficiency improvements or other measures.

Consolidation in the beer industry may impact our market share.

In 2005, SABMiller Plc merged with Grupo Empresarial Bavaria, a Colombian brewer with operations in Colombia, Peru, Ecuador and Panama, forming the then second-largest brewer in the world. In 2010SABMiller Plc acquired Cervecería Argentina S.A. (“CASA Isenbeck”), the third-largest brewer in Argentina, previously subsidiary of Warsteiner Brauerei Hans Cramer GmbH & Co. (“Warsteiner”).

In March 2004, Companhia de Bebidas das Américas (“AmBev”) and Interbrew announced an agreement to merge, creating the world’s largest brewer under the name InBev. Additionally, in January 2007, AmBev assumed control of Quilmes Industrial S.A. (“Quilmes”). In Chile, Quilmes sells its beer through Cervecería Chile S.A. (“Cervecería Chile”). In November 2008 InBev and Anheuser-Busch Companies, Inc. (“Anheuser-Busch”) merged, creating Anheuser-Busch Inbev (“AB Inbev”), the worldwide leader in beer. In 2013, AB Inbev finalized the acquisition of Grupo Modelo.

During 2015 SAB Miller plc accepted an offer from AB Inbev to merge its operations. The merger has not yet been completed as it is subject to regulatory approvals. With this we face a major challenge: we are witnessing one of the largest global mergers in the history of beer and carbonated soft drinks, which will create a powerful global player, capable of producing and distributing more than 700 million hectoliters per year, with presence in more than 65 countries. We are monitoring the scope and implications of the possible regulatory restrictions to this merger in the different countries where SABMiller plc and AB Inbev currently operate, and possible consequences for our operations.

8

Competition in the Chilean beer market may erode our market share and lower our profitability.

Our largest competitor in the Chilean beer market by volume is Cervecería Chile. In the past, Cervecería Chile has engaged in aggressive pricing. If Cervecería Chile were to amplify its aggressive price discounting practices in the future, we cannot assure, given the current environment, that any such discounting or other competitive activities will not have a material adverse impact on our profitability or market share.

Additionally, if commercial conditions in the beer market continue to be relatively favorable in Chile, more enterprises may attempt to enter this market, either by producing beer locally or through importation. While we expect per capita beer consumption in Chile to continue to increase, mitigating the effect of competition, the entry into the market of additional competitors could erode our market share or lead to price discounting.

Our beer brands in Chile may face increased competition from other alcoholic beverages such as wine and spirits, as well as from non-alcoholic beverages, such as carbonated soft drinks.

Beer consumption in Chile may be influenced by changes in the relative price of domestic wine, spirits and/or other non-alcoholic beverages. Increases in domestic wine prices have tended to lead to increases in beer consumption, while reductions in wine prices have tended to reduce or slow the growth of beer consumption. As a result of our lower market share in the Chilean wine, spirits and soft drinks markets as compared to our market share in the Chilean beer market, we expect that our consolidated profitability could be adversely affected if beverage consumers were to shift their consumption from beer to either wine, spirits or non-alcoholic beverages.

Quilmes dominates the beer market in Argentina and we may not be able to maintain our current market share.

In Argentina we face competition from Quilmes and CASA Isenbeck, which as a result of the merger between AB Inbev and SAB Miller plc, if consummated, would become one player in the Argentine beer market. As a result of its dominant position in Argentina, Quilmes’ large size by itself enables it to benefit from economies of scale in the production and distribution of beer throughout Argentina, a position that would strengthen as a result of the merger. Therefore, we cannot assure you that we will be able to grow or maintain our current market share in the Argentine beer market.

Restrictions in the gas supply from Argentina and taxes on carbon dioxide emissions could increase our energy costs, and higher oil prices could increase our distribution expenses.

In the past, the Argentine government restricted gas exports to Chile due to domestic supply problems. This increased the operating cost of our beer plants in Chile and Argentina, and of our non-alcoholic plants in Chile. As a consequence, the Chilean government implemented a strategy to diversify the country’s energy supply. The construction in Quintero of the first plant to process imported LNG (liquefied natural gas), which started its operation in August 2009, brought relief to the energy issue. Taxes on carbon dioxide emissions in Chile will go into effect in 2017, and the cost of these taxes will most likely be passed on to energy prices. We cannot assure that the supply of energy or the cost thereof will not experience future fluctuations. Electric power costs have increased significantly in the past mainly due to hydroelectric plants having lower water reservoir levels, which was exacerbated by the absence of new installed capacity at lower costs. Increases in oil prices or unfavorable hydric conditions could reduce our margins if we are unable to improve efficiencies or increase our prices to offset them.

9

Changes in the labor market in the countries in which we operate may affect margins in our business.

In December 2014, the Chilean government presented to the Chilean Congress a bill for a labor reform which could result in a more rigid labor market. This reform has been approved by the Chilean Congress but is currently pending resolution by the Constitutional Court. The main elements of the labor reform are the following:

· Collective bargaining coverage is expanded to certain employees who were prevented from exercising this right, such as apprentices, temporary workers and others.

· Unions are recognized as the only party entitled to exercise the right to collectively bargain on behalf of the workers.

· Benefits obtained by a union in the course of a negotiation are extended for the benefit of any worker joining that union after the negotiation has concluded. The extension of said benefits to employees would be contingent to the assent of each union.

· Collective bargaining agreements currently in effect would constitute a floor for the negotiation of new conditions of employment. The financial situation of the company or business as of the date of discussions for a new agreement would not have any bearing on ongoing negotiations.

· The employer's right to replace those workers participating in a strike with current or new employees while the strike is taking place is curtailed.

· Modification of the definition of “minimum services” through “emergency teams” for which unions are obliged to provide the personnel required. These minimum services should be of a certain minimum level to prevent accidents and protect the equipment.

· Matters that may be subject to collective bargaining agreements are expanded, allowing the negotiation of more flexible workdays, adaptable systems and others.

· Unions may annually request from large companies information regarding the remunerations and duties associated with each category of employees.

In Argentina, the high levels of inflation could affect our salary expenses.

We depend upon the renewal of certain license agreements to maintain our current operations.

Most of our license agreements include certain conditions that must be met during their term, as well as provisions for their renewal at their expiry date. We cannot assure that such conditions will be fulfilled, and therefore that the agreements will remain in place until their expiration or that they will be renewed, or that any of these contracts will not undergo early termination. Termination of, or failure to renew our existing license agreements, could have an adverse impact on our operations.

Consolidation in the supermarket industry may affect our operations.

The Chilean supermarket industry has gone through a consolidation process, increasing the importance and purchasing power of a few supermarket chains. As a result, we may not be able to negotiate favorable prices, which may adversely affect our sales and profitability.

Additionally, and despite having insurance coverage, this supermarket chain consolidation has the effect of increasing our exposure to counterparty credit risk, given the fact that we have more exposure in the event one of these large customers fails to honor its payment obligations to us for any reason.

Dependence on a single supplier for some important raw materials.

In the case of cans, both in Chile and Argentina we purchase from a single supplier, Rexam, which has production plants in both countries. However, cans could also be imported from other Rexam plants or from alternative suppliers in the region. We have long term contracts for malt in Chile and in Argentina. We purchase one way polyethylene terephthalate resins (“PET”) from severalsuppliers located in China, Mexico and US and in the past we have also purchased in Argentina. While we have alternatives in procuring our supplies, if we were to experience disruptions in our supply chain we cannot assure you we will be able to obtain replacement supplies at favorable pricing or advantageous terms, which may adversely affect our results.

10

Water supply is essential to the development of our businesses.

Water is an essential component for beer, soft drinks, mineral and purified water. While we have adopted policies for the responsible and sustainable use of water, a failure in our water supply or contamination of our wells could negatively affect our sales and profitability.

The Chilean Congress is currently discussing a bill that provides, among others, a new regime of temporary water rights, which apply to future water rights that are granted. The bill would also introduce a system of revocation of water rights, for those not in use. This bill could undergo modifications during its discussion in the Chilean Congress. After its enactment, regulations will be required for the implementation of the new regime, which is not expected to occur during the year 2016.

The supply, production and logistics chain is key to the timely supply of our products to consumer centers.

Our supply, production and logistics chain is crucial for the delivery of our products to consumer centers. An interruption or a significant failure in this chain may negatively affect our results, if the failure is not quickly resolved. An interruption in the chain could be caused by various factors, such as strikes, riots, complaints by communities or other factors which are beyond our control.

If we are unable to protect our information systems against data corruption, cyber-based attacks or network security breaches, our operations could be disrupted.

We are increasingly dependent on information technology networks and systems, including the Internet, to process, transmit and store electronic information. In particular, we depend on our information technology infrastructure for digital marketing activities and electronic communications within the Company and with our clients, suppliers and our subsidiaries. Security breaches of this infrastructure can create system disruptions, shutdowns or unauthorized disclosure of confidential information. If we are unable to prevent such breaches, our operations could be disrupted, or we may suffer financial damage or loss because of lost or misappropriated information.

Possible regulations for labeling materials and promotion of alcoholic beverages and other food products in Chile could adversely affect us.

Currently a bill that modifies law N° 18,455 is in the third phase of being passed. The bill fixes standards for production, elaboration and commercialization of ethyl alcohol, alcoholic beverages and vinegar. The bill aims to establish restrictions on promotion material, labeling and commercialization of alcoholic beverages including warnings about the consumption of alcohol on labeling and promotion materials, restrictions in hours of promotion and prohibition of participation in sports and cultural events, among others. A regulatory change of this nature will affect our alcohol beverages portfolio and certain marketing activities.

On June 26, 2015 decree N° 13 of the Ministry of Health was published which modifies the Sanitary Food Products Regulations (DC 977 of the Ministry of Health) and enforces Law N° 20,606 of 2012 regarding the nutritional composition of food products and its promotion. Both regulations establish certain restrictions on promotion material, labeling, and commercialization of these products that have been classified as being “high” in calories or any of the defined critical nutrients, such as sodium, sugar and saturated fats. Additionally on November 13, 2015 Law N° 20,869 regarding the promotion of food products was published, restricting the time of day promotions for products high in calories or any of the defined critical nutrient can be aired on television and in the cinema.

11

This law will become effective as of June 27, 2016 and will affect a portion of our non-alcoholic portfolio. We are taking measures to mitigate the impact of this new law, though we cannot assure that these measures will be successful.

If further proposed bills are passed, or other regulations restricting the sale of non-alcoholic beverages or sweet snacks are enacted, this could affect consumption of our products and, as a consequence, negatively impact our business.

New environmental regulations, may negatively affect our profitability and reputation.

CCU’s operations are subject to environmental regulations at local, national and international levels. These regulations cover, among other things, emissions, noise, disposal of solid and liquid wastes, and other activities inherent to our industry In Chile a bill has been approved by the Chilean Congress that establishes a framework for waste management and extended producer responsibility, also known as the recycling law, with the objective of lowering the generation of waste of proprietary products as determined by the bill and fostering recycling of the waste.

CCU places special care and dedicates constant efforts to the compliance with environmental regulations. Modifications to the existing regulation might involve new costs and investments by the Company.

Our products are taxed with different duties, particularly with respect to excise taxes on the consumption of alcoholic and non-alcoholic beverages.

The Argentine ad valorem excise tax is 8.7% for beer, and the Chilean ad valorem excise tax is 20.5% for beer and wine, 31.5% for spirits, 18% for non-alcoholic beverages containing more than 15 gr./240ml. of sugar and 10% for non-alcoholic beverages containing 15 gr./240ml. or less of sugar. An increase in the rate of these or any other tax could negatively affect our sales and profitability.

Currency fluctuations may affect our profitability.

Because we purchase some of our supplies at prices set in U.S. dollars, and export wine in U.S. dollars, Canadian dollars, euros and pounds, we are exposed to foreign exchange risks that may adversely affect our financial condition and the results of our operations. Therefore, any future changes in the value of the Chilean peso against said currencies would affect the revenues of our wine export business, as well as the cost of several of our raw materials, especially in the beer and soft drink businesses where prices of raw materials are indexed to the U.S dollar. The effect of the exchange rate variation on export revenues would have an opposite effect on the cost of raw materials expressed in Chilean peso terms.

Catastrophic events in the markets in which we operate could have a material adverse effect on our financial condition.

Natural disasters, climate change, terrorism, pandemics, strikes or other catastrophic events could impair our ability to manufacture, distribute or sell our products. Failure to take adequate steps to mitigate the likelihood or potential impact of such events, or to manage such events effectively if they occur, could adversely affect our sales volume, cost of raw materials, earnings and could have a material effect on our business, operational results, and financial position.

In 2015 Chile was affected by several natural disasters, including the large floods and mudflows in several towns of the Antofagasta, Atacama and Coquimbo regions during March 2015, and an 8.4 magnitude earthquake in the northern regions of Chile, followed by a tsunami on September 17, 2015. These events did not have a significant effect on our operations.

12

A future earthquake, tsunami or other natural disaster, however, could have a significant effect on our business, results of operations and financial condition.

If we are unable to maintain the image and quality of our products our financial results may suffer.

The image and quality of our products is essential for our success and growth. Problems with product quality could tarnish the reputation of our products and may adversely affect our revenues.

If we are unable to finance our operations we may be adversely affected.

A global liquidity crisis or an increase in financial interest rates may eventually limit our ability to obtain the cash needed to fulfill our commitments. Sales could also be affected by a global disruption if consumption decreases sharply, placing stress on our cash position.

RISKS RELATING TO OUR ADSs

We are controlled by one majority shareholder, whose interests may differ from those of holders of our ADSs, and this shareholder may take actions that adversely affect the value of a holder’s ADSs or common stock.

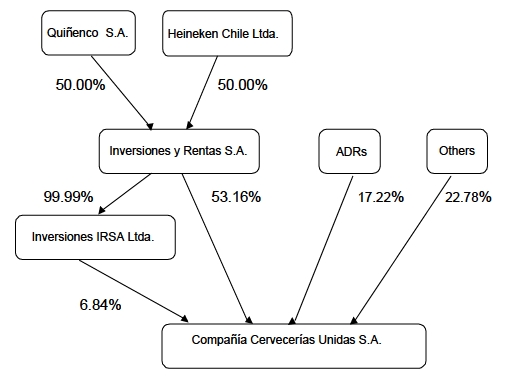

As of March 31, 2016, Inversiones y Rentas S.A. (“IRSA”) a Chilean closed corporation, directly and indirectly owned 60.0% of our shares of common stock. Accordingly, IRSA has the power to control the election of most members of our board of directors and its interests may differ from those of the holders of our ADSs. IRSA also has significant influence in determining the outcome of any corporate transaction submitted to our shareholders for approval, including mergers, consolidations, the sale of all or substantially all of our assets and going-private transactions. In addition, actions by IRSA with respect to the disposal of the shares of common stock that it owns, or the perception that such actions may occur, may adversely affect the trading prices of our ADSs or common stock.

Chilean economic policies, currency fluctuations, exchange controls and currency devaluations may adversely affect the price of our ADSs.

The Chilean government’s economic policies and any future changes in the value of the Chilean peso relative to the U.S. dollar could adversely affect the dollar value and the return on any investment in our ADSs. The Chilean peso has been subject to large nominal devaluations and appreciations in the past and may be subject to significant fluctuations in the future. For example, in the period from December 31, 2014 to December 31, 2015, the daily average value of the Chilean peso relative to the U.S. dollar increased by15% in nominal terms, whereas the year end value increased by 17% based on the observed exchange rate for U.S. dollars on those dates. See “Item 3: Key Information – Selected Financial Data – Exchange Rates.”

While our ADSs trade in U.S. dollars, Chilean trading in the shares of our common stock underlying our ADSs is conducted in Chilean pesos. Cash distributions to be received by the depositary for the shares of our common stock underlying our ADSs will be denominated in Chilean pesos. The depositary will translate any Chilean pesos received by it to U.S. dollars at the then-prevailing exchange rate with the purpose of making dividend and other distribution payments on the ADSs. If the value of the Chilean peso declines relative to the U.S. dollar, the value of our ADSs and any distributions to holders of our ADSs received from the depositary may be adversely affected. See “Item 8: Financial Information – Dividend Policy and Dividends.”

For example, since our financial statements are reported in Chilean pesos, a decline in the value of the Chilean peso against the dollar would reduce our earnings as reported in U.S. dollars. Any dividend we may pay in the future would be denominated in Chilean pesos. A decline in the value of the Chilean peso against the U.S. dollar would reduce the U.S. dollar equivalent of any such dividend. Additionally, in the event of a dividend or other distribution, if exchange rates fluctuateduring any period of time when the ADS depositary cannot convert a foreign currency into dollars, a holder of our ADSs may lose some of the value of the distribution. Also, since dividends in Chile are subject to withholding taxes, which we retain until the following year when the exact amount to be paid is determined, if part of the retained amount is refunded to the shareholders, the amount received by holders of our ADSs would be subject to exchange rate fluctuations between the two dates.

13

Holders of our ADSs may be subject to certain risks due to the fact that holders of our ADSs do not hold shares of our common stock directly.

In order to vote at shareholders’ meetings, if a holder is not registered on the books of the ADS depositary, the holder of our ADSs is required to transfer their ADSs for a certain number of days before a shareholders’ meeting into a blocked account established for that purpose by the ADS depositary. Any ADSs transferred to this blocked account will not be available for transfer during that time. If a holder of our ADSs is registered on the books of the ADS depositary, the holder must give instructions to the ADS depositary not to transfer such holder’s ADSs during such period before the shareholders’ meeting. A holder of our ADSs must therefore receive voting materials from the ADS depositary sufficiently in advance in order to make these transfers or give these instructions. There can be no guarantee that a holder of our ADSs will receive voting materials in time to instruct the ADS depositary on how to vote. It is possible that a holder of our ADSs will not have the opportunity to exercise a right to vote at all. Additionally, a holder of our ADSs may not receive copies of all reports from us or the ADS depositary. A holder of our ADSs may have to arrange with the ADS depositary’s offices to inspect any reports issued.

In the past, Chile has imposed controls on foreign investment and repatriation of investments that affected investments in, and earnings from, our ADSs.

Equity investments in Chile by persons who are not Chilean residents have historically been subject to various exchange control regulations that restrict repatriation of investments and earnings therefrom. In April 2001, the Central Bank eliminated most of the regulations that affected foreign investors, although foreign investors still have to provide the Central Bank with information related to equity investments and must conduct such operations within the formal exchange market. Additional Chilean restrictions applicable to holders of our ADSs, the disposition of the shares underlying them, the repatriation of the proceeds from such disposition or the payment of dividends may be imposed in the future, and we cannot advise you as to the duration or impact of such restrictions if imposed. See also “Item 10: Additional Information, D. Exchange Controls”.

If for any reason, including changes in Chilean law, the depositary for our ADSs were unable to convert Chilean pesos to U.S. dollars, investors would receive dividends and other distributions, if any, in Chilean pesos.

The right of a holder of our ADSs to force us to purchase the underlying shares of our common stock pursuant to Chilean corporate law upon the occurrence of certain events may be limited.

In accordance with Chilean laws and regulations, any shareholder that votes against certain corporate actions or does not attend the meeting at which certain corporate actions are approved and communicates to the corporation their dissent in writing within the time period established by law may exercise a withdrawal right, tender their shares to the company and receive cash compensation for their shares, provided that the shareholder exercises their rights within the prescribed time periods. See “Item 10: Additional Information–Memorandum and Articles of Association–Rights, preferences and restrictions regarding shares.” In our case, the actions triggering a right of withdrawal include the approval of:

· our transformation into a different type of legal entity;

14

· our merger with and/or into another company;

· the transfer of 50% or more of our corporate assets, whether or not liabilities are also transferred, to be determined according to the balance sheet of the previous fiscal year, or the proposal or amendment of any business plan that contemplates the transfer of assets exceeding said percentage; the disposition of 50% or more of the corporate assets of a subsidiary, which represents at least 20% of the assets of the corporation, as well as any disposition of shares which results in the parent company losing its status as controller;

· the granting of real or personal guarantees to secure third-party obligations exceeding 50% of the corporate assets except when the third party is a subsidiary of the company (in which case approval of the board of directors will suffice);

· the creation of preferences for a series of shares or the increase, extension or reduction in the already existing ones. In this case, only dissenting shareholders of the affected series shall have the right to withdraw;

· curing certain formal defects in our charter which otherwise would render it null and void or any modification of our bylaws that grant this right; and

· other cases provided for by statute or in our bylaws, if any.

In addition, shareholders may withdraw if a person becomes the owner of two-thirds or more of the outstanding shares of the corporation as a consequence of a share acquisition and such person does not make a tender offer for the remaining shares within 30 days from the date of such acquisition.

Minority shareholders are also granted the right to withdraw when the controller acquires more than 95% of the shares of an open stock corporation.

Our bylaws do not provide for additional circumstances under which shareholders may withdraw.

Because of the absence of legal precedent as to whether a shareholder that has voted both for and against a proposal, such as the depositary of our ADSs, may exercise withdrawal rights with respect to those shares voted against the proposal, there is doubt as to whether a holder of ADSs will be able to exercise withdrawal rights either directly or through the depositary for the shares of our common stock represented by their ADSs. Accordingly, for a holder of our ADSs to exercise its appraisal rights, it may be required to surrender its ADRs, withdraw the shares of our common stock represented by its ADSs, and vote the shares against the proposal.

Preemptive rights to purchase additional shares of our common stock may be unavailable to holders of our ADSs in certain circumstances and, as a result, their ownership interest in our Company may be diluted.

TheLey sobre Sociedades Anónimas N° 18,046 (“Chilean Corporations Act”) and theReglamento de Sociedades Anónimas, require us, whenever we issue new shares for cash, to grant preemptive rights to all holders of shares of our common stock, including shares of our common stock represented by ADSs, giving those holders the right to purchase a sufficient number of shares to maintain their existing ownership percentage. We may not be able to offer shares to holders of our ADSs pursuant to preemptive rights granted to our shareholders in connection with any future issuance of shares unless a registration statement under the Securities Act is effective with respect to those rights and shares, or an exemption from the registration requirements of the Securities Act is available.

15

We intend to evaluate at the time of any future offerings of shares of our common stock the costs and potential liabilities associated with any registration statement as well as the indirect benefits to us of enabling U.S. owners of our ADSs to exercise preemptive rights and any other factors that we consider appropriate at the time, before making a decision as to whether to file such a registration statement. We cannot assure you that any such registration statement would be filed.

To the extent that a holder of our ADSs is unable to exercise their preemptive rights because a registration statement has not been filed, the depositary will attempt to sell the holder’s preemptive rights and distribute the net proceeds of the sale, net of the depositary’s fees and expenses, to the holder, provided that a secondary market for those rights exists and a premium can be recognized over the cost of the sale. A secondary market for the sale of preemptive rights can be expected to develop if the subscription price of the shares of our common stock upon exercise of the rights is below the prevailing market price of the shares of our common stock. Nonetheless, we cannot assure you that a secondary market in preemptive rights will develop in connection with any future issuance of shares of our common stock or that if a market develops, a premium can be recognized on their sale. Amounts received in exchange for the sale or assignment of preemptive rights relating to shares of our common stock will be taxable in Chile and the United States. See “Item 10: Additional Information –Taxation– Chilean Tax Considerations –Capital Gains” and “–United States Federal IncomeTax Considerations– Taxation of Capital Gains.” If the rights cannot be sold, they will expire and a holder of our ADSs will not realize any value from the grant of the preemptive rights. In either case, the equity interest of a holder of our ADSs in us will be diluted proportionately.

ITEM 4: Information on the Company

A. History and Development of the Company

Our current legal and commercial name is Compañía Cervecerías Unidas S.A. We were incorporated in the Republic of Chile in 1902 as an open stock corporation, following the merger of two existing breweries, one of which traces its origins back to 1850, when Mr. Joaquín Plagemann founded one of the first breweries in Chile in Valparaíso. By 1916, we owned and operated the largest brewing facilities in Chile. Our operations have also included the production and marketing of soft drinks since the beginning of the last century, the bottling and selling of mineral water products since 1960, the production and marketing of wine since 1994, the production and marketing of beer in Argentina since 1995, the production and marketing of pisco since 2003, the production and marketing of sweet snacks products since 2004 and the production and marketing of rum since 2007.

We are subject to a full range of governmental regulation and supervision generally applicable to companies engaged in business in Chile, Argentina, Bolivia, Colombia, Paraguay and Uruguay. These regulations include labor laws, social security laws, public health, consumer protection and environmental laws, securities laws, and antitrust laws. In addition, regulations exist to ensure healthy and safe conditions in facilities for the production and distribution of beverages and sweet snacks products.

Our principal executive offices are located at Vitacura 2670, 23rd floor, Santiago, Chile. Our telephone number in Santiago is (56-2) 2427-3000, and our website is www.ccu.cl. Our authorized representative in the United States is Puglisi & Associates, located at 850 Library Avenue, Suite 204, Newark, Delaware 19715, USA, telephone number (302) 738-6680 and fax number (302) 738-7210. The information on our website is not incorporated by reference into this document.

In 1986, IRSA, our current principal shareholder, acquired its controlling interest in us through purchases of common stock at an auction conducted by a receiver who had assumed control of us following the economic crisis in Chile in the early 80’s, which resulted in our inability to meet our obligations to our creditors. IRSA, at that time, was a joint venture between Quiñenco S.A. (“Quiñenco”) and the Schörghuber Group from Germany through its wholly owned subsidiary Finance Holding International B.V. (“FHI”) of the Netherlands.

16

To our knowledge, none of our common stock is currently owned by governmental entities. Our common stock is listed and traded on the principal Chilean stock exchanges. See “Item 7: Major Shareholders and Related Party Transactions.”

In September 1992, we issued 4,520,582 ADSs, each representing five shares of our common stock, in an international American Depositary Receipt (“ADR”) offering. The underlying ADSs were listed and traded on the NASDAQ, until March 25, 1999. Since that date, the ADSs have been listed and traded on the NYSE. After a capital increase approved by our shareholders in October 1996, we raised approximately US$196 million between December 1996 and April 1999. Part of this capital expansion was accomplished between December 1996 and January 1997 through our second ADR offering in the international markets. On December 20, 2012, the ratio of ADSs to shares of common stock was changed from 1 to 5, to a new ratio of 1 to 2.

On June 18, 2013 the extraordinary shareholders’ meeting approved the issuance of 51,000,000 of ordinary shares which were registered in the Securities Registry of the Superintendency of Securities and Insurance (“SVS”) under N°980 dated July 23, 2013. On November 8, 2013 CCU successfully concluded this capital increase, the total number of shares issued pursuant to the capital increase having been subscribed and paid, raising a total amount of CLP 331,718,929,410. This capital increase, representing our third ADR offering in the international markets, was made in order to continue our expansion plan, which includes organic and inorganic growth in Chile and the surrounding region.

To increase our presence in the premium beer segment, in November 2000 we acquired a 50% stake in Cervecería Austral S.A. (“Cervecería Austral”), located in the city of Punta Arenas, with an annual production capacity of 6.1 million liters. Further, in May 2002, we acquired a 50% stake in Compañía Cervecera Kunstmann S.A. (“CCK”), located in the city of Valdivia.

On April 17, 2003, the Schörghuber Group, at the time an indirect owner of 30.8% of our ownership interest, gave Quiñenco, also at the time an indirect owner of 30.8% of our ownership interest, formal notice of its intent to sell 100% of its interest in FHI to Heineken Americas B.V., a subsidiary of Heineken International B.V. As a result of the sale, Quiñenco and Heineken Americas B.V., the latter through FHI, became the only two shareholders of IRSA, the owner of 61.6% of our equity at that time, each with a 50% interest in IRSA. Heineken International B.V. and FHI subsequently formed Heineken Chile Ltda., to hold the latter’s 50% interest in IRSA. Therefore, Quiñenco and Heineken Chile Ltda. are the only two current shareholders of IRSA, with a 50% equity each. On December 30, 2003, FHI merged into Heineken Americas B.V., which together with Heineken International B.V. remained as the only shareholders of Heineken Chile Ltda. At present IRSA owns, directly and indirectly, 60.0% of our equity.

Prior to November 1994, we independently produced, bottled and distributed carbonated and non-carbonated soft drinks in Chile. We have produced and sold soft drinks in Chile since 1902 and spirits since 2003. In November 1994, we merged our soft drink and mineral water businesses with the one owned by Buenos Aires Embotelladora S.A. (“BAESA”) in Chile (PepsiCo’s bottler in Chile at that time) creating Embotelladoras Chilenas Unidas S.A. (“ECUSA”) for the production, bottling, distribution and marketing of soft drink and mineral water products in Chile. Through ECUSA, we began producing PepsiCo brands under license (currently Pepsi, Pepsi Light, Seven Up, Seven Up Light, Mirinda, Gatorade and Lipton Ice Tea). We have had control of ECUSA since January 1998, when the shareholders agreement was amended. On November 29, 1999 we purchased 45% of ECUSA’s shares owned by BAESA for approximately CLP 54,118 million. We currently own 99.93% of ECUSA’s shares. In January 2001, ECUSA and Schweppes Holdings Ltd. signed an agreement to continue bottling Crush and Canada Dry brands. See “– Production and Marketing – Chile Operating segment.” In December 2015 CCU started to distribute Red Bull in Chile.

17

In October 2013, CCU, together ECUSA, executed a series of contracts and agreements with PepsiCo Inc. and affiliates, which allowed them to expand their current relationship in the non-alcoholic beverages segment with specific focus on carbonated soft drinks, as well as extending its long term duration. The performance of ECUSA as PepsiCo Inc.’s bottler has been recognized by the latter on several occasions including the award granted to ECUSA in Bangkok as Bottler of the Year for the Latin America Region. In 2014, ECUSA received the distinction of “PepsiCo Global Bottler of the Year” from over 200 bottlers worldwide.

In January 2004, we entered the sweet snacks business by means of a joint venture between our CCU Inversiones S.A. and Industria Nacional de Alimentos S.A, a subsidiary of Quiñenco, with a 50% interest each in Calaf S.A. (which has been renamed Foods Compañía de Alimentos CCU S.A., or Foods, a corporation that acquired the trademarks, assets and know-how, among other things, of Calaf S.A.I.C. and Francisca Calaf S.A., traditional Chilean candy makers, renowned for more than a century. In August 2008, Foods bought 50% of Alimentos Nutrabien S.A., a company specializing in muffins and other high quality home-made products under the brand Nutrabien. In 2007 we acquired the brand Natur, adding cereal bars to our portfolio. In 2015 we sold the brands Calaf and Natur to Empresas Carozzi S.A. (“Carozzi”), leaving Foods with only the Nutrabien brand.

In December 2006, we signed a joint venture agreement with Watt’s S.A. (“Watt’s”), a local food related company, under which, as of January 30, 2007, we participate in equal parts in Promarca S.A. (“Promarca”). This new company owns, among others, the brands “Watt’s,” “Watt’s Ice Frut,” “Yogu Yogu” and “Shake a Shake” in Chile. Promarca granted both of its shareholders (New Ecusa S.A., a subsidiary of ECUSA, and Watt´s Dos S.A, a subsidiary of Watt´s S.A), for an indefinite period, the exclusive licenses for the production and sale of the different product categories.

In December 2007, we entered into an agreement with Nestlé Chile S.A. and Nestlé Waters Chile S.A., the latter of which acquired a 20% interest in our subsidiary Aguas CCU-Nestlé Chile S.A. (“Aguas CCU”), the company through which we develop our bottled water business in Chile. As part of this new association, Aguas CCU introduced in 2008 the Nestlé Pure Life brand in Chile. Nestlé Waters Chile S.A. had a call option to increase its ownership in Aguas CCU by an additional 29.9%, which expired on June 5, 2009. On June 4, 2009 ECUSA received a notification from Nestlé Waters Chile S.A. exercising its irrevocable option to buy 29.9% of Aguas CCU equity, within the scope of the association contract. The completion of the deal represented a profit before taxes for ECUSA of CLP 24,439 million. On September 30, 2009 in extraordinary shareholders’ meetings, Aguas CCU and Nestlé Waters Chile S.A. approved the merger of Nestlé Waters Chile S.A. and Aguas CCU. The current shareholders of Aguas CCU are ECUSA (50.10%) and Nestlé Chile S.A. (49.90%).

In December 2012, Aguas CCU completed an acquisition of 51.01% of the company Manantial S.A. (“Manantial”), a Home and Office Delivery (“HOD”) business of purified water in bottles with the use of dispensers. The partnership enabled Aguas CCU to participate in a new business category. The shareholders agreement of Manantial included a call option to purchase the remaining shares. On January 29, 2016 Aguas CCU and ECUSA exercised the call option, acquiring 48.07% and 0.92% of the shares of Manantial respectively. As a consequence, Compañía Cervecerías Unidas S.A. is currently the indirect owner of 100% of the shares of Manantial, remaining as the only direct shareholders of Manantial: (i) Aguas CCU with 99.08% of the capital stock, and (ii) ECUSA with 0.92% of the capital stock.

In February 2003, we began the sale of a new product for our beverage portfolio, pisco, under the brand Ruta Norte. Pisco is a grape spirit very popular in Chile that is produced in the northern part of the country. Our pisco, at that time, was only produced in the Elqui Valley in Region IV of Chile and was sold throughout the country by our beer division sales force. In March 2005, we entered into an association with the second-largest pisco producer at that time, Cooperativa Agrícola Control Pisquero de Elqui y Limarí Ltda. (“Control”). This new joint venture was named Compañía Pisquera de Chile S.A. (“CPCh”), to which the companies contributed principally with assets, commercial brands and – in the case of Control – also some financial liabilities. Currently we own 80% of CPCh and Control owns the remaining 20%. In May 2007, CPCh entered the rum marketwith our proprietary brand Sierra Morena and later, in 2008, added new rum brand extensions and introduced various pisco based cocktails. Since 2011, our international strategy has focused on exports to Argentina, the United States and Asia, including Russia. CPCh signed a licence agreement for the commercialization and distribution in Chile of the pisco brand Bauzá. In addition, CPCh acquired 49% of the licensor company Compañía Pisquera Bauzá S.A. (“Bauza”), owner of the brand in Chile. In January 2016, CPCh sold its interest in Bauzá to Agroproductos Bauzá S.A. Furthermore, during 2011 CPCh began the distribution of Pernod Ricard products in Chile.

18

In December 1995, we entered into a joint venture agreement pursuant to which Anheuser-Busch Incorporated acquired a 4.4% interest in Compañía Cervecerías Unidas Argentina S.A. (“CCU Argentina”). The agreement involved two different contracts: an investment and a licensing contract. In 2008, the licensing contract was extended until 2025 and grants CCU Argentina the exclusive right to produce, package, market, sell and distribute Budweiser beer in Argentina. After subsequent capital increases, the last one in June 2008, Anheuser-Busch Incorporated reduced its interest in CCU Argentina to 4.04% and we increased our participation to 95.96%. In December 2010, our subsidiary Inversiones Invex CCU Ltda. acquired a 4.04% equity stake in CCU Argentina from Anheuser-Busch Investment, S.L. After the acquisition, CCU, through its subsidiary Inversiones Invex CCU Ltda., became the sole equity holder of CCU Argentina. This transaction had no effect on the Budweiser brand production and distribution contract which expires in 2025 (in 2015 for the distribution of the brand in Chile). Currently, CCU´s subsidiaries Inversiones Invex CCU Ltda. and Inversiones Invex CCU Dos Ltda. own 80.649% and 19.351%, respectively, of CCU Argentina´s share capital.

Through CCU Argentina, we began our expansion into Argentina by acquiring an interest in two Argentine breweries: 62.7% of the outstanding shares of Compañía Industrial Cervecera S.A. (“CICSA”), were acquired during January and February 1995 and 98.8% of the outstanding shares of Cervecería Santa Fe S.A. (“CSF”), were acquired in September 1995. In 1997, CCU Argentina increased its interest in CICSA to 97.2% and in CSF to 99.9% through the purchase of non-controlling interests. In January 1998, we decided to merge these two breweries into one company operating under the name of CICSA. Following the merger, CCU Argentina’s interest in CICSA was 99.2%. In April 1998, CCU Argentina completed the purchase of the brands and assets of Cervecería Córdoba S.A. for US$8 million. After the resolution of certain labor issues, we began the production of the Córdoba brand at our Santa Fe plant from the middle of 1998. In April 2008, we bought the Argentine brewer Inversora Cervecera S.A. (“ICSA”) after receiving the approval of the Argentine antitrust authorities. CICSA paid an aggregate amount of US$88 million to acquire ICSA. ICSA owns, among other assets, the Bieckert, Palermo and Imperial beer brands, which together represented approximately 5.8% of the Argentine beer market, and a brewery in Luján, Buenos Aires, with a nominal production capacity of 270 million liters per year. On December 27, 2010, CICSA acquired equity interests in Saénz Briones S.A. and Sidra La Victoria S.A. Through this transaction, CICSA became the controlling shareholder of these companies. These companies own the assets used in the production, packaging and marketing of cider and other spirits businesses in Argentina, which are marketed through several brands, including Sidra Real and Sidra La Victoria. In 2011, we started to export Schneider beer to Paraguay through Bebidas del Paraguay S.A (“Bebidas del Paraguay”), and in 2013 to Uruguay through Milotur S.A. (“Milotur”). In 2012 we signed an agreement by virtue of which we have the exclusive right to produce Heineken beer in Argentina and distribute it in Paraguay. In 2013 we started exporting Heineken to Uruguay through Milotur and in 2015 to Bolivia through Bebidas Bolivianas BBO S.A. (“BBO”). Together, both brands represented 2.0% of the total beer sales volume of CCU Argentina in 2015. Exports to Paraguay, Uruguay and Bolivia represented 84% of CCU Argentina’s total exports in 2015. As of June 6, 2014, CICSA reached agreements with Cervecería Modelo S. de R.L. de CV. and Anheuser-Busch LLC, for the termination of the contract which allows CICSA to import and distribute on an exclusive basis, Corona and Negra Modelo beers in Argentina, and the license for the production and distribution of Budweiser beer in Uruguay. CICSA received compensation in respect of these agreements in the amount of ARS 277.2 million, equivalent to US$34.2 million.

19

In September 2012, CCU acquired 100% of the shares of the Uruguayan companies Milotur S.A., Marzurel S.A. and Coralina S.A. and, indirectly, of Andrimar S.A., a wholly-owned subsidiary of Milotur S.A. These companies own the assets of a business developed in Uruguay that engages in the production and marketing of bottled mineral waters under the Nativa brand, and carbonated soft drinks under the Nix brand. This acquisition is in line with the Company’s strategic plan, which seeks to expand its activities into new markets. Milotur, our afilliate in Uruguay, also commercializes Schneider and Heineken beer brands, the latter due to an amendment to the trademark license agreement in force with Heineken Brouwerijen B.V.

In December 2013, CCU acquired 50.005% of Bebidas del Paraguay, and 49.959% of Distribuidora del Paraguay S.A., entering the Paraguayan market with the production, marketing and sale of non-alcoholic beverages, such as soft drinks, juices and water, and import, marketing and sale of beer, under various brands, both proprietary and under licensees and imported.

In 1994 we purchased 48.4% of the equity of the Chilean wine producer Viña San Pedro S.A. (“VSP”, today “VSPT” as described below) for approximately CLP 17,470 million. During the first half of 1995, VSPT’s capital was increased by approximately CLP 14,599 million, of which we contributed approximately CLP 7,953 million. From August through October 1997, VSPT’s capital was increased again by approximately CLP 11,872 million, of which we contributed approximately CLP 6,617 million, plus approximately CLP 191 million in additional shares bought during October 1997 in the local stock market. Furthermore, in October 1998 and during 1999, we purchased additional shares in VSPT through the local stock exchanges for an amount of approximately CLP 5,526 million. From March through June 1999, VSPT’s capital was increased by approximately CLP 17,464 million, of which we contributed approximately CLP 10,797 million. During 2000, VSPT, through its subsidiary Finca La Celia S.A. (“FLC”), acquired the winery Finca La Celia in Mendoza, Argentina, initiating its international expansion, allowing VSPT to include fine quality Argentine wines into its export product portfolio. In December 2001, Viña Santa Helena (“VSH”) created its own commercial and productive winemaking operation, distinct from its parent, VSPT, under the Viña Santa Helena label in the Colchagua Valley. Between November 2000 and March 2001, VSPT’s capital was increased by approximately CLP 22,279 million, of which we contributed approximately CLP 13,402 million. In August 2003, VSPT formed Viña Tabalí S.A., a joint venture in equal parts with Sociedad Agrícola y Ganadera Río Negro Ltda., for the production of premium wines. This winery is located in the Limarí Valley, Chile’s northernmost winemaking region, which is noted for the production of outstanding wines. In October 2004, VSPT acquired the well-known Manquehuito Pop Wine brand, a sparkling fruit-flavored wine with low alcohol content, broadening its range of products. At VSPT’s extraordinary shareholders meeting held on July 7, 2005, the shareholders voted to increase the number of board members from 7 to 9 and approved a capital increase that was to be partially used for stock option programs. During October and November 2005, VSPT’s capital was increased by approximately CLP 346 million. We did not participate in this capital increase. Viña Misiones de Rengo S.A. and Viña Urmeneta S.A. merged into Viña Valles de Chile S.A., of which the latter is the legal successor, with effect as of June 2013 and in May 2014 Vitivinícola del Maipo S.A merged into Viñas Orgánicas S.A., the latter being the legal successor. Additionally, in April 2015 Viña Santa Helena S.A. merged into Viña San Pedro Tarapacá S.A., pursuant to the Chilean Corporations Act, due to the fact that Viña San Pedro Tarapacá S.A. became the sole shareholder of the company for more than 10 days.

In January 2007, Viña Tabalí S.A. bought the assets of Viña Leyda, located in the Leyda Valley, a new winemaking region south of Casablanca Valley and close to the Pacific Ocean. Viña Leyda produces excellent wines that have won awards in different international contests. After this acquisition, Viña Tabalí S.A. changed its name to Viña Valles de Chile S.A. In September 2007, VSPT bought a 50% interest in Viña Altaïr S.A. which belonged to Château Dassault, in line with our strategy of focusing on premium wines. As a consequence, VSPT owns 100% of said company.