UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-06740

Legg Mason Partners Institutional Trust

(Exact name of registrant as specified in charter)

620 Eighth Avenue, 47th Floor, New York, NY 10018

(Address of principal executive offices) (Zip code)

Marc A. De Oliveira

Franklin Templeton

100 First Stamford Place

Stamford, CT 06902

(Name and address of agent for service)

Registrant’s telephone number, including area code:

877-6LM-FUND/656-3863

Date of fiscal year end: February 28

Date of reporting period: August 31, 2024

| ITEM 1. | REPORT TO STOCKHOLDERS. |

The Semi-Annual Report to Stockholders is filed herewith.

Western Asset SMASh Series M Fund |  | |

Semi-Annual Shareholder Report | August 31, 2024true | ||

| ||

You can find additional information about the Fund at https://www.franklintempleton.com/regulatory-fund-documents. You can also request this information by contacting us at 877-6LM-FUND/656-3863.

Fund Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment*,† |

Western Asset SMASh Series M Fund1 | $0 | 0.00% |

| * | Reflects fee waivers and/or expense reimbursements, without which expenses would have been higher. |

| † | Annualized. |

| 1 | Does not reflect the effect of fees and expenses associated with a separately managed account, or a management fee or other operating expenses of the Fund. |

Total Net Assets | $1,244,832,648 |

Total Number of Portfolio Holdings* | 375 |

Portfolio Turnover Rate | 83% |

| * | Does not include derivatives, except purchased options, if any. |

| * | Does not include derivatives, except purchased options, if any. |

| WHERE CAN I FIND ADDITIONAL INFORMATION ABOUT THE FUND? |

Additional information is available on https://www.franklintempleton.com/regulatory-fund-documents, including its: | |

| • prospectus • proxy voting information • financial information • holdings • tax information |

| Western Asset SMASh Series M Fund | PAGE 1 | 7936-STSR-1024 |

| ITEM 2. | CODE OF ETHICS. |

Not applicable.

| ITEM 3. | AUDIT COMMITTEE FINANCIAL EXPERT. |

Not applicable.

| Item 4. | Principal Accountant Fees and Services. |

Not applicable.

| ITEM 5. | AUDIT COMMITTEE OF LISTED REGISTRANTS. |

Not applicable.

| ITEM 6. | SCHEDULE OF INVESTMENTS. |

| (a) | Please see schedule of investments contained in the Financial Statements and Financial Highlights included under Item 7 of this Form N-CSR. |

| (b) | Not applicable. |

| ITEM 7. | FINANCIAL STATEMENTS AND FINANCIAL HIGLIGHTS FOR OPEN-END MANAGEMENT INVESTMENT COMPANIES. |

SMASh Series M Fund

1 | |

18 | |

19 | |

20 | |

21 | |

22 | |

36 | |

36 | |

36 | |

37 |

Security | Rate | Maturity Date | Face Amount | Value | |

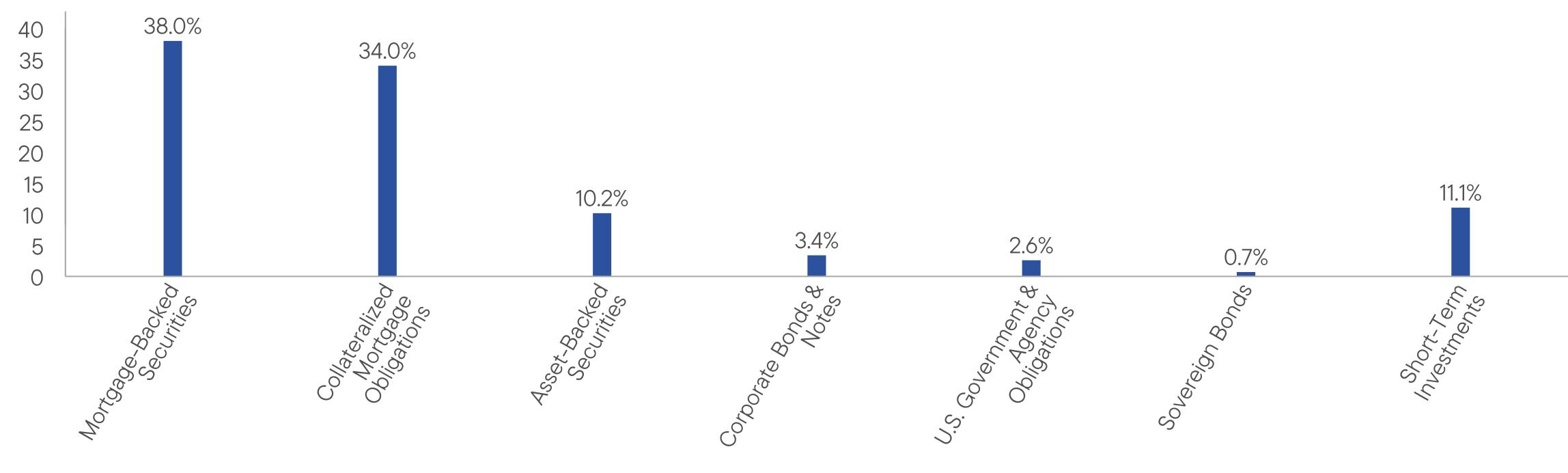

Mortgage-Backed Securities — 46.9% | |||||

FHLMC — 1.8% | |||||

Federal Home Loan Mortgage Corp. (FHLMC) | 5.500% | 12/1/38 | $3,497 | $3,582 | |

Federal Home Loan Mortgage Corp. (FHLMC) | 6.000% | 7/1/41 | 94,366 | 99,096 | |

Federal Home Loan Mortgage Corp. (FHLMC) | 3.500% | 10/1/42- 3/1/43 | 240,980 | 226,878 | |

Federal Home Loan Mortgage Corp. (FHLMC) | 2.000% | 3/1/51- 4/1/51 | 2,388,766 | 1,999,074 | |

Federal Home Loan Mortgage Corp. (FHLMC) | 6.500% | 10/1/53 | 9,470,084 | 9,853,046 | |

Federal Home Loan Mortgage Corp. (FHLMC) (1 year Refinitiv USD IBOR Consumer Cash Fallbacks + 1.619%) | 2.919% | 11/1/47 | 1,035,817 | 1,028,924 (a) | |

Federal Home Loan Mortgage Corp. (FHLMC) (1 year Refinitiv USD IBOR Consumer Cash Fallbacks + 1.621%) | 3.098% | 2/1/50 | 1,998,422 | 1,953,839 (a) | |

Federal Home Loan Mortgage Corp. (FHLMC) (1 year Refinitiv USD IBOR Consumer Cash Fallbacks + 1.627%) | 3.006% | 11/1/48 | 5,340,762 | 5,145,401 (a) | |

Federal Home Loan Mortgage Corp. (FHLMC) (5 year Treasury Constant Maturity Rate + 1.287%) | 2.131% | 3/1/47 | 897,222 | 862,851 (a) | |

Federal Home Loan Mortgage Corp. (FHLMC) Gold | 7.000% | 3/1/39 | 9,802 | 10,500 | |

Federal Home Loan Mortgage Corp. (FHLMC) Gold | 6.500% | 9/1/39 | 33,209 | 34,485 | |

Federal Home Loan Mortgage Corp. (FHLMC) Gold | 4.000% | 4/1/43- 7/1/43 | 532,412 | 514,887 | |

Total FHLMC | 21,732,563 | ||||

FNMA — 9.9% | |||||

Federal National Mortgage Association (FNMA) | 2.560% | 11/1/31 | 4,448,671 | 4,028,915 | |

Federal National Mortgage Association (FNMA) | 6.500% | 11/1/37- 5/1/40 | 183,794 | 192,801 | |

Federal National Mortgage Association (FNMA) | 5.000% | 6/1/38- 12/1/47 | 980,526 | 1,002,297 | |

Federal National Mortgage Association (FNMA) | 7.000% | 2/1/39 | 13,399 | 14,486 | |

Federal National Mortgage Association (FNMA) | 4.500% | 6/1/42- 8/1/58 | 5,719,272 | 5,619,771 | |

Federal National Mortgage Association (FNMA) | 4.000% | 10/1/42- 6/1/57 | 3,891,710 | 3,757,135 | |

1

Security | Rate | Maturity Date | Face Amount | Value | |

FNMA — continued | |||||

Federal National Mortgage Association (FNMA) | 3.000% | 6/1/43- 11/1/48 | $6,911,078 | $6,339,172 | |

Federal National Mortgage Association (FNMA) | 5.500% | 5/1/44- 7/1/53 | 740,221 | 754,908 | |

Federal National Mortgage Association (FNMA) | 2.000% | 8/1/50- 4/1/51 | 5,247,144 | 4,379,706 | |

Federal National Mortgage Association (FNMA) | 6.000% | 11/1/53 | 47,593,764 | 48,788,157 | |

Federal National Mortgage Association (FNMA) | 2.000% | 9/1/54 | 11,800,000 | 9,658,286 (b) | |

Federal National Mortgage Association (FNMA) | 2.500% | 9/1/54 | 8,600,000 | 7,335,034 (b) | |

Federal National Mortgage Association (FNMA) | 5.000% | 9/1/54 | 100,000 | 99,296 (b) | |

Federal National Mortgage Association (FNMA) | 5.500% | 9/1/54 | 29,600,000 | 29,805,613 (b) | |

Federal National Mortgage Association (FNMA) | 2.500% | 9/1/61 | 1,542,655 | 1,294,633 | |

Total FNMA | 123,070,210 | ||||

GNMA — 35.2% | |||||

Government National Mortgage Association (GNMA) | 3.000% | 9/15/42- 11/15/42 | 27,970,913 | 25,728,191 | |

Government National Mortgage Association (GNMA) | 3.500% | 6/15/48- 5/15/50 | 3,557,394 | 3,387,154 | |

Government National Mortgage Association (GNMA) | 4.000% | 3/15/50 | 62,643 | 60,298 | |

Government National Mortgage Association (GNMA) II | 6.000% | 8/20/37- 12/20/41 | 474,673 | 495,329 | |

Government National Mortgage Association (GNMA) II | 4.500% | 1/20/40- 9/20/52 | 36,635,252 | 36,206,416 | |

Government National Mortgage Association (GNMA) II | 5.000% | 7/20/40- 9/20/52 | 5,539,519 | 5,610,650 | |

Government National Mortgage Association (GNMA) II | 3.500% | 6/20/44- 2/20/50 | 25,259,995 | 23,768,751 | |

Government National Mortgage Association (GNMA) II | 4.000% | 9/20/45- 4/20/50 | 30,801,107 | 29,741,362 | |

Government National Mortgage Association (GNMA) II | 3.000% | 1/20/50- 3/20/52 | 662,492 | 597,803 | |

Government National Mortgage Association (GNMA) II | 2.000% | 12/20/50- 3/20/51 | 12,698,990 | 10,411,882 | |

2

Security | Rate | Maturity Date | Face Amount | Value | |

GNMA — continued | |||||

Government National Mortgage Association (GNMA) II | 2.500% | 12/20/50- 10/20/51 | $22,455,651 | $19,471,279 | |

Government National Mortgage Association (GNMA) II | 5.500% | 3/20/53- 8/20/53 | 3,822,031 | 3,854,590 | |

Government National Mortgage Association (GNMA) II | 2.500% | 9/20/54 | 49,600,000 | 43,373,885 (b) | |

Government National Mortgage Association (GNMA) II | 3.000% | 9/20/54 | 68,500,000 | 62,036,689 (b) | |

Government National Mortgage Association (GNMA) II | 3.500% | 9/20/54 | 16,500,000 | 15,368,740 (b) | |

Government National Mortgage Association (GNMA) II | 4.000% | 9/20/54 | 28,500,000 | 27,247,421 (b) | |

Government National Mortgage Association (GNMA) II | 4.500% | 9/20/54 | 32,500,000 | 31,841,113 (b) | |

Government National Mortgage Association (GNMA) II | 5.000% | 9/20/54 | 31,800,000 | 31,747,207 (b) | |

Government National Mortgage Association (GNMA) II | 5.500% | 9/20/54 | 27,000,000 | 27,181,267 (b) | |

Government National Mortgage Association (GNMA) II | 6.000% | 9/20/54 | 40,000,000 | 40,596,889 (b) | |

Total GNMA | 438,726,916 | ||||

Total Mortgage-Backed Securities (Cost — $595,474,442) | 583,529,689 | ||||

Collateralized Mortgage Obligations(c) — 41.9% | |||||

Alternative Loan Trust, 2005-24 1A1 (Federal Reserve U.S. 12 mo. Cumulative Avg 1 Year CMT + 1.310%) | 6.472% | 7/20/35 | 175,245 | 153,802 (a) | |

Alternative Loan Trust, 2005-57CB 4A3 | 5.500% | 12/25/35 | 205,753 | 113,921 | |

American Home Mortgage Investment Trust, 2005-1 1A3 (1 mo. Term SOFR + 0.734%) | 6.084% | 6/25/45 | 33,630 | 33,605 (a) | |

Arbor Realty Commercial Real Estate Notes Ltd., 2021-FL3 A (1 mo. Term SOFR + 1.184%) | 6.521% | 8/15/34 | 1,578,239 | 1,574,298 (a)(d) | |

AREIT Trust, 2021-CRE5 A (1 mo. Term SOFR + 1.194%) | 6.536% | 11/17/38 | 1,607,550 | 1,601,592 (a)(d) | |

Benchmark Mortgage Trust, 2020-B21 B | 2.458% | 12/17/53 | 13,020,000 | 10,512,232 | |

BHMS, 2018-ATLS A (1 mo. Term SOFR + 1.547%) | 6.884% | 7/15/35 | 8,350,000 | 8,350,119 (a)(d) | |

BRSP Ltd., 2021-FL1 A (1 mo. Term SOFR + 1.264%) | 6.606% | 8/19/38 | 3,482,517 | 3,462,528 (a)(d) | |

BX, 2021-MFM1 A (1 mo. Term SOFR + 0.814%) | 6.151% | 1/15/34 | 1,645,597 | 1,632,990 (a)(d) | |

3

Security | Rate | Maturity Date | Face Amount | Value | |

Collateralized Mortgage Obligations(c) — continued | |||||

BX Commercial Mortgage Trust, 2021-VOLT A (1 mo. Term SOFR + 0.814%) | 6.151% | 9/15/36 | $14,070,000 | $13,947,120 (a)(d) | |

BX Commercial Mortgage Trust, 2021-XL2 A (1 mo. Term SOFR + 0.803%) | 6.140% | 10/15/38 | 31,239,445 | 30,870,866 (a)(d) | |

BX Mortgage Trust, 2021-PAC A (1 mo. Term SOFR + 0.804%) | 6.141% | 10/15/36 | 26,580,000 | 26,339,395 (a)(d) | |

BX Trust, 2019-OC11 B | 3.605% | 12/9/41 | 3,200,000 | 2,958,012 (d) | |

BX Trust, 2021-ARIA A (1 mo. Term SOFR + 1.014%) | 6.351% | 10/15/36 | 13,415,000 | 13,315,532 (a)(d) | |

BX Trust, 2022-PSB A (1 mo. Term SOFR + 2.451%) | 7.788% | 8/15/39 | 9,934,177 | 9,977,630 (a)(d) | |

Chevy Chase Funding LLC Mortgage-Backed Certificates, 2003-4A A1 (1 mo. Term SOFR + 0.794%) | 6.072% | 10/25/34 | 493,028 | 475,068 (a)(d) | |

Commercial Mortgage Trust, 2014-CR20 B | 4.239% | 11/10/47 | 1,680,000 | 1,649,950 (a) | |

Commercial Mortgage Trust, 2018-COR3 B | 4.669% | 5/10/51 | 5,310,000 | 4,623,278 (a) | |

CSMC Trust, 2014-USA A2 | 3.953% | 9/15/37 | 3,290,000 | 2,939,838 (d) | |

CSMC Trust, 2017-RPL1 A1 | 2.750% | 7/25/57 | 3,223,987 | 3,107,877 (a)(d) | |

CSMC Trust, 2017-RPL1 M1 | 2.977% | 7/25/57 | 20,370,000 | 17,677,809 (a)(d) | |

CSMC Trust, 2017-RPL3 A1 | 4.000% | 8/1/57 | 10,486,870 | 9,912,282 (a)(d) | |

CSMC Trust, 2017-RPL3 B2 | 4.547% | 8/1/57 | 14,996,353 | 14,442,325 (a)(d) | |

CSMC Trust, 2019-UVIL A | 3.160% | 12/15/41 | 10,000,000 | 9,115,384 (d) | |

CSMC Trust, 2021-AFC1 A1 | 0.830% | 3/25/56 | 4,376,368 | 3,618,492 (a)(d) | |

CSMC Trust, 2021-RPL1 A1 | 4.067% | 9/27/60 | 10,695,678 | 10,708,249 (a)(d) | |

CSMC Trust, 2021-RPL3 A1 | 2.000% | 1/25/60 | 7,490,449 | 6,641,982 (a)(d) | |

CSMC Trust, 2021-RPL4 A1 | 4.068% | 12/27/60 | 5,732,704 | 5,762,229 (a)(d) | |

CSMC Trust, 2022-7R 1A1 (30 Day Average SOFR + 4.500%) | 9.846% | 10/25/66 | 18,005,605 | 17,264,183 (a)(d) | |

Extended Stay America Trust, 2021-ESH A (1 mo. Term SOFR + 1.194%) | 6.531% | 7/15/38 | 7,817,629 | 7,790,436 (a)(d) | |

Federal Home Loan Mortgage Corp. (FHLMC) Multiclass Certificates, 2020-RR07 AX, IO | 2.468% | 9/27/28 | 6,000,000 | 487,846 (a) | |

Federal Home Loan Mortgage Corp. (FHLMC) Multifamily Structured Pass-Through Certificates, K064 X1, IO | 0.730% | 3/25/27 | 46,642,446 | 594,034 (a) | |

Federal Home Loan Mortgage Corp. (FHLMC) Multifamily Structured Pass-Through Certificates, K091 X1, IO | 0.706% | 3/25/29 | 6,506,278 | 146,686 (a) | |

4

Security | Rate | Maturity Date | Face Amount | Value | |

Collateralized Mortgage Obligations(c) — continued | |||||

Federal Home Loan Mortgage Corp. (FHLMC) Multifamily Structured Pass-Through Certificates, K093 X1, IO | 1.082% | 5/25/29 | $5,733,843 | $207,032 (a) | |

Federal Home Loan Mortgage Corp. (FHLMC) Multifamily Structured Pass-Through Certificates, K118 X1, IO | 1.048% | 9/25/30 | 27,269,538 | 1,265,792 (a) | |

Federal Home Loan Mortgage Corp. (FHLMC) Multifamily Structured Pass-Through Certificates, K121 X1, IO | 1.115% | 10/25/30 | 53,801,751 | 2,629,738 (a) | |

Federal Home Loan Mortgage Corp. (FHLMC) Multifamily Structured Pass-Through Certificates, K122 X1, IO | 0.967% | 11/25/30 | 18,364,843 | 790,335 (a) | |

Federal Home Loan Mortgage Corp. (FHLMC) Multifamily Structured Pass-Through Certificates, K740 X1, IO | 0.824% | 9/25/27 | 35,135,214 | 659,889 (a) | |

Federal Home Loan Mortgage Corp. (FHLMC) Multifamily Structured Pass-Through Certificates, K1515 X1, IO | 1.635% | 2/25/35 | 45,073,095 | 4,910,565 (a) | |

Federal Home Loan Mortgage Corp. (FHLMC) Multifamily Structured Pass-Through Certificates, K1516 X1, IO | 1.628% | 5/25/35 | 29,663,476 | 3,456,086 (a) | |

Federal Home Loan Mortgage Corp. (FHLMC) Multifamily Structured Pass-Through Certificates, K1517 X1, IO | 1.436% | 7/25/35 | 40,304,736 | 4,085,836 (a) | |

Federal Home Loan Mortgage Corp. (FHLMC) Reference REMIC, R007 ZA | 6.000% | 5/15/36 | 10,524 | 11,063 | |

Federal Home Loan Mortgage Corp. (FHLMC) REMIC, 3947 SG, IO (-1.000 x 30 Day Average SOFR + 5.836%) | 0.482% | 10/15/41 | 113,276 | 12,787 (a) | |

Federal Home Loan Mortgage Corp. (FHLMC) REMIC, 4298 PI, IO, PAC | 4.000% | 4/15/43 | 42,752 | 531 | |

Federal Home Loan Mortgage Corp. (FHLMC) REMIC, 4813 CJ | 3.000% | 8/15/48 | 406,150 | 358,549 | |

Federal Home Loan Mortgage Corp. (FHLMC) REMIC, 5018 MI, IO | 2.000% | 10/25/50 | 1,250,472 | 169,549 | |

Federal Home Loan Mortgage Corp. (FHLMC) REMIC, 5040 IB, IO | 2.500% | 11/25/50 | 393,313 | 57,381 | |

Federal Home Loan Mortgage Corp. (FHLMC) REMIC, 5274 IO, IO | 2.500% | 1/25/51 | 20,959,412 | 3,546,326 | |

5

Security | Rate | Maturity Date | Face Amount | Value | |

Collateralized Mortgage Obligations(c) — continued | |||||

Federal Home Loan Mortgage Corp. (FHLMC) REMIC, Structured Agency Credit Risk Debt Notes, 2021-DNA2 M2 (30 Day Average SOFR + 2.300%) | 7.649% | 8/25/33 | $13,080,664 | $13,315,464 (a)(d) | |

Federal Home Loan Mortgage Corp. (FHLMC) REMIC, Structured Agency Credit Risk Debt Notes, 2021-DNA3 M2 (30 Day Average SOFR + 2.100%) | 7.449% | 10/25/33 | 25,033,680 | 25,455,039 (a)(d) | |

Federal Home Loan Mortgage Corp. (FHLMC) STRIPS, 328 S4, IO | 0.803% | 2/15/38 | 654,798 | 38,978 (a) | |

Federal Home Loan Mortgage Corp. (FHLMC) Structured Agency Credit Risk Debt Notes, 2015-DNA3 M3F (30 Day Average SOFR + 3.814%) | 9.163% | 4/25/28 | 1,773,872 | 1,816,928 (a) | |

Federal National Mortgage Association (FNMA) — CAS, 2021-R01 1M2 (30 Day Average SOFR + 1.550%) | 6.899% | 10/25/41 | 10,634,681 | 10,680,176 (a)(d) | |

Federal National Mortgage Association (FNMA) ACES, 2018-M15 1A2 | 3.700% | 1/25/36 | 3,000,000 | 2,863,487 | |

Federal National Mortgage Association (FNMA) ACES, 2019-M19 X2, IO | 0.741% | 9/25/29 | 33,907,028 | 830,885 (a) | |

Federal National Mortgage Association (FNMA) ACES, 2019-M22 A2 | 2.522% | 8/25/29 | 11,504,652 | 10,677,175 | |

Federal National Mortgage Association (FNMA) ACES, 2019-M28 XA2, IO | 0.321% | 2/25/30 | 5,254,737 | 46,467 (a) | |

Federal National Mortgage Association (FNMA) ACES, 2019-M28 XA3, IO | 0.707% | 2/25/30 | 9,448,193 | 215,024 (a) | |

Federal National Mortgage Association (FNMA) ACES, 2020-M4 1X2, IO | 0.841% | 2/25/28 | 5,206,224 | 106,970 (a) | |

Federal National Mortgage Association (FNMA) ACES, 2020-M4 1X3, IO | 1.121% | 2/25/28 | 28,272,860 | 783,684 (a) | |

Federal National Mortgage Association (FNMA) ACES, 2020-M26 X3, IO | 1.837% | 1/25/28 | 8,057,211 | 252,814 (a) | |

Federal National Mortgage Association (FNMA) ACES, 2020-M36 X1, IO | 1.543% | 9/25/34 | 2,701,306 | 154,653 (a) | |

Federal National Mortgage Association (FNMA) ACES, 2020-M51 X3, IO | 0.116% | 12/25/30 | 74,520,000 | 327,754 (a) | |

Federal National Mortgage Association (FNMA) ACES, 2020-M54 X, IO | 1.597% | 12/25/33 | 36,522,378 | 2,391,405 (a) | |

Federal National Mortgage Association (FNMA) REMIC, 2011-59 NZ | 5.500% | 7/25/41 | 161,515 | 169,408 | |

6

Security | Rate | Maturity Date | Face Amount | Value | |

Collateralized Mortgage Obligations(c) — continued | |||||

Federal National Mortgage Association (FNMA) REMIC, 2012-28 B | 6.500% | 6/25/39 | $538 | $552 | |

Federal National Mortgage Association (FNMA) REMIC, 2012-75 AO, PO | 0.000% | 3/25/42 | 7,036 | 6,313 | |

Federal National Mortgage Association (FNMA) REMIC, 2012-75 NS, IO (-1.000 x 30 Day Average SOFR + 6.486%) | 1.137% | 7/25/42 | 28,706 | 3,733 (a) | |

Federal National Mortgage Association (FNMA) REMIC, 2012-93 UI, IO | 3.000% | 9/25/27 | 98,769 | 2,737 | |

Federal National Mortgage Association (FNMA) REMIC, 2012-134 SK, IO (-1.000 x 30 Day Average SOFR + 6.036%) | 0.687% | 12/25/42 | 236,392 | 28,105 (a) | |

Federal National Mortgage Association (FNMA) REMIC, 2013-9 CB | 5.500% | 4/25/42 | 46,826 | 48,551 | |

Federal National Mortgage Association (FNMA) REMIC, 2013-14 IG, IO | 4.000% | 3/25/43 | 120,658 | 21,259 | |

Federal National Mortgage Association (FNMA) REMIC, 2013-29 QI, IO | 4.000% | 4/25/43 | 388,279 | 69,889 | |

Federal National Mortgage Association (FNMA) REMIC, 2013-73 IB, IO | 3.500% | 7/25/28 | 240,630 | 7,328 | |

Federal National Mortgage Association (FNMA) REMIC, 2014-47 AI, IO | 0.696% | 8/25/44 | 504,808 | 29,094 (a) | |

Federal National Mortgage Association (FNMA) REMIC, 2020-47 GZ | 2.000% | 7/25/50 | 978,146 | 610,363 | |

Federal National Mortgage Association (FNMA) STRIPS, 390 C3, IO | 6.000% | 7/25/38 | 7,175 | 1,515 | |

Federal National Mortgage Association (FNMA) STRIPS, 407 22, IO | 5.000% | 1/25/39 | 5,031 | 944 | |

Federal National Mortgage Association (FNMA) STRIPS, 407 23, IO | 5.000% | 1/25/39 | 2,619 | 492 (a) | |

Federal National Mortgage Association (FNMA) STRIPS, 407 27, IO | 5.500% | 1/25/39 | 2,722 | 563 (a) | |

Federal National Mortgage Association (FNMA) STRIPS, 407 34, IO | 5.000% | 1/25/38 | 4,241 | 640 | |

Federal National Mortgage Association (FNMA) STRIPS, 407 41, IO | 6.000% | 1/25/38 | 6,344 | 1,306 | |

Federal National Mortgage Association (FNMA) STRIPS, 407 C10, IO | 5.000% | 1/25/38 | 26,387 | 4,116 | |

Federal National Mortgage Association (FNMA) STRIPS, 409 C2, IO | 3.000% | 4/25/27 | 28,789 | 742 | |

7

Security | Rate | Maturity Date | Face Amount | Value | |

Collateralized Mortgage Obligations(c) — continued | |||||

Federal National Mortgage Association (FNMA) STRIPS, 409 C13, IO | 3.500% | 11/25/41 | $42,059 | $6,575 | |

FRESB Mortgage Trust, 2015-SB7 A10 | 2.950% | 9/25/35 | 1,687,349 | 1,651,973 (a) | |

GMACM Mortgage Loan Trust, 2006-AR1 1A1 | 3.619% | 4/19/36 | 330,078 | 267,859 (a) | |

Government National Mortgage Association (GNMA), 2010-85 HS, IO, PAC (-1.000 x 1 mo. Term SOFR + 6.536%) | 1.200% | 1/20/40 | 43 | 0 (a)(e) | |

Government National Mortgage Association (GNMA), 2011-140 AI, IO | 4.000% | 10/16/26 | 10,351 | 1 | |

Government National Mortgage Association (GNMA), 2011-H01 AF (1 mo. Term SOFR + 0.564%) | 5.896% | 11/20/60 | 127,116 | 126,866 (a) | |

Government National Mortgage Association (GNMA), 2011-H11 FB (1 mo. Term SOFR + 0.614%) | 5.946% | 4/20/61 | 186,989 | 186,598 (a) | |

Government National Mortgage Association (GNMA), 2012-43 SN, IO (-1.000 x 1 mo. Term SOFR + 6.486%) | 1.147% | 4/16/42 | 1,209,055 | 194,776 (a) | |

Government National Mortgage Association (GNMA), 2013-105 IO, IO | 0.151% | 6/16/54 | 13,739,161 | 14,324 (a) | |

Government National Mortgage Association (GNMA), 2014-134 IA, IO | 0.141% | 1/16/55 | 49,531,308 | 218,614 (a) | |

Government National Mortgage Association (GNMA), 2014-157 IO, IO | 0.188% | 5/16/55 | 7,552,324 | 46,843 (a) | |

Government National Mortgage Association (GNMA), 2014-176 IA, IO | 4.000% | 11/20/44 | 359,095 | 70,093 | |

Government National Mortgage Association (GNMA), 2015-36 MI, IO | 5.500% | 3/20/45 | 451,007 | 64,106 | |

Government National Mortgage Association (GNMA), 2015-167 OI, IO | 4.000% | 4/16/45 | 189,519 | 34,161 | |

Government National Mortgage Association (GNMA), 2017-28 IO, IO | 0.702% | 2/16/57 | 753,528 | 28,878 (a) | |

Government National Mortgage Association (GNMA), 2018-H07 FD (1 mo. Term SOFR + 0.414%) | 5.746% | 5/20/68 | 392,817 | 393,005 (a) | |

Government National Mortgage Association (GNMA), 2019-90 AB | 3.000% | 7/20/49 | 3,190,790 | 2,872,062 | |

Government National Mortgage Association (GNMA), 2019-H01 FT (1 mo. Term SOFR + 0.514%) | 5.846% | 10/20/68 | 60,388 | 60,226 (a) | |

8

Security | Rate | Maturity Date | Face Amount | Value | |

Collateralized Mortgage Obligations(c) — continued | |||||

Government National Mortgage Association (GNMA), 2019-H08 FE (1 mo. Term SOFR + 0.764%) | 6.096% | 1/20/69 | $390,694 | $387,773 (a) | |

Government National Mortgage Association (GNMA), 2020-47 MI, IO, PAC | 3.500% | 4/20/50 | 1,298,278 | 236,111 | |

Government National Mortgage Association (GNMA), 2020-47 NI, IO, PAC | 3.500% | 4/20/50 | 589,317 | 107,483 | |

Government National Mortgage Association (GNMA), 2020-127 IN, IO | 2.500% | 8/20/50 | 548,677 | 76,225 | |

Government National Mortgage Association (GNMA), 2020-129 IE, IO | 2.500% | 9/20/50 | 573,284 | 78,672 | |

Government National Mortgage Association (GNMA), 2020-160 IH, IO | 2.500% | 10/20/50 | 370,071 | 52,556 | |

Government National Mortgage Association (GNMA), 2020-160 VI, IO | 2.500% | 10/20/50 | 641,043 | 88,967 | |

Government National Mortgage Association (GNMA), 2020-H09 FL (1 mo. Term SOFR + 1.264%) | 6.596% | 5/20/70 | 1,773,923 | 1,795,785 (a) | |

Government National Mortgage Association (GNMA), 2020-H09 NF (1 mo. Term SOFR + 1.364%) | 6.696% | 4/20/70 | 1,802,747 | 1,823,647 (a) | |

Government National Mortgage Association (GNMA), 2020-H12 F (1 mo. Term SOFR + 0.614%) | 5.946% | 7/20/70 | 481,604 | 475,464 (a) | |

Government National Mortgage Association (GNMA), 2020-H13 FC (1 mo. Term SOFR + 0.564%) | 5.896% | 7/20/70 | 223,024 | 219,370 (a) | |

Government National Mortgage Association (GNMA), 2020-H13 FM (1 mo. Term SOFR + 0.514%) | 5.846% | 8/20/70 | 1,798,191 | 1,788,058 (a) | |

Government National Mortgage Association (GNMA), 2020-171 IO, IO | 0.957% | 10/16/60 | 85,723,250 | 5,786,362 (a) | |

Greystone CRE Notes Ltd., 2021-FL3 A (1 mo. Term SOFR + 1.134%) | 6.471% | 7/15/39 | 3,880,000 | 3,859,389 (a)(d) | |

GS Mortgage Securities Corp. Trust, 2021- ROSS C (1 mo. Term SOFR + 2.264%) | 7.601% | 5/15/26 | 2,894,000 | 1,827,422 (a)(d) | |

GS Mortgage Securities Corp. Trust, 2021- ROSS D (1 mo. Term SOFR + 2.764%) | 8.101% | 5/15/26 | 8,660,000 | 4,279,444 (a)(d) | |

GS Mortgage Securities Trust, 2018-GS9 B | 4.321% | 3/10/51 | 1,725,000 | 1,572,814 (a) | |

GS Mortgage-Backed Securities Corp. Trust, 2021-RPL1 A2 | 2.000% | 12/25/60 | 16,090,000 | 13,725,959 (a)(d) | |

9

Security | Rate | Maturity Date | Face Amount | Value | |

Collateralized Mortgage Obligations(c) — continued | |||||

GS Mortgage-Backed Securities Trust, 2018- RPL1 A1A | 3.750% | 10/25/57 | $8,880,920 | $8,662,146 (d) | |

HomeBanc Mortgage Trust, 2004-2 A1 (1 mo. Term SOFR + 0.854%) | 6.132% | 12/25/34 | 913,610 | 862,591 (a) | |

IMPAC CMB Trust, 2004-7 1A1 (1 mo. Term SOFR + 0.854%) | 6.132% | 11/25/34 | 1,424,858 | 1,402,454 (a) | |

JPMBB Commercial Mortgage Securities Trust, 2015-C30 AS | 4.226% | 7/15/48 | 10,544,000 | 10,053,035 (a) | |

JPMorgan Chase Commercial Mortgage Securities Trust, 2014-C20, C | 4.682% | 7/15/47 | 700,000 | 610,563 (a) | |

JPMorgan Mortgage Trust, 2018-4 A1 | 3.500% | 10/25/48 | 1,724,074 | 1,544,612 (a)(d) | |

JPMorgan Resecuritization Trust, 2014-6 1A2 (1 mo. Term SOFR + 0.324%) | 3.244% | 7/27/36 | 3,952,315 | 3,598,282 (a)(d) | |

KREF Ltd., 2021-FL2 A (1 mo. Term SOFR + 1.184%) | 6.523% | 2/15/39 | 4,351,179 | 4,268,189 (a)(d) | |

MASTR Adjustable Rate Mortgages Trust, 2005-7 3A1 | 3.842% | 9/25/35 | 55,683 | 34,094 (a) | |

Merrill Lynch Mortgage Investors Trust, 2006-A1 1A1 | 4.871% | 3/25/36 | 277,460 | 167,385 (a) | |

MF1 Ltd., 2021-FL7 A (1 mo. Term SOFR + 1.194%) | 6.536% | 10/16/36 | 2,916,320 | 2,900,828 (a)(d) | |

MIC Trust, 2023-MIC A | 8.732% | 12/5/38 | 3,470,000 | 3,813,004 (a)(d) | |

Morgan Stanley Bank of America Merrill Lynch Trust, 2017-C33 A5 | 3.599% | 5/15/50 | 5,580,000 | 5,383,033 | |

MSWF Commercial Mortgage Trust, 2023-2 A5 | 6.014% | 12/15/56 | 8,800,000 | 9,568,418 (a) | |

New Residential Mortgage Loan Trust, 2016-3A A1B | 3.250% | 9/25/56 | 2,145,249 | 2,014,990 (a)(d) | |

New Residential Mortgage Loan Trust, 2016-4A A1 | 3.750% | 11/25/56 | 2,673,306 | 2,541,491 (a)(d) | |

New Residential Mortgage Loan Trust, 2017-4A A1 | 4.000% | 5/25/57 | 8,582,710 | 8,268,274 (a)(d) | |

New Residential Mortgage Loan Trust, 2019-2A A1 | 4.250% | 12/25/57 | 10,801,219 | 10,542,661 (a)(d) | |

New Residential Mortgage Loan Trust, 2021- NQM3 A1 | 1.156% | 11/27/56 | 4,319,820 | 3,714,353 (a)(d) | |

OPG Trust, 2021-PORT D (1 mo. Term SOFR + 1.245%) | 6.582% | 10/15/36 | 2,450,500 | 2,386,903 (a)(d) | |

PRKCM Trust, 2021-AFC1 A1 | 1.510% | 8/25/56 | 14,875,671 | 12,518,631 (a)(d) | |

RALI Trust, 2006-QO7 3A2 (1 mo. Term SOFR + 0.524%) | 5.802% | 9/25/46 | 237,459 | 228,450 (a) | |

10

Security | Rate | Maturity Date | Face Amount | Value | |

Collateralized Mortgage Obligations(c) — continued | |||||

RAMP Trust, 2005-SL1 A7 | 8.000% | 5/25/32 | $11,553 | $7,487 | |

SFO Commercial Mortgage Trust, 2021-555 A (1 mo. Term SOFR + 1.264%) | 6.601% | 5/15/38 | 16,490,000 | 15,542,471 (a)(d) | |

SREIT Trust, 2021-PALM A (1 mo. Term SOFR + 0.704%) | 6.041% | 10/15/34 | 12,605,000 | 12,404,710 (a)(d) | |

Structured Adjustable Rate Mortgage Loan Trust, 2004-2 4A1 | 5.897% | 3/25/34 | 54,985 | 52,845 (a) | |

Structured Asset Mortgage Investments II Trust, 2005-AR7 4A1 (Federal Reserve U.S. 12 mo. Cumulative Avg 1 Year CMT + 2.150%) | 7.312% | 3/25/46 | 85,724 | 79,061 (a) | |

Structured Asset Securities Corp. Mortgage Pass-Through Certificates, 2003-9A 2A2 | 6.651% | 3/25/33 | 51,596 | 50,017 (a) | |

Towd Point Mortgage Trust, 2019-HY2 A1 (1 mo. Term SOFR + 1.114%) | 6.392% | 5/25/58 | 4,723,197 | 4,868,401 (a)(d) | |

Towd Point Mortgage Trust, 2020-2 M1B | 3.000% | 4/25/60 | 8,740,000 | 6,988,562 (a)(d) | |

WaMu Mortgage Pass-Through Certificates Trust, 2004-AR13 A1B2 (1 mo. Term SOFR + 1.094%) | 6.372% | 11/25/34 | 3,495,885 | 3,264,629 (a) | |

WaMu Mortgage Pass-Through Certificates Trust, 2005-AR9 A1A (1 mo. Term SOFR + 0.754%) | 6.032% | 7/25/45 | 30,143 | 29,882 (a) | |

Wells Fargo Commercial Mortgage Trust, 2017-C38 A5 | 3.453% | 7/15/50 | 2,030,000 | 1,957,473 | |

WFRBS Commercial Mortgage Trust, 2014- C24 B | 4.204% | 11/15/47 | 1,670,000 | 1,566,489 (a) | |

Total Collateralized Mortgage Obligations (Cost — $551,895,887) | 521,242,477 | ||||

Asset-Backed Securities — 12.5% | |||||

Bayview Financial Asset Trust, 2007-SR1A M2 (1 mo. Term SOFR + 1.014%) | 6.292% | 3/25/37 | 277,838 | 275,531 (a)(d) | |

Blackbird Capital Aircraft Lease Securitization Ltd., 2016-1A A, Step bond (4.213% to 12/15/24 then 6.500%) | 4.213% | 12/16/41 | 9,292,092 | 9,217,313 (d) | |

Countrywide Asset-Backed Certificates Trust, 2004-5 2A (1 mo. Term SOFR + 0.614%) | 5.892% | 10/25/34 | 1,578,850 | 1,538,227 (a) | |

Countrywide Asset-Backed Certificates Trust, 2006-SD3 A1 (1 mo. Term SOFR + 0.774%) | 6.052% | 7/25/36 | 5,601 | 5,554 (a)(d) | |

Foundation Finance Trust, 2021-1A A | 1.270% | 5/15/41 | 2,361,970 | 2,187,340 (d) | |

Goodgreen Trust, 2021-1A A | 2.660% | 10/15/56 | 7,378,699 | 6,311,038 (d) | |

Hertz Vehicle Financing LLC, 2021-1A A | 1.210% | 12/26/25 | 981,333 | 973,022 (d) | |

Hertz Vehicle Financing LP, 2021-2A A | 1.680% | 12/27/27 | 6,380,000 | 5,969,171 (d) | |

Hertz Vehicle Financing LP, 2021-2A B | 2.120% | 12/27/27 | 8,290,000 | 7,718,110 (d) | |

11

Security | Rate | Maturity Date | Face Amount | Value | |

Asset-Backed Securities — continued | |||||

MASTR Asset-Backed Securities Trust, 2007- NCW A1 (1 mo. Term SOFR + 0.414%) | 5.692% | 5/25/37 | $3,757,535 | $3,335,962 (a)(d) | |

Morgan Stanley Mortgage Loan Trust, 2007- 2AX 2A1 (1 mo. Term SOFR + 0.294%) | 5.572% | 12/25/36 | 17,985 | 6,520 (a) | |

Navient Private Education Refi Loan Trust, 2019-FA A2 | 2.600% | 8/15/68 | 7,282,259 | 6,944,346 (d) | |

Navient Student Loan Trust, 2017-2A A (30 Day Average SOFR + 1.164%) | 6.513% | 12/27/66 | 18,428,941 | 18,493,520 (a)(d) | |

Navient Student Loan Trust, 2021-1A A1B (30 Day Average SOFR + 0.714%) | 6.063% | 12/26/69 | 1,694,724 | 1,675,594 (a)(d) | |

Nelnet Student Loan Trust, 2021-A B1 | 2.850% | 4/20/62 | 17,500,000 | 15,184,771 (d) | |

Origen Manufactured Housing Contract Trust, 2007-A A2 | 7.850% | 4/15/37 | 145,842 | 137,347 (a) | |

RAAC Trust, 2006-SP1 M1 (1 mo. Term SOFR + 0.714%) | 5.992% | 9/25/45 | 448,877 | 438,859 (a) | |

Renaissance Home Equity Loan Trust, 2003-2 A | 3.602% | 8/25/33 | 534,759 | 490,341 (a) | |

Renaissance Home Equity Loan Trust, 2007-3 AV2 (1 mo. Term SOFR + 1.114%) | 6.392% | 9/25/37 | 155,999 | 134,005 (a) | |

Renaissance Home Equity Loan Trust, 2007-3 AV3 (1 mo. Term SOFR + 1.914%) | 7.192% | 9/25/37 | 682,999 | 586,642 (a) | |

Residential Funding Securities Corp., 2002- RP2 A1 (1 mo. Term SOFR + 1.614%) | 6.892% | 10/25/32 | 1,503 | 1,485 (a)(d) | |

SLM Student Loan Trust, 2003-10A A4 (90 Day Average SOFR + 0.931%) | 6.284% | 12/17/68 | 5,679,974 | 5,668,988 (a)(d) | |

SMB Private Education Loan Trust, 2020-A A2A | 2.230% | 9/15/37 | 9,086,133 | 8,669,657 (d) | |

SMB Private Education Loan Trust, 2021-A A2B | 1.590% | 1/15/53 | 12,012,140 | 10,964,683 (d) | |

SMB Private Education Loan Trust, 2021-A B | 2.310% | 1/15/53 | 7,389,059 | 7,020,098 (d) | |

SMB Private Education Loan Trust, 2021-C D | 3.930% | 1/15/53 | 2,714,400 | 2,408,732 (d) | |

SMB Private Education Loan Trust, 2023-B A1B (30 Day Average SOFR + 1.800%) | 7.154% | 10/16/56 | 5,256,925 | 5,374,366 (a)(d) | |

SMB Private Education Loan Trust, 2024-A A1A | 5.240% | 3/15/56 | 24,011,534 | 24,377,561 (d) | |

Structured Asset Securities Corp., 2004-SC1 A | 8.145% | 12/25/29 | 5,790 | 5,153 (a)(d) | |

Structured Asset Securities Corp. Mortgage Pass-Through Certificates, 2001-SB1 A2 | 3.375% | 8/25/31 | 22,356 | 22,273 | |

Sunrun Vulcan Issuer LLC, 2021-1A A | 2.460% | 1/30/52 | 2,929,938 | 2,499,145 (d) | |

12

Security | Rate | Maturity Date | Face Amount | Value | |

Asset-Backed Securities — continued | |||||

Thrust Engine Leasing, 2021-1A A | 4.163% | 7/15/40 | $7,584,440 | $7,251,971 (d) | |

Total Asset-Backed Securities (Cost — $163,853,636) | 155,887,325 | ||||

Corporate Bonds & Notes — 4.2% | |||||

Communication Services — 1.1% | |||||

Diversified Telecommunication Services — 0.4% | |||||

AT&T Inc., Senior Notes | 2.250% | 2/1/32 | 1,100,000 | 928,054 | |

Verizon Communications Inc., Senior Notes | 2.355% | 3/15/32 | 2,210,000 | 1,878,479 | |

Verizon Communications Inc., Senior Notes | 4.500% | 8/10/33 | 2,160,000 | 2,101,439 | |

Total Diversified Telecommunication Services | 4,907,972 | ||||

Media — 0.4% | |||||

Charter Communications Operating LLC/ Charter Communications Operating Capital Corp., Senior Secured Notes | 5.375% | 5/1/47 | 900,000 | 750,998 | |

Charter Communications Operating LLC/ Charter Communications Operating Capital Corp., Senior Secured Notes | 5.125% | 7/1/49 | 2,890,000 | 2,317,410 | |

Comcast Corp., Senior Notes | 3.969% | 11/1/47 | 1,460,000 | 1,192,610 | |

Comcast Corp., Senior Notes | 2.887% | 11/1/51 | 1,170,000 | 766,534 | |

Total Media | 5,027,552 | ||||

Wireless Telecommunication Services — 0.3% | |||||

T-Mobile USA Inc., Senior Notes | 3.875% | 4/15/30 | 3,410,000 | 3,281,613 | |

Total Communication Services | 13,217,137 | ||||

Energy — 0.6% | |||||

Oil, Gas & Consumable Fuels — 0.6% | |||||

EOG Resources Inc., Senior Notes | 3.900% | 4/1/35 | 2,210,000 | 2,040,580 | |

EQT Corp., Senior Notes | 7.000% | 2/1/30 | 5,000,000 | 5,450,545 | |

Total Energy | 7,491,125 | ||||

Financials — 0.6% | |||||

Banks — 0.4% | |||||

BAC Capital Trust XIV, Ltd. GTD (3 mo. Term SOFR + 0.662%) | 6.001% | 9/16/24 | 200,000 | 170,685 (a)(f) | |

Banco Santander SA, Senior Notes (4.175% to 3/24/27 then 1 year Treasury Constant Maturity Rate + 2.000%) | 4.175% | 3/24/28 | 800,000 | 786,871 (a) | |

Bank of Nova Scotia, Subordinated Notes (4.588% to 5/4/32 then 5 year Treasury Constant Maturity Rate + 2.050%) | 4.588% | 5/4/37 | 4,420,000 | 4,147,937 (a) | |

13

Security | Rate | Maturity Date | Face Amount | Value | |

Banks — continued | |||||

Cooperatieve Rabobank UA, Senior Notes (3.758% to 4/6/32 then 1 year Treasury Constant Maturity Rate + 1.420%) | 3.758% | 4/6/33 | $880,000 | $812,029 (a)(d) | |

Total Banks | 5,917,522 | ||||

Capital Markets — 0.2% | |||||

UBS AG, Senior Notes | 3.700% | 2/21/25 | 2,250,000 | 2,234,233 | |

Total Financials | 8,151,755 | ||||

Industrials — 1.6% | |||||

Air Freight & Logistics — 1.6% | |||||

DP World Ltd., Senior Notes | 5.625% | 9/25/48 | 20,510,000 | 20,472,313 (d) | |

Materials — 0.3% | |||||

Chemicals — 0.2% | |||||

OCP SA, Senior Notes | 4.500% | 10/22/25 | 1,980,000 | 1,962,620 (d) | |

Metals & Mining — 0.1% | |||||

Freeport-McMoRan Inc., Senior Notes | 5.450% | 3/15/43 | 1,550,000 | 1,519,258 | |

Total Materials | 3,481,878 | ||||

Total Corporate Bonds & Notes (Cost — $54,015,725) | 52,814,208 | ||||

U.S. Government & Agency Obligations — 3.3% | |||||

U.S. Government Obligations — 3.3% | |||||

U.S. Treasury Notes (Cost — $39,494,828) | 4.000% | 1/31/29 | 40,000,000 | 40,410,938 | |

Sovereign Bonds — 0.8% | |||||

Mexico — 0.7% | |||||

Mexico Government International Bond, Senior Notes | 4.600% | 2/10/48 | 6,810,000 | 5,413,876 | |

Mexico Government International Bond, Senior Notes | 5.750% | 10/12/2110 | 3,430,000 | 2,943,968 | |

Total Mexico | 8,357,844 | ||||

Qatar — 0.1% | |||||

Qatar Government International Bond, Senior Notes | 4.817% | 3/14/49 | 1,880,000 | 1,850,261 (d) | |

Total Sovereign Bonds (Cost — $12,597,952) | 10,208,105 | ||||

Total Investments before Short-Term Investments (Cost — $1,417,332,470) | 1,364,092,742 | ||||

Short-Term Investments — 13.7% | |||||

U.S. Treasury Bills — 7.7% | |||||

U.S. Cash Management Bill | 4.048% | 9/12/24 | 34,130,000 | 34,085,503 (g) | |

U.S. Treasury Bills | 5.020% | 10/31/24 | 18,500,000 | 18,349,184 (g) | |

U.S. Treasury Bills | 5.012% | 11/29/24 | 21,960,000 | 21,696,773 (g) | |

U.S. Treasury Bills | 4.505% | 5/15/25 | 21,970,000 | 21,298,804 (g) | |

Total U.S. Treasury Bills (Cost — $95,304,161) | 95,430,264 | ||||

14

Security | Rate | Maturity Date | Face Amount | Value | |

Repurchase Agreements — 2.0% | |||||

Goldman Sachs & Co. repurchase agreement dated 8/30/24; Proceeds at maturity — $25,014,611; (Fully collateralized by U.S. government obligations, 3.750% due 12/31/28; Market value—$25,310,950) (Cost — $25,000,000) | 5.260% | 9/3/24 | $25,000,000 | $25,000,000 | |

Shares | |||||

Overnight Deposits — 4.0% | |||||

BNY Mellon Cash Reserve Fund (Cost — $49,909,425) | 2.100% | 49,909,425 | 49,909,425 (h) | ||

Total Short-Term Investments (Cost — $170,213,586) | 170,339,689 | ||||

Total Investments — 123.3% (Cost — $1,587,546,056) | 1,534,432,431 | ||||

Liabilities in Excess of Other Assets — (23.3)% | (289,599,783 ) | ||||

Total Net Assets — 100.0% | $1,244,832,648 | ||||

(a) | Variable rate security. Interest rate disclosed is as of the most recent information available. Certain variable rate securities are not based on a published reference rate and spread but are determined by the issuer or agent and are based on current market conditions. These securities do not indicate a reference rate and spread in their description above. |

(b) | This security is traded on a to-be-announced (“TBA”) basis. At August 31, 2024, the Fund held TBA securities with a total cost of $326,036,668. |

(c) | Collateralized mortgage obligations are secured by an underlying pool of mortgages or mortgage pass-through certificates that are structured to direct payments on underlying collateral to different series or classes of the obligations. The interest rate may change positively or inversely in relation to one or more interest rates, financial indices or other financial indicators and may be subject to an upper and/or lower limit. |

(d) | Security is exempt from registration under Rule 144A of the Securities Act of 1933. This security may be resold in transactions that are exempt from registration, normally to qualified institutional buyers. This security has been deemed liquid pursuant to guidelines approved by the Board of Trustees. |

(e) | Value is less than $1. |

(f) | Security has no maturity date. The date shown represents the next call date. |

(g) | Rate shown represents yield-to-maturity. |

(h) | Rate shown is one-day yield as of the end of the reporting period. |

15

Abbreviation(s) used in this schedule: | ||

ACES | — | Alternative Credit Enhancement Securities |

CAS | — | Connecticut Avenue Securities |

CMT | — | Constant Maturity Treasury |

GTD | — | Guaranteed |

IBOR | — | Interbank Offered Rate |

IO | — | Interest Only |

PAC | — | Planned Amortization Class |

PO | — | Principal Only |

REMIC | — | Real Estate Mortgage Investment Conduit |

SOFR | — | Secured Overnight Financing Rate |

STRIPS | — | Separate Trading of Registered Interest and Principal Securities |

USD | — | United States Dollar |

Number of Contracts | Expiration Date | Notional Amount | Market Value | Unrealized Appreciation (Depreciation) | |

Contracts to Buy: | |||||

U.S. Treasury 2-Year Notes | 2,068 | 12/24 | $429,187,329 | $429,206,940 | $19,611 |

U.S. Treasury 5-Year Notes | 18,782 | 12/24 | 2,060,831,683 | 2,054,721,500 | (6,110,183 ) |

U.S. Treasury 10-Year Notes | 69 | 12/24 | 7,877,471 | 7,835,812 | (41,659 ) |

U.S. Treasury Long- Term Bonds | 38 | 12/24 | 4,739,660 | 4,678,750 | (60,910 ) |

(6,193,141 ) | |||||

Contracts to Sell: | |||||

U.S. Treasury Ultra 10-Year Notes | 19 | 12/24 | 2,246,764 | 2,231,313 | 15,451 |

U.S. Treasury Ultra Long-Term Bonds | 301 | 12/24 | 40,258,082 | 39,713,188 | 544,894 |

560,345 | |||||

Net unrealized depreciation on open futures contracts | $(5,632,796 ) | ||||

16

CENTRALLY CLEARED CREDIT DEFAULT SWAPS ON CREDIT INDICES — SELL PROTECTION1 | ||||||

Reference Entity | Notional Amount2 | Termination Date | Periodic Payments Received by the Fund† | Market Value3 | Upfront Premiums Paid (Received) | Unrealized Appreciation |

Markit CDX.NA.IG.42 Index | $130,599,000 | 6/20/29 | 1.000% quarterly | $2,895,715 | $2,642,853 | $252,862 |

1 | If the Fund is a seller of protection and a credit event occurs, as defined under the terms of that particular swap agreement, the Fund will either (i) pay to the buyer of protection an amount equal to the notional amount of the swap and take delivery of the referenced obligation or underlying securities comprising the referenced index or (ii) pay a net settlement amount in the form of cash or securities equal to the notional amount of the swap less the recovery value of the referenced obligation or underlying securities comprising the referenced index. |

2 | The maximum potential amount the Fund could be required to pay as a seller of credit protection or receive as a buyer of credit protection if a credit event occurs as defined under the terms of that particular swap agreement. |

3 | The quoted market prices and resulting values for credit default swap agreements on asset-backed securities and credit indices serve as an indicator of the current status of the payment/performance risk and represent the likelihood of an expected loss (or profit) for the credit derivative had the notional amount of the swap agreement been closed/sold as of the period end. Decreasing market values (sell protection) or increasing market values (buy protection), when compared to the notional amount of the swap, represent a deterioration of the referenced entity’s credit soundness and a greater likelihood or risk of default or other credit event occurring as defined under the terms of the agreement. |

† | Percentage shown is an annual percentage rate. |

17

Assets: | |

Investments, at value (Cost — $1,587,546,056) | $1,534,432,431 |

Cash | 1,816 |

Receivable for securities sold | 81,167,310 |

Deposits with brokers for open futures contracts | 25,996,138 |

Interest receivable | 4,535,919 |

Deposits with brokers for centrally cleared swap contracts | 2,806,365 |

Receivable for Fund shares sold | 486,556 |

Principal paydown receivable | 82,681 |

Receivable from brokers — net variation margin on centrally cleared swap contracts | 53,809 |

Receivable from investment manager | 27,122 |

Prepaid expenses | 15,486 |

Total Assets | 1,649,605,633 |

Liabilities: | |

Payable for securities purchased | 377,910,242 |

Payable for Fund shares repurchased | 22,868,626 |

Payable to brokers — net variation margin on open futures contracts | 3,898,217 |

Trustees’ fees payable | 5,486 |

Accrued expenses | 90,414 |

Total Liabilities | 404,772,985 |

Total Net Assets | $1,244,832,648 |

Net Assets: | |

Par value (Note 5) | $1,562 |

Paid-in capital in excess of par value | 1,844,992,517 |

Total distributable earnings (loss) | (600,161,431 ) |

Total Net Assets | $1,244,832,648 |

Shares Outstanding | 156,171,779 |

Net Asset Value | $7.97 |

18

Investment Income: | |

Interest | $31,880,604 |

Total Investment Income | 31,880,604 |

Expenses: | |

Fund accounting fees | 41,374 |

Audit and tax fees | 24,702 |

Registration fees | 23,093 |

Legal fees | 22,808 |

Trustees’ fees | 16,470 |

Shareholder reports | 12,766 |

Commitment fees (Note 6) | 6,202 |

Commodity pool reports | 5,861 |

Transfer agent fees (Note 2) | 1,669 |

Custody fees | 1,274 |

Miscellaneous expenses | 5,937 |

Total Expenses | 162,156 |

Less: Fee waivers and/or expense reimbursements (Note 2) | (162,156 ) |

Net Expenses | — |

Net Investment Income | 31,880,604 |

Realized and Unrealized Gain (Loss) on Investments, Futures Contracts and Swap Contracts (Notes 1, 3 and 4): | |

Net Realized Gain From: | |

Investment transactions | 3,205,084 |

Futures contracts | 36,164,494 |

Swap contracts | 1,921,829 |

Net Realized Gain | 41,291,407 |

Change in Net Unrealized Appreciation (Depreciation) From: | |

Investments | 28,711,530 |

Futures contracts | (7,429,252 ) |

Swap contracts | (1,057,451 ) |

Change in Net Unrealized Appreciation (Depreciation) | 20,224,827 |

Net Gain on Investments, Futures Contracts and Swap Contracts | 61,516,234 |

Increase in Net Assets From Operations | $93,396,838 |

19

For the Six Months Ended August 31, 2024 (unaudited) and the Year Ended February 29, 2024 | August 31 | February 29 |

Operations: | ||

Net investment income | $31,880,604 | $63,381,918 |

Net realized gain (loss) | 41,291,407 | (67,808,570 ) |

Change in net unrealized appreciation (depreciation) | 20,224,827 | 32,643,039 |

Increase in Net Assets From Operations | 93,396,838 | 28,216,387 |

Distributions to Shareholders From (Note 1): | ||

Total distributable earnings | (31,743,872 ) | (67,860,612 ) |

Decrease in Net Assets From Distributions to Shareholders | (31,743,872 ) | (67,860,612 ) |

Fund Share Transactions (Note 5): | ||

Net proceeds from sale of shares | 148,122,591 | 404,132,769 |

Cost of shares repurchased | (308,009,423 ) | (452,739,286 ) |

Decrease in Net Assets From Fund Share Transactions | (159,886,832 ) | (48,606,517 ) |

Decrease in Net Assets | (98,233,866 ) | (88,250,742 ) |

Net Assets: | ||

Beginning of period | 1,343,066,514 | 1,431,317,256 |

End of period | $1,244,832,648 | $1,343,066,514 |

20

For a share of beneficial interest outstanding throughout each year ended February 28, unless otherwise noted: | ||||||

20241,2 | 20241,3 | 20231 | 20221 | 20211 | 20201,3 | |

Net asset value, beginning of period | $7.61 | $7.82 | $10.12 | $10.88 | $11.04 | $10.85 |

Income (loss) from operations: | ||||||

Net investment income | 0.18 | 0.35 | 0.25 | 0.12 | 0.17 | 0.30 |

Net realized and unrealized gain (loss) | 0.36 | (0.18 ) | (2.25 ) | (0.62 ) | 0.43 | 0.67 |

Total income (loss) from operations | 0.54 | 0.17 | (2.00) | (0.50) | 0.60 | 0.97 |

Less distributions from: | ||||||

Net investment income | (0.18 ) | (0.38 ) | (0.30 ) | (0.26 ) | (0.26 ) | (0.33 ) |

Net realized gains | — | — | — | — | (0.50 ) | (0.45 ) |

Total distributions | (0.18 ) | (0.38 ) | (0.30 ) | (0.26 ) | (0.76 ) | (0.78 ) |

Net asset value, end of period | $7.97 | $7.61 | $7.82 | $10.12 | $10.88 | $11.04 |

Total return4 | 7.27 % | 2.17 % | (19.91 )% | (4.69 )% | 5.53 % | 9.14 % |

Net assets, end of period (millions) | $1,245 | $1,343 | $1,431 | $2,164 | $2,706 | $3,300 |

Ratios to average net assets: | ||||||

Gross expenses5 | 0.02 %6 | 0.02 % | 0.02 % | 0.02 % | 0.02 % | 0.02 % |

Net expenses7,8 | 0.00 6 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

Net investment income | 4.77 6 | 4.54 | 2.88 | 1.11 | 1.56 | 2.71 |

Portfolio turnover rate9 | 83 % | 142 % | 83 % | 140 % | 381 % | 486 % |

1 | Per share amounts have been calculated using the average shares method. |

2 | For the six months ended August 31, 2024 (unaudited). |

3 | For the year ended February 29. |

4 | Performance figures do not reflect the effect of fees and expenses associated with a separately managed account, nor a management fee or other operating expenses of the Fund. Such management fees are paid directly or indirectly by the separately managed account sponsor to the Fund’s manager or subadvisers. All operating expenses of the Fund were reimbursed by the manager, pursuant to an expense reimbursement arrangement between the Fund and the manager. If such fees were included, the total return would have been lower. Past performance is no guarantee of future results. Total returns for periods of less than one year are not annualized. |

5 | Gross expenses do not include management fees paid to the manager and subadvisers. Management fees are paid directly or indirectly by the separately managed account sponsor. |

6 | Annualized. |

7 | The Fund’s manager has entered into an expense reimbursement arrangement with the Fund, pursuant to which the Fund’s manager has agreed to reimburse 100% of the Fund’s ordinary operating expenses. The expense reimbursement arrangement does not cover interest, brokerage, taxes and extraordinary expenses. This arrangement cannot be terminated prior to December 31, 2025 without the Board of Trustees’ consent. |

8 | Reflects fee waivers and/or expense reimbursements. |

9 | Including mortgage dollar roll transactions. If mortgage dollar roll transactions had been excluded, the portfolio turnover rates for the respective years/periods presented would have been 37%, 46%, 63%, 53%, 247% and 303%. |

21

22

23

ASSETS | ||||

Description | Quoted Prices (Level 1) | Other Significant Observable Inputs (Level 2) | Significant Unobservable Inputs (Level 3) | Total |

Long-Term Investments†: | ||||

Mortgage-Backed Securities | — | $583,529,689 | — | $583,529,689 |

Collateralized Mortgage Obligations | — | 521,242,477 | — | 521,242,477 |

Asset-Backed Securities | — | 155,887,325 | — | 155,887,325 |

Corporate Bonds & Notes | — | 52,814,208 | — | 52,814,208 |

U.S. Government & Agency Obligations | — | 40,410,938 | — | 40,410,938 |

Sovereign Bonds | — | 10,208,105 | — | 10,208,105 |

Total Long-Term Investments | — | 1,364,092,742 | — | 1,364,092,742 |

Short-Term Investments†: | ||||

U.S. Treasury Bills | — | 95,430,264 | — | 95,430,264 |

Repurchase Agreements | — | 25,000,000 | — | 25,000,000 |

Overnight Deposits | — | 49,909,425 | — | 49,909,425 |

Total Short-Term Investments | — | 170,339,689 | — | 170,339,689 |

Total Investments | — | $1,534,432,431 | — | $1,534,432,431 |

24

ASSETS (cont’d) | ||||

Description | Quoted Prices (Level 1) | Other Significant Observable Inputs (Level 2) | Significant Unobservable Inputs (Level 3) | Total |

Other Financial Instruments: | ||||

Futures Contracts†† | $579,956 | — | — | $579,956 |

Centrally Cleared Credit Default Swaps on Credit Indices — Sell Protection†† | — | $252,862 | — | 252,862 |

Total Other Financial Instruments | $579,956 | $252,862 | — | $832,818 |

Total | $579,956 | $1,534,685,293 | — | $1,535,265,249 |

LIABILITIES | ||||

Description | Quoted Prices (Level 1) | Other Significant Observable Inputs (Level 2) | Significant Unobservable Inputs (Level 3) | Total |

Other Financial Instruments: | ||||

Futures Contracts†† | $6,212,752 | — | — | $6,212,752 |

† | See Schedule of Investments for additional detailed categorizations. |

†† | Reflects the unrealized appreciation (depreciation) of the instruments. |

25

26

27

28

29

30

31

32

Investments | U.S. Government & Agency Obligations | |

Purchases | $24,992,318 | $1,117,694,156 |

Sales | 90,707,796 | 1,041,676,876 |

Cost/Premiums Paid (Received) | Gross Unrealized Appreciation | Gross Unrealized Depreciation | Net Unrealized Appreciation (Depreciation) | |

Securities | $1,595,784,570 | $8,078,036 | $(69,430,175) | $(61,352,139) |

Futures contracts | — | 579,956 | (6,212,752) | (5,632,796) |

Swap contracts | 2,642,853 | 252,862 | — | 252,862 |

33

ASSET DERIVATIVES1 | |||

Interest Rate Risk | Credit Risk | Total | |

Futures contracts2 | $579,956 | — | $579,956 |

Centrally cleared swap contracts3 | — | $252,862 | 252,862 |

Total | $579,956 | $252,862 | $832,818 |

LIABILITY DERIVATIVES1 | |

Interest Rate Risk | |

Futures contracts2 | $6,212,752 |

1 | Generally, the balance sheet location for asset derivatives is receivables/net unrealized appreciation and for liability derivatives is payables/net unrealized depreciation. |

2 | Includes cumulative unrealized appreciation (depreciation) of futures contracts as reported in the Schedule of Investments. Only net variation margin is reported within the receivables and/or payables on the Statement of Assets and Liabilities. |

3 | Includes cumulative unrealized appreciation (depreciation) of centrally cleared swap contracts as reported in the Schedule of Investments. Only net variation margin is reported within the receivables and/or payables on the Statement of Assets and Liabilities. |

AMOUNT OF NET REALIZED GAIN (LOSS) ON DERIVATIVES RECOGNIZED | |||

Interest Rate Risk | Credit Risk | Total | |

Futures contracts | $36,164,494 | — | $36,164,494 |

Swap contracts | — | $1,921,829 | 1,921,829 |

Total | $36,164,494 | $1,921,829 | $38,086,323 |

CHANGE IN NET UNREALIZED APPRECIATION (DEPRECIATION) ON DERIVATIVES RECOGNIZED | |||

Interest Rate Risk | Credit Risk | Total | |

Futures contracts | $(7,429,252 ) | — | $(7,429,252 ) |

Swap contracts | — | $(1,057,451 ) | (1,057,451 ) |

Total | $(7,429,252 ) | $(1,057,451 ) | $(8,486,703 ) |

34

Average Market Value | |

Futures contracts (to buy) | $2,481,931,768 |

Futures contracts (to sell) | 40,182,230 |

Average Notional Balance | |

Credit default swap contracts (sell protection) | $133,931,200 |

Six Months Ended August 31, 2024 | Year Ended February 29, 2024 | |

Shares sold | 19,539,687 | 52,235,644 |

Shares repurchased | (39,855,507 ) | (58,808,672 ) |

Net decrease | (20,315,820 ) | (6,573,028 ) |

35

36

37

38

39

40

Chairman

Services, LLC

3344 Quality Drive

Rancho Cordova, CA 95670-7313

public accounting firm

Baltimore, MD

Legg Mason Funds

620 Eighth Avenue, 47th Floor

New York, NY 10018

Your Privacy Is Our Priority

https://www.franklintempleton.com/help/privacy-policy or contact us for a copy at (800) 632-2301.

| ITEM 8. | CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS FOR OPEN-END MANAGEMENT INVESTMENT COMPANIES. |

The information is disclosed as part of the Financial Statements included in Item 7 of this Form N-CSR.

| ITEM 9. | PROXY DISCLOSURES FOR OPEN-END MANAGEMENT INVESTMENT COMPANIES. |

The information is disclosed as part of the Financial Statements included in Item 7 of this Form N-CSR.

| ITEM 10. | REMUNERATION PAID TO DIRECTORS, OFFICERS, AND OTHERS OF OPEN-END MANAGEMENT INVESTMENT COMPANIES. |

The information is disclosed as part of the Financial Statements included in Item 7 of this Form N-CSR.

| ITEM 11. | STATEMENT REGARDING BASIS FOR APPROVAL OF INVESTMENT ADVISORY CONTRACT. |

The information is disclosed as part of the Financial Statements included in Item 7 of this Form N-CSR, as applicable.

| ITEM 12. | DISCLOSURE OF PROXY VOTING POLICIES AND PROCEDURES FOR CLOSED-END MANAGEMENT INVESTMENT COMPANIES. |

Not applicable.

| ITEM 13. | PORTFOLIO MANAGERS OF CLOSED-END MANAGEMENT INVESTMENT COMPANIES. |

Not applicable.

| ITEM 14. | PURCHASES OF SECURITIES BY CLOSED-END MANAGEMENT INVESTMENT COMPANY AND AFFILIATED PURCHASERS. |

Not applicable.

| ITEM 15. | SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS. |

Not applicable.

| ITEM 16. | CONTROLS AND PROCEDURES. |

| (a) | The registrant’s principal executive officer and principal financial officer have concluded that the registrant’s disclosure controls and procedures (as defined in Rule 30a- 3(c) under the Investment Company Act of 1940, as amended (the “1940 Act”)) are effective as of a date within 90 days of the filing date of this report that includes the disclosure required by this paragraph, based on their evaluation of the disclosure controls and procedures required by Rule 30a-3(b) under the 1940 Act and 15d-15(b) under the Securities Exchange Act of 1934. |

| (b) | There were no changes in the registrant’s internal control over financial reporting (as defined in Rule 30a-3(d) under the 1940 Act) that occurred during the period covered by this report that have materially affected, or are likely to materially affect the registrant’s internal control over financial reporting. |

| ITEM 17. | DISCLOSURE OF SECURITIES LENDING ACTIVITIES FOR CLOSED-END MANAGEMENT INVESTMENT COMPANIES. |

Not applicable.

| ITEM 18. | RECOVERY OF ERRONEOUSLY AWARDED COMPENSATION. |

| (a) | Not applicable. |

| (b) | Not applicable. |

| ITEM 19. | EXHIBITS. |

(a) (1) Not applicable.

Exhibit 99.CODE ETH

(a) (2) Certifications pursuant to section 302 of the Sarbanes-Oxley Act of 2002 attached hereto.

Exhibit 99.CERT

(b) Certifications pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 attached hereto.

Exhibit 99.906CERT

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, the registrant has duly caused this Report to be signed on its behalf by the undersigned, there unto duly authorized.

| Legg Mason Partners Institutional Trust | ||

| By: | /s/ Jane Trust | |

| Jane Trust | ||

| Chief Executive Officer | ||

| Date: | October 24, 2024 | |

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, this report has been signed below by the following persons on behalf of the registrant and in the capacities and on the dates indicated.

| By: | /s/ Jane Trust | |

| Jane Trust | ||

| Chief Executive Officer | ||

| Date: | October 24, 2024 |

| By: | /s/ Christopher Berarducci | |

| Christopher Berarducci | ||

| Principal Financial Officer | ||

| Date: | October 24, 2024 |