Exhibit 99.1

Investor Presentation As of December 31, 2017

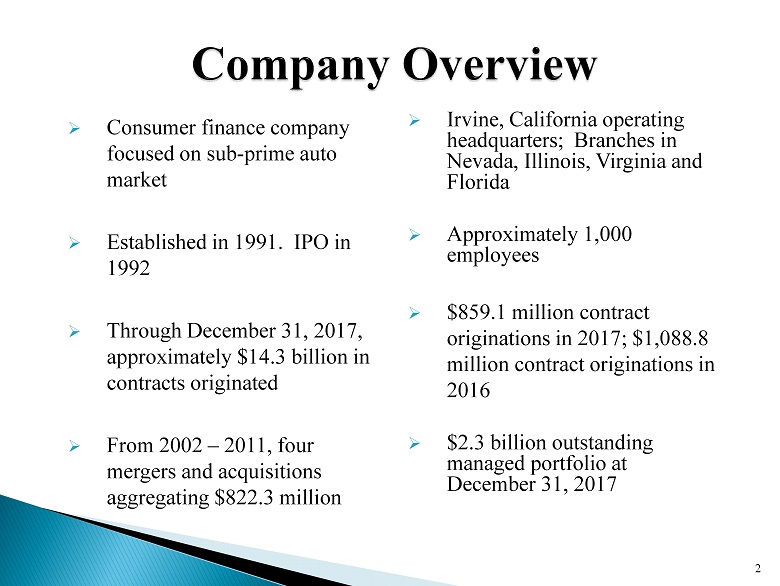

2 » Consumer finance company focused on sub - prime auto market » Established in 1991. IPO in 1992 » Through December 31, 2017, approximately $14.3 billion in contracts originated » From 2002 – 2011, four mergers and acquisitions aggregating $822.3 million » Irvine, California operating headquarters; Branches in Nevada, Illinois, Virginia and Florida » Approximately 1,000 employees » $859.1 million contract originations in 2017; $1,088.8 million contract originations in 2016 » $2.3 billion outstanding managed portfolio at December 31, 2017

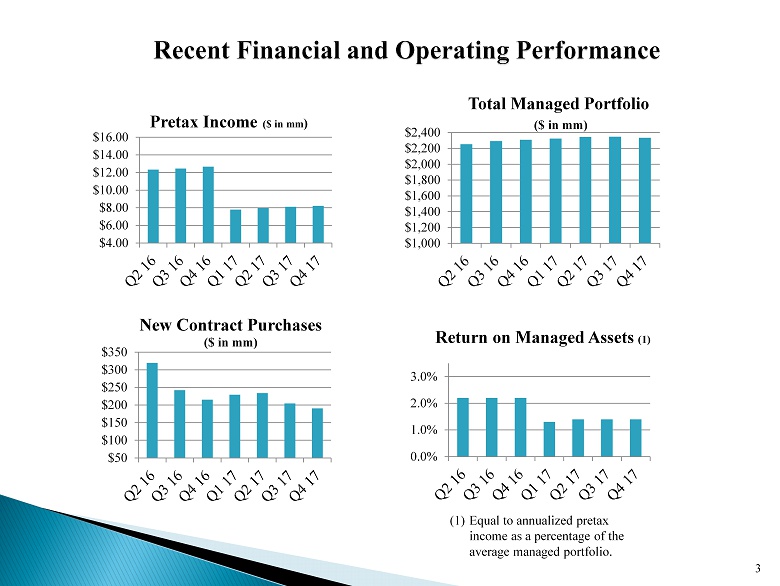

3 $1,000 $1,200 $1,400 $1,600 $1,800 $2,000 $2,200 $2,400 Total Managed Portfolio ($ in mm) $4.00 $6.00 $8.00 $10.00 $12.00 $14.00 $16.00 Pretax Income ($ in mm ) $50 $100 $150 $200 $250 $300 $350 New Contract Purchases ($ in mm) (1) Equal to annualized pretax income as a percentage of the average managed portfolio. 0.0% 1.0% 2.0% 3.0% Return on Managed Assets (1)

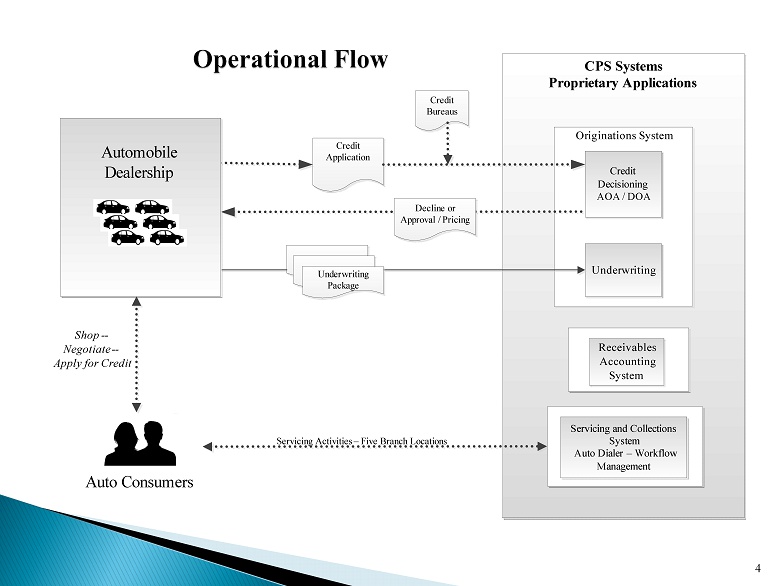

4 CPS Systems Proprietary Applications Credit Decisioning AOA / DOA Underwriting Servicing and Collections System Auto Dialer –Workflow Management Receivables Accounting System Credit Application Servicing Activities –Five Branch Locations Decline or Approval / Pricing Credit Bureaus Underwriting Package Originations System Automobile Dealership Auto Consumers Shop -- Negotiate -- Apply for Credit

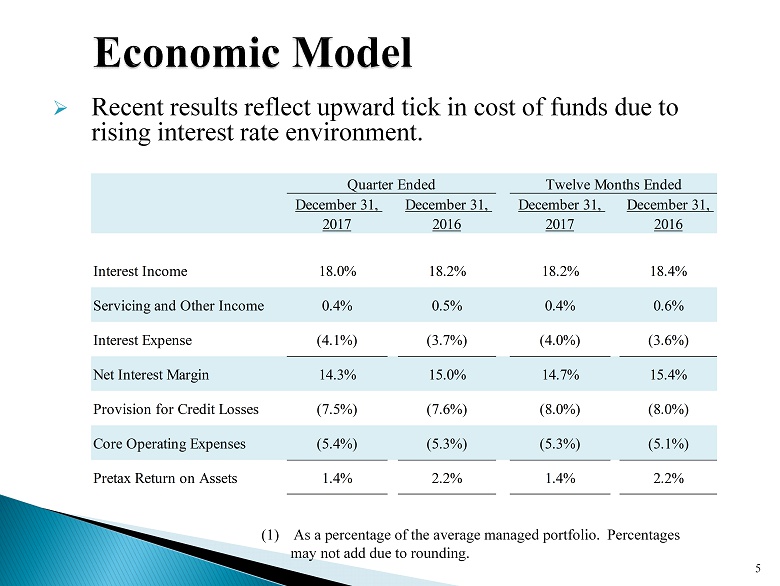

5 » Recent results reflect upward tick in cost of funds due to rising interest rate environment. (1) As a percentage of the average managed portfolio. Percentages may not add due to rounding. December 31, 2017 December 31, 2016 December 31, 2017 December 31, 2016 Interest Income 18.0% 18.2% 18.2% 18.4% Servicing and Other Income 0.4% 0.5% 0.4% 0.6% Interest Expense (4.1%) (3.7%) (4.0%) (3.6%) Net Interest Margin 14.3% 15.0% 14.7% 15.4% Provision for Credit Losses (7.5%) (7.6%) (8.0%) (8.0%) Core Operating Expenses (5.4%) (5.3%) (5.3%) (5.1%) Pretax Return on Assets 1.4% 2.2% 1.4% 2.2% Quarter Ended Twelve Months Ended

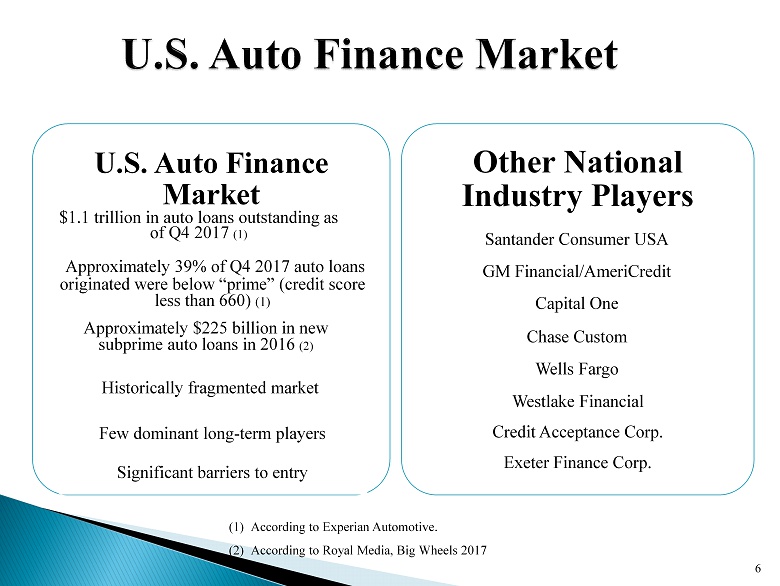

U.S. Auto Finance Market $1.1 trillion in auto loans outstanding as of Q4 2017 (1) Approximately 39% of Q4 2017 auto loans originated were below “prime” (credit score less than 660) (1) Approximately $225 billion in new subprime auto loans in 2016 (2) Historically fragmented market Few dominant long - term players Significant barriers to entry Other National Industry Players Santander Consumer USA GM Financial/AmeriCredit Capital One Chase Custom Wells Fargo Westlake Financial Credit Acceptance Corp. Exeter Finance Corp. 6 (1) According to Experian Automotive. (2) According to Royal Media, Big Wheels 2017

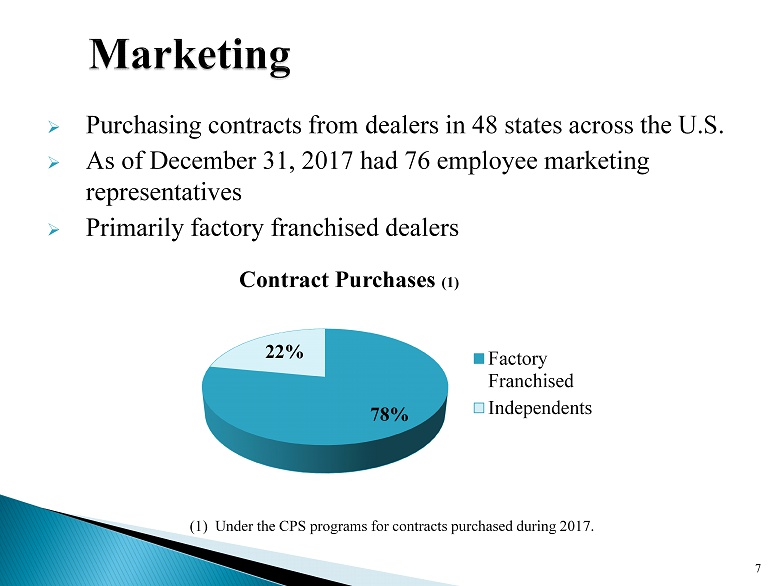

» Purchasing contracts from dealers in 48 states across the U.S. » As of December 31, 2017 had 76 employee marketing representatives » Primarily factory franchised dealers 7 (1) Under the CPS programs for contracts purchased during 2017. 78% 22% Contract Purchases (1) Factory Franchised Independents

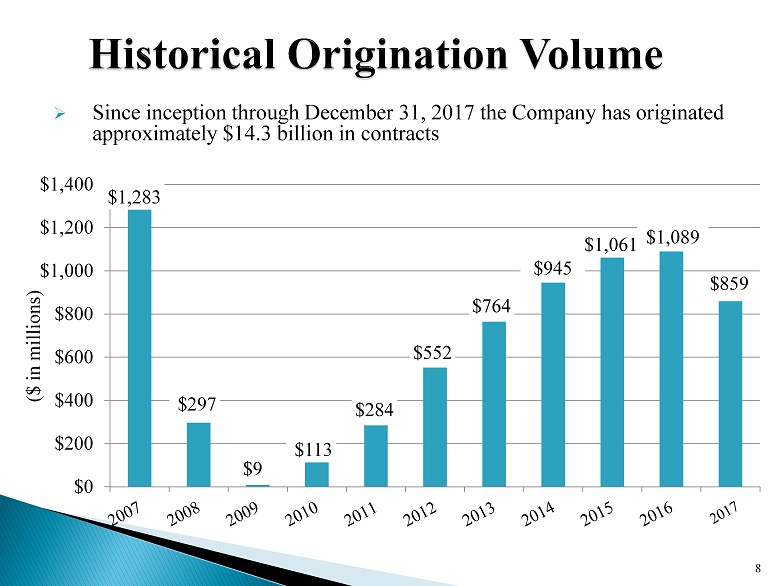

$284 $1,283 $297 $9 $113 $552 $764 $945 $0 $200 $400 $600 $800 $1,000 $1,200 $1,400 ($ in millions) $1,089 8 » Since inception through December 31, 2017 the Company has originated approximately $14.3 billion in contracts $1,061 $859

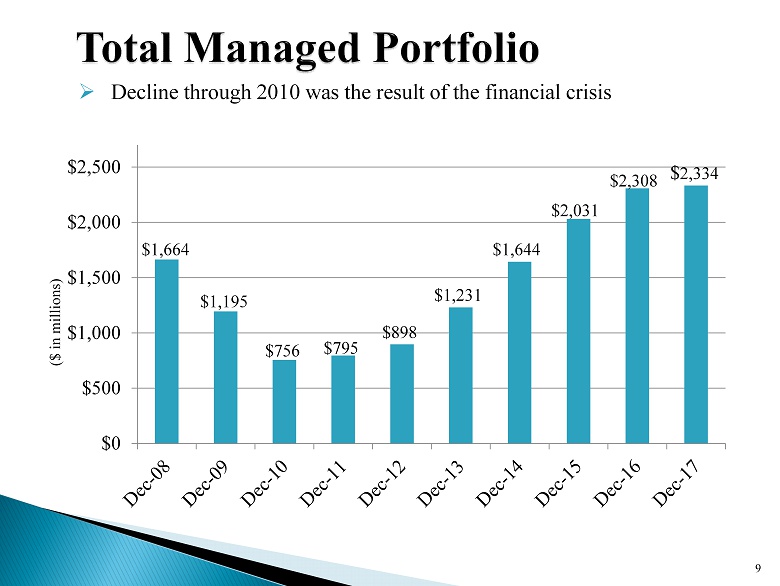

$0 $500 $1,000 $1,500 $2,000 $2,500 $898 ($ in millions) $2,308 $1,664 $1,195 $756 $795 $1,231 $1,644 $2,031 9 » Decline through 2010 was the result of the financial crisis $ 2,334

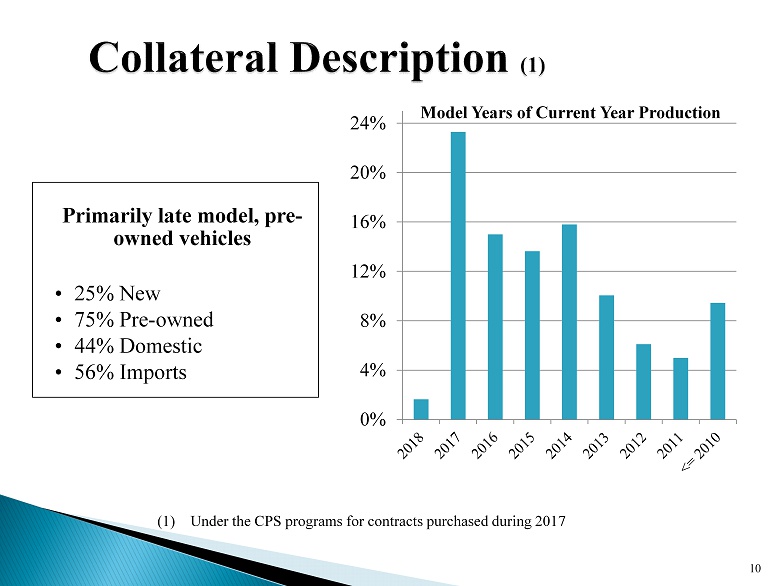

0% 4% 8% 12% 16% 20% 24% Model Years of Current Year Production 10 • 25% New • 75% Pre - owned • 44% Domestic • 56% Imports Primarily late model, pre - owned vehicles (1) Under the CPS programs for contracts purchased during 2017

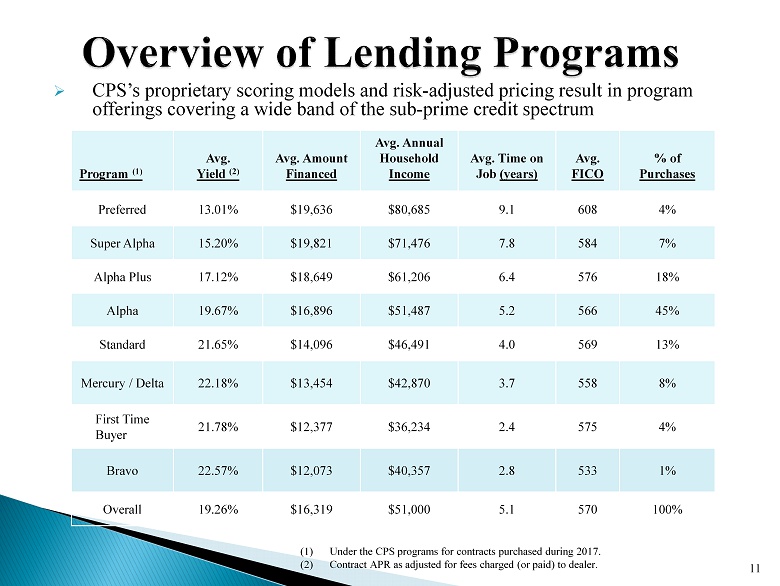

11 » CPS’s proprietary scoring models and risk - adjusted pricing result in program offerings covering a wide band of the sub - prime credit spectrum (1) Under the CPS programs for contracts purchased during 2017. (2) Contract APR as adjusted for fees charged (or paid) to dealer. Program (1) Avg. Yield (2) Avg. Amount Financed Avg. Annual Household Income Avg. Time on Job (years) Avg. FICO % of Purchases Preferred 13.01% $19,636 $80,685 9.1 608 4% Super Alpha 15.20% $19,821 $71,476 7.8 584 7% Alpha Plus 17.12% $18,649 $61,206 6.4 576 18% Alpha 19.67% $16,896 $51,487 5.2 566 45% Standard 21.65% $14,096 $46,491 4.0 569 13% Mercury / Delta 22.18% $13,454 $42,870 3.7 558 8% First Time Buyer 21.78% $12,377 $36,234 2.4 575 4% Bravo 22.57% $12,073 $40,357 2.8 533 1% Overall 19.26% $16,319 $51,000 5.1 570 100%

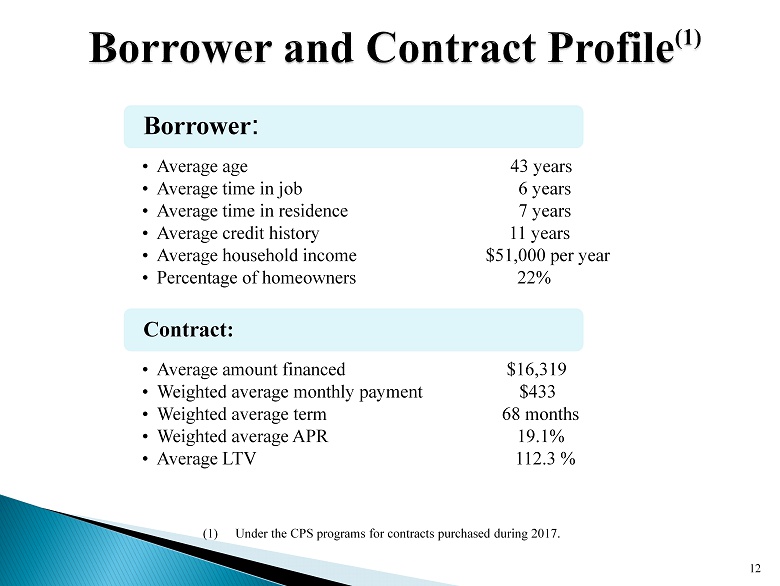

• Average age 43 years • Average time in job 6 years • Average time in residence 7 years • Average credit history 11 years • Average household income $51,000 per year • Percentage of homeowners 22% Borrower : • Average amount financed $16,319 • Weighted average monthly payment $433 • Weighted average term 68 months • Weighted average APR 19.1% • Average LTV 112.3 % Contract: 12 (1) Under the CPS programs for contracts purchased during 2017.

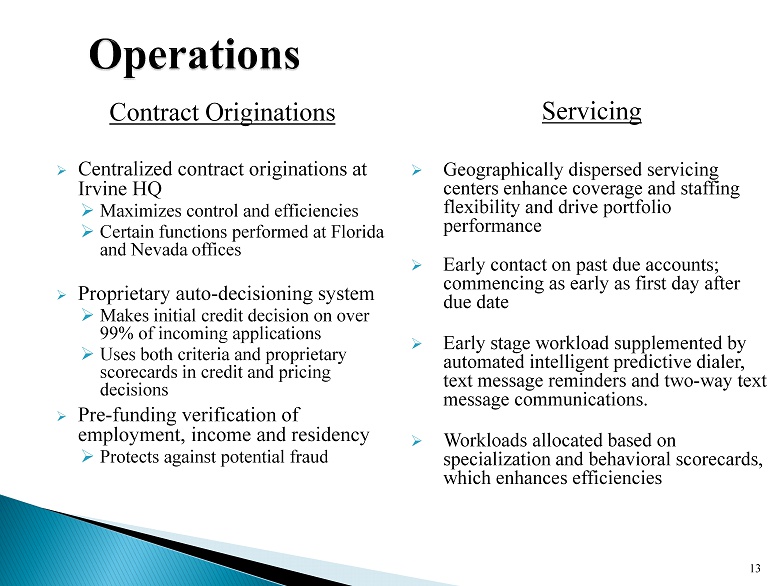

Contract Originations » Centralized contract originations at Irvine HQ » Maximizes control and efficiencies » Certain functions performed at Florida and Nevada offices » Proprietary auto - decisioning system » Makes initial credit decision on over 99% of incoming applications » Uses both criteria and proprietary scorecards in credit and pricing decisions » Pre - funding verification of employment, income and residency » Protects against potential fraud 13 Servicing » Geographically dispersed servicing centers enhance coverage and staffing flexibility and drive portfolio performance » Early contact on past due accounts; commencing as early as first day after due date » Early stage workload supplemented by automated intelligent predictive dialer, text message reminders and two - way text message communications. » Workloads allocated based on specialization and behavioral scorecards, which enhances efficiencies

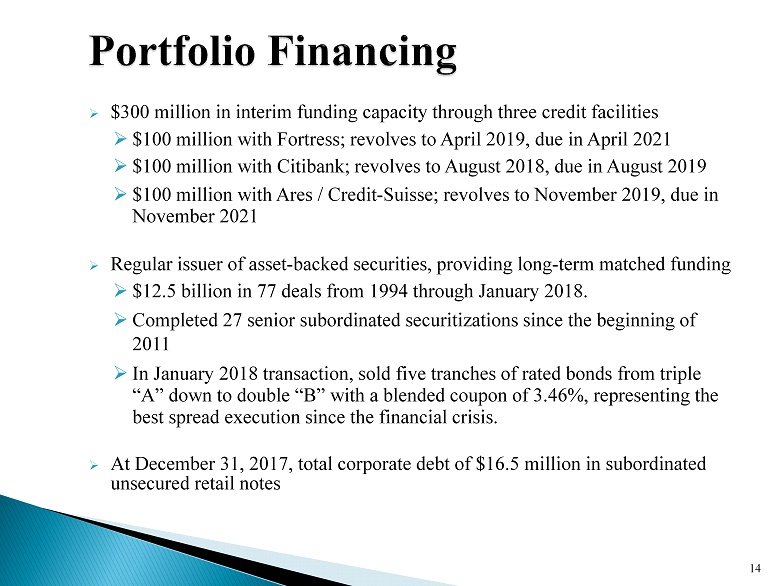

» $300 million in interim funding capacity through three credit facilities » $100 million with Fortress; revolves to April 2019, due in April 2021 » $100 million with Citibank; revolves to August 2018, due in August 2019 » $100 million with Ares / Credit - Suisse; revolves to November 2019, due in November 2021 » Regular issuer of asset - backed securities, providing long - term matched funding » $12.5 billion in 77 deals from 1994 through January 2018. » Completed 27 senior subordinated securitizations since the beginning of 2011 » In January 2018 transaction, sold five tranches of rated bonds from triple “A” down to double “B” with a blended coupon of 3.46%, representing the best spread execution since the financial crisis. » At December 31, 2017, total corporate debt of $16.5 million in subordinated unsecured retail notes 14

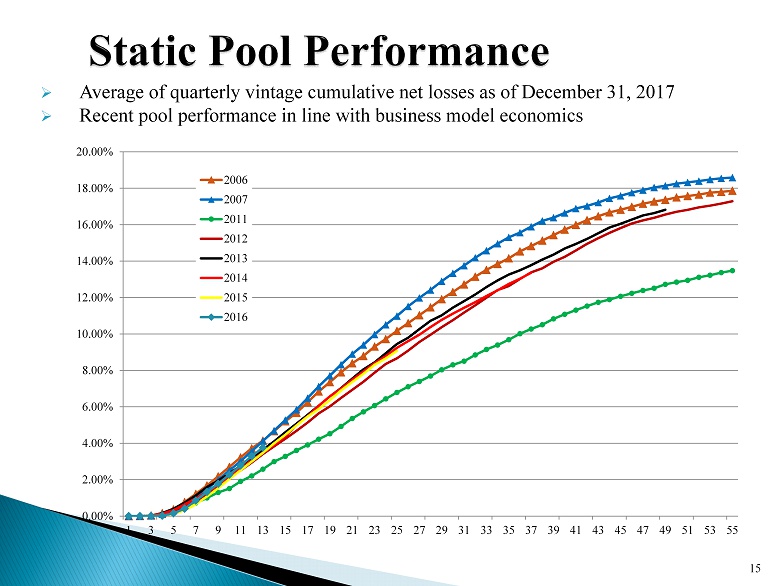

15 » Average of quarterly vintage cumulative net losses as of December 31, 2017 » Recent pool performance in line with business model economics 0.00% 2.00% 4.00% 6.00% 8.00% 10.00% 12.00% 14.00% 16.00% 18.00% 20.00% 1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47 49 51 53 55 2006 2007 2011 2012 2013 2014 2015 2016

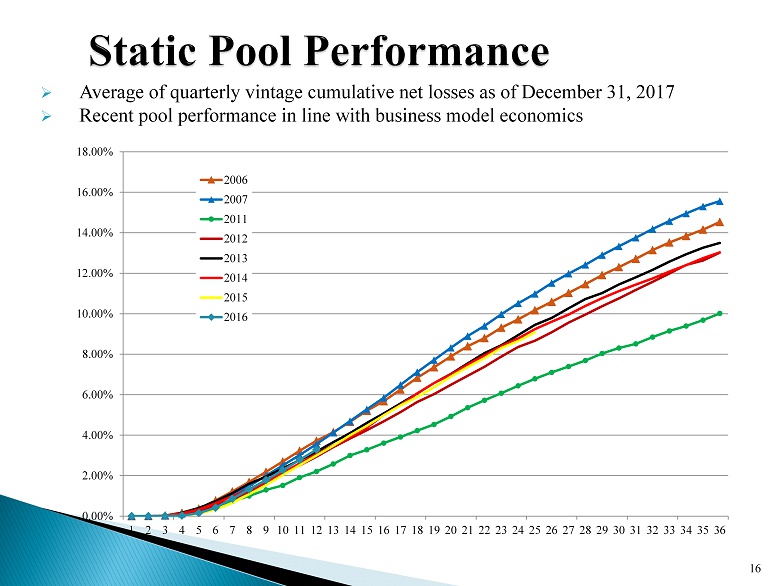

16 » Average of quarterly vintage cumulative net losses as of December 31, 2017 » Recent pool performance in line with business model economics 0.00% 2.00% 4.00% 6.00% 8.00% 10.00% 12.00% 14.00% 16.00% 18.00% 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 2006 2007 2011 2012 2013 2014 2015 2016

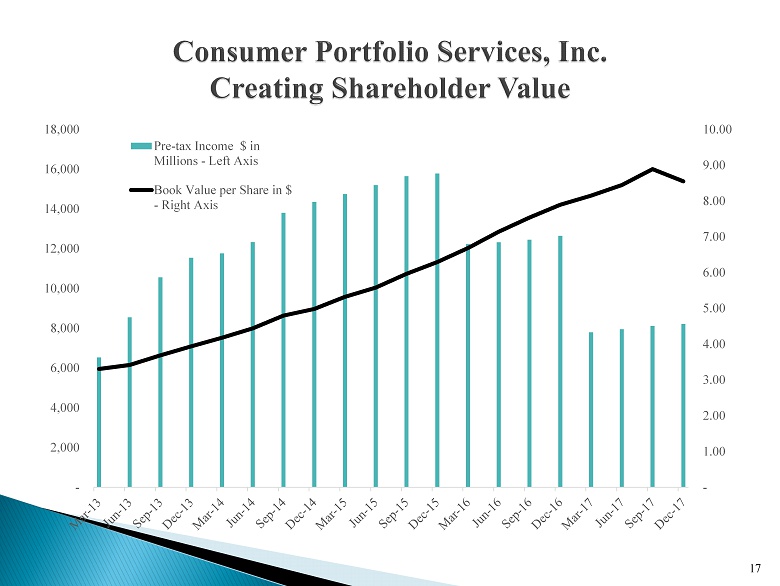

- 2,000 4,000 6,000 8,000 10,000 12,000 14,000 16,000 18,000 - 1.00 2.00 3.00 4.00 5.00 6.00 7.00 8.00 9.00 10.00 Pre-tax Income $ in Millions - Left Axis Book Value per Share in $ - Right Axis 17

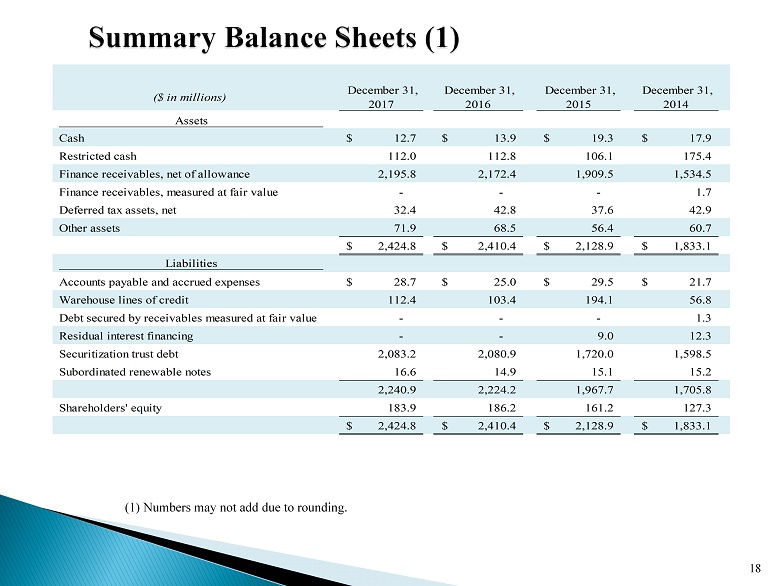

($ in millions) December 31, 2017 December 31, 2016 December 31, 2015 December 31, 2014 Assets Cash 12.7$ 13.9$ 19.3$ 17.9$ Restricted cash 112.0 112.8 106.1 175.4 Finance receivables, net of allowance 2,195.8 2,172.4 1,909.5 1,534.5 Finance receivables, measured at fair value - - - 1.7 Deferred tax assets, net 32.4 42.8 37.6 42.9 Other assets 71.9 68.5 56.4 60.7 2,424.8$ 2,410.4$ 2,128.9$ 1,833.1$ Liabilities Accounts payable and accrued expenses 28.7$ 25.0$ 29.5$ 21.7$ Warehouse lines of credit 112.4 103.4 194.1 56.8 Debt secured by receivables measured at fair value - - - 1.3 Residual interest financing - - 9.0 12.3 Securitization trust debt 2,083.2 2,080.9 1,720.0 1,598.5 Subordinated renewable notes 16.6 14.9 15.1 15.2 2,240.9 2,224.2 1,967.7 1,705.8 Shareholders' equity 183.9 186.2 161.2 127.3 2,424.8$ 2,410.4$ 2,128.9$ 1,833.1$ 18 (1) Numbers may not add due to rounding.

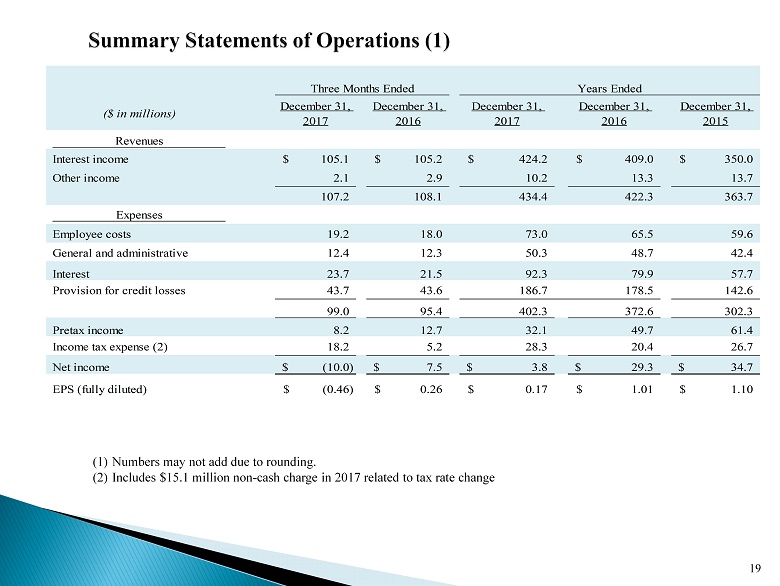

19 ($ in millions) December 31, 2017 December 31, 2016 December 31, 2017 December 31, 2016 December 31, 2015 Revenues Interest income 105.1$ 105.2$ 424.2$ 409.0$ 350.0$ Other income 2.1 2.9 10.2 13.3 13.7 107.2 108.1 434.4 422.3 363.7 Expenses Employee costs 19.2 18.0 73.0 65.5 59.6 General and administrative 12.4 12.3 50.3 48.7 42.4 Interest 23.7 21.5 92.3 79.9 57.7 Provision for credit losses 43.7 43.6 186.7 178.5 142.6 99.0 95.4 402.3 372.6 302.3 Pretax income 8.2 12.7 32.1 49.7 61.4 Income tax expense (2) 18.2 5.2 28.3 20.4 26.7 Net income (10.0)$ 7.5$ 3.8$ 29.3$ 34.7$ EPS (fully diluted) (0.46)$ 0.26$ 0.17$ 1.01$ 1.10$ Years EndedThree Months Ended (1) Numbers may not add due to rounding. (2) Includes $15.1 million non - cash charge in 2017 related to tax rate change

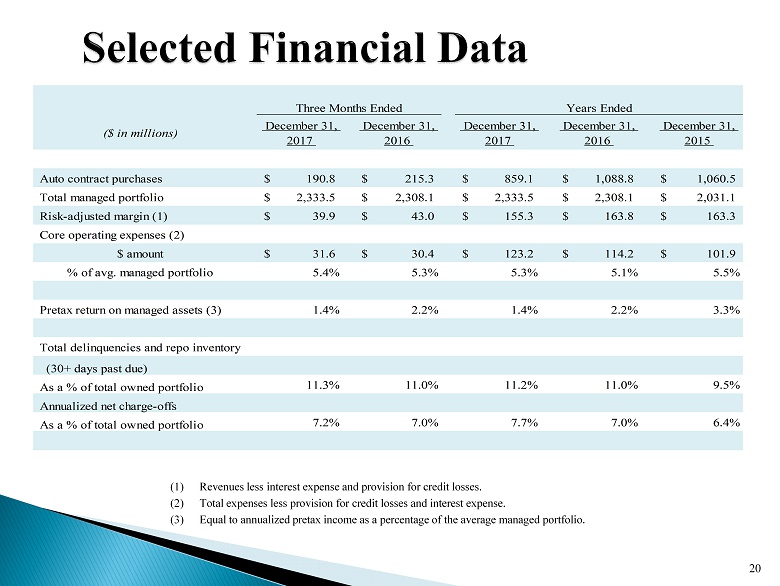

20 (1) Revenues less interest expense and provision for credit losses. (2) Total expenses less provision for credit losses and interest expense. (3) Equal to annualized pretax income as a percentage of the average managed portfolio. ($ in millions) December 31, 2017 December 31, 2016 December 31, 2017 December 31, 2016 December 31, 2015 Auto contract purchases 190.8$ 215.3$ 859.1$ 1,088.8$ 1,060.5$ Total managed portfolio 2,333.5$ 2,308.1$ 2,333.5$ 2,308.1$ 2,031.1$ Risk-adjusted margin (1) 39.9$ 43.0$ 155.3$ 163.8$ 163.3$ Core operating expenses (2) $ amount 31.6$ 30.4$ 123.2$ 114.2$ 101.9$ % of avg. managed portfolio 5.4% 5.3% 5.3% 5.1% 5.5% Pretax return on managed assets (3) 1.4% 2.2% 1.4% 2.2% 3.3% Total delinquencies and repo inventory (30+ days past due) As a % of total owned portfolio 11.3% 11.0% 11.2% 11.0% 9.5% Annualized net charge-offs As a % of total owned portfolio 7.2% 7.0% 7.7% 7.0% 6.4% Three Months Ended Years Ended

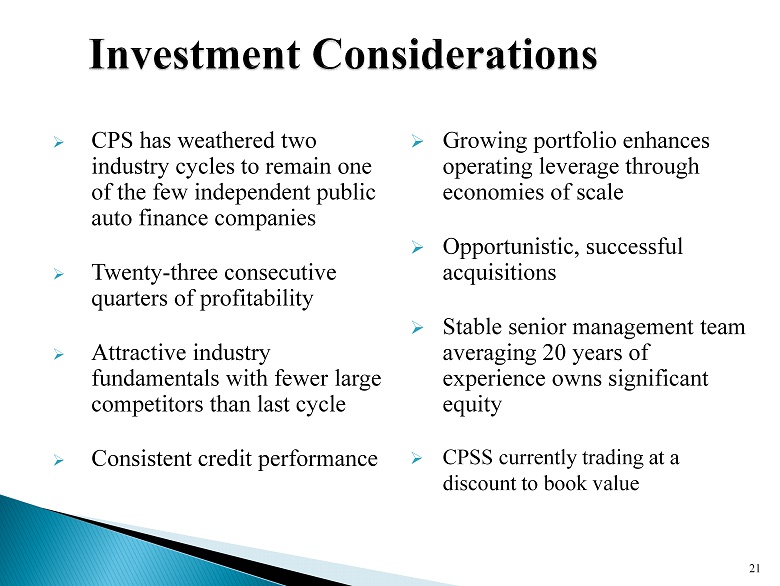

» CPS has weathered two industry cycles to remain one of the few independent public auto finance companies » Twenty - three consecutive quarters of profitability » Attractive industry fundamentals with fewer large competitors than last cycle » Consistent credit performance 21 » Growing portfolio enhances operating leverage through economies of scale » Opportunistic, successful acquisitions » Stable senior management team averaging 20 years of experience owns significant equity » CPSS currently trading at a discount to book value

Any person considering an investment in securities issued by CPS is urged to review the materials filed by CPS with the U . S . Securities and Exchange Commission ("Commission") . Such materials may be found by inquiring of the Commission‘s EDGAR search page (http : //www . sec . gov/edgar/searchedgar/companysearch . html) using CPS's ticker symbol, which is "CPSS . " Risk factors that should be considered are described in Item 1 A, “Risk Factors," of CPS's annual report on Form 10 - K, which report is on file with the Commission and available for review at the Commission's website . Such description of risk factors is incorporated herein by reference . 22

Information included in the preceding slides is believed to be accurate, but is not necessarily complete . Such information should be reviewed in its appropriate context . The implication that historical trends will continue in the future, or that past performance is indicative of future results, is disclaimed . To the extent that one reading the preceding material nevertheless makes such an inference, such inference would be a forward - looking statement, and would be subject to risks and uncertainties that could cause actual results to vary . Such risks include variable economic conditions, adverse portfolio performance (resulting, for example, from increased defaults by the underlying obligors), volatile wholesale values of collateral underlying CPS assets, reliance on warehouse financing and on the capital markets, fluctuating interest rates, increased competition, regulatory changes, the risk of obligor default inherent in sub - prime financing, and exposure to litigation . 23