PrivateBancorp, Inc.

70 W. Madison

Chicago, Illinois 60602

For further information:

Dennis Klaeser

Chief Financial Officer

312-683-7100

dklaeser@pvtb.com

News Release

For Immediate Release

PrivateBancorp Reports First Quarter 2008 Results

Continued Implementation of the Strategic Growth Plan Results in Strong Revenue Growth

| · | Revenue grew 18% over 4th quarter 2007. |

| · | Client deposits grew 12% during first quarter. |

| · | Loans grew 23% during first quarter. |

| · | Total assets topped $6.0 billion. |

| · | Headquarters to move to prominent LaSalle Street address. |

Chicago, IL, April 28, 2008 -- PrivateBancorp, Inc. (NASDAQ: PVTB) today reported a net loss for the first quarter 2008 of $8.9 million, or $0.34 per diluted share, compared to net income of $9.0 million, or $0.41 per diluted share, for the first quarter 2007. The net loss was primarily attributed to expected increases in expenses associated with implementation of our previously announced Strategic Growth Plan. During the quarter, the Company experienced substantial increases in revenue, client deposits and loans, and added a significant number of new clients.

“The Strategic Growth Plan conceived last year has made PrivateBancorp a larger, more diversified company and puts us on course to become the premier middle-market commercial, commercial real estate, private banking and wealth management bank in all of our chosen markets. During the quarter, we added 46 talented, experienced bankers across our network of offices, bringing the total number of managing directors added since we first announced the Plan to 95, “ said Ralph B. Mandell, Chairman of the Board. “I am proud of the team we have assembled and its exceptional capabilities to serve the business needs of our clients.”

“As anticipated, first quarter earnings were negatively affected by costs associated with our Strategic Growth Plan and higher loan loss provision expenses. However, the growth in the first full quarter of the execution of the Plan exceeded our own expectations. The substantial increase in our client base, as evidenced by exceptionally strong loan and deposit growth and our strong pipeline of business, is a testament to our strong business development culture,” said Larry D. Richman, President and CEO.

“We now have in place the essential elements that I believe can substantially enhance the franchise value of PrivateBancorp. The positive reception among our new clients and prospects to PrivateBancorp’s relationship-based client-service model, supported by our enhanced suite of products and services, translated into strong revenue and balance sheet growth during the first quarter, which is especially rewarding given the current economic environment. We continue to execute on our Strategic Growth Plan, building our network of clients and adding new deposit, treasury, cash management and capital markets products and services and substantially enhancing our infrastructure, including risk management capabilities,” added Richman. “Looking forward, we will seek to expand the breadth of our relationships with our existing clients, while expanding our base of new clients in all the markets we serve. To accommodate the growth of our Company, we will move our executive officers, as well as a portion of The PrivateBank – Chicago’s commercial and private bankers, to a new headquarters located at 120 S. LaSalle Street in the heart of Chicago’s financial district - while continuing to maintain offices in our current location at 70 West Madison.”

Execution of the Strategic Growth Plan

As previously disclosed, the Company sought to accomplish several strategic goals in the execution of its Strategic Growth Plan – regain and exceed the Company’s historical growth rate, diversify its business and acquire many new, middle-market clients. To achieve these goals, the Company made a substantial investment in people and infrastructure, laying the foundation for future growth. Although the Company continued to invest in people and infrastructure during the first quarter, going forward we anticipate operating expense growth will moderate. With much of that investment now made, management is focused on key performance indicators – revenue, deposit and loan growth, operating efficiency and profitability, as well as client acquisition success – in order to enhance stockholder value.

In keeping with its Strategic Growth Plan during the first quarter 2008, the Company hired a net total of 34 new Managing Directors, bringing the total number of Managing Directors to 258 at March 31, 2008, compared to 224 at December 31, 2007, a 15% increase. These hires were made across the Company’s offices, including the staffing of four new offices in Cleveland, Ohio, Des Moines, Iowa, Denver, Colorado and Minneapolis, Minnesota. Full-time equivalent (FTE) employees increased 10% to 657 from 597 at December 31, 2007. In total, pursuant to the Strategic Growth Plan, the Company has now completed the hiring of 98 commercial bankers and 52 additional personnel who support the Company’s infrastructure and delivery of its products and services.

During the first quarter 2008, sign-on bonus payments to newly hired employees were $3.7 million compared to $13.7 million in the fourth quarter 2007. The Transformation and Retention Equity Awards outstanding, which were granted by the Company from the time the Strategic Growth Plan was announced and through March 31, 2008, had a value of approximately $62 million at March 31, 2008 compared to approximately $50 million at December 31, 2007. The cost of these Awards will be expensed over the five-year period ending December 31, 2012. Compensation costs associated with these awards totaled $2.2 million for the first quarter 2008 compared to $2.0 million for the fourth quarter 2007.

Balance Sheet Growth

The Company’s investment in people and infrastructure has fueled strong balance sheet growth, which drove the Company’s 18% revenue growth in the first quarter. Given the acceleration in loan growth since inception of the Plan, the Company is focused on balancing growth in its loan portfolio with an emphasis on appropriate sources of funding, including gathering client deposits and other alternative funding sources.

Total assets increased 21% to $6.0 billion at March 31, 2008 from $5.0 billion at December 31, 2007. Total loans increased 23% to $5.1 billion at March 31, 2008 from $4.2 billion at December 31, 2007. The loan category that grew most substantially during the quarter was commercial loans (including both commercial and industrial and owner-occupied commercial real estate loans), which increased to $1.8 billion or 36% of our total loans from $1.3 billion or 32% of total loans at year-end 2007. During the quarter, commercial real estate loans grew to $2.0 billion or 39% of our total loans from $1.6 billion or 38% of total loans at year-end 2007.

Total deposits increased 33% to $5.0 billion at March 31, 2008 from $3.8 billion at December 31, 2007. Approximately one-third of the increase in total deposits, or $398.9 million, came from an increase in client deposits, defined as total deposits less brokered deposits. The other two-thirds of the increase in total deposits came from a combination of increased CDARs™ deposits of $215.5 million and traditional brokered deposits of $639.0 million.

During the quarter, the Company facilitated its deposit growth by aggressively pursuing deposits from existing and new clients, increasing institutional and municipal deposits, expanding its business DDA account balances due to its enhanced treasury management services, and implementation of a CDARs™ deposit program. The CDARs™ deposit program is a deposit services arrangement that effectively achieves FDIC deposit insurance for jumbo deposit relationships, which is an attractive feature to many of our middle-market and private banking clients. These deposits are classified as brokered deposits for regulatory deposit purposes; however, the source of the deposits is our existing and new client relationships and are, therefore, not traditional “brokered” deposits.

As the Company attracts new clients, loan volume tends to lead client deposit volume associated with these new relationships. Longer term as client deposits grow, the Company expects to reduce its reliance on brokered deposits as a percentage of total deposits. The Company has enhanced its suite of deposit products and treasury management services in order to attract more client deposits going forward and is exploring a variety of other funding opportunities.

Funds borrowed, which include federal funds purchased, FHLB advances, borrowings under the Company’s credit facility, and convertible senior notes, decreased to $359.1 million at March 31, 2008 from $560.8 million at December 31, 2007, primarily as a result of the aforementioned increase in client deposits, CDARs™ deposits and traditional brokered deposits.

Credit Quality

During the first quarter 2008, the provision for loan losses increased to $17.1 million, compared to $1.4 million in the first quarter 2007 and $10.2 million in the fourth quarter 2007 due to the substantial loan growth incurred and an increase in non-performing assets, coupled with current market conditions and loans charged off during the quarter.

Non-performing assets to total assets were 1.10% at March 31, 2008, compared to 0.97% at December 31, 2007. Of $65.9 million in total non-performing assets at March 31, 2008, 33% are located in the Georgia market, 27% are located in the Chicago market, 24% are located in the St. Louis market, and 16% are in Michigan. Of total non-performing assets, 59% are construction, 23% are commercial real estate, 8% are commercial, and the remaining 10% are classified as residential real estate and personal. Of the $65.9 million in non-performing assets at March 31, 2008, $42.7 million or 65% relate to residential development loans.

Net charge-offs totaled $4.1 million in the first quarter 2008, or an annualized rate of 0.35% of average total loans, versus net charge-offs of $582,000, or an annualized rate of 0.07% of average total loans, in the prior year first quarter, and net charge-offs of $3.4 million, or an annualized rate of 0.35% of average total loans, in the fourth quarter 2007. The allowance for loan losses as a percentage of total loans was increased to 1.21% at March 31, 2008, compared to 1.17% at December 31, 2007.

Net interest income

The Company experienced net interest margin compression as a result of interest rate cuts by the Federal Reserve during the quarter and because of the increase in non-performing assets. Net interest income totaled $36.3 million in the first quarter 2008, compared to $32.0 million for the first quarter 2007, and $31.7 million for the fourth quarter 2007. Net interest margin (on a tax equivalent basis) decreased to 2.88% for the first quarter 2008, compared to 3.26% in the first quarter 2007, and 2.96% for the fourth quarter 2007. Yields on earning assets decreased by 107 basis points over the prior year quarter while the cost of funds decreased by 65 basis points. During the first quarter, the Company reversed approximately $1.1 million in accrued interest income due to loans that became non-performing, compared to $634,000 in the fourth quarter 2007. The interest reversal during the first quarter accounted for eight basis points of margin compression, which compares to six basis points of margin compression that occurred in the fourth quarter of 2007 as a result of interest reversals.

Non-interest income

Consistent with the Strategic Growth Plan, the Company continues to pursue opportunities to diversify its revenue stream. The PrivateWealth Group fee revenue was $4.4 million during the first quarter 2008, an increase of 15% from $3.8 million in the first quarter 2007, and up 3% from $4.3 million in the fourth quarter 2007. The PrivateWealth Group’s assets under management increased 12% to $3.3 billion at March 31, 2008, from $3.0 billion at March 31, 2007, and were unchanged from December 31, 2007. Fees paid to third-party investment managers were $968,000 in the first quarter 2008, compared to $782,000 in the prior year quarter, and $925,000 in the fourth quarter 2007. Mortgage banking income increased 85% over the prior quarter and 16% over the prior year quarter due to market demand. Other income, which includes banking fee income, income on our bank owned life insurance and other loan fees, increased 64% over the prior quarter and 56% over the prior year quarter. Other income grew primarily as a result of substantial growth in fee income from a variety of services provided to new middle-market banking clients. The Company also recognized $814,000 in securities gains during the first quarter 2008 compared to none in the prior quarter and $79,000 in the prior year quarter due to realized gains made in repositioning the investment portfolio.

One of the goals of the Company’s Strategic Growth Plan is to diversify the Company’s non-interest income by generating new sources of fee income through the offering of new products and services to clients. To that end, the Company has enhanced or introduced a variety of new products and services including lockbox, control disbursement, virtual vault, interest-rate swaps, and foreign exchange services. The Company has begun to see success in accomplishing this goal, as other income was $1.75 million during the first quarter of 2008, an increase of 56% from $1.13 million in the first quarter 2007, and up 64% from $1.06 million in the fourth quarter of 2007.

Non-interest expense

Non-interest expense was $42.9 million in the first quarter 2008, up from $23.4 million in the first quarter 2007 and down from $51.8 million at the fourth quarter 2007. The increase from the prior year quarter was primarily due to increased compensation and marketing expenses related to the investment in the Strategic Growth Plan. As expected, compensation expenses increased to $27.7 million in the first quarter of 2008 compared to $13.7 million during the first quarter of 2007. Included in other operating expenses for the quarter were $2.1 million in operating expenses and disposition costs related to OREO properties.

Capital Resources

As of March 31, 2008, the Company remained well-capitalized for regulatory purposes with a total risk-based capital ratio of 11.5% and Tier 1 risk-based capital ratio of 9.0%, substantially exceeding the well-capitalized thresholds of 10% and 6%, respectively. The Company is committed to maintaining a strong capital position and plans to raise additional regulatory capital in the near future due to anticipated, substantial organic growth in the balance sheet.

About PrivateBancorp, Inc.

PrivateBancorp, Inc., through its PrivateBank subsidiaries, provides distinctive, highly personalized financial services to a growing array of successful middle market privately held and public businesses, affluent individuals, wealthy families, professionals, entrepreneurs and real estate investors. The PrivateBank uses a banking model to develop lifetime relationships with its clients. Through a growing team of highly qualified managing directors, The PrivateBank delivers a sophisticated suite of tailored credit and non-credit solutions, including lending, treasury management, investment products, capital markets products and wealth management and trust services, to meet its clients’ commercial and personal needs. The Company, which had assets of $6.0 billion as of March 31, 2008, has 22 offices located in the Atlanta, Chicago, Cleveland, Denver, Des Moines, Detroit, Kansas City, Milwaukee, Minneapolis, and St. Louis metropolitan areas.

Additional information can be found in the Investor Relations section of PrivateBancorp, Inc.’s website at www.pvtb.com.

Forward-Looking Statements: Statements contained in this news release that are not historical facts may constitute forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended. The Company’s ability to predict results or the actual effect of future plans or strategies is inherently uncertain. Factors which could have a material adverse effect on the operations and future prospects of the Company include, but are not limited to, fluctuations in market rates of interest and loan and deposit pricing in the Company’s market areas, the effect of continued margin pressure on the Company’s earnings, further deterioration in asset quality, the inability to raise additional equity capital on terms acceptable to the Company, or at all, necessary to fund the Company’s continued growth, insufficient liquidity/funding sources or the inability to obtain on terms acceptable to the Company the funding necessary to fund its loan growth, legislative or regulatory changes, adverse developments in the Company’s loan or investment portfolios, slower than anticipated growth of the Company’s business or unanticipated business declines, competition, unforeseen difficulties in integrating new hires, failure to improve operating efficiencies through expense controls, and the possible dilutive effect of potential acquisitions, expansion or future capital raises. These risks and uncertainties should be considered in evaluating forward-looking statements and undue reliance should not be placed on such statements. The Company assumes no obligation to update publicly any of these statements in light of future events unless required under the federal securities laws.

Editor’s Note: Financial highlights attached.

8

Quarterly Consolidated Income Statements

Unaudited

(dollars in thousands)

| 1Q08 | 4Q07 | 3Q07 | 2Q07 | 1Q07 | ||||||||||||||||

| Summary Income Statement | ||||||||||||||||||||

| Interest Income | ||||||||||||||||||||

| Loans, including fees | $ | 76,113 | $ | 71,062 | $ | 72,299 | $ | 70,732 | $ | 68,886 | ||||||||||

| Federal funds sold and interest bearing deposits | 246 | 275 | 259 | 239 | 238 | |||||||||||||||

| Securities: | ||||||||||||||||||||

| Taxable | 4,286 | 3,951 | 3,450 | 3,594 | 3,589 | |||||||||||||||

| Exempt from Federal income taxes | 2,244 | 2,313 | 2,345 | 2,344 | 2,348 | |||||||||||||||

| Total Interest Income | 82,889 | 77,601 | 78,353 | 76,909 | 75,061 | |||||||||||||||

| Interest Expense | ||||||||||||||||||||

| Deposits: | ||||||||||||||||||||

| Interest-bearing demand | 422 | 451 | 475 | 437 | 596 | |||||||||||||||

| Savings and money market deposit accounts | 13,221 | 16,813 | 17,904 | 16,667 | 17,062 | |||||||||||||||

| Brokered deposits and other time deposits | 26,358 | 20,894 | 21,732 | 21,237 | 19,777 | |||||||||||||||

| Funds borrowed | 4,996 | 6,087 | 4,350 | 4,872 | 4084 | |||||||||||||||

| Junior Subordinated deferrable interest debentures held by trusts that issued guaranteed capital debt securities | 1,572 | 1,608 | 1,604 | 1,585 | 1567 | |||||||||||||||

| Total Interest Expense | 46,569 | 45,853 | 46,065 | 44,798 | 43,086 | |||||||||||||||

| Net Interest Income | 36,320 | 31,748 | 32,288 | 32,111 | 31,975 | |||||||||||||||

| Provision for loan losses | 17,133 | 10,171 | 2,399 | 2,958 | 1,406 | |||||||||||||||

| Net Interest Income after Provision for Loan Losses | 19,187 | 21,577 | 29,889 | 29,153 | 30,569 | |||||||||||||||

| Non-interest Income | ||||||||||||||||||||

| The PrivateWealth Group fee revenue | 4,419 | 4,310 | 4,029 | 4,024 | 3,826 | |||||||||||||||

| Mortgage banking income | 1,530 | 828 | 1,157 | 1,229 | 1,314 | |||||||||||||||

| Other income | 1,753 | 1,066 | 1,214 | 1,803 | 1,126 | |||||||||||||||

| Net securities gains (losses) | 814 | - | 366 | (97 | ) | 79 | ||||||||||||||

| Total Non-interest Income | 8,516 | 6,204 | 6,766 | 6,959 | 6,345 | |||||||||||||||

| Non-interest Expense | ||||||||||||||||||||

| Salaries and benefits | 27,749 | 31,673 | 13,083 | 12,734 | 13,729 | |||||||||||||||

| Occupancy expense | 3,845 | 3,918 | 3,336 | 3,160 | 2,790 | |||||||||||||||

| Professional fees | 2,311 | 6,442 | 2,109 | 1,610 | 1,715 | |||||||||||||||

| Wealth management fees | 968 | 925 | 857 | 868 | 782 | |||||||||||||||

| Marketing | 2,828 | 2,422 | 1,058 | 1,330 | 1,289 | |||||||||||||||

| Data processing | 1,220 | 1,282 | 1,039 | 984 | 901 | |||||||||||||||

| Amortization of intangibles | 234 | 240 | 241 | 242 | 243 | |||||||||||||||

| Insurance | 870 | 772 | 452 | 363 | 352 | |||||||||||||||

| Other non-interest expenses | 2,907 | 4,136 | 1,749 | 2,019 | 1,564 | |||||||||||||||

| Total Non-interest Expense | 42,932 | 51,810 | 23,924 | 23,310 | 23,365 | |||||||||||||||

| Minority interest expense | 68 | 78 | 100 | 95 | 90 | |||||||||||||||

| Income Before Income Taxes | (15,297 | ) | (24,107 | ) | 12,631 | 12,707 | 13,459 | |||||||||||||

| Income tax (benefit) provision | (6,364 | ) | (8,962 | ) | 3,466 | 3,956 | 4,423 | |||||||||||||

| Net (loss) income | $ | (8,933 | ) | $ | (15,145 | ) | $ | 9,165 | $ | 8,751 | $ | 9,036 | ||||||||

| Preferred Stock Dividends | 107 | 107 | - | - | - | |||||||||||||||

| Net (loss) income available to Common Shareholders | $ | (9,040 | ) | $ | (15,252 | ) | $ | 9,165 | $ | 8,751 | $ | 9,036 | ||||||||

| Weighted Average Common Shares Outstanding | 26,885,565 | 22,537,167 | 21,223,341 | 21,185,400 | 21,331,021 | |||||||||||||||

| Diluted Average Common Shares Outstanding | 26,885,565 | 22,537,167 | 21,819,333 | 21,810,173 | 22,018,295 | |||||||||||||||

| Per Common Share Information | ||||||||||||||||||||

| Basic | $ | (0.34 | ) | $ | (0.68 | ) | $ | 0.43 | $ | 0.41 | $ | 0.42 | ||||||||

| Diluted | $ | (0.34 | ) | $ | (0.68 | ) | $ | 0.42 | $ | 0.40 | $ | 0.41 | ||||||||

| Dividends | $ | 0.075 | $ | 0.075 | $ | 0.075 | $ | 0.075 | $ | 0.075 |

Note 1: Certain reclassifications have been made to prior period financial statements to place them on a basis comparable with the current period financial statements.

Note 2: Diluted shares are equal to Basic shares for the first quarter 2008 and the fourth quarter 2007 due to the net loss. The calculation of diluted earnings per share results in anti-dilution.

9

Consolidated Balance Sheets

(dollars in thousands)

| 03/31/08 | 12/31/07 | 09/30/07 | 06/30/07 | 03/31/07 | ||||||||||||||||

| unaudited | audited | unaudited | unaudited | unaudited | ||||||||||||||||

| Assets | ||||||||||||||||||||

| Cash and due from banks | $ | 54,576 | $ | 51,331 | $ | 52,922 | $ | 63,074 | $ | 73,736 | ||||||||||

| Fed funds sold and other short-term investments | 22,226 | 13,220 | 22,117 | 19,672 | 17,535 | |||||||||||||||

| Total cash and cash equivalents | 76,802 | 64,551 | 75,039 | 82,746 | 91,271 | |||||||||||||||

| Loans held for sale | 9,659 | 19,358 | 4,262 | 20,905 | 14,928 | |||||||||||||||

| Equity investments | 13,157 | 12,459 | 10,682 | 10,040 | 9,824 | |||||||||||||||

| Investment securities: available-for-sale | 575,798 | 526,271 | 487,266 | 485,814 | 472,200 | |||||||||||||||

| Loans net of unearned discount | 5,136,066 | 4,177,795 | 3,737,523 | 3,705,339 | 3,581,398 | |||||||||||||||

| Allowance for loan losses | (61,974 | ) | (48,891 | ) | (42,113 | ) | (41,280 | ) | (38,893 | ) | ||||||||||

| Net loans | 5,074,092 | 4,128,904 | 3,695,410 | 3,664,059 | 3,542,505 | |||||||||||||||

| Goodwill | 93,341 | 93,341 | 93,357 | 93,043 | 93,043 | |||||||||||||||

| Premises and equipment, net | 26,356 | 25,600 | 24,844 | 23,415 | 21,674 | |||||||||||||||

| Accrued interest receivable | 25,287 | 24,144 | 23,422 | 23,554 | 22,316 | |||||||||||||||

| Other assets | 119,152 | 95,577 | 83,944 | 82,434 | 76,111 | |||||||||||||||

| Total Assets | $ | 6,013,644 | $ | 4,990,205 | $ | 4,498,226 | $ | 4,486,010 | $ | 4,343,872 | ||||||||||

| Liabilities | ||||||||||||||||||||

| Demand deposits: | ||||||||||||||||||||

| Non-interest bearing | $ | 341,779 | $ | 299,043 | $ | 285,003 | $ | 303,455 | $ | 312,648 | ||||||||||

| Interest bearing | 159,003 | 157,761 | 134,428 | 150,324 | 144,812 | |||||||||||||||

| Savings and money market deposit accounts | 1,663,275 | 1,594,172 | 1,577,930 | 1,505,303 | 1,485,783 | |||||||||||||||

| Brokered deposits | 1,396,930 | 542,470 | 500,296 | 630,905 | 631,689 | |||||||||||||||

| Other time | 1,453,479 | 1,167,692 | 1,090,405 | 1,048,558 | 1,007,889 | |||||||||||||||

| Total deposits | 5,014,466 | 3,761,138 | 3,588,062 | 3,638,545 | 3,582,821 | |||||||||||||||

| Funds borrowed | 359,099 | 560,809 | 464,021 | 407,696 | 334,128 | |||||||||||||||

| Junior Subordinated deferrable interest Debentures held by trusts that issued guaranteed capital debt securities | 101,033 | 101,033 | 101,033 | 101,033 | 101,033 | |||||||||||||||

| Accrued interest payable | 17,670 | 16,134 | 13,968 | 14,334 | 15,259 | |||||||||||||||

| Other liabilities | 28,169 | 50,298 | 12,742 | 18,293 | 10,959 | |||||||||||||||

| Total Liabilities | $ | 5,520,437 | $ | 4,489,412 | $ | 4,179,826 | $ | 4,179,901 | $ | 4,044,200 | ||||||||||

| Stockholders' Equity | ||||||||||||||||||||

| Preferred stock | 41,000 | 41,000 | - | - | - | |||||||||||||||

| Common stock | 27,289 | 27,225 | 21,612 | 21,568 | 21,531 | |||||||||||||||

| Treasury stock | (13,925 | ) | (13,559 | ) | (13,475 | ) | (13,148 | ) | (13,068 | ) | ||||||||||

| Additional paid-in-capital | 314,961 | 311,989 | 160,178 | 157,960 | 155,729 | |||||||||||||||

| Retained earnings | 115,016 | 126,204 | 143,585 | 136,057 | 128,904 | |||||||||||||||

| Accumulated other comprehensive income | 8,866 | 7,934 | 6,500 | 3,672 | 6,576 | |||||||||||||||

| Total Stockholders' Equity | $ | 493,207 | $ | 500,793 | $ | 318,400 | $ | 306,109 | $ | 299,672 | ||||||||||

| Total Liabilities and Stockholders' Equity | $ | 6,013,644 | $ | 4,990,205 | $ | 4,498,226 | $ | 4,486,010 | $ | 4,343,872 | ||||||||||

Note 1: Certain reclassifications have been made to prior period financial statements to place them on a basis comparable with the current period financial statements.

10

Key Financial Data

Unaudited

(dollars in thousands except per share data)

| 1Q08 | 4Q07 | 3Q07 | 2Q07 | 1Q07 | ||||||||||||||||

| Selected Statement of Income Data: | ||||||||||||||||||||

| Net interest income | $ | 36,320 | $ | 31,748 | $ | 32,288 | $ | 32,111 | $ | 31,975 | ||||||||||

| Net revenue (1) | $ | 45,862 | $ | 39,009 | $ | 40,126 | $ | 40,142 | $ | 39,393 | ||||||||||

| Income before taxes | $ | (15,297 | ) | $ | (24,107 | ) | $ | 12,631 | $ | 12,707 | $ | 13,459 | ||||||||

| Net (loss) income | $ | (8,933 | ) | $ | (15,145 | ) | $ | 9,165 | $ | 8,751 | $ | 9,036 | ||||||||

| Per Common Share Data: | ||||||||||||||||||||

| Basic earnings per share | $ | (0.34 | ) | $ | (0.68 | ) | $ | 0.43 | $ | 0.41 | $ | 0.42 | ||||||||

| Diluted earnings per share (2) | $ | (0.34 | ) | $ | (0.68 | ) | $ | 0.42 | $ | 0.40 | $ | 0.41 | ||||||||

| Dividends | $ | 0.075 | $ | 0.075 | $ | 0.075 | $ | 0.075 | $ | 0.075 | ||||||||||

| Book value (period end) | $ | 15.97 | $ | 16.89 | $ | 14.73 | $ | 14.19 | $ | 13.92 | ||||||||||

| Tangible book value (period end) (3) | $ | 12.46 | $ | 13.22 | $ | 10.10 | $ | 9.56 | $ | 9.26 | ||||||||||

| Market value (close) | $ | 31.47 | $ | 32.65 | $ | 34.84 | $ | 28.80 | $ | 36.56 | ||||||||||

| Diluted earnings multiple (4) | (23.08 | )x | (12.10 | )x | 20.91 | x | 17.95 | x | 21.99 | x | ||||||||||

| Book value multiple | 1.97 | x | 1.93 | x | 2.36 | x | 2.03 | x | 2.63 | x | ||||||||||

| Share Data: | ||||||||||||||||||||

| Weighted Average Common Shares Outstanding | 26,885,565 | 22,537,167 | 21,223,341 | 21,185,400 | 21,331,021 | |||||||||||||||

| Diluted Average Common Shares Outstanding | 26,885,565 | 22,537,167 | 21,819,333 | 21,810,173 | 22,018,295 | |||||||||||||||

| Common shares issued and outstanding at period end | 28,685,847 | 28,439,447 | 22,182,571 | 22,132,645 | 22,072,896 | |||||||||||||||

| Common shares outstanding at period end | 28,310,760 | 28,075,229 | 21,821,055 | 21,780,773 | 21,723,343 | |||||||||||||||

| Common Stock | 27,289,297 | 27,224,747 | 21,611,721 | 21,567,545 | 21,531,296 | |||||||||||||||

| Preferred Stock | 41,000,005 | 41,000,005 | - | - | - | |||||||||||||||

| Performance Ratios: | ||||||||||||||||||||

| Return on average total assets | -0.66 | % | -1.30 | % | 0.82 | % | 0.80 | % | 0.86 | % | ||||||||||

| Return on average total equity | -7.81 | % | -16.61 | % | 11.80 | % | 11.66 | % | 12.37 | % | ||||||||||

| Dividend payout ratio | -24.23 | % | -14.30 | % | 17.84 | % | 18.64 | % | 18.50 | % | ||||||||||

| Fee revenue as a percent of total revenue (5) | 17.49 | % | 16.35 | % | 16.54 | % | 18.01 | % | 16.39 | % | ||||||||||

| Non-interest income to average assets | 0.63 | % | 0.53 | % | 0.60 | % | 0.64 | % | 0.60 | % | ||||||||||

| Non-interest expense to average assets | 3.18 | % | 4.45 | % | 2.13 | % | 2.13 | % | 2.22 | % | ||||||||||

| Net overhead ratio (6) | 2.55 | % | 3.92 | % | 1.53 | % | 1.49 | % | 1.62 | % | ||||||||||

| Efficiency ratio (7) | 93.61 | % | 132.81 | % | 59.62 | % | 58.07 | % | 59.31 | % | ||||||||||

| Selected Financial Condition Data: | ||||||||||||||||||||

| Core deposits | $ | 3,617,536 | $ | 3,218,668 | $ | 3,087,766 | $ | 3,007,640 | $ | 2,951,132 | ||||||||||

| Wealth management assets under management | $ | 3,314,461 | $ | 3,361,171 | $ | 3,281,576 | $ | 3,119,878 | $ | 2,952,227 | ||||||||||

| Balance Sheet Ratios: | ||||||||||||||||||||

| Loans to Deposits (period end) | 102.42 | % | 111.08 | % | 104.17 | % | 101.84 | % | 99.96 | % | ||||||||||

| Average interest-earning assets to average interest-bearing liabilities | 112.86 | % | 111.32 | % | 110.40 | % | 109.94 | % | 109.75 | % | ||||||||||

Capital Ratios (period end) (8): | ||||||||||||||||||||

| Total equity to total assets | 8.20 | % | 10.04 | % | 7.08 | % | 6.82 | % | 6.90 | % | ||||||||||

| Total risk-based capital ratio | 11.54 | % | 14.20 | % | 10.60 | % | 10.63 | % | 10.45 | % | ||||||||||

| Tier-1 risk-based capital ratio | 9.00 | % | 11.39 | % | 8.07 | % | 8.06 | % | 7.93 | % | ||||||||||

| Leverage ratio | 9.13 | % | 10.93 | % | 7.20 | % | 7.08 | % | 6.95 | % | ||||||||||

| Tangible capital ratio | 6.66 | % | 8.20 | % | 4.96 | % | 4.70 | % | 4.70 | % | ||||||||||

(1) The sum of net interest income, on a tax equivalent basis, plus non-interest income.

(2) Diluted shares are equal to Basic shares for the fourth quarter 2007 due to the net loss. The calculation of diluted earnings per share results in anti-dilution.

(3) Tangible book value is total capital less goodwill and other intangibles divided by outstanding shares at end of period.

(4) Period end closing stock price divided by annualized quarterly earnings for the quarter then ended.

(5) Represents wealth management, mortgage banking and other income as a percentage of the sum of net interest income and wealth management, mortgage banking and other income.

(6) Non-interest expense less non-interest income divided by average total assets.

(7) Non-interest expense divided by the sum of net interest income, on a tax equivalent basis, plus non-interest income.

(8) Capital ratios for the most recent period presented in the press release are based on preliminary data.

11

PrivateBancorp, Inc.

Credit Quality Statistics

Unaudited

(dollars in thousands)

| 1Q08 | 4Q07 | 3Q07 | 2Q07 | 1Q07 | ||||||||||||||||

| Credit Quality Key Ratios: | ||||||||||||||||||||

| Net charge-offs to average loans | 0.35 | % | 0.35 | % | 0.17 | % | 0.06 | % | 0.07 | % | ||||||||||

| Total non-performing loans to total loans | 0.91 | % | 0.93 | % | 0.77 | % | 0.72 | % | 0.28 | % | ||||||||||

| Total non-performing assets to total assets | 1.10 | % | 0.97 | % | 0.80 | % | 0.70 | % | 0.34 | % | ||||||||||

| Nonaccrual loans to: | ||||||||||||||||||||

| total loans | 0.91 | % | 0.93 | % | 0.69 | % | 0.56 | % | 0.13 | % | ||||||||||

| total assets | 0.77 | % | 0.78 | % | 0.57 | % | 0.46 | % | 0.11 | % | ||||||||||

| Allowance for loan losses to: | ||||||||||||||||||||

| total loans | 1.21 | % | 1.17 | % | 1.13 | % | 1.11 | % | 1.09 | % | ||||||||||

| non-performing loans | 133 | % | 125 | % | 145 | % | 155 | % | 391 | % | ||||||||||

| nonaccrual loans | 133 | % | 125 | % | 164 | % | 199 | % | 808 | % | ||||||||||

| Non-performing assets: | ||||||||||||||||||||

| Loans delinquent over 90 days | $ | 23 | $ | 53 | $ | 3,294 | $ | 5,844 | $ | 5,124 | ||||||||||

| Nonaccrual loans | 46,517 | 38,983 | 25,657 | 20,731 | 4,816 | |||||||||||||||

| OREO | 19,346 | 9,265 | 7,044 | 4,683 | 4,831 | |||||||||||||||

| Total non-performing assets | $ | 65,886 | $ | 48,301 | $ | 35,995 | $ | 31,258 | $ | 14,771 | ||||||||||

| Allowance for Loan Losses Summary | ||||||||||||||||||||

| Balance at beginning of period | $ | 48,891 | $ | 42,113 | $ | 41,280 | $ | 38,893 | $ | 38,069 | ||||||||||

| Provision | 17,133 | 10,171 | 2,399 | 2,958 | 1,406 | |||||||||||||||

| Loans charged off | 4,114 | $ | 3,435 | $ | 1,648 | $ | 647 | $ | 586 | |||||||||||

| (Recoveries) | (64 | ) | (42 | ) | (82 | ) | (76 | ) | (4 | ) | ||||||||||

| Balance at end of period | $ | 61,974 | $ | 48,891 | $ | 42,113 | $ | 41,280 | $ | 38,893 | ||||||||||

| Net loan charge-offs (recoveries): | ||||||||||||||||||||

| Commercial real estate | $ | 481 | $ | 1,388 | $ | 295 | $ | (1 | ) | $ | 236 | |||||||||

| Residential real estate | 118 | - | - | - | (1 | ) | ||||||||||||||

| Commercial | 1,099 | 752 | 1,077 | 397 | 273 | |||||||||||||||

| Personal | 206 | 247 | 99 | (1 | ) | 3 | ||||||||||||||

| Home equity | 333 | - | - | - | - | |||||||||||||||

| Construction | 1,813 | 1,006 | 95 | 176 | 71 | |||||||||||||||

| Total net loan charge-offs | $ | 4,050 | $ | 3,393 | $ | 1,566 | $ | 571 | $ | 582 | ||||||||||

Non-performing detail by geographical location at March 31, 2008:

| Non performing Loans | NPLs as % of Total Loans (1) | Other Real Estate Owned | Non performing Assets | NPAs as % of Total Assets (2) | ||||||||||||||||

| Non performing assets | ||||||||||||||||||||

| Chicago | $ | 14,853 | 0.40 | % | $ | 2,893 | $ | 17,746 | 0.40 | % | ||||||||||

| St. Louis (3) | 7,792 | 2.01 | % | 8,133 | 15,925 | 3.19 | % | |||||||||||||

| Michigan | 7,644 | 1.18 | % | 2,722 | 10,366 | 1.20 | % | |||||||||||||

| Georgia | 16,251 | 5.99 | % | 5,598 | 21,849 | 6.29 | % | |||||||||||||

| Wisconsin | - | - | - | - | - | |||||||||||||||

| Consolidated non-performing assets | $ | 46,540 | 0.91 | % | $ | 19,346 | $ | 65,886 | 1.10 | % | ||||||||||

| Non-performing assets (4): | Commercial | Commercial Real Estate | Construction | Residential Real Estate | Personal | |||||||||||||||

| Chicago | 1.48 | % | 3.68 | % | 16.42 | % | 2.34 | % | 3.02 | % | ||||||||||

| St. Louis (3) | 4.42 | % | 10.53 | % | 7.76 | % | 1.10 | % | 0.36 | % | ||||||||||

| Michigan | 0.61 | % | 8.39 | % | 3.17 | % | 3.56 | % | 0.00 | % | ||||||||||

| Georgia | 1.95 | % | 0.00 | % | 31.21 | % | 0.00 | % | 0.00 | % | ||||||||||

| Wisconsin | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | ||||||||||

| Consolidated non-performing assets | 8.46 | % | 22.60 | % | 58.56 | % | 7.00 | % | 3.38 | % | ||||||||||

Note: Non performing loans are defined as loans delinquent > 90 days and non accrual loans. Non performing assets are non performing loans and Other Real Estate owned.

(1) Non performing loans are presented as a percentage of each entities' gross loans

(2) Non performing assets are presented as a percentage of each entities' total assets

(3) St. Louis loans and total assets includes Kansas City total loans and assets. Kansas City had no non-performing assets at 3/31/08.

(4) Non performing assets are presented here as a percentage of consolidated non performing assets

12

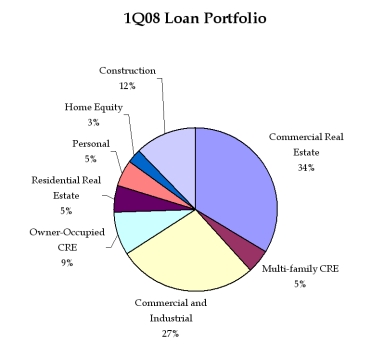

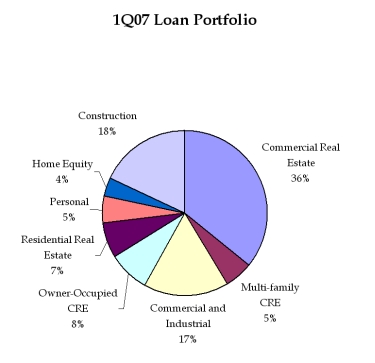

Loan Mix

Unaudited

(dollars in thousands except per share data)

| 1Q08 | 4Q07 | 3Q07 | 2Q07 | 1Q07 | ||||||||||||||||

| Loans by Category: | ||||||||||||||||||||

| Commercial Real Estate | $ | 1,728,783 | $ | 1,386,275 | $ | 1,314,138 | $ | 1,348,201 | $ | 1,288,026 | ||||||||||

| Multi-family CRE | 241,306 | 217,884 | 184,093 | 193,775 | 194,283 | |||||||||||||||

| Total CRE Loans | 1,970,089 | 1,604,159 | 1,498,231 | 1,541,976 | 1,482,309 | |||||||||||||||

| Commercial and Industrial | 1,410,442 | 827,837 | 670,106 | 643,954 | 598,360 | |||||||||||||||

| Owner-Occupied CRE | 437,587 | 483,920 | 370,269 | 319,825 | 289,393 | |||||||||||||||

| Total Commercial Loans | 1,848,029 | 1,311,757 | 1,040,375 | 963,779 | 887,753 | |||||||||||||||

| Residential Real Estate | 282,257 | 265,466 | 260,427 | 247,928 | 247,990 | |||||||||||||||

| Personal | 269,848 | 247,462 | 218,998 | 195,918 | 187,172 | |||||||||||||||

| Home Equity | 144,209 | 135,483 | 133,224 | 137,561 | 133,479 | |||||||||||||||

| Construction | 621,634 | 613,468 | 586,268 | 618,177 | 642,694 | |||||||||||||||

| Total loans | $ | 5,136,066 | $ | 4,177,795 | $ | 3,737,523 | $ | 3,705,339 | $ | 3,581,398 |

|  |

13

Net Interest Margin

Unaudited

(dollars in thousands except per share data)

| 1Q08 | 4Q07 | 3Q07 | 2Q07 | 1Q07 | ||||||||||||||||

| Net interest margin: | ||||||||||||||||||||

| Loans, net of unearned discount | 6.60 | % | 7.30 | % | 7.69 | % | 7.76 | % | 7.84 | % | ||||||||||

| Federal funds sold and interest bearing deposits | 3.20 | % | 6.02 | % | 5.37 | % | 5.15 | % | 3.26 | % | ||||||||||

| Investment Securities (taxable) | 4.97 | % | 5.04 | % | 4.85 | % | 5.16 | % | 5.01 | % | ||||||||||

| Investment Securities (non-taxable) | 6.88 | % | 6.88 | % | 6.90 | % | 6.89 | % | 6.89 | % | ||||||||||

| Yield on average earning assets | 6.49 | % | 7.11 | % | 7.45 | % | 7.53 | % | 7.56 | % | ||||||||||

| Interest bearing deposits | 3.98 | % | 4.54 | % | 4.72 | % | 4.70 | % | 4.67 | % | ||||||||||

| Funds borrowed | 4.47 | % | 4.80 | % | 4.85 | % | 4.94 | % | 4.87 | % | ||||||||||

| Junior Subordinated deferrable interest debentures held by trusts that issued guaranteed capital debt securities | 6.16 | % | 6.23 | % | 6.21 | % | 6.20 | % | 6.21 | % | ||||||||||

| Cost of average interest-bearing liabilities | 4.08 | % | 4.62 | % | 4.78 | % | 4.77 | % | 4.73 | % | ||||||||||

| Net interest spread (1) | 2.41 | % | 2.50 | % | 2.68 | % | 2.76 | % | 2.84 | % | ||||||||||

| Net interest margin (2) | 2.88 | % | 2.96 | % | 3.13 | % | 3.19 | % | 3.26 | % | ||||||||||

| Tax equivalent adjustment to net interest income (3) | $ | 1,026 | $ | 1,057 | $ | 1,072 | $ | 1,072 | $ | 1,073 | ||||||||||

| Average Quarterly Balance Sheet Data: | ||||||||||||||||||||

| Loans, net of unearned discount | $ | 4,592,477 | $ | 3,838,621 | $ | 3,707,499 | $ | 3,631,892 | $ | 3,532,333 | ||||||||||

| Federal funds sold and interest bearing deposits | 25,708 | 14,889 | 15,390 | 14,670 | 29,348 | |||||||||||||||

| Investment Securities (taxable) | 345,183 | 313,333 | 283,948 | 278,753 | 283,148 | |||||||||||||||

| Investment Securities (non-taxable) | 190,009 | 195,836 | 198,148 | 198,166 | 198,780 | |||||||||||||||

| Total Average Earning Assets | $ | 5,153,377 | $ | 4,362,679 | $ | 4,204,985 | $ | 4,123,481 | $ | 4,043,609 | ||||||||||

| Interest bearing deposits | $ | 4,025,000 | $ | 3,328,610 | $ | 3,364,047 | $ | 3,266,557 | $ | 3,249,982 | ||||||||||

| Funds borrowed | 436,658 | 492,197 | 343,820 | 382,991 | 333,312 | |||||||||||||||

| Junior Subordinated deferrable interest Debentures held by trusts that issued guaranteed capital debt securities | 101,033 | 101,033 | 101,033 | 101,033 | 101,033 | |||||||||||||||

| Total Average Interest-bearing Liabilities | $ | 4,562,691 | $ | 3,921,840 | $ | 3,808,900 | $ | 3,750,581 | $ | 3,684,327 |

(1) Yield on average interest-earning assets less rate on average interest-bearing liabilities.

(2) Net interest income, on a tax equivalent basis, divided by average interest-earning assets.

(3) The company adjusts GAAP reported net interest income by the tax equivalent adjustment amount to account for the tax attributes on federally tax exempt municipal securities. For GAAP purposes, tax benefits associated with federally tax exempt municipal securities are recorded as a benefit in income tax expense. The following table reconciles reported net interest income to net interest income on a tax equivalent basis for the periods presented:

| Reconciliation of net interest income to net interest income on a tax equivalent basis | ||||||||||||||||||||

| 1Q08 | 4Q07 | 3Q07 | 2Q07 | 1Q07 | ||||||||||||||||

| Net interest income | $ | 36,320 | $ | 31,748 | $ | 32,288 | $ | 32,111 | $ | 31,975 | ||||||||||

| Tax equivalent adjustment to net interest income | 1,026 | 1,057 | 1,072 | 1,072 | 1,073 | |||||||||||||||

| Net interest income, tax equivalent basis | $ | 37,346 | $ | 32,805 | $ | 33,360 | $ | 33,183 | $ | 33,048 | ||||||||||

14