Filed by PrivateBancorp, Inc.

Pursuant to Rule 425 under the Securities Act of 1933

(Commission File No: 333-137560)

Subject Company: Piedmont Bancshares, Inc.

Set forth below are presentation materials for PrivateBancorp, Inc.’s Investor Presentation at Reuters held on Monday, November 20, 2006:

PrivateBancorp, Inc. Investor Day November 20, 2006 |

PrivateBancorp, Inc. Ralph B. Mandell Chairman of the Board, President and Chief Executive Officer 2 |

In this presentation we may make certain forward-looking statements. The Company’s ability to predict results or the actual effect of future plans or strategies is inherently uncertain. For more information about these risks and uncertainties, we refer you to our public reports on file with the SEC. PrivateBancorp has filed a registration statement on Form S-4 with the Securities and Exchange Commission (the “SEC”), which has been declared effective by the SEC, in connection with its proposed acquisition of Piedmont Bancshares, Inc. (“Piedmont”). The registration statement includes a proxy statement of Piedmont that also constitutes a prospectus of PrivateBancorp (the “proxy statement/prospectus”), which was sent to the shareholders of Piedmont. Piedmont shareholders are advised to read the proxy statement/prospectus, which was filed with the SEC on October 27, 2006, because it contains important information about PrivateBancorp, Piedmont and the proposed transaction. The proxy statement/prospectus and other relevant documents relating to the merger filed by PrivateBancorp can be obtained free of charge from the SEC’s website at www.sec.gov. These documents also can be obtained free of charge by accessing PrivateBancorp’s website at www.pvtb.com under the tab “Investor Relations”. Alternatively, these documents can be obtained free of charge upon request to PrivateBancorp, Inc., Secretary, 70 West Madison, Suite 900, Chicago, Illinois 60602 or by calling (312) 683-7100, or to Piedmont Bancshares, Inc., Attention: President, 3423 Piedmont Road, Suite 225, Atlanta, Georgia 30305, or by calling (404) 926-2400. Forward Looking Statements 3 Information About Private’s Proposed Acquisition of Piedmont Bancshares, Inc. |

Restatement of Financial Information All periods presented reflect the adoption of SFAS 123R, Share-Based Payment, on January 1, 2006, using the modified- retrospective transition method, which is unaudited at this time. 4 |

Presenters Ralph B. Mandell, Chairman of the Board, President and Chief Executive Officer Dennis L. Klaeser, Chief Financial Officer Gary S. Collins, Vice Chairman, The PrivateBank - Chicago Hugh H. McLean, Vice Chairman, The PrivateBank - Chicago Wallace L. Head, Chief Executive Officer, Wealth Management William A. Goldstein, President, Lodestar Investment Counsel, LLC Richard C. Jensen, Chairman, Chief Executive Officer, The PrivateBank – St. Louis John B. Williams, Chief Executive Officer, The PrivateBank – Wisconsin David T. Provost, Chairman, Chief Executive Officer, The PrivateBank – Michigan James A. Ruckstaetter, Chief Credit Officer Christopher J. Zinski, General Counsel Thomas J. Olivieri, Director of Operations Thomas N. Castronovo, Chief Marketing Officer Jerry J. Feldman, Managing Director Calvin Kleinmann, Chairman and Chief Executive Officer, The PrivateBank – Kansas City (in formation) Brian D. Schmitt, President and Chief Executive Officer, Piedmont Bancshares, Inc. 5 |

6 |

• European model of private banking, providing personalized service, continuity, confidentiality and discretion • Target high net worth households and their related businesses • We have a unique staffing model and employ experienced Managing Directors who provide day-to-day consultation and services • Strong insider ownership Strategy 7 |

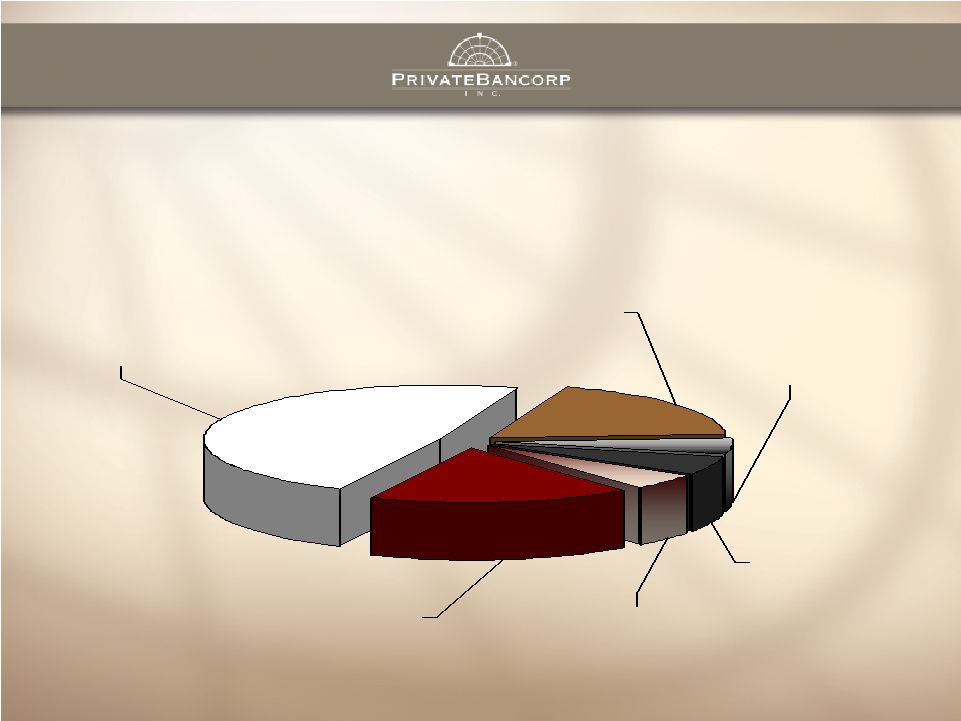

Growth in Affluent Households 11,900 53,583 64,200 263,008 19,592 29,904 25,738 110,836 23,168 137,139 8,282 38,691 0 50,000 100,000 150,000 200,000 250,000 300,000 Market Households with Annual Income over $150,000 1990 Census 2005 Estimate 8 |

(in formation) (pending Piedmont acquisition) 9 |

(in formation) (pending Piedmont acquisition) 10 |

The PrivateBank – Chicago Gary S. Collins Vice Chairman Hugh H. McLean Vice Chairman 11 |

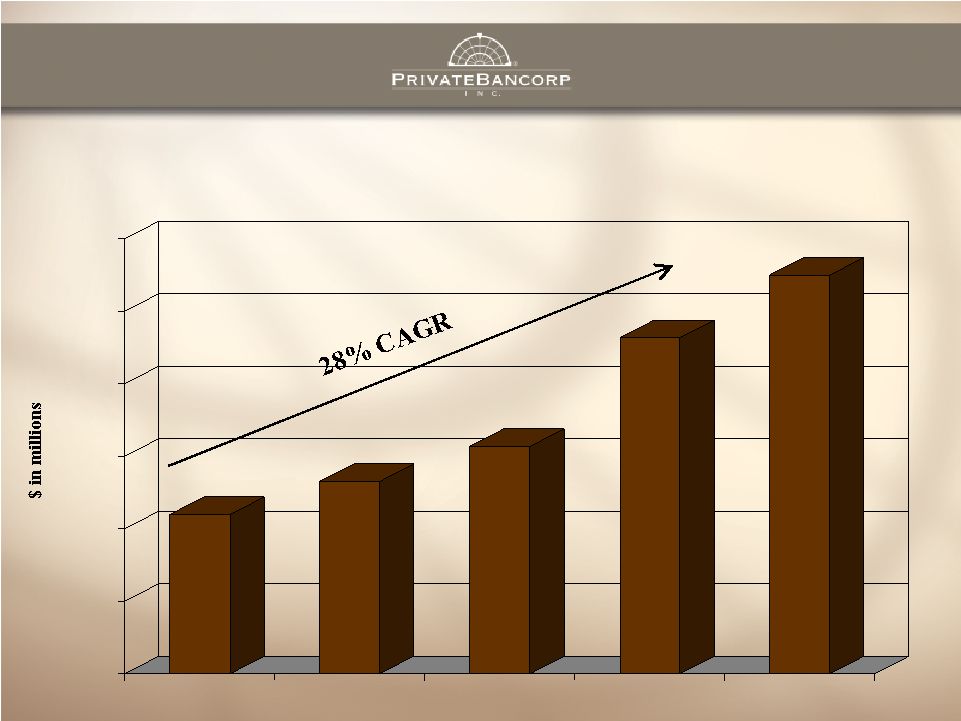

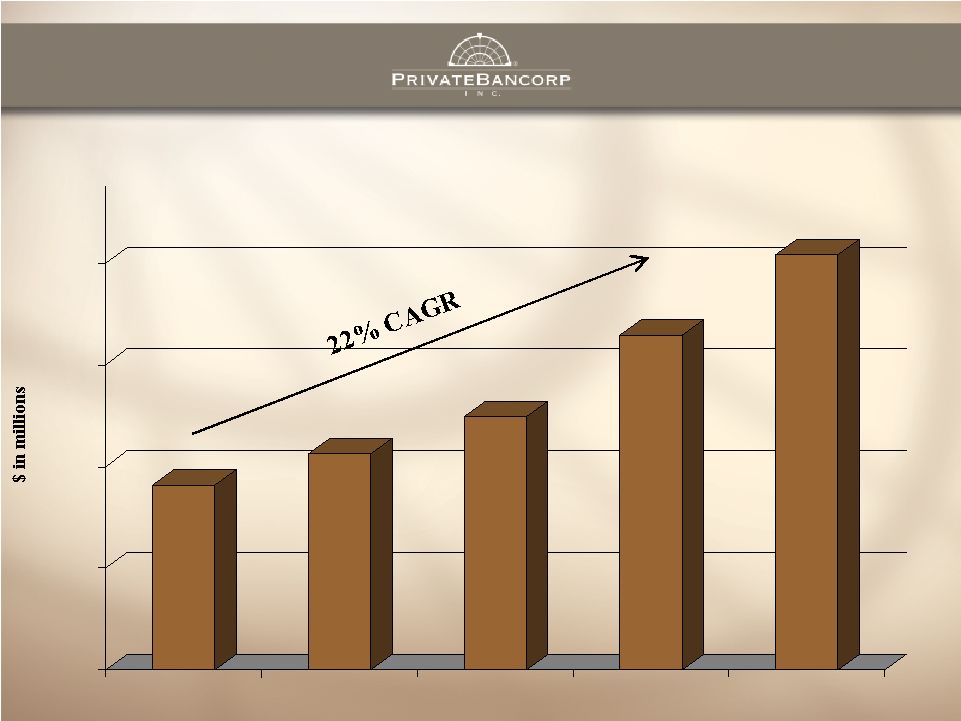

Loan and Core Deposit Growth The PrivateBank - Chicago $707 $861 $1,073 $1,452 $1,878 $2,250 $0 $500 $1,000 $1,500 $2,000 $2,500 $3,000 2001 2002 2003 2004 2005 9/30/2006 Total Loans $666 $863 $1,015 $1,331 $1,670 $1,786 $0 $200 $400 $600 $800 $1,000 $1,200 $1,400 $1,600 $1,800 $2,000 2001 2002 2003 2004 2005 9/30/2006 Total Core Deposits (Excluding Brokered Deposits) The PrivateBank – Chicago is Illinois’ 10 largest bank 12 th |

Key to Growth The PrivateBank - Chicago Continued Recruitment of Managing Directors 13 |

Investment In Our People The PrivateBank - Chicago 28 40 49 61 67 76 0 10 20 30 40 50 60 70 80 Number of Managing Directors The PrivateBank - Chicago 14 |

Current Breakout of MD Staffing The PrivateBank - Chicago Number of Managing Directors As of September 30, 2006 Chicago: 40 Wilmette: 4 Oak Brook: 7 Gold Coast: 3 St. Charles: 7 Winnetka: 4 Lake Forest: 8 Geneva: 3 15 |

Typical Profile of Recruited Managing Director The PrivateBank - Chicago 15+ years of experience with larger bank Accomplished commercial and/or commercial real estate lender Strong sense of service to their clients 16 |

The PrivateBank - Chicago Continuing consolidation in Chicago’s banking market supports high level of recruitment 17 |

2006 Initiative The PrivateBank - Chicago Expansion of existing offices Oak Brook, Geneva, Chicago Headquarters Headquarters Square Footage (75,000) *New Location as of August 4, 2006 18 |

Case Study: Our Newest Office Gold Coast Office The PrivateBank - Chicago 19 |

Gold Coast Statistics The PrivateBank - Chicago Outstanding growth in great market Office Opened: January 2005 Loans Outstanding as of September 30, 2006: $145 Million Deposits Outstanding as of September 30, 2006: $118 Million Managing Directors: 3 20 |

PrivateBancorp, Inc. - Wealth Management Wallace L. Head Chief Executive Officer, Wealth Management Managing Director 21 |

PrivateBancorp's Wealth Management Business Mission and Services Distinctive Characteristics The Business Today Plans For The Future 22 |

PrivateBancorp's Wealth Management Mission “Deliver distinctive, highly personalized wealth management services that are also profitable, sustainable, and complement and help differentiate banking services provided by The PrivateBanks in their individual markets.” 23 |

PrivateBancorp's Wealth Management Services Fiduciary Services (trustee, investment agent, guardian, executor, escrow agent, custodian) Asset Management Services Wealth Advisory Services Note: Personal banking services are provided by our bankers 24 |

Distinctive Characteristics of Wealth Management at PrivateBancorp Services are designed and provided to serve the clients’ best interests Each client works directly with an experienced, trustworthy professional High quality fiduciary services are provided with fully open-architecture investment management 25 |

PrivateBancorp's Wealth Management Today Located in The PrivateBanks (IL, MI, MO, WI) working closely with our bankers 29 MDs/AMDs who average > 20 years of wealth management experience Diversified, stable client base • ~ 1000 client relationships and $2.8B • Most client relationships are < $10M • Relationships range from < $1M to > $250M 26 |

PrivateBancorp's Wealth Management Today 23.1% $2.8B $1.5B AUM & Custody 37.5% $2.6M $1.0M Pre-Tax Net Income $28.8% $14.1M $6.6M Fee Revenue CAGR 2003-2006 2006* 2003 *“Fee Revenue” and “Pre-Tax Net Income” are annualized amounts. “AUM & Custody” is actual amount at 10/31/06. 27 |

PrivateBancorp's Wealth Management Tomorrow Enhanced Resources • National trust powers • Additional experienced MDs/AMDs • Expanded open-architecture investment platform • Additional wealth advisory services 28 |

PrivateBancorp's, Wealth Management Tomorrow Expanded Client Base • Larger % of client relationships > $10M • Fiduciary services provided to family offices and multi-family offices Increased Sources of New Business • More bankers in more PVTB banks • More professional advisors providing referrals • More clients making introductions • Acquisitions of wealth management firms 29 |

Lodestar Investment Counsel, LLC William A. Goldstein President 30 |

What We Do Lodestar One business: manage client assets • Since 1989 we have managed equity, fixed income, and balanced portfolios Conservative, Consistent and Disciplined Respect our clients’ confidentiality Construct customized portfolios 31 |

Who We Are Lodestar William A. Goldstein 44 Years Experience Chairman, Prescott Asset Management President, Selected Special Shares Fund Founder, Burton J. Vincent Chesley & Co. Hornblower & Weeks B.A., Purdue University Robert H. Dearborn 25 Years Experience Principal, Stein Roe & Farnham Officer, Northern Trust Company Chartered Financial Analyst (CFA) B.A., Kenyon College M.B.A., University of Chicago Peter W. Flanzer 20 Years Experience Principal, Cedar Hill Associates Smith Barney Syndicated Equities Corporation Lake Shore Bank B.A., Kenyon College J.D., John Marshall Law School John J. Sobel 14 Years Experience Portfolio Manager Salomon Smith Barney Consulting Group B.A., University of California at Los Angeles M.B.A., University of Washington 32 |

How We Differentiate Ourselves Lodestar Clients meet regularly with Portfolio Managers Clients receive phone calls after purchase or sales, if desired Each portfolio is individually constructed We do it The PrivateBank way • Continuity • Confidentiality • Professionalism 33 |

Our Clients Are Lodestar High Net Worth Individuals Family Trusts Family Foundations 34 |

We Are A Large Cap, GARP, Balanced Account Manager Lodestar 60% Equity 40% Fixed Income Investment Objective • Better than S&P Equity Returns • Less than Market Risk 35 |

Lodestar Taxable Balanced Account Composite Investment Returns Through September 30, 2006 6.02% 2.70% 2.92% 8.56% 8.67% Year to Date 2006 (1/1/06 – 9/30/06) 7.88% 5.71% 5.56% 10.59% 10.78% Inception (1/1/90 – 9/30/06) 6.83% 4.83% 4.60% 8.57% 9.04% Ten Years (Annualized) 5.16% 3.82% 3.47% 6.97% 6.83% Five Years (Annualized) 7.64% 3.01% 3.56% 10.77% 11.17% One Year Total Account Bond Index Bonds Only S&P 500 Index Stocks Only Period Investment returns are gross of fees from Lodestar’s “Taxable Balanced Composite”. This composite includes our firm’s taxable client portfolios which invest in both equity and fixed income securities. Further detail on this Composite and the above information is available on request. 5-Year Muni 36 |

Lodestar Taxable Balanced Account Composite Standard Deviation of Returns Periods Ended December 31, 2005* 2.80 2.23 19.50 15.47 Ten Years 3.75 3.39 17.88 14.56 Inception (1/1/90 - 12/31/05) 3.22 2.63 19.80 15.85 Five Years 5-Year Muni Bond Index Bonds Only S&P 500 Index Stocks Only *One standard deviation of annual returns. 37 |

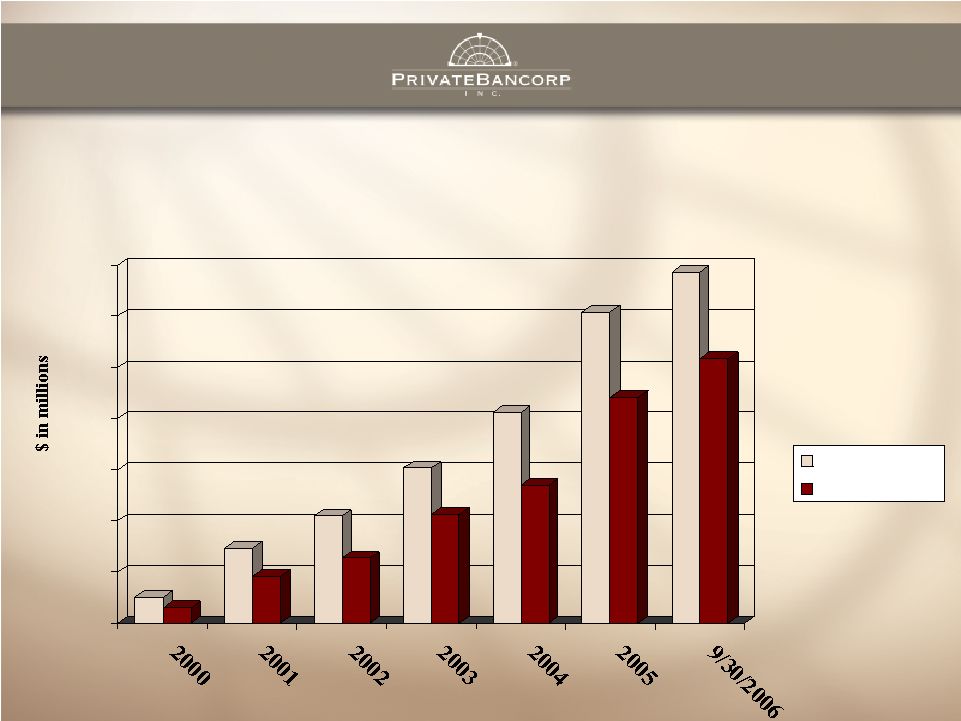

Assets Under Management Lodestar $0 $100,000 $200,000 $300,000 $400,000 $500,000 $600,000 $700,000 $800,000 2000 2001 2002 2003 2004 2005 9/30/2006 38 |

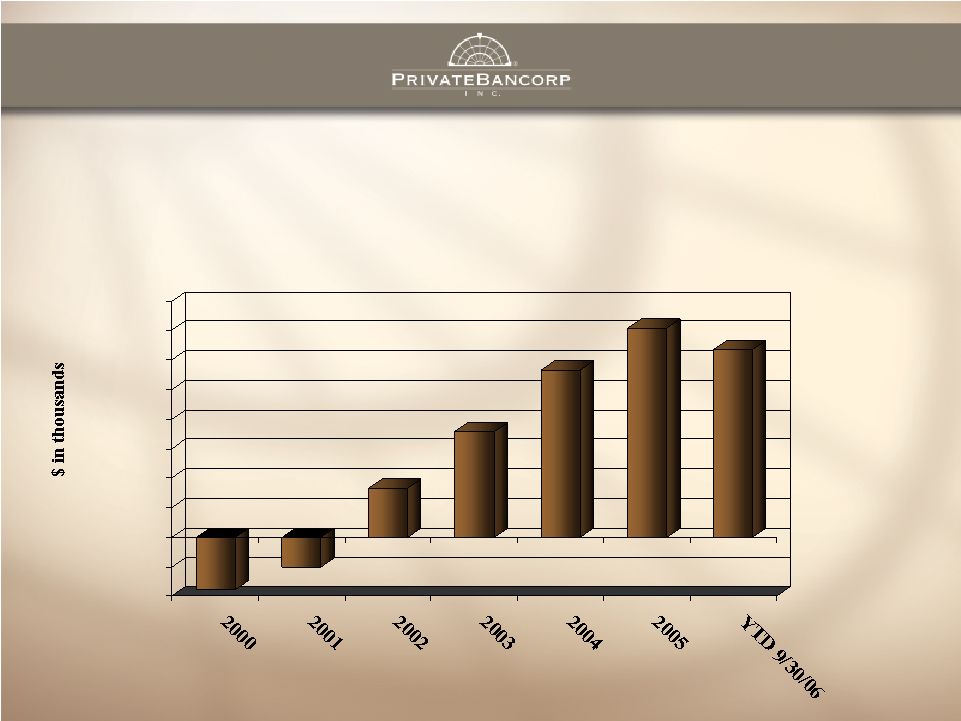

Fee Income Lodestar $0 $500 $1,000 $1,500 $2,000 $2,500 $3,000 $3,500 $4,000 $4,500 2000 2001 2002 2003 2004 2005 YTD 9/30/06 39 |

Pre-Tax Profit Margin Lodestar 0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 30.0% 35.0% 40.0% 2000 2001 2002 2003 2004 2005 YTD 9/30/06 * 2002: Before adjustments to reflect merger with PrivateBank. 40 |

Future Growth Opportunities Lodestar The PrivateBank Formula • Add Portfolio Managers with existing books of business • Continued referrals from existing clients and The PrivateBank • Follow The PrivateBank to new geographic markets 41 |

Our Strengths Lodestar Focus • Our Clients • Disciplined Investment Style Great People • Account Managers and Staff • Virtually no employee turnover A belief in what we do A diverse, loyal client base Lodestar Clients and PrivateBank Clients have a common financial profile 42 |

The PrivateBank – St. Louis Richard C. Jensen Chairman, Chief Executive Officer and Managing Director 43 |

St. Louis Metro Demographics The PrivateBank – St. Louis Population • 2.8 million – Metro Area • 1.0 – St. Louis County Household Incomes Greater Than $150,000 • 43,224 4.27% Population Growth 1990 – 2000 • 4.46% 44 |

St. Louis Employment The PrivateBank – St. Louis Largest Employers • BJC Health Care 25,000 • Boeing 15,000 • Washington University 12,000 • Schnucks Markets 11,000 • St. John’s Mercy 8,500 Corporate Headquarters • 8 of Fortune 500 • 21 of Fortune 1000 45 |

Industry Groups The PrivateBank – St. Louis Aerospace • Boeing Plant & Medical Science • Monsanto • Mallikckrodt • Sigma-Aldrich • Pfizer Automotive • Chrysler • General Motors Financial Services • AG Edwards • Edward Jones • Stifel Nicolaus • Scottstrade • MasterCard Global Operations • Citi Mortgage Food Products • Anheuser-Busch • Sara Lee Bakery Group • Nestle Purina Pet Care • Bunge International 46 |

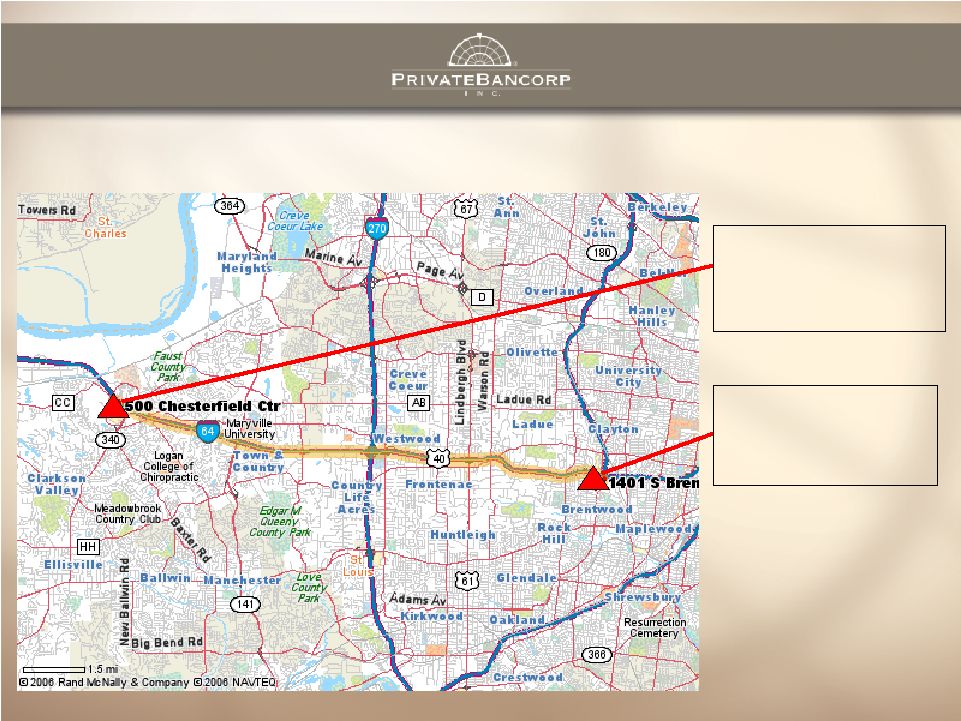

The PrivateBank – St. Louis Chesterfield 500 Chesterfield Center Chesterfield, MO 63017 Brentwood 1401 S. Brentwood 2 Fl. St. Louis, MO 63144 47 nd |

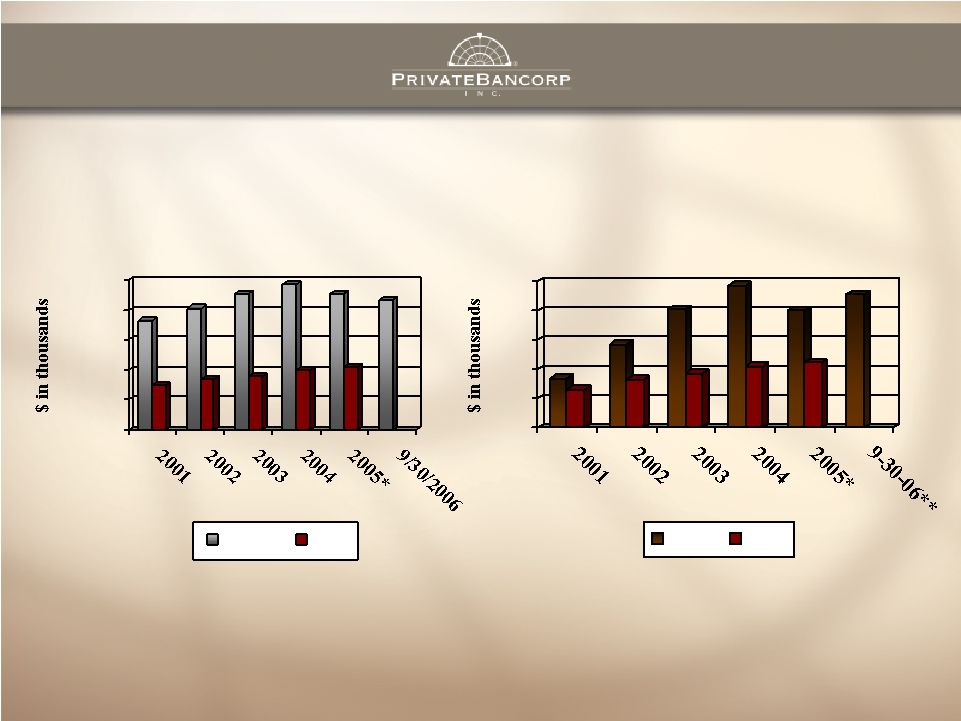

Net Interest Income for St. Louis The PrivateBank – St. Louis $404 $1,838 $4,007 $5,437 $7,656 $11,156 $10,624 $0 $2,000 $4,000 $6,000 $8,000 $10,000 $12,000 2000 2001 2002 2003 2004 2005 YTD 9/30/06 48 |

Gross Loans and Core Deposits for St. Louis The PrivateBank – St. Louis $25.2 $14.7 $73.5 $45.6 $104.7 $63.7 $151.5 $106.3 $206.1 $135.2 $304.4 $220.9 $343.2 $258.3 $0 $50 $100 $150 $200 $250 $300 $350 Gross Loans Core Deposits 49 |

CRE 41% RRE 10% Personal 8% Construction 21% Commercial 20% Demand 15% MMA 30% Interest Bearing 3% Savings and Other Time Deposits 52% Loans and Core Deposits by Category for St. Louis The PrivateBank – St. Louis Loans as of September 30, 2006 Core Deposits as of September 30, 2006 50 |

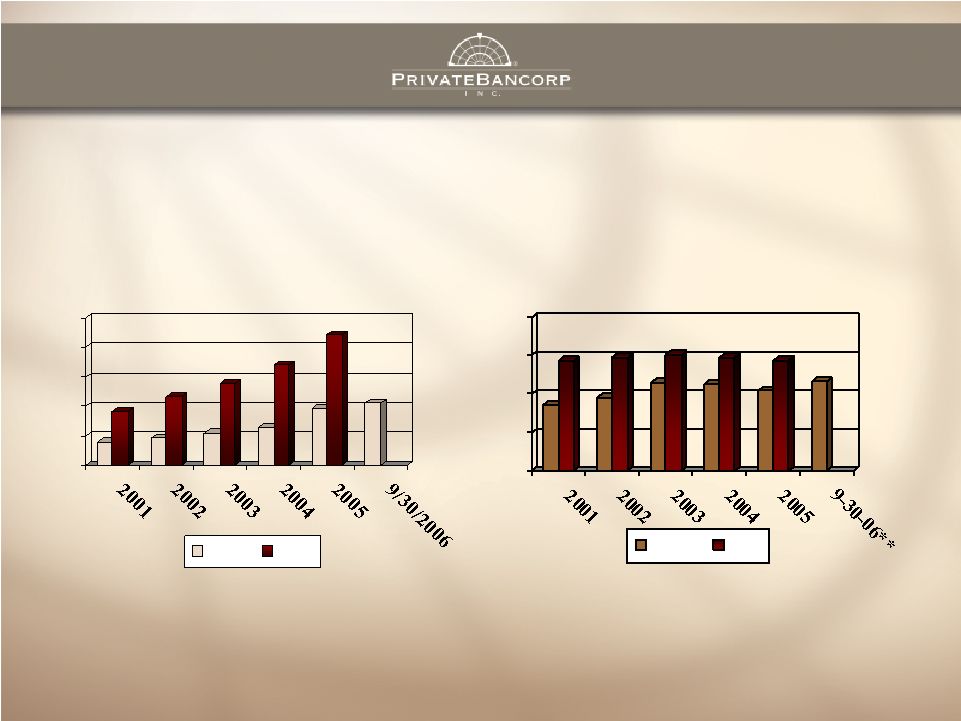

Other Income for St. Louis The PrivateBank – St. Louis $30 $688 $1,996 $3,455 $2,353 $2,147 $1,436 $0 $500 $1,000 $1,500 $2,000 $2,500 $3,000 $3,500 51 |

Net Income for St. Louis The PrivateBank – St. Louis -$894 -$510 $829 $1,785 $2,823 $3,541 $3,181 -$1,000 -$500 $0 $500 $1,000 $1,500 $2,000 $2,500 $3,000 $3,500 $4,000 52 |

Staffing for St. Louis The PrivateBank – St. Louis 0 10 20 30 40 50 60 0 500 1,000 1,500 2,000 2,500 3,000 3,500 4,000 4,500 5,000 # of Employees Core Deposits per FTE 53 |

The PrivateBank – St. Louis Brentwood 54 |

The PrivateBank – St. Louis Chesterfield 55 |

The PrivateBank - Wisconsin Jay B. Williams Chief Executive Officer and Managing Director 56 |

57 |

58 |

The PrivateBank - Wisconsin “Make no little plans; they have no magic to stir men’s blood. Make big plans; aim high in hope and work.” Daniel Hudson Burnham (1846-1912) 59 |

Metro Milwaukee The PrivateBank - Wisconsin 1.5 Million People 25,000 Households with more than $150,000 of Income 60 |

Metro Milwaukee The PrivateBank - Wisconsin 43 Largest Metro Economy GMP $57.11 61 rd |

Home to Fortune 500 Companies The PrivateBank - Wisconsin Johnson Controls Northwestern Mutual Manpower Kohl’s Harley Davidson Rockwell Automation FISERV Marshall & Ilsley 62 |

The PrivateBank - Wisconsin What have we accomplished in one year? 63 |

The PrivateBank - Wisconsin We are Profitable As of October 31, 2006: $158.7 Million in Loan Commitments $89.4 Million in Loans Outstanding $75.0 Million in Core Deposits 64 |

The PrivateBank - Wisconsin Why and how have we accomplished this? 65 |

The PrivateBank - Wisconsin It’s about the People It’s about the Business Model 66 |

The People The PrivateBank - Wisconsin Experienced, Knowledgeable Decision Makers Outstanding Board of Directors 67 |

The Business Model The PrivateBank - Wisconsin Targeted Client Centric Unique Growth Oriented 68 |

The PrivateBank - Wisconsin We understand who we are! 69 |

The PrivateBank - Wisconsin Tangible Image How we are measured: Outstanding credit quality Retention of clients Retention of employees Growth in number of clients Taking leadership roles in our community Mission What we do: In our market we will be recognized as the best provider of financial solutions to affluent households and privately held businesses. Purpose We exist to: Help our clients, employees and their families achieve success Core Values We believe in: Integrity Confidentiality Lifetime Relationships Continuity Responsiveness Execution Focus Drivers of Progress DNA 70 |

The PrivateBank - Wisconsin In 5 years, how will we measure success? 71 |

The PrivateBank - Wisconsin 1) We are a $400 million Asset Bank 2) Highly Profitable 3) Outstanding Credit Quality 4) Retention of Clients and Employees 5) We lived the Business Model 72 |

The PrivateBank - Michigan David T. Provost Chairman, Chief Executive Officer and Managing Director 73 |

Manufacturing 15% Professional/ Business Services 11% Leisure & Hospitality 9% Information 2% Education/ Health Services 13% Government 15% Financial Activities 5% Utilities & Transportation 22% Construction 4% Other Services 4% Michigan Business Diversification (based on the composition of the state’s workforce.) Source: Ryan Beck & Co. 74 |

• 4 wealthiest county in the U.S. • More than half of the top 100 Global Fortune 500 companies have business operations in Oakland County. • Ranks 1 in projected wealth creation for Michigan The PrivateBank - Michigan Oakland County Overview Source: Ryan Beck & Co. 75 st th |

Michigan Locations 76 |

Bloomfield Hills - established 1989 Ranked 4th wealthiest city in the United States and is the richest city outside of California or Florida. Rochester – established 1999 Chosen by CNN/Money as one of the “Best Places to Live” in the US. Grosse Pointe – established 2002 Known for its many estates and prominent families of the industrial pioneers of Michigan. Michigan’s Office Location Overview Source: Ryan Beck & Co. 77 |

Asset Growth The PrivateBank - Michigan $219.5 $265.5 $313.6 $462.9 $555.0 $0 $100 $200 $300 $400 $500 $600 2002 2003 2004 2005 09/30/06 78 |

Deposit Growth The PrivateBank - Michigan $181.4 $212.3 $248.9 $328.9 $408.3 $0 $100 $200 $300 $400 2002 2003 2004 2005 09/30/06 79 |

Deposit Mix The PrivateBank - Michigan IRA's 1% Public Funds 32% CDs < $100,000 3% DDA 8% CDs > $100,000 28% Money Market 24% NOW 4% 80 |

Loan Growth The PrivateBank - Michigan $200.6 $245.1 $295.3 $397.8 $484.5 $0 $100 $200 $300 $400 $500 2002 2003 2004 2005 09/30/06 81 |

Portfolio Mix (Outstanding Loan Balance, Gross) The PrivateBank - Michigan Residential Mortgages 18% Equity Lines 5% Commercial Mortgage/Real Estate 48% Commercial & Residential Construction 6% Installment/ Consumer 4% Commercial & Industrial 19% 82 |

Net Charge-offs to Average Loans The PrivateBank - Michigan 0.00% 0.16% 0.06% 0.00% 0.00% 0.00 0.20 0.40 0.60 0.80 1.00 2002 2003 2004 2005 9/30/2006 83 |

Experienced Management Team The PrivateBank - Michigan Name Title Age Yrs. of Banking David T. Provost Chairman and CEO 52 30 Patrick M. McQueen President and COO 60 42 Robert M. Burch Vice Chairman 63 41 Thomas W. Brown Chief Financial Officer 51 29 Ann M. Deering Chief Credit Officer 48 26 84 |

PrivateBancorp, Inc. James A. Ruckstaetter Chief Credit Officer and and Managing Director 85 |

Culture People Credit Deal 86 |

Organizational Strengths Underwriting Diversification: Chicago St. Louis Michigan Wisconsin Georgia (pending Piedmont acquisition) Kansas City (in formation) 87 |

PrivateBancorp’s Loan Portfolio by Loan Type Construction 13% Home Equity 8% Personal 6% Residential RE 6% Commercial RE 51% Commercial 16% September 30, 2003 September 30, 2006 Construction 15% Commercial 18% Home Equity 4% Personal 5% Commercial RE 50% Residential RE 8% 88 |

PrivateBancorp’s Commercial RE Loans by Loan Type & Collateral Location as of 9/30/06 Resid. 1-4 Family 10% Multi Family 11% Office 12% Warehouse 7% Retail 8% Total Construction 23% Land 19% Mixed Use & Other 10% 89 |

PrivateBancorp’s Commercial RE Loans by Collateral Location as of 9/30/06 IL 63% MO 11% MI 13% WI 3% Other 7% FL 3% 90 |

Asset Quality Ratios PrivateBancorp, Inc. As of 9/30/06 2005 2004 2003 Net Charge-offs to average total loans: Non-performing loans to total loans: Allowance for loan losses to total loans: 0.04% -0.01% 0.04% 0.08% 0.06% 0.04% 0.15% 0.09% 1.11% 1.13% 1.15% 1.23% Year Ended December 31, 91 |

PrivateBancorp, Inc. Christopher J. Zinski General Counsel and Managing Director 92 |

Enhancing PrivateBancorp, Inc.’s Infrastructure to Support Growth A Keen Focus on Three Elements of PrivateBancorp’s Business • Corporate Governance • Strategic Growth • Risk Management 93 |

Corporate Governance Already Strong Focus • Right “Tone at the Top” • Director quality, independence and participation • PrivateBancorp believes good governance promotes its business Board Values Consistently Enhancing Governance Protocols • GC as a regular guide and adviser to the Board • GC supports Governance Committee • GC assumes role as Chief Ethics Officer 94 |

Strategic Growth Strong Track Record • Successful growth outside of Chicago (organic and acquisitive) • Premium on human capital and credit quality • PrivateBancorp believes a national build-out of the model is viable Board Values Enhancing Team to Manage Strategic Growth • Pipeline full of opportunities • Advantage in deal-making to have a senior in-house lawyer • GC expands team handling multiple expansion initiatives and integration 95 |

Risk Management Key Bases Covered • Blending inside/outside resources for best of class/best practices • Accountability • Seasoned, senior managers • PrivateBancorp believes in risk management architecture Board Values adding a Risk Management Officer • GC with leadership role in formal enterprise risk management • GC with FI experience; sensitive to industry risks • GC as adviser to business unit leaders and Board on risk management 96 |

PrivateBancorp, Inc. Thomas J. Olivieri Director of Operations and Managing Director 97 |

Operations Infrastructure Core Processing System – New 7 Year Contract • Cost Controls – Old Contract: 20% fixed, 80% variable – New Contract: 50% fixed, 50% variable • Volumes Aggregated at Holding Company Level • Minimal Conversion Costs for Acquisitions – Technology Supports Growth at Low Cost • Merchant and Branch Capture 98 |

Process Improvement If You Don’t Measure It, You Can’t Manage It Process Teams – Lean Concepts • Cycle Time and Variance Reduction • Quality Assurance – Best Practices • Companywide Best Practices • Industry Best Practices 99 |

Communications Operations Summits • Across Regions, Across Business Units Common Platform • Core Processing • Interoffice Communications Client Contact • CRITICAL: Always Hear the Voice of the Client 100 |

Our Operations Goals Entrepreneurship Within Operations • Delight Internal Clients • Handoffs: Critical to Service Levels • Enabling Our Bankers Experienced Bankers • Build on Quality and Experience • Learn From Each Other Successful Integrations and Launches 101 |

Thomas N. Castronovo Chief Marketing Officer PrivateBancorp, Inc. Director of Marketing & Managing Director The PrivateBank Our Brand – Our Culture 102 |

103 |

Focus Execution Confidentiality Lifetime Relationships Continuity You have arrived. Welcome to The PrivateBank. 104 |

Our core values define our Brand Focus Execution Continuity Confidentiality Lifetime Relationships 105 |

Recruitment Client experience Responsiveness Lines of business Markets Growth opportunities Our Brand guides and aligns our decision making across our regions 106 |

Our brand is defined at all touch points, but especially at each point of human contact. Delivering Our Brand 107 |

Our people bring our brand to life 108 |

Innovative 109 |

Attention to Detail 110 |

Experience |

Integrity 112 |

Personable 113 |

Responsive 114 |

Thorough 115 |

our values live in our people 116 |

Professional 117 |

Entrepreneurial 118 |

Flexible 119 |

Enthusiastic 120 |

Our Brand Differentiation CLIENT CENTERED Flat structure with exceptional insider ownership Stress the client “experience” not products Offices not branches Clients not customers Specific market niche Boutique Focus 121 |

Orientation Culture immersion Ongoing training Standards of Excellence & Corporate Guidelines Branding from the Inside Out 122 |

Key Rewards of Orientation Preserves the PrivateBancorp brand Avoids leaving our image to interpretation Promotes continuity (a core principle) Attracts the best and brightest talent Sets the bar – sets standards for professionalism Maintains differentiation Builds commitment – empowers – connects Instills pride and responsibility Consistency in delivery of the experience/the promise Doesn’t assume everyone ‘gets it’ 123 |

Branding from the Inside Out Marketing Support Defining and enhancing the “client experience” Driving referrals Creating & sustaining loyalty Strengthening Brand identity 124 |

Brand Identity/ Brand Personality High Quality, Signature approach Relevant & Credible Authentic & Consistent Environment Office design Private Destinations Visuals Emotional connection Clean, elegant look Unified visual elements & color palette 125 |

126 |

127 |

128 |

129 |

Brand Identity/ Brand Personality High Quality, Signature approach Relevant & Credible Authentic & Consistent Environment Office design Private Destinations Visuals Emotional connection Clean, elegant look Unified visual elements & color palette 130 |

131 |

132 |

133 |

134 |

135 |

136 |

137 |

138 |

139 |

140 |

141 |

142 |

143 |

144 |

The PrivateBank - Chicago Jerry J. Feldman Managing Director 145 |

Business Background The PrivateBank - Chicago 15 Years in Commercial Banking. 10 Years in Private Business. Why did I join PVTB? 146 |

Commercial Banking is an appropriate line of business for PVTB The PrivateBank - Chicago Logical extension for PVTB's brand and culture. Relationship banking drives high margin business. Continuation of stated objective to pursue growth opportunities. Hundreds of thousands of privately-held companies in greater Chicago area. 147 |

Strategy The PrivateBank - Chicago Leverage reputation, culture and performance of PVTB. Leverage contacts and knowledge of experienced commercial bankers. Thoughtful and consistent approach to the marketplace. 148 |

Target Client Profile The PrivateBank - Chicago Solid companies with strong history of earnings. Strong, smart management with logical business strategies Cash flow and balance sheet strength. 149 |

The PrivateBank – Kansas City (in formation) Cal Kleinmann Chairman and Chief Executive Officer 150 |

Why Kansas City? (in formation) 30% of the gross state products of Kansas and Missouri come from the Kansas City region, totaling $90 billion Kansas City dominates the animal-health niche, representing 40% of the $14.5 billion a year business in the nation, and 26% of it worldwide, with 37 global or U.S. headquarters of industry companies Strong residential and construction market Kansas City is one of the nation’s busiest transportation hubs 151 |

The Kansas City Metro / Johnson County Markets (in formation) 2.4 million residents in Greater Kansas City metropolitan area. Tremendous investment in the downtown, including $270 million for the Sprint Center, $145 million for a new H&R Block headquarters, $150 million to renovate the city’s convention center, and $850 million for the a seven-block entertainment complex. Johnson County, Kansas – consistently one of the fasted growing counties in the U.S Major employers include Sprint Nextel, H&R Block, YRC Worldwide, Hallmark Cards, and Black & Veatch. 152 |

Area Population Growth 2000-2004 (in formation) 0% 2% 4% 6% 8% 10% 12% Johnson County KC Metro Area United States Source: US Census Bureau 153 |

Kansas City Metro Area Leading Indicators (in formation) 57,067 Total 48,412 Local 170 Subsidiary Headquarters 8,328 Branches 157 Headquarters KC Metro Area Number of Businesses Note: Kansas City Metro area includes Johnson and Wyandotte counties in Kansas and Cass, Clay, Platt and Jackson counties in Missouri. Leading Industries in 2005 Government 14.4% Manufacturing 8.4% Fin. Ins. 16.3% RE & Tran 7.4% Commun. 10.4% Const/Min 5.2% (In thousands) Services 37.9% 154 |

One of the fastest-growing major markets in the Midwest A well-educated, extremely productive work force Lower business & life style costs than most major metros Diverse group of major employers (1) Source: KCADC (2) Revenues are for Kansas City metro area companies covered by OneSource. A Target Rich Business Market (in formation) 1,595 857 627 608 0 500 1,000 1,500 2,000 $0-$10M $10-$20M $20M-$50M $50->$1,000M Revenue Revenues for Kansas City metro area companies 155 |

The PrivateBank – Kansas City Team (in formation) Cal Kleinmann Chairman & Chief Executive Officer former Executive Vice President and Head of Private Banking for Gold Bank Paul Clendening President & Chief Operating Officer former President and a Founder of First Commercial Bank Sherman Titens Managing Director and Chief Marketing Officer former Senior Vice President and Director of Marketing for Gold Banc Corp., Inc. Jennifer Bailey Managing Director of Treasury Services former Manager of Treasury Services for Gold Bank 156 |

Strategies for Success Deposits- Focus on funding to business clients, professionals, affluent individuals and non-profits. Lending- Commercial and commercial real estate lending, personal and community lending, residential construction and mortgage lending; emphasize diversity. Start-up Strategy- Opened loan production office November 1, 2006, open as location of The PrivateBank-St. Louis by year- end, open as newly chartered The PrivateBank-Kansas City by mid-year 2007. 157 |

Kansas City Headquarters Location Plaza Colonnade On the Country Club Plaza Kansas City, Missouri 158 |

Piedmont Bancshares, Inc. Brian D. Schmitt President and Chief Executive Officer 159 |

Current MSA Population 5.2 million – 9 Largest Metropolitan Area Projected MSA 2011 - 5.8 million Ranks Third in the Country With Most Fortune 500 Companies (14) Home to 137,000 Businesses 27 Fortune 1,000 Companies World’s Busiest Airport Atlanta is Home to 45 Accredited Colleges/Universities Job Creation 69,100 new jobs – 2005 60,000 new jobs – 2006 (projected) Median Age 33 Median Household Income $51,186 Projected 112,000 Households With Over $1 Million in Investable Assets by 2011 Atlanta, Georgia Overview Piedmont Bank 160 th |

Hospitality & Entertainment 9% Management & Administration 7% Trade 23% Other 13% Construction & Mining 9% Utilities & Transportation 3% Information & Professional Services 11% Finance, Investment & Real Estate 11% Healthcare (Education & Services) 10% Manufacturing 4% Atlanta Business Establishments by Industry Piedmont Bank 161 |

Piedmont Bank Locations Alpharetta Office (Proposed) Norcross Office (Opened March, 2006) Buckhead Office (Opened October, 2001) 162 |

Buckhead – Population 64,000 – Average Household Income $73,257 – 14.2 Million Square Feet of Office Space – Shopping Mecca of the Southeast: 1,400 Retail Units With $1 billion in Annual Sales – 5,000 Hotel Rooms – Robb Report Rated Buckhead One of USA’s “Top Affluent Communities” – Vehicle Traffic Count 50,000 per day Peachtree Corners (Norcross) – Population 35,145 – Average Household Income $87,351 – 7.9 Million Square Feet of Office Space – Vehicle Traffic Count 40,000 per day North Fulton - Alpharetta (Proposed) – Population 199,966 – Average Household Income $103,190 – 14.8 Million Square Feet of Office Space Office Location Overview Piedmont Bank 163 |

Asset Growth Piedmont Bank $94.2 $126.6 $143.0 $191.4 $237.0 $0.0 $50.0 $100.0 $150.0 $200.0 $250.0 2002 2003 2004 2005 Sept. 30, 2006 164 |

Retail 1% Commercial Real Estate 20% Residential Construction 44% SBA 9% Commercial & Industrial 26% Portfolio Mix (Outstanding Loan Balance, Gross) Piedmont Bank 165 |

Deposit Growth Piedmont Bank $64.9 $95.7 $115.5 $155.7 $177.1 $0.0 $50.0 $100.0 $150.0 $200.0 2002 2003 2004 2005 Sept. 30, 2006 166 |

CDs < 100,000 25% DDA 11%* CDs > 100,000 28% Money Market 32% NOW 4% Deposit Mix Piedmont Bank * DDA Consists of 96% Commercial and 4% Retail 167 |

Experienced Management Team Piedmont Bank Years of Name Title Age Banking Brian D. Schmitt President / CEO 45 23 Anthony J. Mannino EVP / CFO 57 36 Mark K. Hancock EVP Lending 45 23 Joseph G. Wirtz EVP Lending 42 20 Sandra W. Fuller Chief Credit Officer 57 37 168 |

Why a Merger with PrivateBancorp? Piedmont Bank Private Understands Human Capital • 100% Employee Retention • Substantially all Directors will continue to serve on Board • Independent Georgia Bank Charter Model of Private Banking • Small Enough to Provide Speed and Flexibility to the Client but yet Large Enough to Handle Their Needs • Wealth Management Unit Provides Long-Term Financial Solutions • Provide Additional Resources to Service Existing Clients Management of Private • Proven Long-Term Success, Leadership 169 |

PrivateBancorp, Inc. Dennis L. Klaeser Chief Financial Officer and Managing Director 170 |

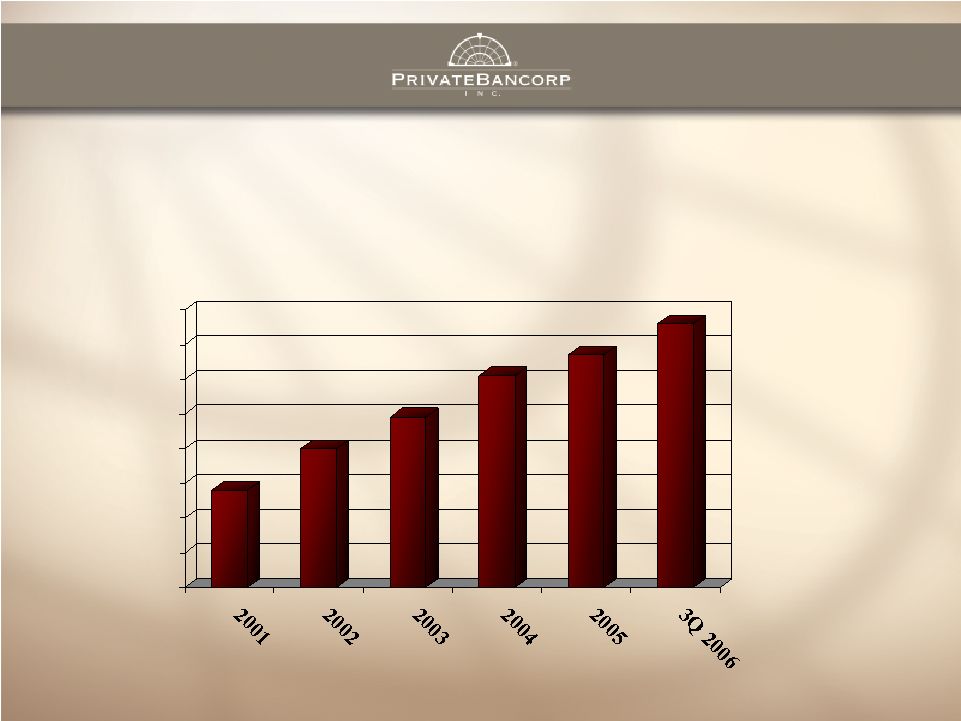

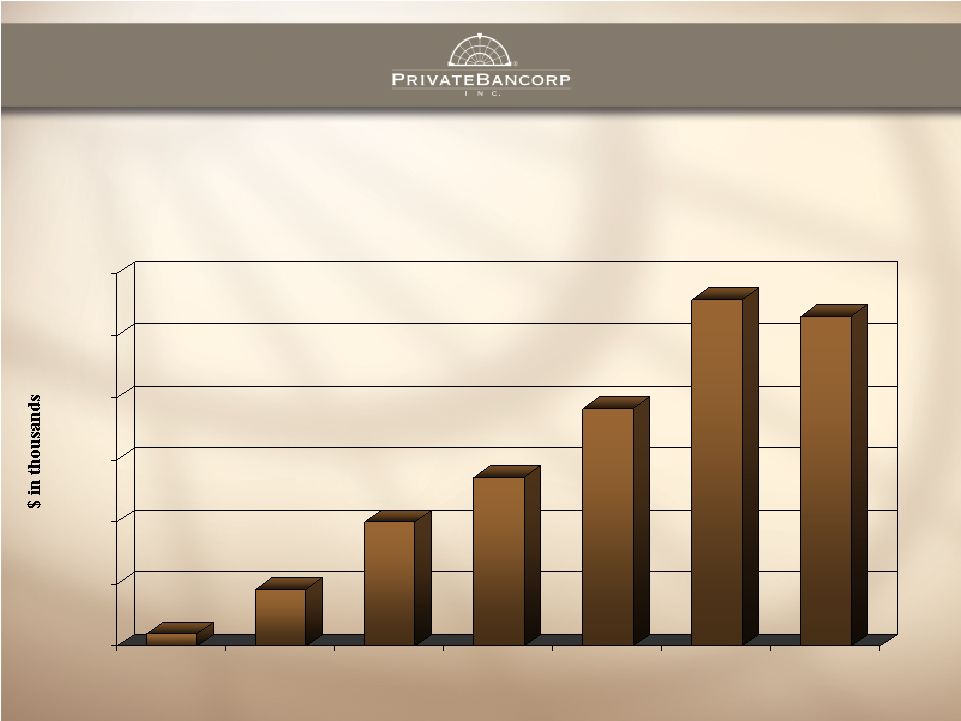

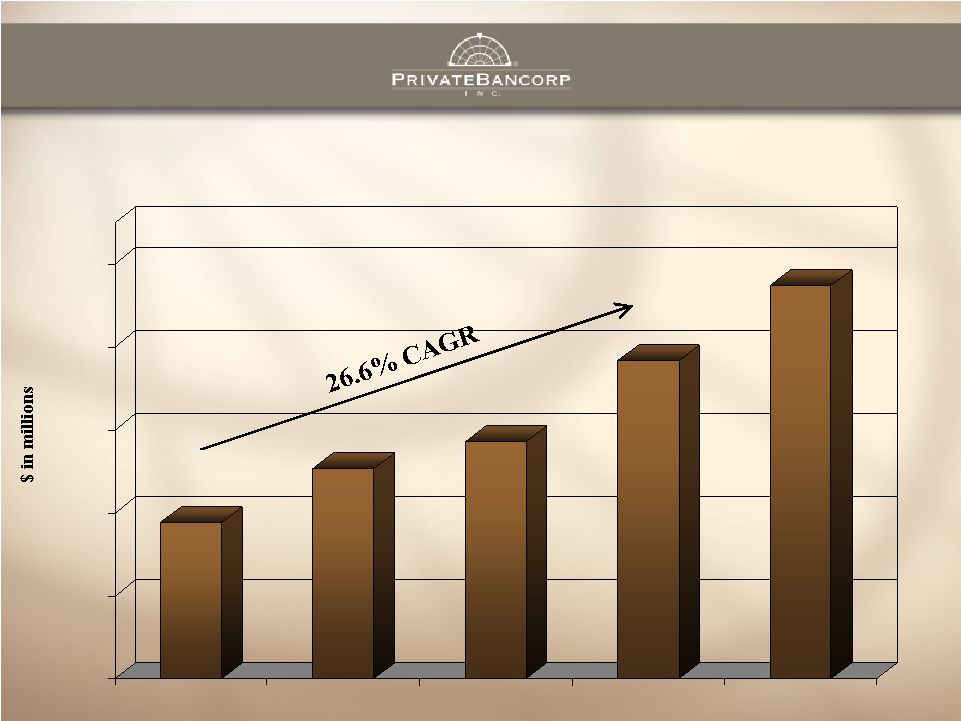

Results: Franchise Growth $519 $730 $830 $778 $1,178 $723 $1,545 $1,240 $1,987 $1,495 $2,539 $1,727 $3,497 $2,437 $3,877 $2,780 $0 $500 $1,000 $1,500 $2,000 $2,500 $3,000 $3,500 $4,000 1999 2000 2001 2002 2003 2004 2005 3Q 2006 Assets Wealth Management AUM Trust Preferred Offering $40M Trust Preferred Offering $50M 2 Common Stock Offering $57M Trust Preferred Offering $20M IPO $17M Bank Assets and Wealth Management Assets Under Management 171 nd |

Loan and Core Deposit Growth $781 $966 $1,225 $1,653 $2,608 $3,137 $0 $500 $1,000 $1,500 $2,000 $2,500 $3,000 $3,500 2001 2002 2003 2004 2005 3Q 2006 Total Loans Loans have a 31% Organic Compounded Annual Growth Rate from 2001-2005 Loans have increased by 30% LTM $712 $925 $1,099 $1,449 $2,237 $2,518 $0 $500 $1,000 $1,500 $2,000 $2,500 $3,000 2001 2002 2003 2004 2005 3Q 2006 Total Core Deposits (Excluding Brokered Deposits) Deposits (Excluding Brokered Deposits) have a 29% Organic Compounded Annual Growth Rate from 2001-2005 Core deposits have increased by 23% LTM 172 |

Execution: Human Capital 0 2,000 4,000 6,000 8,000 10,000 Assets per Employee PVTB Peer 0 20 40 60 80 100 Net Income per Employee PVTB Peer Note: Peer data is averaged and includes banks between $1.5B-$5.0B in Assets per SNL Datasource *PVTB Assets per Employee and Net Income per Employee declined as a result of The PrivateBank – Michigan acquisition in June 2005 **PVTB 3Q 2006 Net Income metric annualized 173 |

Execution: Human Capital 0 200 400 600 800 1,000 Full Time Employees PVTB Peer Peer results are indexed to PVTB 0.00% 0.50% 1.00% 1.50% 2.00% Salaries and Benefits as a percentage of Total Assets PVTB Peer Note: Peer data is averaged and includes banks between $1.5B-$5.0B in Assets per SNL Datasource **PVTB 3Q 2006 Net Income metric annualized 174 |

Capital Ratios at 9-30-06 5.00% 7.26% 6.00% 8.65% 10.00% 10.71% 0.00% 2.00% 4.00% 6.00% 8.00% 10.00% 12.00% Leverage Tier 1 Risk- based Total Risk- based FDIC Required to be Well- Capitalized Actual 175 |

Revenue and Operating Expense Growth $29,321 $3,151 $17,159 $35,200 $1,638 $19,396 $615 $0 $5,000 $10,000 $15,000 $20,000 $25,000 $30,000 $35,000 $40,000 3Q05 Revenue 3Q05 Operating Expense 3Q06 Revenue 3Q06 Operating Expense Moving Expense Operating Expenses Securities Revenue All other Revenue $20,011 $36,838 $32,472 •Revenue from our core business (revenue excluding securities revenue) has grown by 20% year over year. (Assumes securities for both periods are funded at the cost of brokered deposits) •Operating expenses have grown by 13%, excluding the 3Q06 cost of the headquarters move. 176 |

Results: Profitability $0.38 $0.68 $0.99 $1.22 $1.46 $1.07 $1.34 $0.00 $0.20 $0.40 $0.60 $0.80 $1.00 $1.20 $1.40 $1.60 $1.80 Adjusted to reflect the 2-for-1 split of our common stock effective May 31, 2004 177 |

PrivateBancorp, Inc. Ralph B. Mandell Ralph B. Mandell Chairman of the Board, Chairman of the Board, President and President and Chief Executive Officer Chief Executive Officer 178 |

Strategic Objectives Client Focus Objective PrivateBanking Expand PrivateBank footprint to other dynamic markets that meet our demographic criteria •Either de novo or acquisition Wealth Management Develop Wealth Management through acquisition or organic growth • Investment Advisory • Asset Management • Financial & Tax Planning • Trust Services Support in-market growth by expansion of Managing Director group Continue to focus on attracting a talented Managing Director group, as they distinguish us from other organizations 179 |

Key Investment Considerations Proven Management Team Leading Experienced Managing Directors Strategy • Exclusive PrivateBanking Focus • Targeted Market • Unique Staffing Model (Managing Directors) • Meet and Exceed Client Expectations 180 |

Key Investment Considerations Results • Historic Strong Asset Growth • High Credit Quality • Trend of Strong Core Deposit Growth • Developing Wealth Management Franchise • Increasingly Profitable • Poised for Future Growth 181 |

182 |