Canaccord Genuity Growth Conference August 16, 2012 © Exa Corporation. All rights reserved. Exhibit 99.1 |

Safe Harbor Statement © Exa Corporation. All rights reserved. 2 Today’s presentation includes forward-looking statements intended to qualify for the Safe Harbor from liability established by the Private Securities Litigation Reform Act of 1995.These forward-looking statements, including statements regarding our financial expectations, demand for our solutions and growth in our markets, are subject to risks, uncertainties and other factors that could cause actual results to differ materially from those suggested by our forward-looking statements. These factors include, but are not limited to, the risk factors described in our registration statement on Form S-1, declared effective by the SEC on June 27, 2012. Forward- looking information in this presentation represents our outlook as of today, and we do not undertake any obligation to update these forward-looking statements. During today's presentation we may refer to our Adjusted EBITDA and Adjusted Operating Income. These are non-GAAP financial measures that have been adjusted for certain non-cash and other items, and that are not computed in accordance with generally accepted accounting principles. The GAAP measure most comparable to Adjusted EBITDA is our net income (loss). The GAAP measure most comparable to Adjusted Operating Income is our operating income. Reconciliations of our historical Adjusted EBITDA to our net income (loss) and our Adjusted Operating Income to our operating income are included herein. . QUIET PERIOD: Second Quarter ended July 31, 2012 |

Initial Public Offering Summary © Exa Corporation. All rights reserved. 3 Issuer Exa Corporation Listing / Ticker NASDAQ / “EXA” Offering Size $62.8 million Shares Offered 6.28 million (4.2 million primary and 2.1 million secondary) Price $10.00 Pricing Date June 28, 2012 Use of Proceeds Working capital & general corporate purposes Lock-Up Period 180 days Bookrunner Stifel Nicolaus Weisel Co-Managers Baird, Canaccord Genuity, Needham |

Company Overview Leading Provider of Software that Enables Simulation-Driven Product Design 90+ 13 of the top 15 passenger vehicle manufacturers 200+ EBITDA positive past 3 years Highly recurring and visible business model Employees *FY 2011 – FY 2012 10 HQ in Burlington, MA Detroit, Japan, Germany, Korea, France, China 4 © Exa Corporation. All rights reserved. Aerodynamics Thermal Acoustics Revenue Growth* 21% Global Offices Vehicle Manufacturers as Customers |

Key Investment Highlights © Exa Corporation. All rights reserved. 5 Proprietary, Market Leading Technology Tangible, Immediate Value Proposition Growing Multi-billion Dollar Market Opportunity in Transportation Alone Top-tier Global Customers Highly-Visible, Consumption-based Licensing Model Experienced Management Team |

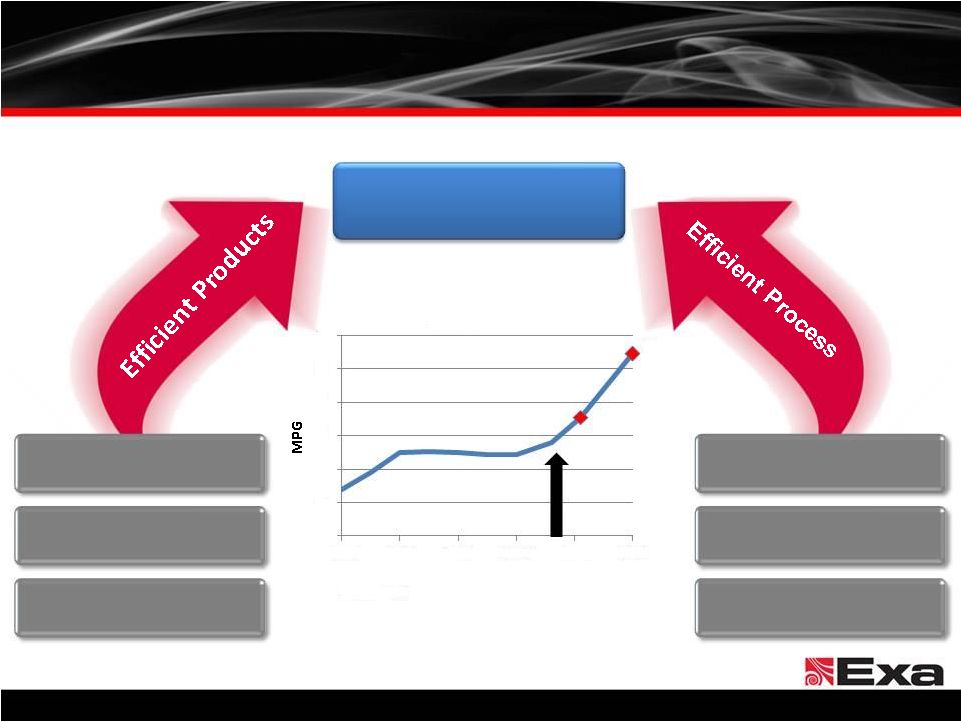

Transportation Market Requirements © Exa Corporation. All rights reserved. 6 Efficiency2 Source: EPA (1) The United States passenger car and light truck CAFE standard continues to rise to 56.2 MPG by 2025 Fewer Prototypes Increased Automation Faster Turnaround Time Simulation-based Simulation-based Design Design Aerodynamics Weight Reduction New Powertrains 0 10 20 30 40 50 60 1975 1985 1995 2005 2015 2025 U.S. CAFE (1) |

Traditional Development Process © Exa Corporation. All rights reserved. 7 Months Expensive ($bn), cumbersome & time-consuming Brute-force approach Design, Redesign Build/Rebuild Physical Prototype Test in Windtunnel, Analyze Results |

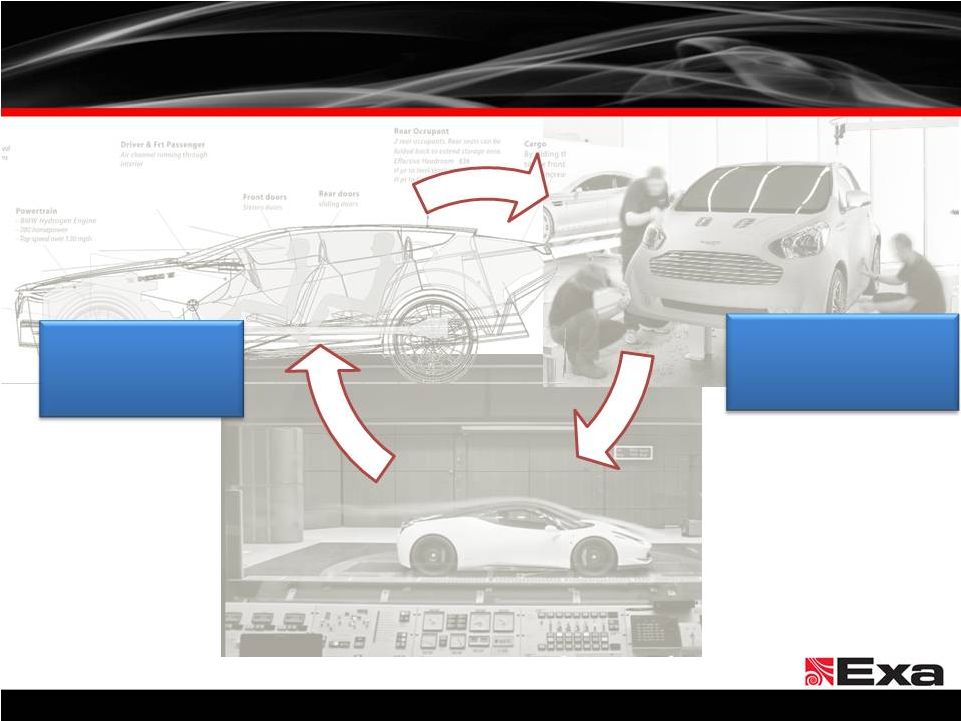

Exa‘s Vehicle Development Process 8 Proprietary Algorithms Geometric Complexity Accurate Results © Exa Corporation. All rights reserved. Days |

Global Customer Base © Exa Corporation. All rights reserved. 9 Passenger Vehicle Truck & Off-Highway Supplier/Other Aerospace |

The Problem Reduce joint fleet CO2 to meet global emissions target by 2020+ Portfolio Diversification Reduce cost of prototypes Enable digital sign-off 10 © Exa Corporation. All rights reserved. The Results Thermal Mgmt & Aerodynamic prototypes eliminated prior to production tooling release Further elimination opportunities for Aeroacoustics & water mgmt in development How JLR Uses Exa’s PowerFLOW |

Customer Engagement Model © Exa Corporation. All rights reserved. 11 Annual Renewals Deeper Deployment Upgrades New Applications Capacity-Based Licensing OnDemand or On Premise |

PowerFLOW Product Suite Simulation Preparation (User-based License) Simulation PowerDELTA ® Import, sort and organize CAD model Apply parametric mesh features Generate surface meshes & check quality PowerFLOW ® Automatic fluid discretization Automatic multi-processor parallelized simulation ~80% of license revenue PowerINSIGHT ™ Streamline & automate the results generation, analysis, and reporting process PowerVIZ ® Analyze results and flow structures with interactive 3D data visualization, movies, & graphs PowerTHERM ® Fully-coupled 3D conduction & radiation solver PowerCOOL ® Fully-coupled cooling system model PowerCASE ™ Set up simulation case parameters & boundary conditions PowerCLAY ® Morph mesh real-time for rapid design iteration & optimization PowerACOUSTICS ® Analyze and predict acoustic noise transmission to the interior Design Iterations Simulation Analysis (User-based License) (Consumption-based License) 12 © Exa Corporation. All rights reserved. |

© Exa Corporation. All rights reserved. 13 Why We Win Differentiated Go-to-market Strategy Return on Investment Deep Domain Expertise Faster Turnaround Time Highest Degree of Simulation Accuracy |

Customer Case Studies 14 © Exa Corporation. All rights reserved. The Problem Demand for more fuel efficient trucks Top buying requirement The Results 24% reduction in aerodynamic drag 12% improvement in fuel economy ~$5,600 annual fuel savings per vehicle |

Customer Case Studies © Exa Corporation. All rights reserved. 15 The Problem Mandatory 90% reduction in nitrous oxides for heavy vehicles The Results Saved product costs by minimizing design changes Reduced number of physical test stages from twenty per vehicle design to three Saved millions of dollars in prototype testing costs Migrated from physical test processes requiring more than 60 days to a digital test process requiring 6 days per iteration |

Growth Strategy © Exa Corporation. All rights reserved. 16 • Migrating from physical to digital- based approaches • Identify new applications to address customer needs • Significantly underpenetrated • Adjacent markets • Expanding presence in BRIC • Core technology is extendable to Aerospace, Oil & Gas and Power Generation among others • Complementary businesses & technologies Deepen Existing Customer Base Enable Additional Applications & Solutions Add New Customers in Ground Transportation Penetrate New Geographies Explore New Verticals Selectively Pursue Acquisitions |

Ed Furlong Chief Financial Officer © Exa Corporation. All rights reserved. |

Key Financial Highlights © Exa Corporation. All rights reserved. 18 Strong, Consistent Revenue Growth Recurring & Predictable Business Model Profitable & Cash Flow Positive Attractive Long-term Model |

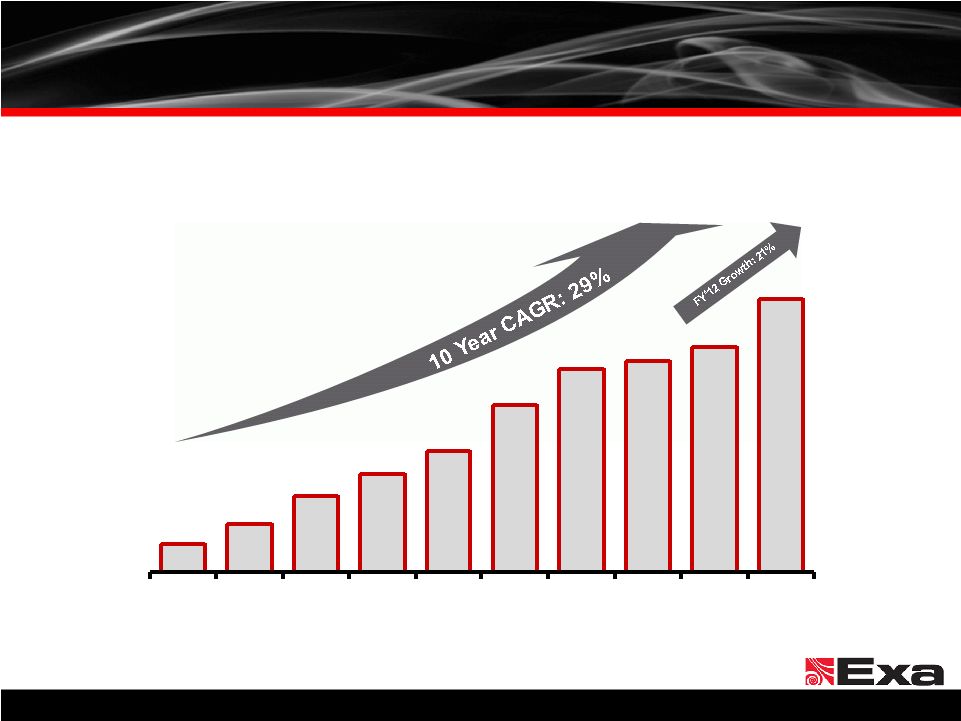

Consistent Revenue Growth © Exa Corporation. All rights reserved. 19 $4.6 $8.0 $12.8 $16.3 $20.3 $28.0 $34.1 $35.6 $37.9 $45.9 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 Revenue $MM (FYE Jan 31) Note: We changed from a December 31 calendar year-end to a January 31st fiscal year-end at the end of December 2006. |

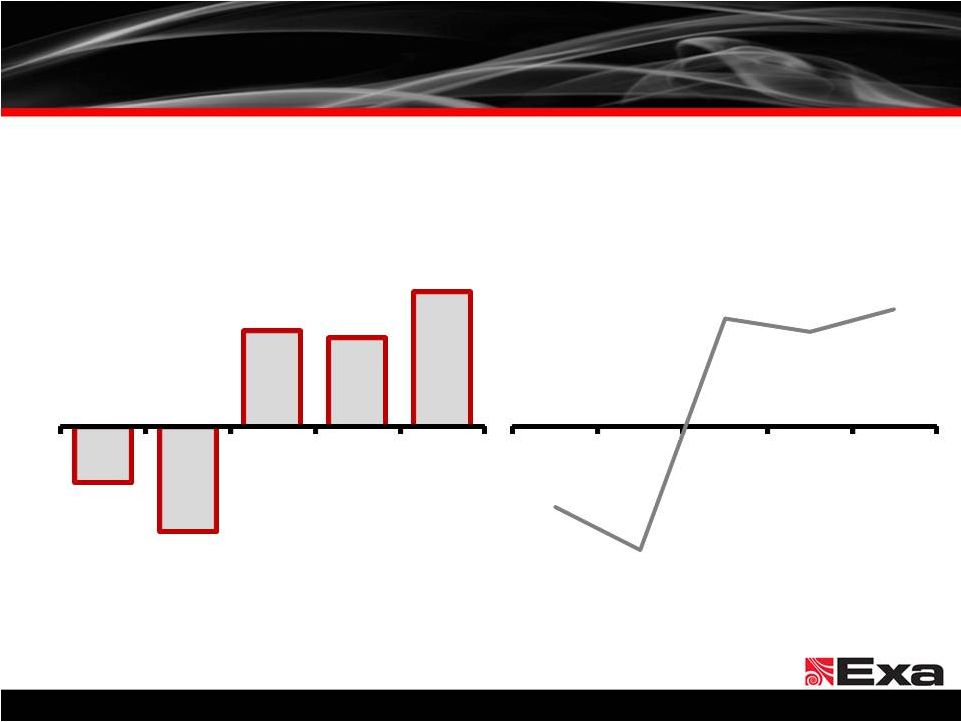

Note: Please see Appendix for detailed definition and reconciliation of Adjusted EBITDA to the comparable GAAP financial measure of net income (loss). We define EBITDA as net income (loss), excluding depreciation and amortization, interest expense, other income (expense), foreign exchange gain (loss) and provision for income taxes. We define Adjusted EBITDA as EBITDA, excluding non-cash share-based compensation expense. Increasing EBITDA 20 © Exa Corporation. All rights reserved. $(3.0) $(5.5) $5.0 $4.7 $7.1 2008 2009 2010 2011 2012 Adjusted EBITDA $MM (FY E Jan 31) (10.6%) (16.2%) 14.2% 12.3% 15.4% 2008 2009 2010 2011 2012 Adjusted EBITDA Margin (FYE Jan 31) |

Renewals on base capacity Renewals including upgrades and expanded capacity 100% 60%+ of our annual revenue was attributable to contracts in place at the beginning of the fiscal year We expect our annual license revenue renewal rate with capacity expansion to remain over 100% We expect to maintain a license revenue renewal rate in the range of 85% to 100% 21 © Exa Corporation. All rights reserved. Highly Recurring & Predictable Model 97% 87% 80% 91% 97% 140% 116% 95% 113% 123% 2008 2009 2010 2011 2012 License Renewal Rate (FY E Jan 31) Note: We compute our license revenue renewal rate for any fiscal year by identifying the customers from whom we derived license revenue in the prior fiscal year and dividing the dollar amount of license revenue that we receive in the current fiscal year from those customers by the dollar amount of license revenue we received from them in the prior fiscal year. |

64% 100% 12% 4% 20% Revenue Visibility (FY E Jan 31) Renewals New Licenses Projects New & Renewal Licenses at Beginning of Year Annual consumption-based licenses Increased consumption of simulation capacity drives growth Delivered on-premise or on-demand Ratable revenue recognition Project revenue is primarily derived from simulation capacity 10 – 15% of project revenue is in deferred revenue at beginning of year 22 © Exa Corporation. All rights reserved. Revenue Detail Note: Revenue visibility percentages are management estimates for fiscal year 2013. |

United States Japan Korea France Germany United Kingdom Sweden Other © Exa Corporation. All rights reserved. 23 License Revenue Project Revenue Revenue Mix 84% 16% License versus Project Revenue 23% 22% 8% 19% 13% 6% 5% 4% Revenue by Geography Note: Data as of FY 2012 |

Managing business with focus on revenue growth with steady improvement in Adjusted EBITDA margin Continue to invest in Sales team to deepen customer penetration and add new customer names Improve margins due to operating leverage, especially in R&D and G&A Targeting mid twenties Adjusted EBITDA margin over time 24 © Exa Corporation. All rights reserved. Target Model |

Appendix © Exa Corporation. All rights reserved. |

© Exa Corporation. All rights reserved. 26 Revenue License $26.8 $30.6 $38.7 $10.0 Project 8.8 7.3 7.2 1.3 Total Revenue $35.6 $37.9 $45.9 $11.3 Revenue Growth 4.4% 6.4% 21.1% 10.2% Operating Expenses Cost of Revenues 9.9 9.9 12.0 3.2 Sales & Marketing 5.2 6.0 6.1 1.6 Research & Development 12.5 12.6 14.2 4.1 General & Administrative 5.6 6.3 7.9 1.9 Adj. Operating Income $2.3 $3.1 $5.7 $0.5 Adj. EBITDA $5.0 $4.7 $7.1 $1.0 FY 2011 FY 2012 Q1 FY13 Key Financial Metrics FY 2010 Adj. excludes non-cash, share-based compensation expense of $1.406, $0.281, $0.636, and $0.241 for FY2010, FY2011, FY2012, and Q1 FY2013 respectively. Please see next slide for detailed definition and reconciliation of Adjusted EBITDA to the comparable GAAP financial measure of net income (loss). |

Adjusted EBITDA – Definition and Reconciliation 27 © Exa Corporation. All rights reserved. Exa Corporation Adjusted EBITDA Reconciliation (In thousands) Three Months Ended Year Ended January 31, April 30, 2008 2009 2010 Restated 2011 Restated 2012 2011 Restated 2012 Net (loss) Income $ (7,514) $ (9,846) $ (1,013) $ 395 $ 14,456 238 $ Depreciation and amortization 2,043 2,853 2,702 1,562 1,405 323 460 Interest expense, net 1,430 1,218 672 1,411 1,284 270 412 Other (income) expense (15) 71 (12) (10) 213 (66) (66) Foreign exchange loss (gain) 560 (549) 766 198 106 464 0 Provision for income tax 419 441 521 839 (11,040) 390 (84) EBITDA (3,077) (5,812) 3,636 4,395 6,424 1,619 733 Non-cash, share based compensation expense 113 291 1,406 281 636 33 241 Adjusted EBITDA $ (2,964) $ (5,521) $ 5,042 $ 4,676 $ 7,060 $ 1,652 $ 974 $ 11 Note: To supplement our consolidated financial statements, which are presented on a GAAP basis, we disclose Adjusted EBITDA, a non-GAAP measure that excludes certain amounts. This non-GAAP measure is not in accordance with, or an alternative for, generally accepted accounting principles in the United States. The GAAP measure most comparable to Adjusted EBITDA is GAAP net income (loss). A reconciliation of this non-GAAP financial measure to the corresponding GAAP measure is included above. We define EBITDA as net income (loss), excluding depreciation and amortization, interest expense, and other income (expense), foreign exchange gain (loss) and provision for income taxes. We define Adjusted EBITDA as EBITDA, excluding non-cash share-based compensation expense. Our management uses this non-GAAP measure when evaluating our operating performance and for internal planning and forecasting purposes. We believe that this measure helps indicate underlying trends in our business, is important in comparing current results with prior period results, and is useful to investors and financial analysts in assessing our operating performance. For example, management considers Adjusted EBITDA to be an important indicator of our operational strength and the performance of our business and a good measure of our historical operating trends. However, Adjusted EBITDA may have limitations as an analytical tool. The non-GAAP financial information presented here should be considered in conjunction with, and not as a substitute for or superior to, the financial information presented in accordance with GAAP and should not be considered a measure of our liquidity. There are significant limitations associated with the use of non-GAAP financial measures. Further, these measures may differ from the non-GAAP information, even where similarly titled, used by other companies and therefore should not be used to compare our performance to that of other companies. In considering our Adjusted EBITDA, investors should take into account the above reconciliation of this non-GAAP financial measure to the comparable GAAP financial measure of net income (loss) that is presented in this “Summary Consolidated Financial Information” in our registration statement on Form S-1 filed with the SEC. |

Ground Transportation Applications 28 © Exa Corporation. All rights reserved. |