Exhibit 99.1

|

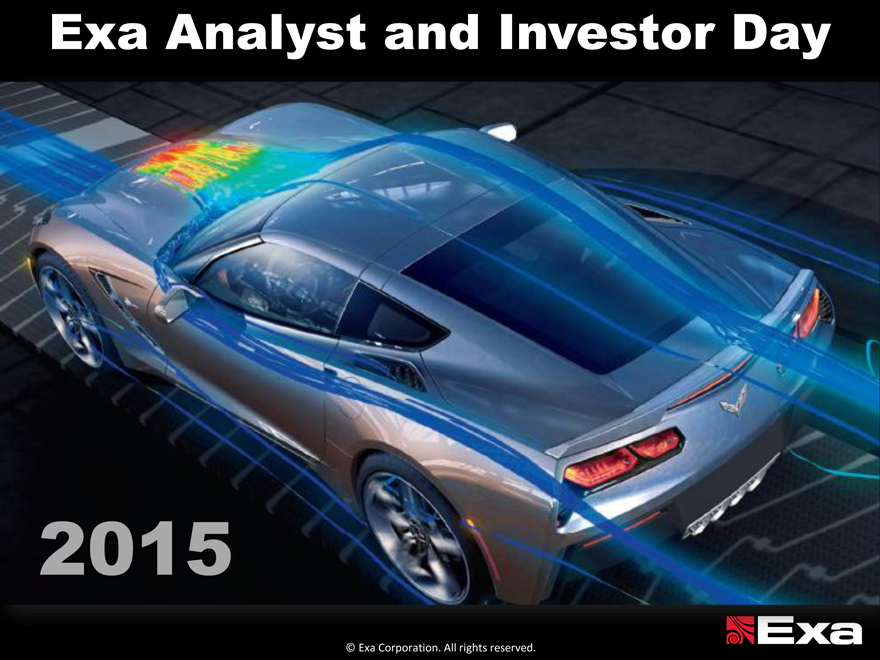

Exa Analyst and Investor Day

2015

© Exa Corporation. All rights reserved.

|

OUR MISSION

Enabling better products through simulation driven design

© Exa Corporation. All rights reserved.

|

© Exa Corporation. All rights reserved.

|

© Exa Corporation. All rights reserved.

|

© Exa Corporation. All rights reserved.

|

© Exa Corporation. All rights reserved.

|

© Exa Corporation. All rights reserved.

|

© Exa Corporation. All rights reserved.

|

© Exa Corporation. All rights reserved.

|

© Exa Corporation. All rights reserved.

|

© Exa Corporation. All rights reserved.

|

Simulate, optimize and move to production with confidence

© Exa Corporation. All rights reserved.

|

Agenda

12:30 1:30 Registration, Lunch, Product Demonstrations

1:30 2:20 Welcome and Market Opportunity, Steve Remondi, CEO

Company Mission and Execution

Addressable Market Opportunity

Exa Deployment and Penetration

2:20 2:40 Customer Perspective: Jaguar Land Rover

Mark Stanton, JLR Director of Vehicle Engineering (via video)

Jean-Paul Roux, Exa SVP European Operations

2:40 3:00 Product Strategy Customer Alignment, Steve Remondi, CEO

Applications and Automation

Cloud Enabling Quick Adoption and Collaboration

3:00 3:30 Break

3:30 4:15 Financial Update, Rick Gilbody, CFO

The Path to Profitability and Continued Revenue Growth

Guidance FY 16 and FY 17

Target Model

4:15 5:00 Q & A

13 © Exa Corporation. All rights reserved.

|

Safe Harbor Statement

Today’s presentation includes forward-looking statements intended to qualify for the Safe Harbor from liability established by the Private Securities Litigation Reform Act of 1995. These forward-looking statements, including statements regarding our financial expectations, demand for our solutions and growth in our markets, are subject to risks, uncertainties and other factors that could cause actual results to differ materially from those suggested by our forward-looking statements. These factors include, but are not limited to, the risk factors described in our Annual Report on Form 10-K for the year ended January 31, 2015, as filed with the SEC on March 24, 2015. Forward-looking information in this presentation represents our outlook as of today, and we do not undertake any obligation to update these forward-looking statements.

During today’s presentation we may refer to our Adjusted EBITDA and non-GAAP operating income. These are non-GAAP financial measures that have been adjusted for certain non-cash and other items, and that is not computed in accordance with generally accepted accounting principles. The GAAP measure most comparable to Adjusted EBITDA is our net income (loss). The GAAP measure most comparable to non-GAAP operating income is operating income (loss). A reconciliation of these non-GAAP measures to their most comparable GAAP measures is included in the Appendix of this presentation.

We will also refer to revenue and total operating expenses on a constant currency basis (as well as measures derived from revenue and total operating expenses on a constant currency basis), which we define as GAAP revenue or operating expenses, adjusted to reverse the impact of changes in the exchange rates of the principal currencies in which our international operations generated revenue and incurred expenses. We calculate revenue and total expenses on a constant currency basis by converting revenue or operating expenses that were generated in foreign currencies to United States dollars at assumed exchange rates equal to the exchange rates in effect for such currencies during the corresponding period of the previous year, rather than the exchange rates actually in effect during the fiscal year of the period in question.

14 © Exa Corporation. All rights reserved.

|

Agenda

12:30 1:30 Registration, Lunch, Product Demonstrations

2:20 2:40 Customer Perspective: Jaguar Land Rover

Mark Stanton, JLR Director of Vehicle Engineering (via video)

Jean-Paul Roux, Exa SVP European Operations

2:40 3:00 Product Strategy Customer Alignment, Steve Remondi, CEO

Applications and Automation

Cloud Enabling Quick Adoption and Collaboration

3:00 3:30 Break

3:30 4:15 Financial Update, Rick Gilbody, CFO

The Path to Profitability and Continued Revenue Growth

Guidance FY 16 and FY 17

Target Model

4:15 5:00 Q & A

15 © Exa Corporation. All rights reserved.

|

Key Messages

Large addressable market … Proven technology and

only fractionally penetrated solutions

Strong and consistent Path to profitability and

execution continued top line growth

© Exa Corporation. All rights reserved.

|

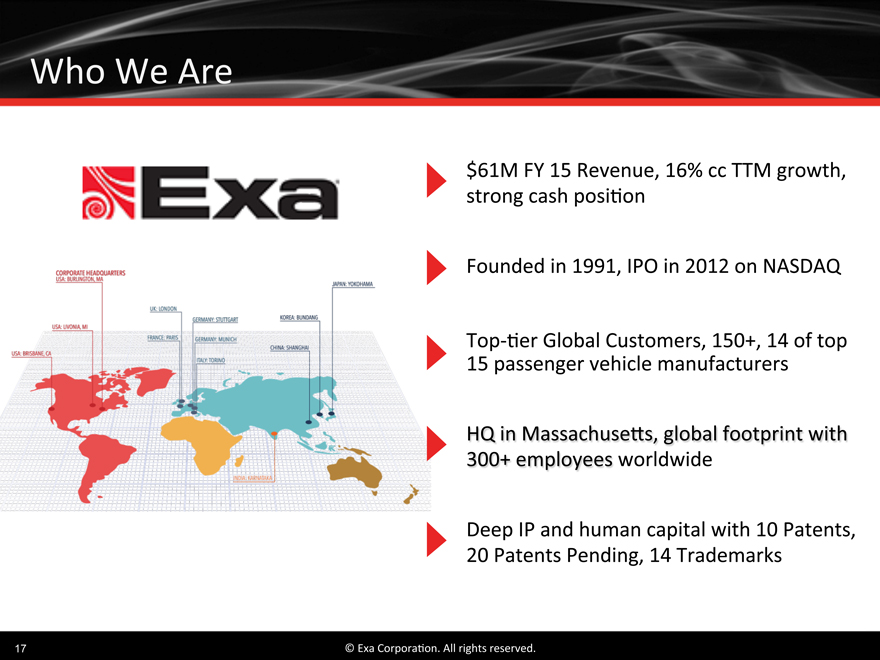

Who We Are

$61M in Revenue, 16% cc TTM growth, strong cash position

Founded in 1991, IPO in 2012 on NASDAQ

Top-tier Global Customers, 150+, 14 of top 15 passenger vehicle manufacturers

HQ in Massachusetts, global footprint with

300+ employees worldwide

Deep IP and human capital with 10 Patents,

20 Patents Pending, 14 Trademarks

17 © Exa Corporation. All rights reserved.

|

What We Deliver

Proprietary, Market Leading Simulation Technology

Tangible, Immediate Value Proposition

Vertical Applications in Ground Transportation and Aerospace

Highly-Visible, Consumption-Based Licensing Model

Consistent Revenue Growth, Accelerating Margins

18 © Exa Corporation. All rights reserved.

|

Global Customer Base

Passenger Vehicle Truck & Off-Highway Supplier/Other

Aerospace

© Exa Corporation. All rights reserved.

|

Key Messages

Large addressable market … Proven technology and

only fractionally penetrated solutions

Macro Market Trends Addressable Market Deployment Status

© Exa Corporation. All rights reserved.

|

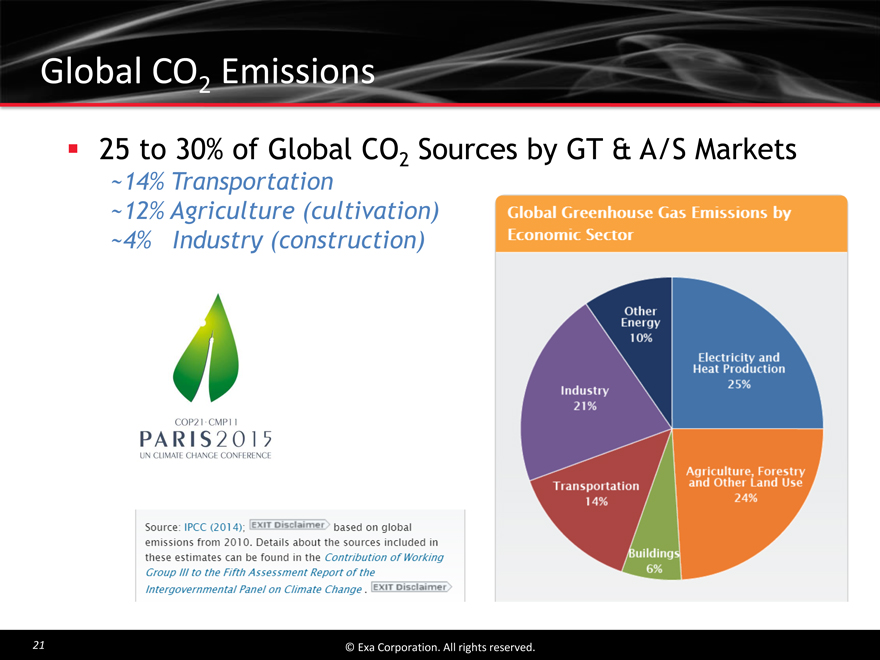

Global CO2 Emissions

25 to 30% of Global CO2 Sources by GT & A/S Markets

~14% Transportation

~12% Agriculture (cultivation) ~4% Industry (construction)

21 © Exa Corporation. All rights reserved.

|

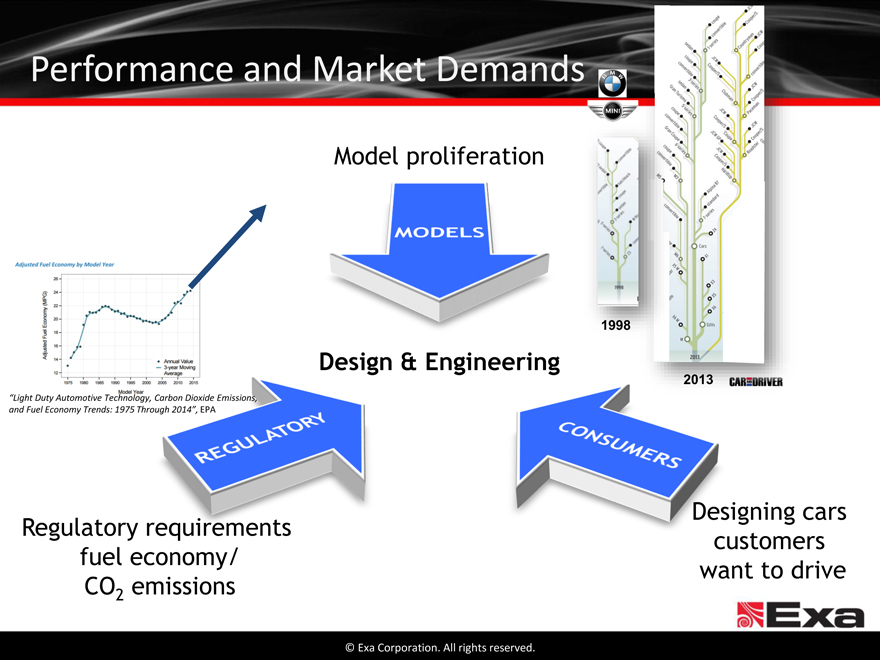

Performance and Market Demands

Model proliferation

1998

Design & Engineering

2013

“Light Duty Automotive Technology, Carbon Dioxide Emissions, and Fuel Economy Trends: 1975 Through 2014”, EPA

Designing cars

Regulatory requirements customers

fuel economy/ want to drive

CO2 emissions

© Exa Corporation. All rights reserved.

|

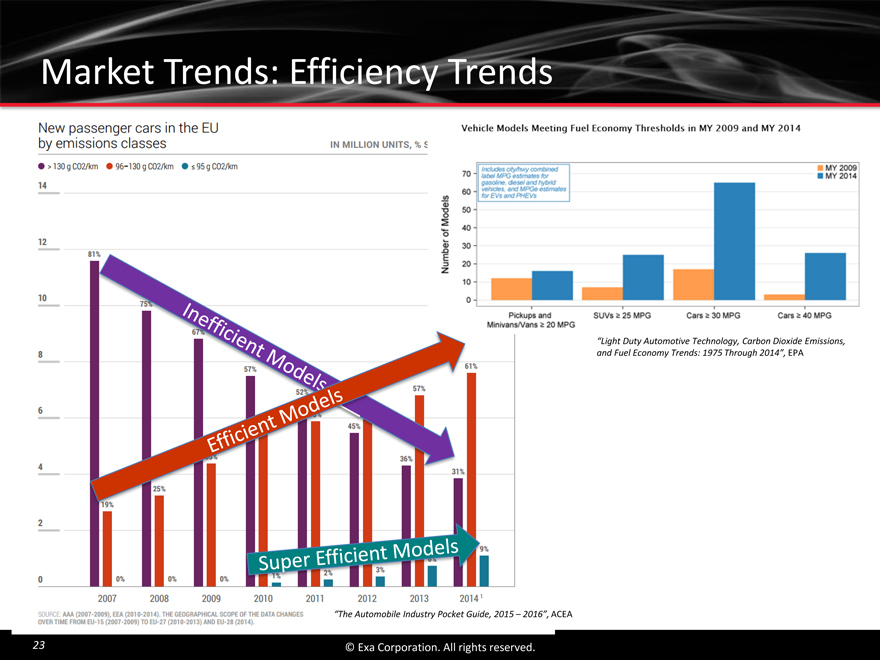

Market Trends: Efficiency Trends

“Light Duty Automotive Technology, Carbon Dioxide Emissions, and Fuel Economy Trends: 1975 Through 2014”, EPA

“The Automobile Industry Pocket Guide, 2015 2016”, ACEA

23 © Exa Corporation. All rights reserved.

|

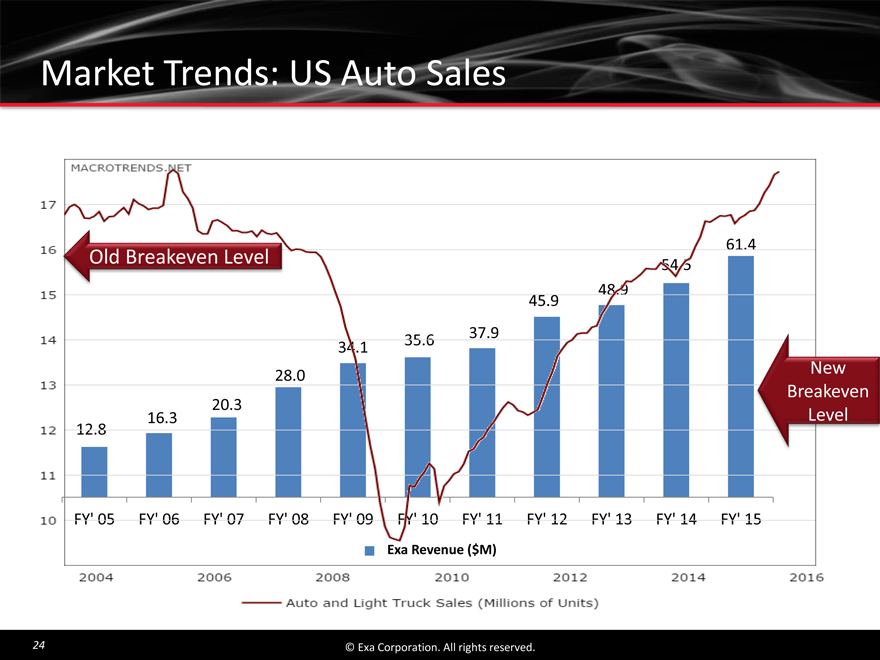

Market Trends: US Auto Sales

Old Breakeven Level

New Breakeven Level

24 © Exa Corporation. All rights reserved.

|

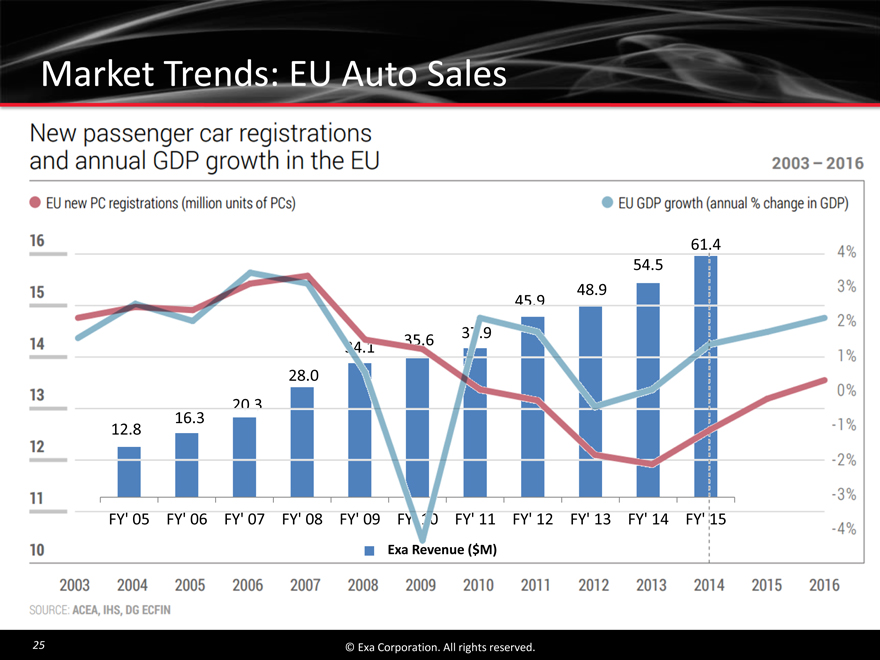

Market Trends: EU Auto Sales

© Exa Corporation. All rights reserved.

25

|

Market Trends: EU Auto Sales

26 © Exa Corporation. All rights reserved.

|

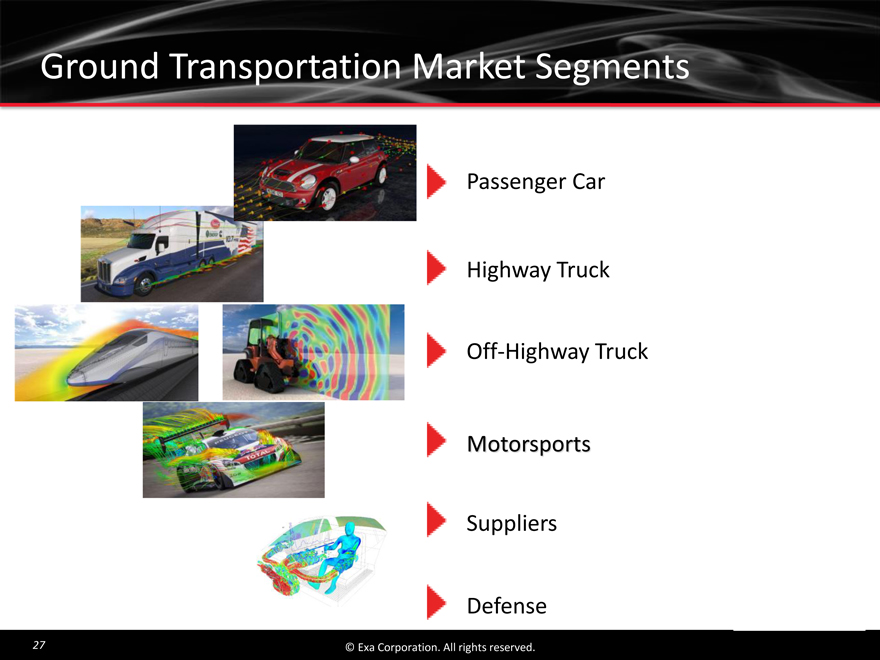

Ground Transportation Market Segments

Passenger Car

Highway Truck

Off-Highway Truck

Motorsports

Suppliers

Defense

27 © Exa Corporation. All rights reserved.

|

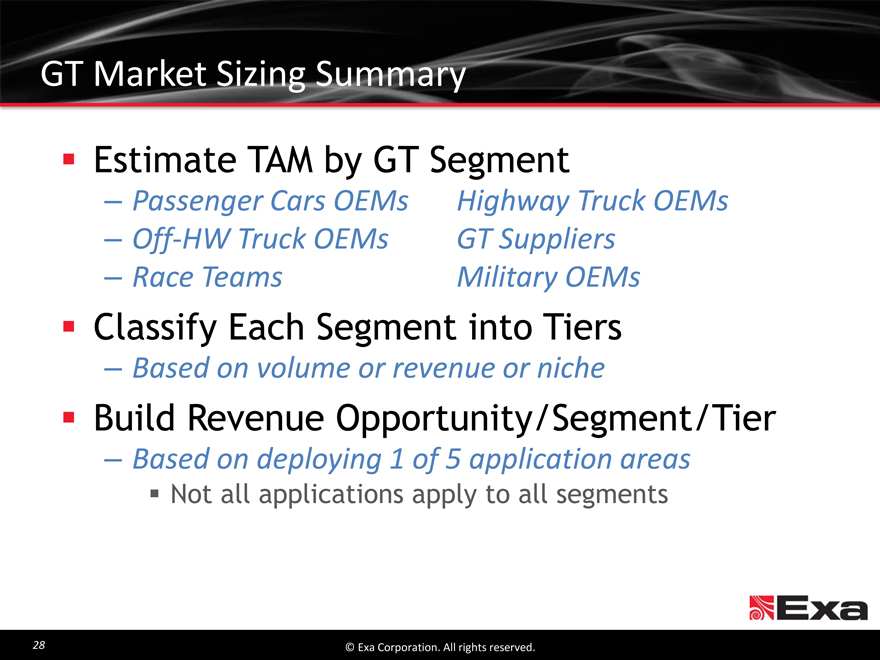

GT Market Sizing Summary

Estimate TAM by GT Segment

Passenger Cars OEMs Highway Truck OEMs

Off-HW Truck OEMs GT Suppliers

Race Teams Military OEMs

Classify Each Segment into Tiers

Based on volume or revenue or niche

Build Revenue Opportunity/Segment/Tier

Based on deploying 1 of 5 application areas

Not all applications apply to all segments

28 © Exa Corporation. All rights reserved.

|

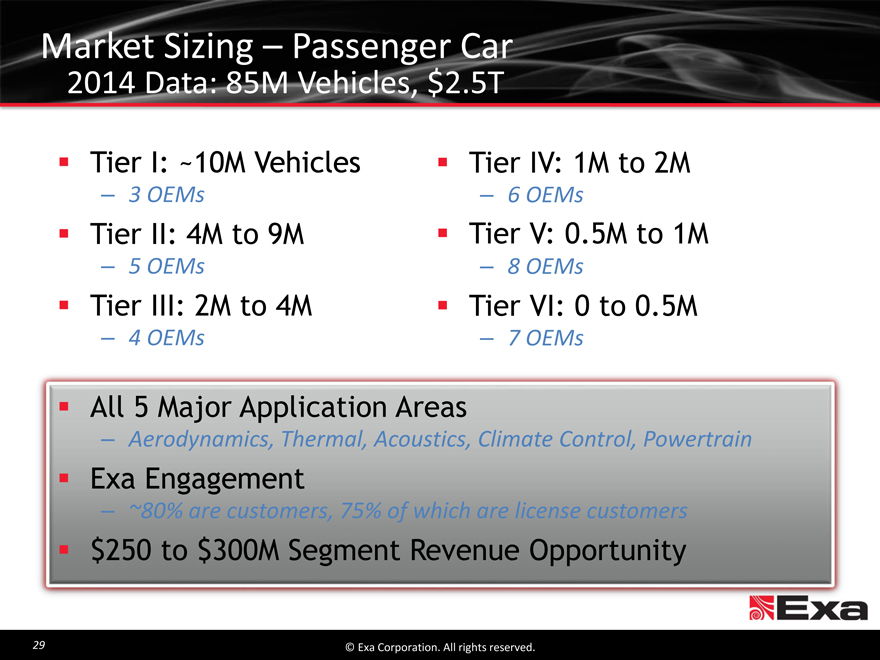

Market Sizing Passenger Car

2014 Data: 85M Vehicles, $2.5T

Tier I: ~10M Vehicles

3 OEMs

Tier II: 4M to 9M

5 OEMs

Tier III: 2M to 4M

4 OEMs

Tier IV: 1M to 2M

6 OEMs

Tier V: 0.5M to 1M

8 OEMs

Tier VI: 0 to 0.5M

7 OEMs

All 5 Major Application Areas

Aerodynamics, Thermal, Acoustics, Climate Control, Powertrain

Exa Engagement

~80% are customers, 75% of which are license customers

$250 to $300M Segment Revenue Opportunity

29 © Exa Corporation. All rights reserved.

|

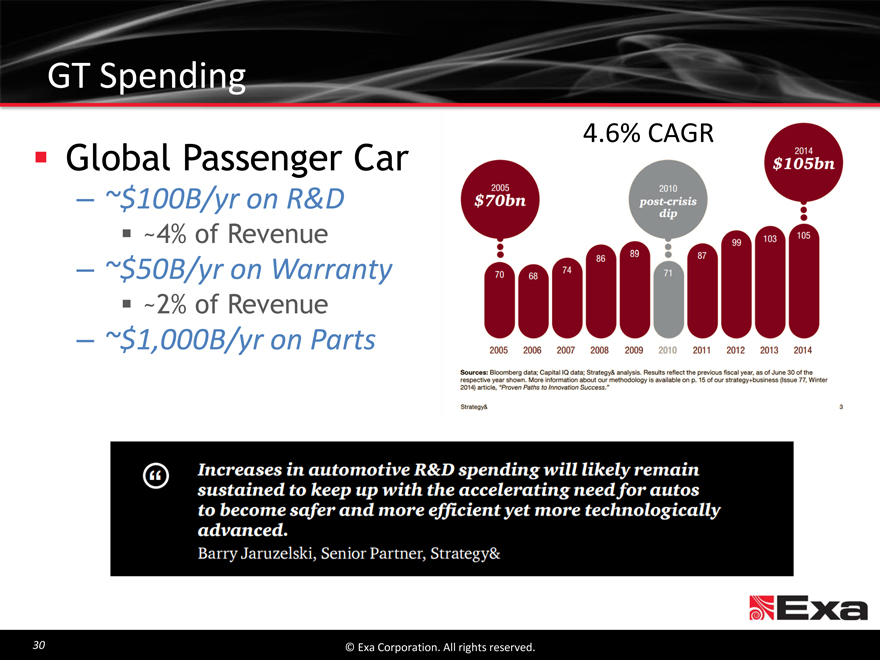

GT Spending

4.6% CAGR

Global Passenger Car

~$100B/yr on R&D

~4% of Revenue

~$50B/yr on Warranty

~2% of Revenue

~$1,000B/yr on Parts

30 © Exa Corporation. All rights reserved.

|

Value Propositions

Reduce Engineering Costs

Prototypes & mockups ($3B)

Testing sessions

Develop first vehicle right & on time

No extension beyond planned schedule (15 to 25% over-runs)

Avoid Late-Stage Problem Discovery

Tooling modifications after tooling release

Additional parts costs

Premium materials, heat shields, batteries, spoilers, underbody panels

Reduce prototype fleet for real-world testing

Improve Post-Launch Economics

Reduce warranty costs

Improve quality scores and market share

1% Point of US market = $4B in revenue and $1B in gross margin

31 © Exa Corporation. All rights reserved.

|

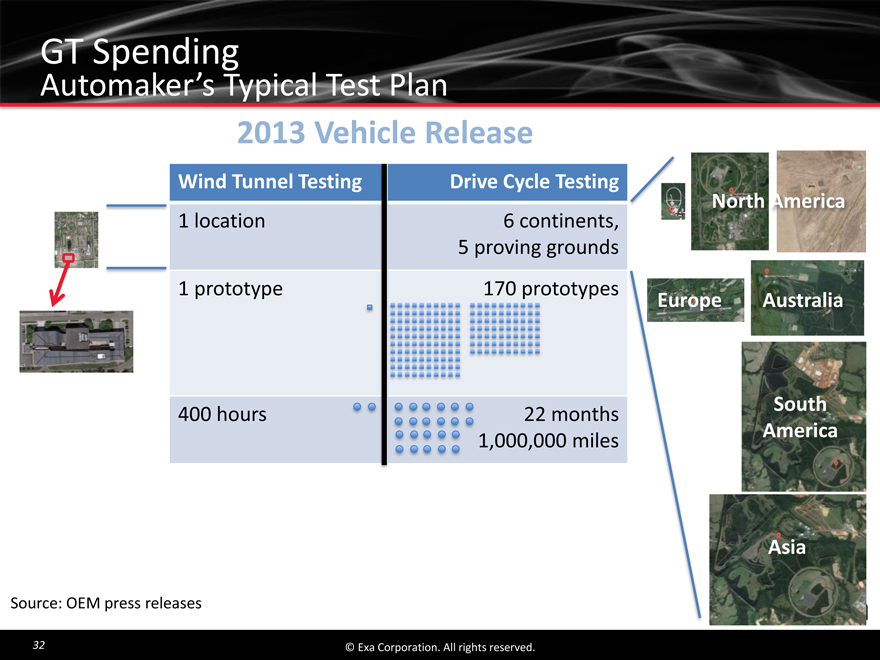

GT Spending

Automaker’s Typical Test Plan

2013 Vehicle Release

Wind Tunnel Testing Drive Cycle Testing

North America

1 location 6 continents,

5 proving grounds

1 prototype 170 prototypes Europe Australia

400 hours 22 months South

1,000,000 miles America

Asia

Source: OEM press releases

32 © Exa Corporation. All rights reserved.

|

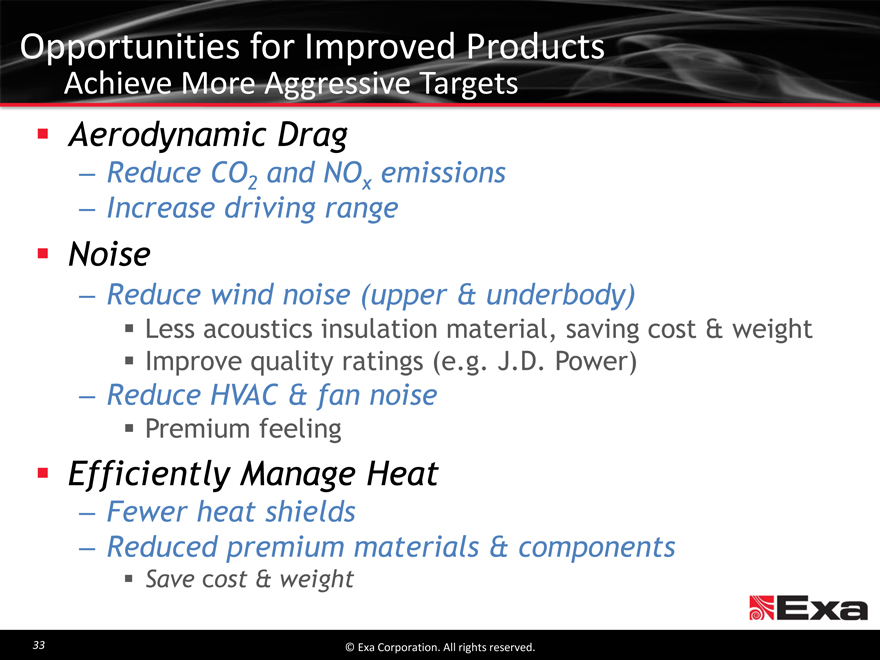

Opportunities for Improved Products

Achieve More Aggressive Targets

Aerodynamic Drag

Reduce CO2 and NOx emissions

Increase driving range

Noise

Reduce wind noise (upper & underbody)

Less acoustics insulation material, saving cost & weight Improve quality ratings (e.g. J.D. Power)

Reduce HVAC & fan noise

Premium feeling

Efficiently Manage Heat

Fewer heat shields

Reduced premium materials & components

Save cost & weight

33 © Exa Corporation. All rights reserved.

|

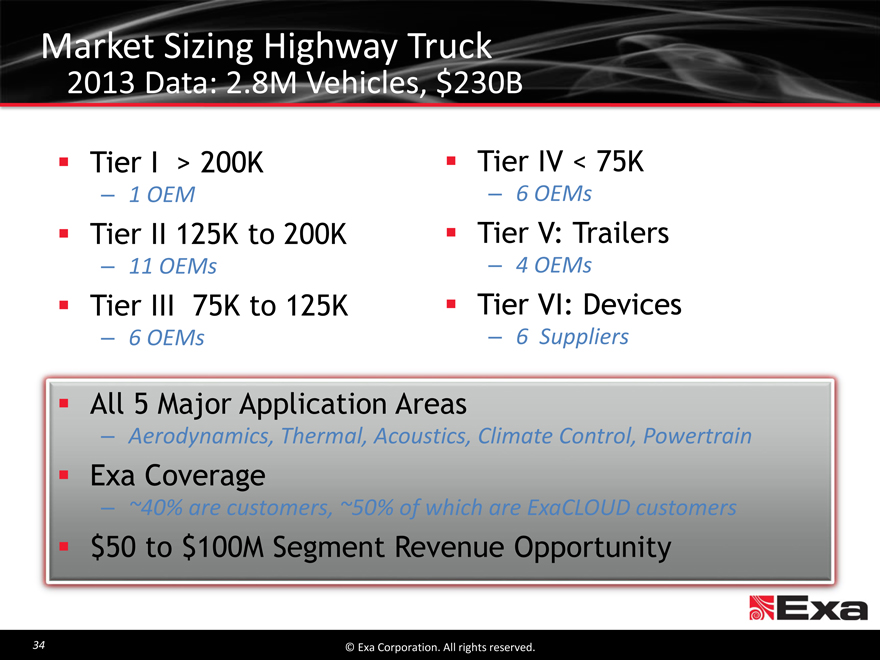

Market Sizing Highway Truck

2013 Data: 2.8M Vehicles, $230B

Tier I > 200K

1 OEM

Tier II 125K to 200K

11 OEMs

Tier IV < 75K

6 OEMs

Tier V: Trailers

4 OEMs

Tier VI: Devices

6 Suppliers

Tier III 75K to 125K

6 OEMs

All 5 Major Application Areas

Aerodynamics, Thermal, Acoustics, Climate Control, Powertrain

Exa Coverage

~40% are customers, ~50% of which are ExaCLOUD customers

$50 to $100M Segment Revenue Opportunity

34 © Exa Corporation. All rights reserved.

|

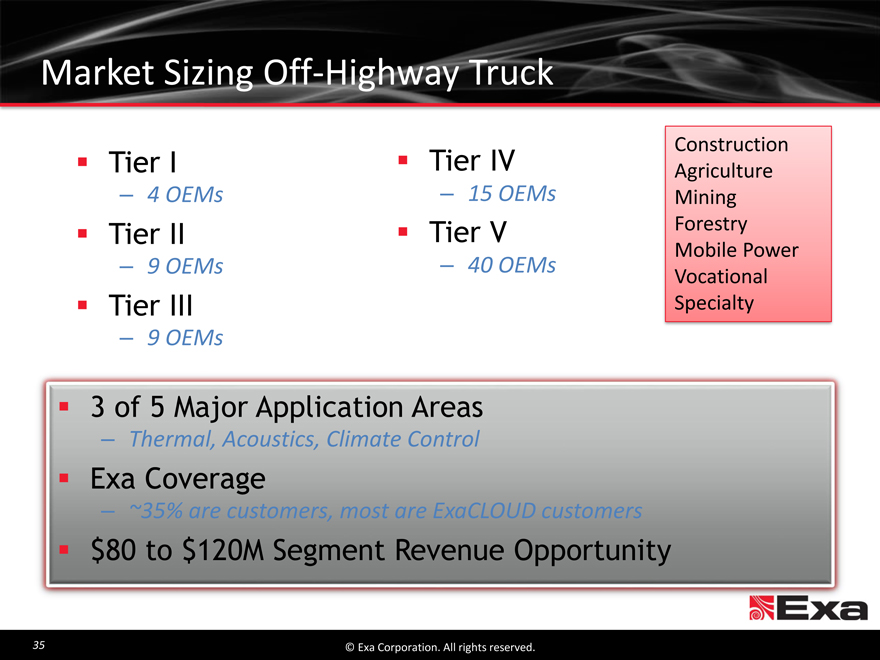

Market Sizing Off-Highway Truck

Construction

Tier I Tier IV Agriculture

4 OEMs 15 OEMs Mining

Tier II Tier V Forestry

Mobile Power

9 OEMs 40 OEMs Vocational

Tier III Specialty

9 OEMs

3 of 5 Major Application Areas

Thermal, Acoustics, Climate Control

Exa Coverage

~35% are customers, most are ExaCLOUD customers

$80 to $120M Segment Revenue Opportunity

35 © Exa Corporation. All rights reserved.

|

Market Sizing Suppliers

Tier I > $25B

3 Suppliers

Tier II $10B to $25B

10 Suppliers

Tier III < $10B

4 Suppliers

Tier IV—Tires

6 Suppliers

Tier V—Components

25 Suppliers

Tier VI—Trains

10 OEMs

Tier VII Mcycles/RVs

5 OEMs

3 of 5 Major Application Areas

Thermal, Acoustics, Climate Control (+ Aero for Tires, Trains, & M/C)

Exa Coverage

~25% of Suppliers & 60% of Train OEMs are customers

$60 to $100M Segment Revenue Opportunity

© Exa Corporation. All rights reserved.

36

|

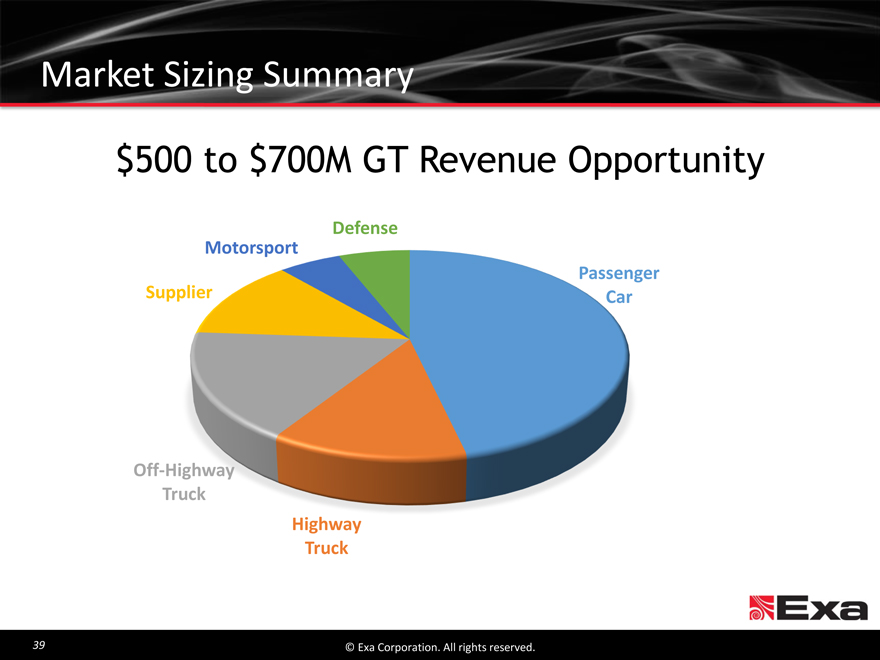

Market Sizing Summary

$500 to $700M GT Revenue Opportunity

Defense

Motorsport

Passenger

Supplier Car

Off-Highway

Truck

Highway

Truck

39 © Exa Corporation. All rights reserved.

|

Why Customers Partner With Exa

Highest Degree of Simulation Accuracy

Faster Turnaround Time

Deep Domain Expertise

Return on Investment

Robustness Deployability

40 © Exa Corporation. All rights reserved.

|

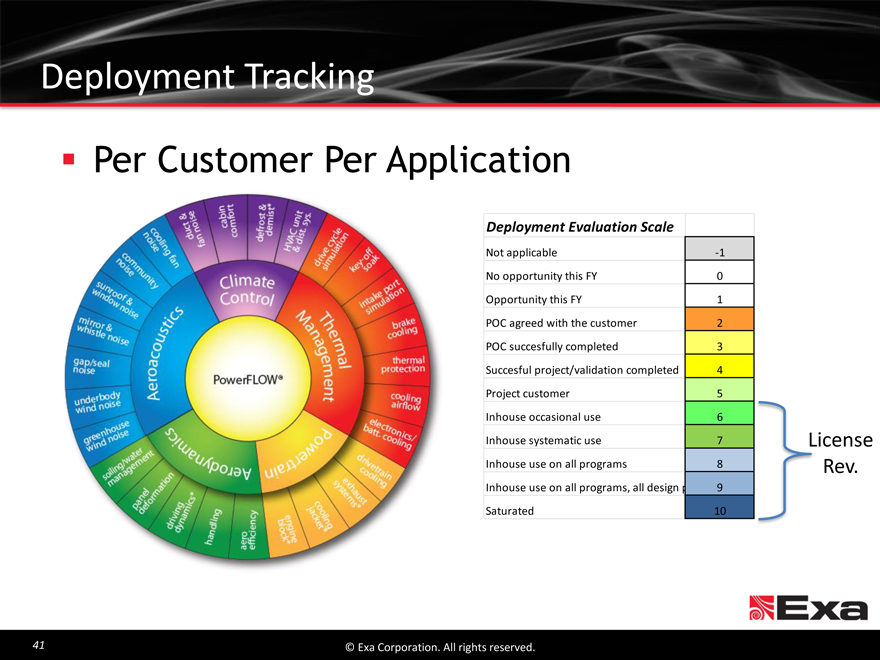

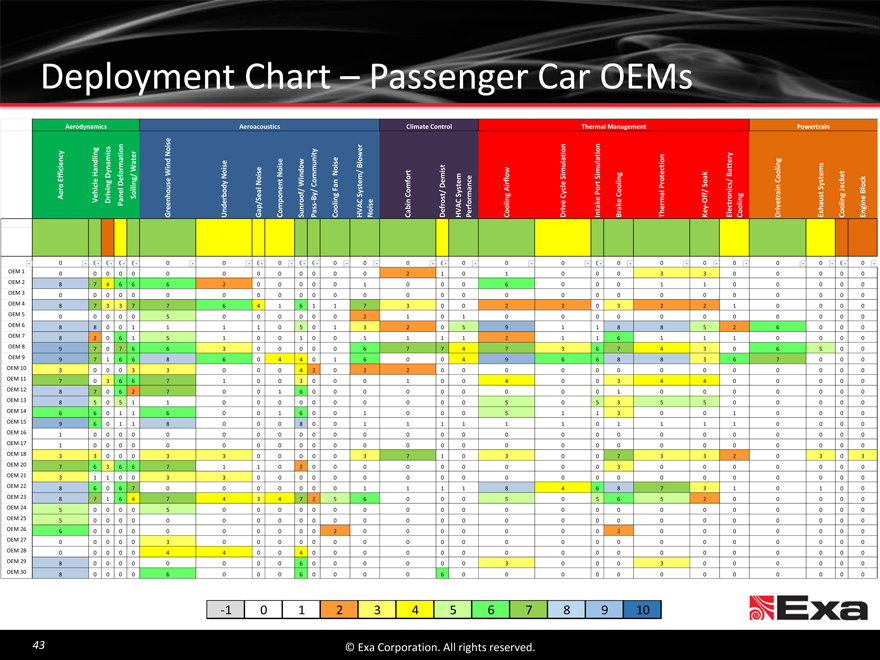

Deployment Tracking

Per Customer Per Application

Deployment Evaluation Scale

Not applicable -1

No opportunity this FY 0

Opportunity this FY 1

POC agreed with the customer 2

POC succesfully completed 3

Succesful project/validation completed 4

Project customer 5

Inhouse occasional use 6

Inhouse systematic use 7 License

Inhouse use on all programs 8 Rev.

Inhouse use on all programs, all design p 9

Saturated 10

41 © Exa Corporation. All rights reserved.

|

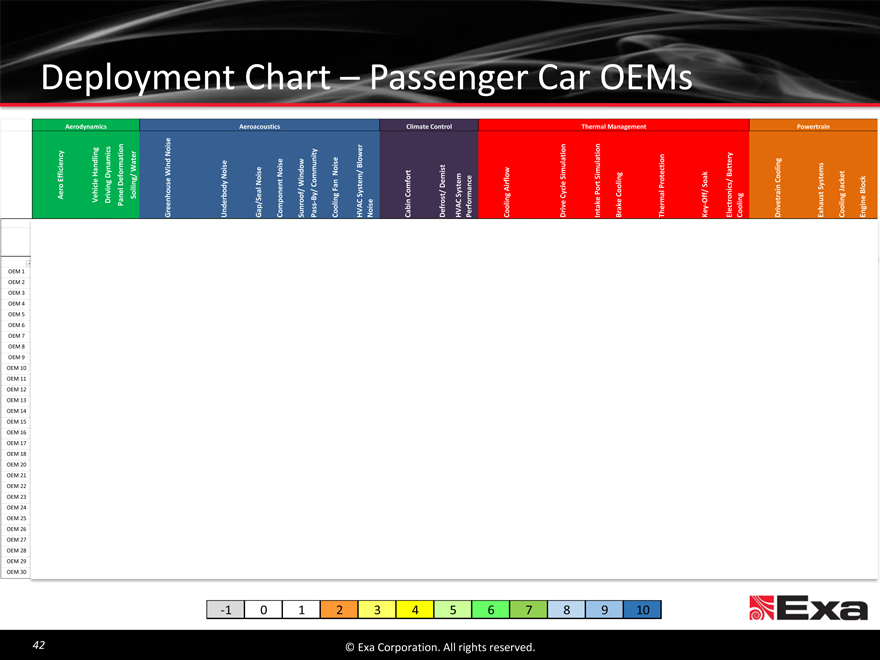

Deployment Chart - Passenger Car OEMs

Aero Efficiency

Vehicle Handling Aerodynamics

Driving Dynamics Panel Deformation Soiling/ Water

Greenhouse Wind Noise

Underbody Noise Deployment

Gap/Seal Noise Aeroacoustics

Component Noise

Sunroof/ Window

Pass-By/ Community Chart Cooling Fan Noise HVAC System/ Blower Noise

Cabin Comfort Climate

Defrost/ Demist Control HVAC System Performance

Cooling Airflow Passenger

Drive Cycle Simulation Car Intake Port Simulation Thermal

Brake Cooling Management

Thermal Protection OEMs Key-Off/ Soak

Electronics/ Battery Cooling

Drivetrain Cooling

Exhaust Systems Powertrain Cooling Jacket

Engine Block

OEM 1 OEM 2 OEM 3 OEM 4 OEM 5 OEM 6 OEM 7 OEM 8 OEM 9 OEM 10 OEM 11 OEM 12 OEM 13 OEM 14 OEM 15 OEM 16 OEM 17 OEM 18 OEM 20 OEM 21 OEM 22 OEM 23 OEM 24 OEM 25 OEM 26 OEM 27 OEM 28 OEM 29 OEM 30

-1 0 1 2 3 4 5 6 7 8 9 10

© Exa Corporation. All rights reserved.

42

|

Deployment Chart Passenger Car OEMs

Aerodynamics Aeroacoustics Climate Control Thermal Management Powertrain

n ise n

c s o y io

i No ion

er t

d nit a g

t e e lat ion t ery

n ow Bl t t

s

iency dling ynami mat nd ower t ec Bat

E ff ic Han D ef or g / Wa e Wi Nois ise No ise mmu Nois r emi e S imu Simul ot / Coolin t ems ket k

icle g D dy No Wi Co stem/ D nc irf low le rt Pr s n S ys ac oc

/ A l / J Bl

t

ero ivin Soilin ous bo Seal onent of/ By/ g Fan Sy Co mfo t Sy stem ma g Cyc Po Co oling Soak o nic g rai s g e

A r — e Off in

s r —

s g

Veh D Panel r eenh Under ap / Co mp Sun ro Pa Co olin VAC Nois e Ca bin ef os VAC Pe rf or Co olin r ive nt ake Brak Th erma ey lectr Co olin r ivet Exhau Co olin En

G G H D H D I K E D

0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

OEM 1 0 0 0 0 0 0 0 0 0 0 0 0 0 2 1 0 1 0 0 0 3 3 0 0 0 0 0

OEM 2 8 7 4 6 6 6 2 0 0 0 0 0 1 0 0 0 6 0 0 0 1 1 0 0 0 0 0

OEM 3 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

OEM 4 8 7 3 3 7 7 6 4 1 6 1 1 7 3 0 0 2 2 0 3 2 2 1 0 0 0 0

OEM 5 0 0 0 0 0 5 0 0 0 0 0 0 2 1 0 1 0 0 0 0 0 0 0 0 0 0 0

OEM 6 8 8 0 0 1 1 1 1 0 5 0 1 3 2 0 5 9 1 1 8 8 5 2 6 0 0 0

OEM 7 8 2 0 6 1 5 1 0 0 1 0 0 1 1 1 1 2 1 1 6 1 1 1 0 0 0 0

OEM 8 9 7 0 7 6 6 3 0 0 0 0 0 6 7 7 4 7 3 6 7 4 3 0 6 5 0 0

OEM 9 9 7 1 6 6 8 6 0 4 4 0 1 6 0 0 4 9 6 6 8 8 3 6 7 0 0 0

OEM 10 3 0 0 0 3 3 0 0 0 4 2 0 2 2 0 0 0 0 0 0 0 0 0 0 0 0 0

OEM 11 7 0 3 6 6 7 1 0 0 3 0 0 0 1 0 0 4 0 0 3 4 4 0 0 0 0 0

OEM 12 8 7 0 6 2 7 0 0 1 6 0 0 0 0 0 0 0 0 0 1 0 0 0 0 0 0 0

OEM 13 8 5 0 5 1 1 0 0 0 0 0 0 0 0 0 0 5 0 5 3 5 5 0 0 0 0 0

OEM 14 6 6 0 1 1 6 0 0 1 6 0 0 1 0 0 0 5 1 1 3 0 0 1 0 0 0 0

OEM 15 9 6 0 1 1 8 0 0 0 8 0 0 1 1 1 1 1 1 0 1 1 1 1 0 0 0 0

OEM 16 1 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

OEM 17 1 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

OEM 18 3 3 0 0 0 3 3 0 0 0 0 0 3 7 1 0 3 0 0 7 3 3 2 0 3 0 3

OEM 20 7 6 3 6 6 7 1 1 0 2 0 0 0 0 0 0 0 0 0 3 0 0 0 0 0 0 0

OEM 21 3 1 1 0 0 3 3 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

OEM 22 8 6 0 6 7 0 0 0 0 0 0 0 1 1 1 1 8 4 6 8 7 3 1 0 1 0 0

OEM 23 8 7 1 6 4 7 4 3 4 7 2 5 6 0 0 0 5 0 5 6 5 2 0 0 0 0 0

OEM 24 5 0 0 0 0 5 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

OEM 25 5 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

OEM 26 6 0 0 0 0 0 0 0 0 0 0 2 0 0 0 0 0 0 0 2 0 0 0 0 0 0 0

OEM 27 0 0 0 0 0 3 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

OEM 28 0 0 0 0 0 4 4 0 0 4 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

OEM 29 8 0 0 0 0 0 0 0 0 6 0 0 0 0 0 0 3 0 0 0 3 0 0 0 0 0 0

OEM 30 8 0 0 0 0 6 0 0 0 6 0 0 0 0 6 0 0 0 0 0 0 0 0 0 0 0 0

-1 0 1 2 3 4 5 6 7 8 9 10

43 © Exa Corporation. All rights reserved.

|

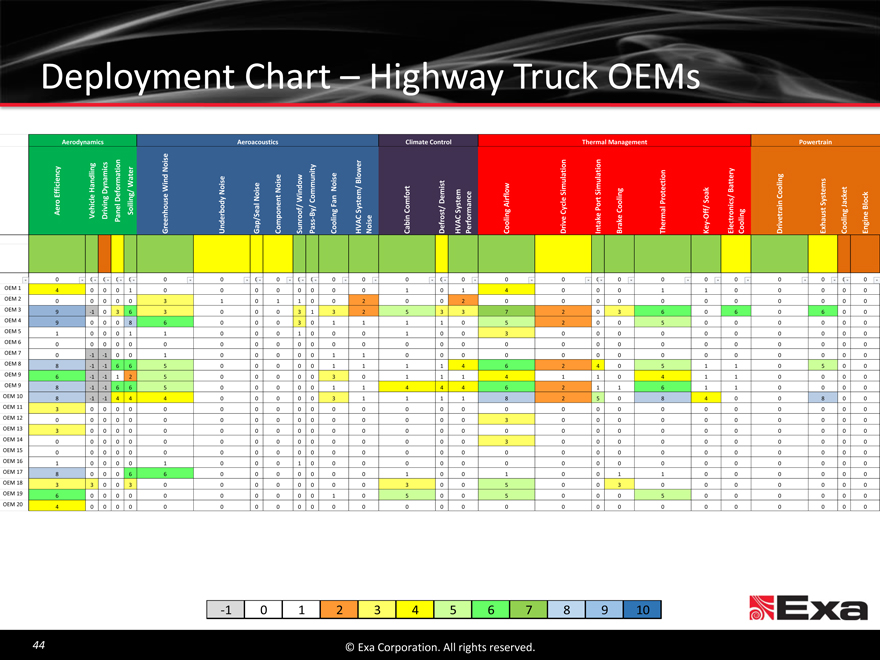

Deployment Chart Highway Truck OEMs

Aerodynamics Aeroacoustics Climate Control Thermal Management Powertrain

se

n n

s y o

y ng c i o Noi w er ion ti y

c l i t nit t n

e o l a o g

is i

n d ma d s e se ow Bl t la t tt er n

o r Win i s e d t w ec

f icien Ha Dynami / Water No i Noi mmu No r o i mu imu g ak Ba oli et

E f l e g Def n g se y No t Win Co n em/ Demis em c e r fl S t S li n Pro t o s/ Co y stems c k ck

i l a n i le r S c n S a

A i i J

o i n il u d n en f / / g F S yst Comfo S yst g Cyc l f / n g ra t g

v S o ho S ea o By n st/ r ma n e Po ma r o n s e Blo

/ — l i C n o C o i e k e t i et a u i n n

Aer Vehic Dri Pa nel een derbo nroo ise i r l Coo er—Of l l i

p i v t a ec i v h g

Gr Un Ga Comp u Pass Coo HVA No Cab Def HVA Perf Coo Dr In Brak h ey l Coo Dr x Coo n

S T K E E E

0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

OEM 1 4 0 0 0 1 0 0 0 0 0 0 0 0 1 0 1 4 0 0 0 1 1 0 0 0 0 0

OEM 2 0 0 0 0 0 3 1 0 1 1 0 0 2 0 0 2 0 0 0 0 0 0 0 0 0 0 0

OEM 3 9 -1 0 3 6 3 0 0 0 3 1 3 2 5 3 3 7 2 0 3 6 0 6 0 6 0 0

OEM 4 9 0 0 0 8 6 0 0 0 3 0 1 1 1 1 0 5 2 0 0 5 0 0 0 0 0 0

OEM 5 1 0 0 0 1 1 0 0 0 1 0 0 0 1 0 0 3 0 0 0 0 0 0 0 0 0 0

OEM 6 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

OEM 7 0 -1 -1 0 0 1 0 0 0 0 0 1 1 0 0 0 0 0 0 0 0 0 0 0 0 0 0

OEM 8 8 -1 -1 6 6 5 0 0 0 0 0 1 1 1 1 4 6 2 4 0 5 1 1 0 5 0 0

OEM 9 6 -1 -1 1 2 5 0 0 0 0 0 3 0 1 1 1 4 1 1 0 4 1 1 0 0 0 0

OEM 9 8 -1 -1 6 6 5 0 0 0 0 0 1 1 4 4 4 6 2 1 1 6 1 1 0 0 0 0

OEM 10 8 -1 -1 4 4 4 0 0 0 0 0 3 1 1 1 1 8 2 5 0 8 4 0 0 8 0 0

OEM 11 3 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

OEM 12 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 3 0 0 0 0 0 0 0 0 0 0

OEM 13 3 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

OEM 14 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 3 0 0 0 0 0 0 0 0 0 0

OEM 15 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

OEM 16 1 0 0 0 0 1 0 0 0 1 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

OEM 17 8 0 0 0 6 6 0 0 0 0 0 0 0 1 0 0 1 0 0 1 1 0 0 0 0 0 0

OEM 18 3 3 0 0 3 0 0 0 0 0 0 0 0 3 0 0 5 0 0 3 0 0 0 0 0 0 0

OEM 19 6 0 0 0 0 0 0 0 0 0 0 1 0 5 0 0 5 0 0 0 5 0 0 0 0 0 0

OEM 20 4 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

-1 0 1 2 3 4 5 6 7 8 9 10

44 © Exa Corporation. All rights reserved.

|

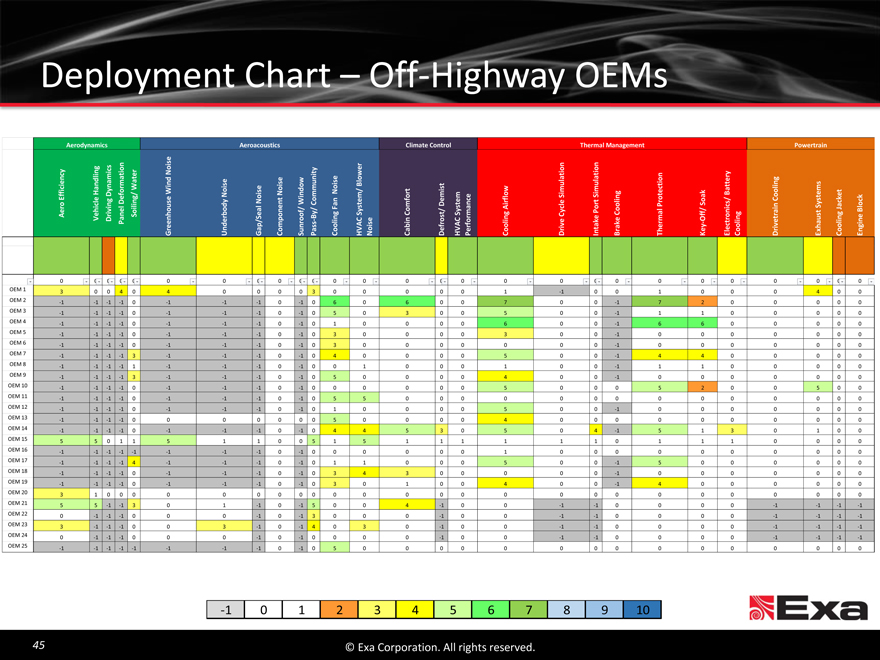

Deployment Chart Off-Highway OEMs

Aerodynamics Aeroacoustics Climate Control Thermal Management Powertrain

e

s

n i n on

i

i ng t o er No ity tio ti

t a

ency dl mics ma e ise Blower la i on ng

s t t i

r e s

o Wa Wi nd Noi i s No imul i mu g ec ems et

S S in t t

ng/ n em/ l o s / c k

Effici e Han g Dyna Def i e No Noise Window mmun t t em nce i l r o S ak c Battery Cool

l l Fa e t Pro Sys Ja ck

f / ys A f/ t

o i Soi us nent Co S Comfort t/ Demi S rflow Po Co

s

A er eal o —By/ i ng C ys e o C orma i ng Cyc e mal Of i ng rain us i ng ine Blo

Dr /S s s i s b in r ve a ke k — vet g

Vehic vin Panel Greenho U n derbody Gap Comp Sunroo Pa Cool HVA No Ca Def HVA Perf Cool Dri n t Bra Th er K ey lectroni Cool Dri Exha Cool En

I E

0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

OEM 1 3 0 0 4 0 4 0 0 0 0 3 0 0 0 0 0 1 -1 0 0 1 0 0 0 4 0 0

OEM 2 -1 -1 -1 -1 0 -1 -1 -1 0 -1 0 6 0 6 0 0 7 0 0 -1 7 2 0 0 0 0 0

OEM 3 -1 -1 -1 -1 0 -1 -1 -1 0 -1 0 5 0 3 0 0 5 0 0 -1 1 1 0 0 0 0 0

OEM 4 -1 -1 -1 -1 0 -1 -1 -1 0 -1 0 1 0 0 0 0 6 0 0 -1 6 6 0 0 0 0 0

OEM 5 -1 -1 -1 -1 0 -1 -1 -1 0 -1 0 3 0 0 0 0 3 0 0 -1 0 0 0 0 0 0 0

OEM 6 -1 -1 -1 -1 0 -1 -1 -1 0 -1 0 3 0 0 0 0 0 0 0 -1 0 0 0 0 0 0 0

OEM 7 -1 -1 -1 -1 3 -1 -1 -1 0 -1 0 4 0 0 0 0 5 0 0 -1 4 4 0 0 0 0 0

OEM 8 -1 -1 -1 -1 1 -1 -1 -1 0 -1 0 0 1 0 0 0 1 0 0 -1 1 1 0 0 0 0 0

OEM 9 -1 -1 -1 -1 3 -1 -1 -1 0 -1 0 5 0 0 0 0 4 0 0 -1 0 0 0 0 0 0 0

OEM 10 -1 -1 -1 -1 0 -1 -1 -1 0 -1 0 0 0 0 0 0 5 0 0 0 5 2 0 0 5 0 0

OEM 11 -1 -1 -1 -1 0 -1 -1 -1 0 -1 0 5 5 0 0 0 0 0 0 0 0 0 0 0 0 0 0

OEM 12 -1 -1 -1 -1 0 -1 -1 -1 0 -1 0 1 0 0 0 0 5 0 0 -1 0 0 0 0 0 0 0

OEM 13 -1 -1 -1 -1 0 0 0 0 0 0 0 5 0 0 0 0 4 0 0 0 0 0 0 0 0 0 0

OEM 14 -1 -1 -1 -1 0 -1 -1 -1 0 -1 0 4 4 5 3 0 5 0 4 -1 5 1 3 0 1 0 0

OEM 15 5 5 0 1 1 5 1 1 0 0 5 1 5 1 1 1 1 1 1 0 1 1 1 0 0 0 0

OEM 16 -1 -1 -1 -1 -1 -1 -1 -1 0 -1 0 0 0 0 0 0 1 0 0 0 0 0 0 0 0 0 0

OEM 17 -1 -1 -1 -1 4 -1 -1 -1 0 -1 0 1 1 0 0 0 5 0 0 -1 5 0 0 0 0 0 0

OEM 18 -1 -1 -1 -1 0 -1 -1 -1 0 -1 0 3 4 3 0 0 0 0 0 -1 0 0 0 0 0 0 0

OEM 19 -1 -1 -1 -1 0 -1 -1 -1 0 -1 0 3 0 1 0 0 4 0 0 -1 4 0 0 0 0 0 0

OEM 20 3 1 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

OEM 21 5 5 -1 -1 3 0 1 -1 0 -1 5 0 0 4 -1 0 0 -1 -1 0 0 0 0 -1 -1 -1 -1

OEM 22 0 -1 -1 -1 0 0 0 -1 0 -1 3 0 0 0 -1 0 0 -1 -1 0 0 0 0 -1 -1 -1 -1

OEM 23 3 -1 -1 -1 0 0 3 -1 0 -1 4 0 3 0 -1 0 0 -1 -1 0 0 0 0 -1 -1 -1 -1

OEM 24 0 -1 -1 -1 0 0 0 -1 0 -1 0 0 0 0 -1 0 0 -1 -1 0 0 0 0 -1 -1 -1 -1

OEM 25 -1 -1 -1 -1 -1 -1 -1 -1 0 -1 0 5 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

-1 0 1 2 3 4 5 6 7 8 9 10

45 © Exa Corporation. All rights reserved.

|

Key Messages

Large addressable market … Proven technology and

only fractionally penetrated solutions

Strong and consistent Path to profitability and

execution continued top line growth

© Exa Corporation. All rights reserved.

|

Agenda

12:30 1:30 Registration, Lunch, Product Demonstrations

1:30 2:20 Welcome and Market Opportunity, Steve Remondi, CEO

Company Mission and Execution

Addressable Market Opportunity

Exa Deployment and Penetration

2:40 3:00 Product Strategy Customer Alignment, Steve Remondi, CEO

Applications and Automation

Cloud Enabling Quick Adoption and Collaboration

3:00 3:30 Break

3:30 4:15 Financial Update, Rick Gilbody, CFO

The Path to Profitability and Continued Revenue Growth

Guidance FY 16 and FY 17

Target Model

4:15 5:00

Q & A

47 © Exa Corporation. All rights reserved.

|

AUDIO ONLY: Jaguar Land Rover Video in Progress

|

Agenda

12:30 1:30 Registration, Lunch, Product Demonstrations

1:30 2:20 Welcome and Market Opportunity, Steve Remondi, CEO

Company Mission and Execution

Addressable Market Opportunity

Exa Deployment and Penetration

2:20 2:40 Customer Perspective: Jaguar Land Rover

Mark Stanton, JLR Director of Vehicle Engineering (via video)

Jean-Paul Roux, Exa SVP European Operations

3:00 3:30 Break

3:30 4:15 Financial Update, Rick Gilbody, CFO

The Path to Profitability and Continued Revenue Growth

Guidance FY 16 and FY 17

Target Model

4:15 5:00

Q & A

51 © Exa Corporation. All rights reserved.

|

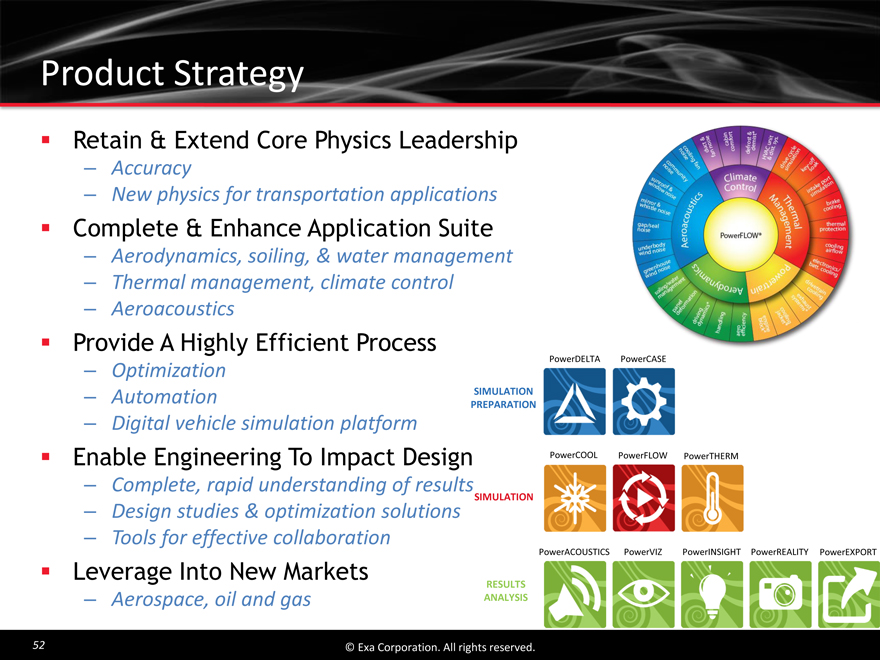

Product Strategy

Retain & Extend Core Physics Leadership

Accuracy

New physics for transportation applications

Complete & Enhance Application Suite

Aerodynamics, soiling, & water management

Thermal management, climate control

Aeroacoustics

Provide A Highly Efficient Process

PowerDELTA PowerCASE

Optimization

Automation SIMULATION

PREPARATION

Digital vehicle simulation platform

Enable Engineering To Impact Design PowerCOOL PowerFLOW PowerTHERM

Complete, rapid understanding of results

SIMULATION

Design studies & optimization solutions

Tools for effective collaboration

PowerACOUSTICS PowerVIZ PowerINSIGHT PowerREALITY PowerEXPORT

Leverage Into New Markets RESULTS

Aerospace, oil and gas ANALYSIS

52 © Exa Corporation. All rights reserved.

|

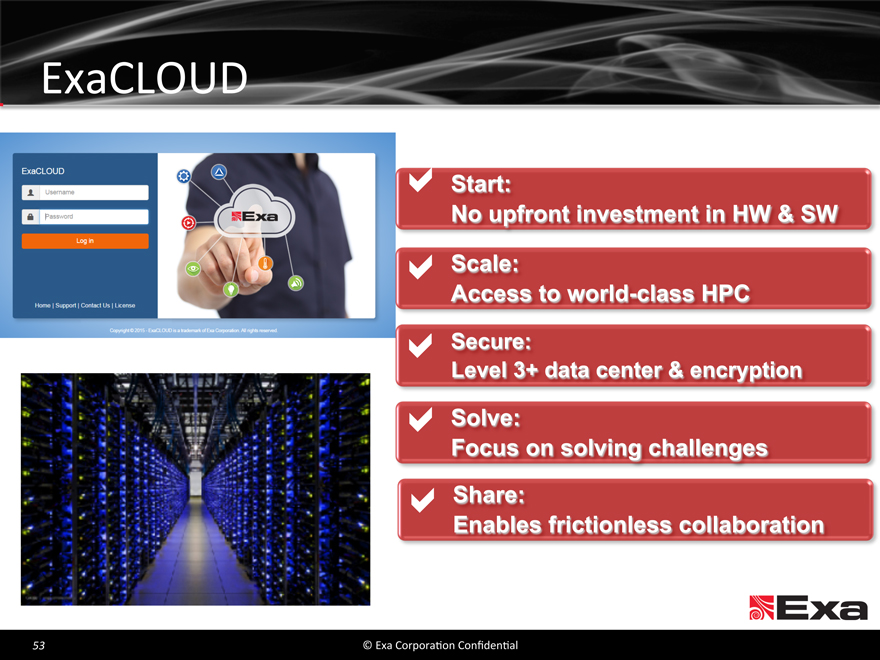

ExaCLOUD

Start:

No upfront investment in HW & SW

Scale:

Access to world class HPC

Secure:

Level 3+ data center & encryption

Solve:

Focus on solving challenges

Share:

Enables frictionless collaboration

53 © Exa Corporation. All rights reserved.

|

AUDIO ONLY: ExaCLOUD Video in Progress

© Exa Corporation. All rights reserved.

|

AUDIO ONLY: PowerINSIGHT Video in Progress

© Exa Corporation. All rights reserved.

|

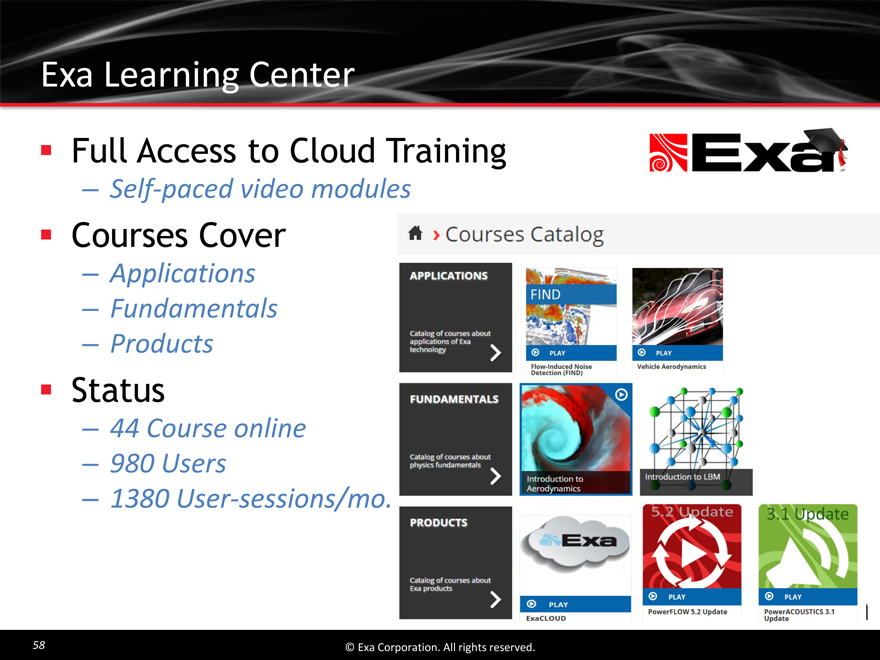

Exa Learning Center

Full Access to Cloud Training

Self-paced video modules

Courses Cover

Applications

Fundamentals

Products

Status

44 Course online

980 Users

1380 User-sessions/mo.

58 © Exa Corporation. All rights reserved.

|

Agenda

12:30 1:30 Registration, Lunch, Product Demonstrations

1:30 2:20 Welcome and Market Opportunity, Steve Remondi, CEO

Company Mission and Execution

Addressable Market Opportunity

Exa Deployment and Penetration

2:20 2:40 Customer Perspective: Jaguar Land Rover

Mark Stanton, JLR Director of Vehicle Engineering (via video)

Jean-Paul Roux, Exa SVP European Operations

2:40 3:00 Product Strategy Customer Alignment, Steve Remondi, CEO

Applications and Automation

Cloud Enabling Quick Adoption and Collaboration

3:30 4:15

Financial Update, Rick Gilbody, CFO

The Path to Profitability and Continued Revenue Growth

Guidance FY 16 and FY 17

Target Model

4:15 5:00

Q & A

|

Agenda

12:30 1:30 Registration, Lunch, Product Demonstrations

1:30 2:20 Welcome and Market Opportunity, Steve Remondi, CEO

Company Mission and Execution

Addressable Market Opportunity

Exa Deployment and Penetration

2:20 2:40 Customer Perspective: Jaguar Land Rover

Mark Stanton, JLR Director of Vehicle Engineering (via video)

Jean-Paul Roux, Exa SVP European Operations

2:40 3:00 Product Strategy Customer Alignment, Steve Remondi, CEO

Applications and Automation

Cloud Enabling Quick Adoption and Collaboration

3:00 3:30

Break

4:15 5:00

Q & A

60 © Exa Corporation. All rights reserved.

|

Key Messages

Strong and consistent Path to profitability and

execution continued top line growth

© Exa Corporation. All rights reserved.

|

Key Financial Highlights

Strong, consistent revenue growth over 10 years

Trailing 12 month revenue growth 16% cc

Recurring, predictable, consumption license business model

Strong balance sheet, no debt

Balancing growth and investment, organically funding, cash neutral

Attractive long-term model, improving margins through revenue mix, deployment and scale

|

Q3 Year-to-Date FY 2016

Note: Revenue, Operating expense and Adjusted EBITDA on a constant currency basis is a non-GAAP financial measure that we define as GAAP revenue, operating expense and Adjusted EBITDA, adjusted to reverse the impact of changes in the average exchange rates of currencies in which our international businesses operate.

63 © Exa Corporation. All rights reserved.

|

Exa Revenue Profile

License Revenue

Highly recurring and visible

On-premise and cloud consumption based license models

Expansion through installed base deployment and new customer acquisition

Ratable revenue recognition

Project Revenue

Fixed fee, on-site and T&M

Customer enablement and application validation

License expansion

Consulting services

© Exa Corporation. All rights reserved.

|

Recurring Revenue Visibility

< 20 % of Next Year Revenue from New Licenses and Projects

New & Renewal Licenses

at 2/1

Renewals by 4/30

100%

90%

81% Recurring Projects *

60% 72%

New Licenses

New Projects *

0% 50% 100%

% of Next Fiscal Year Revenue Expectation

Based on FY15 Data, * estimated split

65 © Exa Corporation. All rights reserved.

|

Investing In Growth

~$12M incremental investment in customer facing resources, product enhancement and market development over the past 30 months

Core product functionality extension

ExaCloud platform

Expansion of core markets

Passenger vehicle applications

Heavy vehicle highway and off-highway

Non- transportation machinery

Extension into new vertical markets

Aerospace

Oil & Gas

66 © Exa Corporation. All rights reserved.

|

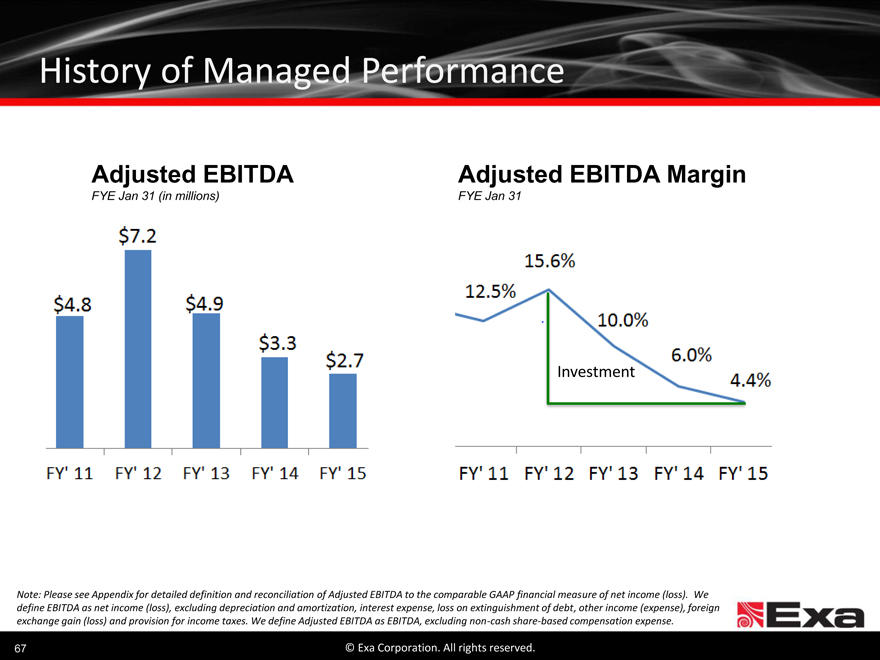

History of Managed Performance

Adjusted EBITDA Adjusted EBITDA Margin

FYE Jan 31 (in millions) FYE Jan 31

Investment

Note: Please see Appendix for detailed definition and reconciliation of Adjusted EBITDA to the comparable GAAP financial measure of net income (loss). We define EBITDA as net income (loss), excluding depreciation and amortization, interest expense, loss on extinguishment of debt, other income (expense), foreign exchange gain (loss) and provision for income taxes. We define Adjusted EBITDA as EBITDA, excluding non-cash share-based compensation expense.

67 © Exa Corporation. All rights reserved.

|

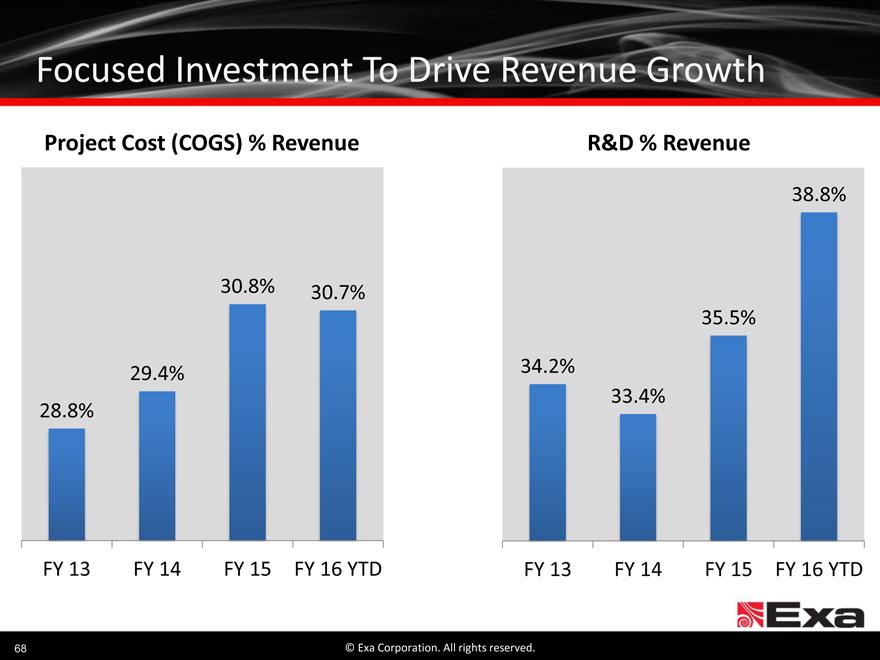

Focused Investment To Drive Revenue Growth

Project Cost (COGS) % Revenue R&D % Revenue

38.8%

30.8% 30.7%

35.5%

29.4% 34.2%

33.4%

28.8%

FY 13 FY 14 FY 15 FY 16 YTD FY 13 FY 14 FY 15 FY 16 YTD

68 © Exa Corporation. All rights reserved.

|

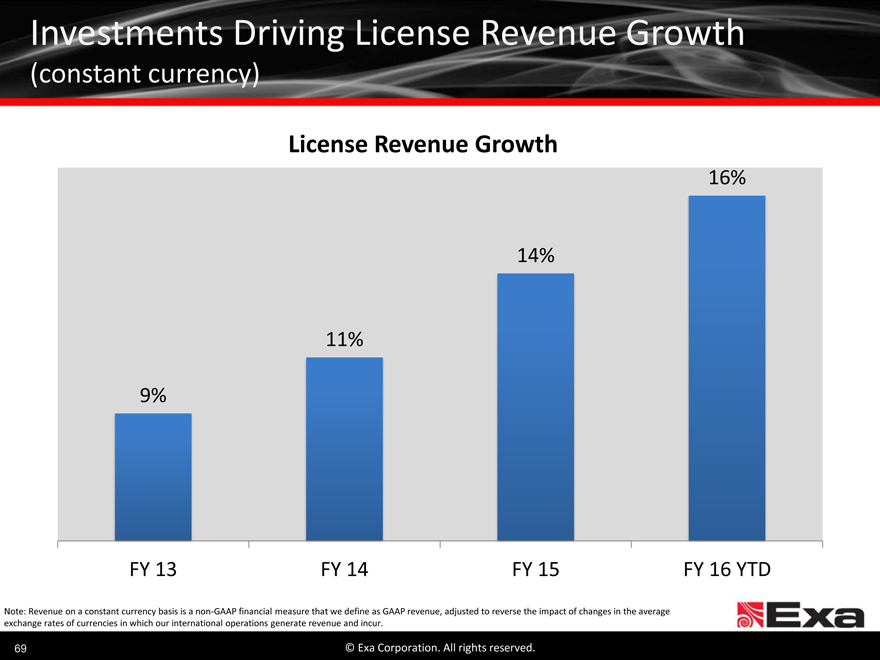

Investments Driving License Revenue Growth

(constant currency)

License Revenue Growth

16%

14%

11%

9%

FY 13 FY 14 FY 15 FY 16 YTD

Note: Revenue on a constant currency basis is a non-GAAP financial measure that we define as GAAP revenue, adjusted to reverse the impact of changes in the average

exchange rates of currencies in which our international operations generate revenue and incur.

69 © Exa Corporation. All rights reserved.

|

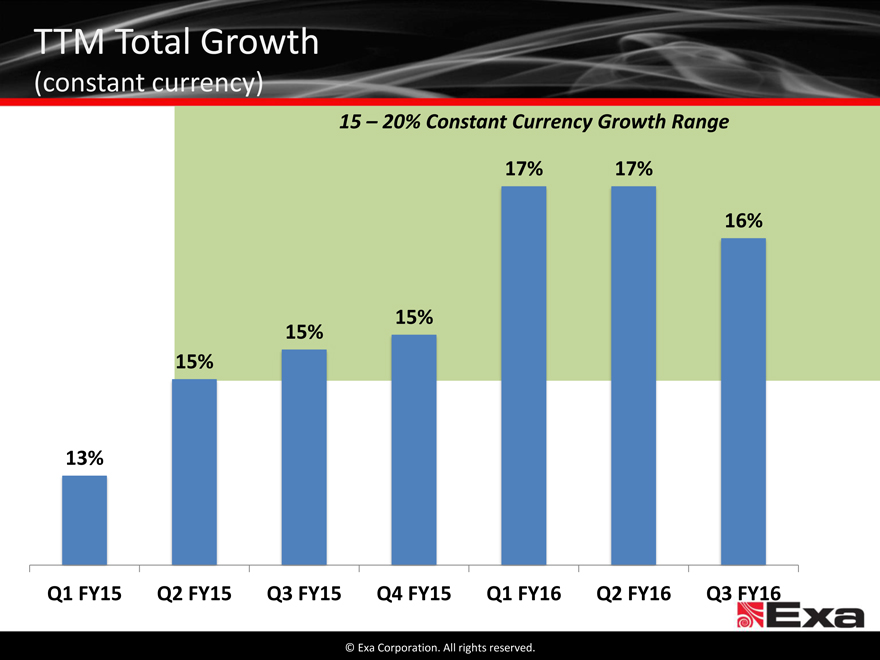

TTM Total Growth

(constant currency)

15 20% Constant Currency Growth Range

17% 17%

16%

15%

15%

15%

13%

Q1 FY15 Q2 FY15 Q3 FY15 Q4 FY15 Q1 FY16 Q2 FY16 Q3 FY16

© Exa Corporation. All rights reserved.

|

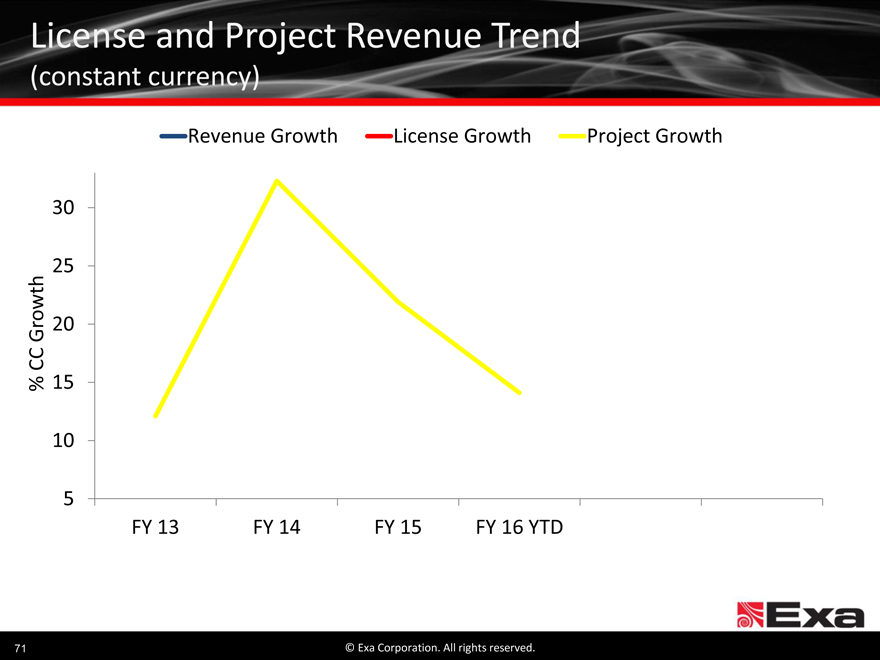

License and Project Revenue Trend

(constant currency)

Revenue Growth License Growth Project Growth

30

25

Growth 20

CC

% 15

10

5

FY 13 FY 14 FY 15 FY 16 YTD

71 © Exa Corporation. All rights reserved.

|

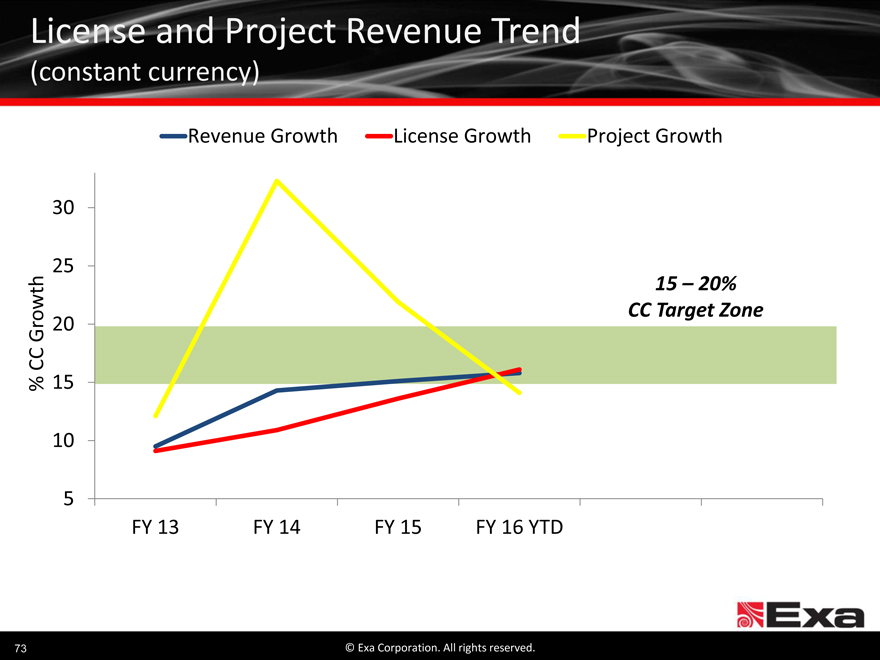

License and Project Revenue Trend

(constant currency)

Revenue Growth License Growth Project Growth

30

25

Growth 20

CC

% 15

10

5

FY 13 FY 14 FY 15 FY 16 YTD

72 © Exa Corporation. All rights reserved.

|

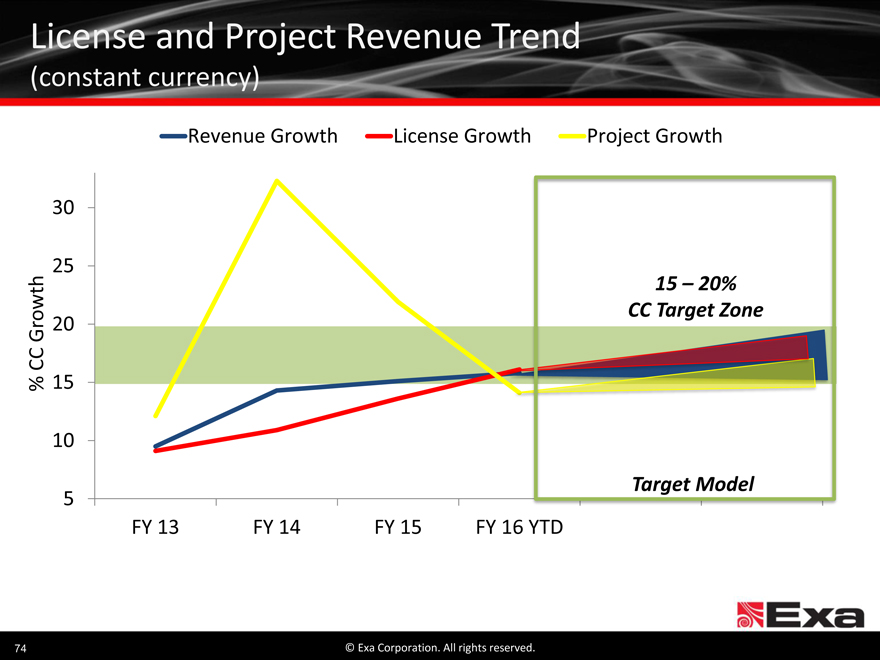

License and Project Revenue Trend

(constant currency)

Revenue Growth License Growth Project Growth

30

25

15 20%

CC Target Zone

Growth 20

CC

% 15

10

5

FY 13 FY 14 FY 15 FY 16 YTD

73 © Exa Corporation. All rights reserved.

|

License and Project Revenue Trend

(constant currency)

Revenue Growth License Growth Project Growth

30

25

Growth 20

CC

% 15

10

Target Model

5

FY 13 FY 14 FY 15 FY 16 YTD

74 © Exa Corporation. All rights reserved.

|

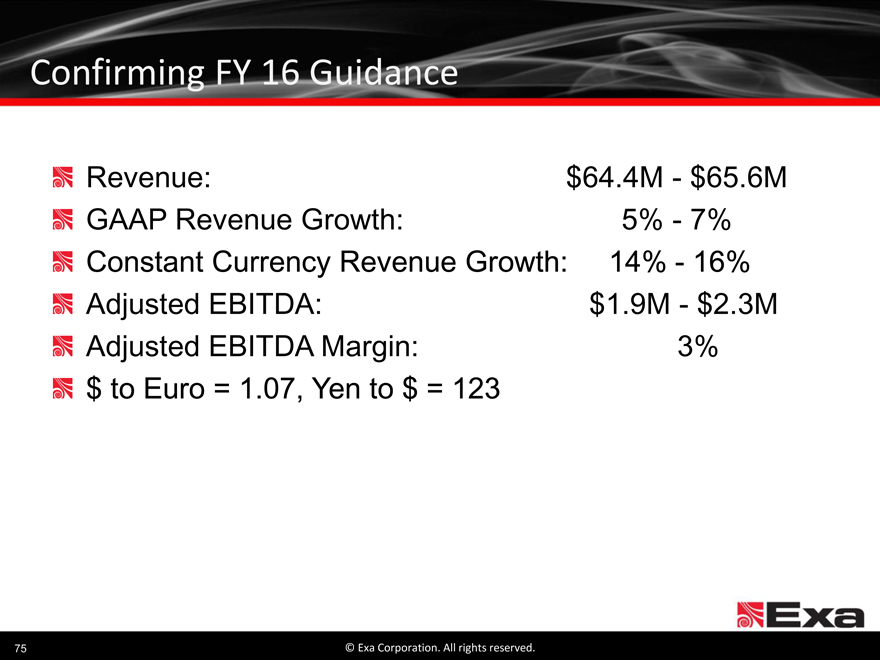

Confirming FY 16 Guidance

Revenue: $64.4M —$65.6M

GAAP Revenue Growth: 5% —7%

Constant Currency Revenue Growth: 14% —16%

Adjusted EBITDA: $1.9M —$2.3M

Adjusted EBITDA Margin: 3%

$ to Euro = 1.07, Yen to $ = 123

75 © Exa Corporation. All rights reserved.

|

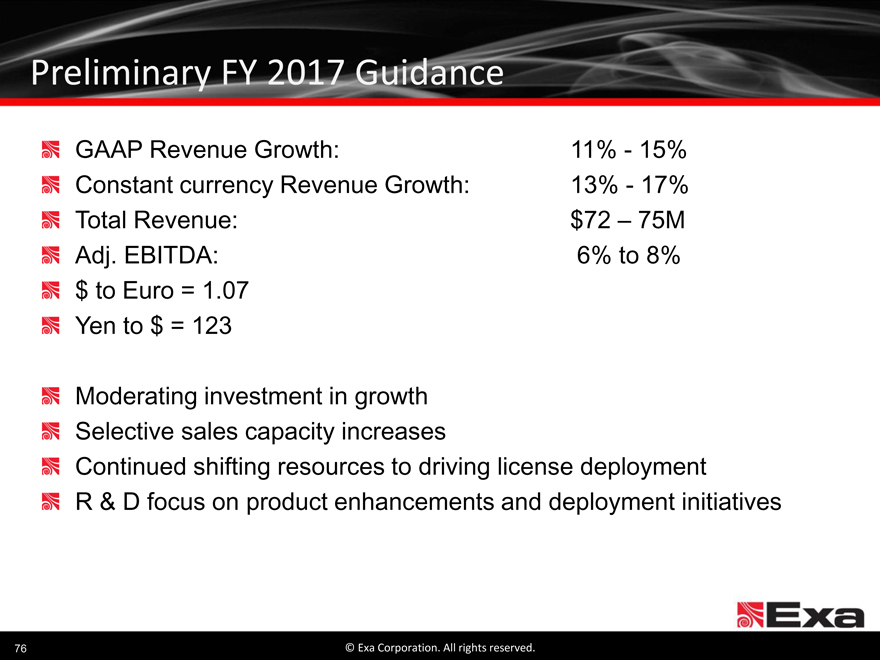

Preliminary FY 2017 Guidance

GAAP Revenue Growth: 11%—15%

Constant currency Revenue Growth: 13%—17%

Total Revenue: $72 75M

Adj. EBITDA: 6% to 8%

$ to Euro = 1.07

Yen to $ = 123

Moderating investment in growth Selective sales capacity increases

Continued shifting resources to driving license deployment R & D focus on product enhancements and deployment initiatives

76 © Exa Corporation. All rights reserved.

|

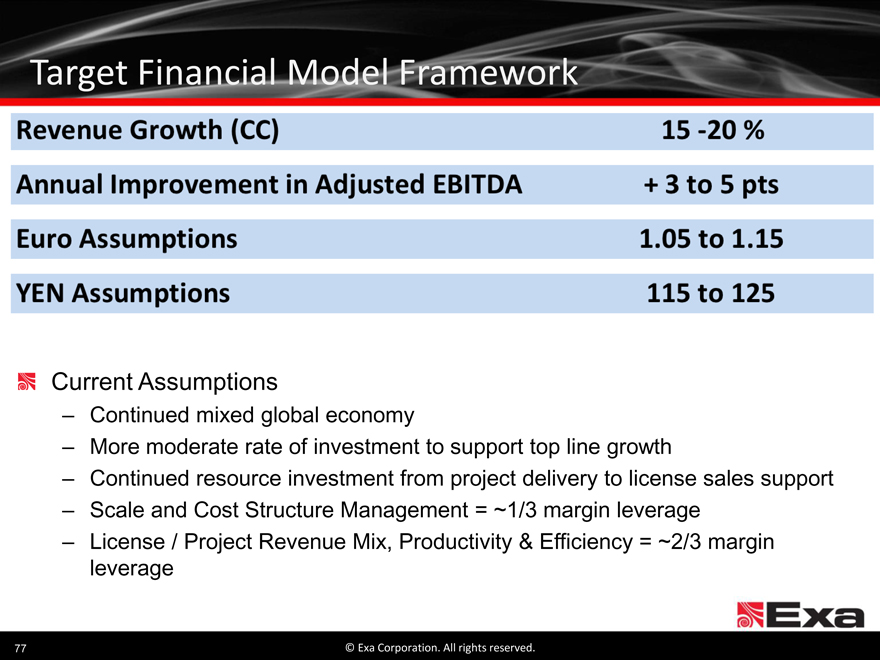

Target Financial Model Framework

Current Assumptions

Continued mixed global economy

More moderate rate of investment to support top line growth

Continued resource investment from project delivery to license sales support

Scale and Cost Structure Management = ~1/3 margin leverage

License / Project Revenue Mix, Productivity & Efficiency = ~2/3 margin leverage

77 © Exa Corporation. All rights reserved.

|

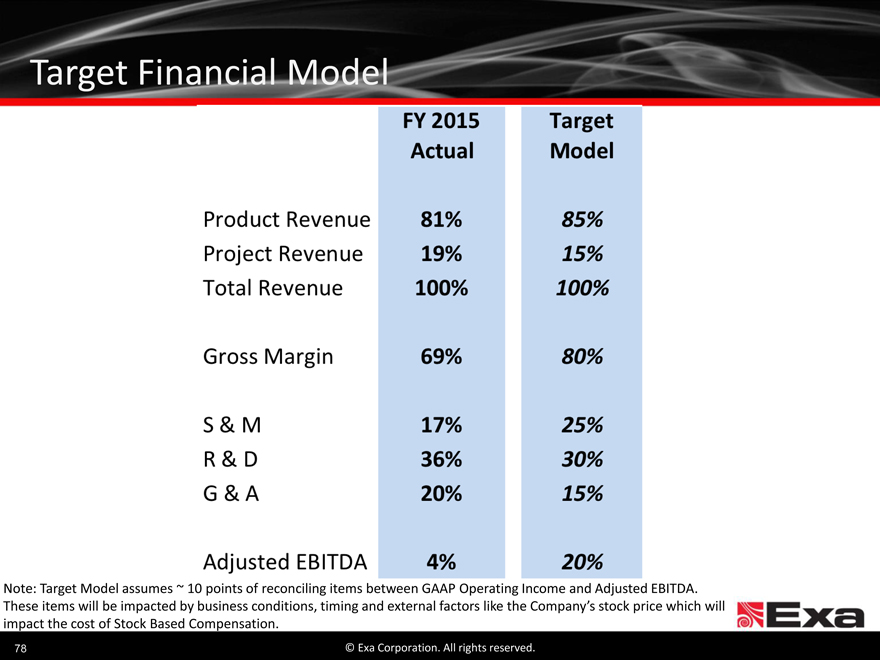

Target Financial Model

Note: Target Model assumes ~ 10 points of reconciling items between GAAP Operating Income and Adjusted EBITDA.

These items will be impacted by business conditions, timing and external factors like the Company’s stock price which will impact the cost of Stock Based Compensation.

78 © Exa Corporation. All rights reserved.

|

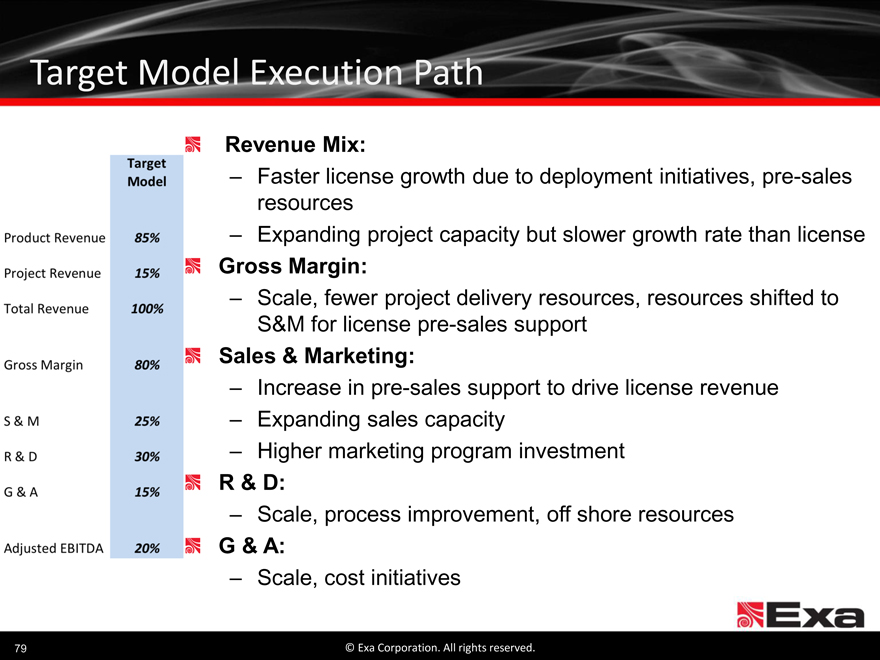

Target Model Execution Path

Revenue Mix:

Faster license growth due to deployment initiatives, pre-sales resources

Expanding project capacity but slower growth rate than license

Gross Margin:

Scale, fewer project delivery resources, resources shifted to

S&M for license pre-sales support

Sales & Marketing:

Increase in pre-sales support to drive license revenue

Expanding sales capacity

Higher marketing program investment

R & D:

Scale, process improvement, off shore resources

G & A:

Scale, cost initiatives

79 © Exa Corporation. All rights reserved.

|

Summary

Strong and expanding market opportunity Significant deployment expansion runway Competitive technical advantage Strong customer base Extended market reach via ExaCLOUD License growth momentum Considerable margin expansion opportunity

80 © Exa Corporation. All rights reserved.

|

Key Messages

Large addressable market … Proven technology and

only fractionally penetrated solutions

Strong and consistent Clear visibility to profitability

execution and continued top line growth

© Exa Corporation. All rights reserved.

|

Agenda

12:30 1:30 Registration, Lunch, Product Demonstrations

1:30 2:20 Welcome and Market Opportunity, Steve Remondi, CEO

Company Mission and Execution

Addressable Market Opportunity

Exa Deployment and Penetration

2:20 2:40

Customer Perspective: Jaguar Land Rover

Mark Stanton, JLR Director of Vehicle Engineering (via video)

Jean-Paul Roux, Exa SVP European Operations

2:40 3:00 Product Strategy Customer Alignment, Steve Remondi, CEO

Applications and Automation

Cloud Enabling Quick Adoption and Collaboration

3:00 3:30 Break

3:30 4:15 Financial Update, Rick Gilbody, CFO

The Path to Profitability and Continued Revenue Growth

Guidance FY 16 and FY 17

Target Model

© Exa Corporation. All rights reserved.

|

Appendix

© Exa Corporation. All rights reserved.

|

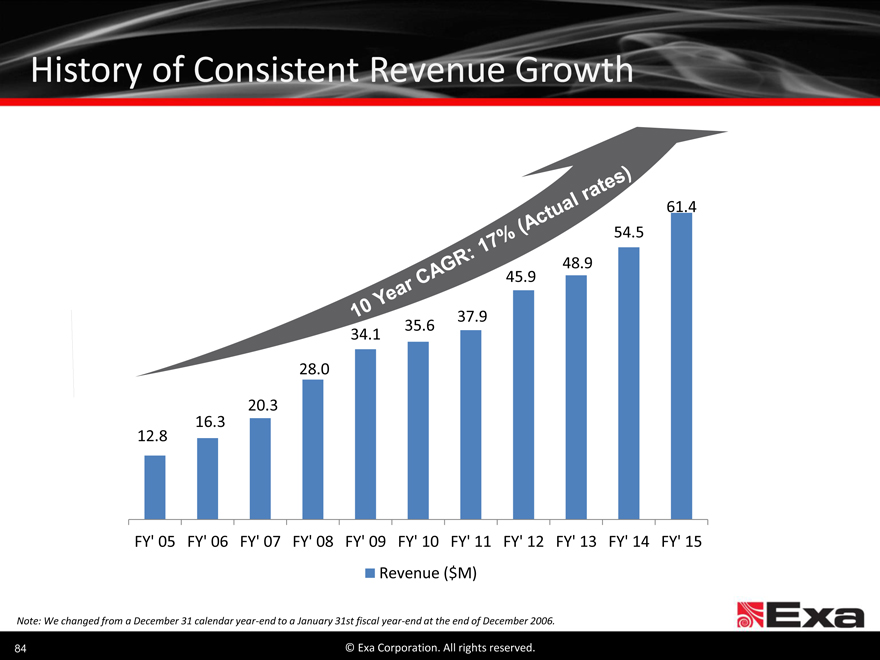

History of Consistent Revenue Growth

61.4

54.5

48.9

45.9

37.9

35.6

34.1

28.0

20.3

16.3

12.8

FY’ 05 FY’ 06 FY’ 07 FY’ 08 FY’ 09 FY’ 10 FY’ 11 FY’ 12 FY’ 13 FY’ 14 FY’ 15

Revenue ($M)

Note: We changed from a December 31 calendar year-end to a January 31st fiscal year-end at the end of December 2006.

84 © Exa Corporation. All rights reserved.

|

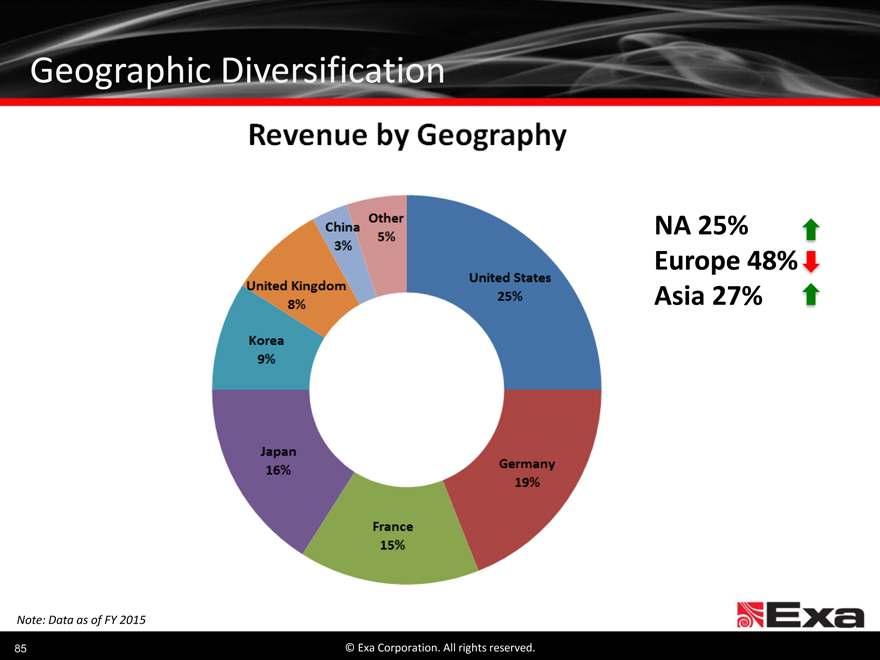

Geographic Diversification

NA 25%

Europe 48%

Asia 27%

Note: Data as of FY 2015

85 © Exa Corporation. All rights reserved.

|

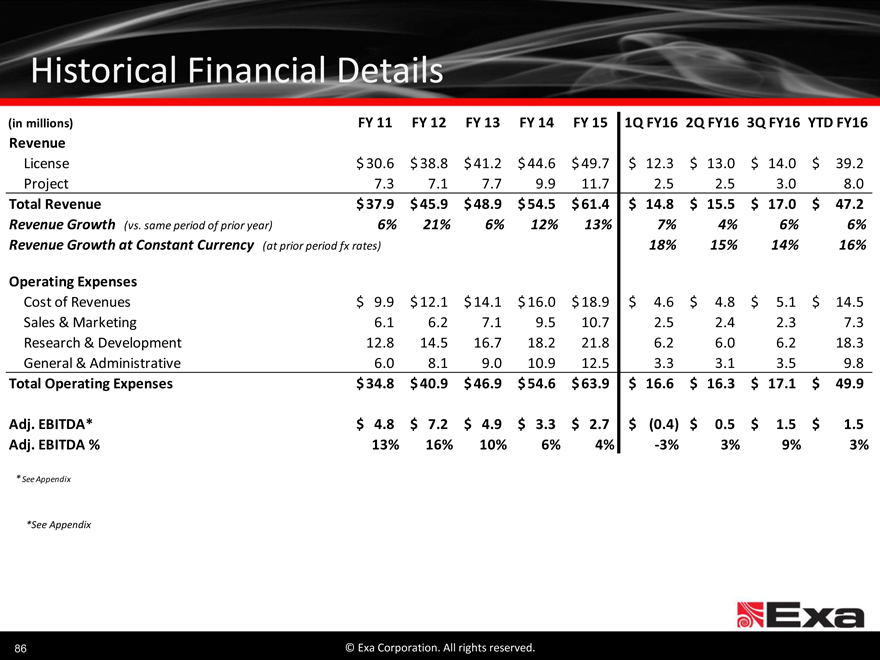

Historical Financial Details

(in millions) FY 11 FY 12 FY 13 FY 14 FY 15 1Q FY16 2Q FY16 3Q FY16 YTD FY16

Revenue

License $ 30.6 $ 38.8 $ 41.2 $ 44.6 $ 49.7 $ 12.3 $ 13.0 $ 14.0 $ 39.2

Project 7.3 7.1 7.7 9.9 11.7 2.5 2.5 3.0 8.0

Total Revenue $ 37.9 $ 45.9 $ 48.9 $ 54.5 $ 61.4 $ 14.8 $ 15.5 $ 17.0 $ 47.2

Revenue Growth (vs. same period of prior year) 6% 21% 6% 12% 13% 7% 4% 6% 6%

Revenue Growth at Constant Currency (at prior period fx rates) 18% 15% 14% 16%

Operating Expenses

Cost of Revenues $ 9.9 $ 12.1 $ 14.1 $ 16.0 $ 18.9 $ 4.6 $ 4.8 $ 5.1 $ 14.5

Sales & Marketing 6.1 6.2 7.1 9.5 10.7 2.5 2.4 2.3 7.3

Research & Development 12.8 14.5 16.7 18.2 21.8 6.2 6.0 6.2 18.3

General & Administrative 6.0 8.1 9.0 10.9 12.5 3.3 3.1 3.5 9.8

Total Operating Expenses $ 34.8 $ 40.9 $ 46.9 $ 54.6 $ 63.9 $ 16.6 $ 16.3 $ 17.1 $ 49.9

Adj. EBITDA* $ 4.8 $ 7.2 $ 4.9 $ 3.3 $ 2.7 $ (0.4) $ 0.5 $ 1.5 $ 1.5

Adj. EBITDA % 13% 16% 10% 6% 4% -3% 3% 9% 3%

* See Appendix

*See Appendix

86 © Exa Corporation. All rights reserved.

|

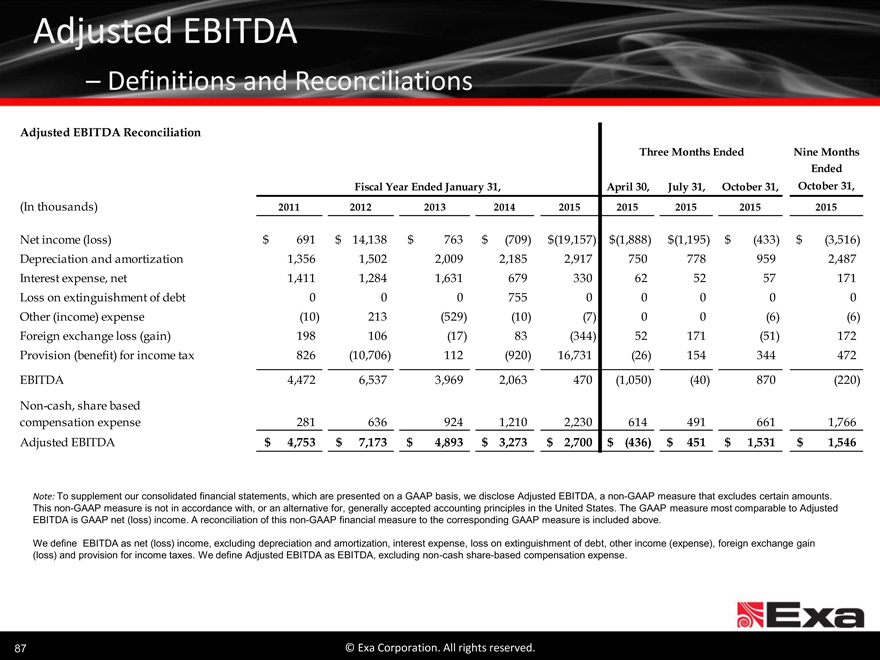

Adjusted EBITDA

Definitions and Reconciliations

Adjusted EBITDA Reconciliation

Three Months Ended Nine Months

Ended

Fiscal Year Ended January 31, April 30, July 31, October 31, October 31,

(In thousands) 2011 2012 2013 2014 2015 2015 2015 2015 2015

Net income (loss) $ 691 $ 14,138 $ 763 $ (709) $(19,157) $ (1,888) $(1,195) $ (433) $ (3,516)

Depreciation and amortization 1,356 1,502 2,009 2,185 2,917 750 778 959 2,487

Interest expense, net 1,411 1,284 1,631 679 330 62 52 57 171

Loss on extinguishment of debt 0 0 0 755 0 0 0 0 0

Other (income) expense (10) 213 (529) (10) (7) 0 0 (6) (6)

Foreign exchange loss (gain) 198 106 (17) 83 (344) 52 171 (51) 172

Provision (benefit) for income tax 826 (10,706) 112 (920) 16,731 (26) 154 344 472

EBITDA 4,472 6,537 3,969 2,063 470 (1,050) (40) 870 (220)

Non-cash, share based

compensation expense 281 636 924 1,210 2,230 614 491 661 1,766

Adjusted EBITDA $ 4,753 $ 7,173 $ 4,893 $ 3,273 $ 2,700 $ (436) $ 451 $ 1,531 $ 1,546

Note: To supplement our consolidated financial statements, which are presented on a GAAP basis, we disclose Adjusted EBITDA, a non-GAAP measure that excludes certain amounts. This non-GAAP measure is not in accordance with, or an alternative for, generally accepted accounting principles in the United States. The GAAP measure most comparable to Adjusted EBITDA is GAAP net (loss) income. A reconciliation of this non-GAAP financial measure to the corresponding GAAP measure is included above.

We define EBITDA as net (loss) income, excluding depreciation and amortization, interest expense, loss on extinguishment of debt, other income (expense), foreign exchange gain (loss) and provision for income taxes. We define Adjusted EBITDA as EBITDA, excluding non-cash share-based compensation expense.

87 © Exa Corporation. All rights reserved.