Free signup for more

- Track your favorite companies

- Receive email alerts for new filings

- Personalized dashboard of news and more

- Access all data and search results

Filing tables

SCI similar filings

- 19 May 14 Submission of Matters to a Vote of Security Holders

- 14 May 14 Service Corporation International Declares Quarterly Cash Dividend

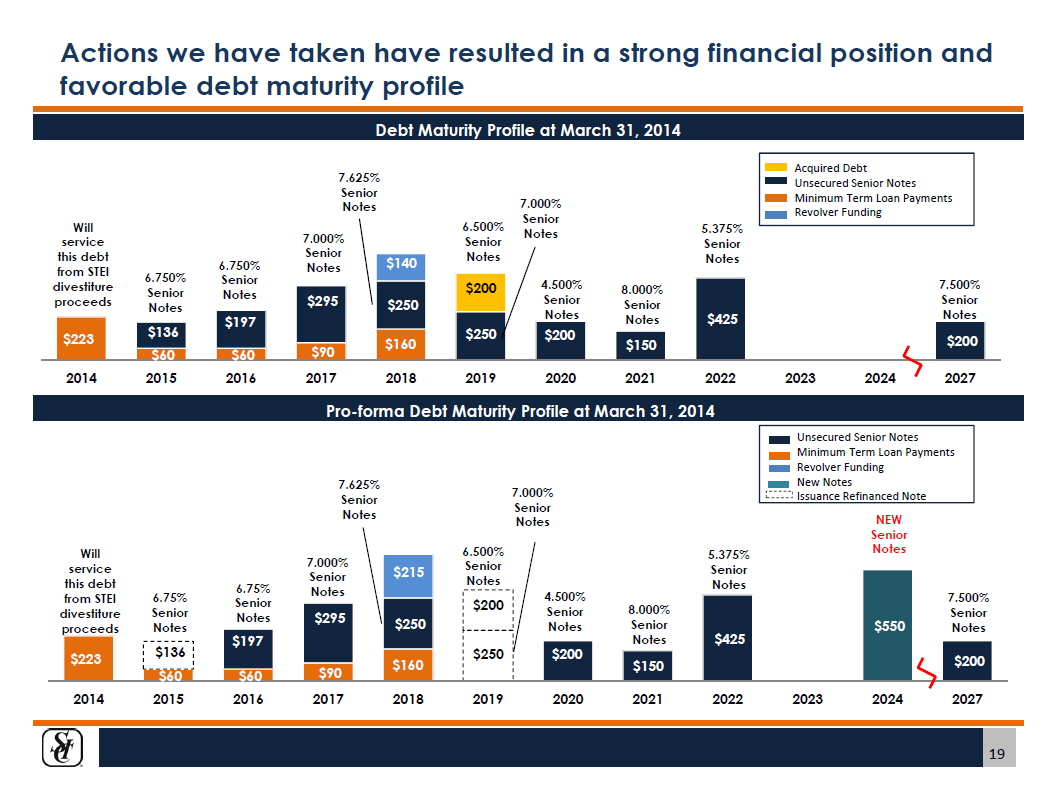

- 12 May 14 Service Corporation International Completes Private Offering of $550 million of 5.375% Senior Notes due 2024

- 29 Apr 14 Regulation FD Disclosure

- 28 Apr 14 Service Corporation International Announces Private Offering of $550 Million of Senior Notes

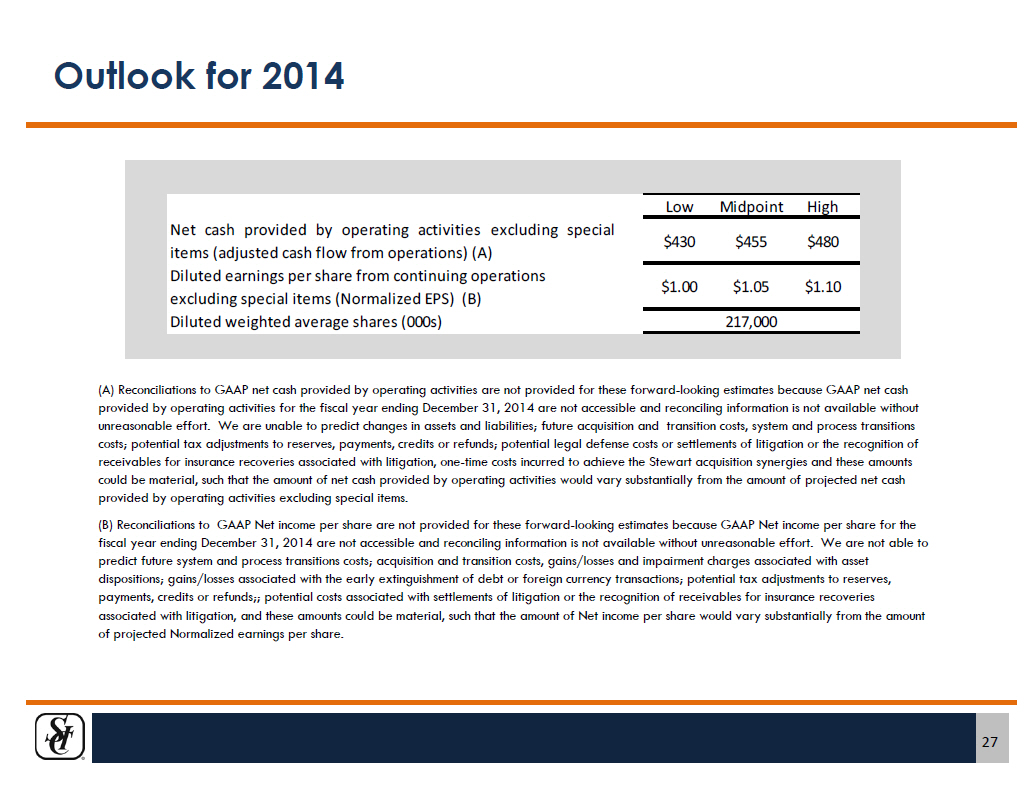

- 23 Apr 14 Service Corporation International Announces First Quarter 2014 Financial Results And Reconfirms Guidance For 2014

- 3 Mar 14 Financial Statements and Exhibits

Filing view

External links