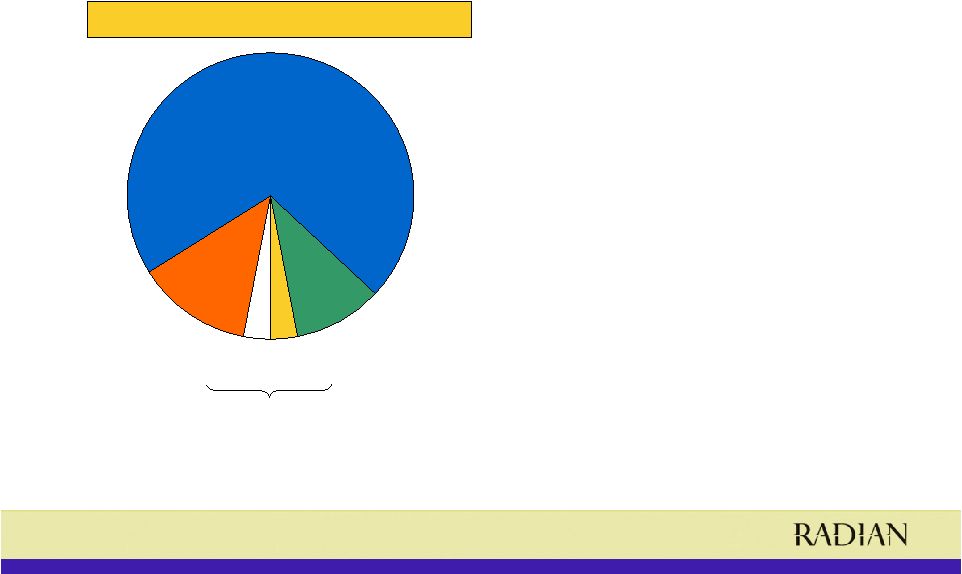

20 NIMS Loss Estimation Methodology • NIMS are bonds whose source of repayment is the excess cash flows coming from other securitizations - Roughly equal to interest income less interest expense less credit losses - Higher losses and faster pre-payment of mortgages in the underlying securitizations decrease a NIM bond’s value by lowering overall cash flows used to pay interest and principal on the bond • A NIMS wrap is a financial guarantee on a NIM bond for payment of principal and interest – typically having a 5 year legal maturity - Claims are paid at maturity when the final amount of any cash shortfall owed to bond holders is known - Accordingly, NIMS cash losses (i.e., paid claims) do not develop like traditional mortgage insurance - Majority of claims are not expected to be paid until 2010 and beyond • Using market based roll rates and internally developed loss assumptions, Radian estimates the losses in the underlying securitizations • Projected pre-payment speeds of the underlying collateral in each securitization incorporate actual historical pre-payment experience • The estimated loss and prepayment speeds are used to estimate the cash flows for each securitization, and thus for each NIM bond • Cash flows are aggregated to arrive at estimated future principal outstanding on each NIM bond at legal maturity • A zero balance implies the cash flows were sufficient to pay the bond off • Any positive balance is paid by Radian, along with any missed interest payments Estimate Losses and Prepayments Estimate Cash Flows Estimate Bond P&I Valuation is more similar to mark to market estimation than a report on current losses |