UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-07154

Cohen & Steers Total Return Realty Fund, Inc.

(Exact name of registrant as specified in charter)

280 Park Avenue, New York, NY 10017

(Address of principal executive offices) (Zip code)

Dana A. DeVivo

Cohen & Steers Capital Management, Inc.

280 Park Avenue

New York, New York 10017

(Name and address of agent for service)

Registrant’s telephone number, including area code: (212) 832-3232

Date of fiscal year end: December 31

Date of reporting period: June 30, 2022

Item 1. Reports to Stockholders.

COHEN & STEERS TOTAL RETURN REALTY FUND, INC.

To Our Shareholders:

We would like to share with you our report for the six months ended June 30, 2022. The total returns for Cohen & Steers Total Return Realty Fund, Inc. (the Fund) and its comparative benchmarks were:

| | | | |

| | | Six Months Ended

June 30, 2022 | |

Cohen & Steers Total Return Realty Fund at Net Asset Valuea | | | –16.62 | % |

Cohen & Steers Total Return Realty Fund at Market Valuea | | | –20.17 | % |

FTSE Nareit All Equity REITs Indexb | | | –19.17 | % |

Blended Benchmark—80% FTSE Nareit All Equity REITs Index/20% ICE BofA REIT Preferred Securities Indexb | | | –18.59 | % |

S&P 500 Indexb | | | –19.96 | % |

The performance data quoted represent past performance. Past performance is no guarantee of future results. The investment return and the principal value of an investment will fluctuate and shares, if sold, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Current total returns of the Fund can be obtained by visiting our website at cohenandsteers.com. The Fund’s returns assume the reinvestment of all dividends and distributions at prices obtained under the Fund’s dividend reinvestment plan. Index performance does not reflect the deduction of any fees, taxes or expenses. An investor cannot invest directly in an index. Performance figures for periods shorter than one year are not annualized.

Managed Distribution Policy

The Fund, acting in accordance with an exemptive order received from the U.S. Securities and Exchange Commission (SEC) and with approval of its Board of Directors (the Board), adopted a managed distribution policy under which the Fund intends to include long-term capital gains, where applicable, as part of the regular monthly cash distributions to its shareholders (the Plan). The Plan gives the Fund greater flexibility to realize long-term capital gains and to distribute those gains on a regular monthly basis. In accordance with the Plan, the Fund currently distributes $0.08 per share on a monthly basis.

The Fund may pay distributions in excess of the Fund’s investment company taxable income and net realized gains. This excess would be a return of capital distributed from the Fund’s assets. Distributions of capital decrease the Fund’s total assets and, therefore, could have the effect of increasing the Fund’s expense ratio. In addition, in order to make these distributions, the Fund may have to sell portfolio securities at a less than opportune time.

| a | As a closed-end investment company, the price of the Fund’s exchange-traded shares will be set by market forces and can deviate from the net asset value (NAV) per share of the Fund. |

| b | The FTSE Nareit All Equity REITs Index contains all tax-qualified REITs with more than 50% of total assets in qualifying real estate assets other than mortgages secured by real property that also meet minimum size and liquidity criteria. The ICE BofA REIT Preferred Securities Index tracks the performance of fixed-rate U.S. dollar-denominated preferred securities issued in the U.S. domestic market including all REITs. The S&P 500 Index is an unmanaged index of 500 large-capitalization stocks that is frequently used as a general measure of U.S. stock market performance. |

1

COHEN & STEERS TOTAL RETURN REALTY FUND, INC.

Shareholders should not draw any conclusions about the Fund’s investment performance from the amount of these distributions or from the terms of the Fund’s Plan. The Fund’s total return based on NAV is presented in the table above as well as in the Consolidated Financial Highlights table.

The Plan provides that the Board may amend or terminate the Plan at any time without prior notice to Fund shareholders; however, at this time, there are no reasonably foreseeable circumstances that might cause the termination. The termination of the Plan could have the effect of creating a trading discount (if the Fund’s stock is trading at or above NAV) or widening an existing trading discount.

Market Review

In the six-month period ended June 30, 2022, U.S. real estate securities declined sharply along with the broader equities market. Amid ongoing supply chain challenges, the U.S. economy slowed abruptly and inflation climbed to a 40-year high as Russia’s invasion of Ukraine in late February led to a pronounced increase in prices for energy and other commodities. Bond yields rose meaningfully and the Federal Reserve (along with most major central banks) began to aggressively raise interest rates to slow demand to check persistently high inflation. While real estate fundamentals generally remained sound, slower growth and higher inflation clouded the outlook for REITs, particularly for sectors lacking pricing power.

Fund Performance

The Fund had a negative total return in the period and outperformed its blended benchmark on a NAV basis but underperformed on a market price basis.

Among REIT common shares, hotels declined but outperformed the benchmark as business and leisure travel continued to rebound (though occupancies remained below pre-pandemic levels). Also, hotels are among the shorter-lease-duration property types, which typically helps the sector’s performance in inflationary environments. The Fund’s security selection in hotels contributed to relative performance.

Despite continued strong demand (and having short-duration leases that can rapidly adjust in inflationary conditions), self storage companies trailed the benchmark on the prospect that a slower economy this year and next could erase the occupancy gains the sector experienced during the pandemic. The Fund’s stock selection in the self storage sector contributed to relative performance. This included an overweight in Public Storage, which investors viewed as a relatively safe haven.

Health care was a relative outperformer, declining less than other REIT sectors as investors favored the shares for the stability of the companies’ rents. An overweight allocation in health care contributed to relative performance.

Residential sectors, including apartments, manufactured homes and single family homes for rent, declined despite demographic tailwinds and a healthy jobs market and as home affordability worsened with sharply higher mortgage rates and the growth in asset values. The Fund’s

selection in residential sectors, particularly apartments, detracted from relative performance. This included having no investment in student housing provider American Campus Communities, which rose as the company agreed to be acquired by a private equity firm in an all-cash deal.

2

COHEN & STEERS TOTAL RETURN REALTY FUND, INC.

Many retail property companies reported record leasing volumes and strong leasing spreads in the period. Despite historically being interest rate-sensitive, net lease property owners outperformed the benchmark given their stable cash flows with long leases amid evidence of solid external growth and increased odds of a recession. Shopping centers modestly underperformed, with grocery-anchored assets seen as being somewhat defensive. Regional mall companies underperformed the index on the marked deterioration in consumer sentiment and its implications for tenants. The Fund’s overweight in free standing REITs aided relative performance, as did our underweight and selection in shopping centers. The portfolio’s overweight allocation in the mall sector (via a position in Simon Property Group) detracted from relative returns. The shares declined meaningfully despite strong demand for Simon’s portfolio of high-quality assets, as concerns of a consumer slowdown took precedence.

Demand for warehouse space remained high, but growth expectations for the industrial sector diminished with Amazon’s plans to scale back the growth of its logistics space usage. In recent years, the internet retailer played a key role in industrial space leasing. However, it is believed that other retailers will continue to add warehouse space, mostly offsetting Amazon’s curtailed plans. The portfolio’s security selection in the industrial sector was a significant factor in relative performance. Contributors included an overweight in refrigerated warehouse specialist Americold, which outperformed as improvements in labor availability translated into better production, higher inventory and pricing power for the company. An overweight in Duke Realty was also beneficial as the company agreed to be acquired by Prologis at a premium price.

Office REITs continued to underperform, as earnings results underscored a difficult leasing environment. Although the number of daily commuters to offices continues to climb, occupancies are still below 50% and the long-term impact on tenant demand due to work-from-home policies remains uncertain, which has also affected asset values. The Fund’s underweight allocation and selection in the office sector contributed to relative performance.

Although lumber prices declined materially in the first half of 2022, timber REITs held up relatively well. With rising mortgage rates and home prices, affordability is stretched and home sales have begun slowing, which we think could impact lumber prices in the future. The timing of our allocations in the sector modestly aided relative returns.

Infrastructure REITs outperformed on healthy leasing activity from wireless carriers rolling out 5G telecom equipment and as mobile data usage continues to grow. The Fund’s stock selection and overweight allocation in the sector was beneficial to relative performance. In contrast, data centers appeared to be caught up in this year’s technology stock selloff. The sector underperformed other REIT categories despite strong underlying fundamentals. Tenant demand has shown no signs of abating, with capital spending for cloud computing expected to accelerate in 2022, for instance. Our underweight in data centers contributed to relative performance. However, this was offset by adverse security selection in the sector.

The Fund held a modest out-of-index investment in private real estate in the period, which offered an attractive yield and access to investments that are often overlooked by listed real estate companies. The Fund’s allocation to private real estate contributed to relative performance.

3

COHEN & STEERS TOTAL RETURN REALTY FUND, INC.

Preferred securities also had broad-based declines, along with other fixed income segments. In addition to preferred securities contending with rising interest rates, the actions and comments from central banks caused credit spreads to widen. The macro headwinds rattling financial markets notwithstanding, fundamentals for issuers of preferreds remained generally solid. The Fund’s security selection in preferred securities aided relative returns. However, the positive effect was partially offset by our underweight in preferreds, which overall outperformed common stocks. The Fund’s out-of-benchmark allocation to corporate bonds also contributed to performance, as these holdings declined but held up better than real estate stocks in the period.

Impact of Derivatives on Fund Performance

The Fund engaged in the buying and selling of single stock options with the intention of enhancing total returns and reducing overall volatility. These contracts did not have a material effect on the Fund’s total return for the six-month period ended June 30, 2022.

The Fund also used forward foreign currency exchange contracts for managing currency risk on certain Fund positions denominated in foreign currencies. The currency forwards did not have a material effect on the Fund’s total return for the six-month period ended June 30, 2022.

Sincerely,

| | |

| |

|

| |

WILLIAM F. SCAPELL | | JASON YABLON |

Portfolio Manager | | Portfolio Manager |

|

|

|

| MATHEW KIRSCHNER |

| Portfolio Manager |

The views and opinions in the preceding commentary are subject to change without notice and are as of the date of the report. There is no guarantee that any market forecast set forth in the commentary will be realized. This material represents an assessment of the market environment at a specific point in time, should not be relied upon as investment advice and is not intended to predict or depict performance of any investment.

4

COHEN & STEERS TOTAL RETURN REALTY FUND, INC.

Visit Cohen & Steers online at cohenandsteers.com

For more information about the Cohen & Steers family of mutual funds, visit cohenandsteers.com. Here you will find fund net asset values, fund fact sheets and portfolio highlights, as well as educational resources and timely market updates.

Our website also provides comprehensive information about Cohen & Steers, including our most recent press releases, profiles of our senior investment professionals and their investment approach to each asset class. The Cohen & Steers family of mutual funds specializes in liquid real assets, including real estate securities, listed infrastructure and natural resource equities, as well as preferred securities and other income solutions.

5

COHEN & STEERS TOTAL RETURN REALTY FUND, INC.

Performance Review (Unaudited)

Average Annual Total Returns—For Periods Ended June 30, 2022

| | | | | | | | | | | | | | | | |

| | | 1 Year | | | 5 Years | | | 10 Years | | | Since Inceptiona | |

Fund at NAV | | | –5.17 | % | | | 7.34 | % | | | 8.59 | % | | | 9.65 | % |

Fund at Market Value | | | –12.20 | % | | | 8.99 | % | | | 8.85 | % | | | 9.40 | % |

The performance data quoted represent past performance. Past performance is no guarantee of future results. The investment return will vary and the principal value of an investment will fluctuate and shares, if sold, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Current total returns of the Fund can be obtained by visiting our website at cohenandsteers.com. The Fund’s returns assume the reinvestment of all dividends and distributions at prices obtained under the Fund’s dividend reinvestment plan. The performance table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the sale of Fund shares.

| a | Commencement of investment operations was September 27, 1993. |

6

COHEN & STEERS TOTAL RETURN REALTY FUND, INC.

June 30, 2022

Top Ten Holdingsa

(Unaudited)

| | | | | | | | |

Security | | Value | | | % of

Net

Assets | |

| | |

American Tower Corp. | | $ | 31,046,517 | | | | 8.9 | |

Prologis, Inc. | | | 20,621,927 | | | | 5.9 | |

Public Storage | | | 17,973,522 | | | | 5.2 | |

Welltower, Inc. | | | 16,245,184 | | | | 4.7 | |

Invitation Homes, Inc. | | | 16,218,645 | | | | 4.7 | |

Realty Income Corp. | | | 15,845,808 | | | | 4.6 | |

Duke Realty Corp. | | | 13,880,645 | | | | 4.0 | |

Equinix, Inc. | | | 12,153,556 | | | | 3.5 | |

Extra Space Storage, Inc. | | | 11,597,761 | | | | 3.3 | |

Simon Property Group, Inc. | | | 11,264,061 | | | | 3.3 | |

| a | Top ten holdings (excluding short-term investments and derivative instruments) are determined on the basis of the value of individual securities held. The Fund may also hold positions in other securities issued by the companies listed above. See the Consolidated Schedule of Investments for additional details on such other positions. |

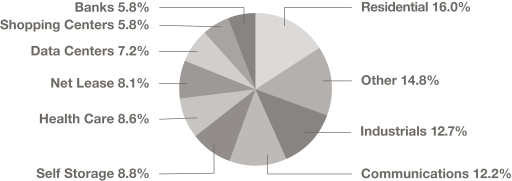

Sector Breakdownb

(Based on Net Assets)

(Unaudited)

| b | Excludes derivative instruments. |

7

COHEN & STEERS TOTAL RETURN REALTY FUND, INC.

CONSOLIDATED SCHEDULE OF INVESTMENTS

June 30, 2022 (Unaudited)

| | | | | | | | | | | | |

| | | | Shares | | | Value | |

COMMON STOCK | | | 79.3% | | | | | | | | | |

COMMUNICATIONS—TOWERS | | | 12.1% | | | | | | | | | |

American Tower Corp. | | | | 121,470 | | | $ | 31,046,517 | |

Crown Castle International Corp. | | | | 64,762 | | | | 10,904,626 | |

| | | | | | | | | |

| | | | 41,951,143 | |

| | | | | |

REAL ESTATE | | | 67.2% | | | | | | | | | |

DATA CENTERS | | | 6.2% | | | | | | | | | |

Digital Realty Trust, Inc. | | | | 71,556 | | | | 9,290,115 | |

Equinix, Inc. | | | | 18,498 | | | | 12,153,556 | |

| | | | | | | | | |

| | | | 21,443,671 | |

| | | | | |

HEALTH CARE | | | 8.6% | | | | | | | | | |

Healthcare Trust of America, Inc., Class A | | | | 133,347 | | | | 3,721,715 | |

Healthpeak Properties, Inc. | | | | 283,149 | | | | 7,336,391 | |

Ventas, Inc. | | | | 51,706 | | | | 2,659,239 | |

Welltower, Inc. | | | | 197,270 | | | | 16,245,184 | |

| | | | | | | | | |

| | | | 29,962,529 | |

| | | | | |

HOTEL | | | 1.4% | | | | | | | | | |

Host Hotels & Resorts, Inc. | | | | 304,256 | | | | 4,770,734 | |

| | | | | | | | | |

INDUSTRIALS | | | 12.3% | | | | | | | | | |

Americold Realty Trust, Inc. | | | | 210,861 | | | | 6,334,265 | |

BG LLH, LLC (Lineage Logistics)a,b | | | | 21,740 | | | | 1,974,209 | |

Duke Realty Corp. | | | | 252,605 | | | | 13,880,645 | |

Prologis, Inc.c | | | | 175,282 | | | | 20,621,927 | |

| | | | | | | | | |

| | | | 42,811,046 | |

| | | | | |

NET LEASE | | | 7.4% | | | | | | | | | |

NETSTREIT Corp.c | | | | 100,044 | | | | 1,887,830 | |

Realty Income Corp. | | | | 232,139 | | | | 15,845,808 | |

Spirit Realty Capital, Inc. | | | | 119,672 | | | | 4,521,208 | |

VICI Properties, Inc. | | | | 117,016 | | | | 3,485,907 | |

| | | | | | | | | |

| | | | 25,740,753 | |

| | | | | |

OFFICE | | | 0.7% | | | | | | | | | |

Highwoods Properties, Inc. | | | | 71,119 | | | | 2,431,559 | |

| | | | | | | | | |

See accompanying notes to the consolidated financial statements.

8

COHEN & STEERS TOTAL RETURN REALTY FUND, INC.

CONSOLIDATED SCHEDULE OF INVESTMENTS—(Continued)

June 30, 2022 (Unaudited)

| | | | | | | | | | | | |

| | | | Shares | | | Value | |

RESIDENTIAL | | | 15.1% | | | | | | | | | |

APARTMENT | | | 8.3% | | | | | | | | | |

Apartment Income REIT Corp. | | | | 67,866 | | | $ | 2,823,226 | |

Camden Property Trust | | | | 34,958 | | | | 4,701,152 | |

Essex Property Trust, Inc. | | | | 20,120 | | | | 5,261,581 | |

Mid-America Apartment Communities, Inc. | | | | 41,239 | | | | 7,203,216 | |

UDR, Inc. | | | | 189,607 | | | | 8,729,506 | |

| | | | | | | | | |

| | | | 28,718,681 | |

| | | | | |

MANUFACTURED HOME | | | 2.1% | | | | | | | | | |

Sun Communities, Inc. | | | | 46,013 | | | | 7,332,632 | |

| | | | | | | | | |

SINGLE FAMILY | | | 4.7% | | | | | | | | | |

Invitation Homes, Inc. | | | | 455,836 | | | | 16,218,645 | |

| | | | | | | | | |

TOTAL RESIDENTIAL | | | | | | | | 52,269,958 | |

| | | | | |

SELF STORAGE | | | 8.5% | | | | | | | | | |

Extra Space Storage, Inc. | | | | 68,174 | | | | 11,597,761 | |

Public Storage | | | | 57,484 | | | | 17,973,522 | |

| | | | | | | | | |

| | | | 29,571,283 | |

| | | | | |

SHOPPING CENTERS | | | 4.8% | | | | | | | | | |

COMMUNITY CENTER | | | 1.5% | | | | | | | | | |

Kimco Realty Corp. | | | | 265,163 | | | | 5,242,273 | |

| | | | | | | | | |

REGIONAL MALL | | | 3.3% | | | | | | | | | |

Simon Property Group, Inc. | | | | 118,669 | | | | 11,264,061 | |

| | | | | | | | | |

Total Shopping Centers | | | | | | | | 16,506,334 | |

| | | | | |

SPECIALTY | | | 1.3% | | | | | | | | | |

Lamar Advertising Co., Class A | | | | 52,966 | | | | 4,659,419 | |

| | | | | | | | | |

TIMBER | | | 0.9% | | | | | | | | | |

Weyerhaeuser Co. | | | | 97,172 | | | | 3,218,337 | |

| | | | | | | | | |

TOTAL REAL ESTATE | | | | | | | | 233,385,623 | |

| | | | | |

TOTAL COMMON STOCK

(Identified cost—$197,957,783) | | | | | | | | 275,336,766 | |

| | | | | |

PREFERRED SECURITIES—$25 PAR VALUE | | | 8.5% | | | | | | | | | |

BANKS | | | 0.6% | | | | | | | | | |

JPMorgan Chase & Co., 5.75%, Series DDd | | | | 25,000 | | | | 622,750 | |

JPMorgan Chase & Co., 4.75%, Series GGd | | | | 25,000 | | | | 533,750 | |

See accompanying notes to the consolidated financial statements.

9

COHEN & STEERS TOTAL RETURN REALTY FUND, INC.

CONSOLIDATED SCHEDULE OF INVESTMENTS—(Continued)

June 30, 2022 (Unaudited)

| | | | | | | | | | | | |

| | | | Shares | | | Value | |

JPMorgan Chase & Co., 4.625%, Series LLd | | | | 22,843 | | | $ | 453,662 | |

Wells Fargo & Co., 4.25%, Series DDd | | | | 9,775 | | | | 171,844 | |

Wells Fargo & Co., 4.75%, Series Zd | | | | 18,400 | | | | 357,880 | |

| | | | | | | | | |

| | | | 2,139,886 | |

| | | | | |

ELECTRIC | | | 0.4% | | | | | | | | | |

CMS Energy Corp., 5.625%, due 3/15/78 | | | | 5,162 | | | | 126,985 | |

CMS Energy Corp., 5.875%, due 10/15/78 | | | | 17,000 | | | | 396,440 | |

CMS Energy Corp., 5.875%, due 3/1/79 | | | | 20,000 | | | | 476,400 | |

DTE Energy Co., 5.25%, due 12/1/77, Series E | | | | 12,000 | | | | 285,600 | |

Southern Co./The, 4.95%, due 1/30/80, Series 2020 | | | | 7,000 | | | | 152,971 | |

| | | | | | | | | |

TOTAL ELECTRIC | | | | | | | | 1,438,396 | |

| | | | | |

FINANCIAL—INVESTMENT BANKER/BROKER | | | 0.1% | | | | | | | | | |

Morgan Stanley, 6.375% to 10/15/24, Series Id,e | | | | 15,000 | | | | 380,100 | |

| | | | | | | | | |

INSURANCE—MULTI-LINE | | | 0.1% | | | | | | | | | |

Allstate Corp./The, 5.10%, Series Hd | | | | 15,000 | | | | 335,400 | |

| | | | | | | | | |

INTEGRATED TELECOMMUNICATIONS SERVICES | | | 0.3% | | | | | | | | | |

AT&T, Inc., 5.625%, due 8/1/67 | | | | 9,578 | | | | 240,695 | |

AT&T, Inc., 5.00%, Series Ad | | | | 15,000 | | | | 310,350 | |

United States Cellular Corp., 5.50%, due 6/1/70 | | | | 21,378 | | | | 400,410 | |

| | | | | | | | | |

| | | | 951,455 | |

| | | | | |

PIPELINES | | | 0.2% | | | | | | | | | |

Energy Transfer LP, 7.60% to 5/15/24, Series Ed,e | | | | 27,235 | | | | 634,576 | |

| | | | | | | | | |

REAL ESTATE | | | 6.8% | | | | | | | | | |

DATA CENTERS | | | 1.0% | | | | | | | | | |

Digital Realty Trust, Inc., 5.85%, Series Kd | | | | 19,588 | | | | 491,071 | |

Digital Realty Trust, Inc., 5.20%, Series Ld | | | | 10,175 | | | | 242,063 | |

DigitalBridge Group, Inc., 7.15%, Series Id | | | | 74,794 | | | | 1,608,071 | |

DigitalBridge Group, Inc., 7.125%, Series Jd | | | | 43,643 | | | | 940,507 | |

KKR Real Estate Finance Trust, Inc., 6.50%, Series Ad | | | | 15,001 | | | | 326,273 | |

| | | | | | | | | |

| | | | 3,607,985 | |

| | | | | |

DIVERSIFIED | | | 1.0% | | | | | | | | | |

Armada Hoffler Properties, Inc., 6.75%, Series Ad | | | | 53,000 | | | | 1,303,270 | |

EPR Properties, 5.75%, Series Gd | | | | 26,472 | | | | 572,060 | |

Lexington Realty Trust, 6.50%, Series C ($50 Par Value)d | | | | 17,289 | | | | 894,647 | |

Urstadt Biddle Properties, Inc., 5.875%, Series Kd | | | | 25,000 | | | | 538,500 | |

| | | | | | | | | |

| | | | 3,308,477 | |

| | | | | |

See accompanying notes to the consolidated financial statements.

10

COHEN & STEERS TOTAL RETURN REALTY FUND, INC.

CONSOLIDATED SCHEDULE OF INVESTMENTS—(Continued)

June 30, 2022 (Unaudited)

| | | | | | | | | | | | |

| | | | Shares | | | Value | |

HOTEL | | | 1.2% | | | | | | | | | |

Pebblebrook Hotel Trust, 6.30%, Series Fd | | | | 28,944 | | | $ | 600,009 | |

Pebblebrook Hotel Trust, 6.375%, Series Gd | | | | 28,566 | | | | 585,603 | |

Pebblebrook Hotel Trust, 5.70%, Series Hd | | | | 24,000 | | | | 450,960 | |

RLJ Lodging Trust, 1.95%, Series Ad | | | | 33,675 | | | | 873,193 | |

Summit Hotel Properties, Inc., 6.25%, Series Ed | | | | 31,105 | | | | 625,833 | |

Summit Hotel Properties, Inc., 5.875%, Series Fd | | | | 19,054 | | | | 362,026 | |

Sunstone Hotel Investors, Inc., 6.125%, Series Hd | | | | 14,000 | | | | 287,280 | |

Sunstone Hotel Investors, Inc., 5.70%, Series Id | | | | 9,827 | | | | 202,436 | |

| | | | | | | | | |

| | | | 3,987,340 | |

| | | | | |

INDUSTRIALS | | | 0.3% | | | | | | | | | |

PS Business Parks, Inc., 5.20%, Series Yd | | | | 18,000 | | | | 336,060 | |

Rexford Industrial Realty, Inc., 5.625%, Series Cd | | | | 23,833 | | | | 586,530 | |

| | | | | | | | | |

| | | | 922,590 | |

| | | | | |

NET LEASE | | | 0.4% | | | | | | | | | |

Agree Realty Corp., 4.25%, Series Ad | | | | 15,501 | | | | 279,793 | |

Spirit Realty Capital, Inc., 6.00%, Series Ad | | | | 47,667 | | | | 1,140,672 | |

| | | | | | | | | |

| | | | 1,420,465 | |

| | | | | |

OFFICE | | | 1.0% | | | | | | | | | |

Arbor Realty Trust, Inc., 6.375%, Series Dd | | | | 7,200 | | | | 147,672 | |

Brookfield Property Partners LP, 5.75%, Series Ad | | | | 23,926 | | | | 408,656 | |

Brookfield Property Preferred LP, 6.25%, due 7/26/81 | | | | 27,000 | | | | 535,950 | |

City Office REIT, Inc., 6.625%, Series Ad | | | | 20,543 | | | | 434,895 | |

Hudson Pacific Properties, Inc., 4.75%, Series Cd | | | | 28,000 | | | | 533,400 | |

SL Green Realty Corp., 6.50%, Series Id | | | | 14,408 | | | | 359,912 | |

TPG RE Finance Trust, Inc., 6.25%, Series Cd | | | | 9,294 | | | | 184,951 | |

Vornado Realty Trust, 5.25%, Series Md | | | | 20,933 | | | | 414,892 | |

Vornado Realty Trust, 5.25%, Series Nd | | | | 22,545 | | | | 440,980 | |

Vornado Realty Trust, 4.45%, Series Od | | | | 9,077 | | | | 154,672 | |

| | | | | | | | | |

| | | | 3,615,980 | |

| | | | | |

RESIDENTIAL | | | 0.9% | | | | | | | | | |

APARTMENT | | | 0.1% | | | | | | | | | |

Centerspace, 6.625%, Series Cd | | | | 19,695 | | | | 507,737 | |

| | | | | | | | | |

MANUFACTURED HOME | | | 0.4% | | | | | | | | | |

Green Brick Partners, Inc., 5.75%, Series Ad | | | | 6,230 | | | | 131,322 | |

UMH Properties, Inc., 6.75%, Series Cd | | | | 33,269 | | | | 836,716 | |

UMH Properties, Inc., 6.375%, Series Dd | | | | 18,731 | | | | 472,583 | |

| | | | | | | | | |

| | | | 1,440,621 | |

| | | | | |

See accompanying notes to the consolidated financial statements.

11

COHEN & STEERS TOTAL RETURN REALTY FUND, INC.

CONSOLIDATED SCHEDULE OF INVESTMENTS—(Continued)

June 30, 2022 (Unaudited)

| | | | | | | | | | | | |

| | | | Shares | | | Value | |

SINGLE FAMILY | | | 0.4% | | | | | | | | | |

American Homes 4 Rent, 5.875%, Series Gd | | | | 23,645 | | | $ | 578,120 | |

American Homes 4 Rent, 6.25%, Series Hd | | | | 24,838 | | | | 630,140 | |

| | | | | | | | | |

| | | | 1,208,260 | |

| | | | | |

TOTAL RESIDENTIAL | | | | | | | | 3,156,618 | |

| | | | | |

SELF STORAGE | | | 0.3% | | | | | | | | | |

National Storage Affiliates Trust, 6.00%, Series Ad | | | | 15,031 | | | | 372,769 | |

Public Storage, 4.875%, Series Id | | | | 4,981 | | | | 113,716 | |

Public Storage, 4.70%, Series Jd | | | | 268 | | | | 5,917 | |

Public Storage, 4.00%, Series Pd | | | | 33,847 | | | | 618,385 | |

| | | | | | | | | |

| | | | 1,110,787 | |

| | | | | |

SHOPPING CENTERS—COMMUNITY CENTER | | | 0.7% | | | | | | | | | |

Saul Centers, Inc., 6.125%, Series Dd | | | | 39,100 | | | | 907,429 | |

Saul Centers, Inc., 6.00%, Series Ed | | | | 21,465 | | | | 485,646 | |

SITE Centers Corp., 6.375%, Series Ad | | | | 48,952 | | | | 1,192,960 | |

| | | | | | | | | |

| | | | 2,586,035 | |

| | | | | |

TOTAL REAL ESTATE | | | | | | | | 23,716,277 | |

| | | | | | | | | | | | |

TOTAL PREFERRED SECURITIES—$25 PAR VALUE

(Identified cost—$32,239,982) | | | | | | | | 29,596,090 | |

| | | | | |

| | | |

| | | | | | Principal

Amount | | | | |

PREFERRED SECURITIES—CAPITAL SECURITIES | | | 8.4% | | | | | | | | | |

BANKS | | | 3.0% | | | | | | | | | |

Bank of America Corp., 6.10% to 3/17/25, Series AAd,e | | | $ | 567,000 | | | | 558,708 | |

Bank of America Corp., 6.125% to 4/27/27, Series TTd,e | | | | 620,000 | | | | 599,462 | |

Bank of America Corp., 6.25% to 9/5/24, Series Xd,e | | | | 875,000 | | | | 852,687 | |

Bank of New York Mellon Corp./The, 3.75% to 12/20/26, Series Id,e | | | | 388,000 | | | | 317,706 | |

Citigroup, Inc., 4.00% to 12/10/25, Series Wd,e | | | | 900,000 | | | | 780,750 | |

Citigroup, Inc., 4.15% to 11/15/26, Series Yd,e | | | | 400,000 | | | | 322,000 | |

Citigroup, Inc., 5.95% to 1/30/23d,e | | | | 430,000 | | | | 422,389 | |

Citigroup, Inc., 5.95% to 5/15/25, Series Pd,e | | | | 400,000 | | | | 371,841 | |

Citigroup, Inc., 6.25% to 8/15/26, Series Td,e | | | | 430,000 | | | | 420,275 | |

Goldman Sachs Group, Inc./The, 4.125% to 11/10/26, Series Vd,e | | | | 400,000 | | | | 327,500 | |

See accompanying notes to the consolidated financial statements.

12

COHEN & STEERS TOTAL RETURN REALTY FUND, INC.

CONSOLIDATED SCHEDULE OF INVESTMENTS—(Continued)

June 30, 2022 (Unaudited)

| | | | | | | | | | | | |

| | | | | | Principal

Amount | | | Value | |

JPMorgan Chase & Co., 6.10% to 10/1/24, Series Xd,e | | | $ | 430,000 | | | $ | 401,803 | |

JPMorgan Chase & Co., 6.125% to 4/30/24, Series Ud,e | | | | 1,000,000 | | | | 952,570 | |

JPMorgan Chase & Co., 6.75% to 2/1/24, Series Sd,e | | | | 1,080,000 | | | | 1,087,884 | |

PNC Financial Services Group, Inc./The, 6.00% to 5/15/27, Series Ud,e | | | | 300,000 | | | | 288,717 | |

Regions Financial Corp., 5.75% to 6/15/25, Series Dd,e | | | | 200,000 | | | | 198,542 | |

SVB Financial Group, 4.00% to 5/15/26, Series Cd,e | | | | 870,000 | | | | 664,010 | |

SVB Financial Group, 4.25% to 11/15/26, Series Dd,e | | | | 550,000 | | | | 416,023 | |

Wells Fargo & Co., 3.90% to 3/15/26, Series BBd,e | | | | 1,120,000 | | | | 965,300 | |

Wells Fargo & Co., 5.875% to 6/15/25, Series Ud,e | | | | 400,000 | | | | 390,960 | |

| | | | | | | | | |

| | | | 10,339,127 | |

| | | | | |

BANKS—FOREIGN | | | 2.2% | | | | | | | | | |

Banco Santander SA, 7.50% to 2/8/24 (Spain)d,e,f,g | | | | 200,000 | | | | 196,250 | |

Barclays PLC, 8.00% to 6/15/24 (United Kingdom)d,e,g | | | | 800,000 | | | | 788,000 | |

BNP Paribas SA, 6.625% to 3/25/24, 144A (France)d,e,g,h | | | | 600,000 | | | | 577,500 | |

Credit Agricole SA, 6.875% to 9/23/24, 144A (France)d,e,g,h | | | | 300,000 | | | | 289,796 | |

Credit Suisse Group AG, 7.125% to 7/29/22 (Switzerland)d,e,f,g | | | | 500,000 | | | | 499,715 | |

Credit Suisse Group AG, 7.50% to 12/11/23, 144A (Switzerland)d,e,g,h | | | | 700,000 | | | | 668,601 | |

Credit Suisse Group AG, 9.75% to 6/23/27, 144A (Switzerland)d,e,g,h | | | | 400,000 | | | | 409,500 | |

Deutsche Bank AG, 7.50% to 4/30/25 (Germany)d,e,g | | | | 400,000 | | | | 364,000 | |

ING Groep N.V., 5.75% to 11/16/26 (Netherlands)d,e,g | | | | 600,000 | | | | 549,501 | |

ING Groep N.V., 6.75% to 4/16/24 (Netherlands)d,e,f,g | | | | 400,000 | | | | 387,476 | |

Lloyds Banking Group PLC, 7.50% to 6/27/24 (United Kingdom)d,e,g | | | | 400,000 | | | | 388,766 | |

Lloyds Banking Group PLC, 7.50% to 9/27/25 (United Kingdom)d,e,g | | | | 800,000 | | | | 781,738 | |

Societe Generale SA, 8.00% to 9/29/25, 144A (France)d,e,g,h | | | | 800,000 | | | | 784,139 | |

UBS Group AG, 7.00% to 1/31/24, 144A (Switzerland)d,e,g,h | | | | 800,000 | | | | 781,298 | |

| | | | | | | | | |

| | | | 7,466,280 | |

| | | | | |

COMMUNICATIONS | | | 0.0% | | | | | | | | | |

SBA Communications Corp., 3.125%, due 2/1/29 | | | | 100,000 | | | | 82,091 | |

| | | | | | | | | |

See accompanying notes to the consolidated financial statements.

13

COHEN & STEERS TOTAL RETURN REALTY FUND, INC.

CONSOLIDATED SCHEDULE OF INVESTMENTS—(Continued)

June 30, 2022 (Unaudited)

| | | | | | | | | | | | |

| | | | | | Principal

Amount | | | Value | |

ELECTRIC | | | 0.1% | | | | | | | | | |

Southern Co./The, 3.75% to 6/15/26, due 9/15/51, Series 21-Ae | | | $ | 535,000 | | | $ | 455,911 | |

| | | | | | | | | |

FINANCIAL | | | 0.5% | | | | | |

CREDIT CARD | | | 0.1% | | | | | |

American Express Co., 3.55% to 9/15/26d,e | | | | 219,000 | | | | 178,728 | |

| | | | | | | | | |

INVESTMENT BANKER/BROKER | | | 0.4% | | | | | |

Charles Schwab Corp./The, 4.00% to 12/1/30, Series Hd,e | | | | 500,000 | | | | 385,500 | |

Charles Schwab Corp./The, 4.00% to 6/1/26, Series Id,e | | | | 1,250,000 | | | | 1,061,138 | |

| | | | | | | | | |

| | | | 1,446,638 | |

| | | | | |

TOTAL FINANCIAL | | | | | | | | 1,625,366 | |

| | | | | |

INSURANCE | | | 0.4% | | | | | | | | | |

LIFE/HEALTH INSURANCE | | | 0.1% | | | | | |

Prudential Financial, Inc., 5.625% to 6/15/23, due 6/15/43e | | | | 300,000 | | | | 293,154 | |

| | | | | | | | | |

LIFE/HEALTH INSURANCE—FOREIGN | | | 0.1% | | | | | |

Dai-ichi Life Insurance Co., Ltd./The, 4.00% to 7/24/26, 144A (Japan)e,h | | | | 300,000 | | | | 282,132 | |

| | | | | | | | | |

PROPERTY CASUALTY | | | 0.1% | | | | | |

Markel Corp., 6.00% to 6/1/25d,e | | | | 350,000 | | | | 345,625 | |

| | | | | | | | | |

PROPERTY CASUALTY—FOREIGN | | | 0.1% | | | | | |

QBE Insurance Group Ltd., 6.75% to 12/2/24, due 12/2/44 (Australia)e,f | | | | 606,000 | | | | 608,029 | |

| | | | | | | | | |

TOTAL INSURANCE | | | | | | | | 1,528,940 | |

| | | | | |

INTEGRATED TELECOMMUNICATIONS SERVICES—FOREIGN | | | 0.3% | | | | | | | | | |

Vodafone Group PLC, 4.125% to 3/4/31, due 6/4/81 (United Kingdom)e | | | | 800,000 | | | | 600,681 | |

Vodafone Group PLC, 7.00% to 1/4/29, due 4/4/79 (United Kingdom)e | | | | 300,000 | | | | 295,172 | |

| | | | | | | | | |

| | | | | | | | 895,853 | |

| | | | | |

PIPELINES | | | 0.2% | | | | | | | | | |

Energy Transfer LP, 6.50% to 11/15/26, Series Hd,e | | | | 200,000 | | | | 177,283 | |

Energy Transfer LP, 7.125% to 5/15/30, Series Gd,e | | | | 515,000 | | | | 443,236 | |

| | | | | | | | | |

| | | | | | | | 620,519 | |

| | | | | |

See accompanying notes to the consolidated financial statements.

14

COHEN & STEERS TOTAL RETURN REALTY FUND, INC.

CONSOLIDATED SCHEDULE OF INVESTMENTS—(Continued)

June 30, 2022 (Unaudited)

| | | | | | | | | | | | |

| | | | | | Principal

Amount | | | Value | |

PIPELINES—FOREIGN | | | 0.1% | | | | | | | | | |

Enbridge, Inc., 6.00% to 1/15/27, due 1/15/77, Series 16-A (Canada)e | | | $ | 300,000 | | | $ | 277,967 | |

| | | | | | | | | |

REAL ESTATE | | | 1.2% | | | | | | | | | |

DIVERSIFIED | | | 0.1% | | | | | |

Spirit Realty LP, 3.40%, due 1/15/30 | | | | 300,000 | | | | 260,084 | |

| | | | | | | | | |

FINANCE | | | 0.3% | | | | | |

Tanger Properties LP, 2.75%, due 9/1/31 | | | | 225,000 | | | | 176,447 | |

VICI Properties LP, 5.125%, due 5/15/32 | | | | 375,000 | | | | 354,158 | |

VICI Properties LP, 5.625%, due 5/15/52 | | | | 200,000 | | | | 182,431 | |

VICI Properties LP / VICI Note Co Inc., 5.75%, due 2/1/27, 144Ah | | | | 500,000 | | | | 475,352 | |

| | | | | | | | | |

| | | | 1,188,388 | |

| | | | | |

HEALTH CARE | | | 0.0% | | | | | |

Sabra Health Care LP, 3.20%, due 12/1/31 | | | | 100,000 | | | | 79,472 | |

| | | | | | | | | |

HOTEL | | | 0.0% | | | | | |

RLJ Lodging Trust LP, 4.00%, due 9/15/29, 144Ah | | | | 200,000 | | | | 164,642 | |

| | | | | | | | | |

INDUSTRIALS | | | 0.1% | | | | | |

Park Intermediate Holdings LLC/PK Domestic Property LLC/PK Finance Co-Issuer, 4.875%, due 5/15/29, 144Ah | | | | 200,000 | | | | 172,060 | |

| | | | | | | | | |

OFFICE | | | 0.1% | | | | | |

Kilroy Realty LP, 2.65%, due 11/15/33 | | | | 75,000 | | | | 58,142 | |

Office Properties Income Trust, 2.40%, due 2/1/27 | | | | 200,000 | | | | 163,587 | |

Vornado Realty LP, 2.15%, due 6/1/26 | | | | 150,000 | | | | 133,830 | |

| | | | | | | | | |

| | | | 355,559 | |

| | | | | |

RETAIL—FOREIGN | | | 0.4% | | | | | |

Scentre Group Trust 2, 4.75% to 6/24/26, due 9/24/80, 144A (Australia)e,h | | | | 600,000 | | | | 535,314 | |

Scentre Group Trust 2, 5.125% to 6/24/30, due 9/24/80, 144A (Australia)e,h | | | | 1,100,000 | | | | 908,257 | |

| | | | | | | | | |

| | | | 1,443,571 | |

| | | | | |

SHOPPING CENTERS | | | 0.2% | | | | | |

Kite Realty Group Trust, 4.75%, due 9/15/30 | | | | 700,000 | | | | 652,457 | |

| | | | | | | | | |

TOTAL REAL ESTATE | | | | | | | | 4,316,233 | |

| | | | | |

See accompanying notes to the consolidated financial statements.

15

COHEN & STEERS TOTAL RETURN REALTY FUND, INC.

CONSOLIDATED SCHEDULE OF INVESTMENTS—(Continued)

June 30, 2022 (Unaudited)

| | | | | | | | | | | | |

| | | | | | Principal

Amount | | | Value | |

TELECOMMUNICATION | | | 0.1% | | | | | | | | | |

Vodafone Group PLC, 6.25% to 7/3/24, due 10/3/78 (United Kingdom)e,f | | | $ | 400,000 | | | $ | 384,755 | |

| | | | | | | | | |

UTILITIES | | | 0.3% | | | | | | | | | |

ELECTRIC | | | 0.2% | | | | | | | | | |

NextEra Energy Capital Holdings, Inc., 5.00%, due 7/15/32 | | | | 210,000 | | | | 215,339 | |

Sempra Energy, 4.125% to 1/1/27, due 4/1/52e | | | | 500,000 | | | | 401,983 | |

| | | | | | | | | |

| | | | 617,322 | |

| | | | | |

ELECTRIC—FOREIGN | | | 0.1% | | | | | |

Algonquin Power & Utilities Corp., 4.75% to 1/18/27, due 1/18/82 (Canada)e | | | | 400,000 | | | | 333,729 | |

| | | | | | | | | |

TOTAL UTILITIES | | | | | | | | 951,051 | |

| | | | | |

TOTAL PREFERRED SECURITIES—CAPITAL SECURITIES

(Identified cost—$32,332,409) | | | | | | | | 28,944,093 | |

| | | | | | | | |

CORPORATE BONDS | | | 0.9% | | | | | | | | | |

COMMUNICATIONS—TOWERS | | | 0.1% | | | | | | | | | |

SBA Communications Corp., 3.875%, due 2/15/27 | | | | 300,000 | | | | 274,544 | |

| | | | | |

FINANCIAL | | | 0.1% | | | | | | | | | |

Ladder Capital Finance Holdings LLLP/Ladder Capital Finance Corp., 4.75%, due 6/15/29, 4.75%, 144Ah | | | | 300,000 | | | | 231,353 | |

| | | | | | | | | |

INTEGRATED TELECOMMUNICATIONS SERVICES | | | 0.1% | | | | | | | | | |

AT&T, Inc., 2.875%, to 3/2/25, Series Bd,e | | | | 500,000 | | | | 459,102 | |

| | | | | | | | | |

REAL ESTATE | | | 0.6% | | | | | | | | | |

DIVERSIFIED | | | 0.2% | | | | | | | | | |

American Finance Trust, Inc./American Finance Operating Partner LP, 4.50%, due 9/30/28, 144Ah | | | | 550,000 | | | | 432,723 | |

CTR Partnership LP/CareTrust Capital Corp.,

3.875%, due 6/30/28, 144Ah | | | | 400,000 | | | | 342,356 | |

| | | | | | | | | |

| | | | 775,079 | |

| | | | | |

HEALTH CARE | | | 0.0% | | | | | | | | | |

Diversified Healthcare Trust, 9.75%, due 6/15/25 | | | | 150,000 | | | | 148,185 | |

| | | | | | | | | |

NET LEASE | | | 0.3% | | | | | | | | | |

Global Net Lease, Inc./Global Net Lease Operating Partnership LP, 3.75%, due 12/15/27, 144Ah | | | | 300,000 | | | | 250,967 | |

See accompanying notes to the consolidated financial statements.

16

COHEN & STEERS TOTAL RETURN REALTY FUND, INC.

CONSOLIDATED SCHEDULE OF INVESTMENTS—(Continued)

June 30, 2022 (Unaudited)

| | | | | | | | | | | | |

| | | | | | Principal

Amount | | | Value | |

VICI Properties LP/VICI Note Co., Inc., 4.125%, due 8/15/30, 144Ah | | | $ | 594,000 | | | $ | 513,691 | |

VICI Properties LP/VICI Note Co., Inc., 4.25%, due 12/1/26, 144Ah | | | | 350,000 | | | | 320,392 | |

| | | | | | | | | |

| | | | 1,085,050 | |

| | | | | |

SHOPPING CENTERS—REGIONAL MALL | | | 0.1% | | | | | | | | | |

Brookfield Property REIT, Inc./BPR Cumulus LLC/BPR Nimbus LLC/GGSI Sellco LLC, 5.75%, due 5/15/26, 144Ah | | | | 250,000 | | | | 228,820 | |

| | | | | | | | | |

TOTAL REAL ESTATE | | | | | | | | 2,237,134 | |

| | | | | |

TOTAL CORPORATE BONDS

(Identified cost—$3,745,207) | | | | | | | | 3,202,133 | |

| | | | | |

| | | |

| | | | | | Ownership* | | | | |

PRIVATE REAL ESTATE—OFFICE | | | 1.1% | | | | | | | | | |

Legacy Gateway JV LLC, Plano, TXb | | | | 7.9% | | | | 3,801,125 | |

| | | | | |

TOTAL PRIVATE REAL ESTATE

(Identified cost—$3,297,269) | | | | | | | | 3,801,125 | |

| | | | | |

| | | |

| | | | | | Shares | | | | |

SHORT-TERM INVESTMENTS | | | 1.8% | | | | | | | | | |

MONEY MARKET FUNDS | | | | | | | | | | | | |

State Street Institutional Treasury Money Market Fund, Premier Class, 1.04%i | | | | 6,061,601 | | | | 6,061,601 | |

| | | | | |

TOTAL SHORT-TERM INVESTMENTS

(Identified cost—$6,061,601) | | | | | | | | 6,061,601 | |

| | | | | |

PURCHASED OPTION CONTRACTS

(Premiums paid—$11,016) | | | 0.0% | | | | | | | | 750 | |

| | | | | |

TOTAL INVESTMENTSIN SECURITIES

(Identified cost—$275,645,267) | | | 98.9% | | | | | | | | 346,942,558 | |

WRITTEN OPTION CONTRACTS

(Premiums received—$92,686) | | | (0.0) | | | | | | | | (91,178 | ) |

SERIES A CUMULATIVE PREFERRED STOCK,AT LIQUIDATION VALUE | | | (0.1) | | | | | | | | (125,000 | ) |

OTHER ASSETSIN EXCESSOF LIABILITIES | | | 0.0 | | | | | | | | 359,910 | |

| | | | | | | | | | | | |

NET ASSETS (Equivalent to $13.17 per share based on 26,348,094 shares of common stock outstanding) | | | 100.0% | | | | | | | $ | 347,086,290 | |

| | | | | | | | | | | | |

See accompanying notes to the consolidated financial statements.

17

COHEN & STEERS TOTAL RETURN REALTY FUND, INC.

CONSOLIDATED SCHEDULE OF INVESTMENTS—(Continued)

June 30, 2022 (Unaudited)

Exchange-Traded Option Contracts

Purchased Options

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| Description | | Exercise

Price | | Expiration

Date | | | Number of

Contracts | | | Notional

Amountj | | | Premiums

Paid | | | Value | |

Call—Equinix Inc. | | $740.00 | | | 7/15/22 | | | | 11 | | | | $722,722 | | | | $11,016 | | | | $750 | |

| | | | | | | | | | | | | | | | | | | | | | |

Written Options

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| Description | | Exercise

Price | | Expiration

Date | | | Number of

Contracts | | | Notional

Amountj | | | Premiums

Received | | | Value | |

Call—Equinix Inc | | $760.00 | | | 7/15/22 | | | | (22 | ) | | $ | (1,445,444 | ) | | $ | (11,518 | ) | | $ | (676 | ) |

Call—American Tower Corp. | | 270.00 | | | 8/19/22 | | | | (25 | ) | | | (638,975 | ) | | | (9,546 | ) | | | (15,000 | ) |

Call—Weyerhaeuser Co. | | 37.00 | | | 8/19/22 | | | | (160 | ) | | | (529,920 | ) | | | (8,966 | ) | | | (8,000 | ) |

Put—Crown Castle International Corp. | | 160.00 | | | 8/19/22 | | | | (36 | ) | | | (606,168 | ) | | | (13,231 | ) | | | (16,200 | ) |

Put—Iron Mountain Inc. | | 47.50 | | | 7/15/22 | | | | (135 | ) | | | (657,315 | ) | | | (11,282 | ) | | | (12,690 | ) |

Put—Digital Realty Trust Inc. | | 125.00 | | | 8/19/22 | | | | (27 | ) | | | (350,541 | ) | | | (6,979 | ) | | | (13,095 | ) |

Put—Prologis Inc. | | 110.00 | | | 8/19/22 | | | | (58 | ) | | | (682,370 | ) | | | (15,540 | ) | | | (21,460 | ) |

| | | | | | | | | (463 | ) | | $ | (4,910,733 | ) | | $ | (77,062 | ) | | $ | (87,121 | ) |

| |

Over-the-Counter Option Contracs

Written Options

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | |

| Description | | Counterparty | | Exercise

Rate | | | Expiration

Date | | | Number of

Contracts | | | Notional

Amountj | | | Premiums

Received | | | Value | |

Put—Americold Realty Trust | | Goldman Sachs International | | | $26.50 | | | | 7/15/22 | | | | (279 | ) | | | $(838,116 | ) | | | $(15,624 | ) | | | $(4,057 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

Forward Foreign Currency Exchange Contracts

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

| Counterparty | | Contracts to

Deliver | | | In Exchange

For | | | Settlement

Date | | | Unrealized

Appreciation

(Depreciation) | |

Brown Brothers Harriman | | USD | | | 25,123 | | | EUR | | | 23,796 | | | | 7/5/22 | | | $ | (186 | ) |

Brown Brothers Harriman | | USD | | | 476,024 | | | EUR | | | 455,286 | | | | 7/5/22 | | | | 1,093 | |

Brown Brothers Harriman | | EUR | | | 479,082 | | | USD | | | 514,882 | | | | 7/5/22 | | | | 12,827 | |

Brown Brothers Harriman | | EUR | | | 445,352 | | | USD | | | 466,457 | | | | 8/2/22 | | | | (1,107 | ) |

| | | | | | | | | | | | | | | | | | $ | 12,627 | |

| |

See accompanying notes to the consolidated financial statements.

18

COHEN & STEERS TOTAL RETURN REALTY FUND, INC.

CONSOLIDATED SCHEDULE OF INVESTMENTS—(Continued)

June 30, 2022 (Unaudited)

Glossary of Portfolio Abbreviations

| | |

EUR | | Euro Currency |

REIT | | Real Estate Investment Trust |

USD | | United States Dollar |

Note: Percentages indicated are based on the net assets of the Fund.

| * | Ownership % represents the Fund’s contractual ownership in the limited liability company prior to the impact of promote structures. |

| a | Restricted security. Aggregate holdings equal 0.4% of the net assets of the Fund. This security was acquired on August 3, 2020, at a cost of $1,335,937 ($62.50 per share). Security value is determined based on significant unobservable inputs (Level 3). |

| b | Security value is determined based on significant unobservable inputs (Level 3). |

| c | All or a portion of the security is pledged in connection with written option contracts. $2,440,639 in aggregate has been pledged as collateral. |

| d | Perpetual security. Perpetual securities have no stated maturity date, but they may be called/redeemed by the issuer. |

| e | Security converts to floating rate after the indicated fixed-rate coupon period. |

| f | Securities exempt from registration under Regulation S of the Securities Act of 1933. These securities are subject to resale restrictions. Aggregate holdings amounted to $2,076,225 which represents 0.6% of the net assets of the Fund, of which 0.0% are illiquid. |

| g | Contingent Capital security (CoCo). CoCos are debt or preferred securities with loss absorption characteristics built into the terms of the security for the benefit of the issuer. Aggregate holdings amounted to $7,466,280 which represents 2.2% of the net assets of the Fund. |

| h | Securities exempt from registration under Rule 144A of the Securities Act of 1933. These securities may only be resold to qualified institutional buyers. Aggregate holdings amounted to $8,368,893 which represents 2.4% of the net assets of the Fund, of which 0.0% are illiquid. |

| i | Rate quoted represents the annualized seven-day yield. |

| j | Represents number of contracts multiplied by notional contract size multiplied by the underlying price. |

See accompanying notes to the consolidated financial statements.

19

COHEN & STEERS TOTAL RETURN REALTY FUND, INC.

CONSOLIDATED STATEMENT OF ASSETS AND LIABILITIES

June 30, 2022 (Unaudited)

| | | | |

ASSETS: | |

Investments in securities, at value (Identified cost—$275,645,267) | | $ | 346,942,558 | |

Cash | | | 121,640 | |

Foreign currency, at value (Identified cost—$402) | | | 393 | |

Receivable for: | | | | |

Dividends and interest | | | 1,160,518 | |

Investment securities sold | | | 491,486 | |

Unrealized appreciation on forward foreign currency exchange contracts | | | 13,920 | |

Other assets | | | 31,612 | |

| | | | |

Total Assets | | | 348,762,127 | |

| | | | |

LIABILITIES: | |

Written option contracts, at value (Premiums received—$92,686) | | | 91,178 | |

Unrealized depreciation on forward foreign currency exchange contracts | | | 1,293 | |

Payable for: | | | | |

Investment securities purchased | | | 961,003 | |

Investment advisory fees | | | 201,555 | |

Administration fees | | | 11,517 | |

Directors’ fees | | | 191 | |

Other liabilities | | | 284,100 | |

| | | | |

Total Liabilities | | | 1,550,837 | |

| | | | |

Series A Cumulative Preferred Stock (Preferred Stock) (125 shares authorized and issued at $1,000 per share) (Note 7) | | | 125,000 | |

| | | | |

NET ASSETS APPLICABLE TO COMMON SHAREHOLDERS | | $ | 347,086,290 | |

| | | | |

NET ASSETS Applicable to Common Shareholders consist of: | |

Paid-in capital | | | 263,329,649 | |

Total distributable earnings/(accumulated loss) | | | 83,756,641 | |

| | | | |

| | $ | 347,086,290 | |

| | | | |

NET ASSET VALUE PER COMMON SHARE: | |

($347,086,290 ÷ 26,348,094 common shares outstanding) | | $ | 13.17 | |

| | | | |

MARKET PRICE PER COMMON SHARE | | $ | 13.25 | |

| | | | |

MARKET PRICE PREMIUM (DISCOUNT) TO NET ASSET VALUE PER COMMON SHARE | | | 0.61 | % |

| | | | |

See accompanying notes to the consolidated financial statements.

20

COHEN & STEERS TOTAL RETURN REALTY FUND, INC.

CONSOLIDATED STATEMENT OF OPERATIONS

For the Six Months Ended June 30, 2022 (Unaudited)

| | | | |

Investment Income: | |

Dividend income | | $ | 3,980,528 | |

Interest income | | | 685,054 | |

| | | | |

Total Investment Income | | | 4,665,582 | |

| | | | |

Expenses: | |

Investment advisory fees | | | 1,330,230 | |

Shareholder reporting expenses | | | 120,468 | |

Professional fees | | | 116,158 | |

Administration fees | | | 103,743 | |

Custodian fees and expenses | | | 38,539 | |

Transfer agent fees and expenses | | | 17,748 | |

Directors’ fees and expenses | | | 6,668 | |

Miscellaneous | | | 10,749 | |

| | | | |

Total Expenses | | | 1,744,303 | |

| | | | |

Net Investment Income (Loss) | | | 2,921,279 | |

| | | | |

Net Realized and Unrealized Gain (Loss): | |

Net realized gain (loss) on: | |

Investments in securities | | | 10,523,324 | |

Written option contracts | | | 246,485 | |

Forward foreign currency exchange contracts | | | 31,387 | |

Foreign currency transactions | | | (1,105 | ) |

| | | | |

Net realized gain (loss) | | | 10,800,091 | |

| | | | |

Net change in unrealized appreciation (depreciation) on: | |

Investments in securities | | | (84,078,127 | ) |

Written option contracts | | | 11,176 | |

Forward foreign currency exchange contracts | | | 16,701 | |

Foreign currency translations | | | 56 | |

| | | | |

Net change in unrealized appreciation (depreciation) | | | (84,050,194 | ) |

| | | | |

Net Realized and Unrealized Gain (Loss) | | | (73,250,103 | ) |

| | | | |

Net Increase (Decrease) in Net Assets Resulting from Operations | | | (70,328,824 | ) |

| | | | |

Distributions Paid to Series A Cumulative Preferred Stockholders (Note 7) | | | (6,416 | ) |

| | | | |

Net Increase (Decrease) in Net Assets Applicable to Common Shareholders From Operations | | $ | (70,335,240 | ) |

| | | | |

See accompanying notes to the consolidated financial statements.

21

COHEN & STEERS TOTAL RETURN REALTY FUND, INC.

CONSOLIDATED STATEMENT OF CHANGES IN NET ASSETS APPLICABLE TO COMMON SHARES (Unaudited)

| | | | | | | | |

| | | For the

Six Months Ended

June 30, 2022 | | | For the

Year Ended

December 31, 2021 | |

Change in Net Assets Applicable to Common Shareholders: | |

From Operations: | | | | | | | | |

Net investment income (loss) | | $ | 2,921,279 | | | $ | 4,693,083 | |

Net realized gain (loss) | | | 10,800,091 | | | | 32,807,106 | |

Net change in unrealized appreciation (depreciation) | | | (84,050,194 | ) | | | 78,142,214 | |

Distributions paid to Series A Cumulative Preferred Stockholders | | | (6,416 | ) | | | — | |

| | | | | | | | |

Net increase (decrease) in net assets applicable to Common Shareholders from operations | | | (70,335,240 | ) | | | 115,642,403 | |

| | | | | | | | |

Distributions to Common Shareholders | | | (12,635,361 | ) | | | (30,739,379 | ) |

| | | | | | | | |

Capital Stock Transactions: | | | | | | | | |

Increase (decrease) in net assets from Fund share transactions | | | 712,300 | | | | 909,057 | |

Decrease in net assets from offering expenses from issuance of preferred stock | | | (19,400 | ) | | | — | |

| | | | | | | | |

Net increase (decrease) in net assets from capital stock transactions | | | 692,900 | | | | 909,057 | |

| | | | | | | | |

Total increase (decrease) in net assets applicable to Common Shareholders | | | (82,277,701 | ) | | | 85,812,081 | |

Net Assets Applicable to Common Shareholders: | | | | | | | | |

Beginning of period | | | 429,363,991 | | | | 343,551,910 | |

| | | | | | | | |

End of period | | $ | 347,086,290 | | | $ | 429,363,991 | |

| | | | | | | | |

See accompanying notes to the consolidated financial statements.

22

COHEN & STEERS TOTAL RETURN REALTY FUND, INC.

CONSOLIDATED FINANCIAL HIGHLIGHTS (Unaudited)

The following table includes selected data for a common share outstanding throughout each period and other performance information derived from the financial statements. It should be read in conjunction with the financial statements and notes thereto.

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | For the Six

Months Ended

June 30, 2022a | | | For the Year Ended December 31, |

Per Share Operating Data: | | 2021a | | | 2020 | | | 2019 | | | 2018 | | | 2017 | |

Net asset value per common share, beginning of period | | | $16.33 | | | | $13.09 | | | | $14.21 | | | | $11.89 | | | | $13.41 | | | | $13.35 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Income (loss) from investment operations: | |

Net investment income (loss)b | | | 0.11 | | | | 0.18 | | | | 0.26 | | | | 0.29 | | | | 0.30 | | | | 0.30 | |

Net realized and unrealized gain (loss) | | | (2.79 | ) | | | 4.23 | | | | (0.37 | ) | | | 2.99 | | | | (0.86 | )c | | | 0.72 | |

Distributions paid to Series A Cumulative Preferred Stockholders | | | (0.00 | )d | | | — | | | | — | | | | — | | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total from investment operations applicable to common shares | | | (2.68 | ) | | | 4.41 | | | | (0.11 | ) | | | 3.28 | | | | (0.56 | ) | | | 1.02 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Less dividends and distributions to common shareholders from: | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | (0.48 | ) | | | (0.21 | ) | | | (0.26 | ) | | | (0.30 | ) | | | (0.30 | ) | | | (0.31 | ) |

Net realized gain | | | — | | | | (0.96 | ) | | | (0.75 | ) | | | (0.66 | ) | | | (0.66 | ) | | | (0.63 | ) |

Tax return of capital | | | — | | | | — | | | | — | | | | — | | | | — | | | | (0.02 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total dividends and distributions to common shareholders | | | (0.48 | ) | | | (1.17 | ) | | | (1.01 | ) | | | (0.96 | ) | | | (0.96 | ) | | | (0.96 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

Anti-dilutive effect from the issuance of reinvested shares | | | — | | | | 0.00 | d | | | 0.00 | d | | | 0.00 | d | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Net increase (decrease) in net asset value per common share | | | (3.16 | ) | | | 3.24 | | | | (1.12 | ) | | | 2.32 | | | | (1.52 | ) | | | 0.06 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

Net asset value per common share, end of period | | | $13.17 | | | | $16.33 | | | | $13.09 | | | | $14.21 | | | | $11.89 | | | | $13.41 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

Market value per common share, end of period | | | $13.25 | | | | $17.16 | | | | $13.27 | | | | $14.48 | | | | $10.75 | | | | $12.77 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

|

| | |

Total net asset value returne | | | –16.62 | %f | | | 34.70 | % | | | 0.01 | % | | | 28.14 | % | | | –4.04 | %c | | | 8.33 | % |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total market value returne | | | –20.17 | %f | | | 39.63 | % | | | –0.50 | % | | | 44.42 | % | | | –8.89 | % | | | 13.82 | % |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

See accompanying notes to the consolidated financial statements.

23

COHEN & STEERS TOTAL RETURN REALTY FUND, INC.

CONSOLIDATED FINANCIAL HIGHLIGHTS (Unaudited)—(Continued)

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | For the Six

Months Ended

June 30, 2022a | | | For the Year Ended December 31, |

Ratios/Supplemental Data: | | 2021a | | | 2020 | | | 2019 | | | 2018 | | | 2017 | |

Net assets applicable to common shareholders, end of period (in millions) | | $ | 347.1 | | | $ | 429.4 | | | $ | 343.6 | | | $ | 372.1 | | | $ | 310.7 | | | $ | 350.6 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Ratios to average daily net assets: | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

Expenses | | | 0.92 | %g,h | | | 0.89 | % | | | 0.88 | % | | | 0.86 | % | | | 0.89 | %c | | | 0.87 | % |

| | | | | | | | | | | | | | | | | | | | | | | | |

Net investment income (loss) | | | 1.54 | %g,h | | | 1.21 | % | | | 2.10 | % | | | 2.16 | % | | | 2.41 | % | | | 2.24 | % |

| | | | | | | | | | | | | | | | | | | | | | | | |

Portfolio turnover rate | | | 15 | %f | | | 38 | % | | | 53 | % | | | 52 | % | | | 29 | % | | | 29 | % |

| | | | | | | | | | | | | | | | | | | | | | | | |

Series A Cumulative Preferred Stock at liquidation value, end of period (in 000s) | | $ | 125.0 | | | | — | | | | — | | | | — | | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Asset coverage ratio for Series A Cumulative Preferred Stock | | | 277,769 | % | | | — | | | | — | | | | — | | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Asset coverage, per $1,000 liquidation value per share of Series A Cumulative Preferred Stock | | $ | 2,777,690 | | | | — | | | | — | | | | — | | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| a | Consolidated (see Note 1). |

| b | Calculation based on average shares outstanding. |

| c | During the reporting period the Fund settled legal claims against two issuers of securities previously held by the Fund. As a result, the net realized and unrealized gain (loss) on investments per share includes proceeds received from the settlements. Without these proceeds the net realized and unrealized gain (loss) on investments per share would have been $(0.87). Additionally, the expense ratio includes extraordinary expenses related to the direct action. Without these expenses, the ratio of expenses to average daily net assets would have been 0.88%. Excluding the proceeds from and expenses relating to the settlements, the total return on a NAV basis would have been -4.10%. |

| d | Amount is less than $0.005. |

| e | Total net asset value return measures the change in net asset value per share over the period indicated. Total market value return is computed based upon the Fund’s market price per share and excludes the effects of brokerage commissions. Dividends and distributions are assumed, for purposes of these calculations, to be reinvested at prices obtained under the Fund’s dividend reinvestment plan. |

| h | Calculated on the basis of average net assets of common stock shareholders. Ratios do not reflect the effect of dividend payments to Series A Cumulative Preferred Stockholders. |

See accompanying notes to the consolidated financial statements.

24

COHEN & STEERS TOTAL RETURN REALTY FUND, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

Note 1. Organization and Significant Accounting Policies

Cohen & Steers Total Return Realty Fund, Inc. (the Fund) was incorporated under the laws of the State of Maryland on September 4, 1992 and is registered under the Investment Company Act of 1940 (the 1940 Act) as a diversified, closed-end management investment company. The Fund’s investment objective is high total return through investment in real estate securities.

Cohen & Steers RFI Trust (the REIT Subsidiary), is a wholly-owned subsidiary of the Fund organized under the laws of the state of Maryland as a statutory trust on September 29, 2021 that commenced operations on November 30, 2021. The REIT Subsidiary acts as an investment vehicle for the Fund in order to effect certain investments on behalf of the Fund, consistent with the Fund’s investment objectives and policies. The Fund expects that it will achieve a significant portion of its exposure to private real estate investments through investment in the REIT Subsidiary. The REIT Subsidiary may use wholly-owned, limited liability companies to contain the exposure of individual private real estate investments. Unlike the Fund, the REIT Subsidiary may invest without limitation in private real estate. Investments in the REIT Subsidiary are limited to 25% of the Fund’s total assets. The Consolidated Schedule of Investments includes positions of the Fund and the REIT Subsidiary. The financial statements have been consolidated and include the accounts of the Fund and the REIT Subsidiary. All significant inter-company balances and transactions have been eliminated in consolidation.

The following is a summary of significant accounting policies consistently followed by the Fund in the preparation of its consolidated financial statements. The Fund is an investment company and, accordingly, follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board Accounting Standards Codification (ASC) Topic 946—Investment Companies. The accounting policies of the Fund are in conformity with accounting principles generally accepted in the United States of America (GAAP). The preparation of the consolidated financial statements in accordance with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the consolidated financial statements and the reported amounts of income and expenses during the reporting period. Actual results could differ from those estimates.

Portfolio Valuation: Investments in securities that are listed on the New York Stock Exchange (NYSE) are valued, except as indicated below, at the last sale price reflected at the close of the NYSE on the business day as of which such value is being determined. If there has been no sale on such day, the securities are valued at the mean of the closing bid and ask prices on such day or, if no ask price is available, at the bid price. Exchange-traded options are valued at their last sale price as of the close of options trading on applicable exchanges on the valuation date. In the absence of a last sale price on such day, options are valued at the average of the quoted bid and ask prices as of the close of business. Over-the-counter (OTC) options are valued based upon prices provided by a third-party pricing service or counterparty. Forward foreign currency exchange contracts are valued daily at the prevailing forward exchange rate.

Securities not listed on the NYSE but listed on other domestic or foreign securities exchanges (including NASDAQ) are valued in a similar manner. Securities traded on more than one securities exchange are valued at the last sale price reflected at the close of the exchange representing the principal market for such securities on the business day as of which such value is being determined. If

25

COHEN & STEERS TOTAL RETURN REALTY FUND, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)—(Continued)

after the close of a foreign market, but prior to the close of business on the day the securities are being valued, market conditions change significantly, certain non-U.S. equity holdings may be fair valued pursuant to procedures established by the Board of Directors.

Readily marketable securities traded in the OTC market, including listed securities whose primary market is believed by Cohen & Steers Capital Management, Inc. (the investment advisor) to be OTC, are valued on the basis of prices provided by a third-party pricing service or third-party broker-dealers when such prices are believed by the investment advisor, pursuant to delegation by the Board of Directors, to reflect the fair value of such securities.

Fixed-income securities are valued on the basis of prices provided by a third-party pricing service or third-party broker-dealers when such prices are believed by the investment advisor, pursuant to delegation by the Board of Directors, to reflect the fair value of such securities. The pricing services or broker-dealers use multiple valuation techniques to determine fair value. In instances where sufficient market activity exists, the pricing services or broker-dealers may utilize a market-based approach through which quotes from market makers are used to determine fair value. In instances where sufficient market activity may not exist or is limited, the pricing services or broker-dealers also utilize proprietary valuation models which may consider market transactions in comparable securities and the various relationships between securities in determining fair value and/or characteristics such as benchmark yield curves, option-adjusted spreads, credit spreads, estimated default rates, coupon rates, anticipated timing of principal repayments, underlying collateral, and other unique security features which are then used to calculate the fair values.

Short-term debt securities with a maturity date of 60 days or less are valued at amortized cost, which approximates fair value. Investments in open-end mutual funds are valued at net asset value (NAV).

The Fund utilizes an independent valuation services firm (the Independent Valuation Advisor) to assist the investment manager in the determination of the Fund’s fair value of private real estate investments held by the REIT Subsidiary. Limited scope appraisals are prepared on a monthly basis and typically include a limited comparable sales and a full discounted cash flow analysis. Annually, a full scope, detailed appraisal report is completed which typically includes market analysis, cost approach, sales comparison approach and an income approach containing a discounted cash flow analysis. The full scope report is prepared by a third-party appraisal firm. The investment manager, including through communication with the Independent Valuation Advisor, monitors for material events that the investment manager believes may be expected to have a material impact on the most recent estimated fair values of such private real estate investments. However, rapidly changing market conditions or material events may not be immediately reflected in the Fund’s or REIT Subsidiary’s daily NAV. The investment manager, in conjunction with the Independent Valuation Advisor, values the private real estate investments using the valuation methodology it deems most appropriate and consistent with industry best practices and market conditions. The investment manager expects the primary methodology used to value private real estate investments will be the income approach. Consistent with industry practices, the income approach incorporates actual contractual lease income, professional judgments regarding comparable rental and operating expense data, the capitalization or discount rate and projections of future rent and expenses based on appropriate market evidence, and other subjective factors. Other methodologies that may also be used to value properties include, among other approaches, sales

26

COHEN & STEERS TOTAL RETURN REALTY FUND, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)—(Continued)

comparisons and cost approaches. Private real estate appraisals are reported on a free and clear basis (i.e. any property-level indebtedness that may be in place is not incorporated into the valuation). Property level debt is valued separately in accordance with GAAP.

The policies and procedures approved by the Fund’s Board of Directors delegate authority to make fair value determinations to the investment advisor, subject to the oversight of the Board of Directors. The investment advisor has established a valuation committee (Valuation Committee) to administer, implement and oversee the fair valuation process according to the policies and procedures approved annually by the Board of Directors. Among other things, these procedures allow the Fund to utilize independent pricing services, quotations from securities and financial instrument dealers and other market sources to determine fair value.

Securities for which market prices are unavailable, or securities for which the investment advisor determines that the bid and/or ask price or a counterparty valuation does not reflect market value, will be valued at fair value, as determined in good faith by the Valuation Committee, pursuant to procedures approved by the Fund’s Board of Directors. Circumstances in which market prices may be unavailable include, but are not limited to, when trading in a security is suspended, the exchange on which the security is traded is subject to an unscheduled close or disruption or material events occur after the close of the exchange on which the security is principally traded. In these circumstances, the Fund determines fair value in a manner that fairly reflects the market value of the security on the valuation date based on consideration of any information or factors it deems appropriate. These may include, but are not limited to, recent transactions in comparable securities, information relating to the specific security and developments in the markets.

For equity securities, including restricted securities, where observable inputs are limited, assumptions about market activity and risk are used and these securities would be categorized as Level 2 or 3 in the hierarchy, depending on the relative significance of the valuation inputs. Securities, including private placements or other restricted securities, for which observable inputs are not available are valued using alternate valuation approaches, including the market approach, the income approach and cost approach, and are categorized as Level 3 in the hierarchy. The market approach considers factors including the price of recent investments in the same or a similar security or financial metrics of comparable securities. The income approach considers factors including expected future cash flows, security specific risks and corresponding discount rates. The cost approach considers factors including the value of the security’s underlying assets and liabilities.

The Fund’s use of fair value pricing may cause the NAV of Fund shares to differ from the NAV that would be calculated using market quotations. Fair value pricing involves subjective judgments and it is possible that the fair value determined for a security may be materially different than the value that could be realized upon the sale of that security.

Fair value is defined as the price that the Fund would expect to receive upon the sale of an investment or expect to pay to transfer a liability in an orderly transaction with an independent buyer in the principal market or, in the absence of a principal market, the most advantageous market for the investment or liability. The hierarchy of inputs that are used in determining the fair value of the Fund’s investments is summarized below.

27

COHEN & STEERS TOTAL RETURN REALTY FUND, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)—(Continued)

| | • | | Level 1—quoted prices in active markets for identical investments |

| | • | | Level 2—other significant observable inputs (including quoted prices for similar investments, interest rates, credit risk, etc.) |

| | • | | Level 3—significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments) |

The inputs or methodology used for valuing investments may or may not be an indication of the risk associated with those investments. Changes in valuation techniques may result in transfers into or out of an assigned level within the disclosure hierarchy.

The following is a summary of the inputs used as of June 30, 2022 in valuing the Fund’s investments carried at value:

| | | | | | | | | | | | | | | | |

| | | Quoted Prices

in Active

Markets for

Identical

Investments

(Level 1) | | | Other

Significant

Observable

Inputs

(Level 2) | | | Significant

Unobservable

Inputs

(Level 3) | | | Total | |

Common Stock: | |

Real Estate—Industrials | | $ | 40,836,837 | | | $ | — | | | $ | 1,974,209 | a | | $ | 42,811,046 | |

Other Industries | | | 232,525,720 | | | | — | | | | — | | | | 232,525,720 | |

Preferred Securities—$25 Par Value | | | 29,596,090 | | | | — | | | | — | | | | 29,596,090 | |

Preferred Securities—Capital Securities | | | — | | | | 28,944,093 | | | | — | | | | 28,944,093 | |

Corporate Bonds | | | — | | | | 3,202,133 | | | | — | | | | 3,202,133 | |

Private Real Estate—Office | | | — | | | | — | | | | 3,801,125 | b | | | 3,801,125 | |

Short-Term Investments | | | — | | | | 6,061,601 | | | | — | | | | 6,061,601 | |

Purchased Option Contracts | | | — | | | | 750 | | | | — | | | | 750 | |

| | | | | | | | | | | | | | | | |

Total Investments in Securitiesc | | $ | 302,958,647 | | | $ | 38,208,577 | | | $ | 5,775,334 | | | $ | 346,942,558 | |

| | | | | | | | | | | | | | | | |

Forward Foreign Currency Exchange Contracts | | $ | — | | | $ | 13,920 | | | $ | — | | | $ | 13,920 | |

| | | | | | | | | | | | | | | | |

Total Derivative Assetsc | | $ | — | | | $ | 13,920 | | | $ | — | | | $ | 13,920 | |

| | | | | | | | | | | | | | | | |

Forward Foreign Currency | | | | | | | | | | | | | | | | |

Exchange Contracts | | $ | — | | | $ | (1,293 | ) | | $ | — | | | $ | (1,293 | ) |

Written Option Contracts | | | (70,245 | ) | | | (16,876 | ) | | | — | | | | (87,121 | ) |

| | | | | | | | | | | | | | | | |

Total Derivative Liabilitiesc | | $ | (70,245 | ) | | $ | (18,169 | ) | | $ | — | | | $ | (88,414 | ) |

| | | | | | | | | | | | | | | | |

| a | Restricted security, where observable inputs are limited, has been fair valued by the Valuation Committee, pursuant to the Fund’s fair value procedures and classified as Level 3 security. |

28

COHEN & STEERS TOTAL RETURN REALTY FUND, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)—(Continued)

| b | Private Real Estate, where observable inputs are limited, has been fair valued by the Valuation Committee, pursuant to the Fund’s fair value procedures and classified as Level 3 security. See Note 1-Portfolio Valuation. |

| c | Portfolio holdings are disclosed individually on the Consolidated Schedule of Investments. |

The following is a reconciliation of investments for which significant unobservable inputs (Level 3) were used in determining fair value:

| | | | | | | | |

| | | Common Stock—

Real Estate—

Industrials | | | Private

Real Estate—

Office | |

Balance as of December 31, 2021 | | $ | 2,182,913 | | | $ | — | |

Purchases | | | — | | | | 7,129,806 | |

Return of capital distribution | | | — | | | | (3,832,537 | ) |

Change in unrealized appreciation (depreciation) | | | (208,704 | ) | | | 503,856 | |

| | | | | | | | |

Balance as of June 30, 2022 | | $ | 1,974,209 | | | $ | 3,801,125 | |

| | | | | | | | |

The change in unrealized appreciation (depreciation) attributable to securities owned on June 30, 2022 which were valued using significant unobservable inputs (Level 3) amounted to $295,152.

The following table summarizes the quantitative inputs and assumptions used for investments categorized in Level 3 of the fair value hierarchy.

| | | | | | | | | | |

| | | Fair Value at