Corporate Presentation November, 2009 James A. Bianco, M.D. Chief Executive Officer Exhibit 99.1 |

Forward Looking Statement This presentation contains forward-looking statements within the meaning of the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995. The forward-looking statements contained in this presentation include statements about future financial and operating results, and risks and uncertainties that could affect CTI’s products under development. These statements are based on management’s current expectations and beliefs and are subject to a number of factors and uncertainties that could cause actual results to differ materially from those described in the forward-looking statements. These statements are not guarantees of future performance, involve certain risks, uncertainties and assumptions that are difficult to predict, and are based upon assumptions as to future events that may not prove accurate. Therefore, actual outcomes and results may differ materially from what is expressed herein. In any forward-looking statement in which CTI expresses an expectation or belief as to future results, such expectation or belief is expressed in good faith and believed to have a reasonable basis, but there can be no assurance that the statement or expectation or belief will result or be achieved or accomplished. The following factors, among others, could cause actual results to differ materially from those described in the forward- looking statements: risks associated with preclinical, clinical and sales and marketing developments in the biopharmaceutical industry in general and in particular including, without limitation, the potential failure of Opaxio™ to prove safe and effective for treatment of non-small cell lung and ovarian cancers, the potential failure of Pixuvri (pixantrone dimaleate) to prove safe and effective (including complete and overall response rates) for treatment of non- Hodgkin’s lymphoma, determinations by regulatory, patent and administrative governmental authorities, competitive factors, technological developments, costs of developing, producing and selling CTI’s products under development; and other economic, business, competitive, and/or regulatory factors affecting CTI’s business generally, including those set forth in CTI’s filings with the SEC, including its Annual Report on Form 10-K for its most recent fiscal year and its most recent Quarterly Report on Form 10-Q, especially in the “Factors Affecting Our Operating Results” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” sections, and its Current Reports on Form 8- K. Except as may be required by law, CTI does not intend to update or alter its forward-looking statements whether as a result of new information, future events, or otherwise. |

Overview Focused on Profitability Pixantrone: a potential breakthrough therapy for lymphoma Potential to become the anthracycline of choice More than 300,000 patients/yr treated with anthracyclines NDA review proceeding on accelerated timetable Only randomized trial to use Complete Remission as 1 0 endpoint Management team with “big-pharma” oncology commercial experience Attractive Late Stage Oncology Pipeline #1 in stock price performance year to date on MTA |

A Powerful Cancer Drug Portfolio Preclinical Phase I Phase II Phase III Marketed NDA review PH 2-3 completed Phase 3 Phase 2-3 Brostallicin Bisplatinates 3rd line relapse aggressive NHL 1st line Ovarian cancer 1st line aggressive NHL (Randomized Phase 2) NP sales = named patient sales 1st line Esophageal cancer +XRT |

Opportunity Assessment Opportunity Assessment • Anthracyclines – 3 rd most commonly used class cytotoxics • >300,000 pts receive anthracyclines each year • Most effective class of anti-cancer drugs: • Curative in lymphoma, leukemia and breast cancer • 66,000 US patients/yr diagnosed with NHL • 31,600 patients with aggressive NHL will receive anthracycline based 1 st line therapy (CHOP-R) • Up to 50% of patients are cured • 16,000 patients relapse after 1 st line – • Anthracyclines not frequently re-applied due to high risk for cardiac damage and congestive failure |

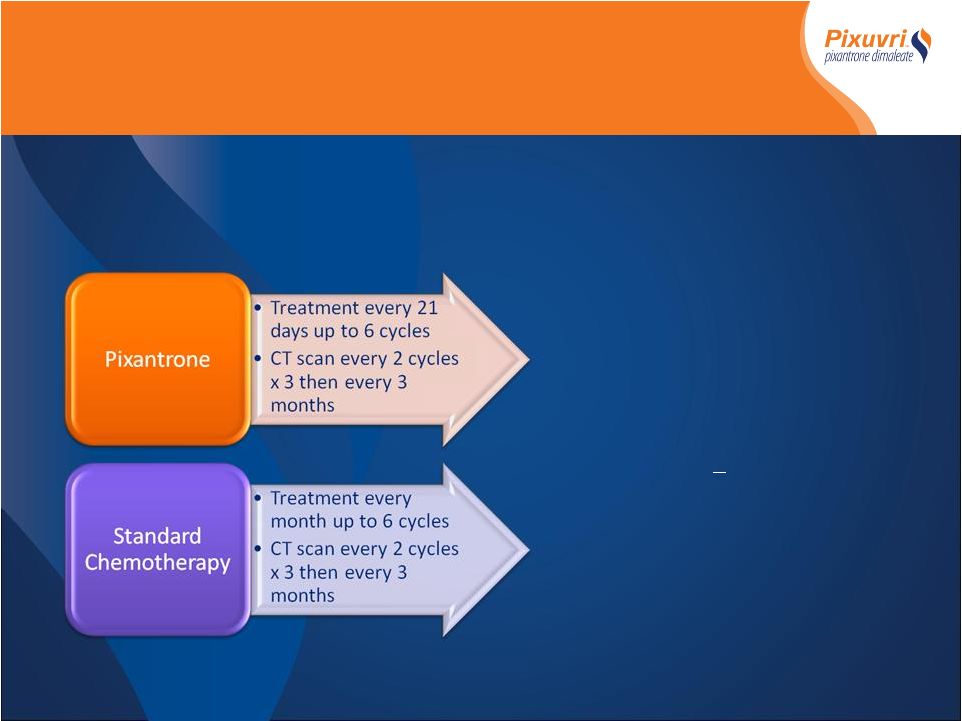

- Randomized Controlled International Multicenter Phase III trial - Relapsed or refractory aggressive NHL (failed 1 st ,2 nd line or beyond) - 140 patients Primary Endpoint* - Complete Remission (CR/CRu) Secondary Endpoints* - Overall Response Rate (ORR) - Responses > 4months - Time to response - Progression Free Survival - Overall Survival - Safety *All response and progression data determined by blinded Independent Assessment Panel (IAP) PIX 301Phase III Study Design PIX 301Phase III Study Design |

*All response and progression data determined by blinded Independent Assessment Panel (IAP) • Superior efficacy over standard of care • Primary endpoint achieved (ITT) • Superior Complete Remission rates 20% Vs. 5.7% p=0.021 • Secondary endpoints achieved (ITT) • Superior ORR 37% Vs. 14.3% p=0.003 • Superior PFS 4.7 months Vs. 2.6 months p=0.007 • Superior duration of response > 4months 25.7% Vs 8.6 p=0.012 • Superior time to response 1.9 Vs 3.6 months p =0.038 • Superior OS 8.1 Vs 6.9 months p=0.5 • Encouraging cardiac safety profile despite median dox- equivalent exposure of 515mg/m2 • Non-dose dependant occurrence of CHF (5 Vs 2) drug relationship unlikely Summary PIX301 Phase III Results Summary PIX301 Phase III Results End of Treatment Evaluation |

Commercial Opportunity 8 |

Business Issue 1: What is the opportunity for Pixuvri in the aggressive Non-Hodgkin’s Lymphoma marketplace? |

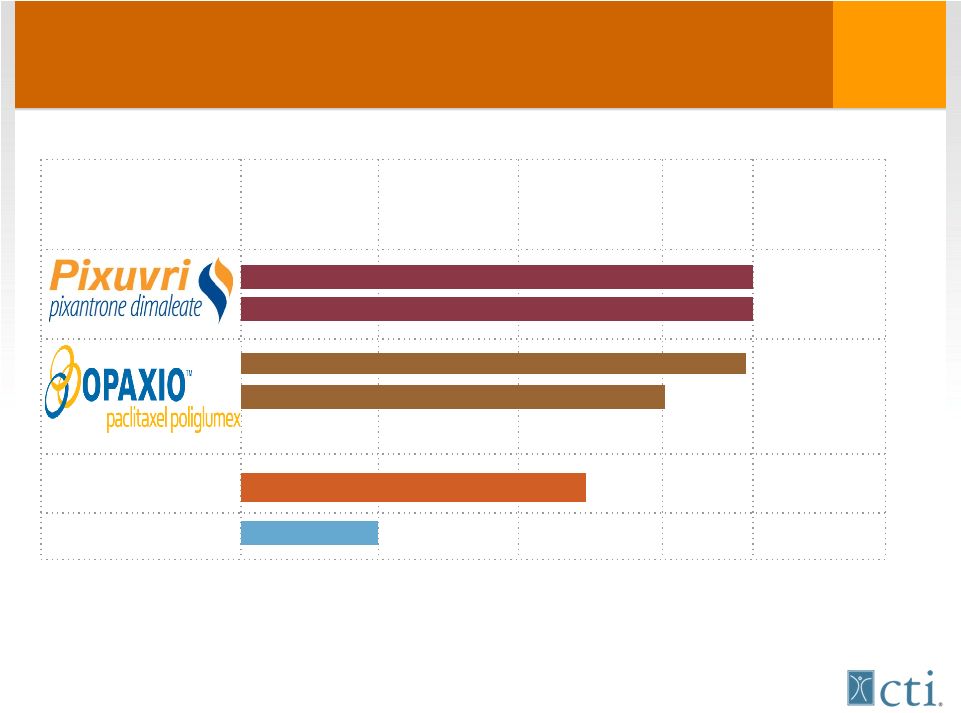

65% of physicians are either extremely or very likely to prescribe Pixuvri. This indicates a sizable opportunity in the aggressive Non-Hodgkins Lymphoma marketplace. Likelihood of Prescribing Pixuvri Physician Data QC1b |

2 Line Therapy Share of Relapsed Non-Hodgkin Lymphoma Patients Receiving Treatment After Pixuvri 3 Line Therapy Mean % Among Total Physicians\with 1 Or more Third Line Treatment Options (n=76) No statistically significant difference @ 90% confidence level between subgroups Note: Reallocated to include modeled baseline share for Pixuvri Note: Other Includes miniBEAM ±R, MINE ±R, GDP ±R, Fludarabine + R, CVP ±R therapies QA1/20, QC2 Pixuvri (Mono/Combo Therapy) CHOP ±R DHAP ±R ESHAP ±R GemOx ±R ICE ±R Rituximab Monotherapy Treanda (bendamustine) ±R Velcade (bortezomib) ±R Refer to Clinical Trial/ Bone Marrow Transplant Other CHOP ±R and ICE ±R have the potential to become vulnerable in the treatment of 2 line patients with the entry of Pixuvri. Less 3 line patients will be referred for clinical trial or considered for bone marrow transplants. Physician Data nd nd rd rd with Pixuvri (B) Current (A) with Pixuvri (B) Current (A) |

Commercial Analysis Commercial Analysis CTI peak Market Research NHL in model Peak Aggressive 1 -line 15% 26% 2 -line 20% 38% 3 -line+ 25% 36% Indolent 1 -line 4% 27% 2 -line 8% 34% 3 -line+ 8% 32% • Assumptions – Pricing $24/mg – $1,200 vial, = average use 36 vials/patient – Exclusivity in the market to 2018 (US) / 2020(EU) – Regulatory approval – aggressive relapsed NHL • US early Q2-2010, EU Q4 -2010 • Modeling assumptions (US only) – Only NHL is included • 1 line 30,029 patients • 2 line 10,150 patients • 3 line 9,767 patients • Peak Penetration – Assumes EU ~70% US market – 15,800 pts US +10,600 pts EU – Total peak patients/yr = 26,400 – Cost per patient/yr = $44,000 st nd rd st nd rd st nd rd |

Novartis – CTI Agreement(s) NVS has option to negotiate a license to pixantrone Provides $104 million in registration/sales milestones $17.5mm on approval for r/r aNHL 28% to 32% royalty on net sales NVS assumes costs and pays CTI to field 35 sales people CTI not obligated to license pixantrone to NVS if terms are not favorable |

|

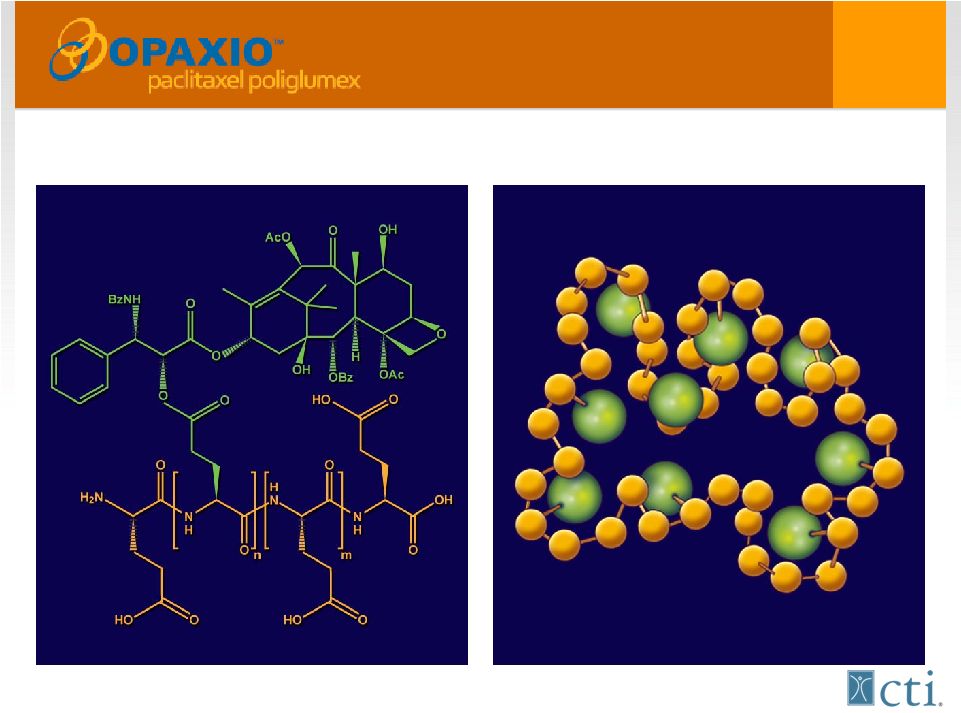

A bioengineered version of Taxol®(paclitaxel) Singer et al. In: Adv Exp Med Biol. 2003; 519:81-99 |

Opaxio Regulatory Status Pivotal trial (GOG212) • GOG to conduct an interim “futility” PFS analysis in 1H 2010 • Market size 15,000 to 20,000 patients/year Additional registration trial in lower esophageal cancer • XRT sensitization • Impressive rates of (45%) pathologic complete remission rates with markedly reduced GI toxicity • Phase III SPA submission1H-2010 |

Novartis–CTI Agreement(s) Worldwide license to OPAXIO • Reimburses for 50% of certain expenses • $270M in potential registration and sales milestones • CTI to field 35 FTE at NVS expense up to $9M • NVS to assume development and commercial expenses • Royalties 20%-25% on WW net sales |

Capital Structure/Financials Dual Listed NASDAQ:CTIC, MTA:CTIC.MI • Liquid stock ~50mm shares/day US/EU (3 month average) • 580mm shares outstanding Cleaning up Balance Sheet • Redeemed $57.4mm debt • Only common stock outstanding Cash end Q3- $55 million |

Upcoming Events Upcoming Events Potential GOG futility PFS analysis on 1 st line maintenance trial Key publications for pixantrone PIX 301 follow-up data at American Society of Hematology (ASH) Annual Meeting Investor/Analyst meeting at ASH on Dec. 5 Dr. John Leonard, Weill/Cornell Med College, NY Presbyterian Dr. Stanley Marks, CMO of Univ. of Pittsburgh Cancer Centers Potential NDA approval of Pixantrone SPA Meeting with FDA for Registration Study of OPAXIO as Radiation Sensitizer in Treatment of Esophageal Cancer |