Cell Therapeutics, Inc. James A. Bianco, M.D. CEO Exhibit 99.1 |

2 Forward Looking Statement The following factors, among others, could cause actual results to differ materially from those described in the forward-looking statements: risks associated with preclinical, clinical and sales and marketing developments in the biopharmaceutical industry in general and in particular, including, without limitation: the potential failure of Opaxio™ (“Opaxio”) to prove safe and effective for treatment of non-small cell lung and ovarian cancers; that the interim survival results for the phase III clinical trial for Opaxio may not be ready in 2012; the potential failure of PixuvriTM (pixantrone dimaleate) (“pixantrone”) to prove safe and effective (including complete and overall response rates) for treatment of relapsed or refractory, aggressive non-Hodgkin’s lymphoma (“NHL”) as determined by the U.S. Food and Drug Administration (the “FDA”) and/or the European Medicines Agency (the “EMA”); that accelerated approval by the FDA of pixantrone may not be possible or occur; that CTI may not be able to address satisfactorily the two key matters raised by the FDA’s Office of New Drugs (the “OND”) or other matters raised by the OND and/or the FDA; that CTI’s interpretation of the guidance provided by the OND may be different than the intent of the OND; that the OND may change its guidance; that the PIX301 study may not be deemed successful; that a re-review of the pixantrone NDA may not be warranted and, if warranted, that the FDA may find pixantrone to not be safe and/or effective; that the PIX301 study may still be deemed to be a failed study; that the FDA may require an additional clinical trial of pixantrone; that if CTI conducts an additional clinical trial, it may not demonstrate the safety and effectiveness of pixantrone; that CTI may not be able to provide satisfactory information in response to the FDA’s Complete Response Letter; that the FDA may not approve the NDA in the first half of 2012 or at all; that CTI may not obtain a PDUFA date of April 2012; that CTI cannot predict or guarantee the pace or geography of enrollment of its clinical trials, including whether or not the majority of the patients will be enrolled in the U.S.; that the commercial launch of pixantrone may not commence in the first half of 2012; that the EMA may not approve the MAA; that CTI cannot guarantee the timing of the approval and launch of its products; that CTI cannot predict the results of the EMA’s Committee for Medicinal Products for Human Use (“CHMP”) opinion or guarantee that the CHMP will provide its recommendation regarding the MAA during the first half of 2012; that CTI cannot guarantee exclusivity in the market for its products; that CTI cannot predict or guarantee that Novartis will exercise its option to negotiate a license for pixantrone or what the actual milestone amounts will be; that CTI cannot guarantee that the Gynecologic Oncology Group will conduct an interim survival analysis in 2012 or what the market size or outcome of such analysis will be; the potential failure of tosedostat to prove safe and effective for the treatment of Acute Myeloid Leukemia (“AML”); that the FDA may not accept the proposed clinical trial design of tosedostat and/or may request additional clinical trials; that clinical trials may not demonstrate the safety and effectiveness of tosedostat; that the phase III pivotal trial for tosedostat for AML and/or myelodysplastic syndromes may not start during the second quarter of 2012; that CTI may not be able to retire its outstanding convertible senior notes due in December 2011; that CTI may not consummate additional financings; that CTI may not be able to maintain its expected burn rate; that CTI’s ability to continue to raise capital as needed to fund its operations; that CTI may not be able to maintain its burn rate as expected; that CTI may be unable to comply with NASDAQ listing standards; determinations by regulatory, patent and administrative governmental authorities; competitive factors; technological developments; costs of developing, producing and selling CTI’s products under development; and other economic, business, competitive, and/or regulatory factors affecting CTI’s business generally, including those set forth in CTI’s filings with the U.S. Securities and Exchange Commission, including its Annual Report on Form 10-K for its most recent fiscal year and its Quarterly Reports on Form 10-Q since its most recent Annual Report on Form 10-K, especially in the “Factors Affecting Our Operating Results” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” sections, and its Current Reports on Form 8-K. Except as may be required by law, CTI does not intend to update or alter its forward-looking statements whether as a result of new information, future events, or otherwise. |

3 Important Advances in Treating Cancer 3 novel “late stage” cancer drug candidates • Pixantrone – marketing authorizations filed; potential approval 2012 • Opaxio – completing final stage (III) clinical testing 2013 • Tosedostat – entering final stage (III) clinical testing 2012 Large market opportunities addressing unmet medical needs Concentrated cancer market makes go to market strategy manageable with attractive ROI Potential for Novartis to exercise option to co-develop and co-commercialize pixantrone |

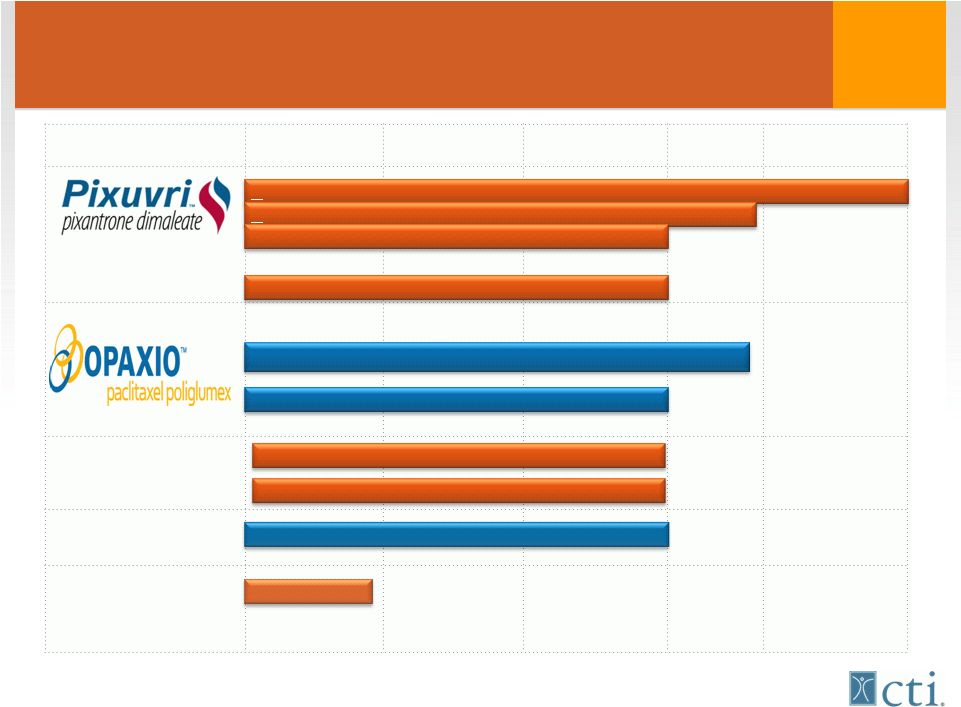

4 Innovative & Established Cancer Drug Pipeline *Tosedostat phase III study expected to initiate Q2-2012 Bisplatinates Brostallicin Tosedostat Preclinical Phase I Phase II Phase III MAA/NDA Under Review > Third-line r/r aggressive NHL (PIX301) > Second-line r/r aggressive NHL (PIX306) First-line aggressive NHL (PIX203) Second-line metastatic breast cancer (NCCTG) First-line Ovarian cancer First-line GBM cancer + XRT Elderly high-risk r/r AML (OPAL) Myelodysplastic Syndrome (MDS)* ER-, PR-, HER2- Metastatic Breast cancer |

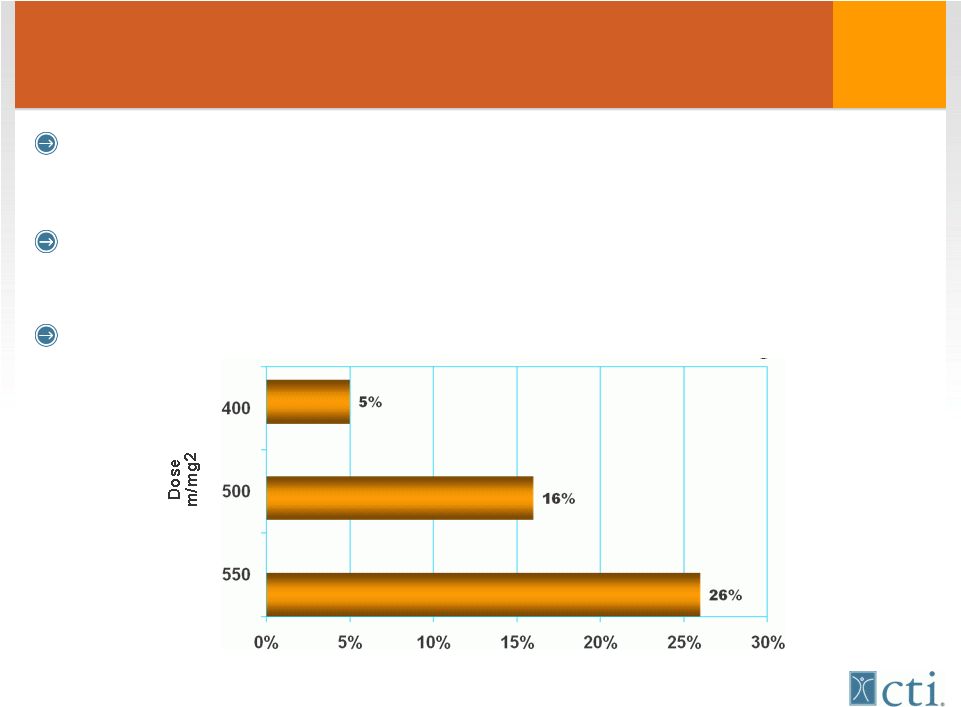

5 Anthracyclines “Cornerstone” potentially curative therapy 1 st line therapy • Breast cancer / acute leukemia / NHL However all anthracyclines cause cumulative, irreversible damage to heart muscle Patients limited to life time maximum dose 450mg/m 2* * Swain et al, chest XRT or cyclophosmaide Incidence of Congestive Heart Failure |

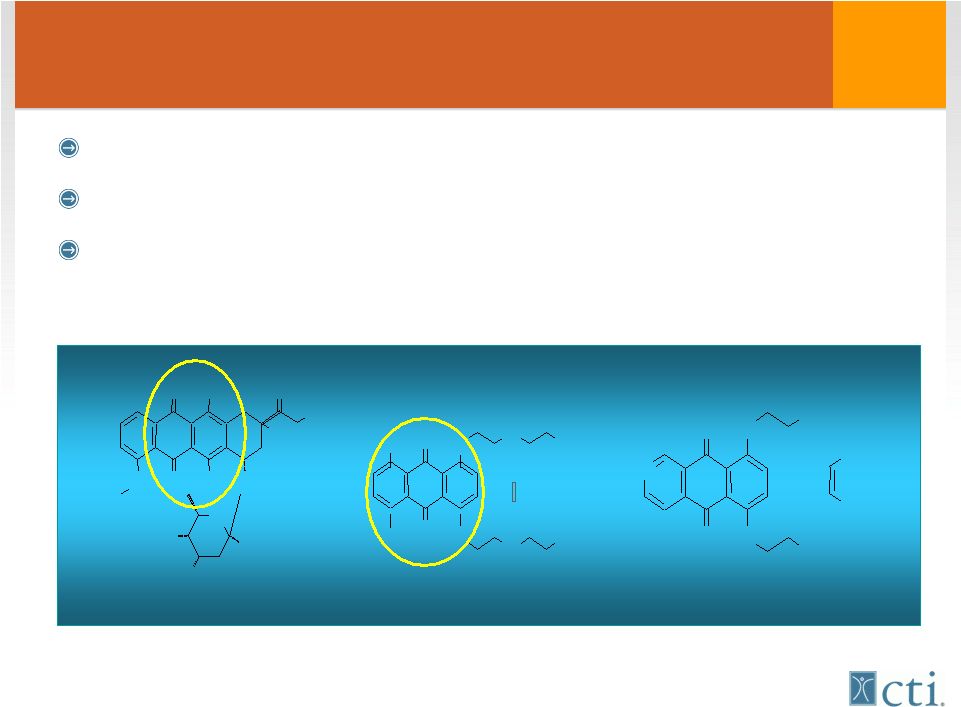

6 Pixuvri™ (pixantrone) Product Advantages More potent DNA alkylator than doxorubicin Lacks structural motifs that lead to cardiac toxicity Significant reductions in biochemical, echo-cardiographic and severe clinical symptoms (CHF) Vs doxorubicin O O O O H O H O H O O H O O O H N H 2 H N O O N H N H N H 2 N H 2 C O O H C O O H O O N H N H N H N H O H O H O H O H Mitoxantrone Doxorubicin 2 HCl Pixantrone Pixantrone 2 |

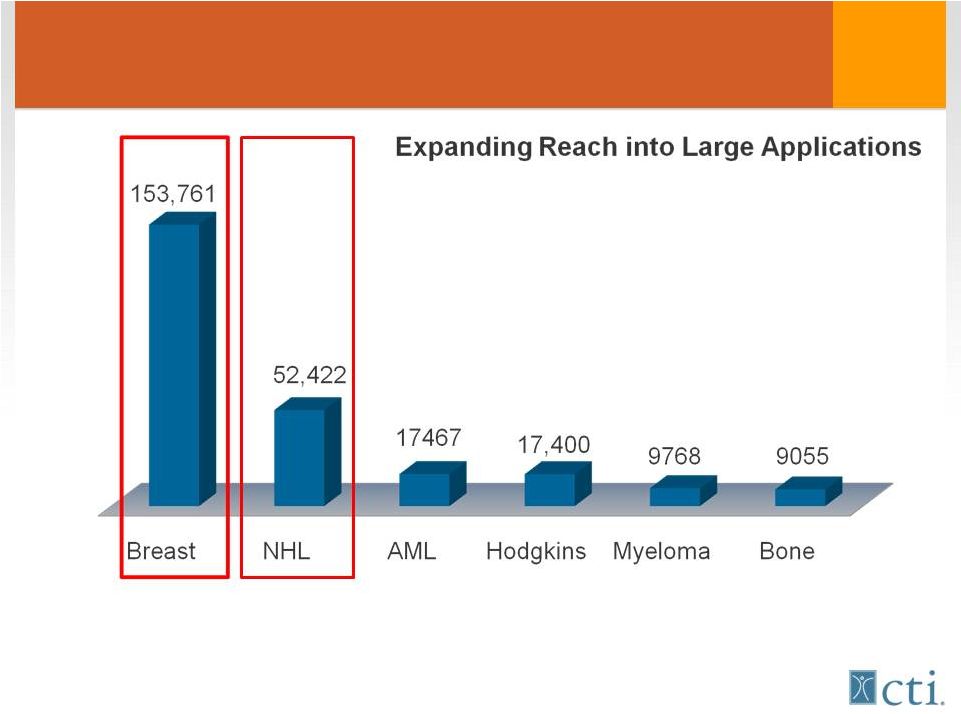

7 Pixuvri™ (pixantrone): Overview Pivotal (PIX301)Trial • Significant increase in Complete and Overall Response rates compared to standard chemotherapy • Significant (40%) decrease in risk of dying or progression of disease over 2 years • Well tolerated, most common side effect – low white cell counts Marketing Applications filed • EU (MAA) – day 180 responses pending • US (NDA) – re-submitted based on FDA (OND) recommendations – expected action date April 2012 Initial indication: r/r aggressive NHL • No approved drugs in EU or US for this patient population Initial market size– 53,000 patients/year (US/EU) |

8 Novartis Pixantrone Option NVS has option to negotiate a license to pixantrone Potentially up to $104 million in registration/sales milestones • $17.5mm on approval for r/r aNHL • 28% to 32% royalty on US net sales • NVS assumes certain costs and pays CTI to field 35 sales people CTI not obligated to license pixantrone to NVS if terms are not favorable |

US Patients/year Treated with Anthracyclines Pixuvri™ Phase II NDA/MAA o Development program to enhance commercial potential post approval o Competitive advantages o Potential to become standard of care Source: Tandem Cancer Audit 2004 9 |

10 Tosedostat: Overview New drug class: tumor selective targeted agent • Works by depriving cancer cells building blocks needed to make proteins essential for their survival • Oral, once daily dosing, well tolerated Encouraging data in elderly r/r AML (Acute Myeloid Leukemia) and r/r MDS (Myelodysplasia or pre-leukemia) Pivotal Phase III study targeted to start Q2 - 2012 Leverages CTI’s access to and expertise in blood-related cancer market • Potential development cost and sales synergies with pixantrone Exclusive development and marketing rights in the Americas |

11 Tosedostat Phase I/II Study |

12 Unmet Medical Need in MDS and AML AML and MDS are common diseases • MDS often progresses to AML Is a disease of elderly • 70% of patients are over age 60 The majority of elderly patients with MDS and AML do not tolerate standard intensive chemotherapy • 35% will die from side effects of standard intensive therapy • Most are currently treated with low dose chemotherapy or hypo- methylating agents There are no approved agents for patients who relapse Significant unmet medical need for better tolerated agents in elderly patients with MDS or AML |

13 Tosedostat: OPAL Interim Study Results Phase II- r/r elderly AML (n=75 patients) • Oral once-a-day dosing for 6 months Encouraging interim data presented at ASCO • 15 of 50 (30%) evaluable patients had bone marrow response; - 6 (12%) of which were complete bone marrow responses • 9 of 23 (39%) patients who previously failed therapy with HMA had a bone marrow response • Well tolerated without chemotherapy like side effects Patients who responded to therapy demonstrated encouraging survival Data to be updated at ASH |

14 Tosedostat Summary Deal Terms & Structure Exclusive co-development and marketing rights in the Americas from Chroma Therapeutics, Ltd Cost-sharing • CTI bears 75% of all development costs • Registration trials aimed at US/EU regulatory approval Initial Payments • $5mm upon execution • $5mm upon initiation of first pivotal trial Success based milestones Royalty rate based on net sales volume |

15 Relapsed or refractory MDS (IPSS>2) • Currently no approved drugs • Existing therapies come off patent in 2011, and 2013 • 18,000 patients/year Relapsed or refractory elderly AML • Currently no approved drugs • 18,300 patients/year Other potential indications (patients/year) • r/r Myeloma – 19,000 • 1 st line MDS: 20,100 • 1 st line Myeloma: 36,000 US Market Size: Selective Blood Related Cancers |

16 Indication WW 2010 sales* Patent expiration MDS $200MM 2013 MDS $534MM 2011 Multiple Myeloma/ Mantle Cell $1.5B 2017 Multiple Myeloma MDS Deletion 5q $2.5B 2019 Tosedostat Market Opportunity: Current targeted agents VELCADE *Information from SEC filings. |

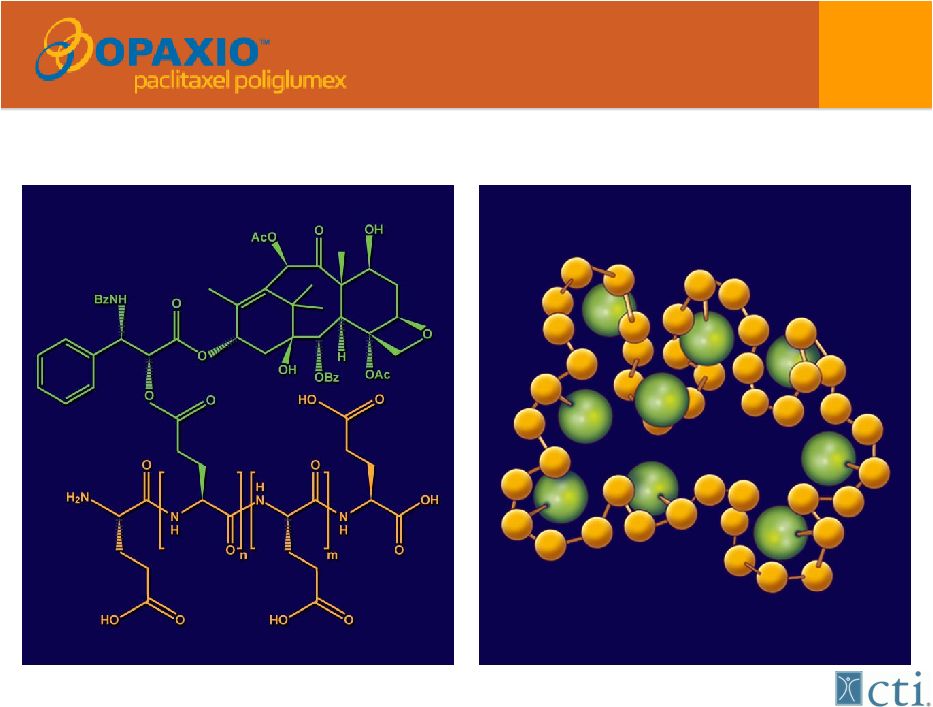

17 A bioengineered version of Taxol® (paclitaxel) Singer et al. In: Adv Exp Med Biol. 2003; 519:81-99 |

18 A bioengineered version of Taxol® (paclitaxel) Taxol® (paclitaxel) 3hr to 24 hr infusion, pre-medications required Opaxio™ 15-20 minute infusion, NO pre-medications required |

19 Opaxio™ 95% of women with advanced Ovarian Cancer achieve CR with standard (taxol/platinum) chemotherapy • Half (median) will relapse within 8 months, and die in 44 months Ovarian Cancer Pivotal trial (GOG212) • Can monthly OPAXIO for 12 months prolong time to progression and improve survival in women with advanced Ovarian cancer when compared to no treatment (observation) • NIH supported cooperative group study • 817 of 1100 patients enrolled • Interim survival analysis anticipated in 2012 - Early stopping criteria for success |

20 Opaxio™ Potential registration route as radiation sensitizer • Tumor selective, 8-12X increase in radiation sensitization vs Taxol (0.8x increase) Malignant Brain Tumor Study (n=25 patients ) • Opaxio added to standard therapy (TMZ+XRT) • Compared to landmark trial* - Median PFS 13.5 months vs. 6.9 months - >50% patients alive at 22 months Vs. historically <25% survive 24 months Randomized multi-center Phase II study underway in high-risk malignant brain tumors • If survival advantage confirmed could serve as basis for approval *Historical landmark study- Stupp R, et al, N. Engl. J. Med. 352:987-09, 2005 |

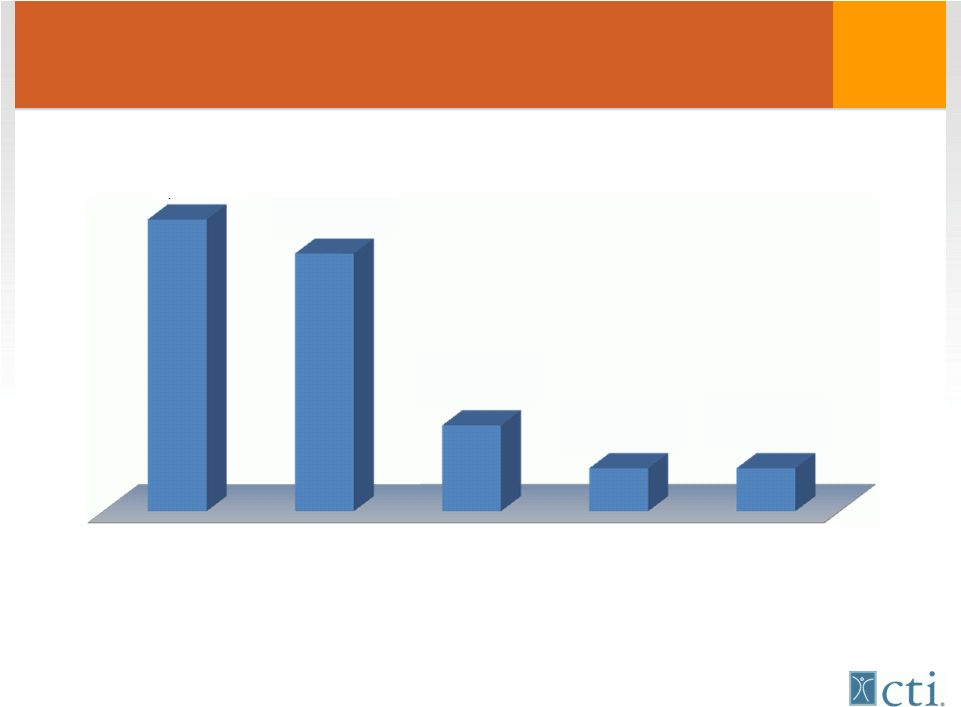

21 US Patients/year Treated with Taxanes Source: Tandem Cancer Audit 2004 NSC Lung Breast Ovarian H&N Prostate 92,400 81,600 27,200 13,600 13,600 |

22 Capital Structure/Financials Dual Listed NASDAQ:CTIC, MTA:CTIC.MI • Shares outstanding ~193 million Only $11mm convertible senior notes outstanding • Due December 2011 Only common shares outstanding Manageable burn rate Cash end of Q3-2011 ~$45.2 million • Excludes :~$8.2 million from settlement agreement |

23 2012 Potential News Flow & Key Milestones Pixantrone • CHMP opinion on MAA and potential approval • FDA review of NDA and potential approval • Novartis decision on pixantrone option Tosedostat • Final OPAL data to be highlighted at ASH • Start of Tosedostat phase III r/r MDS trial Opaxio • OPAXIO phase III ovarian cancer trial interim results |