FORM 6-K

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Report of Foreign Issuer

Pursuant to Rule 13a-16 or 15d-16

of the Securities Exchange Act of 1934

For the month of April, 2021

Commission File Number: 001-12518

Banco Santander, S.A.

(Exact name of registrant as specified in its charter)

Ciudad Grupo Santander

28660 Boadilla del Monte (Madrid) Spain

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

Form 20-F ☒ Form 40-F ☐

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Yes ☐ No ☒

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

Yes ☐ No ☒

BANCO SANTANDER, S.A.

________________________

TABLE OF CONTENTS

| Part 1. January - March 2021 Financial Report | |||||

| January - March | 2021 | ||||

Index

This report was approved by the Board of Directors on 27 April 2021, following a favourable report from the Audit Committee. Important information regarding this report can be found on pages 87 and 88.

Key consolidated data

| BALANCE SHEET (EUR million) | Mar-21 | Dec-20 | % | Mar-20 | % | Dec-20 | |||||||||||||||||

| Total assets | 1,562,879 | 1,508,250 | 3.6 | 1,540,359 | 1.5 | 1,508,250 | |||||||||||||||||

| Loans and advances to customers | 939,760 | 916,199 | 2.6 | 935,407 | 0.5 | 916,199 | |||||||||||||||||

| Customer deposits | 882,854 | 849,310 | 3.9 | 815,459 | 8.3 | 849,310 | |||||||||||||||||

| Total funds | 1,095,970 | 1,056,127 | 3.8 | 1,006,948 | 8.8 | 1,056,127 | |||||||||||||||||

| Total equity | 92,686 | 91,322 | 1.5 | 106,113 | (12.7) | 91,322 | |||||||||||||||||

| Note: Total funds includes customer deposits, mutual funds, pension funds and managed portfolios | |||||||||||||||||||||||

| INCOME STATEMENT (EUR million) | Q1'21 | Q4'20 | % | Q1'20 | % | 2020 | |||||||||||||||||

| Net interest income | 7,956 | 8,019 | (0.8) | 8,487 | (6.3) | 31,994 | |||||||||||||||||

| Total income | 11,390 | 10,924 | 4.3 | 11,809 | (3.5) | 44,279 | |||||||||||||||||

| Net operating income | 6,272 | 5,580 | 12.4 | 6,220 | 0.8 | 23,149 | |||||||||||||||||

| Profit before tax | 3,102 | 1,195 | 159.6 | 1,891 | 64.0 | (2,076) | |||||||||||||||||

| Attributable profit to the parent | 1,608 | 277 | 480.5 | 331 | 385.8 | (8,771) | |||||||||||||||||

| Changes in constant euros: | |||||||||||||||||||||||

| Q1'21 / Q4'20: NII: -1.7%; Total income: +3.6%; Net operating income: +12.7%; Profit before taxes: +162.6%; Attributable profit: +472.1% | |||||||||||||||||||||||

| Q1'21 / Q1'20: NII: +5.1%; Total income: +7.9%; Net operating income: +15.4%; Profit before taxes: +97.3%; Attributable profit: +998.0% | |||||||||||||||||||||||

| EPS, PROFITABILITY AND EFFICIENCY (%) | Q1'21 | Q4'20 | % | Q1'20 | % | 2020 | |||||||||||||||||

EPS (euros) (2) | 0.085 | 0.008 | 951.4 | 0.011 | 670.1 | (0.538) | |||||||||||||||||

| RoE | 9.80 | 5.54 | 1.47 | (9.80) | |||||||||||||||||||

| RoTE | 12.16 | 6.86 | 2.04 | 1.95 | |||||||||||||||||||

| RoA | 0.62 | 0.38 | 0.18 | (0.50) | |||||||||||||||||||

| RoRWA | 1.67 | 1.03 | 0.45 | (1.33) | |||||||||||||||||||

| Efficiency ratio | 44.9 | 47.7 | 47.2 | 47.0 | |||||||||||||||||||

UNDERLYING INCOME STATEMENT (1) (EUR million) | Q1'21 | Q4'20 | % | Q1'20 | % | 2020 | |||||||||||||||||

| Net interest income | 7,956 | 8,019 | (0.8) | 8,487 | (6.3) | 31,994 | |||||||||||||||||

| Total income | 11,390 | 10,995 | 3.6 | 11,814 | (3.6) | 44,600 | |||||||||||||||||

| Net operating income | 6,272 | 5,580 | 12.4 | 6,220 | 0.8 | 23,149 | |||||||||||||||||

| Profit before tax | 3,813 | 2,658 | 43.5 | 1,956 | 94.9 | 9,674 | |||||||||||||||||

| Attributable profit to the parent | 2,138 | 1,423 | 50.2 | 377 | 467.1 | 5,081 | |||||||||||||||||

| Changes in constant euros: | |||||||||||||||||||||||

| Q1'21 / Q4'20: NII: -1.7%; Total income: +2.9%; Net operating income: +8.5%; Profit before taxes: +44.3%; Attributable profit: +50.3% | |||||||||||||||||||||||

| Q1'21 / Q1'20: NII: +5.1%; Total income: +7.8%; Net operating income: +15.0%; Profit before taxes: +132.9%; Attributable profit: +1,015.7% | |||||||||||||||||||||||

UNDERLYING EPS AND PROFITABILITY (1) (%) | Q1'21 | Q4'20 | % | Q1'20 | % | 2020 | |||||||||||||||||

Underlying EPS (euros) (2) | 0.116 | 0.074 | 55.5 | 0.014 | 744.4 | 0.262 | |||||||||||||||||

| Underlying RoE | 10.44 | 6.93 | 1.52 | 5.68 | |||||||||||||||||||

| Underlying RoTE | 12.96 | 8.59 | 2.11 | 7.44 | |||||||||||||||||||

| Underlying RoA | 0.65 | 0.46 | 0.18 | 0.40 | |||||||||||||||||||

| Underlying RoRWA | 1.77 | 1.24 | 0.46 | 1.06 | |||||||||||||||||||

January - March 2021 |  | 3 | ||||||

SOLVENCY(3) (%) | Mar-21 | Dec-20 | Mar-20 | Dec-20 | |||||||||||||||||||

| CET1 phased-in | 12.30 | 12.34 | 11.58 | 12.34 | |||||||||||||||||||

| Phased-in total capital ratio | 16.16 | 16.18 | 15.09 | 16.18 | |||||||||||||||||||

| CREDIT QUALITY (%) | Q1'21 | Q4'20 | Q1'20 | 2020 | |||||||||||||||||||

Cost of credit (4) | 1.08 | 1.28 | 1.17 | 1.28 | |||||||||||||||||||

| NPL ratio | 3.20 | 3.21 | 3.25 | 3.21 | |||||||||||||||||||

| Coverage ratio | 74 | 76 | 71 | 76 | |||||||||||||||||||

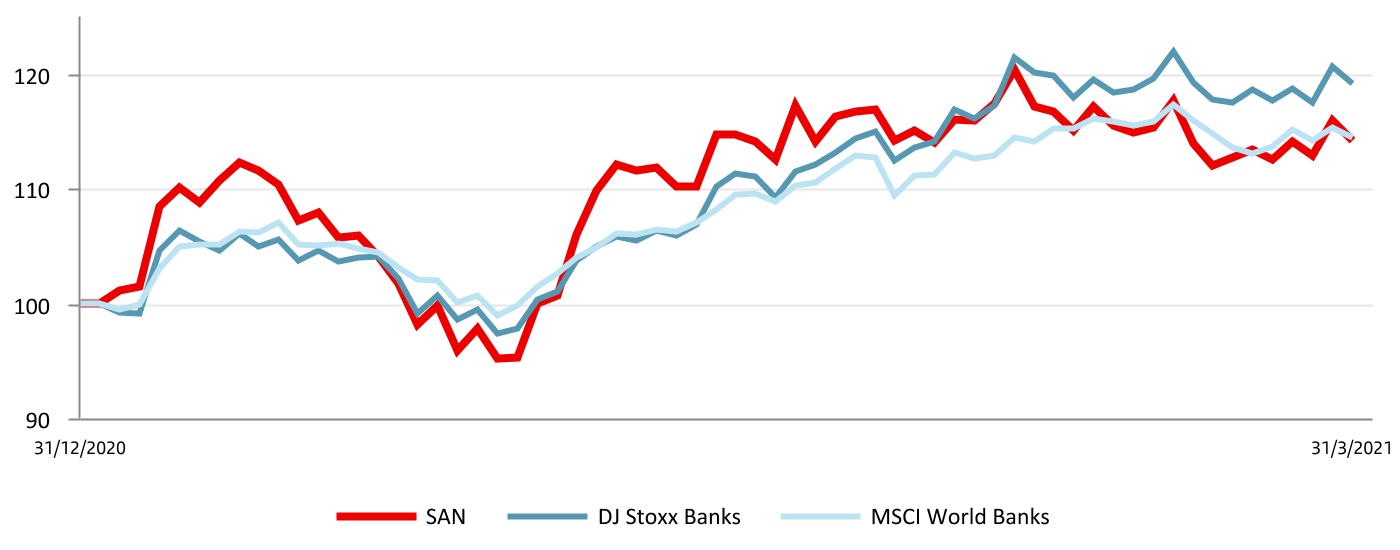

| MARKET CAPITALISATION AND SHARES | Mar-21 | Dec-20 | % | Mar-20 | % | Dec-20 | |||||||||||||||||

| Shares (millions) | 17,341 | 17,341 | 0.0 | 16,618 | 4.3 | 17,341 | |||||||||||||||||

Share price (euros) (2) | 2.897 | 2.538 | 14.1 | 2.126 | 36.3 | 2.538 | |||||||||||||||||

| Market capitalisation (EUR million) | 50,236 | 44,011 | 14.1 | 36,859 | 36.3 | 44,011 | |||||||||||||||||

Tangible book value per share (euros) (2) | 3.84 | 3.79 | 4.03 | 3.79 | |||||||||||||||||||

Price / Tangible book value per share (X) (2) | 0.75 | 0.67 | 0.53 | 0.67 | |||||||||||||||||||

| CUSTOMERS (thousands) | Mar-21 | Dec-20 | % | Mar-20 | % | Dec-20 | |||||||||||||||||

| Total customers | 148,641 | 148,256 | 0.3 | 145,702 | 2.0 | 148,256 | |||||||||||||||||

| Loyal customers | 23,428 | 22,838 | 2.6 | 21,453 | 9.2 | 22,838 | |||||||||||||||||

| Loyal individual customers | 21,441 | 20,901 | 2.6 | 19,645 | 9.1 | 20,901 | |||||||||||||||||

| Loyal SME & corporate customers | 1,987 | 1,938 | 2.6 | 1,808 | 9.9 | 1,938 | |||||||||||||||||

| Digital customers | 44,209 | 42,362 | 4.4 | 38,279 | 15.5 | 42,362 | |||||||||||||||||

| Digital sales / Total sales (%) | 50 | 45 | 41 | 44 | |||||||||||||||||||

| OTHER DATA | Mar-21 | Dec-20 | % | Mar-20 | % | Dec-20 | |||||||||||||||||

| Number of shareholders | 3,937,711 | 4,018,817 | (2.0) | 4,043,974 | (2.6) | 4,018,817 | |||||||||||||||||

| Number of employees | 190,175 | 191,189 | (0.5) | 194,948 | (2.4) | 191,189 | |||||||||||||||||

| Number of branches | 10,817 | 11,236 | (3.7) | 11,902 | (9.1) | 11,236 | |||||||||||||||||

| (1) In addition to financial information prepared in accordance with International Financial Reporting Standards (IFRS) and derived from our consolidated financial statements, this report contains certain financial measures that constitute alternative performance measures (APMs) as defined in the Guidelines on Alternative Performance Measures issued by the European Securities and Markets Authority (ESMA) on 5 October 2015, and other non-IFRS measures, including the figures related to “underlying” results, which do not include the items recorded in the separate line of “net capital gains and provisions”, above the line of attributable profit to the parent. Further details are provided in the “Alternative performance measures” section of the annex to this report. For further details of the APMs and non-IFRS measures used, including its definition or a reconciliation between any applicable management indicators and the financial data presented in the annual consolidated financial statements prepared under IFRS, please see 2020 Annual Financial Report, published in the CNMV on 23 February 2021, our 20-F report for the year ending 31 December 2020 registered with the SEC in the United States as well as the “Alternative performance measures” section of the annex to this report. | ||

| (2) Data adjusted for the capital increase in December 2020. | ||

| (3) The phased-in ratio includes the transitory treatment of IFRS 9, calculated in accordance with article 473 bis of the Capital Requirements Regulation (CRR) and subsequent modifications introduced by Regulation 2020/873 of the European Union. Additionally, the total phased-in capital ratio includes the transitory treatment according to chapter 2, title 1, part 10 of the CRR. | ||

| (4) Allowances for loan-loss provisions over the last 12 months / Average loans and advances to customers over the last 12 months. | ||

| 4 | | January - March 2021 | ||||||

Business model | Group financial information | Financial information by segments | Responsible banking Corporate governance Santander share | Appendix | ||||||||||||||||||||||

Our business model is based on three pillars

1. Our scale Local scale and leadership. Worldwide reach through our global businesses | 2. Customer focus Unique personal banking relationships strengthen customer loyalty | 3. Diversification Our geographic and business diversification makes us more resilient under adverse circumstances | ||||||||||||||||||

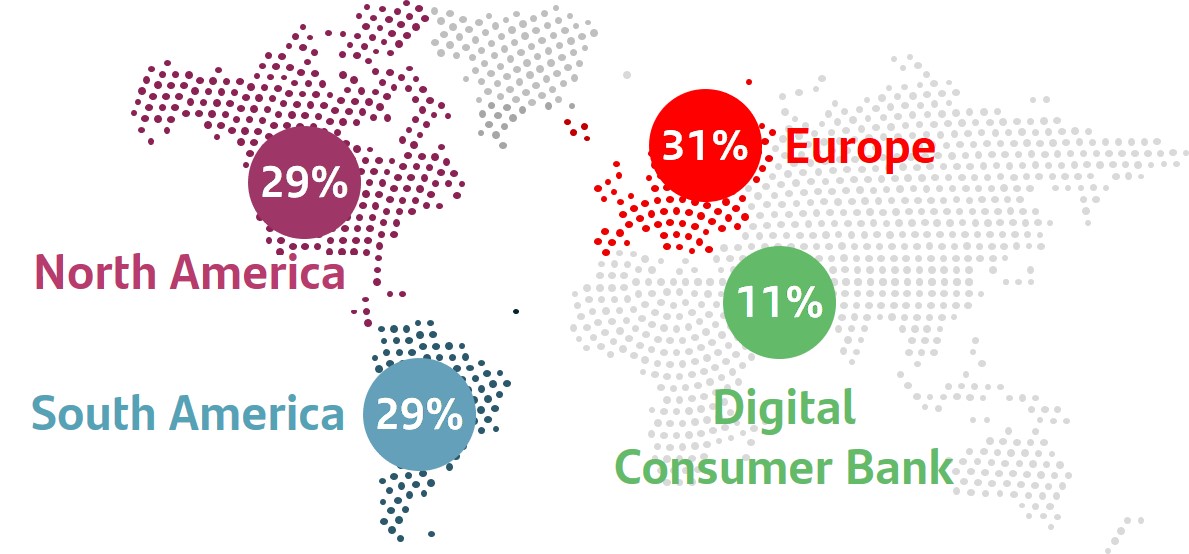

•Geographic diversification3 balanced between mature and emerging markets. | ||||||||||||||||||||

|  | |||||||||||||||||||

| ||||||||||||||||||||

| total customers in Europe and the Americas | ||||||||||||||||||||

|  | •Business diversification between customer segments (individuals, SMEs, mid-market companies and large corporates) | ||||||||||||||||||

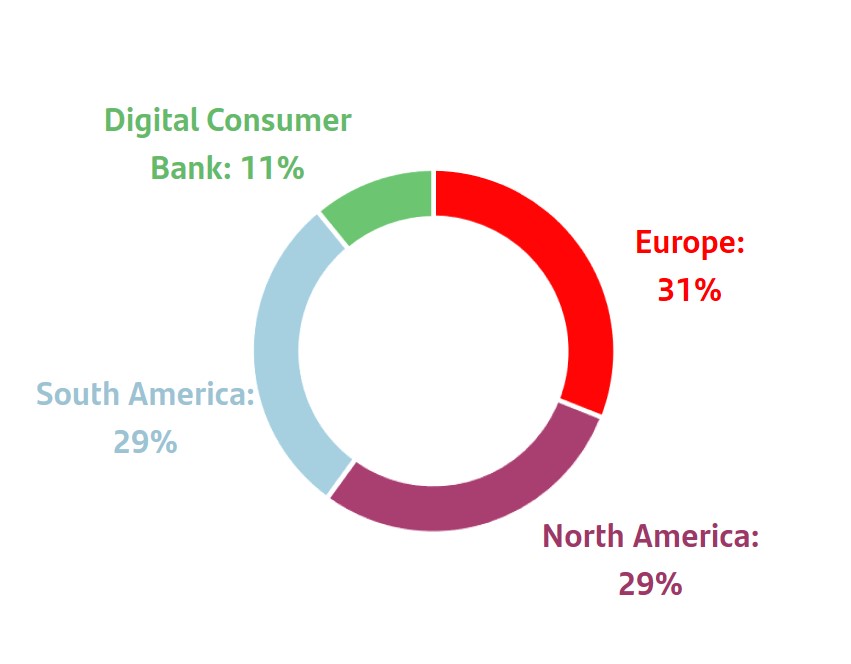

| 1. Market share in lending as of December 2020 including only privately-owned banks. UK benchmark refers to the mortgage market. DCB refers to auto in Europe. | 2. NPS – Customer Satisfaction internal benchmark of active customers’ experience and satisfaction audited by Stiga / Deloitte. | 3. Q1'21 underlying attributable profit by region. Operating areas excluding Corporate Centre. | ||||||||||||||||||

Our corporate culture

The Santander Way remains unchanged to continue to deliver for all our to stakeholders.

Our purpose To help people and businesses prosper. |  | ||||||||||

Our aim To be the best open financial services platform, by acting responsibly and earning the lasting loyalty of our people, customers, shareholders and communities. | |||||||||||

Our how Everything we do should be Simple, Personal and Fair. | |||||||||||

January - March 2021 | | 5 | ||||||

| HIGHLIGHTS OF THE PERIOD | |||||||

u In the first quarter of 2021, we once again demonstrated the strength of our model. We delivered excellent results in an environment marked by new lockdown measures, uneven vaccine roll-outs and the expansion and adjustment of economic policy measures.

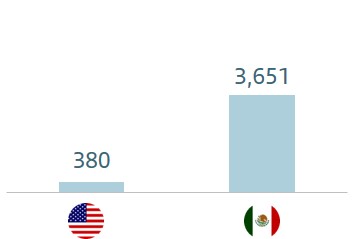

u In line with our strategy to deploy capital in the most profitable businesses, we announced our intention to make a cash offer to repurchase the outstanding shares of Santander Mexico (c. 8.3% of the share capital). The transaction is expected to have a return1 on invested capital (ROIC) of c.14% and improve Banco Santander's earnings per share (EPS)1 by around 0.8% in 2023. Expected impact on the CET1 ratio of -8 bps. The transaction is expected to be completed in the second or third quarter of 2021, following regulatory approvals.

u The board of directors has approved to pay a cash dividend against 2020 earnings, from 4 May 2021, of EUR 2.75 cents per share, the maximum allowed in accordance with the limits set by the European Central Bank (ECB) in its recommendation on 15 December 2020. This will be carried out to implement the premium distribution resolution approved at the general meeting held in October 2020.

| GROWTH | |||||||

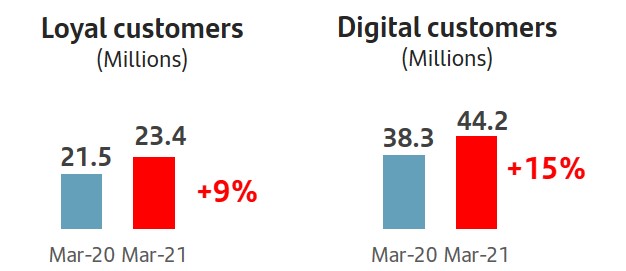

u Digital adoption remains critical: we have more than 44 million digital customers (+15% year-on-year), after a 1.8 million increase in the quarter. In Q1'21, 50% of sales were made through digital channels (41% in Q1'20).

u Loyal customers rose to more than 23 million (+9% year-on-year) and represented 33% of total active customers.

u In the quarter, business volumes continued to be affected by the pandemic and high liquidity in the markets. In this environment, and excluding the exchange rate impact, loans and advances to customers remained flat quarter-on-quarter and increased 2% year-on-year. Customer funds were up 1% in the quarter and 10% year-on-year, due to the higher propensity to save of individuals and corporates.

| PROFITABILITY | |||||||

u Attributable profit amounted to EUR 1,608 million in the quarter, after recording EUR 530 million net of tax from expected restructuring costs for the year as a whole.

u Underlying attributable profit was EUR 2,138 million, significantly higher quarter-on-quarter and year-on-year. Compared to the first quarter of 2020, in constant euros: revenue growth (+8%) and flat costs enabled the efficiency ratio to improve to 45%. In addition, loan-loss provisions recorded its lowest figure since Q1'20.

u Increased profitability: underlying RoTE of 13.0% (2.1% in Q1'20), underlying RoRWA was 1.77% (0.46% in Q1'20) and underlying earnings per share of EUR 0.116 (EUR 0.014 in Q1'20).

| STRENGTH | |||||||

u Cost of credit improved to 1.08% (1.28% in 2020). Total loan-loss reserves in the first quarter exceeded EUR 24 bn, with the total coverage of credit impaired loans at 74%.

u The CET1 ratio was 12.30% (12.34% in December 2020), with strong organic generation of 28 bps (including a -15 bps accrual for shareholder remuneration). On the other hand, negative impacts from restructuring costs (-10 bps), markets (-9 pbs) and regulatory impacts (-13 pbs).

u TNAV per share was EUR 3.84. Including the dividend of EUR 2.75 cents per share, already deducted, growth in the quarter was 2%.

(1) Based on Bloomberg consensus estimates.

| 6 | | January - March 2021 | ||||||

| GRUPO SANTANDER RESULTS | ||||||||

| Grupo Santander. Summarized income statement | ||||||||||||||||||||||||||

| EUR million | ||||||||||||||||||||||||||

| Change | Change | |||||||||||||||||||||||||

| Q1'21 | Q4'20 | % | % excl. FX | Q1'20 | % | % excl. FX | ||||||||||||||||||||

| Net interest income | 7,956 | 8,019 | (0.8) | (1.7) | 8,487 | (6.3) | 5.1 | |||||||||||||||||||

| Net fee income (commission income minus commission expense) | 2,548 | 2,456 | 3.7 | 3.6 | 2,853 | (10.7) | 0.2 | |||||||||||||||||||

| Gains or losses on financial assets and liabilities and exchange differences (net) | 651 | 462 | 40.9 | 40.0 | 287 | 126.8 | 141.3 | |||||||||||||||||||

| Dividend income | 65 | 69 | (5.8) | (6.2) | 57 | 14.0 | 15.3 | |||||||||||||||||||

| Share of results of entities accounted for using the equity method | 76 | (6) | — | — | 98 | (22.4) | (11.3) | |||||||||||||||||||

| Other operating income / expenses | 94 | (76) | — | — | 27 | 248.1 | 119.0 | |||||||||||||||||||

| Total income | 11,390 | 10,924 | 4.3 | 3.6 | 11,809 | (3.5) | 7.9 | |||||||||||||||||||

| Operating expenses | (5,118) | (5,344) | (4.2) | (5.7) | (5,589) | (8.4) | (0.1) | |||||||||||||||||||

| Administrative expenses | (4,435) | (4,634) | (4.3) | (5.8) | (4,860) | (8.7) | (0.4) | |||||||||||||||||||

| Staff costs | (2,688) | (2,685) | 0.1 | (0.7) | (2,899) | (7.3) | 0.4 | |||||||||||||||||||

| Other general administrative expenses | (1,747) | (1,949) | (10.4) | (12.7) | (1,961) | (10.9) | (1.5) | |||||||||||||||||||

| Depreciation and amortization | (683) | (710) | (3.8) | (5.2) | (729) | (6.3) | 1.8 | |||||||||||||||||||

| Provisions or reversal of provisions | (959) | (1,364) | (29.7) | (27.9) | (374) | 156.4 | 192.2 | |||||||||||||||||||

| Impairment or reversal of impairment of financial assets not measured at fair value through profit or loss (net) | (2,056) | (2,844) | (27.7) | (28.7) | (3,934) | (47.7) | (41.5) | |||||||||||||||||||

| Impairment on other assets (net) | (138) | (160) | (13.8) | (11.7) | (14) | 885.7 | 905.7 | |||||||||||||||||||

| Gains or losses on non financial assets and investments, net | 1 | 25 | (96.0) | (97.5) | 18 | (94.4) | (96.4) | |||||||||||||||||||

| Negative goodwill recognised in results | — | (1) | (100.0) | (100.0) | — | — | — | |||||||||||||||||||

| Gains or losses on non-current assets held for sale not classified as discontinued operations | (18) | (41) | (56.1) | (56.1) | (25) | (28.0) | (29.1) | |||||||||||||||||||

| Profit or loss before tax from continuing operations | 3,102 | 1,195 | 159.6 | 162.6 | 1,891 | 64.0 | 97.3 | |||||||||||||||||||

| Tax expense or income from continuing operations | (1,143) | (612) | 86.8 | 91.7 | (1,244) | (8.1) | 1.3 | |||||||||||||||||||

| Profit from the period from continuing operations | 1,959 | 583 | 236.0 | 234.7 | 647 | 202.8 | 341.7 | |||||||||||||||||||

| Profit or loss after tax from discontinued operations | — | — | — | — | — | — | — | |||||||||||||||||||

| Profit for the period | 1,959 | 583 | 236.0 | 234.7 | 647 | 202.8 | 341.7 | |||||||||||||||||||

| Attributable profit to non-controlling interests | (351) | (306) | 14.7 | 15.3 | (316) | 11.1 | 18.1 | |||||||||||||||||||

| Attributable profit to the parent | 1,608 | 277 | 480.5 | 472.1 | 331 | 385.8 | 998.0 | |||||||||||||||||||

EPS (euros) (1) | 0.085 | 0.008 | 951.4 | 0.011 | 670.1 | |||||||||||||||||||||

Diluted EPS (euros) (1) | 0.085 | 0.008 | 948.6 | 0.011 | 669.7 | |||||||||||||||||||||

| Memorandum items: | ||||||||||||||||||||||||||

| Average total assets | 1,526,899 | 1,517,201 | 0.6 | 1,536,725 | (0.6) | |||||||||||||||||||||

| Average stockholders' equity | 81,858 | 82,080 | (0.3) | 99,221 | (17.5) | |||||||||||||||||||||

(1) Data adjusted for the capital increase in December 2020.

January - March 2021 | | 7 | ||||||

| Executive summary | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Profit (Q1'21 vs Q1'20) | Performance (Q1'21 vs Q1'20). In constant euros | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Robust growth spurred by lower provisions and an excellent quarter in SCIB | Higher underlying profit driven by total income, cost control and lower provisions | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Attributable profit | Underlying attrib. profit | Total income | Costs | Provisions | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| EUR 1,608 mn | EUR 2,138 mn | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| EUR 331 mn in Q1'20 | EUR 377 mn in Q1'20 | +7.8% | + 0.1% | -42.9% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Efficiency | Profitability | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| The Group's efficiency ratio improved strongly, mainly driven by Europe | Profitability improved compared to Q1'20 and FY'20, on track to deliver on our 2021 goals | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Group | Europe | RoTE | Underlying RoTE | Underlying RoRWA | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 44.9% | 49.9% | 12.2% | 13.0% | 1.77% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

q2.3 pp vs Q1'20 | q 8.6 pp vs Q1'20 | p10.2 pp vs Q1'20 | p10.9 pp vs Q1'20 | p 1.3 pp vs Q1'20 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

è Results performance compared to Q1'20

The Group presents, both at the total level and for each of the business units, the real changes in euros produced in the income statement, as well as variations excluding the exchange rate effect (FX), on the understanding that the latter provide a better analysis of the Group’s management. For the Group as a whole, exchange rates had a significant impact on revenue (-12 percentage points) and costs (-8 percentage points).

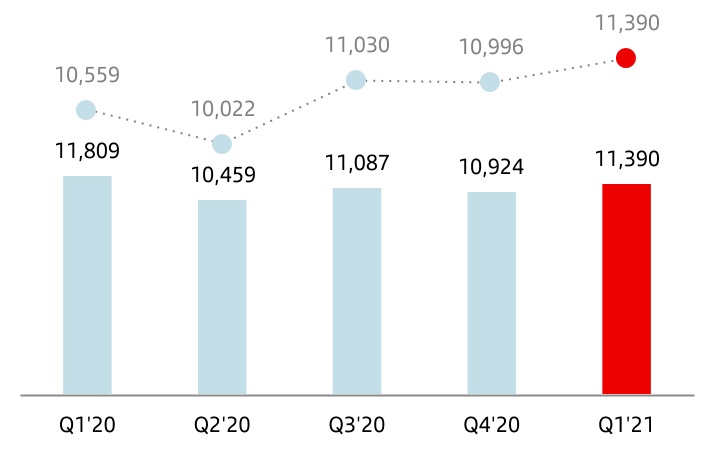

u Revenue

Revenue totalled EUR 11,390 million in the first quarter of 2021, down 4%. If the strong FX impact is taken out, total income increased 8%, with growth in all regions and the majority of countries, showing the strength provided by our geographic and business diversification. Net interest income and net fee income accounted for around 92% of total revenue. By line:

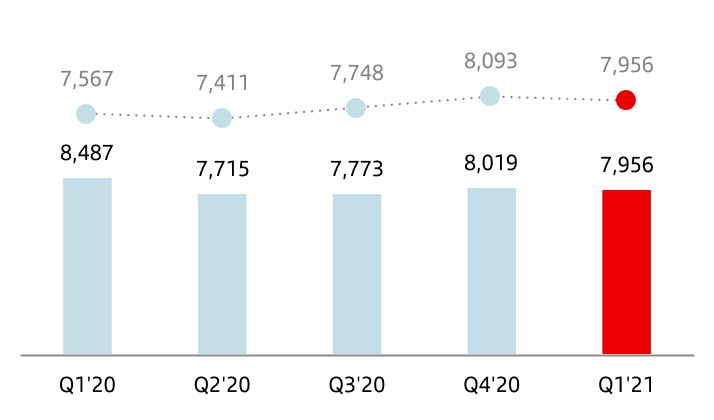

•Net interest income amounted to EUR 7,956 million, 6% less than in Q1'20. Stripping out the exchange rate impact, growth was 5%, mainly due to the net effect of the increase in revenue from higher lending and deposit volumes and the lower cost of the latter, and the reduction in revenue from lower interest rates in many markets.

| Net interest income | |||||

| EUR million | |||||

| constant euros | ||||

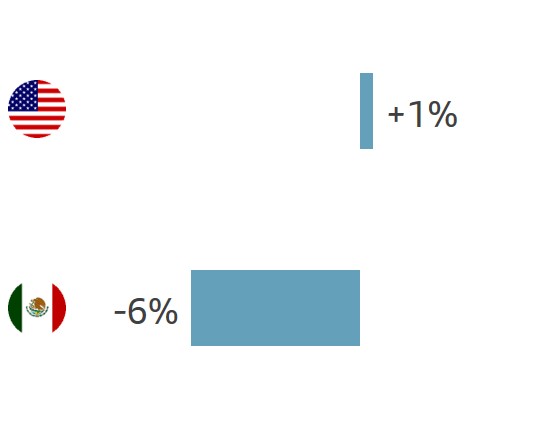

On the one hand, growth was recorded in the UK (+24%), through decisive management deposit repricing actions (mainly the 1I2I3 current account), as well as higher customer balances, partially offset by lower asset yields; Spain (+10%), driven by higher volumes and TLTRO; and Brazil (+6%), due to greater volumes that offset lower interest rates.

On the other hand, Mexico fell 6%, due to lower interest rates and lower portfolio volumes, and the US remained flat despite interest rate cuts.

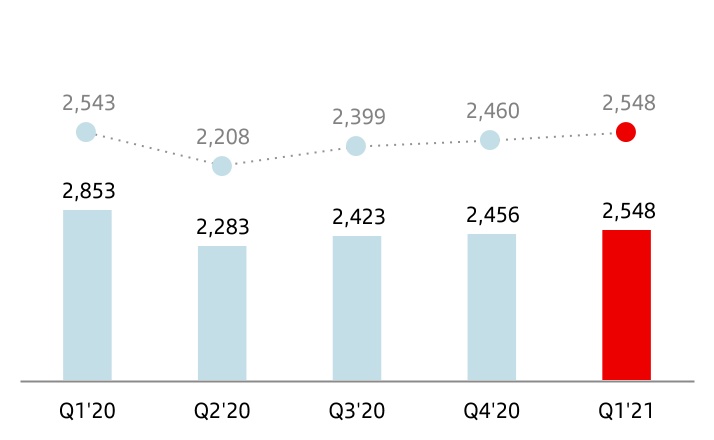

•Net fee income fell 11% year-on-year to EUR 2,548 million. Excluding the exchange rate impact, there was no material change (+0.2%). This item was one of the most affected by the health crisis, mainly from transactional and cards fee income, together with the impact from regulatory changes to overdrafts in the UK that took effect in April 2020.

However, quarterly trends reflected continued growth since the lows reached in the second quarter of 2020.

| Net fee income | |||||

| EUR million | |||||

| constant euros | ||||

| 8 | | January - March 2021 | ||||||

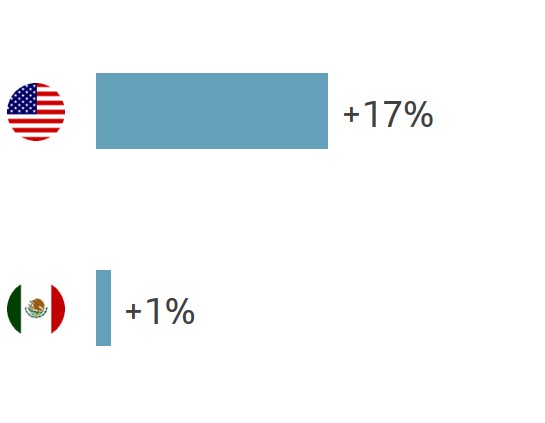

By business, positive performance in value-added products and services. Santander Corporate & Investment Banking surged 28% year-on-year driven by strong markets growth and positive performance in Banking businesses (GDF and GTB). Wealth Management & Insurance rose 3% (including fees ceded to the branch network). Overall, both businesses together accounted for 49% of the Group’s total (SCIB: 18%; WM&I: 31%).

By region, North America grew 7% with rises in the US and Mexico. South America rose 2%, with growth recorded in Chile and Argentina, while Brazil starts to recover. Europe down 4%, with generalized declines in all markets (except Poland), due to lower activity, along with the aforementioned regulatory changes affecting the UK. On the other hand, "Other Europe", which includes the wholesale banking business in the region, increased net fee income by 82%.

•Gains on financial transactions, accounted for 6% of total income and stood at EUR 651 million (EUR 287 million in the first quarter of 2020), strongly driven by Brazil (CIB), Portugal (ALCO portfolio sales) and the US.

•Dividend income was EUR 65 million in the first quarter, 14% higher than in the same period of 2020 (+15% excluding exchange rate effect), after the completion of several dividend payments following last years' reduction, delay or cancellation arising from the pandemic.

•The results of entities accounted for using the equity method reflected the lower contribution from the entities associated to the Group.

•Other operating income amounted to EUR 94 million (EUR 27 million in the first quarter of 2020) driven by the higher results from insurance and leasing.

| Total income | |||||

| EUR million | |||||

| constant euros | ||||

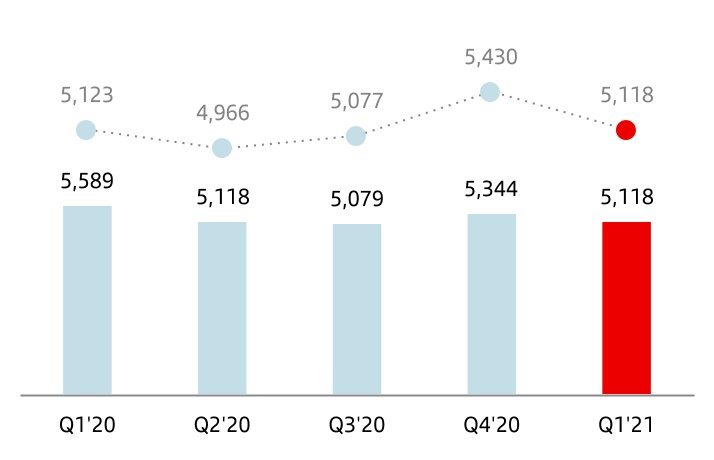

u Costs

Operating costs amounted to EUR 5,118 million, 8% lower year-on-year. Excluding the exchange rate impact, costs remained stable.

This performance reflects the successful management over the last years, as well as the impacts of additional savings measures adopted since the beginning of the crisis.

The efficiency ratio was 44.9%, 2.3 pp higher than last year, driven by overall positive performance across markets, mainly in Europe. This enabled Santander to remain one of the most efficient global banks in the world.

The trends by region and market in constant euros were as follows:

•In Europe, costs were 4% lower, making headway in our cost reduction plan for the year. Falls were recorded in Spain (-8%), the UK (-4%), and Portugal and Poland (both fell -3%). The efficiency ratio in the region improved notably to 50% (-8.6 pp).

•In North America, costs fell 1% in Mexico, driven by technology expenses and amortizations and higher inflation. In the US, they rose only 1% thanks to our disciplined expense management. Saving measures adopted in 2020 are having a positive impact in 2021, which will make funds available for new digital and business initiatives.

•Finally, in South America, the increase in costs (+5%) was greatly distorted by the very high inflation in Argentina. Excluding it, costs rose 1% in nominal terms (Brazil -3% and Chile was virtually flat). The efficiency in the region was 34.4%.

We are building a new operating model across the Group that will enable us to further accelerate transformation and, consequently, further increase productivity while improving customer experience.

| Operating expenses | |||||

| EUR million | |||||

| constant euros | ||||

January - March 2021 | | 9 | ||||||

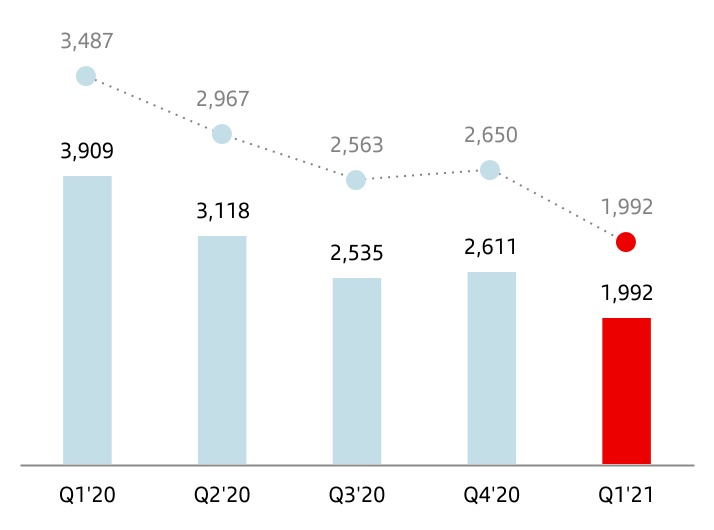

u Provisions or reversal of provisions

Provisions (net of provisions reversals) rose to EUR 959 million (EUR 374 million in Q1'20). This line item includes charges for restructuring costs.

u Impairment or reversal of impairment of financial assets not measured at fair value through profit or loss (net)

Impairment or reversal of impairment on financial assets not measured at fair value through profit or loss (net) was EUR 2,056 million, down 48% year-on-year in euros and -42% in constant euros, mainly from additional provisions recorded in 2020 based on the IFRS 9 forward-looking view and the collective and individual assessments to reflect expected credit losses arising from covid-19.

u Impairment on other assets (net)

Impairment on other assets (net) stood at EUR 138 million. In Q1'20, this line was EUR 14 million.

u Gains or losses on non-financial assets and investments (net)

This item recorded EUR 1 million in the first quarter of 2021, compared to EUR 18 million in the same period of 2020.

| Net loan-loss provisions | |||||

| EUR million | |||||

| constant euros | ||||

u Negative goodwill recognized in results

Both in the first quarter of 2021 as in the first quarter of 2020, this line item recorded EUR 0 million.

u Gains or losses on non-current assets held for sale not classified as discontinued operations

This item, which mainly includes impairment of foreclosed assets recorded and the sale of properties acquired upon foreclosure, totalled -EUR 18 million in the first quarter, compared to -EUR 25 million in the first quarter of 2020.

u Profit before tax

Profit before tax was EUR 3,102 million in the quarter, 64% higher year-on-year (+97% excluding the exchange rate impact) spurred by growth in total income, reduced costs and lower provisions.

u Income tax

Total corporate income tax was EUR 1,143 million (EUR 1,244 million in the first quarter of 2020).

u Attributable profit to non-controlling interests

Attributable profit to non-controlling interests amounted to EUR 351 million, up 11% year-on-year (+18% excluding the exchange rate impact).

u Attributable profit to the parent

Profit attributable to the parent amounted to EUR 1,608 million in 2021, compared with EUR 331 million in the first quarter of 2020.

RoTE stood at 12.2% (2.0% in Q1'20), RoRWA of 1.67% (0.45% in Q1'20) and earnings per share stood at EUR 0.085 (EUR 0.011 in Q1'20).

| 10 | | January - March 2021 | ||||||

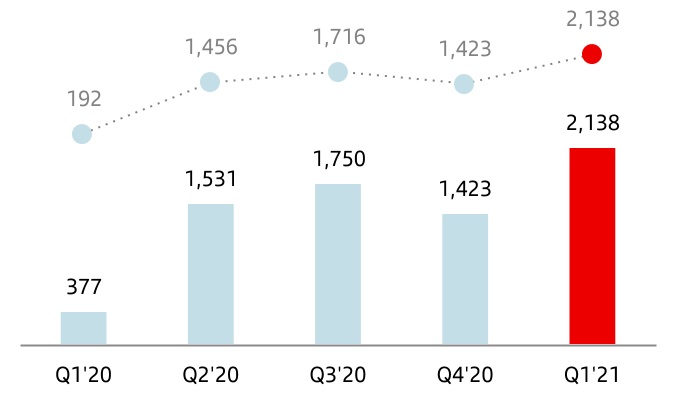

u Underlying attributable profit to the parent

Attributable profit to the parent recorded in the first quarter of 2021 and 2020 was affected by results that are outside the ordinary course of our business and distort the year-on-year comparison, and are detailed below:

•In Q1'21, this result totalled -EUR 530 million due to the recording of restructuring costs as follows: -EUR 293 million in the UK, -EUR 165 million in Portugal, -EUR 16 million in Digital Consumer Bank and -EUR 56 million in the Corporate Centre.

•In the first quarter of 2020, restructuring costs of -EUR 46 million mainly in the UK and Digital Consumer Bank.

For further information see the 'Alternative Performance Measures' section of this report.

Excluding these results from the various P&L lines where they are recorded, and incorporating them separately in the net capital gains and provisions line, the adjusted or underlying attributable profit to the parent was EUR 2,138 million in the first quarter of 2021 and EUR 377 million in the same period last year.

The Group’s cost of credit (considering the last 12 months) stood at 1.08%. Considering the last 3 months, cost of credit was 0.84%, performing better than expected, benefiting from lower provisions in most markets, mainly in the US, Brazil, the UK and Spain.

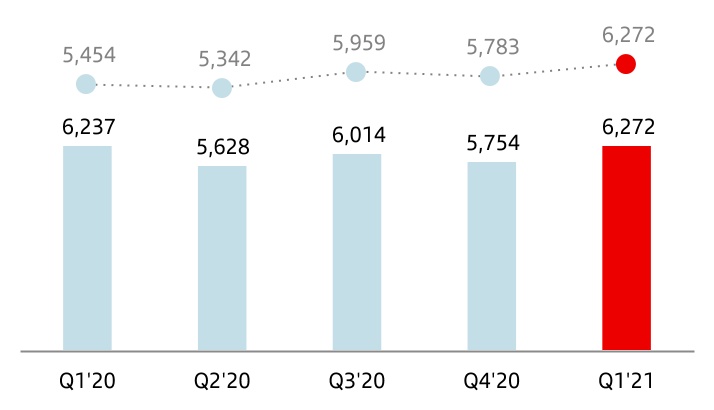

Before the recording of loan-loss provisions, the Group's underlying net operating income (total income less operating expenses) was EUR 6,272 million, a 1% increase year-on-year, which becomes a 15% rise excluding the FX impact, with the following performance of the latter by line and region:

By line:

•Total income up primarily driven by net interest income (+5%) and higher gains on financial transactions.

•Costs remained virtually unchanged, with broad-based declines across Europe and Brazil, and rose 1% in the US, Mexico, Chile and Digital Consumer Bank. Overall efficiency improvement.

By region:

•In Europe, net operating income increased 36% with rises in all markets.

•In North America, net operating income was 4% higher. By country, the US increased 13% and Mexico dropped 7%.

•In South America, growth was 12% with rises of 14% in Brazil, 16% in Chile and 7% in Argentina.

•In Digital Consumer Bank, net operating income increased 1%.

In the first quarter of 2021, the Group’s underlying RoTE was 13.0% (2.1% in Q1'20), underlying RoRWA was 1.77% (0.46% in Q1'20) and underlying earnings per share EUR 0.116 (EUR 0.014 in Q1'20).

| Summarized underlying income statement | ||||||||||||||||||||||||||

| EUR million | Change | Change | ||||||||||||||||||||||||

| Q1'21 | Q4'20 | % | % excl. FX | Q1'20 | % | % excl. FX | ||||||||||||||||||||

| Net interest income | 7,956 | 8,019 | (0.8) | (1.7) | 8,487 | (6.3) | 5.1 | |||||||||||||||||||

| Net fee income | 2,548 | 2,456 | 3.7 | 3.6 | 2,853 | (10.7) | 0.2 | |||||||||||||||||||

Gains (losses) on financial transactions (1) | 651 | 462 | 40.9 | 40.0 | 292 | 122.9 | 141.3 | |||||||||||||||||||

| Other operating income | 235 | 58 | 305.2 | 393.0 | 182 | 29.1 | 26.7 | |||||||||||||||||||

| Total income | 11,390 | 10,995 | 3.6 | 2.9 | 11,814 | (3.6) | 7.8 | |||||||||||||||||||

| Administrative expenses and amortizations | (5,118) | (5,241) | (2.3) | (3.1) | (5,577) | (8.2) | 0.1 | |||||||||||||||||||

| Net operating income | 6,272 | 5,754 | 9.0 | 8.5 | 6,237 | 0.6 | 15.0 | |||||||||||||||||||

| Net loan-loss provisions | (1,992) | (2,611) | (23.7) | (24.8) | (3,909) | (49.0) | (42.9) | |||||||||||||||||||

| Other gains (losses) and provisions | (467) | (485) | (3.7) | (4.9) | (372) | 25.5 | 41.6 | |||||||||||||||||||

| Profit before tax | 3,813 | 2,658 | 43.5 | 44.3 | 1,956 | 94.9 | 132.9 | |||||||||||||||||||

| Tax on profit | (1,324) | (920) | 43.9 | 45.9 | (1,260) | 5.1 | 15.6 | |||||||||||||||||||

| Profit from continuing operations | 2,489 | 1,738 | 43.2 | 43.4 | 696 | 257.6 | 405.5 | |||||||||||||||||||

| Net profit from discontinued operations | — | — | — | (100.0) | — | — | — | |||||||||||||||||||

| Consolidated profit | 2,489 | 1,738 | 43.2 | 43.4 | 696 | 257.6 | 405.5 | |||||||||||||||||||

| Non-controlling interests | (351) | (315) | 11.4 | 12.2 | (319) | 10.0 | 16.7 | |||||||||||||||||||

| Net capital gains and provisions | (530) | (1,146) | (53.8) | (53.6) | (46) | — | — | |||||||||||||||||||

| Attributable profit to the parent | 1,608 | 277 | 480.5 | 472.1 | 331 | 385.8 | 998.0 | |||||||||||||||||||

Underlying attributable profit to the parent (2) | 2,138 | 1,423 | 50.2 | 50.3 | 377 | 467.1 | 1,015.7 | |||||||||||||||||||

(1) Includes exchange differences.

(2) Excludes net capital gains and provisions.

January - March 2021 | | 11 | ||||||

è Results performance compared to the previous quarter

In the first quarter, attributable profit to the parent amounted to EUR 1,608 million, after recording a negative impact of -EUR 530 million, primarily from restructuring costs, in the net capital gains and provisions line.

Stripping them out, attributable profit to the parent amounted to EUR 2,138 million, notably higher than the fourth quarter of 2020 (EUR 1,423 million), which was affected by the contribution to the DGF in Spain and the Bank Levy in the UK.

By line in constant euros:

| Net operating income | |||||

| EUR million | |||||

| constant euros | ||||

•Total income was 3% higher quarter-on-quarter, as the remarkably strong performance in gains on financial transactions and the continued recovery in net fee income (+4%), could absorb the 2% fall in net interest income, affected by some margin pressures and the lower day count.

•Costs were down 3%, mainly driven by North and South America. Conversely, costs in Europe were 2% higher and Digital Consumer Bank was flat.

•Loan-loss provisions plummeted by 25%, with broad-based falls across regions and most countries. Digital Consumer Bank also recorded sharp falls.

| Underlying attributable profit to the parent* | |||||

| EUR million | |||||

| constant euros | ||||

(*) Excluding net capital gains and provisions.

| 12 | | January - March 2021 | ||||||

| Grupo Santander. Condensed balance sheet | |||||||||||||||||

| EUR million | |||||||||||||||||

| Change | |||||||||||||||||

| Assets | Mar-21 | Mar-20 | Absolute | % | Dec-20 | ||||||||||||

| Cash, cash balances at central banks and other demand deposits | 192,925 | 122,456 | 70,469 | 57.5 | 153,839 | ||||||||||||

| Financial assets held for trading | 109,643 | 125,846 | (16,203) | (12.9) | 114,945 | ||||||||||||

| Debt securities | 39,212 | 28,969 | 10,243 | 35.4 | 37,894 | ||||||||||||

| Equity instruments | 11,626 | 8,605 | 3,021 | 35.1 | 9,615 | ||||||||||||

| Loans and advances to customers | 303 | 298 | 5 | 1.7 | 296 | ||||||||||||

| Loans and advances to central banks and credit institutions | 2 | — | 2 | — | 3 | ||||||||||||

| Derivatives | 58,500 | 87,974 | (29,474) | (33.5) | 67,137 | ||||||||||||

| Financial assets designated at fair value through profit or loss | 61,289 | 67,142 | (5,853) | (8.7) | 53,203 | ||||||||||||

| Loans and advances to customers | 27,001 | 31,270 | (4,269) | (13.7) | 24,673 | ||||||||||||

| Loans and advances to central banks and credit institutions | 27,473 | 28,775 | (1,302) | (4.5) | 21,617 | ||||||||||||

| Other (debt securities an equity instruments) | 6,815 | 7,097 | (282) | (4.0) | 6,913 | ||||||||||||

| Financial assets at fair value through other comprehensive income | 113,370 | 110,238 | 3,132 | 2.8 | 120,953 | ||||||||||||

| Debt securities | 101,496 | 99,557 | 1,939 | 1.9 | 108,903 | ||||||||||||

| Equity instruments | 2,793 | 2,291 | 502 | 21.9 | 2,783 | ||||||||||||

| Loans and advances to customers | 9,081 | 8,390 | 691 | 8.2 | 9,267 | ||||||||||||

| Loans and advances to central banks and credit institutions | — | — | — | — | — | ||||||||||||

| Financial assets measured at amortised cost | 981,581 | 981,331 | 250 | — | 958,378 | ||||||||||||

| Debt securities | 26,430 | 26,033 | 397 | 1.5 | 26,078 | ||||||||||||

| Loans and advances to customers | 903,375 | 895,449 | 7,926 | 0.9 | 881,963 | ||||||||||||

| Loans and advances to central banks and credit institutions | 51,776 | 59,849 | (8,073) | (13.5) | 50,337 | ||||||||||||

| Investments in subsidiaries, joint ventures and associates | 7,693 | 8,610 | (917) | (10.7) | 7,622 | ||||||||||||

| Tangible assets | 33,386 | 34,912 | (1,526) | (4.4) | 32,735 | ||||||||||||

| Intangible assets | 15,990 | 26,583 | (10,593) | (39.8) | 15,908 | ||||||||||||

| Goodwill | 12,460 | 23,141 | (10,681) | (46.2) | 12,471 | ||||||||||||

| Other intangible assets | 3,530 | 3,442 | 88 | 2.6 | 3,437 | ||||||||||||

| Other assets | 47,002 | 63,241 | (16,239) | (25.7) | 50,667 | ||||||||||||

| Total assets | 1,562,879 | 1,540,359 | 22,520 | 1.5 | 1,508,250 | ||||||||||||

| Liabilities and shareholders' equity | |||||||||||||||||

| Financial liabilities held for trading | 71,293 | 100,082 | (28,789) | (28.8) | 81,167 | ||||||||||||

| Customer deposits | — | — | — | — | — | ||||||||||||

| Debt securities issued | — | — | — | — | — | ||||||||||||

| Deposits by central banks and credit institutions | — | — | — | — | — | ||||||||||||

| Derivatives | 55,935 | 88,121 | (32,186) | (36.5) | 64,469 | ||||||||||||

| Other | 15,358 | 11,961 | 3,397 | 28.4 | 16,698 | ||||||||||||

| Financial liabilities designated at fair value through profit or loss | 69,977 | 67,337 | 2,640 | 3.9 | 48,038 | ||||||||||||

| Customer deposits | 49,394 | 44,638 | 4,756 | 10.7 | 34,343 | ||||||||||||

| Debt securities issued | 4,538 | 4,287 | 251 | 5.9 | 4,440 | ||||||||||||

| Deposits by central banks and credit institutions | 16,045 | 18,412 | (2,367) | (12.9) | 9,255 | ||||||||||||

| Other | — | — | — | — | — | ||||||||||||

| Financial liabilities measured at amortized cost | 1,290,475 | 1,224,749 | 65,726 | 5.4 | 1,248,188 | ||||||||||||

| Customer deposits | 833,460 | 770,821 | 62,639 | 8.1 | 814,967 | ||||||||||||

| Debt securities issued | 240,765 | 257,606 | (16,841) | (6.5) | 230,829 | ||||||||||||

| Deposits by central banks and credit institutions | 189,095 | 170,275 | 18,820 | 11.1 | 175,424 | ||||||||||||

| Other | 27,155 | 26,047 | 1,108 | 4.3 | 26,968 | ||||||||||||

| Liabilities under insurance contracts | 1,102 | 2,280 | (1,178) | (51.7) | 910 | ||||||||||||

| Provisions | 10,881 | 12,335 | (1,454) | (11.8) | 10,852 | ||||||||||||

| Other liabilities | 26,465 | 27,463 | (998) | (3.6) | 27,773 | ||||||||||||

| Total liabilities | 1,470,193 | 1,434,246 | 35,947 | 2.5 | 1,416,928 | ||||||||||||

| Shareholders' equity | 115,620 | 124,139 | (8,519) | (6.9) | 114,620 | ||||||||||||

| Capital stock | 8,670 | 8,309 | 361 | 4.3 | 8,670 | ||||||||||||

| Reserves | 105,342 | 117,161 | (11,819) | (10.1) | 114,721 | ||||||||||||

| Attributable profit to the Group | 1,608 | 331 | 1,277 | 385.8 | (8,771) | ||||||||||||

| Less: dividends | — | (1,662) | 1,662 | (100.0) | — | ||||||||||||

| Other comprehensive income | (33,154) | (27,761) | (5,393) | 19.4 | (33,144) | ||||||||||||

| Minority interests | 10,220 | 9,735 | 485 | 5.0 | 9,846 | ||||||||||||

| Total equity | 92,686 | 106,113 | (13,427) | (12.7) | 91,322 | ||||||||||||

| Total liabilities and equity | 1,562,879 | 1,540,359 | 22,520 | 1.5 | 1,508,250 | ||||||||||||

January - March 2021 | | 13 | ||||||

| GRUPO SANTANDER BALANCE SHEET | ||||||||

| Executive summary * | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

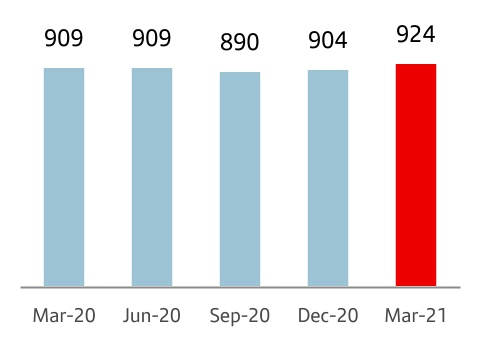

Loans and advances to customers (excl. reverse repos) | Customer funds (deposits excl. repos + mutual funds) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Credit normalization following the uptick at the beginning of the pandemic, due to high liquidity in the system | Strong increase in customer funds benefiting from the higher propensity to save derived from the health crisis | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

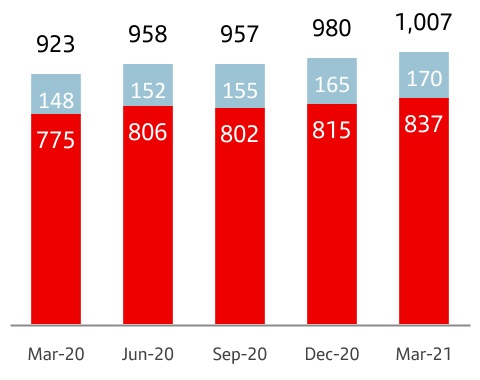

| 924 | p 0.4% QoQ | p 2% YoY | 1,007 | p 1% QoQ | p 10% YoY | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| billion | billion | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

è By segment (YoY change): | è By product (YoY change): | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Of note was the rise in SMEs and corporates | Of note were demand deposits, which account for 66% of customer funds, reflected in the lower costs of deposits | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Individuals | SMEs and corporates | CIB and institutions | Demand | Time | Mutual funds | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| +1% | +7% | -3% | +14% | -9% | +19% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| (*) Changes in constant euros | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Exchange rates had no impact in loans and only -1 pp in customer funds on a year-on-year basis.

è Loans and advances to customers

Gross loans and advances to customers stood at EUR 939,760 million. The Group uses gross loans and advances to customers excluding reverse repos (EUR 924,430 million) for the purpose of analyzing traditional commercial banking loans.

In the first quarter, gross loans and advances to customers excluding reverse repos rose 2%. Without the exchange rate impact, they remained flat (+0.4%), as follws:

•Balances in Europe were stable. Decreases were recorded in Spain, while the UK and Portugal remained broadly stable. Poland rose 2% and 'Other Europe' +9%.

•North America fell 2% dampened by the US, as Mexico increased 2%.

•In South America, 3% growth with all markets increasing, except Chile, that remained flat.

•Digital Consumer Bank (DCB) dropped 1% with slight falls in the main consumer finance units, except Italy and the UK.

Compared to March 2020, a 2% increase was recorded in gross loans and advances to customers excluding reverse repos. Excluding the FX impact, loans also grew 2%, as follows:

•In Europe, 2% growth with all markets increasing except Poland (-1%). Of note was growth in Portugal (+5%), driven by SMEs and mortgages, and Spain (+3%) backed by SMEs and corporates. The UK rose 1%, driven by residential mortgage activity and the government programmes for corporate customers, and "Other Europe" grew 5%, mainly SCIB.

•In North America, Mexico fell 6% as corporate loans began to normalize following the uptick at the beginning of the pandemic and the lower card activity during lockdown, and the US fell 3% affected by Puerto Rico and Bluestem portfolio disposal (+1% excluding their impacts). The region as a whole recorded a 4% decrease (-1% excluding the impact of Puerto Rico and Bluestem portfolio disposal).

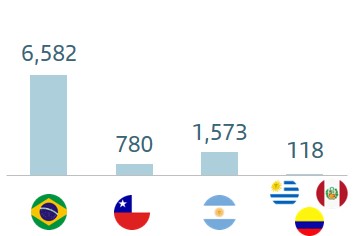

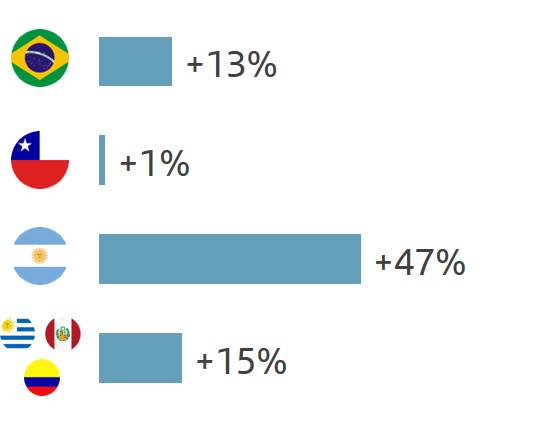

•Growth in South America was 10%, with Argentina up 47% driven by SMEs and cards, Brazil +13% with positive performance in all segments and Chile +1% driven by SMEs and mortgages. Uruguay rose 6%.

•DCB declined slightly (-1%) dampened by the falls recorded in Spain, Poland and the Nordics. On the other hand, Openbank surged 29%, albeit compared to more modest figures.

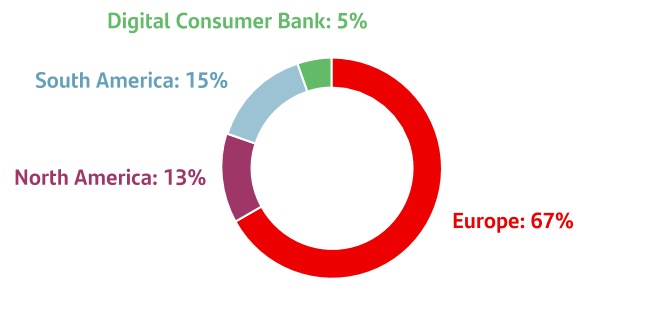

Gross loans and advances to customers excluding reverse repos maintained a balanced structure: individuals (62%), SMEs and corporates (23%) and CIB (15%).

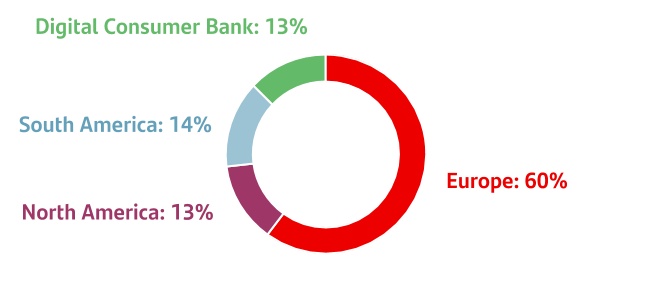

| Gross loans and advances to customers (excl. reverse repos) | |||||

| EUR billion | |||||

| Gross loans and advances to customers (excl. reverse repos) | ||

| % operating areas. March 2021 | ||

| +2 | % | * | |||

| Mar-21 / Mar-20 | |||||

(*) In constant EUR: +2%

| 14 | | January - March 2021 | ||||||

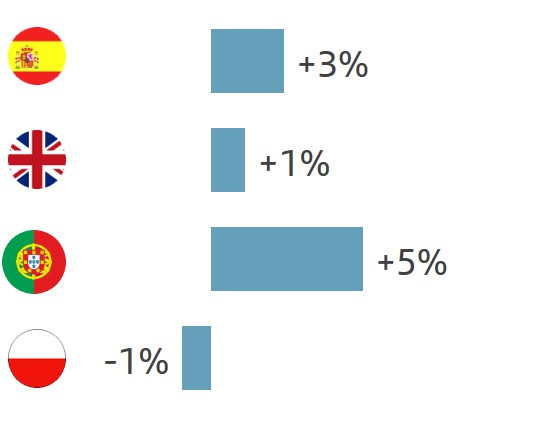

è Customer funds

Customer deposits amounted to EUR 882,854 million in March 2021. The Group uses customer funds (customer deposits excluding repos, plus mutual funds) for the purpose of analyzing traditional retail banking funds.

•In the first quarter, customer funds increased slightly to EUR 1,007,319 million, with the following performance excluding exchange rate impacts:

–By product: demand deposits rose 2% and mutual funds 3%, whilst time deposits decreased 1%.

–By primary segment: customer funds increased 1% in Europe, with 6% growth in Poland, 1% in Portugal and no material changes across other units. North America rose 4% backed by the US, and South America remained stable, as the 2% decrease in Brazil was closely matched by growth across the rest of markets. DCB rose 3%, notably Openbank (+8%).

•Compared to March 2020, customer funds were up 9%. Excluding the exchange rate impact, increase of 10%, as follows:

–By product, deposits excluding repos rose 8%. Demand deposits (+14%) increased in all markets, and time deposits fell 9%, with broad-based declines except Brazil and Argentina. Mutual funds surged 19% underpinned by net inflows and markets recovery.

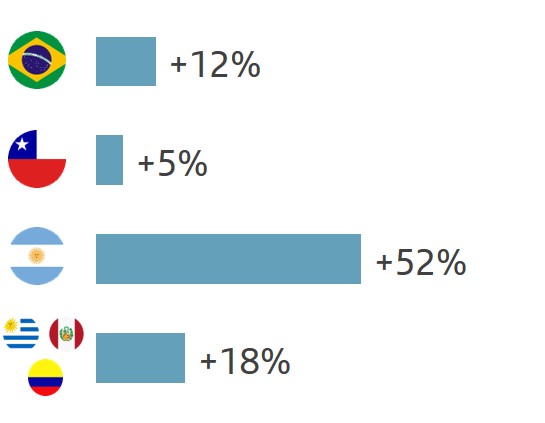

–By country, customer funds rose in all regions and their respective units. Of note were the increases in Argentina (+52%), Poland (+19%), Uruguay (+15%) and Brazil and the US (+12% each). In the remaining markets, growth ranged between +10% in Spain and +1% in Mexico.

–Positive performance also in DCB, which rose 8%. Openbank increased 24%.

With this performance, the weight of demand deposits as a percentage of total customer funds rose 3 pp in the last 12 months to 66%, which resulted in a better cost of deposits.

In addition to capturing customer deposits, the Group, for strategic reasons, maintains a selective policy of issuing securities in the international fixed income markets and strives to adapt the frequency and volume of its market operations to the structural liquidity needs of each unit, as well as to the receptiveness of each market.

In the first quarter of 2021, the Group issued:

•Medium- and long-term senior debt amounting to EUR 3,428 million.

•There were EUR 4,433 million of securitizations placed in the market.

•In order to strengthen the Group’s situation, issuances to meet the TLAC requirement amounting to EUR 4,936 million, all senior non-preferred.

•Maturities of medium- and long-term debt of EUR 4,303 million.

The net loan-to-deposit ratio was 106% (115% in March 2020). The ratio of deposits plus medium- and long-term funding to the Group’s loans was 117%, underscoring the comfortable funding structure.

The Group's access to wholesale funding markets as well as the cost of issuances depends, in part, on the ratings of the rating agencies.

In the first quarter of 2021, the main rating agencies did not review their ratings for Banco Santander S.A: Fitch (long-term senior non-preferred debt at A- and short-term at F2, with a negative outlook), Moody's (A2 for long term debt and P-1 for short-term, with an stable outlook), Standard & Poor’s (A for long term debt and A-1 for short term, with a negative outlook) and DBRS (A high for long term debt and R-1 middle for short term, with an stable outlook).

While sometimes the methodology applied by the agencies limits a bank's rating to the sovereign rating assigned to the country where it is headquartered, Banco Santander, S.A. is still rated above the sovereign debt rating of the Kingdom of Spain by Moody’s and DBRS and at the same level by Fitch and S&P, which demonstrates our financial strength and diversification.

| Customer funds | ||

| EUR billion | ||

| Customer funds | ||

| % operating areas. March 2021 | ||

| +9 | % | * | ||||||

| +15 | % | |||||||

| +8 | % | |||||||

•Total | ||||||||

•Mutual funds | ||||||||

•Deposits exc. repos | ||||||||

| Mar-21 / Mar-20 | ||||||||

(*) In constant EUR: +10%

January - March 2021 | | 15 | ||||||

| SOLVENCY RATIOS | ||||||||

| Executive summary | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Phased-in capital ratio* | Phased-in CET1 ratio* | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| The phased-in CET1 ratio exceeded our 11%-12% target range, resulting in a management buffer of 345 bps | In the quarter, strong organic generation and charges for shareholder remuneration and restructuring costs | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Organic generation of +28 bps (after a -15 bps accrual for shareholder remuneration) | Restructuring costs | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| -10 bps | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| TNAV per share | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

TNAV per share was EUR 3.84. Including the dividend of EUR 2.75 cents per share, already deducted, growth in the quarter was 2%. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

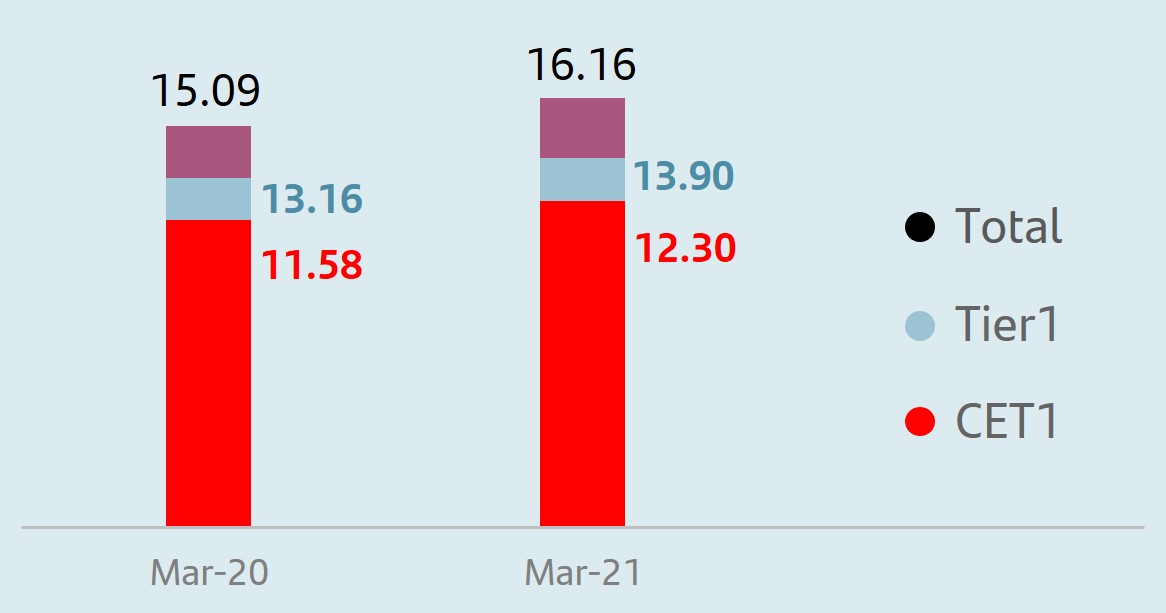

At the end of the quarter, the total phased-in capital ratio stood at 16.16% and the CET1 ratio (phased-in) at 12.30%. We have a strong capital base, comfortably meeting the minimum levels required by the European Central Bank on a consolidated basis (13.01% for the total capital ratio and 8.85% for the CET1 ratio). This results in a CET1 management buffer of 345 bps, compared to the pre-covid-19 buffer of 189 bps.

In the quarter, continued a strong organic capital generation of 28 bps due to underlying profit and management of risk weighted assets. This figure includes a negative impact of 15 bps for shareholder remuneration, equivalent to 40% of this quarter's underlying profit. The bank is accruing 40% of the underlying profit throughout the year for this remuneration, once supervisors allow**.

In addition, the following movements were recorded in the quarter:

•Regulatory impacts and models, -13 bps, of which -6 bps correspond to the IFRS 9 phase-out.

•Market performance, -9 bps.

•Lastly, restructuring costs had a negative impact of -10 bps.

Had the IFRS 9 transitional arrangement not been applied, the total impact on the CET1 ratio was -41 bps, leading to a fully-loaded CET1 ratio of 11.89%.

The phased-in leverage ratio stood at 5.1%, and the fully-loaded at 4.9%.

| Eligible capital. March 2021 | ||||||||

| EUR million | ||||||||

| Phased-in* | Fully-loaded | |||||||

| CET1 | 69,841 | 67,468 | ||||||

| Basic capital | 78,944 | 76,258 | ||||||

| Eligible capital | 91,764 | 89,692 | ||||||

| Risk-weighted assets | 567,797 | 567,342 | ||||||

| CET1 capital ratio | 12.30 | 11.89 | ||||||

| T1 capital ratio | 13.90 | 13.44 | ||||||

| Total capital ratio | 16.16 | 15.81 | ||||||

| Phased-in CET1 ratio performance* | ||

| % | ||

| ||

(*) The phased-in ratio includes the transitory treatment of IFRS 9, calculated in accordance with article 473 bis of the Capital Requirements Regulation (CRR) and subsequent modifications introduced by Regulation 2020/873 of the European Union. Without it, the fully-loaded ratio is 11.89%. Additionally, the Tier 1 and total phased-in capital ratios include the transitory treatment according to chapter 2, title 1, part 10 of the CRR.

(**) Subject to the board and, if applicable, the general shareholders' meeting adopting the pertinent resolutions regarding shareholder remuneration and dividend payment policy

| 16 | | January - March 2021 | ||||||

| RISK MANAGEMENT | ||||||||

| Executive summary | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Credit risk | Market risk | |||||||||||||||||||||||||||||||||||||||||||||||||

| Credit quality indicators began to show signs of normalization | Market risk exposure maintained its low profile, with stable VaR levels amid reduced market uncertainty following progress on vaccination programmes | |||||||||||||||||||||||||||||||||||||||||||||||||

Cost of credit2 | NPL ratio | Coverage ratio | ||||||||||||||||||||||||||||||||||||||||||||||||

| 1.08% | 3.20% | 74% | Q1'21 | Average Var | EUR 9.5 million | |||||||||||||||||||||||||||||||||||||||||||||

q20 bps vs Q4'20 | q1bps vs Q4'20 | q 2 pp vs Q4'20 | ||||||||||||||||||||||||||||||||||||||||||||||||

| Structural and liquidity risk | Operational risk | |||||||||||||||||||||||||||||||||||||||||||||||||

| We maintained a comfortable liquidity position, well above regulatory limits | Our operational risk profile continued to be stable in the first quarter of 2021, as all our subsidiaries have fully adapted their operating guidelines to the new environment | |||||||||||||||||||||||||||||||||||||||||||||||||

LCR 173% p 5 pp vs Q4'20 | ||||||||||||||||||||||||||||||||||||||||||||||||||

u Credit risk management

In the first quarter of 2021 the Group’s NPL ratio stood at 3.20%, showing a slight decrease compared to the previous quarter. This was mainly driven by the growth of the portfolio in SCIB, Brazil and the UK, together with the sale of credit impaired loans portfolios in Spain, in a context in which government liquidity support still play a relevant role together with improving macroeconomic projections.

Credit impaired loans amounted to EUR 32,473 million, a 2% (in constant euros) increase compared to the previous quarter.

In terms of loan-loss provisions, they amounted to EUR 1,992 million in the first quarter of 2021, after the additional amounts built last year to tackle the effects of the covid-19 crisis, reflecting the IFRS 9 forward-looking view and based on a long-term approach to the potential macroeconomic scenarios.

This figure is 25% lower than the previous quarter, following a normalization trend, and 43% lower than in the first quarter of 2020, both in constant euros.

Consequently the Group's cost of credit stood at 1.08%, a 20 bps decrease compared to the previous quarter.

Total loan-loss reserves in the first quarter stood at EUR 24,034 million, with the total coverage of credit impaired loans at 74% (+3 pp year-on-year).

A significant part of our portfolios in Spain and the UK have real estate collateral, which requires lower coverage levels.

| Key metrics performance by geographic area | |||||||||||||||||||||||||||||||||||||||||

Loan-loss provisions 1 | Cost of credit (%) 2 | NPL ratio (%) | Coverage ratio (%) | ||||||||||||||||||||||||||||||||||||||

| Q1'21 | Chg (%) / Q4'20 | Chg (%) / Q1'20 | Q1'21 | Chg (bps) / Q4'20 | Chg (bps) / Q1'20 | Q1'21 | Chg (bps) / Q1'20 | Q1'21 | Chg (pp) / Q1'20 | ||||||||||||||||||||||||||||||||

| Europe | 595 | (36.1) | (40.3) | 0.51 | (7) | 15 | 3.26 | (11) | 50.0 | 3.0 | |||||||||||||||||||||||||||||||

| Spain | 449 | (26.5) | (28.6) | 0.91 | (10) | 27 | 6.18 | (70) | 47.2 | 2.6 | |||||||||||||||||||||||||||||||

| United Kingdom | 18 | (82.1) | (89.6) | 0.21 | (6) | 7 | 1.35 | 36 | 40.5 | 0.8 | |||||||||||||||||||||||||||||||

| Portugal | 35 | (16.9) | (56.9) | 0.38 | (13) | 15 | 3.84 | (72) | 69.2 | 10.2 | |||||||||||||||||||||||||||||||

| Poland | 68 | (14.8) | (24.8) | 1.02 | (7) | 14 | 4.82 | 53 | 70.3 | 2.2 | |||||||||||||||||||||||||||||||

| North America | 393 | (49.3) | (65.3) | 2.34 | (58) | (68) | 2.39 | 37 | 153.4 | (16.7) | |||||||||||||||||||||||||||||||

| USA | 165 | (70.7) | (81.4) | 2.12 | (74) | (101) | 2.11 | 11 | 183.2 | 1.7 | |||||||||||||||||||||||||||||||

| Mexico | 228 | 7.5 | (6.7) | 3.00 | (3) | 31 | 3.21 | 114 | 95.6 | (38.3) | |||||||||||||||||||||||||||||||

| South America | 683 | (6.5) | (33.2) | 2.81 | (52) | (49) | 4.30 | (33) | 98.4 | 5.5 | |||||||||||||||||||||||||||||||

| Brazil | 549 | 0.9 | (30.6) | 3.79 | (55) | (63) | 4.42 | (52) | 116.5 | 8.5 | |||||||||||||||||||||||||||||||

| Chile | 100 | 1.9 | (39.5) | 1.33 | (17) | 8 | 4.74 | 11 | 63.4 | 6.2 | |||||||||||||||||||||||||||||||

| Argentina | 14 | (79.8) | (71.5) | 4.55 | (138) | (93) | 2.32 | (165) | 232.4 | 101.2 | |||||||||||||||||||||||||||||||

| Digital Consumer Bank | 166 | (20.0) | (49.7) | 0.69 | (14) | 7 | 2.23 | 2 | 111.4 | (0.1) | |||||||||||||||||||||||||||||||

| Corporate Centre | 154 | — | — | ||||||||||||||||||||||||||||||||||||||

| TOTAL GROUP | 1,992 | (24.8) | (42.9) | 1.08 | (20) | (9) | 3.20 | (5) | 74.0 | 2.7 | |||||||||||||||||||||||||||||||

| (1) EUR million and % change in constant euros | |||||||||||||||||||||||||||||||||||||||||

| (2) Allowances for loan-loss provisions over the last 12 months / Average loans and advances to customers over the last 12 months | |||||||||||||||||||||||||||||||||||||||||

January - March 2021 | | 17 | ||||||

After the efforts made by the Group to tackle the covid-19 crisis through different support measures with particular focus on moratoria programmes, etc., in the first quarter of 2021, 86% of total moratoria had already expired, showing the expected payment performance with only 5% in stage 3.

The outstanding moratoria are being closely monitored, which totalled EUR 16 bn (mainly in Spain and Portugal), of which c. EUR 7 bn will expire by the end of the second quarter.

Regarding IFRS 9 stages evolution:

•Stage 1 exposures increased by 2.4% vs. the previous quarter, mainly due to new loan originations in SCIB and Brazil.

•Exposure in stage 2 rose in this first quarter after the increase recorded last year, mostly driven by the macroeconomic deterioration caused by the pandemic.

•Stage 3 remained broadly stable.

| Coverage ratio by stage | |||||||||||||||||||||||

| EUR billion | |||||||||||||||||||||||

Exposure1 | Coverage | ||||||||||||||||||||||

| Mar-21 | Dec-20 | Mar-20 | Mar-21 | Dec-20 | Mar-20 | ||||||||||||||||||

| Stage 1 | 885 | 864 | 891 | 0.5 | % | 0.5 | % | 0.6 | % | ||||||||||||||

| Stage 2 | 70 | 69 | 53 | 8.1 | % | 8.5 | % | 8.2 | % | ||||||||||||||

| Stage 3 | 32 | 32 | 33 | 42.5 | % | 43.4 | % | 40.8 | % | ||||||||||||||

(1) Exposure subject to impairment. Additionally, in March 2021 there are EUR 27 billion in loans and advances to customers not subject to impairment recorded at mark to market with changes through P&L (EUR 25 billion in December 2020 and EUR 31 in March 2020).

Stage 1: financial instruments for which no significant increase in credit risk is identified since its initial recognition.

Stage 2: if there has been a significant increase in credit risk since the date of initial recognition but the impairment event has not materialized, the financial instrument is classified in Stage 2.

Stage 3: a financial instrument is catalogued in this stage when it shows effective signs of impairment as a result of one or more events that have already occurred resulting in a loss.

| Credit impaired loans and loan-loss allowances | |||||||||||

| EUR million | |||||||||||

| Change (%) | |||||||||||

| Q1'21 | QoQ | YoY | |||||||||

| Balance at beginning of period | 31,767 | 2.8 | (6.0) | ||||||||

| Net additions | 2,495 | (25.2) | (1.9) | ||||||||

| Increase in scope of consolidation | — | — | — | ||||||||

| Exchange rate differences and other | 444 | — | — | ||||||||

| Write-offs | (2,233) | 5.5 | (15.3) | ||||||||

| Balance at period-end | 32,473 | 2.2 | (0.8) | ||||||||

| Loan-loss allowances | 24,034 | (1.0) | 2.9 | ||||||||

| For impaired assets | 13,804 | 0.17 | 3.29 | ||||||||

| For other assets | 10,230 | (2.50) | 2.33 | ||||||||

u Market risk

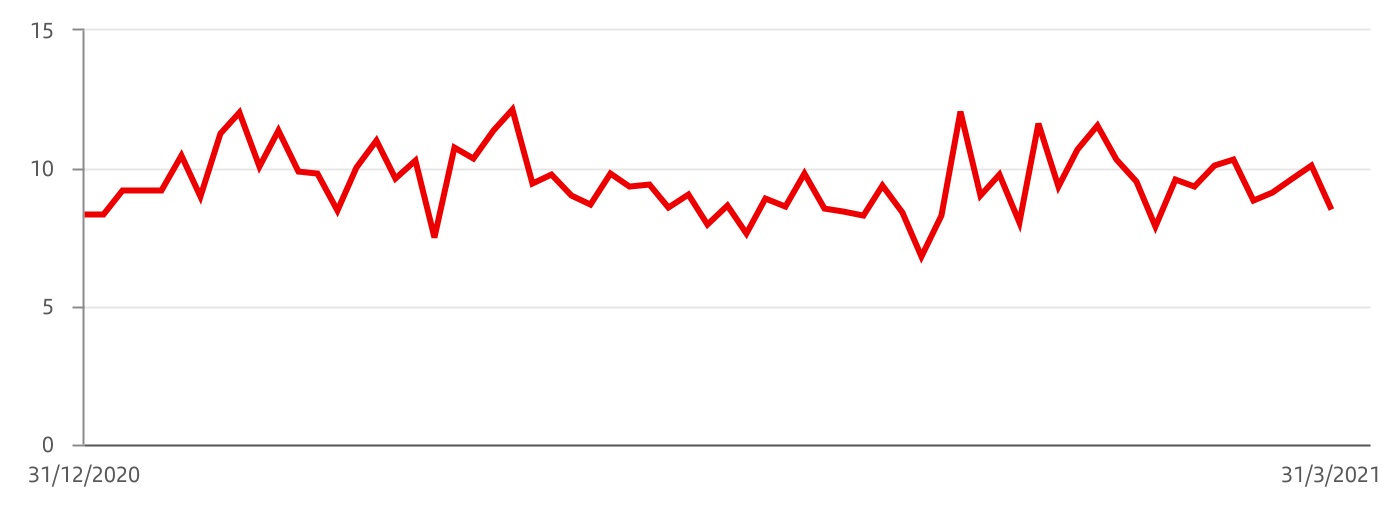

The global corporate banking trading activity is mainly interest rate driven, focused on servicing our customer's needs and measured in daily VaR terms at 99%.

In the first quarter, VaR closed at EUR 8.5 million, fluctuating around an average value of EUR 9.5 million. It remained stable, driven by lower market uncertainty as vaccine roll-out gained traction, although covid-19 evolution is still a concern by the end of Q1’21. These figures remain low compared to the size of the Group’s balance sheet and activity.

It should be also mentioned that there are other positions classified for accounting purposes as trading (total VaR of EUR 8.5 million at the end of March 2021).

Trading portfolios (1). VaR by geographic region | ||||||||||||||

| EUR million | ||||||||||||||

| 2021 | 2020 | |||||||||||||

| First quarter | Average | Latest | Average | |||||||||||

| Total | 9.5 | 8.5 | 15.8 | |||||||||||

| Europe | 7.9 | 8.5 | 10.7 | |||||||||||

| North America | 2.8 | 2.4 | 5.6 | |||||||||||

| South America | 4.6 | 4.8 | 8.0 | |||||||||||

(1) Activity performance in Santander Corporate & Investment Banking markets.

Trading portfolios (1). VaR by market factor | ||||||||||||||

| EUR million | ||||||||||||||

| First quarter | Min. | Avg. | Max. | Last | ||||||||||

| VaR total | 6.8 | 9.5 | 12.1 | 8.5 | ||||||||||

| Diversification effect | (9.1) | (11.5) | (16.0) | (10.0) | ||||||||||

| Interest rate VaR | 6.8 | 9.5 | 13.1 | 8.2 | ||||||||||

| Equity VaR | 2.4 | 3.0 | 4.4 | 2.7 | ||||||||||

| FX VaR | 1.9 | 3.8 | 6.7 | 3.1 | ||||||||||

| Credit spreads VaR | 2.6 | 3.8 | 7.3 | 3.7 | ||||||||||

| Commodities VaR | 0.6 | 0.9 | 2.4 | 0.9 | ||||||||||

(1) Activity performance in Santander Corporate & Investment Banking markets.

NOTE: In the North America, South America and Asia portfolios, VaR corresponding to the credit spreads factor other than sovereign risk is not relevant and is included in the interest rate factor

| 18 | | January - March 2021 | ||||||

Trading portfolios1. VaR performance | ||

| EUR million | ||

(1) Corporate & Investment Banking performance in financial markets.

(1) Corporate & Investment Banking performance in financial markets.u Structural and liquidity risk

•With regards to structural exchange rate risk, the Group's CET1 ratio coverage remained around 100% in order to protect it from foreign currency movements.

•Regarding structural interest rate risk, despite volatility in bond markets and the increase in interest rates amid expectations of rising inflation along the economic recovery, no material issues were detected in the quarter and it remained at comfortable levels.

•Concerning liquidity risk during the first quarter, the Group maintained a comfortable position, supported by a robust and diversified liquidity buffer, with ratios well above regulatory limits.

u Operational risk

•Overall, our operational risk profile continued to be stable during the first quarter of 2021, as the Group´s headquarters and subsidiaries have fully adapted to the new environment. The following aspects were closely monitored during this period:

–Fraud and cyber risk threats across the financial industry, and reinforcement of the control environment (i.e. patching, browsing control, data protection controls, etc.), as well as heightening monitoring as a preventive measure.

–Third party risk exposure, maintaining a close oversight on critical providers, with focus on business continuity capabilities and compliance with service level agreements.

–People risk, due to our employees return to offices and/or work from home situations, which varies across the Group´s subsidiaries. Measures have been implemented to ensure a suitable and safe work environment.

–Evolution of operational risks linked to the existing portfolios derived from government and internal aid programmes.

•As the situation continues to evolve, we are also monitoring the changes in the environment as well as the transition to digital banking in order to identify risk exposures and anticipate actions in order to reduce their impact.

•In terms of the first quarter performance, level of losses in relative terms by Basel categories were lower than in the previous quarter.

January - March 2021 | | 19 | ||||||

| GENERAL BACKGROUND | ||||||||

Grupo Santander ran its business in the first quarter of 2021 in an environment marked by the resurgence of the virus and the consequent selective containment measures, the uneven vaccine roll-out and the expansion and / or adjustment of economic policy measures. More favourable medium-term expectations counterbalanced the challenging short-term horizon, which helped to maintain a relatively positive tone in markets, with more complex episodes arising from the emergence of inflationary risks in the US that caused a hike in long-term interest rates and some weakness in several emerging market currencies.

| Country | GDP Change1 | Economic performance | |||||||||

| Eurozone | -6.7% | Q1'21 indicators point to continued economic weakness, although it is expected to recover in the second half of the year. The unemployment rate did not reflect this deterioration (it remained stable) due to public employment protection programmes. Inflation has picked up so far this year (1.3% year-on-year in March) due to higher indirect taxes, higher energy prices and changes in the CPI basket. | ||||||||

| Spain | -10.8% | The job market recorded a slight deterioration in the first months of 2021, pointing toward a contraction of GDP in Q1'21. The unemployment rate, which ended Q4'20 at 16.1%, could have risen. Inflation rose to 1.3% year-on-year in March, driven by higher energy prices (underlying inflation remained very low, at 0.3% year-on-year). | ||||||||

| United Kingdom | -9.8% | The resurgence of covid-19 cases led to new lockdown measures at the beginning of Q1'21, which combined with the tensions arising from the need of businesses to adapt to the new trade agreement with the EU, led to a further decline of quarterly GDP (c.1.5%). Inflation in March (0.7%) reflected the weak tone in consumption. Unemployment rate ended 2020 at 5%. The UK's official interest rate remained at 0.1%. | ||||||||

| Portugal | -7.6% | After the economy's sharp slump in 2020, covid-19 surges caused the economy to stall again in Q1'21. Tighter lockdown measures will lead to a further reduction quarter-on-quarter. Unemployment rose to 7.2% in January and sluggish consumption rose inflation to 0.5% in March. | ||||||||

| Poland | -2.8% | The economic recession in 2020 was less severe than in other surrounding countries. However, demand in Q1'21 will remain weak dampened by the covid-19 rebound, but we still expect slight growth in the quarter. The unemployment rate stood at 3.1% in Q4'20, inflation remained high (3.2% in March) and Poland's central bank will keep the official interest rate at 0.1%. | ||||||||

| United States | -3.5% | GDP growth slowed to 4.3% quarter-on-quarter annualized in Q4'20. The unemployment rate is gradually declining (6.0% in March) and inflation began to recover (2.6% in March). Vaccines and stimulus roll-out led to a significant outlook improvement, which boosted long-term rates. The Fed remained on hold and stated that it is early to change its policy. | ||||||||

| Mexico | -8.2% | Activity weakened in Q1'21 after the rebound in H2'20, due to the increase in covid-19 infections and the containment of exports. Mexico's central bank lowered the official interest rate to 4% (from 4.25% in Q4'20) and, thereafter, it will monitor the factors that might impact inflation, following the spike recorded in February to 4.7% (3.2% at the end of 2020) and to the climate of market uncertainty. | ||||||||

| Brazil | -4.1% | Economic growth recovered strongly in the second half of the year, after the contraction caused by the pandemic in the first half of 2020. The sharp increase in covid-19 cases and the reintroduction of containment measures will weigh down on Q1'21 GDP growth. Inflation rebounded (6.1% in March) and Brazil's central bank raised the official interest rate to 2.75% (2.0% in Q4'20) to prevent a deterioration in medium-term forecasts. | ||||||||

| Chile | -5.8% | The late 2020 recovery trend continued in January, but it was dampened by the resurgence of the pandemic in Q1'21. However, the country's fast pace of vaccination sustains positive expectations for the coming quarters. Inflation moderated to 2.9% in March, aligned with the 3% target. Chile's official interest rate was stable (0.5%). | ||||||||

| Argentina | -9.9% | GDP contracted in 2020, affected by the pandemic, although it partially recovered in the second half of the year. The resurgence of covid-19 cases in early 2021 suggests a downturn in Q1'21. Inflation remained high (4.8% monthly average in March). The focus will be on the renegotiation of the IMF agreement. | ||||||||

(1) Year-on-year change 2020

| 20 | | January - March 2021 | ||||||

| DESCRIPTION OF SEGMENTS | ||||||||

We base segment reporting on financial information presented to the chief operating decision maker, which excludes certain statutory results items that distort year-on-year comparisons and are not considered for management reporting. This financial information (underlying basis) is computed by adjusting reported results for the effects of certain gains and losses (e.g. capital gains, write-downs, impairment of goodwill, etc.). These gains and losses are items that management and investors ordinarily identify and consider separately to better understand the underlying trends in the business.

Grupo Santander has aligned the information in this chapter with the underlying information used internally for management reporting and with that presented in Grupo Santander's other public documents.

Grupo Santander executive committee has been selected to be its chief operating decision maker. Grupo Santander's operating segments reflect its organizational and managerial structures. The executive committee reviews internal reporting based on these segments to assess performance and allocate resources.

The segments are split by geographic area in which profits are earned and by type of business. We prepare the information by aggregating the figures for Grupo Santander’s various geographic areas and business units, relating it to both the accounting data of the business units integrated in each segment and that provided by management information systems. The general principles applied are the same as those used in Grupo Santander, and accounting integrity is ensured.

On 9 April 2021, we announced that, starting and effective with the financial information for the first quarter of 2021, we would carry out a change in our reportable segments to reflect our new organizational and management structure.

These changes in the reportable segments aim to align the segment information with their management and have no impact on the group’s accounting figures.

a.Main changes in the composition of Grupo Santander's segments

The main changes, which have been applied to management information for all periods included in the consolidated financial statements, are the following:

Primary segments

1.Creation of the new Digital Consumer Bank (DCB) segment, which includes:

•Santander Consumer Finance (SCF), previously included in the Europe segment, and the consumer finance business in the United Kingdom, previously recorded in the country.

•Our fully digital bank Openbank and the Open Digital Services (ODS) platform, which were previously included in the Santander Global Platform segment.

2.Santander Global Platform (SGP), which incorporated our global digital services under a single unit, is no longer a primary segment. Its activities have been distributed as follows:

•Openbank and Open Digital Services (ODS), which, as mentioned above, are now included under the new Digital Consumer Bank reporting segment.

•The business recorded in Global Payment Services (Merchant Solutions -GMS-, Trade Solutions -GTS- and Consumer Solutions -Superdigital and Pago FX-) has been allocated to the three main geographic segments, Europe, North America and South America, with no impact on the information reported for each country.

Secondary segments

1.Creation of the PagoNxt segment, which incorporates simple and accessible digital payment solutions to drive customer loyalty and allows us to combine our most disruptive payment businesses into a single autonomous company, providing global technology solutions for our banks and new customers in the open market, and which has been structured into three businesses, previously included in SGP:

•Merchant Solutions: acquiring solutions for merchants.

•Trade Solutions (GTS): solutions for SMEs and companies operating internationally.

•Consumer Solutions: payment solutions for individuals, including the Superdigital platform, aimed at underbanked populations, and Pago FX, an international payment service in the open market.

2. Annual adjustment of the perimeter of the Global Customer Relationship Model between Retail Banking and Santander Corporate & Investment Banking and between Retail Banking and Wealth Management & Insurance.

3.Elimination of the Santander Global Platform reporting segment:

•Openbank and ODS are now recorded in the Retail Banking segment.

•Merchant Solutions, Trade Solutions, Superdigital and Pago FX form the new PagoNxt reporting segment.

The Group recasted the corresponding information of earlier periods considering the changes included in this section. As stated above, group consolidated figures remain unchanged.

January - March 2021 | | 21 | ||||||

b. Current composition of Grupo Santander segments

Primary segments

This primary level of segmentation, which is based on the Group’s management structure, comprises five reportable segments: four operating areas plus the Corporate Centre. The operating areas are:

Europe: which comprises all business activity carried out in the region, except that included in Digital Consumer Bank. Detailed financial information is provided on Spain, the UK, Portugal and Poland.

North America: which comprises all the business activities carried out in Mexico and the US, which includes the holding company (SHUSA) and the businesses of Santander Bank, Santander Consumer USA, the specialized business unit Banco Santander International, Santander Investment Securities (SIS) and the New York branch.

South America: includes all the financial activities carried out by Grupo Santander through its banks and subsidiary banks in the region. Detailed information is provided on Brazil, Chile, Argentina, Uruguay, Peru and Colombia.

Digital Consumer Bank: includes Santander Consumer Finance, which incorporates the entire consumer finance business in Europe, Openbank and ODS.

Secondary segments

At this secondary level, Grupo Santander is structured into Retail Banking, Santander Corporate & Investment Banking (SCIB), Wealth Management & Insurance (WM&I) and PagoNxt.

Retail Banking: this covers all customer banking businesses, including consumer finance, except those of corporate banking which are managed through Santander Corporate & Investment Banking, asset management, private banking and insurance, which are managed by Wealth Management & Insurance. The results of the hedging positions in each country are also included, conducted within the sphere of their respective assets and liabilities committees.

Santander Corporate & Investment Banking (SCIB): this business reflects revenue from global corporate banking, investment banking and markets worldwide including treasuries managed globally (always after the appropriate distribution with Retail Banking customers), as well as equity business.

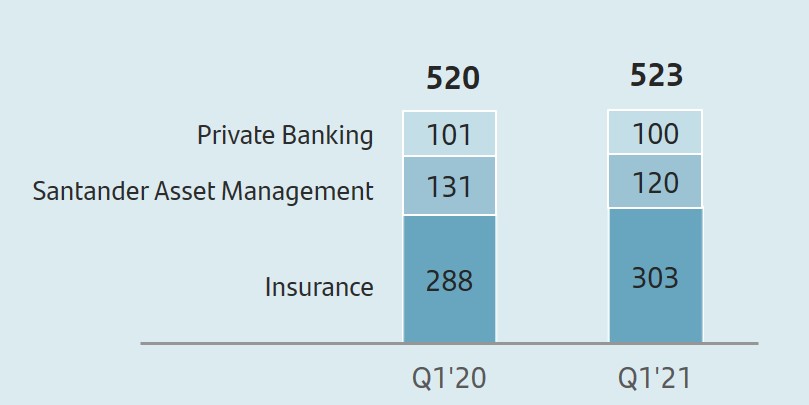

Wealth Management & Insurance: includes the asset management business (Santander Asset Management), the corporate unit of Private Banking and International Private Banking in Miami and Switzerland and the insurance business (Santander Insurance).

PagoNxt: this includes digital payment solutions, providing global technology solutions for our banks and new customers in the open market. It is structured in three businesses: Merchant Solutions, Trade Solutions and Consumer Solutions.

In addition to these operating units, both primary and secondary segments, the Group continues to maintain the area of Corporate Centre, that includes the centralized activities relating to equity stakes in financial companies, financial management of the structural exchange rate position, assumed within the sphere of the Group’s assets and liabilities committee, as well as management of liquidity and of shareholders’ equity via issuances.

As the Group’s holding entity, this area manages all capital and reserves and allocations of capital and liquidity with the rest of businesses. It also incorporates amortization of goodwill but not the costs related to the Group’s central services (charged to the areas), except for corporate and institutional expenses related to the Group’s functioning.