FORM 6-K

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Report of Foreign Issuer

Pursuant to Rule 13a-16 or 15d-16

of the Securities Exchange Act of 1934

For the month of January, 2024

Commission File Number: 001-12518

Banco Santander, S.A.

(Exact name of registrant as specified in its charter)

Ciudad Grupo Santander

28660 Boadilla del Monte (Madrid) Spain

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

Form 20-F ☒ Form 40-F ☐

BANCO SANTANDER, S.A.

________________________

TABLE OF CONTENTS

| Item 1. January - December 2023 Financial Report | |||||

| January - December | 2023 | ||||

Index

This report was approved by the board of directors on 30 January 2024, following a favourable report from the audit committee. Important information regarding this report can be found on pages 89 and 90.

Key consolidated data

| BALANCE SHEET (EUR million) | Dec-23 | Sep-23 | % | Dec-23 | Dec-22 | % | Dec-21 | ||||||||||||||||

| Total assets | 1,797,062 | 1,816,844 | (1.1) | 1,797,062 | 1,734,659 | 3.6 | 1,595,835 | ||||||||||||||||

| Loans and advances to customers | 1,036,349 | 1,039,172 | (0.3) | 1,036,349 | 1,036,004 | 0.0 | 972,682 | ||||||||||||||||

| Customer deposits | 1,047,169 | 1,034,885 | 1.2 | 1,047,169 | 1,009,722 | 3.7 | 900,554 | ||||||||||||||||

| Total funds | 1,306,942 | 1,288,547 | 1.4 | 1,306,942 | 1,239,981 | 5.4 | 1,135,866 | ||||||||||||||||

| Total equity | 104,241 | 102,897 | 1.3 | 104,241 | 97,585 | 6.8 | 97,053 | ||||||||||||||||

| Note: total funds includes customer deposits, mutual funds, pension funds and managed portfolios. | |||||||||||||||||||||||

| INCOME STATEMENT (EUR million) | Q4'23 | Q3'23 | % | 2023 | 2022 | % | 2021 | ||||||||||||||||

| Net interest income | 11,122 | 11,219 | (0.9) | 43,261 | 38,619 | 12.0 | 33,370 | ||||||||||||||||

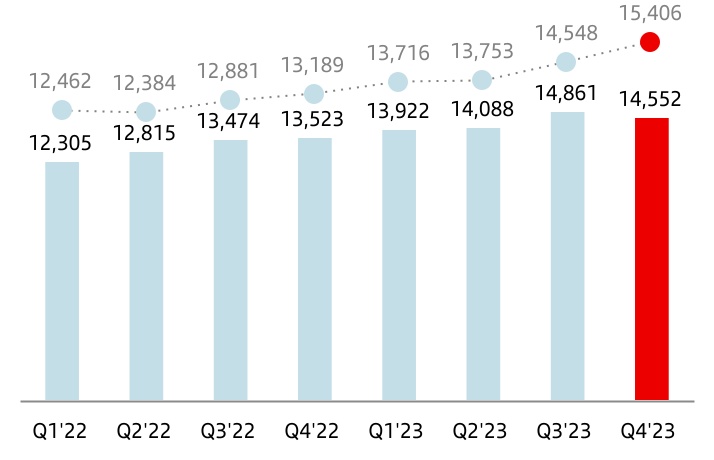

| Total income | 14,552 | 14,861 | (2.1) | 57,423 | 52,117 | 10.2 | 46,404 | ||||||||||||||||

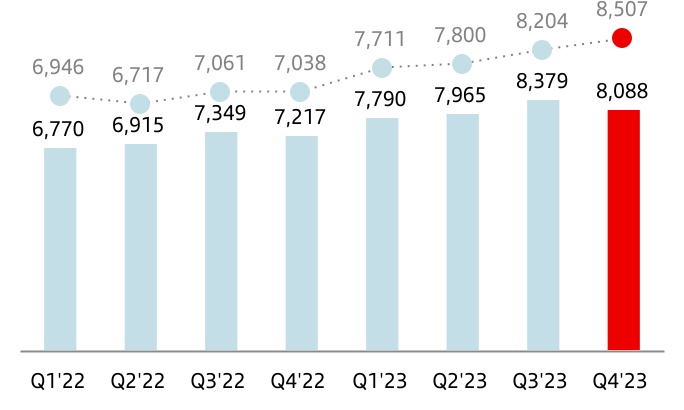

| Net operating income | 8,088 | 8,379 | (3.5) | 31,998 | 28,214 | 13.4 | 24,989 | ||||||||||||||||

| Profit before tax | 3,922 | 4,447 | (11.8) | 16,459 | 15,250 | 7.9 | 14,547 | ||||||||||||||||

| Profit attributable to the parent | 2,933 | 2,902 | 1.1 | 11,076 | 9,605 | 15.3 | 8,124 | ||||||||||||||||

| Changes in constant euros: | |||||||||||||||||||||||

| Q4'23 / Q3'23: NII: +11.1%; Total income: +5.9%; Net operating income: +3.7%; Profit before tax: -2.0%; Attributable profit: +12.1%. | |||||||||||||||||||||||

| 2023 / 2022: NII: +15.8%; Total income: +12.8%; Net operating income: +15.4%; Profit before tax: +9.7%; Attributable profit: +17.7%. | |||||||||||||||||||||||

| EPS, PROFITABILITY AND EFFICIENCY (%) | Q4'23 | Q3'23 | % | 2023 | 2022 | % | 2021 | ||||||||||||||||

| EPS (euros) | 0.18 | 0.17 | 2.2 | 0.65 | 0.54 | 21.5 | 0.44 | ||||||||||||||||

| RoE | 12.36 | 12.28 | 11.91 | 10.67 | 9.66 | ||||||||||||||||||

| RoTE | 15.64 | 15.49 | 15.06 | 13.37 | 11.96 | ||||||||||||||||||

| RoA | 0.71 | 0.71 | 0.69 | 0.63 | 0.62 | ||||||||||||||||||

| RoRWA | 2.04 | 2.02 | 1.96 | 1.77 | 1.69 | ||||||||||||||||||

| Efficiency ratio | 44.4 | 43.6 | 44.1 | 45.8 | 46.2 | ||||||||||||||||||

UNDERLYING INCOME STATEMENT 1 (EUR million) | Q4'23 | Q3'23 | % | 2023 | 2022 | % | 2021 | ||||||||||||||||

| Net interest income | 11,122 | 11,219 | (0.9) | 43,261 | 38,619 | 12.0 | 33,370 | ||||||||||||||||

| Total income | 14,552 | 14,861 | (2.1) | 57,647 | 52,154 | 10.5 | 46,404 | ||||||||||||||||

| Net operating income | 8,088 | 8,379 | (3.5) | 32,222 | 28,251 | 14.1 | 24,989 | ||||||||||||||||

| Profit before tax | 3,922 | 4,447 | (11.8) | 16,698 | 15,250 | 9.5 | 15,260 | ||||||||||||||||

| Profit attributable to the parent | 2,933 | 2,902 | 1.1 | 11,076 | 9,605 | 15.3 | 8,654 | ||||||||||||||||

| Changes in constant euros: | |||||||||||||||||||||||

| Q4'23 / Q3'23: NII: +11.1%; Total income: +5.9%; Net operating income: +3.7%; Profit before tax: -2.0%; Attributable profit: +12.1%. | |||||||||||||||||||||||

| 2023 / 2022: NII: +15.8%; Total income: +13.1%; Net operating income: +16.1%; Profit before tax: +11.3%; Attributable profit: +17.7%. | |||||||||||||||||||||||

UNDERLYING EPS AND PROFITABILITY 1 (%) | Q4'23 | Q3'23 | % | 2023 | 2022 | % | 2021 | ||||||||||||||||

| Underlying EPS (euros) | 0.18 | 0.17 | 2.2 | 0.65 | 0.54 | 21.5 | 0.47 | ||||||||||||||||

| Underlying RoE | 12.36 | 12.28 | 11.91 | 10.67 | 10.29 | ||||||||||||||||||

| Underlying RoTE | 15.64 | 15.49 | 15.06 | 13.37 | 12.73 | ||||||||||||||||||

| Underlying RoA | 0.71 | 0.71 | 0.69 | 0.63 | 0.65 | ||||||||||||||||||

| Underlying RoRWA | 2.04 | 2.02 | 1.96 | 1.77 | 1.78 | ||||||||||||||||||

January - December 2023 |  | 3 | ||||||

| SOLVENCY (%) | Dec-23 | Sep-23 | Dec-23 | Dec-22 | Dec-21 | ||||||||||||||||||

| Fully-loaded CET1 ratio | 12.3 | 12.3 | 12.3 | 12.0 | 12.1 | ||||||||||||||||||

| Fully-loaded total capital ratio | 16.3 | 16.2 | 16.3 | 15.8 | 16.4 | ||||||||||||||||||

| CREDIT QUALITY (%) | Q4'23 | Q3'23 | 2023 | 2022 | 2021 | ||||||||||||||||||

Cost of risk2 | 1.18 | 1.13 | 1.18 | 0.99 | 0.77 | ||||||||||||||||||

| NPL ratio | 3.14 | 3.13 | 3.14 | 3.08 | 3.16 | ||||||||||||||||||

| NPL coverage ratio | 66 | 68 | 66 | 68 | 71 | ||||||||||||||||||

| MARKET CAPITALIZATION AND SHARES | Dec-23 | Sep-23 | % | Dec-23 | Dec-22 | % | Dec-21 | ||||||||||||||||

| Shares (millions) | 16,184 | 16,184 | 0.0 | 16,184 | 16,794 | (3.6) | 17,341 | ||||||||||||||||

| Share price (euros) | 3.780 | 3.619 | 4.4 | 3.780 | 2.803 | 34.9 | 2.941 | ||||||||||||||||

| Market capitalization (EUR million) | 61,168 | 58,562 | 4.4 | 61,168 | 47,066 | 30.0 | 50,990 | ||||||||||||||||

| Tangible book value per share (euros) | 4.76 | 4.61 | 4.76 | 4.26 | 4.12 | ||||||||||||||||||

| Price / Tangible book value per share (X) | 0.79 | 0.79 | 0.79 | 0.66 | 0.71 | ||||||||||||||||||

| CUSTOMERS (thousands) | Q4'23 | Q3'23 | % | 2023 | 2022 | % | 2021 | ||||||||||||||||

| Total customers | 164,542 | 166,250 | (1.0) | 164,542 | 159,844 | 2.9 | 152,943 | ||||||||||||||||

| Active customers | 99,503 | 100,614 | (1.1) | 99,503 | 99,190 | 0.3 | 96,887 | ||||||||||||||||

| Loyal customers | 29,286 | 28,470 | 2.9 | 29,286 | 27,456 | 6.7 | 25,548 | ||||||||||||||||

| Digital customers | 54,161 | 53,568 | 1.1 | 54,161 | 51,471 | 5.2 | 47,489 | ||||||||||||||||

| Digital sales / Total sales (%) | 57.7 | 56.7 | 56.3 | 55.1 | 54.4 | ||||||||||||||||||

| OTHER DATA | Dec-23 | Sep-23 | % | Dec-23 | Dec-22 | % | Dec-21 | ||||||||||||||||

| Number of shareholders | 3,662,377 | 3,703,401 | (1.1) | 3,662,377 | 3,915,388 | (6.5) | 3,936,922 | ||||||||||||||||

| Number of employees | 212,764 | 212,219 | 0.3 | 212,764 | 206,462 | 3.1 | 199,177 | ||||||||||||||||

| Number of branches | 8,518 | 8,652 | (1.5) | 8,518 | 9,019 | (5.6) | 9,229 | ||||||||||||||||

| 1. | In addition to financial information prepared in accordance with International Financial Reporting Standards (IFRS) and derived from our consolidated financial statements, this report contains certain financial measures that constitute alternative performance measures (APMs) as defined in the Guidelines on Alternative Performance Measures issued by the European Securities and Markets Authority (ESMA) on 5 October 2015, and other non-IFRS measures, including the figures related to “underlying” results, which do not include factors that are outside the ordinary course of our business, or have been reclassified within the underlying income statement. Further details are provided in the “Alternative performance measures” section of the appendix to this report. For further details on the APMs and non-IFRS measures used, including their definition or a reconciliation between any applicable management indicators and the financial data presented in the annual consolidated financial statements prepared under IFRS, please see our 2022 Annual Financial Report, published in the CNMV on 28 February 2023, our 20-F report for the year ending 31 December 2022 filed with the SEC in the United States on 1 March 2023 as well as the “Alternative performance measures” section of the appendix to this report. | ||||

| 2. | Allowances for loan-loss provisions over the last 12 months / Average loans and advances to customers over the last 12 months. | ||||

| 4 | | January - December 2023 | ||||||

| Group financial information | Financial information by segment | Responsible banking Corporate governance Santander share | Appendix | |||||||||||||||||||||||

Our business model is based on three pillars

| 01. Customer focus | 02. Our scale | 03. Diversification | ||||||||||||||||||||||||

Digital bank with branches | Local and global scale | Geographic and business diversification. Solid and diversified balance sheet | ||||||||||||||||||||||||

| Transform our business and operating model through our global technology initiatives to build a digital bank with branches that provides access to financial services for our customers through several channels. | In-market scale in each of our core markets in volumes combined with our global scale support greater profitability and provide a competitive advantage over local peers. | Our well-balanced diversification between developing and mature markets, as well as between business and customer segments, delivers recurrent pre-provision profit with low volatility. | ||||||||||||||||||||||||

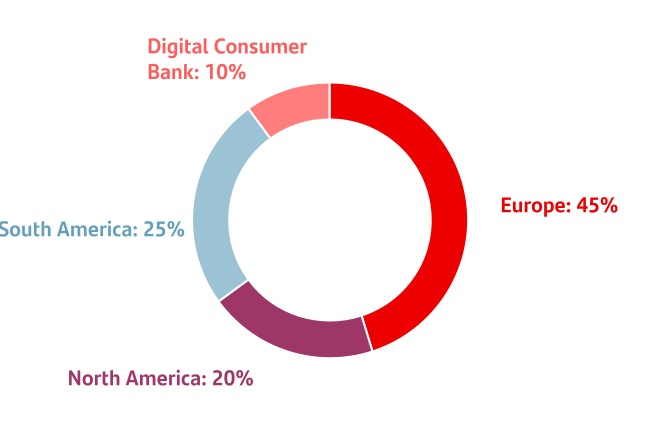

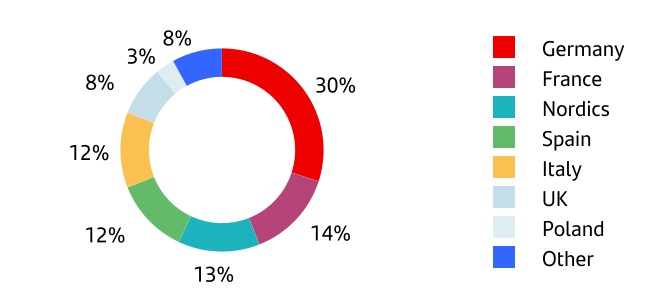

| Top 3 NPS1 | Top 3 in lending2 in 9 of our markets | Contribution to Group profit3 | |||||||||||||||||||||||

| in 7 markets |  | |||||||||||||||||||||||||

| 165 mn total customers |  | ||||||||||||||||||||||||

100 mn active customers | ||||||||||||||||||||||||||

| Our business model remains a source of great strength and resilience | ||||||||||||||||||||||||||

Our corporate culture

The Santander Way remains unchanged to continue to deliver for all our stakeholders

Our purpose To help people and businesses prosper. |  | ||||||||||

Our aim To be the best open financial services platform, by acting responsibly and earning the lasting loyalty of our people, customers, shareholders and communities. | |||||||||||

Our how Everything we do should be Simple, Personal and Fair. | |||||||||||

1.NPS – internal benchmark of individual customers' satisfaction audited by Stiga/Deloitte in H2'23.

2.Market share in lending as of September 2023 including only privately-owned banks. Digital Consumer Bank (DCB) refers to auto in Europe.

3.FY'23 attributable profit by region, as a percentage of total operating areas excluding the Corporate Centre.

January - December 2023 | | 5 | ||||||

Highlights of the period

| PROFIT | |||||||

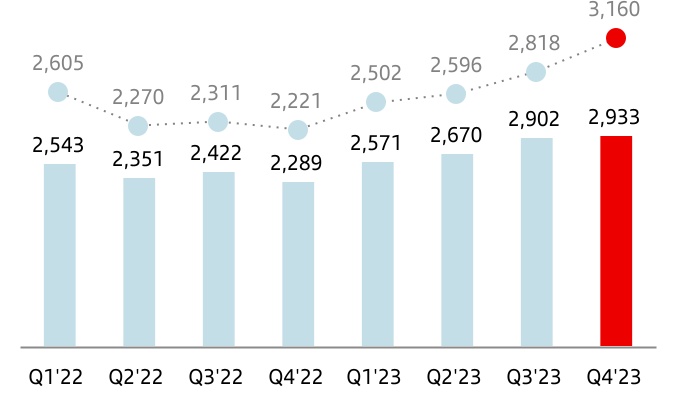

| u | In Q4 2023, attributable profit amounted to EUR 2,933 million, 1% more than in the previous quarter (+12% in constant euros) and 28% more than in Q4 2022 (+42% in constant euros). | |||||||||

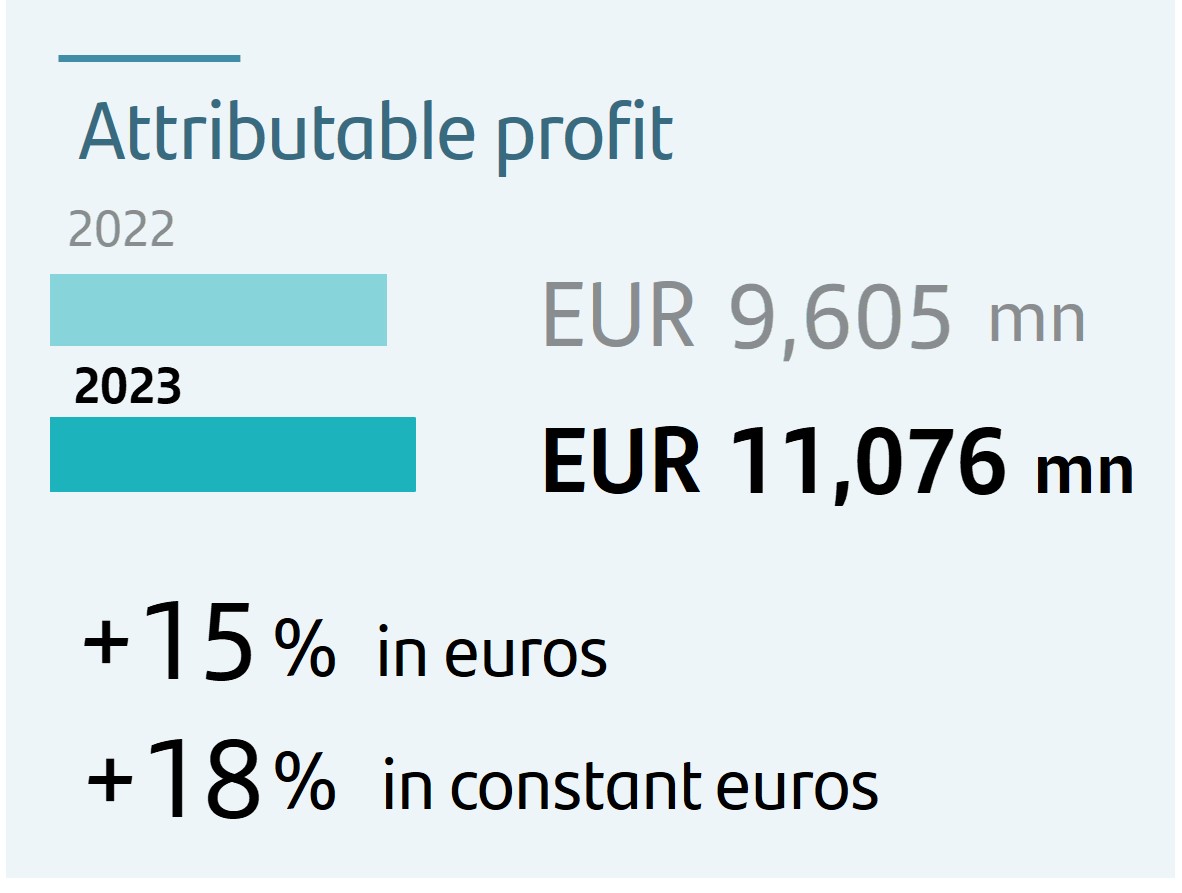

| u | In 2023, attributable profit was EUR 11,076 million, 15% higher than in 2022 (+18% in constant euros) and 18% and 20% higher, respectively, if we exclude the temporary levy on revenue obtained in Spain and DCB in Q1 2023. | ||||||||||

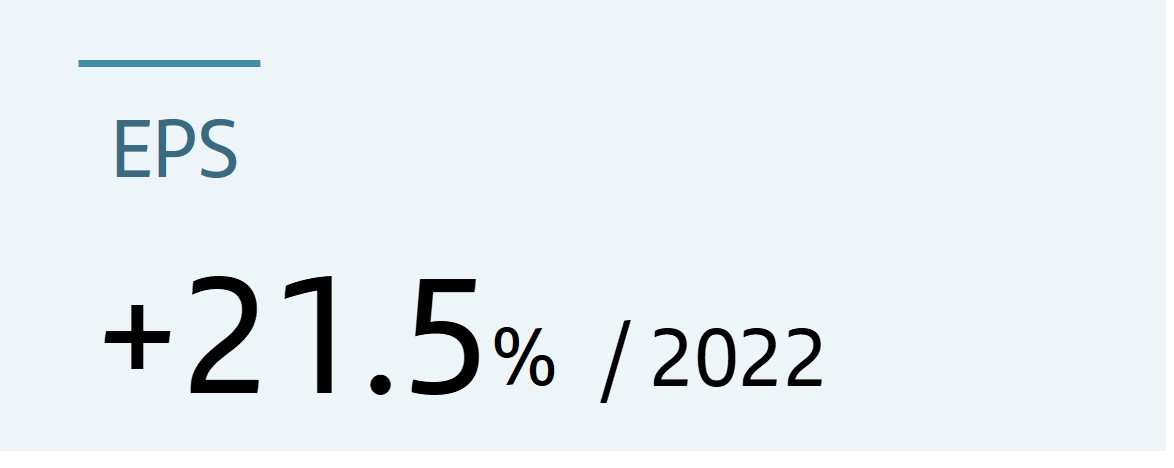

| u | Sustained earnings per share growth, which rose 21.5% compared to 2022 to EUR 65.4 cents, boosted by higher profit and share buybacks in the last 12 months. | |||||||||

| VALUE CREATION | |||||||

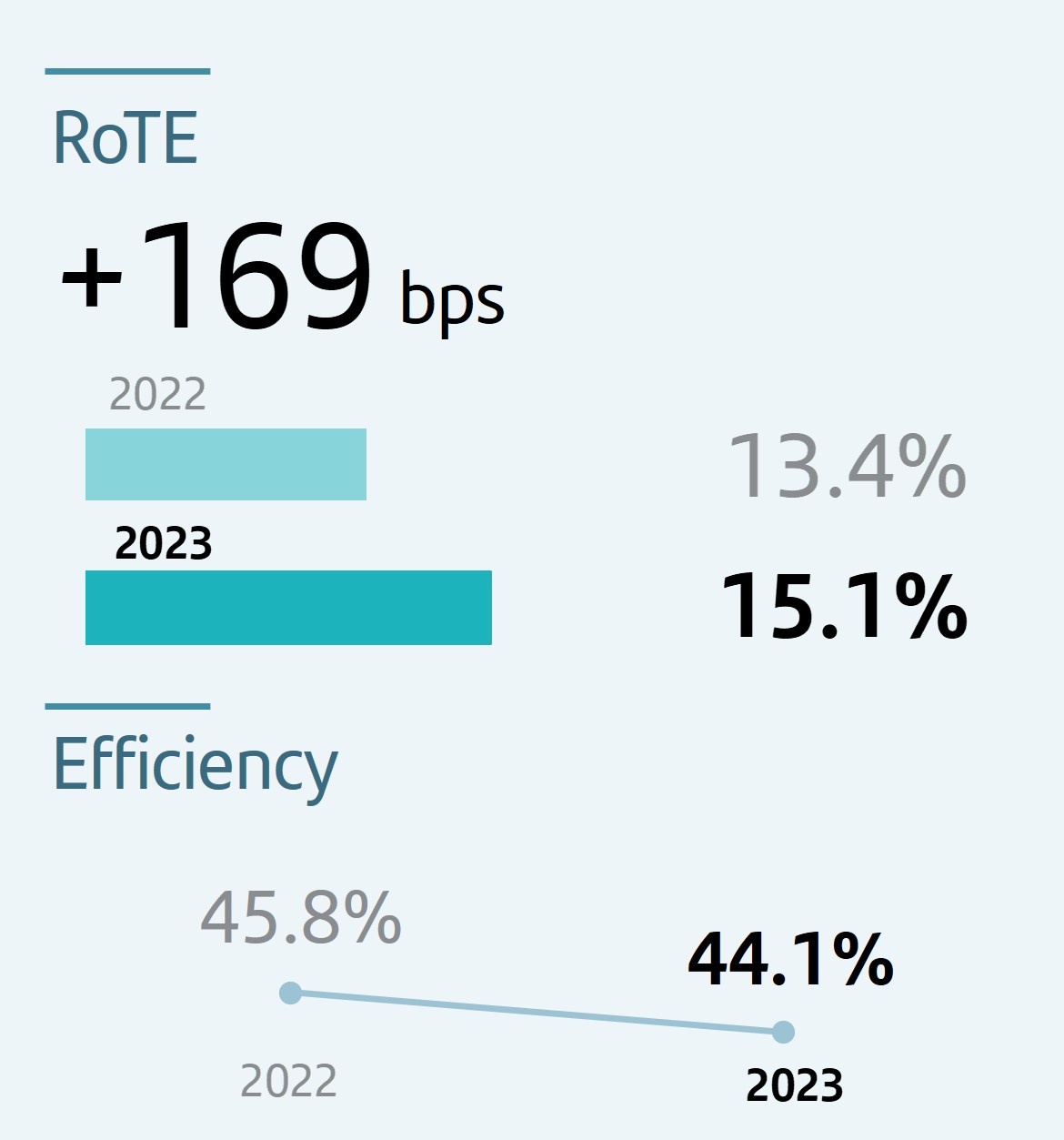

| u | Profitability improved both in the quarter and year-on-year and RoTE reached 15.1%, compared to 13.4% in 2022, supported by double-digit revenue growth. | |||||||||

| u | The acceleration of structural changes towards a simpler and more integrated model through One Transformation, which we are expanding across the Group, is driving efficiency gains and profitable growth. | ||||||||||

| u | The efficiency ratio was 44.1%, improving 1.7 pp compared to 2022, driven mainly by Europe where it decreased 5.2 pp. | ||||||||||

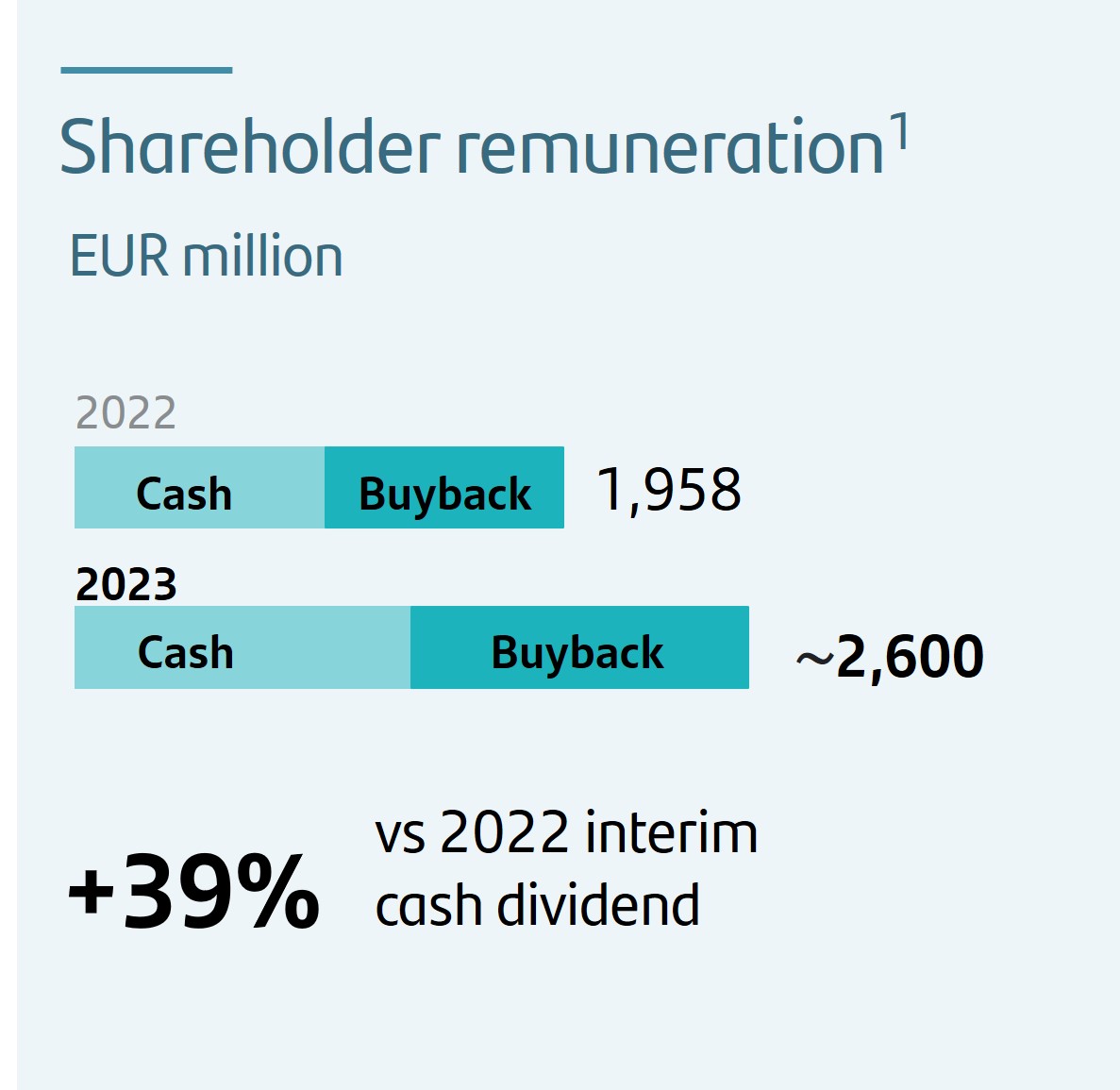

| u | In November, in accordance with the 2023 shareholder remuneration policy, the bank paid an interim cash dividend against 2023 results of EUR 8.10 cents per share. | |||||||||

| u | In addition, between 28 September 2023 and 25 January 2024 we repurchased EUR 1,310 million shares through a share buyback programme. | ||||||||||

| u | The bank's board is expected to propose to the AGM and disclose on the date of the meeting the approval of the final cash dividend, in line with the current shareholder remuneration policy2 of approximately 50% of the Group reported profit (excluding non-cash impacts and direct effect on capital ratios), divided approximately equally between cash dividends and share buybacks. The cash dividend per share paid against 2023 results is expected to be approximately 50% higher than the one paid against 2022. | ||||||||||

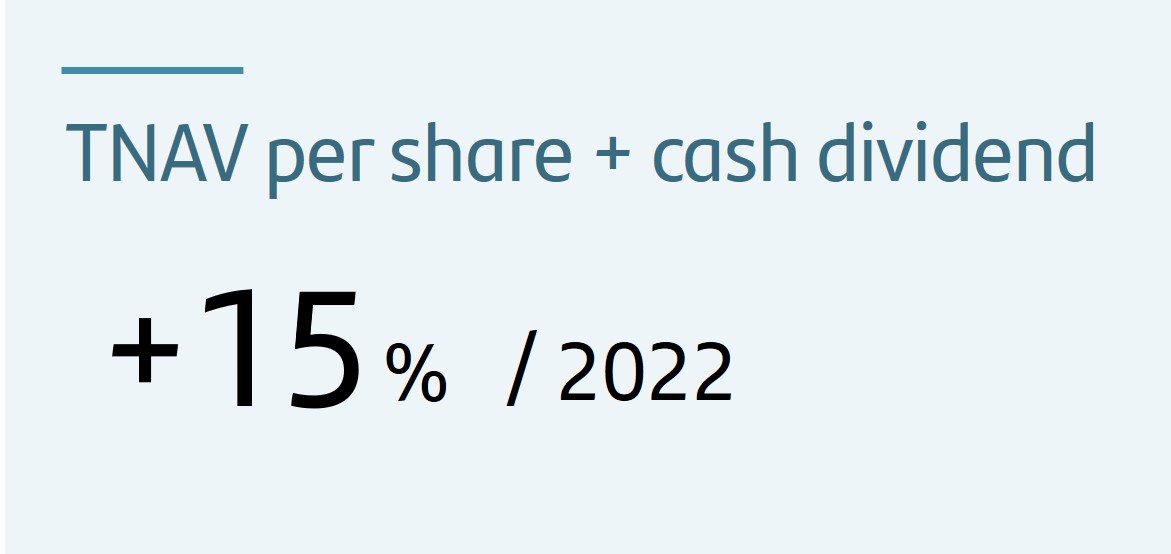

| u | As of December 2023, TNAV per share was EUR 4.76, increasing 3% in the quarter and 12% compared to December 2022. Including the two cash dividends paid in 2023 (EUR 5.95 cents paid in May and EUR 8.10 cents paid in November), TNAV per share + dividend per share increased 15% year-on-year. | |||||||||

1.Interim distribution.

2.The implementation of the shareholder remuneration policy is subject to future corporate and regulatory decisions and approvals.

| 6 | | January - December 2023 | ||||||

| GROWTH | |||||||

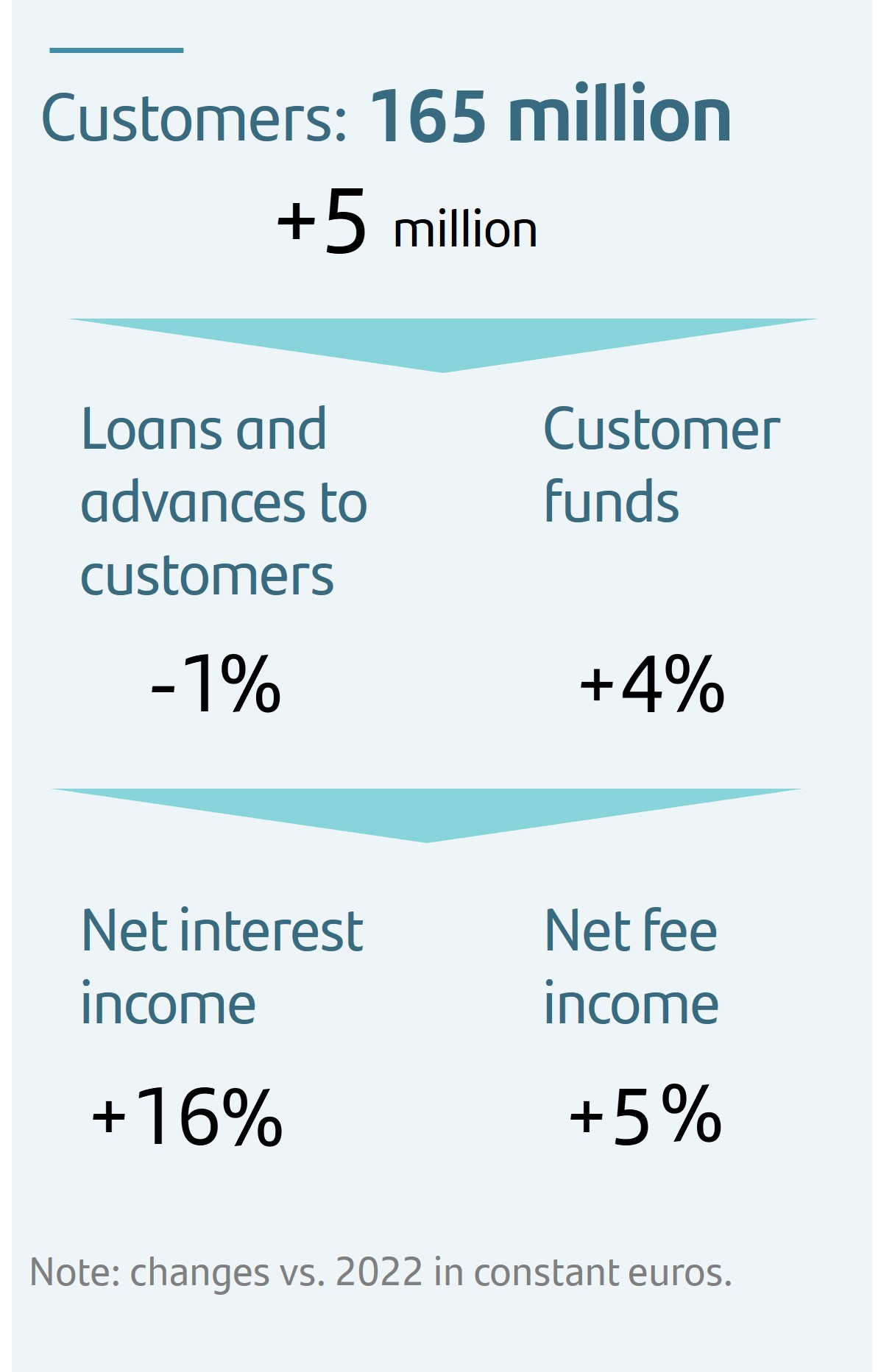

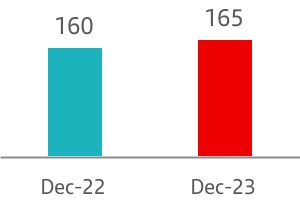

| u | Total customers amounted to 165 million, 5 million more than in 2022. | |||||||||

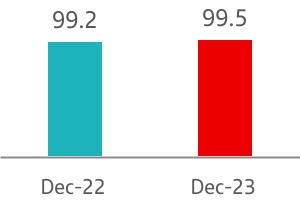

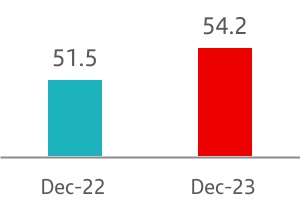

| u | Active customers reached 100 million (99 million in 2022). We have 54 million digital customers, a 5% increase year-on-year. | ||||||||||

| u | Business volumes reflect the impact that the economic and interest rate environment is having on customer behaviour. Even so, loans and advances to customers remained stable. In constant euros, they fell 1% as growth in North America, South America and DCB were offset by the reduction in Europe (lower business demand and mortgage prepayments). Customer funds rose 4% year-on-year in euros (also up 4% in constant euros), having increased EUR 31.3 billion in the last quarter). Deposits rose both in individuals and corporates, maintaining their stable structure where approximately 75% are transactional1. | ||||||||||

| u | Positive sensitivity to higher interest rates, margin management and higher customer activity were reflected in the 12% rise in net interest income and the 2% increase in net fee income (+16% and +5%, respectively, in constant euros). | ||||||||||

| u | SCIB, WM&I, PagoNxt and Auto businesses accounted for 37% of total Group revenue and 42% of net fee income. | ||||||||||

| STRENGTH | |||||||

| u | Credit quality remained robust, driven by strong employment in most regions. The NPL ratio was 3.14%, 6 bps higher than 2022. Total loan-loss reserves reached EUR 23,490 million, resulting in a total coverage ratio of impaired assets of 66%. | |||||||||

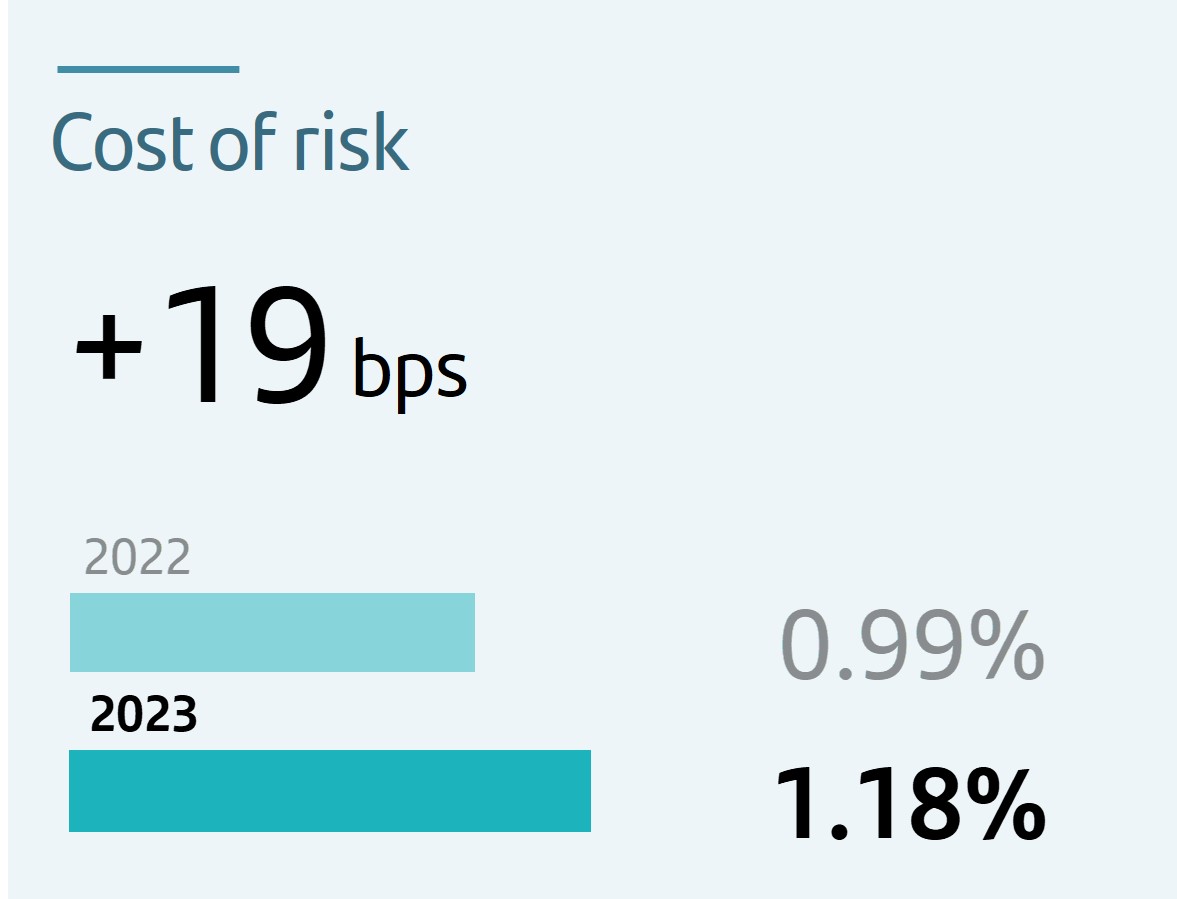

| u | The Group's cost of risk stood at 1.18% (1.13% in September 2023 and 0.99% in December 2022), in line with expectations. The CoR in DCB (0.62%) and Mexico (2.43%) were up from low levels and remained at comfortable levels. Cost of risk in Poland (2.08%) was impacted year-on-year by CHF mortgages. In the US, it rose to 1.92% due to normalization in the auto portfolio in line with expectations, while CoR in Brazil (4.77%) decreased slightly in the year. | ||||||||||

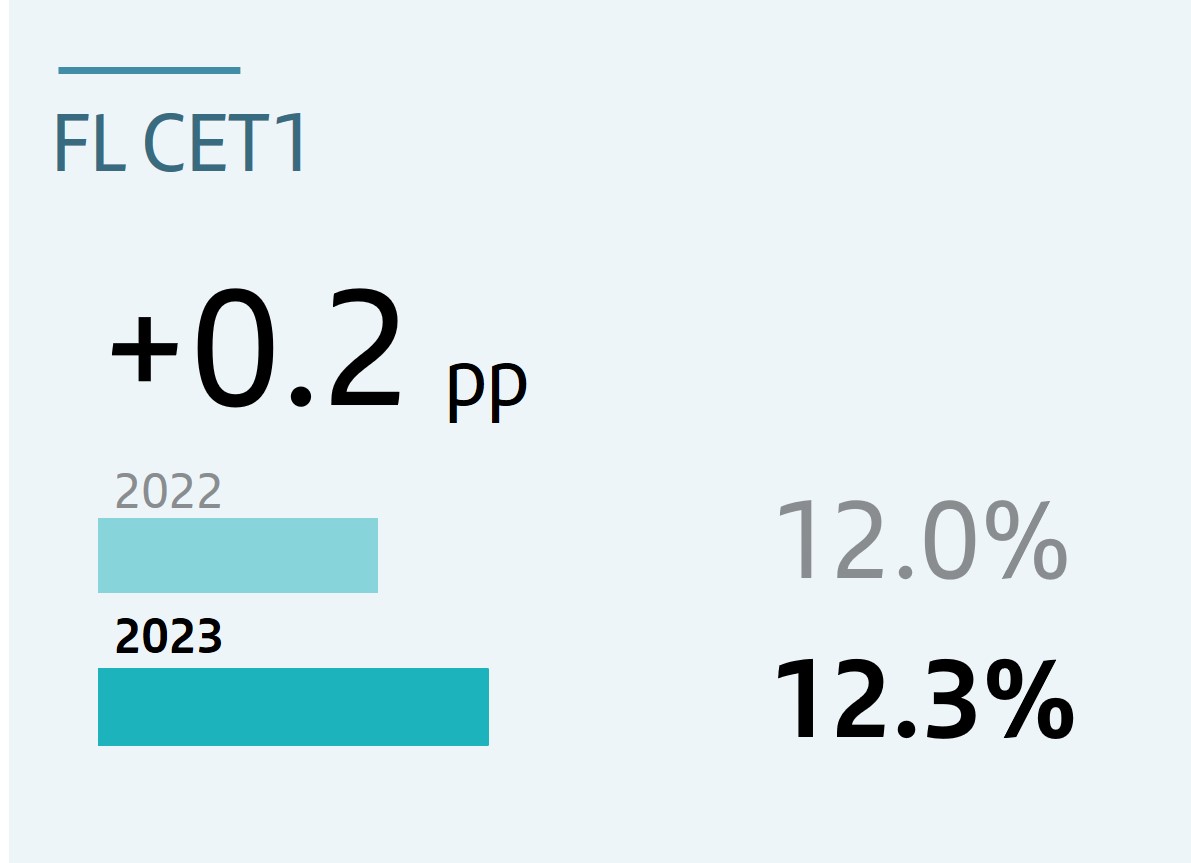

| u | The fully-loaded CET1 ratio ended the year at 12.3%. In the quarter, there were 29 bps of organic generation and a 12 bp charge for a future cash dividend payment against the profit achieved in the fourth quarter of 2023 (in line with the 50% payout target2). Additionally, there was a -26 bp impact relating to the second share buyback programme charged against 2023 results following the publication in Q4 of the EBA's Q&A 2023_6887 on the deduction of share buybacks included in distribution policies. Excluding this impact, the fully-loaded CET1 ratio would have been 12.5%. | |||||||||

| LIQUIDITY | |||||||

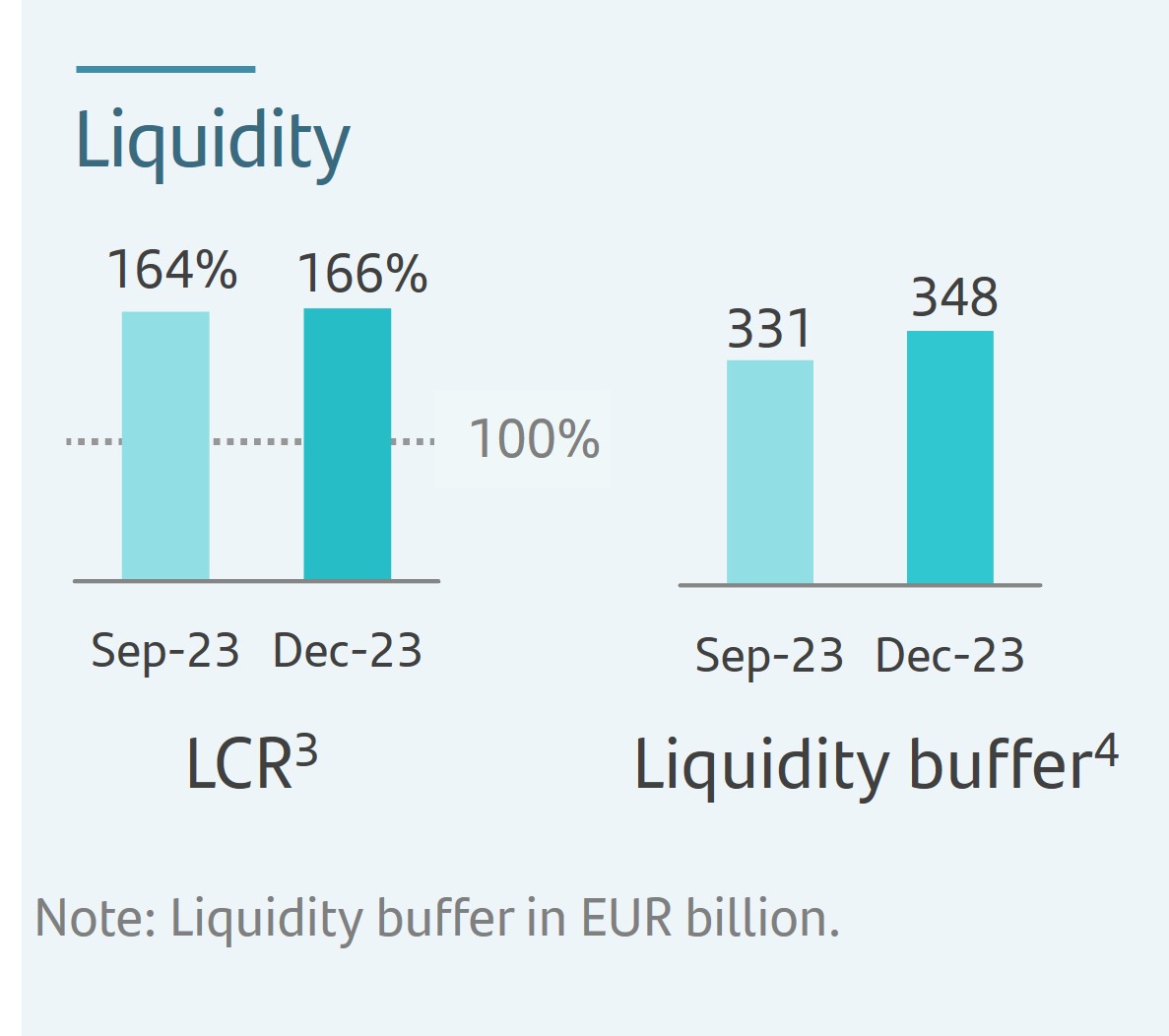

| u | Solid liquidity position with regulatory ratios well above the 100% minimum requirement. The Group liquidity coverage ratio (LCR) increased slightly to 166%. | |||||||||

| u | The liquidity buffer, comprising high quality liquid assets (HQLAs), totalled EUR 348 billion in December 2023, of which 97% were level 1. EUR 218 billion of the total liquidity buffer was in cash4, equivalent to more than 20% of our deposit base. | ||||||||||

| 1. Deposits from individuals and SMEs plus other operational corporate deposits. | |||||||||||

| 2. The implementation of the shareholder remuneration policy is subject to future corporate and regulatory decisions and approvals. | |||||||||||

| 3. Provisional data. | |||||||||||

| 4. Cash, central banks reserves and deposit facility with central banks. | |||||||||||

January - December 2023 | | 7 | ||||||

| GRUPO SANTANDER RESULTS | ||||||||

| Grupo Santander. Summarized income statement | ||||||||||||||||||||||||||

| EUR million | ||||||||||||||||||||||||||

| Change | Change | |||||||||||||||||||||||||

| Q4'23 | Q3'23 | % | % excl. FX | 2023 | 2022 | % | % excl. FX | |||||||||||||||||||

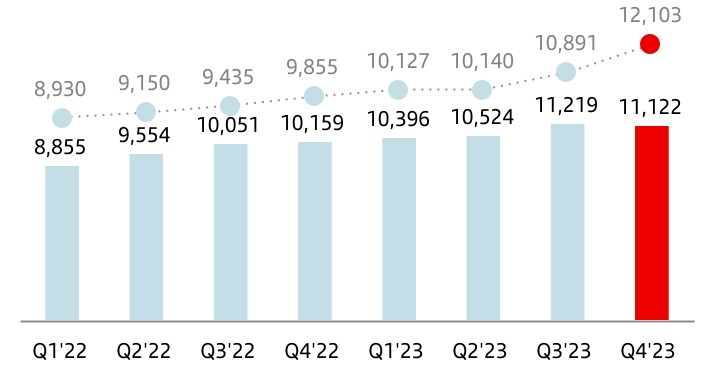

| Net interest income | 11,122 | 11,219 | (0.9) | 11.1 | 43,261 | 38,619 | 12.0 | 15.8 | ||||||||||||||||||

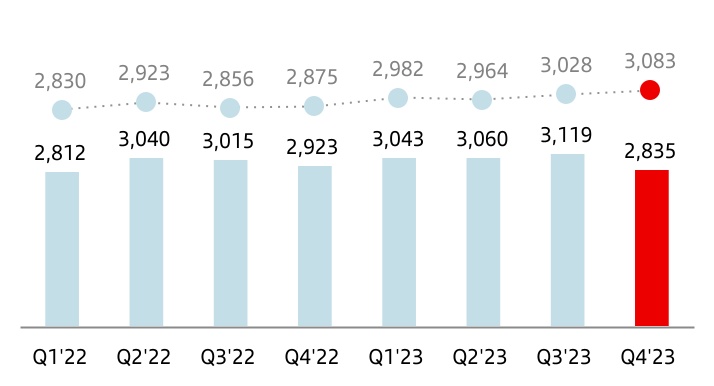

Net fee income1 | 2,835 | 3,119 | (9.1) | 1.8 | 12,057 | 11,790 | 2.3 | 5.0 | ||||||||||||||||||

Gains or losses on financial assets and liabilities and exchange differences2 | 664 | 667 | (0.4) | 48.2 | 2,633 | 1,653 | 59.3 | 77.1 | ||||||||||||||||||

| Dividend income | 97 | 92 | 5.4 | 6.4 | 571 | 488 | 17.0 | 17.4 | ||||||||||||||||||

| Share of results of entities accounted for using the equity method | 151 | 166 | (9.0) | (8.9) | 613 | 702 | (12.7) | (13.3) | ||||||||||||||||||

Other operating income/expenses3 (net) | (317) | (402) | (21.1) | 312.0 | (1,712) | (1,135) | 50.8 | 177.9 | ||||||||||||||||||

| Total income | 14,552 | 14,861 | (2.1) | 5.9 | 57,423 | 52,117 | 10.2 | 12.8 | ||||||||||||||||||

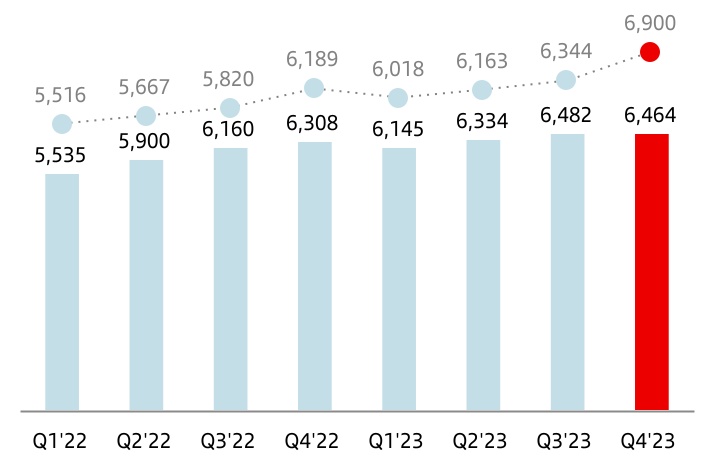

| Operating expenses | (6,464) | (6,482) | (0.3) | 8.8 | (25,425) | (23,903) | 6.4 | 9.6 | ||||||||||||||||||

| Administrative expenses | (5,685) | (5,683) | — | 8.9 | (22,241) | (20,918) | 6.3 | 9.4 | ||||||||||||||||||

| Staff costs | (3,646) | (3,477) | 4.9 | 13.0 | (13,726) | (12,547) | 9.4 | 12.2 | ||||||||||||||||||

| Other general administrative expenses | (2,039) | (2,206) | (7.6) | 2.3 | (8,515) | (8,371) | 1.7 | 5.2 | ||||||||||||||||||

| Depreciation and amortization | (779) | (799) | (2.5) | 8.1 | (3,184) | (2,985) | 6.7 | 11.2 | ||||||||||||||||||

| Provisions or reversal of provisions | (689) | (659) | 4.6 | 17.6 | (2,678) | (1,881) | 42.4 | 55.2 | ||||||||||||||||||

| Impairment or reversal of impairment of financial assets not measured at fair value through profit or loss (net) | (3,479) | (3,240) | 7.4 | 10.5 | (12,956) | (10,863) | 19.3 | 19.6 | ||||||||||||||||||

| Impairment on other assets (net) | (108) | (37) | 191.9 | 88.7 | (237) | (239) | (0.8) | 33.1 | ||||||||||||||||||

| Gains or losses on non-financial assets and investments, net | 33 | 3 | — | — | 313 | 12 | — | — | ||||||||||||||||||

| Negative goodwill recognized in results | 39 | — | — | — | 39 | — | — | — | ||||||||||||||||||

| Gains or losses on non-current assets held for sale not classified as discontinued operations | 38 | 1 | — | — | (20) | 7 | — | — | ||||||||||||||||||

| Profit or loss before tax from continuing operations | 3,922 | 4,447 | (11.8) | (2.0) | 16,459 | 15,250 | 7.9 | 9.7 | ||||||||||||||||||

| Tax expense or income from continuing operations | (724) | (1,271) | (43.0) | (34.6) | (4,276) | (4,486) | (4.7) | (3.3) | ||||||||||||||||||

| Profit from the period from continuing operations | 3,198 | 3,176 | 0.7 | 10.8 | 12,183 | 10,764 | 13.2 | 15.1 | ||||||||||||||||||

| Profit or loss after tax from discontinued operations | — | — | — | — | — | — | — | — | ||||||||||||||||||

| Profit for the period | 3,198 | 3,176 | 0.7 | 10.8 | 12,183 | 10,764 | 13.2 | 15.1 | ||||||||||||||||||

| Profit attributable to non-controlling interests | (265) | (274) | (3.3) | (2.7) | (1,107) | (1,159) | (4.5) | (5.5) | ||||||||||||||||||

| Profit attributable to the parent | 2,933 | 2,902 | 1.1 | 12.1 | 11,076 | 9,605 | 15.3 | 17.7 | ||||||||||||||||||

| EPS (euros) | 0.18 | 0.17 | 2.2 | 0.65 | 0.54 | 21.5 | ||||||||||||||||||||

| Diluted EPS (euros) | 0.17 | 0.17 | 2.1 | 0.65 | 0.54 | 21.3 | ||||||||||||||||||||

| Memorandum items: | ||||||||||||||||||||||||||

| Average total assets | 1,799,535 | 1,784,465 | 0.8 | 1,773,103 | 1,720,273 | 3.1 | ||||||||||||||||||||

| Average stockholders' equity | 94,877 | 94,527 | 0.4 | 93,035 | 89,986 | 3.4 | ||||||||||||||||||||

| NOTE: The summarized income statement groups some lines of the consolidated income statement on page 87 as follows: | |||||

1.‘Commission income’ and ‘Commission expense’. | |||||

2.‘Gain or losses on financial assets and liabilities not measured at fair value through profit or loss, net’; ‘Gain or losses on financial assets and liabilities held for trading, net’; ‘Gains or losses on non-trading financial assets and liabilities mandatorily at fair value through profit or loss’; ‘Gain or losses on financial assets and liabilities measured at fair value through profit or loss, net’; ‘Gain or losses from hedge accounting, net’; and ‘Exchange differences, net’. | |||||

3.‘Other operating income’; ‘Other operating expenses’; ’Income from assets under insurance and reinsurance contracts’; and ‘Expenses from liabilities under insurance and reinsurance contracts’. | |||||

| 8 | | January - December 2023 | ||||||

| Executive summary | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Profit | Performance | |||||||||||||||||||

| Record profit for 2023, after another quarter of strong growth | Trends seen throughout the year continued: revenue growth, improved efficiency and controlled cost of risk | |||||||||||||||||||

| Attributable profit | Total income | Costs | Provisions | |||||||||||||||||

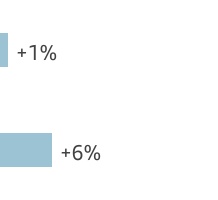

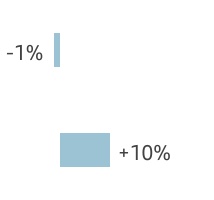

| EUR 11,076 mn | +15% in euros | +11% | +6% | +19% | in euros | |||||||||||||||

| +18% in constant euros | +13% | +10% | +19% | in constant euros | ||||||||||||||||

| Efficiency | Profitability | |||||||||||||||||||

| The Group's efficiency ratio improved driven by Europe | Profitability continued to improve | |||||||||||||||||||

| Group | Europe | RoTE | RoRWA | |||||||||||||||||

| 44.1% | 42.1% | 15.1% | 1.96% | |||||||||||||||||

| -1.7 pp | -5.2 pp | +1.7 pp | +0.19 pp | |||||||||||||||||

| Changes vs. 2022. | ||||||||||||||||||||

Results performance compared to 2022

The Group presents, both at the total Group level and for each of the business units, the changes in euros registered in the income statement, as well as variations excluding the exchange rate effect (FX), understanding that the latter provide a better analysis of the Group’s management of the country units. For the Group, exchange rates had a negative impact of 3 pp in both revenue and costs.

Total income

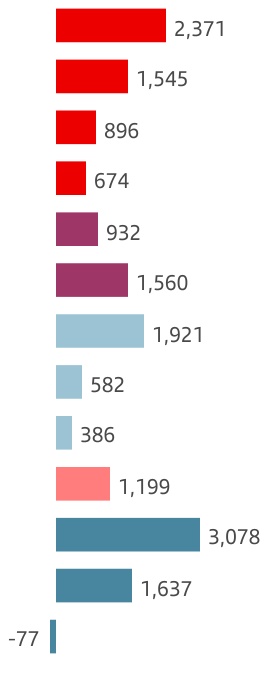

Total income amounted to EUR 57,423 million, double digit growth compared to 2022. In constant euros, total income increased 13% year-on-year. Net interest income and net fee income accounted for 96% of total income. By line:

•Net interest income amounted to EUR 43,261 million, 12% higher than 2022. Stripping out the exchange rate impact, growth was 16%, mainly due to greater volumes in some countries, higher interest rates and margin management.

By region and in constant euros: net interest income in Europe rose 27%, due to the strong positive sensitivity to interest rate rises in our balance sheet in euros. By country: +46% in Spain, +5% in the UK, +96% in Portugal and +25% in Poland.

In North America, it increased 3%, driven mainly by Mexico (+12%) while it decreased 4% in the US.

| Net interest income | |||||

| EUR million | |||||

| constant euros | ||||

Net interest income in South America rose 12%, despite the impact from negative sensitivity to interest rate rises during most of the year in Chile (-23%) and Brazil (+2%).

In DCB, net interest income increased 6%, supported by actively repricing loans and customer deposit growth.

The Corporate Centre recorded lower losses due to higher liquidity buffer remuneration as a result of rising interest rates.

•Net fee income increased 2% compared to 2022, reaching EUR 12,057 million. In constant euros, it was 5% higher.

By region, net fee income rose 7% in North America and 14% in South America. It decreased 2% in Europe due to lower credit volumes and customer attraction campaigns.

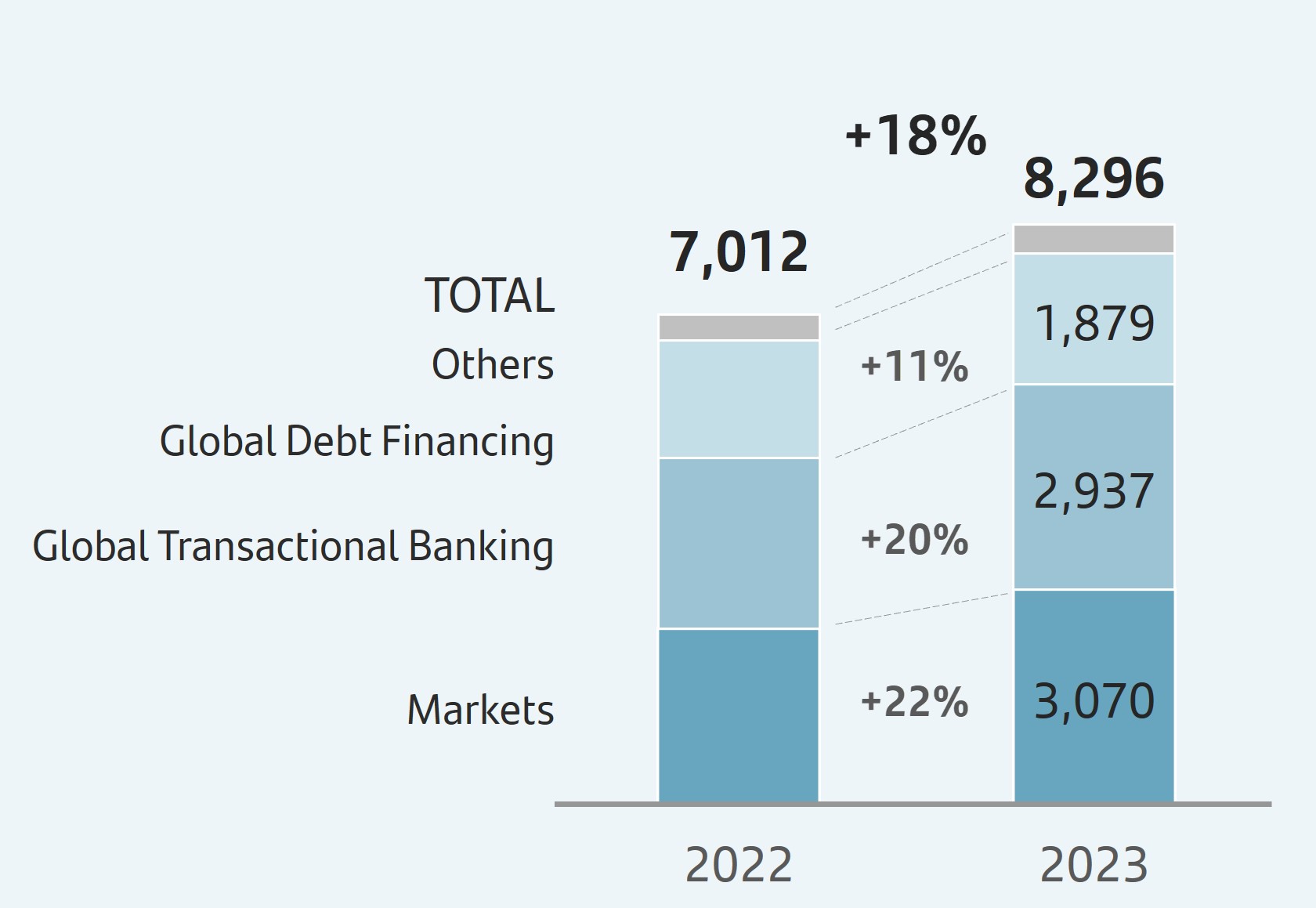

Our scale and global businesses, generated greater activity for our country units and the Group, which was reflected in net fee income growth, particularly in Santander Corporate & Investment Banking (SCIB) and PagoNxt.

In SCIB, there was double-digit net fee income growth spread across its core businesses.

| Net fee income | |||||

| EUR million | |||||

| constant euros | ||||

January - December 2023 | | 9 | ||||||

Net fee income growth was also strong in PagoNxt with double-digit growth year-on-year in total payments volumes.

•Gains on financial transactions stood at EUR 2,633 million (EUR 1,653 million in 2022), driven mainly by customer activity in SCIB and lower losses in the Corporate Centre (driven by higher negative results from the FX hedge in 2022).

•Dividend income was EUR 571 million (EUR 488 million in 2022).

•The income from companies accounted for by the equity method reached EUR 613 million compared to EUR 702 million in 2022.

•Other operating income recorded a loss of EUR 1,712 million (compared to a EUR 1,135 million loss in 2022), owing to the hyperinflation adjustment in Argentina and lower leasing income in the US. This line was also affected by the EUR 224 million charge related to the temporary levy in Spain and DCB recorded in Q1 2023.

In summary, total income increased in all regions, DCB and global businesses. The Corporate Centre also improved, due to the higher liquidity buffer remuneration and the lower negative impact from the FX hedge.

| Total income | |||||

| EUR million | |||||

| constant euros | ||||

Costs

Operating expenses amounted to EUR 25,425 million, 6% more than 2022 (+10% in constant euros), due to higher inflation. In real terms (excluding the impact of average inflation), costs increased 0.4%.

Our cost management continued to focus on improving the efficiency ratio, and as a result, we remained among the most efficient banks in the world. The efficiency ratio stood at 44.1% at the end of 2023, 1.7 pp better than 2022.

Our business transformation plan, One Transformation, continued to progress across our footprint, reflected in greater operating productivity and better business dynamics.

In constant euros, operating expenses by region and market performed as follows:

•In Europe, costs were up 6%. In real terms, they rose 1%, due to increases in Spain, Poland and Portugal, which were partially offset by the fall in the UK (-3%). The region's efficiency ratio stood at 42.1%, improving 5.2 pp year-on-year.

•In North America, costs increased 8%. In real terms, they were up 3%, due to investments in digitalization and technology and other transformation initiatives underway. The efficiency ratio stood at 49.1%.

•In South America, costs rose 17%. In real terms, they were down 3%, despite the salary increases directly linked to inflation. The efficiency ratio stood at 38.5%.

•Digital Consumer Bank's costs increased 8%, +3% in real terms, due to inflation, strategic and transformation investments in leasing and BNPL platforms and business growth. The efficiency ratio stood at 47.6%.

| Operating expenses | |||||

| EUR million | |||||

| constant euros | ||||

| 10 | | January - December 2023 | ||||||

Provisions or reversal of provisions

Provisions (net of provisions reversals) amounted to EUR 2,678 million (EUR 1,881 million in 2022) mainly driven by Spain and Brazil.

Impairment or reversal of impairment of financial assets not measured at fair value through profit or loss (net)

Impairment or reversal of impairment on financial assets not measured at fair value through profit or loss (net) was EUR 12,956 million (EUR 10,863 million in 2022).

This comparison was mainly affected by the provisions resulting from the charges in Poland for CHF mortgages, the increase in the US (due to normalization) and higher provisions recorded in Brazil, in line with credit portfolio growth.

Impairment on other assets (net)

The impairment on other assets (net) was EUR 237 million, compared to an impairment of EUR 239 million in 2022.

Gains or losses on non-financial assets and investments (net)

Net gains on non-financial assets and investments were EUR 313 million in 2023 (gain of EUR 12 million in 2022).

Negative goodwill recognized in results

Negative goodwill of EUR 39 million was recorded in 2023. No negative goodwill was recorded in 2022.

Gains or losses on non-current assets held for sale not classified as discontinued operations

This item, which mainly includes impairment of foreclosed assets recorded and the sale of properties acquired upon foreclosure, recorded a EUR 20 million loss in 2023 (EUR 7 million gain in 2022).

| Net loan-loss provisions | |||||

| EUR million | |||||

| constant euros | ||||

Profit before tax

Profit before tax was EUR 16,459 million in 2023, +8% year-on-year and +10% in constant euros. Good top line performance (double-digit growth in total income minus costs) was partially offset by higher loan-loss provisions and impairments and the temporary levy.

Income tax

Total income tax was EUR 4,276 million (EUR 4,486 million in 2022).

Profit attributable to non-controlling interests

Profit attributable to non-controlling interests amounted to EUR 1,107 million, down 4% year-on-year (-6% in constant euros), due to lower profit in Brazil and DCB as well as the increase in February of the Group's shareholding in Banco Santander México.

Profit attributable to the parent

Profit attributable to the parent amounted to EUR 11,076 million in 2023, compared to EUR 9,605 million in 2022. These results do not fully reflect profit performance due to the temporary levy in Spain mentioned in other sections of the report.

RoTE stood at 15.1% (13.4% in 2022), RoRWA at 1.96% (1.77% in 2022) and earnings per share stood at EUR 0.65 (EUR 0.54 in 2022).

January - December 2023 | | 11 | ||||||

Underlying profit attributable to the parent

Profit attributable to the parent and underlying profit were the same in 2023 (EUR 11,076 million), as profit was not affected by results that fell outside the ordinary course of our business, but there was a reclassification of certain items under some headings of the underlying income statement to better understand the business trends. These items recorded are:

•The temporary levy on revenue in Spain in the first quarter of 2023, totalling EUR 224 million, which was moved from total income to other gains (losses) and provisions.

•Provisions to strengthen the balance sheet in Brazil in the first quarter of 2023, totalling EUR 235 million, net of tax and minority interests.

In 2022, profit attributable to the parent and underlying profit were also the same (EUR 9,605 million), as profit was not affected by results that fell outside the ordinary course of our business, but there was also a reclassification of certain items under some headings of the underlying income statement.

For more details, see the 'Alternative Performance Measures' section in the appendix of this report.

Attributable profit and underlying profit increased 15% in euros and 18% in constant euros compared to 2022.

This growth was mainly boosted by solid revenue performance, which increased 11% in euros and 13% in constant euros year-on-year, and the efficiency improvement (down to 44.1%).

Santander's net operating income was EUR 32,222 million, 14% higher year-on-year. In constant euros, it rose 16% as follows:

•In Europe, net operating income increased 31% with strong improvements in all markets, boosted by 19% growth in total income (mainly due to net interest income in a context of higher interest rates) and costs increasing in line with inflation, resulting in efficiency gains.

•In North America, net operating income rose 2%. In Mexico, it was up 18%, supported by a strong total income growth which more than offset higher transformation costs. In the US, it decreased 10% affected by higher funding costs, investments in building up our CIB and Wealth Management businesses and LLP normalization.

•In South America, net operating income increased 3%, driven by total income growth.

•In Digital Consumer Bank, net operating income increased 4% driven by total income growth (higher net interest income, leasing income and gains on financial transactions). Operating expenses rose due to strategic transformation investments and business growth, as already mentioned.

•In the Corporate Centre, net operating income improved EUR 1,029 million, driven by the improvement of net interest income (higher liquidity buffer remuneration) and gains on financial transactions (FX hedge costs in 2022).

Net loan-loss provisions rose 19% (+19% also in constant euros) mainly due to the normalization in the US and Mexico, CHF mortgage provisions in Poland and portfolio growth in Brazil. This growth was reflected in an increase in the cost of risk to 1.18%, in line with the Group's target for the year.

| Summarized underlying income statement | ||||||||||||||||||||||||||

| EUR million | Change | Change | ||||||||||||||||||||||||

| Q4'23 | Q3'23 | % | % excl. FX | 2023 | 2022 | % | % excl. FX | |||||||||||||||||||

| Net interest income | 11,122 | 11,219 | (0.9) | 11.1 | 43,261 | 38,619 | 12.0 | 15.8 | ||||||||||||||||||

| Net fee income | 2,835 | 3,119 | (9.1) | 1.8 | 12,057 | 11,790 | 2.3 | 5.0 | ||||||||||||||||||

Gains (losses) on financial transactions 1 | 664 | 667 | (0.4) | 48.2 | 2,633 | 1,653 | 59.3 | 77.1 | ||||||||||||||||||

| Other operating income | (69) | (144) | (52.1) | — | (304) | 92 | — | — | ||||||||||||||||||

| Total income | 14,552 | 14,861 | (2.1) | 5.9 | 57,647 | 52,154 | 10.5 | 13.1 | ||||||||||||||||||

| Administrative expenses and amortizations | (6,464) | (6,482) | (0.3) | 8.8 | (25,425) | (23,903) | 6.4 | 9.6 | ||||||||||||||||||

| Net operating income | 8,088 | 8,379 | (3.5) | 3.7 | 32,222 | 28,251 | 14.1 | 16.1 | ||||||||||||||||||

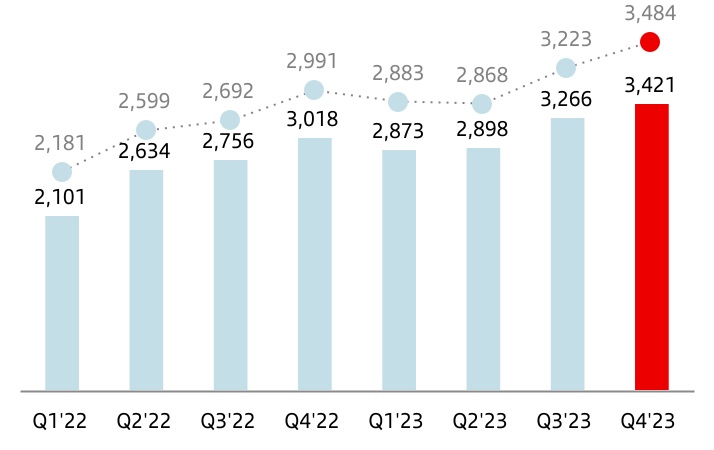

| Net loan-loss provisions | (3,421) | (3,266) | 4.7 | 8.1 | (12,458) | (10,509) | 18.5 | 19.1 | ||||||||||||||||||

| Other gains (losses) and provisions | (745) | (666) | 11.9 | 19.3 | (3,066) | (2,492) | 23.0 | 33.5 | ||||||||||||||||||

| Profit before tax | 3,922 | 4,447 | (11.8) | (2.0) | 16,698 | 15,250 | 9.5 | 11.3 | ||||||||||||||||||

| Tax on profit | (724) | (1,271) | (43.0) | (34.6) | (4,489) | (4,486) | 0.1 | 1.5 | ||||||||||||||||||

| Profit from continuing operations | 3,198 | 3,176 | 0.7 | 10.8 | 12,209 | 10,764 | 13.4 | 15.4 | ||||||||||||||||||

| Net profit from discontinued operations | — | — | — | — | — | — | — | — | ||||||||||||||||||

| Consolidated profit | 3,198 | 3,176 | 0.7 | 10.8 | 12,209 | 10,764 | 13.4 | 15.4 | ||||||||||||||||||

| Non-controlling interests | (265) | (274) | (3.3) | (2.7) | (1,133) | (1,159) | (2.2) | (3.4) | ||||||||||||||||||

| Profit attributable to the parent | 2,933 | 2,902 | 1.1 | 12.1 | 11,076 | 9,605 | 15.3 | 17.7 | ||||||||||||||||||

1. Includes exchange differences.

| 12 | | January - December 2023 | ||||||

Underlying results performance compared to the previous quarter

Underlying profit attributable to the parent and profit attributable to the parent were the same (EUR 2,933 million) in Q4 2023, as profit was not affected by results outside the ordinary course of our business.

Profit increased 1% quarter-on-quarter. Profit in the fourth quarter included a negative EUR 200 million (net of tax) impact relating to the contribution to the Deposit Guarantee Fund (DGF) and the Bank Levy in the UK.

In constant euros, profit increased 12%. The performance of the main lines of the income statement was as follows:

Total income rose 6% in the quarter, driven by the good performance of the top line:

•Net interest income was up 11%, as follows:

–Good NII performance in South America (+38%), backed by the positive impact from lower interest rates in the quarter in Brazil and Chile (the latter benefitting from higher inflation growth in the quarter) and the impact from inflation in Argentina.

–Net interest income in North America rose 1%, driven by Mexico while it remained stable in the US.

–In Europe, net interest income decreased 2%, affected by pressure on liability remuneration in the UK, which was partially offset by growth in Portugal, while Spain and Poland remained stable.

| Net operating income | |||||

| EUR million | |||||

| constant euros | ||||

–Net fee income rose 2%, mainly driven by growth in Spain, Mexico and Argentina.

–In other income, gains on financial transactions increased, dividend earnings decreased and other operating income was impacted by the higher hyperinflation adjustment in Argentina.

•Operating expenses increased 9%, mainly due to inflation.

•Net loan-loss provisions increased, due to the normalization in the US, the increase in Mexico, in line with our expectations, and in Brazil, affected by single names in SCIB portfolio.

| Profit attributable to the parent | |||||

| EUR million | |||||

| constant euros | ||||

January - December 2023 | | 13 | ||||||

| Grupo Santander. Condensed balance sheet | |||||||||||||||||

| EUR million | |||||||||||||||||

| Change | |||||||||||||||||

| Assets | Dec-23 | Dec-22 | Absolute | % | Dec-21 | ||||||||||||

| Cash, cash balances at central banks and other demand deposits | 220,342 | 223,073 | (2,731) | (1.2) | 210,689 | ||||||||||||

| Financial assets held for trading | 176,921 | 156,118 | 20,803 | 13.3 | 116,953 | ||||||||||||

| Debt securities | 62,124 | 41,403 | 20,721 | 50.0 | 26,750 | ||||||||||||

| Equity instruments | 15,057 | 10,066 | 4,991 | 49.6 | 15,077 | ||||||||||||

| Loans and advances to customers | 11,634 | 9,550 | 2,084 | 21.8 | 6,829 | ||||||||||||

| Loans and advances to central banks and credit institutions | 31,778 | 28,097 | 3,681 | 13.1 | 14,005 | ||||||||||||

| Derivatives | 56,328 | 67,002 | (10,674) | (15.9) | 54,292 | ||||||||||||

Financial assets designated at fair value through profit or loss1 | 15,683 | 14,702 | 981 | 6.7 | 21,493 | ||||||||||||

| Loans and advances to customers | 7,201 | 6,642 | 559 | 8.4 | 10,826 | ||||||||||||

| Loans and advances to central banks and credit institutions | 459 | 673 | (214) | (31.8) | 3,152 | ||||||||||||

| Other (debt securities an equity instruments) | 8,023 | 7,387 | 636 | 8.6 | 7,515 | ||||||||||||

| Financial assets at fair value through other comprehensive income | 83,308 | 85,239 | (1,931) | (2.3) | 108,038 | ||||||||||||

| Debt securities | 73,565 | 75,083 | (1,518) | (2.0) | 97,922 | ||||||||||||

| Equity instruments | 1,761 | 1,941 | (180) | (9.3) | 2,453 | ||||||||||||

| Loans and advances to customers | 7,669 | 8,215 | (546) | (6.6) | 7,663 | ||||||||||||

| Loans and advances to central banks and credit institutions | 313 | — | 313 | — | — | ||||||||||||

| Financial assets measured at amortized cost | 1,191,403 | 1,147,044 | 44,359 | 3.9 | 1,037,898 | ||||||||||||

| Debt securities | 103,559 | 73,554 | 30,005 | 40.8 | 35,708 | ||||||||||||

| Loans and advances to customers | 1,009,845 | 1,011,597 | (1,752) | (0.2) | 947,364 | ||||||||||||

| Loans and advances to central banks and credit institutions | 77,999 | 61,893 | 16,106 | 26.0 | 54,826 | ||||||||||||

| Investments in subsidiaries, joint ventures and associates | 7,646 | 7,615 | 31 | 0.4 | 7,525 | ||||||||||||

| Tangible assets | 33,882 | 34,073 | (191) | (0.6) | 33,321 | ||||||||||||

| Intangible assets | 19,871 | 18,645 | 1,226 | 6.6 | 16,584 | ||||||||||||

| Goodwill | 14,017 | 13,741 | 276 | 2.0 | 12,713 | ||||||||||||

| Other intangible assets | 5,854 | 4,904 | 950 | 19.4 | 3,871 | ||||||||||||

Other assets2 | 48,006 | 48,150 | (144) | (0.3) | 43,334 | ||||||||||||

| Total assets | 1,797,062 | 1,734,659 | 62,403 | 3.6 | 1,595,835 | ||||||||||||

| Liabilities and shareholders' equity | |||||||||||||||||

| Financial liabilities held for trading | 122,270 | 115,185 | 7,085 | 6.2 | 79,469 | ||||||||||||

| Customer deposits | 19,837 | 12,226 | 7,611 | 62.3 | 6,141 | ||||||||||||

| Debt securities issued | — | — | — | — | — | ||||||||||||

| Deposits by central banks and credit institutions | 25,670 | 15,553 | 10,117 | 65.0 | 7,526 | ||||||||||||

| Derivatives | 50,589 | 64,891 | (14,302) | (22.0) | 53,566 | ||||||||||||

| Other | 26,174 | 22,515 | 3,659 | 16.3 | 12,236 | ||||||||||||

| Financial liabilities designated at fair value through profit or loss | 40,367 | 40,268 | 99 | 0.2 | 14,943 | ||||||||||||

| Customer deposits | 32,052 | 31,143 | 909 | 2.9 | 7,818 | ||||||||||||

| Debt securities issued | 5,371 | 5,427 | (56) | (1.0) | 5,454 | ||||||||||||

| Deposits by central banks and credit institutions | 2,944 | 3,698 | (754) | (20.4) | 1,671 | ||||||||||||

| Other | — | — | — | — | — | ||||||||||||

| Financial liabilities measured at amortized cost | 1,468,703 | 1,423,858 | 44,845 | 3.1 | 1,349,169 | ||||||||||||

| Customer deposits | 995,280 | 966,353 | 28,927 | 3.0 | 886,595 | ||||||||||||

| Debt securities issued | 303,208 | 274,912 | 28,296 | 10.3 | 240,709 | ||||||||||||

| Deposits by central banks and credit institutions | 130,028 | 145,534 | (15,506) | (10.7) | 191,992 | ||||||||||||

| Other | 40,187 | 37,059 | 3,128 | 8.4 | 29,873 | ||||||||||||

| Liabilities under insurance contracts | 17,799 | 16,426 | 1,373 | 8.4 | 18,560 | ||||||||||||

| Provisions | 8,441 | 8,149 | 292 | 3.6 | 9,583 | ||||||||||||

Other liabilities3 | 35,241 | 33,188 | 2,053 | 6.2 | 27,058 | ||||||||||||

| Total liabilities | 1,692,821 | 1,637,074 | 55,747 | 3.4 | 1,498,782 | ||||||||||||

| Shareholders' equity | 130,443 | 124,732 | 5,711 | 4.6 | 119,649 | ||||||||||||

| Capital stock | 8,092 | 8,397 | (305) | (3.6) | 8,670 | ||||||||||||

Reserves (including treasury stock)4 | 112,573 | 107,709 | 4,864 | 4.5 | 103,691 | ||||||||||||

| Profit attributable to the Group | 11,076 | 9,605 | 1,471 | 15.3 | 8,124 | ||||||||||||

| Less: dividends | (1,298) | (979) | (319) | 32.6 | (836) | ||||||||||||

| Other comprehensive income | (35,020) | (35,628) | 608 | (1.7) | (32,719) | ||||||||||||

| Minority interests | 8,818 | 8,481 | 337 | 4.0 | 10,123 | ||||||||||||

| Total equity | 104,241 | 97,585 | 6,656 | 6.8 | 97,053 | ||||||||||||

| Total liabilities and equity | 1,797,062 | 1,734,659 | 62,403 | 3.6 | 1,595,835 | ||||||||||||

| Note: The condensed balance sheet groups some lines of the consolidated balance sheet on pages 85 and 86 as follows: | ||

1.'Non-trading financial assets mandatorily at fair value through profit or loss' and 'Financial assets designated at fair value through profit or loss'. | ||

2.‘Hedging derivatives’; ‘Changes in the fair value of hedged items in portfolio hedges of interest risk’; 'Assets under insurance or reinsurance contracts'; ‘Tax assets’; ‘Other assets’; and 'Non-current assets held for sale’. | ||

3.‘Hedging derivatives’; ‘Changes in the fair value of hedged items in portfolio hedges of interest rate risk’; ‘Tax liabilities’; ‘Other liabilities’; and ‘Liabilities associated with non-current assets held for sale‘. | ||

4.‘Share premium’; ‘Equity instruments issued other than capital’; ‘Other equity’; ‘Accumulated retained earnings’; ‘Revaluation reserves’; ‘Other reserves’; and ‘Own shares (-)’. | ||

| 14 | | January - December 2023 | ||||||

| GRUPO SANTANDER BALANCE SHEET | ||||||||

| Executive summary | ||||||||||||||||||||||||||||||||||||||

Gross loans and advances to customers (excl. reverse repos) | Customer funds (deposits excl. repos + mutual funds) | |||||||||||||||||||

| Credit performance reflects the impact of the macroeconomic environment and rising interest rates on customer behaviour | Customer funds continued to grow year-on-year | |||||||||||||||||||

Gross loans and advances to customers (excl. reverse repos) | Customer funds (deposits excl. repos + mutual funds) | |||||||||||||||||||

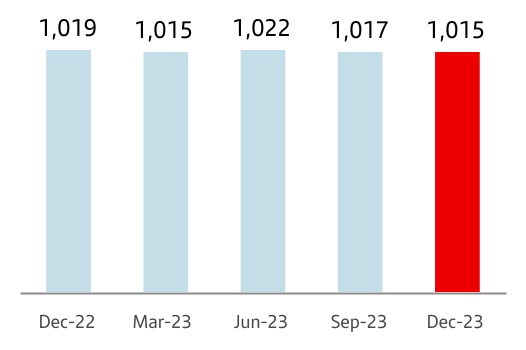

| 1,015 | +0.8% QoQ | 1,177 | +2.7% QoQ | |||||||||||||||||

| EUR billion | -1.0% YoY | EUR billion | +3.9% YoY | |||||||||||||||||

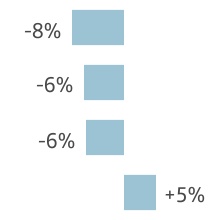

è By segment: | è By product: | |||||||||||||||||||

| Year-on-year decline in corporates, while individuals remained stable | Increase in time deposits and mutual funds shifting away from demand deposits | |||||||||||||||||||

| Individuals | SMEs and corporates | CIB | Demand | Time | Mutual funds | |||||||||||||||

| 0% | -1% | -6% | -7% | +30% | +13% | |||||||||||||||

| Note: changes in constant euros. | ||||||||||||||||||||

Loans and advances to customers

Loans and advances to customers stood at EUR 1,036,349 million as at 31 December 2023, stable during the quarter and in the last 12 months.

For the purpose of analysing traditional commercial banking loans, the Group uses gross loans and advances to customers excluding reverse repos (EUR 1,014,953 million). Additionally, the comments below do not include the exchange rate impact.

In the quarter, gross loans and advances to customers, excluding reverse repos, increased 1%, as follows:

•Flat in Europe with slight falls in Spain, the UK and Portugal, due to rising interest rates, offset by growth in Poland (boosted by CIB).

•Loans in North America increased 1%, driven by 1% growth both in the US and Mexico.

•In South America, loans increased 3%, up 47% in Argentina, +6% in Uruguay, +3% in Brazil and +1% in Chile.

•Loans at Digital Consumer Bank (DCB) increased 3%, growing at Santander Consumer Finance (+3%) and Openbank (+6%).

| Gross loans and advances to customers (excl. reverse repos) | |||||

| EUR billion | |||||

| 0 | % | 1a | |||

| Dec-23 / Dec-22 | |||||

1. In constant EUR: -1%.

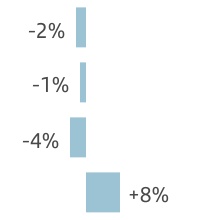

Compared to December 2022, gross loans and advances to customers (excluding reverse repos and in constant euros) declined 1%, as follows:

•In Europe volumes decreased 6%, with falls in almost all markets impacted by higher interest rates. Volumes fell 8% in Spain, 6% in Portugal and 6% in the UK. On the other hand, volumes in Poland increased 5%, mainly due to double digit growth in CIB.

•In North America, growth was 3%. In the US, lending grew 1% propelled by CIB and Multifamily, while lending in Mexico was up 6% with widespread rises across segments (except CIB).

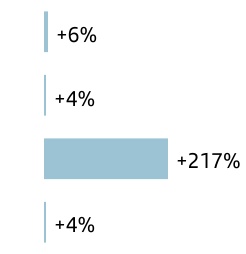

•Growth in South America was 7%. In Argentina, lending increased 217% driven by SMEs, corporates and individuals. In Brazil, it climbed 6% owing to positive performance in SMEs, corporates and individuals. In Chile, loans increased 4% backed by individuals, CIB and consumer finance. In Uruguay, they rose 12% mainly driven by consumer and corporates.

•At DCB, volumes increased 8%, with generalized growth across countries (except the UK). Openbank's loans rose 16%.

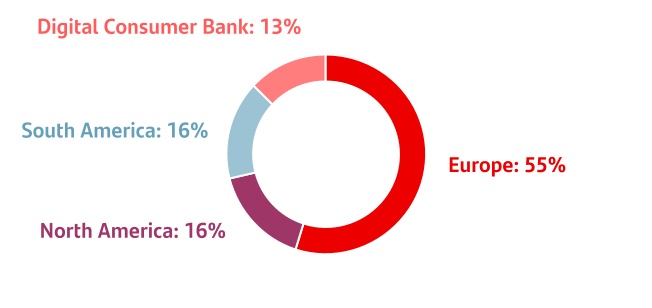

As at December 2023, gross loans and advances to customers excluding reverse repos maintained a balanced structure between individuals (63%), SMEs and corporates (24%) and CIB (13%).

| Gross loans and advances to customers (excl. reverse repos) | ||

| % operating areas. December 2023 | ||

January - December 2023 | | 15 | ||||||

Customer funds

Customer deposits amounted to EUR 1,047,169 million in December 2023, +1% compared to Q3 2023 and +4% year-on-year.

The Group uses customer funds (customer deposits excluding repos, plus mutual funds) for the purpose of analysing traditional retail banking funds, which amounted to EUR 1,176,875 million in December 2023. The comments below do not include the exchange rate impact.

•In the quarter, customer funds increased EUR 31.3 billion in constant euros, as follows:

–By product, customer deposits excluding repos increased EUR 22.1 billion and mutual funds rose EUR 9.2 billion.

–By primary segment, customer funds grew in all regions and DCB, increasing in all countries (except Uruguay).

•Compared to December 2022, customer funds were up 4% in constant euros:

–By product, customer deposits excluding repurchase agreements rose 2%, as higher interest rates resulted in a notable increase in time deposits (+30%), which grew significantly in all markets, to the detriment of demand deposits, which fell 7%. Mutual funds increased (+13%) in all markets (except the US).

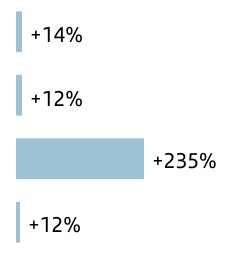

–Customer funds increased 17% in South America with growth in all markets (Argentina: +235%; Brazil: +14%; and Chile: +12%), +3% in North America (the US: -1% and Mexico: +10%), and fell 1% in Europe due to the decreases in Portugal (-4%), Spain (-2%), and the UK (-1%), offset by the growth in Poland (+8%).

–Positive performance in DCB, as customer funds increased 19%.

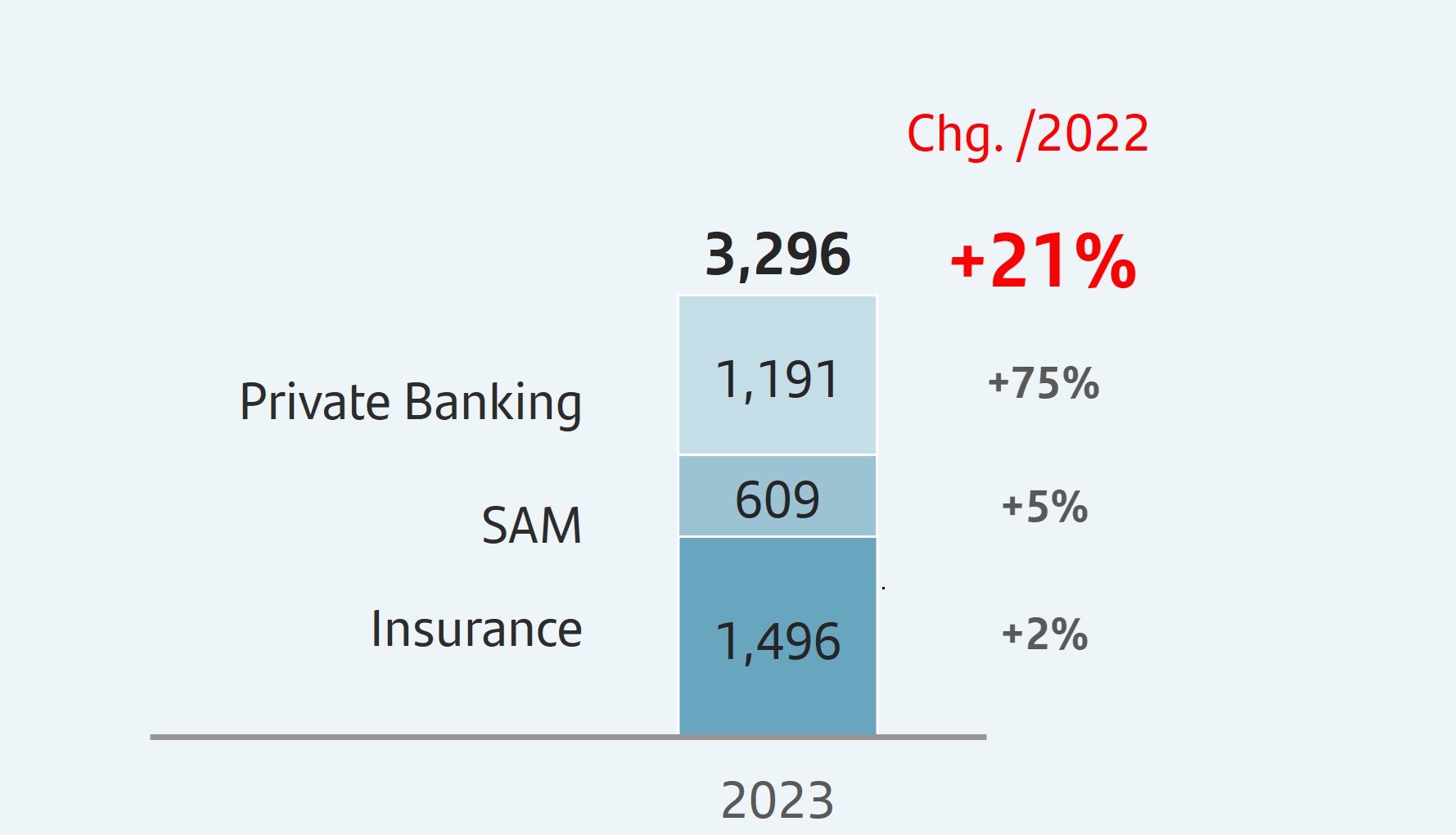

–By secondary segment, there was a solid performance across businesses, particularly Retail Banking and Wealth Management & Insurance.

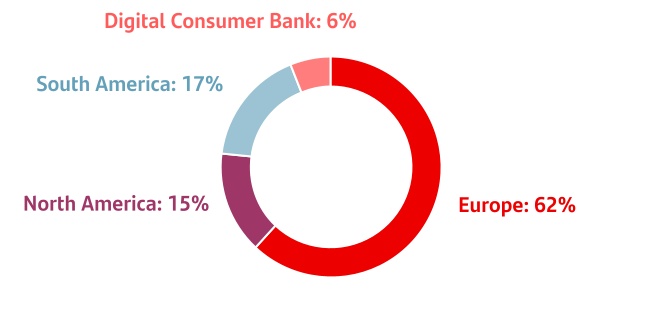

The weight of demand deposits as a percentage of total customer funds was 56%, while time deposits accounted for 26% of the total and mutual funds for 18%.

| Customer funds | ||

| EUR billion | ||

| +4 | % | 1a | ||||||

| +13 | % | |||||||

| +2 | % | |||||||

•Total | ||||||||

• Mutual funds | ||||||||

•Deposits exc. repos | ||||||||

| Dec-23 / Dec-22 | ||||||||

1. In constant EUR: +4%.

In addition to capturing customer deposits, the Group, for strategic reasons, maintains a selective policy of issuing securities in the international fixed income markets and strives to adapt the frequency and volume of its market operations to the structural liquidity needs of each unit, as well as to the receptiveness of each market.

In 2023, the Group issued:

•Medium- and long-term senior debt placed in the market of EUR 21,784 million and covered bonds amounting to EUR 8,706 million (including the first ECA covered bond placed in the market).

•There were EUR 19,942 million of securitizations and other similar transactions placed in the market.

•TLAC eligible instruments issued amounted to EUR 13,987 million to strengthen the Group's position, of which EUR 7,217 million was senior non-preferred, EUR 4,458 million was subordinated debt and EUR 2,313 million was AT1.

•Maturities of medium- and long-term debt totalled EUR 28,929 million.

The net loan-to-deposit ratio was 99% (101% in December 2022). The ratio of deposits plus medium- and long-term funding to the Group’s loans was 127%, underscoring the comfortable funding structure. The liquidity coverage ratio (LCR) was an estimated 166% in December (164% in September 2023).

The Group's access to wholesale funding markets as well as the cost of issuances depends, in part, on the ratings of the rating agencies.

The ratings of Banco Santander, S.A. by the main rating agencies were: Fitch A- senior non-preferred debt, A senior long-term and A/F1 senior short-term; Moody's confirmed its A2 long-term and P-1 short-term ratings in July and maintained its stable outlook above the rating of the Kingdom of Spain; Standard & Poor's (S&P) A+ long-term rating and A-1 short-term rating; and DBRS A High and R-1 Medium short-term. DBRS and Fitch maintained their stable outlooks, above the sovereign's outlook, while S&P also maintained its outlook but in line with the sovereign.

Sometimes the methodology applied by the agencies limits a bank's rating to the sovereign rating of the country where it is headquartered. Banco Santander, S.A. is still rated above the sovereign debt rating of the Kingdom of Spain by Moody’s, DBRS and S&P and at the same level by Fitch, which demonstrates our financial strength and diversification.

| Customer funds | ||

| % operating areas. December 2023 | ||

| 16 | | January - December 2023 | ||||||

| SOLVENCY RATIOS | ||||||||

| Executive summary | ||||||||||||||||||||||||||||||||||||||

| Fully-loaded capital ratio | Fully-loaded CET1 ratio | |||||||||||||||||||

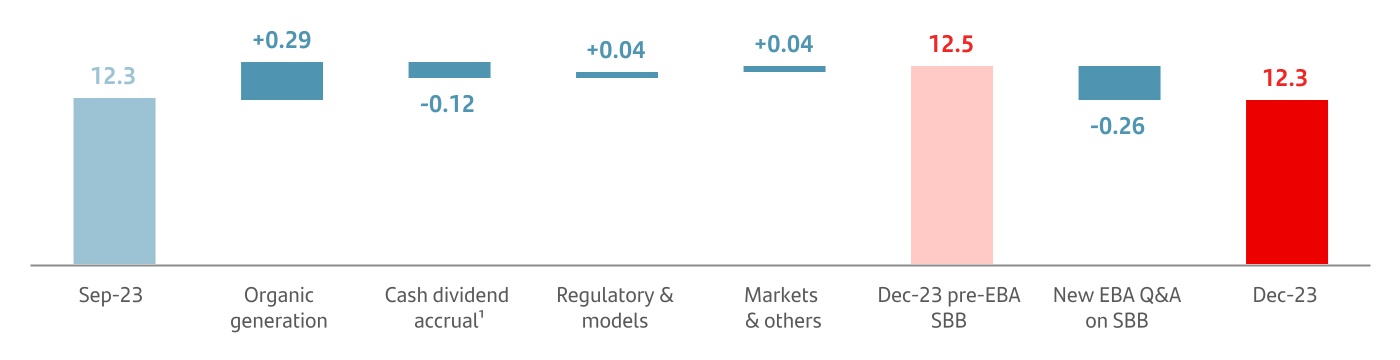

| Fully-loaded CET1 ratio exceeded 12% at the end of December | We continued to generate capital organically in the quarter, backed by profit growth | |||||||||||||||||||

| Fully-loaded CET1 performance (%) | Organic generation | +29 bps | ||||||||||||||||||

| ||||||||||||||||||||

Accrual for shareholder remuneration1 | -38 bps | |||||||||||||||||||

| TNAV per share | ||||||||||||||||||||

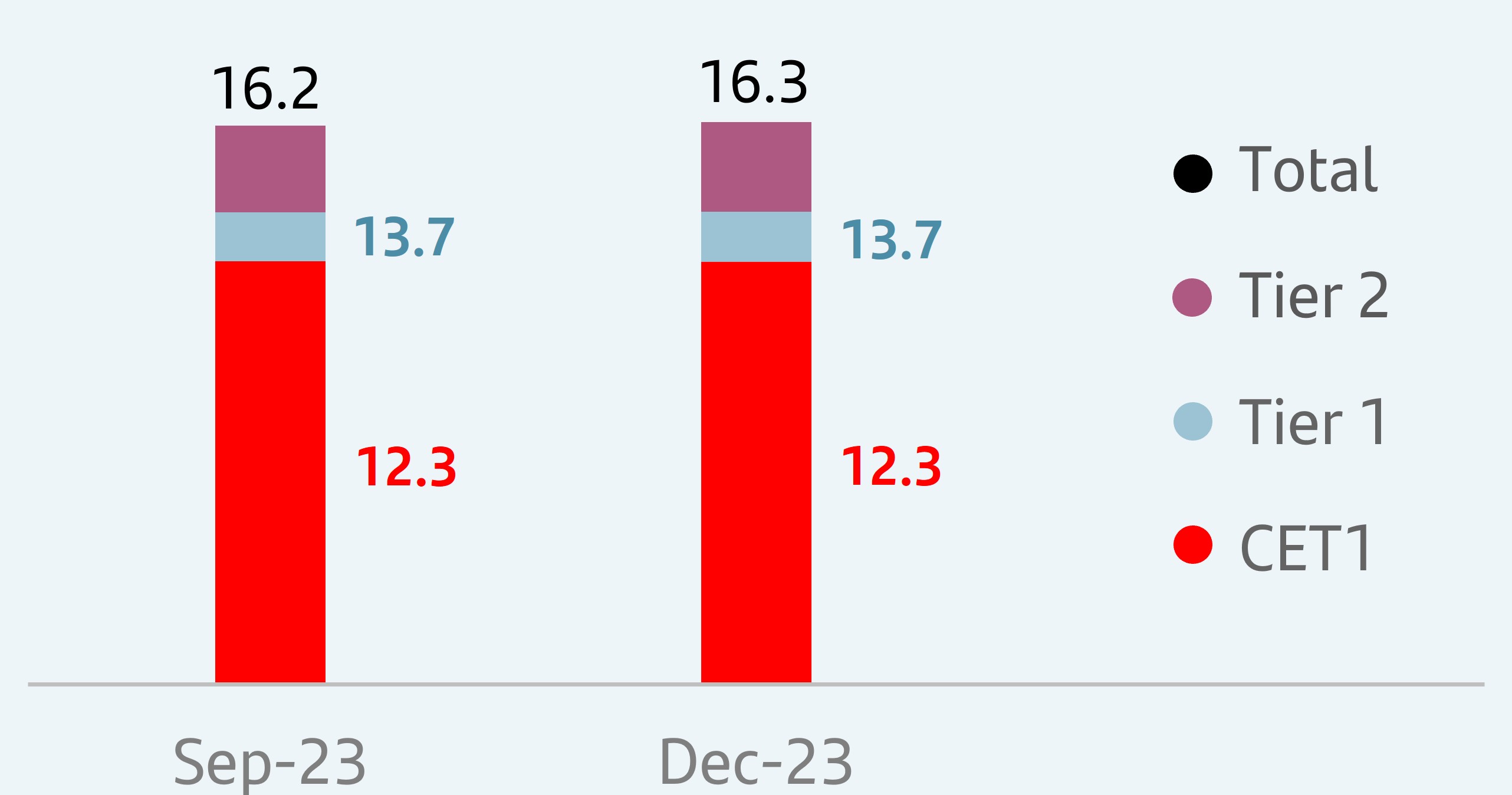

TNAV per share was EUR 4.76, increasing 15% year-on-year including the cash dividends paid in May 2023 and November 2023 | ||||||||||||||||||||

As of end December 2023, the total phased-in capital ratio (applying the IFRS 9 transitional arrangements) stood at 16.4% and the phased-in CET1 ratio at 12.3%. We comfortably meet the levels required by the European Central Bank on a consolidated basis (estimated 13.5% for the total capital ratio and 9.3% for the CET1 ratio)2. This results in a distance to the maximum distributable amount (MDA) of 269 bps and a CET1 management buffer of 304 bps.

The total fully-loaded capital ratio stood at 16.3% and the fully-loaded fully-loaded CET1 ratio at 12.3%.

In the quarter, we generated 29 bps organically and recorded a 12 bp charge for a future cash dividend payment against profit achieved in the fourth quarter of 2023 (in line with our 50% payout target1). There were also positive impacts totalling 8 bps, mainly relating to available-for-sale portfolio valuations, bringing the fully-loaded CET1 ratio to 12.5% at year end.

However, in accordance with the EBA's Q&A 2023_6887 on the deduction of share buybacks included in distribution policies published in Q4, we recorded a -26 bp impact relating to the second share buyback programme charged against 2023 results. As a result, the fully-loaded CET1 ratio stood at 12.3%.

Lastly, the TNAV per share ended December 2023 at EUR 4.76. If we include the last two cash dividends (EUR 5.95 cents paid in May and EUR 8.10 cents paid in November), TNAV plus cash dividend per share increased 15% in the last twelve months (+3% in the quarter).

Lastly, the fully-loaded leverage ratio stood at 4.69%, and the phased-in at 4.71%.

| Eligible capital. December 2023 | ||||||||

| EUR million | ||||||||

| Fully-loaded | Phased-in | |||||||

| CET1 | 76,448 | 76,741 | ||||||

| Basic capital | 85,450 | 85,742 | ||||||

| Eligible capital | 101,747 | 102,240 | ||||||

| Risk-weighted assets | 623,652 | 623,731 | ||||||

| % | % | |||||||

| CET1 capital ratio | 12.3 | 12.3 | ||||||

| Tier 1 capital ratio | 13.7 | 13.8 | ||||||

| Total capital ratio | 16.3 | 16.4 | ||||||

| Fully-loaded CET1 ratio performance | ||

| % | ||

Note: The phased-in ratio includes the transitory treatment of IFRS 9, calculated in accordance with article 473 bis of the Capital Requirements Regulation (CRR2) and subsequent modifications introduced by Regulation 2020/873 of the European Union. Total phased-in capital ratios include the transitory treatment according to chapter 4, title 1, part 10 of the CRR2.

1.The implementation of the shareholder remuneration policy is subject to future corporate and regulatory decisions and approvals.

2.According to a recent resolution from Banco de España, our D-SIB buffer will increase from 1% to 1.25% from January 2024 following a change in methodology. Institutions must hold capital at the consolidated level for the higher of the G-SIB and D-SIB requirements. As at year end 2023 Santander applies a 1% CET1 surcharge, globally (G-SIB) and locally (D-SIB), as they are both set at 1%. Additionally, the ECB revised Banco Santander, S.A.'s P2R requirement establishing a minimum of 1.74% applicable from 1 January 2024.

January - December 2023 | | 17 | ||||||

| RISK MANAGEMENT | ||||||||

| Executive summary | ||||||||||||||||||||||||||||||||||||||

| Credit risk | Market risk | |||||||||||||||||||

| The current macroeconomic environment is putting pressure on credit quality indicators; however, our proactive risk management is keeping them within expected levels | Our risk profile was stable. VaR remained at moderate levels in an economic environment with inflation still at high levels and greater geopolitical risk | |||||||||||||||||||

| Cost of risk | NPL ratio | Coverage ratio | Average VaR | |||||||||||||||||

| 1.18% | 3.14% | 66% | Q4'23 | EUR 13 million | ||||||||||||||||

| +4 bps vs. Q3'23 | +1 bp vs. Q3'23 | -2 pp vs. Q3'23 | ||||||||||||||||||

| Structural and liquidity risk | Operational risk | |||||||||||||||||||

| Robust and diversified liquidity buffer, with ratios well above regulatory requirements | Our operational risk profile remained stable and losses in the quarter were higher than in Q3 2023 | |||||||||||||||||||

| Liquidity Coverage Ratio (LCR) | ||||||||||||||||||||

| 166 | % | +2 pp vs. Q3'23 | ||||||||||||||||||

Our geographical diversification, together with our proactive risk management, based on extensive analytics and model-based decisions focused on product suitability and comprehensive portfolio management, are essential to maintaining a medium-low risk profile, even in the current macroeconomic and geopolitical context.

Credit risk management1

During the Q4 2023, credit impaired loans increased slightly compared to the third quarter, reaching EUR 35,620 million. Year-on-year, they increased 2%, mainly due to rises in in the UK, the US and Mexico, that were partially offset by the decreases in Spain, Portugal and Brazil.

Total risk stood at EUR 1,133,898 million, increasing slightly quarter-on-quarter (+1%) and relatively stable year-on-year, where the increases in South America and DCB were offset by the decline in Europe.

The NPL ratio stood at 3.14%, in line with expectations given the current environment.

Loan-loss provisions amounted to EUR 3,421 million in the quarter and EUR 12,458 million (+19%) in the year, driven by the provisions in the US (normalization of the auto portfolio), DCB (portfolio growth), Mexico (the normalization of provisions and solid growth in loans to individuals) and Poland (related to CHF mortgages). The cost of risk stood at 1.18%, performing in line with expectations.

Total loans-loss reserves reached EUR 23,490 million, flat compared to 2022. The total coverage of credit impaired loans decreased slightly to 66%, but remained at comfortable levels since nearly 68% of the Group's portfolio is secured and the mortgage portfolios in Spain and the UK, in particular, require lower coverage levels.

| Key metrics performance by geographic area | ||||||||||||||||||||||||||||||||||||||

Loan-loss provisions2 | Cost of risk (%)3 | NPL ratio (%) | Total coverage ratio (%) | |||||||||||||||||||||||||||||||||||

| 2023 | Chg (%) / 2022 | 2023 | Chg (bps) / 2022 | 2023 | Chg (bps) / 2022 | 2023 | Chg (p.p.) / 2022 | |||||||||||||||||||||||||||||||

| Europe | 2,533 | 5 | 0.44 | 4 | 2.32 | (5) | 49.3 | (2.5) | ||||||||||||||||||||||||||||||

| North America | 3,733 | 45 | 2.05 | 56 | 4.09 | 106 | 73.8 | (19.4) | ||||||||||||||||||||||||||||||

| South America | 5,401 | 9 | 3.36 | 4 | 5.72 | (49) | 78.4 | 2.4 | ||||||||||||||||||||||||||||||

| Digital Consumer Bank | 792 | 48 | 0.62 | 16 | 2.12 | 6 | 88.0 | (4.8) | ||||||||||||||||||||||||||||||

| TOTAL GROUP | 12,458 | 19 | 1.18 | 18 | 3.14 | 6 | 65.9 | (1.6) | ||||||||||||||||||||||||||||||

1. Changes in constant euros.

2.EUR million and % change in constant euros.

3.Provisions to cover losses due to impairment of loans in the last 12 months / average customer loans and advances of the last 12 months.

For more detailed information on metrics and countries, please see the Alternative Performance Measures section.

| 18 | | January - December 2023 | ||||||

The Group continuously monitors the government liquidity programmes that were launched during the pandemic, where Spain constitutes the majority. 99% of the grace periods have expired, showing no signs of deterioration.

IFRS 9 stages: the distribution of the portfolio remained stable in the quarter in percentage terms.

| Coverage ratio by stage | |||||||||||||||||||||||

| EUR billion | |||||||||||||||||||||||

Exposure1 | Coverage | ||||||||||||||||||||||

| Dec-23 | Sep-23 | Dec-22 | Dec-23 | Sep-23 | Dec-22 | ||||||||||||||||||

| Stage 1 | 1,000 | 1,002 | 1,004 | 0.4 | % | 0.4 | % | 0.4 | % | ||||||||||||||

| Stage 2 | 80 | 77 | 69 | 6.4 | % | 7.0 | % | 7.7 | % | ||||||||||||||

| Stage 3 | 36 | 36 | 35 | 40.6 | % | 40.4 | % | 40.8 | % | ||||||||||||||

1. Exposure subject to impairment. Additionally, in December 2023 there was EUR 19 billion in loans and advances to customers not subject to impairment recorded at mark to market with changes through P&L (EUR 20 billion in September 2023 and EUR 16 billion in December 2022).

Stage 1: financial instruments for which no significant increase in credit risk has been identified since its initial recognition.

Stage 2: if there has been a significant increase in credit risk since the date of initial recognition but the impairment event has not materialized, the financial instrument is classified in Stage 2.

Stage 3: a financial instrument is catalogued in this stage when it shows effective signs of impairment as a result of one or more events that have already occurred resulting in a loss.

| Credit impaired loans and loan-loss allowances | |||||||||||

| EUR million | |||||||||||

| Change (%) | |||||||||||

| Q4'23 | QoQ | YoY | |||||||||

| Balance at beginning of period | 35,558 | 1.7 | (0.1) | ||||||||

| Net additions | 4,276 | 6.7 | 16.7 | ||||||||

| Increase in scope of consolidation | — | (100.0) | — | ||||||||

| Exchange rate differences and other | (414) | 195.7 | (53.7) | ||||||||

| Write-offs | (3,800) | 17.1 | 2.8 | ||||||||

| Balance at period-end | 35,620 | 0.2 | 2.7 | ||||||||

| Loan-loss allowances | 23,490 | (2.2) | 0.3 | ||||||||

| For impaired assets | 14,464 | 0.8 | 2.2 | ||||||||

| For other assets | 9,026 | (6.6) | (2.7) | ||||||||

Market risk

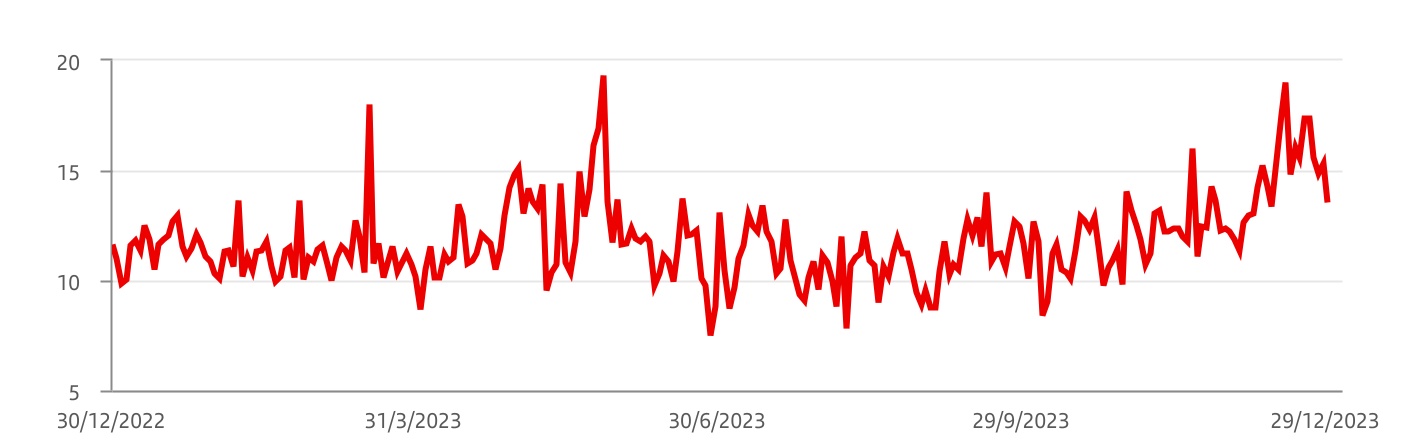

The market risk associated with global corporate banking trading activity is focused on serving the needs of our customers. It is measured in terms of daily VaR at 99% and is mainly produced by possible interest rate movements.

In the fourth quarter, the average VaR was EUR 13 million. Despite the increase of the geopolitical risk as a result of the conflict in the Middle East, market volatility remained moderate given the signs of resilience of the economies in an environment with still high, but improving, inflation. Towards the end of the quarter, volatility ticked up slightly coinciding with the last meetings of the year of the main central banks.

By market factor, VaR evolution continued to be driven mainly by interest rate risk. These risk figures remain low compared to the size of the Group's balance sheet and activity.

Trading portfolios.1 VaR by geographic region | ||||||||||||||

| EUR million | ||||||||||||||

| 2023 | 2022 | |||||||||||||

| Fourth quarter | Average | Last | Average | |||||||||||

| Total | 12.7 | 13.5 | 14.7 | |||||||||||

| Europe | 10.9 | 11.8 | 13.4 | |||||||||||

| North America | 5.3 | 5.0 | 2.7 | |||||||||||

| South America | 6.8 | 7.0 | 8.2 | |||||||||||

1. Activity performance in Santander Corporate & Investment Banking markets.

Trading portfolios.1 VaR by market factor | ||||||||||||||

| EUR million | ||||||||||||||

| Fourth quarter 2023 | Min. | Avg. | Max. | Last | ||||||||||

| VaR total | 8.4 | 12.7 | 19.0 | 13.5 | ||||||||||

| Diversification effect | (11.1) | (15.9) | (22.3) | (17.1) | ||||||||||

| Interest rate VaR | 9.2 | 12.3 | 17.5 | 11.1 | ||||||||||

| Equity VaR | 1.4 | 3.0 | 6.2 | 6.0 | ||||||||||

| FX VaR | 3.6 | 5.8 | 8.6 | 4.8 | ||||||||||

| Credit spreads VaR | 4.1 | 5.4 | 6.4 | 6.1 | ||||||||||

| Commodities VaR | 1.2 | 2.1 | 2.6 | 2.6 | ||||||||||

1.Activity performance in Santander Corporate & Investment Banking markets.

Note: In the North America, South America and Asia portfolios, VaR corresponding to the credit spreads factor other than sovereign risk is not relevant and is included in the interest rate factor.

January - December 2023 | | 19 | ||||||

Trading portfolios1. VaR performance | ||

| EUR million | ||

1. Corporate & Investment Banking performance in financial markets.

Structural and liquidity risk

Structural exchange rate risk: mainly driven by transactions in foreign currencies related to permanent financial investments, their results and related hedges. Our dynamic management of this risk seeks to limit the impact of foreign exchange rate movements on the CET1 ratio. In the quarter, hedging of currencies impacting this ratio remained close to 100%.

Structural interest rate risk: in the fourth quarter of the year, although inflation continued at high levels, its gradual correction reduced pressure on market interest rates. The markets consider that the central banks have finished this cycle of monetary policy tightening following several consecutive meetings keeping official rates stable. In this context, our structural debt portfolios performed positively and risk remained at comfortable levels during the period.

Liquidity risk: the Group maintained its comfortable liquidity risk position in the fourth quarter, supported by a robust and diversified liquidity buffer, with ratios well above regulatory limits.

Operational risk

Our operational risk profile remained stable in the fourth quarter of 2023 but, operational risk losses increased compared to the previous quarter.

The Group continuously monitors the evolution of specific legal cases, as well as external fraud, two of the main components of operational risk losses.

During the fourth quarter, the following aspects were closely monitored:

•IT risks arising from transformation plans related to business strategy and development of digital capabilities, as well as proactive management of obsolete technology and IT services provided by third parties, to ensure availability of services and operations.

•Regulatory compliance across the Group (such as ESG or operational resilience), as well as increasing supervisory activity.

•External fraud, mainly in online banking transactions (e.g. customer fraud) and in the loans admissions processes (e.g. identity theft).

•Financial Crime Compliance monitoring, compliance with international financial measures and sanctions and prevention programme upgrades in certain subsidiaries.

•Cyber threats across the financial industry, focused on alerts derived from the war in Ukraine and the Middle East, strengthening the bank's monitoring and control environment mechanisms.

•Third party risk exposure, maintaining close oversight of critical suppliers and focusing on their control environment (business continuity capabilities, supply chains, cyber risk management and compliance with service level agreements).

| 20 | | January - December 2023 | ||||||

| GENERAL BACKGROUND | ||||||||

In 2023, Santander operated in an environment dominated by higher interest rates as central banks looked to contain inflation, which gradually eased during the year. The world's major economies withstood monetary policy tightening well, although activity levels have been falling slowly. Labour markets were also resilient, with unemployment rates at or close to full employment in most of Santander's footprint.

| Country | GDP Change1 | Economic performance | |||||||||

| Eurozone | +0.5% | The positive start to the year, supported by the normalization of global supply chains and reduced uncertainty around energy supply, lost momentum in the second half of the year as interest rates rose, industry struggled to adjust to higher energy costs and households remained cautious about consumption. Inflation eased (2.9% in December) after the ECB raised its interest rates by 450 basis points in this monetary cycle. | ||||||||

| Spain | +2.4% | During the first half of the year, GDP growth was driven by the external sector, especially tourism. In the second half of the year, private consumption took over as the main growth driver. Solid labour market, with a record number of people registered in Social Security. Inflation closed the year at 3.1% (3.6% on average) with a decline in all components and a greater-than-expected moderation in core inflation (3.8%). | ||||||||

| United Kingdom | +0.5% | Economic growth remained practically flat. The labour market remained tight, putting pressure on inflation from the cost side. However, inflation eased during the year and it stood at 4% in December, far from the 11.1% peak in October 2022. The Bank of England paused rate hikes at 5.25%, unchanged since August. | ||||||||

| Portugal | +2.1% | Growth decelerated throughout the year as demand in the rest of the European Union continued to cool. Despite this, the labour market remained at full employment (6.1% in Q3'23) and inflation moderated rapidly (1.4% in December). Moody's upgraded the sovereign's rating to A3, supported by economic and fiscal reforms. | ||||||||

| Poland | +0.6% | Economic growth picked up during the year backed by domestic demand. Consumption was supported by a strong labour market, with full employment, and a marked increase in real household income driven by double-digit wage growth coupled with inflation falling to 6.2% in December. In response, the central bank paused its monetary easing, leaving the official rate at 5.75%. | ||||||||

| United States | +2.5% | The economy grew more than expected, particularly private consumption. The labour market tensions eased slightly but remains very solid. Inflation moderated significantly (3.4% in December), which led the Fed to suggest that interest rate hikes are over (the federal funds target range to 5.25%-5.5%). | ||||||||

| Mexico | +3.5% | Economic growth was surprisingly robust, driven by construction, linked to both nearshoring and infrastructure projects and the resilience of services. Inflation fell significantly to 4.7% (7.8% in the previous year). The central bank's official rate has been stable at 11.25% since the first quarter of the year and it suggested a possible first cut in early 2024. | ||||||||

| Brazil | +2.8% | The economy grew well, driven by agricultural, mining and services, but showed signs of a slowdown in the second half of the year. Inflation continued to fall (4.6% in December, 5.8% average in the year), allowing the central bank to begin to cut official rates in August, from 13.75% in December 2022 to 11.75% at year end. | ||||||||

| Chile | 0.0% | The economy completed the adjustment process initiated at the end of 2022. The second half of the year showed signs of recovery, supported by household consumption and exports. Inflation fell back sharply (3.9% vs. 12.8% in 2022) which enabled the central bank to begin to reduce rates in July, with a total reduction of 200 bps, ending the year at 8.25%. | ||||||||

| Argentina | -1.5% | The economy contracted due to the severe droughts, which reduced agricultural production and soybean exports (which have a large weight in GDP). Inflation accelerated, fuelled by the depreciation of the Argentine peso. On 10 December, a new government took office and presented an IMF-backed stabilization plan focused on correcting imbalances. | ||||||||

1. Estimated year-on-year changes for 2023.

January - December 2023 | | 21 | ||||||

| DESCRIPTION OF SEGMENTS | ||||||||

We base segment reporting on financial information presented to the chief operating decision maker, which excludes certain statutory result items considered outside the ordinary course of our business (e.g. capital gains, write-downs, impairment of goodwill) or reclassifies certain items under some headings of the underlying (or "adjusted") income statement to better understand the underlying business trends.

Santander has aligned the information in this chapter with the information used internally for management reporting and with that presented in the Group's other public documents.

Santander's executive committee has been selected to be its chief operating decision maker. The Group's operating segments reflect its organizational and managerial structures. The executive committee reviews internal reporting based on these segments to assess performance and allocate resources.

The segments are split by geographic area in which profits are earned or by type of business. We prepare the information by aggregating the figures for Santander’s various geographic areas and business units, relating it to both the accounting data of the business units integrated in each segment and information provided by management information systems. The same general principles as those used in the Group are applied.

In 2023, Santander maintained the criteria applied in 2022, with two exceptions:

•In the secondary segments: usual annual customer perimeter adjustment between Retail Banking and Santander Corporate & Investment Banking and between Retail Banking and Wealth Management & Insurance.

•In the Group's financial statements: as a result of the implementation from 1 January 2023 of the amendments to IFRS 17 (new general accounting standard for insurance contracts), the Group retrospectively performed a reclassification in the balance sheet to 'Liabilities under insurance or reinsurance contracts', related to the different treatment established by this new standard for the components of an insurance contract. This reclassification was made in the corresponding segments.

For comparative purposes, the 2022 data has been restated to include these changes.

In terms of the operating segment structure, the Group maintained the two levels of segmentation applied in 2022.

Primary segments

This primary level of segmentation, which is based on the Group’s management structure, comprises five reportable segments: four operating areas plus the Corporate Centre. The operating areas are:

Europe: comprises all business activity carried out in the region, except that included in Digital Consumer Bank. Detailed financial information is provided on Spain, the UK, Portugal and Poland.

North America: comprises all the business activities carried out in Mexico and the US, which includes the holding company (SHUSA) and the businesses of Santander Bank, Santander Consumer USA (SC USA), the specialized business unit Banco Santander International, the New York branch and Santander US Capital Markets (SanCap).

South America: includes all the financial activities carried out by Grupo Santander through its banks and subsidiary banks in the region. Detailed information is provided on Brazil, Chile, Argentina, Uruguay, Peru and Colombia.

Digital Consumer Bank: includes Santander Consumer Finance, which incorporates the entire consumer finance business in Europe, Openbank and Open Digital Services (ODS).

| 22 | | January - December 2023 | ||||||

Secondary segments

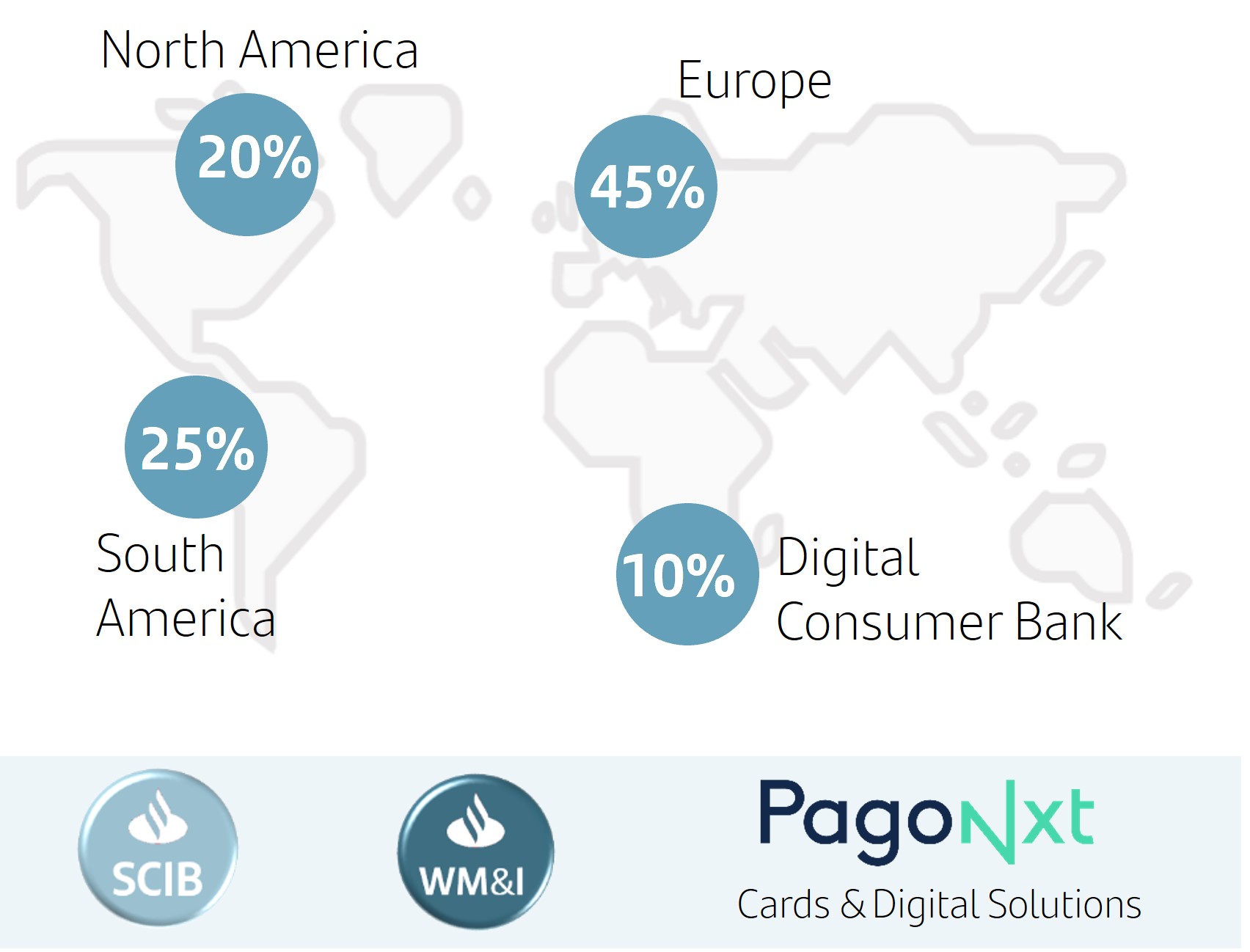

At this secondary level, Grupo Santander is structured into Retail Banking, Santander Corporate & Investment Banking (SCIB), Wealth Management & Insurance (WM&I) and PagoNxt.

Retail Banking: this covers all customer banking businesses, including consumer finance, except those of corporate banking which are managed through Santander Corporate & Investment Banking and asset management, private banking and insurance, which are managed by Wealth Management & Insurance. The results of the hedging positions in each country are also included, conducted within the sphere of their respective assets and liabilities committees.

Santander Corporate & Investment Banking: this business includes global corporate banking, investment banking and markets worldwide including treasuries managed globally, as well as equity business.

Wealth Management & Insurance: includes the asset management business (Santander Asset Management), the corporate unit of Private Banking and International Private Banking in Miami and Switzerland (Santander Private Banking) and the insurance business (Santander Insurance).

PagoNxt: this includes digital payment solutions, providing global technology solutions for our banks and new customers in the open market. It is structured into four businesses: Merchant, International Trade, Payments and Consumer.

In addition to these operating units, both primary and secondary segments, the Group continues to maintain the Corporate Centre, which includes the centralized activities relating to equity stakes in financial companies, financial management of the structural exchange rate position, assumed within the sphere of the Group’s assets and liabilities committee, as well as management of liquidity and shareholders’ equity via issuances.