FORM 6-K

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Report of Foreign Issuer

Pursuant to Rule 13a-16 or 15d-16

of the Securities Exchange Act of 1934

For the month of April, 2024

Commission File Number: 001-12518

Banco Santander, S.A.

(Exact name of registrant as specified in its charter)

Ciudad Grupo Santander

28660 Boadilla del Monte (Madrid) Spain

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

Form 20-F ☒ Form 40-F ☐

BANCO SANTANDER, S.A.

________________________

TABLE OF CONTENTS

| Item 1. January - March 2024 Financial Report | |||||

| January - March | 2024 | ||||

Index

This report was approved by the board of directors on 29 April 2024, following a favourable report from the audit committee. Important information regarding this report can be found on pages 90 and 91.

Key consolidated data

| BALANCE SHEET (EUR million) | Mar-24 | Dec-23 | % | Mar-23 | % | Dec-23 | |||||||||||||||||

| Total assets | 1,800,006 | 1,797,062 | 0.2 | 1,749,402 | 2.9 | 1,797,062 | |||||||||||||||||

| Loans and advances to customers | 1,049,533 | 1,036,349 | 1.3 | 1,041,388 | 0.8 | 1,036,349 | |||||||||||||||||

| Customer deposits | 1,044,453 | 1,047,169 | (0.3) | 998,949 | 4.6 | 1,047,169 | |||||||||||||||||

| Total funds | 1,315,779 | 1,306,942 | 0.7 | 1,237,015 | 6.4 | 1,306,942 | |||||||||||||||||

| Total equity | 105,025 | 104,241 | 0.8 | 99,490 | 5.6 | 104,241 | |||||||||||||||||

| Note: total funds includes customer deposits, mutual funds, pension funds and managed portfolios. | |||||||||||||||||||||||

| INCOME STATEMENT (EUR million) | Q1'24 | Q4'23 | % | Q1'23 | % | 2023 | |||||||||||||||||

| Net interest income | 11,983 | 11,122 | 7.7 | 10,396 | 15.3 | 43,261 | |||||||||||||||||

| Total income | 15,045 | 14,552 | 3.4 | 13,922 | 8.1 | 57,423 | |||||||||||||||||

| Net operating income | 8,498 | 8,088 | 5.1 | 7,777 | 9.3 | 31,998 | |||||||||||||||||

| Profit before tax | 4,583 | 3,922 | 16.9 | 3,832 | 19.6 | 16,459 | |||||||||||||||||

| Profit attributable to the parent | 2,852 | 2,933 | (2.8) | 2,571 | 10.9 | 11,076 | |||||||||||||||||

| Changes in constant euros: | |||||||||||||||||||||||

| Q1'24 / Q4'23: NII: +7.7%; Total income: +3.4%; Net operating income: +5.2%; Profit before tax: +17.1%; Attributable profit: -2.7%. | |||||||||||||||||||||||

| Q1'24 / Q1'23: NII: +13.2%; Total income: +6.3%; Net operating income: +7.2%; Profit before tax: +17.5%; Attributable profit: +8.8%. | |||||||||||||||||||||||

EPS, PROFITABILITY AND EFFICIENCY (%) 1 | Q1'24 | Q4'23 | % | Q1'23 | % | 2023 | |||||||||||||||||

| EPS (euros) | 0.17 | 0.18 | (2.7) | 0.15 | 13.7 | 0.65 | |||||||||||||||||

| RoE | 11.9 | 12.4 | 11.4 | 11.9 | |||||||||||||||||||

| RoTE | 14.9 | 15.6 | 14.4 | 15.1 | |||||||||||||||||||

| RoA | 0.69 | 0.71 | 0.66 | 0.69 | |||||||||||||||||||

| RoRWA | 1.96 | 2.04 | 1.86 | 1.96 | |||||||||||||||||||

Efficiency ratio 2 | 42.6 | 44.4 | 44.1 | 44.1 | |||||||||||||||||||

UNDERLYING INCOME STATEMENT 2 (EUR million) | Q1'24 | Q4'23 | % | Q1'23 | % | 2023 | |||||||||||||||||

| Net interest income | 11,983 | 11,122 | 7.7 | 10,185 | 17.7 | 43,261 | |||||||||||||||||

| Total income | 15,380 | 14,552 | 5.7 | 13,935 | 10.4 | 57,647 | |||||||||||||||||

| Net operating income | 8,833 | 8,088 | 9.2 | 7,790 | 13.4 | 32,222 | |||||||||||||||||

| Profit before tax | 4,583 | 3,922 | 16.9 | 4,095 | 11.9 | 16,698 | |||||||||||||||||

| Profit attributable to the parent | 2,852 | 2,933 | (2.8) | 2,571 | 10.9 | 11,076 | |||||||||||||||||

| Changes in constant euros: | |||||||||||||||||||||||

| Q1'24 / Q4'23: NII: +7.7%; Total income: +5.7%; Net operating income: +9.3%; Profit before tax: +17.1%; Attributable profit: -2.7%. | |||||||||||||||||||||||

| Q1'24 / Q1'23: NII: +15.6%; Total income: +8.6%; Net operating income: +11.3%; Profit before tax: +9.8%; Attributable profit: +8.8%. | |||||||||||||||||||||||

Note: for Argentina and any grouping which includes it, the variations in constant euros have been calculated considering the ARS exchange rate on the last working day for each of the periods presented. For further information, see the section 'Alternative performance measures' in the appendix to this report. | ||

January - March 2024 |  | 3 | ||||||

| SOLVENCY (%) | Mar-24 | Dec-23 | Mar-23 | Dec-23 | |||||||||||||||||||

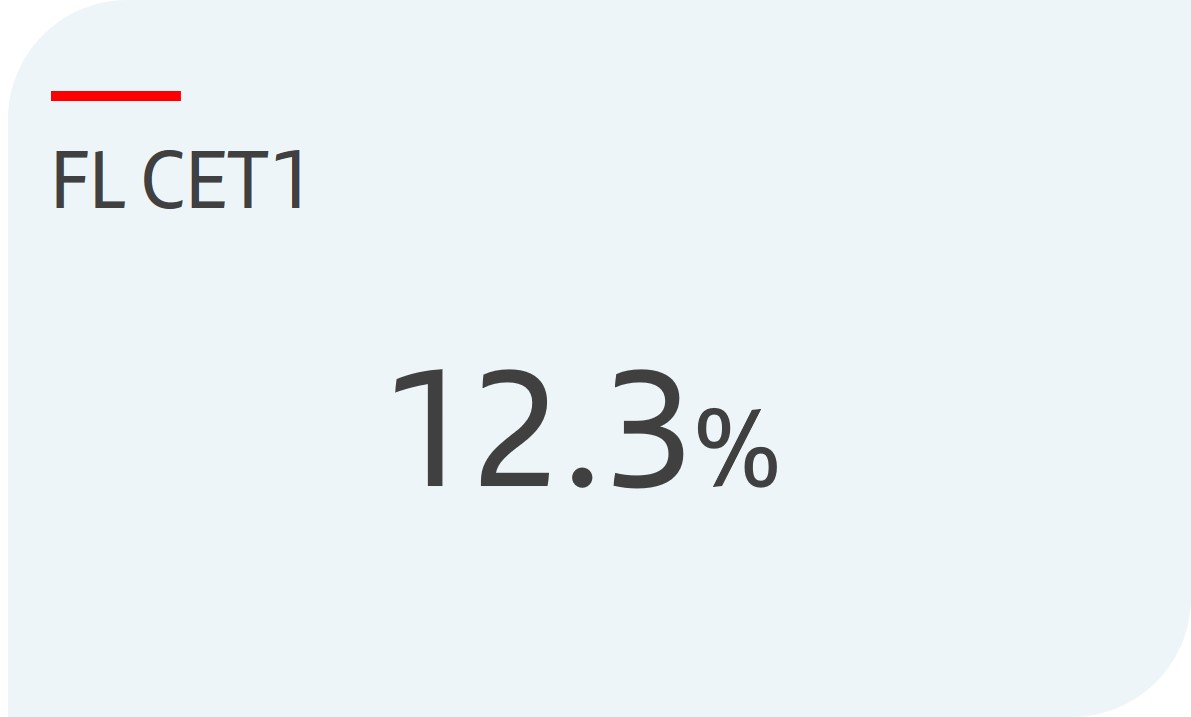

| Fully-loaded CET1 ratio | 12.3 | 12.3 | 12.2 | 12.3 | |||||||||||||||||||

| Fully-loaded total capital ratio | 16.5 | 16.3 | 15.8 | 16.3 | |||||||||||||||||||

| CREDIT QUALITY (%) | Q1'24 | Q4'23 | Q1'23 | 2023 | |||||||||||||||||||

Cost of risk 2, 3 | 1.20 | 1.18 | 1.05 | 1.18 | |||||||||||||||||||

| NPL ratio | 3.10 | 3.14 | 3.05 | 3.14 | |||||||||||||||||||

| NPL coverage ratio | 66 | 66 | 68 | 66 | |||||||||||||||||||

| MARKET CAPITALIZATION AND SHARES | Mar-24 | Dec-23 | % | Mar-23 | % | Dec-23 | |||||||||||||||||

| Shares (millions) | 15,826 | 16,184 | (2.2) | 16,454 | (3.8) | 16,184 | |||||||||||||||||

| Share price (euros) | 4.522 | 3.780 | 19.6 | 3.426 | 32.0 | 3.780 | |||||||||||||||||

| Market capitalization (EUR million) | 71,555 | 61,168 | 17.0 | 56,371 | 26.9 | 61,168 | |||||||||||||||||

| Tangible book value per share (euros) | 4.86 | 4.76 | 4.41 | 4.76 | |||||||||||||||||||

| Price / Tangible book value per share (X) | 0.93 | 0.79 | 0.78 | 0.79 | |||||||||||||||||||

| CUSTOMERS (thousands) | Q1'24 | Q4'23 | % | Q1'23 | % | 2023 | |||||||||||||||||

| Total customers | 165,752 | 164,542 | 0.7 | 161,155 | 2.9 | 164,542 | |||||||||||||||||

| Active customers | 100,092 | 99,503 | 0.6 | 99,262 | 0.8 | 99,503 | |||||||||||||||||

| Digital customers | 55,305 | 54,161 | 2.1 | 51,919 | 6.5 | 54,161 | |||||||||||||||||

| OTHER DATA | Mar-24 | Dec-23 | % | Mar-23 | % | Dec-23 | |||||||||||||||||

| Number of shareholders | 3,584,294 | 3,662,377 | (2.1) | 3,881,758 | (7.7) | 3,662,377 | |||||||||||||||||

| Number of employees | 211,141 | 212,764 | (0.8) | 210,168 | 0.5 | 212,764 | |||||||||||||||||

| Number of branches | 8,405 | 8,518 | (1.3) | 8,993 | (6.5) | 8,518 | |||||||||||||||||

| 1. | For further information, see the section 'Alternative performance measures' in the appendix to this report. | ||||

| 2. | In addition to financial information prepared in accordance with International Financial Reporting Standards (IFRS) and derived from our consolidated financial statements, this report contains certain financial measures that constitute alternative performance measures (APMs) as defined in the Guidelines on Alternative Performance Measures issued by the European Securities and Markets Authority (ESMA) on 5 October 2015, and other non-IFRS measures, including the figures related to “underlying” results, which do not include factors that are outside the ordinary course of our business, or have been reclassified within the underlying income statement. Further details are provided in the “Alternative performance measures” section of the appendix to this report. For further details on the APMs and non-IFRS measures used, including their definition or a reconciliation between any applicable management indicators and the financial data presented in the annual consolidated financial statements prepared under IFRS, please see our 2023 Annual Financial Report, published in the CNMV on 19 February 2024, our 20-F report for the year ending 31 December 2023 filed with the SEC in the United States on 21 February 2024 as well as the “Alternative performance measures” section of the appendix to this report. | ||||

| 3. | Allowances for loan-loss provisions over the last 12 months / Average loans and advances to customers over the last 12 months. | ||||

| 4 | | January - March 2024 | ||||||

| Group financial information | Financial information by segment | Responsible banking Corporate governance Santander share | Appendix | ||||||||||||||||||||||||||

Our business model

| Customer focus | ||||||||||||||||||||||||||

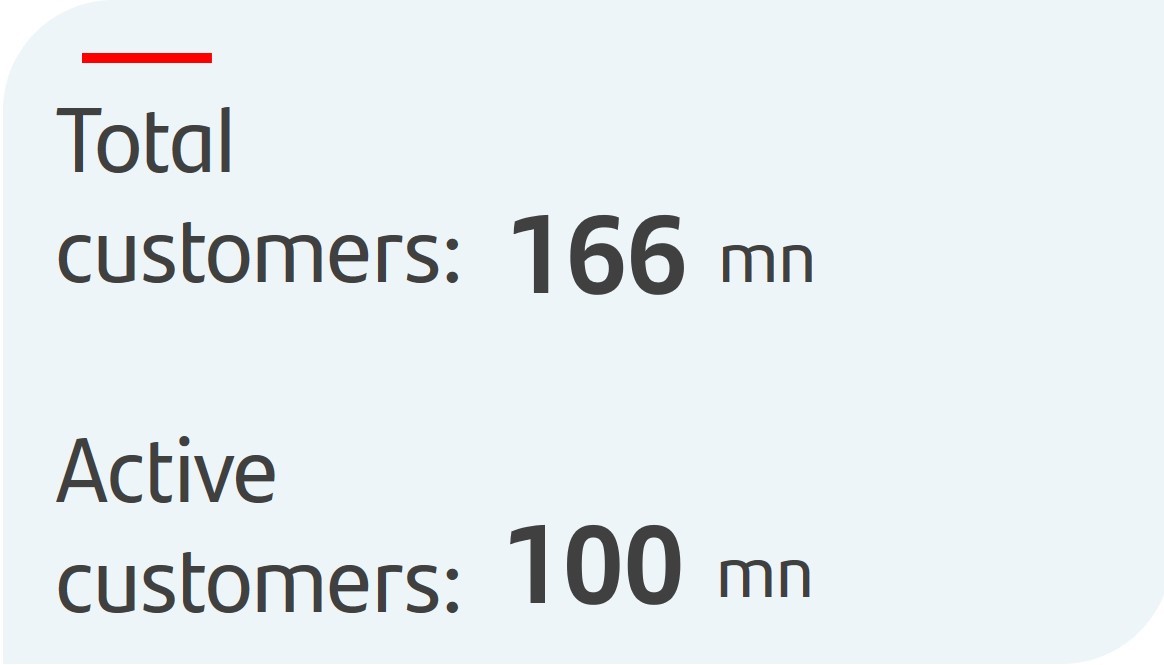

| Building a digital bank with branches | → New operating model to build a digital bank with branches, with a multichannel offer to fulfil all our customers' financial needs. | 166 mn | 100 mn | |||||||||||||||||||||||

| total customers | active customers | |||||||||||||||||||||||||

| Scale | ||||||||||||||||||||||||||

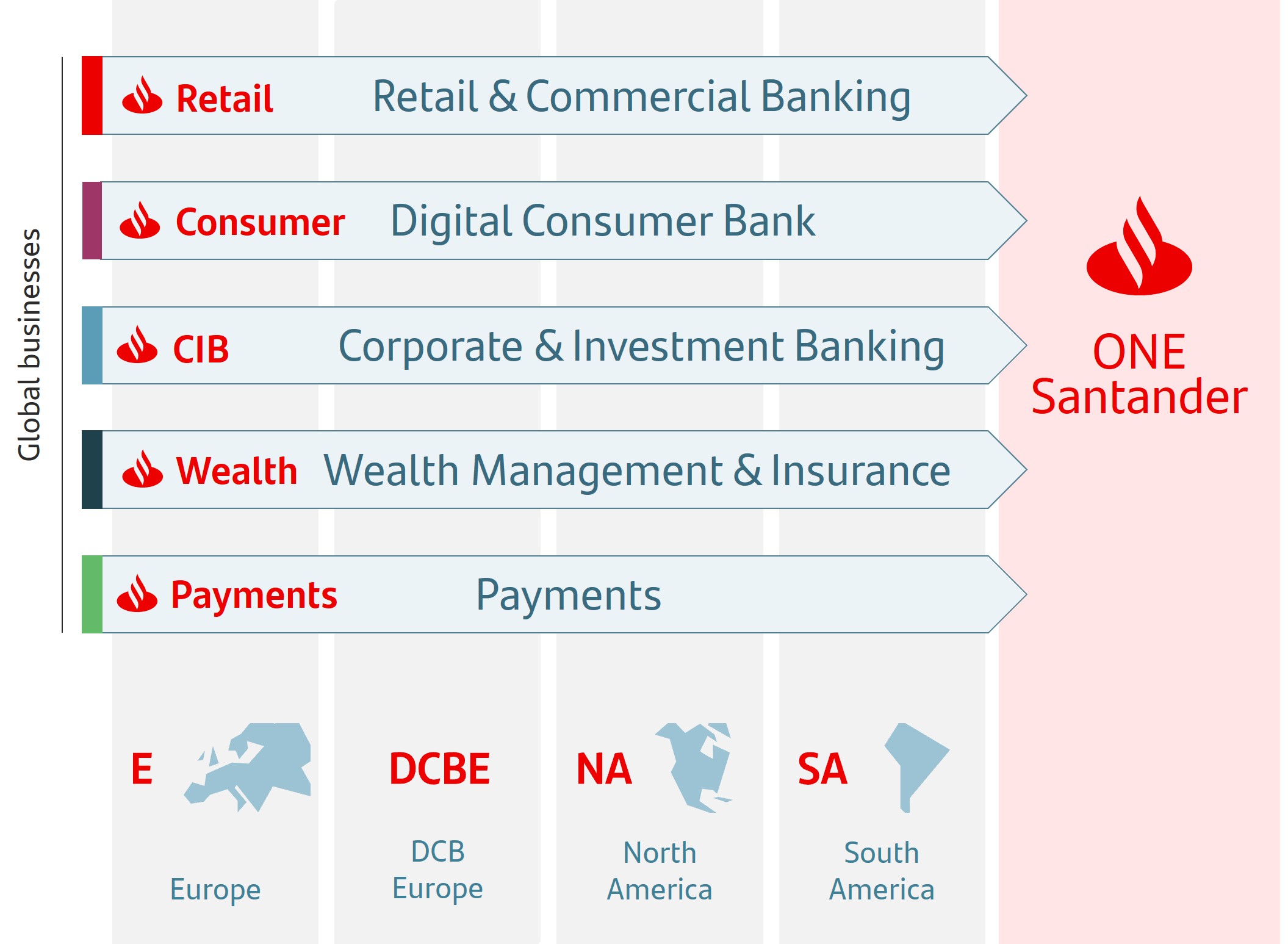

→ Our global and in-market scale helps us to improve our local banks' profitability, adding value and network benefits. → Our activities are organized under five global businesses: Retail & Commercial Banking (Retail), Digital Consumer Bank (Consumer), Corporate & Investment Banking (CIB), Wealth Management & Insurance (Wealth) and Payments. → Our five global businesses and our presence in Europe, DCB Europe, North America and South America support value creation based on the profitable growth and operational leverage that ONE Santander provides. | ||||||||||||||||||||||||||

| Global and in-market scale |  | |||||||||||||||||||||||||

| Diversification | ||||||||||||||||||||||||||

| Business, geographical and balance sheet | → Well-balanced diversification between businesses and markets with a solid and simple balance sheet that gives us recurrent net operating income with low volatility and more predictable results. | |||||||||||||||||||||||||

Our corporate culture

The Santander Way remains unchanged to continue to deliver for all our stakeholders

Our purpose To help people and businesses prosper. |  | ||||||||||

Our aim To be the best open financial services platform, by acting responsibly and earning the lasting loyalty of our people, customers, shareholders and communities. | |||||||||||

Our how Everything we do should be Simple, Personal and Fair. | |||||||||||

January - March 2024 | | 5 | ||||||

Group Financial Information

General background

In Q1 2024, Santander operated in an environment characterized by a gentle global economic slowdown, with relatively stable interest rates and a gradual decline in inflation in most regions. Geopolitical tensions, while still present, have not resulted in significant economic impacts. Labour markets withstood the monetary tightening period, with unemployment rates at or close to full employment across most of Santander's footprint.

| Country | GDP Change1 | Economic performance | |||||||||

| Eurozone | +0.5% | After stagnating in 2023, business and consumer confidence point to a scenario of GDP growth in Q1 2024. Inflation continued to moderate (2.4% in March). Despite this, the ECB held interest rates at 4%, waiting for wage moderation to be confirmed. We expect the first interest rate cut in June, if the appropriate circumstances exist for the ECB to start lowering interest rates. | ||||||||

| Spain | +2.5% | Q1 2024 PMI and social security affiliation numbers suggest that GDP will continue to grow at a higher pace than the eurozone driven by private consumption. The labour market remains strong, with employment numbers at record levels. Inflation rebounded to 3.2% due to the normalization in electricity VAT, while core inflation continued to moderate (3.3%). | ||||||||

| United Kingdom | +0.1% | Following stagnation in 2023, monthly GDP grew in February 0.1% (+0.3% in January). The labour market remains resilient, with an unemployment rate of 4.2% in January. Inflation is starting to fall back, declining to 3.2% in March from 3.4% in February, it is expected to reach the 2% target in June. The central bank maintained its interest rate at 5.25%. | ||||||||

| Portugal | +2.5% | The economy ended the year with an acceleration in growth that is starting to lose momentum in 2024. Despite this, Q1 2024 indicators are encouraging with an upturn in industrial production, economic sentiment and economic activity indicators. Labour market data remain strong with an unemployment rate close to full employment (6.6% in Q4 2023). Inflation moderated in March (2.3%). | ||||||||

| Poland | +0.1% | There was moderate year-on-year growth in 2023. Economic indicators in 2024 are beginning to show strength, which could drive GDP growth in Q1 2024 to close to 2.1%. The upturn in consumption continues to be supported by a labour market with full employment (unemployment rate of 3.1% in Q4 2023), with high wage growth (+12.9% in February). As a result, the central bank held interest rates stable at 5.75% despite falling inflation (2% in March). | ||||||||

| United States | +2.5% | Economic growth remained very robust in Q1 2024, supported by strong job creation. Inflation, which behaved worse than expected in the first three months of the year (3.5% in March), raised doubts about the Fed's expected interest rate cuts this year. | ||||||||

| Mexico | +3.2% | The economy has started 2024 with dynamism, driven by manufacturing and exports. Inflation moderated to 4.4% in March (4.7% at the end of 2023), leading to the central bank's first interest rate cut in March, -25 bps to 11%. | ||||||||

| Brazil | +2.9% | Following a slowdown in Q4 2023, the economy has regained momentum at the beginning of 2024, especially in private consumption and employment. Inflation fell to 3.9% in March (4.6% at the end of 2023). The central bank has continued its cycle of cuts in the official interest rate, with decreases of 50 bps in both the January and March meetings, to 10.75% (from 11.75% at the end of 2023). | ||||||||

| Chile | +0.2% | After a weak 2023, the economy is recovering, with growth in mining, industry and services. Inflation continued to decline (3.2% in March vs. 3.4% at the end of 2023), very close to the 3% target. The central bank continued its process of rapid interest rate cuts, with a reduction of 100 bps in Q1 2024 and 75 bps in April to 6.5% (8.25% at the end of 2023). | ||||||||

| Argentina | -1.6% | The economy remained weak at the beginning of the year, due to the impact of the fiscal adjustment programme and high inflation (15% monthly average in Q1 2024), still affected by the sharp depreciation of the peso in December 2023. The external sector is showing signs of recovery, with increases in exports and in international foreign exchange reserves. | ||||||||

1.Estimated year-on-year changes for 2023.

| 6 | | January - March 2024 | ||||||

| Financial information by segment | Responsible banking Corporate governance Santander share | Appendix | |||||||||||||||||||||||||||

| Group performance | |||||||||||||||||||||||||||||

Highlights of the period

| Main figures | |||||||||||

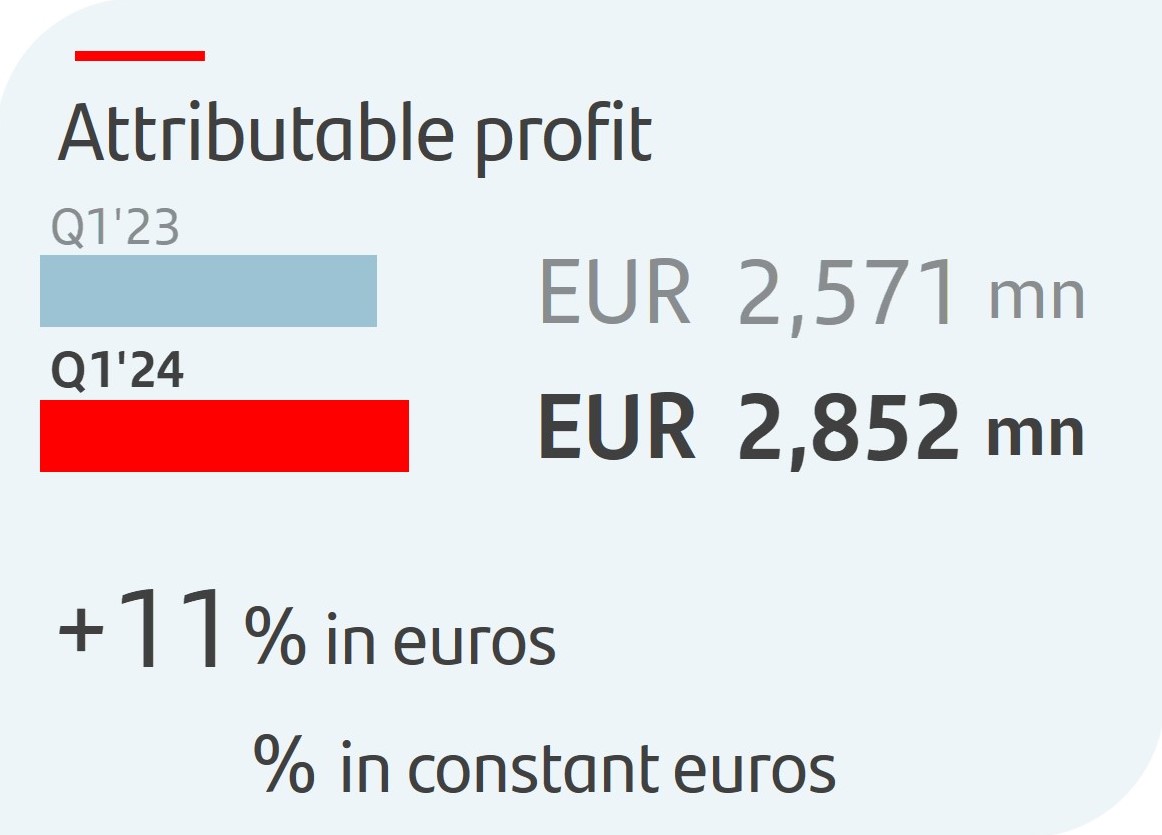

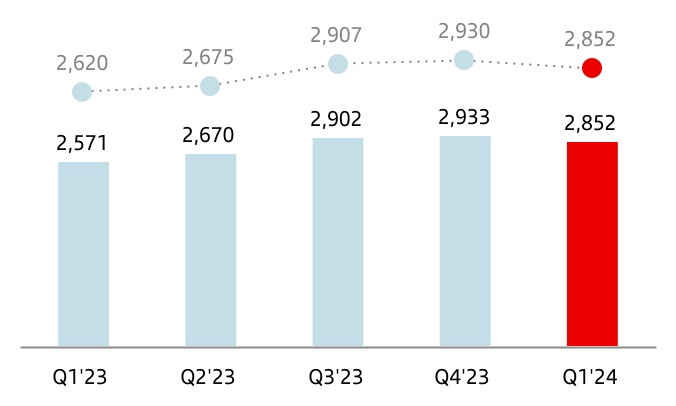

| u | In Q1 2024, attributable profit amounted to EUR 2,852 million, 11% more than in Q1 2023 (+9% in constant euros) with double-digit growth in Retail, Wealth and Payments. | |||||||||

| u | The results in the quarter were affected by the EUR 335 million charge due to the temporary levy on revenue obtained in Spain, 50% higher than in 2023. Excluding this impact, profit would have been EUR 3,187 million. | ||||||||||

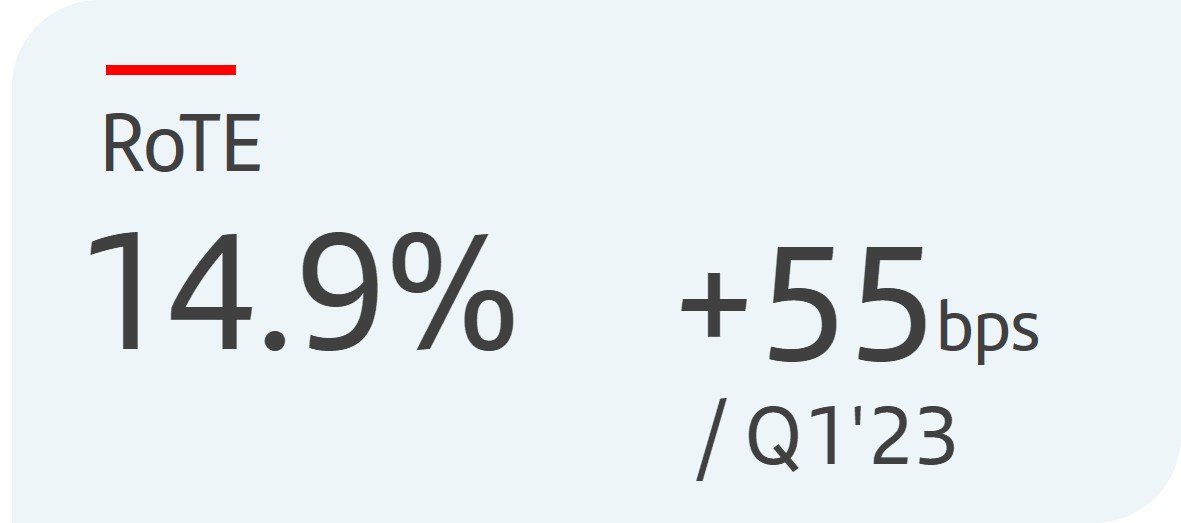

| u | In terms of profitability, RoTE stood at 14.9% compared to 14.4% in the same period of 2023. Annualizing the impact of the temporary levy, RoTEs were 16.2% and 15.3%, respectively. | |||||||||

| u | Sustained earnings per share growth, which rose 14% compared to Q1 2023 to EUR 17.0 cents, boosted by higher profit and share buybacks in the last 12 months. | ||||||||||

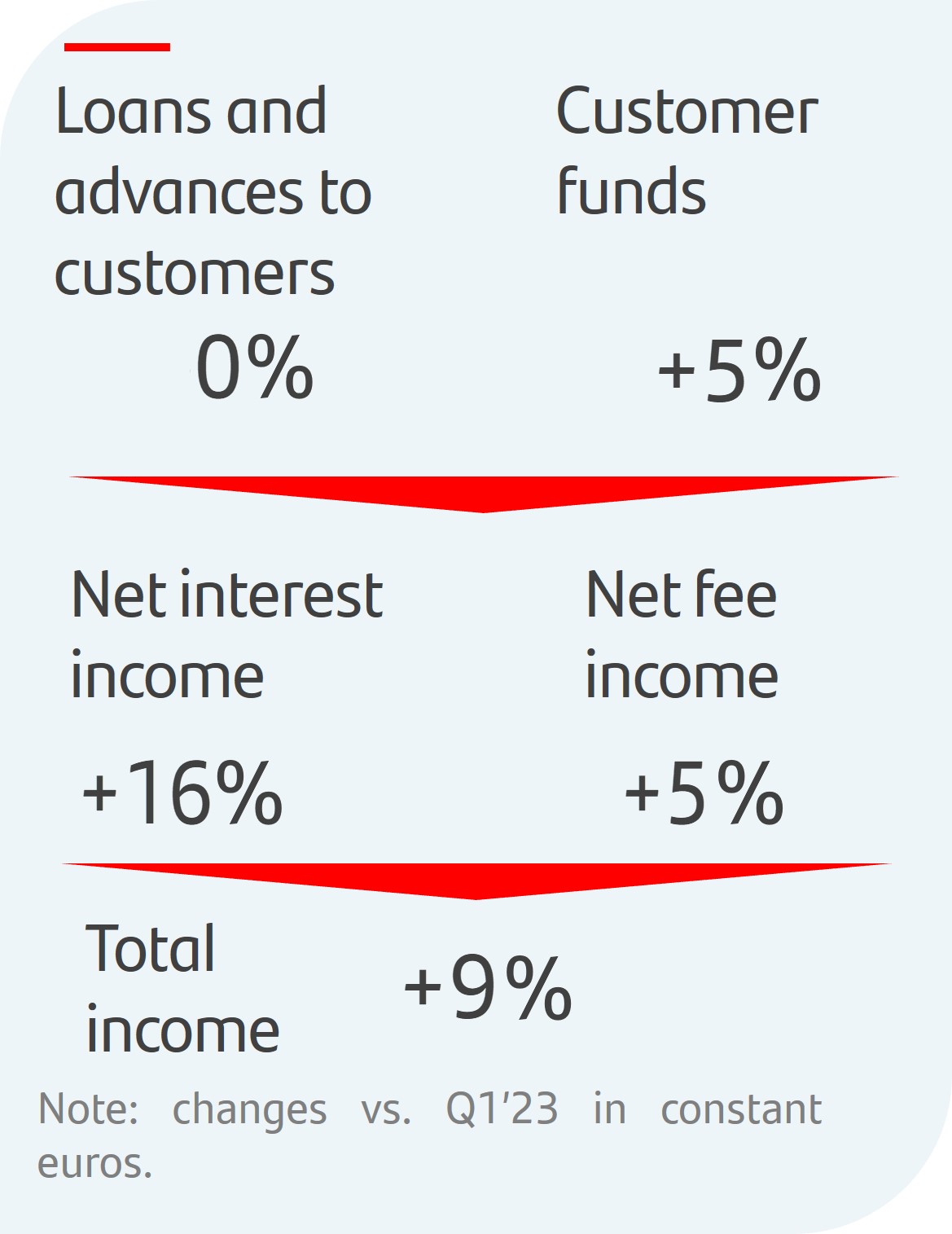

| u | Business volumes reflect the impact that the economic and interest rate environment had on customer behaviour and our active capital management. Even so, gross loans and advances to customers (excluding reverse repos) remained stable in euros and in constant euros, as growth in Consumer, Wealth and Payments was offset by the reduction in Retail in Europe (in individuals, SMEs and corporates) and CIB (mainly Global Transaction Banking) in Spain and Brazil. Customer funds (customer deposits excluding repurchase agreements plus customer funds) rose 6% year-on-year in euros (up 5% in constant euros). Deposits rose in all businesses and regions maintaining a stable structure. | |||||||||

| u | The benefits from our global scale, margin management and higher customer activity were reflected in year-on-year increases in net interest income (+18%, +16% in constant euros) and net fee income (+6%, +5%, in constant euros), resulting in total income growth of 10% (+9% in constant euros). | ||||||||||

| u | Structural changes towards a simpler and more integrated model through ONE Transformation, which we are expanding across the Group, are contributing to efficiency gains and profitable growth, particularly evident in our Retail and Consumer businesses. | |||||||||

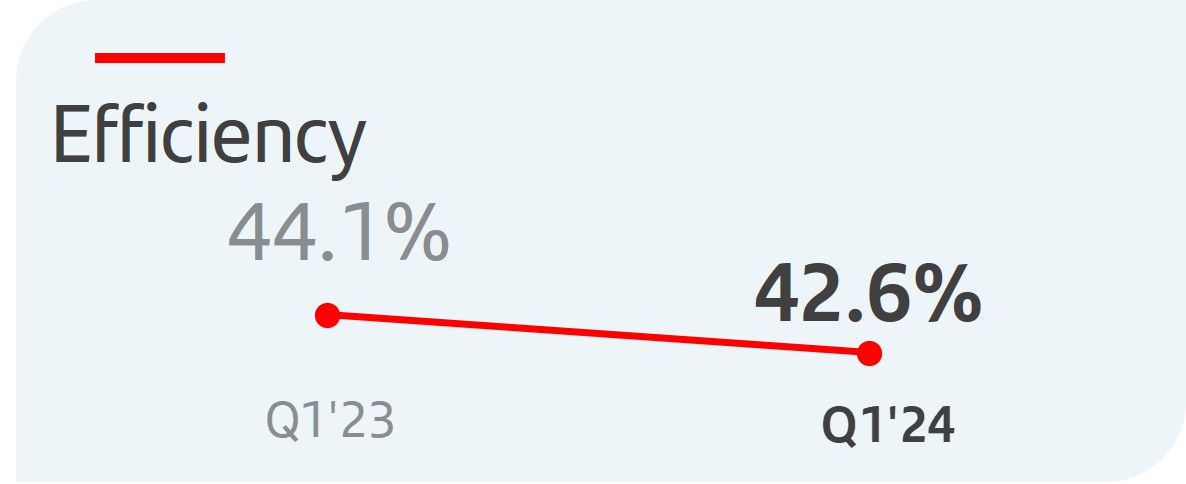

| u | The efficiency ratio improved 1.5 pp compared to Q1 2023 to 42.6%, driven mainly by Retail which decreased 3.9 pp. | ||||||||||

| u | Credit quality remains robust, driven by strong employment and the macroeconomic environment across our footprint. The NPL ratio was 3.10%, 5 bps higher year-on-year. Total loan-loss reserves reached EUR 23,542 million, resulting in a total coverage ratio of 66%. | |||||||||

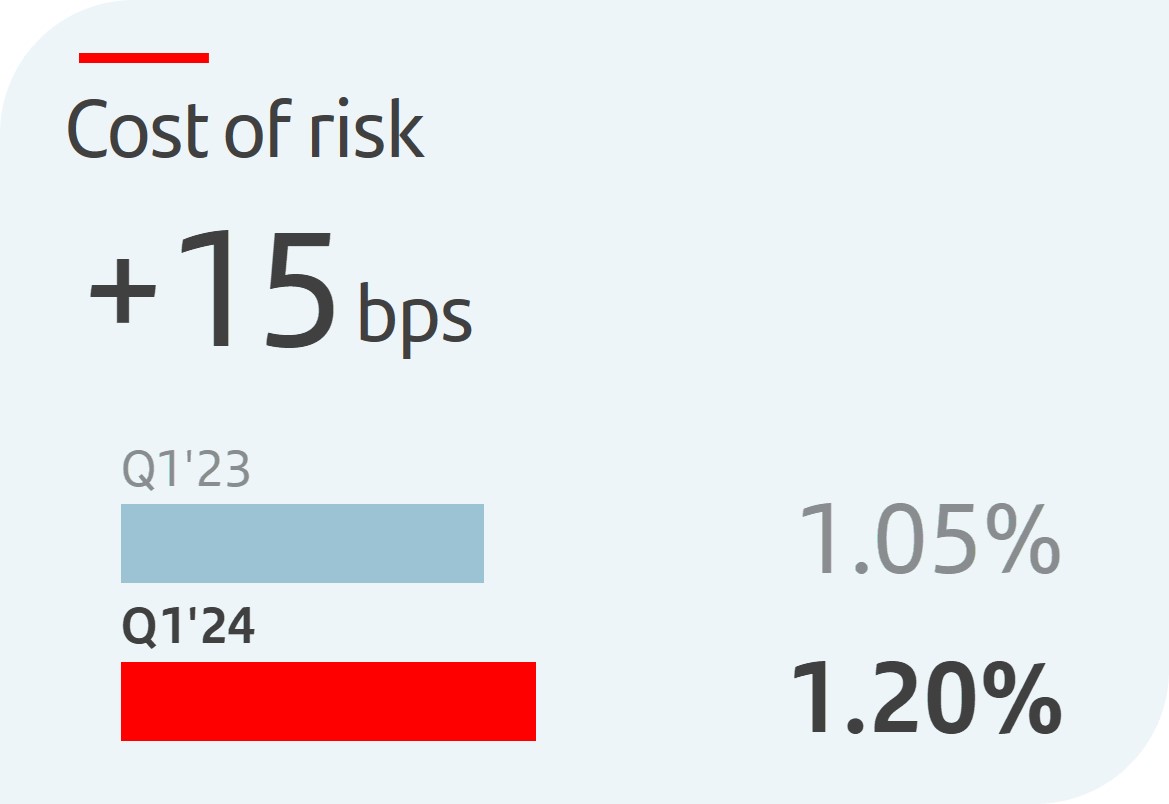

| u | The Group's cost of risk stood at 1.20% (1.18% in December 2023 and 1.05% in March 2023), in line with our public target and in line with expectations. Retail and Consumer accounted for 85% of Group's net loan-loss provisions. In Retail, cost of risk remained under control at 1.03%. In Consumer (2.12%), CoR continued to normalize and remained at controlled levels and in line with expectations. | ||||||||||

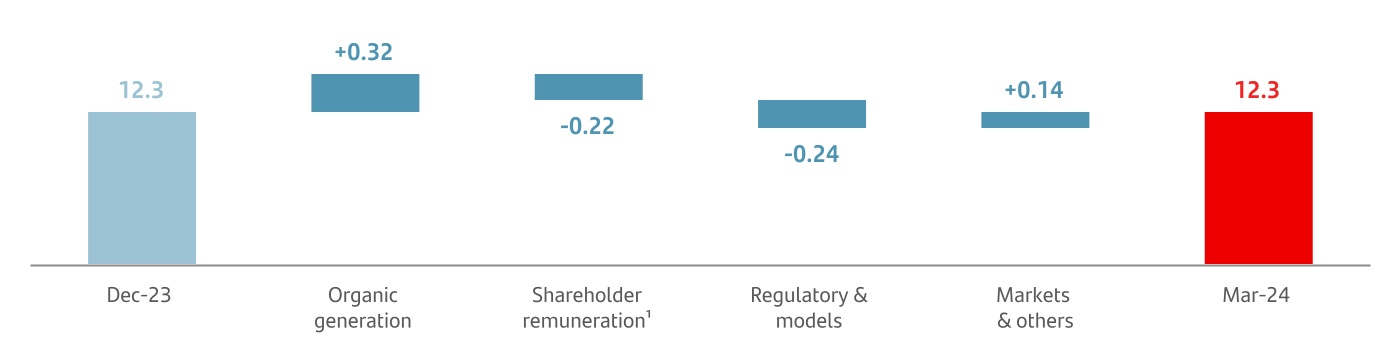

| u | The fully-loaded CET1 ratio stood at 12.3%. In the quarter, there were 32 bps of organic generation (after absorbing the negative 5 bp impact due to the temporary levy on revenue earned in Spain) and a 22 bp charge for a future cash dividend payment against Q1 2024 in line with the 50% payout target1. Additionally, there was a -24 bp regulatory impact relating to a parameter change regarding maturities in CIB models. Lastly, there were positive impacts of 14 bps mostly relating to deductions (DTAs, intangibles, etc) and available-for-sale portfolio valuations. | |||||||||

1.The implementation of the shareholder remuneration policy is subject to future corporate and regulatory decisions and approvals.

January - March 2024 | | 7 | ||||||

| Financial information by segment | Responsible banking Corporate governance Santander share | Appendix | |||||||||||||||||||||||||||

| Group performance | |||||||||||||||||||||||||||||

| Think Value | |||||||

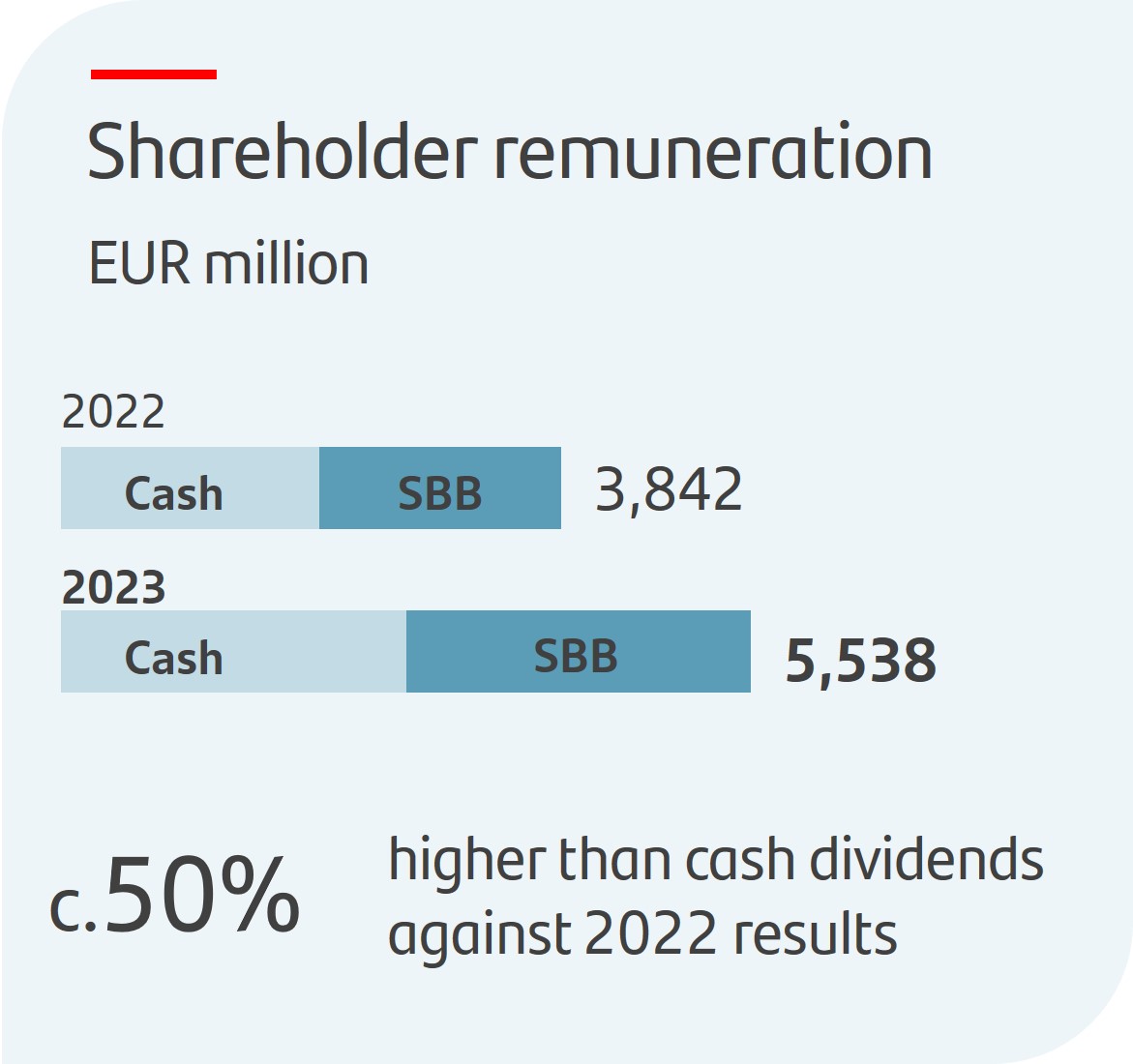

| u | On 22 March 2024, the AGM approved a cash dividend of EUR 9.50 cents per share that will be paid from 2 May 2024. Including the cash dividend paid in November 2023 (EUR 8.10 cents), the total cash dividend per share paid against 2023 results will be EUR 17.60 cents, around 50% more than the dividends paid against 2022 results. | |||||||||

| u | In addition to this payment, there are two share buyback programmes. The first has already been completed for a total of EUR 1,310 million, and the second started on 20 February 2024 having been approved by the board of directors and having obtained the required regulatory authorization, for a maximum amount of EUR 1,459 million. Following the completion of the second share buyback programme, the Group will have repurchased c.11% of its outstanding shares since we began our buybacks in 2021. | ||||||||||

| u | Total shareholder remuneration1 against 2023 results is therefore expected to be EUR 5,538 million, 44% higher than the remuneration against 2022 results, distributed approximately equally between cash dividends and share buybacks. | ||||||||||

| |||||||||||

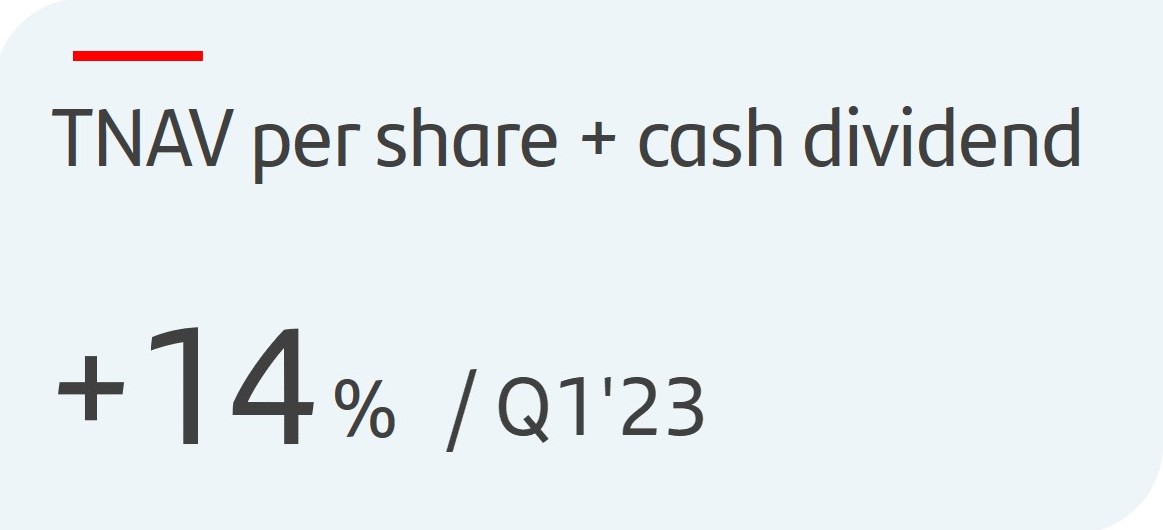

| u | As at March 2023, TNAV was EUR 4.86. Including both dividends charged against 2023 results, the TNAV per share + dividend per share increased 14% year-on-year and 4% in the quarter. | ||||||||||

| Think Customer | |||||||

| u | Total customers amounted to 166 million, 5 million more than in March 2023 and we have 100 million active customers. | |||||||||

| u | Transaction volumes per active customer rose 11% year-on-year in Q1 2024. | ||||||||||

| u | We continue to deliver great customer experience and improve our service quality, ranking in the top 3 in NPS2 in seven of our markets. | ||||||||||

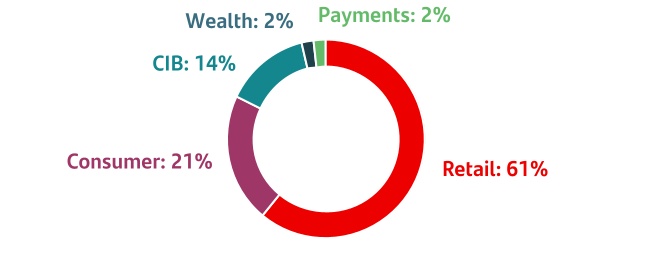

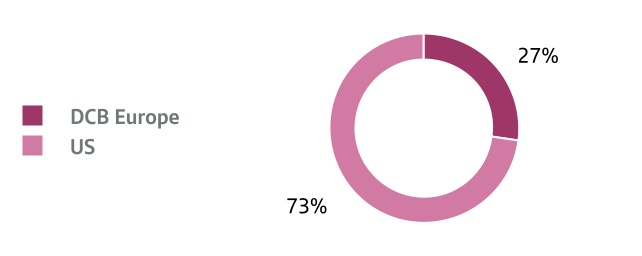

| Think Global | |||||||

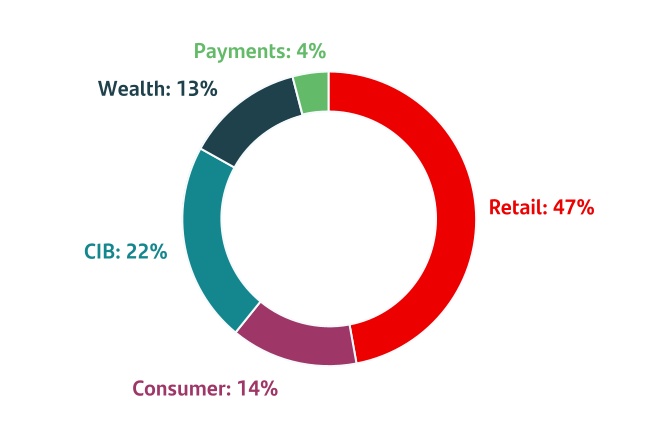

Contribution to Group revenue3 | Year-on-year changes | |||||||||||||

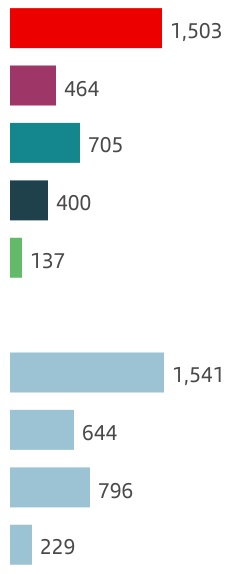

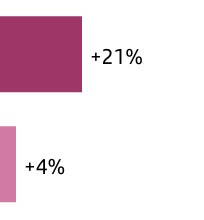

| u | In Retail, attributable profit was EUR 1,503 million (+26% in euros and +22% in constant euros) driven by a positive performance in total income, cost management and lower provisions. | ||||||||||||

| u | Efficiency improved 3.9 pp to 41.1%, cost of risk remained controlled (1.03%) and RoTE increased to 15.6% (17.6% annualizing the impact of the temporary levy). | |||||||||||||

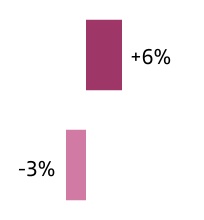

| u | In Consumer, net operating income increased 7%, supported by total income growth (4%) and flat costs. However, attributable profit fell (-5% in euros and in constant euros) to EUR 464 million, impacted by cost of risk normalization. | ||||||||||||

| u | Efficiency stood at 41.2%, improving 1.9 pp, cost of risk was 2.12% and RoTE stood at 11.2% (11.9% annualizing the impact of the temporary levy). | |||||||||||||

| u | In CIB, we achieved record total income. However, attributable profit (EUR 705 million) declined 5% (in euros and constant euros), impacted by costs relating to our transformation investments and higher LLPs (net releases in Q1 2023). | ||||||||||||

| u | The efficiency ratio was 42.0%, remaining one the best in the sector. RoTE was 19.2% (19.7% annualizing the impact of the temporary levy). | |||||||||||||

| u | In Wealth, attributable profit amounted to EUR 400 million, 27% higher year-on-year (+25% in constant euros) driven by higher activity and margin management in a favourable interest rate environment. If we include fees ceded to the commercial network, profit was EUR 838 million (+16% in constant euros). | ||||||||||||

| u | Efficiency improved 4.0 pp to 34.4% and RoTE was 77.3% (80.4% annualizing the impact of the temporary levy). | |||||||||||||

| u | In Payments, attributable profit was EUR 137 million, 29% higher year-on-year in euros (+22% in constant euros) supported by lower LLPs in our Cards business. | ||||||||||||

| u | Cost of risk increased 16 bps to 6.89%. In PagoNxt, EBITDA margin was 17.0% (+10 pp). | |||||||||||||

1.In line with the current shareholder remuneration policy of approximately 50% of the Group's reported profit (excluding non-cash, non-capital ratios impact items), divided approximately equally between cash dividends and share repurchases. Execution of the shareholder remuneration policy is subject to future corporate and regulatory decisions and approvals.

2.Net Promoter Score, internal benchmark of individual customers' satisfaction audited by Stiga/Deloitte in H2'23.

3.As % of total operating areas, excluding the Corporate Centre.

| 8 | | January - March 2024 | ||||||

Grupo Santander results

| Grupo Santander. Summarized income statement | ||||||||||||||||||||||||||

| EUR million | ||||||||||||||||||||||||||

| Change | Change | |||||||||||||||||||||||||

| Q1'24 | Q4'23 | % | % excl. FX | Q1'23 | % | % excl. FX | ||||||||||||||||||||

| Net interest income | 11,983 | 11,122 | 7.7 | 7.7 | 10,396 | 15.3 | 13.2 | |||||||||||||||||||

Net fee income1 | 3,240 | 2,835 | 14.3 | 14.4 | 3,043 | 6.5 | 4.8 | |||||||||||||||||||

Gains or losses on financial assets and liabilities and exchange differences2 | 623 | 664 | (6.2) | (6.0) | 715 | (12.9) | (12.6) | |||||||||||||||||||

| Dividend income | 93 | 97 | (4.1) | (4.3) | 63 | 47.6 | 46.8 | |||||||||||||||||||

| Share of results of entities accounted for using the equity method | 123 | 151 | (18.5) | (18.3) | 126 | (2.4) | (3.9) | |||||||||||||||||||

Other operating income/expenses3 (net) | (1,017) | (317) | 220.8 | 219.0 | (421) | 141.6 | 136.6 | |||||||||||||||||||

| Total income | 15,045 | 14,552 | 3.4 | 3.4 | 13,922 | 8.1 | 6.3 | |||||||||||||||||||

| Operating expenses | (6,547) | (6,464) | 1.3 | 1.3 | (6,145) | 6.5 | 5.2 | |||||||||||||||||||

| Administrative expenses | (5,719) | (5,685) | 0.6 | 0.6 | (5,356) | 6.8 | 5.4 | |||||||||||||||||||

| Staff costs | (3,594) | (3,646) | (1.4) | (1.5) | (3,245) | 10.8 | 9.4 | |||||||||||||||||||

| Other general administrative expenses | (2,125) | (2,039) | 4.2 | 4.3 | (2,111) | 0.7 | (0.7) | |||||||||||||||||||

| Depreciation and amortization | (828) | (779) | 6.3 | 6.4 | (789) | 4.9 | 3.9 | |||||||||||||||||||

| Provisions or reversal of provisions | (633) | (689) | (8.1) | (8.3) | (642) | (1.4) | (3.8) | |||||||||||||||||||

| Impairment or reversal of impairment of financial assets not measured at fair value through profit or loss (net) | (3,134) | (3,479) | (9.9) | (9.8) | (3,301) | (5.1) | (7.0) | |||||||||||||||||||

| Impairment on other assets (net) | (129) | (108) | 19.4 | 18.9 | (22) | 486.4 | 484.5 | |||||||||||||||||||

| Gains or losses on non-financial assets and investments, net | 2 | 33 | (93.9) | (94.6) | 26 | (92.3) | (93.3) | |||||||||||||||||||

| Negative goodwill recognized in results | 0 | 39 | — | — | 0 | — | — | |||||||||||||||||||

| Gains or losses on non-current assets held for sale not classified as discontinued operations | (21) | 38 | — | — | (6) | 250.0 | 209.6 | |||||||||||||||||||

| Profit or loss before tax from continuing operations | 4,583 | 3,922 | 16.9 | 17.1 | 3,832 | 19.6 | 17.5 | |||||||||||||||||||

| Tax expense or income from continuing operations | (1,468) | (724) | 102.8 | 102.9 | (967) | 51.8 | 49.0 | |||||||||||||||||||

| Profit from the period from continuing operations | 3,115 | 3,198 | (2.6) | (2.3) | 2,865 | 8.7 | 6.9 | |||||||||||||||||||

| Profit or loss after tax from discontinued operations | — | — | — | — | — | — | — | |||||||||||||||||||

| Profit for the period | 3,115 | 3,198 | (2.6) | (2.3) | 2,865 | 8.7 | 6.9 | |||||||||||||||||||

| Profit attributable to non-controlling interests | (263) | (265) | (0.8) | 1.4 | (294) | (10.5) | (10.7) | |||||||||||||||||||

| Profit attributable to the parent | 2,852 | 2,933 | (2.8) | (2.7) | 2,571 | 10.9 | 8.8 | |||||||||||||||||||

| EPS (euros) | 0.17 | 0.18 | (2.7) | 0.15 | 13.7 | |||||||||||||||||||||

| Diluted EPS (euros) | 0.17 | 0.17 | (2.6) | 0.15 | 13.6 | |||||||||||||||||||||

| Memorandum items: | ||||||||||||||||||||||||||

| Average total assets | 1,804,334 | 1,799,535 | 0.3 | 1,742,316 | 3.6 | |||||||||||||||||||||

| Average stockholders' equity | 96,308 | 94,877 | 1.5 | 90,353 | 6.6 | |||||||||||||||||||||

| NOTE: The summarized income statement groups some lines of the consolidated income statement on page 88 as follows: | |||||

1.‘Commission income’ and ‘Commission expense’. | |||||

2.‘Gain or losses on financial assets and liabilities not measured at fair value through profit or loss, net’; ‘Gain or losses on financial assets and liabilities held for trading, net’; ‘Gains or losses on non-trading financial assets and liabilities mandatorily at fair value through profit or loss’; ‘Gain or losses on financial assets and liabilities measured at fair value through profit or loss, net’; ‘Gain or losses from hedge accounting, net’; and ‘Exchange differences, net’. | |||||

3.‘Other operating income’; ‘Other operating expenses’; ’Income from insurance and reinsurance contracts’; and ‘Expenses from insurance and reinsurance contracts’. | |||||

January - March 2024 | | 9 | ||||||

| Executive summary | ||||||||||||||||||||||||||||||||||||||

→ Positive start to the year, with strong profit growth despite the higher impact from the temporary levy on revenue earned in Spain → Continuation of 2023 trends: record quarter in net interest income and net fee income → Efficiency improvement and profitable growth supported by the operational leverage resulting from ONE Transformation → Risk indicators were stable, due to good risk management, the economic environment and low unemployment | ||||||||||||||||||||

| Attributable profit | RoTE | RoRWA | ||||||||||||||||||

| EUR 2,852 mn | +11% in euros | 14.9% | 1.96% | |||||||||||||||||

| +9% in constant euros | +55 bps | +10 bps | ||||||||||||||||||

| Changes vs. Q1 2023. | ||||||||||||||||||||

Results performance compared to Q1 2023

The Group presents, both at the total Group level and for each of the business units, the changes in euros registered in the income statement, as well as variations excluding the exchange rate effect (except for Argentina and any grouping which includes it; for further information, see methodology in the section 'Alternative performance measures' in the appendix to this report), understanding that the latter provide a better analysis of the Group’s management. At the Group level, exchange rates had a positive impact of 2 pp in revenue and a negative impact of 1 pp in costs.

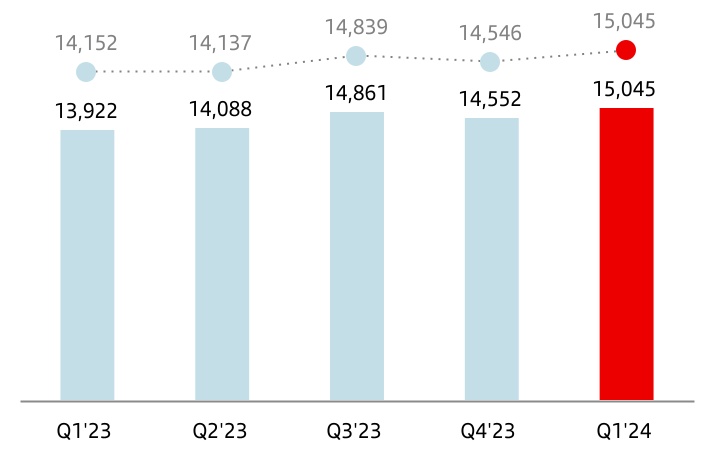

Total income

Total income amounted to EUR 15,045 million, up 8% year-on-year and increased 6% in constant euros. By line:

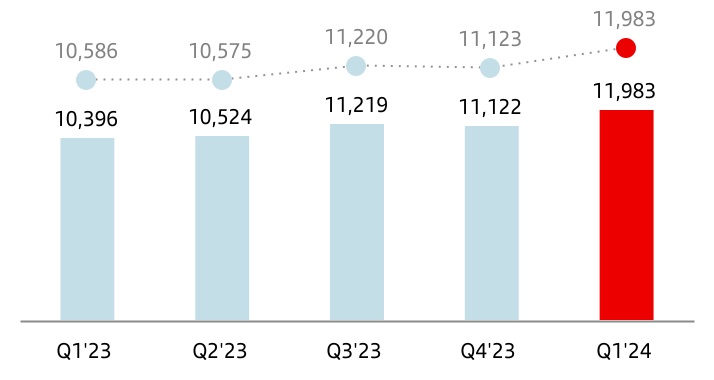

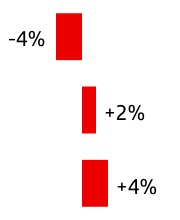

•Net interest income (NII) amounted to EUR 11,983 million, 15% higher than Q1 2023 with widespread growth across businesses and regions. In constant euros, it rose 13%, by business:

–Strong growth in Retail, with increases across all regions but especially in Europe, driven by good margin management, and in South America, which benefitted from lower deposit costs following interest rate cuts and higher volumes, particularly in Brazil.

–In Consumer, NII rose driven by higher volumes in Europe and lower interest rates favouring consumption in Brazil.

–CIB increased strongly, backed by robust performances in all its businesses.

–In Wealth, double-digit rise due to good commercial activity in Private Banking and good margin management in the favourable interest rate environment.

| Net interest income | |||||

| EUR million | |||||

| constant euros | ||||

–In Payments, strong growth due to the increases in both PagoNxt and Cards.

In addition, NII in Q1 2023 included a positive EUR 211 million impact from the reversal of tax liabilities in Brazil.

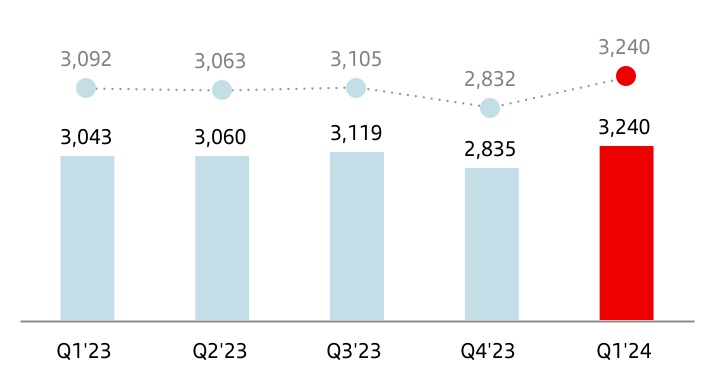

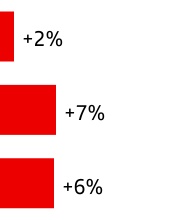

•Net fee income amounted to EUR 3,240 million, up 6% compared to Q1 2023. In constant euros, it was 5% higher, by business:

– In Retail, net fee income increased, with growth across most countries, but especially in Mexico (insurance) and Brazil (account maintenance and insurance).

– In Consumer, net fee income rose double digits, supported by insurance in DCB Europe and Brazil.

– In CIB, it increased, driven by greater activity in Global Banking.

– In Wealth, double-digit growth in net fee income, benefitting from increased activity in Private Banking and Asset Management.

– In Payments, net fee income declined year-on-year due to Cards, impacted by a one-time positive fee recorded in Q1 2023 from commercial agreements in Brazil, campaigns to increase loyalty in Mexico and new regulation on interchange fees in Chile.

| Net fee income | |||||

| EUR million | |||||

| constant euros | ||||

| 10 | | January - March 2024 | ||||||

•Gains on financial transactions declined to EUR 623 million (EUR 715 million in Q1 2023) driven by the higher losses in the Corporate Centre (with higher negative results from the FX hedge).

•Dividend income was EUR 93 million (EUR 63 million in Q1 2023).

•The income from companies accounted for by the equity method reached EUR 123 million, compared to EUR 126 million in Q1 2023.

•Other operating income recorded a loss of EUR 1,017 million (compared to a EUR 421 million loss in Q1 2023), owing to the hyperinflation adjustment in Argentina and the EUR 335 million charge relating to the temporary levy on revenue earned in Spain (EUR 224 million in Q1 2023).

In summary, a robust performance in total income, with increases across all businesses (except Payments which was flat) and regions, reaching record figures both in net interest income and net fee income.

| Total income | |||||

| EUR million | |||||

| constant euros | ||||

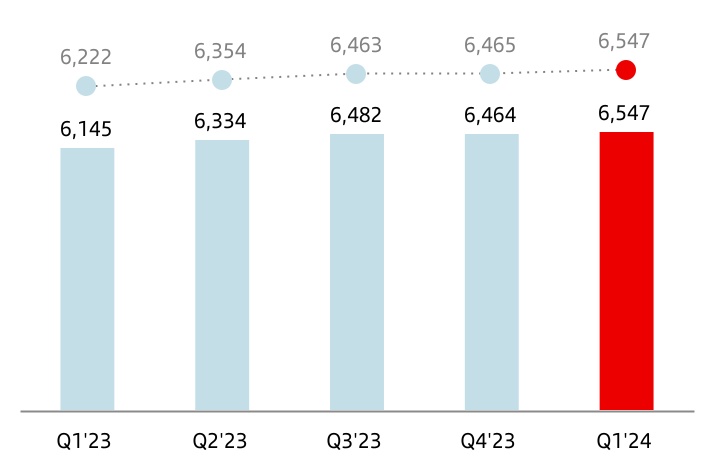

Costs

Operating expenses amounted to EUR 6,547 million, 7% more than Q1 2023 (+5% in constant euros), mainly due to the impact of inflation. In real terms (excluding the impact of average inflation and in constant euros), costs increased 1% year-on-year.

Our cost management continued to focus on structurally improving our efficiency, and as a result, we increased our operating leverage and remained among the most efficient banks in the world.

Our business transformation plan, One Transformation, continued to progress across our footprint, reflected in greater operating productivity and better business dynamics.

In constant euros, operating expenses by business performed as follows:

•In Retail, costs increased 4% driven by higher personnel and transformation costs in the UK, Poland, Mexico and Brazil, with good performances in Spain and the US. In real terms, without the impact of inflation, costs remained flat.

•In Consumer, they remained flat but decreased 4% in real terms reflecting cost discipline in the US, which enabled us to absorb our strategic investments in buy now, pay later and leasing platforms (launched in two European markets).

•In CIB, the 19% rise in costs (+15% in real terms) reflects the investments in transformation and in new products and capabilities in the US.

•In Wealth, costs were up 5% impacted by inflation as in real terms they increased just 1% due to investments in key initiatives, such as strengthening our Private Banking teams.

•In Payments, costs were 8% higher affected by inflationary pressures (+4% in real terms), and platform investments in both PagoNxt and Cards.

| Operating expenses | |||||

| EUR million | |||||

| constant euros | ||||

January - March 2024 | | 11 | ||||||

Provisions or reversal of provisions

Provisions (net of provisions reversals) amounted to EUR 633 million (EUR 642 million in Q1 2023).

Impairment or reversal of impairment of financial assets not measured at fair value through profit or loss (net)

Impairment or reversal of impairment on financial assets not measured at fair value through profit or loss (net) was EUR 3,134 million (EUR 3,301 million in Q1 2023, affected by higher provisions recorded in Brazil). Credit quality indicators remained stable, supported by the good performance of the global economy and labour markets across our footprint.

Impairment on other assets (net)

The impairment on other assets (net) was EUR 129 million, compared to an impairment of EUR 22 million in the Q1 2023.

Gains or losses on non-financial assets and investments (net)

Net gains on non-financial assets and investments were EUR 2 million in Q1 2024 (gain of EUR 26 million in Q1 2023).

Negative goodwill recognized in results

There was no negative goodwill recorded in Q1 2024 or in Q1 2023.

| Net loan-loss provisions | |||||

| EUR million | |||||

| constant euros | ||||

Gains or losses on non-current assets held for sale not classified as discontinued operations

This item, which mainly includes impairment of foreclosed assets recorded and the sale of properties acquired upon foreclosure, recorded a EUR 21 million loss in Q1 2024 (EUR 6 million loss in Q1 2023).

Profit before tax

Profit before tax was EUR 4,583 million in Q1 2024, +20% year-on-year. In constant euros, it rose 18% supported by the solid performance in net interest income and net fee income, which more than offset the inflationary impact on costs and the investments in transformation and digitalization, as well as the impact of the temporary levy on revenue earned in Spain.

Income tax

Total income tax rose to EUR 1,468 million compared to EUR 967 million in Q1 2023, partially driven by lower tax related to the aforementioned reversal of tax liabilities in Brazil.

Profit attributable to non-controlling interests

Profit attributable to non-controlling interests amounted to EUR 263 million, EUR 31 million less than in Q1 2023 due to DCB Europe.

Profit attributable to the parent

Profit attributable to the parent amounted to EUR 2,852 million in Q1 2024, compared to EUR 2,571 million in the same period in 2023. These results do not fully reflect profit performance due to the impact of the temporary levy on revenue earned in Spain mentioned in other sections of the report.

RoTE stood at 14.9% (14.4% in Q1 2023), RoRWA at 1.96% (1.86% in Q1 2023) and earnings per share stood at EUR 0.17 (EUR 0.15 in Q1 2023).

Annualizing the impact of the temporary levy on revenue earned in Spain, RoTE would be 16.2%.

| 12 | | January - March 2024 | ||||||

Underlying profit attributable to the parent

Profit attributable to the parent and underlying profit were the same in Q1 2024 (EUR 2,852 million), and in Q1 2023 (EUR 2,571 million) as profit was not affected by results that fell outside the ordinary course of our business, but there was a reclassification of certain items under some headings of the underlying statement to better understand the business trends. These items are:

•The impact of the temporary levy on revenue earned in Spain totalling EUR 335 million in Q1 2024, and EUR 224 million in Q1 2023, which was moved from total income to other gains (losses) and provisions.

•Additionally, results in Brazil related to reversal of tax liabilities amounted to EUR 261 million (EUR 211 million recorded in NII and a positive impact of EUR 50 million in tax) and provisions to strengthen the balance sheet, which, net of tax, totalled EUR 261 million (EUR 474 million recorded in net loan-loss provisions and a positive impact of EUR 213 million in tax). As the impact from these movements on profit was zero, we have netted them from the underlying account lines to facilitate comparison between quarters.

For more details, see the 'Alternative Performance Measures' section in the appendix of this report.

Attributable profit and underlying profit increased 11% in euros and 9% in constant euros compared to Q1 2023.

On a like-for-like basis, excluding the impact of the temporary levy on revenue earned in Spain, profit increased by 14% and 12% in constant euros.

This profit growth was mainly boosted by a solid performance in total income, which increased 10% in euros and 9% in constant euros year-on-year, and by the efficiency improvement (down to 42.6%).

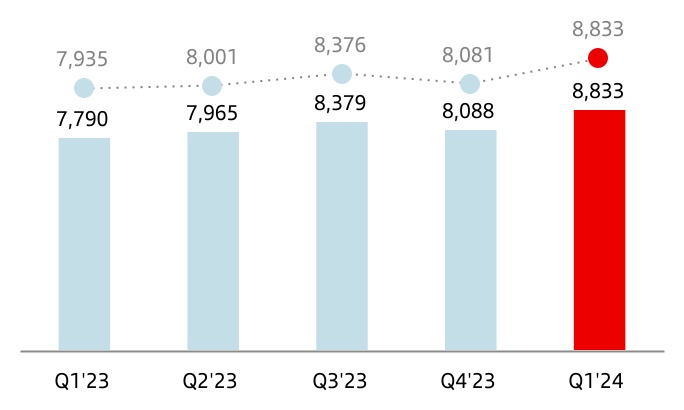

Santander's net operating income was EUR 8,833 million, 13% higher year-on-year. In constant euros, it rose 11% as follows:

•In Retail, net operating income was 21% up, with strong improvements in all regions, supported by revenue growth (+13%) due to good margin management reflected in net interest income, and cost discipline, with costs growing in line with inflation.

•In Consumer, it increased 7%, supported by sustained revenue growth, due to active loan repricing, focus on profitability in Europe (where volumes are increasing) and the increase in customer deposits. Costs were controlled, remaining stable in an environment of persistently high inflation.

•In CIB, despite good revenue dynamics driven by strong growth in North America, net operating income declined 3% due to the increase in costs, impacted by our investments in new products and capabilities, as mentioned earlier.

•In Wealth, net operating income rose 24% as total income growth outpaced costs, due to good commercial activity in Private Banking and Asset Management, which supported a 4 pp efficiency improvement to 34.4%.

•In Payments, net operating income decreased 7%, due to lower revenue (one-time positive fee recorded in Q1 2023 in Brazil, loyalty campaigns in Mexico and new regulation in Chile) and investments in the development of global platforms.

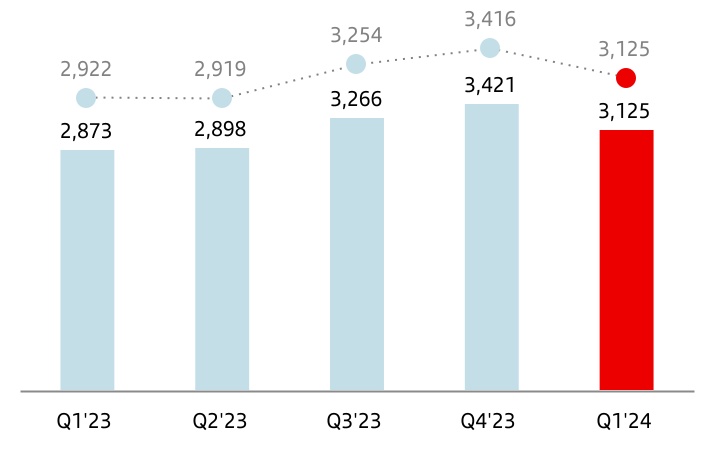

Net loan-loss provisions rose 9% (+7% in constant euros) mainly due to the normalization and higher volumes in Consumer. Cost of risk remained stable at 1.20%, in line with the Group's target for the year.

| Summarized underlying income statement | ||||||||||||||||||||||||||

| EUR million | Change | Change | ||||||||||||||||||||||||

| Q1'24 | Q4'23 | % | % excl. FX | Q1'23 | % | % excl. FX | ||||||||||||||||||||

| Net interest income | 11,983 | 11,122 | 7.7 | 7.7 | 10,185 | 17.7 | 15.6 | |||||||||||||||||||

| Net fee income | 3,240 | 2,835 | 14.3 | 14.4 | 3,043 | 6.5 | 4.8 | |||||||||||||||||||

Gains (losses) on financial transactions 1 | 623 | 664 | (6.2) | (5.9) | 715 | (12.9) | (12.6) | |||||||||||||||||||

| Other operating income | (466) | (69) | 575.4 | 557.7 | (8) | — | — | |||||||||||||||||||

| Total income | 15,380 | 14,552 | 5.7 | 5.7 | 13,935 | 10.4 | 8.6 | |||||||||||||||||||

| Administrative expenses and amortizations | (6,547) | (6,464) | 1.3 | 1.3 | (6,145) | 6.5 | 5.2 | |||||||||||||||||||

| Net operating income | 8,833 | 8,088 | 9.2 | 9.3 | 7,790 | 13.4 | 11.3 | |||||||||||||||||||

| Net loan-loss provisions | (3,125) | (3,421) | (8.7) | (8.5) | (2,873) | 8.8 | 6.9 | |||||||||||||||||||

| Other gains (losses) and provisions | (1,125) | (745) | 51.0 | 49.9 | (822) | 36.9 | 34.0 | |||||||||||||||||||

| Profit before tax | 4,583 | 3,922 | 16.9 | 17.1 | 4,095 | 11.9 | 9.8 | |||||||||||||||||||

| Tax on profit | (1,468) | (724) | 102.8 | 102.6 | (1,230) | 19.3 | 16.7 | |||||||||||||||||||

| Profit from continuing operations | 3,115 | 3,198 | (2.6) | (2.3) | 2,865 | 8.7 | 6.9 | |||||||||||||||||||

| Net profit from discontinued operations | — | — | — | — | — | — | — | |||||||||||||||||||

| Consolidated profit | 3,115 | 3,198 | (2.6) | (2.3) | 2,865 | 8.7 | 6.9 | |||||||||||||||||||

| Non-controlling interests | (263) | (265) | (0.8) | 1.3 | (294) | (10.5) | (10.8) | |||||||||||||||||||

| Profit attributable to the parent | 2,852 | 2,933 | (2.8) | (2.7) | 2,571 | 10.9 | 8.8 | |||||||||||||||||||

1.Includes exchange differences.

January - March 2024 | | 13 | ||||||

Underlying results performance compared to the previous quarter

Underlying profit attributable to the parent and profit attributable to the parent were the same, EUR 2,852 million in Q1 2024, and EUR 2,933 million in Q4 2023, as profit was not affected by results outside the ordinary course of our business.

Profit decreased 3% quarter-on-quarter in euros. In constant euros, it also decreased 3% with the performance of the main lines of the income statement as follows:

Total income rose 6%, driven by the positive performance of the main lines:

•Net interest income was up 8%, with growth in all businesses. In Retail, NII was supported by good margin management and Consumer by active portfolio repricing, focus on profitability and the increase in deposits.

•Net fee income increased 14% compared to the previous quarter, registering a record quarter of EUR 3,240 million, driven by growth of CIB in the US, and the increased commercial activity in Retail.

| Net operating income | |||||

| EUR million | |||||

| constant euros | ||||

•Gains on financial transactions fell 6%, with good performance in CIB that partially offset higher losses in the Corporate Centre.

•Operating expenses in Q1 2024 increased 1% quarter-on-quarter. This performance benefited from declines in Consumer, Wealth and the Corporate Centre, as well as in CIB (following the pick up in the previous quarter due the greater impact relating to the investments mentioned earlier), which offset the increases in Retail, impacted by inflation in Argentina, and in Payments, from platform investments.

•Net loan-loss provisions dropped 9% explained by single names in CIB in Q4 2023 and lower provisions in Retail.

•Other gain (losses) and provisions recorded a loss of EUR 1,125 million, which includes the charge of EUR 335 million for the temporary levy on revenue earned in Spain, compared to the loss of EUR 745 million recorded in Q4 2023.

| Profit attributable to the parent | |||||

| EUR million | |||||

| constant euros | ||||

| 14 | | January - March 2024 | ||||||

Grupo Santander balance sheet

| Grupo Santander. Condensed balance sheet | |||||||||||||||||

| EUR million | |||||||||||||||||

| Change | |||||||||||||||||

| Assets | Mar-24 | Mar-23 | Absolute | % | Dec-23 | ||||||||||||

| Cash, cash balances at central banks and other demand deposits | 174,161 | 203,359 | (29,198) | (14.4) | 220,342 | ||||||||||||

| Financial assets held for trading | 209,589 | 172,889 | 36,700 | 21.2 | 176,921 | ||||||||||||

| Debt securities | 71,983 | 46,295 | 25,688 | 55.5 | 62,124 | ||||||||||||

| Equity instruments | 19,805 | 13,704 | 6,101 | 44.5 | 15,057 | ||||||||||||

| Loans and advances to customers | 18,722 | 10,512 | 8,210 | 78.1 | 11,634 | ||||||||||||

| Loans and advances to central banks and credit institutions | 39,146 | 36,150 | 2,996 | 8.3 | 31,778 | ||||||||||||

| Derivatives | 59,933 | 66,228 | (6,295) | (9.5) | 56,328 | ||||||||||||

Financial assets designated at fair value through profit or loss1 | 14,919 | 15,411 | (492) | (3.2) | 15,683 | ||||||||||||

| Loans and advances to customers | 6,474 | 6,979 | (505) | (7.2) | 7,201 | ||||||||||||

| Loans and advances to central banks and credit institutions | 455 | 647 | (192) | (29.7) | 459 | ||||||||||||

| Other (debt securities an equity instruments) | 7,990 | 7,785 | 205 | 2.6 | 8,023 | ||||||||||||

| Financial assets at fair value through other comprehensive income | 84,183 | 84,214 | (31) | — | 83,308 | ||||||||||||

| Debt securities | 73,638 | 73,406 | 232 | 0.3 | 73,565 | ||||||||||||

| Equity instruments | 1,916 | 1,997 | (81) | (4.1) | 1,761 | ||||||||||||

| Loans and advances to customers | 8,282 | 8,510 | (228) | (2.7) | 7,669 | ||||||||||||

| Loans and advances to central banks and credit institutions | 347 | 301 | 46 | 15.3 | 313 | ||||||||||||

| Financial assets measured at amortized cost | 1,207,699 | 1,165,387 | 42,312 | 3.6 | 1,191,403 | ||||||||||||

| Debt securities | 112,589 | 83,928 | 28,661 | 34.1 | 103,559 | ||||||||||||

| Loans and advances to customers | 1,016,055 | 1,015,387 | 668 | 0.1 | 1,009,845 | ||||||||||||

| Loans and advances to central banks and credit institutions | 79,055 | 66,072 | 12,983 | 19.6 | 77,999 | ||||||||||||

| Investments in subsidiaries, joint ventures and associates | 7,685 | 7,668 | 17 | 0.2 | 7,646 | ||||||||||||

| Tangible assets | 34,229 | 33,989 | 240 | 0.7 | 33,882 | ||||||||||||

| Intangible assets | 19,910 | 18,880 | 1,030 | 5.5 | 19,871 | ||||||||||||

| Goodwill | 14,028 | 13,870 | 158 | 1.1 | 14,017 | ||||||||||||

| Other intangible assets | 5,882 | 5,010 | 872 | 17.4 | 5,854 | ||||||||||||

Other assets2 | 47,631 | 47,605 | 26 | 0.1 | 48,006 | ||||||||||||

| Total assets | 1,800,006 | 1,749,402 | 50,604 | 2.9 | 1,797,062 | ||||||||||||

| Liabilities and shareholders' equity | |||||||||||||||||

| Financial liabilities held for trading | 130,466 | 123,716 | 6,750 | 5.5 | 122,270 | ||||||||||||

| Customer deposits | 24,338 | 14,139 | 10,199 | 72.1 | 19,837 | ||||||||||||

| Debt securities issued | 0 | 0 | — | — | 0 | ||||||||||||

| Deposits by central banks and credit institutions | 21,095 | 24,066 | (2,971) | (12.3) | 25,670 | ||||||||||||

| Derivatives | 54,454 | 63,070 | (8,616) | (13.7) | 50,589 | ||||||||||||

| Other | 30,579 | 22,441 | 8,138 | 36.3 | 26,174 | ||||||||||||

| Financial liabilities designated at fair value through profit or loss | 38,583 | 37,096 | 1,487 | 4.0 | 40,367 | ||||||||||||

| Customer deposits | 29,532 | 28,441 | 1,091 | 3.8 | 32,052 | ||||||||||||

| Debt securities issued | 5,933 | 5,726 | 207 | 3.6 | 5,371 | ||||||||||||

| Deposits by central banks and credit institutions | 3,100 | 2,929 | 171 | 5.8 | 2,944 | ||||||||||||

| Other | 18 | — | 18 | — | — | ||||||||||||

| Financial liabilities measured at amortized cost | 1,465,644 | 1,429,788 | 35,856 | 2.5 | 1,468,703 | ||||||||||||

| Customer deposits | 990,583 | 956,369 | 34,214 | 3.6 | 995,280 | ||||||||||||

| Debt securities issued | 310,627 | 281,033 | 29,594 | 10.5 | 303,208 | ||||||||||||

| Deposits by central banks and credit institutions | 121,424 | 152,446 | (31,022) | (20.3) | 130,028 | ||||||||||||

| Other | 43,010 | 39,940 | 3,070 | 7.7 | 40,187 | ||||||||||||

| Liabilities under insurance contracts | 17,738 | 17,274 | 464 | 2.7 | 17,799 | ||||||||||||

| Provisions | 8,387 | 8,089 | 316 | 3.9 | 8,441 | ||||||||||||

Other liabilities3 | 34,163 | 33,949 | 196 | 0.6 | 35,241 | ||||||||||||

| Total liabilities | 1,694,981 | 1,649,912 | 45,069 | 2.7 | 1,692,821 | ||||||||||||

| Shareholders' equity | 130,876 | 125,061 | 5,815 | 4.6 | 130,443 | ||||||||||||

| Capital stock | 7,913 | 8,227 | (314) | (3.8) | 8,092 | ||||||||||||

Reserves (including treasury stock)4 | 120,111 | 114,263 | 5,848 | 5.1 | 112,573 | ||||||||||||

| Profit attributable to the Group | 2,852 | 2,571 | 281 | 10.9 | 11,076 | ||||||||||||

| Less: dividends | 0 | — | — | — | (1,298) | ||||||||||||

| Other comprehensive income | (34,620) | (34,498) | (122) | 0.4 | (35,020) | ||||||||||||

| Minority interests | 8,769 | 8,927 | (158) | (1.8) | 8,818 | ||||||||||||

| Total equity | 105,025 | 99,490 | 5,535 | 5.6 | 104,241 | ||||||||||||

| Total liabilities and equity | 1,800,006 | 1,749,402 | 50,604 | 2.9 | 1,797,062 | ||||||||||||

| Note: The condensed balance sheet groups some lines of the consolidated balance sheet on pages 86 and 87 as follows: | ||

1.'Non-trading financial assets mandatorily at fair value through profit or loss' and 'Financial assets designated at fair value through profit or loss'. | ||

2.‘Hedging derivatives’; ‘Changes in the fair value of hedged items in portfolio hedges of interest risk’; 'Assets under reinsurance contracts'; ‘Tax assets’; ‘Other assets’; and 'Non-current assets held for sale’. | ||

3.‘Hedging derivatives’; ‘Changes in the fair value of hedged items in portfolio hedges of interest rate risk’; ‘Tax liabilities’; ‘Other liabilities’; and ‘Liabilities associated with non-current assets held for sale‘. | ||

4.‘Share premium’; ‘Equity instruments issued other than capital’; ‘Other equity’; ‘Accumulated retained earnings’; ‘Revaluation reserves’; ‘Other reserves’; and ‘Own shares (-)’. | ||

January - March 2024 | | 15 | ||||||

| Executive summary | ||||||||||||||||||||||||||||||||||||||

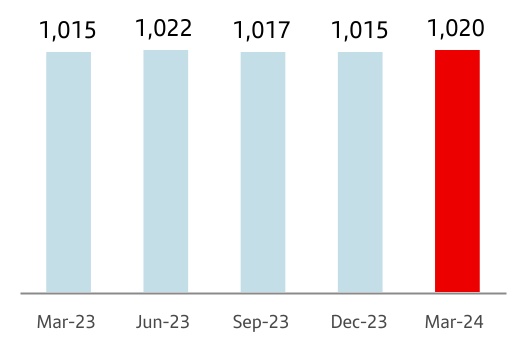

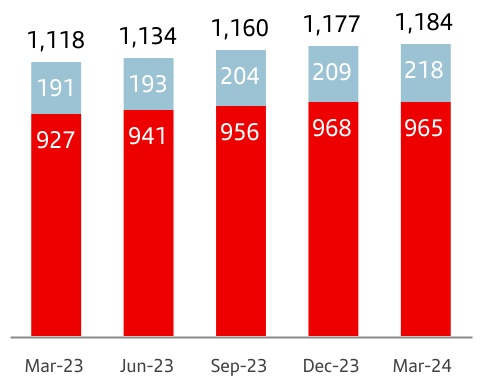

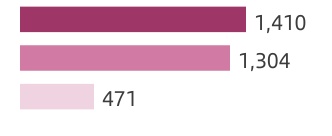

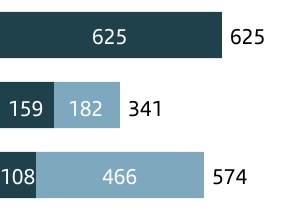

Gross loans and advances to customers (excl. reverse repos) | Customer funds (deposits excl. repos + mutual funds) | |||||||||||||||||||

| Credit remained stable, reflecting the macroeconomic and interest rate environment | Customer funds continued to grow year-on-year. The quarter was affected by the drop in wholesale loans | |||||||||||||||||||

Gross loans and advances to customers (excl. reverse repos) | Customer funds (deposits excl. repos + mutual funds) | |||||||||||||||||||

| 1,020 | +0.1% QoQ | 1,184 | +0.1% QoQ | |||||||||||||||||

| EUR billion | -0.3% YoY | EUR billion | +4.8% YoY | |||||||||||||||||

è By segment: | è By product: | |||||||||||||||||||

| Year-on-year decline in Retail and CIB, partially offset by growth in Consumer | Increase in time deposits and mutual funds at the expense of demand deposits | |||||||||||||||||||

| Retail | Consumer | CIB | Demand | Time | Mutual funds | |||||||||||||||

| -2% | +4% | -1% | -4% | +24% | +14% | |||||||||||||||

| Note: changes in constant euros. | ||||||||||||||||||||

Loans and advances to customers

Loans and advances to customers stood at EUR 1,049,533 million as at end March 2024, a 1% increase both quarter-on-quarter and year-on-year.

For the purpose of analysing traditional banking loans, the Group uses gross loans and advances to customers excluding reverse repos (EUR 1,020,404 million). Additionally, the comments below do not include the exchange rate impact (except for Argentina and any grouping which includes it; for further information, see methodology in the section 'Alternative performance measures' in the appendix to this report).

In Q1 2024, gross loans and advances to customers, excluding reverse repos, were stable, as follows:

•They were flat in Retail, in individuals, SMEs and corporates, with slight declines in Spain and the UK which were offset by growth in South America, coming from individuals.

•In Consumer, loans remained stable as a result of our focus on prioritizing profitable growth over volumes. Growth in Brazil, as a result of lower interest rates which favour consumption, was offset by falls in the US.

•In CIB, loans were up 1%, with growth in North America and South America, while they fell in Europe.

•They increased 1% in both Wealth and Payments.

| Gross loans and advances to customers (excl. reverse repos) | |||||

| EUR billion | |||||

| 0 | % | 1a | |||

| Mar-24 / Mar-23 | |||||

1. In constant EUR: 0%.

Compared to March 2023, gross loans and advances to customers (excluding reverse repos and in constant euros) also remained stable, as follows:

•In Retail, loans declined 2%, with falls in Spain, the UK and Portugal, in mortgages to individuals due to early repayments, and reductions in SMEs and corporates. This was partially offset by growth in Mexico and Brazil.

•They rose 4% in Consumer boosted by the good performance in Auto in Europe and Brazil.

•In CIB, they declined 1% due to lower volumes in Spain and Brazil, partially offset by growth in the US.

•They increased 4% in Wealth and 7% in Payments.

As at end March 2023, gross loans and advances to customers excluding reverse repos maintained a diversified structure among the markets in which the Group operates: Europe (55%), North America (16%), South America (16%), DCB Europe (13%).

| Gross loans and advances to customers (excl. reverse repos) | ||

| % operating areas. March 2024 | ||

| 16 | | January - March 2024 | ||||||

Customer funds

Customer deposits amounted to EUR 1,044,453 million in March 2023, flat quarter-on-quarter, and increasing 5% year-on-year.

The Group uses customer funds (customer deposits excluding repos, plus mutual funds) for the purpose of analysing traditional retail banking funds, which amounted to EUR 1,183,594 million as at end March 2023. Additionally, the comments below do not include the exchange rate impact (except for Argentina and any grouping which includes it; for further information, see methodology in the section 'Alternative performance measures' in the appendix to this report).

In the quarter, customer funds increased EUR 1.7 billion in constant euros, as follows:

•By product, customer deposits excluding repos decreased EUR 8.1 billion and mutual funds rose EUR 9.9 billion.

•By primary segment, customer funds grew 3% in Consumer and 5% in Wealth, while they remained stable in Retail. On the other hand, in CIB they fell 7%.

Compared to March 2023, customer funds were up 5% in constant euros:

•By product, customer deposits excluding repurchase agreements rose 3%, as higher interest rates resulted in a notable increase in time deposits (+24%), which grew significantly in all markets, to the detriment of demand deposits, which fell 4%. Mutual funds increased (+14%).

•By business, customer funds rose 3% in Retail, backed by strong growth in Brazil, Mexico and the UK, +13% in Consumer due to growth in Europe and the US, +3% in CIB, driven by volumes growth in South America, and in Wealth, they increased 9% due to mutual funds. By secondary segment, good performance in all regions, with strong growth in Brazil, the UK, Mexico and DCB Europe.

As at March 2023, customer funds maintained a diversified structure among the markets in which the Group operates: Europe (61%), North America (15%), South America (17%), DCB Europe (7%). The weight of demand deposits as a percentage of total customer funds was 56%, while time deposits accounted for 26% of the total, and mutual funds for 18%.

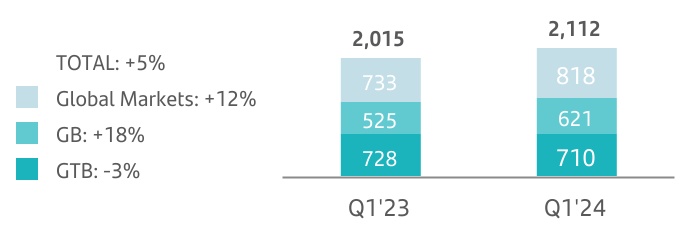

| Customer funds | ||

| EUR billion | ||

| +6 | % | 1a | ||||||

| +15 | % | |||||||

| +4 | % | |||||||

•Total | ||||||||

• Mutual funds | ||||||||

•Deposits exc. repos | ||||||||

| Mar-24 / Mar-23 | ||||||||

1. In constant EUR: +5%.

In addition to capturing customer deposits, the Group, for strategic reasons, maintains a selective policy of issuing securities in the international fixed income markets and strives to adapt the frequency and volume of its market operations to the structural liquidity needs of each unit, as well as to the receptiveness of each market.

In Q1 2024, the Group issued:

•Medium- and long-term senior debt placed in the market of EUR 9,506 million and covered bonds amounting to EUR 4,246 million.

•TLAC eligible instruments issued amounted to EUR 6,446 million to strengthen the Group's position, of which EUR 4,049 million was senior non-preferred, EUR 2,398 million was subordinated debt.

•Maturities of medium- and long-term debt totalled EUR 8,689 million.

The net loan-to-deposit ratio was 100% (104% in March 2023). The ratio of deposits plus medium- and long-term funding to the Group’s loans was 126%, underscoring the comfortable funding structure. The liquidity coverage ratio (LCR) was an estimated 160% in March (166% in December 2023).

The Group's access to wholesale funding markets as well as the cost of issuances depends, in part, on the ratings of the rating agencies.

The ratings of Banco Santander, S.A. by the main rating agencies were Fitch: A- for senior non-preferred debt, A- for senior long-term and A/F1 for senior short-term; Moody's confirmed its A2 long-term and P-1 short-term ratings in April of this year, and also improved its outlook from stable to positive following the same movement in the rating of the Kingdom of Spain, remaining two notches above sovereign; Standard & Poor's (S&P): A+ for long-term rating and A-1 for short-term rating; and DBRS: A High for long-term and R-1 Medium for short-term. DBRS and Fitch maintained their stable outlooks, above the sovereign's outlook, while S&P also maintained its outlook but in line with the sovereign.

Sometimes the methodology applied by the agencies limits a bank's rating to the sovereign rating of the country where it is headquartered. Banco Santander, S.A. is still rated above the sovereign debt rating of the Kingdom of Spain by Moody’s, DBRS and S&P and at the same level by Fitch, which demonstrates our financial strength and diversification.

| Customer funds | ||

| % operating areas. March 2024 | ||

January - March 2024 | | 17 | ||||||

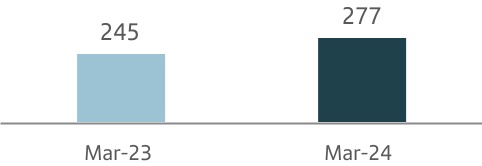

Solvency ratios

| Executive summary | ||||||||||||||||||||||||||||||||||||||

| Fully-loaded capital ratio | Fully-loaded CET1 ratio | |||||||||||||||||||

| The fully-loaded CET1 ratio exceeded 12% at the end of March, in line with the Group's objective | We continued to generate capital organically in the quarter, backed by profit growth | |||||||||||||||||||

| Fully-loaded CET1 performance (%) | Organic generation | +32 bps | ||||||||||||||||||

| ||||||||||||||||||||

Accrual for shareholder remuneration1 | -22 bps | |||||||||||||||||||

| TNAV per share | ||||||||||||||||||||

TNAV per share was EUR 4.86, increasing 4% quarter-on-quarter and 14% year-on-year including the cash dividends. | ||||||||||||||||||||

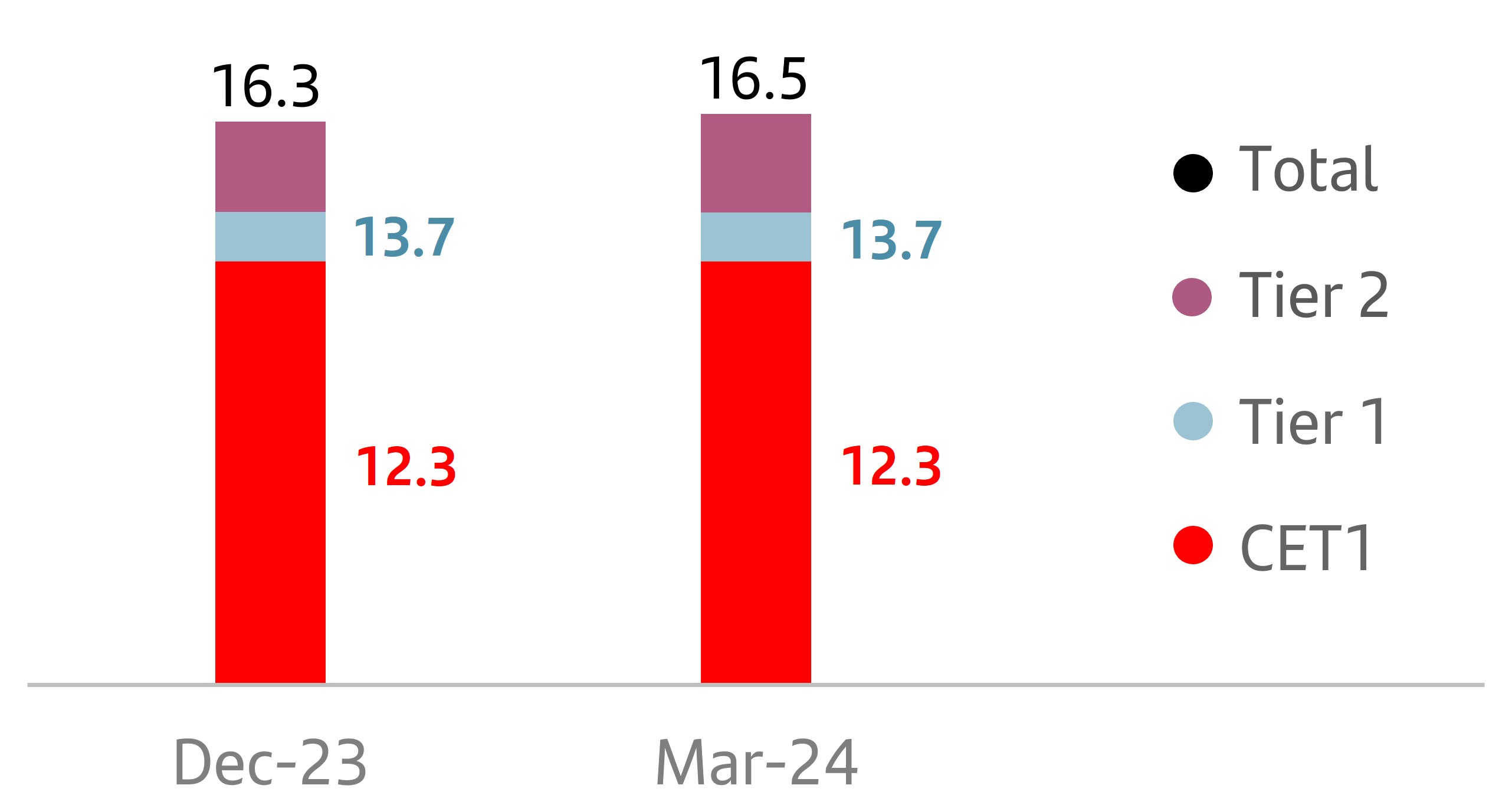

As of end March 2024, the total phased-in capital ratio (applying the IFRS 9 transitional arrangements) stood at 16.6% and the phased-in CET1 ratio at 12.3%. We comfortably meet the levels required by the European Central Bank on a consolidated basis (estimated 13.9% for the total capital ratio and 9.6% for the CET1 ratio)2. This results in a distance to the maximum distributable amount (MDA) of 226 bps and a CET1 management buffer of 266 bps.

In fully-loaded terms, we generated 32 bps organically in the quarter (having absorbed -5 bps due to the temporary levy on revenue earned in Spain) and recorded a 22 bp charge for shareholder remuneration against profit earned in Q1 2024 (split between cash dividends and share buybacks) in line with our 50% payout target1.

We recorded a 24 bp charge in the quarter mainly relating to a parameter change regarding maturities in CIB models. Finally, there was a 14 bp positive impact mainly relating to deductions (DTAs, intangibles, etc) and changes in available-for-sale portfolio valuations, bringing the fully-loaded CET1 ratio to 12.3%.

The total fully-loaded capital ratio stood at 16.5%.

TNAV per share ended the quarter at EUR 4.86. Including the cash dividend paid in November 2023 (EUR 8.10 cents) and the second cash dividend charged against 2023 results (EUR 9.50 cents) approved in March, TNAV plus cash dividend per share increased 14% in the last twelve months (+4% in the quarter).

Lastly, the fully-loaded leverage ratio stood at 4.74%, and the phased-in at 4.75%.

| Eligible capital. March 2024 | ||||||||

| EUR million | ||||||||

| Fully-loaded | Phased-in | |||||||

| CET1 | 78,512 | 78,628 | ||||||

| Basic capital | 87,616 | 87,733 | ||||||

| Eligible capital | 105,905 | 106,226 | ||||||

| Risk-weighted assets | 640,507 | 640,382 | ||||||

| % | % | |||||||

| CET1 capital ratio | 12.3 | 12.3 | ||||||

| Tier 1 capital ratio | 13.7 | 13.7 | ||||||

| Total capital ratio | 16.5 | 16.6 | ||||||

| Fully-loaded CET1 ratio performance | ||

| % | ||

Note: The phased-in ratio includes the transitory treatment of IFRS 9, calculated in accordance with article 473 bis of the Capital Requirements Regulation (CRR2) and subsequent modifications introduced by Regulation 2020/873 of the European Union. Total phased-in capital ratios include the transitory treatment according to chapter 4, title 1, part 10 of the CRR2.

1.Shareholder remuneration charged against profit earned in Q1 2024 (split between cash dividends and share buybacks) in line with our 50% payout target. The implementation of the shareholder remuneration policy is subject to future corporate and regulatory decisions and approvals.

2.On 1 January 2024, our systemic buffer requirement increased from 1% to 1.25% due to a higher D-SIB requirement due to i) a methodological change by the ECB which was later adopted by Banco de España and ii) because institutions must hold capital at the consolidated level for the higher of the G-SIB (currently at 1%) and D-SIB requirements. Additionally, the ECB revised Banco Santander, S.A.'s P2R requirement from 1.58% to 1.74%, mainly due to a change in the ECB's methodology.

| 18 | | January - March 2024 | ||||||

Risk management

| Executive summary | ||||||||||||||||||||||||||||||||||||||

| Credit risk | Market risk | |||||||||||||||||||

| Despite the current macroeconomic environment, credit quality indicators remain within expected levels due to proactive risk management | VaR remained at moderate levels, despite persistent inflation and geopolitical tensions that led to occasional spikes in market volatility | |||||||||||||||||||

| Cost of risk | NPL ratio | Coverage ratio | Average VaR | |||||||||||||||||

| 1.20% | 3.10% | 66% | Q1'24 | EUR 17 million | +EUR 4 mn / Q4'23 | |||||||||||||||

| +2 bps vs. Q4'23 | -4 bps vs. Q4'23 | 0 pp vs. Q4'23 | ||||||||||||||||||

| Structural and liquidity risk | Operational risk | |||||||||||||||||||

| Robust and diversified liquidity buffer, with ratios well above regulatory requirements | The operational risk profile remained stable in the quarter. In terms of losses, there was a reduction compared to the previous quarter. | |||||||||||||||||||

| Liquidity Coverage Ratio (LCR) | ||||||||||||||||||||

| 160% | -6 pp vs. Q4'23 | |||||||||||||||||||

Credit risk 1

During the first quarter of the year, the main factors influencing market behaviour, affecting credit demand and household and corporate affordability were inflation (which remained high, but it is beginning to show signs of coming under control), the delay of central banks interest rate cuts and the uncertainty about economic growth.

Additionally, market volatility and economic activity were affected by other factors such as continuing geopolitical tensions, the pressure on fuel prices due to attacks on Russian refineries, and

the weakness of some regional banks in the US due to their commercial real estate exposures. On the other hand, China’s industrial production and retail sales exceeded expectations in the first two months of the year.

Our geographic diversification and business, together with our proactive risk management, based on customer knowledge and prudent balance sheet management, among others, help us to maintain a medium-low risk profile even in a less favourable macroeconomic and geopolitical environment.

| Key risk metrics | ||||||||||||||||||||||||||||||||||||||||||||||||||

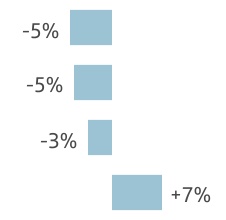

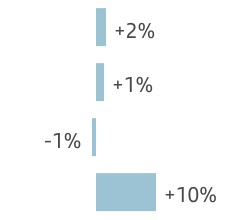

Net loan-loss provisions 2 | Cost of risk (%) 3 | NPL ratio (%) | NPL coverage ratio (%) | |||||||||||||||||||||||||||||||||||||||||||||||

| Q1'24 | Chg (%) / Q4'23 | Chg (%) / Q1'23 | Q1'24 | Chg (bps) / Q4'23 | Chg (bps) / Q1'23 | Q1'24 | Chg (bps) / Q4'23 | Chg (bps) / Q1'23 | Q1'24 | Chg (pp) / Q4'23 | Chg (pp) / Q1'23 | |||||||||||||||||||||||||||||||||||||||

| Retail | 1,523 | (11.8) | (1.6) | 1.03 | 0 | 11 | 3.24 | 3 | 5 | 60 | (1.4) | (2.7) | ||||||||||||||||||||||||||||||||||||||

| Consumer | 1,137 | 1.5 | 24.5 | 2.12 | 8 | 32 | 4.86 | 12 | 82 | 76 | (0.4) | (15.1) | ||||||||||||||||||||||||||||||||||||||

| CIB | 40 | (80.5) | — | 0.14 | 4 | (2) | 1.14 | (22) | (28) | 46 | 5.0 | 10.9 | ||||||||||||||||||||||||||||||||||||||

| Wealth | 4 | — | — | -0.05 | 2 | (15) | 0.64 | (76) | (20) | 62 | 32.3 | (0.6) | ||||||||||||||||||||||||||||||||||||||

| Payments | 418 | 14.1 | (14.4) | 6.89 | (34) | 16 | 4.85 | (18) | (13) | 145 | 5.0 | 1.3 | ||||||||||||||||||||||||||||||||||||||

| TOTAL GROUP | 3,125 | (8.5) | 6.9 | 1.20 | 2 | 15 | 3.10 | (4) | 5 | 66 | 0.1 | (1.8) | ||||||||||||||||||||||||||||||||||||||

| Europe | 484 | (17.5) | (26.3) | 0.41 | (3) | (1) | 2.32 | 0 | (3) | 49 | (0.2) | (1.9) | ||||||||||||||||||||||||||||||||||||||

| North America | 985 | (12.6) | 19.8 | 2.15 | 10 | 52 | 4.07 | (2) | 112 | 74 | 0.3 | (20.7) | ||||||||||||||||||||||||||||||||||||||

| South America | 1,378 | (11.0) | 10.0 | 3.44 | 8 | 5 | 5.37 | (35) | (62) | 80 | 2.0 | 4.0 | ||||||||||||||||||||||||||||||||||||||

| DCBE | 276 | 80.4 | 42.7 | 0.67 | 5 | 19 | 2.27 | 14 | 22 | 86 | (1.9) | (7.4) | ||||||||||||||||||||||||||||||||||||||

| TOTAL GROUP | 3,125 | (8.5) | 6.9 | 1.20 | 2 | 15 | 3.10 | (4) | 5 | 66 | 0.1 | (1.8) | ||||||||||||||||||||||||||||||||||||||

1.Changes in constant euros.

2.EUR million and % change in constant euros.

3.Provisions to cover losses due to impairment of loans in the last 12 months / average customer loans and advances of the last 12 months.

For more detailed information, please see the Alternative Performance Measures section.

January - March 2024 | | 19 | ||||||

In terms of credit quality during Q1 2024:

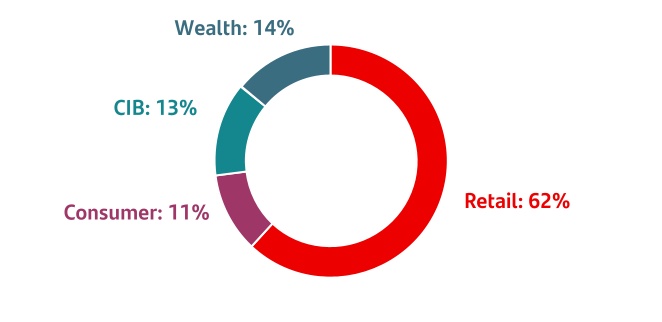

•The NPL ratio stood at 3.10% (-4 bps compared to Q4 2023), mainly due to the performance of credit impaired loans, which stood at EUR 35,637 million (stable in the quarter), supported by positive performances in CIB, Wealth and Payments that offset the increases in Retail (+1.8%) and Consumer (+1.7%). Gross credit risk with customers increased 1% in the quarter to EUR 1,150 billion, distributed mainly among Retail (57% of the Group’s total credit portfolio), Consumer (18%) and CIB (20%) businesses.

•Net loan-loss provisions rose 7% year-on-year to EUR 3,125 million affected by provisions in the US, Mexico, Brazil and DCB Europe. In the quarter, LLPs declined 9%, supported by Europe, North America and South America. The cost of risk was 1.20%, remaining in line with our target for the year.

•The total coverage ratio for credit impaired loans remained stable at 66%, with loan-loss allowances at EUR 23,542 million (stable in the quarter). The coverage ratio remained at comfortable levels considering that 68% of the Group’s portfolio has guaranteed.

The IFRS 9 stage distribution of the portfolio remained stable in the quarter in percentage terms.

| Coverage ratio by stage | |||||||||||||||||||||||

| EUR billion | |||||||||||||||||||||||

Exposure1 | Coverage | ||||||||||||||||||||||

| Mar-24 | Dec-23 | Mar-23 | Mar-24 | Dec-23 | Mar-23 | ||||||||||||||||||

| Stage 1 | 1,007 | 1,000 | 1,005 | 0.4 | % | 0.4 | % | 0.4 | % | ||||||||||||||

| Stage 2 | 83 | 80 | 72 | 6.3 | % | 6.4 | % | 7.4 | % | ||||||||||||||

| Stage 3 | 36 | 36 | 34 | 40.5 | % | 40.6 | % | 40.1 | % | ||||||||||||||

1. Exposure subject to impairment. Additionally, in March 2024 there was EUR 25 billion in loans and advances to customers not subject to impairment recorded at mark to market with changes through P&L (EUR 19 billion in December 2023 and EUR 17 billion in March 2023).

Stage 1: financial instruments for which no significant increase in credit risk has been identified since its initial recognition.

Stage 2: if there has been a significant increase in credit risk since the date of initial recognition but the impairment event has not materialized, the financial instrument is classified in Stage 2.

Stage 3: a financial instrument is catalogued in this stage when it shows effective signs of impairment as a result of one or more events that have already occurred resulting in a loss.

| Credit impaired loans and loan-loss allowances | |||||||||||

| EUR million | |||||||||||

| Change (%) | |||||||||||

| Q1'24 | QoQ | YoY | |||||||||

| Balance at beginning of period | 35,620 | 0.2 | 2.7 | ||||||||

| Net additions | 3,167 | (25.9) | (1.9) | ||||||||

| Increase in scope of consolidation | — | — | — | ||||||||

| Exchange rate differences and other | 45 | — | (84.2) | ||||||||

| Write-offs | (3,195) | (15.9) | (14.6) | ||||||||

| Balance at period-end | 35,637 | 0.0 | 3.5 | ||||||||

| Loan-loss allowances | 23,542 | 0.2 | 0.7 | ||||||||

| For impaired assets | 14,441 | (0.2) | 4.6 | ||||||||

| For other assets | 9,101 | 0.8 | (5.1) | ||||||||

Our Retail, Consumer, CIB and Payments businesses account for 95% of the Group's total portfolio. The performance of the main businesses in the first quarter was as follows:

| Retail & Commercial Banking | Credit risk exposure | |||||||||

| 57% of total Group | |||||||||||

Traditional banking business focusing on simplification and digitalization of products, services and processes and with a clear transformation strategy. It mainly comprises a high quality mortgage portfolio (where 90% of loans have an LTV lower than 80%) and a corporate portfolio where more than 53% have real guarantees or property collateral.

The NPL ratio rose 3 bps to 3.24%, driven by the increase in credit impaired loans, mainly in Europe. Gross credit risk with customers remained stable in the quarter, as the slight business growth in corporates was offset by the pre-payment of loans by individuals.

Net loan-loss provisions declined 2% year-on-year, mainly due to the positive performance of the European portfolios, and were 12% lower quarter-on-quarter driven by Europe and Brazil. The cost of risk stood at 1.03%, remaining at controlled levels and largely unchanged in the quarter.

The total coverage ratio of credit impaired loans decreased 1 pp in the quarter. This business includes the mortgage portfolios in Spain and the UK which have high-quality collateral, and so we are comfortable with the current coverage levels.

| Digital Consumer Bank | Credit risk exposure | |||||||||

| 18% of total Group | |||||||||||

Business mainly dedicated to vehicle financing through strategic alliances and leasing business.

The NPL ratio increased 12 bps in the quarter to 4.86%, as a result of the credit impaired loan growth (+2% compared to the December 2023), which amounted to EUR 10,114 million and was mainly affected by the European portfolios, while performance in the US was positive (motivated by the tax season). On the other hand, gross credit risk with customers remained stable in the quarter.

Net loan-loss provisions increased 24% year-o n-year due to normalization in the US and +2% in the quarter affected by provisions in DCB Europe and Brazil, while performance in the US was positive (motivated by the tax season). The cost of risk stood at 2.12%, increasing in line with expectations.

The coverage of credit impaired loans stood at 76%, a level we are comfortable with, considering more than 80% of the portfolio is vehicles financing.

| Corporate & Investment Banking | Credit risk exposure | |||||||||

| 20% of total Group | |||||||||||

Business dedicated to supporting high credit quality wholesale clients (80% of which are rated above investment grade) providing them advisory and high value added solutions.

The NPL ratio stood at 1.14%, -22 bps in the quarter, due to the positive portfolio performance of the Group’s main countries, backed by a credit impaired loans reduction (-11% vs. December 2023). This was supported by the good results obtained in large corporates at the end of the year.

Net loan-loss provisions stood at EUR 40 million compared to net releases in Q1 2023. They improved 81% compared to Q4 2023

| 20 | | January - March 2024 | ||||||

when there were provisions for one-off cases in Brazil. The cost of risk stood at 0.14%.

The coverage ratio of credit impaired loans was 46%, +5 pp in the quarter, which we believe to be an adequate level considering the credit quality of the portfolio.

| Payments | Credit risk exposure | |||||||||

| 2% of total Group | |||||||||||

Includes PagoNxt (one of the largest payment processors and account-to-account direct transfers) which brings together all the Group’s payments businesses and Cards (with about 100 million cards worldwide).

The NPL ratio stood at 4.85% (-18 bps vs. the previous quarter), due to the reduction in impaired loans, which showed a slight improvement in the quarter (-2%), on the back of the positive performance in South America (-2%) and Mexico (-4%). On the other hand, gross credit risk with customers increased 1% compared to Q4 2023.

Net loan-loss provisions, which are mainly in the Cards portfolio, fell 14% year-on-year, driven primarily by Brazil, but picked up 14% compared to Q4 2023. The cost of risk was 6.89%.

The total coverage ratio of credit impaired assets increased by 5 pp in the quarter, remaining at levels we are comfortable with.

Market risk

Focus remained on the central bank meetings. In the quarter, the Fed left the federal funds target rate range unchanged, and the Bank of England and the ECB also held their interest rates. Stock markets rose and market rates have become more volatile driven by expectations of rate cuts by the main central banks.

In Latin America, monetary policy meetings led to interest rate cuts in the quarter as expected in Brazil (-100 bps to 10.75%) and Mexico (-25 bps to 11%). In markets, exchange rates were stable (except for the Chilean peso).

The market risk associated with global corporate banking trading activity is focused on serving the needs of our customers. It is measured in terms of daily VaR at 99% and is mainly produced by possible interest rate movements.

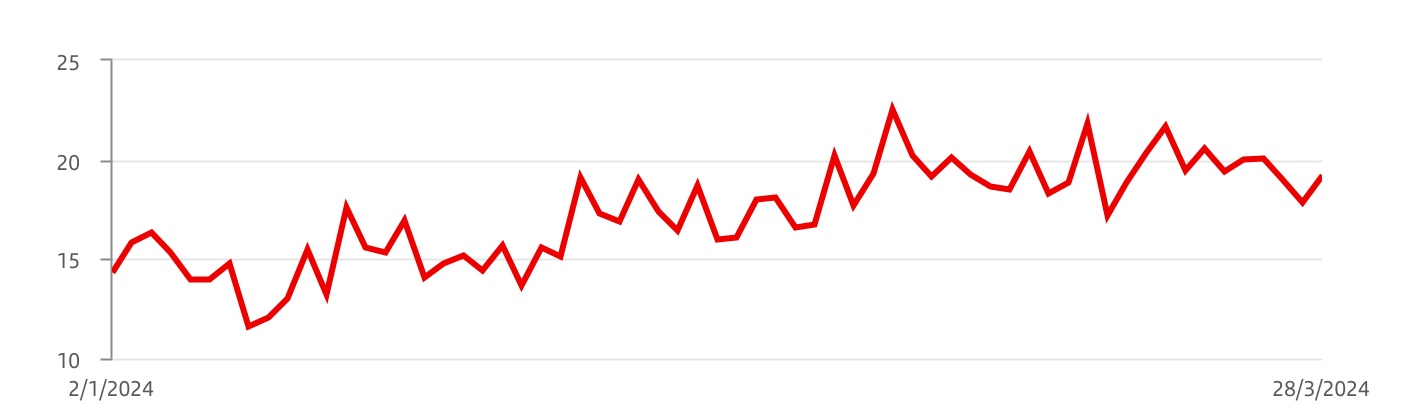

In the first quarter, the average VaR reached a value of EUR 17 million (EUR 4 million more than the previous quarter), due to the persistent geopolitical and macroeconomic tensions. In the second half of the period, VaR experienced a slight rise mainly due to increased exposure to interest rate risk in South America.

By market risk factor, VaR continued to be mostly driven by interest rate risk. These VaR figures remained low compared to the size of the balance sheet and the activity of the Group.

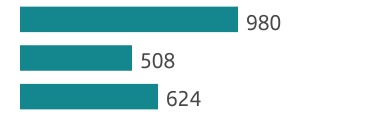

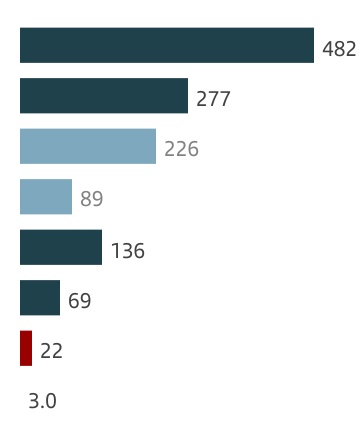

Trading portfolios.1 VaR by geographic region | ||||||||||||||

| EUR million | ||||||||||||||

| 2024 | 2023 | |||||||||||||

| First quarter | Average | Last | Average | |||||||||||

| Total | 17.3 | 19.2 | 11.3 | |||||||||||

| Europe | 12.7 | 11.1 | 9.0 | |||||||||||

| North America | 6.6 | 5.6 | 2.7 | |||||||||||

| South America | 9.3 | 11.9 | 6.6 | |||||||||||

1. Activity performance in Santander Corporate & Investment Banking markets.

Trading portfolios.1 VaR by market factor | ||||||||||||||

| EUR million | ||||||||||||||

| First quarter 2024 | Min. | Avg. | Max. | Last | ||||||||||

| VaR total | 11.6 | 17.3 | 22.5 | 19.2 | ||||||||||

| Diversification effect | (12.9) | (18.5) | (25.4) | (15.9) | ||||||||||

| Interest rate VaR | 11.4 | 17.2 | 23.1 | 18.7 | ||||||||||

| Equity VaR | 2.8 | 4.2 | 6.0 | 3.5 | ||||||||||

| FX VaR | 4.2 | 6.1 | 8.4 | 5.0 | ||||||||||

| Credit spreads VaR | 4.1 | 5.2 | 6.2 | 4.5 | ||||||||||

| Commodities VaR | 2.0 | 3.2 | 4.1 | 3.4 | ||||||||||

1.Activity performance in Santander Corporate & Investment Banking markets.

Note: In the North America, South America and Asia portfolios, VaR corresponding to the credit spreads factor other than sovereign risk is not relevant and is included in the interest rate factor.

Trading portfolios1. VaR performance | ||

| EUR million | ||

January - March 2024 | | 21 | ||||||

Structural and liquidity risk

Structural exchange rate risk: Mainly driven by transactions in foreign currencies related to permanent financial investments, their results and related hedges. Our dynamic management of this risk seeks to limit the impact of foreign exchange rate movements on the CET1 ratio. In the quarter, hedging of currencies impacting this ratio remained close to 100%.