0000891478ifrs-full:WeightedAverageMemberifrs-full:InterestRateSwapContractMembersan:FlowDiscountingMethodOnSwapRateMembersan:SwapRateMeasurementInputMemberifrs-full:FinancialAssetsAtFairValueThroughProfitOrLossClassifiedAsHeldForTradingCategoryMember2024-06-300000891478san:ForborneLoanPortfolioMemberifrs-full:GrossCarryingAmountMemberifrs-full:CreditRiskMembersan:IfrsUncollateralizedMembersan:LoansAndReceivablesMember2023-12-31

FORM 6-K

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Report of Foreign Issuer

Pursuant to Rule 13a-16 or 15d-16

of the Securities Exchange Act of 1934

For the month of July, 2024

Commission File Number: 001-12518

Banco Santander, S.A.

(Exact name of registrant as specified in its charter)

Ciudad Grupo Santander

28660 Boadilla del Monte (Madrid) Spain

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

Form 20-F ☒ Form 40-F ☐

BANCO SANTANDER, S.A.

________________________

TABLE OF CONTENTS

| Part 1 | |||||

| Interim consolidated directors’ report | |||||

| Interim unaudited consolidated financial statements | |||||

| Part 2 | |||||

| Supplemental information | |||||

| Part 1. Interim consolidated directors' report and interim unaudited consolidated financial statements | |||||

| January - June | 2024 | ||||

| Interim consolidated directors' report | ||||||||

| Business model | ||||||||

Corporate governance | ||||||||

| Interim condensed consolidated financial statements | ||||||||

This report was approved by the board of directors on 23 July 2024, following a favourable report from the audit committee. Important information regarding this report can be found on pages 92 and 93.

Key consolidated data

| BALANCE SHEET (EUR million) | Jun-24 | Mar-24 | % | Jun-24 | Jun-23 | % | Dec-23 | ||||||||||||||||

| Total assets | 1,786,261 | 1,800,006 | (0.8) | 1,786,261 | 1,780,493 | 0.3 | 1,797,062 | ||||||||||||||||

| Loans and advances to customers | 1,065,596 | 1,049,533 | 1.5 | 1,065,596 | 1,045,044 | 2.0 | 1,036,349 | ||||||||||||||||

| Customer deposits | 1,037,646 | 1,044,453 | (0.7) | 1,037,646 | 1,013,778 | 2.4 | 1,047,169 | ||||||||||||||||

| Total funds | 1,309,903 | 1,315,779 | (0.4) | 1,309,903 | 1,255,783 | 4.3 | 1,306,942 | ||||||||||||||||

| Total equity | 103,648 | 105,025 | (1.3) | 103,648 | 102,044 | 1.6 | 104,241 | ||||||||||||||||

| Note: total funds includes customer deposits, mutual funds, pension funds and managed portfolios. | |||||||||||||||||||||||

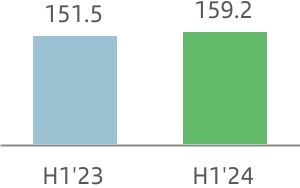

| INCOME STATEMENT (EUR million) | Q2'24 | Q1'24 | % | H1'24 | H1'23 | % | 2023 | ||||||||||||||||

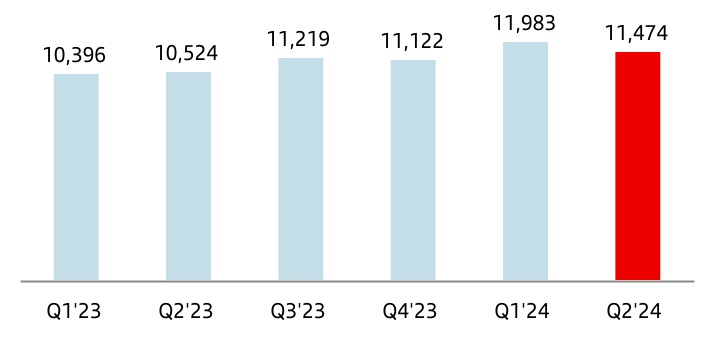

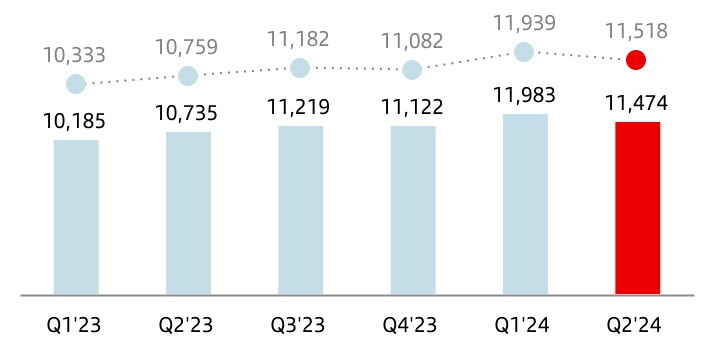

| Net interest income | 11,474 | 11,983 | (4.2) | 23,457 | 20,920 | 12.1 | 43,261 | ||||||||||||||||

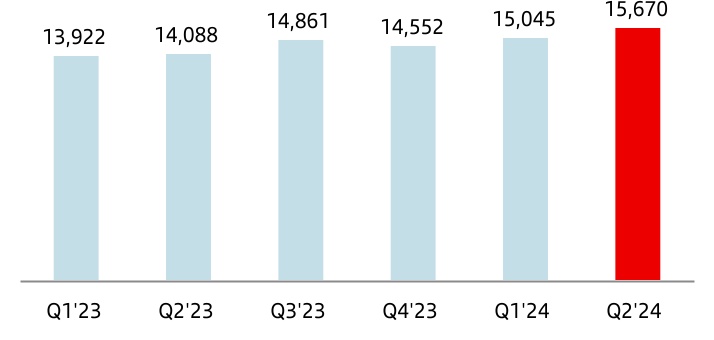

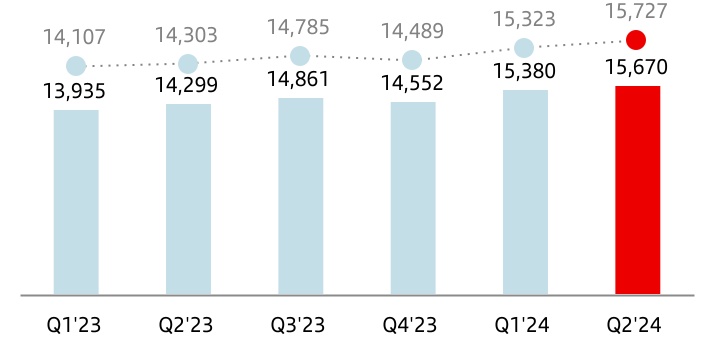

| Total income | 15,670 | 15,045 | 4.2 | 30,715 | 28,010 | 9.7 | 57,423 | ||||||||||||||||

| Net operating income | 9,304 | 8,498 | 9.5 | 17,802 | 15,531 | 14.6 | 31,998 | ||||||||||||||||

| Profit before tax | 4,925 | 4,583 | 7.5 | 9,508 | 8,090 | 17.5 | 16,459 | ||||||||||||||||

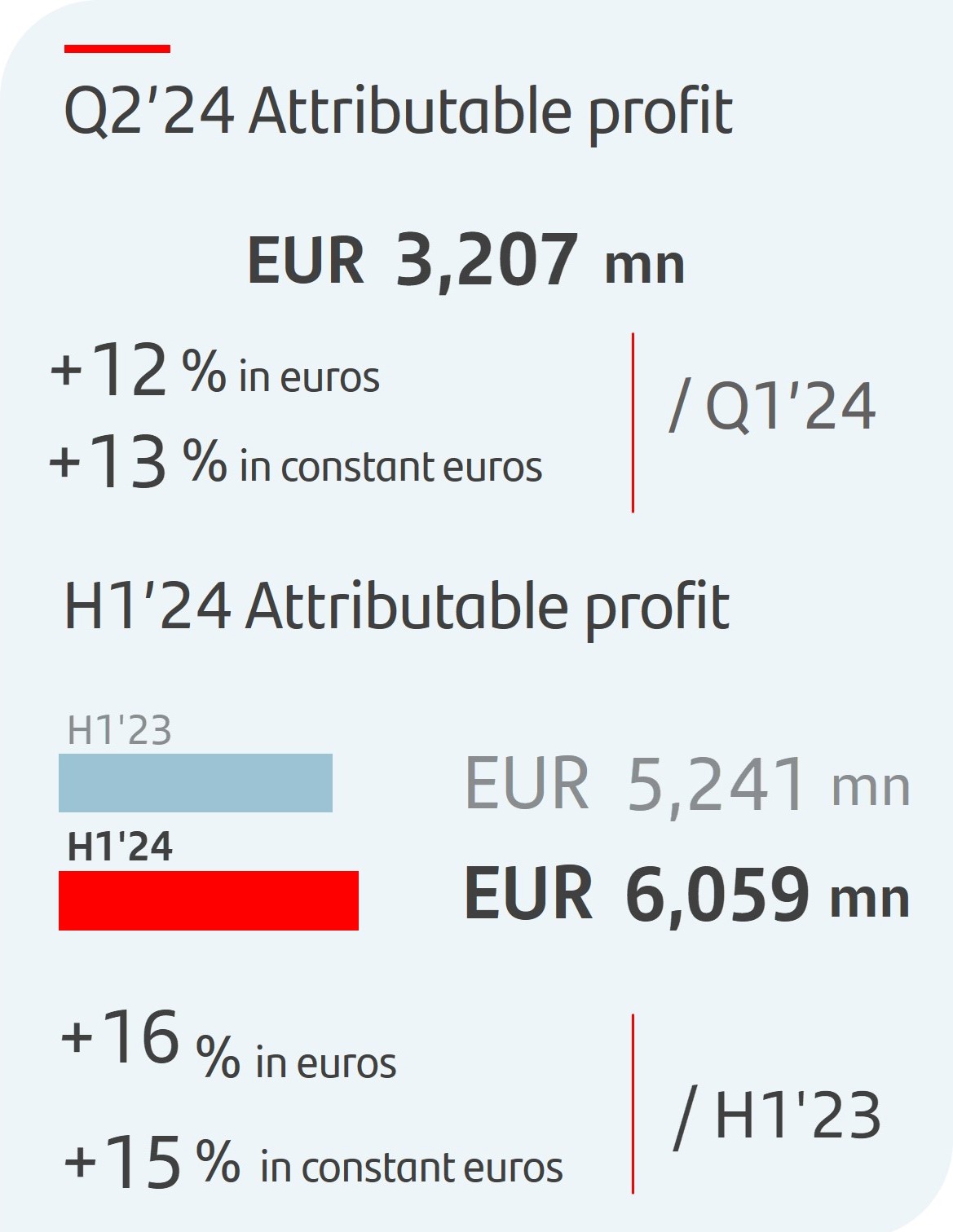

| Profit attributable to the parent | 3,207 | 2,852 | 12.4 | 6,059 | 5,241 | 15.6 | 11,076 | ||||||||||||||||

EPS, PROFITABILITY AND EFFICIENCY (%) 1 | Q2'24 | Q1'24 | % | H1'24 | H1'23 | % | 2023 | ||||||||||||||||

| EPS (euros) | 0.20 | 0.17 | 15.4 | 0.37 | 0.31 | 19.2 | 0.65 | ||||||||||||||||

| RoE | 13.4 | 11.8 | 12.6 | 11.5 | 11.9 | ||||||||||||||||||

| RoTE | 16.8 | 14.9 | 15.9 | 14.5 | 15.1 | ||||||||||||||||||

| RoA | 0.78 | 0.69 | 0.74 | 0.67 | 0.69 | ||||||||||||||||||

| RoRWA | 2.18 | 1.96 | 2.07 | 1.88 | 1.96 | ||||||||||||||||||

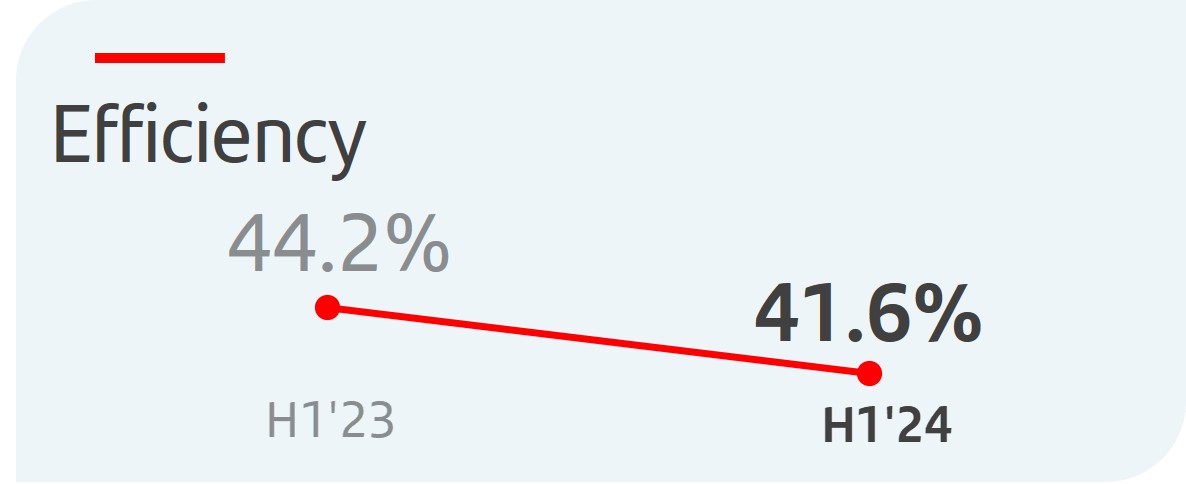

Efficiency ratio 2 | 40.6 | 42.6 | 41.6 | 44.2 | 44.1 | ||||||||||||||||||

UNDERLYING INCOME STATEMENT 2 (EUR million) | Q2'24 | Q1'24 | % | H1'24 | H1'23 | % | 2023 | ||||||||||||||||

| Net interest income | 11,474 | 11,983 | (4.2) | 23,457 | 20,920 | 12.1 | 43,261 | ||||||||||||||||

| Total income | 15,670 | 15,380 | 1.9 | 31,050 | 28,234 | 10.0 | 57,647 | ||||||||||||||||

| Net operating income | 9,304 | 8,833 | 5.3 | 18,137 | 15,755 | 15.1 | 32,222 | ||||||||||||||||

| Profit before tax | 4,925 | 4,583 | 7.5 | 9,508 | 8,329 | 14.2 | 16,698 | ||||||||||||||||

| Profit attributable to the parent | 3,207 | 2,852 | 12.4 | 6,059 | 5,241 | 15.6 | 11,076 | ||||||||||||||||

| Changes in constant euros: | |||||||||||||||||||||||

| Q2'24 / Q1'24: NII: -3.5%; Total income: +2.6%; Net operating income: +6.3%; Profit before tax: +8.2%; Attributable profit: +13.1%. | |||||||||||||||||||||||

| H1'24 / H1'23: NII: +11.2%; Total income: +9.3%; Net operating income: +14.3%; Profit before tax: +13.3%; Attributable profit: +14.7%. | |||||||||||||||||||||||

Note: for Argentina and any grouping which includes it, the variations in constant euros have been calculated considering the Argentine peso exchange rate on the last working day for each of the periods presented. Additionally, from Q2 2024 onwards, a theoretical rate, which differs from official exchange rate, has been used for the Argentine peso as it better reflects the evolution of inflation (we continue to apply the official ARS exchange rate to all prior periods). For further information, see the section 'Alternative performance measures' in the appendix to this report. | ||

January - June 2024 |  | 3 | ||||||

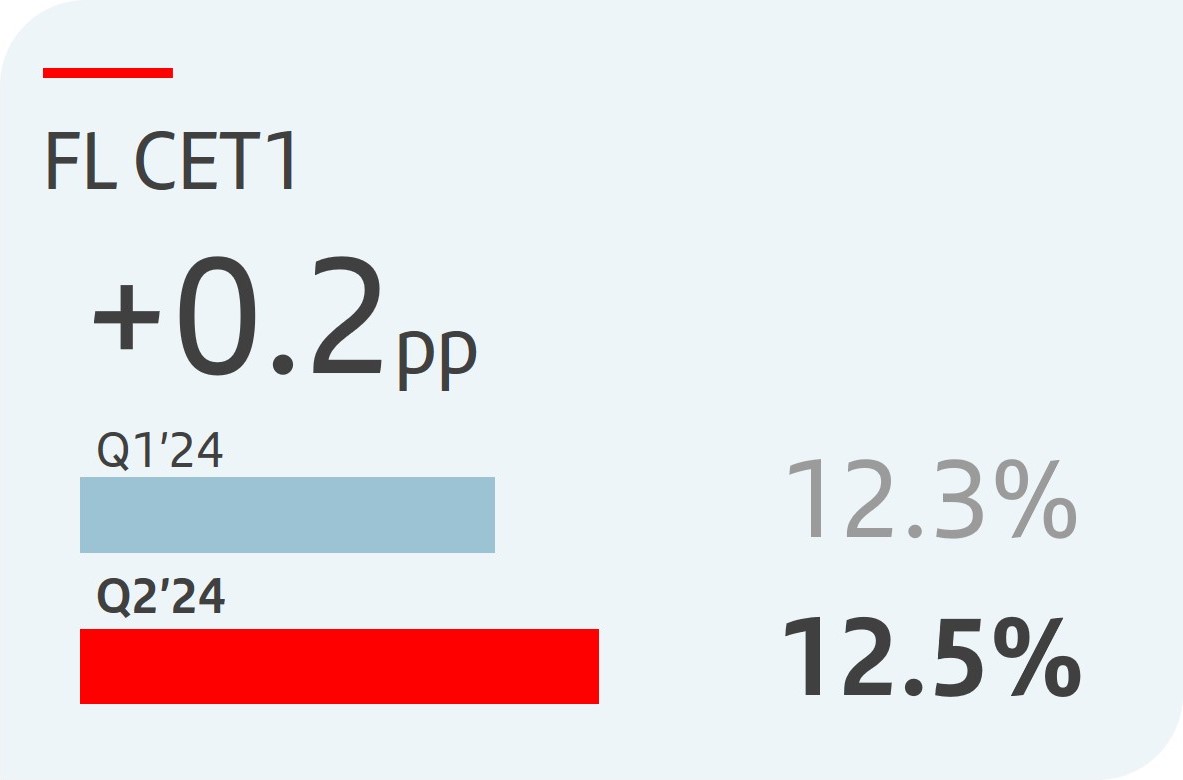

| SOLVENCY (%) | Jun-24 | Mar-24 | Jun-24 | Jun-23 | Dec-23 | ||||||||||||||||||

| Fully-loaded CET1 ratio | 12.5 | 12.3 | 12.5 | 12.2 | 12.3 | ||||||||||||||||||

| Fully-loaded total capital ratio | 16.4 | 16.5 | 16.4 | 15.9 | 16.3 | ||||||||||||||||||

| CREDIT QUALITY (%) | Q2'24 | Q1'24 | H1'24 | H1'23 | 2023 | ||||||||||||||||||

Cost of risk 2, 3 | 1.21 | 1.20 | 1.21 | 1.08 | 1.18 | ||||||||||||||||||

| NPL ratio | 3.02 | 3.10 | 3.02 | 3.07 | 3.14 | ||||||||||||||||||

| NPL coverage ratio | 66 | 66 | 66 | 68 | 66 | ||||||||||||||||||

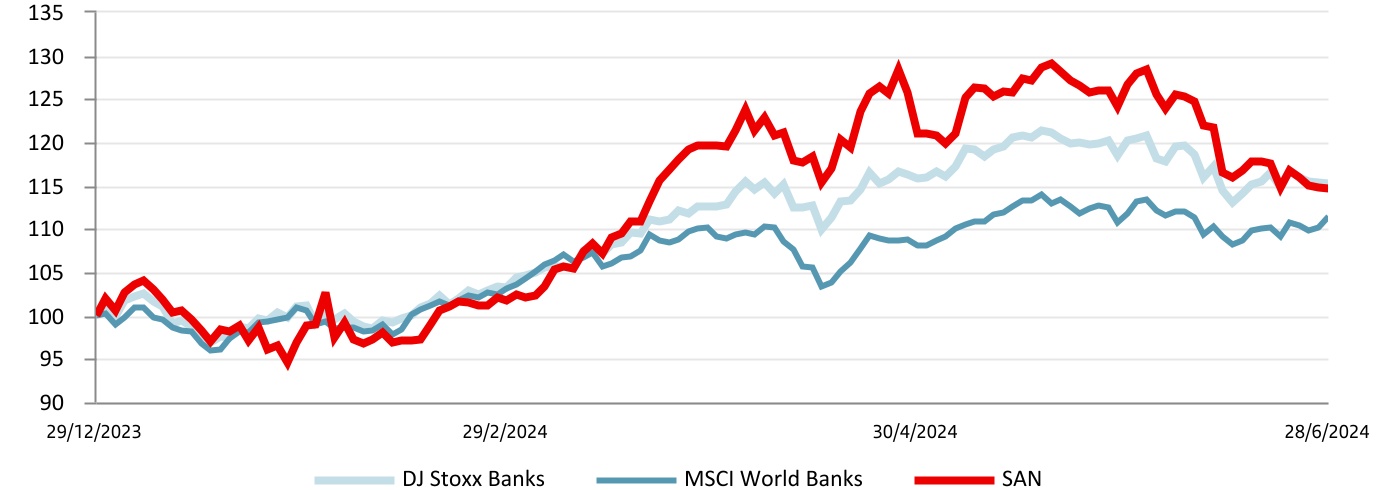

| MARKET CAPITALIZATION AND SHARES | Jun-24 | Mar-24 | % | Jun-24 | Jun-23 | % | Dec-23 | ||||||||||||||||

| Shares (millions) | 15,494 | 15,826 | (2.1) | 15,494 | 16,184 | (4.3) | 16,184 | ||||||||||||||||

| Share price (euros) | 4.331 | 4.522 | (4.2) | 4.331 | 3.385 | 27.9 | 3.780 | ||||||||||||||||

| Market capitalization (EUR million) | 67,098 | 71,555 | (6.2) | 67,098 | 54,783 | 22.5 | 61,168 | ||||||||||||||||

| Tangible book value per share (euros) | 4.94 | 4.86 | 4.94 | 4.57 | 4.76 | ||||||||||||||||||

| Price / Tangible book value per share (X) | 0.88 | 0.93 | 0.88 | 0.74 | 0.79 | ||||||||||||||||||

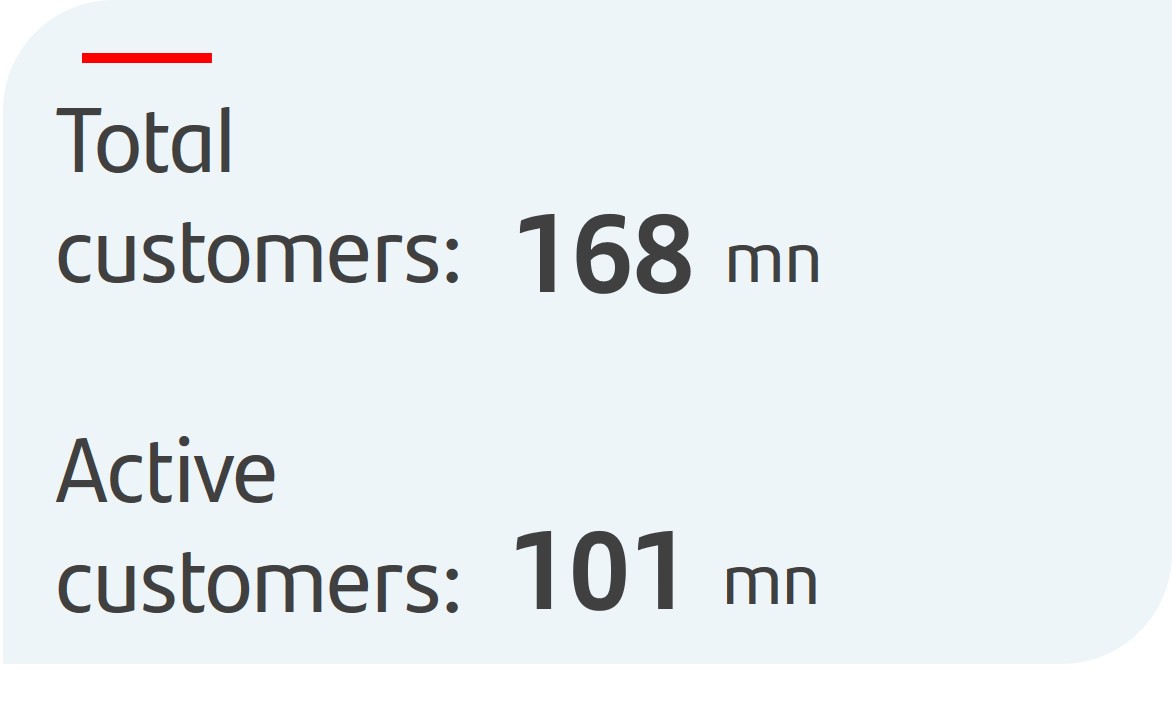

| CUSTOMERS (thousands) | Q2'24 | Q1'24 | % | H1'24 | H1'23 | % | 2023 | ||||||||||||||||

| Total customers | 168,243 | 165,752 | 1.5 | 168,243 | 163,756 | 2.7 | 164,542 | ||||||||||||||||

| Active customers | 101,277 | 100,092 | 1.2 | 101,277 | 99,472 | 1.8 | 99,503 | ||||||||||||||||

| Digital customers | 57,000 | 55,305 | 3.1 | 57,000 | 52,517 | 8.5 | 54,161 | ||||||||||||||||

| OTHER DATA | Jun-24 | Mar-24 | % | Jun-24 | Jun-23 | % | Dec-23 | ||||||||||||||||

| Number of shareholders | 3,526,649 | 3,584,294 | (1.6) | 3,526,649 | 3,802,161 | (7.2) | 3,662,377 | ||||||||||||||||

| Number of employees | 209,553 | 211,141 | (0.8) | 209,553 | 212,410 | (1.3) | 212,764 | ||||||||||||||||

| Number of branches | 8,285 | 8,405 | (1.4) | 8,285 | 8,823 | (6.1) | 8,518 | ||||||||||||||||

| 1. | For further information, see the section 'Alternative performance measures' in the appendix to this report. | ||||

| 2. | In addition to financial information prepared in accordance with International Financial Reporting Standards (IFRS) and derived from our consolidated financial statements, this report contains certain financial measures that constitute alternative performance measures (APMs) as defined in the Guidelines on Alternative Performance Measures issued by the European Securities and Markets Authority (ESMA) on 5 October 2015, and other non-IFRS measures, including the figures related to “underlying” results, which do not include factors that are outside the ordinary course of our business, or have been reclassified within the underlying income statement. Further details are provided in the 'Alternative performance measures' section of the appendix to this report. For further details on the APMs and non-IFRS measures used, including their definition or a reconciliation between any applicable management indicators and the financial data presented in the annual consolidated financial statements prepared under IFRS, please see our 2023 Annual Financial Report, published in the CNMV on 19 February 2024, our 20-F report for the year ending 31 December 2023 filed with the SEC in the United States on 21 February 2024 as well as the 'Alternative performance measures' section of the appendix to this report. | ||||

| 3. | Allowances for loan-loss provisions over the last 12 months / Average loans and advances to customers over the last 12 months. | ||||

| 4 | | January - June 2024 | ||||||

| Group financial information | Financial information by segment | Responsible banking Corporate governance Santander share | Appendix | ||||||||||||||||||||||||||

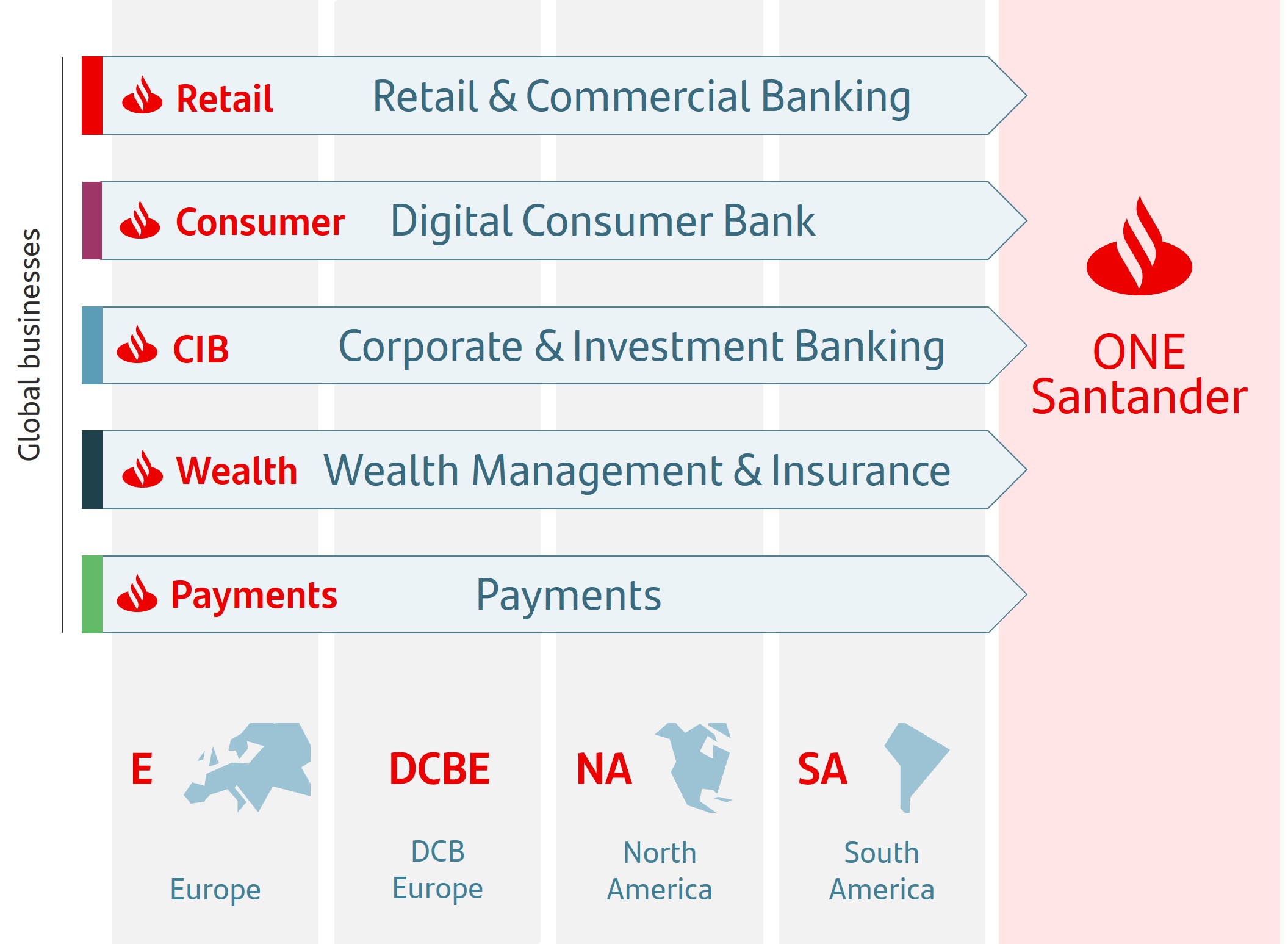

Our business model

| Customer focus | ||||||||||||||||||||||||||

| Building a digital bank with branches | → New operating model to build a digital bank with branches, with a multichannel offer to fulfil all our customers' financial needs. | 168 mn | 101 mn | |||||||||||||||||||||||

| total customers | active customers | |||||||||||||||||||||||||

| Scale | ||||||||||||||||||||||||||

→ Our global and in-market scale helps us to improve our local banks' profitability, adding value and network benefits. → Our activities are organized under five global businesses: Retail & Commercial Banking (Retail), Digital Consumer Bank (Consumer), Corporate & Investment Banking (CIB), Wealth Management & Insurance (Wealth) and Payments. → Our five global businesses and our presence in Europe, DCB Europe, North America and South America support value creation based on the profitable growth and operational leverage that ONE Santander provides. | ||||||||||||||||||||||||||

| Global and in-market scale |  | |||||||||||||||||||||||||

| Diversification | ||||||||||||||||||||||||||

| Business, geographical and balance sheet | → Well-balanced diversification between businesses and markets with a solid and simple balance sheet that gives us recurrent net operating income with low volatility and more predictable results. | |||||||||||||||||||||||||

Our corporate culture

The Santander Way remains unchanged to continue to deliver for all our stakeholders

Our purpose To help people and businesses prosper. |  | ||||||||||

Our aim To be the best open financial services platform, by acting responsibly and earning the lasting loyalty of our people, customers, shareholders and communities. | |||||||||||

Our how Everything we do should be Simple, Personal and Fair. | |||||||||||

January - June 2024 | | 5 | ||||||

Group financial information

General background

In H1 2024, Santander operated in an environment characterized by a gentle global economic slowdown, with relatively stable interest rates and a gradual decline in inflation in most regions. Geopolitical tensions, while still present, have not resulted in significant economic impacts. Labour markets withstood the monetary tightening period, with unemployment rates at or close to full employment across most of Santander's footprint.

| Country | GDP Change1 | Economic performance | |||||||||

| Eurozone | +0.4% | Having stagnated in 2023, the economy has entered a phase of soft recovery driven by external demand. Inflation continued to moderate (+2.5% year-on-year in June), which allowed for a 25 bp interest rate cut in June. The ECB is expected to make further interest rate cuts in the second half of the year, but it will depend on whether inflation continues to approach the ECB's target. | ||||||||

| Spain | +2.5% | In Q1 2024, GDP grew 2.5% year-on-year, supported by strong exports of services, while investment remained below pre-pandemic levels. The labour market remains strong, with the number of people enrolled in social security at record levels. In June, inflation was rose 3.4% year-on-year, while core inflation remained at 3%, due to persistently high inflation in services sector. | ||||||||

| United Kingdom | +0.3% | The economy grew in Q1 2024, ending the technical recession that began in H2 2023. The outlook has also improved, with increased business and consumer confidence and real wage growth. The unemployment rate remained low, although it increased to 4.4% in April. Inflation continues to decline (2.0% year-on-year in June) due to lower food prices. Inflationary pressures on wages and services led the Bank of England to hold the official interest rate at 5.25%. | ||||||||

| Portugal | +1.5% | Growth in Q1 2024 surprised positively due to the contribution from external demand. On the other hand, the contribution from domestic demand decreased, due to the slowdown in investment and private consumption. Labour market data remained strong with employment rising and unemployment at low levels (6.5% in May). After moderating in recent months, inflation rose slightly in June (2.8% year-on-year). | ||||||||

| Poland | +2.0% | In Q1 2024, GDP rose supported by private consumption. Supply constraints in the labour market and resilient labour demand kept the unemployment rate low (4.9% in June), supporting higher wages (+11.4% year-on-year in May). Inflation is within the central bank’s target range (2.6% year-on-year in June). However, core inflation remained high (+3.8% year-on-year in May) and, as such, the central bank decided to hold interest rates at 5.75%. | ||||||||

| United States | +2.9% | Domestic demand grew at a good pace in Q1 2024, but private consumption showed signs of slowdown in Q2 2024. The unemployment rate rose to 4.1% in June. Inflation, which had increased in Q1 2024, has since declined (3.0% year-on-year in June). | ||||||||

| Mexico | +1.6% | After having started the year with slight growth, the economy is now showing signs of weakening, though the labour market remains resilient. Year-on-year inflation rebounded to 5.0% in June. After a first 25 bp interest rate cut in Q1 2024, the central bank held interest rates at 11% in Q2 2024. | ||||||||

| Brazil | +2.5% | The economy recovered dynamism in early 2024, driven by private consumption, investment and a strong labour market. Year-on-year inflation rebounded to 4.2% in June and medium-term expectations rose, moving away from the target. Following the latest interest rate cut in May (-25 bps to 10.5%), the central bank held interest rates in June. | ||||||||

| Chile | +2.3% | After a weak 2023, the economy is recovering with growth in mining, industry and services sectors. Inflation rose slightly to 4.2% year-on-year in June. The central bank continued its process of rapid interest rate cuts, with a 150 bp reduction in Q2 2024 to 5.75%, though it said that interest rate cuts will slow down. | ||||||||

| Argentina | -5.1% | The economy remained weak at the beginning of the year, due to the impact of the fiscal and monetary adjustments and high inflation, although inflation has moderated faster than expected as the year has progressed (down to a monthly average of 5.9% during Q2 2024). The external sector is showing signs of recovery, with increases in exports and trade surpluses, in contrast to the 2023 deficit. | ||||||||

1.Year-on-year changes for Q1'24.

| 6 | | January - June 2024 | ||||||

Highlights of the period

Main figures | |||||||||||

| u | In Q2 2024, profit attributable to the parent was EUR 3,207 million, a new record quarter, despite charges totalling EUR 452 million (provisions relating to our CHF mortgage portfolio in Poland and write-downs after discontinuing our merchant platform in Germany and Superdigital in Latin America). | |||||||||

| u | Attributable profit was 12% higher compared to Q1 2024 (+13% in constant euros), mainly driven by the good performance in Retail, Consumer and Wealth, and after having recorded the temporary levy on revenue obtained in Spain in Q1 2024 and the aforementioned charges in Q2 2024. | ||||||||||

| u | Attributable profit increased 20% (in both euros and constant euros) compared to Q2 2023, with Retail, Wealth and Consumer growing. No contribution to the Single Resolution Fund (SRF) has been recorded in 2024, as contributions ended in 2023. | ||||||||||

| u | In H1 2024, attributable profit was EUR 6,059 million, 16% higher than in the same period of 2023 (+15% in constant euros) boosted by solid revenue growth across all global businesses and regions. | ||||||||||

| u | These positive results enabled us to improve the targets we had set for the year in revenue (from mid-single digit growth to high-single digit growth), efficiency (from less than 43% to close to 42%) and profitability (from 16% RoTE to more than 16%), while maintaining our objectives in capital and cost of risk. | ||||||||||

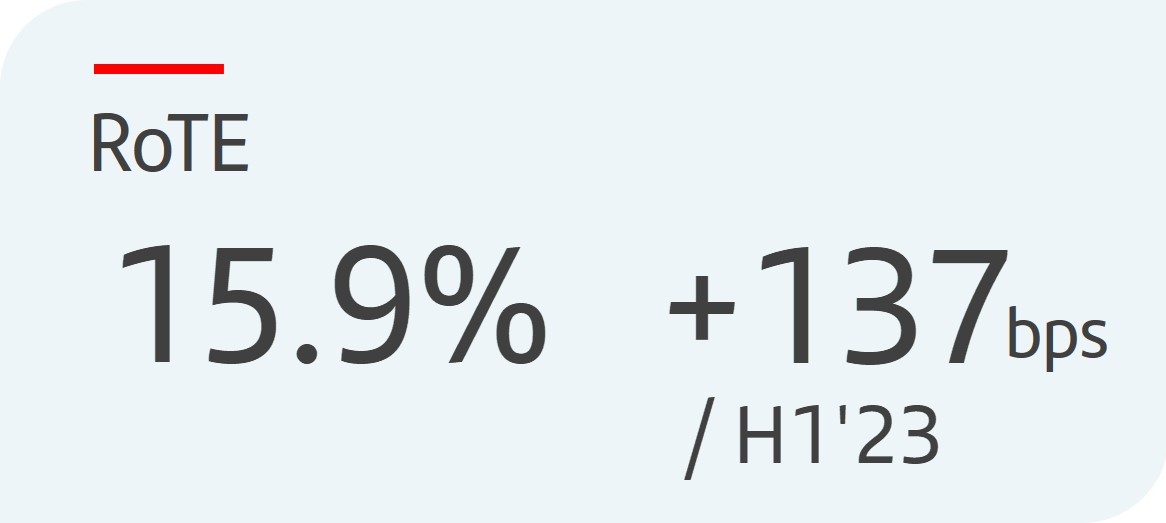

| u | Profitability improved year-on-year and quarter-on-quarter. RoTE stood at 15.9% in H1 2024, compared to 14.5% in the same period of 2023. Annualizing the impact of the temporary levy on revenue obtained in Spain, RoTE was 16.3%, boosted by strong revenue growth. | |||||||||

| u | Sustained earnings per share growth in H1 2024, which rose 19% compared to H1 2023 to EUR 36.7 cents, supported by the positive performance in results and the share buybacks in the last 12 months. | ||||||||||

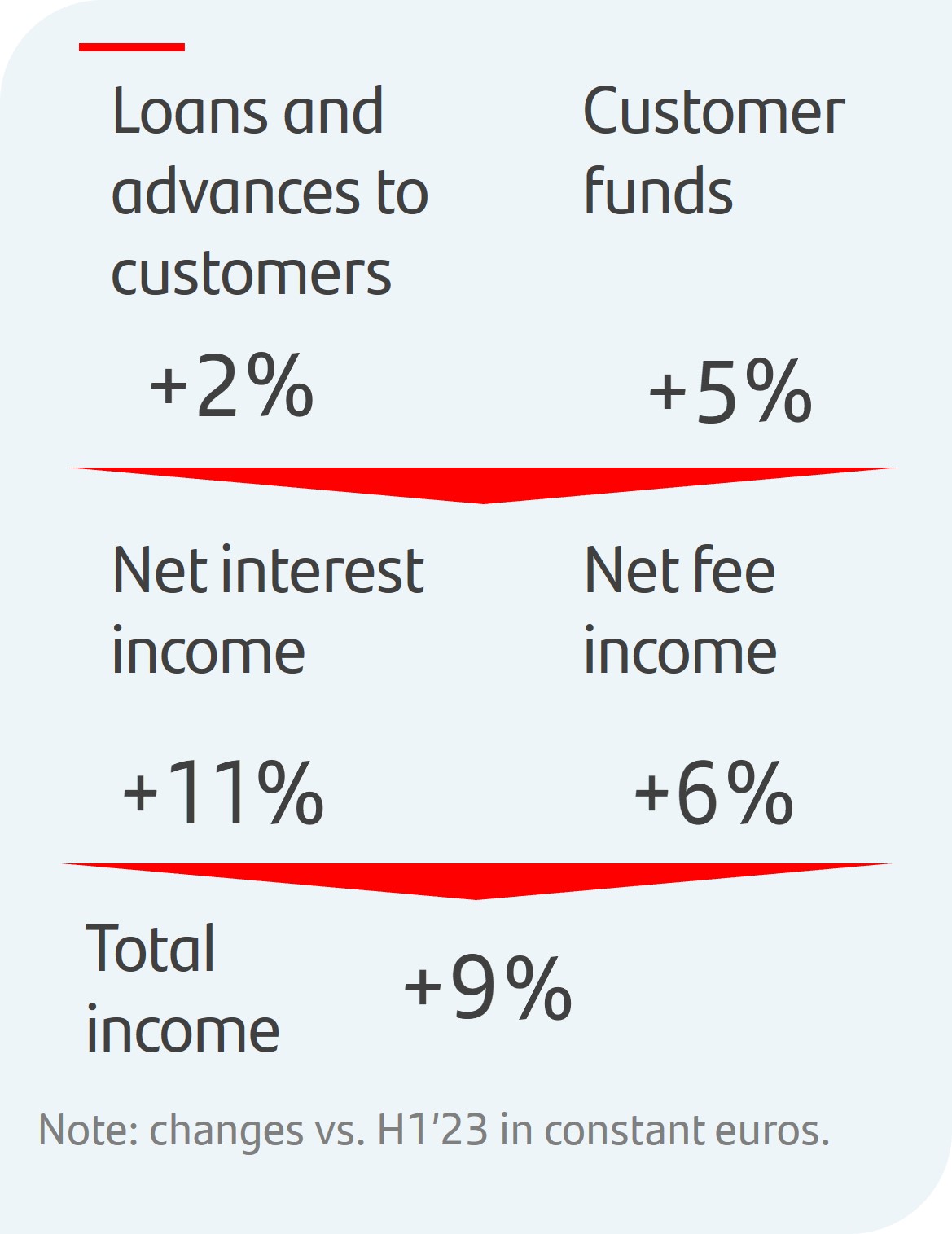

| u | Business volumes continued to reflect the impact that the economic and interest rate environment had on customer behaviour and our active and disciplined capital management. Gross loans and advances to customers (excluding reverse repos) increased 2% year-on-year in constant euros, with all businesses growing except Retail, which decreased slightly as higher volumes in South America and Mexico largely offset lower loans in Europe and the US. Customer funds (customer deposits excluding repurchase agreements plus mutual funds) rose 5% year-on-year in constant euros, with deposits growing across all businesses except CIB (lower volumes in Spain and the US), while mutual funds rose double digits. | |||||||||

| u | The benefits from our global scale, margin management and higher customer activity were reflected in year-on-year increases in net interest income (+12% in euros, +11% in constant euros) and net fee income (+6% both in euros and constant euros), resulting in total income growth of 10% in euros (+9% in constant euros). | ||||||||||

| u | Structural changes towards a simpler and more integrated model through ONE Transformation are contributing to efficiency gains and profitable growth. The efficiency ratio improved 2.6 pp compared to H1 2023 to 41.6%, driven mainly by Retail and Consumer. | |||||||||

| u | Credit quality remains robust, driven by the strong macroeconomic environment and employment across our footprint. The NPL ratio was 3.02%, improving 5 bps year-on-year. Total loan-loss reserves reached EUR 23,323 million, resulting in a total coverage ratio of 66%. | |||||||||

| u | The Group's cost of risk stood at 1.21% (1.18% in December 2023 and 1.08% in June 2023), in line with our expectations. Retail and Consumer accounted for 85% of Group's net loan-loss provisions. In Retail, the cost of risk remained under control at 1.03%. In Consumer, CoR continued to normalize (to 2.17%) and remained at controlled levels and in line with expectations. | ||||||||||

| u | As at end June 2024, the fully-loaded CET1 ratio stood at 12.5%. In the quarter, we generated 52 bps organically, including a 7 bp positive contribution from RWAs, as RWA growth was more than offset by significant risk transfer and asset rotation initiatives. We also recorded a 25 bp charge for shareholder remuneration against profit earned in Q2 2024 in line with our 50% payout target1. Additionally, we recorded charges of -7 bps relating to deductions, mainly intangible assets and held to collect and sell portfolio valuations. There were no significant regulatory charges in the quarter. | |||||||||

1.In line with the current shareholder remuneration policy of approximately 50% of the Group's reported profit (excluding non-cash, non-capital ratios impact items), divided approximately equally between cash dividends and share repurchases. Execution of the shareholder remuneration policy is subject to future corporate and regulatory decisions and approvals.

January - June 2024 | | 7 | ||||||

| Think Value | |||||||

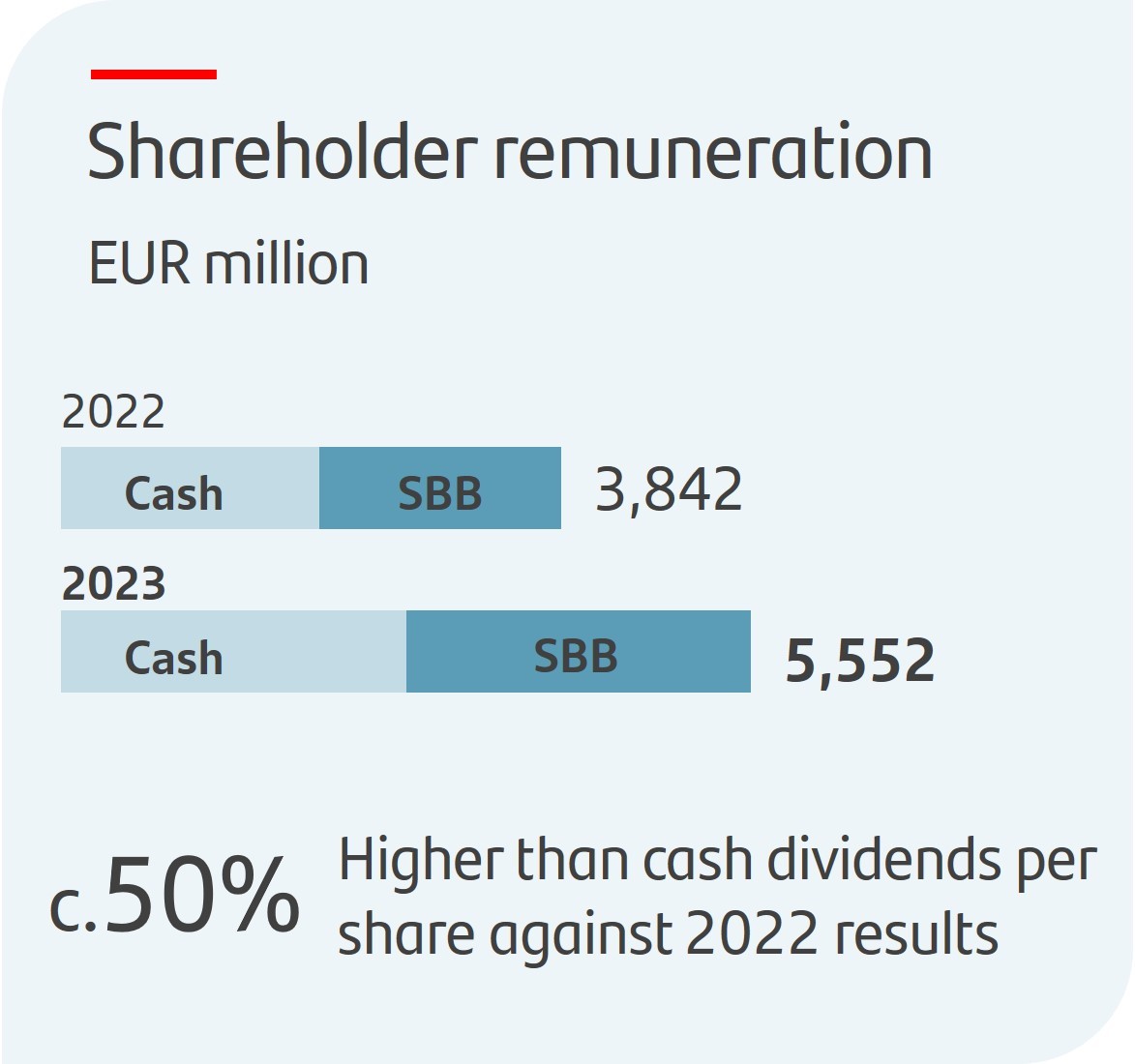

| u | The AGM approved a cash dividend of EUR 9.50 cents per share that was paid in May. Including the cash dividend per share paid in November 2023 (EUR 8.10 cents), the total cash dividend per share paid against 2023 results was EUR 17.60 cents, around 50% more than the dividends per share paid against 2022 results. | |||||||||

| u | In addition to this payment, there were two share buyback programmes which have been completed for a total of EUR 2,769 million. Including purchases made under such buyback programmes, the Group has repurchased c.11% of its outstanding shares since we began our buybacks in 2021. | ||||||||||

| u | Total shareholder remuneration against 2023 results totalled EUR 5,552 million, 45% higher than the remuneration against 2022 results, distributed approximately equally between cash dividends and share buybacks. | ||||||||||

| |||||||||||

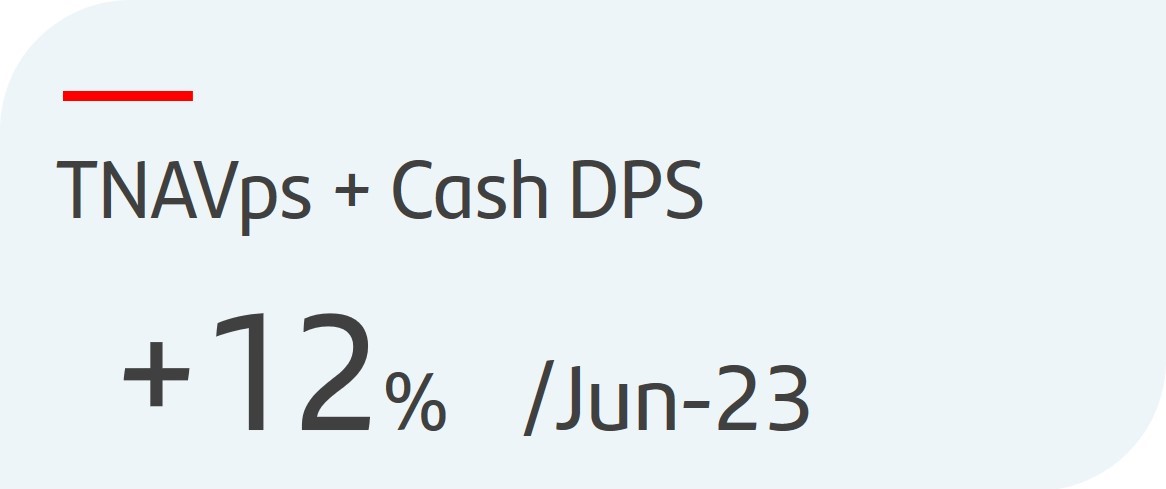

| u | As at end June 2024, TNAV per share was EUR 4.94. Including both cash dividends charged against 2023 results, the TNAV per share + cash dividend per share increased 12% year-on-year. | ||||||||||

| Think Customer | |||||||

| u | Our efforts to simplify and improve our product offering and quality of service were reflected in a more than 4 million year-on-year increase in total customers to 168 million, while active customers reached 101 million, up almost 2 million year-on-year. | |||||||||

| u | Transaction volumes per active customer rose 9% year-on-year in H1 2024. | ||||||||||

| u | We continue to deliver great customer experience and improve our service quality, ranking in the top 3 in NPS1 in seven of our markets. | ||||||||||

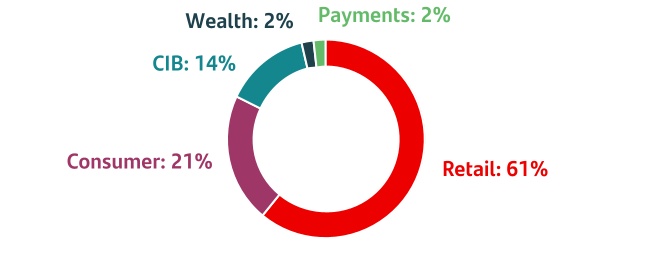

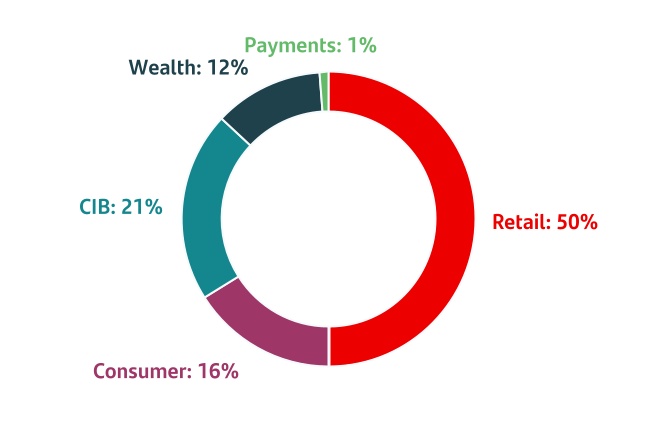

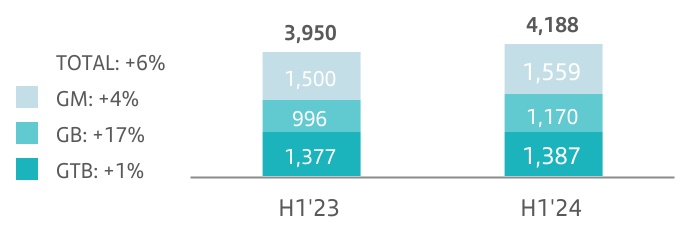

| Think Global | |||||||

Contribution to Group revenue2 | Year-on-year changes in constant euros | |||||||||||||

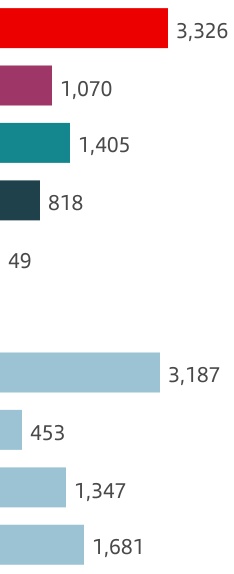

| u | In Retail, attributable profit was EUR 3,326 million (+35%) driven by double-digit growth in total income and the good performance in costs (due to our transformation efforts) and provisions. | ||||||||||||

| u | Efficiency improved 4.8 pp to 39.5%, cost of risk remained controlled (1.03%) and RoTE increased to 17.4% (18.1% annualizing the impact of the temporary levy). | |||||||||||||

| u | In Consumer, net operating income increased 12%, supported by total income growth (+7%) and good cost management, reaching an attributable profit of EUR 1,070 million, (+4%) despite higher LLPs (CHF mortgages, cost of risk normalization, higher volumes and some regulatory impacts). | ||||||||||||

| u | Efficiency stood at 40.6%, improving 2.7 pp, cost of risk was 2.17% and RoTE stood at 12.8% (13.0% annualizing the impact of the temporary levy). | |||||||||||||

| u | In CIB, revenue continued to grow, reaching record figures for H1 2024. However, attributable profit (EUR 1,405 million), declined 5%, impacted by costs relating to our transformation investments and lower gains on financial transactions in Brazil. | ||||||||||||

| u | The efficiency ratio was 43.4%, remaining one the best in the sector. RoTE was 19.0% (19.1% annualizing the impact of the temporary levy). | |||||||||||||

| u | In Wealth, attributable profit amounted to EUR 818 million (+14%) driven by higher activity and margin management, boosted especially by Private Banking. | ||||||||||||

| u | Efficiency improved 2.3 pp to 34.4% and RoTE was 79.3% (80.4% annualizing the impact of the temporary levy). | |||||||||||||

| u | In Payments, attributable profit reached EUR 49 million, impacted by write-downs in PagoNxt related to the discontinuation of our merchant platform in Germany and Superdigital in Latin America. Excluding it, profit would be 30% higher than in H1 2023, due to revenue growth and lower LLPs. | ||||||||||||

| u | Cost of risk slightly improved 8 bps to 7.03%. In PagoNxt, EBITDA margin was 20.1% (+8.9 pp year-on-year). | |||||||||||||

1.Net Promoter Score, internal benchmark of individual customers' satisfaction audited by Stiga/Deloitte in H1 2024.

2.As % of total operating areas, excluding the Corporate Centre.

| 8 | | January - June 2024 | ||||||

Grupo Santander results

| Grupo Santander. Summarized income statement | ||||||||||||||||||||||||||

| EUR million | ||||||||||||||||||||||||||

| Change | Change | |||||||||||||||||||||||||

| Q2'24 | Q1'24 | % | H1'24 | H1'23 | % | |||||||||||||||||||||

| Net interest income | 11,474 | 11,983 | (4.2) | 23,457 | 20,920 | 12.1 | ||||||||||||||||||||

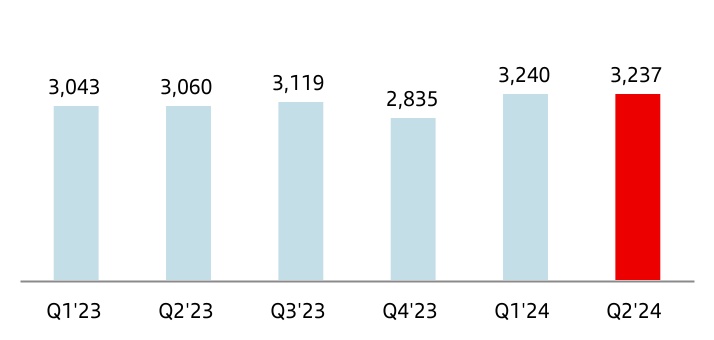

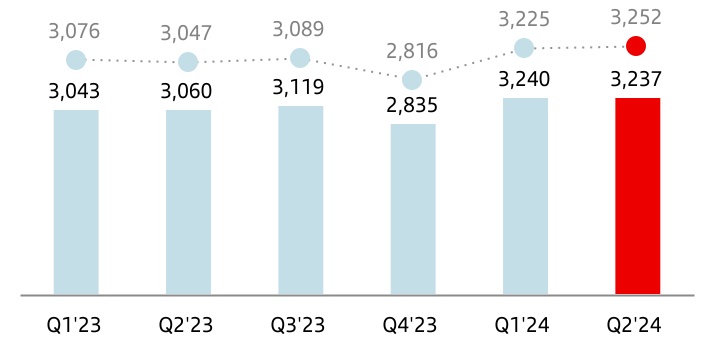

Net fee income1 | 3,237 | 3,240 | (0.1) | 6,477 | 6,103 | 6.1 | ||||||||||||||||||||

Gains or losses on financial assets and liabilities and exchange differences2 | 334 | 623 | (46.4) | 957 | 1,302 | (26.5) | ||||||||||||||||||||

| Dividend income | 400 | 93 | 330.1 | 493 | 382 | 29.1 | ||||||||||||||||||||

| Share of results of entities accounted for using the equity method | 180 | 123 | 46.3 | 303 | 296 | 2.4 | ||||||||||||||||||||

Other operating income/expenses3 (net) | 45 | (1,017) | — | (972) | (993) | (2.1) | ||||||||||||||||||||

| Total income | 15,670 | 15,045 | 4.2 | 30,715 | 28,010 | 9.7 | ||||||||||||||||||||

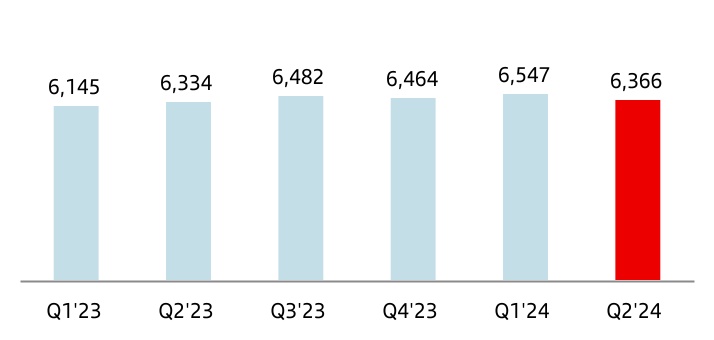

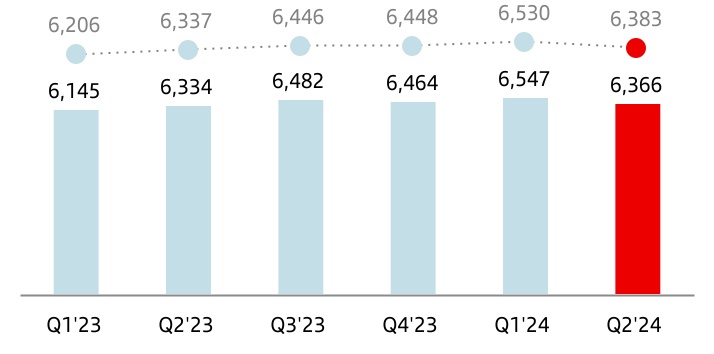

| Operating expenses | (6,366) | (6,547) | (2.8) | (12,913) | (12,479) | 3.5 | ||||||||||||||||||||

| Administrative expenses | (5,538) | (5,719) | (3.2) | (11,257) | (10,873) | 3.5 | ||||||||||||||||||||

| Staff costs | (3,467) | (3,594) | (3.5) | (7,061) | (6,603) | 6.9 | ||||||||||||||||||||

| Other general administrative expenses | (2,071) | (2,125) | (2.5) | (4,196) | (4,270) | (1.7) | ||||||||||||||||||||

| Depreciation and amortization | (828) | (828) | 0.0 | (1,656) | (1,606) | 3.1 | ||||||||||||||||||||

| Provisions or reversal of provisions | (1,129) | (633) | 78.4 | (1,762) | (1,330) | 32.5 | ||||||||||||||||||||

| Impairment or reversal of impairment of financial assets not measured at fair value through profit or loss (net) | (3,443) | (3,134) | 9.9 | (6,577) | (6,237) | 5.5 | ||||||||||||||||||||

| Impairment on other assets (net) | (161) | (129) | 24.8 | (290) | (92) | 215.2 | ||||||||||||||||||||

| Gains or losses on non-financial assets and investments, net | 364 | 2 | — | 366 | 277 | 32.1 | ||||||||||||||||||||

| Negative goodwill recognized in results | — | — | — | — | — | — | ||||||||||||||||||||

| Gains or losses on non-current assets held for sale not classified as discontinued operations | (10) | (21) | (52.4) | (31) | (59) | (47.5) | ||||||||||||||||||||

| Profit or loss before tax from continuing operations | 4,925 | 4,583 | 7.5 | 9,508 | 8,090 | 17.5 | ||||||||||||||||||||

| Tax expense or income from continuing operations | (1,448) | (1,468) | (1.4) | (2,916) | (2,281) | 27.8 | ||||||||||||||||||||

| Profit from the period from continuing operations | 3,477 | 3,115 | 11.6 | 6,592 | 5,809 | 13.5 | ||||||||||||||||||||

| Profit or loss after tax from discontinued operations | — | — | — | — | — | — | ||||||||||||||||||||

| Profit for the period | 3,477 | 3,115 | 11.6 | 6,592 | 5,809 | 13.5 | ||||||||||||||||||||

| Profit attributable to non-controlling interests | (270) | (263) | 2.7 | (533) | (568) | (6.2) | ||||||||||||||||||||

| Profit attributable to the parent | 3,207 | 2,852 | 12.4 | 6,059 | 5,241 | 15.6 | ||||||||||||||||||||

| EPS (euros) | 0.20 | 0.17 | 15.4 | 0.37 | 0.31 | 19.2 | ||||||||||||||||||||

| Diluted EPS (euros) | 0.20 | 0.17 | 15.4 | 0.37 | 0.31 | 19.2 | ||||||||||||||||||||

| Memorandum items: | ||||||||||||||||||||||||||

| Average total assets | 1,780,522 | 1,804,334 | (1.3) | 1,792,428 | 1,754,207 | 2.2 | ||||||||||||||||||||

| Average stockholders' equity | 95,994 | 96,308 | (0.3) | 96,151 | 91,368 | 5.2 | ||||||||||||||||||||

| Note: the summarized income statement groups some lines of the consolidated statutory income statement on page 90 as follows: | |||||

1.‘Commission income’ and ‘Commission expense’. | |||||

2.‘Gain or losses on financial assets and liabilities not measured at fair value through profit or loss, net’; ‘Gain or losses on financial assets and liabilities held for trading, net’; ‘Gains or losses on non-trading financial assets and liabilities mandatorily at fair value through profit or loss’; ‘Gain or losses on financial assets and liabilities measured at fair value through profit or loss, net’; ‘Gain or losses from hedge accounting, net’; and ‘Exchange differences, net’. | |||||

3.‘Other operating income’; ‘Other operating expenses’; ’Income from insurance and reinsurance contracts’; and ‘Expenses from insurance and reinsurance contracts’. | |||||

January - June 2024 | | 9 | ||||||

| Statutory income statement | ||||||||||||||||||||||||||||||||||||||

Results performance compared to H1 2023

In Q2 2024, profit attributable to the parent totalled EUR 3,207 million, reaching a new quarterly record, despite incorporating charges of EUR 452 million net of tax and minority interests: EUR 209 million related to higher provisions for our CHF mortgage portfolio in Poland (in Retail and Consumer), which brings the current ratio of these on-balance sheet assets to provisions to 100%; and EUR 243 million from write-downs in PagoNxt related to the discontinuation of our merchant platform in Germany (to focus on our core markets) and Superdigital in Latin America (in line with our strategy to promote the use of our common platforms across the Group to maximize operational leverage and provide the best service, while increasing access to banking services in the mass segment).

Additionally, from Q2 2024 onwards, a theoretical exchange rate has been used for the Argentine peso. For further information, see the 'Alternative performance measures' section in the appendix to this report.

Profit attributable to the parent amounted to EUR 6,059 million in H1 2024, compared to EUR 5,241 million in the same period in 2023, 16% higher year-on-year. This increase is due to the good performance of total income, which grew at a much faster pace than operating expenses, and with provisions growing in line with expectations, driven by the normalization in our Consumer business. SRF contributions ended in 2023 and therefore there is no contribution in 2024.

Total income

Total income amounted to EUR 30,715 million, up 10% year-on-year. By line:

•Net interest income (NII) totalled EUR 23,457 million, 12% higher than in H1 2023 with widespread growth across businesses and regions.

Growth was driven by Retail in Europe, due to good price management, and greater volumes and good margin management in Retail in Brazil and Consumer, benefitting from a lower interest rate environment given the negative sensitivity of its balance sheet. NII was also backed by increased activity in CIB, Wealth and Payments.

| Net interest income | |||||

| EUR million | |||||

•Net fee income amounted to EUR 6,477 million, up 6% compared to H1 2023, with solid performance across all our businesses, except Payments which was impacted by a one-time positive fee recorded in Q1 2023.

| Net fee income | |||||

| EUR million | |||||

•Gains or losses on financial assets and liabilities and exchange differences declined to EUR 957 million (EUR 1,302 million in H1 2023) affected by lower results in CIB, mainly in Brazil in a weak market.

•Dividend income was EUR 493 million (EUR 382 million in H1 2023).

•Income from companies accounted for by the equity method reached EUR 303 million, compared to EUR 296 million in H1 2023.

•Other operating income recorded a loss of EUR 972 million (compared to a EUR 993 million loss in H1 2023), owing to the negative impact from hyperinflation adjustment in Argentina (EUR 687 million), and the temporary levy on revenue earned in Spain (EUR 335 million in Q1 2024 and EUR 224 million in Q1 2023). As mentioned above, no contributions to the SRF were charged in 2024 (EUR 293 million in Q2 2023).

| Total income | |||||

| EUR million | |||||

All in all, good performance of total income, supported by year-on-year growth across all our businesses and regions.

| 10 | | January - June 2024 | ||||||

Operating expenses

Operating expenses in H1 2024 amounted to EUR 12,913 million, and rose 3% year-on-year (at a much slower pace than total income), mainly due to the impact of inflation.

Our cost management continued to focus on structurally improving our efficiency and, as a result, we remained among the most efficient banks in the world.

We continued to drive our business transformation plan, ONE Transformation, across our footprint, reflected in greater operational leverage and better business dynamics.

| Operating expenses | |||||

| EUR million | |||||

Provisions or reversal of provisions

Provisions (net of provisions reversals) amounted to EUR 1,762 million and included a write-down in PagoNxt related to the discontinuation of our Superdigital platform in Latin America. In H1 2023, this provisions totalled EUR 1,330 million.

Impairment or reversal of impairment of financial assets not measured at fair value through profit or loss (net)

Impairment or reversal of impairment on financial assets not measured at fair value through profit or loss (net) was EUR 6,577 million (EUR 6,237 million in H1 2023), driven by volumes growth, normalization and regulatory impacts in Consumer. It also includes provisions for our CHF mortgage portfolio in Poland, both in H1 2024 and H1 2023.

Credit quality indicators remained robust, supported by the good performance of the global economy and labour markets across our footprint.

Impairment on other assets (net)

The impairment on other assets (net) was EUR 290 million, including the write-down in PagoNxt related to the discontinuation of our merchant platform in Germany. In H1 2023, impairments totalled EUR 92 million.

Gains or losses on non-financial assets and investments (net)

Net gains on non-financial assets and investments were EUR 366 million in H1 2024, including a EUR 352 million capital gain resulting from having closed the joint-venture agreement with Sodexo in Brazil. In H1 2023 net gains were EUR 277 million .

Negative goodwill recognized in results

There was no negative goodwill recorded in H1 2024 or in H1 2023.

Gains or losses on non-current assets held for sale not classified as discontinued operations

This item, which mainly includes impairment of foreclosed assets recorded and the sale of properties acquired upon foreclosure, recorded a EUR 31 million loss in H1 2024 (EUR 59 million loss in H1 2023).

Profit before tax

Profit before tax was EUR 9,508 million in H1 2024, up 18% year-on-year, supported by the solid performance in net interest income and net fee income.

Income tax

Total income tax amounted to EUR 2,916 million compared to EUR 2,281 million in H1 2023.

Profit attributable to non-controlling interests

Profit attributable to non-controlling interests amounted to EUR 533 million (EUR 568 million in H1 2023).

Profit attributable to the parent

Profit attributable to the parent rose to EUR 6,059 million in H1 2024, compared to EUR 5,241 million in the same period in 2023, 16% higher year-on-year.

These results do not fully reflect the underlying business performance due to the impact of the aforementioned charges.

January - June 2024 | | 11 | ||||||

| Underlying income statement | ||||||||||||||||||||||||||||||||||||||

→ Record profit in the quarter and first half of the year, with solid revenue growth in all our global businesses and regions. → Efficiency improvement and profitable growth, supported by the operational leverage resulting from ONE Transformation. → Risk indicators were robust, due to good risk management, the economic environment and low unemployment. → Positive 2024 results enabled us to improve our targets for the year in revenue, efficiency and profitability. | ||||||||||||||||||||

| Attributable profit | RoTE | RoRWA | ||||||||||||||||||

| EUR 6,059 million | +16% in euros | 15.9% | 2.07% | |||||||||||||||||

| +15% in constant euros | +1.4 pp | +0.2 pp | ||||||||||||||||||

| Note: changes vs. H1 2023. | ||||||||||||||||||||

Results performance compared to H1 2023

The Group presents, both at the total Group level and for each of the business units, the changes in euros registered in the income statement, as well as variations excluding the exchange rate effect (i.e. in constant euros) except for Argentina and any grouping which includes it, understanding that the latter provide a better analysis of the Group’s management. Additionally, from Q2 2024 onwards, a theoretical exchange rate has been used for the Argentine peso. For further information, see the 'Alternative performance measures' section in the appendix to this report.

At the Group level, exchange rates had a positive impact of 0.7 pp in revenue and a negative impact of 0.5 pp in costs.

To better understand the business trends, we reclassified certain items under some headings of the underlying income statement. These items explain the differences between the statutory and underlying income statements and are:

•In H1 2024:

–The impact of the temporary levy on revenue earned in Spain totalling EUR 335 million in Q1 2024, which was moved from total income to other gains (losses) and provisions.

–Provisions which strengthen the balance sheet in Brazil of EUR 352 million in Q2 2024 (EUR 174 million net of tax and minority interests).

•In H1 2023:

–The impact of the temporary levy on revenue earned in Spain totalling EUR 224 million in Q1 2023, which was moved from total income to other gains (losses) and provisions.

–Provisions which strengthen the balance sheet in Brazil of EUR 235 million, net of tax and minority interests in Q1 2023.

For more details, see the 'Alternative Performance Measures' section in the appendix of this report.

As profit was not affected by results that fell outside the ordinary course of our business, no amount was recorded in the net capital gains and provisions line in H1 2024 or in H1 2023 and so both profit attributable to the parent and underlying profit were the same; EUR 6,059 million in H1 2024 and EUR 5,241 million in H1 2023. This represents a 16% year-on-year increase, a 15% rise in constant euros.

This year-on-year comparison is impacted by a higher charge of the temporary levy and by the EUR 243 million net of tax and minority interests from the write-downs in PagoNxt in Q2 2024 related to the discontinuation of our merchant platform in Germany and Superdigital in Latin America. Additionally, there was no contribution to the SRF in 2024, as contributions ended in 2023.

| Summarized underlying income statement | ||||||||||||||||||||||||||

| EUR million | Change | Change | ||||||||||||||||||||||||

| Q2'24 | Q1'24 | % | % excl. FX | H1'24 | H1'23 | % | % excl. FX | |||||||||||||||||||

| Net interest income | 11,474 | 11,983 | (4.2) | (3.5) | 23,457 | 20,920 | 12.1 | 11.2 | ||||||||||||||||||

| Net fee income | 3,237 | 3,240 | (0.1) | 0.8 | 6,477 | 6,103 | 6.1 | 5.8 | ||||||||||||||||||

Gains (losses) on financial transactions 1 | 334 | 623 | (46.4) | (46.4) | 957 | 1,302 | (26.5) | (25.7) | ||||||||||||||||||

| Other operating income | 625 | (466) | — | — | 159 | (91) | — | — | ||||||||||||||||||

| Total income | 15,670 | 15,380 | 1.9 | 2.6 | 31,050 | 28,234 | 10.0 | 9.3 | ||||||||||||||||||

| Administrative expenses and amortizations | (6,366) | (6,547) | (2.8) | (2.3) | (12,913) | (12,479) | 3.5 | 3.0 | ||||||||||||||||||

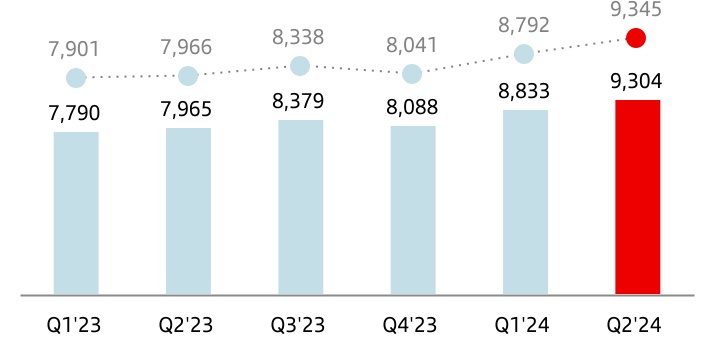

| Net operating income | 9,304 | 8,833 | 5.3 | 6.3 | 18,137 | 15,755 | 15.1 | 14.3 | ||||||||||||||||||

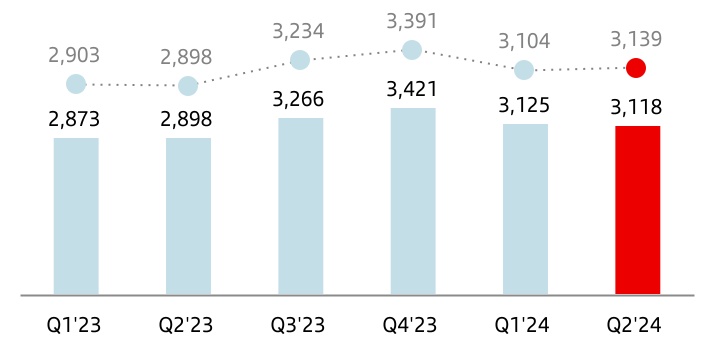

| Net loan-loss provisions | (3,118) | (3,125) | (0.2) | 1.1 | (6,243) | (5,771) | 8.2 | 7.6 | ||||||||||||||||||

| Other gains (losses) and provisions | (1,261) | (1,125) | 12.1 | 12.8 | (2,386) | (1,655) | 44.2 | 42.7 | ||||||||||||||||||

| Profit before tax | 4,925 | 4,583 | 7.5 | 8.2 | 9,508 | 8,329 | 14.2 | 13.3 | ||||||||||||||||||

| Tax on profit | (1,448) | (1,468) | (1.4) | (0.4) | (2,916) | (2,494) | 16.9 | 15.6 | ||||||||||||||||||

| Profit from continuing operations | 3,477 | 3,115 | 11.6 | 12.2 | 6,592 | 5,835 | 13.0 | 12.3 | ||||||||||||||||||

| Net profit from discontinued operations | — | — | — | — | — | — | — | — | ||||||||||||||||||

| Consolidated profit | 3,477 | 3,115 | 11.6 | 12.2 | 6,592 | 5,835 | 13.0 | 12.3 | ||||||||||||||||||

| Non-controlling interests | (270) | (263) | 2.7 | 2.9 | (533) | (594) | (10.3) | (9.3) | ||||||||||||||||||

| Net capital gains and provisions | — | — | — | — | — | — | — | — | ||||||||||||||||||

| Profit attributable to the parent | 3,207 | 2,852 | 12.4 | 13.1 | 6,059 | 5,241 | 15.6 | 14.7 | ||||||||||||||||||

Underlying profit attributable to the parent 2 | 3,207 | 2,852 | 12.4 | 13.1 | 6,059 | 5,241 | 15.6 | 14.7 | ||||||||||||||||||

1. Includes exchange differences.

2. Excludes net capital gains and provisions.

| 12 | | January - June 2024 | ||||||

Total income amounted to EUR 31,050 million, a new record, up 10% year-on-year. In constant euros, total income rose 9% year-on-year, as follows:

•Net interest income (NII) was 11% higher than H1 2023 with growth across businesses and regions:

–Strong growth in Retail, (+12%) with increases in all regions, especially in Europe, driven by good liability margin management, and in South America which benefitted from higher volumes and lower deposit costs in Brazil and Chile following interest rate cuts.

–In Consumer, NII rose 7% supported by our active asset repricing actions and volumes growth in Europe, and higher volumes and lower interest rates in Brazil (favouring consumption).

–CIB increased strongly (+22%), backed by solid performance in Global Banking.

–In Wealth, NII rose 13%, driven by good margin management and increased activity in Private Banking in a favourable macroeconomic environment.

–In Payments, NII rose 10% driven by the solid performance in Cards, which is the main NII business in Payments, driven by higher volumes in Mexico and Brazil.

| Net interest income | |||||

| EUR million | |||||

| constant euros | ||||

•Net fee income grew 6% compared with H1 2023, reaching a new record of EUR 6,477 million with widespread growth across all businesses except Payments, whose year-on-year comparison was impacted by a one-time positive fee from commercial agreements in Brazil in Q1 2023. By business:

–In Retail, net fee income increased 3%, supported by growth across most countries, especially in Brazil, mainly due to insurance and foreign exchange fees.

–In Consumer, net fee income rose 27%, driven by growth in Europe due to increased insurance penetration (particularly in Germany), in Brazil boosted by volumes growth, and in the US in part due to auto fees.

–In CIB, it increased 12%, driven by greater activity in Global Banking, backed by our US Banking Build-Out (BBO) initiatives.

–In Wealth, net fee income rose 15%, mainly due to the good commercial activity in Private Banking and Asset Management.

–In Payments, it declined 7% affected by the impact of the aforementioned one-time positive fee in Q1 2023 in Cards,

while net fee income rose in PagoNxt due to the good performance in Ebury and the increase in Getnet in Chile, Mexico and Europe.

| Net fee income | |||||

| EUR million | |||||

| constant euros | ||||

•Gains on financial transactions declined 26% driven by CIB (lower gains in Global Markets down from a very strong H1 2023, especially by Brazil in a weak market, partially offset by higher results in Retail.

•Other operating income included a greater negative impact from hyperinflation adjustment in Argentina. In 2024, there is no contribution to the SRF, as contributions ended in 2023.

This positive performance in revenue during H1 2024, enabled us to improve growth expectations for the whole year and upgrade our total income target from mid-single digit growth to high-single digits.

| Total income | |||||

| EUR million | |||||

| constant euros | ||||

•Administrative expenses and amortizations in H1 2024 totalled EUR 12,913 million, up 3% year-on-year. In real terms, excluding the impact of the average inflation, and in constant euros, they were 1% lower year-on-year.

Our cost management continued to focus on structurally improving our efficiency. As a result, we remained among the most efficient banks in the world with an efficiency of 41.6%, having improved 2.6 pp vs. H1 2023 and better than our target for 2024. This is why we have upgraded our efficiency ratio target from under 43% to close to 42%.

We continued to progress with our business transformation plan, ONE Transformation, reflected in greater operational leverage and better business dynamics. By business and in constant euros:

January - June 2024 | | 13 | ||||||

–In Retail, costs remained flat, but were down 4% in real terms (i.e excluding inflation), driven by the efforts in transformation (mainly in Spain and the US) and the lower costs in Argentina. The efficiency ratio stood at 39.5%, improving 4.8 pp year-on-year.

–In Consumer, costs were stable year-on-year, in real terms they fell 3% driven by cost discipline in the US, absorbing strategic investments in platforms in leasing (launched in two European markets) and check-out lending. This resulted in a 2.7 pp improvement in the efficiency ratio year-on-year, falling to 40.6%.

–In CIB, they increased by 20%, +16% in real terms, due to our investments in new products and capabilities, as we invest for future growth. The efficiency ratio stood at 43.4%.

–In Wealth, costs rose 5% mainly due to inflation. In real terms, they increased 2% due to investments in key initiatives such as reinforcing our Private Banking teams to respond to higher commercial activity. The efficiency ratio improved 2.3 pp year-on-year to 34.4%.

–In Payments, they were 4% up impacted by inflationary pressures, as they were flat in real terms despite investments in global platforms in both PagoNxt and Cards. The efficiency ratio remained relatively stable year-on-year at 46.9%.

| Operating expenses | |||||

| EUR million | |||||

| constant euros | ||||

Net operating income in H1 2024 grew 15% year-on-year (14% in constant euros), reaching a new record of EUR 18,137 million.

| Net operating income | |||||

| EUR million | |||||

| constant euros | ||||

•Net loan-loss provisions in H1 2024 amounted to EUR 6,243 million, up 8%. In constant euros, they also increased 8%, as the good performance in Retail, due to lower levels of provisions in Europe, partially offset the expected increase in Consumer, driven by the normalization of the cost of risk from very low levels, volumes growth and regulatory impacts.

Additionally, we increased the coverage of the CHF mortgage portfolio in Poland. The cost of risk stood at 1.21%, in line with the Group’s target for 2024.

| Net loan-loss provisions | |||||

| EUR million | |||||

| constant euros | ||||

•Other gains (losses) and provisions had a loss of EUR 2,386 million, versus a EUR 1,655 million loss in H1 2023, mainly affected by write-downs in PagoNxt related to the discontinuation of our merchant platform in Germany and Superdigital in Latin America, as well as by the higher impact of the temporary levy on revenue earned in Spain.

•Profit attributable to the parent in H1 2024 was EUR 6,059 million, 16% more than in the same period in 2023 (+15% in constant euros), supported by double-digit net operating income growth, as total income greatly outpaced cost growth.

| Profit attributable to the parent | |||||

| EUR million | |||||

| constant euros | ||||

RoTE in H1 2024 stood at 15.9% (14.5% in H1 2023), RoRWA at 2.07% (1.88% in H1 2023) and earnings per share stood at EUR 0.37 (EUR 0.31 in H1 2023). Annualizing the impact of the temporary levy on revenue earned in Spain, RoTE in H1 2024 would have been 16.3%. Positive H1 2024 results enabled us to improve our profitability target for the year, from a 16% RoTE to more than 16%.

| 14 | | January - June 2024 | ||||||

Underlying results performance compared to Q1 2024

Underlying profit attributable to the parent and profit attributable to the parent were the same both in Q2 2024, at EUR 3,207 million, and in Q1 2024, at EUR 2,852 million, as profit was not affected by results outside the ordinary course of our business.

Quarterly variations in the income statement are impacted by the application of the new theoretical exchange rate for the Argentine peso. For further information, see the 'Alternative performance measures' section in the appendix to this report.

Profit increased 12% compared to Q1 2024. In constant euros, it increased 13%, by line:

Total income rose 3% driven by the positive performance of the main lines:

•Net interest income decreased 4%, largely impacted by Argentina. Excluding Argentina, it rose 2% driven by Retail (mainly Brazil and Chile supported by lower cost of deposits and greater volumes) and the increased activity in CIB.

•Net fee income grew 1% quarter-on-quarter. Excluding Argentina, they rose 3%, backed by the good performances in Retail, Consumer and Payments.

•Gains on financial transactions fell 46% (-42% excluding Argentina), due to the performance in CIB, mainly in Brazil, partially offset by higher results in Retail and the Corporate Centre.

•Operating expenses in Q2 2024 fell 2% quarter-on-quarter. Excluding Argentina, they were flat as cost efficiencies captured in Retail were offset by our investments in CIB.

•Net loan-loss provisions were practically flat, as the significant declines in Consumer in the US and Brazil offset the increase in Retail, due to volumes growth, and higher CHF provisions in Poland (Retail and Consumer).

•Other gains (losses) and provisions had a EUR 1,261 million loss in Q2 2024, which includes the write-downs in PagoNxt related to the discontinuation of our merchant platform in Germany and Superdigital in Latin America, compared to a EUR 1,125 million loss recorded in Q1 2024, which was affected by the impact of the temporary tax on revenue earned in Spain.

January - June 2024 | | 15 | ||||||

Grupo Santander balance sheet

| Grupo Santander. Condensed balance sheet | |||||||||||||||||

| EUR million | |||||||||||||||||

| Change | |||||||||||||||||

| Assets | Jun-24 | Jun-23 | Absolute | % | Dec-23 | ||||||||||||

| Cash, cash balances at central banks and other demand deposits | 156,234 | 207,546 | (51,312) | (24.7) | 220,342 | ||||||||||||

| Financial assets held for trading | 206,874 | 183,834 | 23,040 | 12.5 | 176,921 | ||||||||||||

| Debt securities | 71,523 | 55,823 | 15,700 | 28.1 | 62,124 | ||||||||||||

| Equity instruments | 16,764 | 13,349 | 3,415 | 25.6 | 15,057 | ||||||||||||

| Loans and advances to customers | 19,899 | 11,051 | 8,848 | 80.1 | 11,634 | ||||||||||||

| Loans and advances to central banks and credit institutions | 39,760 | 35,998 | 3,762 | 10.5 | 31,778 | ||||||||||||

| Derivatives | 58,928 | 67,613 | (8,685) | (12.8) | 56,328 | ||||||||||||

Financial assets designated at fair value through profit or loss1 | 15,335 | 15,441 | (106) | (0.7) | 15,683 | ||||||||||||

| Loans and advances to customers | 6,601 | 6,782 | (181) | (2.7) | 7,201 | ||||||||||||

| Loans and advances to central banks and credit institutions | 444 | 627 | (183) | (29.2) | 459 | ||||||||||||

| Other (debt securities an equity instruments) | 8,290 | 8,032 | 258 | 3.2 | 8,023 | ||||||||||||

| Financial assets at fair value through other comprehensive income | 82,270 | 86,756 | (4,486) | (5.2) | 83,308 | ||||||||||||

| Debt securities | 71,160 | 76,010 | (4,850) | (6.4) | 73,565 | ||||||||||||

| Equity instruments | 1,842 | 1,729 | 113 | 6.5 | 1,761 | ||||||||||||

| Loans and advances to customers | 8,933 | 8,714 | 219 | 2.5 | 7,669 | ||||||||||||

| Loans and advances to central banks and credit institutions | 335 | 303 | 32 | 10.6 | 313 | ||||||||||||

| Financial assets measured at amortized cost | 1,217,341 | 1,180,302 | 37,039 | 3.1 | 1,191,403 | ||||||||||||

| Debt securities | 114,347 | 91,559 | 22,788 | 24.9 | 103,559 | ||||||||||||

| Loans and advances to customers | 1,030,163 | 1,018,497 | 11,666 | 1.1 | 1,009,845 | ||||||||||||

| Loans and advances to central banks and credit institutions | 72,831 | 70,246 | 2,585 | 3.7 | 77,999 | ||||||||||||

| Investments in subsidiaries, joint ventures and associates | 8,235 | 7,679 | 556 | 7.2 | 7,646 | ||||||||||||

| Tangible assets | 33,709 | 34,159 | (450) | (1.3) | 33,882 | ||||||||||||

| Intangible assets | 19,359 | 19,528 | (169) | (0.9) | 19,871 | ||||||||||||

| Goodwill | 13,668 | 14,126 | (458) | (3.2) | 14,017 | ||||||||||||

| Other intangible assets | 5,691 | 5,402 | 289 | 5.3 | 5,854 | ||||||||||||

Other assets2 | 46,904 | 45,248 | 1,656 | 3.7 | 48,006 | ||||||||||||

| Total assets | 1,786,261 | 1,780,493 | 5,768 | 0.3 | 1,797,062 | ||||||||||||

| Liabilities and shareholders' equity | |||||||||||||||||

| Financial liabilities held for trading | 133,856 | 134,888 | (1,032) | (0.8) | 122,270 | ||||||||||||

| Customer deposits | 23,729 | 19,921 | 3,808 | 19.1 | 19,837 | ||||||||||||

| Debt securities issued | — | — | — | — | — | ||||||||||||

| Deposits by central banks and credit institutions | 28,213 | 30,356 | (2,143) | (7.1) | 25,670 | ||||||||||||

| Derivatives | 52,261 | 62,259 | (9,998) | (16.1) | 50,589 | ||||||||||||

| Other | 29,653 | 22,352 | 7,301 | 32.7 | 26,174 | ||||||||||||

| Financial liabilities designated at fair value through profit or loss | 34,493 | 36,220 | (1,727) | (4.8) | 40,367 | ||||||||||||

| Customer deposits | 24,809 | 27,297 | (2,488) | (9.1) | 32,052 | ||||||||||||

| Debt securities issued | 6,726 | 5,684 | 1,042 | 18.3 | 5,371 | ||||||||||||

| Deposits by central banks and credit institutions | 2,942 | 3,239 | (297) | (9.2) | 2,944 | ||||||||||||

| Other | 16 | — | 16 | — | — | ||||||||||||

| Financial liabilities measured at amortized cost | 1,454,896 | 1,446,882 | 8,014 | 0.6 | 1,468,703 | ||||||||||||

| Customer deposits | 989,108 | 966,560 | 22,548 | 2.3 | 995,280 | ||||||||||||

| Debt securities issued | 305,136 | 285,869 | 19,267 | 6.7 | 303,208 | ||||||||||||

| Deposits by central banks and credit institutions | 117,752 | 149,348 | (31,596) | (21.2) | 130,028 | ||||||||||||

| Other | 42,900 | 45,105 | (2,205) | (4.9) | 40,187 | ||||||||||||

| Liabilities under insurance contracts | 17,592 | 17,584 | 8 | 0.0 | 17,799 | ||||||||||||

| Provisions | 8,401 | 8,389 | 12 | 0.1 | 8,441 | ||||||||||||

Other liabilities3 | 33,375 | 34,486 | (1,111) | (3.2) | 35,241 | ||||||||||||

| Total liabilities | 1,682,613 | 1,678,449 | 4,164 | 0.2 | 1,692,821 | ||||||||||||

| Shareholders' equity | 132,836 | 127,258 | 5,578 | 4.4 | 130,443 | ||||||||||||

| Capital stock | 7,747 | 8,092 | (345) | (4.3) | 8,092 | ||||||||||||

Reserves (including treasury stock)4 | 119,030 | 113,925 | 5,105 | 4.5 | 112,573 | ||||||||||||

| Profit attributable to the Group | 6,059 | 5,241 | 818 | 15.6 | 11,076 | ||||||||||||

| Less: dividends | — | — | — | — | (1,298) | ||||||||||||

| Other comprehensive income | (36,963) | (33,789) | (3,174) | 9.4 | (35,020) | ||||||||||||

| Minority interests | 7,775 | 8,575 | (800) | (9.3) | 8,818 | ||||||||||||

| Total equity | 103,648 | 102,044 | 1,604 | 1.6 | 104,241 | ||||||||||||

| Total liabilities and equity | 1,786,261 | 1,780,493 | 5,768 | 0.3 | 1,797,062 | ||||||||||||

| Note: The condensed balance sheet groups some lines of the consolidated balance sheet on pages 88 and 89 as follows: | ||

1.'Non-trading financial assets mandatorily at fair value through profit or loss' and 'Financial assets designated at fair value through profit or loss'. | ||

2.‘Hedging derivatives’; ‘Changes in the fair value of hedged items in portfolio hedges of interest risk’; 'Assets under reinsurance contracts'; ‘Tax assets’; ‘Other assets’; and 'Non-current assets held for sale’. | ||

3.‘Hedging derivatives’; ‘Changes in the fair value of hedged items in portfolio hedges of interest rate risk’; ‘Tax liabilities’; ‘Other liabilities’; and ‘Liabilities associated with non-current assets held for sale‘. | ||

4.‘Share premium’; ‘Equity instruments issued other than capital’; ‘Other equity’; ‘Accumulated retained earnings’; ‘Revaluation reserves’; ‘Other reserves’; and ‘Own shares (-)’. | ||

| 16 | | January - June 2024 | ||||||

| Balance sheet | ||||||||||||||||||||||||||||||||||||||

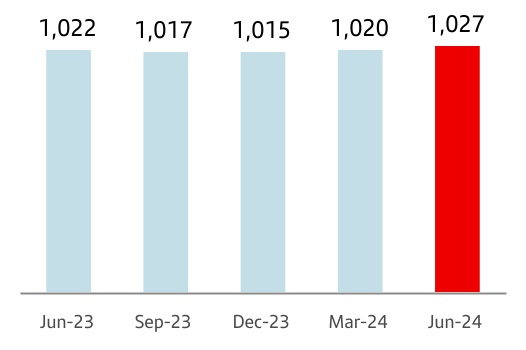

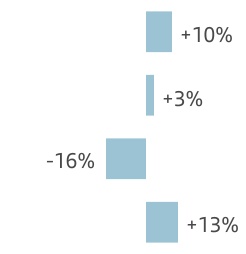

Gross loans and advances to customers (excl. reverse repos) | Customer funds (deposits excl. repos + mutual funds) | |||||||||||||||||||

| Lending volumes rose 2% year-on-year. Quarter-on-quarter, lending volumes also increased 2%, with growth across most businesses and regions. | Customer funds grew year-on-year and remained flat quarter-on-quarter, as the decline in corporate deposits was offset by higher mutual funds. | |||||||||||||||||||

Gross loans and advances to customers (excl. reverse repos) | Customer funds (deposits excl. repos + mutual funds) | |||||||||||||||||||

| 1,027 | +2% QoQ | 1,171 | 0% QoQ | |||||||||||||||||

| EUR billion | +2% YoY | EUR billion | +5% YoY | |||||||||||||||||

è By segment: | è By product: | |||||||||||||||||||

| Solid growth year-on-year in our Consumer and CIB businesses, with a slight decrease in Retail. | Year-on-year growth in time deposits and mutual funds at the expense of demand deposits. | |||||||||||||||||||

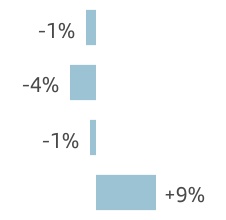

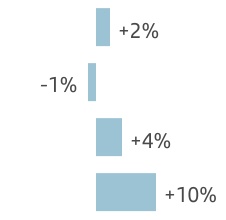

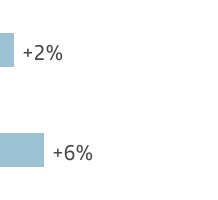

| Retail | Consumer | CIB | Demand | Time | Mutual funds | |||||||||||||||

| -1% | +6% | +7% | -1% | +12% | +17% | |||||||||||||||

| Note: changes in constant euros. | ||||||||||||||||||||

Loans and advances to customers

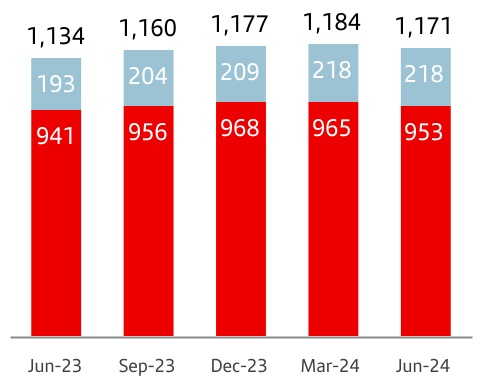

Loans and advances to customers stood at EUR 1,065,596 million as at end June 2024, a 2% increase both year-on-year and quarter-on-quarter.

For the purpose of analysing traditional banking loans, the Group uses gross loans and advances to customers excluding reverse repos (EUR 1,027,346 million). Additionally, the comments below do not include the exchange rate impact (i.e in constant euros), except for Argentina and any grouping which includes it. From Q2 2024 onwards, a theoretical exchange rate has been used for the Argentine peso. For further information, see the 'Alternative performance measures' section in the appendix to this report. However, the use of this new exchange rate did not significantly impact quarter-on-quarter balance variations given the small size of Argentina’s balance sheet relative to the total Group.

In Q2 2024, gross loans and advances to customers, excluding reverse repos, rose 2% quarter-on-quarter in constant euros, as follows:

•They increased 1% in Retail, driven by growth in corporates, as individuals and SMEs were stable. By region, they increased in South America (mainly in Brazil), North America (mainly Mexico) and were flat in Europe (good performance in Spain and Poland offset the fall in the UK).

•In Consumer, loans grew 3%, driven by the increases in auto in Europe, the US and Brazil.

| Gross loans and advances to customers (excl. reverse repos) | |||||

| EUR billion | |||||

| +1 | % | 1 | |||

| Jun-24 / Jun-23 | |||||

1. In constant euros: +2%.

•In CIB, loans grew 5%, with increases in all regions, especially in Spain driven by higher activity levels.

•They increased 1% in Wealth and declined 1% in Payments.

Compared to June 2023, gross loans and advances to customers (excluding reverse repos and in constant euros) grew 2%, as follows:

•In Retail, they dropped 1%, as falls in the UK (in line with our strategy of increasing profitability) and Spain (affected by mortgage prepayments and lower SME lending) was partially offset by growth in Brazil, Poland, Mexico and Chile.

•They rose 6% in Consumer, boosted by the good performance in auto in Europe and Brazil.

•In CIB, they grew 7% boosted by solid growth in the US, on the back of our US BBO initiatives.

•They increased 3% in Wealth and 4% in Payments.

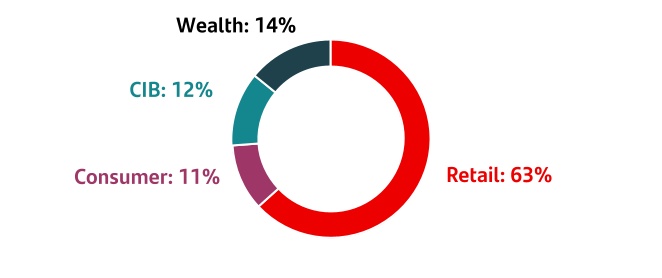

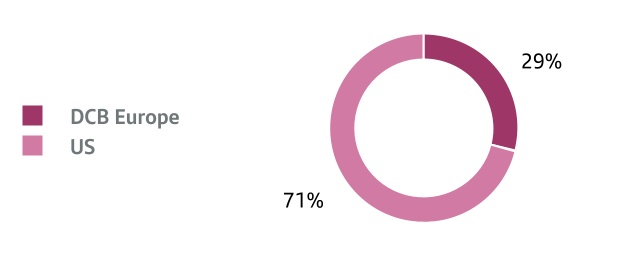

As at end June 2024, gross loans and advances to customers excluding reverse repos maintained a diversified mix among the markets in which the Group operates: Europe (55%), DCB Europe (14%), North America (16%) and South America (15%).

| Gross loans and advances to customers (excl. reverse repos) | ||

| % operating areas. June 2024 | ||

January - June 2024 | | 17 | ||||||

Customer funds

Customer deposits amounted to EUR 1,037,646 million in June 2024, falling 1% quarter-on-quarter and growing 2% year-on-year.

The Group uses customer funds (customer deposits excluding repos, plus mutual funds) for the purpose of analysing traditional retail banking funds, which amounted to EUR 1,171,085 million as at end June 2024. Additionally, the comments below do not include the exchange rate impact (i.e in constant euros), except for Argentina and any grouping which includes it. From Q2 2024 onwards, a theoretical exchange rate has been used for the Argentine peso. For further information, see the 'Alternative performance measures' section in the appendix to this report. However, the use of this new exchange rate did not significantly impact quarter-on-quarter balance variations given the small size of Argentina’s balance sheet relative to the total Group.

In the quarter, customer funds were flat in constant euros, as follows:

•By product, customer deposits excluding repos decreased slightly, offset by mutual funds which grew 3%.

•By primary segment, customer funds grew 3% in Consumer, up 1% in Retail and Wealth. On the other hand, they fell 7% in CIB, mainly driven by strategy changes to reduce excess corporate deposits.

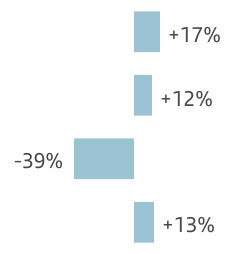

Compared to June 2023, customer funds were up 5% in constant euros:

•By product, deposits excluding repurchase agreements rose 2%, driven by an increase in time deposits (+12%) given the current interest rate environment, with time deposit growth in most markets (except in the US and Argentina), to the detriment of demand deposits, which fell 1%. Mutual funds increased 17%.

•By business, they rose 4% in Retail, backed by strong growth in Brazil, Spain, Mexico and Poland, up 14% in Consumer as part of our strategy to increase deposit funding, while they fell 3% in CIB due to lower volumes in Spain and the US, and increased 10% in Wealth, due to mutual funds.

•By secondary segment, strong growth in Brazil, Spain Mexico, Poland and DCB Europe.

As at June 2024, customer funds maintained a diversified mix among the markets in which the Group operates: Europe (62%), DCB Europe (7%), North America (14%) and South America (17%). The weight of demand deposits as a percentage of total customer funds was 56%, while time deposits accounted for 25% of the total and mutual funds for 19%.

| Customer funds | ||

| EUR billion | ||

| +3 | % | 1a | ||||||

| +13 | % | |||||||

| +1 | % | |||||||

•Total | ||||||||

• Mutual funds | ||||||||

•Deposits exc. repos | ||||||||

| Jun-24 / Jun-23 | ||||||||

1. In constant euros: +5%.

In addition to capturing customer deposits, the Group, for strategic reasons, maintains a selective policy of issuing securities in the international fixed income markets and strives to adapt the frequency and volume of its market operations to the structural liquidity needs of each unit, as well as to the receptiveness of each market.

In H1 2024, the Group issued:

•Medium- and long-term senior debt placed in the market of EUR 12,053 million and covered bonds amounting to EUR 6,272 million.

•TLAC eligible instruments issued amounted to EUR 11,998 million, of which EUR 8,092 million was senior non-preferred, EUR 2,406 million was subordinated debt and EUR 1,500 million was AT1.

•Maturities of medium- and long-term debt totalled EUR 25,682 million.

The net loan-to-deposit ratio was 103% (103% in June 2023). The ratio of deposits plus medium- and long-term funding to the Group’s loans was 123%, underscoring the comfortable funding structure. The liquidity coverage ratio (LCR) was an estimated 163% in June 2024 (158% in June 2023).

The Group's access to wholesale funding markets and the cost of issuances depends, in part, on the ratings of the rating agencies.

| Rating agencies | |||||||||||

| Long term | Short term | Outlook | |||||||||

| Fitch Ratings | A-(Senior A) | F2 (Senior F1) | Stable | ||||||||

| Moody's | A2 | P-1 | Positive | ||||||||

| Standard & Poor's | A+ | A-1 | Stable | ||||||||

| DBRS | A (High) | R-1 (Middle) | Stable | ||||||||

Moody's confirmed its A2 long-term and P-1 short-term ratings in April of this year, and also improved its outlook from stable to positive following the same movement in the rating of the Kingdom of Spain, remaining two notches above sovereign. In April, Standard & Poor's (S&P) rated our additional tier 1 debt as BBB- (investment grade), a new rating for this instrument.

In terms of outlooks, DBRS and Fitch maintained their stable outlooks, above the sovereign's, while S&P also maintained its outlook but in line with the sovereign.

Sometimes the methodology applied by the agencies limits a bank's rating to the sovereign rating of the country where it is headquartered. Banco Santander, S.A. is still rated above the sovereign debt rating of the Kingdom of Spain by Moody’s, DBRS and S&P and at the same level by Fitch, which demonstrates our financial strength and diversification.

| Customer funds | ||

| % operating areas. June 2024 | ||

| 18 | | January - June 2024 | ||||||

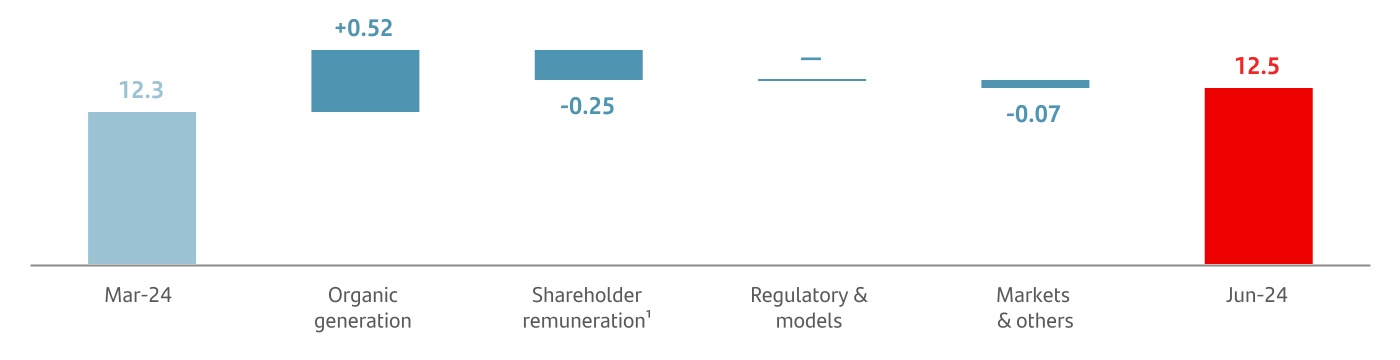

Solvency ratios

| Executive summary | ||||||||||||||||||||||||||||||||||||||

| Fully-loaded capital ratio | Fully-loaded CET1 ratio | |||||||||||||||||||

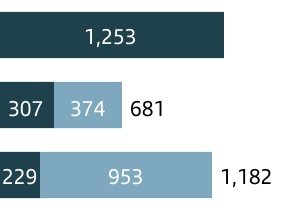

| The fully-loaded CET1 ratio remained above 12% at the end of June, in line with the Group's objective. | We continued to generate capital organically in the quarter, backed by profit growth. | |||||||||||||||||||

| Fully-loaded CET1 performance (%) | Organic generation | +52 bps | ||||||||||||||||||

| ||||||||||||||||||||

Accrual for shareholder remuneration1 | -25 bps | |||||||||||||||||||

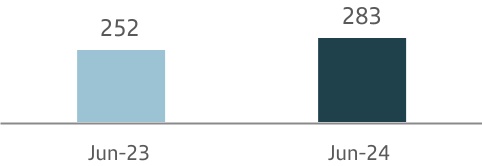

| TNAV per share | ||||||||||||||||||||

TNAV per share was EUR 4.94, increasing 12% year-on-year including the cash dividends. | ||||||||||||||||||||

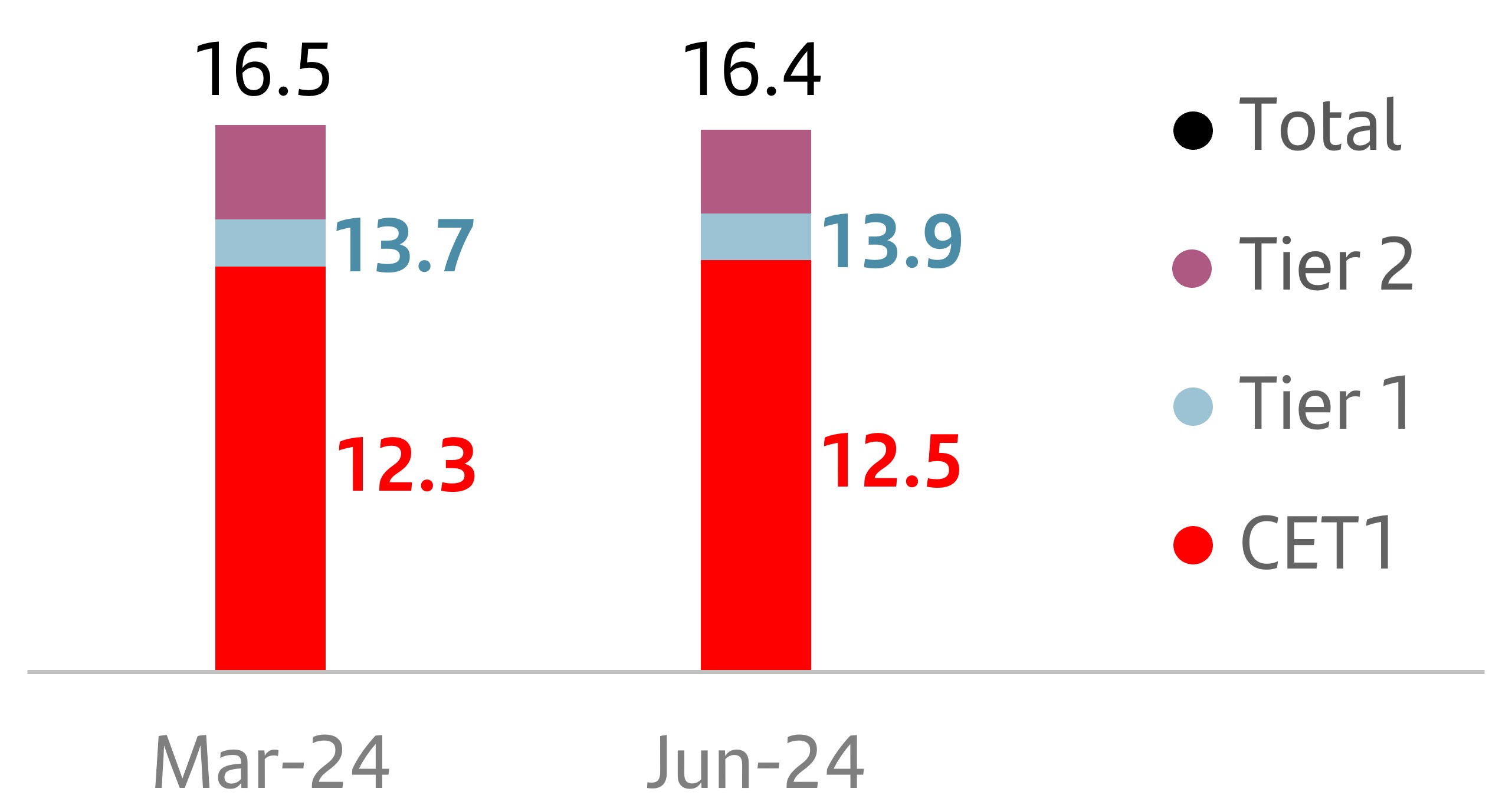

As at end June 2024, the total phased-in capital ratio (applying the IFRS 9 transitional arrangements) stood at 16.7% and the phased-in CET1 ratio at 12.5%. We comfortably meet the levels required by the ECB on a consolidated basis (estimated 13.9% for the total capital ratio and 9.6% for the CET1 ratio)2. This resulted in a distance to the maximum distributable amount (MDA) of 245 bps and a CET1 management buffer of 286 bps.

In fully-loaded terms, we generated 52 bps organically in the quarter, including a 7 bp positive contribution from RWAs, as RWA growth was more than offset by significant risk transfer and asset rotation initiatives. We also recorded a 25 bp charge for shareholder remuneration against profit earned in Q2 2024 in line with our 50% payout target1.

Additionally, we recorded charges of -7 bps relating to deductions, mainly intangible assets and held to collect and sell portfolio valuations. There were no significant regulatory charges in the quarter.

This resulted in a fully-loaded CET1 ratio of 12.5%. The total fully-loaded capital ratio stood at 16.4%.

TNAV per share ended the quarter at EUR 4.94. Including the cash dividend paid in November 2023 (EUR 8.10 cents) and the second cash dividend charged against 2023 results (EUR 9.50 cents) paid in May, TNAV plus cash dividend per share increased 12% in the last twelve months (+2% in the quarter).

Lastly, the fully-loaded leverage ratio stood at 4.74% and the phased-in was also 4.74%.

Eligible capital. June 2024 | ||||||||

| EUR million | ||||||||

| Fully-loaded | Phased-in | |||||||

| CET1 | 77,848 | 77,975 | ||||||

| Basic capital | 86,681 | 86,809 | ||||||

| Eligible capital | 102,419 | 104,420 | ||||||

| Risk-weighted assets | 625,017 | 624,831 | ||||||

| % | % | |||||||

| CET1 capital ratio | 12.5 | 12.5 | ||||||

| Tier 1 capital ratio | 13.9 | 13.9 | ||||||

| Total capital ratio | 16.4 | 16.7 | ||||||

| Fully-loaded CET1 ratio performance | ||

| % | ||

Note: The phased-in ratio includes the transitory treatment of IFRS 9, calculated in accordance with article 473 bis of the Capital Requirements Regulation (CRR2) and subsequent modifications introduced by Regulation 2020/873 of the European Union. Total phased-in capital ratios include the transitory treatment according to chapter 4, title 1, part 10 of the CRR2.

1.Shareholder remuneration charged against profit earned in Q2 2024 in line with our target of approximately 50% payout, divided approximately equally between cash dividends and share repurchases. The implementation of the shareholder remuneration policy is subject to future corporate and regulatory decisions and approvals.

2.On 1 January 2024, our systemic buffer requirement increased from 1% to 1.25% due to a higher D-SIB requirement due to i) a methodological change by the ECB which was later adopted by Banco de España and ii) because institutions must hold capital at the consolidated level for the higher of the G-SIB (currently at 1%) and D-SIB requirements. Additionally, the ECB revised Banco Santander, S.A.'s P2R requirement from 1.58% to 1.74%, mainly due to a change in the ECB's methodology.

January - June 2024 | | 19 | ||||||

Risk management

| Executive summary | ||||||||||||||||||||||||||||||||||||||

| Credit risk | Market risk | |||||||||||||||||||

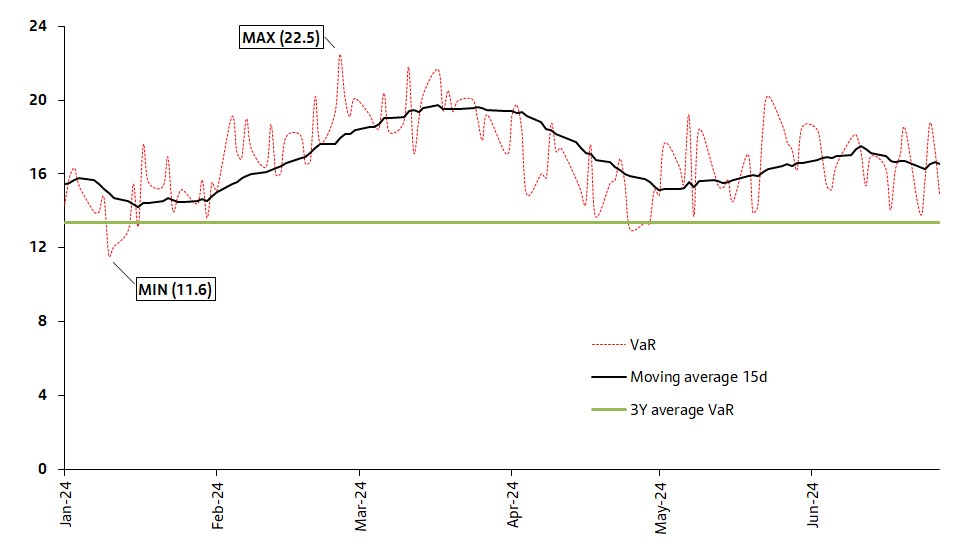

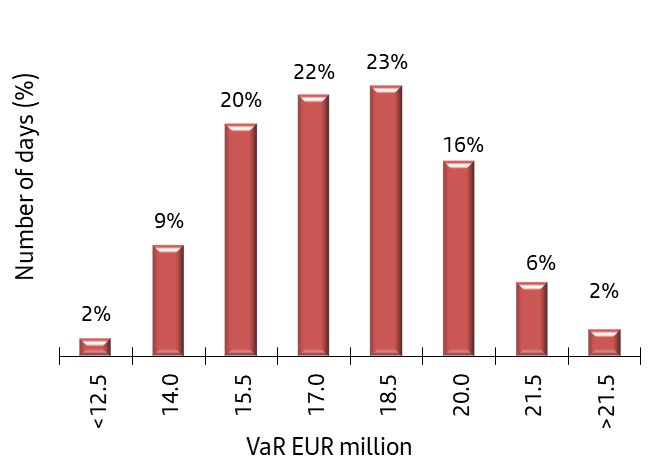

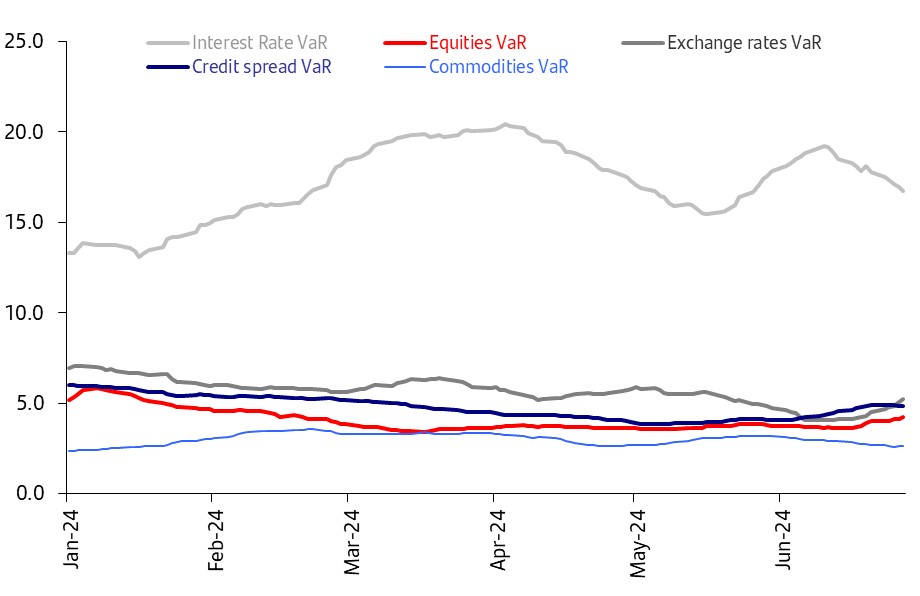

| Credit quality indicators remain within expected levels due to proactive risk management, despite the macroeconomic and geopolitical environment. | Stability in our risk profile. VaR remained at moderate levels in an economic environment with persistent inflation and greater geopolitical risk. | |||||||||||||||||||

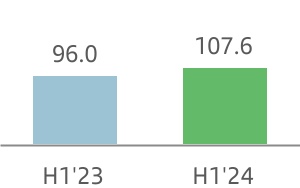

| Cost of risk | NPL ratio | Coverage ratio | Average VaR | |||||||||||||||||

| 1.21% | 3.02% | 66% | Q2'24 | EUR 16 million | -EUR 1 mn / Q1'24 | |||||||||||||||

| +1 bps vs. Q1'24 | -8 bps vs. Q1'24 | 0 pp vs. Q1'24 | ||||||||||||||||||

| Structural and liquidity risk | Operational risk | |||||||||||||||||||

| Robust and diversified liquidity buffer, with ratios well above regulatory requirements. | The operational risk profile deteriorated slightly in Q2 2024, caused by an increase in execution and cyber risk. Operational losses have increased compared to Q1 2024. | |||||||||||||||||||

| Liquidity Coverage Ratio (LCR) | ||||||||||||||||||||

| 163% | +5 pp vs. Q1'24 | |||||||||||||||||||

Credit risk 1

During H1 2024, one of the main factors influencing market behaviour was the uncertainly around the decline of inflation, where the ECB recently cut interest rates slightly while the Federal Reserve and the Bank of England held rates. Other determining factors were the growing geopolitical tensions and the various electoral processes in Europe and Latin America.

Nevertheless, in the current soft-landing scenario with a slight slowdown in inflation, economic activity has not been significantly affected, partially due to strong labour markets and fiscal policies that have been supportive of households and businesses.

Our business model, together with our conservative risk management, help us to maintain a medium-low risk profile even in a less favourable macroeconomic and geopolitical environment.

| Key risk metrics | |||||||||||||||||||||||||||||||||||||||||||||||||||||

Net loan-loss provisions 2 | Cost of risk (%) 3 | NPL ratio (%) | NPL coverage ratio (%) | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Q2'24 | H1'24 | Chg (%) / H1'23 | Chg (%) / Q1'24 | H1'24 | Chg (bps) / H1'23 | Chg (bps) / Q1'24 | H1'24 | Chg (bps) / H1'23 | Chg (bps) / Q1'24 | H1'24 | Chg (pp) / H1'23 | Chg (pp) / Q1'24 | |||||||||||||||||||||||||||||||||||||||||

| Retail | 1,564 | 3,087 | (1.3) | 4.6 | 1.03 | 11 | 0 | 3.15 | (7) | (9) | 60.4 | (2.8) | 0.3 | ||||||||||||||||||||||||||||||||||||||||

| Consumer | 1,055 | 2,193 | 21.4 | (7.0) | 2.17 | 31 | 4 | 4.81 | 63 | (5) | 75.9 | (12.0) | (0.2) | ||||||||||||||||||||||||||||||||||||||||

| CIB | 56 | 96 | — | 39.4 | 0.15 | (4) | 1 | 1.05 | (33) | (9) | 45.0 | 8.2 | (1.3) | ||||||||||||||||||||||||||||||||||||||||

| Wealth | 10 | 14 | — | 147.9 | 0.05 | 6 | 11 | 0.77 | (5) | 14 | 64.6 | 11.4 | 3.0 | ||||||||||||||||||||||||||||||||||||||||

| Payments | 434 | 852 | (2.8) | 6.0 | 7.03 | (8) | 14 | 5.00 | (13) | 15 | 149.5 | 7.4 | 4.6 | ||||||||||||||||||||||||||||||||||||||||

| TOTAL GROUP | 3,118 | 6,243 | 7.6 | 1.1 | 1.21 | 13 | 1 | 3.02 | (5) | (8) | 66.5 | (1.9) | 0.4 | ||||||||||||||||||||||||||||||||||||||||

| Europe | 532 | 1,017 | (22.7) | 9.6 | 0.39 | (3) | (2) | 2.25 | (11) | (7) | 49.1 | (1.9) | 0.0 | ||||||||||||||||||||||||||||||||||||||||

| DCB Europe | 308 | 584 | 39.5 | 12.0 | 0.72 | 17 | 5 | 2.31 | 28 | 5 | 85.4 | (9.0) | (0.7) | ||||||||||||||||||||||||||||||||||||||||

| North America | 908 | 1,893 | 21.2 | (8.1) | 2.23 | 54 | 9 | 3.93 | 70 | (14) | 74.3 | (15.7) | 0.1 | ||||||||||||||||||||||||||||||||||||||||

| South America | 1,370 | 2,748 | 9.5 | 2.7 | 3.50 | 18 | 5 | 5.30 | (58) | (7) | 81.5 | 3.7 | 1.2 | ||||||||||||||||||||||||||||||||||||||||

| TOTAL GROUP | 3,118 | 6,243 | 7.6 | 1.1 | 1.21 | 13 | 1 | 3.02 | (5) | (8) | 66.5 | (1.9) | 0.4 | ||||||||||||||||||||||||||||||||||||||||

1.Changes in constant euros.

2.EUR million and % change in constant euros.

3.Provisions to cover losses due to impairment of loans in the last 12 months / average customer loans and advances of the last 12 months.

| 20 | | January - June 2024 | ||||||

In terms of credit quality:

•The NPL ratio stood at 3.02% (-8 bps compared to Q1 2024), mainly driven by higher gross credit risk with customers (total risk), that increased 2% quarter-on-quarter, reaching EUR 1,164 billion, while credit impaired loans remained stable in the quarter at EUR 35,091 million, due to the good performance in Retail.

•Net loan-loss provisions rose 8% year-on-year in H1 2024 to EUR 6,243 million, due to the expected normalization in Consumer and increases in Retail in Mexico and Brazil, partially offset by lower levels of provisions in the European Retail portfolio.

In the quarter, provisions slightly increased (+1%), as lower provisions in the Consumer portfolio in the US offset higher provisions in CHF mortgage portfolio.

The cost of risk was 1.21%, remaining in line with our target for the year, in a context of a slight increase in credit risk exposure in the last 12 months.

•The total coverage ratio for credit impaired loans remained flat in the quarter at 66%, with loan-loss allowances of EUR 23,323 million. The coverage ratio remained at comfortable levels considering that 68% of the Group’s portfolio backed by quality collateral.

The IFRS 9 stage distribution of the portfolio was largely unchanged in the quarter in percentage terms. Stage 2 balances increased slightly due to changes in the classification criteria, improving our early risk detection systems. It does not significantly affect the total loan-loss provisions.

| Coverage ratio by stage | |||||||||||||||||||||||

| EUR billion | |||||||||||||||||||||||

Exposure1 | Coverage | ||||||||||||||||||||||

| Jun-24 | Mar-24 | Jun-23 | Jun-24 | Mar-24 | Jun-23 | ||||||||||||||||||

| Stage 1 | 1,008 | 1,007 | 1,011 | 0.4 | % | 0.4 | % | 0.4 | % | ||||||||||||||

| Stage 2 | 94 | 83 | 75 | 5.6 | % | 6.3 | % | 7.2 | % | ||||||||||||||

| Stage 3 | 35 | 36 | 35 | 41.2 | % | 40.5 | % | 41.0 | % | ||||||||||||||

Stage 1: financial instruments for which no significant increase in credit risk has been identified since its initial recognition.

Stage 2: if there has been a significant increase in credit risk since the date of initial recognition but the impairment event has not materialized, the financial instrument is classified in Stage 2.

Stage 3: a financial instrument is catalogued in this stage when it shows effective signs of impairment as a result of one or more events that have already occurred resulting in a loss.

| Credit impaired loans and loan-loss allowances | |||||||||||

| EUR million | |||||||||||

| Change (%) | |||||||||||

| Q2'24 | QoQ | YoY | |||||||||

| Balance at beginning of period | 35,637 | — | 3.5 | ||||||||

| Net additions | 3,296 | 4.1 | 4.8 | ||||||||

| Increase in scope of consolidation | 13 | — | — | ||||||||

| Exchange rate differences and other | (611) | — | — | ||||||||

| Write-offs | (3,244) | 1.5 | 6.0 | ||||||||

| Balance at period-end | 35,091 | (1.5) | 0.4 | ||||||||

| Loan-loss allowances | 23,323 | (0.9) | (2.4) | ||||||||

| For impaired assets | 14,461 | 0.1 | 0.9 | ||||||||

| For other assets | 8,862 | (2.6) | (7.5) | ||||||||