united states

securities and exchange commission

washington, d.c. 20549

form n-csr

certified shareholder report of registered management

investment companies

Investment Company Act file number 811-07254

Johnson Mutual Funds Trust

(Exact name of registrant as specified in charter)

3777 West Fork Road, Cincinnati, Ohio 45247

(Address of principal executive offices) (Zip code)

Marc E. Figgins, CFO, 3777 West Fork Road, Cincinnati, Ohio 45247

(Name and address of agent for service)

Registrant's telephone number, including area code:(513) 661-3100

Date of fiscal year end:12/31

Date of reporting period:12/31/23

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

| JOHNSON MUTUAL FUNDS | DECEMBER 31, 2023 |

Table of Contents

| Letter from the Fund President | 1 |

| Performance Review and Management Discussion | |

| Equity Income Fund | 3 |

| Opportunity Fund | 5 |

| International Fund | 7 |

| Municipal Income Fund | 8 |

| Portfolio of Investments | |

| Equity Income Fund | 10 |

| Opportunity Fund | 11 |

| International Fund | 13 |

| Municipal Income Fund | 15 |

| Statements of Assets and Liabilities | 20 |

| Statements of Operations | 22 |

| Statements of Changes in Net Assets | 24 |

| Financial Highlights | |

| Equity Income Fund | 27 |

| Opportunity Fund | 29 |

| International Fund | 31 |

| Municipal Income Fund | 32 |

| Notes to the Financial Statements | 33 |

| Disclosure of Expenses | 41 |

| Operation and Effectiveness of the Funds’ Liquidity Risk management Program | 42 |

| Additional Information | 43 |

| Report of Independent Registered Public Accounting Firm | 44 |

| Trustees and Officers | 45 |

| Trustees and Officers, Transfer Agent and Fund Accountant, Custodian, Independent Registered Public Accounting Firm, Legal Counsel | Back Page |

| LETTER FROM THE FUND PRESIDENT | DECEMBER 2023 |

We are pleased to present you with the Johnson Mutual Funds’ 2023 Annual Report to Shareholders. On the following pages, we have provided commentary on the performance of each of the Funds for 2023 as well as their relative performance compared to an appropriate benchmark.

The remainder of the report provides the holdings of each Johnson Mutual Fund as well as other financial data and notes.

2023 was the year of the market mood swing. The year began plagued by fear and uncertainty as the Federal Reserve (the “Fed”) aggressively tightened policy, and economists were all but certain this would be the year the economy would buckle under the Fed’s pressure. By early spring, Leading Economic Indicators were at levels only previously seen in a recession or on the verge of entering a recession. To make matters worse, the abrupt failure of Silicon Valley Bank rattled investors and sent markets tumbling.

By summer, optimism emerged as investors grew confident that the banking crisis was contained, and overall market sentiment began to improve. Throughout the second half of the year the combination of steady economic data and convincing progress on inflation propelled risk assets higher.

One notable exception, however, was the bond market. The combination of stronger than expected economic data and inflation still running hotter than desired propelled interest rates to new highs as the market embraced the Fed’s promise to keep rates “higher for longer”. For a moment, the Bloomberg Aggregate Index (“AGG”) seemed destined to post its third straight year of negative returns.

However, that changed abruptly, after a slowing pace of hiring was revealed in the October payrolls report. The Federal Reserve further added fuel to the fourth-quarter bond market rally at its December meeting, when it disclosed plans to cut rates a few times in the coming year. From its October lows, the AGG climbed nearly 10% and erased its entire YTD deficit, closing the year up 5.53%.

The sudden dovish shift from the Federal Reserve sent equities even higher with the S&P 500 returning 11.69% in the fourth quarter alone. The swift decline in rates and increasing hopes of an economic soft landing were celebrated by the market, leading to significant gains in interest rate-sensitive sectors, such as Real Estate (18.83%), Technology (17.17%), and Financials (14.03%).

All told the S&P 500 climbed 26.29% during 2023 to finish the year just below its all-time record high set in January 2022. On the surface the stock market appears to be signaling that the Fed has engineered a soft landing for the economy. However, the story of equity markets in 2023 remained the market concentration of the largest mega-cap, growth-oriented stocks. While the market-cap weighted S&P 500 is close to reaching a new all-time high, the equal weighted S&P 500 lagged materially, finishing the year up only 13.88%, the largest spread between the two indices since 1998.

Diversification was not only detrimental within the large cap equity space, but across market capitalization and geographic regions as well. The US mid and small cap stocks underperformed their large cap peers by a wide margin. Globally both developed and emerging market equities failed to keep pace with domestic indices.

LOOKING AHEAD

Diversification in portfolios will matter again as it always has. This narrow equity market leadership is unlikely to last forever. If history teaches us anything, it is that we would be wise to avoid that level of concentration in portfolios. From energy producers in 1980, to Japanese conglomerates in the 1990s, to tech stocks in the 2000s, to emerging markets commodity producers in the 2010s, every decade provides a new example of why it is unwise to concentrate on themes that drove the market in the recent past.

The Johnson forward looking outlook on the market remains mixed. While the Fed’s perceived more dovish commentary in December marked a notable potential shift in policy, a full cyclical upswing in the economy seems distant. The continuation of slowing economic trends and a potential recession could result in increased stock market volatility.

It is also important to highlight that the valuation on the market is not cheap, and that is based on earnings that may come under further pressure. Utilizing current consensus earnings estimates, the S&P 500 is trading at 19.5x forward earnings. While valuation is a poor predictor of return in the short term, it can provide a good indication toward longer term, 10-year return expectations. With the starting Price-to-Earnings ratio of 19.5x the regression would indicate equity returns over the next 10 years to average in the 3-6% range.

| LETTER FROM THE FUND PRESIDENT | DECEMBER 2023 |

Bonds, for their part, look to be particularly attractive. The yield on an intermediate duration bond portfolio is near 4.5%. While yields have come down slightly from their highs earlier in the year, fixed income securities once again provide for the diversification benefit that did not exist in the lower rate environments of the past several years. In periods of risk aversion, fixed income will again be able to provide a benefit to portfolios as a hedge against increasing risks. And with bond portfolios yielding near 4.5% or better, the outlook for bond returns going forward has not been this high in many years (The best indication of long-term returns for fixed income is the starting yield).

Either way, the playbook here at Johnson will remain the same: a diversified portfolio of high-quality securities is the most resilient and reliable path to long-term success.

Disclaimer: Any expectations presented should not be taken as a guarantee or other assurance as to future results. Our opinions are a reflection of our best judgment at the time this presentation was created, and we disclaim any obligation to update or alter forward-looking statements as a result of new information, future events or otherwise. The material contained herein is based upon proprietary information and is provided purely for reference and as such is confidential and intended solely for those to whom it was provided by Johnson Investment Counsel. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.

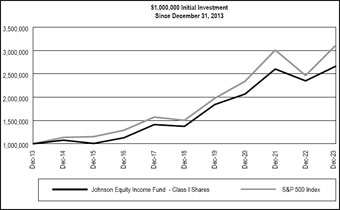

| JOHNSON EQUITY INCOME FUND | PERFORMANCE REVIEW – DECEMBER 31, 2023 |

The Johnson Equity Income Fund achieved a total return of 13.42% in 2023, underperforming the S&P 500 Index’s (the “Index”) 26.29% return. While the Fund’s absolute return for the year was positive, the significant outperformance of a few mega-cap stocks in the Index, dubbed the ‘Magnificent 7’, was the defining feature of 2023. These seven stocks hailed from three sectors – Information Technology (+58%), Communication Services (+55%), and Consumer Discretionary (+42%). These sectors provided outsized returns during the year and were the only three sectors that outperformed the Index. The other seven sectors severely underperformed the Index with four of these sectors – Health Care (+2%), Consumer Staples (+0.5%), Energy (-1%), and Utilities (-7%) – not participating at all.

Both sector allocation and stock selection contributed to the Fund’s underperformance in 2023. The Fund was meaningfully underweighted each of the three outperforming sectors and modestly overweight each of the four sectors mentioned above that did not participate in the year’s strong appreciation. As for stock selection, overconcentration of the Index in the ‘Magnificent 7’ mega cap companies, which now comprise ~29% of the overall Index, was a significant contributor to the Fund’s underperformance.

The Fund benefited from a few standout performers. Adobe and Intuit collectively provided over 120 bps of positive relative performance within Technology. The Fund’s position in Cencora (formerly AmerisourceBergen) and not owning pharmaceutical companies Pfizer and Johnson & Johnson resulted in a positive Health Care sector contribution. Infrastructure spending beneficiary, nVent Electric, has increased 40.2% over the Fund’s holding period during the year, which resulted in a positive contribution from the Industrials sector.

In summary, 2023 was a difficult environment for dividend-focused strategies like this Fund, given the factors mentioned above. With the Federal Reserve’s perceived policy shift in December, the market has begun to anticipate that interest rate cuts may come quicker than anticipated. Against a backdrop of weakening economic indicators, the perceived shift raises questions about whether the economy is headed for a soft landing or a recession. A near term headwind to the Fund’s relative performance could be an environment led by lower quality, cyclical stocks. However, if we do see stock market volatility increase due to the return of recession fears, the Fund has a strong history of relative outperformance during significant market declines. We will continue to maintain our bottom-up quality discipline to provide positive shareholder value over the full market cycle.

| AVERAGE ANNUAL TOTAL RETURNS | AS OF DECEMBER 31, 2023 |

| | EQUITY INCOME FUND | |

| | — CLASS I SHARES | S&P 500 INDEX |

| ONE YEAR | 13.42% | 26.29% |

| THREE YEARS | 8.84% | 10.00% |

| FIVE YEARS | 14.18% | 15.69% |

| TEN YEARS | 10.30% | 12.03% |

| HOLDINGS BY INDUSTRY SECTOR |

| SECTOR ALLOCATION | | % OF NET ASSETS |

| TECHNOLOGY | | | 24.6 | % |

| HEALTH CARE | | | 15.2 | % |

| FINANCIALS | | | 13.6 | % |

| INDUSTRIALS | | | 12.1 | % |

| CONSUMER STAPLES | | | 7.7 | % |

| CONSUMER DISCRETIONARY | | | 6.7 | % |

| ENERGY | | | 5.9 | % |

| UTILITIES | | | 5.9 | % |

| COMMUNICATIONS | | | 5.2 | % |

| REAL ESTATE | | | 2.1 | % |

| MONEY MARKET FUNDS | | | 0.9 | % |

| OTHER: | | | | |

| NET OTHER ASSETS (LIABILITIES) | | | 0.1 | % |

| | | | 100.0 | % |

Above average dividend income and long-term capital growth is the objective of the Johnson Equity Income Fund, and the primary assets are stocks of large-sized U.S. companies. The data on this page is unaudited. The data on this page represents past performance and is not a guarantee of future results. Investment returns and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Six-month returns are not annualized. The average annual total return numbers include changes in the Fund’s or Index’s share price, plus reinvestment of any dividends and capital gains. The Fund’s performance is after all fees and expenses, whereas the Index does not incur fees or expenses. A shareholder cannot invest directly in the S&P 500 Index. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The S&P 500 Index is the established benchmark. Current performance may be lower or higher than the performance data quoted. To obtain performance data current to the most recent month end, please call 1-800-541-0170.

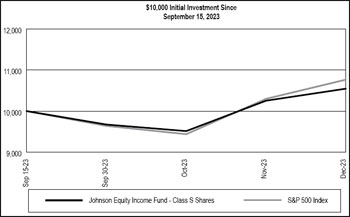

| JOHNSON EQUITY INCOME FUND | PERFORMANCE REVIEW – DECEMBER 31, 2023 |

| AVERAGE ANNUAL TOTAL RETURNS | AS OF DECEMBER 31, 2023 |

| | EQUITY INCOME FUND | |

| | — CLASS S SHARES | S&P 500 INDEX |

| SINCE INCEPTION* | 5.46% | 7.66% |

| * | Inception date was September 15, 2023 |

Above average dividend income and long-term capital growth is the objective of the Johnson Equity Income Fund, and the primary assets are stocks of large-sized U.S. companies. The data on this page is unaudited. The data on this page represents past performance and is not a guarantee of future results. Investment returns and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Six-month returns are not annualized. The average annual total return numbers include changes in the Fund’s or Index’s share price, plus reinvestment of any dividends and capital gains. The Fund’s performance is after all fees and expenses, whereas the Index does not incur fees or expenses. A shareholder cannot invest directly in the S&P 500 Index. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The S&P 500 Index is the established benchmark. Current performance may be lower or higher than the performance data quoted. To obtain performance data current to the most recent month end, please call 1-800-541-0170.

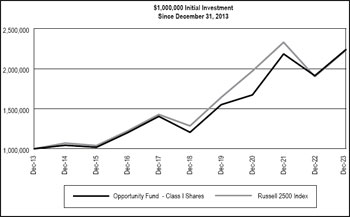

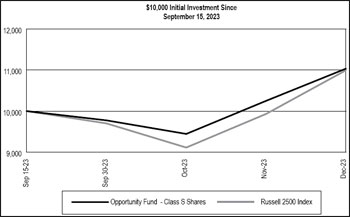

| JOHNSON OPPORTUNITY FUND | PERFORMANCE REVIEW – DECEMBER 31, 2023 |

The Johnson Opportunity Fund delivered a net total return of +17.12% in 2023, slightly trailing the Russell 2500 Index’s +17.42% return. It was a year of ebb and flow for SMID (small to mid) Cap stocks, with four major market corrections occurring within the year, notably a more than 20% decline following a banking industry crisis in March that led to a few large bank failures. Markets also grappled with interest rate volatility, assessing when Federal Reserve policy would transition from tightening to easing. As the Fed communicated a more dovish message late in the year, stocks finished the final two months of 2023 with a robust market rally.

The Fund’s performance in 2023 benefited from its strategic preference for high quality stocks. The team’s quantitative factor inputs emphasizing quality, valuation, and momentum were also a favorable influence. Sector positioning and security selection had positive attribution effects, and the slight Fund underperformance on a net basis can be attributed to fees and the drag of a small cash position.

The top contributing stock was Hawkins, a specialty chemicals manufacturer benefiting from robust pricing trends that drove record cash flows and balance sheet strengthening. Other top performers included Coca-Cola Consolidated, a distributor of Coca-Cola brands, and Fair Isaac Corp., best known for its FICO score credit assessment product. Both stocks were driven higher by robust earnings growth that exceeded market expectations. An overweight position in Industrials proved valuable with nVent Electric and Watsco among the biggest winners. A strategic underweight position in the Energy sector also proved advantageous as oil prices slid 11% over the course of the year.

On the downside, the worst performing stock was Signature Bank, which was taken over by regulators after an unexpected bank run on deposits, rendering its shares nearly worthless. The Health Care sector was a material underperformer for the year and included many of the Fund’s bottom performers, including AMN Healthcare Services, Jazz Pharmaceuticals, and Global Medical. This sector has faced challenges in the post-pandemic recovery and many companies continued to have disappointing earnings as they struggled to resume normal growth trends.

Market valuation appears contingent on companies achieving the mid-teens earnings growth rate indicated by the 2024 consensus. While annual forecasts often begin with such growth expectations, they rarely finish there as the year progresses. It is troubling to see that revision trends have not yet turned positive, and growth rates would likely still turn negative in a recession, which remains a threat. Amid a year marked by transitioning monetary policy, significant U.S. elections, and ongoing international conflicts, the team maintains a bottom-up focus in the face of macroeconomic uncertainty. Quality investing minimizes the reliance on timing the market cycle and aligns with companies well-equipped to navigate hard-to-predict market environments.

| AVERAGE ANNUAL TOTAL RETURNS | AS OF DECEMBER 31, 2023 |

| | OPPORTUNITY | |

| | FUND | |

| | — CLASS I SHARES | RUSSELL 2500 INDEX |

| ONE YEAR | 17.12% | 17.42% |

| THREE YEARS | 10.22% | 4.24% |

| FIVE YEARS | 13.18% | 11.67% |

| TEN YEARS | 8.39% | 8.36% |

| HOLDINGS BY INDUSTRY SECTOR |

| | | % OF |

| SECTOR ALLOCATION | | NET ASSETS |

| TECHNOLOGY | | | 21.1 | % |

| INDUSTRIALS | | | 17.1 | % |

| FINANCIALS | | | 12.8 | % |

| HEALTH CARE | | | 12.2 | % |

| MATERIALS | | | 9.5 | % |

| CONSUMER DISCRETIONARY | | | 9.1 | % |

| REAL ESTATE | | | 6.0 | % |

| UTILITIES | | | 4.0 | % |

| CONSUMER STAPLES | | | 3.2 | % |

| ENERGY | | | 2.4 | % |

| MONEY MARKET FUNDS | | | 1.4 | % |

| COMMUNICATIONS | | | 1.3 | % |

| OTHER: | | | | |

| NET OTHER ASSETS (LIABILITIES) | | | -0.1 | % |

| | | | 100.0 | % |

Long-term capital growth is the objective of the Johnson Opportunity Fund, and the primary assets are equity securities of medium sized companies. The data on this page is unaudited. The data on this page represents past performance and is not a guarantee of future results. Investment returns and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The average annual total return numbers include changes in the Fund’s or Index’s share price, plus reinvestment of any dividends and capital gains. Six-month returns are not annualized. The Fund’s performance is after all fees and expenses, whereas the Index does not incur fees or expenses. A shareholder cannot invest directly in the Russell 2500 Index. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The Russell 2500 Index is the established benchmark. Current performance may be lower or higher than the performance data quoted. To obtain performance data current to the most recent month end, please call 1-800-541-0170.

| JOHNSON OPPORTUNITY FUND | PERFORMANCE REVIEW – DECEMBER 31, 2023 |

| AVERAGE ANNUAL TOTAL RETURNS | AS OF DECEMBER 31, 2023 |

| | OPPORTUNITY FUND | |

| | — CLASS S SHARES | RUSSELL 2500 INDEX |

| SINCE INCEPTION* | 10.35% | 9.95% |

| * | Inception date was September 15, 2023 |

Long-term capital growth is the objective of the Johnson Opportunity Fund, and the primary assets are equity securities of medium sized companies. The data on this page is unaudited. The data on this page represents past performance and is not a guarantee of future results. Investment returns and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The average annual total return numbers include changes in the Fund’s or Index’s share price, plus reinvestment of any dividends and capital gains. Six-month returns are not annualized. The Fund’s performance is after all fees and expenses, whereas the Index does not incur fees or expenses. A shareholder cannot invest directly in the Russell 2500 Index. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The Russell 2500 Index is the established benchmark. Current performance may be lower or higher than the performance data quoted. To obtain performance data current to the most recent month end, please call 1-800-541-0170.

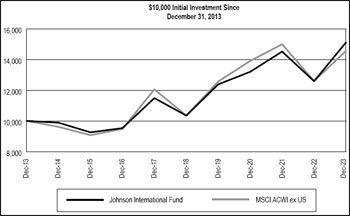

| JOHNSON INTERNATIONAL FUND | PERFORMANCE REVIEW – DECEMBER 31, 2023 |

The Johnson International Fund had a total net return of +20.07% in 2023, outperforming the MSCI ACWI ex-US Index’s +15.62% return. This result placed the Fund in the top 20% of funds within its Morningstar Foreign Large Value peer group for the calendar year.

Without its own group of mega-cap technology stocks driving index returns higher, the less concentrated MSCI ACWI ex-US Index lagged the more technology-weighted US stock market. The positive absolute international returns were despite foreign company earnings slipping into negative growth and were further explained by rising valuation. Stocks corrected in August through October as interest rates rose but recaptured those losses in the final months of the year as the economy continued to avoid a decline, and investors looked ahead to the end of tight central bank monetary policies.

The Fund’s outperformance can mostly be attributed to positive security selection, which was shown in eight of the eleven sectors. An overweight tilt in developed markets (+18.2%) versus emerging markets (+9.8%) was also additive. The top performing Technology sector was a favorable overweight position, reflecting high demand for capacity-constrained products and capturing optimism for secular growth related to artificial intelligence. Five of the top ten stocks were from the Technology space, including Lenovo Group, Open Text, United Microelectronics, Taiwan Semiconductor Manufacturing, and SAP. Another significant contributor was Novo Nordisk, whose earnings boomed in large part due to its first mover advantage in the marketing of GLP-1 weight loss drugs.

Chinese stocks broadly declined for the second straight year, and this included many of the Fund’s weakest performers, including Daqo New Energy, JD.com, Alibaba Group, and Tencent Holdings. The Fund was underweight Chinese stocks, though, which added value. The most negative stock contributor was Kering, a luxury apparel and accessories company known for its Gucci brand that struggled to grow as expected due to a weak Chinese consumer and poor brand momentum.

Earnings revision trends have not yet turned positive, and a global recession remains a threat. The direction of the global economy and stock markets is likely to be shaped by the success of central bank monetary policy transitions and the course of events in ongoing international conflicts (both military and political). In the face of macroeconomic uncertainty, valuation can help buffer a riskier path. If the economy sees a soft-landing recovery, international stocks, after lagging U.S. stocks for multiple years, may see a relative growth rate advantage as well, as companies return to positive earnings growth after a down year for profits.

| AVERAGE ANNUAL TOTAL RETURNS | AS OF DECEMBER 31, 2023 |

| | INTERNATIONAL | MSCI ACWI EX US |

| | FUND | INDEX |

| ONE YEAR | 20.03% | 15.62% |

| THREE YEARS | 4.61% | 1.55% |

| FIVE YEARS | 7.87% | 7.08% |

| TEN YEARS | 4.21% | 3.83% |

| HOLDINGS BY COUNTRY |

| % OF TOTAL INVESTMENTS | | AS OF DECEMBER 31, 2023 |

| JAPAN | 16.66% | | AUSTRALIA | 2.17% |

| UNITED KINGDOM | 10.45% | | MEXICO | 2.80% |

| FRANCE | 9.18% | | UNITED STATES | 1.00% |

| CANADA | 8.38% | | INDIA | 2.47% |

| SWITZERLAND | 7.39% | | SOUTH KOREA | 2.45% |

| GERMANY | 6.97% | | SPAIN | 1.99% |

| TAIWAN | 3.76% | | BRAZIL | 2.75% |

| HONGKONG | 3.91% | | DENMARK | 2.29% |

| CHINA | 3.10% | | NETHERLANDS | 2.05% |

| CAYMAN ISLANDS | 2.38% | | OTHER* | 7.85% |

| * | Countries in “Other” category include: Israel, Italy, Jersey, Luxembourg, Phillipines, Russia, Singapore, South Africa and Sweden |

Long-term capital growth is the objective of the Johnson International Fund, and the primary assets are equity securities of foreign companies traded on U.S. exchanges and ADRs (American Depository Receipts). The data on this page is unaudited. The data on this page represents past performance and is not a guarantee of future results. Investment returns and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Six-month returns are not annualized. The average annual total return numbers include changes in the Fund’s or Index’s share price, plus reinvestment of any dividends and capital gains. The Fund’s performance is after all fees and expenses, whereas neither Index incurs fees nor expenses. A shareholder cannot invest directly in the MSCI ACWI ex US Index. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The MSCI ACWI ex US Index is the primary benchmark. Current performance may be lower or higher than the performance data quoted. To obtain performance data current to the most recent month end, please call 1-800-541-0170.

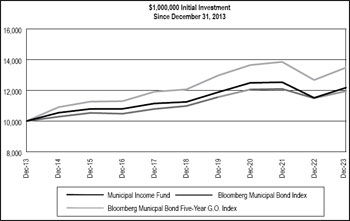

| JOHNSON MUNICIPAL INCOME FUND | PERFORMANCE REVIEW – DECEMBER 31, 2023 |

The Johnson Municipal Income fund provided a total return of 5.76% during 2023 compared to 6.40% for the Bloomberg Barclays Municipal Bond Index.

After rising sharply throughout 2022, municipal bond yields fell across every tenor of the curve in 2023 with majority of the downward move occurring toward the end of the year. Dovish communications from the Federal Reserve indicated the end of their rate hiking cycle following their acknowledgment of the progress made on inflation throughout the year. Tax-exempt municipal bonds outperformed most other fixed-income products as municipal bond yields rallied to a greater degree relative to U.S. treasury yields. Despite the strong performance, municipal bond mutual funds continued to experience outflows over the year as investors remained fearful of rising interest rates, and tax-loss harvesting activity continued. New municipal bond issuance in 2023 remained below that of 2022 and the trailing five-year average as issuers were reluctant to issue debt amidst the volatile interest rate environment and lackluster investor demand. Longer maturity bonds and lower quality issuers outperformed the general market as municipal bond rates fell and lower quality spreads tightened, as the low level of supply underwhelmed the market. As a result, the Fund’s longer duration positioning relative to its benchmark was a deterrent to performance while its focus on higher-quality securities acted as a headwind. We maintain a high-quality focus as lower quality securities remain expensive relative to prior periods and offer minimal compensation in terms of additional yield.

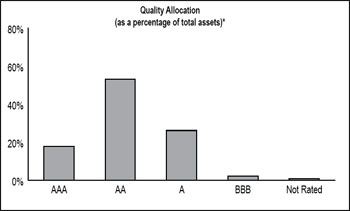

Investor sentiment regarding municipal credit health remained optimistic thanks to the tailwinds of strong tax revenue collection growth from pre-pandemic levels and a strong labor market. However, a degree of uncertainty remains for lower quality and economically sensitive-revenue dependent municipal issuers. Weakening economic conditions and the digestion of higher interest rates could result in a slowing of revenue collections, stretching the credit health of economically sensitive sectors. Still, higher-quality issuers’ balance sheets remain robust as reserve balances are near all-time highs, supporting a more advantageous foundation for a potential economic slowdown relative to lower quality. The Fund avoids economically sensitive securities by maintaining a strict focus on high quality municipal issuers, as over 71% of the Fund is rated AA or higher.

Looking forward to next year, municipal bond yields remain well-above decade-long averages across the curve, positioning municipal bonds to provide investors with meaningful current income and act as a reliable hedge against risk asset volatility. Despite proactive measures from the Fed to ease policy restrictions, a full cyclical upswing in the economy seems distant, leading the Fund to maintain a defensive posture in the portfolio driven by valuation paired with a modestly longer duration than the benchmark.

| AVERAGE ANNUAL TOTAL RETURNS | AS OF DECEMBER 31, 2023 |

| | | | BLOOMBERG |

| | MUNICIPAL | BLOOMBERG | MUNICIPAL |

| | INCOME | MUNICIPAL | BOND 5 YEAR |

| | FUND | BOND INDEX | GO INDEX |

| ONE YEAR | 5.76% | 6.40% | 4.05% |

| THREE YEARS | -0.85% | -0.40% | -0.30% |

| FIVE YEARS | 1.60% | 2.25% | 1.71% |

| TEN YEARS | 1.99% | 3.03% | 1.80% |

A high level of federally tax-free income over the long term consistent with preservation of capital is the objective of the Johnson Municipal Income Fund, and the primary assets are intermediate term Ohio municipal bonds. The data on this page is unaudited and represents past performance and is not a guarantee of future results. Investment returns and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Six-month returns are not annualized. The average annual total return numbers include changes in the Fund’s or Index’s share price, plus reinvestment of any income and capital gains. The Fund’s performance is after all fees and expenses, whereas the Index does not incur fees or expenses. A shareholder cannot invest directly in the Bloomberg Capital Municipal Bond Index nor in the Bloomberg Capital Five Year General Obligation Municipal Bond Index. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The Bloomberg Capital Municipal Bond Index is the primary benchmark, and the Bloomberg Capital Five Year General Obligation Municipal Bond Index is a supplementary index. Current performance may be lower or higher than the performance data quoted. To obtain performance data current to the most recent month end, please call 1-800-541-0170.

| JOHNSON MUNICIPAL INCOME FUND | PERFORMANCE REVIEW – DECEMBER 31, 2023 |

| * | As rated by either Standard & Poor’s or Moody’s Rating Agencies. |

(If rated by both, the lower rating is represented.)

| HOLDINGS BY STATE OF ISSUANCE % OF TOTAL INVESTMENTS |

| OHIO | 77.03% | | INDIANA | 1.26 |

| KENTUCKY | 6.47% | | SOUTH CAROLINA | 0.65% |

| N/A | 3.34% | | ALABAMA | 0.57% |

| MISSOURI | 2.89% | | VIRGINIA | 0.57% |

| PENNSYLVANIA | 2.70% | | GEORGIA | 0.54% |

| COLORADO | 1.80% | | MICHIGAN | 0.40% |

| TEXAS | 1.45% | | NORTH DAKOTA | 0.33% |

| EQUITY INCOME FUND | PORTFOLIO OF INVESTMENTS AS OF DECEMBER 31, 2023 |

| COMMON STOCKS — 99.0% | | Shares | | | Value | |

| Communications — 5.2% | | | | | | | | |

| Alphabet, Inc. - Class A (a) | | | 175,812 | | | $ | 24,559,178 | |

| Comcast Corp. - Class A | | | 177,800 | | | | 7,796,530 | |

| | | | | | | | 32,355,708 | |

| Consumer Discretionary — 6.7% | | | | | | | | |

| Genuine Parts Co. | | | 72,000 | | | | 9,972,000 | |

| Lowe’s Cos., Inc. | | | 57,000 | | | | 12,685,350 | |

| McDonald’s Corp. | | | 42,500 | | | | 12,601,675 | |

| TJX Cos., Inc. (The) | | | 65,485 | | | | 6,143,148 | |

| | | | | | | | 41,402,173 | |

| Consumer Staples — 7.7% | | | | | | | | |

| Coca-Cola Co. (The) | | | 215,320 | | | | 12,688,807 | |

| Estee Lauder Cos., Inc. (The) - Class A | | | 80,000 | | | | 11,700,000 | |

| PepsiCo, Inc. | | | 35,900 | | | | 6,097,256 | |

| Procter & Gamble Co. (The) | | | 36,690 | | | | 5,376,553 | |

| Walmart, Inc. | | | 75,555 | | | | 11,911,246 | |

| | | | | | | | 47,773,862 | |

| Energy — 5.9% | | | | | | | | |

| Chevron Corp. | | | 125,760 | | | | 18,758,362 | |

| Williams Cos., Inc. (The) | | | 514,300 | | | | 17,913,069 | |

| | | | | | | | 36,671,431 | |

| Financials — 13.6% | | | | | | | | |

| American Financial Group, Inc. | | | 158,900 | | | | 18,891,621 | |

| Axis Capital Holdings Ltd. | | | 215,050 | | | | 11,907,319 | |

| Everest Group Ltd. | | | 30,200 | | | | 10,678,116 | |

| Marsh & McLennan Cos., Inc. | | | 61,600 | | | | 11,671,352 | |

| Nasdaq, Inc. | | | 349,300 | | | | 20,308,302 | |

| Willis Towers Watson plc | | | 44,870 | | | | 10,822,644 | |

| | | | | | | | 84,279,354 | |

| Health Care — 15.2% | | | | | | | | |

| Abbott Laboratories | | | 100,518 | | | | 11,064,016 | |

| Cencora, Inc. | | | 94,000 | | | | 19,305,719 | |

| Danaher Corp. | | | 75,343 | | | | 17,429,849 | |

| Medtronic plc | | | 108,836 | | | | 8,965,910 | |

| UnitedHealth Group, Inc. | | | 35,250 | | | | 18,558,068 | |

| Zimmer Biomet Holdings, Inc. | | | 103,900 | | | | 12,644,630 | |

| Zoetis, Inc. | | | 32,892 | | | | 6,491,894 | |

| | | | | | | | 94,460,086 | |

| Industrials — 12.1% | | | | | | | | |

| Amphenol Corp. - Class A | | | 132,300 | | | | 13,114,899 | |

| Honeywell International, Inc. | | | 53,350 | | | | 11,188,029 | |

| Illinois Tool Works, Inc. | | | 52,000 | | | | 13,620,880 | |

| Nordson Corp. | | | 46,300 | | | | 12,230,608 | |

| Northrop Grumman Corp. | | | 27,000 | | | | 12,639,780 | |

| Waste Management, Inc. | | | 68,600 | | | | 12,286,260 | |

| | | | | | | | 75,080,456 | |

| Real Estate — 2.1% | | | | | | | | |

| American Tower Corp. | | | 61,187 | | | | 13,209,050 | |

| COMMON STOCKS — 99.0% | | Shares | | | Value | |

| Technology — 24.6% | | | | | | | | |

| Accenture plc - Class A | | | 41,790 | | | $ | 14,664,528 | |

| Adobe, Inc. (a) | | | 20,060 | | | | 11,967,796 | |

| Analog Devices, Inc. | | | 59,200 | | | | 11,754,752 | |

| Apple,Inc. | | | 61,760 | | | | 11,890,653 | |

| ASML Holding N.V. | | | 9,100 | | | | 6,887,972 | |

| Intuit, Inc. | | | 21,250 | | | | 13,281,888 | |

| Mastercard, Inc. - Class A | | | 29,750 | | | | 12,688,673 | |

| Microsoft Corp. | | | 60,260 | | | | 22,660,169 | |

| Roper Technologies, Inc. | | | 26,000 | | | | 14,174,420 | |

| S&P Global,Inc. | | | 28,657 | | | | 12,623,982 | |

| Taiwan Semiconductor Manufacturing Co. Ltd. - ADR | | | 63,000 | | | | 6,552,000 | |

| Visa, Inc. - Class A | | | 50,600 | | | | 13,173,710 | |

| | | | | | | | 152,320,543 | |

| Utilities — 5.9% | | | | | | | | |

| Alliant Energy Corp. | | | 352,910 | | | | 18,104,283 | |

| American Electric Power Co., Inc. | | | 227,600 | | | | 18,485,672 | |

| | | | | | | | 36,589,955 | |

| Total Common Stocks | | | | | | | | |

| (Cost $436,991,063) | | | | | | $ | 614,142,618 | |

| | | | | | | | | |

| MONEY MARKET FUNDS — 0.9% | | | | | | | | |

| First American Government Obligations Fund - Class Z, 5.25% (b) (Cost $5,511,764) | | | 5,511,764 | | | | 5,511,764 | |

| | | | | | | | | |

| Investments at Value — 99.9% | | | | | | | | |

| (Cost $442,502,827) | | | | | | $ | 619,654,382 | |

| | | | | | | | | |

| Other Assets in Excess of Liabilities — 0.1% | | | | | | | 502,027 | |

| | | | | | | | | |

| Net Assets — 100.0% | | | | | | $ | 620,156,409 | |

| (a) | Non-income producing security. |

| (b) | The rate shown is the 7-day effective yield as of December 31, 2023. |

ADR - American Depositary Receipt

N.V. - Naamloze Vennootschap

plc - Public Limited Company

| The accompanying notes are an integral part of these financial statements. |

| OPPORTUNITY FUND | PORTFOLIO OF INVESTMENTS AS OF DECEMBER 31, 2023 |

| COMMON STOCKS — 98.7% | | Shares | | | Value | |

| Communications — 1.3% | | | | | | | | |

| New York Times Co. (The) - Class A | | | 34,300 | | | $ | 1,680,357 | |

| | | | | | | | | |

| Consumer Discretionary — 9.1% | | | | | | | | |

| Floor & Decor Holdings, Inc. - Class A (a) | | | 9,900 | | | | 1,104,444 | |

| LKQ Corp. | | | 40,100 | | | | 1,916,379 | |

| NVR, Inc. (a) | | | 250 | | | | 1,750,113 | |

| Rush Enterprises, Inc. - Class A | | | 38,100 | | | | 1,916,430 | |

| Steven Madden Ltd. | | | 42,300 | | | | 1,776,600 | |

| Texas Roadhouse, Inc. | | | 11,900 | | | | 1,454,537 | |

| Williams-Sonoma, Inc. | | | 10,900 | | | | 2,199,402 | |

| | | | | | | | 12,117,905 | |

| Consumer Staples — 3.2% | | | | | | | | |

| BJ’s Wholesale Club Holdings, Inc. (a) | | | 28,700 | | | | 1,913,142 | |

| Coca-Cola Consolidated, Inc. | | | 2,500 | | | | 2,321,000 | |

| | | | | | | | 4,234,142 | |

| Energy — 2.4% | | | | | | | | |

| DT Midstream, Inc. | | | 25,000 | | | | 1,370,000 | |

| World Kinect Corp. | | | 81,300 | | | | 1,852,014 | |

| | | | | | | | 3,222,014 | |

| Financials — 12.8% | | | | | | | | |

| American Financial Group, Inc. | | | 18,000 | | | | 2,140,020 | |

| Arrow Financial Corp. | | | 55,597 | | | | 1,553,380 | |

| Axis Capital Holdings Ltd. | | | 36,700 | | | | 2,032,079 | |

| Diamond Hill Investment Group, Inc. | | | 4,900 | | | | 811,391 | |

| East West Bancorp, Inc. | | | 28,700 | | | | 2,064,965 | |

| Everest Group Ltd. | | | 5,400 | | | | 1,909,332 | |

| Farmers National Banc Corp. | | | 100,400 | | | | 1,450,780 | |

| SEI Investments Co. | | | 35,100 | | | | 2,230,605 | |

| Wintrust Financial Corp. | | | 30,300 | | | | 2,810,325 | |

| | | | | | | | 17,002,877 | |

| Health Care — 12.2% | | | | | | | | |

| Charles River Laboratories International, Inc. (a) | | | 12,000 | | | | 2,836,800 | |

| Chemed Corp. | | | 3,500 | | | | 2,046,625 | |

| Jazz Pharmaceuticals plc (a) | | | 11,600 | | | | 1,426,800 | |

| LeMaitre Vascular, Inc. | | | 35,400 | | | | 2,009,304 | |

| Option Care Health, Inc. (a) | | | 55,500 | | | | 1,869,795 | |

| Quest Diagnostics, Inc. | | | 7,100 | | | | 978,948 | |

| Repligen Corp. (a) | | | 9,900 | | | | 1,780,020 | |

| U.S. Physical Therapy, Inc. | | | 19,400 | | | | 1,806,916 | |

| Universal Health Services, Inc. - Class B | | | 10,200 | | | | 1,554,888 | |

| | | | | | | | 16,310,096 | |

| Industrials — 17.1% | | | | | | | | |

| A.O. Smith Corp. | | | 30,900 | | | | 2,547,396 | |

| AMN Healthcare Services, Inc. (a) | | | 19,700 | | | | 1,475,136 | |

| COMMON STOCKS — 98.7% | | Shares | | | Value | |

| Applied Industrial Technologies, Inc. | | | 14,700 | | | $ | 2,538,543 | |

| Comfort Systems USA, Inc. | | | 6,200 | | | | 1,275,154 | |

| Core & Main, Inc. - Class A (a) | | | 31,900 | | | | 1,289,079 | |

| Donaldson Co., Inc. | | | 29,100 | | | | 1,901,685 | |

| Gorman-Rupp Co. (The) | | | 50,500 | | | | 1,794,265 | |

| Hubbell, Inc. | | | 5,200 | | | | 1,710,436 | |

| IDEX Corp. | | | 6,900 | | | | 1,498,059 | |

| Littelfuse, Inc. | | | 4,600 | | | | 1,230,776 | |

| Nordson Corp. | | | 9,300 | | | | 2,456,688 | |

| SiteOne Landscape Supply, Inc. (a) | | | 8,200 | | | | 1,332,500 | |

| Watts Water Technologies, Inc. - Class A | | | 8,400 | | | | 1,750,056 | |

| | | | | | | | 22,799,773 | |

| Materials — 9.5% | | | | | | | | |

| Avery Dennison Corp. | | | 11,600 | | | | 2,345,056 | |

| H.B. Fuller Co. | | | 27,600 | | | | 2,246,916 | |

| Hawkins, Inc. | | | 34,000 | | | | 2,394,280 | |

| Reliance Steel & Aluminum Co. | | | 3,400 | | | | 950,912 | |

| RPM International, Inc. | | | 15,600 | | | | 1,741,428 | |

| Sonoco Products Co. | | | 26,700 | | | | 1,491,729 | |

| UFP Industries, Inc. | | | 11,700 | | | | 1,468,935 | |

| | | | | | | | 12,639,256 | |

| Real Estate — 6.0% | | | | | | | | |

| Camden Property Trust | | | 6,400 | | | | 635,456 | |

| Community Healthcare Trust, Inc. | | | 49,300 | | | | 1,313,352 | |

| Equity LifeStyle Properties, Inc. | | | 13,000 | | | | 917,020 | |

| Jones Lang LaSalle, Inc. (a) | | | 8,800 | | | | 1,662,056 | |

| NNN REIT, Inc. | | | 46,900 | | | | 2,021,390 | |

| STAG Industrial, Inc. | | | 37,400 | | | | 1,468,324 | |

| | | | | | | | 8,017,598 | |

| Technology — 21.1% | | | | | | | | |

| Amdocs Ltd. | | | 18,600 | | | | 1,634,754 | |

| Bentley Systems, Inc. - Class B | | | 25,200 | | | | 1,314,936 | |

| Blackbaud, Inc. (a) | | | 23,800 | | | | 2,063,460 | |

| CACI International, Inc. - Class A (a) | | | 5,300 | | | | 1,716,458 | |

| Dynatrace, Inc. (a) | | | 36,600 | | | | 2,001,654 | |

| Fair Isaac Corp. (a) | | | 1,200 | | | | 1,396,812 | |

| Genpact Ltd. | | | 42,200 | | | | 1,464,762 | |

| Globant S.A. (a) | | | 5,700 | | | | 1,356,486 | |

| ICF International, Inc. | | | 8,700 | | | | 1,166,583 | |

| Jack Henry & Associates, Inc. | | | 8,400 | | | | 1,372,644 | |

| Leidos Holdings, Inc. | | | 19,700 | | | | 2,132,328 | |

| MAXIMUS, Inc. | | | 22,800 | | | | 1,912,008 | |

| Paylocity Holding Corp. (a) | | | 6,900 | | | | 1,137,465 | |

| PTC, Inc. (a) | | | 9,200 | | | | 1,609,632 | |

| Sapiens International Corp. N.V. | | | 57,300 | | | | 1,658,262 | |

| Tyler Technologies, Inc. (a) | | | 4,350 | | | | 1,818,822 | |

| WEX, Inc. (a) | | | 4,900 | | | | 953,295 | |

| The accompanying notes are an integral part of these financial statements. |

| OPPORTUNITY FUND | PORTFOLIO OF INVESTMENTS AS OF DECEMBER 31, 2023 |

| COMMON STOCKS — 98.7% | | Shares | | | Value | |

| Zebra Technologies Corp. - Class A (a) | | | 5,000 | | | $ | 1,366,650 | |

| | | | | | | | 28,077,011 | |

| Utilities — 4.0% | | | | | | | | |

| Atmos Energy Corp. | | | 14,500 | | | | 1,680,550 | |

| Portland General Electric Co. | | | 32,200 | | | | 1,395,548 | |

| Unitil Corp. | | | 42,200 | | | | 2,218,454 | |

| | | | | | | | 5,294,552 | |

| Total Common Stocks | | | | | | | | |

| (Cost $103,192,570) | | | | | | $ | 131,395,581 | |

| | | | | | | | | |

| MONEY MARKET FUNDS — 1.4% | | | | | | | | |

| First American Government Obligations Fund - Class Z, 5.25% (b) (Cost $1,865,482) | | | 1,865,482 | | | | 1,865,482 | |

| | | | | | | | | |

| Investments at Value — 100.1% | | | | | | | | |

| (Cost $105,058,052) | | | | | | $ | 133,261,063 | |

| | | | | | | | | |

| Liabilities in Excess of Other Assets — (0.1%) | | | | | | | (135,531 | ) |

| | | | | | | | | |

| Net Assets — 100.0% | | | | | | $ | 133,125,532 | |

| (a) | Non-income producing security. |

| (b) | The rate shown is the 7-day effective yield as of December 31, 2023. |

N.V. - Naamloze Vennootschap

plc - Public Limited Company

S.A. - Societe Anonyme

| The accompanying notes are an integral part of these financial statements. |

| INTERNATIONAL FUND | PORTFOLIO OF INVESTMENTS AS OF DECEMBER 31, 2023 |

| COMMON STOCKS — 98.7% | | Shares | | | Value | |

| Communications — 8.8% | | | | | | | | |

| Baidu, Inc. - ADR (a) | | | 1,800 | | | $ | 214,362 | |

| Deutsche Telekom AG - ADR | | | 7,100 | | | | 171,323 | |

| KDDI Corp. - ADR | | | 22,600 | | | | 355,950 | |

| Orange S.A. - ADR | | | 7,500 | | | | 85,725 | |

| PDLT, Inc. - ADR | | | 11,000 | | | | 257,730 | |

| Publicis Groupe S.A. - ADR | | | 22,100 | | | | 512,366 | |

| RTL Group S.A. - ADR | | | 15,000 | | | | 57,929 | |

| SK Telecom Co. Ltd. - ADR | | | 4,600 | | | | 98,440 | |

| Tencent Holdings Ltd. - ADR | | | 8,400 | | | | 317,436 | |

| WPP plc - ADR | | | 1,800 | | | | 85,626 | |

| | | | | | | | 2,156,887 | |

| Consumer Discretionary — 8.2% | | | | | | | | |

| Alibaba Group Holding Ltd. - ADR | | | 2,000 | | | | 155,020 | |

| Bridgestone Corp. - ADR | | | 8,200 | | | | 168,510 | |

| Bunzl plc - ADR | | | 7,700 | | | | 315,238 | |

| CIE Financiere Richemont S.A. - ADR | | | 22,000 | | | | 303,050 | |

| Daimler Truck Holding AG - ADR | | | 2,200 | | | | 41,140 | |

| Honda Motor Co. Ltd. - ADR | | | 5,500 | | | | 170,005 | |

| JD.com, Inc. - ADR | | | 1,700 | | | | 49,113 | |

| Magna International, Inc. | | | 6,000 | | | | 354,480 | |

| Mercedes-Benz Group AG | | | 3,600 | | | | 248,760 | |

| Toyota Motor Corp. - ADR | | | 1,100 | | | | 201,718 | |

| | | | | | | | 2,007,034 | |

| Consumer Staples — 8.2% | | | | | | | | |

| ITOCHU Corp. - ADR | | | 3,700 | | | | 301,328 | |

| L’Oreal S.A. - ADR | | | 2,800 | | | | 278,348 | |

| Nestlé S.A. - ADR | | | 2,800 | | | | 323,764 | |

| Reckitt Benckiser Group plc - ADR | | | 5,900 | | | | 81,066 | |

| Shoprite Holdings Ltd. - ADR | | | 32,100 | | | | 474,599 | |

| Unilever plc - ADR | | | 2,200 | | | | 106,656 | |

| Wal-Mart de Mexico S.A.B. de C.V.-ADR | | | 10,600 | | | | 447,532 | |

| | | | | | | | 2,013,293 | |

| Energy — 3.1% | | | | | | | | |

| BP plc - ADR | | | 4,000 | | | | 141,600 | |

| Gazprom PJSC - ADR (a)(b) | | | 14,000 | | | | 140 | |

| Shell plc - ADR | | | 4,600 | | | | 302,680 | |

| TotalEnergies SE - ADR | | | 2,352 | | | | 158,478 | |

| Woodside Energy Group Ltd. - ADR | | | 7,599 | | | | 160,263 | |

| | | | | | | | 763,161 | |

| Financials — 19.0% | | | | | | | | |

| Admiral Group plc - ADR | | | 8,200 | | | | 278,718 | |

| Allianz SE - ADR | | | 10,700 | | | | 285,583 | |

| Banco Santander S.A. - ADR | | | 37,155 | | | | 153,822 | |

| Bank of Montreal | | | 1,240 | | | | 122,686 | |

| Barclays plc - ADR | | | 15,000 | | | | 118,200 | |

| BNP Paribas S.A. - ADR | | | 6,100 | | | | 211,914 | |

| COMMON STOCKS — 98.7% | | Shares | | | Value | |

| China Construction Bank Corp. - ADR | | | 23,000 | | | $ | 273,010 | |

| Deutsche Boerse AG - ADR | | | 7,000 | | | | 143,815 | |

| Industrial & Commercial Bank of China Ltd. - ADR | | | 33,800 | | | | 328,536 | |

| KB Financial Group, Inc. - ADR | | | 2,400 | | | | 99,288 | |

| Legal & General Group plc - ADR | | | 9,900 | | | | 161,964 | |

| Manulife Financial Corp. | | | 7,720 | | | | 170,612 | |

| Mitsubishi UFJ Financial Group, Inc. - ADR | | | 40,000 | | | | 344,400 | |

| ORIX Corp. - ADR | | | 2,450 | | | | 228,806 | |

| Royal Bank of Canada | | | 1,900 | | | | 192,147 | |

| Sumitomo Mitsui Financial Group, Inc. - ADR | | | 56,100 | | | | 543,047 | |

| Tokio Marine Holdings, Inc. - ADR | | | 18,900 | | | | 470,988 | |

| Toronto-Dominion Bank (The) | | | 2,700 | | | | 174,474 | |

| United Overseas Bank Ltd. - ADR | | | 4,100 | | | | 177,448 | |

| Zurich Insurance Group AG - ADR | | | 3,240 | | | | 169,403 | |

| | | | | | | | 4,648,861 | |

| Health Care — 9.5% | | | | | | | | |

| Alcon, Inc. | | | 2,900 | | | | 226,548 | |

| Astellas Pharma, Inc. - ADR | | | 17,600 | | | | 209,440 | |

| Bayer AG - ADR | | | 10,700 | | | | 98,761 | |

| Dr. Reddy’s Laboratories Ltd. - ADR | | | 3,340 | | | | 232,397 | |

| Novartis AG - ADR | | | 2,480 | | | | 250,406 | |

| Novo Nordisk A/S - ADR | | | 5,400 | | | | 558,630 | |

| Roche Holding AG - ADR | | | 10,500 | | | | 380,415 | |

| Sandoz Group A.G. - ADR (a) | | | 496 | | | | 15,877 | |

| Sanofi - ADR | | | 2,000 | | | | 99,460 | |

| Takeda Pharmaceutical Co. Ltd. - ADR | | | 9,340 | | | | 133,282 | |

| Taro Pharmaceutical Industries Ltd. (a) | | | 3,000 | | | | 125,340 | |

| | | | | | | | 2,330,556 | |

| Industrials — 7.8% | | | | | | | | |

| ABB Ltd. - ADR | | | 2,900 | | | | 128,470 | |

| Accelleron Industries AG | | | 145 | | | | 4,520 | |

| Atlas Copco AB - ADR | | | 28,400 | | | | 488,764 | |

| BAE Systems plc - ADR | | | 3,800 | | | | 219,708 | |

| Compass Group plc - ADR | | | 6,500 | | | | 180,765 | |

| Schneider Electric SE - ADR | | | 13,200 | | | | 531,037 | |

| Sensata Technologies Holding plc | | | 2,200 | | | | 82,654 | |

| Siemens AG - ADR | | | 2,900 | | | | 271,266 | |

| | | | | | | | 1,907,184 | |

| Materials — 9.9% | | | | | | | | |

| Air Liquide S.A. - ADR | | | 5,025 | | | | 195,724 | |

| BASF SE - ADR | | | 7,400 | | | | 99,308 | |

| BHP Group Ltd. - ADR | | | 5,400 | | | | 368,874 | |

| Cemex S.A.B. de C.V. - ADR (a) | | | 30,300 | | | | 234,825 | |

| The accompanying notes are an integral part of these financial statements. |

| INTERNATIONAL FUND | PORTFOLIO OF INVESTMENTS AS OF DECEMBER 31, 2023 |

| COMMON STOCKS — 98.7% | | Shares | | | Value | |

| Companhia Siderurgica Nacional S.A.-ADR | | | 57,100 | | | $ | 224,403 | |

| Newmont Corp. - ADR | | | 4,360 | | | | 180,460 | |

| Nitto Denko Corp. - ADR | | | 9,000 | | | | 335,160 | |

| POSCO Holdings, Inc. - ADR | | | 4,200 | | | | 399,462 | |

| Rio Tinto plc - ADR | | | 1,570 | | | | 116,902 | |

| Vale S.A. - ADR | | | 17,300 | | | | 274,378 | |

| | | | | | | | 2,429,496 | |

| Real Estate — 1.6% | | | | | | | | |

| Sun Hung Kai Properties Ltd. - ADR | | | 34,700 | | | | 374,760 | |

| | | | | | | | | |

| Technology — 19.1% | | | | | | | | |

| ASML Holding N.V. | | | 660 | | | | 499,567 | |

| Capgemini SE - ADR | | | 4,000 | | | | 167,400 | |

| CGI, Inc. (a) | | | 5,100 | | | | 546,771 | |

| Infosys Ltd. - ADR | | | 20,100 | | | | 369,438 | |

| Lenovo Group Ltd. - ADR | | | 20,700 | | | | 578,979 | |

| Open Text Corp. | | | 11,500 | | | | 483,230 | |

| PDD Holdings, Inc. - ADR (a) | | | 1,200 | | | | 175,572 | |

| RELX plc - ADR | | | 4,200 | | | | 166,572 | |

| SAPSE-ADR | | | 2,200 | | | | 340,098 | |

| Sony Group Corp. - ADR | | | 4,500 | | | | 426,105 | |

| Taiwan Semiconductor Manufacturing Co. Ltd. - ADR | | | 4,300 | | | | 447,200 | |

| United Microelectronics Corp. - ADR | | | 55,700 | | | | 471,222 | |

| | | | | | | | 4,672,154 | |

| Utilities — 3.5% | | | | | | | | |

| Enel S.p.A. - ADR | | | 33,700 | | | | 249,212 | |

| Iberdrola S.A. - ADR | | | 6,300 | | | | 330,749 | |

| National Grid plc - ADR | | | 1,629 | | | | 110,756 | |

| SSE plc - ADR | | | 6,900 | | | | 165,738 | |

| | | | | | | | 856,455 | |

| | | | | | | | | |

| Total Common Stocks | | | | | | | | |

| (Cost $16,916,192) | | | | | | $ | 24,159,841 | |

| PREFERRED STOCKS — 0.7% | | Shares | | | Value | |

| Financials — 0.7% | | | | | | | | |

| Itau Unibanco Holding S.A. - ADR (Cost $129,573) | | | 24,800 | | | $ | 172,360 | |

| | | | | | | | | |

| MONEY MARKET FUNDS — 0.3% | | | | | | | | |

| First American Government Obligations Fund - Class Z, 5.25% (c) (Cost $63,663) | | | 63,663 | | | | 63,663 | |

| | | | | | | | | |

| Investments at Value — 99.7% | | | | | | | | |

| (Cost $17,109,428) | | | | | | $ | 24,395,864 | |

| | | | | | | | | |

| Other Assets in Excess of Liabilities — 0.3% | | | | | | | 55,055 | |

| | | | | | | | | |

| Net Assets — 100.0% | | | | | | $ | 24,450,869 | |

| (a) | Non-income producing security. |

| (b) | This security is currently restricted from trading and is valued using Level 3 inputs as of December 31, 2023. The total fair value of Level 3 securities as of December 31, 2023 is $140. |

| (c) | The rate shown is the 7-day effective yield as of December 31, 2023. |

A/S - Aktieselskab

AB - Aktiebolag

ADR - American Depositary Receipt

AG - Aktiengesellschaft

N.V. - Naamloze Vennootschap

plc - Public Limited Company

PJSC - Public Joint Stock Company

S.A. - Societe Anonyme

S.A.B. de C.V. - Societe Anonima Bursatil de Capital Variable

S.p.A. - Societa per azioni

SE - Societe Europaea

| The accompanying notes are an integral part of these financial statements. |

| MUNICIPAL INCOME FUND | PORTFOLIO OF INVESTMENTS AS OF DECEMBER 31, 2023 |

| MUNICIPAL BONDS — 99.0% | | Coupon | | Maturity | | Par Value | | | Value | |

| General Obligation - City — 6.9% | | | | | | | | | | | | |

| Cincinnati Ohio GO Unlimited, Series 2017-A | | 4.000% | | 12/01/32 | | $ | 1,000,000 | | | $ | 1,057,826 | |

| Columbus Ohio GO Unlimited, Series 2015-A | | 3.000% | | 07/01/27 | | | 2,565,000 | | | | 2,560,468 | |

| Columbus Ohio GO Unlimited, Series 2022-A | | 5.000% | | 04/01/38 | | | 750,000 | | | | 866,900 | |

| Columbus Ohio GO Unlimited, Series 2022-A | | 5.000% | | 04/01/41 | | | 3,120,000 | | | | 3,557,033 | |

| Copley Township Ohio Safety Facilities Improvement, Series 2023 | | 4.000% | | 12/01/36 | | | 775,000 | | | | 807,070 | |

| Copley Township Ohio Safety Facilities Improvement, Series 2023 | | 4.000% | | 12/01/37 | | | 810,000 | | | | 839,243 | |

| Lakewood Ohio GO Limited, Series A | | 4.000% | | 12/01/28 | | | 840,000 | | | | 877,861 | |

| Reynoldsburg Ohio GO Limited, Series 2018 | | 4.000% | | 12/01/30 | | | 1,000,000 | | | | 1,064,930 | |

| Strongsville Ohio GO Limited, Series 2016 | | 4.000% | | 12/01/30 | | | 350,000 | | | | 354,470 | |

| | | | | | | | | | | | 11,985,801 | |

| General Obligation - County — 1.5% | | | | | | | | | | | | |

| Lorain County Ohio GO Unlimited, Series 2017 | | 4.000% | | 12/01/30 | | | 450,000 | | | | 455,617 | |

| Lucas County Ohio GO Limited, Series 2017 | | 4.000% | | 10/01/28 | | | 1,000,000 | | | | 1,027,901 | |

| Lucas County Ohio GO Limited, Series 2018 | | 4.000% | | 10/01/29 | | | 605,000 | | | | 622,502 | |

| Summit County Ohio GO Limited, Series 2016 | | 4.000% | | 12/01/31 | | | 500,000 | | | | 505,976 | |

| | | | | | | | | | | | 2,611,996 | |

| General Obligation - State — 1.9% | | | | | | | | | | | | |

| Pennsylvania GO Unlimited, Series 2018 | | 4.000% | | 03/01/37 | | | 1,000,000 | | | | 1,032,933 | |

| Washington GO Unlimited, Series 2022-A | | 5.000% | | 08/01/44 | | | 2,000,000 | | | | 2,217,914 | |

| | | | | | | | | | | | 3,250,847 | |

| Higher Education — 27.9% | | | | | | | | | | | | |

| Bowling Green State University Ohio Revenue, Series 2017-B | | 5.000% | | 06/01/30 | | | 750,000 | | | | 808,108 | |

| Bowling Green State University Ohio Revenue, Series 2020-A | | 5.000% | | 06/01/37 | | | 1,000,000 | | | | 1,108,086 | |

| Bowling Green State University Ohio Revenue, Series 2020-A | | 4.000% | | 06/01/45 | | | 2,830,000 | | | | 2,851,368 | |

| Cuyahoga County Ohio Community College GO Unlimited, Series 2018 | | 4.000% | | 12/01/33 | | | 1,275,000 | | | | 1,323,650 | |

| Indiana Financial Authorities Educational Facilities Revenue, Series 2021 | | 4.000% | | 02/01/29 | | | 940,000 | | | | 986,721 | |

| Indiana Financial Authorities Educational Facilities Revenue, Series 2021 | | 5.000% | | 02/01/32 | | | 1,065,000 | | | | 1,199,642 | |

| Kent State University Ohio Revenue, Series 2019 | | 5.000% | | 05/01/31 | | | 1,000,000 | | | | 1,174,360 | |

| Kent State University Ohio Revenue, Series 2022 | | 5.000% | | 05/01/35 | | | 2,000,000 | | | | 2,354,758 | |

| Kent State University Ohio Revenue, Series 2020-A | | 5.000% | | 05/01/45 | | | 950,000 | | | | 1,029,526 | |

| Miami University Ohio General Receipts Revenue, Series 2017 | | 5.000% | | 09/01/31 | | | 735,000 | | | | 779,400 | |

| Miami University Ohio General Receipts Revenue, Series 2020-A | | 4.000% | | 09/01/36 | | | 1,000,000 | | | | 1,054,463 | |

| Miami University Ohio General Receipts Revenue, Series 2020-A | | 4.000% | | 09/01/45 | | | 3,110,000 | | | | 3,148,201 | |

| Ohio Higher Education Facilities Revenue - Case Western Reserve University, Series 2021-A | | 4.000% | | 12/01/44 | | | 1,250,000 | | | | 1,269,280 | |

| Ohio Higher Education Facilities Revenue - Denison University, Series 2017-A | | 5.000% | | 11/01/42 | | | 1,700,000 | | | | 1,785,734 | |

| Ohio Higher Education Facilities Revenue - Denison University | | 5.000% | | 11/01/53 | | | 5,000,000 | | | | 5,498,948 | |

| Ohio Higher Education Facilities Revenue - Oberlin College, Series A | | 5.250% | | 10/01/53 | | | 1,000,000 | | | | 1,123,356 | |

| Ohio Higher Education Facilities Revenue - University of Dayton, Series 2018-B | | 4.000% | | 12/01/33 | | | 620,000 | | | | 641,073 | |

| Ohio Higher Education Facilities Revenue - University of Dayton, Series 2018-A | | 5.000% | | 02/01/35 | | | 1,350,000 | | | | 1,497,971 | |

| Ohio Higher Education Facilities Revenue - University of Dayton | | 4.000% | | 02/01/36 | | | 1,050,000 | | | | 1,092,603 | |

| Ohio Higher Education Facilities Revenue - University of Dayton, Series 2018-A | | 5.000% | | 12/01/36 | | | 2,010,000 | | | | 2,150,187 | |

| Ohio Higher Education Facilities Revenue - University of Dayton, Series 2018-B | | 5.000% | | 12/01/36 | | | 470,000 | | | | 502,780 | |

| Ohio Higher Education Facilities Revenue - Xavier University, Series 2020 | | 5.000% | | 05/01/29 | | | 540,000 | | | | 602,051 | |

| The accompanying notes are an integral part of these financial statements. |

| MUNICIPAL INCOME FUND | PORTFOLIO OF INVESTMENTS AS OF DECEMBER 31, 2023 |

| MUNICIPAL BONDS — 99.0% | | Coupon | | Maturity | | Par Value | | | Value | |

| Ohio Higher Education Facilities Revenue - Xavier University, Series 2020 | | 5.000% | | 05/01/30 | | $ | 570,000 | | | $ | 645,305 | |

| Ohio Higher Education Facilities Revenue - Xavier University, Series 2020 | | 5.000% | | 05/01/32 | | | 630,000 | | | | 709,357 | |

| Ohio Higher Education Facilities Revenue - Xavier University, Series 2015-C | | 5.000% | | 05/01/32 | | | 1,000,000 | | | | 1,028,771 | |

| Ohio Higher Education Facilities Revenue - Xavier University | | 4.500% | | 05/01/36 | | | 1,000,000 | | | | 1,024,494 | |

| Ohio Higher Education Facilities Revenue - Xavier University, Series 2020 | | 4.000% | | 05/01/38 | | | 600,000 | | | | 611,241 | |

| University of Akron Ohio General Receipts Revenue, Series 2016-A | | 5.000% | | 01/01/27 | | | 350,000 | | | | 368,235 | |

| University of Akron Ohio General Receipts Revenue, Series 2015-A | | 5.000% | | 01/01/28 | | | 410,000 | | | | 418,066 | |

| University of Akron Ohio General Receipts Revenue, Series 2016-A | | 5.000% | | 01/01/29 | | | 435,000 | | | | 458,175 | |

| University of Akron Ohio General Receipts Revenue, Series 2014-A | | 5.000% | | 01/01/29 | | | 650,000 | | | | 650,945 | |

| University of Akron Ohio General Receipts Revenue, Series 2015-A | | 5.000% | | 01/01/30 | | | 720,000 | | | | 734,340 | |

| University of Akron Ohio General Receipts Revenue, Series 2016-A | | 5.000% | | 01/01/33 | | | 1,000,000 | | | | 1,053,403 | |

| University of Akron Ohio General Receipts Revenue, Series 2018-A | | 5.000% | | 01/01/34 | | | 400,000 | | | | 434,123 | |

| University of Cincinnati General Receipts Revenue, Series 2019-A | | 5.000% | | 06/01/36 | | | 1,250,000 | | | | 1,400,243 | |

| University of Cincinnati General Receipts Revenue, Series C | | 5.000% | | 06/01/39 | | | 1,250,000 | | | | 1,276,494 | |

| University of North Dakota Certificate of Participation, Series 2021-A | | 4.000% | | 06/01/37 | | | 555,000 | | | | 573,688 | |

| University of Toledo Revenue, Series B | | 5.000% | | 06/01/27 | | | 1,590,000 | | | | 1,704,198 | |

| University of Toledo Revenue, Series B | | 5.000% | | 06/01/31 | | | 500,000 | | | | 572,655 | |

| University of Toledo Revenue, Series 2017-A | | 5.000% | | 06/01/34 | | | 1,000,000 | | | | 1,068,445 | |

| | | | | | | | | | | | 48,714,444 | |

| Hospital/Health Bonds — 8.6% | | | | | | | | | | | | |

| Franklin County Ohio Hospital Revenue Nationwide Childrens, Series 2016-C | | 5.000% | | 11/01/32 | | | 500,000 | | | | 545,822 | |

| Franklin County Ohio Hospital Revenue Nationwide Childrens, Series 2016-C | | 4.000% | | 11/01/36 | | | 800,000 | | | | 818,852 | |

| Franklin County Ohio Hospital Revenue Nationwide Childrens, Series 2016-C | | 4.000% | | 11/01/40 | | | 1,340,000 | | | | 1,347,062 | |

| Franklin County Ohio Hospital Revenue Nationwide Childrens, Series 2019-A | | 5.000% | | 11/01/48 | | | 3,100,000 | | | | 3,468,020 | |

| Hamilton County Ohio Hospital Facilities Revenue Cincinnati Children’s, Series 2019-CC | | 5.000% | | 11/15/41 | | | 2,410,000 | | | | 2,797,501 | |

| Hamilton County Ohio Hospital Facilities Revenue Cincinnati Children’s Hospital, Series 2019-CC | | 5.000% | | 11/15/49 | | | 1,300,000 | | | | 1,486,012 | |

| Ohio Hospital Facility Revenue Refunding Cleveland Clinic Health, Series 2017-A | | 4.000% | | 01/01/36 | | | 3,100,000 | | | | 3,204,069 | |

| Ohio Hospital Facility Revenue Refunding Cleveland Clinic Health, Series 2019-B | | 4.000% | | 01/01/42 | | | 1,320,000 | | | | 1,332,502 | |

| | | | | | | | | | | | 14,999,840 | |

| Housing — 9.2% | | | | | | | | | | | | |

| Colorado State Certificate of Participation, Series 2020-A | | 4.000% | | 12/15/34 | | | 1,000,000 | | | | 1,071,994 | |

| Colorado State Certificate of Participation, Series 2020-A | | 4.000% | | 12/15/39 | | | 2,000,000 | | | | 2,062,374 | |

| FHLMC, Series M-053 | | 2.550% | | 06/15/35 | | | 3,785,000 | | | | 3,141,529 | |

| FHLMC Multifamily ML Certificates (Freddie Mac Guaranty Agreement), Series A-US | | 3.400% | | 01/25/36 | | | 1,853,241 | | | | 1,696,035 | |

| Kentucky Certificates of Participation, Series 2018-A | | 4.000% | | 04/15/28 | | | 695,000 | | | | 732,821 | |

| Kentucky Certificates of Participation, Series A | | 4.000% | | 04/15/31 | | | 500,000 | | | | 520,943 | |

| Kentucky Property and Buildings Commission Revenue, Series A | | 5.000% | | 05/01/34 | | | 2,340,000 | | | | 2,739,694 | |

| The accompanying notes are an integral part of these financial statements. |

| MUNICIPAL INCOME FUND | PORTFOLIO OF INVESTMENTS AS OF DECEMBER 31, 2023 |

| MUNICIPAL BONDS — 99.0% | | Coupon | | Maturity | | Par Value | | | Value | |

| Missouri State Housing Development Commission Single Family Mortgage Revenue, Series 2019 SER C | | 3.875% | | 05/01/50 | | $ | 1,125,000 | | | $ | 1,126,286 | |

| Missouri State Housing Development Commission Single Family Mortgage Revenue, Series 2020-C | | 3.500% | | 11/01/50 | | | 1,935,000 | | | | 1,917,324 | |

| Missouri State Housing Development Commission Single Family Mortgage Revenue, Series 2020-A | | 3.500% | | 11/01/50 | | | 605,000 | | | | 599,588 | |

| Ohio Housing Finance Agency Residential Mortgage Revenue, Series 2017-A | | 3.700% | | 03/01/32 | | | 520,000 | | | | 519,867 | |

| | | | | | | | | | | | 16,128,455 | |

| Other Revenue — 6.7% | | | | | | | | | | | | |

| Akron Ohio Income Tax Revenue, Series 2019 | | 4.000% | | 12/01/31 | | | 870,000 | | | | 921,767 | |

| Cincinnati Ohio Economic Development Revenue (Baldwin 300 Project), Series D | | 4.750% | | 11/01/30 | | | 500,000 | | | | 524,969 | |

| Cincinnati Ohio Economic Development Revenue (Baldwin 300 Project), Series D | | 5.000% | | 11/01/32 | | | 525,000 | | | | 554,990 | |

| Hamilton County Ohio Economic Development King Highland Community Urban Redevelopment Corp. Revenue, Series 2015 | | 5.000% | | 06/01/30 | | | 655,000 | | | | 673,417 | |

| Mobile Alabama Industrial Development Board Pollution Control Revenue, Series 2008-B | | 2.900% | | 07/15/34 | | | 1,000,000 | | | | 999,242 | |

| Monroe County Georgia Development Authority Pollution Control Revenue, Series 2009 | | 1.000% | | 07/01/49 | | | 1,000,000 | | | | 940,396 | |

| Ohio Special Obligation Revenue, Series 2016-C | | 5.000% | | 12/01/29 | | | 510,000 | | | | 547,719 | |

| Ohio Special Obligation Revenue, Series 2020-B | | 5.000% | | 04/01/39 | | | 1,000,000 | | | | 1,108,760 | |

| Ohio Turnpike Revenue, Series 2021-A | | 5.000% | | 02/15/46 | | | 1,990,000 | | | | 2,175,381 | |

| Riversouth Ohio Authority Revenue, Series 2016 | | 4.000% | | 12/01/31 | | | 700,000 | | | | 720,258 | |

| St. Xavier High School, Inc. Ohio Revenue, Series 2020-A | | 4.000% | | 04/01/36 | | | 400,000 | | | | 411,604 | |

| St. Xavier High School, Inc. Ohio Revenue, Series 2020-A | | 4.000% | | 04/01/37 | | | 575,000 | | | | 586,523 | |

| St. Xavier High School, Inc. Ohio Revenue, Series 2020-A | | 4.000% | | 04/01/38 | | | 400,000 | | | | 405,115 | |

| St. Xavier High School, Inc. Ohio Revenue, Series 2020-A | | 4.000% | | 04/01/39 | | | 400,000 | | | | 403,132 | |

| Summit County Ohio Development Finance Authority, Series 2018 | | 4.000% | | 12/01/27 | | | 220,000 | | | | 225,403 | |

| Summit County Ohio Development Finance Authority, Series 2018 | | 4.000% | | 12/01/28 | | | 435,000 | | | | 446,208 | |

| | | | | | | | | | | | 11,644,884 | |

| Revenue Bonds - Facility — 0.7% | | | | | | | | | | | | |

| Franklin County Convention Facilities Authority, Series 2019 | | 5.000% | | 12/01/30 | | | 600,000 | | | | 694,571 | |

| Franklin County Convention Facilities Authority, Series 2019 | | 5.000% | | 12/01/32 | | | 505,000 | | | | 584,081 | |

| | | | | | | | | | | | 1,278,652 | |

| Revenue Bonds - Water & Sewer — 7.2% | | | | | | | | | | | | |

| Ohio State Water Development Authority Revenue, Series 2020-A | | 5.000% | | 12/01/39 | | | 1,165,000 | | | | 1,306,584 | |

| Ohio State Water Development Authority Revenue, Series 2021 | | 5.000% | | 06/01/46 | | | 4,215,000 | | | | 4,695,209 | |

| Ohio State Water Development Authority Revenue, Series 2021-A | | 4.000% | | 12/01/46 | | | 3,880,000 | | | | 3,973,289 | |

| Ohio Water Development Authority Revenue Pollution Control, Series 2021-A | | 5.000% | | 12/01/40 | | | 1,000,000 | | | | 1,143,459 | |

| St. Charles County Missouri Public Water Supply Dist. 2 Certificates of Participation, Series 2016-C | | 4.000% | | 12/01/31 | | | 400,000 | | | | 412,417 | |

| Wise County Virginia Soil & Wastewater, Series 2010-A | | 1.200% | | 11/01/40 | | | 1,000,000 | | | | 986,387 | |

| | | | | | | | | | | | 12,517,345 | |

| School District — 22.2% | | | | | | | | | | | | |

| Arcanum-Butler Ohio LSD GO, Series 2016 | | 4.000% | | 12/01/29 | | | 675,000 | | | | 683,268 | |

| Arcanum-Butler Ohio LSD GO, Series 2016 | | 4.000% | | 12/01/30 | | | 650,000 | | | | 657,969 | |

| Athens City School District, Series 2019-A | | 4.000% | | 12/01/33 | | | 750,000 | | | | 802,604 | |

| Baytown Texas Certificates Obligation, Series 2022 | | 4.250% | | 02/01/40 | | | 1,045,000 | | | | 1,101,921 | |

| The accompanying notes are an integral part of these financial statements. |

| MUNICIPAL INCOME FUND | PORTFOLIO OF INVESTMENTS AS OF DECEMBER 31, 2023 |

| MUNICIPAL BONDS — 99.0% | | Coupon | | Maturity | | Par Value | | | Value | |

| Bellbrook-Sugarcreek Ohio LSD GO Unlimited, Series 2016 | | 4.000% | | 12/01/31 | | $ | 325,000 | | | $ | 335,478 | |

| Bellefontaine Ohio SCD GO Unlimited (National RE Insured), Series 2005 | | 5.500% | | 12/01/26 | | | 615,000 | | | | 638,920 | |

| Berea Ohio CSD GO Unlimited, Series 2017 | | 4.000% | | 12/01/31 | | | 500,000 | | | | 515,154 | |

| Bexar Texas Refunding Limited, Series 2019 | | 4.000% | | 06/15/37 | | | 1,360,000 | | | | 1,415,598 | |

| Big Walnut Ohio LSD GO Unlimited, Series 2019 | | 4.000% | | 12/01/33 | | | 500,000 | | | | 531,689 | |

| Brecksville Ohio GO Limited, Series 2022 | | 4.000% | | 12/01/51 | | | 1,885,000 | | | | 1,898,510 | |

| Bullit Kentucky School District Finance Corp., Series 2023-A | | 4.000% | | 03/01/37 | | | 1,255,000 | | | | 1,301,731 | |

| Chillicothe Ohio SD GO Unlimited (AGM Insured), Series 2016 | | 4.000% | | 12/01/29 | | | 400,000 | | | | 403,991 | |

| Cleveland Heights and University Heights Ohio CSD GO Unlimited, Series 2017 | | 4.000% | | 12/01/32 | | | 1,000,000 | | | | 1,041,214 | |

| Columbus Ohio CSD GO Unlimited, Series 2016-B | | 4.000% | | 12/01/29 | | | 400,000 | | | | 416,191 | |

| Dexter Michigan CSD GO Unlimited, Series 2017 | | 4.000% | | 05/01/31 | | | 670,000 | | | | 701,693 | |

| Dublin Ohio CSD Facilities Construction and Improvement, Series 2019-A | | 4.000% | | 12/01/34 | | | 500,000 | | | | 531,016 | |

| Elyria Ohio SCD GO Unlimited (SDCP), Series A | | 4.000% | | 12/01/30 | | | 1,000,000 | | | | 1,045,529 | |

| Grandview Heights Ohio Municipal Facilities Construction and Improvement, Series 2023 | | 4.000% | | 12/01/46 | | | 3,000,000 | | | | 3,081,324 | |

| Green County Ohio Vocational SD GO Unlimited, Series 2019 | | 4.000% | | 12/01/35 | | | 1,000,000 | | | | 1,055,728 | |

| Hudson Ohio CSD GO Unlimited, Series 2018 | | 4.000% | | 12/01/33 | | | 800,000 | | | | 830,525 | |

| Johnstown-Monroe Ohio LSD GO Unlimited, Series 2016 | | 4.000% | | 12/01/29 | | | 800,000 | | | | 836,777 | |

| Kettering Ohio CSD GO Unlimited, Series 2016 | | 4.000% | | 12/01/30 | | | 400,000 | | | | 412,139 | |

| Kettering Ohio CSD GO Unlimited, Series 2007 | | 5.250% | | 12/01/31 | | | 500,000 | | | | 555,987 | |

| Lakewood Ohio GO Limited, Series A | | 5.000% | | 12/01/36 | | | 500,000 | | | | 537,644 | |

| Logan Hocking Ohio LSD Certificates of Participation, Series 2018 | | 4.000% | | 12/01/32 | | | 420,000 | | | | 427,902 | |

| McCracken County Kentucky SD Finance Corp., Series 2022 | | 5.000% | | 08/01/32 | | | 580,000 | | | | 686,342 | |

| McCreary County Kentucky SD Finance Corp., Series 2022 | | 4.000% | | 12/01/35 | | | 560,000 | | | | 582,455 | |

| Menifee County Kentucky SD Financial Corp. Revenue, Series 2019 | | 3.000% | | 08/01/27 | | | 615,000 | | | | 612,428 | |

| Milford Ohio Exempt Village SD Go Unlimited (AGM Insured), Series 2007 | | 5.500% | | 12/01/30 | | | 1,260,000 | | | | 1,418,932 | |

| Olentangy LSD Ohio Go Unlimited, Series 2016 | | 4.000% | | 12/01/31 | | | 1,000,000 | | | | 1,039,339 | |

| Owen County Kentucky SD Revenue, Series 2017 | | 4.000% | | 04/01/27 | | | 1,320,000 | | | | 1,376,291 | |

| Palm Beach Florida SD Certificate of Participation, Series 2021-A | | 5.000% | | 08/01/39 | | | 1,000,000 | | | | 1,118,242 | |

| Pickerington Ohio LSD Capital Appreciation Refunding, Series 2023 | | 4.375% | | 12/01/49 | | | 1,000,000 | | | | 1,043,409 | |

| Popular Bluff Missouri R-I School District Lease Certificates of Participation, Series 2023 | | 5.000% | | 03/01/30 | | | 500,000 | | | | 555,082 | |

| Princeton Ohio CSD GO Unlimited (National RE Insured), Series 2006 | | 5.250% | | 12/01/30 | | | 1,735,000 | | | | 2,001,894 | |

| Pulaski County Kentucky SD Finance Corp. School Building Revenue, Series 2023 | | 4.250% | | 06/01/40 | | | 1,000,000 | | | | 1,036,059 | |

| Teays Valley Ohio LSD Refunding, Series 2016 | | 4.000% | | 12/01/32 | | | 580,000 | | | | 591,997 | |

| Toledo Ohio CSD GO Unlimited, Series 2015 | | 5.000% | | 12/01/29 | | | 660,000 | | | | 690,961 | |

| Trotwood-Madison Ohio CSD GO Unlimited (SDCP), Series 2016 | | 4.000% | | 12/01/28 | | | 410,000 | | | | 427,778 | |

| Trotwood-Madison Ohio CSD GO Unlimited (SDCP), Series 2016 | | 4.000% | | 12/01/29 | | | 500,000 | | | | 522,459 | |

| Trotwood-Madison Ohio CSD GO Unlimited (SDCP), Series 2016 | | 4.000% | | 12/01/30 | | | 350,000 | | | | 365,735 | |

| Upper Arlington Ohio Special Obligation Income Tax Revenue Community Center, Series 2023 | | 4.000% | | 12/01/35 | | | 500,000 | | | | 537,911 | |

| Upper Arlington Ohio Special Obligation Income Tax Revenue Community Center, Series 2023 | | 4.000% | | 12/01/37 | | | 500,000 | | | | 527,633 | |

| Wentzville R-IV SD Of Saint Charles County Missouri Certificates of Participation, Series 2016 | | 4.000% | | 04/01/30 | | | 395,000 | | | | 401,018 | |

| Westerville Ohio SCD Certificate of Participation, Series 2018 | | 5.000% | | 12/01/32 | | | 555,000 | | | | 607,314 | |

| The accompanying notes are an integral part of these financial statements. |

| MUNICIPAL INCOME FUND | PORTFOLIO OF INVESTMENTS AS OF DECEMBER 31, 2023 |

| MUNICIPAL BONDS — 99.0% | | Coupon | | Maturity | | Par Value | | | Value | |

| Willoughby-Eastlake Ohio CSD Certificates of Participation (BAM Insured), Series 2017 | | 4.000% | | 03/01/30 | | $ | 810,000 | | | $ | 816,284 | |

| | | | | | | | | | | | 38,720,065 | |

| State Agency — 6.2% | | | | | | | | | | | | |

| Kentucky Association of Counties Finance Corp. Revenue, Series 2018-E | | 4.000% | | 02/01/29 | | | 575,000 | | | | 595,261 | |

| Kentucky Property and Buildings Commission Revenue, Series A | | 5.000% | | 08/01/29 | | | 600,000 | | | | 619,170 | |

| Kentucky Property and Buildings Commission Revenue | | 5.000% | | 08/01/30 | | | 600,000 | | | | 621,300 | |

| Ohio Common Schools, Series 2019-A | | 5.000% | | 06/15/39 | | | 2,000,000 | | | | 2,202,725 | |

| Ohio Higher Education, Series 2017-A | | 5.000% | | 05/01/31 | | | 850,000 | | | | 877,491 | |

| Ohio Housing Finance Agency Residential Mortgage Revenue, Series 2021-A | | 3.000% | | 03/01/52 | | | 1,700,000 | | | | 1,647,597 | |

| Ohio Infrastructure Improvement, Series 2021-A | | 5.000% | | 03/01/41 | | | 1,500,000 | | | | 1,708,364 | |

| Pennsylvania State Refunding, Series 2017 | | 4.000% | | 01/01/30 | | | 645,000 | | | | 672,958 | |

| South Carolina Jobs Economic Development Authority Hospital Facilities Revenue, Series 2022-A | | 5.000% | | 10/01/35 | | | 1,000,000 | | | | 1,124,954 | |

| Washington Certificates of Participation, Series 2022-A | | 5.000% | | 01/01/41 | | | 675,000 | | | | 761,795 | |

| | | | | | | | | | | | 10,831,615 | |

| | | | | | | | | | | | | |

| Total Municipal Bonds (Cost $180,680,087) | | | | | | | | | | $ | 172,683,944 | |

| | | | | | | | | | | | | |

| MONEY MARKET FUNDS — 0.5% | | Shares | | | Value | |

| Dreyfus AMT-Free Tax Cash Management Fund - Institutional Class, 3.90% (a) (Cost $950,706) | | 951,302 | | | $ | 951,207 | |

| | | | | | | | | | | | | |

| Investments at Value — 99.5% (Cost $181,630,793) | | | | | | | | | | $ | 173,635,151 | |

| | | | | | | | | | | | | |

| Other Assets in Excess of Liabilities — 0.5% | | | | | | | | | | | 908,597 | |

| | | | | | | | | | | | | |

| Net Assets — 100.0% | | | | | | | | | | $ | 174,543,748 | |

| (a) | The rate shown is the 7-day effective yield as of December 31, 2023. |

| The accompanying notes are an integral part of these financial statements. |

| JOHNSON MUTUAL FUNDS | DECEMBER 31, 2023 |

| Statements of Assets and Liabilities | |

| | | Equity | | | Opportunity | |

| | | Income Fund | | | Fund | |

| Assets: | | | | | | | | |

| Investment Securities at Value* | | $ | 619,654,382 | | | $ | 133,261,063 | |

| Dividends Receivable | | | 691,691 | | | | 119,820 | |

| Fund Shares Sold Receivable | | | 249,545 | | | | 4,840 | |

| Total Assets | | $ | 620,595,618 | | | $ | 133,385,723 | |

| | | | | | | | | |

| Liabilities: | | | | | | | | |

| Accrued Management Fees | | $ | 390,560 | | | $ | 99,330 | |

| Accrued Shareholder Servicing Fees — Class S | | | 28,345 | | | | 4,183 | |

| Fund Shares Redeemed Payable | | | 20,304 | | | | 156,678 | |

| Total Liabilities | | $ | 439,209 | | | $ | 260,191 | |

| | | | | | | | | |

| Net Assets | | $ | 620,156,409 | | | $ | 133,125,532 | |

| | | | | | | | | |

| Net Assets Consist of: | | | | | | | | |

| Paid-In Capital | | $ | 436,450,598 | | | $ | 104,922,485 | |

| Distrbutable Earnings | | | 183,705,811 | | | | 28,203,047 | |

| | | | | | | | | |

| Net Assets | | $ | 620,156,409 | | | $ | 133,125,532 | |

| | | | | | | | | |

| Pricing of Class I Shares | | | | | | | | |

| Net Assets applicable to Class I Shares | | $ | 484,818,921 | | | $ | 112,884,318 | |

| Shares Outstanding (Unlimited Amount Authorized) | | | 14,198,458 | | | | 2,262,848 | |

| Offering, Redemption and Net Asset Value Per Share | | $ | 34.15 | | | $ | 49.89 | |

| | | | | | | | | |

| Pricing of Class S Shares | | | | | | | | |